NOMURA GLOBAL CHEMICAL INDUSTRY LEADER CONFERENCE, ROME · Nomura Global Chemical Industry Leader...

26

CREATING TOMORROW'S SOLUTIONS NOMURA GLOBAL CHEMICAL INDUSTRY LEADER CONFERENCE, ROME Dr. Rudolf Staudigl, CEO, March 2012

Transcript of NOMURA GLOBAL CHEMICAL INDUSTRY LEADER CONFERENCE, ROME · Nomura Global Chemical Industry Leader...

CREATING TOMORROW'S SOLUTIONS

NOMURA GLOBAL CHEMICAL INDUSTRY LEADER CONFERENCE, ROME

Dr. Rudolf Staudigl, CEO, March 2012

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 1

DISCLAIMER

The information contained in this presentation is for background purposes only and is subject toamendment, revision and updating. Certain statements and information contained in thispresentation may relate to future expectations and other forward-looking statements that arebased on management's current views and assumptions and involve known and unknown risksand uncertainties. In addition to statements which are forward-looking by reason of context,including without limitation, statements referring to risk limitations, operational profitability,financial strength, performance targets, profitable growth opportunities, and risk adequate pricing,other words such as "may, will, should, expects, plans, intends, anticipates, believes, estimates,predicts, or continue", "potential, future, or further", and similar expressions identify forward-looking statements. By their nature, forward-looking statements involve a number of risks,uncertainties and assumptions which could cause actual results or events to differ materiallyfrom those expressed or implied by the forward-looking statements. These include, among otherfactors, changing business or other market conditions and the prospects for growth anticipatedby the Company's management. These and other factors could adversely affect the outcomeand financial effects of the plans and events described herein. Statements contained in thispresentation regarding past trends or activities should not be taken as a representation that suchtrends or activities will continue in the future. The Company does not undertake any obligation toupdate or revise any statements contained in this presentation, whether as a result of newinformation, future events or otherwise. In particular, you should not place undue reliance onforward-looking statements, which speak only as of the date of this presentation.

