OECD Skills Outlook Global Launch - Skills and Global Value Chains

61

OECD Skills Outlook Global Launch Skills and Global Value Chains @UniofBathIPR, @OECDEduSkills #OECDSkills 4 May 2017 Andreas Schleicher Andrew Wyckoff

-

Upload

eduskills-oecd -

Category

Education

-

view

17.075 -

download

1

Transcript of OECD Skills Outlook Global Launch - Skills and Global Value Chains

OECD Skills Outlook

Global Launch

Skills and Global Value Chains

@UniofBathIPR, @OECDEduSkills

#OECDSkills

4 May 2017

Andreas Schleicher

Andrew Wyckoff

People are at the centre of Global Value Chains

2

What Global Value Chains (GVCs) mean

Value added

The Smiling Curve

3

R&D

Design

Logistic

purchase

Production

Assembling

Logistic

s

Market

ing

Service

s

Pre-production

Upstream activities

Post-production

Downstream activities

Production

Value

chain

activities

4

A comprehensive approach

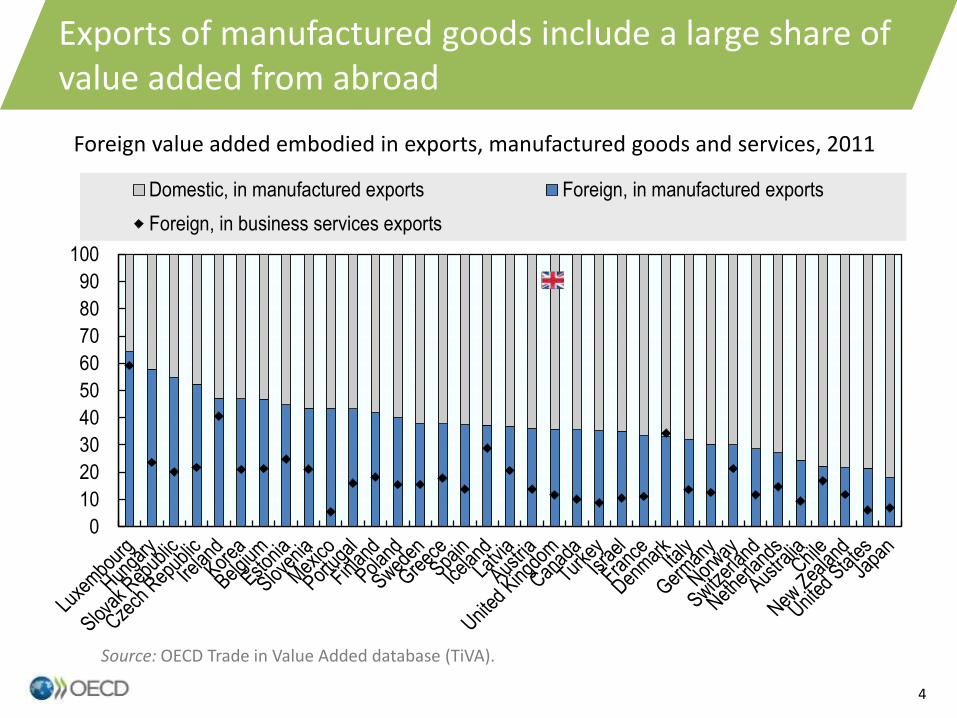

Exports of manufactured goods include a large share of value added from abroad

Foreign value added embodied in exports, manufactured goods and services, 2011

0

10

20

30

40

50

60

70

80

90

100

Domestic, in manufactured exports Foreign, in manufactured exports

Foreign, in business services exports

Source: OECD Trade in Value Added database (TiVA).

0102030405060708090

%

EU28 East and Southeast Asia (excl. China) NAFTAChina Rest of the world

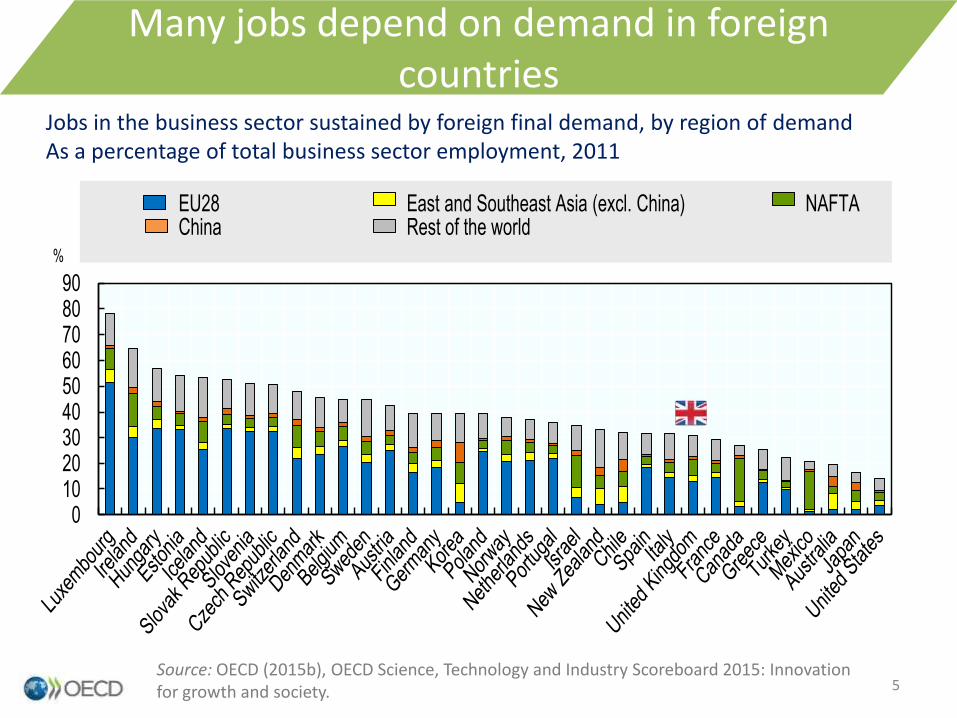

Many jobs depend on demand in foreign countries

Source: OECD (2015b), OECD Science, Technology and Industry Scoreboard 2015: Innovation for growth and society.

Jobs in the business sector sustained by foreign final demand, by region of demandAs a percentage of total business sector employment, 2011

5

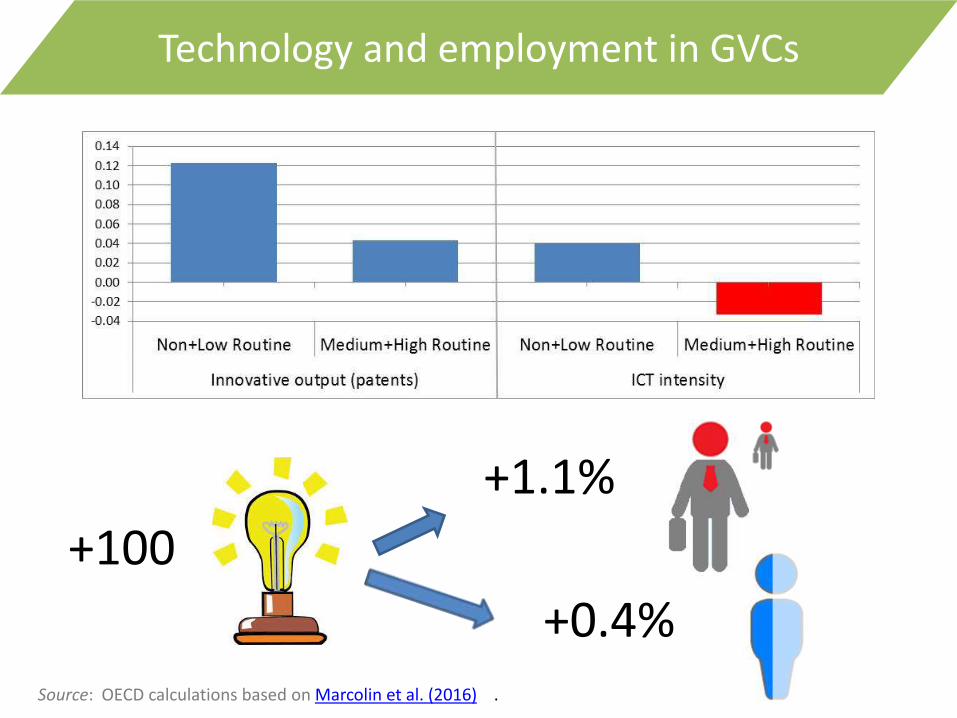

+100

+1.1%

+0.4%Source: OECD calculations based on Marcolin et al. (2016) .

Technology and employment in GVCs

7

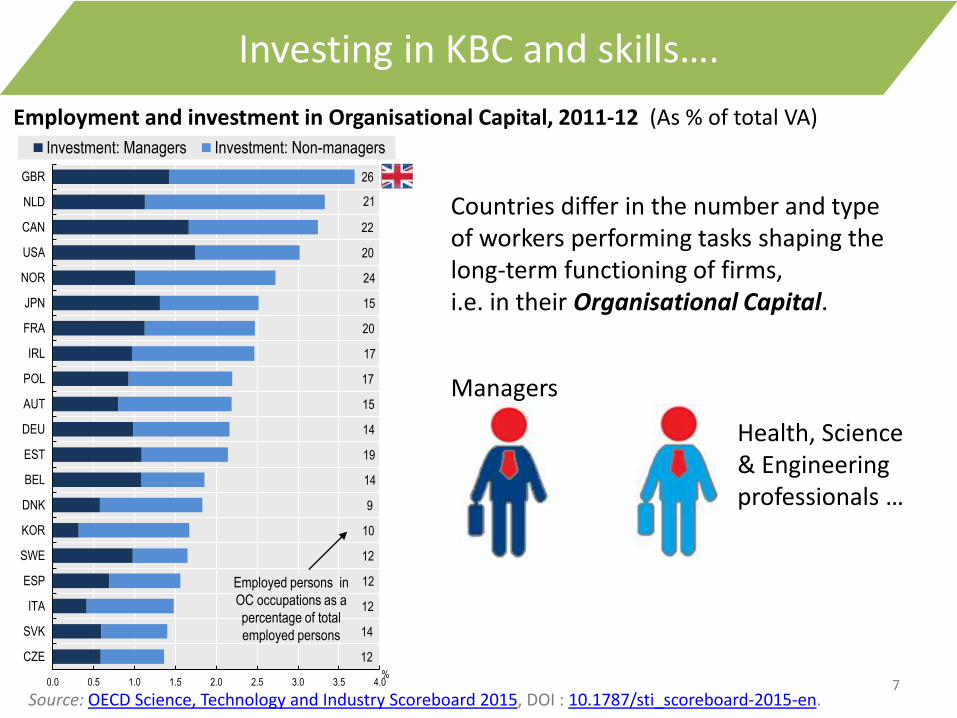

Investing in KBC and skills….

Countries differ in the number and type of workers performing tasks shaping the long-term functioning of firms, i.e. in their Organisational Capital.

Health, Science & Engineering professionals …

12

14

12

12

12

10

9

14

19

14

15

17

17

20

15

24

20

22

21

26

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

CZE

SVK

ITA

ESP

SWE

KOR

DNK

BEL

EST

DEU

AUT

POL

IRL

FRA

JPN

NOR

USA

CAN

NLD

GBR

%

Investment: Managers Investment: Non-managers

Employed persons in

OC occupations as a

percentage of total

employed persons

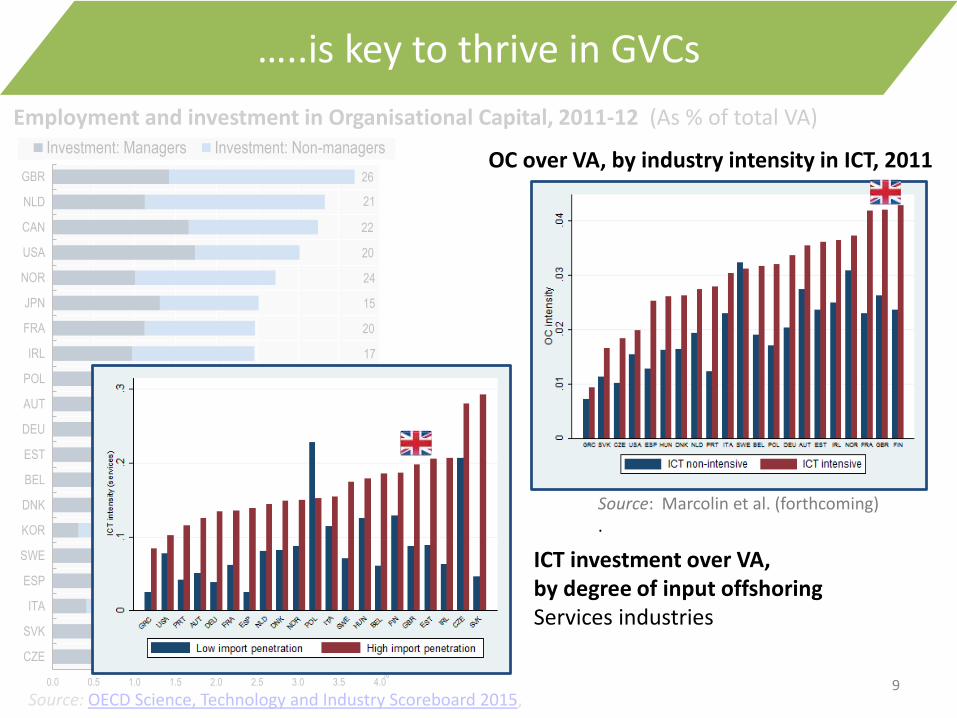

Employment and investment in Organisational Capital, 2011-12 (As % of total VA)

Source: OECD Science, Technology and Industry Scoreboard 2015, DOI : 10.1787/sti_scoreboard-2015-en.

Managers

8

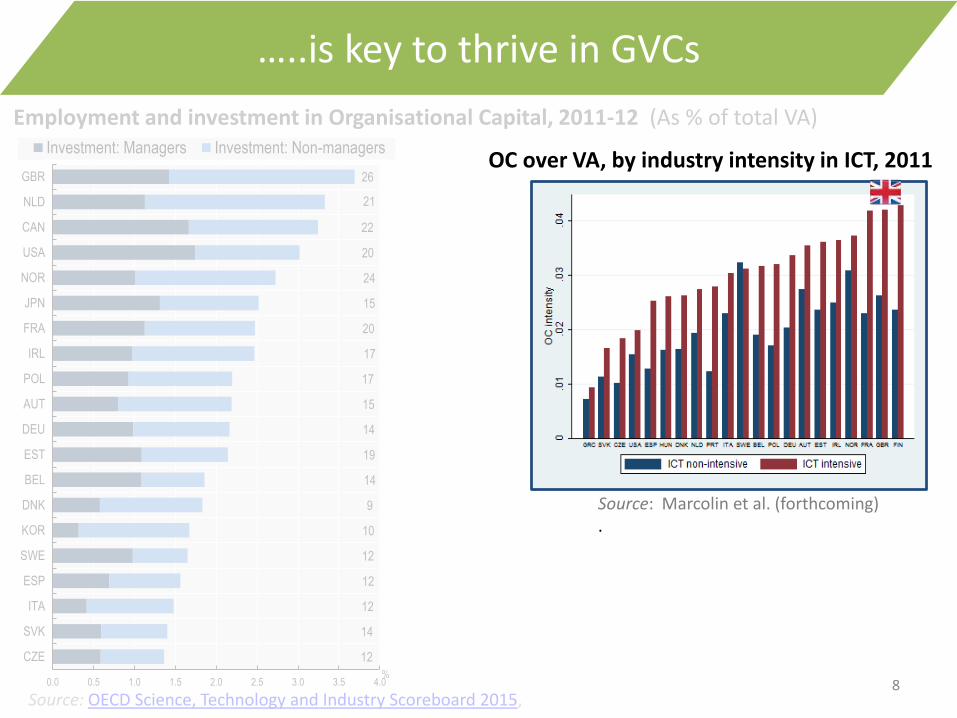

…..is key to thrive in GVCs

Source: OECD Science, Technology and Industry Scoreboard 2015,

12

14

12

12

12

10

9

14

19

14

15

17

17

20

15

24

20

22

21

26

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

CZE

SVK

ITA

ESP

SWE

KOR

DNK

BEL

EST

DEU

AUT

POL

IRL

FRA

JPN

NOR

USA

CAN

NLD

GBR

%

Investment: Managers Investment: Non-managers

Employment and investment in Organisational Capital, 2011-12 (As % of total VA)

Source: Marcolin et al. (forthcoming) .

