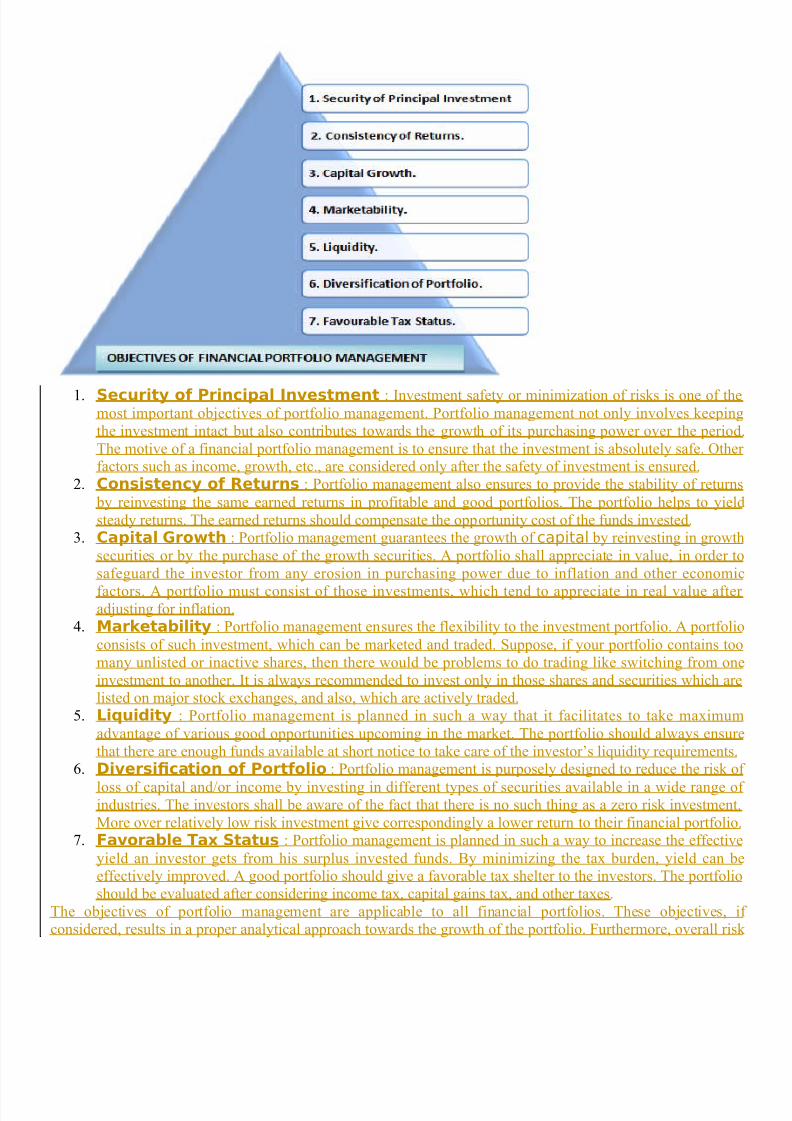

Notes Saim

57

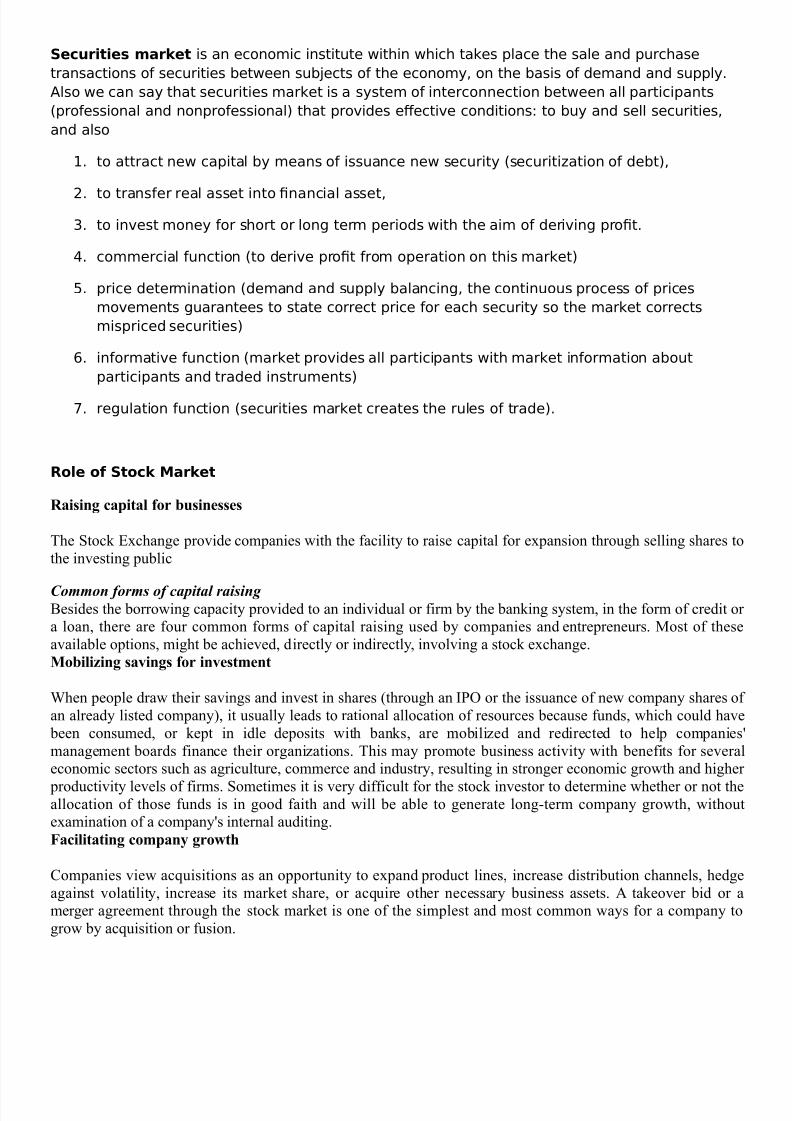

Unit-1 Introduction Indian Stock Markets ar e one of the oldest in Asia. Its history dates back to nearly 200 years ago. The earliest r ecords o f security dea lings in Ind ia are meag er and obscure. The East India Company as the dominant institution in those days and business in its loan securities used to be transacted toards the close of the eighteenth century. !y "#$0%s business on corporate stocks and shares in !ank and Cotton presses took place in !ombay. Though the trading list as broader in "#$&' there ere only half a do(en brokers recogni(ed by banks and merchants during "#)0 and "#*0. The "#*0%s itnessed a ra pid de+elopment o f commerc ial enterprise a nd bro kerage bu siness attracted many men into the ,eld and by "#-0 the number of brokers increased into -0. In "#-0-" the American Ci+il /ar broke out and cotton supply from nited States of Europe as stopped1 thus' the %Share Mania% in India begun. The number of brokers increased to about 200 to 2*0. oe+er' at the end of the American Ci+il /ar' in "#-*' a disastrous slump began 3for e4ample' !ank of !ombay Share hich had touched 5s 2#*0 could only be sold at 5s. #67. At the end of the American Ci+il /ar' the brokers ho thri+ed out of Ci+il /ar in "#6)' found a place in a street 3no appropriately called as 8alal Street7 here they ould con+eniently assemble and transact business. In "##6' they formally established in !ombay' the 9:ati+e Share and Stock !rokers% Association9 3hich is alternati+ely knon as 9 The Stock E4change 97. In "#&*' the Stock E4change ac;uired a premise in the same street and it as inaugurated in "#&&. Thus' the St ock E4chan ge at !ombay as consolidated. Structure of Capital Market in India Securities market / Stock Market

-

Upload

nishant-sharma -

Category

Documents

-

view

233 -

download

1

Transcript of Notes Saim

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 1/57

Unit-1

Introduction

Indian Stock Markets are one of the oldest in Asia. Its history dates back to nearly 200 years ago.

The earliest records of security dealings in India are meager and obscure. The East India

Company as the dominant institution in those days and business in its loan securities used to

be transacted toards the close of the eighteenth century.

!y "#$0%s business on corporate stocks and shares in !ank and Cotton presses took place in

!ombay. Though the trading list as broader in "#$&' there ere only half a do(en brokers

recogni(ed by banks and merchants during "#)0 and "#*0.

The "#*0%s itnessed a rapid de+elopment of commercial enterprise and brokerage business

attracted many men into the ,eld and by "#-0 the number of brokers increased into -0.

In "#-0-" the American Ci+il /ar broke out and cotton supply from nited States of Europe as

stopped1 thus' the %Share Mania% in India begun. The number of brokers increased to about 200 to

2*0. oe+er' at the end of the American Ci+il /ar' in "#-*' a disastrous slump began 3for

e4ample' !ank of !ombay Share hich had touched 5s 2#*0 could only be sold at 5s. #67.

At the end of the American Ci+il /ar' the brokers ho thri+ed out of Ci+il /ar in "#6)' found a

place in a street 3no appropriately called as 8alal Street7 here they ould con+eniently

assemble and transact business. In "##6' they formally established in !ombay' the 9:ati+e Share

and Stock !rokers% Association9 3hich is alternati+ely knon as 9 The Stock E4change 97. In

"#&*' the Stock E4change ac;uired a premise in the same street and it as inaugurated in "#&&.

Thus' the Stock E4change at !ombay as consolidated.

Structure of Capital Market in India

Securities market / Stock Market

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 2/57

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 3/57

Profit sharing

Both casual and professional stock investors, as large as institutional investors or as small as an ordinarymiddle(class family, through dividends and stock price increases that may result in capital gains, share in thewealth of profitable businesses. nprofitable and troubled businesses may result in capital losses forshareholders.Corporate governance

By having a wide and varied scope of owners, companies generally tend to improve management standards andefficiency to satisfy the demands of these shareholders, and the more stringent rules for public corporationsimposed by public stock exchanges and the government. )onse*uently, it is alleged that public companies!companies that are owned by shareholders who are members of the general public and trade shares on publicexchanges% tend to have better management records than privately held companies !those companies whereshares are not publicly traded, often owned by the company founders and-or their families and heirs, orotherwise by a small group of investors%.Creating investment opportunities for small investors

+s opposed to other businesses that re*uire huge capital outlay, investing in shares is open to both the large andsmall stock investors because a person buys the number of shares they can afford. Therefore the Stock

Exchange provides the opportunity for small investors to own shares of the same companies as large investors.

Levels of securities market

Primary market

The primary market s that part of the capital markets that deals with the issue of new securities. )ompanies,governments or public sector institutions can obtain funding through the sale of a new stock or bond issue. Thisis typically done through a syndicate of securities dealers. The process of selling new issues to investors is

called underwriting. "n the case of a new stock issue, this sale is a public offering. ealers earn a commissionthat is built into the price of the security offering, though it can be found in the prospectus. #rimary marketscreates long term instruments through which corporate entities borrow from capital market.

Features of primary markets are:

• This is the market for new long term e*uity capital. The primary market is the market where the

securities are sold for the first time. Therefore it is also called the new issue market !/"M%.• "n a primary issue, the securities are issued by the company directly to investors.

• The company receives the money and issues new security certificates to the investors.

• #rimary issues are used by companies for the purpose of setting up new business or for expanding or

moderni&ing the existing business.

• The primary market performs the crucial function of facilitating capital formation in the economy.• The new issue market does not include certain other sources of new long term external finance, such as

loans from financial institutions. Borrowers in the new issue market may be raising capital forconverting private capital into public capital0 this is known as 1going public.1

Primary market Primary Functions

1 !ri"ination- #eals $it% !ri"in of ne$ Issue &%e proposal is analy'ed in terms of

t%e nature of t%e security( t%e si'e of t%e issue( time of t%e issue and )oatation

met%od of t%e issue

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 4/57

* Under$ritin"- Contract +et$een Issuin" Company and Under$riter Under$riter

"ives assurance t%at( in case investor $ill not su,scri,e minimum num,er of s%are

t%en t%ey $ill su,scri,e &%ey also increases Investor condence

. #istri,ution-

• ?ublic ?lacement• ?ri+ate ?lacement•

5ight Issue• @=er of Sale

Primary market Secondary Functions1 &o promote a ne$ company* &o %elp to epand a ne$ company. &o %elp in diversication of t%e product0 &o c%anneli'e t%e savin"s of t%e investors &o %elp t%e companies to raise capital2 &o %elp t%e secondary market in %elpin" in tradin" of t%e securities

Participant in Primary Market

1 Mana"er to t%e issue-• Construction of the prospectus.• Appointment of the registrar• Appointment of the banker• Appointment of the underriter.• !udget for the Issue* Re"istrar to t%e issue-• 5ecei+e the share application from +arious collection centers.• 5ecommend the basis of allotment• 8ispatching the share certi,cates•

Share allocation• Appro+al of the prospectus.. Under$riter0 +anker to t%e issue• Collection of the application form and application money• Takes commission beside brokerage.• May be a ,nancial institution or a bank or a :!C. 3dvertisin" 3"encies-Prepare 3dvertisement and promote t%e companies Issue in various media2 &%e nancial Institution4enerally under$rite t%e issues of t%e companies

Primary market Secondary market Relationthe new issue Market and stock exchanges are inseparably connected2

3. The securities issued in the /ew "ssue Market are invariably listed on a recognised stock exchange,subse*uent to their issue. This is of immense utility to potential investors who feel assured that should theyreceive an allotment of new issues, they will subse*uently be able to dispose them of at any time. The facilities provided by the secondary markets, thus, widen the initial market for them.