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 2

20%

3%19%

33%25%

OUR BUSINESS PORTFOLIO – A FOUNDATION FOR GROWTH

POLYSILICON

• Cost and quality leader

• Strong no. 2 in capacity

• Impeccable growth record

SILICONES

• Strong no. 3

• Commodity base & specialty strength

• High focus on China / Asia

Siltronic

• Strong no. 3

• Technology leader

• Balanced base of customers

POLYMERS

• No. 1 in dispersible polymer powders

• No. 1 in VAE dispersions

• Global footprint

BIOSOLUTIONS

• High potential for future development

Innovation & Engineering

FY 2011Sales €4,910m

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 3

SOLID GROWTH PERFORMANCE – OUTPACING GDP CYCLES

• Leading market shares

• Leading production and process technology

• Addressing multiple growth platforms

• Strong productivity and cost focus

• World-scale production sites

Sales Performance

3,3373,781

4,298

3,719

2,756

4,9104,748

0

1,000

2,000

3,000

4,000

5,000

2005 2006 2007 2008 2009 2010 2011

0%

10%

20%

30%

Sales in €m EBITDA margin %

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 4

GROWTH SUPPORTED THROUGH SUBSTITUTION, INNOVATION AND EMERGING MARKETS

1,1191,287

1,361 1,409

1,239

1,581 1,594

0%

5%

10%

15%

20%

25%

0

300

600

900

1,200

1,500

1,800

2005 2006 2007 2008 2009 2010 2011

Sales in €m EBITDA margin %

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 5

VERSATILE SILICONES IN MORE THAN 3,000 PRODUCTS

insulating

releasing

dielectric strength

hydrophobic softening

gloss sustaining

adherent

heat resistant

low temper. flexibility