OC over VA, by industry intensity in ICT, 2011

9

…..is key to thrive in GVCs

Source: OECD Science, Technology and Industry Scoreboard 2015,

ICT investment over VA, by degree of input offshoringServices industries

12

14

12

12

12

10

9

14

19

14

15

17

17

20

15

24

20

22

21

26

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

CZE

SVK

ITA

ESP

SWE

KOR

DNK

BEL

EST

DEU

AUT

POL

IRL

FRA

JPN

NOR

USA

CAN

NLD

GBR

%

Investment: Managers Investment: Non-managers

Employment and investment in Organisational Capital, 2011-12 (As % of total VA)

Source: Marcolin et al. (forthcoming) .

OC over VA, by industry intensity in ICT, 2011

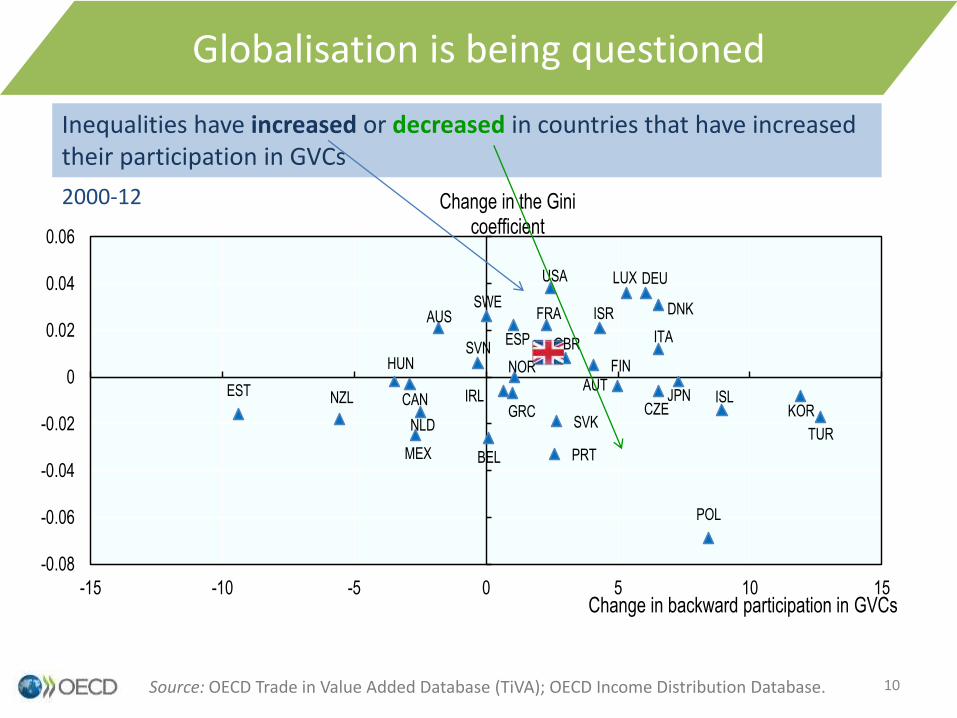

Globalisation is being questioned

AUS

AUT

BEL

CANCZE

DNK

EST

FIN

FRA

DEU

GRC

HUN

ISL

ISR

ITA

JPNKOR

LUX

MEX

NLD

NZL

NOR

POL

PRT

SVK

SVNESP

SWE

TUR

GBR

USA

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

-15 -10 -5 0 5 10 15

Change in the Gini coefficient

Change in backward participation in GVCs

IRL

Inequalities have increased or decreased in countries that have increased their participation in GVCs

Source: OECD Trade in Value Added Database (TiVA); OECD Income Distribution Database.

2000-12

10

Skills Matter for globalisation

11

• Realise productivity gains – offered by new technologies and participation in GVCs

• Protect workers against negative impact– Job losses, lower job quality

• Specialise in advanced industries and services– Innovation, higher productivity, job creation

12Why skills?

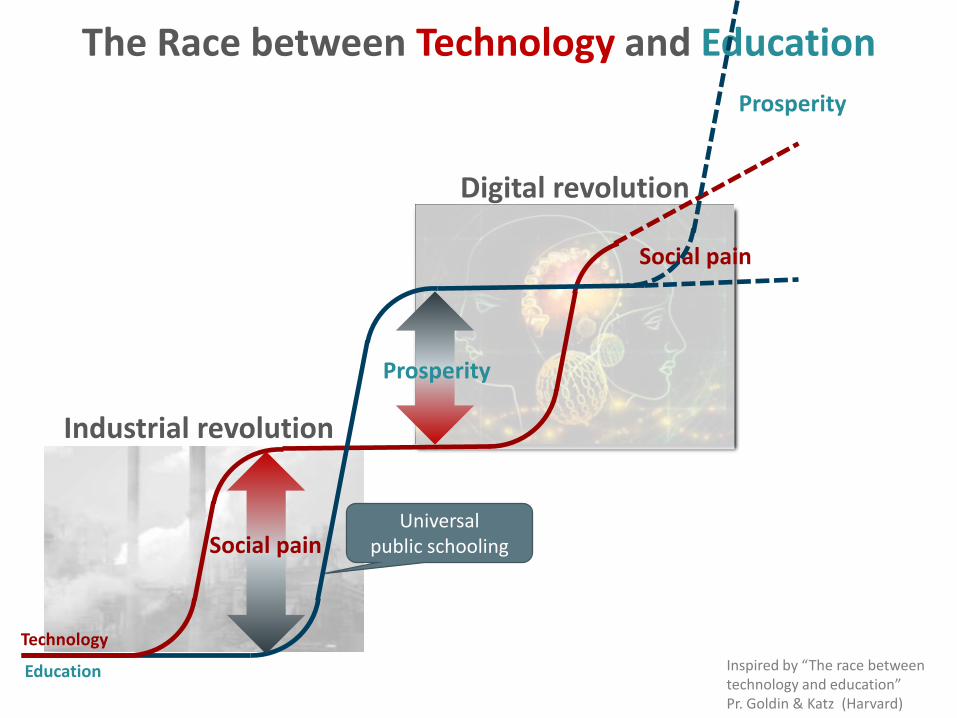

The Race between Technology and Education

Inspired by “The race between technology and education” Pr. Goldin & Katz (Harvard)

Industrial revolution

Digital revolution

Social pain

Universal public schooling

Technology

Education

Prosperity

Social pain

Prosperity

0

0.5

1

1.5

2

2.5

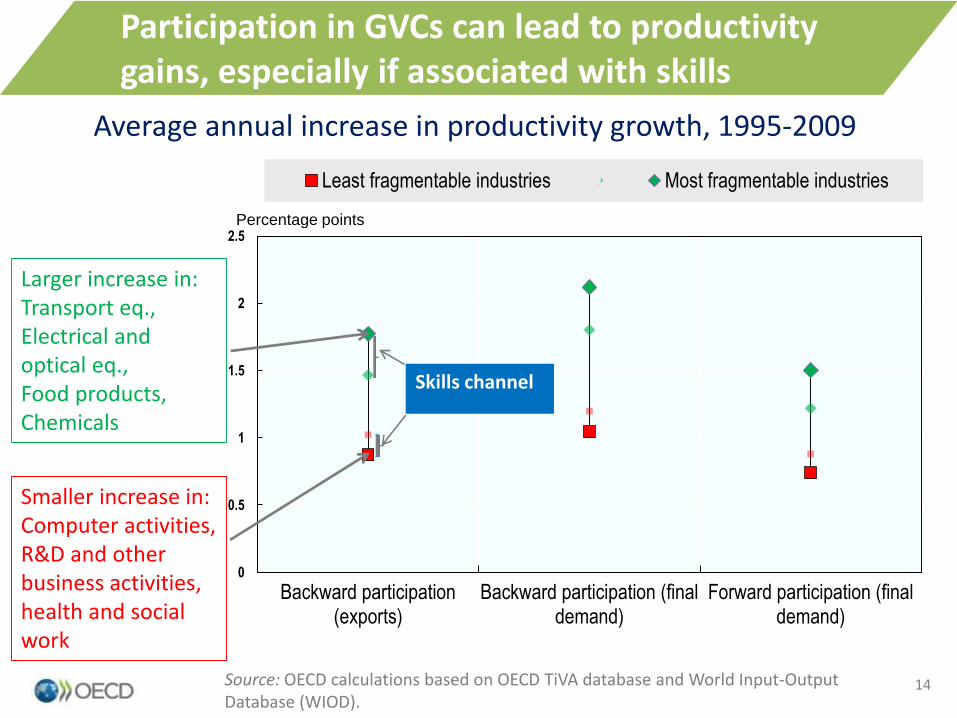

Backward participation(exports)

Backward participation (finaldemand)

Forward participation (finaldemand)

Least fragmentable industries Most fragmentable industries

Percentage points

Average annual increase in productivity growth, 1995-2009

Larger increase in: Transport eq., Electrical and optical eq., Food products, Chemicals

Smaller increase in:Computer activities, R&D and other business activities, health and social work

Source: OECD calculations based on OECD TiVA database and World Input-Output Database (WIOD).

Participation in GVCs can lead to productivity gains, especially if associated with skills

14

Skills channel

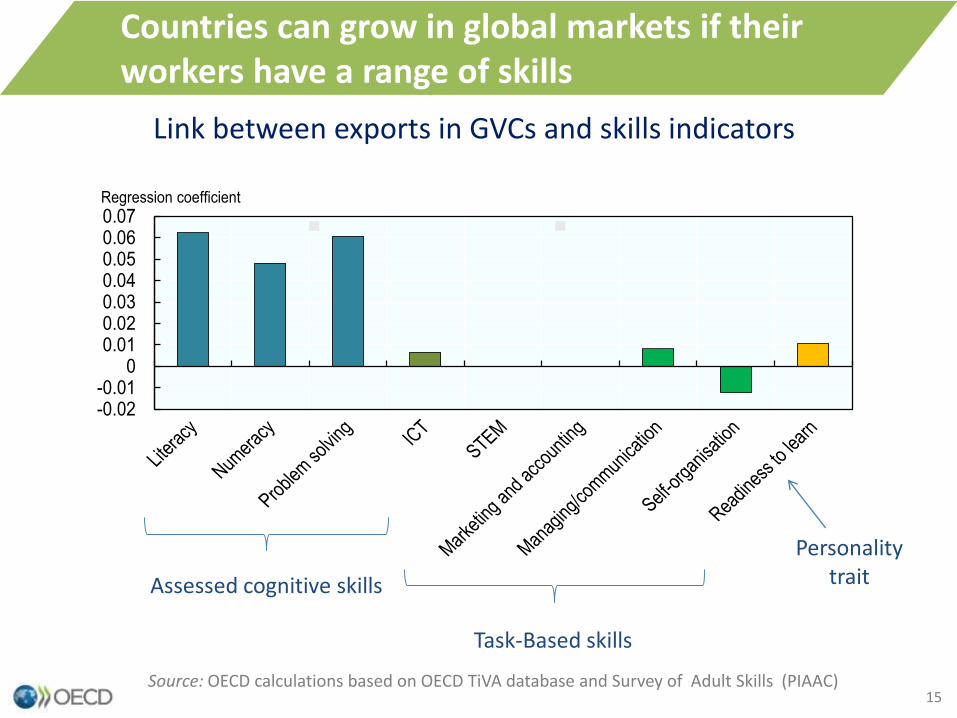

15

Link between exports in GVCs and skills indicators

Source: OECD calculations based on OECD TiVA database and Survey of Adult Skills (PIAAC)

Countries can grow in global markets if their workers have a range of skills

-0.02-0.01

00.010.020.030.040.050.060.07Regression coefficient

Assessed cognitive skills

Task-Based skills

Personality trait

• Sources of inequality– Skill-biased technological change and institutions:

important sources

– Competition from low-cost countries: another source

• What people do and the type of skills they develop makes a difference– More educated workers enjoy higher job quality

– Gap in job strain between low and highly educated workers is larger in countries more active in GVCs

• Investing in skills particularly important in countries engaged in lower end of GVCs

16Impact of GVCs on inequalities within countries

17

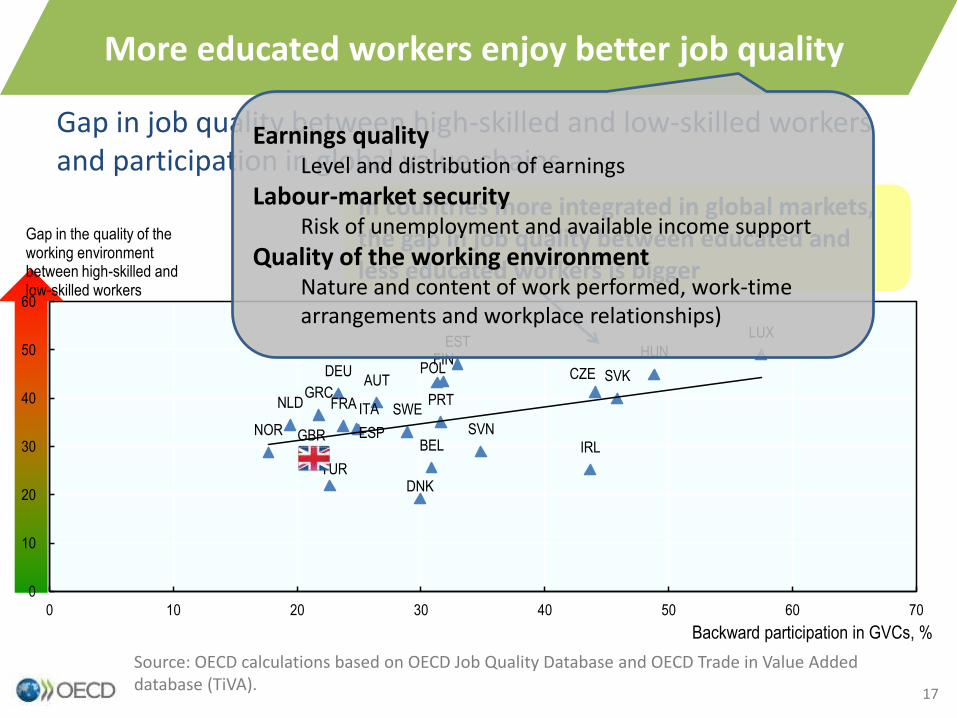

Gap in job quality between high-skilled and low-skilled workersand participation in global value chains

More educated workers enjoy better job quality

AUT

BEL

CZE

DNK

ESTFIN

FRA

DEU

GRC

HUN

IRL

ITA

LUX

NLD

NOR

POL

PRT

SVK

SVNESP

SWE

TUR

GBR

0

10

20

30

40

50

60

0 10 20 30 40 50 60 70

Gap in the quality of the working environment between high-skilled and low-skilled workers

Backward participation in GVCs, %

In countries more integrated in global markets, the gap in job quality between educated and less educated workers is bigger

Source: OECD calculations based on OECD Job Quality Database and OECD Trade in Value Added database (TiVA).

