Notenstein Compass, April 213 Notenstein ass omp C fileNotenstein Compass, April 213 – 1 –...

4

Notenstein Compass, April 2013 – 1 – Arbitrary and uncoordinated expropriation of depositors in Cyprus, ongoing record-high unemployment in many parts of Europe and political stalemate in Italy – these are just some of the events that made headlines in the first quarter. The equity markets, however, were unperturbed: the Swiss Market Index climbed an impressive 14.5 percent, its third- best quarterly performance since the turn of the century. The small island state of Cyprus made headlines as its gov- ernment, under direction and pressure from the EU, set out to help itself to depositors’ savings, thus sparking debate about legal security across Europe. You can read more on this topic in this month’s Notenstein Dialogue. Another type of creeping expropriation is taking place through negative real interest rates for the euro and US dol- lar. With interest rate policy in many countries keeping yields on government bonds lower than inflation, consum- ers are experiencing a real loss of purchasing power. Under such conditions, the current stock market rally is not surprising: valuations on equities with real-asset characteris- tics and stable dividend yields are back near their historical averages and are thus fairly valued. However, they remain attractive compared to other asset classes – particularly bonds, where sharp price gains suggest that any potential bubble is more likely to be found in the fixed-income segment. The ex- pansionary monetary policy measures adopted by central banks in industrialised countries around the world give a boost to equities, but not exclusively; this dabbling style of policy-making has a stark effect on currencies as well. The yen provides an instructive example. The Bank of Japan has left no stone unturned in seeking to exit the deflationary spi- ral (“Muddling along”) and artificially stimulate the economy, but such measures are toxic for fixed-income investments in the medium term. In light of the distortions in the currency markets, we continue to favour real-asset currencies such as the Swedish krona, Canadian dollar and Australian dollar. While currencies in the industrialised nations seem to be in a global race to the bottom, those in the emerging markets appear to be heading for an upturn. As the global economy’s centre of gravity shifts, the currencies of the “Golden East” and other emerging markets will become stronger, and their economies more competitive, than ever. Another key trend is the growing middle class in Asia. The Asia-Pacific region is already home to around one quarter of the world’s middle class, and in 20 years the figure will be two thirds. Some two billion Asians are set to enter the middle class, bringing along purchasing power and a shopping list. This is a bright prospect for globally active Western companies that can adjust to changing markets. Martin Schenk Dr Ivan Adamovich Head of Private Banking Head of Private Banking Switzerland International Notenstein Compass

Transcript of Notenstein Compass, April 213 Notenstein ass omp C fileNotenstein Compass, April 213 – 1 –...

Notenstein Compass, April 2013

– 1 –

Arbitrary and uncoordinated expropriation of depositors in Cyprus, ongoing record-high unemployment in many parts of Europe and political stalemate in Italy – these are just some of the events that made headlines in the first quarter. The equity markets, however, were unperturbed: the Swiss Market Index climbed an impressive 14.5 percent, its third-best quarterly performance since the turn of the century.

The small island state of Cyprus made headlines as its gov-

ernment, under direction and pressure from the EU, set out

to help itself to depositors’ savings, thus sparking debate

about legal security across Europe. You can read more on

this topic in this month’s Notenstein Dialogue.

Another type of creeping expropriation is taking place

through negative real interest rates for the euro and US dol-

lar. With interest rate policy in many countries keeping

yields on government bonds lower than inflation, consum-

ers are experiencing a real loss of purchasing power.

Under such conditions, the current stock market rally is not

surprising: valuations on equities with real-asset characteris-

tics and stable dividend yields are back near their historical

averages and are thus fairly valued. However, they remain

attractive compared to other asset classes – particularly bonds,

where sharp price gains suggest that any potential bubble is

more likely to be found in the fixed-income segment. The ex-

pansionary monetary policy measures adopted by central

banks in industrialised countries around the world give a

boost to equities, but not exclusively; this dabbling style of

policy-making has a stark effect on currencies as well. The

yen provides an instructive example. The Bank of Japan has

left no stone unturned in seeking to exit the deflationary spi-

ral (“Muddling along”) and artificially stimulate the economy,

but such measures are toxic for fixed-income investments

in the medium term. In light of the distortions in the currency

markets, we continue to favour real-asset currencies such as

the Swedish krona, Canadian dollar and Australian dollar.

