OCBOA Accounting and Auditing - CPAライセンス申請サ...

245

1 OCBOA Accounting and Auditing by Publish Date 7-2-2013

Transcript of OCBOA Accounting and Auditing - CPAライセンス申請サ...

1

OCBOA Accounting and Auditing

by

Publish Date 7-2-2013

3

Contents Chapter 1 - Other Comprehensive Bases of Accounting .................................... 14

OBJECTIVES .................................................................................................. 14 OVERVIEW ..................................................................................................... 14 Pure Cash Basis .............................................................................................. 15 Modified Cash Basis ........................................................................................ 15 Income Tax Basis ............................................................................................ 16 HISTORY OF OCBOA AND ACCOUNTING STANDARDS ............................ 16 DETERMINING WHETHER TO ISSUE OCBOA FINANCIAL STATEMENTS 17 BASIC FINANCIAL STATEMENTS ................................................................. 20 Economic Resources and Obligations ............................................................. 21 Changes in Economic Resources and Obligations .......................................... 21 Cash Flows ..................................................................................................... 21 Financial Statement Titles ............................................................................... 22 KEY ISSUES IN PREPARING OCBOA FINANCIAL STATEMENTS .............. 22 Recognition ..................................................................................................... 23 Measurement .................................................................................................. 23 Presentation .................................................................................................... 23 Disclosures ...................................................................................................... 24 Reporting ......................................................................................................... 24 GENERALLY ACCEPTED ACCOUNTING PRINCIPLES ............................... 24

CHAPTER 2 ........................................................................................................ 29 OBJECTIVES .................................................................................................. 29 OVERVIEW ..................................................................................................... 29 THE AICPA CODE OF PROFESSIONAL CONDUCT .................................... 29 Form and Content ........................................................................................... 30 Rule 201: General Standards .......................................................................... 31 Professional Competence ............................................................................... 31 Due Professional Care .................................................................................... 31 Planning and Supervision ................................................................................ 32 Sufficient Relevant Data .................................................................................. 32 Rule 202: Compliance with Standards ............................................................ 32 Interpretations of Rules of Conduct ................................................................. 33 Ethics Rulings .................................................................................................. 33 OCBOA FINANCIAL STATEMENT GUIDANCE ............................................. 33 AU Section 623 ............................................................................................... 34 Financial Statement Titles ............................................................................... 34 Disclosures ...................................................................................................... 35 AU Section 623 Interpretation ......................................................................... 35 AR Section 100 and Related Interpretation ..................................................... 38 Technical Practice Aids ................................................................................... 39 STATEMENTS ON QUALITY CONTROL STANDARDS ................................ 41 Elements of a Quality Control System ............................................................. 41 Independence, Integrity, and Objectivity ......................................................... 42 Personnel Management ........................................................................................................ 42

Acceptance and Continuance of Clients and Engagements .................................................. 42

4

Engagement Performance ..................................................................................................... 43

Monitoring ............................................................................................................................. 43

Administration of the Quality Control System .................................................. 43 Monitoring a Firm's System of Quality Control ................................................ 44 Inspection Procedures ........................................................................................................... 44

Pre‐Issuance or Post‐Issuance Review of Selected Engagements ......................................... 45

Practitioner-in-Charge ..................................................................................... 45 Personnel Management .................................................................................. 46 Competencies ................................................................................................. 46 Gaining Competencies .................................................................................... 47 Competencies Expected in Performing Accounting, Auditing, and Attestation Engagements .................................................................................................. 49 Interrelationship of Competencies and Other Elements of a Firm's System of Quality Control ................................................................................................. 50 The Relationship of the Competency Requirement of the Uniform Accountancy Act to the Personnel Management Element of Quality Control ....................... 50 History of Peer Review .................................................................................... 51 Objectives of Peer Review .............................................................................. 51 Strategies for Peer Review .............................................................................. 52 Philosophy at the Top ............................................................................................................ 52

Communicate the Philosophy ............................................................................................... 53

Identify a Coordinator ........................................................................................................... 53

Institute an Internal Inspection Process ................................................................................ 53

Prepare for the Recommendations ....................................................................................... 53

Peer Review Follow‐up .......................................................................................................... 54

Chapter 3 – Engagement Planning and Consideration ....................................... 55 OBJECTIVES .................................................................................................. 55 OVERVIEW ..................................................................................................... 55 CLIENT ACCEPTANCE AND RETENTION .................................................... 55 Ethical Considerations ..................................................................................... 56 Independence ........................................................................................................................ 56

Management Integrity........................................................................................................... 56

Professional Competency and Staff Availability .................................................................... 56

CLIENT ACCEPTANCE PROCEDURES ........................................................ 57 Evaluate Prospective Clients ........................................................................... 57 Interview the Prospective Client ...................................................................... 58 Read the Prospective Client's Financial Statements ....................................... 58 Develop a Preliminary Understanding of the Prospective Client's Accounting Records ........................................................................................................... 59 Contact Third Parties Familiar with the Prospective Client .............................. 60 Identify Intended Users of the Financial Statements ....................................... 60 Assess the Firm's Capabilities ......................................................................... 60 OTHER ENGAGEMENT ACCEPTANCE CONSIDERATIONS ....................... 60 Recognizing Danger Signs .............................................................................. 60 Valuable Lessons from Litigation ..................................................................... 61

5

Documentation ................................................................................................ 62 INDEPENDENCE CONSIDERATIONS ........................................................... 62 Understanding the Nature of the Services ....................................................... 63 Evaluating the Client's Understanding of Its Responsibilities .......................... 64 Bookkeeping.................................................................................................... 65 Payroll and Other Disbursement ..................................................................... 65 Benefit Plan Administration ............................................................................. 66 Investment Advising and Investment Managing .............................................. 66 Corporate Finance Consulting and Advising ................................................... 66 Appraisal, Valuation, and Actuarial .................................................................. 67 Executive and Employee Search ..................................................................... 67 Business Risk Consulting ................................................................................ 67 COMMUNICATION WITH THE PREDECESSOR CPA .................................. 68 Audit Engagements ......................................................................................... 68 Compilation and Review Engagements ........................................................... 69 ESTABLISHING AN UNDERSTANDING WITH THE CLIENT ........................ 71 Audit Engagements ......................................................................................... 71 Engagement Letters ........................................................................................ 72 Other Engagement Letter Considerations ............................................................................. 73

Compilation and Review Engagements ........................................................... 73 Scope of the Engagement ............................................................................... 75 Identification of Financial Statements Presented ................................................................. 75

Identification of the Number of Reporting Periods............................................................... 76

Identification of Accounting Methods Used and Any Departures ........................................ 76

Footnote Disclosures Required ............................................................................................. 76

Presentation of Supplementary Information ........................................................................ 77

The Engagement Letter ......................................................................................................... 77

Other Documentation Methods ............................................................................................ 78

