O REConnect Energy Solutions E N REC, Energy Efficiency

11

Page 1 Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only O P E N A C C E S S Vol. XXIII July 2012 www.reconnectenergy.com Dear Readers, REC market crashed in the July trading session. Demand fell by 55% as compared to previous month, and prices fell 17% on IEX and 10% on PXIL. Concerns over enforcement, or rather the lack of it, combined with the natural increase in RECs availability are the key drivers. Without clear enforcement signals, we expect this situaon to connue in the foreseeable future. The main arcle this month should also be read in the context of the need for enforce- ment. The Forum of Regulators released a comprehensive report on the cost of RPO. This made headlines as the report found the immediate impact of compliance will be “1 paise per unit”. In the arcle, we analysed the report and aempted to disll the volumi- nous report into a short read. As always, detailed trading stascs, analysis and regulatory updates are available in this newsleer. Happy reading and we look forward to hear- ing feedback from you. -Team REConnect REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management Analysis of report on RPO trajectory and impact From Management’s Desk Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis The Forum of Regulators (FOR) recently released a study of RPO trajectory and its impact on overall power cost. This made headlines as the study found that the impact is less than 1 paise per unit. The argument is that Discom’s/ consumers can easily absorb this. We analysed the report, parcularly in the context of RPO enforcement. Ambious targets: The report set out to assess the impact of RPO as capacies will be built in the 12th plan. The 12th plan target is to add close to 32 GW of capacity by 2017. This is compared to 6.7 GW and 14.6 GW achieved in the last 2 plan periods. Compared to the past, the 12th plan is certainly very ambious in its scope. One of the bedrocks of the 12th plan is RPO, since a lot of the oth- er incenves like Accelerated Depreciaon and Generaon Based Incenves have been done away with in relavely mature technologies like wind (which is planned to contribute 15 GW or 47% of the total capacity added). Impact of RPO: The report suggests that the achievable RPO in FY 12 is 6.1%. This will increase to 10.7% - 11.4% by 2017. Comparable targets of the Naonal Acon Plan for Climate Change (NAPCC) are 7% and 12% respecvely. This suggests a significant progress in meeng NAPCC targets. However, the RPO trajectory assumed in the report differs in many instances from the trajec- tory provided in the state RPO regulaon – for example, the report assumes that the AP’s RPO requirement will move from 5% to 12% from 2012 to 2017, but the regulaon provides for a constant 5%. This implies that for achieving the RE growth envisaged in the 12th plan, states will also have to amend the exisng RPO regulaons. In the above period, RE power available is likely to increase 3 fold from 55 billion units to 155 billion units.

Transcript of O REConnect Energy Solutions E N REC, Energy Efficiency

Page

1

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

July 2012

www.reconnectenergy.com

Dear Readers, REC market crashed in the July trading session. Demand fell by 55% as compared to previous month, and prices fell 17% on IEX and 10% on PXIL. Concerns over enforcement, or rather the lack of it, combined with the natural increase in RECs availability are the key drivers. Without clear enforcement signals, we expect this situation to continue in the foreseeable future.

The main article this month should also be read in the context of the need for enforce-ment. The Forum of Regulators released a comprehensive report on the cost of RPO. This made headlines as the report found the immediate impact of compliance will be “1 paise per unit”. In the article, we analysed the report and attempted to distill the volumi-nous report into a short read.

As always, detailed trading statistics, analysis and regulatory updates are available in this newsletter.

Happy reading and we look forward to hear-ing feedback from you.

-Team REConnect

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Analysis of report on RPO trajectory and impact

From Management’s Desk

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

The Forum of Regulators (FOR) recently released a study of RPO trajectory and its impact on overall power cost. This made headlines as the study found that the impact is less than 1 paise per unit. The argument is that Discom’s/ consumers can easily absorb this. We analysed the report, particularly in the context of RPO enforcement.