UV stable

radiation resistant defoaming

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 6

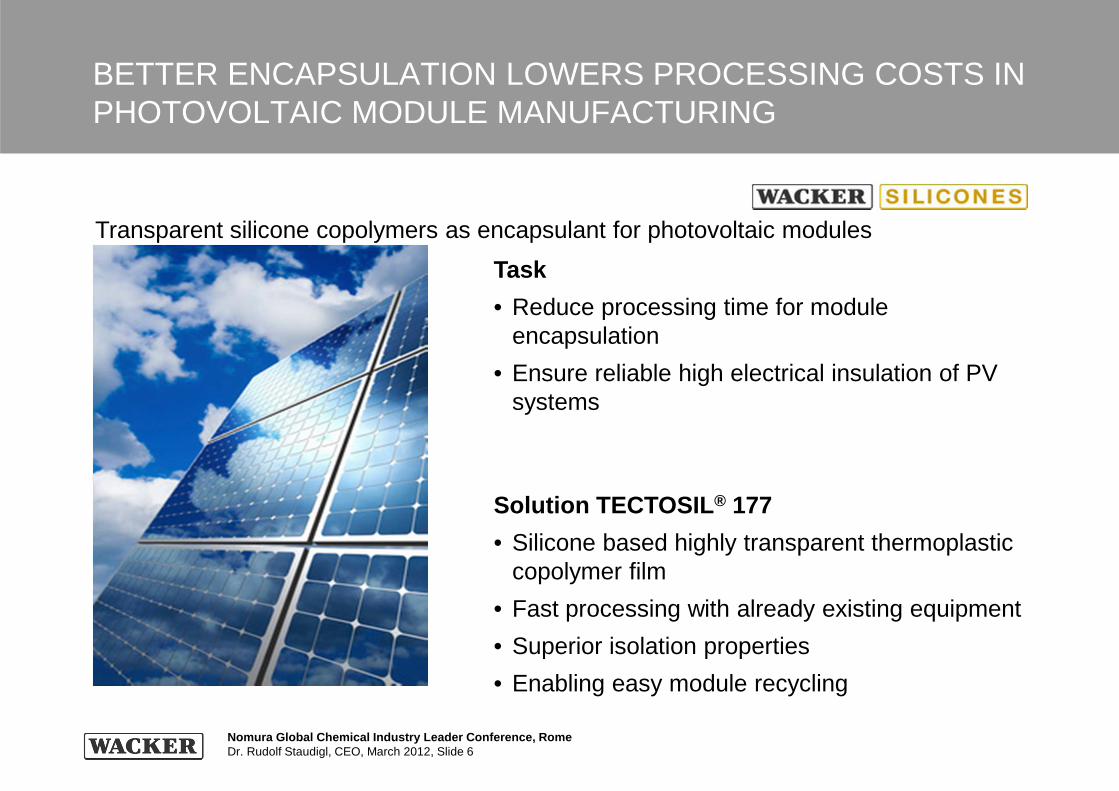

BETTER ENCAPSULATION LOWERS PROCESSING COSTS IN PHOTOVOLTAIC MODULE MANUFACTURING

Transparent silicone copolymers as encapsulant for photovoltaic modules

Task

• Reduce processing time for module encapsulation

• Ensure reliable high electrical insulation of PV systems

Solution TECTOSIL ® 177

• Silicone based highly transparent thermoplastic copolymer film

• Fast processing with already existing equipment

• Superior isolation properties

• Enabling easy module recycling

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 7

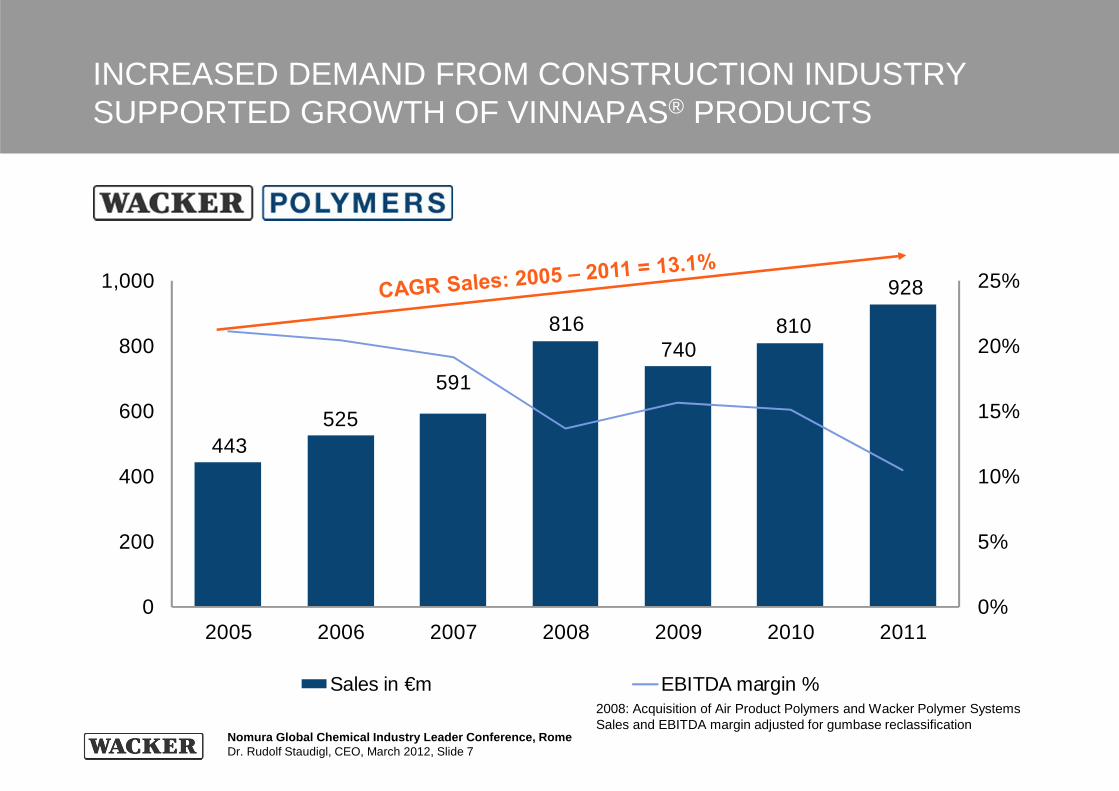

443525

591

816740

810

928

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1,000

2005 2006 2007 2008 2009 2010 2011

Sales in €m EBITDA margin %

INCREASED DEMAND FROM CONSTRUCTION INDUSTRY SUPPORTED GROWTH OF VINNAPAS® PRODUCTS

2008: Acquisition of Air Product Polymers and Wacker Polymer SystemsSales and EBITDA margin adjusted for gumbase reclassification

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 8

DISPERSIONS FOR VARIOUS APPLICATIONS –SUBSTITUTING COMPETING TECHNOLOGIES

ADHESIVES

COATINGS

ENGINEERED FABRICS

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 9

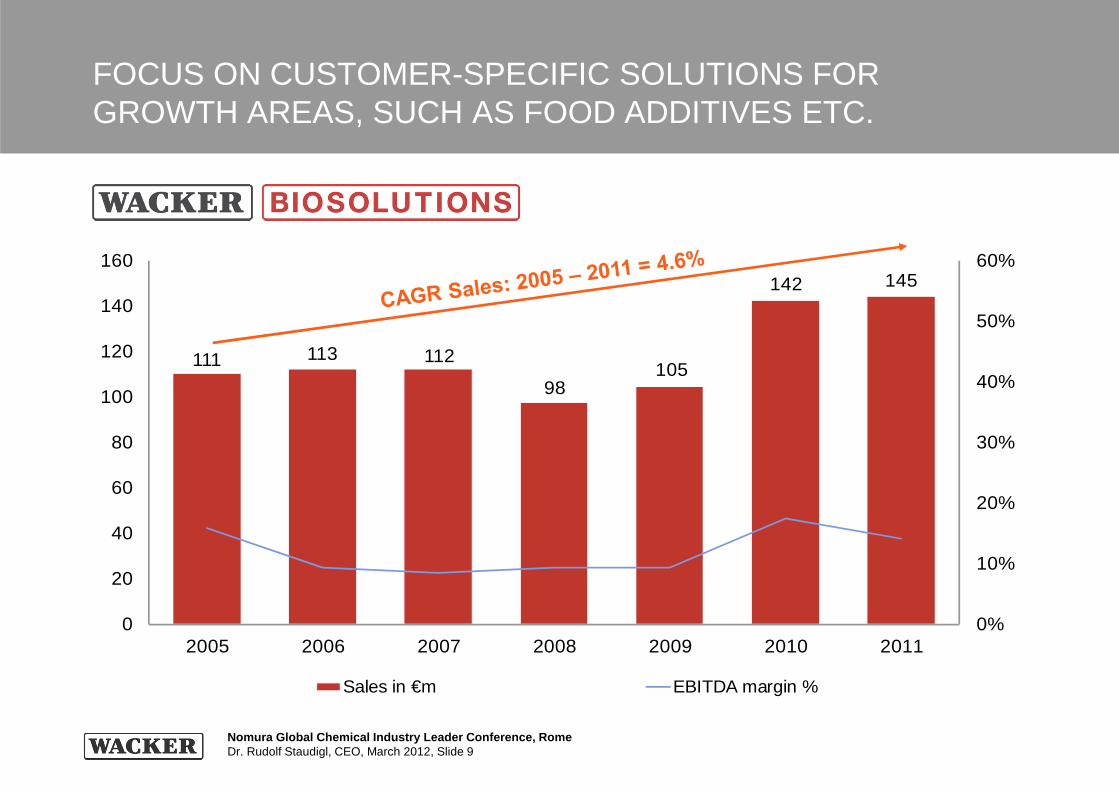

111 113 112

98105

142 145

0%

10%

20%

30%

40%

50%

60%

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010 2011

Sales in €m EBITDA margin %

FOCUS ON CUSTOMER-SPECIFIC SOLUTIONS FOR GROWTH AREAS, SUCH AS FOOD ADDITIVES ETC.