Chapter 4 - Primary Financial Statement Considerations ................................... 79 OBJECTIVES .................................................................................................. 79 PRIMARY FINANCIAL STATEMENTS ........................................................... 79 Economic Resources and Obligations ............................................................. 80 Changes in Economic Resources and Obligations .......................................... 80 Cash Flows ..................................................................................................... 80 Statement of Retained Earnings ...................................................................... 81 Comprehensive Income .................................................................................. 81 Presentation .................................................................................................... 81 FINANCIAL STATEMENT TITLES .................................................................. 82 Balance Sheet Title Alternatives ...................................................................... 83 Income Statement Title Alternatives ................................................................ 83 Statement of Cash Flows Title Alternatives ..................................................... 83 FINANCIAL STATEMENT CAPTIONS ............................................................ 84 Classified versus Unclassified Presentation .................................................... 84 OTHER PRESENTATION ISSUES ................................................................. 85 Consolidation Accounting ................................................................................ 85 Change from GAAP to OCBOA ....................................................................... 86

6

REFERENCES IN THE FINANCIAL STATEMENTS ...................................... 86 References to the Notes .................................................................................. 86 References to Selected Information ................................................................ 87 References to the Accountant's Report ........................................................... 87 Management-Use-Only Financial Statements ................................................. 87 Placing the Reference ..................................................................................... 88 FINANCIAL STATEMENT DISCLOSURES .................................................... 88 Format of Disclosures ..................................................................................... 88 Title of Notes ................................................................................................... 88 Summary of Significant Accounting Policies ................................................... 89 Specific Disclosures ........................................................................................ 90 Cash basis .............................................................................................................................. 90

Tax basis ................................................................................................................................ 90

Interim Financial Statements ........................................................................... 91 Financial Statement Items ............................................................................... 91 Assets and Liabilities ....................................................................................... 92 Stockholders' Equity ........................................................................................ 92 Subsequent Events ......................................................................................... 92 Risks and Uncertainties ................................................................................... 93 Omission of Disclosures .................................................................................. 93 SUPPLEMENTARY INFORMATION ............................................................... 94 Reporting on Supplementary Information ........................................................ 95 FORM AND STYLE OF PRESENTATION ...................................................... 96 Title Page ........................................................................................................ 96 Accountant's Report ........................................................................................ 96

Chapter 5 - Cash and Modified Cash-Basis Financial Statements...................... 98 OBJECTIVES .................................................................................................. 98 OVERVIEW OF CASH-BASIS FINANCIAL STATEMENTS ............................ 98 Pure Cash Basis of Accounting ....................................................................... 98 Modified Cash Basis of Accounting ................................................................. 99 ISSUES TO CONSIDER IN CASH-BASIS FINANCIAL STATEMENTS ....... 100 Choosing the Appropriate Basis of Accounting ............................................. 100 Change in Basis of Accounting ...................................................................... 101 Change in Accounting Principle..................................................................... 101 Changes in Equity Accounts ......................................................................... 102 Statement of Cash Flows .............................................................................. 103 PURE CASH BASIS ...................................................................................... 103 Measurement and Recognition Considerations ............................................. 103 Cash and Cash Equivalents .................................................................................................. 103

Investments ......................................................................................................................... 104

Property, Plant, and Equipment .......................................................................................... 104

Debt ..................................................................................................................................... 104

Agency Transactions ............................................................................................................ 104

Income Taxes ....................................................................................................................... 104

MODIFIED CASH BASIS .............................................................................. 104 Acceptable Modifications ............................................................................... 105

7

Modified Cash Basis versus GAAP ............................................................... 106 Measurement and Recognition Considerations ............................................. 106 Inventory ............................................................................................................................. 107

Non‐ Trade Receivables ....................................................................................................... 107

Investments ......................................................................................................................... 108

Prepaid Expenses ................................................................................................................. 108

Property, Plant, and Equipment .......................................................................................... 108

Depreciation ........................................................................................................................ 109

Current and Long‐Term Liabilities ....................................................................................... 109

Revenue ............................................................................................................................... 109

Income Taxes ....................................................................................................................... 109

DISCLOSURES IN CASH-BASIS FINANCIAL STATEMENTS ..................... 109 Recommendations ........................................................................................ 110 Basis of Accounting ....................................................................................... 110 Pure Cash Basis .................................................................................................................... 110

Modified Cash Basis ............................................................................................................. 111

Summary of Significant Accounting Policies ................................................. 111 Income Taxes ....................................................................................................................... 112

Consolidation ....................................................................................................................... 112

Inventory ............................................................................................................................. 113

Property and Equipment ..................................................................................................... 113

Commitments and Contingencies .................................................................. 114 Uncertainties ................................................................................................. 115 Subsequent Events ....................................................................................... 116 Asset Impairment .......................................................................................... 116 Changes in Accounting Principles or Estimates ............................................ 116 Investments ................................................................................................... 116 Property and Equipment ................................................................................ 117 Terms of Debt Agreements ........................................................................... 117 Restrictions on Assets and Equity ................................................................. 117 Employee Benefit Plans ................................................................................ 117 Income Taxes ................................................................................................ 117 Disclosures in Pure Cash-Basis Presentations ............................................. 117

Chapter 6 - Income Tax Basis Financial Statements ........................................ 119 OBJECTIVES ................................................................................................ 119 OVERVIEW ................................................................................................... 119 IRS ACCOUNTING METHODS .................................................................... 120 Inventories ..................................................................................................... 120 Exceptions ..................................................................................................... 121 Qualifying Small Business Taxpayer ............................................................. 121 Qualifying Taxpayer ...................................................................................... 122 Methods Permitted ........................................................................................ 122 C Corporations ..................................................................................................................... 122

S Corporations ..................................................................................................................... 122

8

Partnerships ......................................................................................................................... 122

Sole Proprietorships ............................................................................................................ 122

ISSUES TO CONSIDER IN INCOME TAX BASIS FINANCIAL STATEMENTS ...................................................................................................................... 123 Nontaxed Entities .......................................................................................... 123 Nontaxable Revenues and Nondeductible Expenses .................................... 123 Tax Changes ................................................................................................. 124 Change in Basis of Accounting ............................................................................................. 124

Change in Tax Law or Accounting Principle ......................................................................... 124

Change in Fiscal Year ........................................................................................................... 125

Changes in Equity and Capital Accounts ............................................................................. 126

ACCRUAL METHOD ..................................................................................... 126 Safe Harbor Rule ........................................................................................... 127 Recurring Item Exception .............................................................................. 127 Revenue and Expense Measurement and Presentation Issues .................... 128 Revenues ............................................................................................................................. 128

Rental Income and Expense ................................................................................................ 128

Nontaxable Revenues and Nondeductible Expenses .......................................................... 129

Balance Sheet Measurement and Presentation Issues ................................. 129 Receivables .......................................................................................................................... 129

Inventories ........................................................................................................................... 129

Investments ......................................................................................................................... 130

Prepaid Expenses ................................................................................................................. 130

Property and Equipment ..................................................................................................... 130

Intangible Assets.................................................................................................................. 131

Liabilities .............................................................................................................................. 131

CASH METHOD ............................................................................................ 131 Constructive Receipt ..................................................................................... 131 Expenses ...................................................................................................... 132 Measurement and Presentation Issues ......................................................... 132 Inventories ........................................................................................................................... 132

Prepaid Expenses ................................................................................................................. 132

