Noranda Income Fund Annual Report 2016 EN.pdfNoranda Income Fund (TSX: NIF.UN) is the responsibility...

85

Noranda Income Fund Annual Report 2016

Transcript of Noranda Income Fund Annual Report 2016 EN.pdfNoranda Income Fund (TSX: NIF.UN) is the responsibility...

Noranda Income Fund Annual Report 2016

1

Table of contents Management’s Discussion and Analysis 2

Interim Condensed Consolidated Financial Statements 37

2

Noranda Income Fund Management’s Discussion and Analysis

December 31, 2016

3

MANAGEMENT’S DISCUSSION AND ANALYSIS

This Management’s Discussion and Analysis (“MD&A”) of the financial position and results of operations of Noranda Income Fund (TSX: NIF.UN) is the responsibility of management and it has been prepared as at February 28, 2017. The board of trustees of Noranda Operating Trust carries out its responsibility by reviewing this disclosure principally through its Audit Committee and it approves this disclosure prior to its publication. This MD&A provides a review of the consolidated financial position, results of operations and performance of Noranda Income Fund (the “Fund”), Noranda Operating Trust (the “Operating Trust”), 1884699 Ontario Inc. (“Ontario Inc.”), Canadian Electrolytic Zinc Limited (the “Manager” and, alternatively, the “Administrator”) and Noranda Income Limited Partnership (the “Partnership”) for the years ended December 31, 2016 and 2015. The Partnership owns an electrolytic zinc plant and processing facility (the “Processing Facility”). The Processing Facility produces refined zinc metal and various by-products from zinc concentrate purchased from mining operations and sells refined zinc products to customers in the open market. The Fund earns a processing fee for transforming zinc concentrate into zinc metal and it earns additional revenue from premiums, by-product revenues and metal gains. See “Net Revenues under Market Terms” below. The Processing Facility is located in the town of Salaberry-de-Valleyfield, Quebec, approximately 70 kilometres southwest of Montreal, on a site situated on the St. Lawrence Seaway along major transportation networks which connect it to its principal markets in the United States and Canada. Zinc is central to our daily lives. Its main use is to galvanize steel for the construction and automotive industries. Zinc is also used in the production of die-castings and brass. Zinc powders, oxide and dust are used in the manufacture of batteries, rubber tires, pigments and various creams. The Fund has prepared its audited Consolidated Financial Statements for the years ended December 31, 2016 and 2015 in accordance with International Financial Reporting Standards (“IFRS”). The MD&A should be read in conjunction with these statements. All amounts are expressed in Canadian dollars, the Fund’s reporting and functional currency, except where indicated. Additional information relating to the Fund, including the Fund’s Annual Information Form dated March 28, 2016 is available on SEDAR at www.sedar.com.

This MD&A contains forward-looking information and forward-looking statements within the meaning of applicable securities laws. See “Forward-Looking Information” below. 2016 Highlights

Glencore Canada renewed the Supply and Processing Agreement to May 2022, with the current fixed processing fee ending May 3, 2017 and continuing on market terms thereafter.

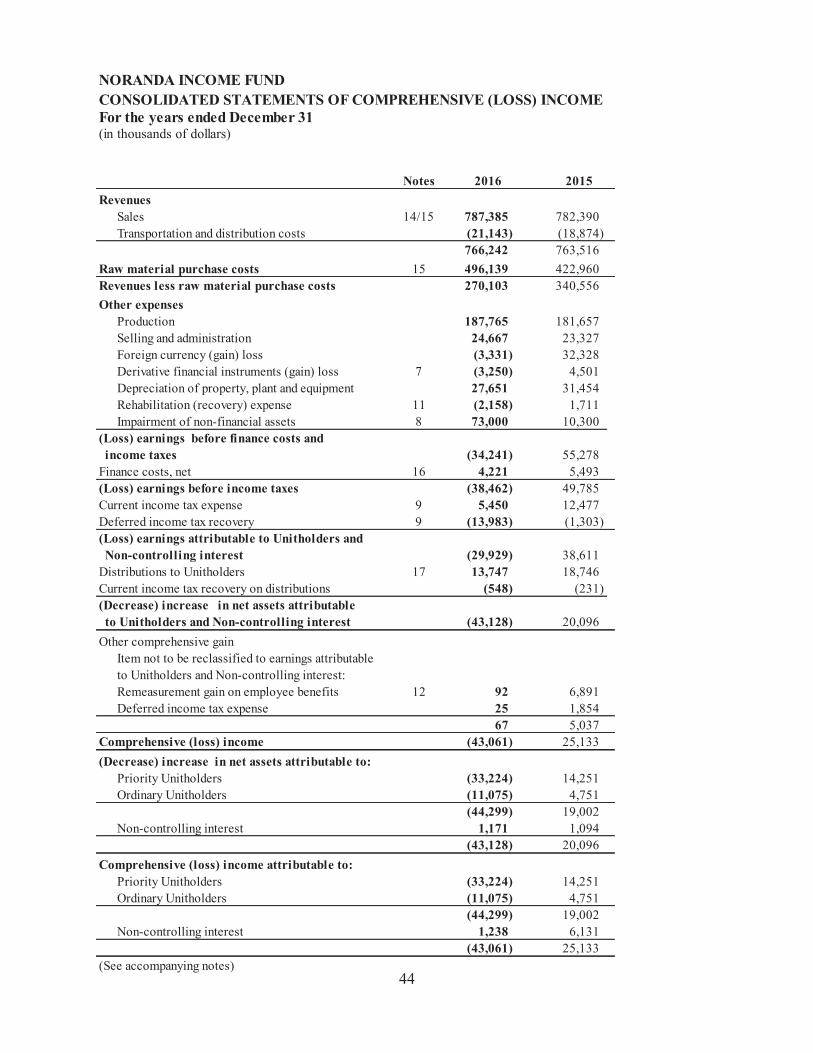

The Fund repaid the remaining $22.5 million of Senior Secured Notes in 2016. The Fund’s asset-based revolving credit facility (the “ABL Facility”) was extended to November 15, 2017. Zinc metal sales increased 4% to 273,052 tonnes in 2016, in line with the Fund’s target for the year. Adjusted Net Revenues1 for 2016 was $285.8 million, down 5% from $301.0 million for 2015. Production costs per tonne of zinc produced for 2016 were down 2% from 2015. Loss before income taxes of $38.5 million in 2016, compared to earnings before income taxes of $49.8

million in 2015, due largely to non-cash asset impairment charges of $73 million recorded in 2016. The year-over-year decline in earnings was also due to lower zinc metal premiums and lower sulphuric acid

1 Adjusted Net Revenues means revenues less raw material purchase costs (“Net Revenues”) excluding unrealized concentrate settlement adjustments and after foreign exchange gain/loss and derivative financial instruments gain/loss. Net Revenues is reconciled to Adjusted Net Revenues below.

4

revenues partially offset by a weaker average Canadian dollar in 2016 compared to the US dollar, lower depreciation and reclamation, higher zinc metal sales and lower unit production costs.

Zinc metal production increased 2% to 277,022 tonnes in 2016, exceeding the Fund’s target for the year.

Highlights Subsequent to Year ended December 31, 2016

Glencore Canada and the Fund reached an agreement whereby Glencore will supply all of the Processing Facility’s zinc concentrate requirements and purchase all the zinc metal production for the 12 month period ending April 30, 2018.

In light of the prevailing market conditions now facing the Fund, the Board of Trustees announced the suspension of future monthly distributions to unitholders on January 31, 2017.

On February 12, 2017, unionized workers initiated a strike at the Processing Facility. In response to the strike, management secured the operations in the days following and has resumed partial production with staff operating the facility. Management is in the process of evaluating its production capacity under this scenario. The Fund has attempted to minimize the impact on customers by shipping inventory and new production.

OVERVIEW

Business and Agreement Overview The Fund is an unincorporated open-ended trust, established under the laws of Ontario, whose priority units (the “Priority Units”) trade on the Toronto Stock Exchange (“TSX”) under the symbol “NIF.UN”. The Manager, a wholly-owned subsidiary of Glencore Canada, operates and manages the Operating Trust and the Partnership, and administers the Fund. The board of trustees of the Operating Trust (the “Board” or the “Trustees”), the majority of whom are independent from Glencore Canada (the “Independent Committee”), oversees the Fund. The Fund is, in turn, the sole unitholder of the Operating Trust. The Fund was created to acquire the Processing Facility, located in Salaberry-de-Valleyfield, Québec, from Noranda Inc.2 in 2002. Concurrently with the creation of the Fund and the acquisition of the Processing Facility, the Manager entered into various 15-year agreements with the Fund and/or the Operating Trust relating to the management, administration and operation of the Fund, the Operating Trust, the Partnership and the Processing Facility. The initial term of the agreements will expire on May 2, 2017. The agreements have been renewed for a five-year term ending May 2, 2022 at market terms and will automatically renew for five-year terms thereafter, unless Glencore Canada provides written notice to the contrary at least 180 days prior to the expiry of the applicable term. Upon the termination of the operating and management agreement, the Partnership is required to acquire the Manager from Glencore Canada. The agreements include:

a) An administration agreement dated April 18, 2002 between the Fund and the Administrator (the “Administration Agreement”) pursuant to which Computershare Trust Company of Canada, the sole trustee of the Fund (the “Sole Trustee”), has delegated all of its power and authority to the Administrator, and the Administrator provides administrative and support services to the Fund.

b) A management services agreement dated April 18, 2002 between the Operating Trust and the Manager (the

“Management Services Agreement”) pursuant to which the Manager provides management services to the Operating Trust.

2 On June 30, 2005, Noranda Inc. changed its name to Falconbridge Limited (“Falconbridge”) following a corporate amalgamation. Falconbridge subsequently changed its name to Xstrata Canada Corporation (“Xstrata Canada”) after being acquired by Xstrata plc. In May 2013, Glencore International plc completed its merger with Xstrata plc with the combined company now called Glencore plc (“Glencore”). Xstrata Canada changed its name to Glencore Canada following the merger. The Manager is a wholly-owned subsidiary of Glencore Canada.

5

c) An operating and management agreement dated May 3, 2002 between the Manager and the Partnership (the “O&M Agreement”) pursuant to which the Manager operates and maintains on an ongoing basis the Processing Facility owned by the Partnership and provides management services to the Partnership.

d) The supply and processing agreement dated May 3, 2002 between Glencore Canada and the Partnership

(the “Supply and Processing Agreement”) under which Glencore Canada is obligated, except in certain circumstances, to sell to the Partnership until May 2, 2017 all of its zinc concentrate requirements up to 550,000 tonnes of zinc concentrate per year at a concentrate price based on the price of zinc metal on the London Metal Exchange (“LME”) for the “payable zinc metal” contained in the concentrate, less a fixed, escalating processing fee (calculated in Canadian dollars). Pursuant to the Supply and Processing Agreement, Glencore Canada acts as exclusive agent for the Partnership to arrange for purchases of any additional zinc concentrate in excess of the 550,000 tonne amount described above, and for sales of zinc metal and by-products and related hedging and derivative arrangements.

Supply of Zinc Concentrate beyond May 2, 2017

On May 3, 2017, the Supply and Processing Agreement will be automatically renewed for a period of five years through May 2, 2022. Under the renewal term, commencing on May 3, 2017, Glencore Canada will arrange, as agent on behalf of the Fund, for the purchase of the zinc concentrate required by the Fund at market terms. Glencore Canada will continue to act as agent for the sales of zinc metal and by-products and related hedging and derivative arrangements. The transition to market terms will represent a significant change from the fixed processing fee the Fund has benefited from since its inception. As a result of the change to market terms, the Fund’s financial results will differ materially in the future, beginning in the second quarter of 2017. Glencore Canada will continue to act as Manager of Noranda Operating Trust and of the Partnership and as Administrator of the Fund, in accordance with the Operating and Management Agreement, the Management and Services Agreement and the Administration Agreement, respectively, which have all been extended for a period of five years ending on May 2, 2022.

On January 31, 2017, the Fund announced that it had reached an agreement pursuant to which Glencore Canada will supply the Fund with all of its zinc concentrate requirements and purchase all of the Fund’s metal for the twelve month period ending April 30, 2018 on a principal basis. See “Outlook for the Fund” below. Further details concerning these arrangements relating to the management, administration and operation of the Fund and its subsidiaries, and the supply and processing of concentrate at the Processing Facility are described under “Related Party Transactions” below. Net Revenues under Market Terms As noted above, the Fund will pay market prices for the zinc concentrate that it purchases after the expiry of the initial term of the Supply and Processing Agreement on May 2, 2017. As a result, the Fund expects the make-up of Net Revenues to be different going forward. Treatment Charges vs. Processing Fees The principal factor affecting the Fund’s performance will continue to be the processing of zinc concentrate into zinc metal. The change to market prices will result in the Fund earning treatment charges that are similar in nature to the processing fees currently being earned in that they are generated from the processing of zinc concentrate into zinc metal. However, unlike the current processing fees, these treatment charges will fluctuate with market conditions and will be priced in US dollars per dry metric tonne of feed, instead of Canadian dollars per pound of zinc payable. Treatment charges are also expected to make up a smaller portion of Net Revenues compared to the current processing fee because of the zinc metal recovery gain described below.