Ambitious targets:

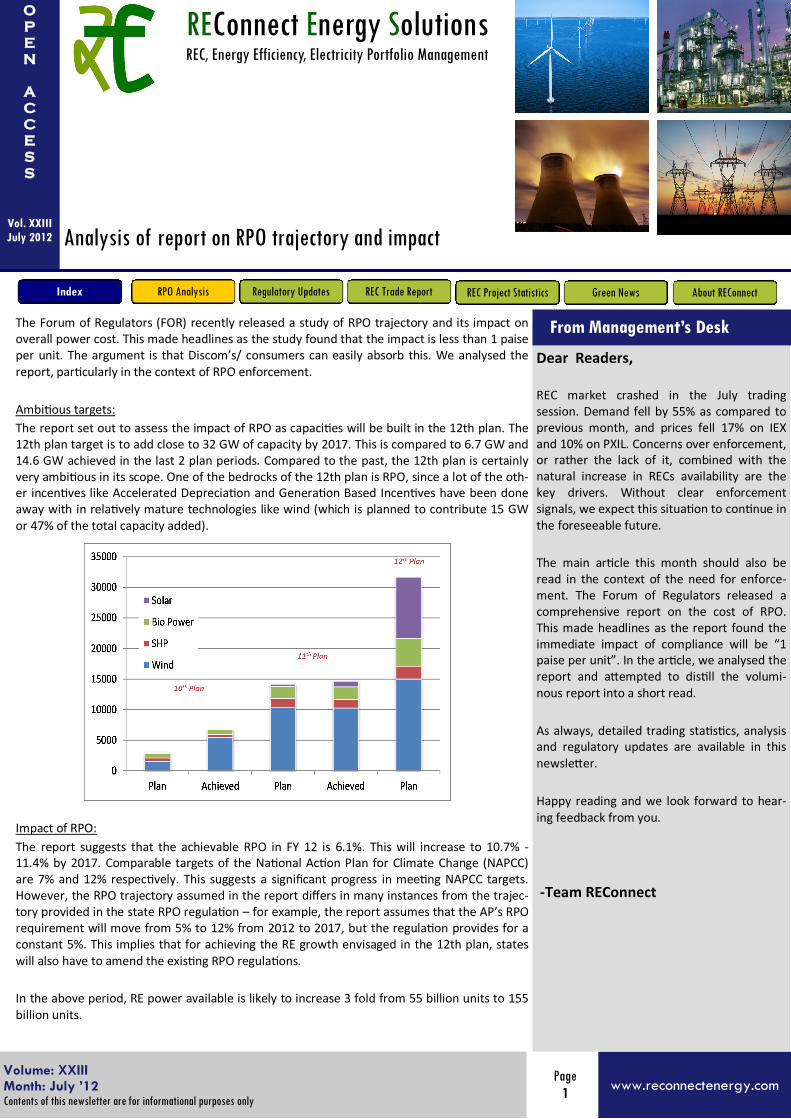

The report set out to assess the impact of RPO as capacities will be built in the 12th plan. The 12th plan target is to add close to 32 GW of capacity by 2017. This is compared to 6.7 GW and 14.6 GW achieved in the last 2 plan periods. Compared to the past, the 12th plan is certainly very ambitious in its scope. One of the bedrocks of the 12th plan is RPO, since a lot of the oth-er incentives like Accelerated Depreciation and Generation Based Incentives have been done away with in relatively mature technologies like wind (which is planned to contribute 15 GW or 47% of the total capacity added).

Impact of RPO:

The report suggests that the achievable RPO in FY 12 is 6.1%. This will increase to 10.7% - 11.4% by 2017. Comparable targets of the National Action Plan for Climate Change (NAPCC) are 7% and 12% respectively. This suggests a significant progress in meeting NAPCC targets. However, the RPO trajectory assumed in the report differs in many instances from the trajec-tory provided in the state RPO regulation – for example, the report assumes that the AP’s RPO requirement will move from 5% to 12% from 2012 to 2017, but the regulation provides for a constant 5%. This implies that for achieving the RE growth envisaged in the 12th plan, states will also have to amend the existing RPO regulations.

In the above period, RE power available is likely to increase 3 fold from 55 billion units to 155 billion units.

