NMI 103 Financial Management Principles - ASU Guides for NMI/NMI_103... · NMI 103 – Financial...

79

Timely, relevant knowledge and tools for today’s nonprofit professional. A Professional Development Entity of the NMI 103 Financial Management Principles Version 1.2 Mail Code 4120 ▪ 411 N. Central Ave ▪ Suite 500 ▪ Phoenix, AZ 85004-0691 ▪ 602-496-0500 ▪ Fax: 602-496-0952 http://nmi.asu.edu ▪ http://lodestar.asu.edu

Transcript of NMI 103 Financial Management Principles - ASU Guides for NMI/NMI_103... · NMI 103 – Financial...

Timely, relevant knowledge and tools for today’s nonprofit professional.

A Professional Development Entity of the

NMI 103 Financial Management Principles

Version 1.2

Mail Code 4120 ▪ 411 N. Central Ave ▪ Suite 500 ▪ Phoenix, AZ 85004-0691 ▪ 602-496-0500 ▪ Fax: 602-496-0952 http://nmi.asu.edu ▪ http://lodestar.asu.edu

Copyright © 2014 Arizona Board of Regents for and on behalf of the ASU Lodestar Center for Philanthropy and Nonprofit Innovation, College of Public Programs, Arizona State University.

Copying of Materials Expressly Prohibited.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the express written permission of the ASU Lodestar Center, except for brief quotations in critical reviews. The authors may be reached at the ASU Lodestar Center, 411 N. Central Ave., Suite 500, Phoenix, AZ 85004-0691

TABLE OF CONTENTS

COURSE OVERVIEW __________________________________________________ 2

Description ___________________________________________________________ 2 Course Schedule ______________________________________________________ 2 Course Methods _______________________________________________________ 2 Course Map __________________________________________________________ 3 Learning Objectives ____________________________________________________ 4

DAY ONE ____________________________________________________________ 4

Intro of Course Participants and Major Financial Governance Players _____________ 5 Accounting Basics – Key Financial Terms ___________________________________ 8 Cash Versus Accural Accounting _________________________________________ 16 Standard Set of External Financial Statements ______________________________ 19 Financial Reports 1: Statement of Financial Position __________________________ 21 Financial Reports 2: Statement of Activities _________________________________ 27 Financial Reports 3: Statement of Functional Expenses _______________________ 33 Financial Reports 4: Statement of Cash Flow _______________________________ 35 Financial Reports: Accountants Report and Footnotes ________________________ 37 Contribution versus Exchange Transactions ________________________________ 46

DAY TWO __________________________________________________________ 49

Internal Controls ______________________________________________________ 50 Five Internal Controls for the Very Small Nonprofit _________________________ 52

Financial Planning and Budgeting ________________________________________ 55 Meaningful Budget Work by the Board ___________________________________ 56 Youth Education Skills (YES) Organization _______________________________ 62

Presentation of Budget _________________________________________________ 67 Tax Form 990 – A Public Relations Tool ___________________________________ 67

APPENDIX __________________________________________________________ 71

Key Financial Terms_________________________________________________ 71 Pet Rescue Budget Answers __________________________________________ 75 By Groups to Analyze 990s ___________________________________________ 76

© NMI 103 – Financial Management Principles | Participant Guide 1

Course Overview Description In this course, you will learn how to read, interpret, and manage a nonprofit organization from a standard set of financial statements. You will also learn basic accounting principles and the importance of internal controls to protect the assets of your organization. Finally, you will learn how to analyze and use tax form 990, along with your organization’s annual report, as a public relations tool.

Course Schedule Friday: 9:00 a.m. – 5:00 p.m. Saturday: 9:00 a.m. – 5:00 p.m.

Course Methods Learning in this course will occur through your active participation in large and small group discussions. You’ll also complete brief, un-graded exercises based on instructor-generated presentations, articles, case studies, and other Internet or media resources. As adult learners, you bring a rich array of prior knowledge, skills, and experience to build on and share with each other. Facilitating the exchange of new and existing information is a key method NMI instructors use to expand your learning and enable you to immediately apply that learning to your nonprofit organization and your career.

2 NMI 103 – Financial Management Principles | Participant Guide ©

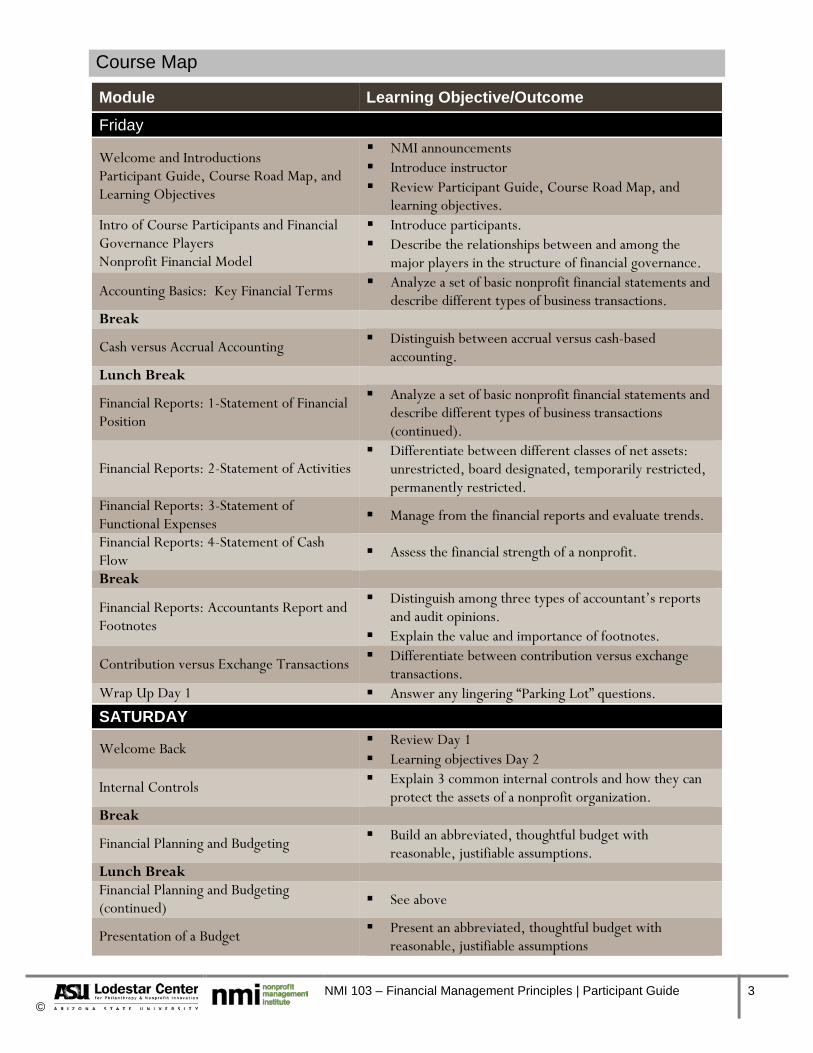

Course Map

Module Learning Objective/Outcome Friday

Welcome and Introductions Participant Guide, Course Road Map, and Learning Objectives

NMI announcements Introduce instructor Review Participant Guide, Course Road Map, and

learning objectives. Intro of Course Participants and Financial Governance Players Nonprofit Financial Model

Introduce participants. Describe the relationships between and among the

major players in the structure of financial governance.

Accounting Basics: Key Financial Terms Analyze a set of basic nonprofit financial statements and describe different types of business transactions.

Break

Cash versus Accrual Accounting Distinguish between accrual versus cash-based accounting.

Lunch Break

Financial Reports: 1-Statement of Financial Position

Analyze a set of basic nonprofit financial statements and describe different types of business transactions (continued).

Financial Reports: 2-Statement of Activities Differentiate between different classes of net assets:

unrestricted, board designated, temporarily restricted, permanently restricted.

Financial Reports: 3-Statement of Functional Expenses Manage from the financial reports and evaluate trends.

Financial Reports: 4-Statement of Cash Flow Assess the financial strength of a nonprofit.

Break

Financial Reports: Accountants Report and Footnotes

Distinguish among three types of accountant’s reports and audit opinions.

Explain the value and importance of footnotes.

Contribution versus Exchange Transactions Differentiate between contribution versus exchange transactions.

Wrap Up Day 1 Answer any lingering “Parking Lot” questions.

SATURDAY

Welcome Back Review Day 1 Learning objectives Day 2

Internal Controls Explain 3 common internal controls and how they can protect the assets of a nonprofit organization.

Break

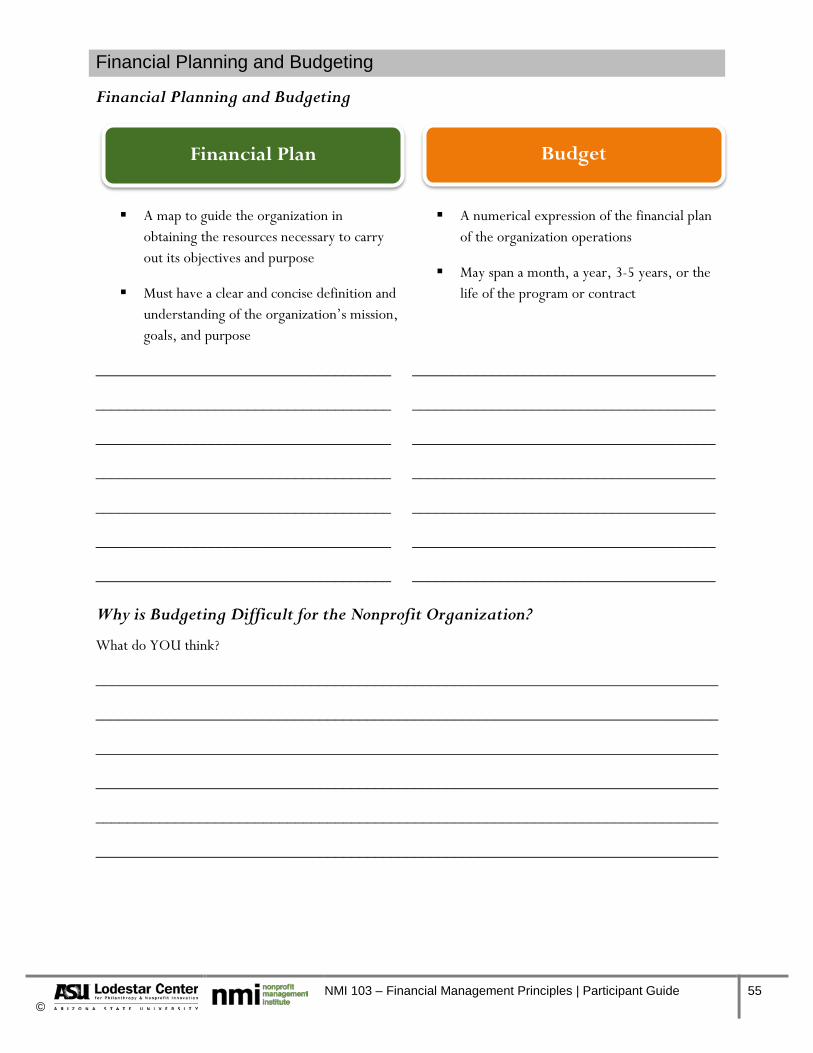

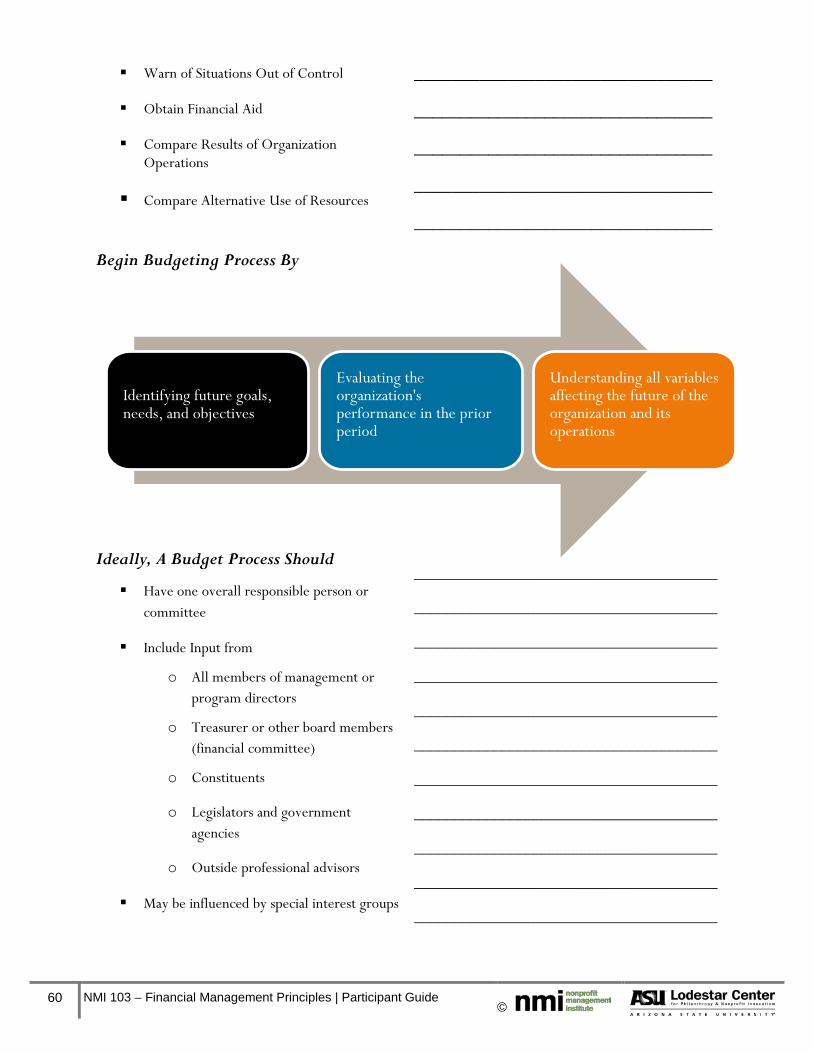

Financial Planning and Budgeting Build an abbreviated, thoughtful budget with reasonable, justifiable assumptions.

