NPA MANGEMENT

62

A PROJECT REPORT ON NPA MANAGEMENT Submitted in the partial fulfillment of the requirement for the award of Degree of Masters of Management Studies Under the University of Mumbai Submitted By: Mr. MOHD ARIF [email protected] 9320804505 Under the guidance of: Dr. N. MAHESH A C PATIL COLLEGE OF ENGINEERING MANAGEMENT STUDIES & RESEARCH SECTOR-4, KHARGHAR NAVI MUMBAI-410210 1

-

Upload

mohd-arif-khan -

Category

Documents

-

view

135 -

download

0

description

PROJECT REPORT ON NPA MANGEMENT

Transcript of NPA MANGEMENT

A

PROJECT REPORT

ON

NPA MANAGEMENT

Submitted in the partial fulfillment of the requirement for the award of

Degree of Masters of Management Studies

Under the University of Mumbai

Submitted By:

Mr. MOHD ARIF

9320804505

Under the guidance of:

Dr. N. MAHESH

A C PATIL COLLEGE OF ENGINEERING MANAGEMENT

STUDIES & RESEARCH SECTOR-4, KHARGHAR

NAVI MUMBAI-410210

1

Acknowledgement

I express my sincere thanks to Dr. N.MAHESH (HOD) of MMS Department of A C Patil

college of Engineering management studies & research, for his valuable suggestion and

help to prepare this project.

I wish to take opportunity to express my deep sense of gratitude to Dr. D. G. BORSE

Director of A C Patil college of Engineering management studies & research. He has been a

constant source of inspiration.

I express my deep sense o gratitude to Prof. NILIMA ASTHANKAR and to other faculty

members of the MMS department, for offering me suggestion and help me in successfully

completing my project.

Finally it is my foremost duty to thank my parents who has also been the source of

inspiration.

Reg No.08126

Place: MUMBAI

Date: 12/02/2010 MOHD ARIF

2

Declaration

I hereby declare that this project report ”NPA MANAGEMENT” is a record of work

carried out by me under the guidance of Dr .N .MAHESH in the partial fulfillment of the

requirement for the award to degree of Masters of Management Studies.

I also hereby declare that this project report is the result of my own effort and has not

been submitted at any time to any other University or institute for the award of any degree or

diploma.

Reg No.08126

Place: MUMBAI

Date: 12/02/2010 MOHD ARIF

3

COLLEGE CERTIFICATE

This is to certify that Mr. MOHD ARIF a student of A C PATIL COLLEGE OF

ENGINEERING MANAGEMENT STUDIES & RESEARCH, KHARGHAR has

completed his specialization project on “NPA MANAGEMENT” in the field of finance

under the guidance of Dr. N. MAHESH.

Dr. N. MAHESH Dr. D. G. BORSE

(HEAD OF DEPARTMENT) (DIRECTOR)

4

5

GUIDE CERTIFICATE

This is to certify that Mr. MOHD ARIF student of final year of Masters of

Management Studies of A.C PATIL COLLEGE OF ENGINEERING MANAGEMENT

STUDIES & RESEARCH specializing in FINANCE has prepared his specialization project

report titled “NPA MANAGEMENT” under my guidance for the partial fulfillment of

Masters of Management Studies from University of Mumbai in the Academic year (2008-10)

Place: MUMBAI

Date: 12/02/2010 Dr. N. MAHESH

6

Chapter 1

1.1 INTRODUCTION

The accumulation of huge non-performing assets in banks has assumed great

importance. The depth of the problem of bad debts was first realized only in early 1990s.

The magnitude of NPAs in banks and financial institutions is over Rs.1,50,000 crores.

While gross NPA reflects the quality of the loans made by banks, net NPA shows

the actual burden of banks. Now it is increasingly evident that the major defaulters are the

big borrowers coming from the non-priority sector. The banks and financial institutions have

to take the initiative to reduce NPAs in a time bound strategic approach.

Public sector banks figure prominently in the debate not only because they

dominate the banking industries, but also since they have much larger NPAs compared with

the private sector banks. This raises a concern in the industry and academia because it is

generally felt that NPAs reduce the profitability of a banks, weaken its financial health and

erode its solvency.

7

1.2 INRODUCTION TO BANKING:

Banking is nothing but a service. Banks are business organizations selling banking

services. Banks continuously reassess how a customer views bank services, what are new and

emerging customer aspirations and how these can be satisfied.

ORIGIN:

Since the banking activities were started in different periods in different countries,

there is no unanimous view regarding the origin of the word bank. The word bank is derived

from the French word ‘banco’ or ‘Bancus’, which means a bench. Infact the early Jews in

Lombardy transacted their banking business sitting on benches. When the business ailed, the

benches were broken and hence the word bankrupt came in to vogue.

DEFINITION:

The Indian Banking Companies Act, 1949 section 5(b), defines banking as

“accepting for purpose of lending or investing of deposits from the public, repayable on

demand or otherwise and withdrawals by cheque, drafts, and orders or otherwise”.

Banks are backbone of our society. A bank must meet the financial needs of a customer, by

acting as a custodian of his assets, providing credit facilities and assisting him to speedily put

through financial transaction of one type or another. Banking when you comer to think of it is

people. It is not figures, files and ledgers. Bank services needs considerable improvement on

an emergent basis. The time has come for banks to look inward to find out what is the nature

and quality of the products they sell, what is the product demanded by the customer.