6

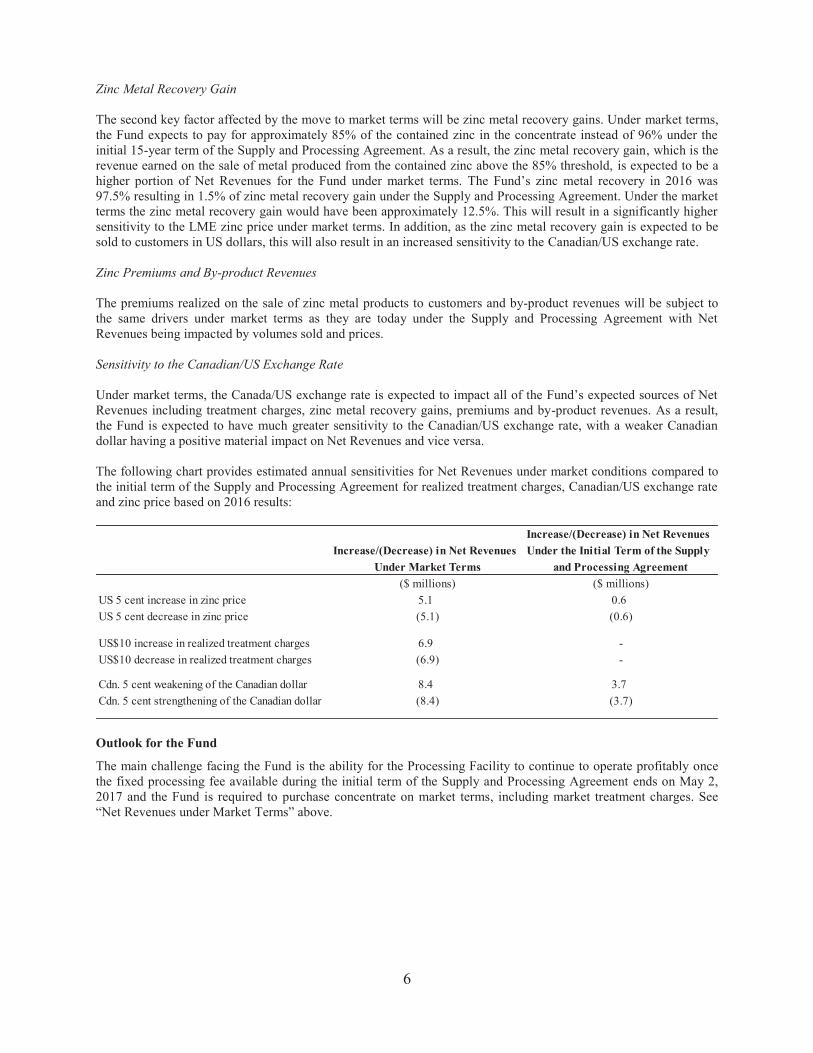

Zinc Metal Recovery Gain The second key factor affected by the move to market terms will be zinc metal recovery gains. Under market terms, the Fund expects to pay for approximately 85% of the contained zinc in the concentrate instead of 96% under the initial 15-year term of the Supply and Processing Agreement. As a result, the zinc metal recovery gain, which is the revenue earned on the sale of metal produced from the contained zinc above the 85% threshold, is expected to be a higher portion of Net Revenues for the Fund under market terms. The Fund’s zinc metal recovery in 2016 was 97.5% resulting in 1.5% of zinc metal recovery gain under the Supply and Processing Agreement. Under the market terms the zinc metal recovery gain would have been approximately 12.5%. This will result in a significantly higher sensitivity to the LME zinc price under market terms. In addition, as the zinc metal recovery gain is expected to be sold to customers in US dollars, this will also result in an increased sensitivity to the Canadian/US exchange rate. Zinc Premiums and By-product Revenues The premiums realized on the sale of zinc metal products to customers and by-product revenues will be subject to the same drivers under market terms as they are today under the Supply and Processing Agreement with Net Revenues being impacted by volumes sold and prices. Sensitivity to the Canadian/US Exchange Rate Under market terms, the Canada/US exchange rate is expected to impact all of the Fund’s expected sources of Net Revenues including treatment charges, zinc metal recovery gains, premiums and by-product revenues. As a result, the Fund is expected to have much greater sensitivity to the Canadian/US exchange rate, with a weaker Canadian dollar having a positive material impact on Net Revenues and vice versa. The following chart provides estimated annual sensitivities for Net Revenues under market conditions compared to the initial term of the Supply and Processing Agreement for realized treatment charges, Canadian/US exchange rate and zinc price based on 2016 results:

Increase/(Decrease) in Net RevenuesIncrease/(Decrease) in Net Revenues Under the Initial Term of the Supply

Under Market Terms and Processing Agreement($ millions) ($ millions)

US 5 cent increase in zinc price 5.1 0.6US 5 cent decrease in zinc price (5.1) (0.6)

US$10 increase in realized treatment charges 6.9 -US$10 decrease in realized treatment charges (6.9) -

Cdn. 5 cent weakening of the Canadian dollar 8.4 3.7Cdn. 5 cent strengthening of the Canadian dollar (8.4) (3.7)

Outlook for the Fund

The main challenge facing the Fund is the ability for the Processing Facility to continue to operate profitably once the fixed processing fee available during the initial term of the Supply and Processing Agreement ends on May 2, 2017 and the Fund is required to purchase concentrate on market terms, including market treatment charges. See “Net Revenues under Market Terms” above.

7

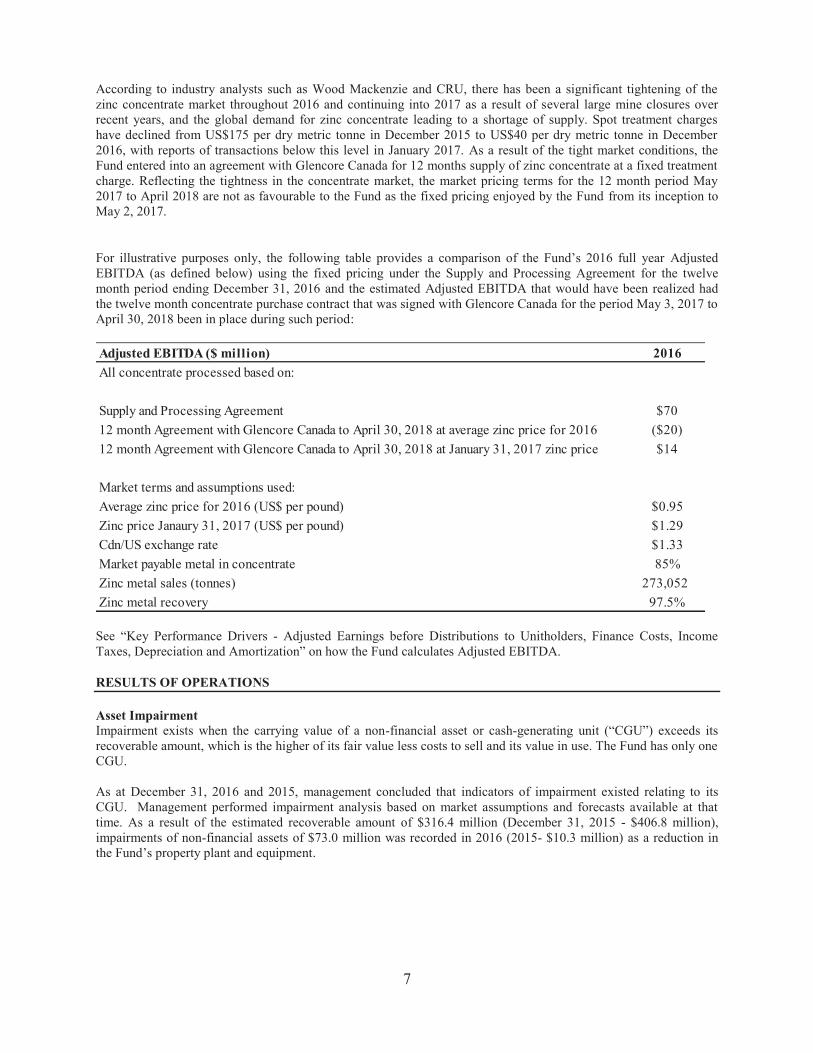

According to industry analysts such as Wood Mackenzie and CRU, there has been a significant tightening of the zinc concentrate market throughout 2016 and continuing into 2017 as a result of several large mine closures over recent years, and the global demand for zinc concentrate leading to a shortage of supply. Spot treatment charges have declined from US$175 per dry metric tonne in December 2015 to US$40 per dry metric tonne in December 2016, with reports of transactions below this level in January 2017. As a result of the tight market conditions, the Fund entered into an agreement with Glencore Canada for 12 months supply of zinc concentrate at a fixed treatment charge. Reflecting the tightness in the concentrate market, the market pricing terms for the 12 month period May 2017 to April 2018 are not as favourable to the Fund as the fixed pricing enjoyed by the Fund from its inception to May 2, 2017.

For illustrative purposes only, the following table provides a comparison of the Fund’s 2016 full year Adjusted EBITDA (as defined below) using the fixed pricing under the Supply and Processing Agreement for the twelve month period ending December 31, 2016 and the estimated Adjusted EBITDA that would have been realized had the twelve month concentrate purchase contract that was signed with Glencore Canada for the period May 3, 2017 to April 30, 2018 been in place during such period:

Adjusted EBITDA ($ million) 2016All concentrate processed based on:

Supply and Processing Agreement $7012 month Agreement with Glencore Canada to April 30, 2018 at average zinc price for 2016 ($20)12 month Agreement with Glencore Canada to April 30, 2018 at January 31, 2017 zinc price $14

Market terms and assumptions used:Average zinc price for 2016 (US$ per pound) $0.95Zinc price Janaury 31, 2017 (US$ per pound) $1.29Cdn/US exchange rate $1.33Market payable metal in concentrate 85%Zinc metal sales (tonnes) 273,052Zinc metal recovery 97.5%

See “Key Performance Drivers - Adjusted Earnings before Distributions to Unitholders, Finance Costs, Income Taxes, Depreciation and Amortization” on how the Fund calculates Adjusted EBITDA. RESULTS OF OPERATIONS Asset Impairment Impairment exists when the carrying value of a non-financial asset or cash-generating unit (“CGU”) exceeds its recoverable amount, which is the higher of its fair value less costs to sell and its value in use. The Fund has only one CGU. As at December 31, 2016 and 2015, management concluded that indicators of impairment existed relating to its CGU. Management performed impairment analysis based on market assumptions and forecasts available at that time. As a result of the estimated recoverable amount of $316.4 million (December 31, 2015 - $406.8 million), impairments of non-financial assets of $73.0 million was recorded in 2016 (2015- $10.3 million) as a reduction in the Fund’s property plant and equipment.

8

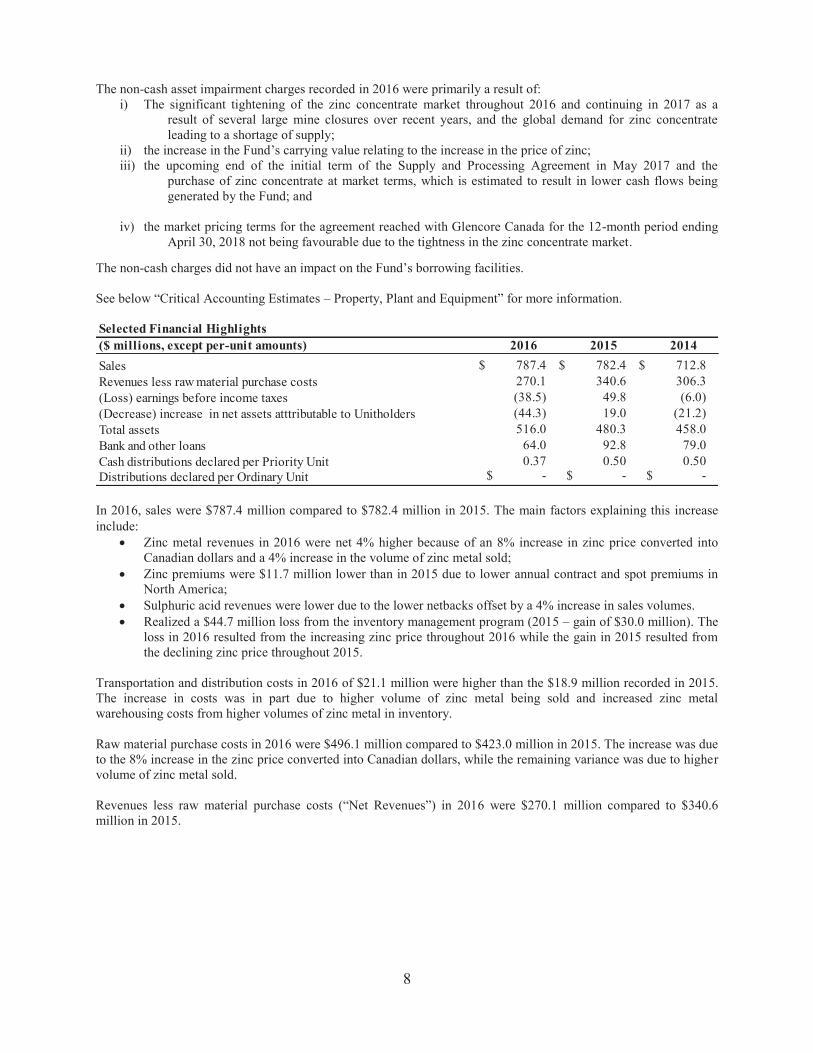

The non-cash asset impairment charges recorded in 2016 were primarily a result of:

i) The significant tightening of the zinc concentrate market throughout 2016 and continuing in 2017 as a result of several large mine closures over recent years, and the global demand for zinc concentrate leading to a shortage of supply;

ii) the increase in the Fund’s carrying value relating to the increase in the price of zinc; iii) the upcoming end of the initial term of the Supply and Processing Agreement in May 2017 and the

purchase of zinc concentrate at market terms, which is estimated to result in lower cash flows being generated by the Fund; and

iv) the market pricing terms for the agreement reached with Glencore Canada for the 12-month period ending April 30, 2018 not being favourable due to the tightness in the zinc concentrate market.