Earnings qualityLevel and distribution of earnings

Labour-market securityRisk of unemployment and available income support

Quality of the working environmentNature and content of work performed, work-time arrangements and workplace relationships)

18

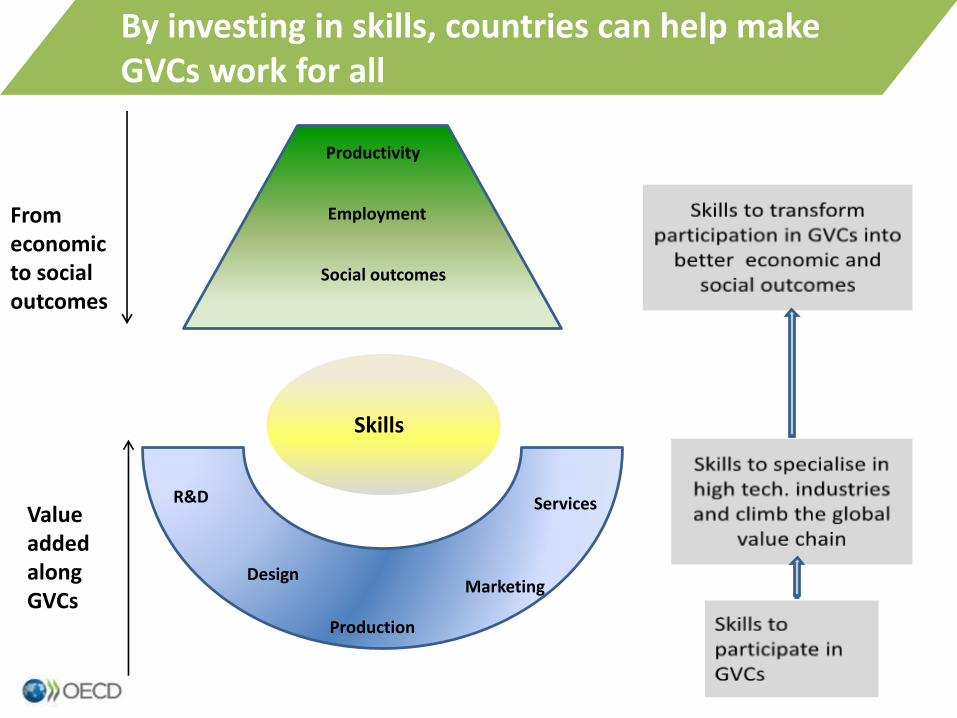

Production

Marketing

Services

Design

R&DValue added along GVCs

From economic to social outcomes

By investing in skills, countries can help make GVCs work for all

Skills

Employment

Social outcomes

Productivity

19

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

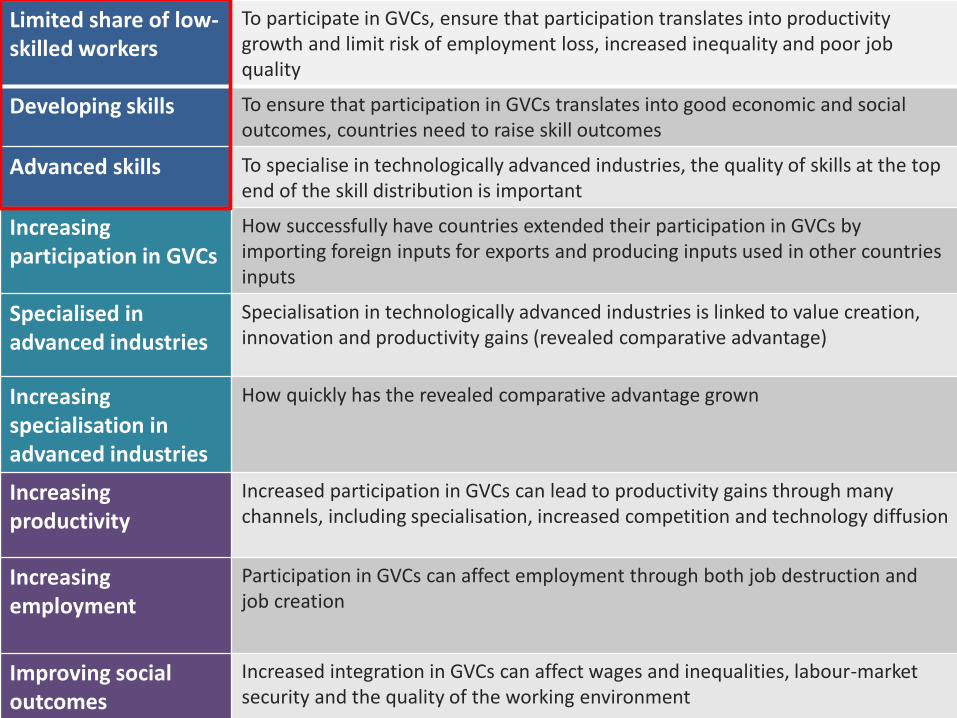

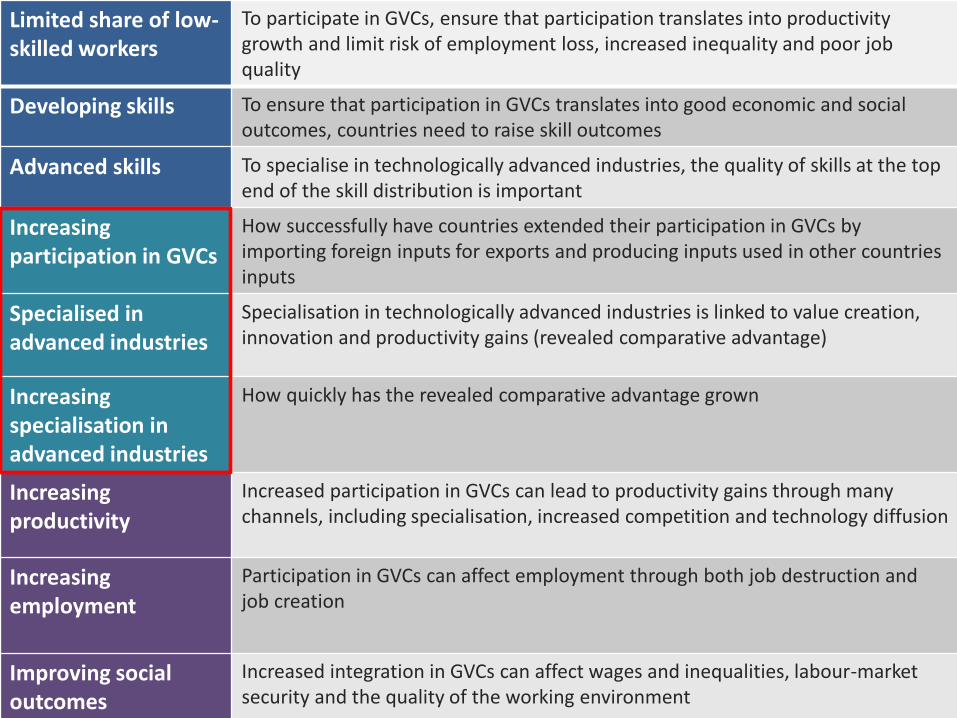

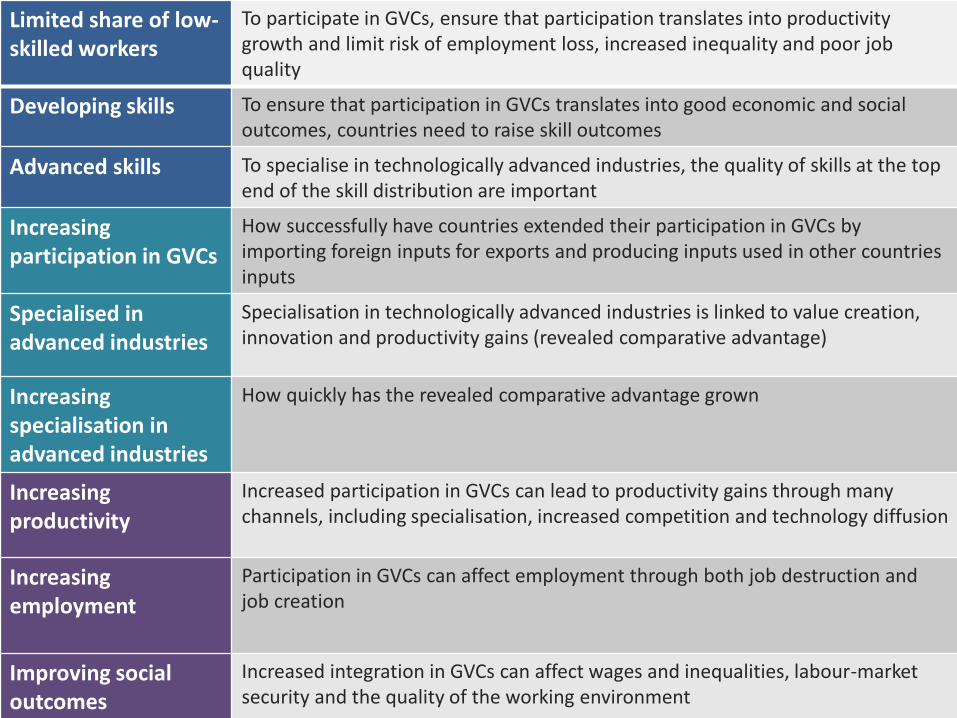

Limited share of low-skilled workers

To participate in GVCs, ensure that participation translates into productivity growth and limit risk of employment loss, increased inequality and poor job quality

Developing skills To ensure that participation in GVCs translates into good economic and social outcomes, countries need to raise skill outcomes

Advanced skills To specialise in technologically advanced industries, the quality of skills at the top end of the skill distribution is important

Increasing participation in GVCs

How successfully have countries extended their participation in GVCs by importing foreign inputs for exports and producing inputs used in other countries inputs

Specialised in advanced industries

Specialisation in technologically advanced industries is linked to value creation, innovation and productivity gains (revealed comparative advantage)

Increasing specialisation in advanced industries

How quickly has the revealed comparative advantage grown

Increasing productivity

Increased participation in GVCs can lead to productivity gains through many channels, including specialisation, increased competition and technology diffusion

Increasing employment

Participation in GVCs can affect employment through both job destruction and job creation

Improving social outcomes

Increased integration in GVCs can affect wages and inequalities, labour-market security and the quality of the working environment

0

10

20

30

40

50

60

70

%

Workers

In both literacy and numeracy In literacy only In numeracy only

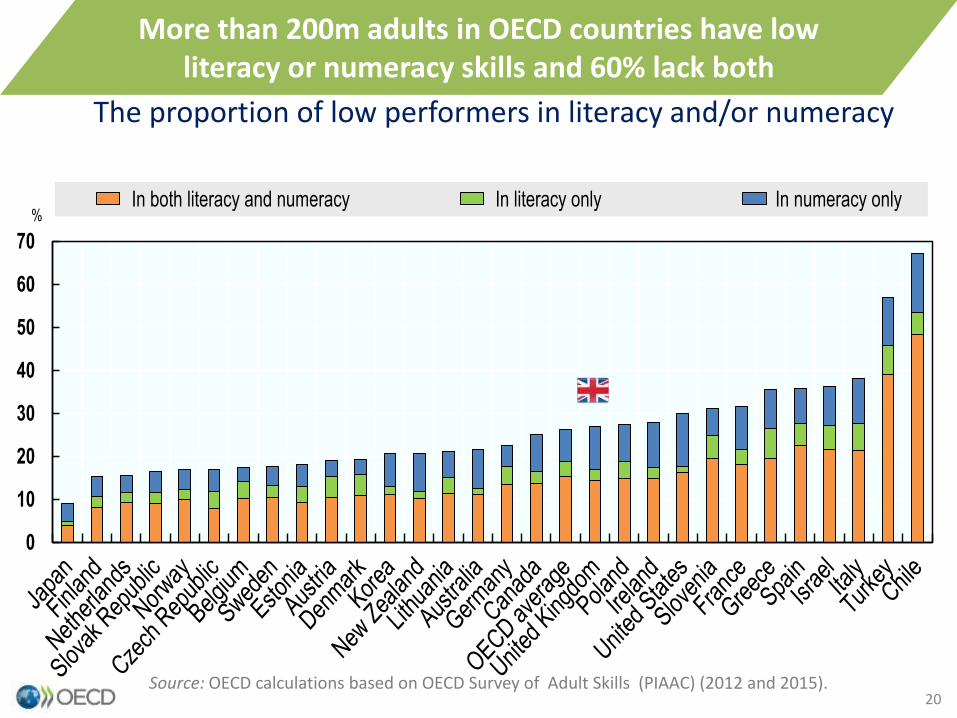

The proportion of low performers in literacy and/or numeracy

Source: OECD calculations based on OECD Survey of Adult Skills (PIAAC) (2012 and 2015).20

More than 200m adults in OECD countries have low literacy or numeracy skills and 60% lack both

100 80 60 40 20 0 20 40

TurkeyGreece

ChileLithuania

Israel

United StatesPoland

Russian FederationIreland

Slovak RepublicEngland (UK)

Northern Ireland (UK)Japan

OECD averageSlovenia

EstoniaDenmark

AustriaAustralia

CanadaNew Zealand

Germany

Czech RepublicNorway

Flanders (Belgium)Netherlands

SwedenFinland

KoreaSingapore

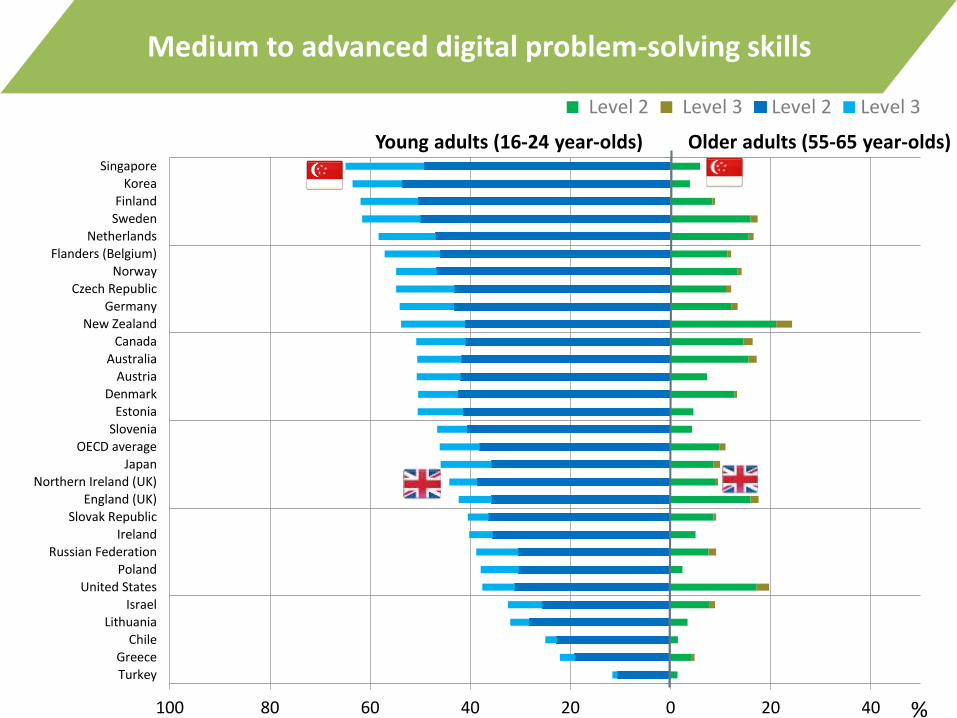

Level 2 Level 3 Level 2 Level 3

Young adults (16-24 year-olds) Older adults (55-65 year-olds)