It would be unrealistic today to believe that banks are mere financial institutions, working for

profit. Banks essentially are now social organizations, regarding financial services to sub

serving the socio-economic objectives of the society.

8

IN INDIA:

India has a system of indigenous banking from very early times, though it was not

similar to banking of modern times. There is evidence to show that money lending existed

even during the Vedic period. With the advent of the English traders in the seventeenth

century and the establishment of trading centers by the East India Company encouraged the

establishment of what were known as the agency houses? The trading firms which undertook

banking operations for the benefit of their constituents. Some of the houses established during

the period were Alexander and Co. and Ferguson & Co. There were also Presidency Banks,

Joint stock banks and Exchange banks which took up gradually one after the other.

IMPERIAL BANK:

The Presidency Banks referred to above were amalgamated into the Imperial Bank of

India, which was brought into existence on 27th January 1921 by the Imperial Bank of India

Act 1920. This Act, however, gave the bank no power to issue notes and this left out without

control over the currency of the country. But it was allowed to hold Government balances and

to manage public debt and clearing houses till the establishment of Reserve Bank Of India in

1935 which apart from taking over all these functions from the Imperial Bank of India, was

given the privilege of acting as an agent of the latter in places where it had no branches.

COMMERCIAL BANKS:

Amongst the banking institutions in the organized sector, the commercial banks initially were

established as corporate bodies with share holdings by private individuals, but subsequently

there has been a drift towards central ownership and control. Today 27 banks constitute the

strong public sectors in Indian Commercial Banking. Up to late 60’s Commercial Banks are

mainly engaged in financing organized trade, commerce & industry , since then they are

actively participating in financing agriculture, small-scale business ands small borrowers

also.

9

FUNCTIONS OF COMMERCIAL BANKS:

Commercial banks perform several crucial functions, which may be classified into two

categories:

(a) Primary functions and

(b) Secondary functions

PRIMARY FUNCTIONS:

Primary banking functions of the commercial banks include:

I) acceptance of deposits from public

II) lending funds

III) use of cheque system and

IV) remittance of funds

SECONDARY FUNCTIONS:

Commercial banks perform a multitude of other non banking functions, which may be

classified as

(a) Agency service

(b) General utility services

NATIONALIZATION OF COMMERCIAL BANKS:

The major historical event in the history of banking in India after independence is

undoubtedly the nationalization of the 14 major banks on 19th July 1969. In 1980, six more

private sector banks are nationalized extending the public domain further over the banking

sector. Nationalization was deemed as a major step in achieving the socialistic pattern of

society. The nationalized banks were to increase lending to areas of importance to the

10

government and to use their resources for sub-serving the common good. A detailed scheme

of objectives, regulations, management, etc was drawn up for these banks.

Nationalization was recognition of the potential of the banking system to promote broader

economic objectives. The banks had to reach out and expand their networks so that the

concept of mass banking was given importance over class banking.

THE RESERVE BANK OF INDIA [RBI]:

The Central Bank of India called the Reserve Bank of India was constituted under the

Reserve Bank of India Act, 1934 to regulate the issue of bank notes and keeping of reserves

with a view to securing monetary stability in India and generally to operate the currency and

credit system of India to its advantage. Amongst its multifarious functions affecting the

Indian Financial System, the RBI regulates and prohibits the issue of prospectus or

advertisement soliciting deposits of money, regulates the functioning of non-banking

institutions and transacts Government business. Its regulatory involvement in the Indian

Capital Markets is primarily of debt management through primary dealers, foreign exchange

control and liquidity support to market participants. The RBI regulates participants in the

securities markets when a foreign transaction is involved. Transactions that include Indian

issuers issuing of security outside India, such as GDRs and ADRs, and Financial Institutional

Investors (FIIs) or Foreign Brokers selling, buying or dealing in Indian Securities need the

permission of RBI.

As the central banking authority of India, the Reserve Bank of India performs the following

traditional functions of the central bank:

I. It provides currency and operates as the clearing system for the banks.

II. It formulates and implements monetary and credit policies.

III. It functions as the banker’s bank.

IV. It supervises the operations of credit institutions.

V. It regulates foreign exchange transactions.

VI. It moderates the fluctuations in the exchange value of the rupee.

11

In addition to the traditional function of the central banking authority, the

Reserve Bank of India performs several functions aimed at developing the

Indian financial system:

It seeks to integrate the unorganized financial sector with the organized

financial sector.

It encourages the extension of the commercial banking system in the

rural areas.

It influences the allocation of credit.

It promotes the development of new institutions.

12

13

Chapter. 2

LITERATURE REVIEW

1. Economic an political weekly, October 16, 2004, CARLTON PEREIRA,pg 4602-4604

“INVESTING IN NPAs”.

2. THE TREASURY MANAGEMENT, DECEMBER 2004, vinay kumar,PG62-

66”securitisation:issues and perspectives”

At The Global Level, SECURITISATION is becoming more popular among Fis. It is

meant to avoid disparity between assets and liabilities of banks/Fis. In order to promote

securitization in India RBI has constituted a working group on assets securitization. Though

securitization is in a nascent stage, it holds great promise in areas like infrastructure, power

and housing.