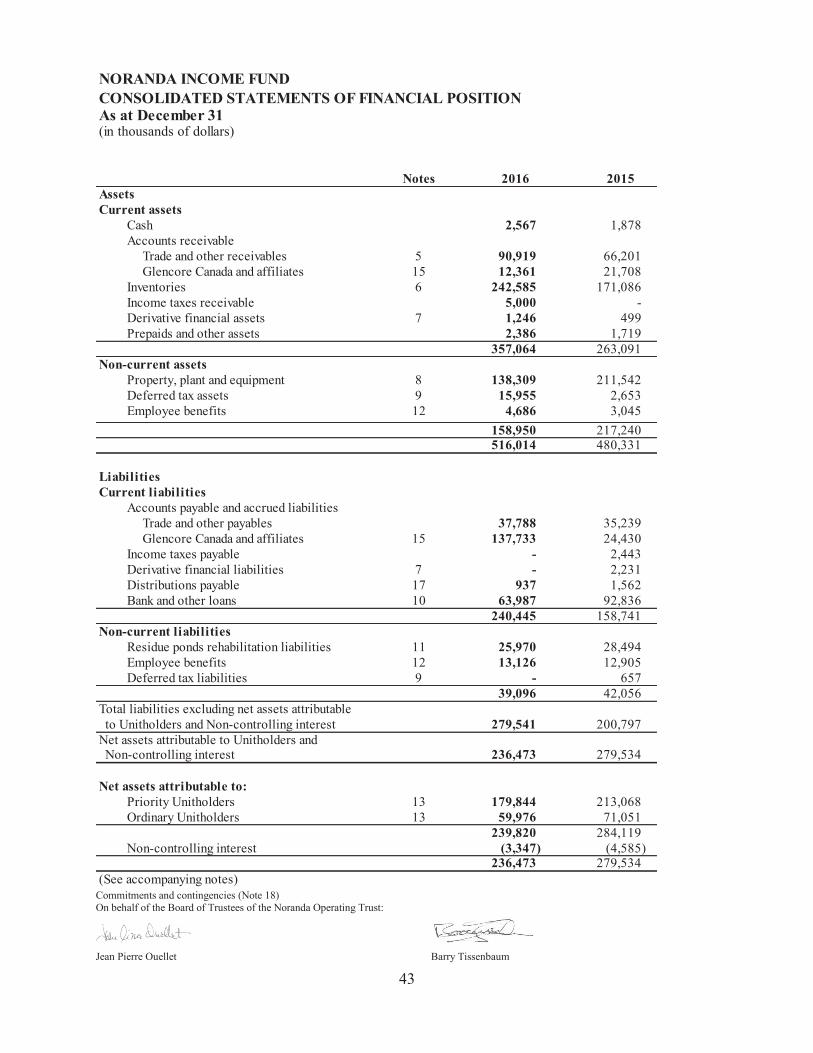

The non-cash charges did not have an impact on the Fund’s borrowing facilities. See below “Critical Accounting Estimates – Property, Plant and Equipment” for more information. Selected Financial Highlights($ millions, except per-unit amounts) 2016 2015 2014Sales $ 787.4 $ 782.4 $ 712.8 Revenues less raw material purchase costs 270.1 340.6 306.3 (Loss) earnings before income taxes (38.5) 49.8 (6.0)(Decrease) increase in net assets atttributable to Unitholders (44.3) 19.0 (21.2)Total assets 516.0 480.3 458.0 Bank and other loans 64.0 92.8 79.0 Cash distributions declared per Priority Unit 0.37 0.50 0.50 Distributions declared per Ordinary Unit $ - $ - $ - In 2016, sales were $787.4 million compared to $782.4 million in 2015. The main factors explaining this increase include:

Zinc metal revenues in 2016 were net 4% higher because of an 8% increase in zinc price converted into Canadian dollars and a 4% increase in the volume of zinc metal sold;

Zinc premiums were $11.7 million lower than in 2015 due to lower annual contract and spot premiums in North America;

Sulphuric acid revenues were lower due to the lower netbacks offset by a 4% increase in sales volumes. Realized a $44.7 million loss from the inventory management program (2015 – gain of $30.0 million). The

loss in 2016 resulted from the increasing zinc price throughout 2016 while the gain in 2015 resulted from the declining zinc price throughout 2015.

Transportation and distribution costs in 2016 of $21.1 million were higher than the $18.9 million recorded in 2015. The increase in costs was in part due to higher volume of zinc metal being sold and increased zinc metal warehousing costs from higher volumes of zinc metal in inventory. Raw material purchase costs in 2016 were $496.1 million compared to $423.0 million in 2015. The increase was due to the 8% increase in the zinc price converted into Canadian dollars, while the remaining variance was due to higher volume of zinc metal sold. Revenues less raw material purchase costs (“Net Revenues”) in 2016 were $270.1 million compared to $340.6 million in 2015.

9

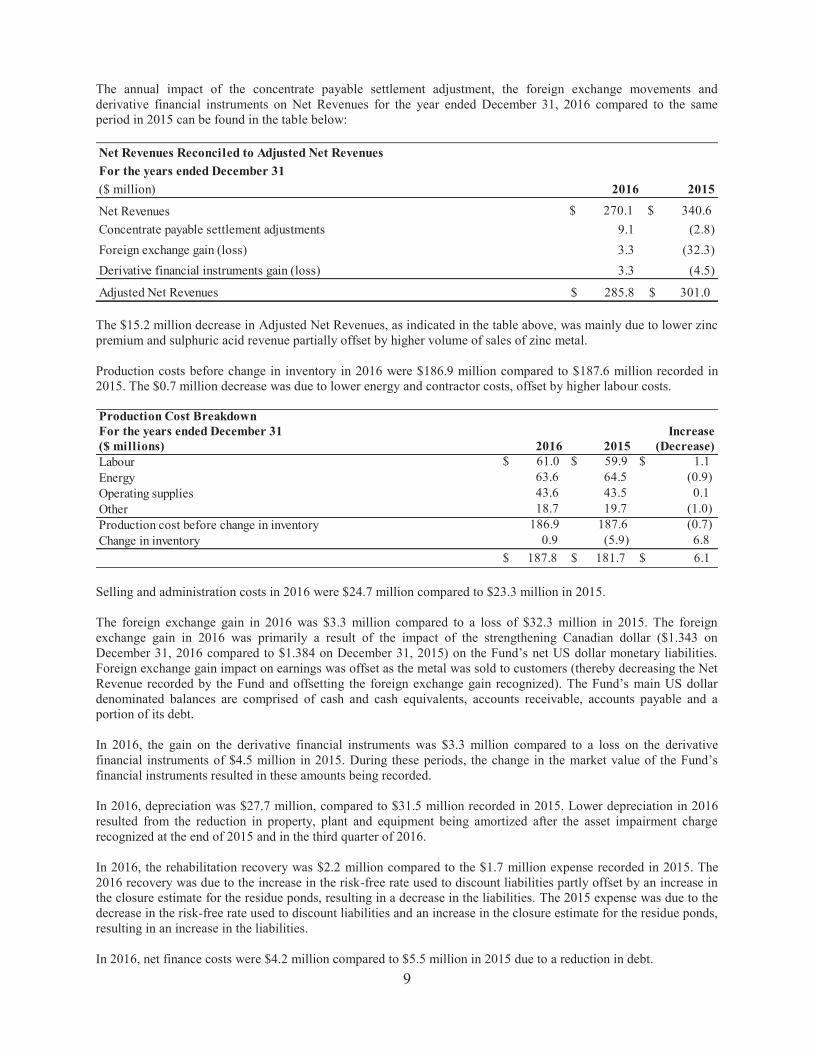

The annual impact of the concentrate payable settlement adjustment, the foreign exchange movements and derivative financial instruments on Net Revenues for the year ended December 31, 2016 compared to the same period in 2015 can be found in the table below: Net Revenues Reconciled to Adjusted Net RevenuesFor the years ended December 31($ million) 2016 2015

Net Revenues $ 270.1 $ 340.6 Concentrate payable settlement adjustments 9.1 (2.8) Foreign exchange gain (loss) 3.3 (32.3) Derivative financial instruments gain (loss) 3.3 (4.5)

Adjusted Net Revenues 285.8$ 301.0$ The $15.2 million decrease in Adjusted Net Revenues, as indicated in the table above, was mainly due to lower zinc premium and sulphuric acid revenue partially offset by higher volume of sales of zinc metal. Production costs before change in inventory in 2016 were $186.9 million compared to $187.6 million recorded in 2015. The $0.7 million decrease was due to lower energy and contractor costs, offset by higher labour costs. Production Cost BreakdownFor the years ended December 31 Increase($ millions) 2016 2015 (Decrease)Labour $ 61.0 $ 59.9 $ 1.1 Energy 63.6 64.5 (0.9)Operating supplies 43.6 43.5 0.1 Other 18.7 19.7 (1.0)Production cost before change in inventory 186.9 187.6 (0.7)Change in inventory 0.9 (5.9) 6.8

$ 187.8 $ 181.7 $ 6.1 Selling and administration costs in 2016 were $24.7 million compared to $23.3 million in 2015. The foreign exchange gain in 2016 was $3.3 million compared to a loss of $32.3 million in 2015. The foreign exchange gain in 2016 was primarily a result of the impact of the strengthening Canadian dollar ($1.343 on December 31, 2016 compared to $1.384 on December 31, 2015) on the Fund’s net US dollar monetary liabilities. Foreign exchange gain impact on earnings was offset as the metal was sold to customers (thereby decreasing the Net Revenue recorded by the Fund and offsetting the foreign exchange gain recognized). The Fund’s main US dollar denominated balances are comprised of cash and cash equivalents, accounts receivable, accounts payable and a portion of its debt. In 2016, the gain on the derivative financial instruments was $3.3 million compared to a loss on the derivative financial instruments of $4.5 million in 2015. During these periods, the change in the market value of the Fund’s financial instruments resulted in these amounts being recorded. In 2016, depreciation was $27.7 million, compared to $31.5 million recorded in 2015. Lower depreciation in 2016 resulted from the reduction in property, plant and equipment being amortized after the asset impairment charge recognized at the end of 2015 and in the third quarter of 2016. In 2016, the rehabilitation recovery was $2.2 million compared to the $1.7 million expense recorded in 2015. The 2016 recovery was due to the increase in the risk-free rate used to discount liabilities partly offset by an increase in the closure estimate for the residue ponds, resulting in a decrease in the liabilities. The 2015 expense was due to the decrease in the risk-free rate used to discount liabilities and an increase in the closure estimate for the residue ponds, resulting in an increase in the liabilities. In 2016, net finance costs were $4.2 million compared to $5.5 million in 2015 due to a reduction in debt.

