not a replacement for the prospectus. Please read the ... Value Death Benefit: 1.10% . ... Note: If...

72

For financial professional use only. Not for use with the public. For financial professional use only. Not for use with the public. The material contained in this presentation is not a replacement for the prospectus. Please read the product prospectus for complete information and full disclosure, including risks, charges and fees.

Transcript of not a replacement for the prospectus. Please read the ... Value Death Benefit: 1.10% . ... Note: If...

For financial professional use only. Not for use with the public. For financial professional use only. Not for use with the public.

The material contained in this presentation is not a replacement for the prospectus. Please read the product prospectus for complete information and full disclosure, including risks, charges and fees.

Product-Specific Training – Polaris Variable Annuities

For financial professional use only. Not for use with the public.

3

Polaris Variable Annuity Product Line Guaranteed Living Benefits

• Polaris Income Plus® & Polaris Income Builder® • Polaris Income Plus DailySM • Fees

Investing with Polaris Death Benefits Polaris Select Investor Variable Annuity Overview Additional Information

Table of Contents

Polaris Variable Annuity

Product Line

5

Comprehensive Product Line

Product CDSC Duration

Mortality & Expense Charge

Polaris Platinum III 7 Years 1.30%

Polaris Platinum III with Early Access Rider 4 Years

1.70% Years 1-4 1.30% Years 5+

Polaris Choice IV 4 Years 1.65%

Polaris Select Investor 5 Years

1.10%* 1.40%**

0 years 1.35%*

1.70%**

* Account Value Death Benefit

** With Optional Return of Premium Death Benefit

The “C-Share” is an optional rider that must be elected at contract issue.

Polaris Variable Annuities are issued by American General Life Insurance Company. CDSC stands for Contingent Deferred Sales Charge, also known as a withdrawal charge. Fees, charges and other information regarding these products will be covered later in the presentation.

For financial professional use only. Not for use with the public.

6

Charges, Fees & Important Information

For financial professional use only. Not for use with the public.

Please see the prospectus for details.

Polaris Platinum III 7-year withdrawal charge: 8-7-6-5-4-3-2-0%

Polaris Choice IV 4-year withdrawal charge: 8-7-6-5-0%

Maximum issue age 85 (lower if certain features are elected) 85 (lower if certain features are elected)

Minimum initial investment $10,000 (Non-Qualified); $4,000 (Qualified) $25,000 (Non-Qualified and Qualified)

Minimum additional investment $500 (NQ and Q); $100 Automated Bank Draft $500 (NQ and Q); $100 Automated Bank Draft

Annualized M&E charge 1.30% 1.65%

Annual contract charge $50, waived for contracts of $75,000 or more* (Fee may be lower in certain states. Please see prospectus)

$50, waived for contracts of $75,000 or more* (Fee may be lower in certain states. Please see prospectus)

Total portfolio operating expenses as of 12/31/15 and 1/31/16, respectively Total portfolio operating expenses: 0.55% to 2.20% Total portfolio operating expenses: 0.55% to 2.20%

Free withdrawals during the withdrawal charge period

Greater of: 10% of purchase payments not yet withdrawn each contract year or, if an income protection option is elected, the maximum annual withdrawal amount

Greater of: 10% of purchase payments not yet withdrawn each contract year or, if an income protection option is elected, the maximum annual withdrawal amount

Automatic Asset Allocation Rebalancing Quarterly, semi annually or annually Quarterly, semi annually or annually

Dollar Cost Averaging/Fixed Accounts Dollar Cost Averaging/Fixed Accounts 6-month & 1-year DCA; 1-year Fixed Account option

Nursing home waiver1 Included in contract Included in contract

Optional Feature Early Access: additional 0.40% for the first 4 contract years Reduces standard withdrawal charge schedule to 4 years

Not Applicable

Optional Income Protection Features2

Polaris Income Plus, Polaris Income Builder, and Polaris Income Plus Daily Initial: 1.10% Single Life; 1.35% Joint Life Min: 0.60%; Max: 2.20% Single Life; 2.70% Joint Life

Polaris Income Plus, Polaris Income Builder, and Polaris Income Plus Daily Initial: 1.10% Single Life; 1.35% Joint Life Min: 0.60%; Max: 2.20% Single Life; 2.70% Joint Life

Optional Family Protection Feature Maximum Anniversary Value Death Benefit: 0.25% Max issue age: 80

Maximum Anniversary Value Death Benefit: 0.25% Max issue age: 80

1Not available in all states. Please see prospectus. 2Only one optional income protection feature may be elected at contract issue. Fee rate is guaranteed for one year. After one year, fee rate will be adjusted quarterly based on a pre-determined, non-discretionary formula. Annualized fee calculated as a percentage of the Income Base, deducted from contract value quarterly. The maximum annualized fee rate decrease or increase is 0.25% each quarter. *In New York, Oregon, Texas and Washington, charge will be deducted pro-rata from variable portfolios only. M&E charge deducted from the average daily ending net asset values.

7

Charges, Fees & Important Information

For financial professional use only. Not for use with the public.

Please see the prospectus for details.

Polaris Select Investor “B-share”; 5-year withdrawal charge: 7-7-6-6-5-0%

Polaris Select Investor “C-share”; No surrender charge when feature is elected

Maximum issue age1 85: Standard Death Benefit 75: Return of Premium Death Benefit

85: Standard Death Benefit 75: Return of Premium Death Benefit

Minimum initial investment $25,000 (Non-Qualified and Qualified) $25,000 (Non-Qualified and Qualified)

Minimum addt’l investment2 $500 (NQ and Q) $500 (NQ and Q)

Annualized M&E charge Account Value Death Benefit: 1.10% With Optional Return of Premium Death Benefit: 1.40% (0.30% fee)

Account Value Death Benefit: 1.35% With Optional Return of Premium Death Benefit: 1.70% (0.35% fee)

Annual contract charge $50, waived for contracts of $75,000 or more on contract anniversary.* (Fee may be lower in certain states. Please see prospectus)

$50, waived for contracts of $75,000 or more on contract anniversary.* (Fee may be lower in certain states. Please see prospectus)

Total annual portfolio operating expenses as of 5/31/15 and 12/31/16, respectively

Total portfolio operating expenses: 0.36% to 14.40%** Total portfolio operating expenses: 0.36% to 14.40%**

Free withdrawals during the withdrawal charge period

Greater of: 10% of purchase payments not yet withdrawn each contract year, and still subject to withdrawal charges. Note: if a client is taking their contract’s RMD, any withdrawal charges applicable to such withdrawals are currently waived.

All withdrawals are penalty free

Automatic Asset Allocation Rebalancing Quarterly, semi annually or annually Quarterly, semi annually or annually

Dollar Cost Averaging 6-month & 1-year DCA 6-month & 1-year DCA

Fixed Accounts 1-year Fixed Account option Not available when feature is elected

Nursing home waiver Included in contract (Not available in all states. Please see prospectus.) N/A

Optional Protection Features Not Applicable Not Applicable 1If jointly owned, age is based on the older owner. 2Additional purchase payments will not be accepted on or after the 86th birthday. *In New York, Oregon, Texas and Washington, charge will be deducted pro-rata from variable portfolios only. **Maximum expense shown is subject to a contractual waiver of 13.34%, through 4/30/17, that reduces the fee to 1.06%. M&E charge deducted from the average daily ending net asset values.

Guaranteed Living

Benefits

Note: Guaranteed living benefit features are not available on Polaris Select Investor.

9

Polaris Income Plus®

Polaris Income Builder®

Polaris Income Plus DailySM

Note: If a client elects an optional income protection feature, there are multiple ways to invest. We’ll cover the investment requirements later in this presentation.

A Choice of Income Protection Features

Optional living benefit features are available at contract issue for an additional fee. Age restrictions, investment requirements and other limitations apply. Guarantees are backed by the claims-paying ability of the issuing insurance company. Please see prospectus for complete details regarding Guaranteed Living Benefits.

For financial professional use only. Not for use with the public.

10

Guaranteed Living Benefit Comparison Polaris Income Plus® Polaris Income Builder® Polaris Income Plus DailySM

Issue Ages 45 – 80 65 – 80 45 - 80

Annual Fee (% of Income Base)

1.10% (max. 2.20%) Single Life 1.35% (max. 2.70%) Joint Life

Same Same

Income Credit Period 12 years Same Not Applicable

Income Credit

Gross 6% simple interest annually

Partial Income Credit (Net Income Credit) available in years withdrawals taken during the Income Credit Period provided that withdrawals do not exceed Maximum Annual Withdrawal Amount

Note: The income credit is applied to the Income Base as simple interest and does not increase the Income Credit Base.