3. Chartered Secretary, February 2003, V. S. Datey, Pg. 128-135 “THE SARFAESI ACT”

The securities and reconstruction of financial assets and enforcement of security

interest act, 2002 made effective on 21.6.2002 is a step to reduce NPAs of Banks. The act

also makes provision for asset reconstruction and securitization.

14

Chapter 3

RESEARCH METHODOLOGY

3.1 Type of Research

The research methodology adopted for carrying out the study were

In this project Descriptive research methodologies were use.

At the first stage theoretical study is attempted.

At the second stage Historical study is attempted.

At the Third stage Comparative study of NPA is undertaken.

3.2 OBJECTIVES OF THE STUDY

The basic idea behind undertaking the Grand Project on NPA was to:

To evaluate NPAs (Gross and Net) in different banks.

To evaluate NPA level in different economic situation.

To Know the Concept of Non Performing Asset

To Know the Impact of NPAs

To Know the Reasons for NPAs

To learn Preventive Measures

3.3 Scope of the Study

Concept of Non Performing Asset

Impact of NPAs

Reasons for NPAs

Preventive Measures

Tools to manage NPAs

15

3.4 Limitations of the project:

Due to time constraint depth analysis could not be made.

Some of the information is considered confidential and not available for the study.

The data taken for interpretation is for a limited period.

3.5 Sampling plan

To prepare this Project we took five banks from public sector as well as five banks from

private sector.

3.6 Data collection

The data collected for the study was secondary data in Nature.

16

Chapter 4

About the topic

4.1 INTRODUCTION:

It’s a known fact that the banks and financial institutions in India face the problem of

swelling non-performing assets (NPA’s) and the issue is becoming more and more

unmanageable. In order to bring the situation under control, some steps have been taken

recently. The Securitization and Reconstruction of Financial Assets and Enforcement of

Security Interest Act, 2002 was passed by parliament, which is an important step towards

elimination or reduction of NPA’s.

EMERGENCE OF THE WORD NON-PERFORMING ASSET:

The issues relating to definition, management or the mismanagement and

recommendations calling for spectacular solutions to the problem of non-performing

advances of banks are being deliberated at frequent intervals during last decade or so.

In late 80s the concept of classification of bank advances in several health code categories

took place though the terminology non-performing advances did not exist at that time. This is

followed by early 90s Anglo-American model of categorization of bank lending portfolio in

several blocks of nomenclature in that included the non-performing advances.

The rapid popularity of the phenomenon can be ascribed to the opening up of the Indian

economy and consequent pressure from western powers to influence our banking system in

the name of international standards of accounting, congruence of banking supervision by

Basle committee, and so on.

The sudden shock of guidelines relating to non-performing advances and simultaneous of

income recognition made the Indian banking system totter and a number of public sector

17

banks started incurring losses from the mid-nineties. Then came the recommendations of the

Narasimham committee with the proposition of creating asset-reconstruction fund for

cleaning the balance sheets of the banks of non-performi8ng advances as a one-time measure.

MEANING OF NPA’s:

An asset is classified as non-performing asset (NPA’s) if the borrower does not pay

dues in the form of principal and interest for a period of 180 days. However with effect from

March 2004, default status would be given to a borrower if dues are not paid for 90 days, if

any advance or credit facilities granted by bank to a borrower become non-performing, then

the bank will have to treat all the advances/credit facilities granted to that borrower as non-

performing without having any regard to the fact that there may still exist certain advances/

credit facilities having performing status. In simple words, an asset which ceases to yield is a

non-performing asset.

DEFINITION GIVEN BY THE NARASIMHAM COMMITTEE:

The committee has defined non-performing assets as advances here, as on the date of

balance sheet,

1. In respect of term loans, interest remains past due for a period of more than 90 days.

2. Overdrafts and cash credits accounts remain out of order for more than 90 days.

3. date Bills purchased and discounted remain over due and unpaid for a period of more

than 90 days.

An amount is considered past due when it remains outstanding for 30 days beyond the

due

.

18

4.2 Types of NPA

A] Gross NPAA] Gross NPA

B] Net NPAB] Net NPA

A] Gross NPA:A] Gross NPA:

Gross NPAs are the sum total of all loan assets that are classified as NPAs as per RBI

guidelines as on Balance Sheet date. Gross NPA reflects the quality of the loans made by

banks. It consists of all the non standard assets like as sub-standard, doubtful, and loss

assets.