10

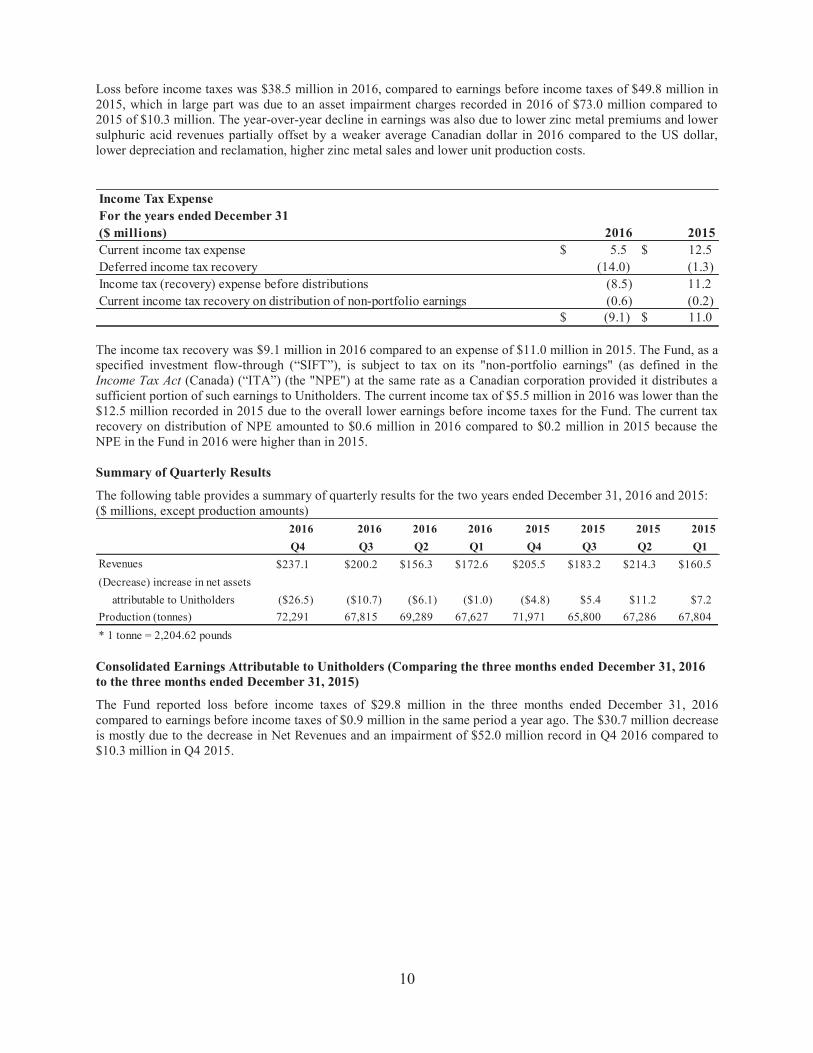

Loss before income taxes was $38.5 million in 2016, compared to earnings before income taxes of $49.8 million in 2015, which in large part was due to an asset impairment charges recorded in 2016 of $73.0 million compared to 2015 of $10.3 million. The year-over-year decline in earnings was also due to lower zinc metal premiums and lower sulphuric acid revenues partially offset by a weaker average Canadian dollar in 2016 compared to the US dollar, lower depreciation and reclamation, higher zinc metal sales and lower unit production costs.

Income Tax ExpenseFor the years ended December 31($ millions) 2016 2015Current income tax expense $ 5.5 $ 12.5 Deferred income tax recovery (14.0) (1.3)Income tax (recovery) expense before distributions (8.5) 11.2 Current income tax recovery on distribution of non-portfolio earnings (0.6) (0.2)

$ (9.1) $ 11.0 The income tax recovery was $9.1 million in 2016 compared to an expense of $11.0 million in 2015. The Fund, as a specified investment flow-through (“SIFT”), is subject to tax on its "non-portfolio earnings" (as defined in the Income Tax Act (Canada) (“ITA”) (the "NPE") at the same rate as a Canadian corporation provided it distributes a sufficient portion of such earnings to Unitholders. The current income tax of $5.5 million in 2016 was lower than the $12.5 million recorded in 2015 due to the overall lower earnings before income taxes for the Fund. The current tax recovery on distribution of NPE amounted to $0.6 million in 2016 compared to $0.2 million in 2015 because the NPE in the Fund in 2016 were higher than in 2015. Summary of Quarterly Results

The following table provides a summary of quarterly results for the two years ended December 31, 2016 and 2015: ($ millions, except production amounts)

2016 2016 2016 2016 2015 2015 2015 2015Q4 Q3 Q2 Q1 Q4 Q3 Q2 Q1

Revenues $237.1 $200.2 $156.3 $172.6 $205.5 $183.2 $214.3 $160.5(Decrease) increase in net assets attributable to Unitholders ($26.5) ($10.7) ($6.1) ($1.0) ($4.8) $5.4 $11.2 $7.2Production (tonnes) 72,291 67,815 69,289 67,627 71,971 65,800 67,286 67,804 * 1 tonne = 2,204.62 pounds Consolidated Earnings Attributable to Unitholders (Comparing the three months ended December 31, 2016 to the three months ended December 31, 2015)

The Fund reported loss before income taxes of $29.8 million in the three months ended December 31, 2016 compared to earnings before income taxes of $0.9 million in the same period a year ago. The $30.7 million decrease is mostly due to the decrease in Net Revenues and an impairment of $52.0 million record in Q4 2016 compared to $10.3 million in Q4 2015.

11

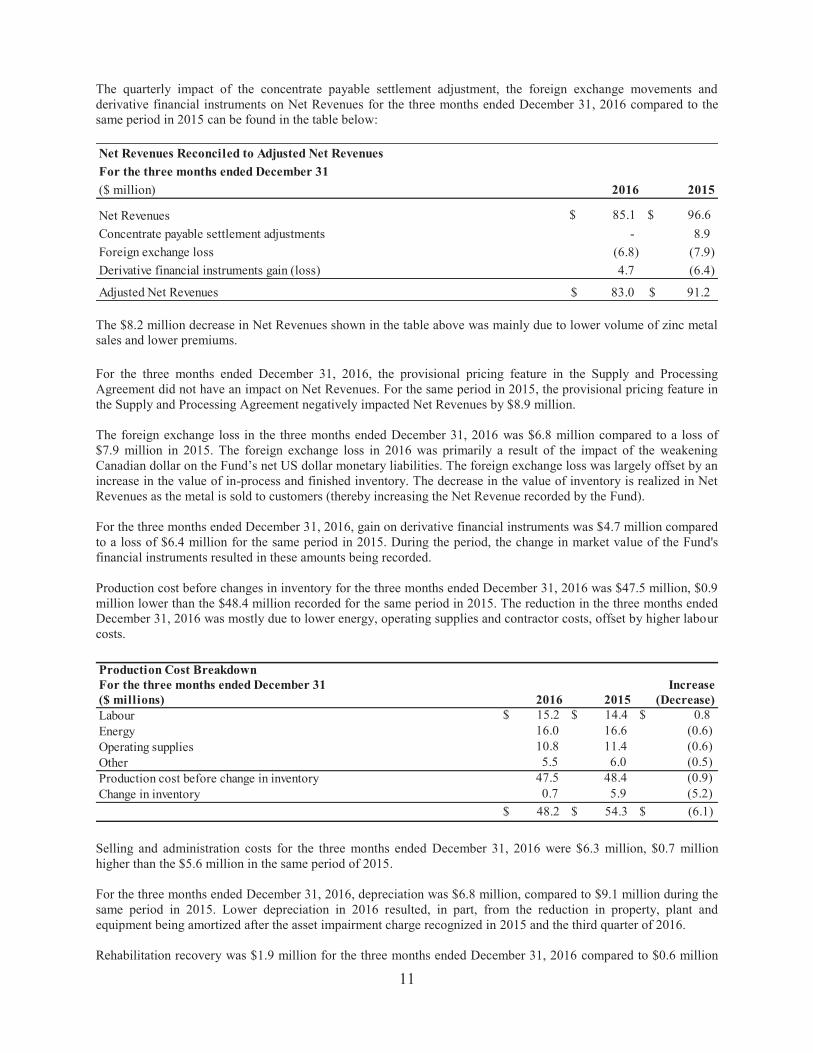

The quarterly impact of the concentrate payable settlement adjustment, the foreign exchange movements and derivative financial instruments on Net Revenues for the three months ended December 31, 2016 compared to the same period in 2015 can be found in the table below:

Net Revenues Reconciled to Adjusted Net RevenuesFor the three months ended December 31($ million) 2016 2015

Net Revenues $ 85.1 $ 96.6 Concentrate payable settlement adjustments - 8.9 Foreign exchange loss (6.8) (7.9) Derivative financial instruments gain (loss) 4.7 (6.4)

Adjusted Net Revenues 83.0$ 91.2$ The $8.2 million decrease in Net Revenues shown in the table above was mainly due to lower volume of zinc metal sales and lower premiums. For the three months ended December 31, 2016, the provisional pricing feature in the Supply and Processing Agreement did not have an impact on Net Revenues. For the same period in 2015, the provisional pricing feature in the Supply and Processing Agreement negatively impacted Net Revenues by $8.9 million. The foreign exchange loss in the three months ended December 31, 2016 was $6.8 million compared to a loss of $7.9 million in 2015. The foreign exchange loss in 2016 was primarily a result of the impact of the weakening Canadian dollar on the Fund’s net US dollar monetary liabilities. The foreign exchange loss was largely offset by an increase in the value of in-process and finished inventory. The decrease in the value of inventory is realized in Net Revenues as the metal is sold to customers (thereby increasing the Net Revenue recorded by the Fund). For the three months ended December 31, 2016, gain on derivative financial instruments was $4.7 million compared to a loss of $6.4 million for the same period in 2015. During the period, the change in market value of the Fund's financial instruments resulted in these amounts being recorded. Production cost before changes in inventory for the three months ended December 31, 2016 was $47.5 million, $0.9 million lower than the $48.4 million recorded for the same period in 2015. The reduction in the three months ended December 31, 2016 was mostly due to lower energy, operating supplies and contractor costs, offset by higher labour costs. Production Cost BreakdownFor the three months ended December 31 Increase($ millions) 2016 2015 (Decrease)Labour $ 15.2 $ 14.4 $ 0.8 Energy 16.0 16.6 (0.6)Operating supplies 10.8 11.4 (0.6)Other 5.5 6.0 (0.5)Production cost before change in inventory 47.5 48.4 (0.9)Change in inventory 0.7 5.9 (5.2)

$ 48.2 $ 54.3 $ (6.1) Selling and administration costs for the three months ended December 31, 2016 were $6.3 million, $0.7 million higher than the $5.6 million in the same period of 2015. For the three months ended December 31, 2016, depreciation was $6.8 million, compared to $9.1 million during the same period in 2015. Lower depreciation in 2016 resulted, in part, from the reduction in property, plant and equipment being amortized after the asset impairment charge recognized in 2015 and the third quarter of 2016. Rehabilitation recovery was $1.9 million for the three months ended December 31, 2016 compared to $0.6 million

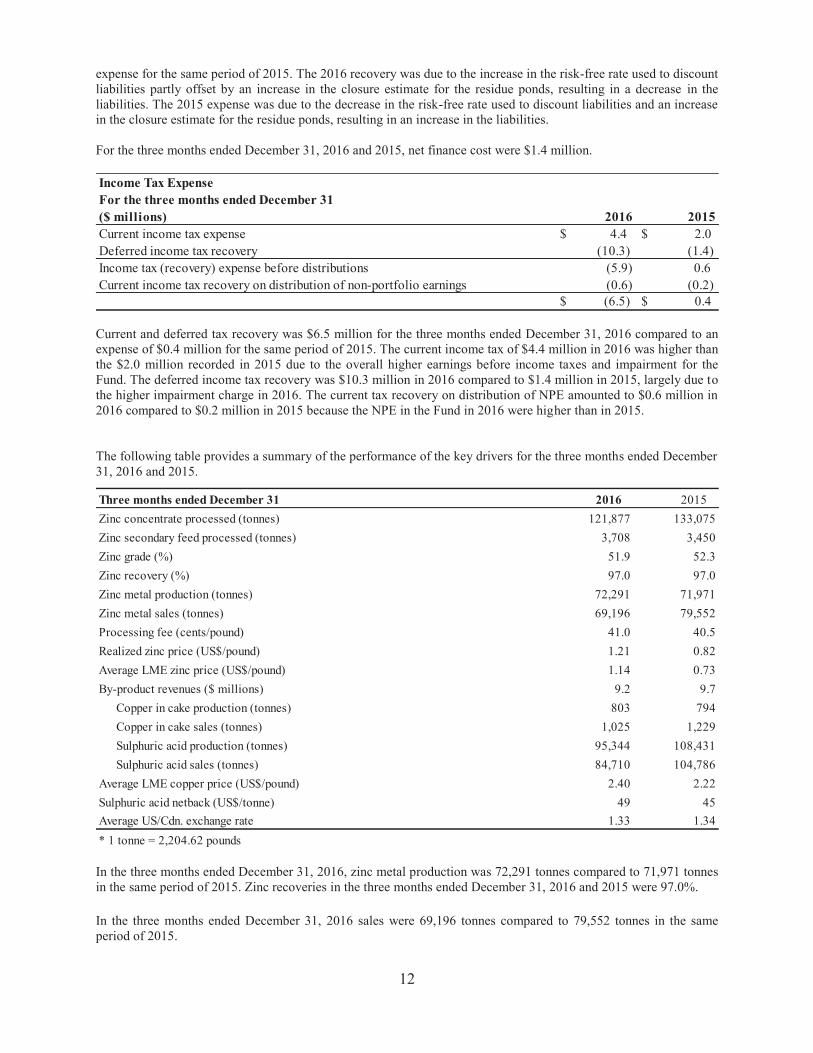

12

expense for the same period of 2015. The 2016 recovery was due to the increase in the risk-free rate used to discount liabilities partly offset by an increase in the closure estimate for the residue ponds, resulting in a decrease in the liabilities. The 2015 expense was due to the decrease in the risk-free rate used to discount liabilities and an increase in the closure estimate for the residue ponds, resulting in an increase in the liabilities. For the three months ended December 31, 2016 and 2015, net finance cost were $1.4 million. Income Tax ExpenseFor the three months ended December 31($ millions) 2016 2015Current income tax expense $ 4.4 $ 2.0 Deferred income tax recovery (10.3) (1.4)Income tax (recovery) expense before distributions (5.9) 0.6 Current income tax recovery on distribution of non-portfolio earnings (0.6) (0.2)

$ (6.5) $ 0.4 Current and deferred tax recovery was $6.5 million for the three months ended December 31, 2016 compared to an expense of $0.4 million for the same period of 2015. The current income tax of $4.4 million in 2016 was higher than the $2.0 million recorded in 2015 due to the overall higher earnings before income taxes and impairment for the Fund. The deferred income tax recovery was $10.3 million in 2016 compared to $1.4 million in 2015, largely due to the higher impairment charge in 2016. The current tax recovery on distribution of NPE amounted to $0.6 million in 2016 compared to $0.2 million in 2015 because the NPE in the Fund in 2016 were higher than in 2015. The following table provides a summary of the performance of the key drivers for the three months ended December 31, 2016 and 2015.