%

Medium to advanced digital problem-solving skills

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

Literacy skills Numeracy skills Problem solving skillsin technology-rich

environments

Physical skills

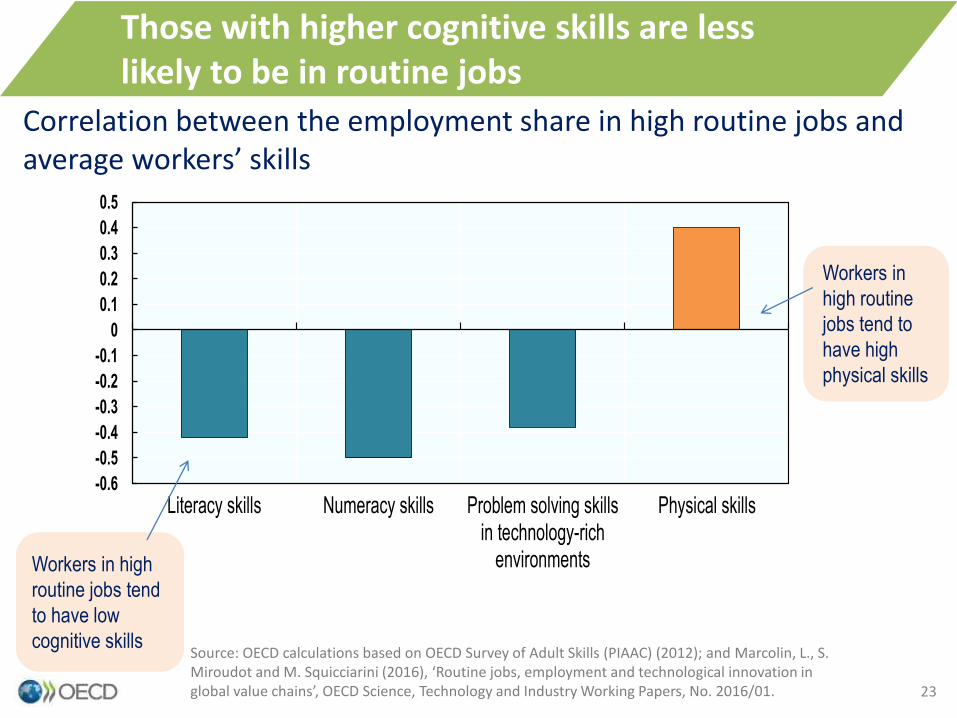

Correlation between the employment share in high routine jobs and average workers’ skills

Workers in high

routine jobs tend

to have low

cognitive skillsSource: OECD calculations based on OECD Survey of Adult Skills (PIAAC) (2012); and Marcolin, L., S. Miroudot and M. Squicciarini (2016), ‘Routine jobs, employment and technological innovation in global value chains’, OECD Science, Technology and Industry Working Papers, No. 2016/01.

Workers in

high routine

jobs tend to

have high

physical skills

23

Those with higher cognitive skills are less likely to be in routine jobs

24

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

Limited share of low-skilled workers

To participate in GVCs, ensure that participation translates into productivity growth and limit risk of employment loss, increased inequality and poor job quality

Developing skills To ensure that participation in GVCs translates into good economic and social outcomes, countries need to raise skill outcomes

Advanced skills To specialise in technologically advanced industries, the quality of skills at the top end of the skill distribution is important

Increasing participation in GVCs

How successfully have countries extended their participation in GVCs by importing foreign inputs for exports and producing inputs used in other countries inputs

Specialised in advanced industries

Specialisation in technologically advanced industries is linked to value creation, innovation and productivity gains (revealed comparative advantage)

Increasing specialisation in advanced industries

How quickly has the revealed comparative advantage grown

Increasing productivity

Increased participation in GVCs can lead to productivity gains through many channels, including specialisation, increased competition and technology diffusion

Increasing employment

Participation in GVCs can affect employment through both job destruction and job creation

Improving social outcomes

Increased integration in GVCs can affect wages and inequalities, labour-market security and the quality of the working environment

Countries can shape their specialisation within global value chains through the skills of their populations

25

26

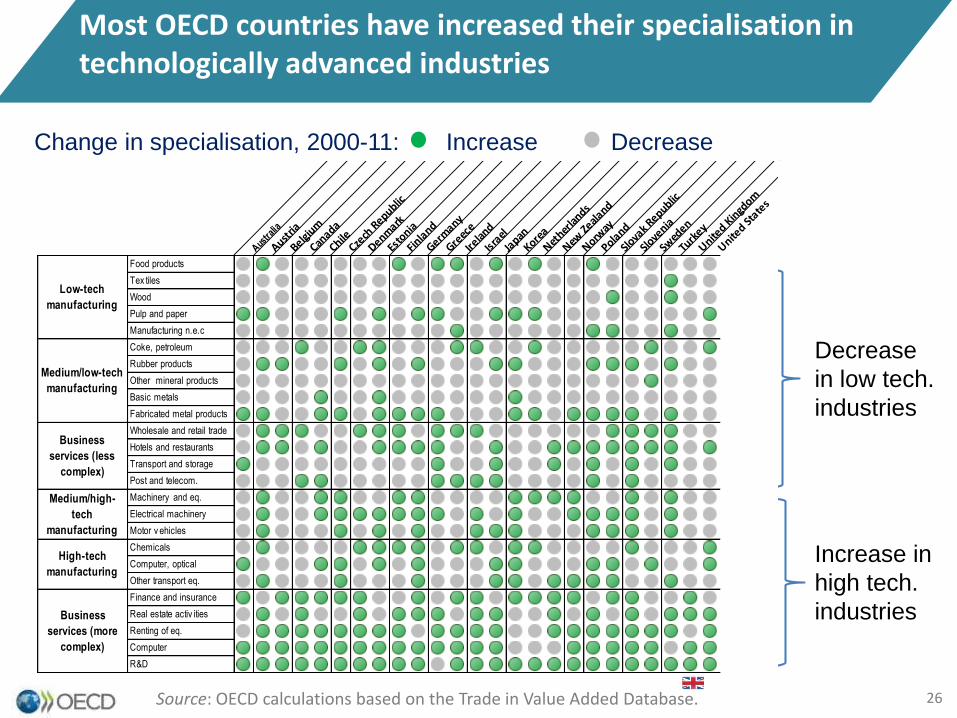

Change in specialisation, 2000-11: Increase Decrease

Source: OECD calculations based on the Trade in Value Added Database.

Most OECD countries have increased their specialisation in technologically advanced industries

Decrease

in low tech.

industries

Increase in

high tech.

industries

Austra

lia

Austria

Belgium

Canada

ChileCze

ch R

epublic

Denmark

Esto

nia

Finla

nd

Germany

Greec

e

Irelan

d

Israel

Japan

Korea

Nether

lands

New Ze

aland

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingd

om

United St

ates

Low-tech

manufacturing

Food products

Tex tiles

Wood

Pulp and paper

Manufacturing n.e.c

Coke, petroleum

Rubber products

Other mineral products

Basic metals

Fabricated metal products

Wholesale and retail trade

Hotels and restaurants

Transport and storage

Post and telecom.

Machinery and eq.

Electrical machinery

Motor v ehicles

Chemicals

Computer, optical

Other transport eq.

Finance and insurance

Real estate activ ities

Renting of eq.

Computer

R&D

Low-tech

manufacturing

Medium/low-tech

manufacturing

Business

services (less

complex)

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

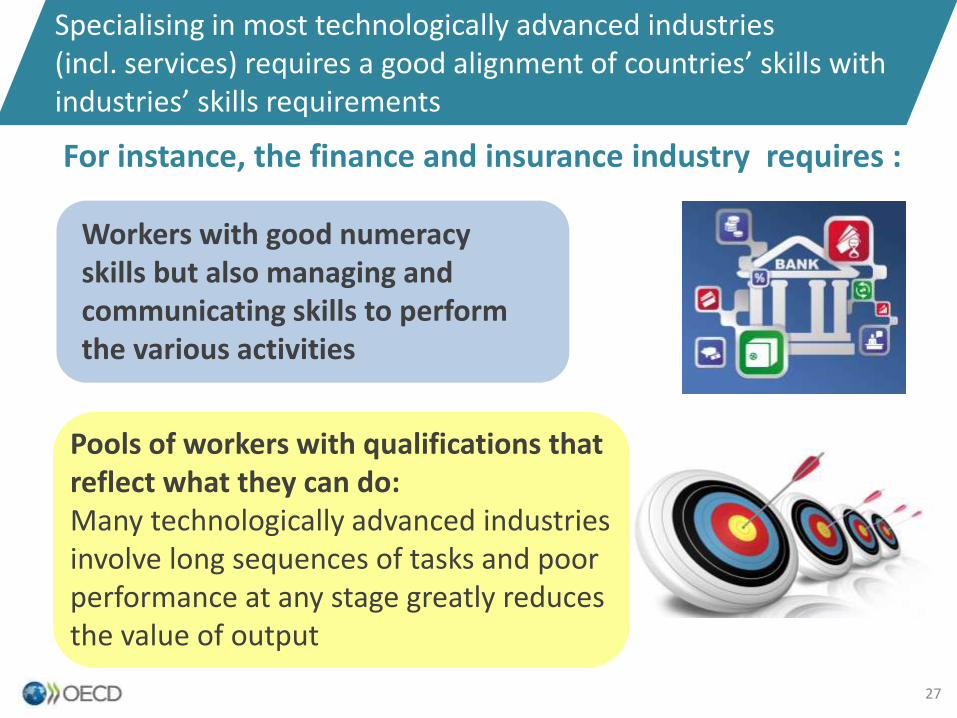

Specialising in most technologically advanced industries (incl. services) requires a good alignment of countries’ skills with industries’ skills requirements

For instance, the finance and insurance industry requires :

Workers with good numeracy skills but also managing and communicating skills to perform the various activities

Pools of workers with qualifications that reflect what they can do:Many technologically advanced industries involve long sequences of tasks and poor performance at any stage greatly reduces the value of output

27

30

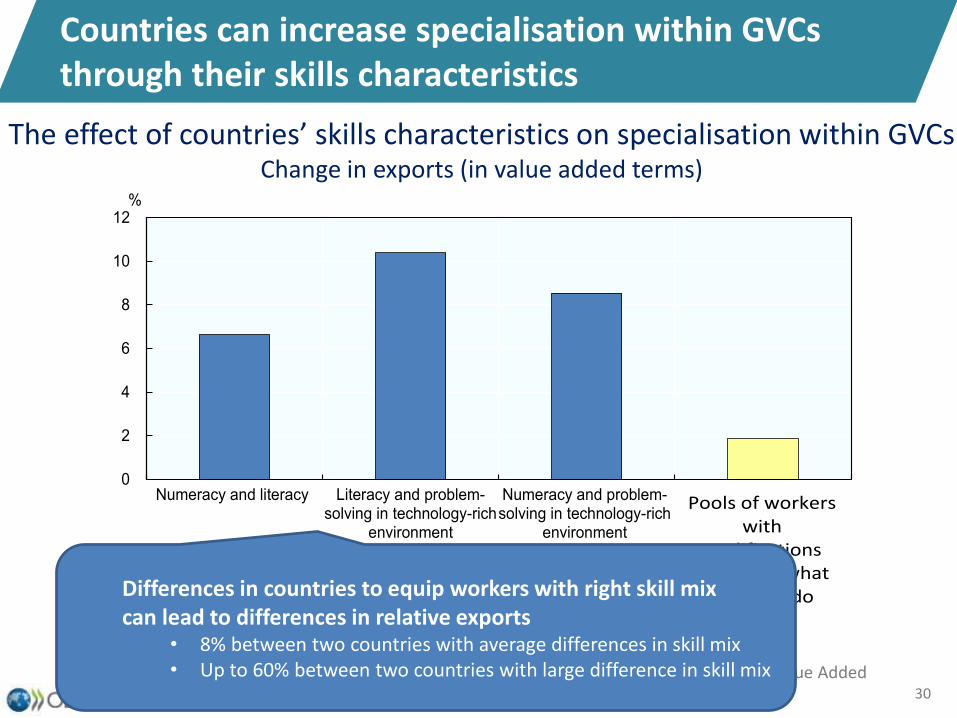

Countries can increase specialisation within GVCs through their skills characteristics

The effect of countries’ skills characteristics on specialisation within GVCsChange in exports (in value added terms)

Source: OECD calculations based on the Survey of Adult Skills (PIAAC) and Trade in Value Added Database.