Page

2

www.reconnectenergy.com

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

The most important findings of the report is that RPO compliance will have a relatively small impact on the overall cost of power. The report found that the impact in the immediate term is 1 paise per unit, and this will decrease to -0.5 paise by 2017. Howev-er, three things need to be kept in mind – first that this is “incremental” impact – ie, year on year, and not absolute. Second that this is on the basis if “time value”, ie in today’s prices. Another way to interpret this is that investments made by Discom’s today in RE power will actually help them save costs by 2017. Third, that these are national aggregates. To achieve all this by a burden as low as 1 paise per unit means RPOs will have to be equitable across the country, and more importantly will have to be enforced across the country. Another aspect is that the cost impact will differ widely from state to state and on the basis of tech-nologies. Its all about enforcement, enforcement, enforcement: One of the most important requirement for achieving the “1 paise” cost will be enforcement of RPO. As an example, if one state were to enforce RPO while another not, then the consumers in the enforcing state will have to bear additional burden. In the con-text of the present scenario, this is the most urgent aspect of the market to tackle. There is very little to show for enforcement by state ERCs after four months from the end of the first compliance period. Even basic data about the extent of the RPO met by different obligated entities in states has not been compiled and made available. It is in this context that the market crash of July 2012 can be understood (another important aspect is the rapid growth in supply of RECs). Impact on investors: From an investor’s perspective, the ambitious targets of the 12th plan are very encouraging, and so is the past record of meeting and exceeding those targets. However, the RPO/ REC mechanism has now taken centerstage, and will be the single biggest factor in achieving the 12th plan target. This should worry planners and investors, as in the short term, the mechanics for enforcement are not in place to the extent required. This is already evident from the lack of participation in the market by State Discom’s (barring some very minor exceptions) and a situation of oversupply even in a nascent market. The report does mention some remedial measures, but does not provide significant details. The reports states: “India could use the recently established National Clean Energy Fund, which finances research and innovative projects in clean technologies, as a vehicle to accumulate and channel renewable energy subsidies and reduce the financial burden on utilities. The existence of a fully financed national fund to subsidize RE would remove market uncertainty and make states and utilities more willing to implement renewable energy goals.” This is definitely worth considering, but there are risks – moving from one subsidy mechanism to another is no solution, particularly when the basic framework of a market mechanism is now already in place. Such a fund should be strictly based on progress made in RE generation, reform of distribution and “open access” mechanism, and should have a limited lifespan.

Page

3

www.reconnectenergy.com

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Amendment to APPC notification in Karnataka for FY 12-13:

In a recent amendment to the APPC (Rs.2.73/unit) which was declared by Karnataka Electricity Regulatory Commission (KERC) March 2012 has been revised to Rs.2.60/unit for the financial year 2012-13. They have also notified that the variation in pooled cost of 13 paise per unit shall be adjusted in the future bills in three equal installments by ESCOMS.

APPC reduced in Himachal Pradesh for FY12-13 :

In a recent order by Himachal Pradesh Electricity Commission (HPERC), the APPC for Himachal Pradesh was discovered at Rs.2.20 per unit for the financial year 2012-13. For the previous financial year it was calculated out to be Rs.2.24 per unit ( a drop of 4 paisa per unit) .

Appointment of Compliance Auditor in REC Mechanism :

In an order, Central Electricity Regulatory Commission (CERC) an-nounced empanelment of Compliance Auditors in the area of REC mechanism. The Commission formed a Consultancy Evaluation Com-mittee (CEC) to evaluate the bids presented from different firms and further recommend them to do the auditing.

The reports prepared by the Compliance Auditor will be submitted to the Central Agency for their comments and then it will be forwarded to the Commission.

Regulatory Updates

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Please note our Office Address at Gurgaon and Bangalore

@Gurgaon

216, Nirvana Courtyard Nirvana Country, Sector 50 Gurgaon- 122018, Haryana Phone No: 0124-4103216 Fax: +91 80 3072 3571

@Bangalore

4123, 1st Floor,6th Cross,19th Main HAL 2nd Stage, Indira Nagar Bangalore-560 008 , Karnataka Phone No.: 80 6547 3383/84, Fax: +91 80 3072 3571

Page

4

www.reconnectenergy.com

Demand fell off the cliff this month, mainly driven by enforcement concerns and expectations of price fall in the future (due to increasing supply). Aggregate demand reduced to 161,000 RECs from 350,000 last month (-54%). On the other hand, supply of RECs increased from 360,000 to 467,000 (increase of 30%). Of these, 158,000 RECs were sold (last month – 236,000; down by 33%).