Gross 6% simple interest annually

Note: The income credit is applied to the Income Base as simple interest and does not increase the Income Credit Base.

No Income Credit

Contract Value Step-up Frequency (while contract value remains)

Annual (on Contract Anniversary) Annual (on Contract Anniversary)

Daily

Prior to 1st withdrawal: locks in highest daily value in real time

After 1st withdrawal: highest daily value locked in at anniversary (look-back)

Minimum Income Base Guarantee

Minimum Income Base: 200% of the first Benefit Year’s Purchase Payments if no withdrawals have been taken during the first 12 contract years.

Same First Benefit Year’s Purchase Payments, provided withdrawals are taken within the features parameters

High-level Investment Rules

10% Secure Value Account 90% Volatility Control Portfolios

10% Secure Value Account 90% Volatility Control Portfolios

10% Secure Value Account 90% Portfolio Allocator Models, Managed Allocation Portfolios, Asset Allocation Portfolios

For financial professional use only. Not for use with the public.

11

Guaranteed living benefits can provide value to investors, but require consideration of the following:

These features offer lifetime income guarantees, so it is important to understand the client’s long-term investment horizon, risk and fee tolerance, and income requirements. These features carry an additional fee that will impact the performance of the variable annuity and its underlying investments over time. Based on market conditions and/or withdrawal activity, clients may never benefit from the feature. These features have restrictions on investment selection. Withdrawals in excess of the annual withdrawal amount will reduce the value of the benefit, in some cases, by an amount far greater than the withdrawal itself. These features do not accept additional premiums after the 1st contract year. These features provide a guarantee of a series of withdrawals, not a guarantee of principal, account value or a death benefit. Polaris variable annuities can also provide guaranteed income for life without purchasing an optional benefit by electing the lifetime income option when annuitizing the contract. We offer multiple features with different absolute guarantees. It’s important to evaluate each feature and work with your client to determine which may be best suited to their needs.

Important Information

For financial professional use only. Not for use with the public.

Polaris Income Plus® Polaris Income Builder®

For financial professional use only. Not for use with the public.

13

Income Base automatically steps up to lock in greater of investment gains or an annual income credit of up to 6% on contract anniversaries for up to 12 years.

At the end of the first 12 years, clients will continue to have the opportunity to lock in investment gains on contract anniversaries provided contract value remains.

If no withdrawals are taken during the first 12 years, the minimum income base on the 12th contract anniversary is equal to 200% of eligible first-year purchase payments.

If withdrawals of less than 6% of the Income Base are taken within the feature’s parameters, your clients can receive a partial income credit on their next contract anniversary for guaranteed rising income.

The opportunity for guaranteed rising income ends if the contract’s value is completely depleted within the first 12 contract years*.

Minimum issue age 45; maximum issue age 80

Polaris Income Plus®

The Income Base is automatically evaluated on contract anniversaries prior to the Latest Annuity Date provided contract value remains.

*Guaranteed lifetime income payments will cease if the contract value is depleted by excess withdrawals.

Polaris Income Plus is subject to additional fees, age restrictions and other limitations. There is no assurance that withdrawal amounts will keep pace with inflation. In a strong market, clients may pay for this optional feature and not need to use it. If Polaris Income Plus is elected, investment requirements apply, which with Income Options 1, 2 and 3 include an automatic allocation of 10% of each investment to the Secure Value Account (a fixed account with a 1-year term) with the balance to certain designated portfolios described later in this presentation. Please refer to the prospectus for additional information.

For financial professional use only. Not for use with the public.

14

Polaris Income Plus®

With Income Option 3, maximum annual withdrawal percentage is guaranteed for life.

*If the contract value is completely depleted due to market volatility and/or withdrawals taken within the feature’s parameters, clients will receive the protected income payment (PIP). The PIP is calculated as a percentage of the Income Base. If withdrawals begin before age 65 and the Income Base increases due to investment gains on a contract anniversary on or after the 65th birthday, the protected income payment will automatically increase to 4% of the Income Base. In the event your client chooses Income Option 2, but takes withdrawals before age 65, the withdrawal rate will revert to Income Option 1 parameters for withdrawals under age 65. To realize the benefits, clients must take withdrawals within the applicable parameters. Excess withdrawals reduce the Income Base and the Income Credit Base and also reduce the maximum annual withdrawal amount that can be withdrawn under the feature.

For financial professional use only. Not for use with the public.

Clients must choose their desired Income Option at time of contract purchase and the election may not be changed

15

6% income credit on each contract anniversary during the first 12 contract years (income credit available in years withdrawals are not taken).

After the first 12 contract years, clients will continue to have the opportunity to lock in investment gains on contract anniversaries provided contract value remains.*

If no withdrawals are taken during the first 12 years, clients can count on a minimum income base on the 12th contract anniversary that’s equal to 200% of their eligible first-year purchase payments.

Minimum issue age 65; maximum issue age 80.

Note: This feature does not offer guaranteed rising income (no partial income credit is available.

Polaris Income Builder®

For financial professional use only. Not for use with the public.

*The Income Base is automatically evaluated on contract anniversaries prior to the Latest Annuity Date provided contract value remains. Income Builder is subject to additional fees, age restrictions and other limitations. The growth is the opportunity for an increase in the Income Base which is the amount on which guaranteed annual withdrawals are based. There is no assurance that withdrawal amounts will keep pace with inflation. In a strong market, clients may pay for this optional feature and not need to use it. Guarantees, including optional benefits, are backed by the claims-paying ability of the issuing insurance company. If Polaris Income Builder is elected, investment requirements apply, including an automatic allocation of 10% of each investment to the Secure Value Account (a fixed account with a 1-year term). Please refer to the prospectus for additional information.

16

Polaris Income Builder®

With Polaris Income Builder, maximum annual withdrawal percentage is guaranteed for life.

* If the contract value is completely depleted due to market volatility and/or withdrawals taken within the feature’s parameters, clients will receive the protected income payment (PIP). The PIP is calculated as a percentage of the Income Base. To realize the benefits, clients must take withdrawals within the applicable parameters. Excess withdrawals reduce the Income Base and the Income Credit Base and also reduce the maximum annual withdrawal amount that can be withdrawn under the feature.

For financial professional use only. Not for use with the public.

17

How Polaris Income Plus & Income Builder Can Work

Hypothetical illustrations are not to scale and are intended solely to depict how Polaris Income Plus and Income Builder can work. The “Before withdrawals begin” example assumes no withdrawals are taken during the period illustrated. Hypothetical contract value assumes an initial purchase payment at contract issue and no additional purchase payments. Illustrations do not reflect the actual performance of any particular investment. Please see the prospectus for details.

During the first 12 contract years, Income Plus and Income Builder lock in the greater of investment gains or an annual income credit of up to 6% on contract anniversaries for lifetime income. (No partial income credit is available.) The full 6% income credit is available in years that withdrawals are not taken.

For financial professional use only. Not for use with the public.

18

How Polaris Income Plus & Income Builder Can Work

Hypothetical illustrations are not to scale and are intended solely to depict how Polaris Income Plus and Income Builder can work. The “Before withdrawals begin” example assumes no withdrawals are taken during the period illustrated. Hypothetical contract value assumes an initial purchase payment at contract issue and no additional purchase payments. Illustrations do not reflect the actual performance of any particular investment. Please see the prospectus for details.

If no withdrawals occur within the first 12 contract years, the Income Base is guaranteed to be at least 200% of purchase payments received in the first contract year.

For financial professional use only. Not for use with the public.

19

How Polaris Income Plus Can Work

Note: Guaranteed rising income or partial income credits are not available with Polaris Income Builder. Hypothetical illustrations are not to scale and are intended solely to depict how Polaris Income Plus can work. Hypothetical contract value assumes an initial purchase payment at contract issue and no additional purchase payments. Illustrations do not reflect the actual performance of any particular investment. Please see the prospectus for details.

With Polaris Income Plus, if withdrawals are less than 6% of the Income Base and within the feature’s parameters during the first 12 contract years, a partial income credit can be received for guaranteed rising income.

For financial professional use only. Not for use with the public.

Polaris Income Plus DailySM

For financial professional use only. Not for use with the public.

21

A choice of three income options, including one that offers annual withdrawals of up to 7%, depending on a client’s age and when he or she begins taking withdrawals.

Opportunity to capture the highest daily value for retirement income. Prior to the first withdrawal, the Income Base automatically steps up every time the daily contract value is higher than the current Income Base.