Lunch Break Financial Planning and Budgeting (continued) See above

Presentation of a Budget Present an abbreviated, thoughtful budget with reasonable, justifiable assumptions

© NMI 103 – Financial Management Principles | Participant Guide 3

Module Learning Objective/Outcome Break

Tax Form 990 – A Public Relations Tool Analyze the main components of a Tax Form 990,

explain where the public can find them, and how they can be used as a public relations tool

Course Wrap-Up Answer any lingering “Parking Lot” questions

Learning Objectives After taking this course, you will be able to do the following:

Describe the relationships between and among the major players in the structure of financial

governance.

Analyze a set of basic nonprofit financial statements and describe different types of business transactions.

Distinguish between accrual versus cash based accounting.

Differentiate between different classes of net assets.

Analyze financial reports and evaluate trends.

Determine the financial strength of a nonprofit.

Distinguish among three types of accountant’s reports and audit opinions.

Differentiate between contribution versus exchange transactions.

Explain common internal controls and how they can protect the assets of an organization.

Develop a budget with reasonable, justifiable assumptions.

Analyze the main components of a 990; explain where the public can find them, and how they can be used as a public relations tool.

4 NMI 103 – Financial Management Principles | Participant Guide ©

Day One

Intro of Course Participants and Major Financial Governance Players

Introducing Course Participants

Pair Share with a Partner…

Your name

Your title

Your organization

What challenges, concerns, or specific needs do you have about financial management in your organization?

______________________________________________________________________________

______________________________________________________________________________

What is your role with regard to financial management?

______________________________________________________________________________

______________________________________________________________________________

Sketch and share a simple organization chart of all the major financial players in your organization

© NMI 103 – Financial Management Principles | Participant Guide 5

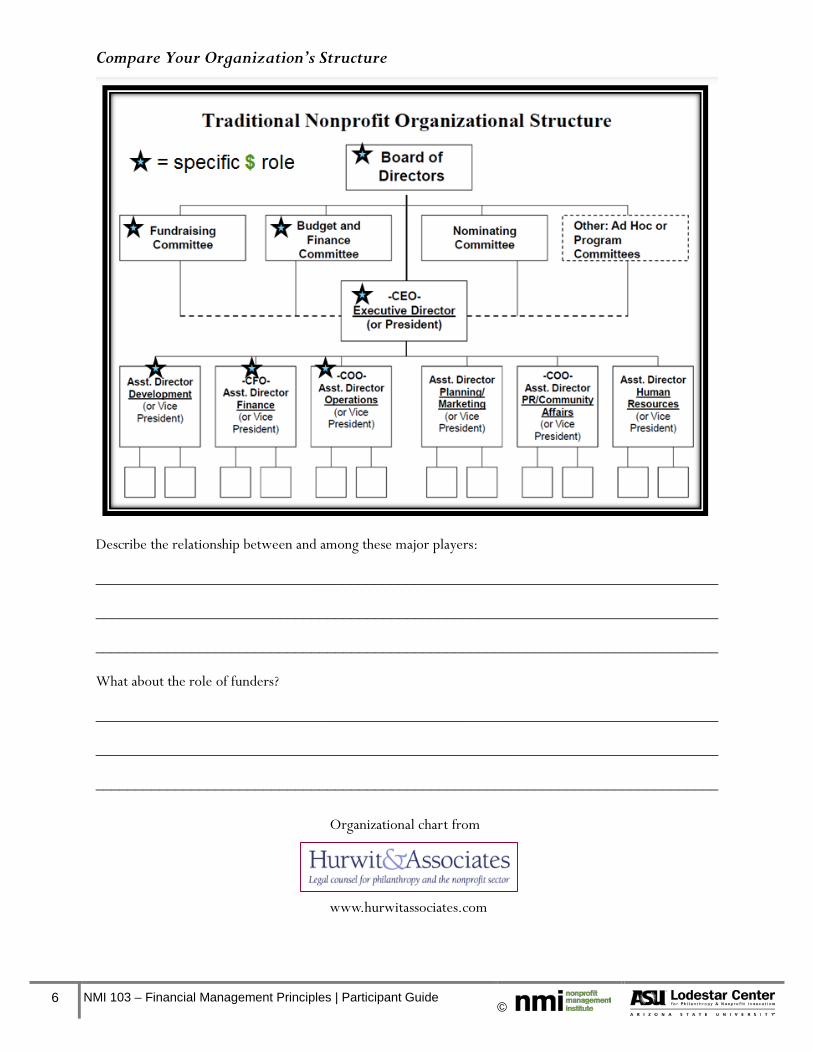

Compare Your Organization’s Structure

Describe the relationship between and among these major players:

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

What about the role of funders?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Organizational chart from

www.hurwitassociates.com

6 NMI 103 – Financial Management Principles | Participant Guide ©

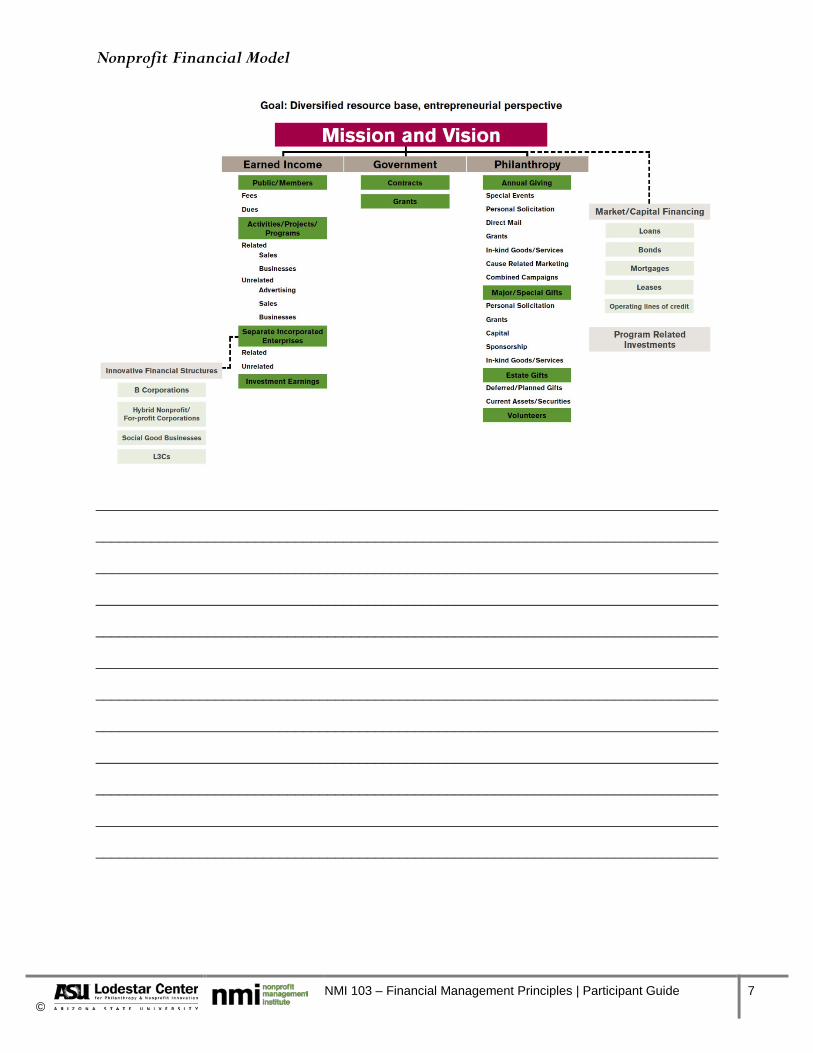

Nonprofit Financial Model

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 7

Accounting Basics – Key Financial Terms Matching Exercise

Instructions: Even if you are unsure about your answers, make your best guess about the definitions and descriptions for the following key financial terms.

Match the financial term with its definition.

a. Calendar Year b. Fiscal Year c. Asset

d. Liability e. Net Assets f. Revenues

g. Expenses h. Depreciation

1. _____ Contributions and earnings that increase the overall net assets of the organization and/or decrease liabilities.

2. _____ Costs and payments that represent the use of assets to operate an organization for fundraising, programs, or management and general.

3. _____ Annual reporting cycle that ends on a date, usually the last day of a month, other than December 31.

4. _____ The amount of assets in excess of liabilities. Also, the accumulation of revenues in excess of expenses since the inception of the organization.

5. _____ Items of economic obligations of the organization to outsiders (and in some cases for future periods)

6. _____ Cash and economic resources that are expected to benefit future cash inflows or help reduce future cash outflows.

7. _____ A process of allocating the cost of a long-lived asset or how much of an asset’s value has been used up.

8. _____ Annual reporting cycle that ends on December 31.

8 NMI 103 – Financial Management Principles | Participant Guide ©

Mark an “A” next to the item, if it is an ASSET. Mark an “L,” if it is a LIABILITY.

9. _____ Cash and cash equivalents 10. _____ Fixed assets

11. _____ Deferred revenues 12. _____ Accounts receivable

13. _____ Accounts payable 14. _____ Cash received in advance of performing service

15. _____ Inventory 16. _____ Prepaid expenses

17. _____ Accrued expenses 18. _____ Notes payable

Match the type of financial report with its description.

a. Statement of Financial Position b. Statement of Activities

c. Statement of Cashflows d. Statement of Functional Expenses

19. _____ Only required by Voluntary Health & Welfare organizations, this provides additional detail about the expenses of the organization and reports how much of the expenses were in direct support of the organization’s programs, how much was for management and general activities and how much was for fundraising.

20. _____ Reports revenues and expenses. Revenues over expenses (net income) or expenses over revenue (net loss). When added to net assets at the end of last year must equal the end of this year’s net assets.

21. _____ Reports financial assets, liabilities and net assets of the organization. Total assets must equal liabilities plus net assets.

22. _____ Reports operations, investing and financing activities that affected the amount of cash on hand throughout the year.

Match the type of accountants’ reports with its description. a. Compilation b. Audit c. Agreed-Upon-Procedures

d. Review e. Single Audit

22. _____ A report issued by an outside independent CPA when that CPA has done some limited testing of the financial information. The report does not express an opinion on the accuracy of the financial information, but rather states whether or not any misstatements came to their attention during the limited testing.

23. _____ A report issued by an outside independent CPA on findings based on specific procedures performed related to a financial statement component or other written assertion as requested by the client. The report does not express an opinion on the accuracy of the financial statements or internal

© NMI 103 – Financial Management Principles | Participant Guide 9

controls taken as a whole, but rather reports on the results of certain agree-upon tests of the financial management system.

24. _____ A report issued by an outside CPA when that CPA has taken information, provided by management, and put it into the form of a financial statement. The CPA does not do any testing of the information provided and, accordingly, does not express an opinion or provide any assurance of the accuracy of the financial information provided.