4. Secondly, the stock exchanges exercise considerable control over the organisation of new issues. "n terms ofthe regulatory framework relating to dealings in securities, new issues, which seek stock exchange *uotation

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 5/57

have to comply with statutory rules as well as regulations framed by the stock exchanges with the ob5ect ofensuring fair dealings in them.

6. 7undamentally, the markets for new and old securities are, economically, an integral part of a single marketthe industrial securities market. Thus they are susceptible to common influence and act and react upon eachother. Broadly, new issues increase when stock values are rising and vice versa.

+lso, the *uantitative predominance of old securities in the market usually ensures that it is these which set the

tone of the market as a whole and govern the prices and acceptability of new issues.

Thus, we see that the capital market, with particular reference to company scraps, performs two distinctfunctions providing funds for trading in existing securities and funds for fresh issues of capital by thecompanies either through public issue or right issue or by private placement.

hile in many respects, the market mechanism for capital markets is the same as for commodities, there is afundamental difference that renders the former more complex, i.e. in the case of an ordinary commodity, it may be bought or sold several times, but it is used up in consumption after some time. "n the case of the capitalmarket nothing is consumed away.Every year there is new supply and so the cumulative total of funds dealt with goes on rising and the /ew "ssue

Market provides a common ground for facilitating this transfer process of funds from the suppliers !comprisinginvestors, individual, corporate and institutional% to the companies attempting to raise fresh capital.The exact amount available for investment in a particular company, however, depends on macro factors like rateof growth of the economy, total money supply, savings potential and the marginal propensity to save0 and microfactors like performance of a particular class of companies, facilities available for li*uidation of investment andthe individual preference of an investor, etc.

Primary market Secondary market #i5erences". In the ,rst place' :e Issue Market deals ith Bne securities' i.e. securities hich ere

not pre+iously a+ailable and are o=ered to the in+esting public for the ,rst time. Themarket' therefore' deri+es its name from the fact that it makes a+ailable a ne block ofsecurities for public subscription.

2. The stock market on the other hand' is a market for Bold securities i.e. those hich ha+ealready been issued and ha+e been granted stock e4change listing. These are purchasedand sold continuously among in+estors ithout in+ol+ement of the companies hosesecurities constitute the stockintrade e4cept in the strictly limited sense of ha+ing toregister the transfer of onership of the securities.

$. A related aspect of these to parts is the nature of their contribution to industrial,nancing. The :e Issue Market pro+ides the issuing company ith additional funds forstarting a ne enterprise or for either e4pansion or di+ersi,cation of an e4isting one' andthus its contribution to company ,nancing is direct. The role of the stock e4change +isa+is supply of capital is indirect.

). Apart from this' the to parts of the market di=er organisationally' e.g. the stocke4changes ha+e physical e4istence and are located in particular geographical areas. The:e Issue Market en<oys neither any tangible form nor any administrati+e organisationalsetup' and nor is sub<ect to any centralised control and administration for the e4ecution ofits business it is recognised by the ser+ices that it renders to the lenders and borroers ofcapital funds at the time of any particular operation.

Investor Protection in Primary market1 Provision of all t%e relevant Information* Provision of 3ccurate information$. &ransparent allotment procedure $it%out any ,ias

In order to o,serve a,ove t%e follo$in" are done

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 6/57

". ?ro<ect Appraisal2. nderriting$. 8isclosure of the ?rospectus). Clearance by the stock E4change*. Signing by the board of directors-. 5edressal of the In+estors grie+ances6. SE!Is 5ole

Secondary MarketA stock ec%an"e is a form of e4change hich pro+ides ser+ices for stock brokers and tradersto trade stocks' bonds' and other securities. Stock e4changes also pro+ide facilities for issue andredemption of securities and other ,nancial instruments' and capital e+ents including thepayment of income and di+idends. Securities traded on a stock e4change include shares issuedby companies' unit trusts' deri+ati+es' pooled in+estment products and bonds.

To be able to trade a security on a certain stock e4change' it must be listed there. sually' thereis a central location at least for record keeping' but trade is increasingly less linked to such aphysical place' as modern markets are electronic netorks' hich gi+es them ad+antages ofincreased speed and reduced cost of transactions. Trade on an e4change is by members only.

The initial o=ering of stocks and bonds to in+estors is by de,nition done in the primary marketand subse;uent trading is done in the secondary market. A stock e4change is often the mostimportant component of a stock market. Supply and demand in stock markets are dri+en by+arious factors that' as in all free markets' a=ect the price of stocks 3see stock +aluation.

There is usually no compulsion to issue stock +ia the stock e4change itself' nor must stock besubse;uently traded on the e4change. Such trading is said to be of exchange or o+erthecounter. This is the usual ay that deri+ati+es and bonds are traded. Increasingly' stocke4changes are part of a global market for securities.

Role and Functions of Secondary MarketRole

• Creatin" investment opportunities for small investors• Prot s%arin"• Facilitatin" company "ro$t%• Mo,ili'in" savin"s for investment• Common forms of capital raising• Raisin" capital for ,usinesses

Functions• Maintain 3ctive &radin"• Fiation of Price• 6nsure safe and Fair trade Practices• 3ids in Financin" t%e Industry• #issemination of t%e information•

Performance Inducer

Re"ulatory Mec%anism in Secondary Market&%ree tier structure

". Ministry of ,nance2. SE!I$. Do+erning !oard

Ministry of ,nance". Super+isory function o+er SE!I2. Appellate function against SE!I$. icensing of dealers

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 7/57

). 5ecognition to stock e4change*. Appointment of the board of go+ernors

SE!I". 5egulation of !usiness2. In+estor ?rotection$. ?re+ent raudulent trade practices). Takeo+er and Amalgamation*. @ther poers

Do+erning !oard". Consist of "$ members.2. - members from ithin$. $ public representati+es nominated by the board of go+ernors). :ot more than$ members appointed by the central go+ernment*. :ot more than three by SE!I.-. E4ecuti+e directors by the stock e4change.6. @ne third of the elected members are retires at ADM. They can be re elected.#. There are also ?residents and Fice president elected by the go+erning board.

Functionin" of Stock Market Trading in Indian stock e4changes are limited to listed securities of public limited companies. They are broadly di+ided into to categories' namely' speci,ed securities 3forard list7 and nonspeci,ed securities 3cash list7. E;uity shares of di+idend paying' grothoriented companies itha paidup capital of at least 5s.*0 million and a market capitali(ation of at least 5s."00 millionand ha+ing more than 20'000 shareholders are' normally' put in the speci,ed group and thebalance in nonspeci,ed group.

To types of transactions can be carried out on the Indian stock e4changes> 3a7 spot deli+erytransactions 9for deli+ery and payment ithin the time or on the date stipulated hen enteringinto the contract hich shall not be more than ") days folloing the date of the contract9 > and3b7 forard transactions 9deli+ery and payment can be e4tended by further period of ") dayseach so that the o+erall period does not e4ceed &0 days from the date of the contract9. Thelatter is permitted only in the case of speci,ed shares. The brokers ho carry o+er the outstandings pay carry o+er charges hich are usually determined by the rates of interestpre+ailing. A member broker in an Indian stock e4change can act as an agent' buy and sell securities for hisclients on a commission basis and also can act as a trader or dealer as a principal' buy and sellsecurities on his on account and risk' in contrast ith the practice pre+ailing on :e Gork andondon Stock E4changes' here a member can act as a <obber or a broker only.

The nature of trading on Indian Stock E4changes are that of age old con+entional style of facetoface trading ith bids and o=ers being made by open outcry. oe+er' there is a great amount ofe=ort to moderni(e the Indian stock e4changes in the +ery recent times.

!ver &%e Counter 6c%an"e of India 7!&C6I8 The traditional trading mechanism pre+ailed in the Indian stock markets ga+e ay to manyfunctional ineHciencies' such as' absence of li;uidity' lack of transparency' unduly longsettlement periods' hich a=ected the small in+estors to a great e4tent. To pro+ide impro+edser+ices to in+estors' the country%s ,rst electronic stock e4change @TCEI as created in "&&2by country%s premier ,nancial institutions nit Trust of India' Industrial Credit and In+estmentCorporation of India' Industrial 8e+elopment !ank of India' S!I Capital Markets' Industrial inanceCorporation of India' Deneral Insurance Corporation and its subsidiaries and Canara !ankinancial Ser+ices.

@TC has a uni;ue feature of trading compared to other traditional e4changes. That is' certi,catesof listed securities and initiated debentures are not traded at @TC. The original certi,cate ill be

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 8/57

safely ith the custodian. !ut' a counter receipt is generated out at the counter hichsubstitutes the share certi,cate and is used for all transactions.In the case of permitted securities' the system is similar to a traditional stock e4change. Thedi=erence is that the deli+ery and payment procedure ill be completed ithin ") days.Compared to the traditional E4changes' @TC E4change netork has the folloing ad+antages>

• @TCEI has idely dispersed trading mechanism across the country hich pro+ides greaterli;uidity and lesser risk of intermediary charges.

• Dreater transparency and accuracy of prices is obtained due to the screenbased scriplesstrading.

• Since the e4act price of the transaction is shon on the computer screen' the in+estorgets to kno the e4act price at hich she is trading.

• aster settlement and transfer process compared to other e4changes.• In the case of an @TC issue 3ne issue7' the allotment procedure is completed in a month

and trading commences after a month of the issue closure' hereas it takes a longerperiod for the same ith respect to other e4changes.

+enets and limitations of Stock Market+enets

". Creating a market for the company%s shares2. Enhancing the status and ,nancial standing of the company$. Increasing public aareness and public interest in the company and its products). ?ro+iding the company ith an opportunity to implement share option schemes for their

employees*. Accessing to additional fund raising in the future by means of ne issues of shares or

other securities-. acilitating ac;uisition opportunities by use of the company%s shares6. @=ering e4isting shareholders a ready means of reali(ing their in+estments

Limitations• Increasing accountability to public shareholders• :eed to maintain di+idend and pro,t groth trends• Chances of possible takeo+er and merger.•

:eed to obser+e and adhere strictly to the rules and regulations by go+erning bodies• Increasing costs in complying ith higher le+el of reporting re;uirements• Su=ering a loss of pri+acy as a result of media interest

&%e Security and 6c%an"e +oard of India• It as oHcially act by The Do+ernment of India in the year "&## and gi+en statutory

poers in "&&2 ith SE!I Act "&&2 being passed by the Indian ?arliament. SE!I has it%sead;uarter at the business district of !andra Jurla Comple4 in Mumbai' and has:orthern' Eastern' Southern and /estern 5egional @Hces in :e 8elhi' Jolkata' Chennaiand Ahmedabad respecti+ely.

• Controller of Capital Issues as the regulatory authority before SE!I came into e4istence1it deri+ed authority from the Capital Issues 3Control7 Act' "&)6.

• Initially SE!I as a non statutory body ithout any statutory poer. oe+er in the year of

"&&*' the SE!I as gi+en additional statutory poer by the Do+ernment of India throughan amendment to the Securities and E4change !oard of India Act "&&2. In April' "&&# theSE!I as constituted as the regulator of capital markets in India under a resolution of theDo+ernment of India.

• The SE!I is managed by its members' hich consists of folloing> a7 The chairman ho is

nominated by nion Do+ernment of India. b7 To members' i.e. @Hcers from nioninance Ministry. c7 @ne member from The 5eser+e !ank of India. d7 The remaining *members are nominated by nion Do+ernment of India' out of them at least $ shall beholetime members.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 9/57

!,9ectives of Security and 6c%an"e +oard of India• To promote and de+elop stock market• To protect the interest of the in+estors in stock market.• To regulate the stock market

Functions of Security and 6c%an"e +oard of IndiaIn order to pursue the ob<ecti+es SE!I has the folloing functions>

". 5egulate the orking of the stock market.2. 5egistration and licensing of the participants.$. 5egistration and regulation of the collecti+e in+estment schemes.). ?romotion of self regulatory organi(ation*. ?re+enting unfair trade practices.-. ?romoting in+estor education.6. Training of the intermediaries.#. ?re+enting Insider trading' circular trading.&. 5egulating Mergers' takeo+ers' Amalgamations etc."0.ndertaking Inspections' Calling for the information' audits of the stocks' sei(ure of the

accounts.&%e Security and 6c%an"e +oard of India !r"ani'ation

• ?rimary 8epartment or ?rimary market 5egulation• Issue Management and Intermediary 8epartment or Intermediaries regulation• Secondary Market 8epartment or secondary market regulation• Institutional 8epartment or the regulation of Merger' takeo+ers' Amalgamations ets.• In+estigation 8epartment or In+estigation purpose.• Ad+isory Committee or ad+ice regarding regulation of primary and secondary market.

S6+I:s Role in Primary Market". Entry :orms• $ year of 8i+idend ?ayment• or e4isting company should full,l norms if the issue is ,+e time s the pre issue.• If a company does not ha+e a track record' it could go of public issue but its pro<ect must

be appraised by a public ,nancial institution.• or a public issue a company must ha+e * promotes of 5s " lac of the net capital o=er

made to public.2. ?romoter Contribution

• :ot less than 20K of the issued capital.• Entire promoter contribution should be recei+ed before the issue.• The promoter issue should not be more than 20K and it ill be locked for * years.

