Nuclear Energy: Industry update and the implications for ...

16

Nuclear Energy: Industry update and the implications for fluorspar David Landry, P.Eng, Cameco Corporation

Transcript of Nuclear Energy: Industry update and the implications for ...

Nuclear Energy: Industry update and the implications for

fluorspar

David Landry, P.Eng, Cameco Corporation

Safety Moment – INPO - Lessons Learned from Fukushima

• Institute of Nuclear Power Operations

• http://www.wano.info/publications/

• Strong Safety Culture • Organizations should focus on strengthening the application

of safety culture principles associated with questioning

attitude, decision making, the special & unique aspects of

your technology and organizational learning

Safety Moment – INPO - Lessons Learned from Fukushima

• How does your organization avoid “group thinking” or accepting

unverified assumptions when making decisions that could

effect safety?

• How would your organization provide the needed level of

questioning and challenging of assumptions during a complex

event?

• What additional approaches are used during an event when

important decisions must be made relatively quickly?

• When discussing issues that could effect plant safety or

reliability, how effective is your organization in asking “What is

the worst that could happen?”

• How does your organization avoid complacency?

Source: INPO 11-005 Addendum August 2012

Overview

• Nuclear Energy & Fluorspar

• Key Market Drivers for Nuclear Energy

• Impact of Fukushima

• Nuclear Energy Outlook

Nuclear Energy & Fluorspar

Source: Cameco Corporation

Conversion UF6

• UF6 conversion requires approx. 1

mass unit of HF to convert 2 mass

units of U from UO3 to UF6

• HF production requires approx. 2

mass units of CaF2 to produce 1

mass unit of HF

95%

Key Market Drivers for Nuclear Energy

• Rising global demand for energy

• Increasing global population

• Industrialization of emerging economies

• Increasing wealth of emerging

economies

• Global climate change

• Pressure to reduce carbon emissions

Key Market Drivers for Nuclear Energy

Source: World Energy Outlook 2011, OECD / International Energy Agency

World Electricity Consumption (TWh)

Fukushima event recap – March 11, 2011

• Magnitude 9.0 Earthquake

• East coast of Japan

• Loss of multiple power sources

• Series of tsunamis

• Core melt at 3 reactor units

• Contamination of the surrounding area

• Comprehensive global safety review

Nuclear Energy Outlook – Fukushima: Direct Impacts

Source: Cameco Corporation

Japan 48 units operating

6 units permanently

closed

46 units remain offline

2 allowed to restart

Germany 9 units operating

8 units prematurely shutdown

phase-out by 2022

Switzerland 5 units operating

no new builds or license

extensions

phase-out by 2034

Belgium 7 units operating

no license extensions

phase-out by 2025

Italy referendum

– ‘no’

Nuclear Energy Outlook – Key Growth Countries

Source: Cameco Corporation

China 12 GWe /

15 operating

26 under construction

50 planned

60 - 70 GWe by 2020

~160 GWe by 2030

Russia 24 GWe /

33 operating

10 under construction

18 planned

33 GWe by 2020

43 GWe by 2030

India 5 GWe /

20 operating

7 under construction

20 GWe by 2020

48 GWe by 2030

South

Korea

22 GWe /

23 operating

4 under construction

29 GWe by 2020

40 GWe by 2030

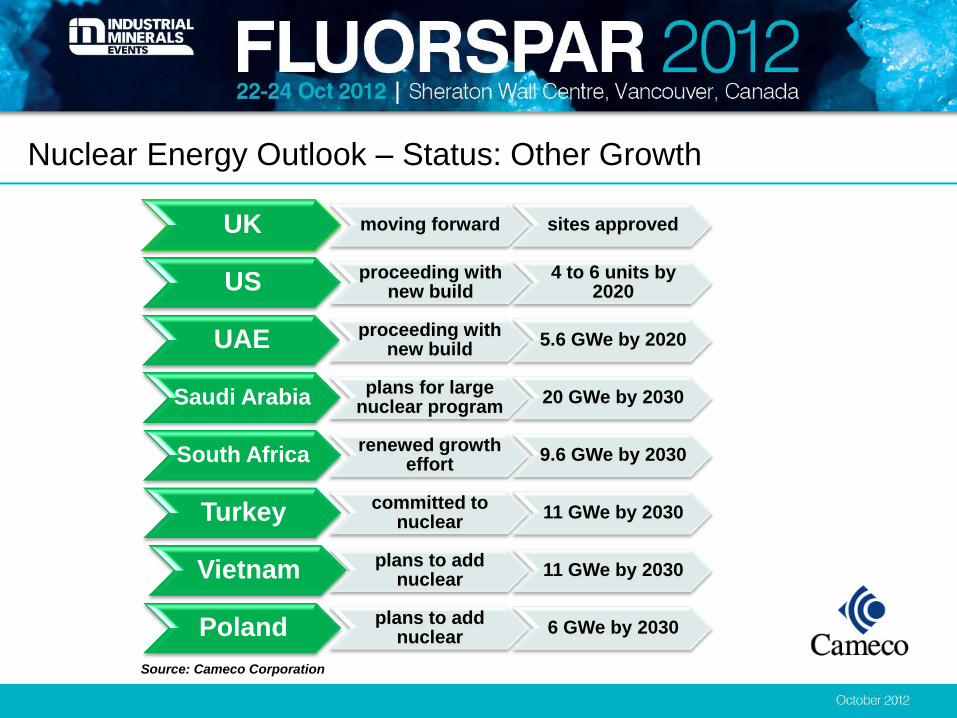

Nuclear Energy Outlook – Status: Other Growth

Source: Cameco Corporation

UK moving forward sites approved

US proceeding with new build

4 to 6 units by 2020

UAE proceeding with new build

5.6 GWe by 2020

Saudi Arabia plans for large

nuclear program 20 GWe by 2030

South Africa renewed growth

effort 9.6 GWe by 2030

Turkey committed to nuclear

11 GWe by 2030

Vietnam plans to add nuclear

11 GWe by 2030

Poland plans to add nuclear

6 GWe by 2030

New Build Outlook – Planned Reactors 2012 to 2021

Source: Cameco Corporation

Region /

Country

Operable

July 2012

New Shut Operable

2021

Change

Americas 127 11 6 132 5

Europe 137 11 14 134 (3)

Asia 77 14 1 90 13

Other* 6 7 - 13 7

India 20 15 - 35 15

China 15 52 - 67 52

Russia &

E. Europe**

49 17 11 55 6

Total 431 127 32 526 95

*Other: Iran, Pakistan, South Africa, Turkey, United Arab Emirates

**E. Europe: Armenia, Belarus, Ukraine

Nuclear Energy Outlook – Expected Annual World Consumption

Source: Cameco Corporation

million lbs U3O8

230

Increase of 55 M lb U3O8

or 21,200 mT U

(avg annual growth rate = 3%)

Requires over 21,000 mT CaF2

acid spar to produce sufficient

HF quantity for UF6 conversion

Assumptions: Stoichiometric ratios,

no HF from secondary sources, All

U to UF6 (Note ~95% of reactors

are light water reactors)

Summary

• Short Term:

• Some reactors shutdown

• Industry pause to learn from event

• Policy

• Long Term:

• Industry fundamentals remain sound

• Growth projected at 3% annual rate

Closing Summary

• World Electricity consumption to double

over the next two decades

• Uranium consumption to grow at 3%

per annum

• Acid spar required to support this

growth is projected at 2000 mT per

annum growth

Questions?

David Landry, P.Eng,

Cameco Corporation

Port Hope, ON, Canada