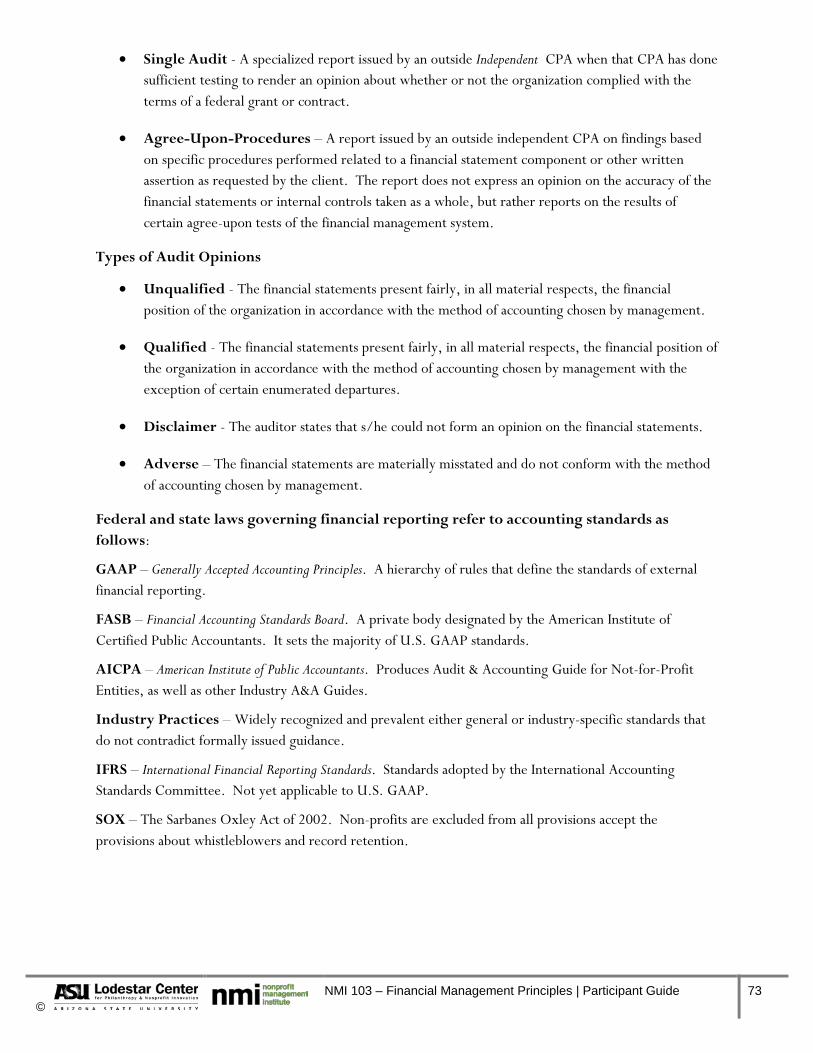

25. _____ A specialized report issued by an outside Independent CPA when that CPA has done sufficient testing to render an opinion about whether or not the organization complied with the terms of a federal grant or contract.

26. _____ A report issued by an outside independent CPA when that CPA has done sufficient testing of the financial information to be able to render an opinion about whether or not the financial information fairly represents the financial position of the organization in all material respects when the financial statements are taken as a whole.

Match the type of audit opinion with its description.

a. Unqualified b. Qualified c. Disclaimer d. Adverse

26. _____ The financial statements are materially misstated and do not conform with the method of accounting chosen by management.

27. _____ The auditor states that s/he could not form an opinion on the financial statements.

28. _____ The financial statements present fairly, in all material respects, the financial position of the organization in accordance with the method of accounting chosen by management.

29. _____ The financial statements present fairly, in all material respects, the financial position of the organization in accordance with the method of accounting chosen by management with the exception of certain enumerated departures.

10 NMI 103 – Financial Management Principles | Participant Guide ©

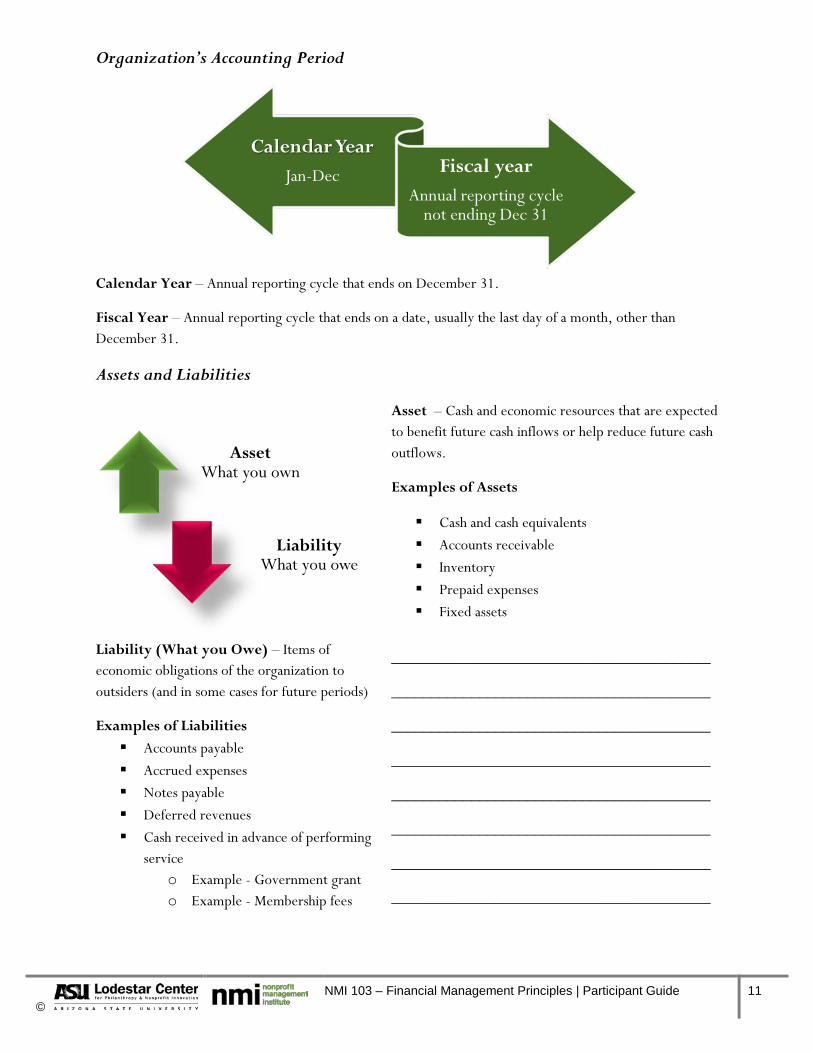

Organization’s Accounting Period

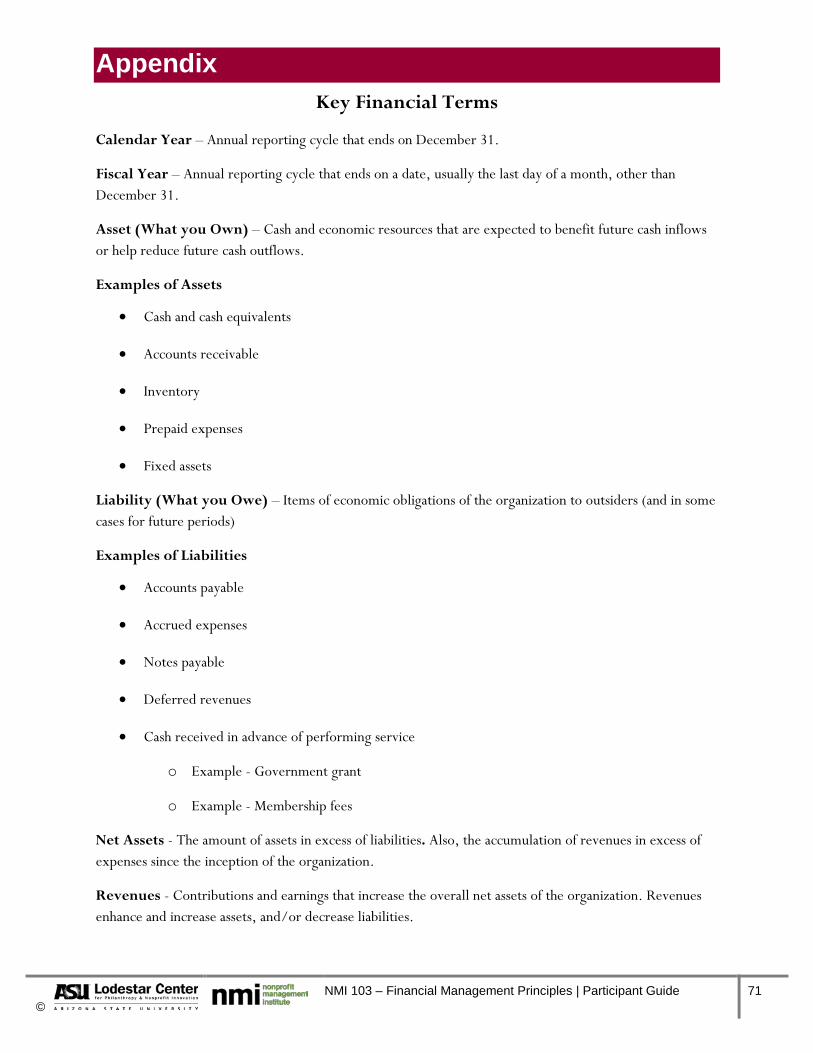

Calendar Year – Annual reporting cycle that ends on December 31.

Fiscal Year – Annual reporting cycle that ends on a date, usually the last day of a month, other than December 31.

Assets and Liabilities

Asset – Cash and economic resources that are expected to benefit future cash inflows or help reduce future cash outflows.

Examples of Assets

Cash and cash equivalents Accounts receivable Inventory Prepaid expenses Fixed assets

Liability (What you Owe) – Items of economic obligations of the organization to outsiders (and in some cases for future periods)

Examples of Liabilities Accounts payable Accrued expenses Notes payable Deferred revenues Cash received in advance of performing

service o Example - Government grant o Example - Membership fees

________________________________________

________________________________________

________________________________________

________________________________________

________________________________________

________________________________________

________________________________________

________________________________________

Asset What you own

Liability What you owe

© NMI 103 – Financial Management Principles | Participant Guide 11

Calendar YearJan-Dec Fiscal year

Annual reporting cycle not ending Dec 31

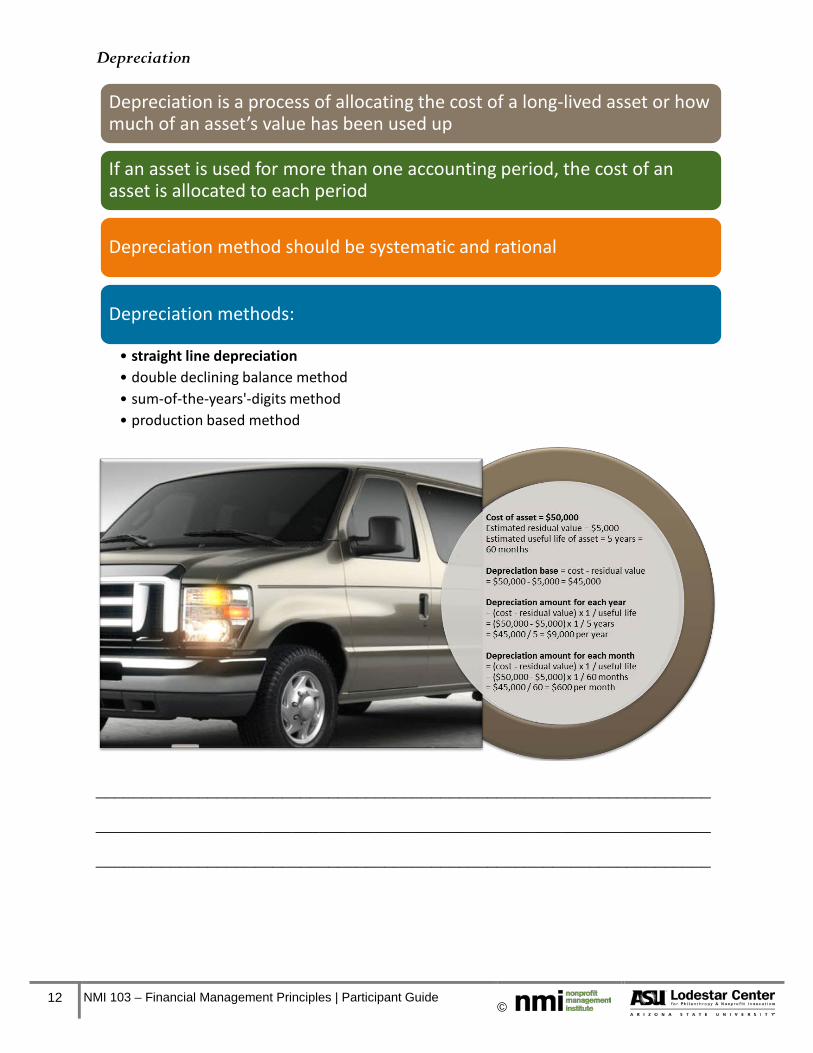

Depreciation

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

Depreciation is a process of allocating the cost of a long-lived asset or how much of an asset’s value has been used up

If an asset is used for more than one accounting period, the cost of an asset is allocated to each period

Depreciation method should be systematic and rational

Depreciation methods:

• straight line depreciation• double declining balance method• sum-of-the-years'-digits method• production based method

12 NMI 103 – Financial Management Principles | Participant Guide ©

Key Financial Terms on Statement of Activities

Types of Financial Reports

Statement of Financial Position - Reports financial assets, liabilities and net assets of the organization. Total assets must equal liabilities plus net assets.