$. 8isclosure). Allocation of shares*. Market intermediaries

S6+I:s Role in Secondary Market1 4overnin" +oard* Infrastructure

. Settlement and clearin"0 Price sta,ili'ation #elistin"

Unit-*Concept of Risk 5isk is the potential of loss 3an undesirable outcome' hoe+er not necessarily so7resulting from a gi+en action' acti+ity andor inaction. The notion implies that achoice ha+ing an inLuence on the outcome sometimes e4ists 3or e4isted7.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 10/57

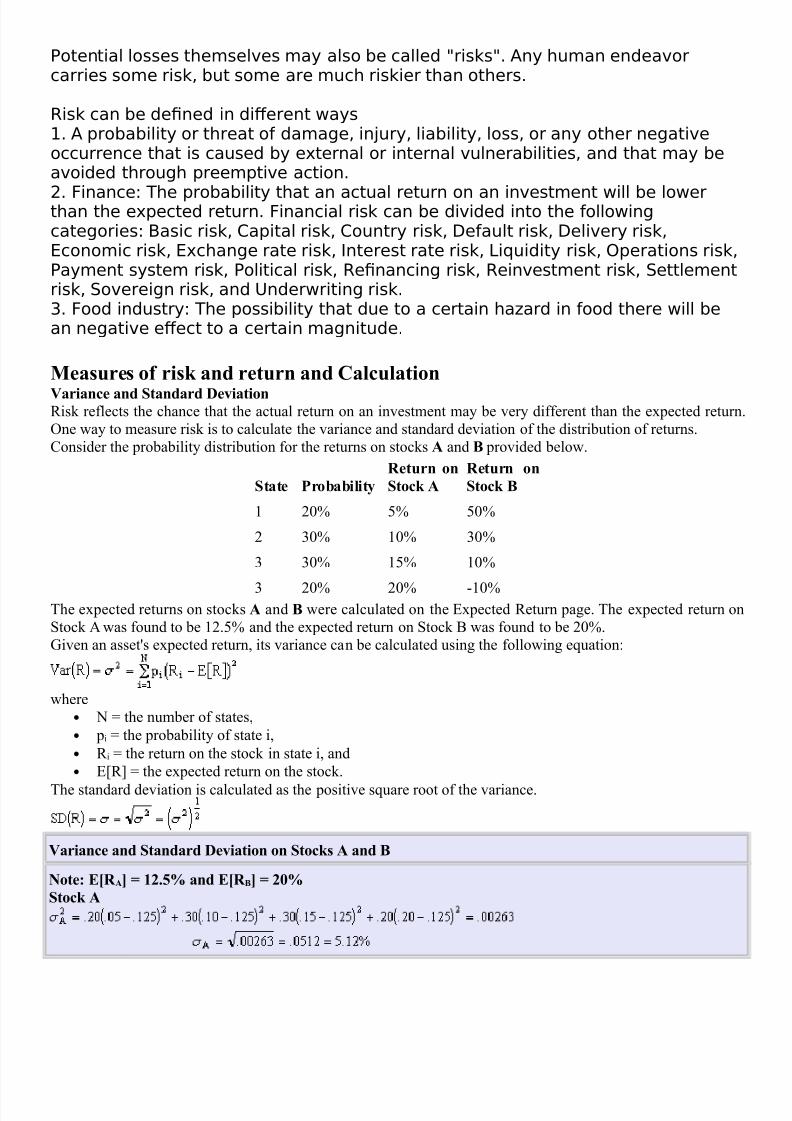

?otential losses themsel+es may also be called 9risks9. Any human endea+orcarries some risk' but some are much riskier than others. 5isk can be de,ned in di=erent ays". A probability or threat of damage' in<ury' liability' loss' or any other negati+eoccurrence that is caused by e4ternal or internal +ulnerabilities' and that may bea+oided through preempti+e action.

2. inance> The probability that an actual return on an in+estment ill be loerthan the e4pected return. inancial risk can be di+ided into the folloingcategories> !asic risk' Capital risk' Country risk' 8efault risk' 8eli+ery risk'Economic risk' E4change rate risk' Interest rate risk' i;uidity risk' @perations risk'?ayment system risk' ?olitical risk' 5e,nancing risk' 5ein+estment risk' Settlementrisk' So+ereign risk' and nderriting risk.$. ood industry> The possibility that due to a certain ha(ard in food there ill bean negati+e e=ect to a certain magnitude.

Measures of risk and return and Calculation

ariance and !tandard "eviation8isk reflects the chance that the actual return on an investment may be very different than the expected return$ne way to measure risk is to calculate the variance and standard deviation of the distribution of returns.)onsider the probability distribution for the returns on stocks # and $ provided below.

!tate Probability

Return on

!tock #

Return on

!tock $

3 49: ;: ;9:

4 69: 39: 69:

6 69: 3;: 39:

6 49: 49: (39:The expected returns on stocks # and $ were calculated on the Expected 8eturn page. The expected return onStock + was found to be 34.;: and the expected return on Stock B was found to be 49:.<iven an asset's expected return, its variance can be calculated using the following e*uation2

where• / = the number of states,

• pi = the probability of state i,

• 8 i = the return on the stock in state i, and• E>8? = the expected return on the stock.

The standard deviation is calculated as the positive s*uare root of the variance.

ariance and !tandard "eviation on !tocks # and $

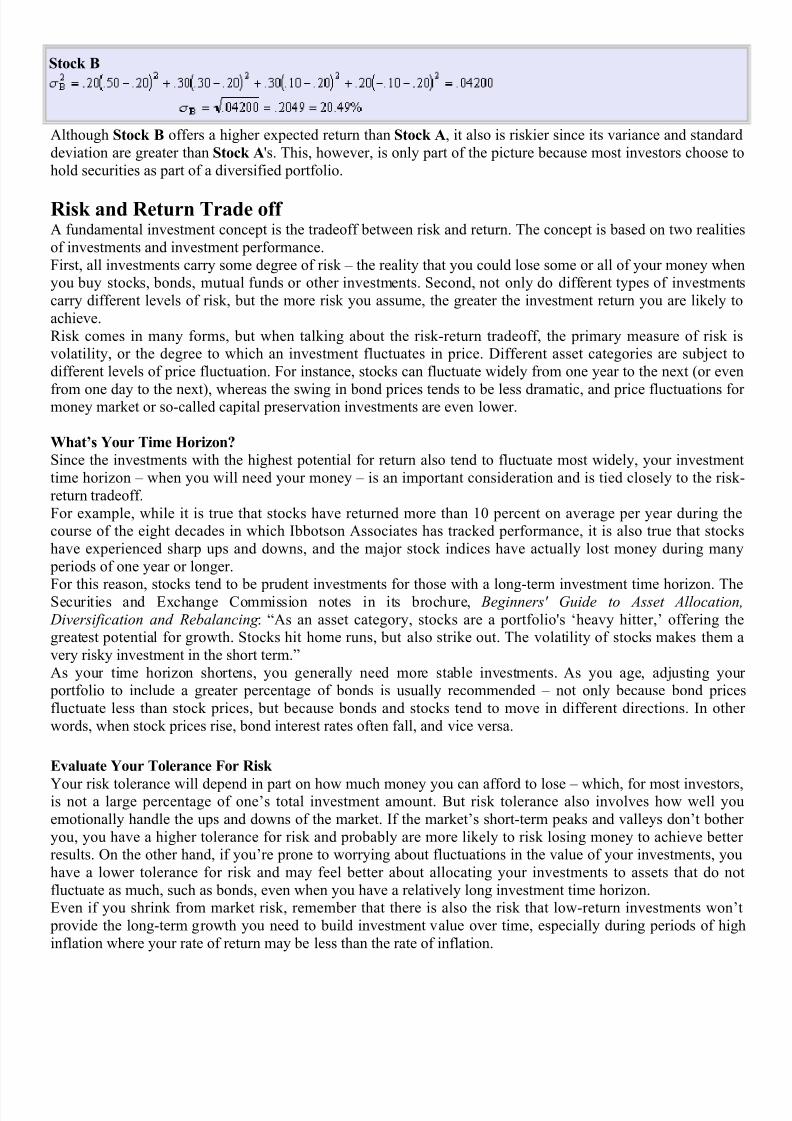

%ote: &'R #( ) *+,-. and &'R $( ) +/. !tock #

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 11/57

!tock $

+lthough !tock $ offers a higher expected return than !tock #, it also is riskier since its variance and standarddeviation are greater than !tock #'s. This, however, is only part of the picture because most investors choose tohold securities as part of a diversified portfolio.

Risk and Return Trade off + fundamental investment concept is the tradeoff between risk and return. The concept is based on two realitiesof investments and investment performance.7irst, all investments carry some degree of risk @ the reality that you could lose some or all of your money whenyou buy stocks, bonds, mutual funds or other investments. Second, not only do different types of investmentscarry different levels of risk, but the more risk you assume, the greater the investment return you are likely toachieve.8isk comes in many forms, but when talking about the risk(return tradeoff, the primary measure of risk isvolatility, or the degree to which an investment fluctuates in price. ifferent asset categories are sub5ect todifferent levels of price fluctuation. 7or instance, stocks can fluctuate widely from one year to the next !or even

from one day to the next%, whereas the swing in bond prices tends to be less dramatic, and price fluctuations formoney market or so(called capital preservation investments are even lower.

0hat1s 2our Time 3orizon4

Since the investments with the highest potential for return also tend to fluctuate most widely, your investmenttime hori&on @ when you will need your money @ is an important consideration and is tied closely to the risk(return tradeoff.7or example, while it is true that stocks have returned more than 39 percent on average per year during thecourse of the eight decades in which "bbotson +ssociates has tracked performance, it is also true that stockshave experienced sharp ups and downs, and the ma5or stock indices have actually lost money during many periods of one year or longer.

7or this reason, stocks tend to be prudent investments for those with a long(term investment time hori&on. TheSecurities and Exchange )ommission notes in its brochure, Beginners' Guide to Asset Allocation,

Diversification and Rebalancing 2 A+s an asset category, stocks are a portfolio's heavy hitter,C offering thegreatest potential for growth. Stocks hit home runs, but also strike out. The volatility of stocks makes them avery risky investment in the short term.D+s your time hori&on shortens, you generally need more stable investments. +s you age, ad5usting your portfolio to include a greater percentage of bonds is usually recommended @ not only because bond pricesfluctuate less than stock prices, but because bonds and stocks tend to move in different directions. "n otherwords, when stock prices rise, bond interest rates often fall, and vice versa.

&valuate 2our Tolerance For Risk

our risk tolerance will depend in part on how much money you can afford to lose @ which, for most investors,is not a large percentage of oneCs total investment amount. But risk tolerance also involves how well youemotionally handle the ups and downs of the market. "f the marketCs short(term peaks and valleys donCt botheryou, you have a higher tolerance for risk and probably are more likely to risk losing money to achieve betterresults. $n the other hand, if youCre prone to worrying about fluctuations in the value of your investments, youhave a lower tolerance for risk and may feel better about allocating your investments to assets that do notfluctuate as much, such as bonds, even when you have a relatively long investment time hori&on.Even if you shrink from market risk, remember that there is also the risk that low(return investments wonCt provide the long(term growth you need to build investment value over time, especially during periods of highinflation where your rate of return may be less than the rate of inflation.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 12/57

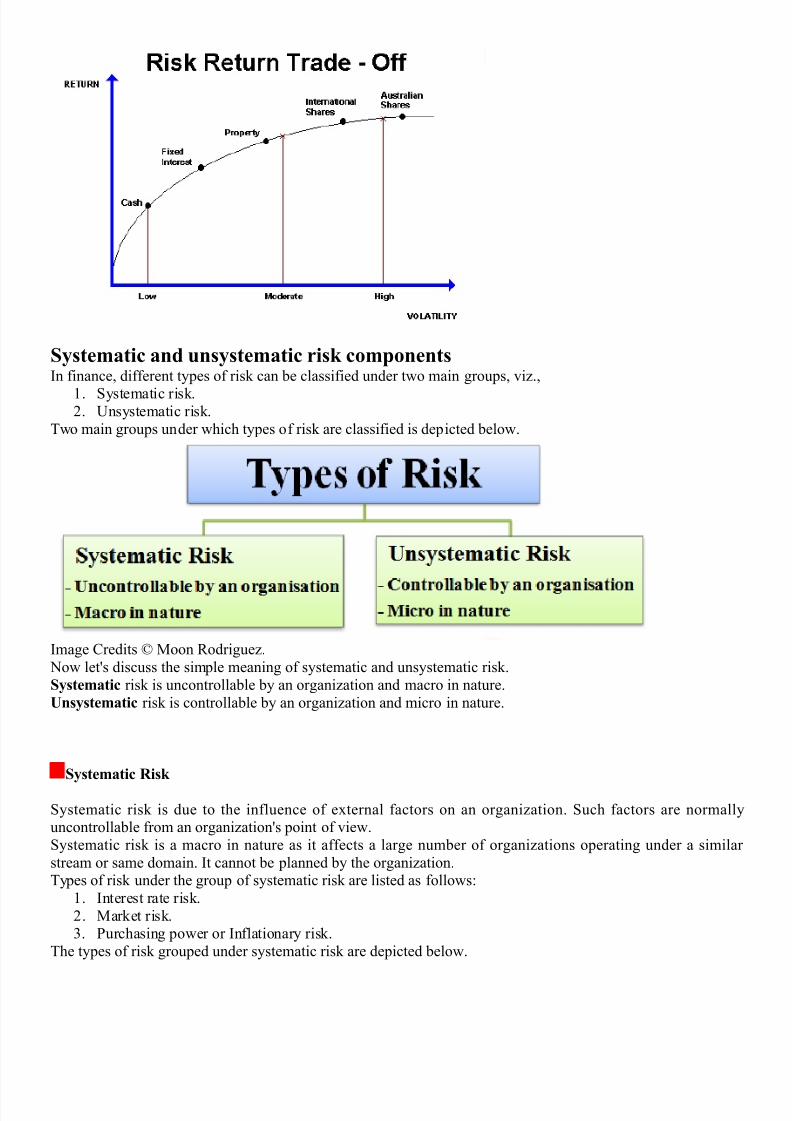

!ystematic and unsystematic risk components"n finance, different types of risk can be classified under two main groups, vi&.,