While currencies in the industrialised nations seem to be in

a global race to the bottom, those in the emerging markets

appear to be heading for an upturn. As the global economy’s

centre of gravity shifts, the currencies of the “Golden East”

and other emerging markets will become stronger, and their

economies more competitive, than ever. Another key trend

is the growing middle class in Asia. The Asia-Pacific region

is already home to around one quarter of the world’s middle

class, and in 20 years the figure will be two thirds. Some two

billion Asians are set to enter the middle class, bringing

along purchasing power and a shopping list. This is a bright

prospect for globally active Western companies that can

adjust to changing markets.

Martin Schenk Dr Ivan Adamovich

Head of Private Banking Head of Private Banking

Switzerland International

Notenstein Compass

Notenstein Compass, April 2013

– 2 –

Equities: hitting all-time highs

Nikkei: +19%, SMI: +15%, Dow Jones: +11% – results that

would be respectable for a “normal” year on the stock ex-

change currently apply to just the first quarter of the year.

The rally in recent months lifted valuation levels in many

markets back towards their historical averages, with the re-

sult that equities are no longer “cheaply” but rather “fairly”

valued. Investors may now be wondering how much upside

potential still exists for shares.

Economic conditions remain promising for equities. Although

global economic growth has been weak and Europe is mired

in recession, the outlook for future global growth is brighter

today than it was six months ago. The US economy is gather-

ing pace, China’s is reviving and Japan appears to have halted

its downward economic spiral. Against a backdrop of increas-

ing but sluggish growth accompanied by low or negative infla-

tion, central banks have free rein to extend stimulus measures.

At the same time, the systemic risks that have plagued the

financial markets over the last five years are retreating into

the background. The muted market reaction to such factors

as the election drama in Italy and the resurgence of the euro

crisis in Cyprus indicates that investors are increasingly refo-

cusing on the fundamental data for individual markets. Equi-

ties are also enjoying a revival among both private and in-

stitutional investors, who recently began channelling more

money into this asset class after several years of shunning it.

In this constructive environment, it seems realistic to expect

equity risk premiums to decline further, towards levels pre-

dating the financial crisis.

In the context of investment portfolios, however, the oft-

cited historical valuation comparison is less relevant than

the relative appeal of various asset classes. After all, investors

can only purchase assets that are available today – they can-

not invest at yesterday’s prices. The obvious preference for

equities compared to other assets, particularly cash and

fixed-income paper, can be largely attributed to the antici-

pated surplus earnings on shares.

Paper currencies race to depreciate: currency wars?

When considering the relative attractiveness of various invest-

ments, the adage “Don’t fight the Fed” comes to mind. With

their ultra-low interest rate policies and government bond

purchasing programmes, the US currency guardians and other

big central banks are exerting pressure on interest rates,

encouraging investors to assume more risk and ultimately

changing the anticipated relative returns between asset classes.

Both investment grade bonds, i.e. bonds with good or very

good credit ratings, and more speculative fixed-income pa-

per have become comparably expensive. Investors’ quest for

returns has reduced risk premiums far further on bonds than

on equities, which implies that central-bank monetary policy

is setting up equities as the asset class with the most promis-

ing risk-return profile.

However, this extremely easy and increasingly creative mon-

etary policy is leaving its mark not only on equities; it has also

had a growing influence on currencies in recent years. The

Japanese yen and pound sterling made the most prominent

headlines as the two weakest currencies in the year to date.