It can be calculated with the help of following ratio:

Gross NPAs Ratio Gross NPAs

Gross Advances

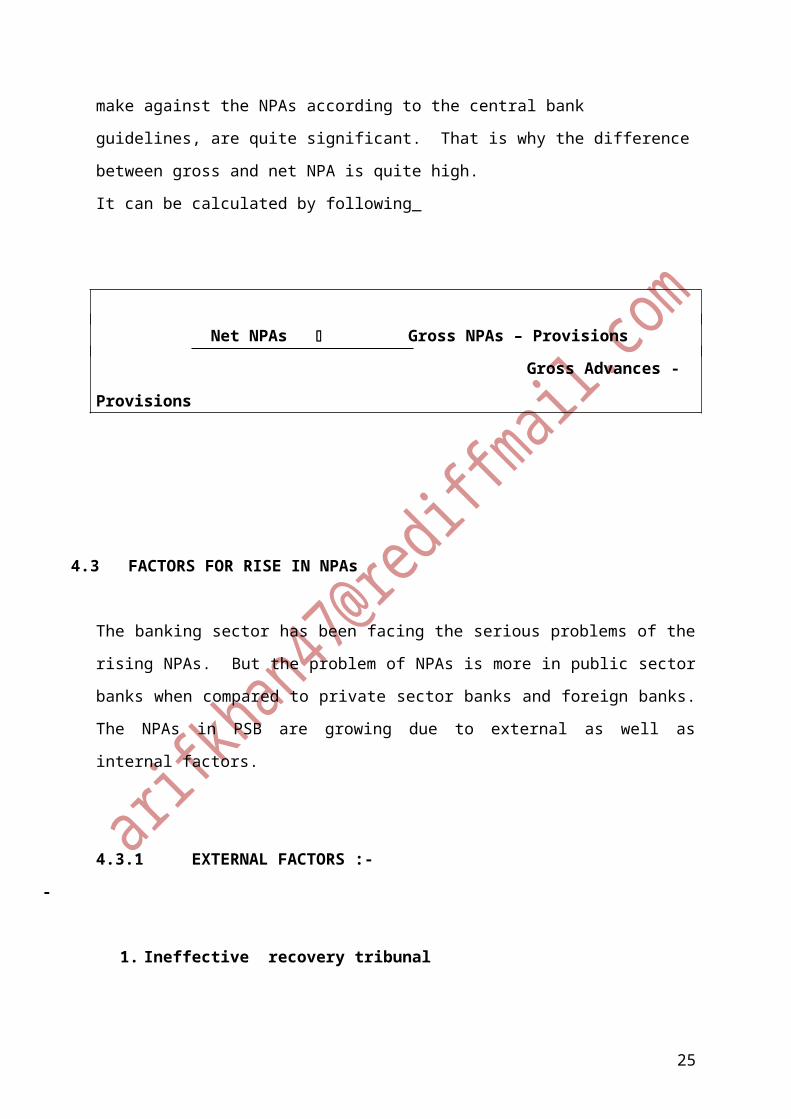

B] Net NPA:B] Net NPA:

Net NPAs are those type of NPAs in which the bank has deducted the provision regarding

NPAs. Net NPA shows the actual burden of banks. Since in India, bank balance sheets

contain a huge amount of NPAs and the process of recovery and write off of loans is very

time consuming, the provisions the banks have to make against the NPAs according to the

central bank guidelines, are quite significant. That is why the difference between gross and

net NPA is quite high.

It can be calculated by following_

Net NPAs Gross NPAs – Provisions

Gross Advances - Provisions

19

4.3 FACTORS FOR RISE IN NPAs

The banking sector has been facing the serious problems of the rising NPAs. But the

problem of NPAs is more in public sector banks when compared to private sector banks and

foreign banks. The NPAs in PSB are growing due to external as well as internal factors.

4.3.1 EXTERNAL FACTORS :-

-

1. Ineffective recovery tribunal

The Govt. has set of numbers of recovery tribunals, which works for recovery of loans

and advances. Due to their negligence and ineffectiveness in their work the bank

suffers the consequence of non-recover, their by reducing their profitability and

liquidity.

2. Willful Defaults

There are borrowers who are able to payback loans but are intentionally withdrawing

it. These groups of people should be identified and proper measures should be taken

in order to get back the money extended to them as advances and loans.

3. Natural calamities

This is the measure factor, which is creating alarming rise in NPAs of the PSBs. every

now and then India is hit by major natural calamities thus making the borrowers

unable to pay back there loans. Thus the bank has to make large amount of provisions

in order to compensate those loans, hence end up the fiscal with a reduced profit.

Mainly ours farmers depends on rain fall for cropping. Due to irregularities of rain fall

the farmers are not to achieve the production level thus they are not repaying the

loans.

20

4. Industrial sickness

Improper project handling , ineffective management , lack of adequate resources ,

lack of advance technology , day to day changing govt. Policies give birth to

industrial sickness. Hence the banks that finance those industries ultimately end up

with a low recovery of their loans reducing their profit and liquidity.

5. Lack of demand

Entrepreneurs in India could not foresee their product demand and starts production

which ultimately piles up their product thus making them unable to pay back the

money they borrow to operate these activities. The banks recover the amount by

selling of their assets, which covers a minimum label. Thus the banks record the non

recovered part as NPAs and has to make provision for it.

6. Change on Govt. policies

With every new govt. banking sector gets new policies for its operation. Thus it has to

cope with the changing principles and policies for the regulation of the rising of

NPAs.

The fallout of handloom sector is continuing as most of the weavers Co-operative

societies have become defunct largely due to withdrawal of state patronage. The

rehabilitation plan worked out by the Central government to revive the handloom

sector has not yet been implemented. So the over dues due to the handloom sectors

are becoming NPAs.

4.3.2 INTERNAL FACTORS :-

1 Defective Lending process

21

There are three cardinal principles of bank lending that have been followed by the

commercial banks since long

.