After clients begin taking withdrawals, their Income Base can continue to step up on each contract anniversary to lock in the highest daily value during the prior contract year.*

Minimum issue age 45; maximum issue age 80

Polaris Income Plus DailySM

For financial professional use only. Not for use with the public.

* The Income Base is the amount on which guaranteed withdrawals and the annual fee for the feature are based. It is not the same as the contract value; it is not a liquidation value nor is it available as a lump sum.

If no withdrawals have been taken from the contract, the Income Base is increased daily to the Step-up Value (if any). After the first withdrawal has been taken, the Income Base is increased on the next contract anniversary looking back to the Step-Up Value (if any) on each day since the first withdrawal. (This is referred to as the “first look-back.”) After the first look-back, the Income Base is increased on each contract anniversary looking back to the Step-Up Value on each day since the last contract anniversary. The Step-up Value is a value used to determine the Income Base. It is equal to the current contract value if the contract value is higher than the current Income Base. The Step-up Value (if any) is re-determined each day.

Guarantees are backed by the claims-paying ability of the issuing insurance company.

22

Polaris Income Plus DailySM

If clients begin taking withdrawals on or after their 5th contract anniversary and they are at least age 65, OR if they are age 68 or older, the following withdrawal rates apply:

If clients begin taking withdrawals on or after their 5th contract anniversary and they are younger than age 65, the following withdrawal rates apply:

The protected income payment will be paid in the event the contract value is completely depleted due to market volatility and/or withdrawals taken within the feature’s parameters.

For financial professional use only. Not for use with the public.

23

Polaris Income Plus DailySM

If client begins taking withdrawal before the 5th contract anniversary and is age 65 to age 67, the following withdrawal rates apply:

If client begins withdrawal before the 5th contract anniversary and is younger than age 65, the following withdrawal rates apply:

For financial professional use only. Not for use with the public.

24

How Polaris Income Plus Daily SM Can Work

1Based on approximate number of trading days each year for the New York Stock Exchange.

Hypothetical illustrations are not to scale and are intended solely to depict how Polaris Income Plus Daily can work. The “Before withdrawals begin” example assumes no withdrawals are taken during the period illustrated. Hypothetical contract value assumes an initial purchase payment at contract issue and no additional purchase payments. Illustrations do not reflect the actual performance of any particular investment.

Note: This feature can offer your clients income protection for different types of markets. In a rising market, it may offer the benefit of a step-up to the Income Base. In a flat, declining or extended down market, your clients may not receive the benefit of a step-up, but their initial Income Base will remain protected for guaranteed lifetime income. Depending on investment performance and income needs, your clients may not need to rely on this optional insurance feature, which is available at contract issue for an additional annual fee. It is important to note, if the Income Base is increased , it may have the effect of increasing the dollar amount of the feature’s fee. Please see the prospectus for details.

Before withdrawals begin, clients have the potential to capture investment gains to the Income Base for future retirement income 252 times every year1

For financial professional use only. Not for use with the public.

25

How Polaris Income Plus Daily SM Can Work

Hypothetical illustrations are not to scale and are intended solely to depict how Polaris Income Plus Daily can work. Hypothetical contract value assumes an initial purchase payment at contract issue and no additional purchase payments. Illustrations do not reflect the actual performance of any particular investment.

After withdrawals begin, the Income Base can automatically increase on each contract anniversary to lock in client’s highest daily value for rising income.

26

Income Base: The amount on which guaranteed withdrawals and the annual fee for the feature are based. It is not the same as the contract value; it is not a liquidation value nor is it available as a lump sum. The Income Base is initially equal to the first purchase payment. We will not accept purchase payments on or after the first contract anniversary if an income protection feature is elected. If no withdrawals have been taken from the contract, the Income Base is increased daily to the Step-up Value (if any). After the first withdrawal has been taken, the Income Base is increased on the next contract anniversary looking back to the Step-Up Value (if any) on each day since the first withdrawal. (This is referred to as the “first look-back.”) After the first look-back, the Income Base is increased on each contract anniversary looking back to the Step-Up Value on each day since the last contract anniversary. If the contract value has been reduced to zero, the Income Base will no longer be recalculated. The Income Base will be increased each time a purchase payment is made during the first contract year. The Income Base will be adjusted for excess withdrawals.

Step-up Value is a value used to determine the Income Base. It is equal to the current contract value if the contract value is higher than the current Income Base. The Step-up Value (if any) is redetermined each day.

Maximum Annual Withdrawal Amount: The maximum amount of income you can take each year.

Protected Income Payment: The amount of annual income you will receive for life if your contract value is completely depleted due to market volatility and/or withdrawals taken within the feature’s parameters.

To realize the feature’s full benefits, withdrawals must be taken within certain parameters. Withdrawals that exceed the feature’s parameters are known as excess withdrawals. If your clients take an excess withdrawal: 1) The Income Base will be reduced by the amount in excess of the maximum annual withdrawal amount, and 2) Income Plus Daily locks in the highest daily value since the time of the excess withdrawal on the next contract anniversary. If an excess withdrawal reduces the contract value to zero, the feature will terminate and your client will no longer be eligible to take withdrawals or receive lifetime income payments.

There is no assurance that withdrawal amounts will keep up with inflation.

Withdrawals of taxable amounts are subject to ordinary income tax and, if taken prior to age 59½, an additional 10% federal tax may apply. Withdrawals may be subject to withdrawal charges if they exceed certain parameters.

This feature can offer income protection for different types of markets. In a rising market, it may offer the benefit of a step up to the Income Base. In a flat, declining or extended down market, your clients may not receive the benefit of a step-up, but their initial Income Base will remain protected for guaranteed lifetime income. Depending on investment performance and income needs, your clients may not need to rely on this optional insurance feature.

Additional Information

Fees

For financial professional use only. Not for use with the public.

28

Calculation of Fee

For financial professional use only. Not for use with the public.

Historically, the fee for any living benefit has generally been set to cover the ongoing cost of hedging during the entire time a client owns the contract. However, hedging costs continuously change as market volatility moves the cost of the hedges up or down. With our protection-based pricing, the client shares in the cost of hedging when volatility goes up, but clients have the opportunity for a lower fee rate when the cost of hedging goes down.

Fee rate guaranteed for the first year. After the first year, the fee rate will be adjusted quarterly by a rate of 5 basis points annualized for every 1 point

move in the average of all values of the VIX® Volatility Index as reported by the Chicago Board Options Exchange, during the quarter for which the fee is being calculated based on a baseline VIX of 20.

The fee rate can decrease or increase and is subject to a quarterly cap on adjustments and an overall fee rate cap and floor for the life of the contract.

Quarterly fee rate cannot decrease or increase by more than 6.25 basis points from the prior quarter (25 basis points annualized rate).

The fee is calculated as a percentage of the Income Base deducted from contract value quarterly; in New York, the charge will be deducted pro-rata from variable portfolios only.

Polaris Income Plus, Income Builder, and Income Plus Daily share a common fee calculation

Option Initial Fee Rate

Minimum Fee Rate for Life of Contract

Maximum Fee Rate for Life of Contract

Maximum Annualized Fee Rate Decrease/Increase Each Quarter

Single Life 1.10% 0.60% 2.20% 0.25%

Joint Life 1.35% 0.60% 2.70% 0.25%

29

Key points to keep in mind: The VIX generally has had an inverse relationship to the equity

market—expressed by greater volatility in bear markets and lower volatility in bull markets.

Clients are always protected from dramatic temporary swings in volatility by the quarterly cap on the fee rate adjustment and the use of the quarterly average of the VIX in determining each quarter’s fee. Even during the period at the end of 2008 when the market was

experiencing substantial turmoil and the VIX value topped 80, the cap element of the fee structure would have reduced the impact of the large, temporary swing in the VIX index.

Additionally, the fee rate would have returned to a lower level within two quarters.

20-Year Fee Illustration – Single Life

For financial professional use only. Not for use with the public.

Past performance is no guarantee of future results.

30

This illustration helps demonstrate how protection-based pricing would have worked over the period shown.

20-Year Fee Illustration – Single Life

For financial professional use only. Not for use with the public.

Please note that the Polaris Income Plus and Polaris Income Builder features were not available during this entire period (2/20/90-2/20/15). This illustration reflects quarterly fee rate adjustments beginning 05/20/1991, after the one year fee rate guarantee period has ended. Fee rate illustrated is for the Single Life option. Past performance is no guarantee of future results and your clients’ fee rates may be different than those illustrated.

Investment Requirements: - Polaris Income Plus & Income Builder - Polaris Income Plus Daily

For financial professional use only. Not for use with the public.

32

Experienced Money Managers

For financial professional use only. Not for use with the public.