0

2

4

6

8

10

12

Numeracy and literacy Literacy and problem-solving in technology-rich

environment

Numeracy and problem-solving in technology-rich

environment

%

Skills mix

Pools of workers with

qualifications reflecting what

they can doDifferences in countries to equip workers with right skill mix can lead to differences in relative exports

• 8% between two countries with average differences in skill mix• Up to 60% between two countries with large difference in skill mix

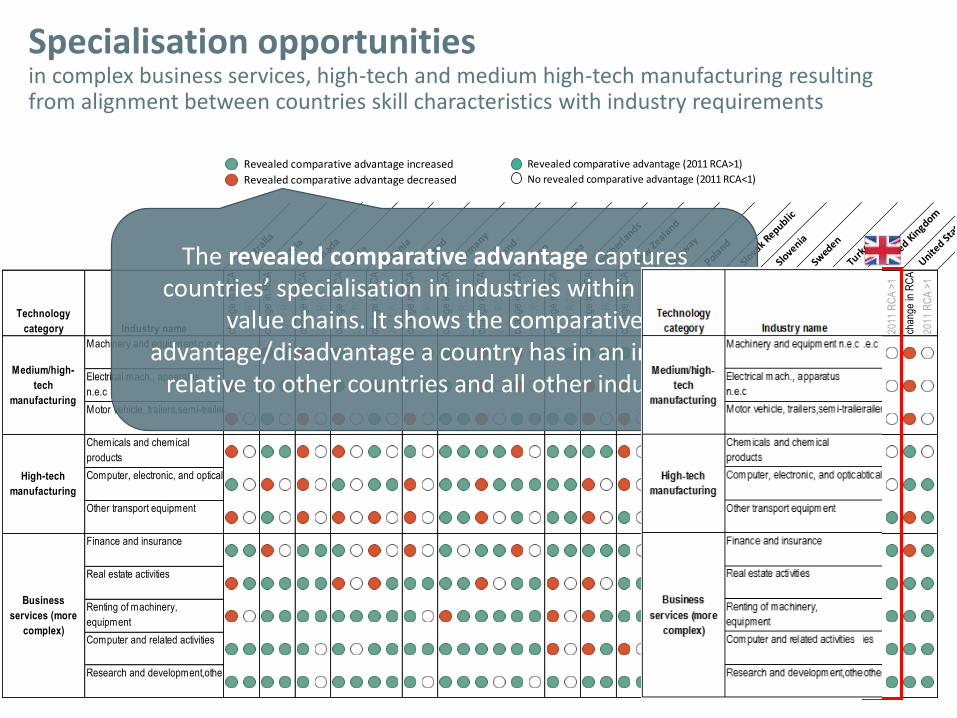

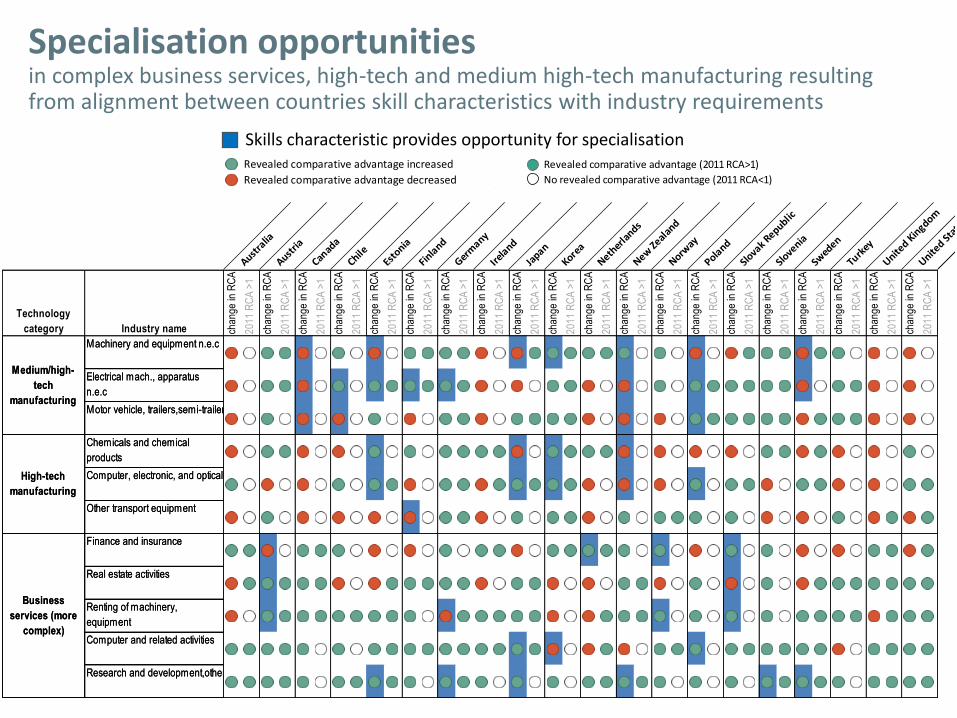

Specialisation opportunitiesin complex business services, high-tech and medium high-tech manufacturing resulting from alignment between countries skill characteristics with industry requirements

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

The revealed comparative advantage captures countries’ specialisation in industries within global

value chains. It shows the comparative advantage/disadvantage a country has in an industry

relative to other countries and all other industries

Revealed comparative advantage (2011 RCA>1)

No revealed comparative advantage (2011 RCA<1)

Specialisation opportunitiesin complex business services, high-tech and medium high-tech manufacturing resulting from alignment between countries skill characteristics with industry requirements

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

Skills characteristic provides opportunity for specialisationRevealed comparative advantage (2011 RCA>1)

No revealed comparative advantage (2011 RCA<1)

Specialisation opportunitiesin complex business services, high-tech and medium high-tech manufacturing resulting from alignment between countries skill characteristics with industry requirements

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

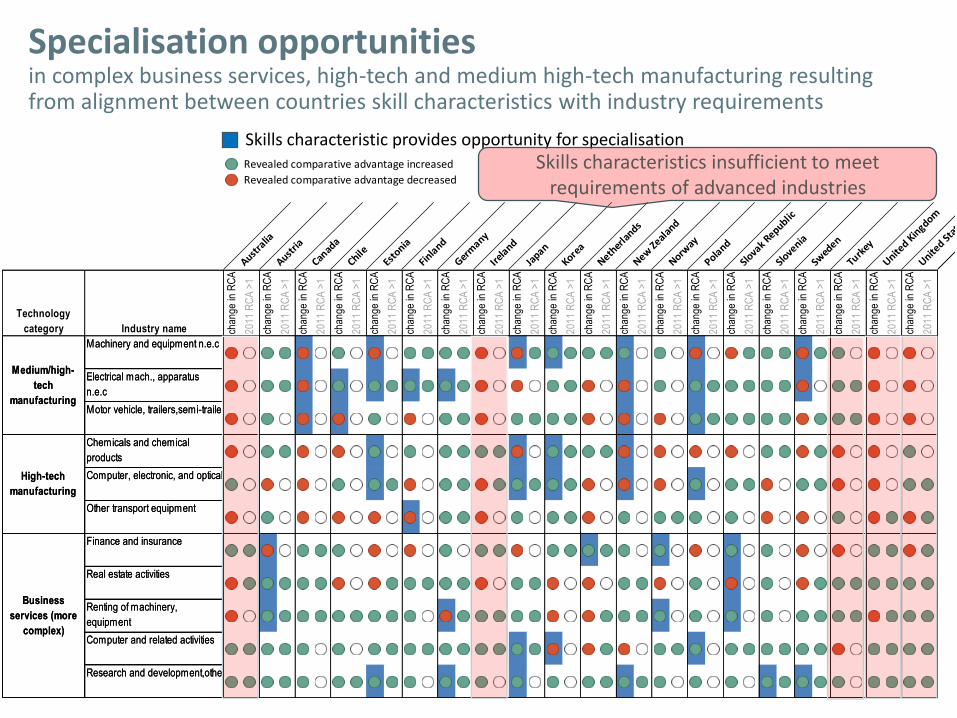

Skills characteristic provides opportunity for specialisationSkills characteristics insufficient to meet

requirements of advanced industries

Specialisation opportunitiesin complex business services, high-tech and medium high-tech manufacturing resulting from alignment between countries skill characteristics with industry requirements

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

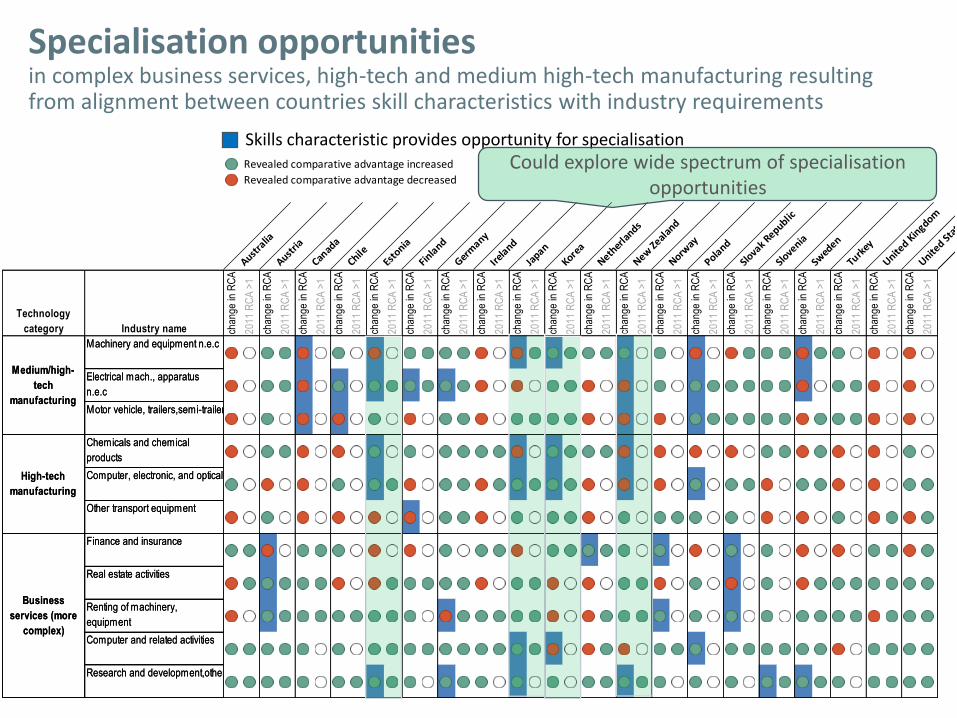

Skills characteristic provides opportunity for specialisationCould explore wide spectrum of specialisation

opportunities

Specialisation opportunitiesin complex business services, high-tech and medium high-tech manufacturing resulting from alignment between countries skill characteristics with industry requirements

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

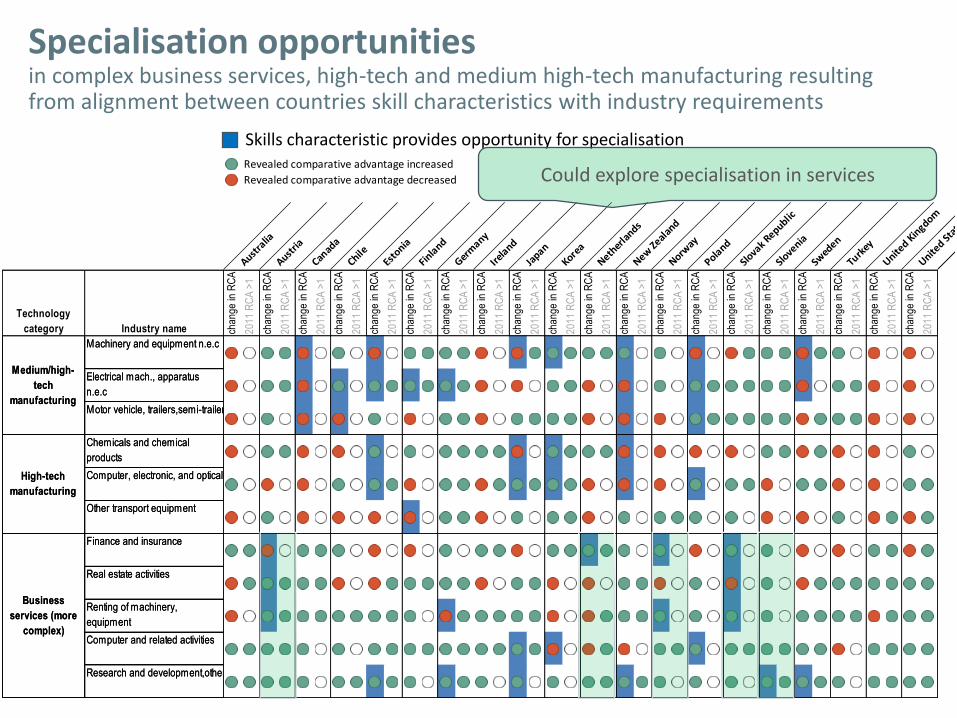

Skills characteristic provides opportunity for specialisation

Could explore specialisation in services

Specialisation opportunitiesin complex business services, high-tech and medium high-tech manufacturing resulting from alignment between countries skill characteristics with industry requirements

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

Revealed comparative advantage increased

Revealed comparative advantage decreased

Austra

lia

Austria

Canad

a

ChileEs

tonia

Finla

nd

Germ

any

Irela

nd

Japan

Korea

Nether

lands

New Zeal

and

Norway

Poland

Slova

k Republic

Slove

nia

Swed

en

Turk

ey

United K

ingdom

United St

ates

Technology

category Industry name chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

chan

ge in

RC

A

2011

RC

A >

1

Machinery and equipment n.e.c

Electrical mach., apparatus

n.e.c

Motor vehicle, trailers,semi-trailers

Chemicals and chemical

products

Computer, electronic, and optical

Other transport equipment

Finance and insurance

Real estate activities

Renting of machinery,

equipment

Computer and related activities

Research and development,others

Medium/high-

tech

manufacturing

High-tech

manufacturing

Business

services (more

complex)

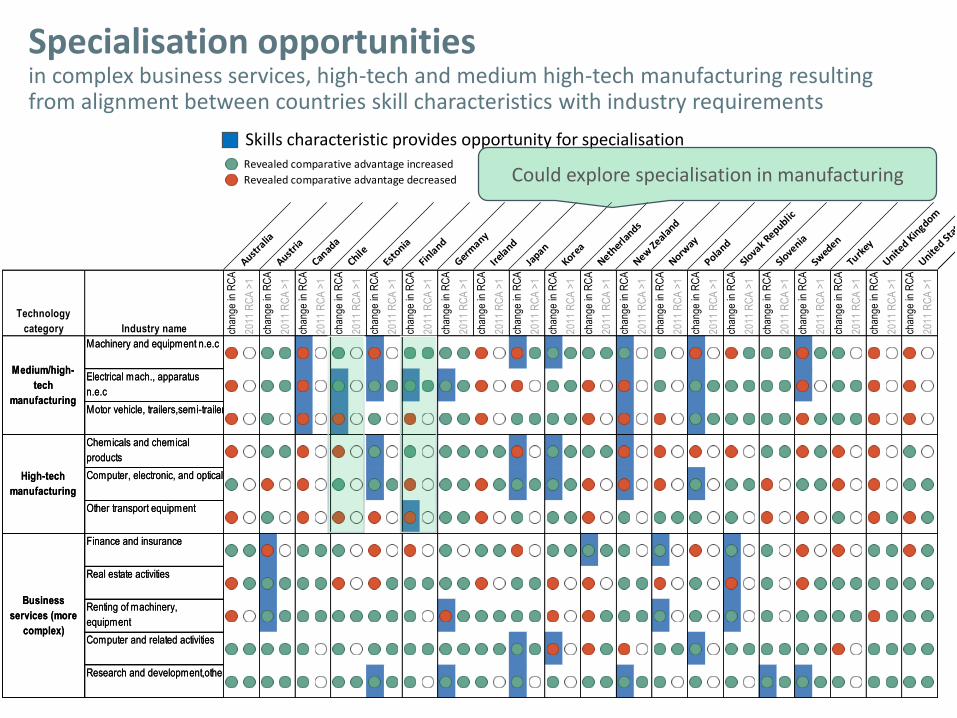

Skills characteristic provides opportunity for specialisation

Could explore specialisation in manufacturing

37

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

Limited share of low-skilled workers

To participate in GVCs, ensure that participation translates into productivity growth and limit risk of employment loss, increased inequality and poor job quality

Developing skills To ensure that participation in GVCs translates into good economic and social outcomes, countries need to raise skill outcomes

Advanced skills To specialise in technologically advanced industries, the quality of skills at the top end of the skill distribution are important

Increasing participation in GVCs

How successfully have countries extended their participation in GVCs by importing foreign inputs for exports and producing inputs used in other countries inputs

Specialised in advanced industries

Specialisation in technologically advanced industries is linked to value creation, innovation and productivity gains (revealed comparative advantage)

Increasing specialisation in advanced industries

How quickly has the revealed comparative advantage grown

Increasing productivity

Increased participation in GVCs can lead to productivity gains through many channels, including specialisation, increased competition and technology diffusion

Increasing employment

Participation in GVCs can affect employment through both job destruction and job creation

Improving social outcomes

Increased integration in GVCs can affect wages and inequalities, labour-market security and the quality of the working environment

