NZ Farming Systems Uruguay results briefing hy08 presentation... · NZ Farming Systems Uruguay ......

22

1 NZ Farming Systems Uruguay NZ Farming Systems Uruguay Briefing on trading results and operations Six months to 31 December 2007

Transcript of NZ Farming Systems Uruguay results briefing hy08 presentation... · NZ Farming Systems Uruguay ......

1

NZ Farming Systems UruguayNZ Farming Systems Uruguay

Briefing on trading results

and operations

Six months to 31 December 2007

2

ContentContent

• Overview 3

• Background 6

• Operations 16

• Outlook 20

3

OverviewOverview

• Second six months in the establishment year

• Strong foundation laid for success

• Impact of boom in dairy prices

– Accelerated land purchases

– Expanded capital base

• Farm development program accelerated

• Listing within NZX50

4

Capital base expanded

• IPO in December 2006 raised NZ$105m

• Institutional placement of NZ$39m in April 2007

• Call of remaining 50c per share in December 2007

• Institutional placement and rights issue in December 2007 raise additional NZ$110m

• Shares on issue now 244.2m

5

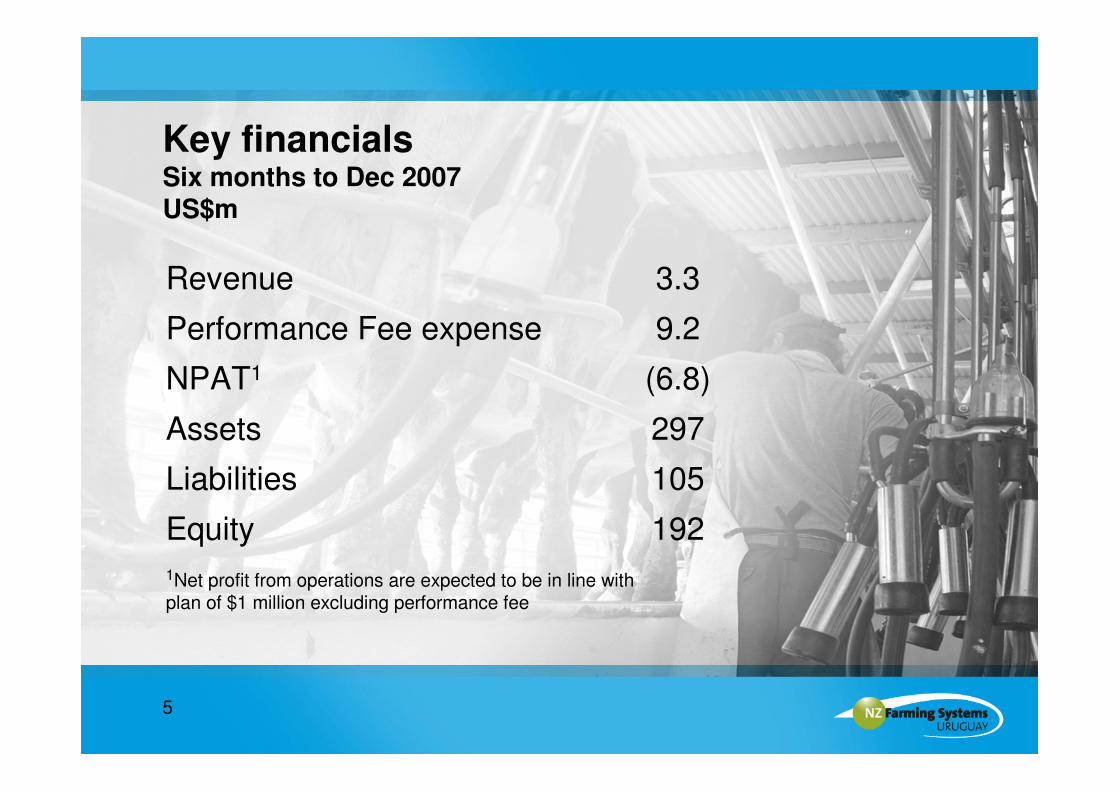

Key financialsSix months to Dec 2007US$m

Revenue 3.3

Performance Fee expense 9.2

NPAT1 (6.8)