10% of initial and additional investments will need to be allocated to the Secure Value Account, an interest-earning fixed account with a one-year term. 90% of initial and additional investments may be allocated within designated investment limitations determined by the guaranteed living benefit elected. Participation in quarterly automatic asset rebalancing is also required. While certain Polaris portfolios may be similar to other funds managed by the same investment adviser, this does not mean that a portfolio’s investment results will be comparable to the investment results of other similar funds, including other funds with the same investment adviser. There may be material differences between similar funds and the Polaris portfolios, such as fees and expenses, portfolio management, portfolio holdings and the timing of cash flows. The portfolios’ investment results will likely differ, and may be higher or lower than the investment results of other similar funds. 2American Funds SAST Portfolios and the VCP Managed Asset Allocation SAST Portfolio® invest in the American Funds Insurance Series, which has the same investment manager (Capital Research and Management Company) as American Funds. 3Money managers, with the exception of SunAmerica Asset Management, LLC, are not affiliated with American General Life, US Life or American International Group, Inc. (AIG). Money managers and portfolios are subject to change. Please see the prospectus.

33

Investment Requirements

10% of your client’s initial and additional investments will automatically be allocated to the Secure Value Account. The Secure Value Account is a fixed account with a one-year term.

90% of your client’s investment can be invested in one of the following ways:

1. Choose a “Check the Box” Option SunAmerica Dynamic Strategy Portfolio SA BlackRock VCP Global Multi Asset Portfolio VCP Managed Asset Allocation SAST Portfolio

30% 30% 30%

SunAmerica Dynamic Allocation Portfolio SA Schroders VCP Global Allocation Portfolio VCP Value Portfolio

30% 30% 30%

SA T. Rowe Price VCP Balanced Portfolio VCP Total Return Balanced Portfolio SA Schroders VCP Global Allocation Portfolio

30% 30% 30%

SunAmerica Dynamic Allocation Portfolio SA BlackRock VCP Global Multi Asset Portfolio VCP Total Return Balanced Portfolio SA T. Rowe Price VCP Balanced Portfolio

30% 20% 20% 20%

Polaris Income Plus and Income Builder Multiple Ways to Invest: If your clients elect an optional income protection feature, there are multiple ways they can invest their money to meet the associated investment requirements.

For financial professional use only. Not for use with the public.

34

Investment Requirements

2. Or Build a Customized Allocation. Your clients may choose among these options to meet the 90% total allocation:

• SA BlackRock VCP Global Multi Asset Portfolio

• SA Schroders VCP Global Allocation Portfolio

• SA T. Rowe Price VCP Balanced Portfolio

• VCP Managed Asset Allocation SAST Portfolio (Capital Research and Management Company)

• VCP Total Return Balanced Portfolio (PIMCO)

• VCP Value Portfolio (Invesco Advisers, Inc.) The allocation to the options above may not exceed 50% per individual portfolio.

• SunAmerica Dynamic Allocation Portfolio

• SunAmerica Dynamic Strategy Portfolio

• Bond Portfolios: Corporate Bond (Federated Investment Management Company); Global Bond (Goldman Sachs Asset Management International); Government and Quality Bond (Wellington Management Company LLP); Real Return (Wellington Management Company LLP); SA JP Morgan MFS® Core Bond (Multi-managed); Ultra Short Bond Portfolio (Dimensional Fund Advisors LP)

Clients may use a Dollar Cost Averaging (DCA) fixed account to systematically invest in the investment choices available. The target DCA instructions must follow the investment requirements described.

If clients elect the optional income protection feature, participation in quarterly automatic asset rebalancing is also required. Amounts allocated to the Secure Value Account will not be rebalanced and are not available for transfer as long as the feature is in effect. Keep in mind, because rebalancing resets the allocation among variable portfolios, it may have a positive or negative impact on performance.

The investment requirements may reduce the need to rely on an income protection guarantee because they allocate the investment across asset classes and potentially limit exposure to market volatility. Since the Income Base cannot decrease as a result of declines in the market, a volatility management strategy may, under certain market conditions, provide little additional benefit under the feature. Of course, if your clients decide not to elect optional income protection, they may invest in any of the investment options offered in Polaris.

For financial professional use only. Not for use with the public.

Polaris Income Plus and Income Builder

35

Available Volatility Control Portfolios

VCP Managed Asset Allocation SAST Portfolio

A balanced portfolio that provides access to American Funds and diversification among equities (stocks), fixed income (bonds) and money market instruments through the underlying fund in which the Portfolio invests. • Investment goals: Seeks high total return (including income and capital gains) consistent with the preservation of

capital over the long term while seeking to manage volatility and provide downside protection. • Portfolio Management: Capital Research and Management Company; Milliman Financial Risk Management LLC

(subadviser to the Portfolio’s risk-management overlay).

VCP Total Return Balanced Portfolio

A balanced portfolio that leverages the fixed income and equity investment expertise of Pacific Investment Management Company LLC (PIMCO). • Investment goals: Seeks capital appreciation and income while managing portfolio volatility. • Portfolio Management: SunAmerica Asset Management , LLC (investment adviser); Pacific Investment

Management Company LLC (subadviser).

VCP Value Portfolio

A balanced portfolio that capitalizes on the value style investing expertise of Invesco Advisers, Inc. • Investment goals: Seeks current income and moderate capital appreciation while managing portfolio volatility. • Portfolio Management: SunAmerica Asset Management, LLC (investment adviser); Invesco

Advisers,Inc.(subadviser).

VCP Managed Asset Allocation SAST Portfolio: Hedge assets include cash and liquid transparent financial futures contracts that are tailored to the underlying holdings in the American Funds Insurance Series Asset Allocation Fund. Futures contracts on major equity indices, U.S. Treasury bonds, and currencies are typically used. Futures contracts are used only to reduce risk relative to a long-equity portfolio. In situations of extreme market volatility, the exchange-traded futures could potentially reduce the Master Protected Fund’s net economic exposure to equity securities to 0%. The Portfolio is subject to the risk that the strategy that will be used to stabilize the volatility of the Master Fund and reduce its downside exposure may not produce the desired result. In addition, the use of the risk-management overlay may cause the Master Fund’s return to lag that of the underlying fund in certain rising market conditions.

VCP Total Return Balanced Portfolio: The Portfolio may invest a significant portion of its assets in derivatives. As a result, performance could be primarily dependent on securities the Portfolio does not own. The Portfolio will generally achieve equity exposure by investing in derivatives rather than through direct investments in equity securities. The Portfolio may also invest directly in equity securities and ETFs to achieve its goal.

VCP Value Portfolio: The Portfolio’s target volatility level is not a total return performance target. Total return performance is not expected to be within any specified target range. The Portfolio’s ability to achieve current income may be adversely affected if dividends on the Portfolio’s equity securities are reduced or discontinued or if prevailing interest rates on the Portfolio’s debt securities decline. Although the Portfolio seeks investments in undervalued companies, judgments that a particular security is undervalued may prove incorrect.

For financial professional use only. Not for use with the public.

36

Available Volatility Control Portfolios

For financial professional use only. Not for use with the public.

SA BlackRock VCP Global Multi Asset Portfolio

A global tactical asset allocation strategy that actively controls volatility to seek a more consistent investment experience.

• Investment goals: Seeks capital appreciation and income while managing portfolio volatility.

• Portfolio management: SunAmerica Asset Management, LLC (investment adviser); BlackRock Investment Management, LLC (subadviser).

SA Schroders VCP Global Allocation Portfolio

Actively invests across markets and asset classes with the aim to provide growth potential and control volatility.

• Investment goals: Seeks capital appreciation and income while managing portfolio volatility.

• Portfolio management: SunAmerica Asset Management, LLC (investment adviser); Schroder Investment Management North America Inc. (subadviser) .

SA T. Rowe Price VCP Balanced Portfolio

A broadly diversified balanced portfolio, combining the value added from the firm’s expertise in portfolio design, asset allocation and active management with an integrated approach for stabilizing the portfolio’s volatility.

• Investment goals: Seeks capital appreciation and income while managing portfolio volatility.

• Portfolio management: SunAmerica Asset Management, LLC (investment adviser); T. Rowe Price Associates, Inc. (subadviser).

SA BlackRock VCP Global Multi Asset Portfolio: The Portfolio’s volatility management strategy may adjust the composition of the Portfolio’s riskier assets, such as equity and below investment grade fixed income securities, and/or may allocate assets away from riskier assets into cash or short-term fixed income securities. In selecting equity and fixed income investments, judgments that evaluate the attractiveness of countries and sectors may prove incorrect. The value of the Portfolio’s foreign investments may fluctuate due to changes in currency exchange rates.