38

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

39

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

UK

40

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

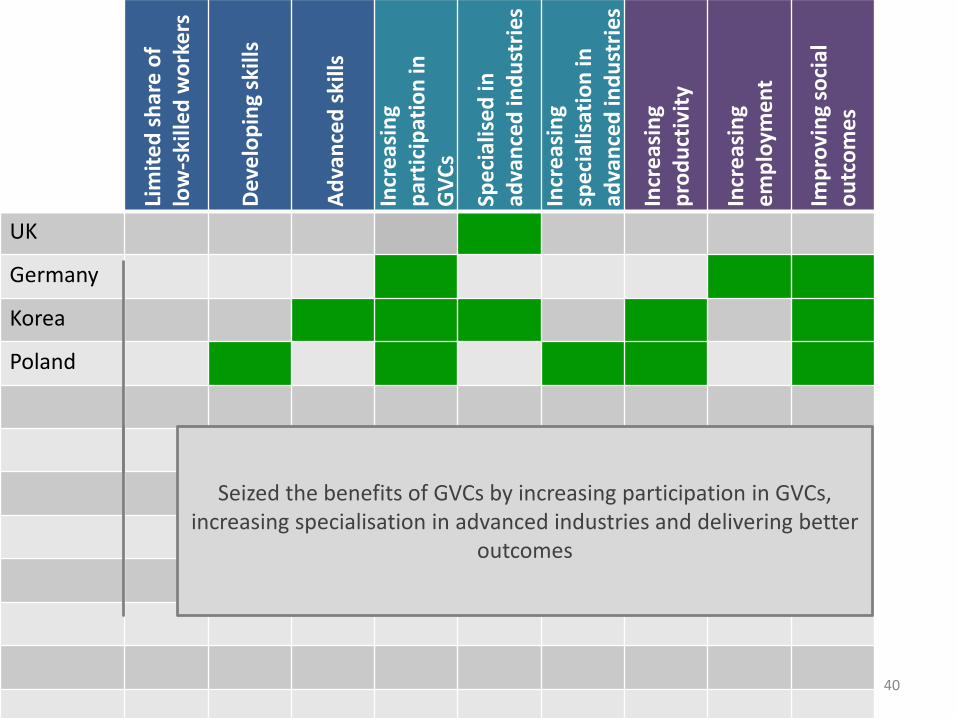

UK

Germany

Korea

Poland

Seized the benefits of GVCs by increasing participation in GVCs, increasing specialisation in advanced industries and delivering better

outcomes

41

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

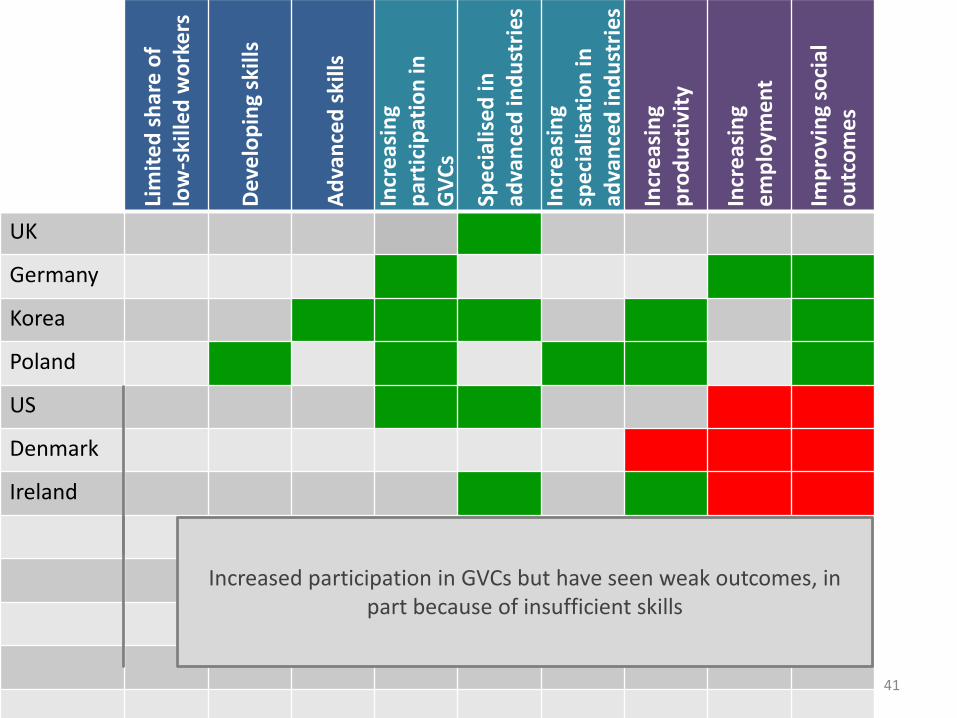

UK

Germany

Korea

Poland

US

Denmark

Ireland

Increased participation in GVCs but have seen weak outcomes, in part because of insufficient skills

42

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

UK

Germany

Korea

Poland

US

Denmark

Ireland

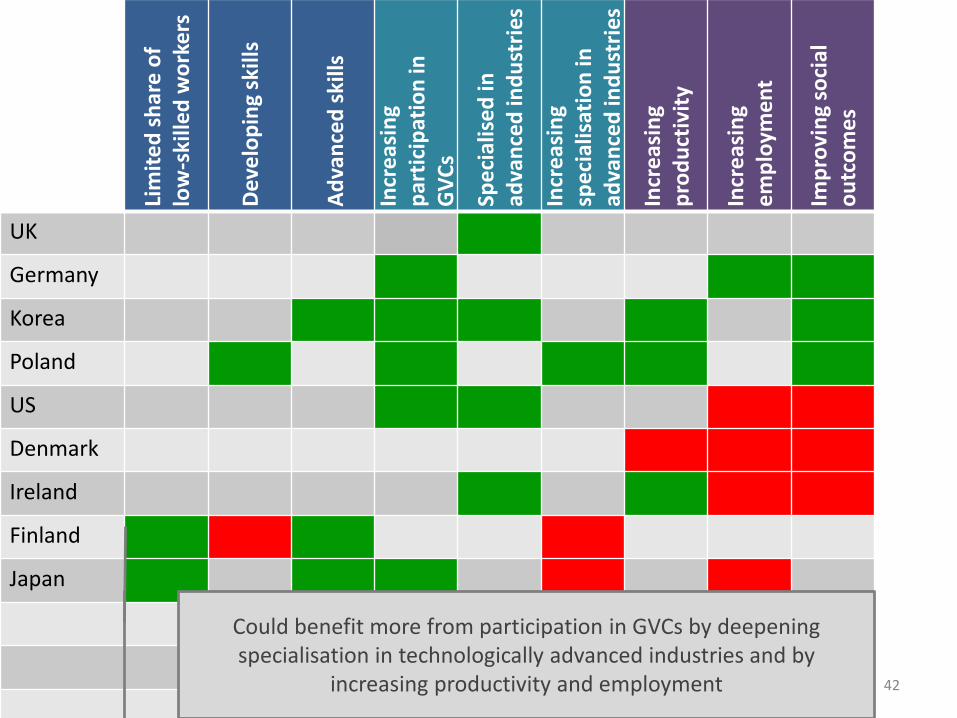

Finland

Japan

Could benefit more from participation in GVCs by deepening specialisation in technologically advanced industries and by

increasing productivity and employment

43

Lim

ite

d s

har

e o

f lo

w-s

kille

d w

ork

ers

De

velo

pin

g sk

ills

Ad

van

ced

ski

lls

Incr

eas

ing

par

tici

pat

ion

in

GV

Cs

Spe

cial

ised

in

adva

nce

d in

du

stri

es

Incr

eas

ing

spe

cial

isat

ion

in

adva

nce

d in

du

stri

es

Incr

eas

ing

pro

du

ctiv

ity

Incr

eas

ing

em

plo

ymen

t

Imp

rovi

ng

soci

al

ou

tco

me

s

UK

Germany

Korea

Poland

US

Denmark

Ireland

Finland

Japan

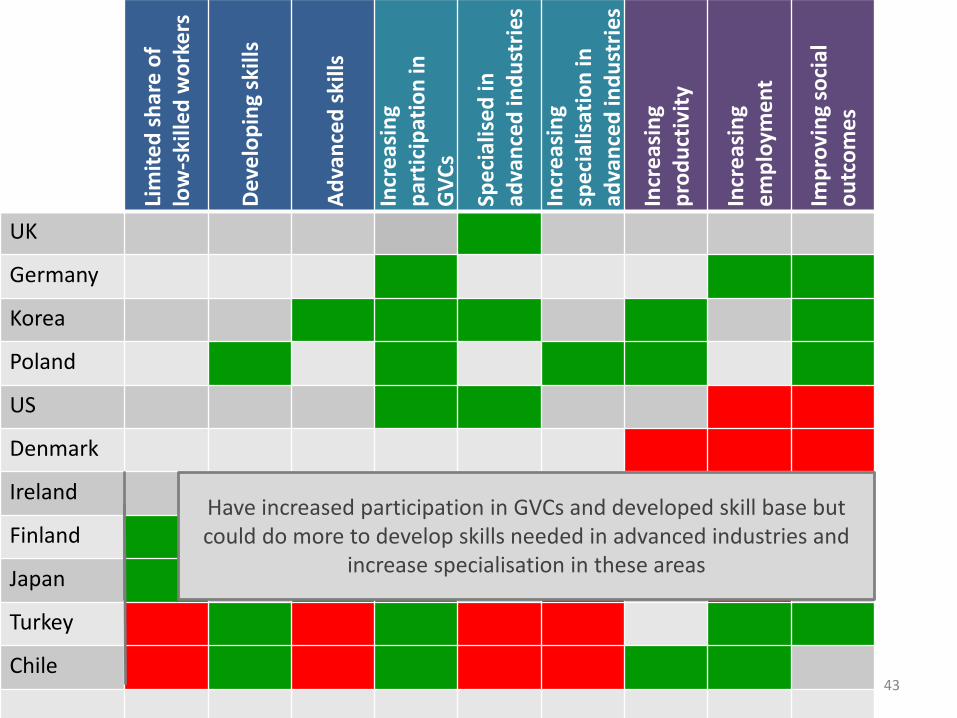

Turkey

Chile

Have increased participation in GVCs and developed skill base but could do more to develop skills needed in advanced industries and

increase specialisation in these areas

Implications for education and training policies

Implications for: Education and training policies

44

• Improve quality of education and training

• Better connect the worlds of learning and work– Countries comparative advantage emerges from interactions between skills

characteristics and industry requirements

• Remove barriers to further skills development– Don’t expect workers to accept they lose their jobs if they don’t feel

prepared to get or create a new one

45Implications for skills policies

180 200 220 240 260 280 300Score

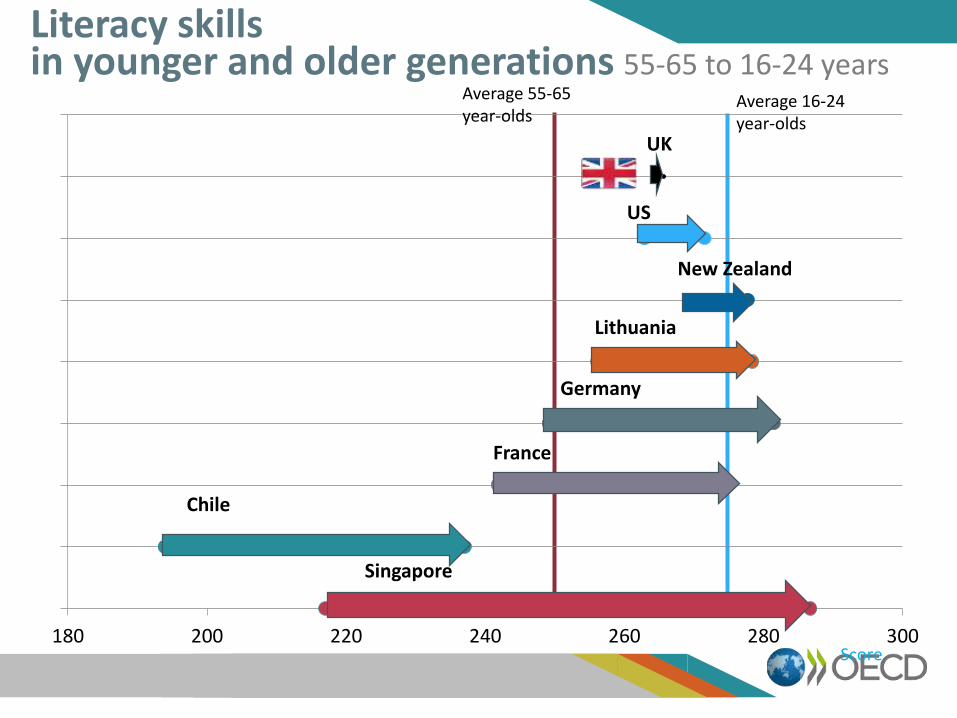

Literacy skillsin younger and older generations 55-65 to 16-24 years

Average 55-65 year-olds

Average 16-24 year-olds

Chile

Singapore

Lithuania

France

Germany

New Zealand

US

UK

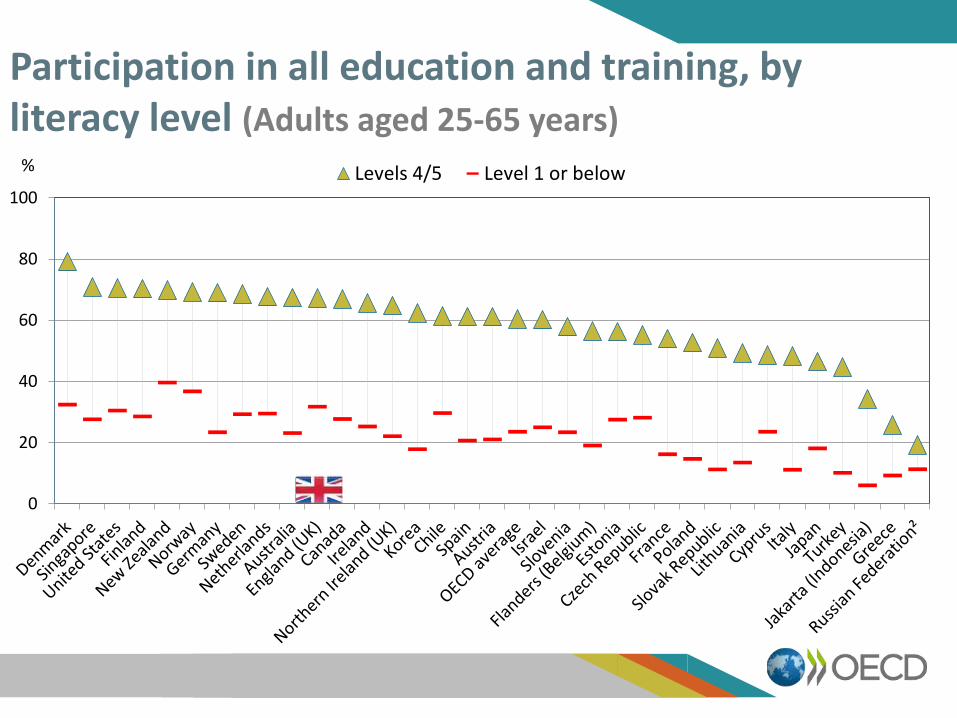

Participation in all education and training, by literacy level (Adults aged 25-65 years)