I. Principles of safety

II. Principle of liquidity

III. Principles of profitability

2 Principles of safety :-

By safety it means that the borrower is in a position to repay the loan both principal and

interest. The repayment of loan depends upon the borrowers:

I Capacity to pay

II Willingness to pay

3 Reputation of borrower

The banker should, therefore take utmost care in ensuring that the enterprise or

business for which a loan is sought is a sound one and the borrower is capable of

carrying it out successfully .he should be a person of integrity and good character.

4 Inappropriate technology

Due to inappropriate technology and management information system, market driven

decisions on real time basis can not be taken. Proper MIS and financial accounting

22

system is not implemented in the banks, which leads to poor credit collection, thus

NPA. All the branches of the bank should be computerized.

5 Improper SWOT analysis

The improper strength, weakness, opportunity and threat analysis is another

reason for rise in NPAs. While providing unsecured advances the banks

depend more on the honesty, integrity, and financial soundness and credit

worthiness of the borrower.

6 Purpose of the loan

When bankers give loan, he should analyze the purpose of the loan. To ensure safety and

liquidity, banks should grant loan for productive purpose only. Bank should analyze the

profitability, viability, long term acceptability of the project while financing.

7 Poor credit appraisal system

Poor credit appraisal is another factor for the rise in NPAs. Due to poor credit appraisal the

bank gives advances to those who are not able to repay it back. They should use good

credit appraisal to decrease the NPAs.

8 Managerial deficiencies

The banker should always select the borrower very carefully and should take tangible

assets as security to safe guard its interests. When accepting securities banks should

consider the_

1. Marketability

2. Acceptability

3. Safety

23

4. Transferability.

The banker should follow the principle of diversification of risk based on the famous

maxim “do not keep all the eggs in one basket”; it means that the banker should not grant

advances to a few big farms only or to concentrate them in few industries or in a few cities.

If a new big customer meets misfortune or certain traders or industries affected adversely,

the overall position of the bank will not be affected.

9 Absence of regular industrial visit

The irregularities in spot visit also increases the NPAs. Absence of regularly visit of bank

officials to the customer point decreases the collection of interest and principals on the

loan. The NPAs due to willful defaulters can be collected by regular visits.

10 Re loaning process

Non remittance of recoveries to higher financing agencies and re loaning of the same have

already affected the smooth operation of the credit cycle.

Due to re loaning to the defaulters and CCBs and PACs, the NPAs of OSCB is increasing

day by day.

24

4.4 PROBLEMS DUE TO NPA

1. Owners do not receive a market return on there capital .in the worst case, if the banks

fails, owners loose their assets. In modern times this may affect a broad pool of

shareholders.

2. Depositors do not receive a market return on saving. In the worst case if the bank

fails, depositors loose their assets or uninsured balance.

3. Banks redistribute losses to other borrowers by charging higher interest rates, lower

deposit rates and higher lending rates repress saving and financial market, which

hamper economic growth.

4. Non performing loans epitomize bad investment. They misallocate credit from good

projects, which do not receive funding, to failed projects. Bad investment ends up in

misallocation of capital, and by extension, labour and natural resources.

Non performing asset may spill over the banking system and contract the money

stock, which may lead to economic contraction. This spill over effect can channelize

through liquidity or bank insolvency:

a) When many borrowers fail to pay interest, banks may experience liquidity

shortage. This can jam payment across the country,

b) Illiquidity constraints bank in paying depositors

.c) Undercapitalized banks exceeds the banks capital base.

The three letters Strike terror in banking sector and business circle today. NPA is

short form of “Non Performing Asset”. The dreaded NPA rule says simply this: when

interest or other due to a bank remains unpaid for more than 90 days, the entire bank

loan automatically turns a non performing asset. The recovery of loan has always

been problem for banks and financial institution. To come out of these first we need to

think is it possible to avoid NPA, no can not be then left is to look after the factor

responsible for it and managing those factors.

Interest and/or instalment of principal remains overdue for two harvest seasons

but for a period not exceeding two half years in the case of an advance granted

for agricultural purposes, and

25

Any amount to be received remains overdue for a period of more than 90 days in

respect of other accounts.

As a facilitating measure for smooth transition to 90 days norm, banks have been

advised to move over to charging of interest at monthly rests, by April 1, 2002.

However, the date of classification of an advance as NPA should not be changed on

account of charging of interest at monthly rests. Banks should, therefore, continue to

classify an account as NPA only if the interest charged during any quarter is not

serviced fully within 180 days from the end of the quarter with effect from April 1,

2002 and 90 days from the end of the quarter with effect from March 31, 2004.

26

4.54.5 Impact of NPAImpact of NPA

4.5.1 Profitability:-4.5.1 Profitability:-

NPA means booking of money in terms of bad asset, which occurred due to wrong

choice of client. Because of the money getting blocked the prodigality of bank decreases

not only by the amount of NPA but NPA lead to opportunity cost also as that much of

profit invested in some return earning project/asset. So NPA doesn’t affect current profit

but also future stream of profit, which may lead to loss of some long-term beneficial

opportunity. Another impact of reduction in profitability is low ROI (return on

investment), which adversely affect current earning of bank.