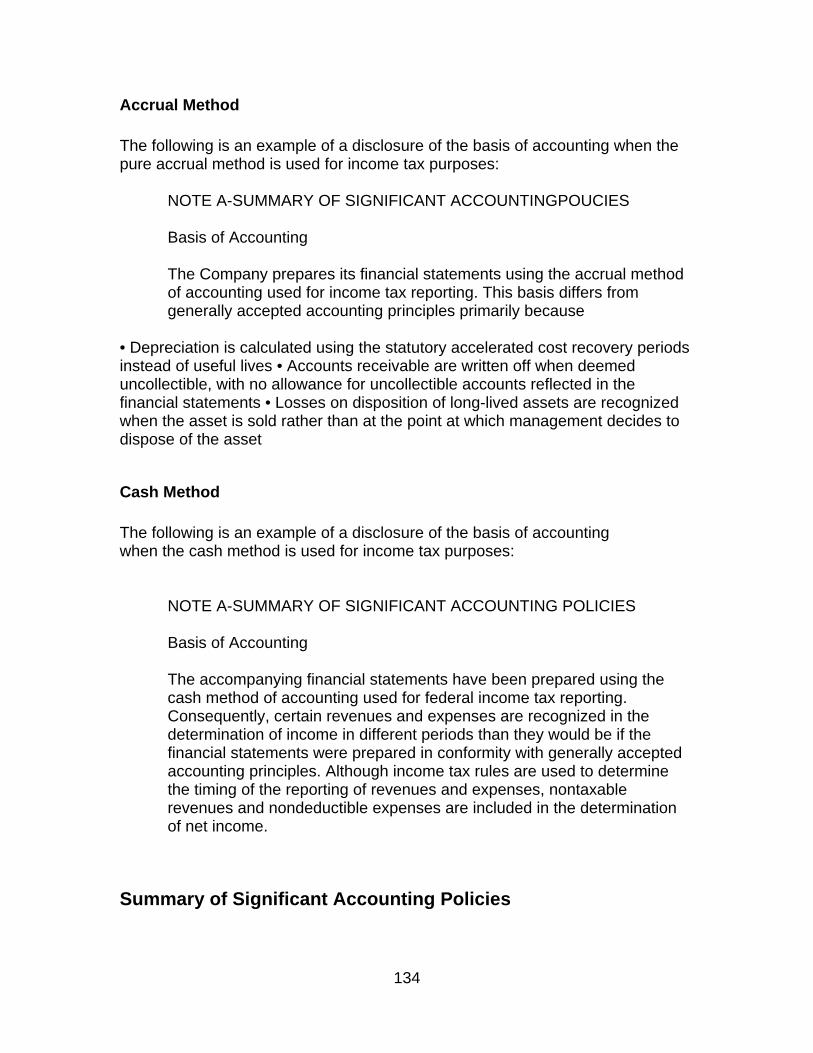

DISCLOSURES IN INCOME TAX BASIS FINANCIAL STATEMENTS ......... 133 Recommendations ........................................................................................ 133 Basis of Accounting ....................................................................................... 133 Accrual Method ................................................................................................................... 134

Cash Method ....................................................................................................................... 134

Summary of Significant Accounting Policies ................................................. 134 Income Taxes ....................................................................................................................... 135

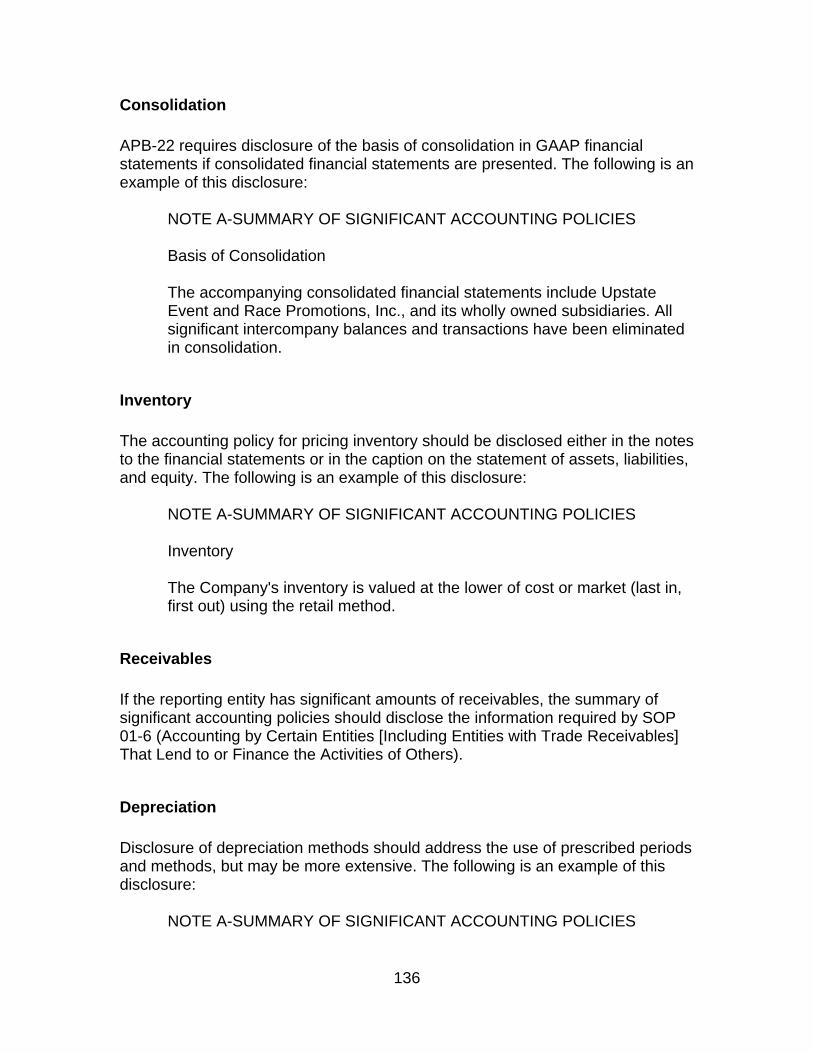

Consolidation ....................................................................................................................... 136

Inventory ............................................................................................................................. 136

Receivables .......................................................................................................................... 136

Depreciation ........................................................................................................................ 136

Start‐Up Costs ...................................................................................................................... 137