3. Systematic risk.4. nsystematic risk.

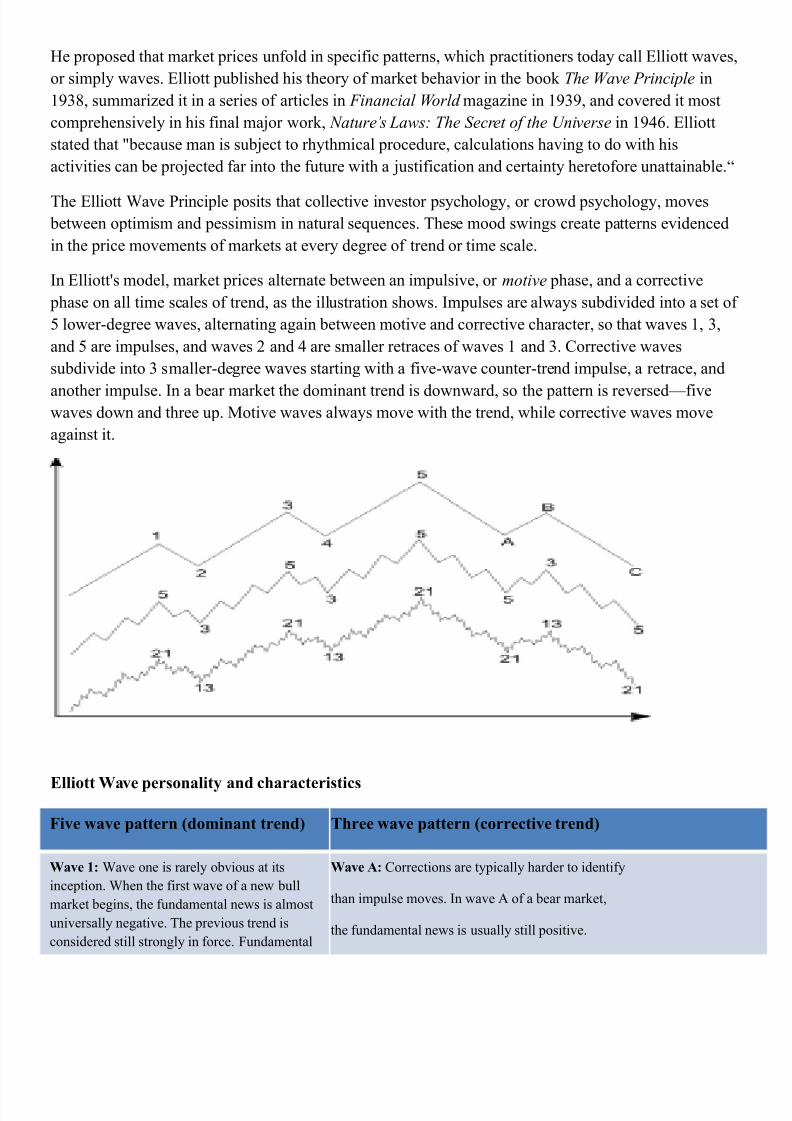

Two main groups under which types of risk are classified is depicted below.

"mage )redits F Moon 8odrigue&. /ow let's discuss the simple meaning of systematic and unsystematic risk.!ystematic risk is uncontrollable by an organi&ation and macro in nature.5nsystematic risk is controllable by an organi&ation and micro in nature.

!ystematic Risk

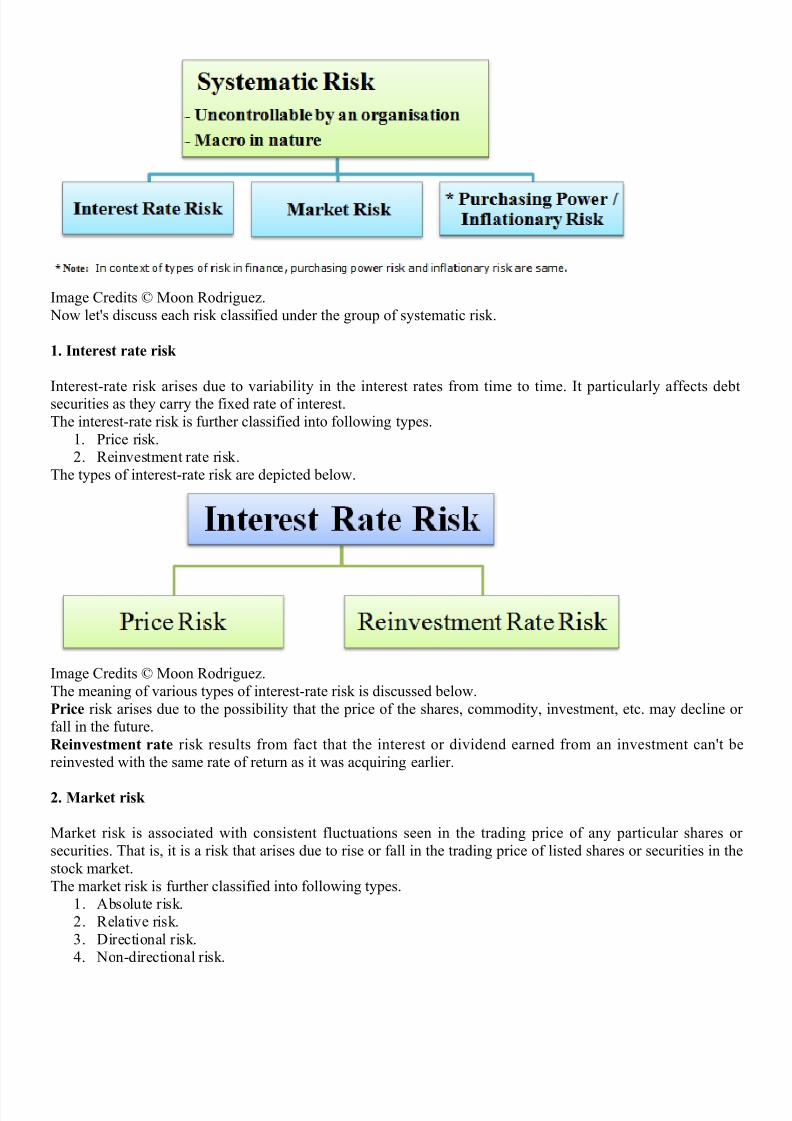

Systematic risk is due to the influence of external factors on an organi&ation. Such factors are normallyuncontrollable from an organi&ation's point of view.Systematic risk is a macro in nature as it affects a large number of organi&ations operating under a similarstream or same domain. "t cannot be planned by the organi&ation.Types of risk under the group of systematic risk are listed as follows2

3. "nterest rate risk.4. Market risk.6. #urchasing power or "nflationary risk.

The types of risk grouped under systematic risk are depicted below.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 13/57

"mage )redits F Moon 8odrigue&. /ow let's discuss each risk classified under the group of systematic risk.

*, 6nterest rate risk

"nterest(rate risk arises due to variability in the interest rates from time to time. "t particularly affects debtsecurities as they carry the fixed rate of interest.The interest(rate risk is further classified into following types.

3. #rice risk.4. 8einvestment rate risk.

The types of interest(rate risk are depicted below.

"mage )redits F Moon 8odrigue&.The meaning of various types of interest(rate risk is discussed below.Price risk arises due to the possibility that the price of the shares, commodity, investment, etc. may decline orfall in the future.Reinvestment rate risk results from fact that the interest or dividend earned from an investment can't bereinvested with the same rate of return as it was ac*uiring earlier.

+, Market risk

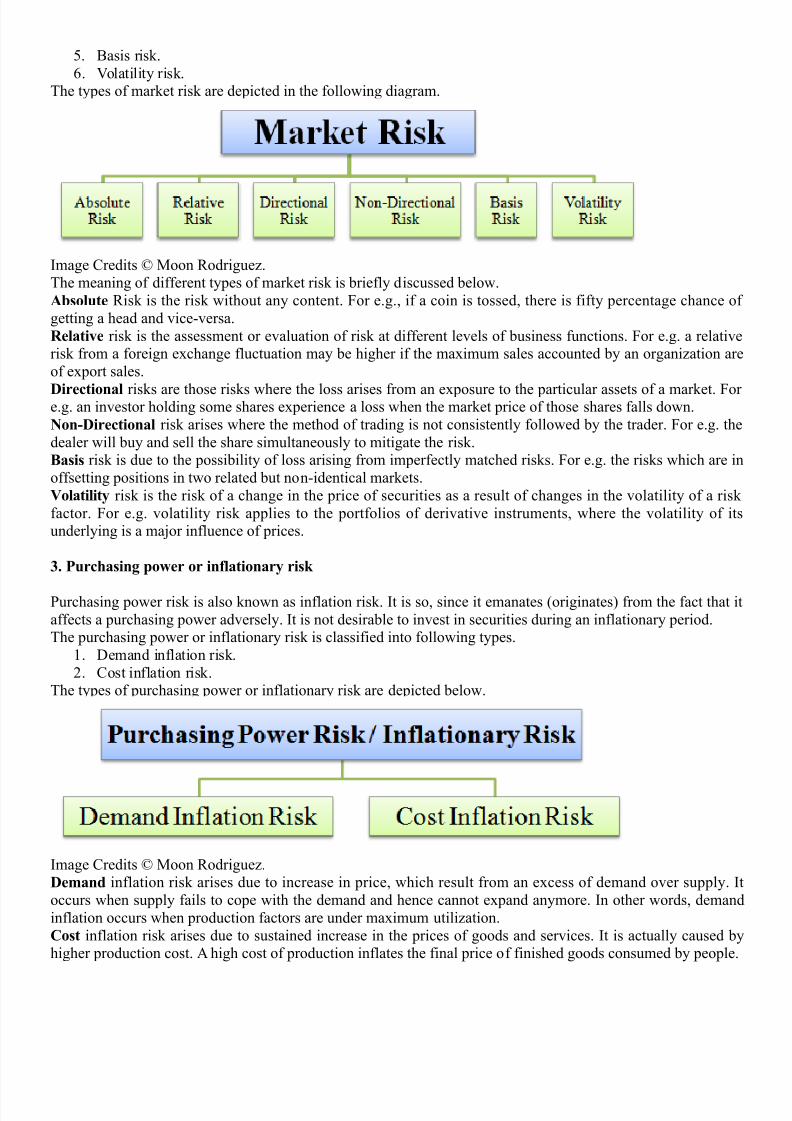

Market risk is associated with consistent fluctuations seen in the trading price of any particular shares orsecurities. That is, it is a risk that arises due to rise or fall in the trading price of listed shares or securities in thestock market.The market risk is further classified into following types.

3. +bsolute risk.4. 8elative risk.6. irectional risk.G. /on(directional risk.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 14/57

;. Basis risk.H. Iolatility risk.

The types of market risk are depicted in the following diagram.

"mage )redits F Moon 8odrigue&.The meaning of different types of market risk is briefly discussed below.#bsolute 8isk is the risk without any content. 7or e.g., if a coin is tossed, there is fifty percentage chance ofgetting a head and vice(versa.Relative risk is the assessment or evaluation of risk at different levels of business functions. 7or e.g. a relativerisk from a foreign exchange fluctuation may be higher if the maximum sales accounted by an organi&ation areof export sales.

"irectional risks are those risks where the loss arises from an exposure to the particular assets of a market. 7ore.g. an investor holding some shares experience a loss when the market price of those shares falls down.%on7"irectional risk arises where the method of trading is not consistently followed by the trader. 7or e.g. thedealer will buy and sell the share simultaneously to mitigate the risk.$asis risk is due to the possibility of loss arising from imperfectly matched risks. 7or e.g. the risks which are inoffsetting positions in two related but non(identical markets.olatility risk is the risk of a change in the price of securities as a result of changes in the volatility of a riskfactor. 7or e.g. volatility risk applies to the portfolios of derivative instruments, where the volatility of itsunderlying is a ma5or influence of prices.

8, Purchasing power or inflationary risk

#urchasing power risk is also known as inflation risk. "t is so, since it emanates !originates% from the fact that itaffects a purchasing power adversely. "t is not desirable to invest in securities during an inflationary period.The purchasing power or inflationary risk is classified into following types.

3. emand inflation risk.4. )ost inflation risk.

The types of purchasing power or inflationary risk are depicted below.