The yen’s frailty can be attributed to the Japanese gov-

ernment’s no-holds-barred scramble to exit a long-term de-

flationary spiral. Its combination of expansionary monetary

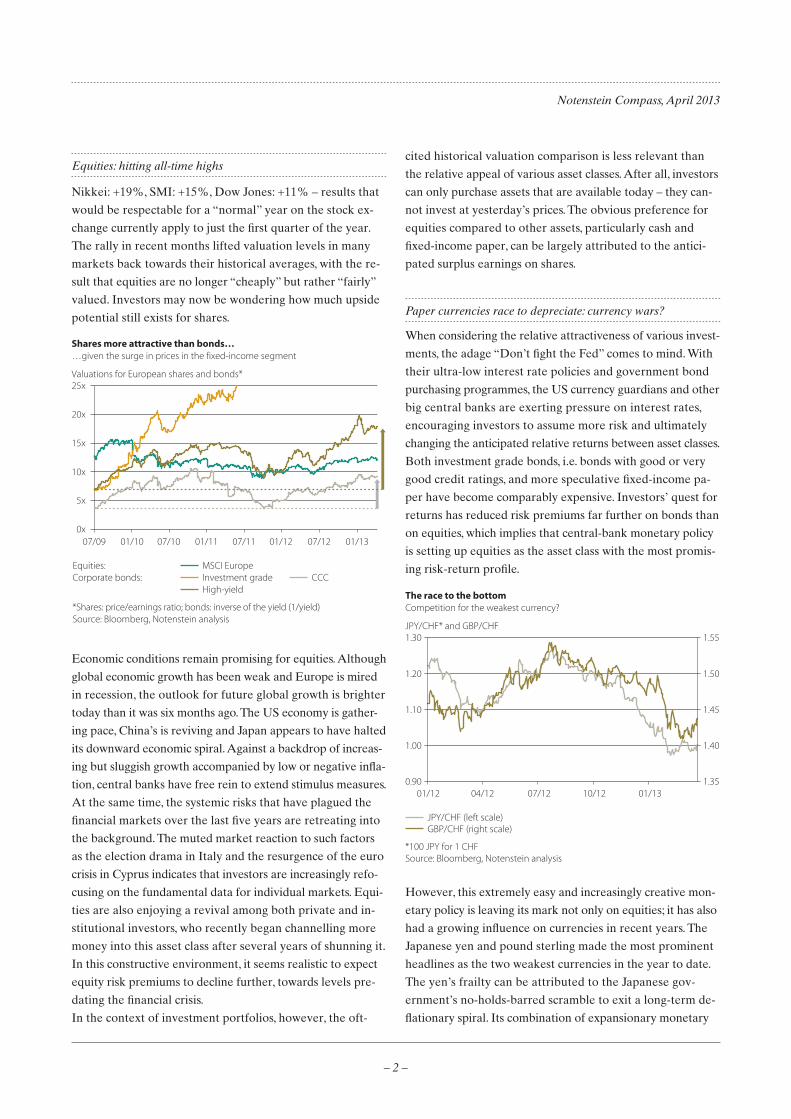

Valuations for European shares and bonds*

0x

5x

10x

20x

25x

Equities: MSCI EuropeCorporate bonds: Investment grade

High-yieldCCC

*Shares: price/earnings ratio; bonds: inverse of the yield (1/yield)

15x

07/09 01/10 07/10 01/11 07/11 01/12 07/12 01/13

Source: Bloomberg, Notenstein analysis

…given the surge in prices in the fixed-income segmentShares more attractive than bonds…

JPY/CHF* and GBP/CHF

0.90

1.00

1.10

1.20

1.30

1.35

1.40

1.45

1.50

1.55

01/12 04/12 07/12 10/12 01/13

GBP/CHF (right scale)JPY/CHF (left scale)

Competition for the weakest currency?The race to the bottom

Source: Bloomberg, Notenstein analysis*100 JPY for 1 CHF

Notenstein Compass, April 2013

– 3 –

policy and debt-financed economic stimulus programmes, gar-

nished with an inflation target of 2 percent, which the new

central bank governor Haruhiko Kuroda aims to reach within

two years, was christened “Abenomics” after Japan’s prime

minister. Thanks to this cocktail of measures, the yen has de-

preciated by some 20 percent since October 2012. In the UK,

on the other hand, it is the loss of the country’s AAA credit

rating and an economy on the verge of recession that have

hobbled sterling. In order to stimulate the economy, Chan-

cellor of the Exchequer George Osborne recently gave the

nod to the Bank of England to ease monetary policy even

further, granting the central bank more flexibility to pursue

its inflation target of 2 percent – a goal that has proved elu-

sive over the last five years. The market reaction proves

that such monetary policy dabbling cripples a currency: in-

flation expectations climbed higher while sterling lost

ground.