9

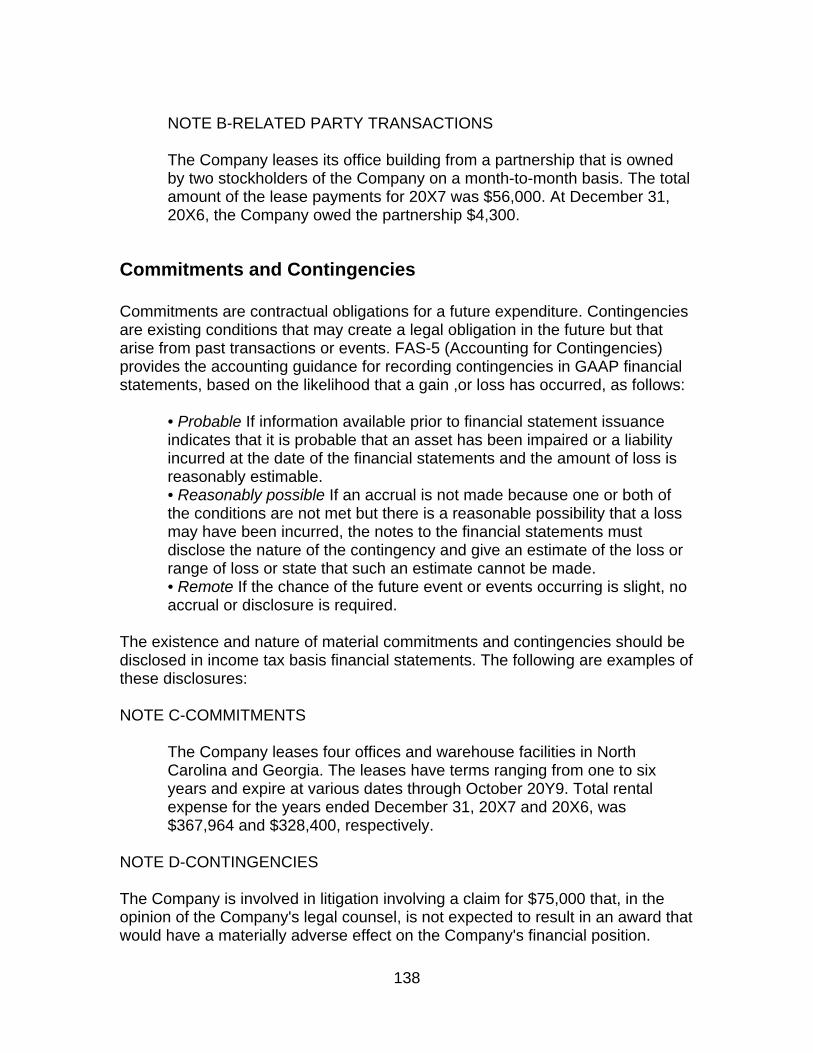

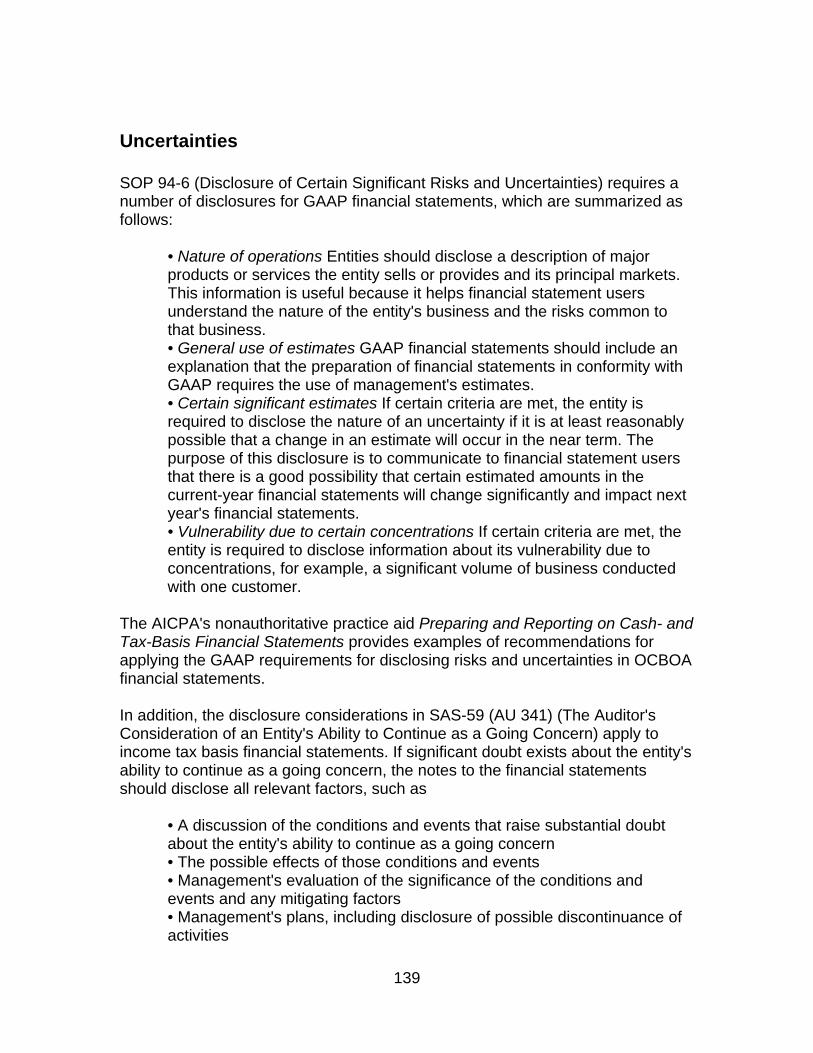

Related- Party Transactions .......................................................................... 137 Commitments and Contingencies .................................................................. 138 Uncertainties ................................................................................................. 139 Subsequent Events ....................................................................................... 140 Asset Impairment .......................................................................................... 140 Changes in Accounting Principles or Estimates ............................................ 140 Investments ................................................................................................... 140 Property and Equipment ................................................................................ 141 Terms of Debt Agreements ........................................................................... 141 Restrictions on Assets and Equity ................................................................. 141 Employee Benefit Plans ................................................................................ 141 Income Taxes ................................................................................................ 141

Chapter 7 – Other Basis of Accounting ............................................................. 143 OBJECTIVES ................................................................................................ 143 INTRODUCTION ........................................................................................... 143 REGULATORY BASIS OF ACCOUNTING ................................................... 143 Insurance Companies ................................................................................... 143 Regulatory Basis versus Contractual Basis ................................................... 144 Insurance Companies ................................................................................... 144 Financial Institutions ...................................................................................... 148 Not-for-Profit Organizations ........................................................................... 148 Construction Contractors ............................................................................... 149 Prescribed Forms .......................................................................................... 149 OTHER BASES OF ACCOUNTING .............................................................. 150 Substantial Support ....................................................................................... 150 Definite Criteria .............................................................................................. 151 All Material Items ........................................................................................... 151 Price-Level Basis ........................................................................................... 151 Current Value Basis ...................................................................................... 152 Liquidation Basis ........................................................................................... 154 Agreed-Upon Basis ....................................................................................... 154 Incomplete Presentations ................................................................................................... 155

Presentation That Is not in Conformity with GAAP or OCBOA ...................... 158 Chapter 8 – Unique Entities .............................................................................. 162

OBJECTIVES ................................................................................................ 162 INTRODUCTION ........................................................................................... 162 PERSONAL FINANCIAL STATEMENTS ...................................................... 162 Issues to Consider in Personal Financial Statements ................................... 163 Ownership of Assets ............................................................................................................ 163

Choosing the Basis of Accounting ....................................................................................... 163

Basic Financial Statements .................................................................................................. 164

Cash Basis Financial Statements .................................................................. 165 Pure Cash ............................................................................................................................. 165

Modified Cash ...................................................................................................................... 165

Historical Cost Basis Financial Statements ................................................... 166 Establishing Historical Cost of Assets .................................................................................. 166

10

Cash and Cash Equivalents .................................................................................................. 166