"mage )redits F Moon 8odrigue&."emand inflation risk arises due to increase in price, which result from an excess of demand over supply. "toccurs when supply fails to cope with the demand and hence cannot expand anymore. "n other words, demandinflation occurs when production factors are under maximum utili&ation.Cost inflation risk arises due to sustained increase in the prices of goods and services. "t is actually caused byhigher production cost. + high cost of production inflates the final price of finished goods consumed by people.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 15/57

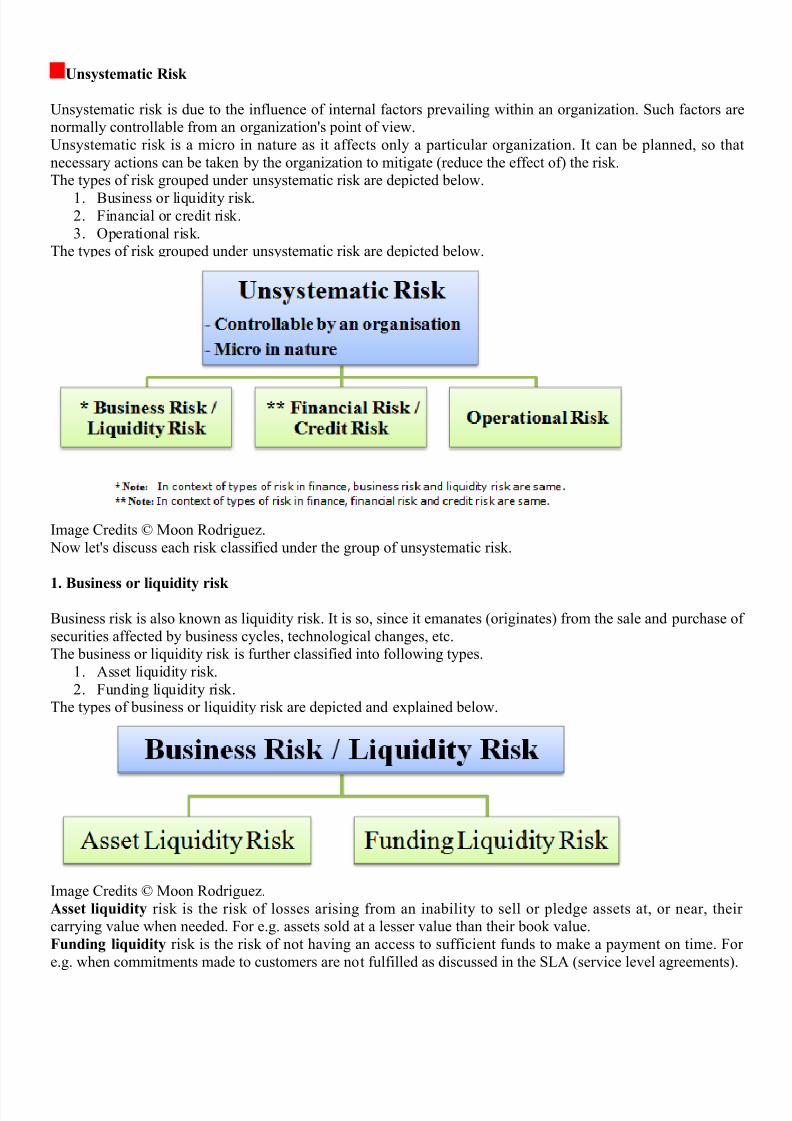

5nsystematic Risk

nsystematic risk is due to the influence of internal factors prevailing within an organi&ation. Such factors arenormally controllable from an organi&ation's point of view.nsystematic risk is a micro in nature as it affects only a particular organi&ation. "t can be planned, so thatnecessary actions can be taken by the organi&ation to mitigate !reduce the effect of% the risk.The types of risk grouped under unsystematic risk are depicted below.

3. Business or li*uidity risk.4. 7inancial or credit risk.6. $perational risk.

The types of risk grouped under unsystematic risk are depicted below.

"mage )redits F Moon 8odrigue&. /ow let's discuss each risk classified under the group of unsystematic risk.

*, $usiness or li9uidity risk

Business risk is also known as li*uidity risk. "t is so, since it emanates !originates% from the sale and purchase ofsecurities affected by business cycles, technological changes, etc.The business or li*uidity risk is further classified into following types.

3. +sset li*uidity risk.4. 7unding li*uidity risk.

The types of business or li*uidity risk are depicted and explained below.

"mage )redits F Moon 8odrigue&.#sset li9uidity risk is the risk of losses arising from an inability to sell or pledge assets at, or near, theircarrying value when needed. 7or e.g. assets sold at a lesser value than their book value.Funding li9uidity risk is the risk of not having an access to sufficient funds to make a payment on time. 7ore.g. when commitments made to customers are not fulfilled as discussed in the SJ+ !service level agreements%.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 16/57

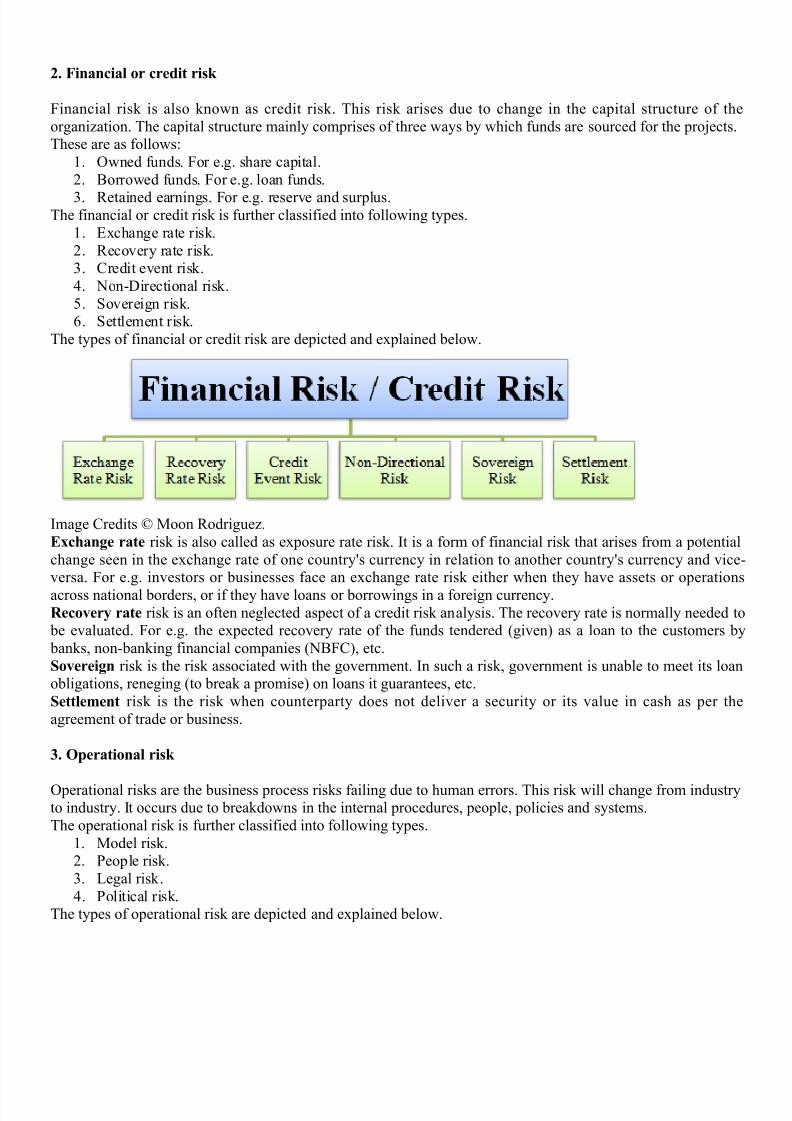

+, Financial or credit risk

7inancial risk is also known as credit risk. This risk arises due to change in the capital structure of theorgani&ation. The capital structure mainly comprises of three ways by which funds are sourced for the pro5ects.These are as follows2

3. $wned funds. 7or e.g. share capital.4. Borrowed funds. 7or e.g. loan funds.

6. 8etained earnings. 7or e.g. reserve and surplus.The financial or credit risk is further classified into following types.

3. Exchange rate risk.4. 8ecovery rate risk.6. )redit event risk.G. /on(irectional risk.;. Sovereign risk.H. Settlement risk.

The types of financial or credit risk are depicted and explained below.

"mage )redits F Moon 8odrigue&.&change rate risk is also called as exposure rate risk. "t is a form of financial risk that arises from a potentialchange seen in the exchange rate of one country's currency in relation to another country's currency and vice(versa. 7or e.g. investors or businesses face an exchange rate risk either when they have assets or operationsacross national borders, or if they have loans or borrowings in a foreign currency.Recovery rate risk is an often neglected aspect of a credit risk analysis. The recovery rate is normally needed to be evaluated. 7or e.g. the expected recovery rate of the funds tendered !given% as a loan to the customers by banks, non(banking financial companies !/B7)%, etc.!overeign risk is the risk associated with the government. "n such a risk, government is unable to meet its loanobligations, reneging !to break a promise% on loans it guarantees, etc.!ettlement risk is the risk when counterparty does not deliver a security or its value in cash as per theagreement of trade or business.

8, ;perational risk

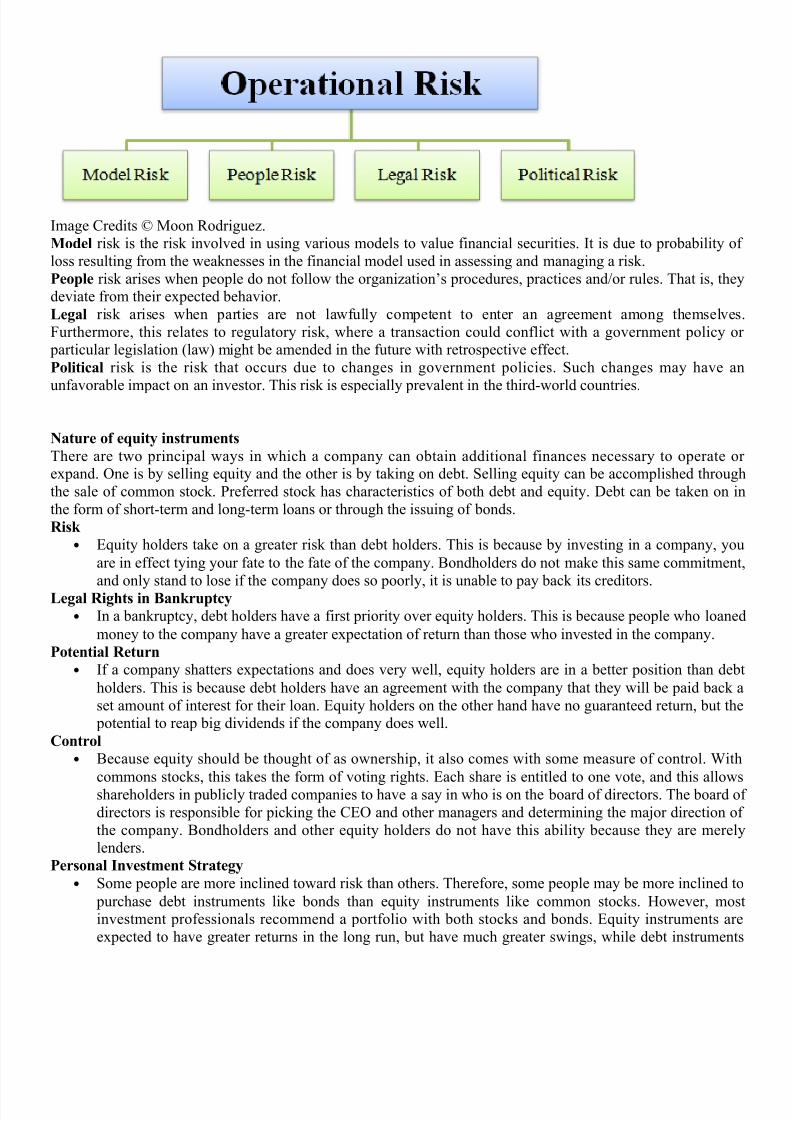

$perational risks are the business process risks failing due to human errors. This risk will change from industryto industry. "t occurs due to breakdowns in the internal procedures, people, policies and systems.The operational risk is further classified into following types.

3. Model risk.4. #eople risk.6. Jegal risk.G. #olitical risk.

The types of operational risk are depicted and explained below.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 17/57

"mage )redits F Moon 8odrigue&.Model risk is the risk involved in using various models to value financial securities. "t is due to probability ofloss resulting from the weaknesses in the financial model used in assessing and managing a risk.People risk arises when people do not follow the organi&ationCs procedures, practices and-or rules. That is, theydeviate from their expected behavior.<egal risk arises when parties are not lawfully competent to enter an agreement among themselves7urthermore, this relates to regulatory risk, where a transaction could conflict with a government policy or particular legislation !law% might be amended in the future with retrospective effect.Political risk is the risk that occurs due to changes in government policies. Such changes may have an

unfavorable impact on an investor. This risk is especially prevalent in the third(world countries.

%ature of e9uity instruments

There are two principal ways in which a company can obtain additional finances necessary to operate orexpand. $ne is by selling e*uity and the other is by taking on debt. Selling e*uity can be accomplished throughthe sale of common stock. #referred stock has characteristics of both debt and e*uity. ebt can be taken on inthe form of short(term and long(term loans or through the issuing of bonds.Risk

• E*uity holders take on a greater risk than debt holders. This is because by investing in a company, you

are in effect tying your fate to the fate of the company. Bondholders do not make this same commitment

and only stand to lose if the company does so poorly, it is unable to pay back its creditors.<egal Rights in $ankruptcy

• "n a bankruptcy, debt holders have a first priority over e*uity holders. This is because people who loaned

money to the company have a greater expectation of return than those who invested in the company.Potential Return

• "f a company shatters expectations and does very well, e*uity holders are in a better position than debt

holders. This is because debt holders have an agreement with the company that they will be paid back aset amount of interest for their loan. E*uity holders on the other hand have no guaranteed return, but the potential to reap big dividends if the company does well.