SA Schroders VCP Global Allocation Portfolio: The Portfolio may make substantial use of derivatives. As a result, performance could be primarily dependent on securities the Portfolio does not own. In selecting equity and fixed income investments, judgments that evaluate the attractiveness of countries and sectors may prove incorrect. The value of the Portfolio’s foreign investments may fluctuate due to changes in currency exchange rates.

SA T. Rowe Price VCP Balanced Portfolio: The Portfolio’s approach for stabilizing volatility may not produce the desired results. The value of the Portfolio’s foreign investments may fluctuate due to changes in currency exchange rates.

37

Investment Requirements - Polaris Income Plus Daily

With Polaris Income Plus Daily, your clients can build a customized allocation using any combination of certain portfolios, including Managed Allocation Portfolios, OR they can choose a Polaris Portfolio Allocator model designed by Morningstar Investment Management LLC.

Clients remain in control of their investment’s allocation and they have the flexibility to change their mix of investments at any time, provided they choose from the available investment options described.

Participation in quarterly automatic asset rebalancing is required.

For financial professional use only. Not for use with the public.

10% Secure Value Account – an interest-earning fixed account with a one-year term

90%

Polaris Portfolio Allocator Model (Model 1, Model 2, Model 3, or Model 4) - OR - Build a Customized Allocation using one or any combination of 24 portfolios listed on the following page

Polaris Income Plus Daily Multiple Ways to Invest: If your clients elect Polaris Income Plus Daily, there are multiple ways they can invest their money in 28 investment options.

38

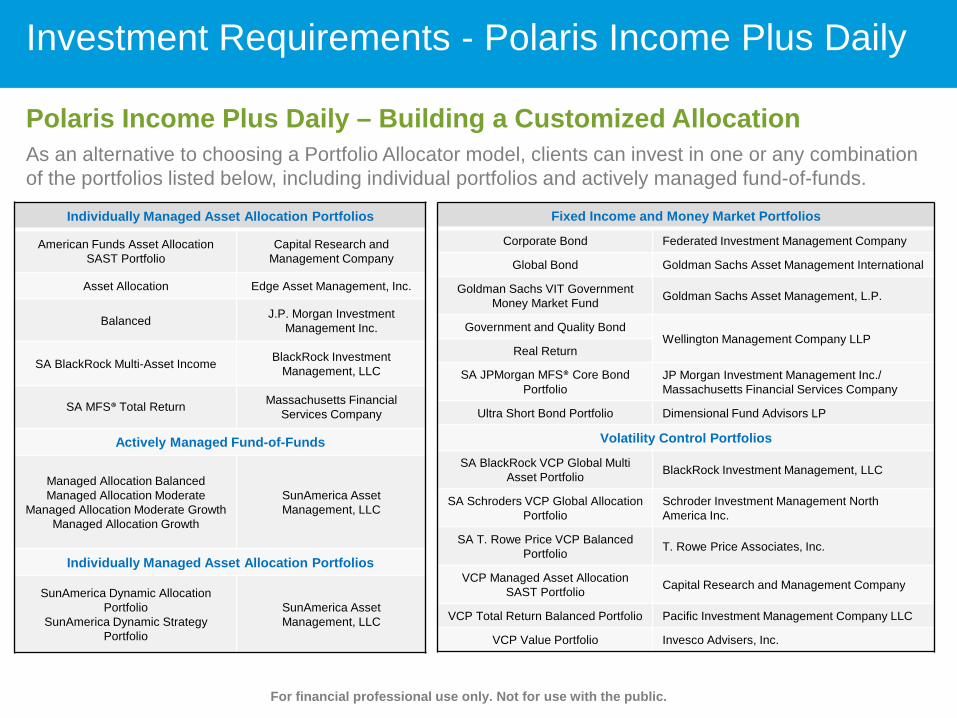

Polaris Income Plus Daily – Building a Customized Allocation As an alternative to choosing a Portfolio Allocator model, clients can invest in one or any combination of the portfolios listed below, including individual portfolios and actively managed fund-of-funds.

For financial professional use only. Not for use with the public.

Investment Requirements - Polaris Income Plus Daily

Individually Managed Asset Allocation Portfolios

American Funds Asset Allocation SAST Portfolio

Capital Research and Management Company

Asset Allocation Edge Asset Management, Inc.

Balanced J.P. Morgan Investment Management Inc.

SA BlackRock Multi-Asset Income BlackRock Investment Management, LLC

SA MFS® Total Return Massachusetts Financial Services Company

Actively Managed Fund-of-Funds

Managed Allocation Balanced Managed Allocation Moderate

Managed Allocation Moderate Growth Managed Allocation Growth

SunAmerica Asset Management, LLC

Individually Managed Asset Allocation Portfolios

SunAmerica Dynamic Allocation Portfolio

SunAmerica Dynamic Strategy Portfolio

SunAmerica Asset Management, LLC

Fixed Income and Money Market Portfolios

Corporate Bond Federated Investment Management Company

Global Bond Goldman Sachs Asset Management International

Goldman Sachs VIT Government Money Market Fund Goldman Sachs Asset Management, L.P.

Government and Quality Bond Wellington Management Company LLP

Real Return

SA JPMorgan MFS® Core Bond Portfolio

JP Morgan Investment Management Inc./ Massachusetts Financial Services Company

Ultra Short Bond Portfolio Dimensional Fund Advisors LP

Volatility Control Portfolios

SA BlackRock VCP Global Multi Asset Portfolio BlackRock Investment Management, LLC

SA Schroders VCP Global Allocation Portfolio

Schroder Investment Management North America Inc.

SA T. Rowe Price VCP Balanced Portfolio T. Rowe Price Associates, Inc.

VCP Managed Asset Allocation SAST Portfolio Capital Research and Management Company

VCP Total Return Balanced Portfolio Pacific Investment Management Company LLC

VCP Value Portfolio Invesco Advisers, Inc.

39

While Volatility Control Portfolios employ risk management processes that seek to manage volatility within the Portfolio, volatility may result from rapid or dramatic price swings. A Portfolio could experience high levels of volatility in both rising and falling markets. Due to market conditions or other factors, the actual or realized volatility of a Portfolio for any particular period of time may be materially higher or lower than the target level. Efforts to manage a Portfolio’s volatility could limit a Portfolio’s gains in rising markets, may expose the Portfolio to costs to which it would otherwise not have been exposed, and if unsuccessful may result in substantial losses.

Each Portfolio is subject to derivative and leverage risks. These investment strategies may be riskier than other investment strategies and may result in gains or losses substantially greater than the cost of the position. While these strategies can be useful and inexpensive ways of reducing risk, they are sometimes ineffective due to unexpected changes in the market, exchange rates or other factors. When a Portfolio uses derivatives for leverage, the Portfolio will tend to be more volatile, resulting in larger gains or losses in response to the fluctuating prices of the Portfolio’s investments.

Each Portfolio is subject to other risks including short sales risk and counterparty risk. Losses from short sales are potentially unlimited, whereas losses from purchases can be no greater than the total amount invested. Counterparty risk is the risk that a counterparty will not perform its obligations. Small movements in interest rates (both increases and decreases) may quickly and significantly reduce the value of certain mortgage-backed securities. These securities are also subject to risk of default, particularly during periods of economic downturn. Credit risk (i.e., the risk that an issuer might not pay interest when due or repay principal at maturity of the obligation) could affect the value of the investments in the Portfolio.

Each Portfolio is subject to risk of conflict with insurance company interests given certain aspects of portfolio management are intended to mitigate the financial risks the insurer faces in connection with optional income protection guarantees.

Certain Portfolios and their underlying portfolios (if applicable) may engage in frequent trading of portfolio securities to achieve their investment goals. Active trading may result in high portfolio turnover and correspondingly greater transaction costs. Investments are subject to certain risks including stock market and interest rate fluctuations, as well as additional risks associated with investments in certain asset classes.

More about Volatility Control Portfolios

For financial professional use only. Not for use with the public.

40

There is no assurance that a Portfolio’s investment process will achieve its specific investment objectives. Portfolios that invest in stocks and bonds are subject to risk, including stock market and interest rate fluctuations.

Portfolios that invest in bonds are subject to changes in their value when prevailing interest rates change. Portfolios that invest in non-U.S. stocks and bonds, including emerging market investments, are subject to additional risks such as political and social instability, differing securities regulations and accounting standards, limited public information, plus special risks that may include foreign taxation, currency risks, risks associated with possible differences in financial standards, and other monetary and political risks associated with future political and economic developments.