Life Insurance Policies ......................................................................................................... 166

Receivables .......................................................................................................................... 167

Business Interests ................................................................................................................ 167

Real Estate ........................................................................................................................... 167

Future Interests ................................................................................................................... 167

Income Taxes ....................................................................................................................... 168

Commitments ...................................................................................................................... 168

Other Liabilities ................................................................................................................... 169

Accounting Methods ........................................................................................................... 169

Receivables .......................................................................................................................... 170

Business Interests ................................................................................................................ 170

Income Taxes ....................................................................................................................... 170

Disclosures in Personal Financial Statements .............................................. 170 Recommendations ........................................................................................ 171 Basis of Accounting.............................................................................................................. 171

Summary of Significant Accounting Policies ................................................. 172 Other Disclosures .......................................................................................... 172 Personal Financial Statement Engagement Issues ....................................... 173 Accepting the Client ............................................................................................................ 173

Understanding the Client's Accounting Records ........................................... 175 Consider Obtaining a Representation Letter ................................................. 177 Audit of Personal Financial Statements ......................................................... 177 Reporting Standards ..................................................................................... 177 NOT-FOR-PROFIT ORGANIZATIONS ......................................................... 179 Issues to Consider in Not-for-Profit Financial Statements ............................. 179 Fund Accounting .................................................................................................................. 179

Statement of Functional Expenses ...................................................................................... 180

Cash-Basis Financial Statements .................................................................. 180 Pure Cash ............................................................................................................................. 180

Modified Cash ...................................................................................................................... 181

Pledges ................................................................................................................................ 181

Investments ......................................................................................................................... 181

Property and Equipment ..................................................................................................... 182

Net Assets ............................................................................................................................ 182

FAS-117 ........................................................................................................ 182 Income Tax Basis Financial Statements ....................................................... 183 Accounting Methods ........................................................................................................... 184

Pledges ................................................................................................................................ 184

Grants Receivable ................................................................................................................ 184

Investments ......................................................................................................................... 184

Grants Payable ..................................................................................................................... 184

Deferred Revenue ............................................................................................................... 185

11

Net Assets ............................................................................................................................ 185

Contributions ....................................................................................................................... 186

Depreciation ........................................................................................................................ 187

Taxes .................................................................................................................................... 187

FAS-117 ........................................................................................................ 187 Disclosures in Not-for-Profit Financial Statements ........................................ 187 Basis of Accounting.............................................................................................................. 188

Summary of Significant Accounting Policies ................................................. 188 Tax Exempt Status ............................................................................................................... 189

Pledges ................................................................................................................................ 189

Investments ......................................................................................................................... 190

Deferred Revenue ............................................................................................................... 190

Net Assets ............................................................................................................................ 190

Donated Services ................................................................................................................. 191

Donated Materials, Equipment, or Facilities ....................................................................... 191

Functional Expenses ............................................................................................................ 192

Chapter 9 - Auditing OCBOA Financial Statements .......................................... 193 OBJECTIVES ................................................................................................ 193 INTRODUCTION ........................................................................................... 193 AUDIT PROCEDURES ................................................................................. 193 AUDIT REPORTS ......................................................................................... 195 Auditor's Standard Report ............................................................................. 197 TYPES OF AUDIT OPINIONS ...................................................................... 197 Unqualified Opinion ....................................................................................... 197 Qualified Opinion ........................................................................................... 198 Adverse Opinion ............................................................................................ 198 Disclaimer of Opinion .................................................................................... 198 Conditions Precluding an Unqualified Opinion .............................................. 199 Scope Limitations .......................................................................................... 199 Qualified Opinion Due to a Scope Limitation ...................................................................... 200

Disclaimer of Opinion Due to a Scope Limitation ................................................................ 200

Departures from the OCBOA......................................................................... 201 Qualified Opinion Due to a Departure from the OCBOA .................................................... 201

Adverse Opinion Due to a Departure from the OCBOA ...................................................... 202

Accounting Changes ............................................................................................................ 202

Lack of Independence ................................................................................... 203 Unqualified Audit Reports with Explanatory Language Added ...................... 204 Substantial Doubt about the Entity's Ability to Continue as a Going Concern204 Reissued Reports and Going‐Concern Matters ................................................................... 205

Reliance on Third‐Party Funding ......................................................................................... 206

Lack of Consistency in Accounting Principles or in the Method of Their Application ..................................................................................................... 206 Modification to the Standard Auditor's Report as a Result of a Lack of Consistency ................................................................................................... 207

12

Emphasis of a Matter .................................................................................... 207 Change from GAAP to OCBOA ..................................................................... 208 Part of the Audit is Performed by Other Auditors........................................... 208 REPORTING ON COMPARATIVE FINANCIAL STATEMENTS ................... 208 REPORTING ON INFORMATION ACCOMPANYING THE BASIC FINANCIAL STATEMENTS .............................................................................................. 209 Reporting on Voluntary Additional Information .............................................. 209 DATING OF THE AUDITOR'S REPORT ....................................................... 210 Events Occurring after Completion of Fieldwork but before Issuance of Report ...................................................................................................................... 210 Effect of Subsequent Events Requiring Adjustment of the Financial Statements .............. 211

Effect of Subsequent Events Requiring Disclosure .............................................................. 211

Methods Available for Dating the Auditor's Report for a Subsequent Event ..................... 212

RESTRICTING THE USE OF AN AUDITOR'S REPORT .............................. 212 Circumstances Requiring Reports to Be Restricted ...................................... 213 Specified Parties in Restricted-Use Reports ................................................. 213 Restricted-Use Report Language .................................................................. 214

Chapter 10 - Compiling and Reviewing OCBOA Financial Statements ............ 215 OBJECTIVES ................................................................................................ 215 INTRODUCTION ........................................................................................... 215 COMPILATION ENGAGEMENT PROCEDURES ......................................... 215 Traditional Compilations ................................................................................ 216 Knowledge of the Industry .................................................................................................. 216

Knowledge of the Client ...................................................................................................... 217

Necessity to Perform Other Accounting Services................................................................ 217

Awareness Concerning Information Supplied ..................................................................... 217

Reading the Financial Statements ....................................................................................... 218

Management-Use-Only Compilations ............................................................ 218 Understanding with the Client ............................................................................................ 218

Third Parties ........................................................................................................................ 219

Management‐Use‐Only Compilation Program .................................................................... 220

REVIEW ENGAGEMENT PROCEDURES ................................................... 220 Accounting Principles and Practices ............................................................. 220 Analytical Procedures .................................................................................... 221 Inquiries ......................................................................................................... 221 Types of Inquiries ................................................................................................................ 221

Other Review Procedures ............................................................................. 223 Management Representations ...................................................................... 224 Documentation .............................................................................................. 225 REPORTING STANDARDS .......................................................................... 225 Compilation Reports ...................................................................................... 225 Review Reports ............................................................................................. 226 Association with Financial Statements .......................................................... 227 Financial Statement Legends ........................................................................ 227 Report Address ............................................................................................. 228