Control

• Because e*uity should be thought of as ownership, it also comes with some measure of control. ith

commons stocks, this takes the form of voting rights. Each share is entitled to one vote, and this allowsshareholders in publicly traded companies to have a say in who is on the board of directors. The board ofdirectors is responsible for picking the )E$ and other managers and determining the ma5or direction ofthe company. Bondholders and other e*uity holders do not have this ability because they are merelylenders.

Personal 6nvestment !trategy

• Some people are more inclined toward risk than others. Therefore, some people may be more inclined to

purchase debt instruments like bonds than e*uity instruments like common stocks. Kowever, mostinvestment professionals recommend a portfolio with both stocks and bonds. E*uity instruments areexpected to have greater returns in the long run, but have much greater swings, while debt instruments

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 18/57

produce lower returns with fewer swings. "t is recommended that as you get older, you put more of yourinvestments into debt and less into e*uity.

&9uity aluation Models!tock aluation MethodsStocks have two types of valuations. $ne is a value created using some type of cash flow, sales orfundamental earnings analysis. The other value is dictated by how much an investor is willing to pay for

a particular share of stock and by how much other investors are willing to sell a stock for !in otherwords, by supply and demand%. Both of these values change over time as investors change the way theyanaly&e stocks and as they become more or less confident in the future of stocks.

The fundamental valuation is the valuation that people use to 5ustify stock prices. The most commonexample of this type of valuation methodology is #-E ratio, which stands for #rice to Earnings 8atio.This form of valuation is based on historic ratios and statistics and aims to assign value to a stock basedon measurable attributes. This form of valuation is typically what drives long(term stock prices.The other way stocks are valued is based on supply and demand. The more people that want to buy thestock, the higher its price will be. +nd conversely, the more people that want to sell the stock, the lowerthe price will be. This form of valuation is very hard to understand or predict, and it often drives the

short(term stock market trends.

There are many different ways to value stocks. The key is to take each approach into account whileformulating an overall opinion of the stock. "f the valuation of a company is lower or higher than othersimilar stocks, then the next step would be to determine the reasons.

&arnings Per !hare =&P!>. E#S is the net income available to common shareholders of the company divided by the number ofshares outstanding. They usually have a <++# E#S number !which means that it is computed using allof mutually agreed upon accounting rules% and a #ro 7orma E#S figure !which means that they havead5usted the income to exclude any one time items as well as some non(cash items like amorti&ation of

goodwill or stock option expenses%. The most important thing to look for in the E#S figure is the overall*uality of earnings. Make sure the company is not trying to manipulate their E#S numbers to make itlook like they are more profitable. +lso, look at the growth in E#S over the past several *uarters - yearsto understand how volatile their E#S is, and to see if they are an underachiever or an overachiever. "nother words, have they consistently beaten expectations or are they constantly restating and loweringtheir forecastsL

The E#S number that most analysts use is the pro forma E#S. To compute this number, use the netincome that excludes any one(time gains or losses and excludes any non(cash expenses like stockoptions or amorti&ation of goodwill. Then divide this number by the number of fully diluted sharesoutstanding. Kistorical E#S figures and forecasts for the next 3@4 years can be found by visiting free

financial sites such as ahoo 7inance !enter the ticker and then click on 1estimates1%.Through fundamental investment research, one can determine their own E#S forecasts and apply othervaluation techni*ues below.

Price to &arnings =P?&>. /ow that you have several E#S figures !historical and forecasts%, you'll be able to look at the mostcommon valuation techni*ue used by analysts, the price to earnings ratio, or #-E. To compute this figuretake the stock price and divide it by the annual E#S figure. 7or example, if the stock is trading at 39and the E#S is 9.;9, the #-E is 49 times. To get a good feeling of what #-E multiple a stock trades at, besure to look at the historical and forward ratios.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 19/57

Kistorical #-Es are computed by taking the current price divided by the sum of the E#S for the last four*uarters, or for the previous year. ou should also look at the historical trends of the #-E by viewing achart of its historical #-E over the last several years !you can find on most finance sites like ahoo7inance%. Specifically you want to find out what range the #-E has traded in so that you can determine if the current #-E is high or low versus its historical average.

7orward #-Es reflect the future growth of the company into the figure. 7orward #-Es are computed bytaking the current stock price divided by the sum of the E#S estimates for the next four *uarters, or for

the E#S estimate for next calendar or fiscal year or two.#-Es change constantly. "f there is a large price change in a stock you are watching, or if the earnings!E#S% estimates change, the ratio is recomputed.

The p-E has the following advantages2

3. #-E ratio indicates price per rupee of the share earning. This would help to compare the prices of stocks,which have different E#S.

4. #-E ratio are helpful in analysing the stocks of the companies that do not pay dividend but haveearnings. "t should be noted that when there is loss, #-E ratio analyses is difficult to use.

6. The variables used in #-E ratio model are easier to estimate than the variables in the discounting models.

ith this ratio model the investor can only find the relative position of the different stocks. "t does notindicate what price is appropriate for a particular stock.

The anticipated return model

The expected return can be determined with the help of the following formula2

E!r%= Summation #i N 8i

here #i is the associated probability8i are the returns in different years.

3olding period return model

8eturn can be calculated with the help of the following formula28= !#rice changeO )ash dividend%- #urchase price8= ! O #tO3 @ #t%- #there,8 is the returns is the dividends#tO3 is the #rice at the end of the period

#t is the initial price

Present alue of the Return Model

#rice of the share,#o= 3-3Or O #3-3Or here,#o is the price of the share3 is the next year dividend8 is Expected rate of return#3 is Selling price at the end of one year periodith this model price of the share and also selling price of the share can be determined.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 20/57

Constant @rowth rate model

#rice of the share is given by the formula2#o= 3-r(ghere#o is the price of the share3 is the dividend of the next year 8 is the expected rate of return< is the constant growth

+ssumption( Stable dividend policy and constant stable rate of returnN /ote= if theoretical value P +ctual #rice then Buy

"f theoretical value Q +ctual #rice then sell"f #resent rate of return P re*uired rate of return then Buy"f #resent rate of return Q re*uired rate of return then Sell

+onds( ;ature and 6valuation of +ondsA bonds price and yield determine its +alue in the secondary market. @b+iously' a bondmust ha+e a price at hich it can be bought and sold 3see nderstanding !ond Market?ricesN belo for more7' and a bonds yield is the actual annual return an in+estor cane4pect if the bond is held to maturity. Gield is therefore based on the purchase price of

the bond as ell as the coupon.

A bonds price alays mo+es in the opposite direction of its yield' as illustrated abo+e. The key to understanding this critical feature of the bond market is to recogni(e that abonds price reLects the +alue of the income that it pro+ides through its regular couponinterest payments. /hen pre+ailing interest rates fall O notably rates on go+ernmentbonds O older bonds of all types become more +aluable because they ere sold in ahigher interestrate en+ironment and therefore ha+e higher coupons. In+estors holdingolder bonds can charge a premiumN to sell them in the secondary market. @n the otherhand' if interest rates rise' older bonds may become less +aluable because their couponsare relati+ely lo' and older bonds therefore trade at a discount.N

Since go+ernments began to issue bonds more fre;uently in the early tentieth centuryand ga+e rise to the modern bond market' in+estors ha+e purchased bonds for se+eralreasons> capital preser+ation' income' di+ersi,cation and as a potential hedge againsteconomic eakness or deLation. /hen the bond market became larger and more di+ersein the "&60s and "�s' bonds began to undergo greater and more fre;uent pricechanges and many in+estors began to trade bonds' taking ad+antage of anotherpotential bene,t> price' or capital' appreciation.

Capital preservation< nlike e;uities' bonds should repay principal at a speci,ed date'or maturity. This makes bonds appealing to in+estors ho do not ant to risk losingcapital and to those ho must meet a liability at a particular time in the future. !ondsha+e the added bene,t of o=ering interest at a set rate that is often higher than shortterm sa+ings rates. Income< Most bonds pro+ide the in+estor ith ,4edN income. @n a set schedule'hether ;uarterly' tice a year or annually' the bond issuer sends the bondholder aninterest payment' hich can be spent or rein+ested in other bonds. Stocks can alsopro+ide income through di+idend payments' but di+idends tend to be smaller than bondcoupon payments' and companies make di+idend payments at their discretion' hilebond issuers are obligated to make coupon payments.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 21/57

Capital appreciation< !ond prices can rise for se+eral reasons' including a drop ininterest rates and an impro+ement in the credit standing of the issuer. If a bond is held tomaturity' any price gains o+er the life of the bond are not reali(ed1 instead' the bondsprice typically re+erts to par 3"007 as it nears maturity and repayment of the principal.oe+er' by selling bonds after they ha+e risen in price O and before maturity O in+estorscan reali(e price appreciation' also knon as capital appreciation' on bonds. Capturingthe capital appreciation on bonds increases their total return' hich is the combination of

income and capital appreciation. In+esting for total return has become one of the mostidely used bond strategies o+er the past )0 years. 3or more' see !ond In+estmentStrategiesN.7

#iversication< Including bonds in an in+estment portfolio can help di+ersify theportfolio. Many in+estors di+ersify among a ide +ariety of assets' from e;uities andbonds to commodities and alternati+e in+estments' in an e=ort to reduce the risk of lo'or e+en negati+e' returns on their portfolios.

+ond Risk Interest Rate Risk

Fariability in return from the debt to in+estors is caused by the changes is in the marketinterest rate. #efault Risk The failure to pay the agreed amount of the debt instrument by the issuer in full' ontime or both are default risk.Marketa,ility Risk Fariability in return caused by the diHculty in selling the bonds ;uickly ithout ha+ing tomake a substantial concession is knon as marketability risk.Calla,ility Risk The uncertainty created in the in+estors return by the issuer ability to call the bonds atany time.+ond Return<olding ?eriod 5eturnP 3?rice gain or oss during the holding period Q Coupon interestrate7 ?rice at the beginning of the holding period

=ield &o Maturity GTM is the single discount factor that present +alue of the future cash Los from a bonde;ual to the current price of the bond. /e can also say that GTM is the rate of the returnan in+estor can e4pect to earn if the bond is held till maturity.3ssumption<

". There should not be any default.2. The in+estor hold the bond till maturity.$. All the coupon should be rein+ested immediately at the same time interest rate

as the same time yield to maturity of the bond.&%e formula is > G P C Q 3? or 8 Gear of Maturity7 3?o Q 7 2 /here G PGTMCP Coupon 5ate? or 8P ?remium or 8iscount?oP ?resent FalueP ace Falue

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 22/57

?resent FalueP C"3"Qy7" Q C23"Qy72 QRRRRRRR..Q 3Couponn Q face +alue73"Qy7n

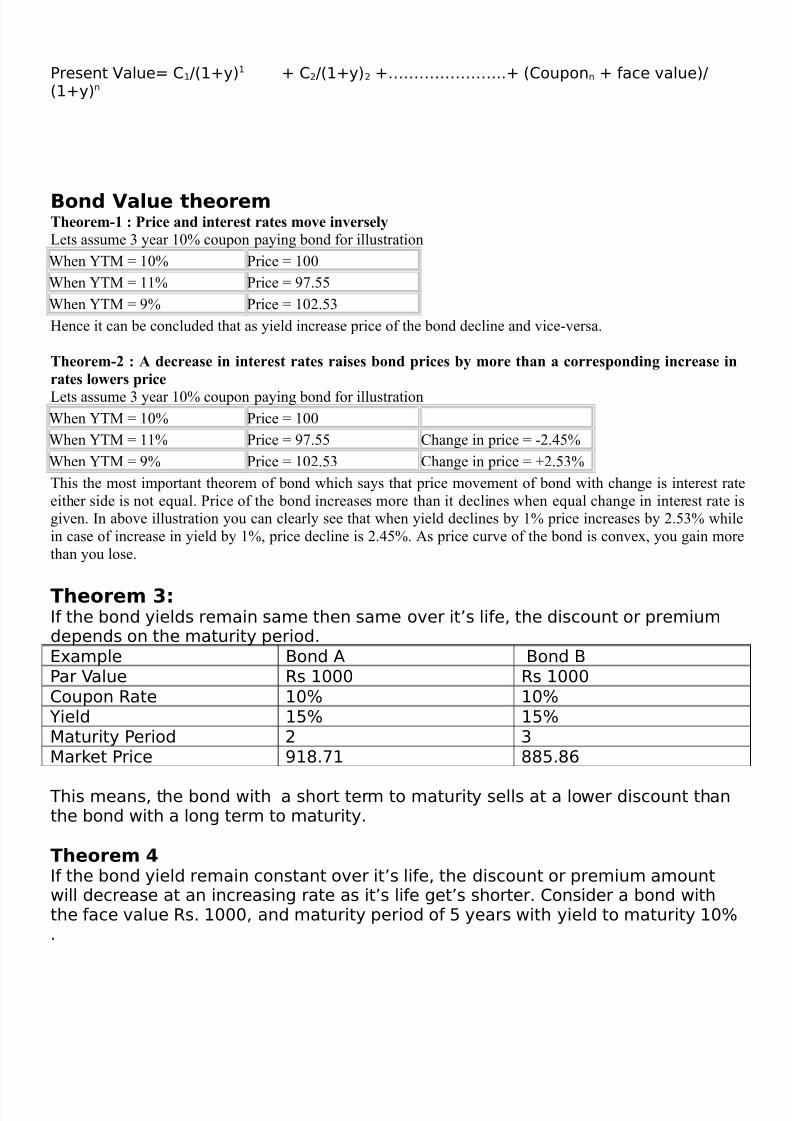

+ond >alue t%eoremTheorem7* : Price and interest rates move inversely

Jets assume 6 year 39: coupon paying bond for illustration

hen TM = 39: #rice = 399

hen TM = 33: #rice = R.;;

hen TM = R: #rice = 394.;6

Kence it can be concluded that as yield increase price of the bond decline and vice(versa.