Investments that concentrate on one economic sector or geographic region are generally subject to greater volatility than more diverse investments. Portfolios that invest in technology companies are subject to additional risks and may be affected by short product cycles, aggressive pricing, competition from new market entrants and obsolescence of existing technology. Portfolio returns may be considerably more volatile than a portfolio that does not invest in technology companies.

Portfolios that invest in small and mid-size company stocks are generally riskier and more volatile than portfolios that invest in larger, more established companies.

Portfolios that invest in high-yield bonds may be subject to greater price swings than portfolios that invest in higher-rated bonds. The payment of interest and principal is not assured.

Portfolios that invest in real estate investment trusts (REITs) involve risks such as refinancing, economic conditions in the real estate industry, changes in property values, dependency on real estate management, and other risks associated with a concentration in one sector or geographic region.

Investments in securities related to gold and other precious metals and minerals are speculative and impacted by a host of worldwide economic, financial and political factors.

Money market instruments generally offer stability and income, but an investment in these securities, like investments in other portfolios, is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. An investment in the Cash Management portfolio is subject to potential loss of principal; unlike certain money market instruments, it does not seek to maintain a net asset value of $1.

Additional Risks

For financial professional use only. Not for use with the public.

41

Anniversary Value is the contract value on the contract anniversary (including any spousal continuation contributions).

Highest Anniversary Value: The current anniversary value that is greater than: 1) all previous anniversary values, and 2) purchase payments received prior to the first contract anniversary.

Income Base is the amount on which guaranteed withdrawals and the annual fee for the feature are based. It is not a liquidation value nor is it available as a lump sum. The Income Base is initially equal to the first purchase payment. Purchase payments received in the first contract year only will be included in the Income Base. We will not accept purchase payments on or after the first contract anniversary if an income protection feature is elected. On each contract anniversary, the Income Base is set to equal the greater of (a) the highest anniversary value, or (b) the Income Base plus the income credit amount (if eligible) during the income credit period. The Income Base is automatically evaluated on contract anniversaries while the contract value is greater than zero and the feature is still in effect, provided your client has not reached the Latest Annuity Date (95th birthday). On the 12th contract anniversary, the Income Base may be increased to the Minimum Income Base (200% of purchase payments received in the first contract year) if no withdrawals have been taken from the contract. The Income Base will be increased each time a purchase payment is made during the first contract year. The Income Base will be adjusted for excess withdrawals.

Income Credit is the amount that may be added to the Income Base, calculated as a percentage of the Income Credit Base.

Income Credit Base is a component of the feature that is used to calculate the income credit. Initially, the Income Credit Base is equal to the first purchase payment. If the Income Base steps up to the highest anniversary value on a contract anniversary, the Income Credit Base will also step up to this amount. Please note that the Income Credit Base is not increased if the Income Base steps up due to the addition of the income credit. The Income Credit Base will be increased each time a purchase payment is made during the first contract year. The Income Credit Base will be adjusted for excess withdrawals.

Income Credit Period: The period of time over which an income credit may be added to the Income Base. It begins on the contract issue date and ends 12 years later.

Excess Withdrawal: Any withdrawal, or portion of a withdrawal, that exceeds the maximum annual withdrawal amount, which then reduces the Income Base and Income Credit Base proportionately.

Joint Life Option: In the event of a death, spousal continuation must be elected to provide guaranteed income for the lifetime of the remaining spouse. The fee for the Joint Life option will continue to be charged. The Joint Life option will automatically be cancelled if a death benefit is paid and the contract is not continued by the spouse, or if the surviving original spouse dies.

Single Life Option will automatically be cancelled if a death benefit is paid or if the owner (or older owner if jointly owned) dies.

Key Terms & Definitions

For financial professional use only. Not for use with the public.

42

These features may not be appropriate for use with contributory IRAs (IRA, Roth and SEP) or retirement plans and accounts 401 and 457) if clients plan to make ongoing contributions. Purchase payments are only permitted in the first contract year and are included in the Income Base. We will not accept purchase payments on or after the first contract anniversary if an income protection feature is elected. Clients should consult with a tax advisor concerning their particular circumstances.

These features may be cancelled on the 5th contract anniversary, or any contract quarter anniversary after that. Amounts allocated to the Secure Value Account (SVA) will be automatically transferred to the 1-year fixed account, if available. If the 1-year fixed account is not available, the amounts will be transferred to the Ultra Short Bond Portfolio. Once the cancellation becomes effective, the associated fee will no longer be charged going forward. These features cannot be re-elected following cancellation.

Withdrawals Annual withdrawals of up to the maximum annual withdrawal amount (MAWA) do not reduce the Income Base and the Income Credit

Base (if applicable). If clients take a withdrawal that exceeds the MAWA (known as an “excess withdrawal”), their Income Base and Income Credit Base will be reduced proportionately by the amount in excess of the MAWA. In addition, with Polaris Income Plus, an income credit will not be available on the next contract anniversary. (Note: with Polaris Income Builder, an income credit is not available in years any withdrawals are taken.) Excess withdrawals that reduce the Income Base and the Income Credit Base also reduce the MAWA that can be withdrawn under the feature.

If an excess withdrawal reduces the contract value to zero, the feature will terminate and your clients will no longer be eligible to take withdrawals or receive lifetime income payments.

The amount available for withdrawals may change over time. It may increase on contract anniversaries if the Income Base increases, or decrease if your clients take an excess withdrawal that reduces their Income Base. If your clients select Polaris Income Plus, Income Option 1 or 2, and their contract value is completely depleted due to market volatility and/or withdrawals taken within the feature’s MAWA, they will receive the protected income payment. As a result, the amount available for lifetime income will decrease. If your clients select Polaris Income Plus, Income Option 3, or Polaris Income Builder and their contract value is completely depleted due to market volatility and/or withdrawals taken within the feature’s MAWA, the annual amount of lifetime income will not change; annual income paid to your clients after this point is simply referred to as the protected income payment.

If your clients have elected an income protection feature, withdrawals up to the MAWA are free of withdrawal charges. Withdrawals that exceed the MAWA may be subject to a withdrawal charge.

Partial withdrawals reduce other benefits available under the contract, such as the death benefit, as well as the amount available upon surrender. If your clients elect Polaris Income Plus and take withdrawals during the first 12 contract years that reduce or eliminate the available income credit, future income may be lower than if a partial or full income credit was added to the Income Base. If your clients elect Polaris Income Builder and take withdrawals during the first 12 contract years, future income may be lower than if they had waited to take withdrawals and an income credit was added to the Income Base.

Key Terms & Definitions

For financial professional use only. Not for use with the public.

Investing with Polaris

Without the election of a Guaranteed Living Benefit rider

44

Investing with Polaris

For financial professional use only. Not for use with the public.

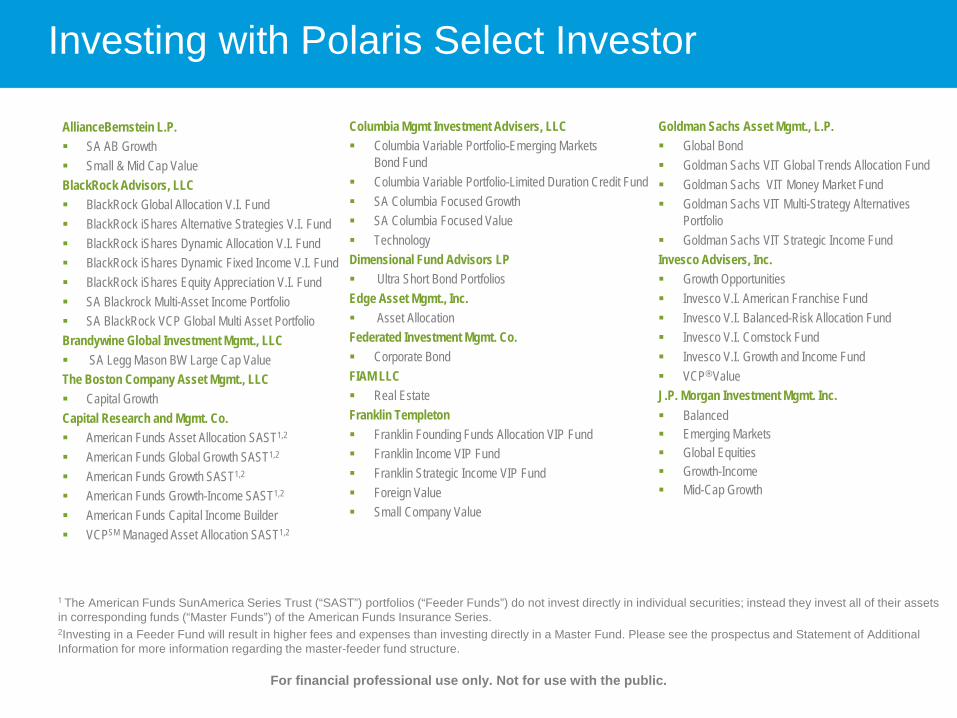

AllianceBernstein L.P. SA AB Growth Small & Mid Cap Value The Boston Company Asset Mgmt., LLC Capital Growth BlackRock Investment Mgmt., LLC SA BlackRock Multi-Asset Income