Detailed analysis of Non-solar REC trading: The market clearing price on IEX and PXIL was Rs. 2,000 and Rs.2,202 respectively. (Last month it was Rs. 2,402 at IEX and Rs. 2,460 at PXIL; down 17% and 10% respectively).

The price fall is not surprising, given the steep fall in demand. The low demand and cleared volume leaves an overhang of close to 350,000 RECs this month. Next month this is likely to result in significant oversupply, putting further pressure on prices.

Detailed analysis of Solar REC trading: In the third session of Solar REC trading demand fell marginally from last month (from 9,619 to 8,754; down 9%). RECs bid for sale also reduced marginally to 549 from 563 last month (-2%). The market clearing price on both power exchanges was Rs. 12,800 (Its rose from Rs.12750 on IEX and Rs.12506 on PXIL). Only 179 Solar RECs were sold (last month it was 342).

Total market value exceeded Rs 32 crore, of which Rs 22 lakhs were from Solar RECs. This is down 44% in aggregate

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Review of REC Trading-July 2012

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

5

www.reconnectenergy.com

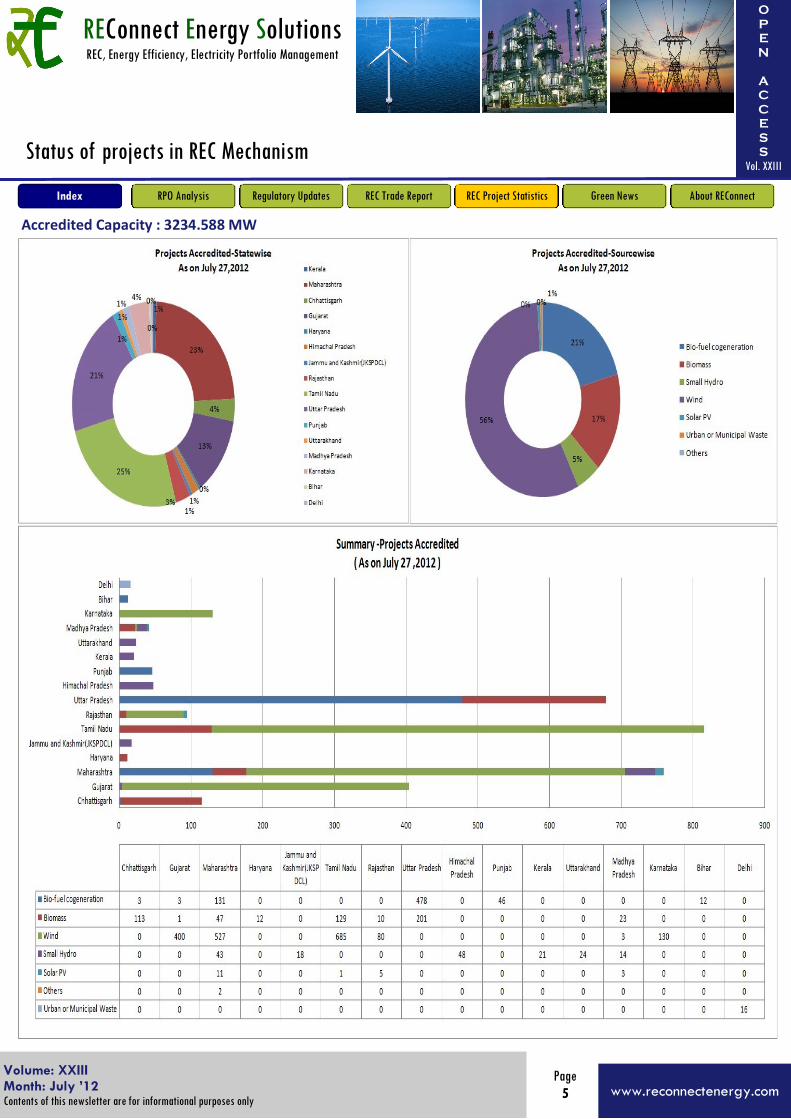

Status of projects in REC Mechanism

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Accredited Capacity : 3234.588 MW

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

6

www.reconnectenergy.com

Status of projects in REC Mechanism

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Registered Capacity : 2915.173 MW