Theorem7+ : # decrease in interest rates raises bond prices by more than a corresponding increase in

rates lowers price

Jets assume 6 year 39: coupon paying bond for illustration

hen TM = 39: #rice = 399

hen TM = 33: #rice = R.;; )hange in price = (4.G;:

hen TM = R: #rice = 394.;6 )hange in price = O4.;6:

This the most important theorem of bond which says that price movement of bond with change is interest rateeither side is not e*ual. #rice of the bond increases more than it declines when e*ual change in interest rate isgiven. "n above illustration you can clearly see that when yield declines by 3: price increases by 4.;6: whilein case of increase in yield by 3:, price decline is 4.G;:. +s price curve of the bond is convex, you gain morethan you lose.

&%eorem .<If the bond yields remain same then same o+er its life' the discount or premiumdepends on the maturity period.E4ample !ond A !ond !?ar Falue 5s "000 5s "000Coupon 5ate "0K "0K

Gield "*K "*KMaturity ?eriod 2 $Market ?rice &"#.6" ##*.#-

This means' the bond ith a short term to maturity sells at a loer discount thanthe bond ith a long term to maturity.

&%eorem 0If the bond yield remain constant o+er its life' the discount or premium amountill decrease at an increasing rate as its life gets shorter. Consider a bond iththe face +alue 5s. "000' and maturity period of * years ith yield to maturity "0K.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 23/57

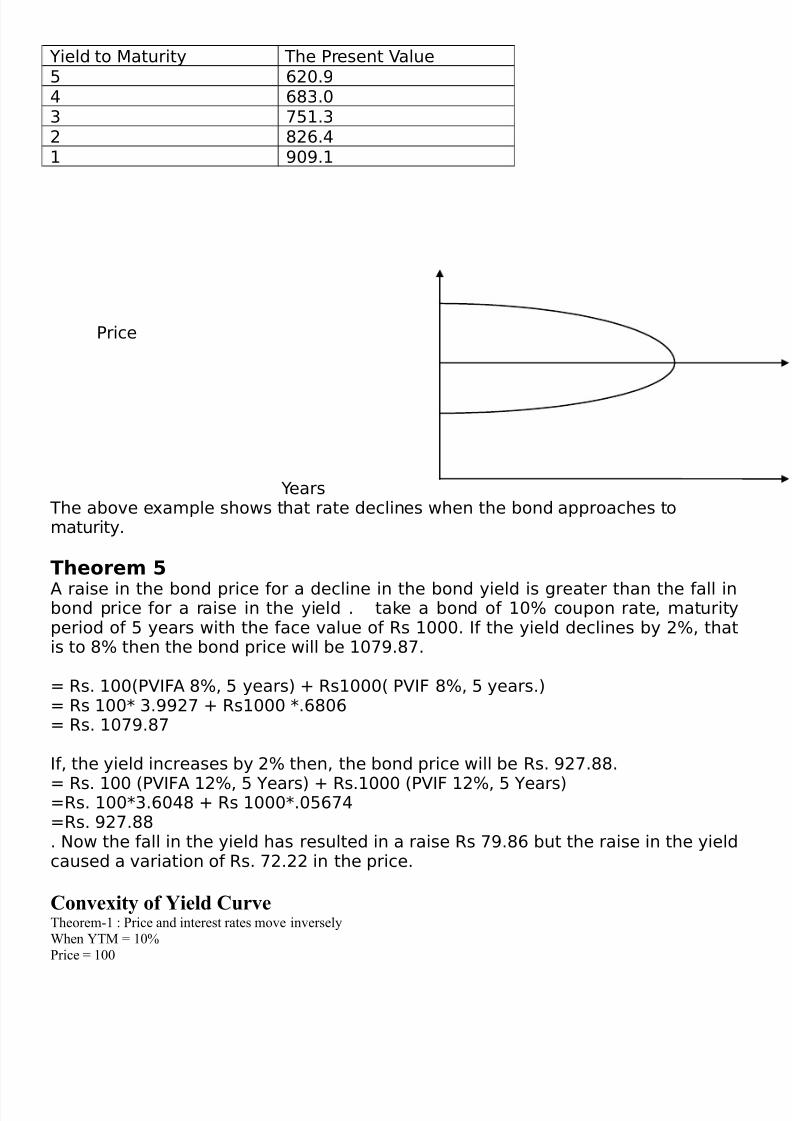

Gield to Maturity The ?resent Falue* -20.&) -#$.0$ 6*".$2 #2-.)" &0&."

?rice

Gears The abo+e e4ample shos that rate declines hen the bond approaches tomaturity.

&%eorem

A raise in the bond price for a decline in the bond yield is greater than the fall inbond price for a raise in the yield . take a bond of "0K coupon rate' maturityperiod of * years ith the face +alue of 5s "000. If the yield declines by 2K' thatis to #K then the bond price ill be "06&.#6.

P 5s. "003?FIA #K' * years7 Q 5s"0003 ?FI #K' * years.7P 5s "00 $.&&26 Q 5s"000 .-#0-P 5s. "06&.#6

If' the yield increases by 2K then' the bond price ill be 5s. &26.##.

P 5s. "00 3?FIA "2K' * Gears7 Q 5s."000 3?FI "2K' * Gears7P5s. "00$.-0)# Q 5s "000.0*-6)P5s. &26.##. :o the fall in the yield has resulted in a raise 5s 6&.#- but the raise in the yieldcaused a +ariation of 5s. 62.22 in the price.

Conveity of 2ield CurveTheorem(3 2 #rice and interest rates move inverselyhen TM = 39:#rice = 399

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 24/57

hen TM = 33:#rice = R.;;hen TM = R:#rice = 394.;6Theorem(4 2 + decrease in interest rates raises bond prices by more than a corresponding increase in rates lowers pricehen TM = 39:#rice = 399

hen TM = 33:

#rice = R.;;)hange in price = (4.G;:hen TM = R:#rice = 394.;6)hange in price = O4.;6:This the most important theorem of bond which says that price movement of bond with change is interest rate eitherside is not e*ual. #rice of the bond increases more than it declines when e*ual change in interest rate is given. "n aboveillustration you can clearly see that when yield declines by 3: price increases by 4.;6: while in case of increase in yield by 3:, price decline is 4.G;:. +s price curve of the bond is convex, you gain more than you lose.

The term !tructure of the 6nterest rate =2ield Curve>The bond porfolio manager is often concerned with two aspects of the interest rate2 the level of the interest ratethe term structure of the interest rate. The relationship between the yield and the time or years to maturity iscalled the term structure. The term structure is also known as yield curve. "n analy&ing the effect of maturity on

yield curve other influences held constant. sually pure discount instrument are selected to eliminate the effectof coupon payment. The bond chosen do not have early redemption features. The maturity dates are different but the risks, tax liabilities and redemption possibilities are similar.

"uration

uration measures the time structure of the bond and the bond interest rate risk. The time structure of theinvestment in bonds is expressed in two ways. The common way to state is how many years he has to wait untilthe bond matures and the principles money is paid back. This is known as asset time to maturity or its years tomaturity. The other way is to measure the average time until all the interest coupons and the principle isrecovered. This is called MacaulayCs duration. uration is defined as the weighted average of the time period tothe maturity, weights present values of the cash flow in each time period. The formula is.= )3-!3Or%- #9 O )4-!3Or%4-#9O)t-!3Or%t-#9NTuration =

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 25/57

)= )ash flows8 = )urrent TMT= number of years#I !)%= #resent value of the cash flow#9= Sum of the present value of the cash flows.<eneral 8ules2

• Jarger the coupon rate, lower the duration and less volatile the bond price.• Jonger the term to maturity, longer the duration and more the volatile bond.

• Kigher the TM, lower the bond duration and bond volatility, and vice versa.• "n a &ero coupon bond, the bonds term to maturity and uration are the same.

"mportance of the duration2The concept of the duration is important because it provide the length of a bond, helpful in evolvingimmuni&ation! the techni*ue that make the bond portfolio holder to be relatively certain about the promisedstream of the cash flows.% strategies for the portfolio management and measures the sensitivity of the bond price to changes in the interest rate.

Fundamental analysis

3. Economic +nalysis4. "ndustry analysis

6. )ompany +nalysis3. Economic +nalysisEconomic "ndicators

• <#• /ational "ncome• Employment• "nflation

8egression Model4. "ndustry +nalysis

• <rowth• )ost Structure and #rofitability

• /ature of the "ndustry• /ature of the )ompetition• <overnment policy• Jabor market condition

8esearch and development

Fundamental analysis ? Technical #nalysis

. )ompany analysis• )apital structure• <rowth of the company and sales• Stability of the sales•

Earning of the company• 7inancial statement

Technical #nalysis

"t is the process of identifying the time reversal at an earlier stage to formulate buying and selling strategies.ith the help of many indicators we can prdict the price volume and demand supply of the stocks.+ssumptions2

3. The market discount everything.4. The market value is determined by the demand and supply.6. The market always moves in trend

Technical #nalysis

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 26/57

Technical tools:

3. ow theory4. Iolume Trade6. Moving +verageG. $dd Jot Trading

"ow theory

Based on Kypothesis

• /o individual buyer or seller influence the ma5or trend in market.• Market discounts everything.• "t is not a tool to beat the market. "t provide a way to understand it better.

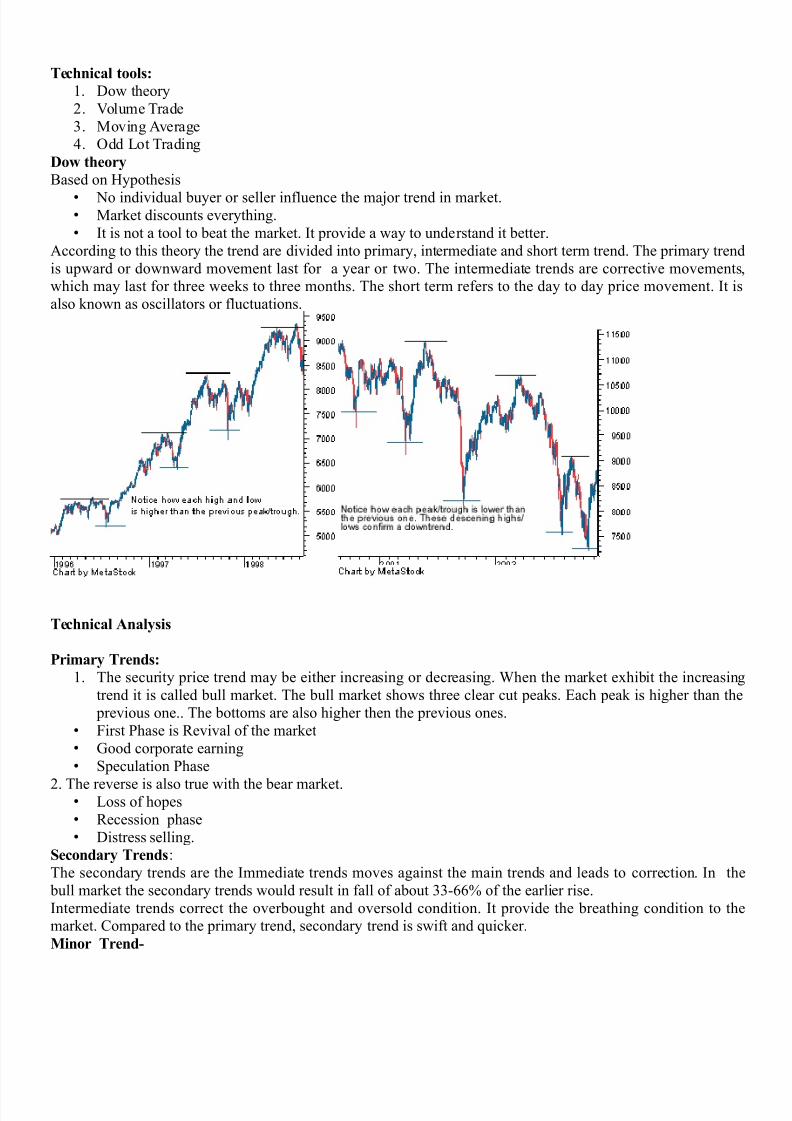

+ccording to this theory the trend are divided into primary, intermediate and short term trend. The primary trendis upward or downward movement last for a year or two. The intermediate trends are corrective movements,which may last for three weeks to three months. The short term refers to the day to day price movement. "t isalso known as oscillators or fluctuations.

Technical #nalysis

Primary Trends:

3. The security price trend may be either increasing or decreasing. hen the market exhibit the increasingtrend it is called bull market. The bull market shows three clear cut peaks. Each peak is higher than the previous one.. The bottoms are also higher then the previous ones.

• 7irst #hase is 8evival of the market• <ood corporate earning• Speculation #hase

4. The reverse is also true with the bear market.• Joss of hopes• 8ecession phase• istress selling.

!econdary Trends2The secondary trends are the "mmediate trends moves against the main trends and leads to correction. "n the bull market the secondary trends would result in fall of about 66(HH: of the earlier rise."ntermediate trends correct the overbought and oversold condition. "t provide the breathing condition to themarket. )ompared to the primary trend, secondary trend is swift and *uicker.Minor Trend7

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 27/57

Minor trend or tertiary moves are called as random wriggles. They are simply the daily price fluctuationsMinor trends tries to correct the secondary trend movement. "t is better for the investors to concentrate on the primary and secondary trends.