Portfolio SA BlackRock VCP Global Multi Asset

Portfolio Brandywine Global Investment Mgmt., LLC SA Legg Mason BW Large Cap Value Capital Research and Mgmt. Co. American Funds Asset Allocation SAST1 American Funds Global Growth SAST1

American Funds Growth SAST1

American Funds Growth-Income SAST1

VCP Managed Asset Allocation SAST1, 2

Goldman Sachs Asset Mgmt. Global Bond Goldman Sachs VIT Gov’t. Money

Market Fund Invesco Advisers, Inc. Growth Opportunities Invesco V.I. American Franchise Fund

Invesco V.I. Comstock Fund

Invesco V.I. Growth and Income Fund

VCPSM Value

J.P. Morgan Inv. Mgmt. Inc. Balanced Emerging Markets Global Equities Growth-Income Mid-Cap Growth Lord Abbett & Co. LLC Lord Abbett Growth and Income

1 American Funds SAST Portfolios and the VCP Managed Asset Allocation SAST Portfolio invest in the American Funds Insurance Series, which has the same investment manager (Capital Research and Management Company) as American Funds. The American Funds SunAmerica Series Trust (SAST) portfolios (Feeder Funds) do not invest directly in individual securities; instead they invest all of the assets in corresponding funds ("Master Funds") of the American Funds Insurance Series ("AFIS"). Investing in a Feeder Fund will result in higher fees and expenses than investing directly in a Master Fund. Please see the prospectus and Statement of Additional Information for more information regarding the master-feeder fund structure. 2 The VCP Managed Asset Allocation SAST Portfolio (“Feeder Fund”) does not invest directly in individual securities; instead it invests in shares of the American Funds Insurance Series® Managed Risk Asset Allocation FundSM (the “Master Fund”). In turn, the Master Fund invests in shares of an underlying fund, the American Funds Insurance Series®

Asset Allocation Fund (the “Underlying Fund”), hedge instruments (primarily exchange-traded futures) and cash or cash equivalents. Investing in a Feeder Fund will result in higher fees and expenses than investing in a portfolio that invests directly in securities. Financial Services Company.

Columbia Mgmt. Investment Advisers, LLC Technology Dimensional Fund Advisors L.P. Ultra Short Bond Portfolio Edge Asset Mgmt., Inc. Asset Allocation Federated Investment Mgmt. Co. Corporate Bond FIAM LLC Real Estate Franklin Templeton Foreign Value Franklin Income VIP Fund Franklin Founding Funds Allocation

VIP Fund Small Company Value

45

Investing with Polaris

For financial professional use only. Not for use with the public.

Marsico Capital Mgmt., LLC SA Marsico Focused Growth Massachusetts Financial Services Company Blue Chip Growth SA MFS® Massachusetts Investors Trust SA MFS® Total Return Telecom Utility Morgan Stanley Investment Mgmt. Inc. International Diversified Equities OppenheimerFunds, Inc. Equity Opportunities Pacific Investment Mgmt. Co., LLC VCP Total Return BalancedSM

PineBridge Investments LLC High-Yield Bond Putnam Investment Mgmt., LLC Int’l Growth and Income Schroder Investment Mgmt. North America Inc. SA Schroders VCP Global Allocation Portfolio

3 The overall portfolio’s average level of exposure to the equity market is expected to be approximately 60% to 65% over the long term. However, the exposure will range from a minimum of 25% to a maximum of 100%. 4 SA JPMorgan MFS Core Bond Portfolio is subadvised by J.P. Morgan Investment Management Inc. and Massachusetts Financial Services Company.

SunAmerica Asset Mgmt., LLC “Dogs” of Wall Street SunAmerica Dynamic Allocation Portfolio3

SunAmerica Dynamic Strategy Portfolio3

T. Rowe Price SA T. Rowe Price VCP Balanced Portfolio Wellington Mgmt. Company LLP Capital Appreciation Government and Quality Bond Growth Natural Resources Real Return Wells Capital Mgmt. Incorporated Aggressive Growth Fundamental Growth Multi- Managed SA JPMorgan MFS Core Bond4

46

Polaris Portfolio Allocator Models1, 2

• Four Morningstar Investment Management-designed asset allocation models, available at no additional cost.

• Each Polaris Portfolio Allocator model is designed to meet specific investment goals.

• The models range from lower risk and reward potential (Model 1) to higher risk and reward potential (Model 4).

Investing with Polaris

For financial professional use only. Not for use with the public.

1 Polaris Portfolio Allocator should not be relied upon as providing individualized investment recommendations. The models are considered “static” because the portfolios and the percentages of contract value allocated to each portfolio within a model will not be changed by us. To maintain the target asset allocation of a model, your client can elect to have their investment rebalanced quarterly, semiannually, or annually. Please note that due to market returns and other factors, over time the asset allocation models may no longer align with their original investment objective. Once your client invests in a model, their investment will not be updated yearly unless you contact us with new instructions. 2 All four of the models are available with Polaris Income Plus Daily, or if your client chooses not to elect an optional income protection feature.

The Polaris Portfolio Allocator models and Investor Questionnaire are designed and licensed by Morningstar Investment Management LLC (“Morningstar"). These materials are provided for educational purposes only and should not be considered investment advice. Morningstar does not endorse and/or recommend specific financial products that may be used in conjunction with the models and questionnaire.

Death Benefits

For financial professional use only. Not for use with the public.

48

Standard Death Benefit Available at no additional charge.

Maximum Anniversary Value Optional benefit, available for an additional fee of 0.25%.1

“Locks in” highest contract anniversary value prior to 83rd birthday.

Spousal Continuation Allows for step up to the death benefit value if spousal joint owner

or spousal beneficiary continues contract upon death of original owner.

Death Benefits

For financial professional use only. Not for use with the public.

Certain features are optional and available at contract issue for an additional fee. Guarantees are backed by the claims-paying ability of the issuing insurance company. 1 Annualized fee deducted from the average daily ending net asset values.

49

This standard option is automatically provided if an optional death benefit is not elected and: Provides beneficiaries the greater of:

– Contract value at death, – Net purchase payments (defined as total purchase payments,

adjusted for withdrawals).

Maximum issue age is 85.

Death Benefits – Standard Return of Principal

For financial professional use only. Not for use with the public.

Guarantees are backed by the claims-paying ability of the issuing insurance company.

When calculating the standard or enhanced death benefit value, adjustments are made to account for withdrawals, any charges applicable to withdrawals and additional purchase payments. The calculation will differ if the client has elected an income protection option. Please see the prospectus for details.

50

Optional feature that “locks in” the highest contract anniversary value prior to the client’s 83rd birthday, adjusted for withdrawals.

Provides beneficiaries with the greatest of: Contract value at death, Net purchase payments (defined as total purchase payments,

adjusted for withdrawals), or The maximum anniversary value before their 83rd birthday

(adjusted for any withdrawals since that anniversary), plus any net purchase payments received after that anniversary. Net purchase payments are defined as total purchase payments, adjusted for withdrawals.

Maximum issue age for this option is 80.

Death Benefits – Maximum Anniversary Value

For financial professional use only. Not for use with the public.

When calculating the standard or enhanced death benefit value, adjustments are made to account for withdrawals, any charges applicable to withdrawals and additional purchase payments. The calculation will differ if the client has elected an income protection option. Please see the prospectus for details.

Product-Specific Training – Polaris Select Investor Variable Annuity

For financial professional use only. Not for use with the public.

52

With Polaris Select Investor Variable Annuity – an investment-focused variable annuity, clients can seek to meet their investment objectives by choosing from a wide array of investment options using one of these different approaches: 1. Build a customized allocation

• With 90+ investment choices, clients can select from a wide range of investments from 30+ experienced money managers and more than 22 distinct asset classes.

2. Diversify with an asset allocation model • The Polaris Portfolio Allocator models are designed by Morningstar Investment

Management LLC to help clients take advantage of the potential benefits of asset allocation.