4.5.2. Liquidity:-4.5.2. Liquidity:-

Money is getting blocked, decreased profit lead to lack of enough cash at hand which lead

to borrowing money for shot\rtes period of time which lead to additional cost to the

company. Difficulty in operating the functions of bank is another cause of NPA due to

lack of money. Routine payments and dues.

4.5.34.5.3 Involvement of management:-Involvement of management:-

Time and efforts of management is another indirect cost which bank has to bear due

to NPA. Time and efforts of management in handling and managing NPA would have

diverted to some fruitful activities, which would have given good returns. Now day’s

banks have special employees to deal and handle NPAs, which is additional cost to

the bank.

27

4.5.44.5.4 Credit loss:-Credit loss:-

Bank is facing problem of NPA then it adversely affect the value of bank in terms of

market credit. It will lose it’s goodwill and brand image and credit which have negative

impact to the people who are putting their money in the banks .

28

Chapter 5

Preventive measures of NPA

5.1 Early identification:

I) Identification of accounts showing early warning signals.

II) High values NPA’s should be given focused attention.

III) A systematic review of problems loans should be done. The time norms for the

problem loan review should be adhered to. Action plan to be drawn up for each

account and follow up.

5.2 Recovery:

Actual recovery occurs in the accounting in which the total recovery of the dues is

warranted. Through regular pre and post sanction monitoring, follow-ups, the NPA’s can

be eliminated.

5.3 Up gradation:

The NPA accounts in which part recovery of the total, dues will upgrade the account

from NPA to performing asset. Generally the NPA accounts with less than 2 years of the

age under NPA are covered. The main characteristic of these accounts is after

elimination from NPA, also these accounts continued to be part of advances. Since

lending is a main business of the banks up gradation of accounts is preferred.

Substandard accounts to be specially targeted for up gradation.

Up gradation strategies would include adjustment of irregularity, repayment of over

due interest/installment and up gradation following restructuring/ rehabilitation.

29

Replacement/re-schedulement of loans should be done in deserving cases promptly.

After 1 year of successful implementation, account to be reviewed for up gradation.

5.4 Rehabilitation:

Rehabilitation of units should be taken up in deserving cases.

5.5 Repayment:

Fixing repayment programme for accounts while continued viability is in doubt.

Fixing installments for irregular amount were limits to be continued with reduced

exposure.

5.6 Compromise:

Through compromise the accounts are closed by negotiated settlement with the

borrowers as per the compromise policy of the bank. Generally compromises are encouraged

in cases of chronic NPA accounts.

Compromise proposals need to be considered where necessary, and in time.

Option of OTS through Lok Adalat should be examined.

30

Chapter 6

RECOVERY TOOLS AND THEIR EFFECTIVENESS:

6.1. DEBT RECOVERY TRIBUNALS:

Lack of expeditious court remedies has been one of the major impediments

experienced by banks and financial institutions in the recovery of NPA. On the basis

of the recommendation of Tiwari Committee(1981) and Narsimham Committee on

financial systems(1991), which emphasized the need for the establishment of special

tribunals for banks and financial institutions, the recovery of debts due to banks and

financial institutions act was enacted in1993.

The act applies only to cases where the amount of debt due to banks/financial

institution is Rs 10 lakhs or above. Filing of cases at the DRT has been a cause of

concern for almost every bank in the country today. One reason for the slow pace is

the requisite infrastructure at the respective DRT was inadequate to handle the huge

number of cases pending with it. There has been a decision to add about 7 more DRT

to the existing 22 DRT and 5 appellate authorities. This enables the banks to settle

some of the pending NPAs.

6.2. LOK ADALATS:

For recovery of smaller loans, the Lok Adalat has proved a very good agency for quick

justice and settlement of dues. The Gujarat State Legal Service Authority and the DRT,

Ahmadabad have nominated and appointed conciliators to deal with the cases before the

Lok Adalat comprising of retired High Court Judge and two members from senior

advocates/industrialists/executives of the banks. These Adalats in the state of Gujarat

31

have been found to be useful as supplement to the efforts of the efforts of the recovery by

the DRTs. Such agencies should be established in all the states.

6.3. ASSET RECONSTRUCTION COMPANY:

The setting of Asset Reconstruction Company may be another channel to discount the

NPAs of the bank to such an agency and to developing the process of securitization of

banks loan assets for providing liquidity. Perhaps secondary market of derivatives based

on securitized assets could also be developed as in individual countries.

6.4. REVENUE RECOVERY ACT:

In some states, revenue recovery act has been made applicable to banks. Since this is also

expeditious process of adjudicating claims, banks may be notified to cover the Act by

state.

32

THE SECURITISATION AND RECONSTRUCTION OF FINANCIAL

ASSETS AND ENFORCEMENT OF SECURITY INTEREST ACT, 2002

(SARFAESI ACT):

There was an acute need being felt for assistance to the banks and other financial

institutions in the recovery of loans, for there were heavy losses being incurred on

account of unpaid debts. To regulate securitization and reconstruction of financial assets

and enforcement of security interest the president, on 21st day of June 2002 promulgated

the securitization and reconstruction of financial assets and enforcement of Security

Interest Act.