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 10

NEW APPLICATIONS DRIVE GROWTH IN CYCLODEXTRINS

Cyclodextrin Effects and Selected Applications

Beverages

Vitamin & Catechin water,Catechin-rich green tea

Dietary Supplements

CoQ10-γ-CD complex

Cyclodextrins enables the following effect (examples):- Masking- Stabilizing- Making bioavailable

WACKER is the only manufacturer of Cyclodextrins with a world-scale plant able to produce all types: Alpha-, Beta- and Gamma-Cyclodextrins.

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 11

SUPPLYING THE LEADING SUBSTRATE FOR FAST GROWING INDUSTRIES: SOLAR AND SEMI

288 326457

828

1,121

1,369

1,448

0%

10%

20%

30%

40%

50%

60%

0

300

600

900

1,200

1,500

1,800

2005 2006 2007 2008 2009 2010 2011

Sales in €m EBITDA margin %

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 12

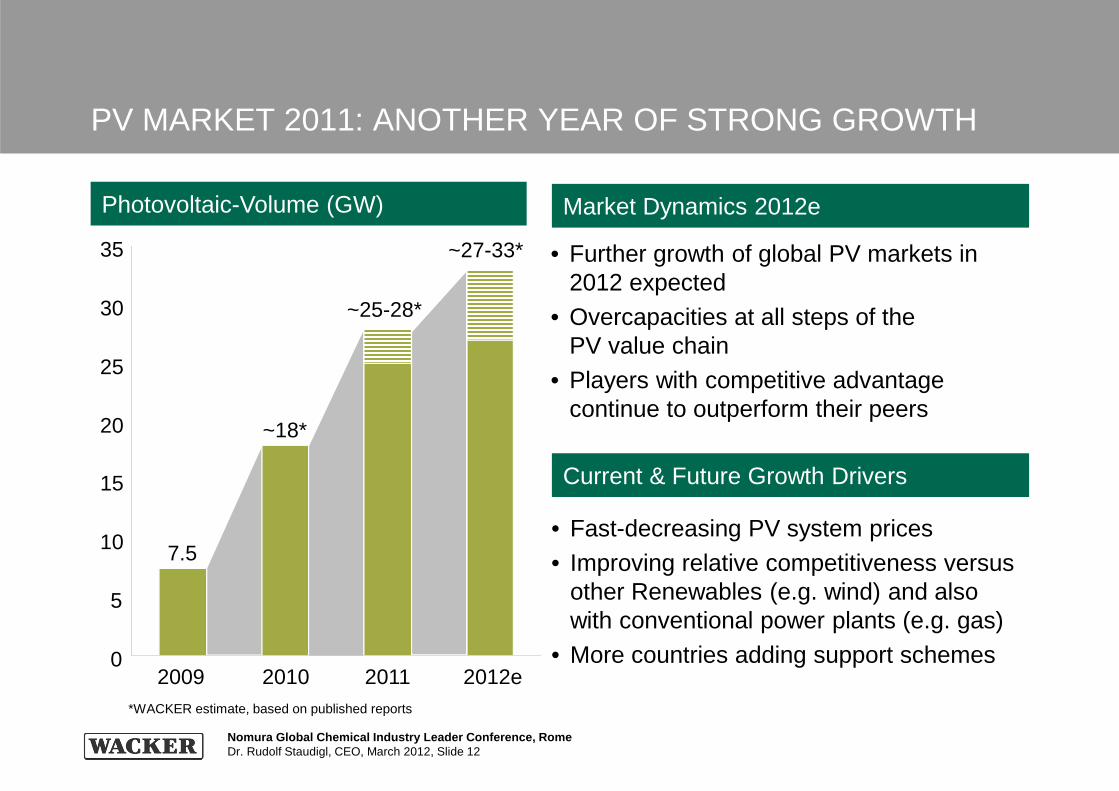

PV MARKET 2011: ANOTHER YEAR OF STRONG GROWTH

Photovoltaic-Volume (GW) Market Dynamics 2012e

• Further growth of global PV markets in 2012 expected

• Overcapacities at all steps of the PV value chain

• Players with competitive advantage continue to outperform their peers

• Fast-decreasing PV system prices • Improving relative competitiveness versus

other Renewables (e.g. wind) and also with conventional power plants (e.g. gas)