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

7

www.reconnectenergy.com

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

“Make renewable energy certificate trading simpler to encourage corporate”, Dr. Pramod Deo, Chairman, CERC Involving public sector units and providing incentives to buyers are the main challenges for creating voluntary markets for re-newable energy certificate (REC) in India, said Dr. Pramod Deo, Chairman, Central Electricity Regulatory Commission (CERC). http://articles.timesofindia.indiatimes.com/2012-07-14/pune/32674662_1_renewable-energy-rec-central-electricity-regulatory-commission Power Grid plans green corridor for renewable energy Power Grid Corporation has a Rs 42,000-crore plan for setting up an exclusive countrywide green corridor for renewable ener-gy transmission. Presenting the company’s Q1 results here on Wednesday, Mr R. N. Nayak, Chairman and Managing Director, said this would be done over a period of five years. The investment was for transmission of 40 GW of renewable energy ca-pacity by 2030. http://www.thehindubusinessline.com/companies/article3682979.ece MNRE seeks financial assistance for off-grid solar schemes With a view to meet rural energy needs, the Ministry of New and Renewable Energy (MNRE) plans to seek financial assistance from the National Clean Energy Fund (NCEF) to aid off-grid solar projects across the country . http://ibnlive.in.com/generalnewsfeed/news/mnre-seeks-finnaical-assistance-for-offgrid-solar-schemes/1022712.html India Can Boost Clean-Energy Targets at Minimal Cost: Forum of Regulators (FOR) India, the world’s fourth-biggest energy consumer, can increase renewable power purchase targets for distributors at minimal cost, Forum of Regulators said. http://www.bloomberg.com/news/2012-07-20/india-can-boost-clean-energy-targets-at-minimal-cost-panel-says.html

TERI to guide telecom sector on going green Leading industry bodies representing the GSM, CDMA and tower service providers have engaged The Energy and Resources Institute to create a blueprint to implement green solutions to reduce their carbon footprint, an executive aware of the devel-opment said. The country's premier research institute on environment sustainability will bring out a roadmap for tower com-panies on reducing their diesel consumption, which will receive a final approval by the telecoms department. http://articles.economictimes.indiatimes.com/2012-07-25/news/32829482_1_rural-towers-urban-towers-tower-companies

BHEL commissions 5 Mw solar power plant Bharat Heavy Electricals Ltd (BHEL) has commissioned a 5-Mw grid-connected solar power plant at Shivasamudram near Man-dya. This is the single largest solar photovoltaic (PV) power plant in Karnataka. The plant has been set up by BHEL for the state-owned power producer, Karnataka Power Corporation Limited (KPCL), at a cost of Rs 62 crore. http://www.business-standard.com/india/news/bhel-commissions-5-mw-solar-power-plant/481400/

Ministry of New and Renewable Energy wants utilities to pay for renewable energy first In view of the weak financial conditions of the electricity distribution companies, the Ministry of New and Renewable Energy (MNRE) is trying ensure timely payments to the renewable energy project developers. It is already started discussions with the SERCs to figure out the modalities and soon going to write them to ensure first priority to the renewable power producers when it comes to payments. http://articles.economictimes.indiatimes.com/2012-07-10/news/32618337_1_renewable-energy-renewable-power-mw-of-solar-power

Green News

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

8

www.reconnectenergy.com

Status of RPOs across various states in India - As on April 24 , 2012

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

State

Status of Regulation

2012–13 RPO Obligation

RPO on CPP?

RPO on OA Users?

Penalty ?

Andhra Pradesh Final 4.75 % + 0.25 %

Yes

Yes

Not Specified

Assam Final

4.05 % + 0.15 %

Yes

Yes

Yes (RECmax)

Arunachal Pradesh Final 4.1 % +0.1 % Yes Yes Yes (RECmax)

Bihar

Final

3.25 % + 0..75 %

Yes

Yes

Yes (RECmax)

Chhattisgarh

Final

5.25 % + 0.50 %

Yes

Yes

Yes (RECmax)

Delhi Draft

3.25 %+ 0.15 %

Yes

Yes

Yes (RECmax)

Gujarat

Final

6.00 % + 1.00 %

Yet to be notified

Yes

Yes (RECmax)

Haryana

Final

1.50 % + 0.50 %

Yes

Yes

Yes (RECmax)

Himachal Pradesh

Final

10.00 % + 0.25 %

Yes

Yes

Yes (RECmax)