Three months ended December 31 2016 2015Zinc concentrate processed (tonnes) 121,877 133,075Zinc secondary feed processed (tonnes) 3,708 3,450Zinc grade (%) 51.9 52.3Zinc recovery (%) 97.0 97.0Zinc metal production (tonnes) 72,291 71,971Zinc metal sales (tonnes) 69,196 79,552Processing fee (cents/pound) 41.0 40.5Realized zinc price (US$/pound) 1.21 0.82Average LME zinc price (US$/pound) 1.14 0.73By-product revenues ($ millions) 9.2 9.7

Copper in cake production (tonnes) 803 794Copper in cake sales (tonnes) 1,025 1,229Sulphuric acid production (tonnes) 95,344 108,431Sulphuric acid sales (tonnes) 84,710 104,786

Average LME copper price (US$/pound) 2.40 2.22Sulphuric acid netback (US$/tonne) 49 45Average US/Cdn. exchange rate 1.33 1.34* 1 tonne = 2,204.62 pounds In the three months ended December 31, 2016, zinc metal production was 72,291 tonnes compared to 71,971 tonnes in the same period of 2015. Zinc recoveries in the three months ended December 31, 2016 and 2015 were 97.0%. In the three months ended December 31, 2016 sales were 69,196 tonnes compared to 79,552 tonnes in the same period of 2015.

13

In the three months ended December 31, 2016, the Fund generated $9.2 million in revenue from the sale of its copper in cake and sulphuric acid compared to $9.7 million achieved for the same period of 2015. Revenues from the sale of sulphuric acid were $5.5 million in the three months ended December 31, 2016, a decrease of $0.8 from $6.3 million in the same period of 2015. Sulphuric acid sales totalled 84,710 tonnes in the three months ended December 31 of 2016, compared to 104,786 tonnes for the same period of 2015. In the three months ended December 31 2016, sulphuric acid netbacks were US$49 per tonne compared to US$45 per tonne for the same period of 2015. Copper in cake revenues were $3.7 million in the three months ended December 31, 2016 compared to $3.4 million for the same period of 2015. The volume of copper produced and sold is dependent on the copper content in the zinc concentrates that are consumed during the year. Copper in cake sales volumes in the three months ended December 31, 2016 totalled 1,025 tonnes compared to 1,229 tonnes in the corresponding period of 2015. Cash provided by operating activities in the three months ended December 31, 2016 was $35.2 million, including a positive $19.6 million decrease in non-cash working capital due to a decrease in accounts receivables and an increase in accounts payable partially offset by an increase in the inventory. In the same period of 2015, cash provided by operating activities was $43.9 million, which was positively impacted by a $15.3 million decrease in non-cash working capital due to a reduction in accounts receivable and inventory and an increase in accounts payable. Capital expenditures in the three months ended December 31, 2016 were $13.6 million, compared to $9.8 million for the same period of 2015. During the three months ended December 31, 2016, $7.0 million was spent on acid plant and roaster equipment, $2.7 million purchases of anodes, while sustaining capital accounted for most of the remaining expenditures. Cash distributions paid to Priority Unitholders during the three months ended December 31, 2016 totalled $2.8 million, compared to $4.7 million for the same period of 2015. KEY PERFORMANCE DRIVERS

The principal factor affecting the Fund’s performance is the processing of zinc concentrates into zinc metal. This activity results in the Fund earning a processing fee. In 2016, the processing fee accounted for 73% of the Fund’s Net Revenues (2015 – 69%). A second key factor affecting the performance of the Fund is the premiums that are realized on the sale of zinc products to customers. Zinc metal is sold to customers on the basis of an LME zinc price plus a premium that is negotiated between the buyer and seller. Premiums can vary according to various factors including product form, quantity, quality and payment terms. In 2016, product premiums accounted for 14% of the Fund’s Net Revenues (2015 – 17%). By-product revenues (copper in cake and sulphuric acid) and zinc metal recovery gains generated 9% and 4%, respectively, of the Fund’s Net Revenues in 2016 (2015 – 11% and 3%). The Canada/US exchange rate also impacts the Fund’s performance through premiums, by-product revenues and zinc recovery gains which, collectively, represented 27% of the 2016 Net Revenues (2015 – 31%). As the processing fee is earned in Canadian dollars, 73% of the Fund’s Net Revenues are not exposed to currency risk. Please see “Net Revenues under Market Terms” above for a discussion on the impact of moving to market terms on May 3, 2017 (following the completion of the initial term of the Supply and Processing Agreement). Two other performance drivers that impact the Fund are cost containment and a disciplined use of capital. The Fund provides annual guidance for a number of its key performance drivers, including production, sales, and processing fee. In light of the unionized workers’ strike at the Processing Facility and uncertainty about its duration, the Fund has deferred providing guidance for zinc metal production and sales targets for 2017 until an appropriate time.

14

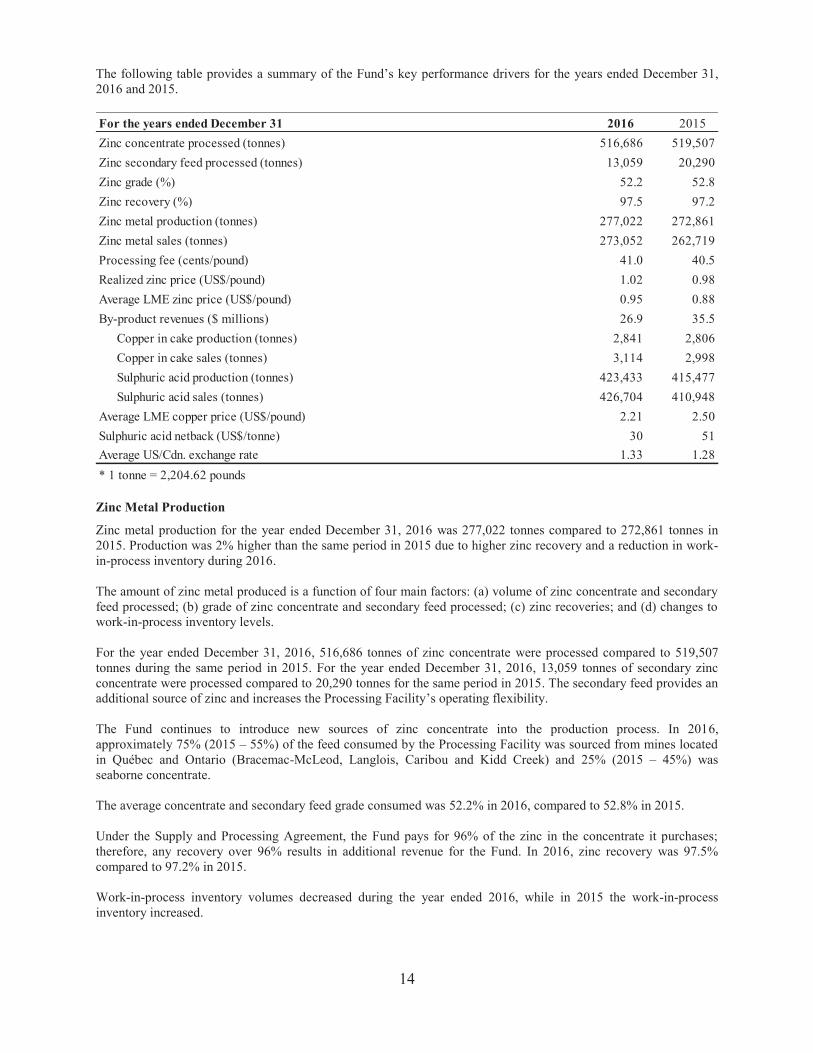

The following table provides a summary of the Fund’s key performance drivers for the years ended December 31, 2016 and 2015. For the years ended December 31 2016 2015Zinc concentrate processed (tonnes) 516,686 519,507Zinc secondary feed processed (tonnes) 13,059 20,290Zinc grade (%) 52.2 52.8Zinc recovery (%) 97.5 97.2Zinc metal production (tonnes) 277,022 272,861Zinc metal sales (tonnes) 273,052 262,719Processing fee (cents/pound) 41.0 40.5Realized zinc price (US$/pound) 1.02 0.98Average LME zinc price (US$/pound) 0.95 0.88By-product revenues ($ millions) 26.9 35.5

Copper in cake production (tonnes) 2,841 2,806Copper in cake sales (tonnes) 3,114 2,998Sulphuric acid production (tonnes) 423,433 415,477Sulphuric acid sales (tonnes) 426,704 410,948

Average LME copper price (US$/pound) 2.21 2.50Sulphuric acid netback (US$/tonne) 30 51Average US/Cdn. exchange rate 1.33 1.28* 1 tonne = 2,204.62 pounds Zinc Metal Production

Zinc metal production for the year ended December 31, 2016 was 277,022 tonnes compared to 272,861 tonnes in 2015. Production was 2% higher than the same period in 2015 due to higher zinc recovery and a reduction in work-in-process inventory during 2016. The amount of zinc metal produced is a function of four main factors: (a) volume of zinc concentrate and secondary feed processed; (b) grade of zinc concentrate and secondary feed processed; (c) zinc recoveries; and (d) changes to work-in-process inventory levels. For the year ended December 31, 2016, 516,686 tonnes of zinc concentrate were processed compared to 519,507 tonnes during the same period in 2015. For the year ended December 31, 2016, 13,059 tonnes of secondary zinc concentrate were processed compared to 20,290 tonnes for the same period in 2015. The secondary feed provides an additional source of zinc and increases the Processing Facility’s operating flexibility. The Fund continues to introduce new sources of zinc concentrate into the production process. In 2016, approximately 75% (2015 – 55%) of the feed consumed by the Processing Facility was sourced from mines located in Québec and Ontario (Bracemac-McLeod, Langlois, Caribou and Kidd Creek) and 25% (2015 – 45%) was seaborne concentrate. The average concentrate and secondary feed grade consumed was 52.2% in 2016, compared to 52.8% in 2015. Under the Supply and Processing Agreement, the Fund pays for 96% of the zinc in the concentrate it purchases; therefore, any recovery over 96% results in additional revenue for the Fund. In 2016, zinc recovery was 97.5% compared to 97.2% in 2015. Work-in-process inventory volumes decreased during the year ended 2016, while in 2015 the work-in-process inventory increased.

15

The Processing Facility may experience an increase in its costs, working capital requirements and/or capital expenditures as a result of being required to treat a more varied feed quality stream. Higher levels of impurities may also negatively impact the volume of zinc concentrate that can be processed, resulting in a lower overall production. Concentrate inventory levels are expected to continue to be variable, due to large and irregular seaborne deliveries of concentrate and the requirement to mix feed qualities to maximize the Processing Facility’s production. Sales Zinc metal is used in a wide range of industries. Its major use is in the production of galvanized steel. Sales in 2016 were 273,052 tonnes compared to 262,719 tonnes in 2015. During the year ended December 31, 2016, zinc metal inventories increased by approximately 4,000 tonnes. Processing Fee For 2016, the processing fee was $0.410 per pound ($904 per tonne), compared to $0.405 per pound ($893 per tonne) in 2015. The processing fee under the Supply and Processing Agreement is adjusted annually: (i) upward by 1% and (ii) upward or downward by 10% of the year-over-year percentage change in the average cost of electricity per megawatt hour for the Processing Facility. Based on the annual 1% increase and the average increase in electricity costs, the processing fee for the period ending May 2, 2017 is expected to be $0.414 per pound ($914 per tonne). After May 2, 2017, the processing fee is replaced with market treatment charges (see “Net Revenues under Market Terms” above). Realized Zinc Price, Average LME Zinc Price and Premiums The following table provides a summary of the realized zinc price and the average LME zinc price for the years ended December 31, 2016 and 2015.