• More countries adding support schemes

Current & Future Growth Drivers

*WACKER estimate, based on published reports

7.5

~18*

~25-28*

~27-33*

0

5

10

15

20

25

30

35

2009 2010 2011 2012e

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 13

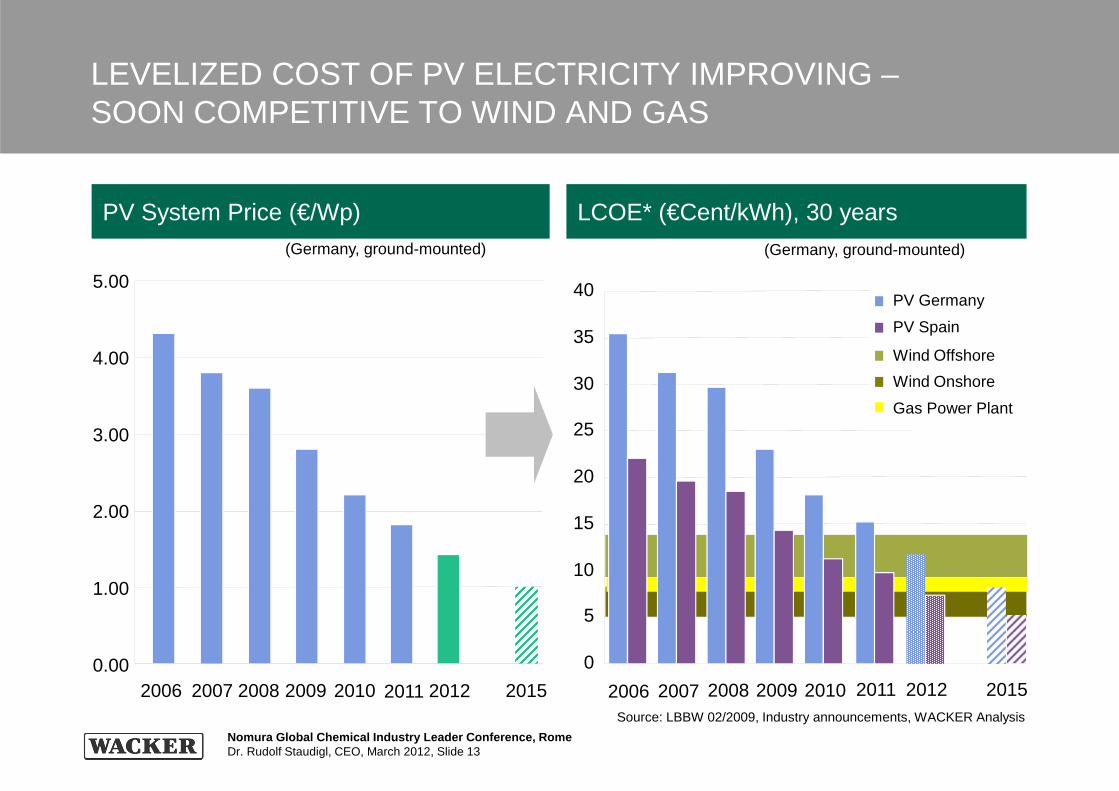

LEVELIZED COST OF PV ELECTRICITY IMPROVING –SOON COMPETITIVE TO WIND AND GAS

0.00

1.00

2.00

3.00

4.00

5.00

2006 2007 2008 2009 2010 2012 2015

PV System Price (€/Wp) LCOE* (€Cent/kWh), 30 years

0

5

10

15

20

25

30

35

40

2006 2007 2008 2009 2010 2012 2015

(Germany, ground-mounted) (Germany, ground-mounted)

2011 2011

PV Germany

PV Spain

Wind Offshore

Wind Onshore

Gas Power Plant

Source: LBBW 02/2009, Industry announcements, WACKER Analysis

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 14

CONTINUOUS TREND TOWARDS INCREASING MODULE EFFICIENCIES FAVORS ADVANCED C-SI TECHNOLOGY

Development of Module Efficiencies (%) Comments

Source: market surveys, industry announcements, WACKER estimates

• Module efficiencies are continuously increasing – highest efficiencies with monocrystalline solar cells

• CdTe based modules are losing ground compared to c-Si technology

• Module efficiencies with high impact on overall module manufacturing costs

• High quality polysilicon supports highest solar cell efficiencies and best practice processes, yields & cost structures