Asia’s middle class: the market of tomorrow

The recent developments in the forex markets have given

rise to talk of “currency wars”, suggesting that central banks

are purposefully weakening their domestic currencies. While

Japan’s intention to weaken the yen is fairly obvious, it is

more difficult to discern such purpose in the UK. In any case,

investors are less concerned about whether a currency depre-

ciates as a result of a concerted effort to provide vitally nec-

essary economic stimulus, or as a result of expansionary mon-

etary policy. Rather, they seek diversified investments in

fundamentally strong currencies that are not caught up in the

depreciation spiral, and in gold, a real asset.

Just ten years ago, Asian currencies were under enormous de-

preciation pressure and many countries were having problems

with their balance of payments. Today, these currencies are so

strong that they are affecting the competitiveness of the re-

gion. Asia’s increasing significance is not only evident in the fi-

nancial markets; the shift in the world’s economic centre of

gravity from West to East is even more obvious in the upward

mobility of wide swathes of the population. Just a few years

ago, less than one quarter of the world’s middle class lived in

the emerging markets of Asia. Today, a wave of households in

these developing regions are on the verge of entering the mid-

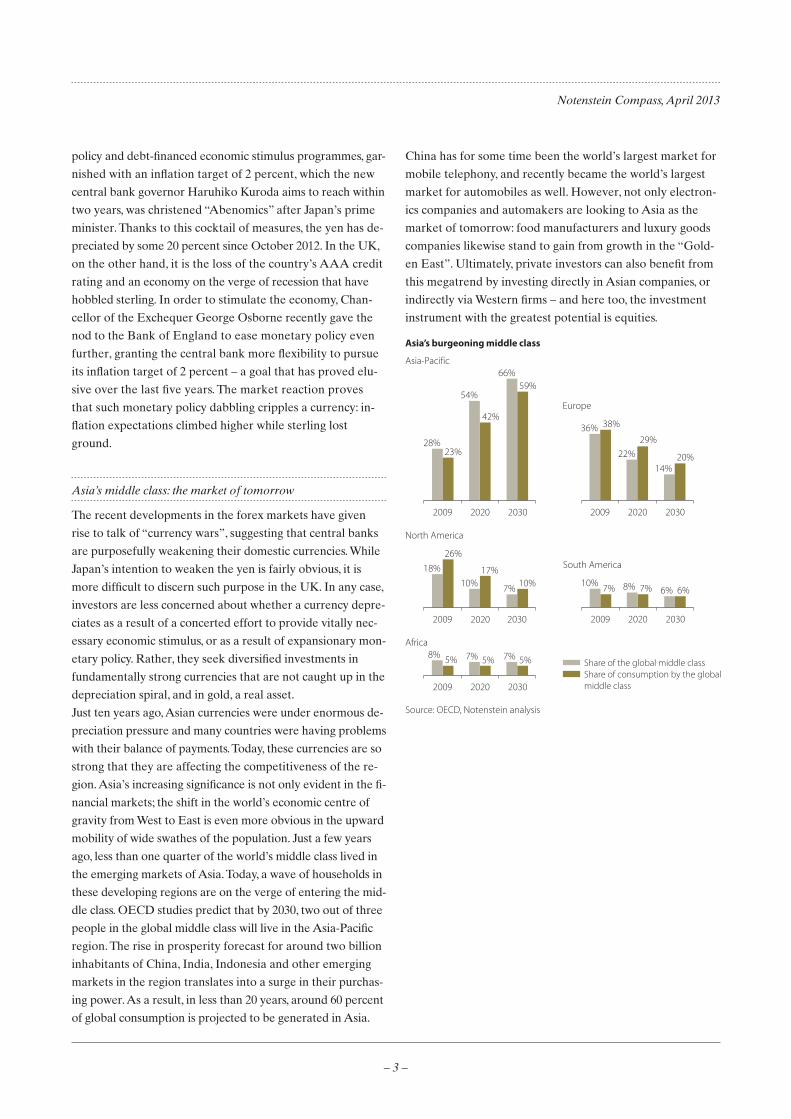

dle class. OECD studies predict that by 2030, two out of three

people in the global middle class will live in the Asia-Pacific

region. The rise in prosperity forecast for around two billion

inhabitants of China, India, Indonesia and other emerging

markets in the region translates into a surge in their purchas-

ing power. As a result, in less than 20 years, around 60 percent

of global consumption is projected to be generated in Asia.