Definition of securitization:

Securitization means acquisition of financial assets by any securitization company or

reconstruction company from any originator, whether by raising of funds by such

Securitization Company or Reconstruction Company from qualified institutional buyers

by issue of security receipts representing undivided interest in such financial assets.

Measures for assets reconstruction:

When the borrower fails to repay the loan amount, then according to RBI guidelines the

construction company can take following measures:

The proper management of business of the borrower, by change in, or take over

of, the management of the business of the borrower.

The sale or lease of a part or whole of the business of the borrower.

Rescheduling of payments of debts payable by the borrower.

Enforcement of security interest in accordance with the provisions of this Act.

Settlement of dues payable by the borrower.

Taking possession of secured assets in accordance with the provisions of the act.

33

34

STEPS OR INTIATVES TAKEN BY RBI TO CURTAIL NPA :

Recognizing the fact that the origin of Non-performance could be at the initial stage of loan

decision-making, RBI had impressed upon banks from time to time, to strengthen credit

appraisal and credit supervision. After sanction and dispersal of credit, banks are required to

closely monitor the operation of the borrower units and accounts by way of ostentation of

periodic stock/operation statements brought down, end use, etc. in the cases of incipient cases

sickness, nursing back the sick units, etc. problem accounts above a certain outstanding

balance are required to be monitored individually by designated senior officials of the bank.

In respect of accounts where the classification of assets of the banks are required to take

prompt steps to recover the dues and staff accountability is required to be examined.

Banks have also been advised to take decisions regarding finding of source expeditiously and

to effectively follow up the cases of suit filed and decreed accounts. During periodic

discussions with bank management, special emphasis is given on monitoring of large NPA

accounts at the highest level in the banks and also on reductions of NPA through up

gradation, recovery and compromise settlements. RBI has advised and accordingly bank

boards have laid down policies in regard to credit dispensation, recovery of credit etc. Banks

have constituted recovery cells, recovery branches and NPA management departments and

fixed recovery targets.

Policies evolved and steps taken in this regard are critically examined during the annual on

sight inspection of banks. The off sights returns also provide RBI and insight into the quality

of credit portfolio at quarterly intervals.

Introduction of prudential norms on income recognition, asset classification , provisioning

during 1992-93 and other steps initiated apart from beginning in transparency in the loan

portfolio of banking industry have significantly contributed towards improvement of the pre-

sanction appraisal and post sanction supervision which is reflected in lowering of the levels

of fresh accretion of non-performing advances of banks after 1992.

RBI impressed upon the banks to strengthen the credit appraisal and credit

supervision.

Adoption of 90 days norm for recognition of loan impairment as against the

current norm of 180 days effective March 2004.

35

Reduction in transition period of sub-standard asset to doubtful category to

12 months as against the current norm of 18 months effective from March

2005.

Revision in the CRAR norms in terms of new Basel Capital Accord after

2005.

In cases of incipient sickness, detailed guidelines have been issued to banks

to take steps for avoiding sickness, nursing back the sick units etc.

During periodic description with bank management special emphasis is

given on monitoring of large NPA accounts at the highest level in the banks

and also on reduction of NPAs through up gradation, recovery and

compromise settlements.

RBI has advised and accordingly bank’s boards laid down policies in regard

to credit dispensation, recovery of credit, etc.

Policies evolved and steps taken are critically examined during the annual

on sight inspection of banks.

36

ANALYSIS

For the purpose of analysis and comparison between private sector and public

sector banks, I have taken five-five banks in both sector to compare the non performing assets

of banks and Deposits-Investment-Advances

Deposit – Investment – Advances is the first in the analysis because due to these we

can understand the where the bank stands in the competitive market.

DEPOSIT-INVESTMENT-ADVANCES (RS.CRORE) of both sector banks and comparison

among them,for the year 2008-09.

PRIVATE SECTOR BANKS

BANK DEPOSIT INVESTMENT ADVANCES

AXIS 117374 46330 81557

HDFC 142812 58818 98883

ICICI 230510 103058 195865

KOTAK 15645 9110 16625

INDUSIND 21037 6930 15795

TOTAL 527378 224246 408725

37

At the end of march 2009, in private sector ICICI Bank is the highest deposit-investment-

advances figures in rupees crore, second is HDFC Bank and KOTAK Bank has least figures.

PUBLIC SECTOR BANK

BANK DEPOSIT INVESTMENT ADVANCES

CORP BANK 73984 24938 48512

BOI 189708 52607 144732

DENA 43050 12473 28878

PNB 209760 78605 154703

UBI 138416 67645 96960

TOTAL 654918 236268 473785

.In public sector banks Punjab National Bank has highest deposit-investment-

advances ,Union bank of india and Bank of India are almost the similar in numbers and Dena

38

Bank is stands for last in public sector bank. When we compare the private sector banks with

public sector banks among these banks, we can understand the more number of people prefer

to choose public sector banks for deposit-investment.

ICICI BANK AND PUNJAB NATIONAL BANK :-

\

BANK DEPOSIT INVESTMENT ADVANCES

ICICI BANK 230,510 103058 195,865

PNB 209760 78605 154703

But when we compare the private sector bank ICICI Bank with the public sector banks ICICI

Bank is more deposit-investment figures and first in the all banks.