6

8

10

12

14

16

18

20

2005 2006 2007 2008 2009 2010 2011

Mainstream Mono

Mainstream Multi

CdTe

Super Mono

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 15

GROWING WITH THE MARKET – FULL PRODUCTION POTENTIAL AT ALL PLATFORMS UP TO 150KT

The ramp of Poly 11 plant in Tennessee will start in late 2013

Actual Polysilicon Shipments and Planned Year-End Capacities (kt)

6

18

118

32

30

52

2006 2007 2008 2009 2010 2011 2012e 2014e

70

Year-End Capacities

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 16

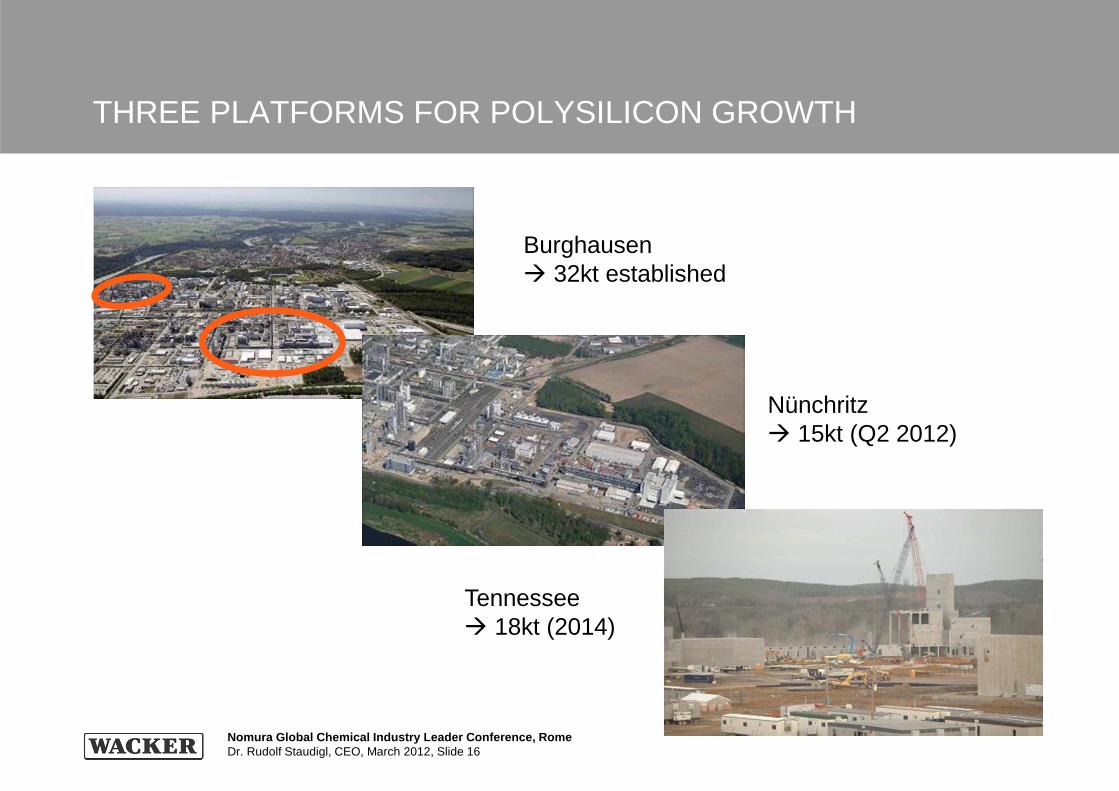

THREE PLATFORMS FOR POLYSILICON GROWTH

Burghausen� 32kt established

Nünchritz� 15kt (Q2 2012)

Tennessee� 18kt (2014)