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

Statement of Activities - Reports revenues and expenses. Revenues over expenses (net income) or expenses over revenue (net loss). When added to net assets at the end of last year, must equal the end of this year’s net assets.

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

Statement of Cashflows - Reports operations, investing, and financing activities that affected the amount of cash on hand throughout the year.

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

Net AssetsThe amount of assets in excess of liabilities. Also,the accumulation of revenues in excess of expenses since the inception of the organization.

RevenuesContributions and earnings that increase the overall net assets of the organization. Revenues enhance and increase assets, and/or decrease liabilities.

ExpensesCosts and payments that represent the use of assets to operate an organization. Expenses can be for fundraising, programs, or management and general.

© NMI 103 – Financial Management Principles | Participant Guide 13

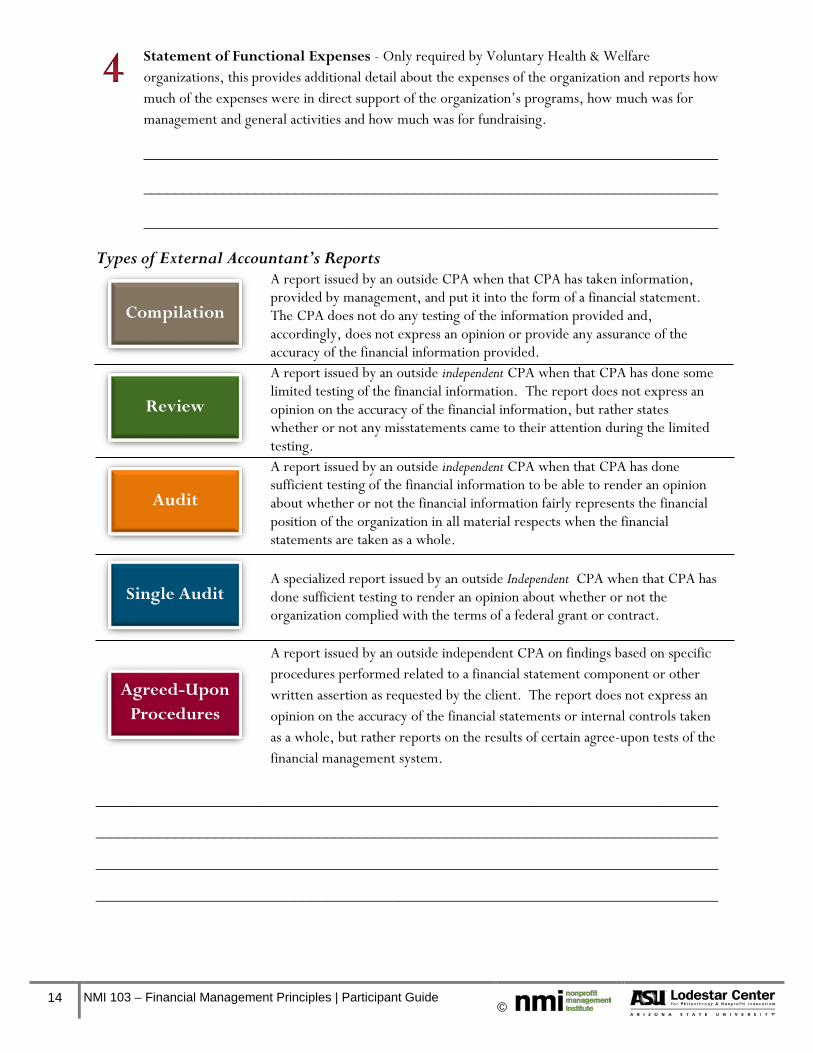

Statement of Functional Expenses - Only required by Voluntary Health & Welfare organizations, this provides additional detail about the expenses of the organization and reports how much of the expenses were in direct support of the organization’s programs, how much was for management and general activities and how much was for fundraising.

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

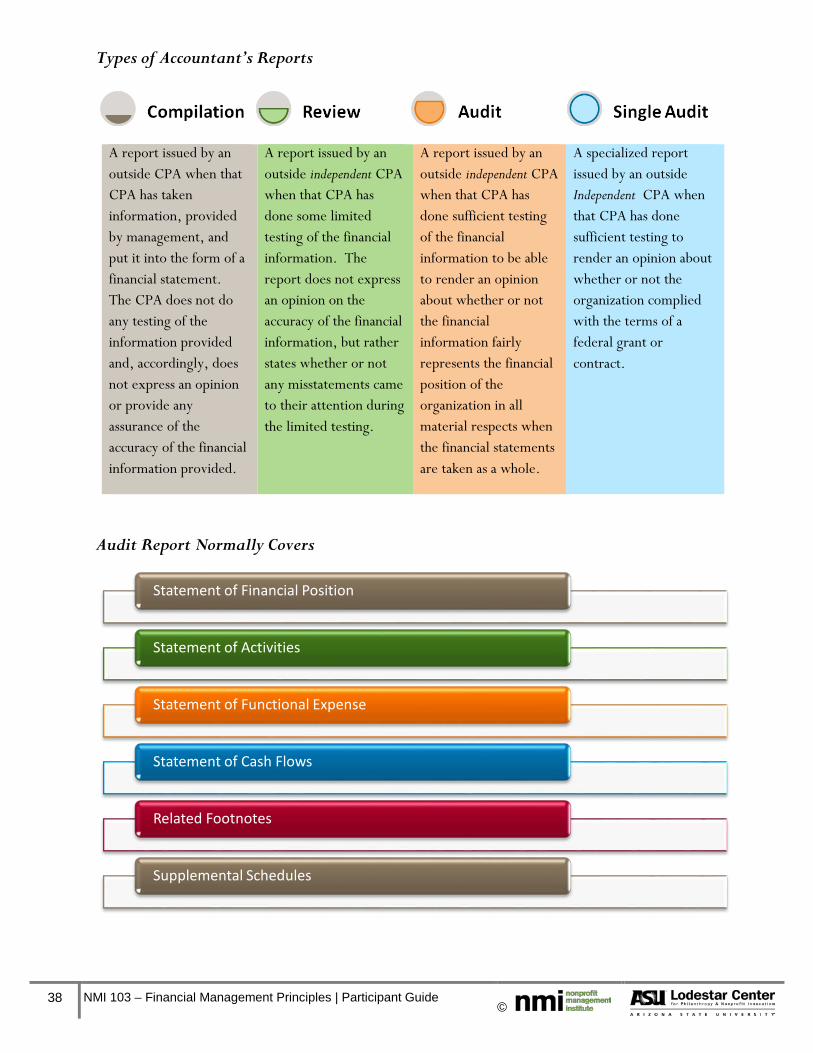

Types of External Accountant’s Reports

A report issued by an outside CPA when that CPA has taken information, provided by management, and put it into the form of a financial statement. The CPA does not do any testing of the information provided and, accordingly, does not express an opinion or provide any assurance of the accuracy of the financial information provided.

A report issued by an outside independent CPA when that CPA has done some limited testing of the financial information. The report does not express an opinion on the accuracy of the financial information, but rather states whether or not any misstatements came to their attention during the limited testing.

A report issued by an outside independent CPA when that CPA has done sufficient testing of the financial information to be able to render an opinion about whether or not the financial information fairly represents the financial position of the organization in all material respects when the financial statements are taken as a whole.

A specialized report issued by an outside Independent CPA when that CPA has done sufficient testing to render an opinion about whether or not the organization complied with the terms of a federal grant or contract.

A report issued by an outside independent CPA on findings based on specific procedures performed related to a financial statement component or other written assertion as requested by the client. The report does not express an opinion on the accuracy of the financial statements or internal controls taken as a whole, but rather reports on the results of certain agree-upon tests of the financial management system.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Compilation