%Increase

(Decr 2016 2015 (Decrease)Realized zinc price (US$/pound) 1.02 0.98 4%Average LME zinc price (US$/pound) 0.95 0.88 8%

Years endedDecember 31,

The realized zinc prices reflected US$0.07 per pound premium to the average LME zinc price for the years ended December 31, 2016 compared to US$0.10 in the same period of 2015. By-products The Fund produces copper in cake and sulphuric acid as by-products from refining zinc concentrate. In 2016, the Fund generated $26.9 million in revenue from the sale of its copper in cake and sulphuric acid compared to $35.5 million in 2015. Copper in Cake Copper in cake revenues in 2016 were slightly higher at $9.8 million compared to $8.9 million in 2015. Lower copper prices were partially offset by higher sales volumes. In 2016, copper prices were $2.21 per pound, compared to $2.50 per pound in 2015. The copper in cake sales volumes increased to 3,114 tonnes in 2016 from 2,998 tonnes in the prior year.

16

Sulphuric Acid Revenues from the sale of sulphuric acid decreased to $17.1 million in 2016 from $26.6 million in 2015. Sulphuric acid netbacks in 2016 were US$30 per tonne, compared to US$51 in 2015. The lower netbacks in 2016 reflected the impact of lower annual contract and purchase order contract pricing. Sales volumes were higher in 2016 at 426,704 tonnes compared to 410,948 tonnes in the previous year. Exchange Rate A weaker Canadian dollar has a positive impact on the US dollar components of the Fund’s Net Revenues (premiums, by-products and zinc recovery gains). In 2016, a one-cent Canadian dollar weakening would have positively impacted the Fund’s annual cash flow from operations before working capital changes by approximately $0.8 million. In 2016, the average Canadian dollar weakened to $1.33 per US dollar compared to an average of $1.28 per US dollar in 2015. Production Costs Production costs include labour, energy, supplies and other costs directly associated with the production process, plus or minus changes in inventory levels. Production costs before change in inventory in 2016 were $186.9 million compared to $187.6 million recorded in 2015. The $0.7 million decrease was due to lower energy and contractor costs, offset by higher labour costs. In November 2016, the Fund submitted an application to the Quebec Ministry of Finance for its program for electricity rate reduction for large industrial electricity consumers. In February 2017, the Fund received notice that its application had been accepted conditional to meeting additional milestones. There can be no assurance that the Fund will be able to meet those milestones. Capital Expenditures Capital spending was $27.2 million in 2016 compared to $29.9 million in 2015. Most of the annual 2016 capital investment was spent on sustaining the Fund’s operations, including $11.1 million on acid plant and roaster equipment, $8.0 million on replacement anodes in the cell house and the balance on other sustaining capital. Comparatively, in 2015, capital investment spent on sustaining the Fund’s operations included $9.6 million spent on replacement anodes for the cell house, $11.1 million spent on major roasting and acid plant equipment and the balance on other sustaining capital. In light of the unionized workers’ strike at the Processing Facility and uncertainty about its duration, the Fund has deferred providing guidance for capital expenditures for 2017 until an appropriate time.

Adjusted Earnings before Distributions to Unitholders, Finance Costs, Income Taxes, Depreciation and Amortization (“Adjusted EBITDA”) Adjusted EBITDA is used by the Fund as an indication of cash generated from operations. Adjusted EBITDA is not a recognized measure under IFRS and therefore the Fund’s method of calculating Adjusted EBITDA is unlikely to be comparable to methods used by other entities. The Fund’s Adjusted EBITDA is calculated by starting from earnings before finance costs and income taxes and adjusting for all of the non-cash items such as depreciation, gain or loss on the sale of assets, changes in fair value of embedded derivatives and non-cash gain or loss on derivative financial instruments. In addition, an adjustment is made to reflect the net change in the rehabilitation liabilities (reclamation (recovery) expense less site restoration expenditures) and the net change in employee benefits (non-cash employee benefit expenses less employer contributions).

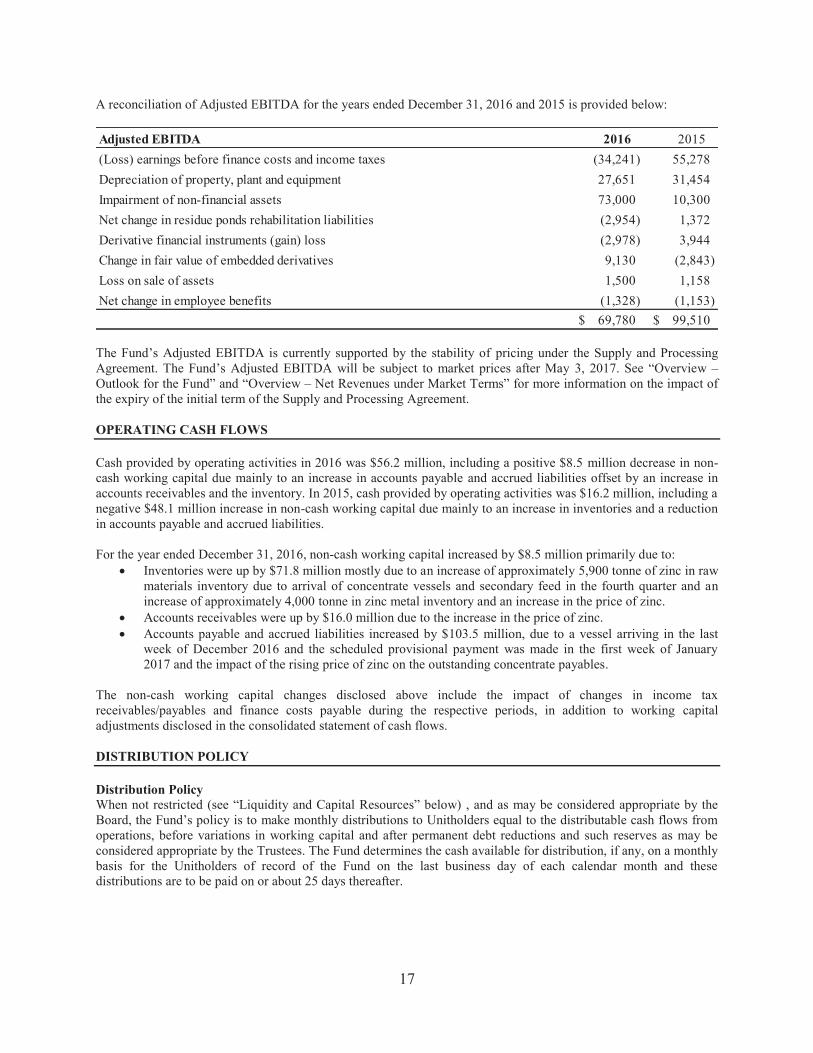

17

A reconciliation of Adjusted EBITDA for the years ended December 31, 2016 and 2015 is provided below: Adjusted EBITDA 2016 2015(Loss) earnings before finance costs and income taxes (34,241) 55,278 Depreciation of property, plant and equipment 27,651 31,454 Impairment of non-financial assets 73,000 10,300 Net change in residue ponds rehabilitation liabilities (2,954) 1,372 Derivative financial instruments (gain) loss (2,978) 3,944 Change in fair value of embedded derivatives 9,130 (2,843) Loss on sale of assets 1,500 1,158 Net change in employee benefits (1,328) (1,153)

69,780$ 99,510$ The Fund’s Adjusted EBITDA is currently supported by the stability of pricing under the Supply and Processing Agreement. The Fund’s Adjusted EBITDA will be subject to market prices after May 3, 2017. See “Overview – Outlook for the Fund” and “Overview – Net Revenues under Market Terms” for more information on the impact of the expiry of the initial term of the Supply and Processing Agreement. OPERATING CASH FLOWS Cash provided by operating activities in 2016 was $56.2 million, including a positive $8.5 million decrease in non-cash working capital due mainly to an increase in accounts payable and accrued liabilities offset by an increase in accounts receivables and the inventory. In 2015, cash provided by operating activities was $16.2 million, including a negative $48.1 million increase in non-cash working capital due mainly to an increase in inventories and a reduction in accounts payable and accrued liabilities. For the year ended December 31, 2016, non-cash working capital increased by $8.5 million primarily due to:

Inventories were up by $71.8 million mostly due to an increase of approximately 5,900 tonne of zinc in raw materials inventory due to arrival of concentrate vessels and secondary feed in the fourth quarter and an increase of approximately 4,000 tonne in zinc metal inventory and an increase in the price of zinc.

Accounts receivables were up by $16.0 million due to the increase in the price of zinc. Accounts payable and accrued liabilities increased by $103.5 million, due to a vessel arriving in the last

week of December 2016 and the scheduled provisional payment was made in the first week of January 2017 and the impact of the rising price of zinc on the outstanding concentrate payables.

The non-cash working capital changes disclosed above include the impact of changes in income tax receivables/payables and finance costs payable during the respective periods, in addition to working capital adjustments disclosed in the consolidated statement of cash flows. DISTRIBUTION POLICY Distribution Policy When not restricted (see “Liquidity and Capital Resources” below) , and as may be considered appropriate by the Board, the Fund’s policy is to make monthly distributions to Unitholders equal to the distributable cash flows from operations, before variations in working capital and after permanent debt reductions and such reserves as may be considered appropriate by the Trustees. The Fund determines the cash available for distribution, if any, on a monthly basis for the Unitholders of record of the Fund on the last business day of each calendar month and these distributions are to be paid on or about 25 days thereafter.

18

In determining whether there shall be a distribution and the level thereof, the Board periodically reviews the Fund’s financial performance, business environment and prospects, and determines the appropriate levels of reserves. The Board also continues to evaluate on a monthly basis the expected future cash flows of the Fund as well as the reserves that may be required in the future. Given the uncertainty of future pricing and market conditions for zinc concentrate, and the reduced profitability and prospects for the Fund, the Board declared distributions for the months August 2016 to January 2017 of $0.025 per Priority Unit, as compared to $0.04167 per Priority Unit for the months of January to July 2016. On January 31, 2017, in light of the prevailing market conditions now facing the Fund, the Board announced the suspension of future monthly distributions to unitholders. There is no assurance that monthly distributions will resume in the future. See “Overview – Outlook for the Fund” above. Cash distributions on the Ordinary Units of the Partnership held indirectly by Glencore Canada are subordinated to distributions on Priority Units of the Fund until May 2017, except upon the occurrence of certain events. As a result of Glencore Canada’s subordination, no distributions have been declared to the Ordinary Units since January 2009. The accumulated distribution deficiency amount was $34.2 million as at December 31, 2016 and $34.5 million as at February 28, 2017. For further details on the terms of the subordination, reference should be made to the Fund’s Partnership Agreement dated May 1, 2002, which is available on SEDAR at www.sedar.com. In the event of an exchange of Ordinary Units on a one-for-one basis for Priority Units on or after May 2, 2017, or earlier upon the occurrence of an early exchange event, the holder of Ordinary Units has the right to receive a promissory note in the amount of the outstanding accumulated deficiency amount. Subsequent to an exchange, the promissory note reflecting the remaining outstanding accumulated deficiency amount continues, however, there is no further accumulation of the accumulated deficiency amount. Any deficiency amount related to the promissory note is not payable by the Fund until such time that excess cash is available for distribution above the monthly cash distribution of $0.08333 per Priority Unit, and a cash distribution above $0.08333 is approved by the Board. The Fund, as a SIFT, is subject to tax on its NPE at the same rate as a Canadian corporation provided it distributes a sufficient portion of such earnings to Unitholders. The Fund is required by its Trust Indenture to distribute each year amounts equal to the sum of its non-NPE and a specified percentage of its NPE (2016 and 2015 - 73.1%) for the year so as, to the extent possible, minimize its liability for tax under the ITA in the year. Such distributions are to be made in cash, unless the Fund is restricted from distributing cash or sufficient cash is not available, in which case such distributions are to be satisfied in whole or in part by the issuance of additional Priority Units having a value equal to the amount of cash which is unavailable for distribution. Following such an “in-kind” distribution, the Priority Units are automatically consolidated such that each certificate representing a number of units prior to the “in-kind’ distribution of additional units is deemed to represent the same number of units after the distribution of additional units and the consolidation. The Fund’s distribution policy and practices are impacted by various risks, uncertainties and other factors, which are discussed in greater detail in this section and in the sections entitled “Liquidity and Capital Resources” and “Forward-Looking Information” below.