China has for some time been the world’s largest market for

mobile telephony, and recently became the world’s largest

market for automobiles as well. However, not only electron-

ics companies and automakers are looking to Asia as the

market of tomorrow: food manufacturers and luxury goods

companies likewise stand to gain from growth in the “Gold-

en East”. Ultimately, private investors can also benefit from

this megatrend by investing directly in Asian companies, or

indirectly via Western firms – and here too, the investment

instrument with the greatest potential is equities.

7%8% 5% 5% 7% 5%

2009 2020 2030

Africa

18%10% 7%

26%

17%10%

2009 2020 2030

North America

8%10% 7% 7% 6%6%

2009 2020 2030

South America

22%29%

36% 38%

20%14%

2009 2020 2030

Europe54%

42%

28%23%

59%66%

2009 2020 2030

Asia-Pacific

Share of the global middle classShare of consumption by the globalmiddle class

Asia’s burgeoning middle class

Source: OECD, Notenstein analysis

Notenstein Compass, April 2013

– 4 –

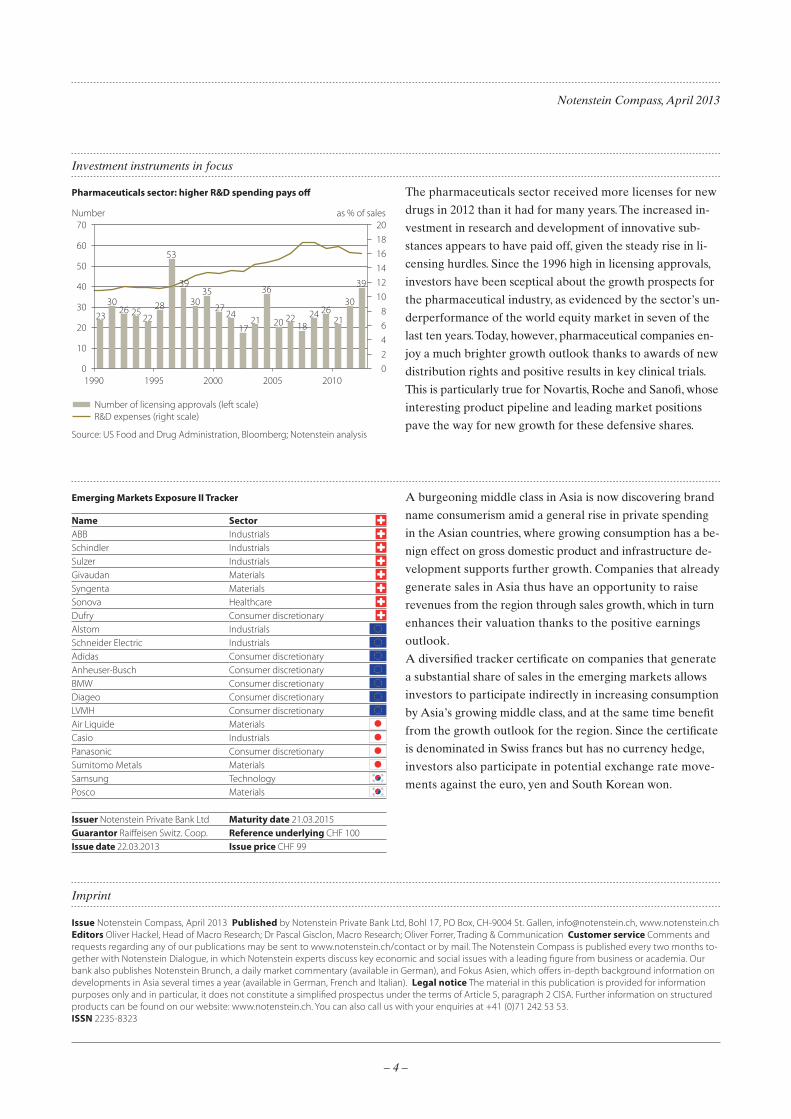

Pharmaceuticals sector: higher R&D spending pays off The pharmaceuticals sector received more licenses for new