J&K

Final

4.75 %+0.25 %

Yes

Yes

Yes (RECmax)

Jharkhand

Final

3.00 % + 1.00 %

Yes (>5MW)

Yes

Yes (RECmax)

Karnataka

Final

10 % + 0.25 % (BESCOM,MESCOM,CHESCO

M), 7 % + 0.25 % for others

Yes (>5MW)

5% RPO

Yes (>5MW)

5% RPO

Yes (RECmax)

Kerala

Final

3.35 %+0.25 %

Yes

Yes

Yes (RECmax)

Madhya Pradesh

Final

3.40 % + 0.60 %

Yes

Yes

Yes (RECmax)

Maharashtra

Final

7.75 % + 0.25 %

Yes

Yes

Yes (RECmax)

Meghalaya

Final

0.60 % + 0.40 %

Yes

Yes

Yes (RECmax)

Orissa

Final

5.35 % + 0.15 %

Yes(>5MW)

Yes

Yes (RECmax)

Punjab

Final

2.83 %+0.07 %

Yes

Yes

Yes (RECmax)

Rajasthan

Final

7.10 % + JNNSM

Yes

Yes

Yes (RECmax)

Tamil Nadu

Final

8.95 % + 0.05 %

Yes

Yes

Yes (RECmax)

Tripura

Final

0.90 % + 0.10 %

Yes (>5MW)

Yes

Yes (RECmax)

Uttrakhand

Final

4.5 % + 0.025 % Yes

Yes

Yes (RECmax)

Uttar Pradesh

Final

5.00 %+ 1.00 %

Yes

Yes

Yes (RECmax)

West Bengal

Final

4 % + NA

NA

NA

REC not recognized

JERC for Goa and UTs

Final

2.60 % + 0.40 % Yes

Yes

Yes (RECmax)

JERC for Manipur and Mizoram

Final

4.75 % + 0.25% (Man) 6.75% + 0.25% (Miz)

Yes

Yes

Yes (RECmax)

Nagaland

Final

7.75 % + 0.25%

Yes

Yes

Yes (RECmax)

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

9

www.reconnectenergy.com

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Dear Readers,

Our previous newsletters are available at our website www.reconnectenergy.com and can be downloaded from :

http://www.reconnectenergy.com/rec/index.php/newsletters-on-rec-mechanism.html The summary of our previous newsletters we have published is available below.

Volume XII: August 2011 REC & RPO: The Dilemma of Double Accounting of “Green Tags”

Volume XIII: September 2011

Metering Issues in CPPs and Co-Gen: From REC Perspective

Volume XIV: October 2011

Introduction to Renewable Regulatory Fund

Volume XV: November 2011 Renewable Purchase Obligation – A Demand - Supply Analysis

Volume XVI: December 2011

Analysis of Draft RPO of Andhra Pradesh + REC Market Update

Volume XVII: January 2012

Voluntary Market for RECs

Volume XVIII: February 2012 Off Grid Projects and REC: A new socio-development tool?

Volume XIX: March 2012

Applicability of RPO on Co-Generation Projects (An Update)

Volume XX: April 2012

Analysis of the Energy Savings Certificate Markets

Volume XXI: May 2012 Trading of First Solar RECs - Interview with Mr Vikalp Mundra of M&B Switchgear Ltd

Volume XXII: June 2012

Waste-to-energy projects and REC Mechanism, and REC trading updates

Past Newsletters

Feedback:

We wholeheartedly thank you for providing your valuable feed-back on our last newsletter. Your feedback on the

newsletter keeps us motivated and would certainly help us to improve the quality of it. Kindly keep writing to us.

We are eager hear your views.