13

Report Date ................................................................................................... 228 Report Signature ........................................................................................... 229 Reporting on a Single Financial Statement ................................................... 229 MODIFICATIONS TO THE STANDARD REPORT ....................................... 230 Lack of Independence ................................................................................... 230 Departures from the OCBOA......................................................................... 230 Report Modification Is Adequate ........................................................................................ 231

Report Modification Is Inadequate ..................................................................................... 231

Restricted Use Financial Statements ............................................................ 232 Omission of Substantially All Disclosures ...................................................... 232 Inclusion of More than a Few Disclosures ..................................................... 234 Scope Limitations .......................................................................................... 234 Uncertainties ................................................................................................. 235 Uncertainties Related to Going Concern ....................................................... 236 Change in Accounting Principles ................................................................... 238 Change in an Accounting Principle (Correction of an Error) ............................................... 239

Supplementary Information ........................................................................... 239 Supplementary Information ................................................................................................ 240

Presentation of Supplementary Information ...................................................................... 240

Supplementary Information Prepared by the Client ........................................................... 241

Emphasis of a Matter .................................................................................... 242 REPORTING ON COMPARATIVE FINANCIAL STATEMENTS ................... 243

GLOSSARY ...................................................................................................... 244

14

Chapter 1 - Other Comprehensive Bases of Accounting

OBJECTIVES At the end of this section, the student should be able to:

Recognize what the term OCBOA means. Identify the three basis of accounting that are recognized and the types of

organizations that would use each type. Indicate the different reasons why OCBOA financial statements are

beneficial to clients and why they might be used by a CPA.

OVERVIEW The term" other comprehensive bases of accounting" (OCBOA) refers to bases of accounting other than generally accepted accounting principles (GAAP). The primary guidance for OCBOA financial statements is SAS-62 (AU 623) (Special Reports). Unlike GAAP, there is no standard-setting organization for OCBOA. Instead, preparers and accountants have interpreted the audit guidance in AU 623 for purposes of preparing OCBOA financial statements. AU 623.03 states that "an independent auditor's judgment concerning the overall presentation of financial statements should be applied within an identifiable framework." Ordinarily, that framework is provided by GAAP; but AU 623 allows a comprehensive basis of accounting other than GAAP to be used. AU 623.04 recognizes the following OCBOAs:

• The basis of accounting that a reporting entity uses to comply with the requirements or the financial reporting provisions of the governmental regulatory agency under whose jurisdiction the entity is included • The basis of accounting that the reporting entity uses or expects to use to file its income tax return for the period covered by the financial statements • The cash receipts and disbursements basis of accounting, and modifications of the cash basis that have substantial support, such as recording depreciation on fixed assets or accruing income taxes • A definite set of criteria having substantial support that is applied to all material items appearing in financial statements, such as the price-level basis of accounting

NOTE: The Statements on Auditing Standards (SAS) promulgated by the AICPA's Auditing Standards Board are codified in the AICPA Professional

15

Standards, Volume 1, as AU sections 100 through 900. The Statements on Standards for Accounting and Review Services (SSARS) are codified in the AICPA Professional Standards, Volume 1, as AR sections 50 through 600. The Statements on Standards for Attestation Engagements (SSAE) are codified in the AICPA Professional Standards, Volume 1, as AT sections 101 through 701. References in this book to AU sections, AR sections, and AT sections refer to these AICPA standards.

Pure Cash Basis Under the cash receipts and disbursements basis of accounting ("pure cash basis"), only transactions that increase or decrease cash and cash equivalents are reflected in the financial statement. The pure cash basis recognizes all cash disbursements as expenses and all cash receipts as revenues. In practice, the pure cash basis of accounting is rare. Entities that use the pure cash basis of accounting typically have the following characteristics:

• They are not profit-oriented • Their operations are simple • Their accounting and finance functions are unsophisticated • There is only one major activity • Capital expenditures and long-term debt are not significant

Entities that use the pure cash basis of accounting can include school activity funds, civic ventures, trusts and estates, political action committees, and political campaigns.

Modified Cash Basis The modified cash basis of accounting is described by AU 623.04 as the pure cash basis incorporating modifications that have substantial support. These modifications generally include the recognition of certain transactions on an accrual basis, as entities would recognize them under GAAP. However, the appropriate modifications and the extent of those modifications are not clearly defined in the literature. Entities that use the modified cash basis of accounting generally possess the following characteristics:

• They are profit-oriented • They distribute profits as collected (e.g., through bonuses and retirement plan contributions)

16

• They have significant inventory and credit arrangements with vendors • They make material capital expenditures or incur material amounts of debt • Their operations are somewhat sophisticated, and accounting for them may be complex

Examples of entities that use the modified cash basis of accounting are professional associations of doctors, lawyers, and CPAs.

Income Tax Basis The income tax basis of accounting is typically based on federal income tax laws. However, income tax laws generally do not address financial statement presentation or disclosure considerations. Typically, entities that use the tax basis of accounting are either

• Profit-oriented enterprises (such as small closely held companies for which conversion to GAAP would be costly) • Partnerships whose partnership agreements require the use of the tax basis of accounting • Not-for-profit organizations seeking relief from the requirements of FAS-116 and FAS-U7

HISTORY OF OCBOA AND ACCOUNTING STANDARDS The AICPA has commissioned several studies to examine the problem of standards overload. In 1976, the AICPA's Committee on GAAP for Smaller and/ or Closely Held Businesses recommended that the FASB distinguish disclosures required by GAAP from those that merely provide additional data. The committee also recommended that the AICPA develop a method of reporting on financial statements where some or all footnote disclosures are omitted. In 1981, the Special Committee on Accounting Standards Overload was given the following charge: To study accounting standards overload and to consider alternative means of providing relief from accounting standards which are found not to be cost effective, particularly for small, closely held businesses, and to report thereon to the board of directors. The committee recommended the use of the income tax basis of accounting as an alternative to GAAP financial statements for small businesses for the following reasons:

17

• Taxpaying entities already must maintain records of the tax basis of assets and liabilities. Preparing tax basis financial statements would eliminate the need to also maintain records of the GAAP basis of assets and liabilities. • Most financial statement users recognize and understand the tax basis of accounting. • Many users are satisfied with financial statements prepared on the tax basis; those who need more information are generally able to require GAAP statements. • Few measurement guidelines need to be established.

The committee also recommended minimum disclosure, measurement, and reporting guidelines for income tax basis financial statements. In addition, in 1983 the FASB issued a special report entitled "Financial Reporting by Privately Owned Companies: Summary of Responses to FASB Invitation to Comment" that summarized the responses to a FASB Invitation to Comment issued in 1981, which included questionnaires tailored to three groups: (1) managers of private and small public companies, (2) users of financial statements of those companies, and (3) public accountants who served those companies. The report did not draw any conclusions or make any recommendations concerning accounting standards.

DETERMINING WHETHER TO ISSUE OCBOA FINANCIAL STATEMENTS OCBOA financial statements are beneficial to clients for many reasons. One of the major benefits is that some clients can understand OCBOA financial statements better than GAAP financial statements. It is not uncommon for the owner / manager of a privately held company to fully understand the measurement issues represented in tax returns but have little grasp of the measurement and disclosure complexities in GAAP financial statements. Another major advantage: Because accountants do not need to consider the measurement requirements of GAAP, the OCBOA financial statements can often be prepared on a more timely and cost-efficient basis. For cash-basis financial statements, many of the measurement principles associated with GAAP simply do not exist; for tax-basis financial statements, the CPA has already addressed the measurement issues in the tax returns. It is estimated that CPAs can save up to 20% to 30% or more in certain cases because of the reduced time and cost in preparing and reporting on OCBOA financial statements.