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 17

300 350

FOUR LEADING POLYSILICON PRODUCERS WITH COMPETITIVE ADVANTAGE

50 150 250

Estimated demand2012€/kg

MT200100

SUPPLIER# 10 - n

SUPPLIERTop 4

SUPPLIER# 5-9

Relative Cost Position of Polysilicon Competitors

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 18

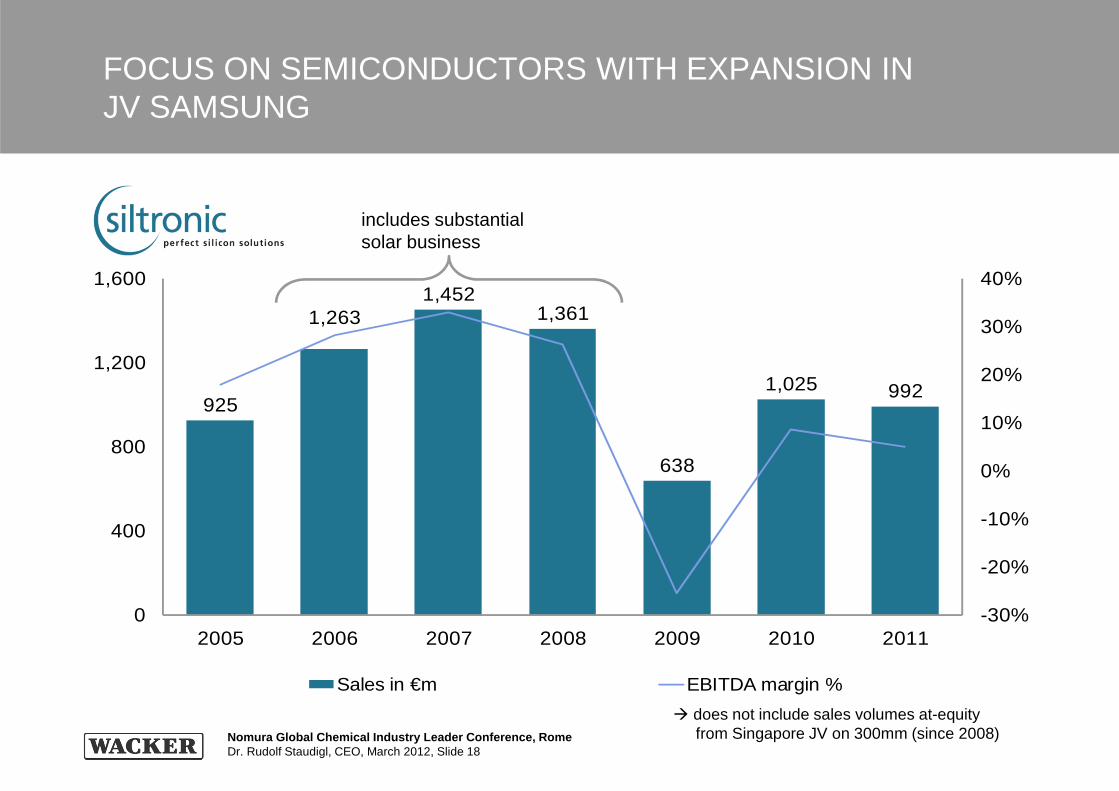

FOCUS ON SEMICONDUCTORS WITH EXPANSION IN JV SAMSUNG

925

1,2631,452

1,361

638

1,025 992

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

400

800

1,200

1,600

2005 2006 2007 2008 2009 2010 2011

Sales in €m EBITDA margin %

includes substantial solar business

� does not include sales volumes at-equity from Singapore JV on 300mm (since 2008)