Technical #nalysis

olume of trade A

ow gave special emphasis on volume. Iolume expands along with the bull and bear market and narrows down

in the bear market. "f the volume falls with the rise or vice versa, it is the matter of concern for the investors andthe trend may not persist for the longer time. Technical analyst used volume as an excellent method ofconfirming the trend. The market is said to be bullish when small volume of trade and large volume trade followfall in price and the rise in price.Jarge rise in price or large fall in price leads to large increase in volume . Jarge volume with rise in priceindicates that bull market and the large volume with fall in price indicates bear market."f the volume declines for consecutive five days, then it will be continue for another four days and the same istrue in increasing volume.;dd lot trading7

Shares are generally sold in lot of hundreds. Share which are sold in smaller lot fewer than 399 are called oddlot. Such buyers and sellers are also called odd lotters. $dd lot purchase to odd lot sale !#urchase : sales% is

called as lot index. The increase in odd lot purchase results in an increase in the index. 8elatively more sellingleads to fall in the index. "t is generally considered that the professional investors is more informed and strongerthan odd lotters. hen the professional investors dominate the market, the market is considered weak. Thenotion behind is that odd lot purchase is concentrated at the top of the market cycle and selling at the bottom.Kigh odd lot purchase forecast fall in the market price and low purchaseUsales ratio are presumed to occurtowards the end of bear market.Moving average7

The market indices do not rise or fall in straight line. The upward and downward movements are interrupted bythe counter moves. The underlying trend can be studied by smoothing of the data. To smooth the data movingaverage techni*ue is used.The word moving means that the body of the data moves ahead to include the recent observations. "f it is five

day moving average, on the sixth day the body of the data moves to include the sixth day observationeliminating the first dayCs observation. Jikewise it continues. "n this method, closing price of the stock is used.The moving average are used to study the movement of the market as well as the individual scrip prices. Themoving average indicates that the underlying trend in the scrip. The period of average determines the period ofthe trend that is being identified. 7ro underlying short term trend, a39 day or 69 day moving average are used"n the case of medium term trend ;9 day to 34; day are adopt. 499 day moving average is used to identify thelong term trend.

"ifference between Fundamental and Technical #nalysis

$asis Fundamental #nalysis Technical #nalysis

efinition2 )alculates stock value using economicfactors, known as fundamentals. ses price movement of security to predict future price movements

ata gathered from2 7inancial statements )harts

Stock bought2 hen price falls below intrinsic valuehen trader believes they can sell iton for a higher price

Time hori&on2 Jong(term approach Short(term approach

7unction2 "nvesting Trade

)oncepts used28eturn on E*uity !8$E% and 8eturn on+ssets !8$+%

ow Theory, #rice ata

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 28/57

Iision2 looks backward as well as forward looks backward

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 29/57

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 30/57

7eature of the options23. The option is exercisable by the owner - buyer only.4. The owner has limited liability.6. $ption owners has no voting right.G. $ptions have high degree $f risk to the option writer.;. These are popular they allow the profit from favourable movement in exchange rate.H. 7lexibility in investors needs.. /o certificate issued by the company

Call options

The call option that gives the right to buy in its contract gives the particulars of the following:

*, The name of the company whose shares are to be purchased,

+, The number of the shares to be purchased,

8, The purchase price or the eercise price or the strike price of the shares to be bought,

B, The epiration date,

&le:

Jet us + who owns 399 shares of 8eliance "ndustries, which on 39 ec, 4934 sold for 8s 33R #er share. Kecould give !or sell% to B the right to buy that 399 shares at any time during the next 4 months at a price of 8s34; per share. The price 8s34; is called the exercise price.. /ow the seller of the option, + is the option seller

or write. 7or providing the option, + will charge premium from B. Jet us assume the premium of 8s 6. "n thiscondition B has to pay 8s. 399N6= 699 as premium to + to make him sign the contract. hen the exercise priceis less than the current market price of the underlying stock the option is in the money. 7or example the price ofthe reliance share after 4 months is 8s369 it is said to be in the money. But if the price falls to the 8s 349 theoption is said to be out of the money. The advantage is that B has to pay only 8s. 699 and get more profit if the price rise beyond 8s. 34;.

Put options

The put option gives the right to sell an asset or security to someone else, 6t is not an obligation but an

option in its contract gives the particulars of the following:

*, The name of the company whose shares are to be sold,

+, The number of the shares to be sold,8, The purchase price or the eercise price or the strike price of the shares to be sold,

B, The epiration date,

&le:

Jet us assume that + thinks that 8eliance industries stock price can decline from its current level of 8s 33R pershare during the next two months. Ke could buy a put option to sell the 399 shares at 8s 34; which is thestriking price. + being the buyer of the option to sell the shares, has to pay premium in order to get the writer Bto sign the contract and to assume risk.Jet us take the premium as 8s ; per share. /ow + has to pay 8s 399N;=;99 to B. "f the price falls to 8s 33;, +stands gain because he can sell it at 8s 34; i.e. 399N34;=34;99. The gain is 8s. 34;99(33;99 !#resent value%(;99 premium. +t the same time if the price has increased to 8s 369 per share, + will not exercise the option and

his loss is only 8s. ;99.

;ption Pricing ModelThe Black(Scholes model for calculating the premium of an option was introduced in 3R6 in a paper entitled,1The #ricing of $ptions and )orporate Jiabilities1 published in the Journal of Political Economy. The formula,developed by three economists @ 7ischer Black, Myron Scholes and 8obert Merton @ is perhaps the world'smost well(known options pricing model. Black passed away two years before Scholes and Merton wereawarded the 3RR /obel #ri&e in Economics for their work in finding a new method to determine the value ofderivatives !the /obel #ri&e is not given posthumously0 however, the /obel committee acknowledged Black'srole in the Black(Scholes model%.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 31/57

The Black(Scholes model is used to calculate the theoretical price of European put and call options,ignoring any dividends paid during the option's lifetime. hile the original Black(Scholes model did not takeinto consideration the effects of dividends paid during the life of the option, the model can be adapted toaccount for dividends by determining the ex(dividend date value of the underlying stock..The model makes certain assumptions, including2

The options are European and can only be exercised at expiration• /o dividends are paid out during the life of the option

• Efficient markets !i.e., market movements cannot be predicted%• /o commissions• The risk(free rate and volatility of the underlying are known and constant• 7ollows a lognormal distribution0 that is, returns on the underlying are normally distributed.

The formula, shown in 7igure in next slide, takes the following variables into consideration2

)urrent underlying price• $ptions strike price• Time until expiration, expressed as a percent of a year• "mplied volatility• 8isk(free interest rates

#dvantages and disadvantages of $lack 7scholes Model

+dvantages2The main advantage of the black scholes model is speed( it let you to calculate a very large number of

option in a very short time.isadvantages2

• "t calculate the price at one point of time therefore it can be used for only +merican style exerciseoption.

• Most of the options traded in stock exchanges are +merican style. Therefore itCs use is limited.• "ts is used for call option pricing only.

$inomial Model for option Pricing

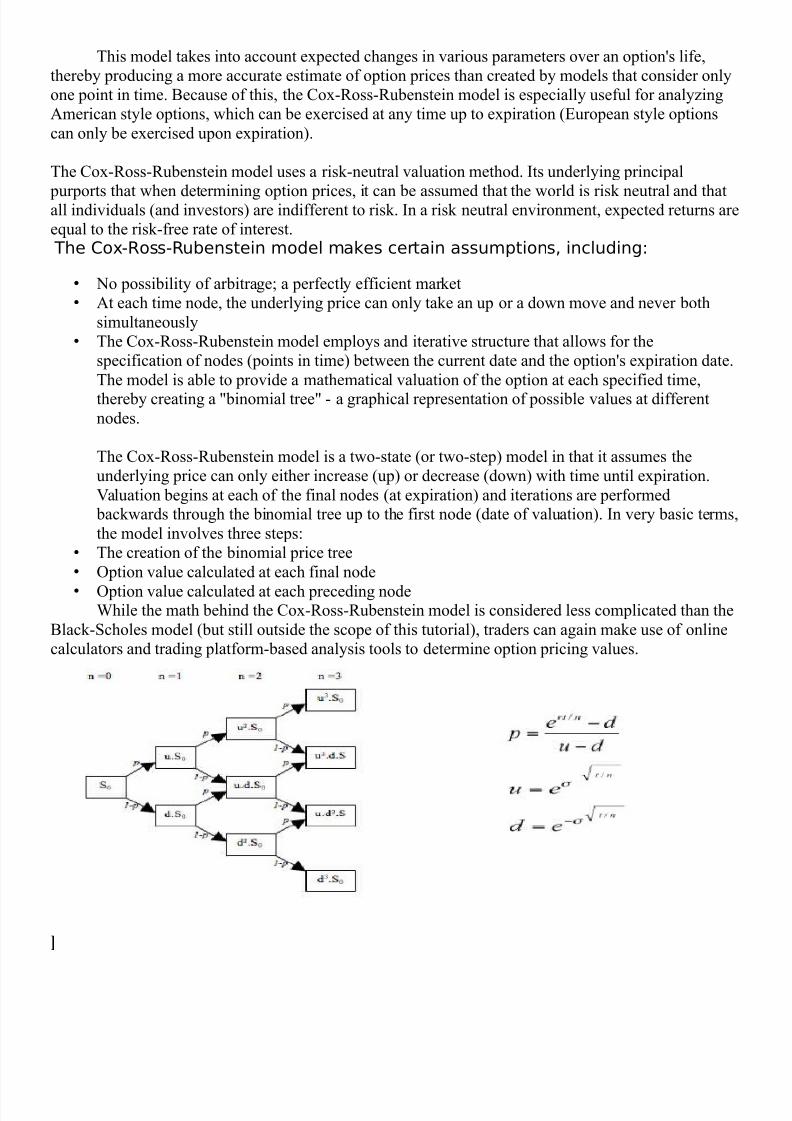

The )ox(8ubenstein !or )ox(8oss(8ubenstein% binomial option pricing model is a variation of theoriginal Black(Scholes option pricing model. "t was first proposed in 3RR by financialeconomists-engineers Vohn )arrington )ox, Stephen 8oss and Mark Edward 8ubenstein. The model is popular because it considers the underlying instrument over a period of time, instead of 5ust at one point in time.

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 32/57

This model takes into account expected changes in various parameters over an option's life,thereby producing a more accurate estimate of option prices than created by models that consider onlyone point in time. Because of this, the )ox(8oss(8ubenstein model is especially useful for analy&ing+merican style options, which can be exercised at any time up to expiration !European style optionscan only be exercised upon expiration%.

The )ox(8oss(8ubenstein model uses a risk(neutral valuation method. "ts underlying principal

purports that when determining option prices, it can be assumed that the world is risk neutral and thatall individuals !and investors% are indifferent to risk. "n a risk neutral environment, expected returns aree*ual to the risk(free rate of interest. The Co45oss5ubenstein model makes certain assumptions' including>

• /o possibility of arbitrage0 a perfectly efficient market• +t each time node, the underlying price can only take an up or a down move and never both

simultaneously• The )ox(8oss(8ubenstein model employs and iterative structure that allows for the

specification of nodes !points in time% between the current date and the option's expiration date.The model is able to provide a mathematical valuation of the option at each specified time,thereby creating a 1binomial tree1 ( a graphical representation of possible values at differentnodes.

The )ox(8oss(8ubenstein model is a two(state !or two(step% model in that it assumes theunderlying price can only either increase !up% or decrease !down% with time until expiration.Ialuation begins at each of the final nodes !at expiration% and iterations are performed backwards through the binomial tree up to the first node !date of valuation%. "n very basic terms,the model involves three steps2

• The creation of the binomial price tree• $ption value calculated at each final node• $ption value calculated at each preceding node

hile the math behind the )ox(8oss(8ubenstein model is considered less complicated than theBlack(Scholes model !but still outside the scope of this tutorial%, traders can again make use of onlinecalculators and trading platform(based analysis tools to determine option pricing values.

(

8/17/2019 Notes Saim

http://slidepdf.com/reader/full/notes-saim 33/57

Futures"n finance, a futures contract !more collo*uially, futures% is a standardi&ed contract between two parties to buyor sell a specified asset of standardi&ed *uantity and *uality for a price agreed upon today !the futures price orstrike price% with delivery and payment occurring at a specified future date, the delivery date. The contracts arenegotiated at a futures exchange, which acts as an intermediary between the two parties. The party agreeing to buy the underlying asset in the future, the 1buyer1 of the contract, is said to be 1long1, and the party agreeing tosell the asset in the future, the 1seller1 of the contract, is said to be 1short1. The terminology reflects theexpectations of the partiesWthe buyer hopes or expects that the asset price is going to increase, while the sellerhopes or expects that it will decrease in near future.

"n many cases, the underlying asset to a futures contract may not be traditional commodities at all @ thatis, for financial futures the underlying item can be any financial instrument !also including currency, bonds, andstocks%0 they can be also based on intangible assets or referenced items, such as stock indexes and interest rates.nlike an option both parties of a futures contract must fulfill the contract on the delivery date. The sellerdelivers the underlying asset to the buyer, or, if it is a cash(settled futures contract, then cash is transferred fromthe futures trader who sustained a loss to the one who made a profit. To exit the commitment prior to thesettlement date, the holder of a futures position can close out its contract obligations by taking the opposite

position on another futures contract on the same asset and settlement date. The difference in futures prices isthen a profit or loss.