18

In advising clients about the use of an OCBOA, accountants should consider the following issues:

• Does the entity have inventory? (If so, the pure cash basis may not be helpful.) • What basis of accounting does the entity use in preparing its income tax return? (If the accrual basis is used, preparing financial statements on the same basis makes sense.) • Is the entity highly leveraged? (Lenders may require GAAP financial statements.) • Are there outside investors? (GAAP financial statements may provide information required by such users.) • Does the entity's cash flow parallel its income and expenses? (The pure cash basis may be appropriate.) • Does the entity anticipate going public? (If so, the entity will need a history of GAAP financial statements.) • Was the entity formed for tax purposes? (If yes, the owners are probably interested in the tax effects of transactions and the income tax basis would be appropriate.) • Is the entity subject to bonding requirements? (Most bonding companies only accept GAAP financial statements.)

OCBOA financial statements may be prepared for any entity that is not required, contractually or otherwise, to issue GAAP financial statements. As a practical matter, OCBOA financial statements may be considered anytime the following conditions are met:

• The users of the financial statements-those who are internal as well as those who are external to the entity-understand an OCBOA presentation and find it relevant to their needs. • It is cost-effective to prepare OCBOA financial statements. • The operations of the entity are conducive to an OCBOA presentation.

The AICPA's nonauthoritative practice aid Preparing and Reporting on Cash- and Tax-Basis Financial Statements lists the following characteristics of entities that should consider issuing cash- or tax-basis financial statements: General Condition

Specific Characteristic

User needs: third parties •The entity has no third-party users of the financial statements (e.g., the entity is a small closely held business with no third-party debt).

•The entity's debt is secured rather than unsecured.

19

•The entity's creditors do not require GAAP financial statements.

User needs: owners and managers •The owners and managers are closely involved in the day-to-day operations of the business and have a fairly accurate picture of the entity's financial position

•The business's owners are primarily interested in cash flows (e.g., a professional corporation of physicians that distributes its cash-basis earnings through salaries, bonuses, and retirement plan contributions).

• The owners are primarily interested in the tax implications of transactions (e.g., partners in a partnership who are concerned about the tax effects of transactions that will be reflected on their personal tax returns).

Cost-effective • The entity's cost of complying with GAAP would exceed the benefits (e.g., a small construction contractor would be required to account for long-term contracts using the percentage-of-completion method and would be required to compute deferred taxes).

• The entity is not subject to Internal Revenue Code rules that would require it to prepare its tax return on the accrual method of accounting (If the entity is required to use the accrual method for income tax purposes, the differences between a tax-basis presentation and GAAP might not be sufficient to provide substantial cost savings.)

Operations • Capital expenditures and long-term financing are not significant to the entity.

As the foregoing table indicates, understanding the needs of the financial statement users is the most important step in helping clients decide whether to issue OCBOA financial statements.

Note: Financial statement users may be more inclined in certain situations to accept OCBOA financial statements if the client also provides additional information outside the basic financial statements. For example, a lender

20

might accept tax-basis financial statements from a borrower if the borrower also provides the lender with an aged listing of receivables.

OCBOA financial statements should not be issued if the results will be misleading. AU 623.09 includes the following guidance:

The auditor should apply essentially the same criteria to financial statements prepared on an other comprehensive basis of accounting as he or she does to financial statements prepared in conformity with generally accepted accounting principles. Therefore, the auditor's opinion should be based on his or her judgment regarding whether the financial statements, including the related notes, are informative of matters the may affect their use, understanding, and interpretation.

The foregoing statement indicates that the auditor has a responsibility to determine whether the financial statements are misleading. The AICPA's nonauthoritative practice aid Preparing and Reporting on Cash- and Tax-Basis Financial Statements states that the accountant should consider whether OCBOA financial statements could be misleading whenever the following conditions are present:

• The entity has substantial unfunded obligations, commitments, and contingent liabilities that would not be recorded on the cash or tax basis. • The entity has delayed paying accounts payable and other current liabilities not shown on a cash-basis statement. • The financial statements have been compiled with substantially all disclosures omitted.

BASIC FINANCIAL STATEMENTS By default, generally accepted accounting principles are applicable when a CPA conducts an audit, compilation, or review of and reports on any financial statement. A financial statement may be, for example, that of a corporation, a consolidated group of corporations, a combined group of affiliated entities, a not-for-profit organization, a governmental unit, an estate or trust, a partnership, a proprietorship, a segment of any of these, or an individual. The term "financial statement" refers to a presentation of financial data, including accompanying notes, derived from the accounting records and intended to communicate an entity's economic resources or obligations at a point in time or the changes therein for a period of time in conformity with a comprehensive basis of accounting. The following financial presentations are examples of financial statements:

• Balance sheet

21

• Statement of income • Statement of comprehensive income • Statement of retained earnings • Statement of cash flows • Statement of changes in owners' equity • Statement of assets and liabilities (with or without owners' equity accounts) • Statement of revenues and expenses • Statement of financial position • Statement of activities • Summary of operations • Statement of operations by product lines • Statement of cash receipts and disbursements

In an OCBOA presentation, the basic financial statements typically present financial position and results of operations as measured under the OCBOA, descriptions of accounting policies, and notes to the financial statements. However, an exception to this exists for entities that use the pure cash basis of accounting. Under the pure cash basis of accounting, a statement of assets, liabilities, and equity is needless because the cash balance is the only item that appears. Consequently, entities using the pure cash basis of accounting present a single statement titled "Statement of Cash Receipts and Disbursements."

Economic Resources and Obligations By definition "financial statements" are a presentation of financial data intended to communicate an entity's economic resources or obligations on a specific date. When GAAP financial statements are prepared, a financial statement of this nature is referred to as a "balance sheet" or "statement of financial position."

Changes in Economic Resources and Obligations By definition "financial statements" are a presentation of financial data intended to communicate changes in an entity's economic resources or obligations. When GAAP financial statements are prepared, a financial statement of this nature is referred to as an "income statement" or "statement of operations."

Cash Flows FAS-95 (Statement of Cash Flows) states that "a business enterprise that provides a set of financial statements that reports both financial position and results of operations shall provide a statement of cash flows for each period for which results of operations are provided." However, Interpretation No. 14 of SAS-

22

62 (AU 9623.94) states that "a statement of cash flows is not required" in presentations using the cash, modified cash, or income tax basis of accounting.

Note: Whether a statement of cash flows is necessary for a basis of accounting established by a governmental regulatory agency depends on the specific requirements established by the agency.

Although a statement of cash flows is not required in cash, modified cash, or income tax basis presentations, if a presentation of cash receipts and disbursements is presented in a format similar to a statement of cash flows, or if the entity chooses to present a statement of cash flows (for example in a presentation on the accrual basis of accounting used for federal income tax reporting), the statement should either conform to the requirements for a GAAP presentation or communicate their substance.