0

20

40

60

80

100

Levels 4/5 Level 1 or below%

• Improve quality of education and training

• Better connect the worlds of learning and work– Countries comparative advantage emerges from interactions between skills

characteristics and industry requirements

• Remove barriers to further skills development– Don’t expect workers to accept they lose their jobs if they don’t feel

prepared to get or create a new one

• Ensure relevant and reliable qualifications– There is huge variation in the skills of people with similar qualifications

48Implications for skills policies

49

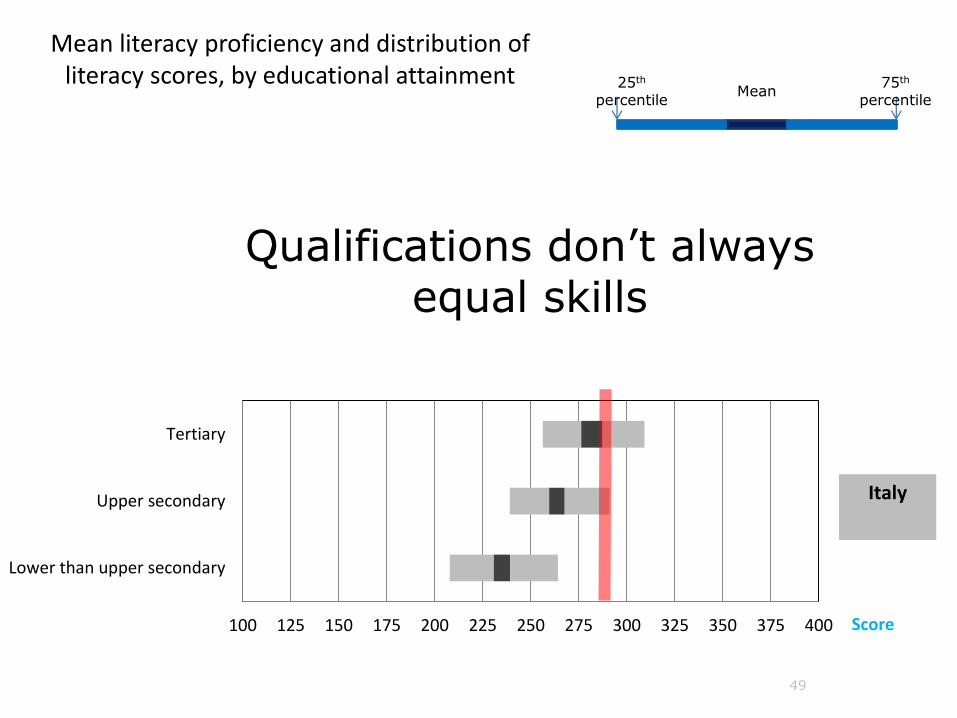

Mean literacy proficiency and distribution of literacy scores, by educational attainment

100 125 150 175 200 225 250 275 300 325 350 375 400

Lower than upper secondary

Upper secondary

Tertiary

Italy

Score

25th

percentileMean

75th

percentile

Lower than upper secondary

Upper secondary

Tertiary

100 125 150 175 200 225 250 275 300 325 350 375 400

Japan

Score

Qualifications don’t alwaysequal skills

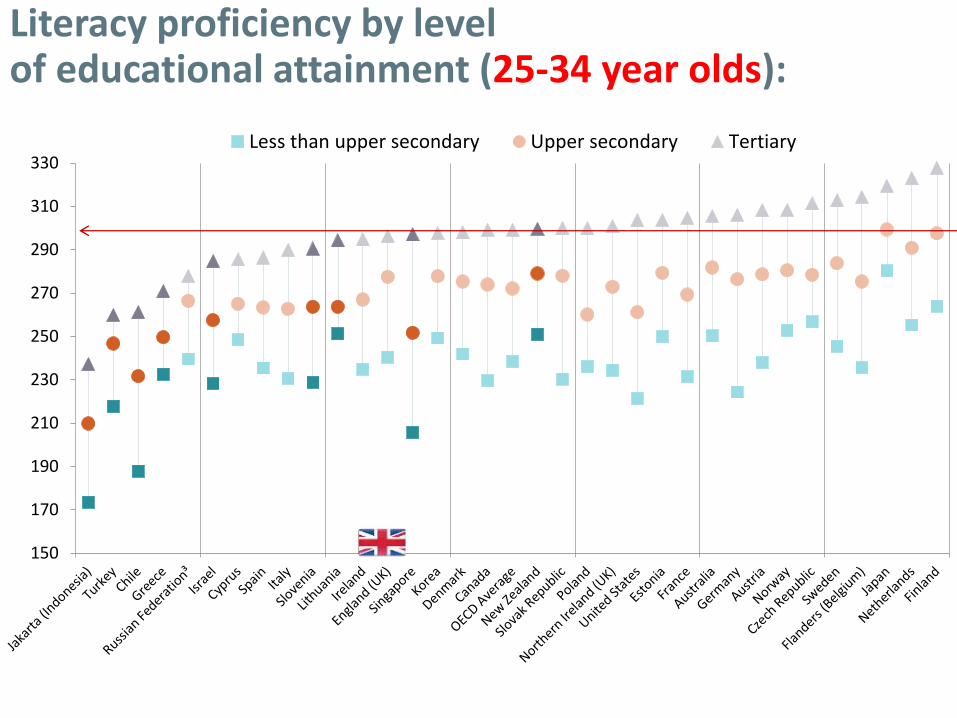

150

170

190

210

230

250

270

290

310

330Less than upper secondary Upper secondary Tertiary

Literacy proficiency by levelof educational attainment (25-34 year olds):

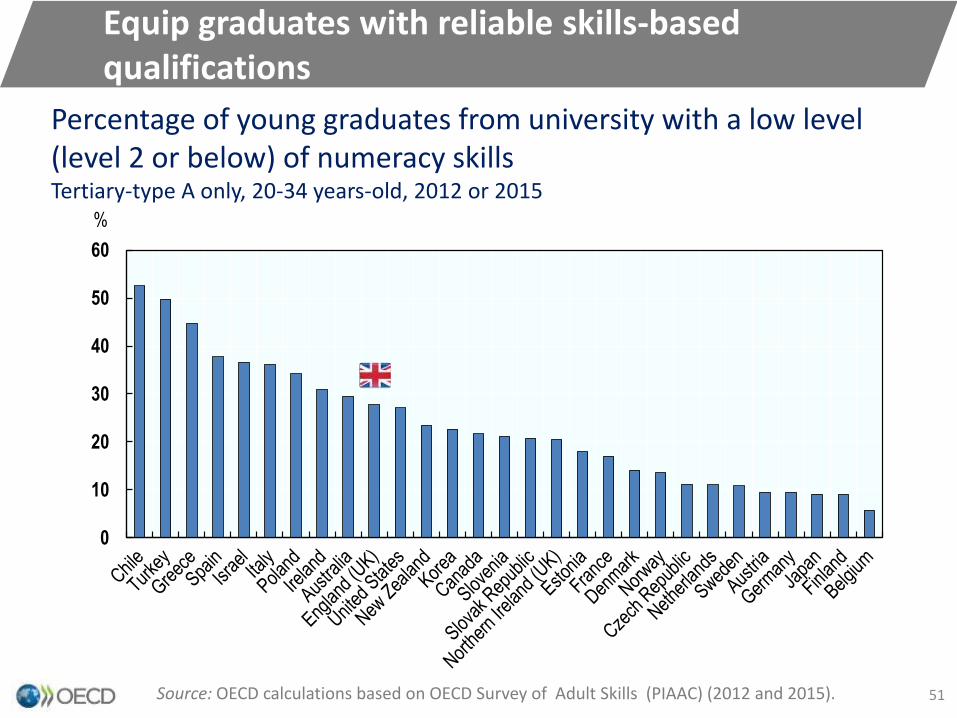

Equip graduates with reliable skills-based qualifications

0

10

20

30

40

50

60

%

Percentage of young graduates from university with a low level (level 2 or below) of numeracy skillsTertiary-type A only, 20-34 years-old, 2012 or 2015

Source: OECD calculations based on OECD Survey of Adult Skills (PIAAC) (2012 and 2015). 51

• Improve quality of education and training

• Better connect the worlds of learning and work– Countries comparative advantage emerges from interactions between skills

characteristics and industry requirements

• Remove barriers to further skills development– Don’t expect workers to accept they lose their jobs if they don’t feel

prepared to get or create a new one

• Ensure relevant and reliable qualifications– There is huge variation in the skills of people with similar qualifications

• Use skills more effectively– Skills can enable countries to perform well in GVCs, but only if people are

working where they use their skills effectively

– Combine flexibility to firms with security for workers

52Implications for skills policies

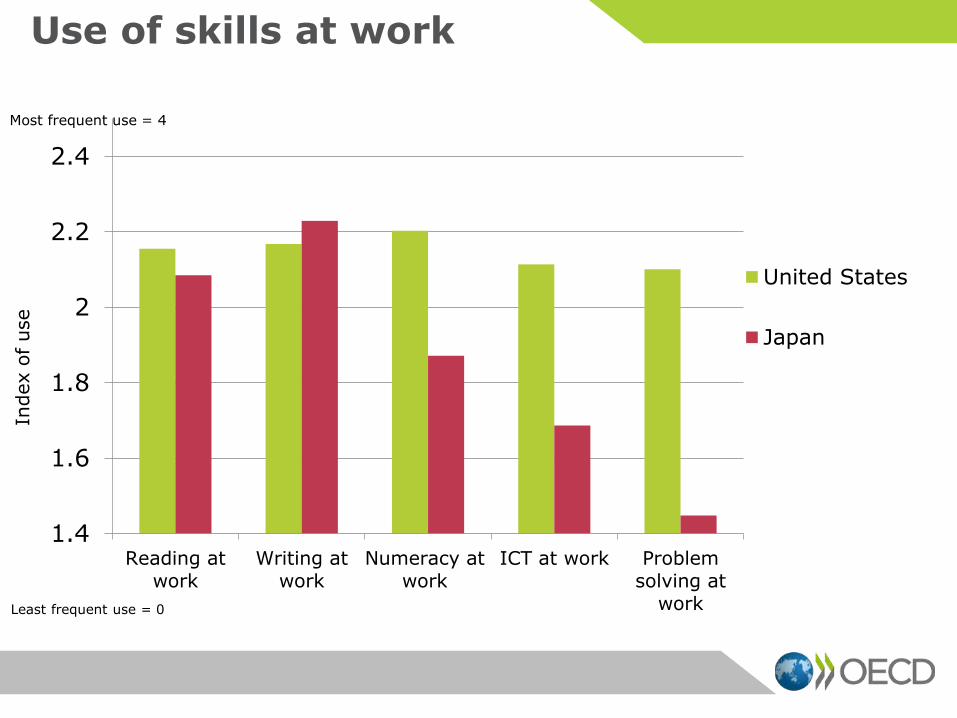

Use of skills at work

1.4

1.6

1.8

2

2.2

2.4

Reading atwork

Writing atwork

Numeracy atwork

ICT at work Problemsolving at

work

United States

Japan

Most frequent use = 4

Least frequent use = 0

Index o

f use

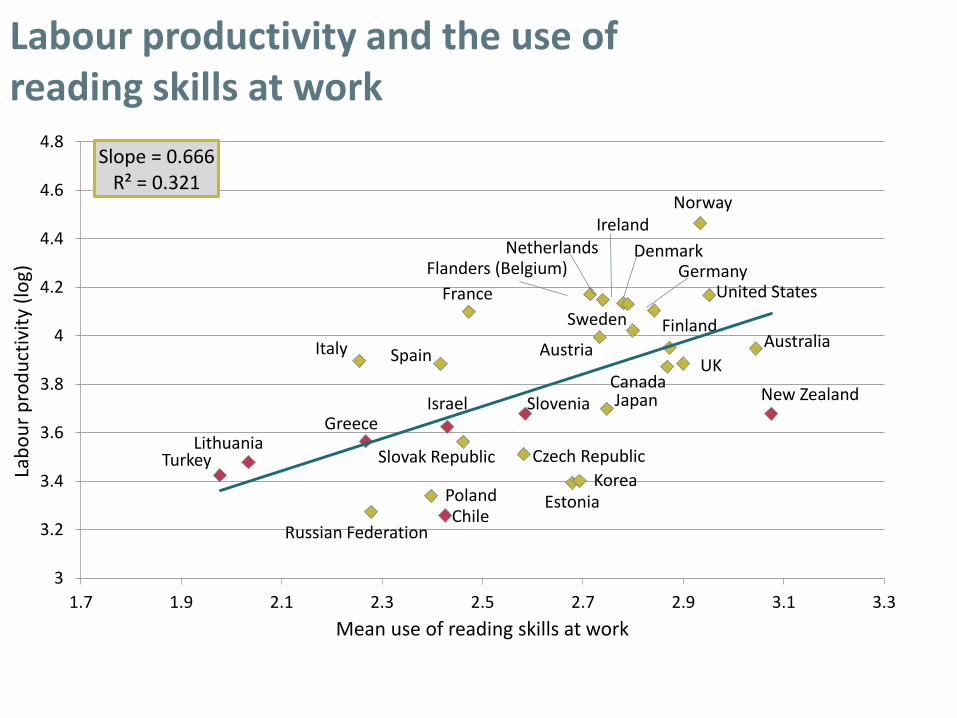

Labour productivity and the use of reading skills at work

AustraliaAustria

Canada

Chile

Czech Republic

Denmark

Estonia

Finland

Flanders (Belgium)

FranceGermany

Greece

Ireland

Israel

Italy

Japan

Korea

Lithuania

Netherlands

New Zealand

Norway

Poland

Russian Federation

Slovak Republic

Slovenia

Spain

Sweden

Turkey

UK

United States

Slope = 0.666R² = 0.321

3

3.2

3.4

3.6

3.8

4

4.2

4.4

4.6

4.8

1.7 1.9 2.1 2.3 2.5 2.7 2.9 3.1 3.3

Lab

ou

r p

rod

uct

ivit

y (l

og)

Mean use of reading skills at work

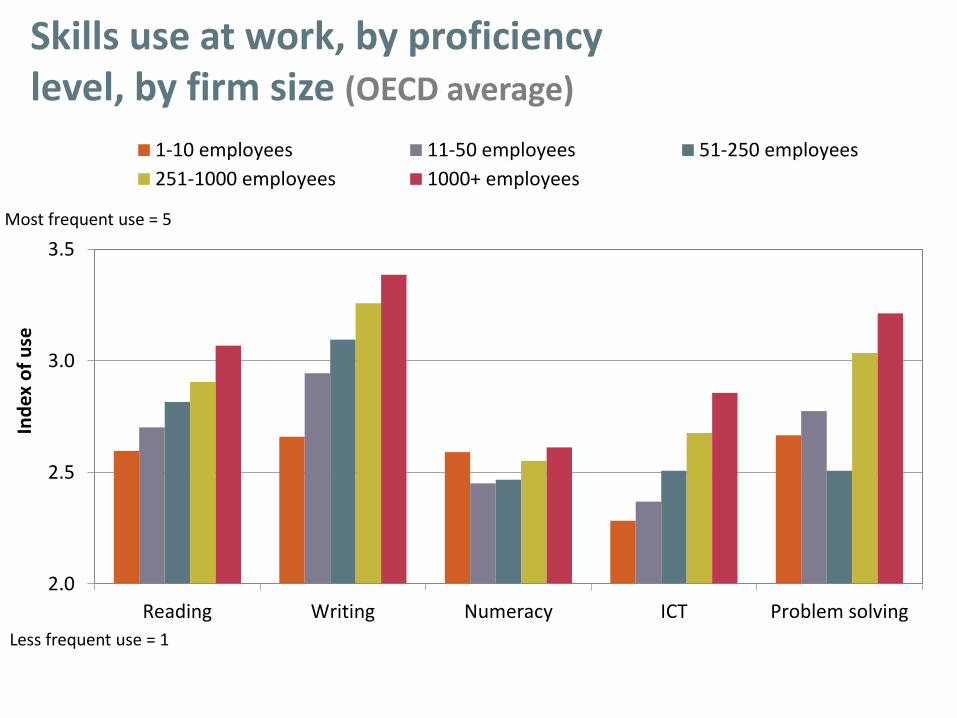

2.0

2.5

3.0

3.5

Reading Writing Numeracy ICT Problem solving

Ind

ex o

f u

se

1-10 employees 11-50 employees 51-250 employees

251-1000 employees 1000+ employees

Skills use at work, by proficiency level, by firm size (OECD average)