Assets 297

Liabilities 105

Equity 192

1Net profit from operations are expected to be in line with plan of $1 million excluding performance fee

6

BackgroundBackground

NZS formed in 2006 to capitalise on:

• High international prices for milk commodity products

• Potential to boost productivity

• High quality, low cost farm land and conversion to NZ-style pasture-based dairy farms

7

Substantial increase in milk prices

• Uruguayan milk price increased from US18c to US31c per litre between Dec 06 and Dec 07

• Record prices are due to supply constraints and changes in underlying demand

• Prices may ease over time but a change is apparent in the supply/demand balance

8

Growing international demand

• Rising incomes in non-OECD countries

• Urbanisation, and changes in diets and tastes, in Asia

• Increasing presence of western retail chains in Asian countries

• Population growth

SOURCE: FAO

9

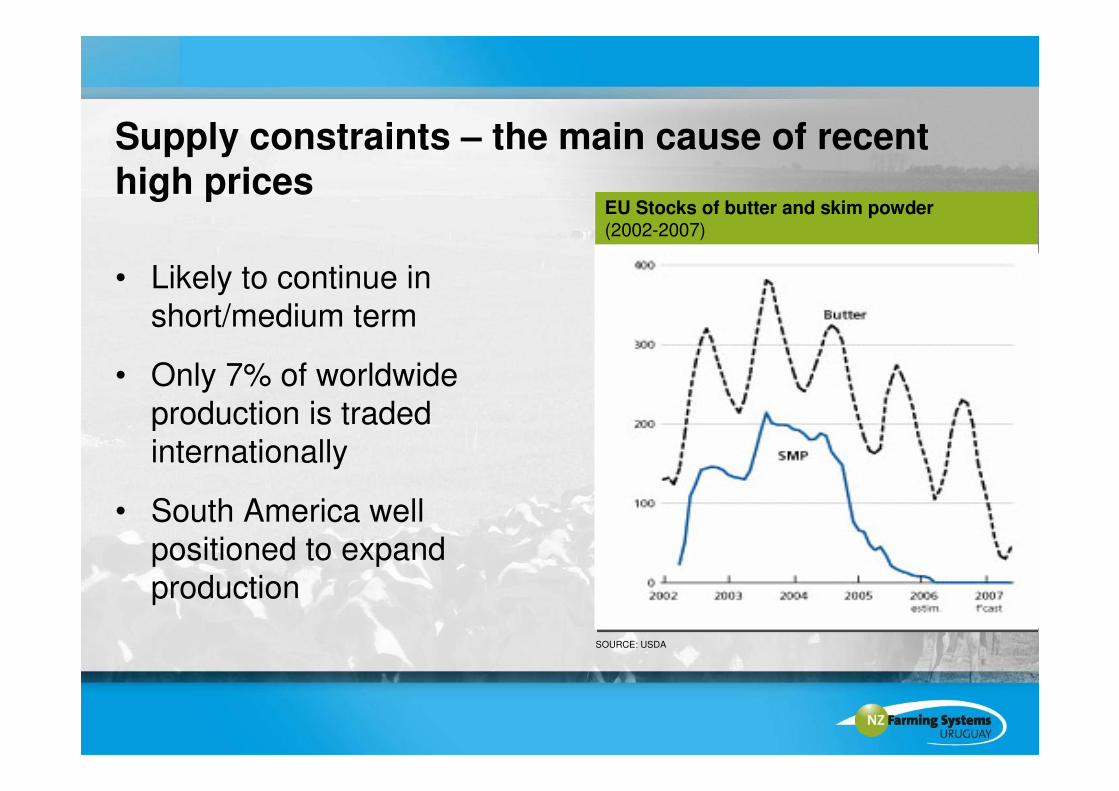

Supply constraints – the main cause of recent high prices

• Likely to continue in short/medium term

• Only 7% of worldwide production is traded internationally

• South America well positioned to expand production

EU Stocks of butter and skim powder(2002-2007)

SOURCE: USDA

10

Development model taking shape on the ground

• Purchase and conversion costs about US$5,500/ha

• Profitability increases over four years

• Business model assumes milking on 60% of farm area and half this area is irrigated