39

Analysis and comparisons of NPA

There are two concepts related to non-performing assets_ gross and net. Gross refers to all

NPAs on a bank’s balance sheet irrespective of the provisions made. It consists of all the non

standard assets, viz. sub standard, doubtful, and loss assets. A loan asset is classified as ‘ sub

standard” if it remains NPA up to a period of 18 months; “ doubtful” if it remains NPA for

more than 18 months; and loss, without any waiting period, where the dues are considered

not collectible or marginally collectible.

Net NPA is gross NPA less provisions. Since in India, bank balance sheets contains a huge

amount of NPAs and the process of recovery and write off of loans is very time consuming,

the provisions the banks have to make against the NPA according to the central bank

guidelines, are quite significant.

Here, we can see that there is huge difference between gross and net NPA. While gross

NPA reflects the quality of the loans made by banks, net NPA shows the actual burden

of banks. The requirements for provisions are :

100% for loss assets

100% of the unsecured portion plus 20-50% of the secured portion, depending on the

period for which the account has remained in the doubtful category

10% general provision on the outstanding balance under the sub standard category.

Here, there are gross and net NPA data for 2008-09 we taken for comparison among banks.

These data are NPA AS PERCENTAGE OF TOTAL ASSETS. As we discuss earlier that

gross NPA reflects the quality of the loans made by banks.

40

PUBLIC SECTOR BANKS (2008-09)

BANK GROSS NPA NET NPA

CORP BANK 1.14 0.29

BOI 1.71 0.44

DENA 2.13 1.09

PNB 1.77 0.17

UBI 1.96 0.34

Among the public sector banks, Dena Bank has highest gross NPA as a percentage of total

assets in the year 2008-09 and also net NPA. Punjab National Bank shows vast difference

between gross and net NPA. BOI and UBI have almost similar figures.

41

PRIVATE SECTOR BANKS (2008-09)

BANK GROSS NPA NET NPA

AXIS 0.86 0.35

HDFC 1.98 0.63

ICICI 4.32 2.09

KOTAK 3.64 2.02

INDUSIND 1.61 1.14

Among the private sector banks AXIS bank has the lowest Gross NPA as well as Net NPA,

while ICICI bank has the highest Gross NPA

COMPARISON OF GROSS NPA WITH ALL BANKS FOR THE YEAR 2008-

09. The growing NPAs affects the health of banks, profitability and efficiency. In the

long run, it eats up the net worth of the banks. We can say that NPA is not a healthy

sign for financial institutions. Here we take all the ten banks gross NPA together for

42

better understanding. Average of these ten banks gross NPAs is 1.29 as percentage of

total assets. So if we compare in private sector banks AXIS and HDFC Bank are

below average of all banks and in public sector BOB and BOI. Average of these five

private sector banks gross NPA is 1.25 and average of public sector banks is 1.33.

Which is higher in compare of private sector banks.

GROSS NPA :-

COMPARISON OF NET NPA WITH ALL BANKS FOR THE YEAR 2008-09.

Average of these ten bank’s net NPA is 0.56. And in the public sector banks all these

five banks are below this. But in private sector banks there are three banks are above

average. The difference between private and public banks average is also vast.

Private sector banks net NPA average is 0.71 and in public sector banks it is 0.41 as

percentage of total assets. As we know that net NPA shows actual burden of banks.

IndusInd bank has highest net NPA figure and HDFC Bank has lowest in comparison.

NET NPA of banks:-

banks ICICI Bank has the highest NPA in both sector in compare to other private sector

banks

43

SUMMARY OF FINDINGS :

The main causes for NPA is willful default, followed by improper selection of

borrowers and then lack of supervision and follow up.

We can observe that majority of respondents say that staff involvement in the

processing helps to reduce the NPAs and other respondent’s feel that proper

documentation helps in reducing NPA.

The Bank has converted NPA to good assets in few branches.

44

CONCLUSION:

The problem of non-performing assets has been a major issue for the banking industry. The

RBI which is the apex body for controlling the level of non-performing assets has been

giving guidelines and getting norms for the banks in order to control the incidents of defaults.

This study on management of non-performing assets with specific reference to J&K bank was

conducted, to find out the reasons for the incidence of non-performing assets and how public

sector banks managed it and its effect on performance of the bank.

The NPA of Jammu & Kashmir Bank Limited was studied and it was observed that

all branches of bank had NPA.

The study revealed that the J&K bank has been successful in controlling its level of

Non-performing assets as compared to the recent banking industry trends.

The causes for NPA in Jammu & Kashmir Bank Limited were analyzed, the extent to

which profitability has been reduced, was also analyzed.

45

46

BIBLOGRAPHY:

(A) TEXT BOOKS

1.) Financial Management by P.N. Reddy, H.R. Appannaiah and B.G.Satyaprasad.

2.) Financial Management by Prassana Chandra (Tata Mc Graw Hill Publications).

3.) Business Research Methods by O.R. Krishnaswami and B.G.

Satyaprasad.

4.) Law and Practice of Banking by H.R. Appannaiah, P.N. Reddy and S.Vijayendra.

5.) Greater Kashmir.

6.) Hand book of banking information by N S Tour.

(B) WEBSITES

1.) www.banking .com

2.) www.rbi.org

47