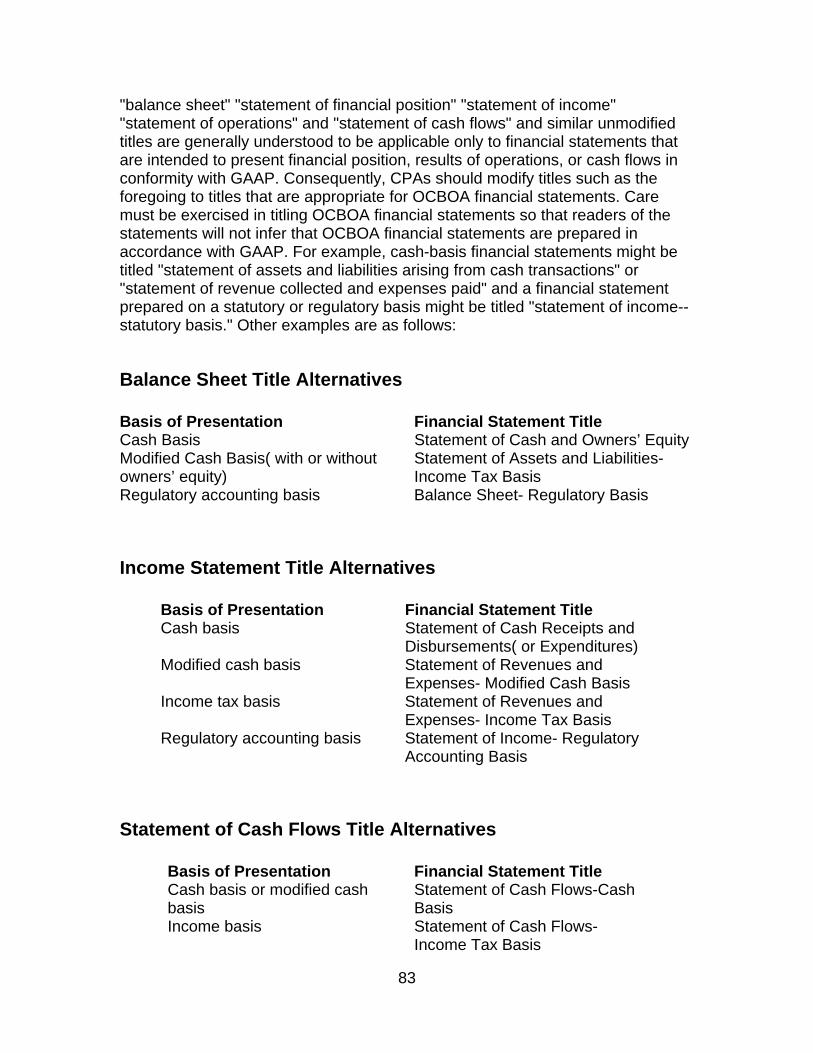

Financial Statement Titles When OCBOA financial statements are prepared, it is inappropriate to use titles that would normally be associated with GAAP financial statements. AU 623.07 addresses the issue of OCBOA financial statement titles. Terms such as "balance sheet," "statement of financial position," "statement of income," "statement of operations," "statement of cash flows," and similar unmodified titles are generally understood to be applicable only to financial statements that are intended to present financial position, results of operations, or cash flows in conformity with GAAP. Consequently, CPAs should modify such titles to ones that are appropriate for OCBOA financial statements. Care must be exercised in titling OCBOA financial statements so that readers of the statements will not infer that OCBOA financial statements are prepared in accordance with GAAP. For example, cash-basis financial statements might be titled" statement of assets and liabilities arising from cash transactions" or "statement of revenue collected and expenses paid," and a financial statement prepared on a statutory or regulatory basis might be titled "statement of income-statutory basis."

KEY ISSUES IN PREPARING OCBOA FINANCIAL STATEMENTS A basis of accounting (including an OCBOA) is a framework for determining what information is presented in the financial statements and related notes and how it is presented. However, many issues arise in practice for which there is no authoritative guidance. These issues are summarized as follows.

23

Recognition Recognition deals with when an item should be reported in the financial statements. Transactions should be recognized in the financial statements based on the basis of accounting used. More specifically, an item and the information about it should be recognized in the financial statements when the following four criteria are met:

1. Definition: The item meets the definition of an element of a financial statement. 2. Measurability: The item has a relevant attribute that can be reliably measured. 3. Relevance: The information about the item may make a difference to financial statement users. 4. Reliability: The information is representationally faithful, verifiable, and neutral.

For example, cash-basis financial statements recognize transactions when cash is received or paid. Tax-basis financial statements recognize transactions when they would be recognized in the entity's tax return.

Measurement "Measurement" is how an item is quantified. The item must have a relevant attribute that can be quantified monetarily with sufficient reliability. Some items that meet the definition of a financial statement element are not measurable. Cash-basis financial statements measure an item based on the amount of cash received or paid. Tax-basis financial statements measure items based on amounts that would be reported in the entity's tax return. Recognition and measurement issues for cash-basis financial statements are addressed in Chapter 5, "Cash and Modified Cash-Basis Financial Statements." Recognition and measurement issues for income tax basis financial statements are addressed in Chapter 6, "Income Tax Basis Financial Statements."

Presentation Although transactions are recognized and measured according to the OCBOA, they are generally presented in the financial statements according to GAAP presentation guidelines. That is, revenues and expenses (measured in accordance with the OCBOA) are presented in a statement of income and assets, liabilities, and equity (measured in accordance with the OCBOA) are presented in a statement of financial position.

24

Financial statement form and style considerations are discussed further in Chapter 4, "Primary Financial Statement Considerations."

Disclosures Some information is better provided, or can only be provided, by notes to the financial statements, by supplementary information, or by other means. A common misconception about OCBOA financial statements is that the requirements for disclosure are significantly different from those for GAAP financial statements. According to AU 623.09, OCBOA financial statements should include all informative disclosures that are appropriate for the basis of accounting used. Thus, the disclosures required for OCBOA financial statements are essentially the same as those required for GAAP financial statements. Specifically, informative disclosures can be classified in the following categories:

• Summary of significant accounting policies • Financial statement items • Presentation requirements • Other information

Disclosure issues relevant to each basis of accounting are discussed further in the pertinent chapters throughout this book.

Reporting Certain modifications must be made when reporting on OCBOA financial statements. The statement titles in the reports must reflect the OCBOA statement titles. Audit reports must disclose the basis of presentation, refer to the note that describes the basis, and include a statement that the basis is a comprehensive basis of accounting other than GAAP. When compiled financial statements omit substantially all disclosures, the compilation report must reflect OCBOA titles and disclose the basis of accounting. Other compilation and review reports must reflect the OCBOA statement titles. Chapter 9, "Auditing OCBOA Financial Statements: Procedures and Reporting," discusses audit reports on OCBOA financial statements in further detail. Chapter 10, "Compiling and Reviewing OCBOA Financial Statements: Procedures and Reporting," discusses compilation and review reports on OCBOA financial statements in further detail.

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES

25