Most frequent use = 5

Less frequent use = 1

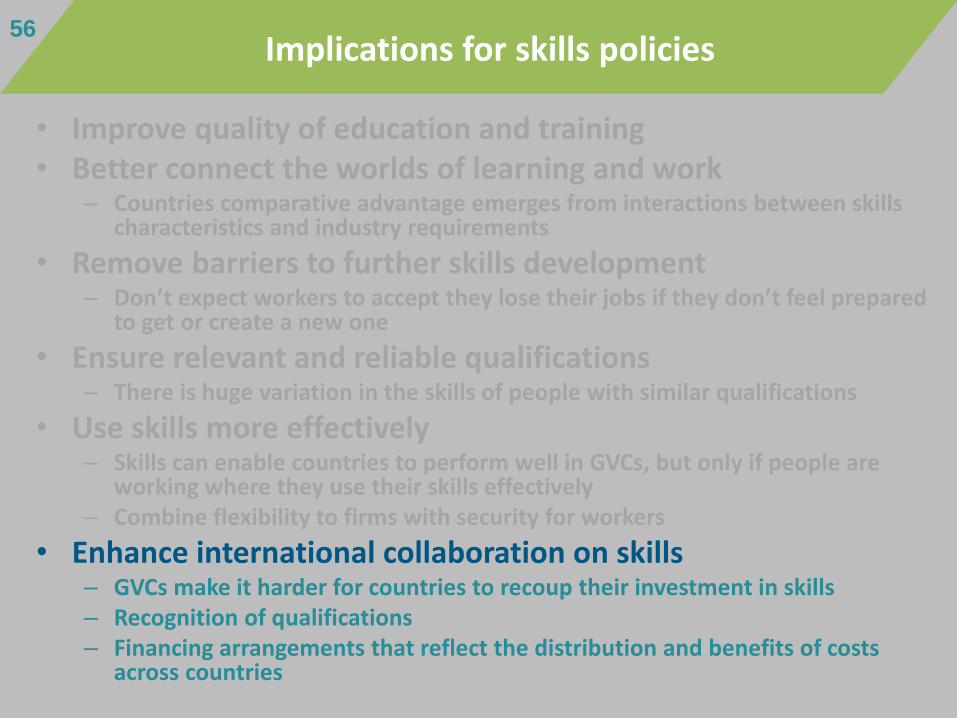

• Improve quality of education and training• Better connect the worlds of learning and work

– Countries comparative advantage emerges from interactions between skills characteristics and industry requirements

• Remove barriers to further skills development– Don’t expect workers to accept they lose their jobs if they don’t feel prepared

to get or create a new one

• Ensure relevant and reliable qualifications– There is huge variation in the skills of people with similar qualifications

• Use skills more effectively– Skills can enable countries to perform well in GVCs, but only if people are

working where they use their skills effectively– Combine flexibility to firms with security for workers

• Enhance international collaboration on skills– GVCs make it harder for countries to recoup their investment in skills– Recognition of qualifications– Financing arrangements that reflect the distribution and benefits of costs

across countries

56Implications for skills policies

Implications for education and training policies

Policy effort has to go beyond education and training policies

57

Adopt a whole-of-government approach

58

Co-ordinate these policies with other policy domains: Industry Innovation Trade Investment And others…

Look at full range of reforms affecting skills: Education and training Labour market Firms’ organisation and management

practices Migration And others…

59

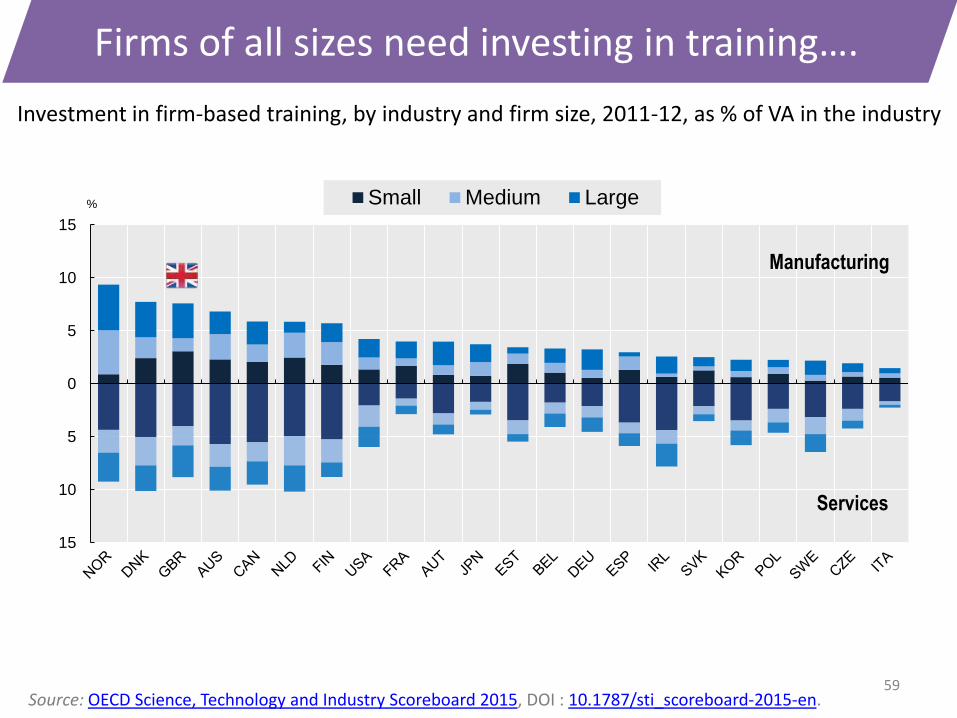

Firms of all sizes need investing in training….

15

10

5

0

5

10

15

% Small Medium Large

Manufacturing

Services

Investment in firm-based training, by industry and firm size, 2011-12, as % of VA in the industry

Source: OECD Science, Technology and Industry Scoreboard 2015, DOI : 10.1787/sti_scoreboard-2015-en.

… and financial incentives aligned for skills development

0

2

4

6

8

10

12

14

% of wage before education

How much earning needs to increase after education so that people earn back the cost of an investment in lifelong learning

Source: OECD (2017), Taxation and Skills, OECD Tax Policy Studies, No. 24.

Financial incentives are low

60

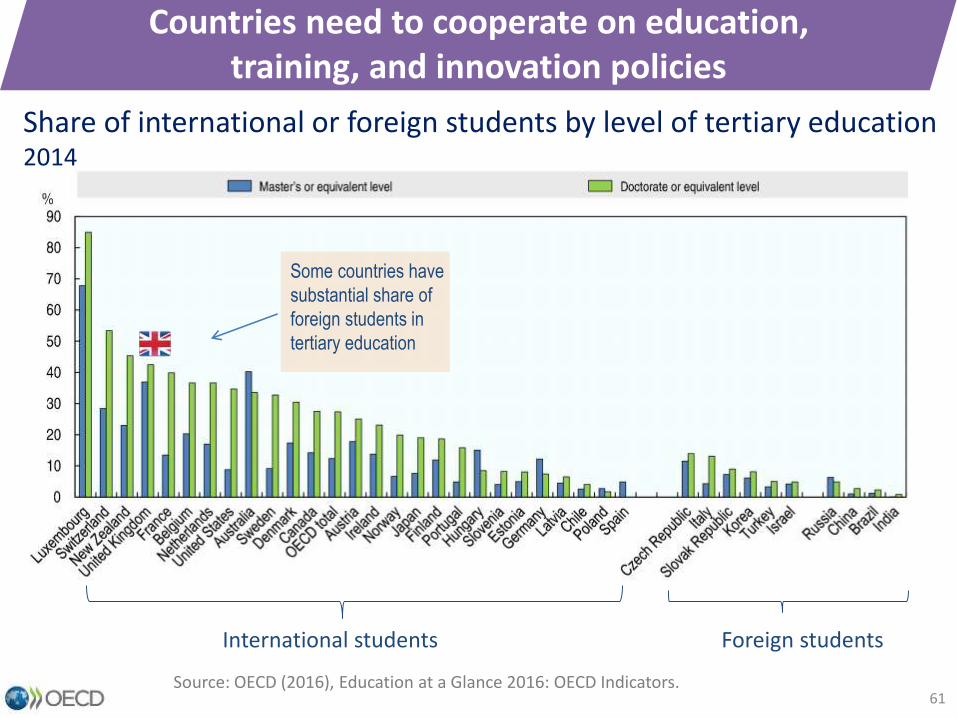

Countries need to cooperate on education, training, and innovation policies

Share of international or foreign students by level of tertiary education 2014

International students Foreign students

Some countries have

substantial share of

foreign students in

tertiary education

Source: OECD (2016), Education at a Glance 2016: OECD Indicators.61

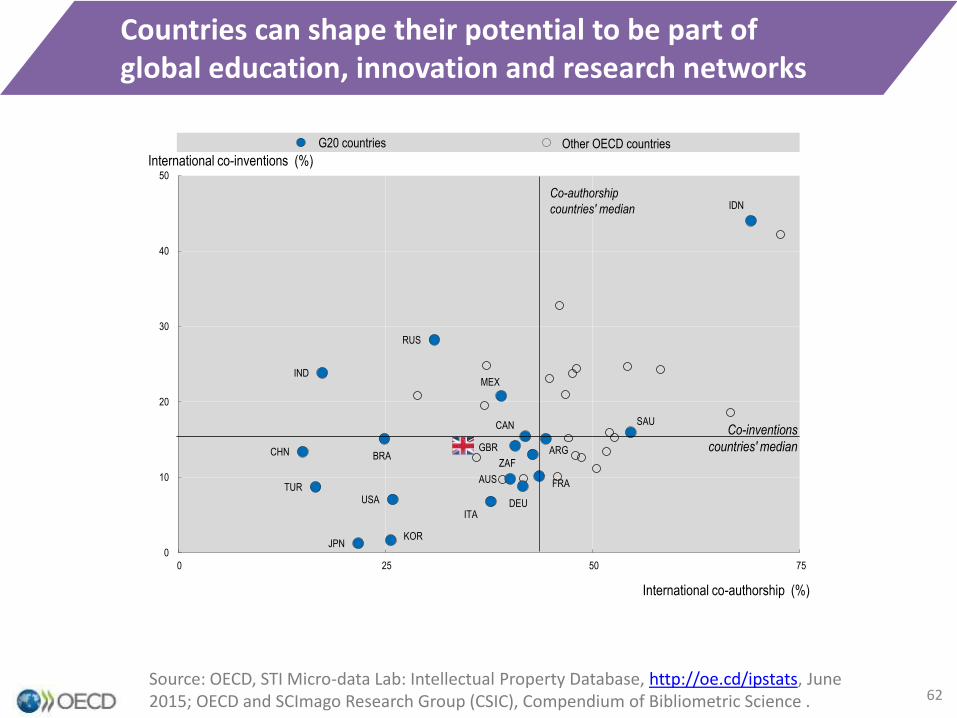

Countries can shape their potential to be part of global education, innovation and research networks

Source: OECD, STI Micro-data Lab: Intellectual Property Database, http://oe.cd/ipstats, June 2015; OECD and SCImago Research Group (CSIC), Compendium of Bibliometric Science . 62

ARG

AUS

BRA

CAN

CHN

FRA

DEU

IND

IDN

ITA

JPNKOR

MEX

RUS

SAU

ZAF

TUR

GBR

USA

0

10

20

30

40

50

0 25 50 75

International co-inventions (%)

International co-authorship (%)

G20 countries Other OECD countries

Co-inventions

countries' median

Co-authorship

countries' median

Implications for education and training policies

Implications for: Education and training policies

63

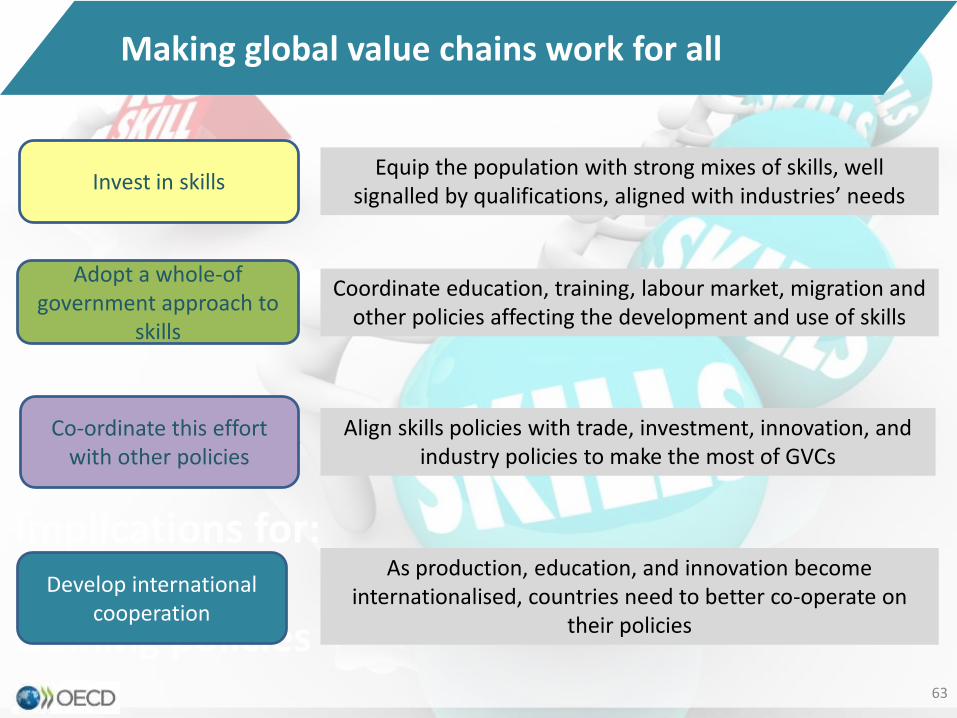

Making global value chains work for all

Invest in skills

Adopt a whole-of government approach to

skills

Co-ordinate this effort with other policies

Develop international cooperation

Equip the population with strong mixes of skills, well signalled by qualifications, aligned with industries’ needs

Coordinate education, training, labour market, migration and other policies affecting the development and use of skills

Align skills policies with trade, investment, innovation, and industry policies to make the most of GVCs

As production, education, and innovation become internationalised, countries need to better co-operate on

their policies