Review

Audit

Single Audit

Agreed-Upon Procedures

14 NMI 103 – Financial Management Principles | Participant Guide ©

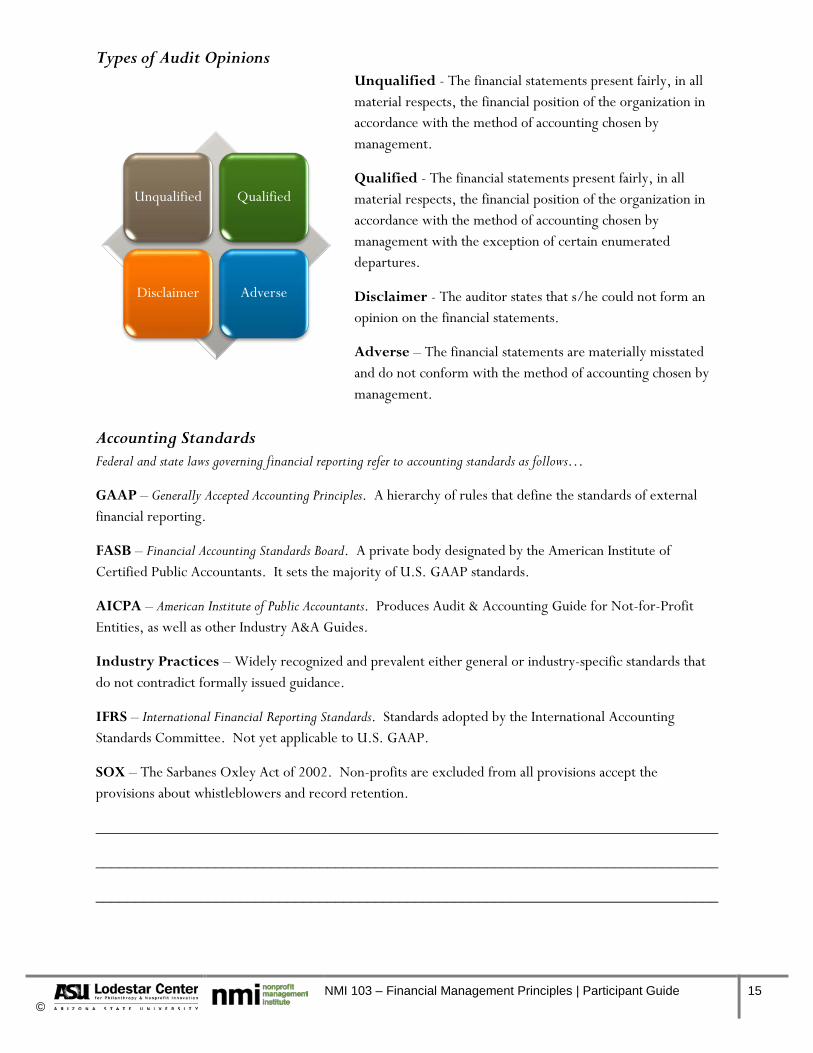

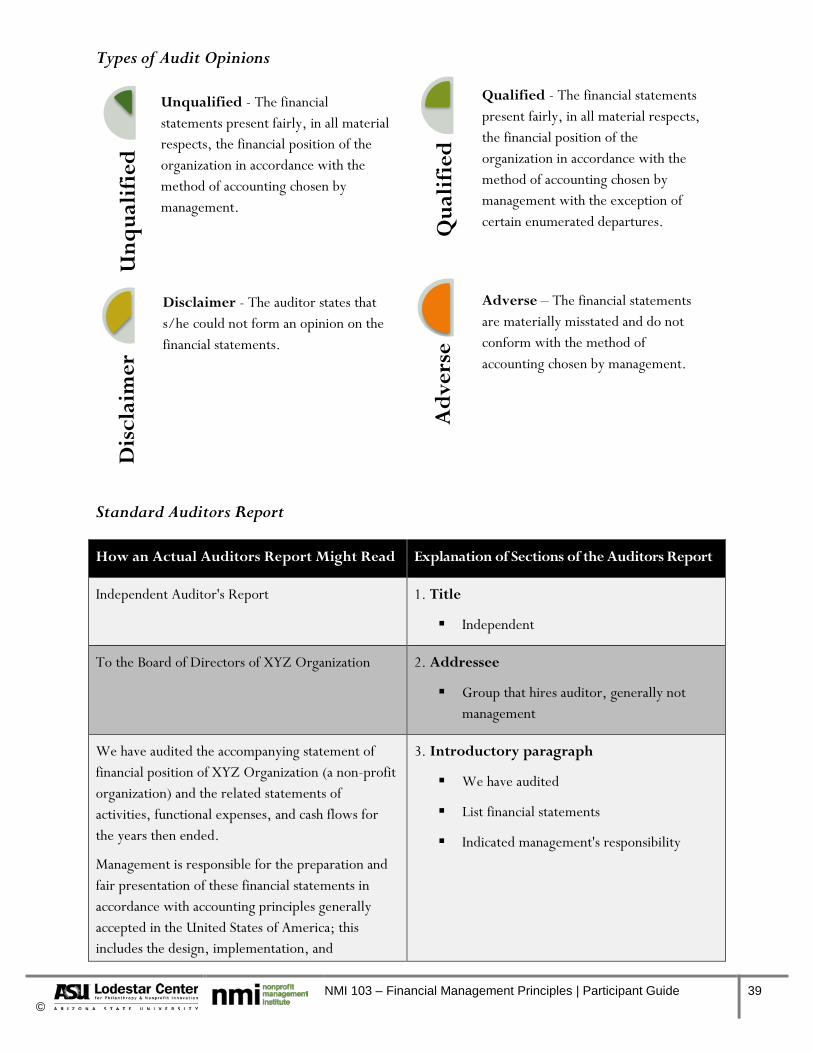

Types of Audit Opinions

Unqualified - The financial statements present fairly, in all material respects, the financial position of the organization in accordance with the method of accounting chosen by management.

Qualified - The financial statements present fairly, in all material respects, the financial position of the organization in accordance with the method of accounting chosen by management with the exception of certain enumerated departures.

Disclaimer - The auditor states that s/he could not form an opinion on the financial statements.

Adverse – The financial statements are materially misstated and do not conform with the method of accounting chosen by management.

Accounting Standards Federal and state laws governing financial reporting refer to accounting standards as follows…

GAAP – Generally Accepted Accounting Principles. A hierarchy of rules that define the standards of external financial reporting.

FASB – Financial Accounting Standards Board. A private body designated by the American Institute of Certified Public Accountants. It sets the majority of U.S. GAAP standards.

AICPA – American Institute of Public Accountants. Produces Audit & Accounting Guide for Not-for-Profit Entities, as well as other Industry A&A Guides.

Industry Practices – Widely recognized and prevalent either general or industry-specific standards that do not contradict formally issued guidance.

IFRS – International Financial Reporting Standards. Standards adopted by the International Accounting Standards Committee. Not yet applicable to U.S. GAAP.

SOX – The Sarbanes Oxley Act of 2002. Non-profits are excluded from all provisions accept the provisions about whistleblowers and record retention.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Unqualified Qualified

Disclaimer Adverse

© NMI 103 – Financial Management Principles | Participant Guide 15

Accrual Basis: Transactions are recorded as revenue is earned and expenses are incurred. Not tied to the receipt or payment of cash

Cash versus Accrual Accounting Cash versus Accrual Accounting Video

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

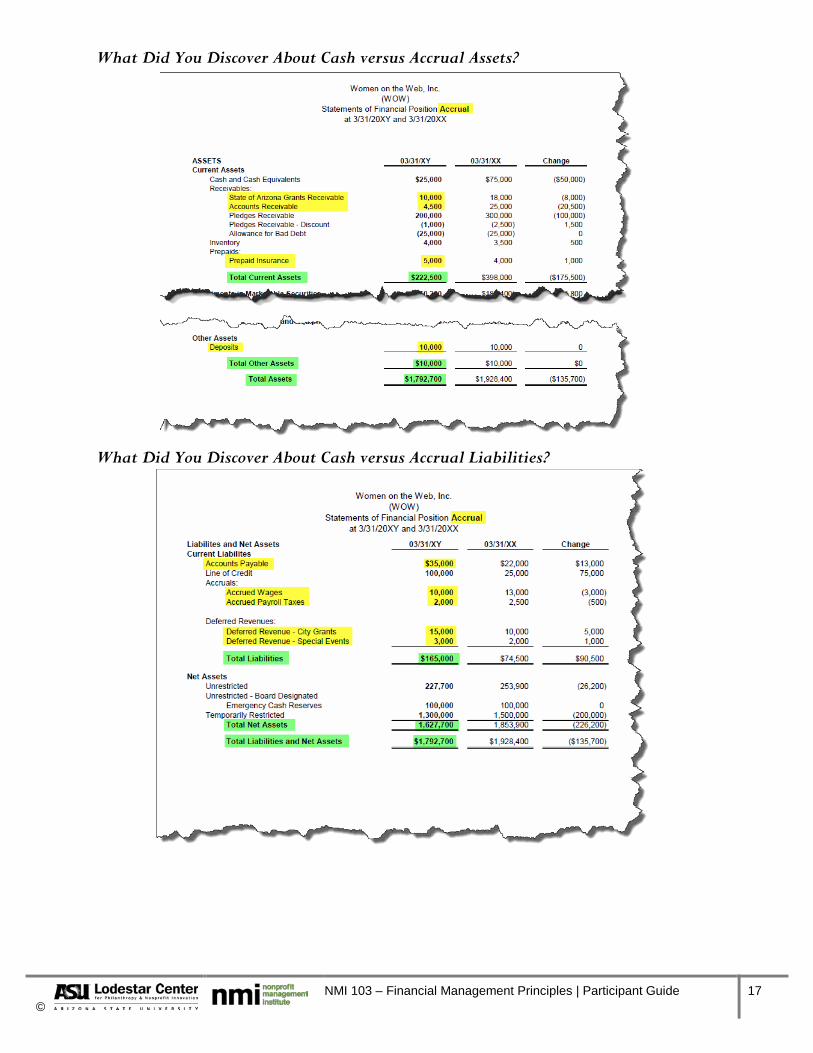

Open WOW Statements of Financial Position Accrual and WOW Statements of Financial Position Cash

Compare Cash versus Accrual Assets

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Compare Cash versus Accrual Liabilities

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Cash Basis: Transactions are recorded as cash is received and disbursed

16 NMI 103 – Financial Management Principles | Participant Guide ©

What Did You Discover About Cash versus Accrual Assets?

What Did You Discover About Cash versus Accrual Liabilities?

© NMI 103 – Financial Management Principles | Participant Guide 17

Effect on Financial Statements of Cash versus Accrual Accounting

Cash Accounting Versus Accrual Accounting

Instructions: Answer the following questions to determine the effect on financial statements that use cash accounting versus accrual accounting methods.

1. On December 31, 2011, a donor promises to send in $1,000 during 2012.

a. Does this create a change to the Cash financial statements or Accrual statements?

______________________________________________________________________________

2. The donor makes the promised payment of $1,000 early on March 15, 2012.

a. Does this create income to the Accrual Statement of Activities?

______________________________________________________________________________

b. Does this create income to the Cash Statement of Activities?

______________________________________________________________________________

3. Would the account called “Prepaid Insurance Expense” appear on the Cash Statement of Financial Position?

______________________________________________________________________________

4. Would the account called “Prepaid Insurance Expense” appear on the Accrual Statement of Financial Position?

______________________________________________________________________________

5. The organization that reports on a Cash basis receives a bill for Office Supplies for $300 and puts in the file to be paid in 15 days. Is there an impact on the Statement of Financial Position?

______________________________________________________________________________

6. In that instance for the Cash basis, is there an impact on the Cash basis Statement of Activities?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

7. The organization that reports on an Accrual basis receives a bill for Office Supplies for $300 and puts it in the file to be paid in 15 days. Is there an impact on the Statement of Financial Position?

18 NMI 103 – Financial Management Principles | Participant Guide ©

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

8. In that instance for the Accrual basis, is there an impact on the Accrual basis Statement of Activities?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

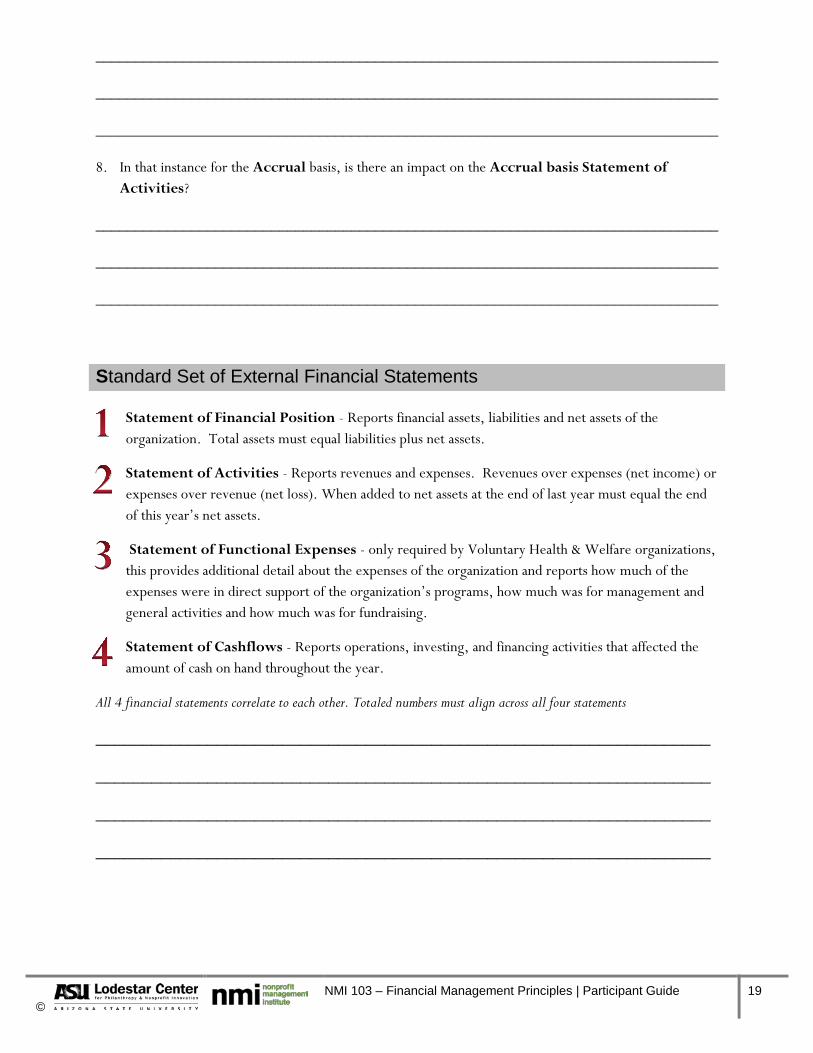

Standard Set of External Financial Statements

Statement of Financial Position - Reports financial assets, liabilities and net assets of the organization. Total assets must equal liabilities plus net assets.

Statement of Activities - Reports revenues and expenses. Revenues over expenses (net income) or expenses over revenue (net loss). When added to net assets at the end of last year must equal the end of this year’s net assets.

Statement of Functional Expenses - only required by Voluntary Health & Welfare organizations, this provides additional detail about the expenses of the organization and reports how much of the expenses were in direct support of the organization’s programs, how much was for management and general activities and how much was for fundraising.

Statement of Cashflows - Reports operations, investing, and financing activities that affected the amount of cash on hand throughout the year.