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 19

SD in 150mm-equivalent

200 mm

300 mm

2011: DEMAND FOR SMALL DIAMETERS CONSIDERABLY REDUCED – 300 MM MARKET LESS AFFECTED

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 20

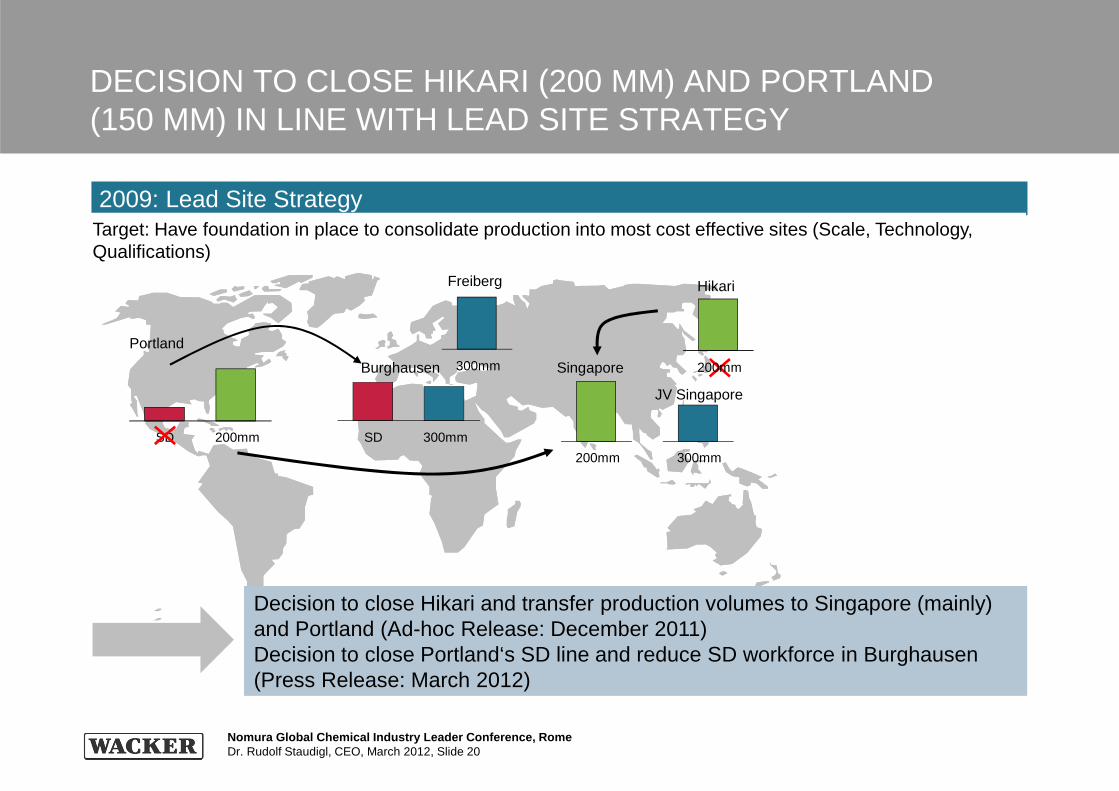

Burghausen

Freiberg

Portland

Singapore

Hikari

JV Singapore

SD 200mm SD 300mm

300mm

200mm 300mm

200mm

DECISION TO CLOSE HIKARI (200 MM) AND PORTLAND (150 MM) IN LINE WITH LEAD SITE STRATEGY

Decision to close Hikari and transfer production volumes to Singapore (mainly) and Portland (Ad-hoc Release: December 2011)Decision to close Portland‘s SD line and reduce SD workforce in Burghausen (Press Release: March 2012)

2009: Lead Site StrategyTarget: Have foundation in place to consolidate production into most cost effective sites (Scale, Technology, Qualifications)

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 21

SILTRONIC FOCUSES ON INVESTMENT IN SSW (PARTNERSHIP WITH SAMSUNG)

• Fab in operations since mid 2008

• Attractive cost position

• Further capacity increase from debottlenecking

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 22

WACKER: GOOD PERFORMANCE IN A DIFFICULT ENVIRONMENT

in €m FY 2011 FY 2010 Change in %

Sales 4,910 4,748 3

EBITDA 1,104 1,195 -8

EBITDA margin 22% 25% -

EBIT 603 765 -21

EBIT margin 12% 16% -

Result for the period 356 497 -28

EPS in € 7.10 9.88 -28

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 23

42% 44%

37% 37%

8% 9%

12% 10%

12/31/11 12/31/10

FinancialDebt

PensionAccruals

Accruals &Liabilities

Equity

WACKER MAINTAINS SOLID FINANCIAL STRUCTURE

Characteristics 12/31/11Assets

Total €6.2bn €5.5n

LiabilitiesTotal

€6.2bn €5.5bn

Balance Sheet (%)• Noncurrent assets: €3,996m

• Securities, cash and cash equivalents: €874m

• Provisions for pensions: €527m

• Net financial receivables: €96m

• Equity: €2,630m

• Total advance payments received (12/31/11): €1,203m

• Capex: €981m

• Schuldscheindarlehen (promissory notes) for €300m issued in Feb, 201261% 61%

25% 25%

14% 14%

12/31/11 12/31/10

Securities,Cash & Cash E.

CurrentAssets

NoncurrentAssets

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 24

OUTLOOK 2012: MACROECONOMIC UNCERTAINTIES PREVAILING

• Macroeconomic environment• Prevailing macro uncertainties, impacting corporate financing / project financing• Germany expected flat• Growth in the U.S. and emerging countries (e.g., China, India)• Potential revaluation of Euro vs. other leading currencies

• WACKER industries• Chemicals:

• market expected to grow in 2012• less impact from raw material inflation

• Solar industry:• world market with further growth in 2012 • still overcapacities throughout value chain

• Semiconductors:• overall, no significant growth in 2012 expected• split development: 300 mm wafers growing, smaller diameters declining

Nomura Global Chemical Industry Leader Conference, RomeDr. Rudolf Staudigl, CEO, March 2012, Slide 25

THANK YOU FOR YOUR INTEREST

Q1 2012 RESULTS WILL BE PUBLISHED ONMAY 4th, 2012