3. Pick from Select Strategies that include alternative investments • The Select Strategies, designed by SunAmerica Asset Management, LLC

(SAAMCo) combine a pre-selected allocation of six alternative portfolios with a corresponding Polaris Portfolio Allocator model.

Investing with Polaris Select Investor

For financial professional use only. Not for use with the public.

53

Experienced Money Managers

For financial professional use only. Not for use with the public.

Money managers and portfolios are subject to change. Please see the prospectus. 3American Funds SAST Portfolios and the VCP Managed Asset Allocation SAST Portfolio® invest in the American Funds Insurance Series, which has the same investment manager (Capital Research and Management Company) as American Funds. 4A Waddell & Reed investment management company. While certain portfolios offered in Polaris Select Investor may be similar to other funds managed by the same investment adviser, this does not mean that a portfolio’s investment results will be comparable to the investment results of other similar funds, including other funds with the same investment adviser. There may be material differences between similar funds and the Polaris portfolios, such as fees and expenses, portfolio management, portfolio holdings and the timing of cash flows. The portfolios’ investment results will likely differ, and may be higher or lower than the investment results of other similar funds. Money managers, with the exception of SunAmerica Asset Management, LLC and VALIC, are not affiliated with American General Life, US Life or American International Group, Inc. (AIG). Money managers and portfolios are subject to change. Please see the prospectus.

54

Multiple Asset Classes

For financial professional use only. Not for use with the public.

Equity Fixed Income/Cash Asset Allocation Large Growth Money Market Traditional

Large Core Short-Term Bond Income-Oriented

Large Value Inflation Protected Securities Risk-Managed

Small and Mid-Cap Growth Corporate Govt. Bond Tactical

Small and Mid-Cap Core High-Yield Bond Multi-Alternatives

Small and Mid-Cap Value Foreign and Global Bond

Multi-Cap Multi-Sector/Non-Traditional Bond

Specialty

Foreign and Global Stock

Emerging Markets

55

Investing with Polaris Select Investor

For financial professional use only. Not for use with the public.

AllianceBernstein L.P. SA AB Growth Small & Mid Cap Value BlackRock Advisors, LLC BlackRock Global Allocation V.I. Fund BlackRock iShares Alternative Strategies V.I. Fund BlackRock iShares Dynamic Allocation V.I. Fund BlackRock iShares Dynamic Fixed Income V.I. Fund BlackRock iShares Equity Appreciation V.I. Fund SA Blackrock Multi-Asset Income Portfolio SA BlackRock VCP Global Multi Asset Portfolio Brandywine Global Investment Mgmt., LLC SA Legg Mason BW Large Cap Value The Boston Company Asset Mgmt., LLC Capital Growth Capital Research and Mgmt. Co.

American Funds Asset Allocation SAST1,2 American Funds Global Growth SAST1,2

American Funds Growth SAST1,2

American Funds Growth-Income SAST1,2

American Funds Capital Income Builder VCPSM Managed Asset Allocation SAST1,2

Columbia Mgmt Investment Advisers, LLC Columbia Variable Portfolio-Emerging Markets

Bond Fund Columbia Variable Portfolio-Limited Duration Credit Fund SA Columbia Focused Growth SA Columbia Focused Value Technology Dimensional Fund Advisors LP Ultra Short Bond Portfolios Edge Asset Mgmt., Inc. Asset Allocation Federated Investment Mgmt. Co. Corporate Bond FIAM LLC Real Estate Franklin Templeton Franklin Founding Funds Allocation VIP Fund Franklin Income VIP Fund Franklin Strategic Income VIP Fund Foreign Value Small Company Value

Goldman Sachs Asset Mgmt., L.P. Global Bond Goldman Sachs VIT Global Trends Allocation Fund Goldman Sachs VIT Money Market Fund Goldman Sachs VIT Multi-Strategy Alternatives

Portfolio Goldman Sachs VIT Strategic Income Fund Invesco Advisers, Inc. Growth Opportunities Invesco V.I. American Franchise Fund

Invesco V.I. Balanced-Risk Allocation Fund

Invesco V.I. Comstock Fund

Invesco V.I. Growth and Income Fund

VCP® Value

J.P. Morgan Investment Mgmt. Inc. Balanced Emerging Markets Global Equities Growth-Income Mid-Cap Growth

1 The American Funds SunAmerica Series Trust (“SAST”) portfolios (“Feeder Funds”) do not invest directly in individual securities; instead they invest all of their assets in corresponding funds (“Master Funds”) of the American Funds Insurance Series. 2Investing in a Feeder Fund will result in higher fees and expenses than investing directly in a Master Fund. Please see the prospectus and Statement of Additional Information for more information regarding the master-feeder fund structure.

56

Investing with Polaris Select Investor

For financial professional use only. Not for use with the public.

Lord Abbett & Co. LLC Lord Abbett Bond Debenture Lord Abbett Fundamental Equity Lord Abbett Growth and Income Lord Abbett Short Duration Income

Marsico Capital Mgmt., LLC SA Marsico Focused Growth Massachusetts Financial Services Company Blue Chip Growth SA MFS® Massachusetts Investors Trust SA MFS® Total Return Telecom Utility Morgan Stanley Investment Mgmt. Inc. International Diversified Equities Morgan Stanley UIF Global Infrastructure Portfolio Neuberger Berman Neuberger Berman AMT Absolute Return

Multi-Manager Portfolio OppenheimerFunds, Inc. Equity Opportunities Pacific Investment Mgmt. Co., LLC PIMCO All Asset Portfolio PIMCO Emerging Markets Bond Portfolio PIMCO Unconstrained Bond Portfolio VCP Total Return Balanced® Portfolio

PineBridge Investments LLC High-Yield Bond Putnam Investment Mgmt., LLC Asset Allocation: Diversified Growth Int’l Growth and Income Schroder Investment Mgmt. North America Inc. SA Schroders VCP Global Allocation Portfolio SunAmerica Asset Mgmt., LLC “Dogs” of Wall Street Managed Allocation Balanced Managed Allocation Growth Managed Allocation Moderate Managed Allocation Moderate Growth VALIC Company I Global Social Awareness Fund VALIC Company I International Equities Index Fund VALIC Company I Mid Cap Index Fund VALIC Company I Nasdaq-100 Index Fund VALIC Company I Small Cap Index Fund VALIC Company I Stock Index Fund T. Rowe Price Associates, Inc. SA T. Rowe Price VCP Balanced Portfolio Stock Waddell & Reed Investment Mgmt. Company IVY Funds VIP Asset Strategy

Wellington Mgmt. Company, LLP Capital Appreciation Government and Quality Bond Growth Natural Resources Real Return Wells Capital Mgmt. Incorporated Aggressive Growth Fundamental Growth Multi-Managed Diversified Fixed Income International Equity Large Cap Growth Large Cap Value Mid Cap Growth Mid Cap Value SA JPMorgan MFS Core Bond Small Cap SunAmerica Dynamic Allocation Portfolio®

SunAmerica Dynamic Strategy Portfolio®

57

Polaris Portfolio Allocator Models1, 2

Four Morningstar Investment Management-designed asset allocation models, available at no additional cost.

Each Polaris Portfolio Allocator model is designed to meet specific investment goals. The models range from lower risk and reward potential (Model 1) to

higher risk and reward potential (Model 4).

Investing with Polaris Select Investor

For financial professional use only. Not for use with the public.

1 Polaris Portfolio Allocator should not be relied upon as providing individualized investment recommendations. The models are considered “static” because the portfolios and the percentages of contract value allocated to each portfolio within a model will not be changed by us. To maintain the target asset allocation of a model, your client can elect to have their investment rebalanced quarterly, semiannually, or annually. Please note that due to market returns and other factors, over time the asset allocation models may no longer align with their original investment objective. Once your client invests in a model, their investment will not be updated yearly unless you contact us with new instructions. 2 All four of the models are available if your client chooses not to elect an optional income protection feature.

The Polaris Portfolio Allocator models and Investor Questionnaire are designed and licensed by Morningstar Investment Management LLC (“Morningstar"). These materials are provided for educational purposes only and should not be considered investment advice. Morningstar does not endorse and/or recommend specific financial products that may be used in conjunction with the models and questionnaire.

58

Select Strategies

Four Select Strategies designed by SunAmerica Asset Management , LLC (SAAMCo) offer the option to add alternatives to a client’s investment.

Each of the Select Strategies allocates 70% of a client’s investment in one of the four corresponding Polaris Portfolio Allocator Models and 30% in a pre-set allocation of alternative funds.

Investing with Polaris Select Investor

For financial professional use only. Not for use with the public.