All 4 financial statements correlate to each other. Totaled numbers must align across all four statements

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 19

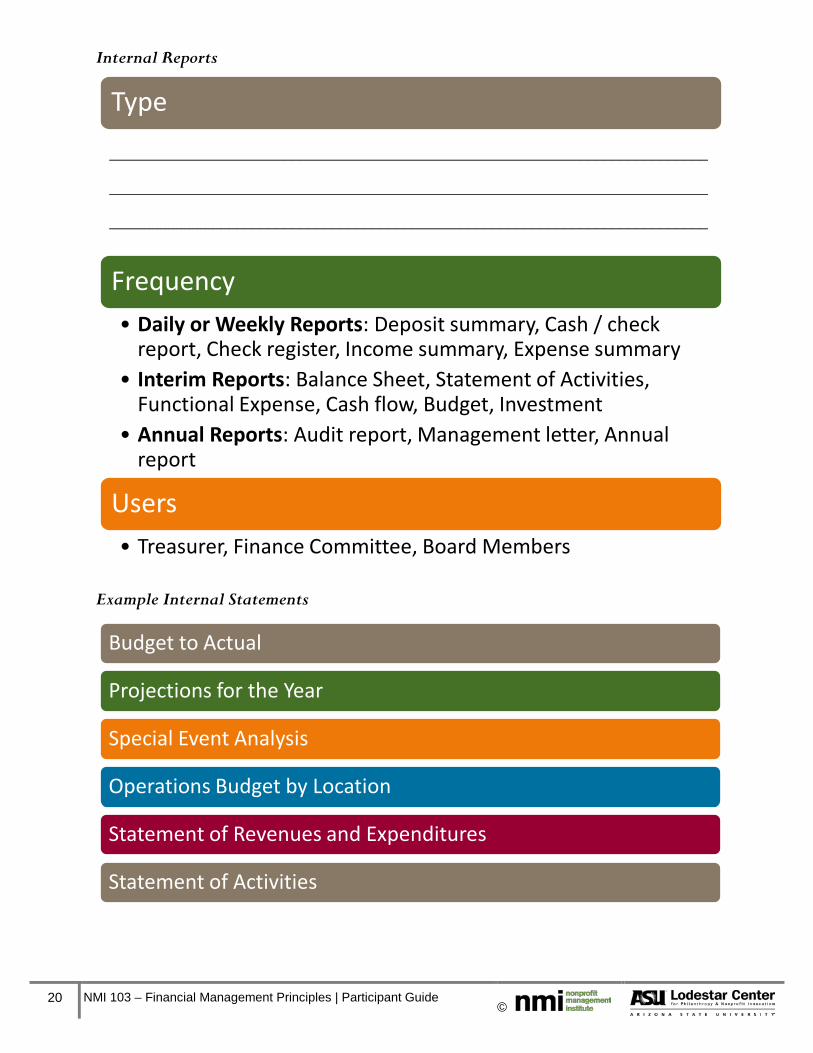

Internal Reports

Example Internal Statements

Type

Frequency• Daily or Weekly Reports: Deposit summary, Cash / check

report, Check register, Income summary, Expense summary• Interim Reports: Balance Sheet, Statement of Activities,

Functional Expense, Cash flow, Budget, Investment• Annual Reports: Audit report, Management letter, Annual

report

Users• Treasurer, Finance Committee, Board Members

Budget to Actual

Projections for the Year

Special Event Analysis

Operations Budget by Location

Statement of Revenues and Expenditures

Statement of Activities

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

20 NMI 103 – Financial Management Principles | Participant Guide ©

Why So Many Different Statements?

People within an organization need different statements (or levels of reporting) depending on their needs/role. For example…

Accountants or bookkeepers know details, how each statement relates to the other, and which statement is needed by members of an organization

An Executive Director needs all 4 statements and to know how the numbers across statements tie together and should be in agreement

Board members mainly need reports with high level numbers and not as much detail, unless a question arises

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

Financial Reports 1: Statement of Financial Position

Statement of Financial Position

A “snap shot” of what an organization ownsand owes at a moment in time (net worth)

© NMI 103 – Financial Management Principles | Participant Guide 21

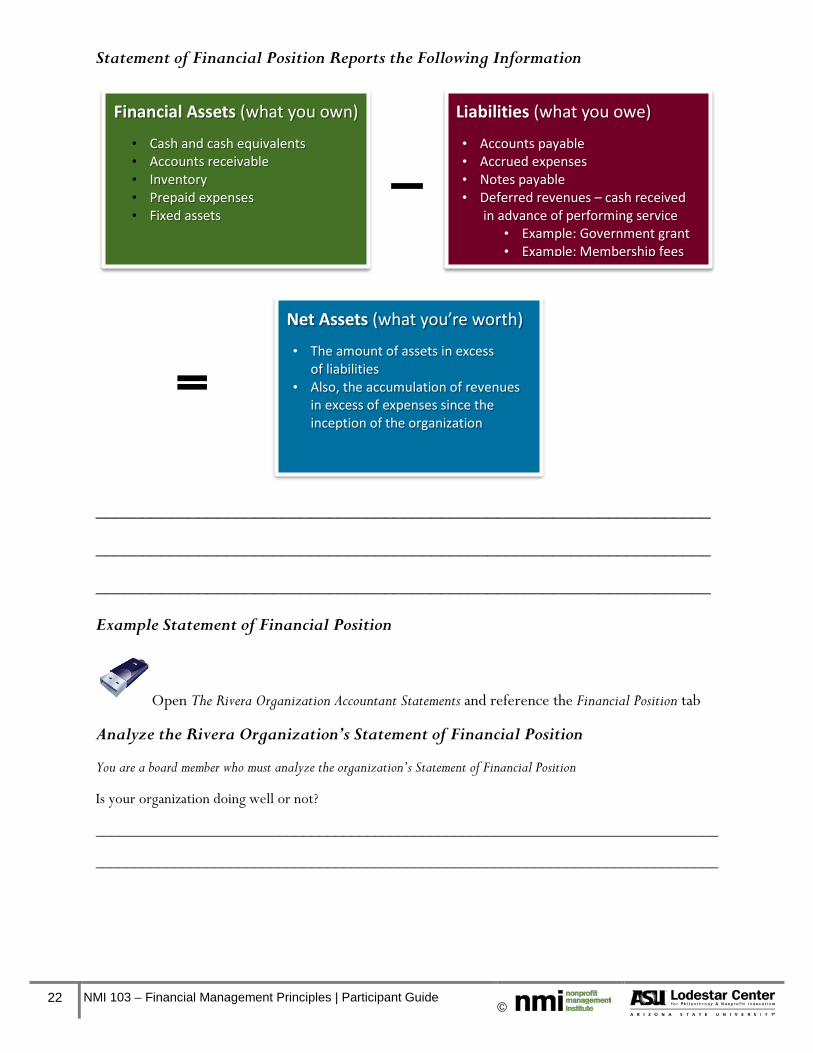

Statement of Financial Position Reports the Following Information

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

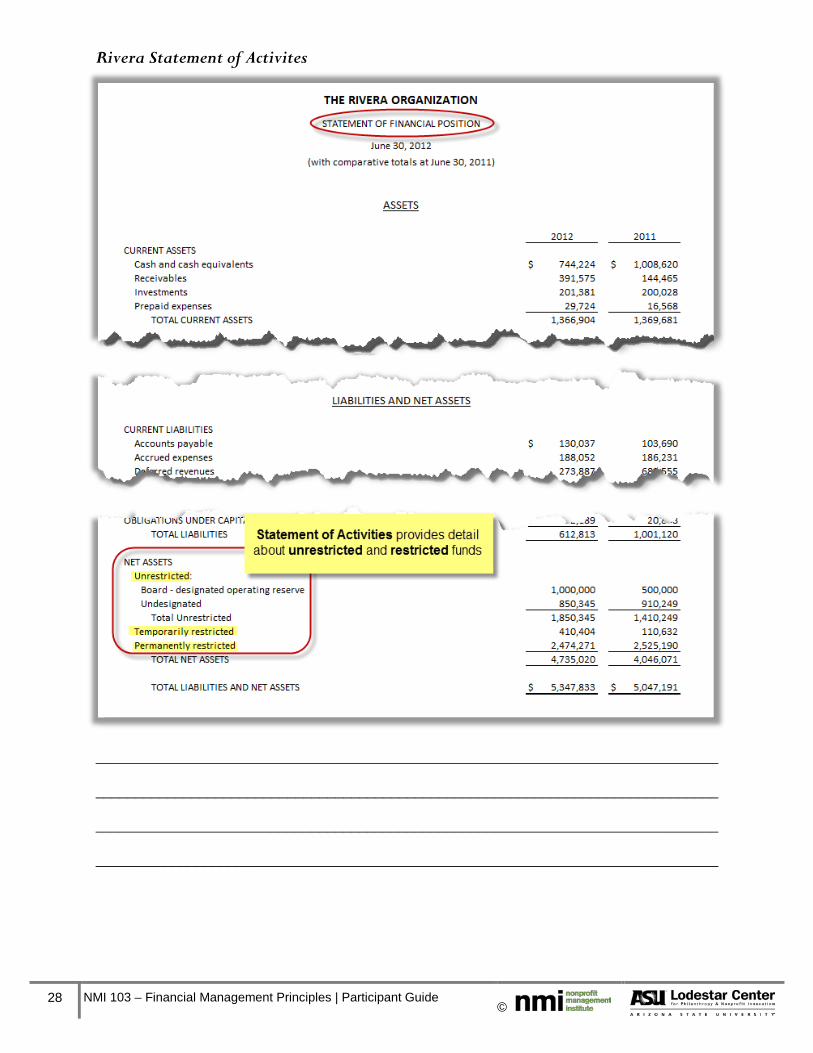

Example Statement of Financial Position

Open The Rivera Organization Accountant Statements and reference the Financial Position tab

Analyze the Rivera Organization’s Statement of Financial Position

You are a board member who must analyze the organization’s Statement of Financial Position

Is your organization doing well or not?

______________________________________________________________________________

______________________________________________________________________________

Financial Assets (what you own)

• Cash and cash equivalents • Accounts receivable • Inventory • Prepaid expenses • Fixed assets

Liabilities (what you owe)

• Accounts payable • Accrued expenses • Notes payable • Deferred revenues – cash received

in advance of performing service • Example: Government grant • Example: Membership fees

Net Assets (what you’re worth)

• The amount of assets in excess of liabilities

• Also, the accumulation of revenues in excess of expenses since the inception of the organization

22 NMI 103 – Financial Management Principles | Participant Guide ©

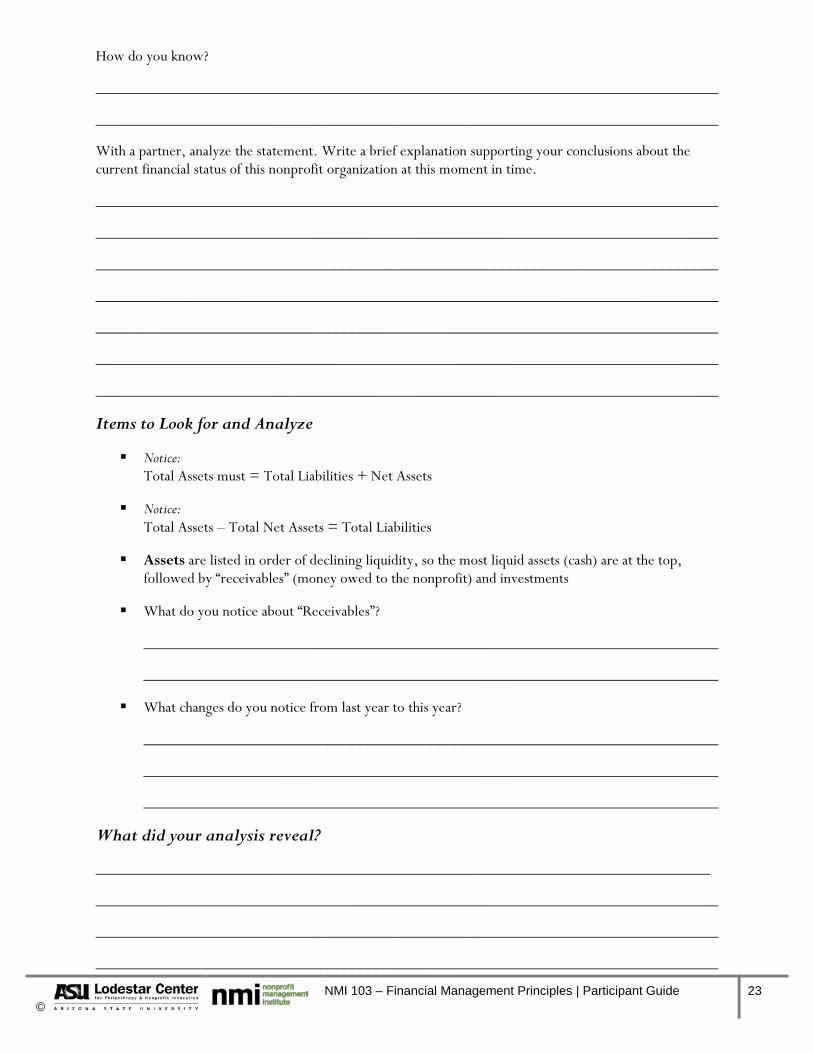

How do you know?