• Current land holdings will be fully productive by 2012

11

Rapid progress on establishment

• Accelerated land acquisition

• 30,980 hectares at 31 December

• 3 regional hubs

• Average price US$2,400 per hectare

12

Development plans on track

• Development plans prepared for all properties and under way

• New Zealand GM of Farm Operations appointed

• 4 Managers employed from NZ, with more to follow as dairy farming increases

• Accelerated pasture development

13

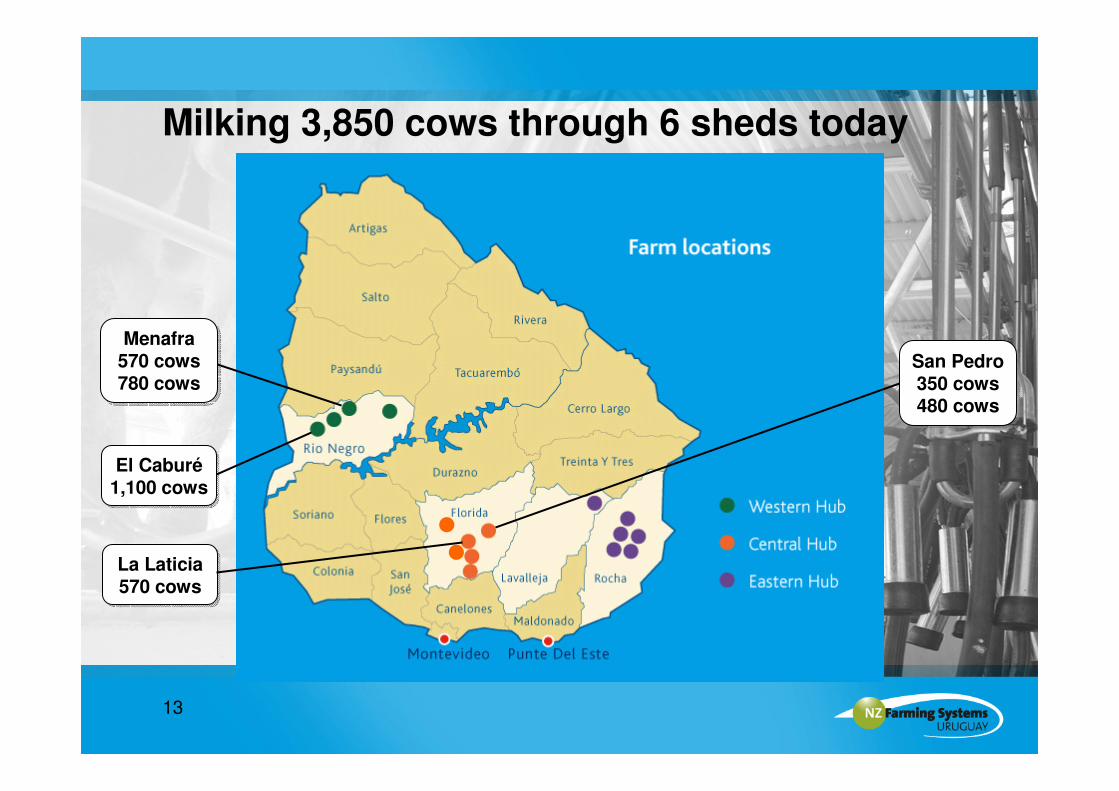

Milking 3,850 cows through 6 sheds today

El Caburé1,100 cows

El Caburé1,100 cows

Menafra570 cows780 cows

Menafra570 cows780 cows

La Laticia570 cows

La Laticia570 cows

San Pedro350 cows480 cows

San Pedro350 cows480 cows

14

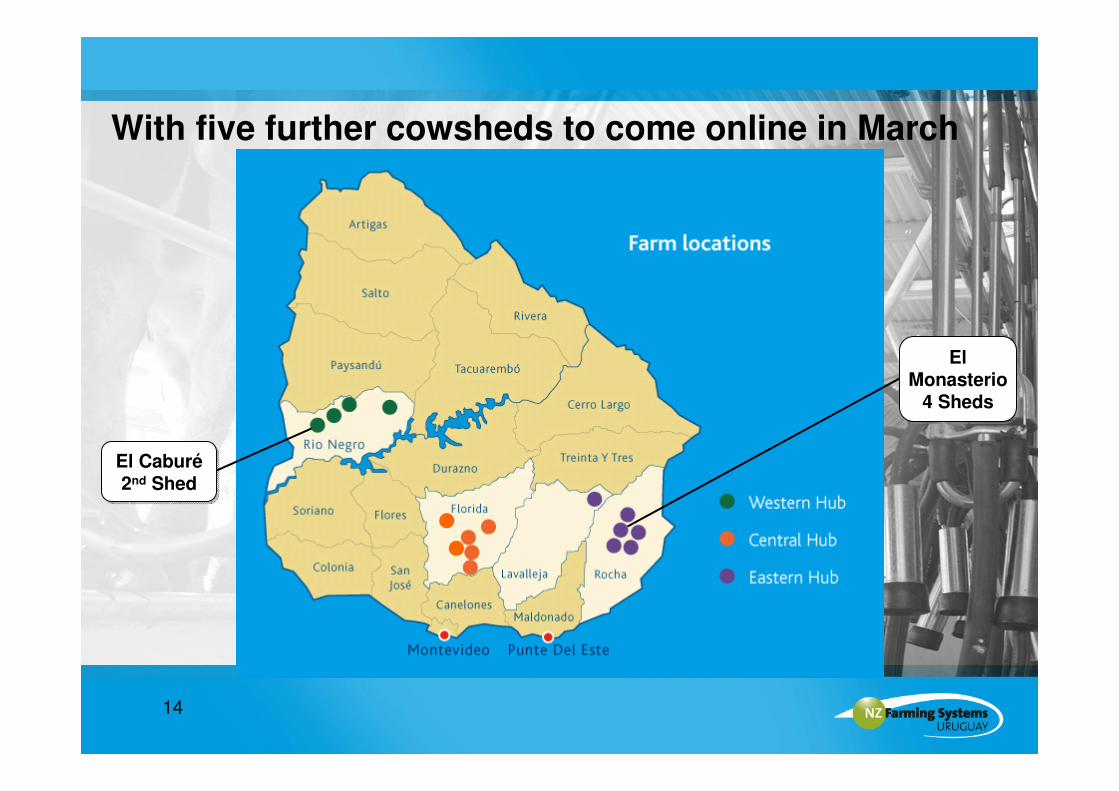

With five further cowsheds to come online in March

El Caburé2nd Shed

El Caburé2nd Shed

El Monasterio

4 Sheds

El Monasterio

4 Sheds

15

Rapid increase in Dairy livestock purchased

38,75723,568Total

1,403496Other stock

12,14713,401Beef cattle

2,3421,832Dairy calves

15,1513,890Dairy heifers

7,7143,949Dairy cows

31 Dec 0730 June 07Quantity

16

Operations on trackOperations on track

• Local staff are performing well

• Good condition of animals despite dry summer

• Expenses managed tightly

• Some cost inflation

• Rising demand for dairy cows increased prices

17

Climate – has been dry but rained in early February

Source: INIA

Accumulated Rainfall (Nov 07 – Jan 08) Soil Moisture (Jan 08, % Field Capacity)

18

Farm productivity meeting expectations

• Farm productivity confirms that levels comparable with NZ can be achieved

• Daily pasture growth rates similar to NZ

• All milk supplied to Conaprole

19

Our current focus – June half-year 08

• Focus on dairy development

• 22,000 hectares being regrassed

• Continued focus on acquisition of land & dairy stock

• 5 new milking sheds to be commissioned

• Local manager recruitment and training

• Expected production of 1.5 million kg milk solids for FY08

20

OutlookOutlook

• Milk price likely to increase to at least US35c/litre (NZ$6.86/kg milk solids) for the next 6 months

• Net profit from operations are expected to be in line with plan of $1 million excluding performance fee

• Drought in NZ & Australia should extend the current high milk prices

• Longer-term demand for dairy products likely to outstrip supply

21

• Inaugural Fonterra Chairman

• Grew up on a dairy farm north of Auckland

• Moved to South Island, (Ashburton) in 1980

• One of the pioneers of large scale dairying in the South Island

Additional Independent Director –John Roadley

22