Best Regards, Team - REConnect

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

10

www.reconnectenergy.com

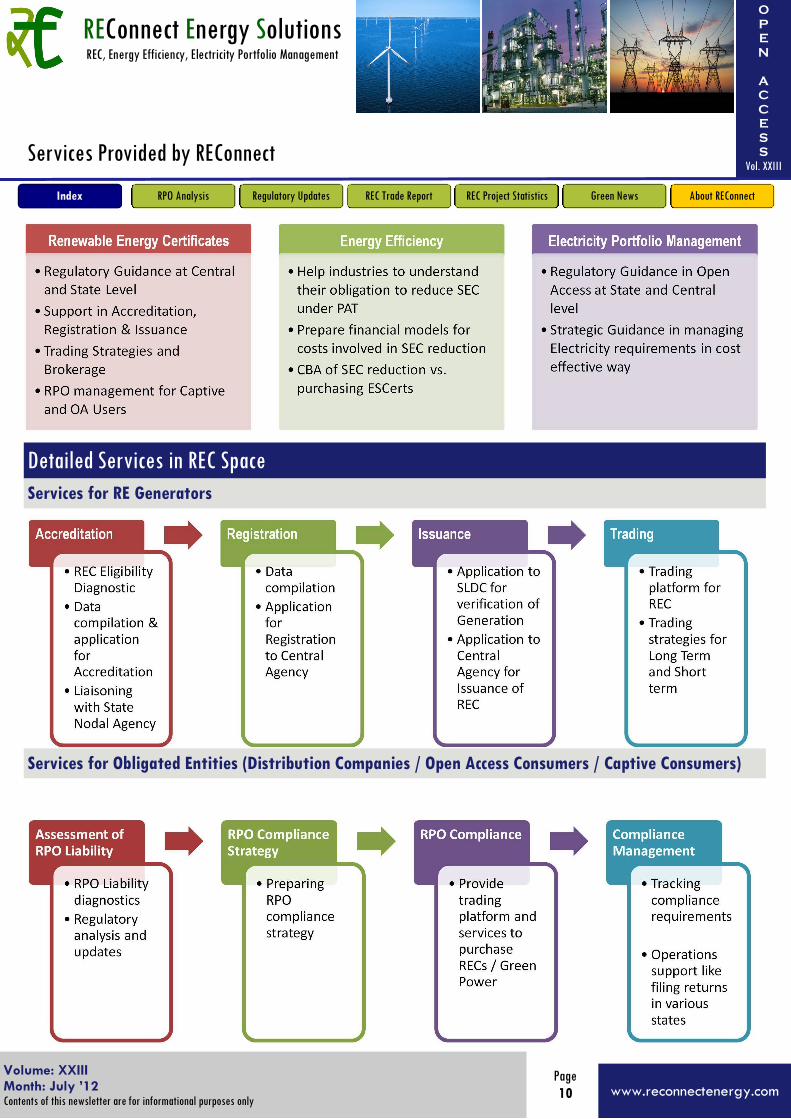

Services Provided by REConnect

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Detailed Services in REC Space

Services for RE Generators

Services for Obligated Entities (Distribution Companies / Open Access Consumers / Captive Consumers)

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Page

11

www.reconnectenergy.com

REConnect is a venture focused on the Renewable Energy Certificates,

Energy Efficiency and Electricity Portfolio Management.

REConnect’s team has extensive experience in the environmental markets

both in India and internationally:

Worked in the international carbon markets for several years and has

expertise in the consulting and trading of emissions reductions

Extensive knowledge about various Renewable Energy Certificate and

Energy Efficiency Certificate markets in USA, Europe and Australia etc.

Worked with Indian Energy Exchange (IEX), India’s leading power ex-

change, and have extensive knowledge and experience of power mar-

kets

Alumnus of Columbia University, an Ivy League University in USA, and

IIT Bombay

Highly experienced core team worked with organizations like

J P Morgan, Indian Energy Exchange, Asia Carbon and Gensol.

Contact REConnect

New Delhi Vibhav Nuwal [email protected] +91 88006 79988

Bangalore

Vishal Pandya [email protected] +91 96202 21101 Suresh Kumar (for RPO) [email protected] +91 99727 24727 Mumbai Ramkumar K [email protected] +91 99303 59992

Chennai Rajesh Vaidyula [email protected] +91 99404 78306 Ahmedabad Mohit Tyagi [email protected] +91 96650 42397

About REConnect

REConnect Energy Solutions REC, Energy Efficiency, Electricity Portfolio Management

Regulatory Updates REC Trade Report REC Project Statistics Green News About REConnect Index RPO Analysis

Volume: XII Month: June ’12 Contents of this newsletter are for informational purposes only

O

P

E

N

A

C

C

E

S

S

Vol. XXIII

Volume: XXIII Month: July ’12 Contents of this newsletter are for informational purposes only