______________________________________________________________________________

______________________________________________________________________________

With a partner, analyze the statement. Write a brief explanation supporting your conclusions about the current financial status of this nonprofit organization at this moment in time.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Items to Look for and Analyze

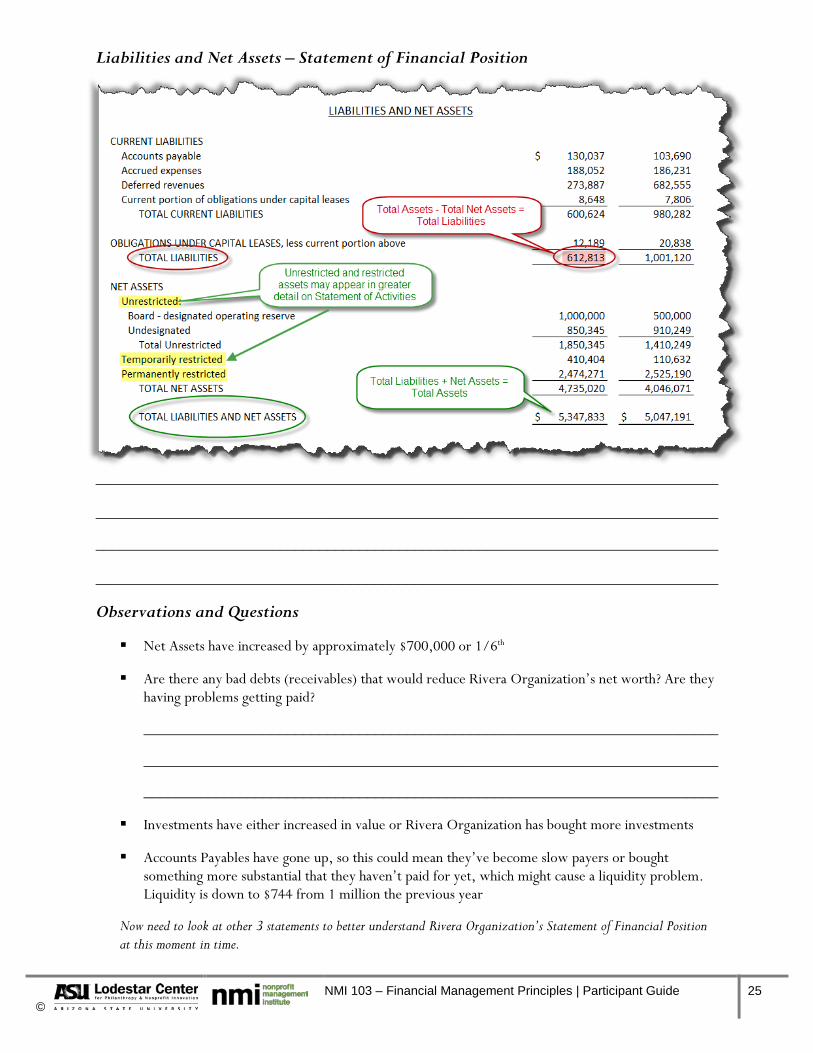

Notice: Total Assets must = Total Liabilities + Net Assets

Notice: Total Assets – Total Net Assets = Total Liabilities

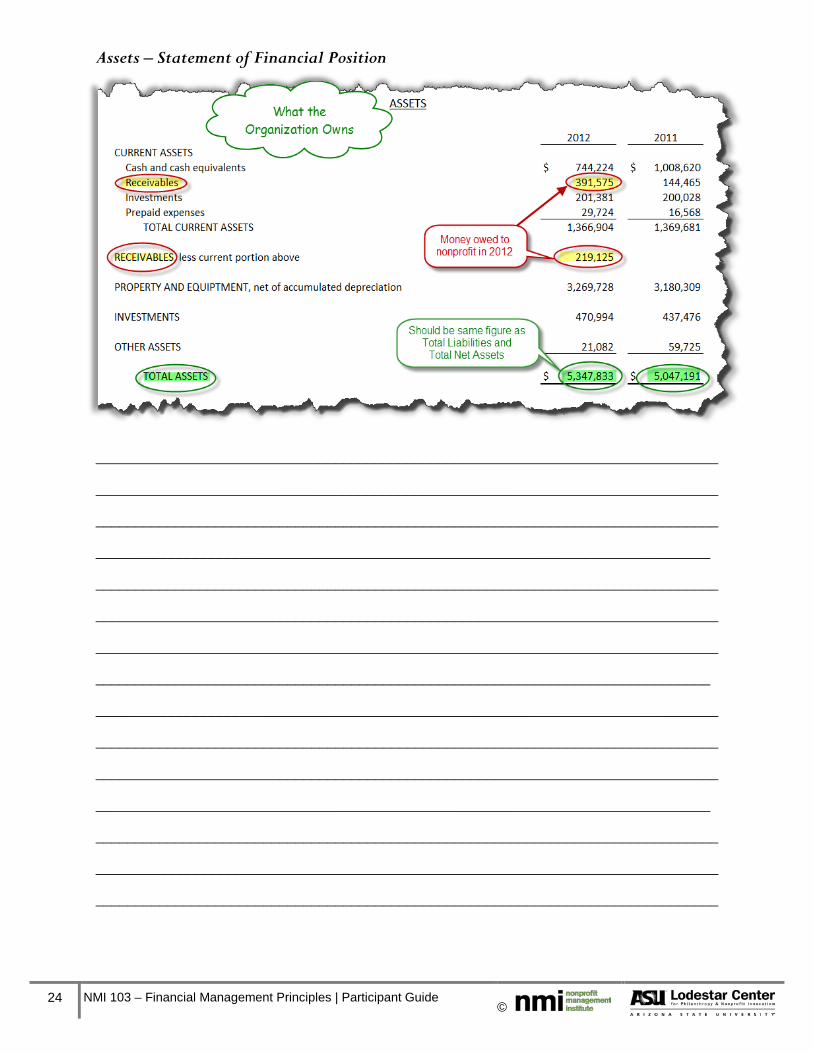

Assets are listed in order of declining liquidity, so the most liquid assets (cash) are at the top, followed by “receivables” (money owed to the nonprofit) and investments

What do you notice about “Receivables”?

________________________________________________________________________

________________________________________________________________________

What changes do you notice from last year to this year?

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

What did your analysis reveal?

_____________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 23

Assets – Statement of Financial Position

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

_____________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

_____________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

_____________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

24 NMI 103 – Financial Management Principles | Participant Guide ©

Liabilities and Net Assets – Statement of Financial Position

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Observations and Questions

Net Assets have increased by approximately $700,000 or 1/6th

Are there any bad debts (receivables) that would reduce Rivera Organization’s net worth? Are they having problems getting paid?

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

Investments have either increased in value or Rivera Organization has bought more investments

Accounts Payables have gone up, so this could mean they’ve become slow payers or bought something more substantial that they haven’t paid for yet, which might cause a liquidity problem. Liquidity is down to $744 from 1 million the previous year

Now need to look at other 3 statements to better understand Rivera Organization’s Statement of Financial Position at this moment in time.

© NMI 103 – Financial Management Principles | Participant Guide 25

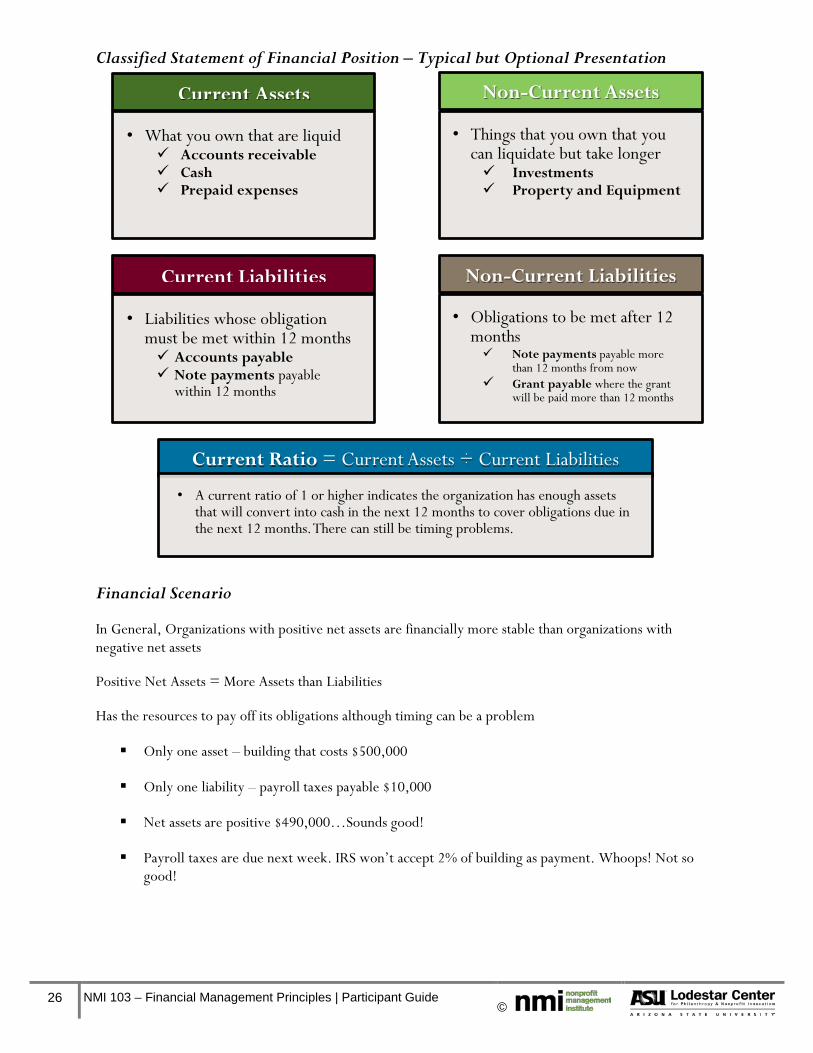

Classified Statement of Financial Position – Typical but Optional Presentation

Financial Scenario

In General, Organizations with positive net assets are financially more stable than organizations with negative net assets

Positive Net Assets = More Assets than Liabilities

Has the resources to pay off its obligations although timing can be a problem

Only one asset – building that costs $500,000

Only one liability – payroll taxes payable $10,000

Net assets are positive $490,000…Sounds good!

Payroll taxes are due next week. IRS won’t accept 2% of building as payment. Whoops! Not so good!

Current Assets

• What you own that are liquid Accounts receivable Cash Prepaid expenses

Non-Current Assets

• Things that you own that you can liquidate but take longer Investments Property and Equipment

Current Liabilities

• Liabilities whose obligation must be met within 12 months Accounts payable Note payments payable

within 12 months

Non-Current Liabilities

• Obligations to be met after 12 months Note payments payable more

than 12 months from now Grant payable where the grant

will be paid more than 12 months

Current Ratio = Current Assets ÷ Current Liabilities

• A current ratio of 1 or higher indicates the organization has enough assets that will convert into cash in the next 12 months to cover obligations due in the next 12 months. There can still be timing problems.