19

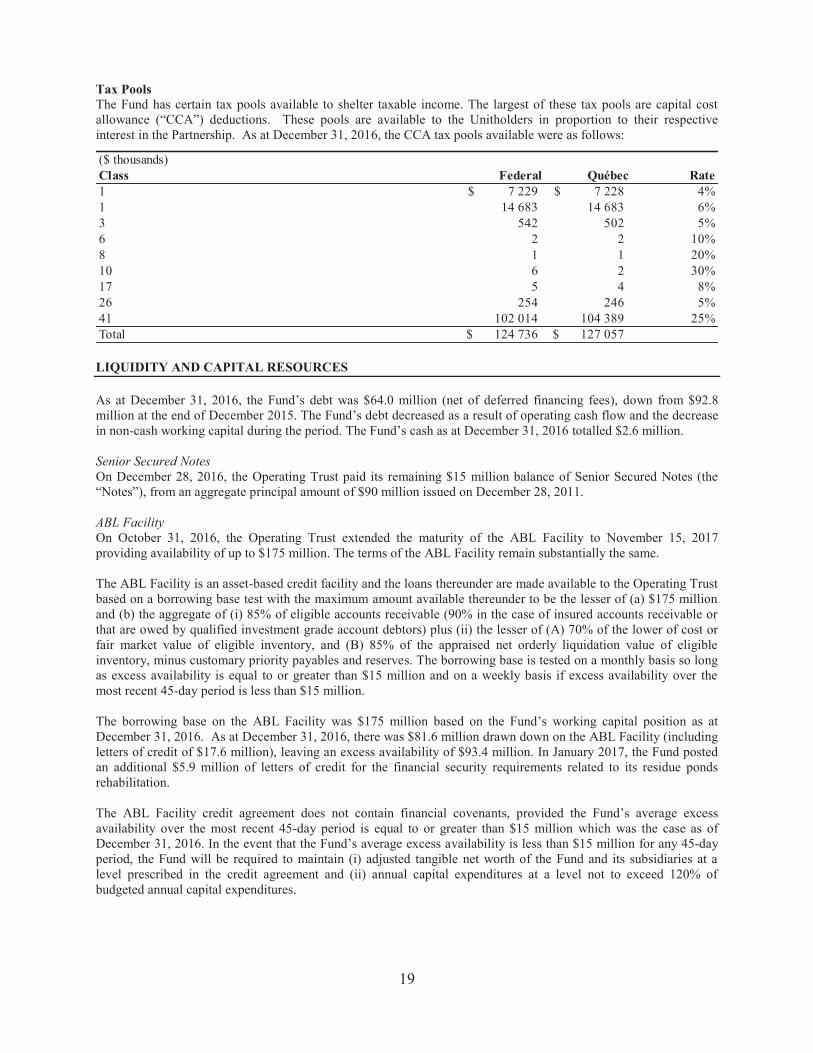

Tax Pools The Fund has certain tax pools available to shelter taxable income. The largest of these tax pools are capital cost allowance (“CCA”) deductions. These pools are available to the Unitholders in proportion to their respective interest in the Partnership. As at December 31, 2016, the CCA tax pools available were as follows:

($ thousands)Class Federal Québec Rate1 7 229$ 7 228$ 4%1 14 683 14 683 6%3 542 502 5%6 2 2 10%8 1 1 20%10 6 2 30%17 5 4 8%26 254 246 5%41 102 014 104 389 25%Total 124 736$ 127 057$ LIQUIDITY AND CAPITAL RESOURCES As at December 31, 2016, the Fund’s debt was $64.0 million (net of deferred financing fees), down from $92.8 million at the end of December 2015. The Fund’s debt decreased as a result of operating cash flow and the decrease in non-cash working capital during the period. The Fund’s cash as at December 31, 2016 totalled $2.6 million. Senior Secured Notes On December 28, 2016, the Operating Trust paid its remaining $15 million balance of Senior Secured Notes (the “Notes”), from an aggregate principal amount of $90 million issued on December 28, 2011. ABL Facility On October 31, 2016, the Operating Trust extended the maturity of the ABL Facility to November 15, 2017 providing availability of up to $175 million. The terms of the ABL Facility remain substantially the same. The ABL Facility is an asset-based credit facility and the loans thereunder are made available to the Operating Trust based on a borrowing base test with the maximum amount available thereunder to be the lesser of (a) $175 million and (b) the aggregate of (i) 85% of eligible accounts receivable (90% in the case of insured accounts receivable or that are owed by qualified investment grade account debtors) plus (ii) the lesser of (A) 70% of the lower of cost or fair market value of eligible inventory, and (B) 85% of the appraised net orderly liquidation value of eligible inventory, minus customary priority payables and reserves. The borrowing base is tested on a monthly basis so long as excess availability is equal to or greater than $15 million and on a weekly basis if excess availability over the most recent 45-day period is less than $15 million. The borrowing base on the ABL Facility was $175 million based on the Fund’s working capital position as at December 31, 2016. As at December 31, 2016, there was $81.6 million drawn down on the ABL Facility (including letters of credit of $17.6 million), leaving an excess availability of $93.4 million. In January 2017, the Fund posted an additional $5.9 million of letters of credit for the financial security requirements related to its residue ponds rehabilitation. The ABL Facility credit agreement does not contain financial covenants, provided the Fund’s average excess availability over the most recent 45-day period is equal to or greater than $15 million which was the case as of December 31, 2016. In the event that the Fund’s average excess availability is less than $15 million for any 45-day period, the Fund will be required to maintain (i) adjusted tangible net worth of the Fund and its subsidiaries at a level prescribed in the credit agreement and (ii) annual capital expenditures at a level not to exceed 120% of budgeted annual capital expenditures.

20

The Fund believes that an asset-based credit facility is an appropriate credit instrument for its working capital requirements. Management plans to extend the current facility or obtain a new asset-based credit facility in advance of the maturity of the ABL Facility on November 15, 2017. There is no assurance that the Fund will be able to extend the current facility or obtain a new asset-based credit facility by the maturity of the ABL Facility. The ABL Facility credit agreement lists events that constitute an event of default, should they occur. They include the non-payment by the Operating Trust of principal, interest or other obligations of the Operating Trust in respect of the ABL Facility credit agreement and a breach of any covenant pursuant to the ABL Facility credit agreement, subject to customary cure periods where applicable. If any event of default occurs under the ABL Facility credit agreement, the ABL Facility lenders will be under no further obligation to make advances to the Operating Trust and may require the Operating Trust to repay any outstanding obligations pursuant to the ABL Facility credit agreement. The ABL Facility is fully and unconditionally guaranteed, on a senior secured basis, by the Fund, the Manager, Ontario Inc., the Partnership and NILP General Partner Ltd., the Partnership’s general partner. Financial Security In 2013, the Québec government amended the Mining Act regulation, which affects the amount of financial security to be posted by the Fund. In January 2015, the Partnership received approval of the updated residue pond cost estimate by the government of Québec. As of December 31, 2016, the Fund has posted $17.6 million of financial security in the form of letters of credit under the Mining Act regulation. The financial security requirements increased by $5.9 million made in January 2017 (through an increase in the letters of credit) for a total of $23.5 million. The Fund has now met its financial security obligations based on the updated residue pond cost estimate. The Fund currently meets its financial security obligations by posting letters of credit, thereby reducing the excess availability on the ABL Facility. Some of the risks, uncertainties and assumptions underlying this information can be found in the sections entitled “Risks and Uncertainties” and “Forward-Looking Information” below. OUTSTANDING UNITS

Outstanding Unit Data As at February 28, 2017

Priority Units 37,489,975

Ordinary Units and Special Fund Units 12,500,000

As noted above, a wholly-owned subsidiary of Glencore Canada holds 12,500,000 Ordinary Units of the Partnership, which represent all of the outstanding Ordinary Units of the Partnership, and which are exchangeable for Priority Units on a one-for-one basis only after May 2, 2017, or earlier upon the occurrence of certain events. The 12,500,000 outstanding special voting units of the Fund listed above (the “Special Fund Units”) provide voting rights in respect of the Fund to the holder of Ordinary Units. Further details concerning the rights, privileges and restrictions attached to the Fund’s outstanding Priority Units and Special Fund Units and the outstanding Ordinary Units of the Partnership, are contained in the Fund’s Annual Information Form under the section entitled “General Description of the Capital Structure”. A copy is available on SEDAR at www.sedar.com.

21

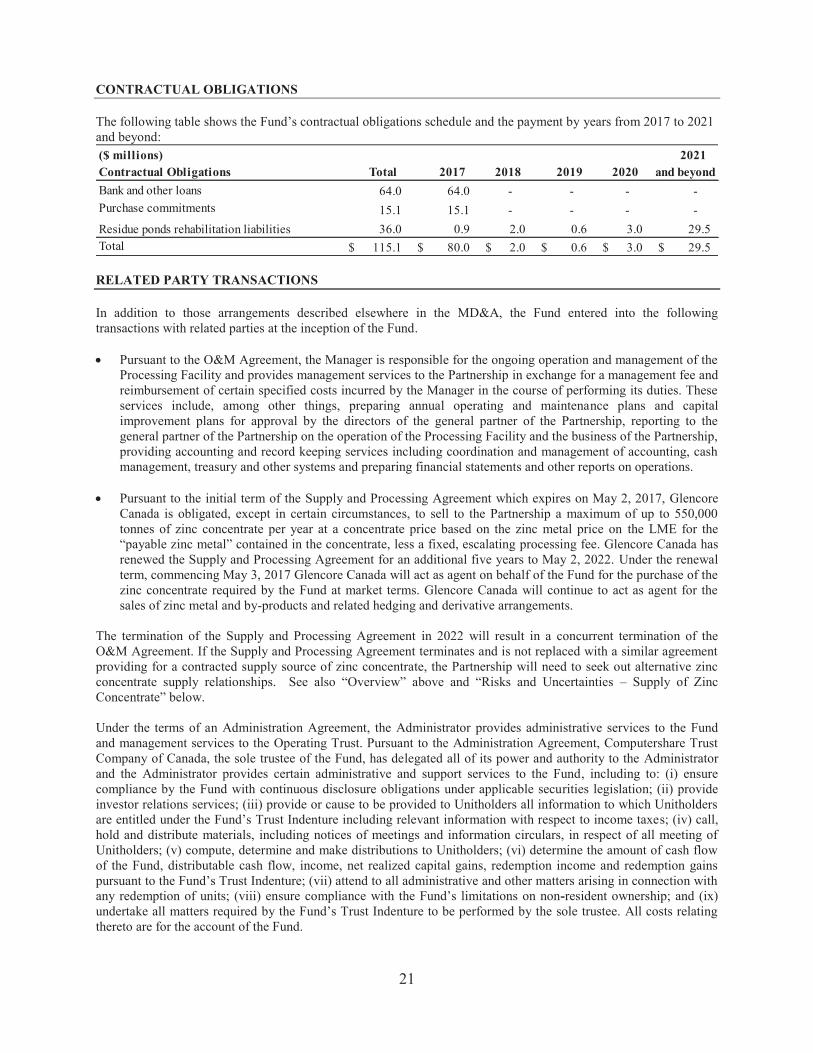

CONTRACTUAL OBLIGATIONS The following table shows the Fund’s contractual obligations schedule and the payment by years from 2017 to 2021 and beyond: ($ millions) 2021Contractual Obligations Total 2017 2018 2019 2020 and beyondBank and other loans 64.0 64.0 - - - - Purchase commitments 15.1 15.1 - - - - Residue ponds rehabilitation liabilities 36.0 0.9 2.0 0.6 3.0 29.5 Total 115.1$ 80.0$ 2.0$ 0.6$ 3.0$ 29.5$ RELATED PARTY TRANSACTIONS In addition to those arrangements described elsewhere in the MD&A, the Fund entered into the following transactions with related parties at the inception of the Fund. Pursuant to the O&M Agreement, the Manager is responsible for the ongoing operation and management of the

Processing Facility and provides management services to the Partnership in exchange for a management fee and reimbursement of certain specified costs incurred by the Manager in the course of performing its duties. These services include, among other things, preparing annual operating and maintenance plans and capital improvement plans for approval by the directors of the general partner of the Partnership, reporting to the general partner of the Partnership on the operation of the Processing Facility and the business of the Partnership, providing accounting and record keeping services including coordination and management of accounting, cash management, treasury and other systems and preparing financial statements and other reports on operations.

Pursuant to the initial term of the Supply and Processing Agreement which expires on May 2, 2017, Glencore

Canada is obligated, except in certain circumstances, to sell to the Partnership a maximum of up to 550,000 tonnes of zinc concentrate per year at a concentrate price based on the zinc metal price on the LME for the “payable zinc metal” contained in the concentrate, less a fixed, escalating processing fee. Glencore Canada has renewed the Supply and Processing Agreement for an additional five years to May 2, 2022. Under the renewal term, commencing May 3, 2017 Glencore Canada will act as agent on behalf of the Fund for the purchase of the zinc concentrate required by the Fund at market terms. Glencore Canada will continue to act as agent for the sales of zinc metal and by-products and related hedging and derivative arrangements.

The termination of the Supply and Processing Agreement in 2022 will result in a concurrent termination of the O&M Agreement. If the Supply and Processing Agreement terminates and is not replaced with a similar agreement providing for a contracted supply source of zinc concentrate, the Partnership will need to seek out alternative zinc concentrate supply relationships. See also “Overview” above and “Risks and Uncertainties – Supply of Zinc Concentrate” below. Under the terms of an Administration Agreement, the Administrator provides administrative services to the Fund and management services to the Operating Trust. Pursuant to the Administration Agreement, Computershare Trust Company of Canada, the sole trustee of the Fund, has delegated all of its power and authority to the Administrator and the Administrator provides certain administrative and support services to the Fund, including to: (i) ensure compliance by the Fund with continuous disclosure obligations under applicable securities legislation; (ii) provide investor relations services; (iii) provide or cause to be provided to Unitholders all information to which Unitholders are entitled under the Fund’s Trust Indenture including relevant information with respect to income taxes; (iv) call, hold and distribute materials, including notices of meetings and information circulars, in respect of all meeting of Unitholders; (v) compute, determine and make distributions to Unitholders; (vi) determine the amount of cash flow of the Fund, distributable cash flow, income, net realized capital gains, redemption income and redemption gains pursuant to the Fund’s Trust Indenture; (vii) attend to all administrative and other matters arising in connection with any redemption of units; (viii) ensure compliance with the Fund’s limitations on non-resident ownership; and (ix) undertake all matters required by the Fund’s Trust Indenture to be performed by the sole trustee. All costs relating thereto are for the account of the Fund.