drugs in 2012 than it had for many years. The increased in-

vestment in research and development of innovative sub-

stances appears to have paid off, given the steady rise in li-

censing hurdles. Since the 1996 high in licensing approvals,

investors have been sceptical about the growth prospects for

the pharmaceutical industry, as evidenced by the sector’s un-

derperformance of the world equity market in seven of the

last ten years. Today, however, pharmaceutical companies en-

joy a much brighter growth outlook thanks to awards of new

distribution rights and positive results in key clinical trials.

This is particularly true for Novartis, Roche and Sanofi, whose

interesting product pipeline and leading market positions

pave the way for new growth for these defensive shares.

Emerging Markets Exposure II Tracker A burgeoning middle class in Asia is now discovering brand

name consumerism amid a general rise in private spending

in the Asian countries, where growing consumption has a be-

nign effect on gross domestic product and infrastructure de-

velopment supports further growth. Companies that already

generate sales in Asia thus have an opportunity to raise

revenues from the region through sales growth, which in turn

enhances their valuation thanks to the positive earnings

outlook.

A diversified tracker certificate on companies that generate

a substantial share of sales in the emerging markets allows

investors to participate indirectly in increasing consumption

by Asia’s growing middle class, and at the same time benefit

from the growth outlook for the region. Since the certificate

is denominated in Swiss francs but has no currency hedge,

investors also participate in potential exchange rate move-

ments against the euro, yen and South Korean won.

Issue Notenstein Compass, April 2013 Published by Notenstein Private Bank Ltd, Bohl 17, PO Box, CH-9004 St. Gallen, [email protected], www.notenstein.ch Editors Oliver Hackel, Head of Macro Research; Dr Pascal Gisclon, Macro Research; Oliver Forrer, Trading & Communication Customer service Comments and requests regarding any of our publications may be sent to www.notenstein.ch/contact or by mail. The Notenstein Compass is published every two months to- gether with Notenstein Dialogue, in which Notenstein experts discuss key economic and social issues with a leading figure from business or academia. Our bank also publishes Notenstein Brunch, a daily market commentary (available in German), and Fokus Asien, which offers in-depth background information on developments in Asia several times a year (available in German, French and Italian). Legal notice The material in this publication is provided for information purposes only and in particular, it does not constitute a simplified prospectus under the terms of Article 5, paragraph 2 CISA. Further information on structured products can be found on our website: www.notenstein.ch. You can also call us with your enquiries at +41 (0)71 242 53 53.ISSN 2235-8323

Investment instruments in focus

Imprint

Number as % of sales70 20

1990 1995 2000 2005 2010

2823

3026 25

22

53

39

3035

2724

1721

36

20 2218

24 2621

30

39

60

50

40

30

20

10

0

1816141210

86420

Number of licensing approvals (left scale)R&D expenses (right scale)

Source: US Food and Drug Administration, Bloomberg; Notenstein analysis

Name SectorABB IndustrialsSchindler IndustrialsSulzer IndustrialsGivaudan MaterialsSyngenta MaterialsSonova HealthcareDufry Consumer discretionaryAlstom IndustrialsSchneider Electric IndustrialsAdidas Consumer discretionaryAnheuser-Busch Consumer discretionaryBMW Consumer discretionaryDiageo Consumer discretionaryLVMH Consumer discretionaryAir Liquide MaterialsCasio IndustrialsPanasonic Consumer discretionarySumitomo Metals MaterialsSamsung TechnologyPosco Materials

Issuer Notenstein Private Bank Ltd Maturity date 21.03.2015Guarantor Raiffeisen Switz. Coop. Reference underlying CHF 100Issue date 22.03.2013 Issue price CHF 99