22

Pursuant to the Management Services Agreement, the Manager provides management services to the Operating Trust. These services include assisting the Operating Trust in: (i) developing, implementing and monitoring a strategic plan; (ii) developing an annual business plan which may include operational and capital expenditures budgets when appropriate; (iii) developing acquisition strategies, investigating potential acquisitions and analyzing the feasibility of potential acquisitions; (iv) carrying out acquisitions or dispositions and related financings required for such transactions; (v) assisting in connection with any financing of the Operating Trust or the Fund; (vi) computing, determining and making distributions to unitholders of distributions properly payable by the Operating Trust; (vii) providing technical and evaluation services on equipment, processes and techniques relating to the operations of the business; (viii) supervising the operation of the Operating Trust’s business; and (ix) preparing, planning and co-ordinating management and Trustees’ meetings. In consideration for providing the services under the Management Services Agreement, the Manager is entitled to reimbursement of its direct and indirect costs and expenses incurred in connection with its duties under the Management Services Agreement. For further details concerning the above agreements, reference is made to the Management Information Circular of the Fund dated April 4, 2016 the Fund’s Annual Information Form dated March 28, 2016 (under the headings “Glencore Canada Corporation – Major Agreements” and “The Administrator and Manager”), and the notes to the Audited Consolidated Financial Statements of the Fund for the year ended December 31, 2016. Copies are available on SEDAR at www.sedar.com. Any agreements entered into by Glencore Canada as exclusive agent on behalf of the Partnership with any party related to Glencore Canada, and which are material to the Partnership, must be on terms that are, collectively, no less favourable to the Partnership than those available at the time from a reputable, non-related party. These agreements must be reviewed and approved by the majority of the independent Trustees of the Operating Trust. In addition, Glencore Canada and the Manager have entered into various agreements and provided certain consents in connection with providing credit support in respect of the Operating Trust’s existing ABL Facility. During the year ended December 31, 2016, Glencore Canada sold to the Partnership $542 million of zinc concentrate (2015 – $412.7 million) and provided $2.2 million in sales agency services (2015 - $ 1.7 million). The sales agency services are provided on a cost recovery basis. The administration, management and operating services provided by the Manager are provided on a cost recovery basis and for a management fee of $0.3 million per annum, adjusted upward annually by 2%. As a result of the Administration Agreement between the Fund and the Administrator, the Management Services Agreement between the Operating Trust and the Manager and the O&M Agreement between the Partnership and the Manager, the Manager has been paid the following amounts for administration, management and operating services with respect to the Fund, its subsidiaries and its assets for the years ended December 31, 2016 and 2015: Services provided by Glencore Canada($ millions) 2016 2015Salary and benefits* $70.7 $69.6Support services 2.2 2.1O&M Agreement management fee 0.3 0.3Total $73.2 $72.0

* This represents all amounts paid in respect of salaries and benefits for all of the employees of the Manager in connection with the operation of the Processing Facility and the services provided to the Fund, the Operating Trust and the Partnership.

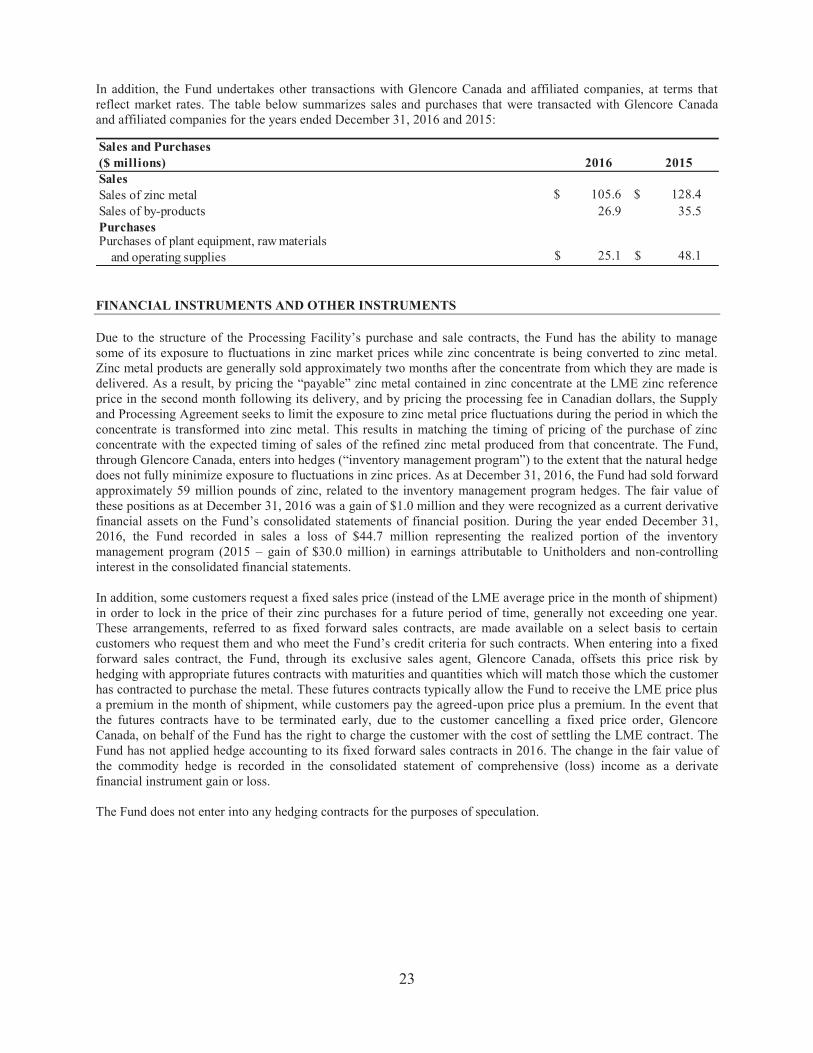

23

In addition, the Fund undertakes other transactions with Glencore Canada and affiliated companies, at terms that reflect market rates. The table below summarizes sales and purchases that were transacted with Glencore Canada and affiliated companies for the years ended December 31, 2016 and 2015:

Sales and Purchases ($ millions) 2016 2015SalesSales of zinc metal $ 105.6 $ 128.4 Sales of by-products 26.9 35.5PurchasesPurchases of plant equipment, raw materials and operating supplies $ 25.1 $ 48.1 FINANCIAL INSTRUMENTS AND OTHER INSTRUMENTS Due to the structure of the Processing Facility’s purchase and sale contracts, the Fund has the ability to manage some of its exposure to fluctuations in zinc market prices while zinc concentrate is being converted to zinc metal. Zinc metal products are generally sold approximately two months after the concentrate from which they are made is delivered. As a result, by pricing the “payable” zinc metal contained in zinc concentrate at the LME zinc reference price in the second month following its delivery, and by pricing the processing fee in Canadian dollars, the Supply and Processing Agreement seeks to limit the exposure to zinc metal price fluctuations during the period in which the concentrate is transformed into zinc metal. This results in matching the timing of pricing of the purchase of zinc concentrate with the expected timing of sales of the refined zinc metal produced from that concentrate. The Fund, through Glencore Canada, enters into hedges (“inventory management program”) to the extent that the natural hedge does not fully minimize exposure to fluctuations in zinc prices. As at December 31, 2016, the Fund had sold forward approximately 59 million pounds of zinc, related to the inventory management program hedges. The fair value of these positions as at December 31, 2016 was a gain of $1.0 million and they were recognized as a current derivative financial assets on the Fund’s consolidated statements of financial position. During the year ended December 31, 2016, the Fund recorded in sales a loss of $44.7 million representing the realized portion of the inventory management program (2015 – gain of $30.0 million) in earnings attributable to Unitholders and non-controlling interest in the consolidated financial statements. In addition, some customers request a fixed sales price (instead of the LME average price in the month of shipment) in order to lock in the price of their zinc purchases for a future period of time, generally not exceeding one year. These arrangements, referred to as fixed forward sales contracts, are made available on a select basis to certain customers who request them and who meet the Fund’s credit criteria for such contracts. When entering into a fixed forward sales contract, the Fund, through its exclusive sales agent, Glencore Canada, offsets this price risk by hedging with appropriate futures contracts with maturities and quantities which will match those which the customer has contracted to purchase the metal. These futures contracts typically allow the Fund to receive the LME price plus a premium in the month of shipment, while customers pay the agreed-upon price plus a premium. In the event that the futures contracts have to be terminated early, due to the customer cancelling a fixed price order, Glencore Canada, on behalf of the Fund has the right to charge the customer with the cost of settling the LME contract. The Fund has not applied hedge accounting to its fixed forward sales contracts in 2016. The change in the fair value of the commodity hedge is recorded in the consolidated statement of comprehensive (loss) income as a derivate financial instrument gain or loss. The Fund does not enter into any hedging contracts for the purposes of speculation.

24

The Fund has separated and recorded at fair value, embedded derivatives resulting from the provisional pricing feature in the Supply and Processing Agreement. Under the terms of this agreement, final prices for purchases of concentrate (“quotational pricing”) are based on the LME price prevailing on a specified future date after shipment (“quotational period”). The Fund accounts for changes in the fair value of unsettled concentrate payable amounts resulting from quotational pricing with reference to forward LME rates for the remaining quotational period through gains or losses recorded in raw material purchases costs and corresponding adjustments in accounts payable and accrued liabilities. During the year ended December 31, 2016, the Fund recorded an increase of raw material purchase costs of $9.1 million related to the change in fair value of the embedded derivatives resulting from the quotational pricing feature of its zinc concentrate payables (2015 – a decrease of $2.8 million). The Fund has exposure to the US dollar for its cash, accounts receivable, inventory, accounts payable and accrued liabilities and bank debt. The Fund attempts to manage the overall economic exposure to the US dollar by matching US dollar assets to US dollar liabilities. This currency exposure is managed in part through US dollar overnight transactions. As at December 31, 2016, the Fund had sold forward US dollars with a notional amount of US$104 million and bought forward dollars with a notional amount of $140 million. An unrealized gain of $0.2 million related to these open positions was recorded as at December 31, 2016. CRITICAL ACCOUNTING ESTIMATES Reference should be made to the Fund’s Audited Consolidated Financial Statements and the notes thereto for the year ended December 31, 2016. A copy is available on SEDAR at www.sedar.com. Property, Plant and Equipment Included in the $516.0 million of assets as at December 31, 2016 ($480.3 million as at December 31, 2015) were property, plant and equipment with a carrying value of $138.3 million (2015 – $211.5 million). This amount represented 27% (2015 – 44%) of the book value of the asset base. As such, the estimates used in accounting for property, plant and equipment and the related amortization charges are critical and have a material impact on the Fund’s financial condition and earnings. Property, plant and equipment are recorded at cost and the amortization is based on estimated service lives of the assets, calculated on a straight line basis. Assets under construction are not amortized until put into use. Impairment exists when the carrying value of a non-financial asset or cash-generating unit (“CGU”) exceeds its recoverable amount, which is the higher of its fair value less costs to sell and its value in use. The Fund has only one CGU. As at December 31, 2016 and 2015, management concluded that an indicator of impairment existed relating to its CGU. As a result of the estimated recoverable amount, an impairment loss of $73.0 million was recorded in 2016 ($10.3 million in 2015), all as a reduction in the Fund’s property plant and equipment. Management uses the higher of its fair value less costs to sell and its value in use to determine the recoverable amount which is based on a discounted cash flow model with cash flows expected to be generated from the Processing Facility over its remaining useful life and a terminal value. Cash flows include future investments that may enhance the performance through increased production volumes or reduction in production costs and eventual disposal of the CGU being tested. The recoverable amount is based on detailed budgets and forecasts and requires estimates and assumptions that a market participant may take into account. The indicators for impairment were primarily i) the significant tightening of the zinc concentrate market throughout 2016 and continuing in 2017 as a result of several large mine closures over recent years, and the global demand for zinc concentrate leading to a shortage of supply; ii) the increase in the Fund’s carrying value relating to the increase in the price of zinc; iii) the upcoming end of the initial term of the Supply and Processing Agreement in May 2017 and the purchase of zinc concentrate at market terms, which is estimated to result in lower cash flows being generated by the Fund; and iv) the market pricing terms for the agreement reached with Glencore Canada for the 12-month period ending April 30, 2018 not being favourable due to the tightness in the zinc concentrate market.

25

The determination of fair value less costs to sell or value in use is most sensitive to the following key assumptions:

Continued supply of concentrate after the initial term of the Supply and Processing Agreement at market terms

Estimated market treatment charges after the end of the initial term of the Supply and Processing Agreement based on industry forecasts and treatment charge rates as a proportion of the associated purchase price

Price of zinc, copper and sulphuric acid and zinc premium based on industry forecasts Remaining useful life of the assets and terminal value Capital expenditures Production volumes (including recoverable quantities) Estimated production costs Discount rates Foreign exchange rates Rehabilitation expenditures