26 NMI 103 – Financial Management Principles | Participant Guide ©

Statement of Financial Position – Summary and Brief Discussion

Can a nonprofit organization have too much in net assets?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

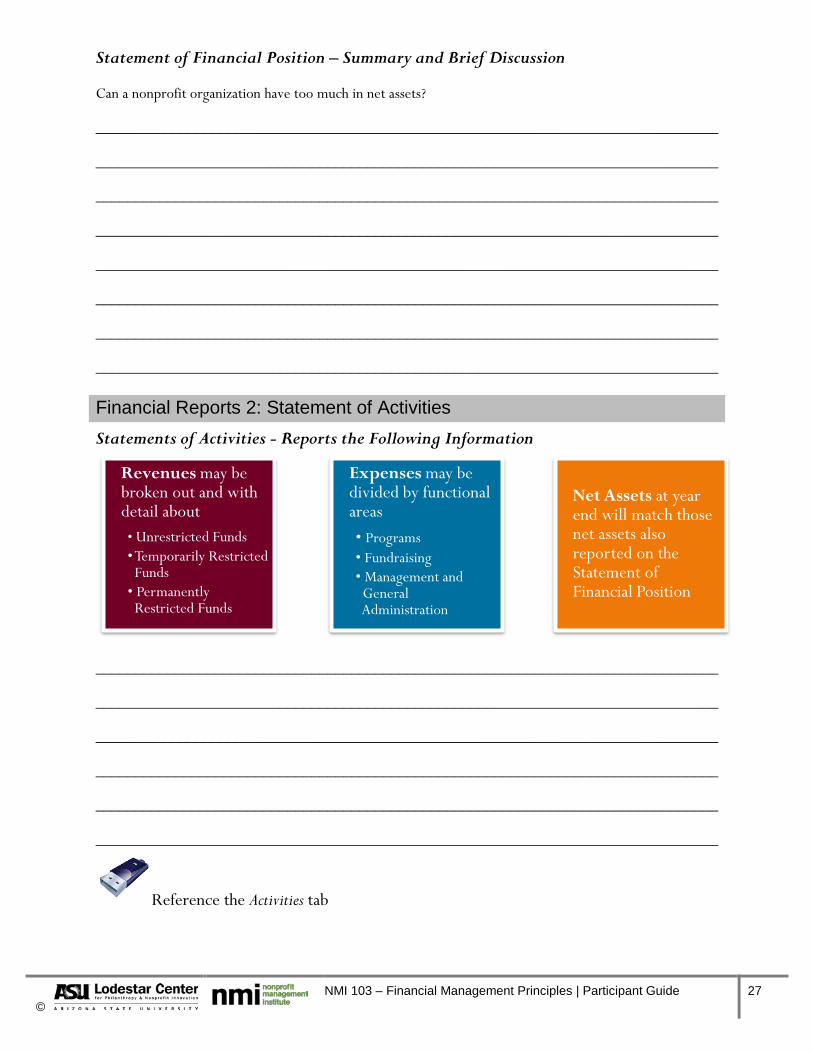

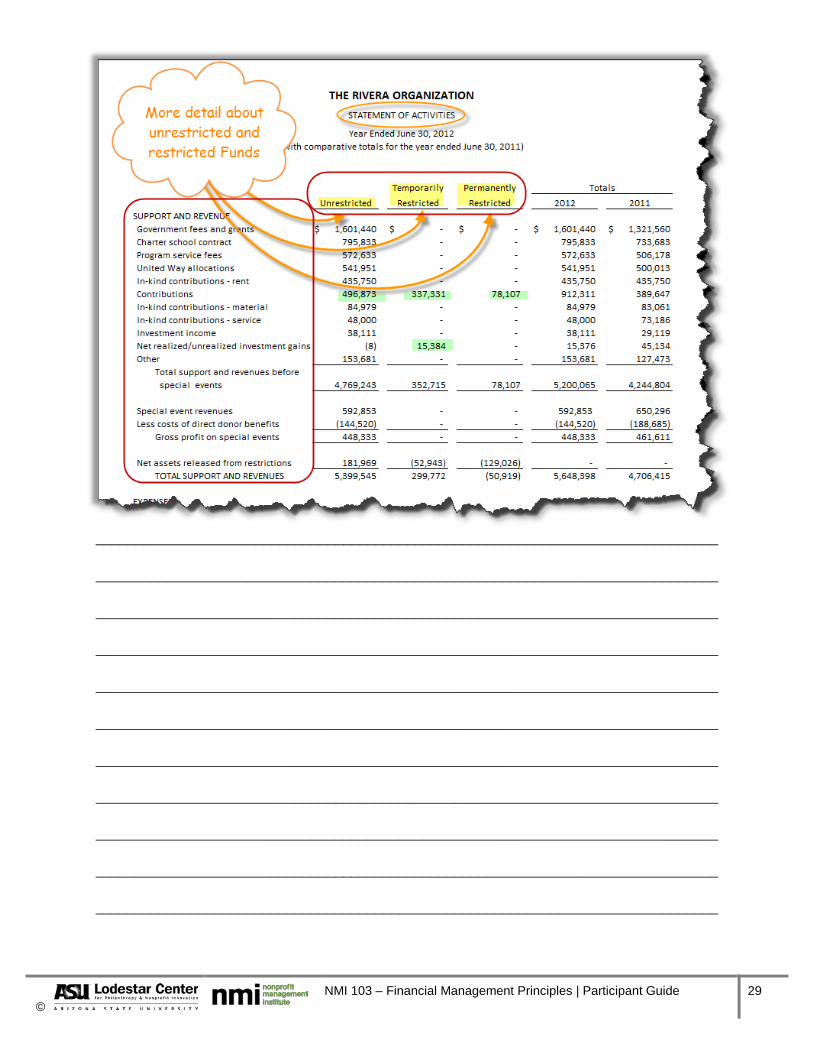

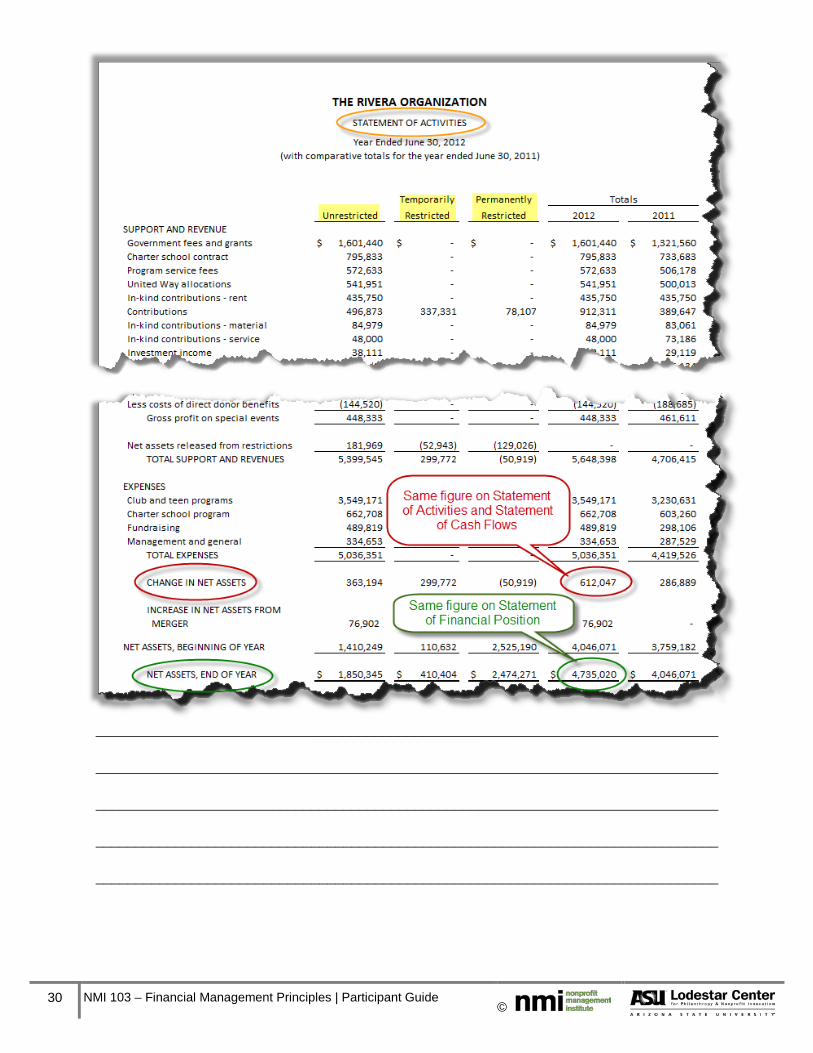

Financial Reports 2: Statement of Activities Statements of Activities - Reports the Following Information

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Reference the Activities tab

Revenues may be broken out and with detail about• Unrestricted Funds•Temporarily Restricted

Funds• Permanently Restricted Funds

Expenses may be divided by functional areas• Programs• Fundraising• Management and General Administration

Net Assets at year end will match those net assets also reported on the Statement of Financial Position

© NMI 103 – Financial Management Principles | Participant Guide 27

Rivera Statement of Activites

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

28 NMI 103 – Financial Management Principles | Participant Guide ©

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 29

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

30 NMI 103 – Financial Management Principles | Participant Guide ©

Classes of Net Assets – What Does the Donor Want?

Unrestricted

Undesignated

Board Designated

_______________________________________________

_______________________________________________

_______________________________________________

______________________________________________________________________________

______________________________________________________________________________

Restricted

Temporarily

Permanently ________________________________________________

________________________________________________

________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Managing Restricted Funds Video

Quiz – Circle the correct classification

1. An individual sends a check for $3,000 to support the nonprofits work

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 31

2. A foundation rewards a grant for $15,000 for a computer system

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

3. A foundation awards $60,000 over three years for general operating support. The second and third year payments will be made after the financial audit and narrative report is submitted

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

4. An individual gives $100,000 to provide scholarships for campers in perpetuity from the interest and investment earnings

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

32 NMI 103 – Financial Management Principles | Participant Guide ©

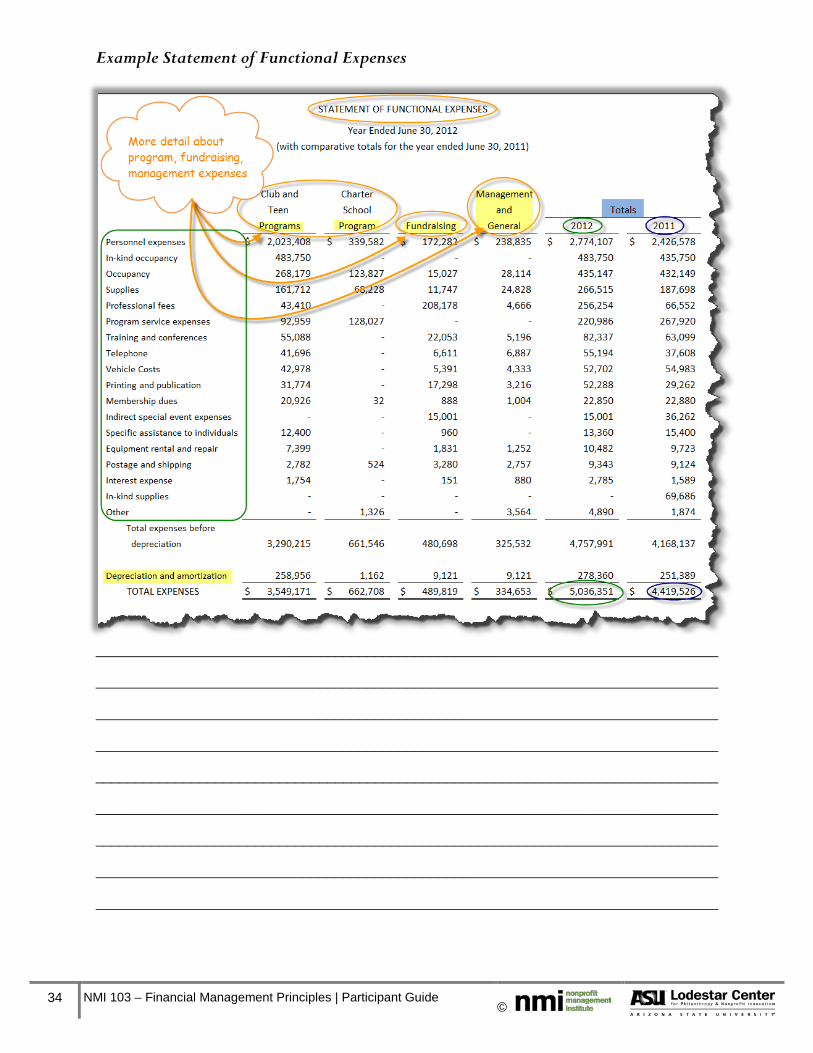

Financial Reports 3: Statement of Functional Expenses Statement of Functional Expenses

Reference the Functional Expenses tab

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Only required for voluntary health and welfare organizations; Optional statement for all other organizations

Detailed view of expenses already captured on the Statement of Activities

Functional Expenses may be broken out into• Programs• Fundraising• Management and General

Administration

This statement less likely to appear at the Board level

© NMI 103 – Financial Management Principles | Participant Guide 33

Example Statement of Functional Expenses

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

34 NMI 103 – Financial Management Principles | Participant Guide ©

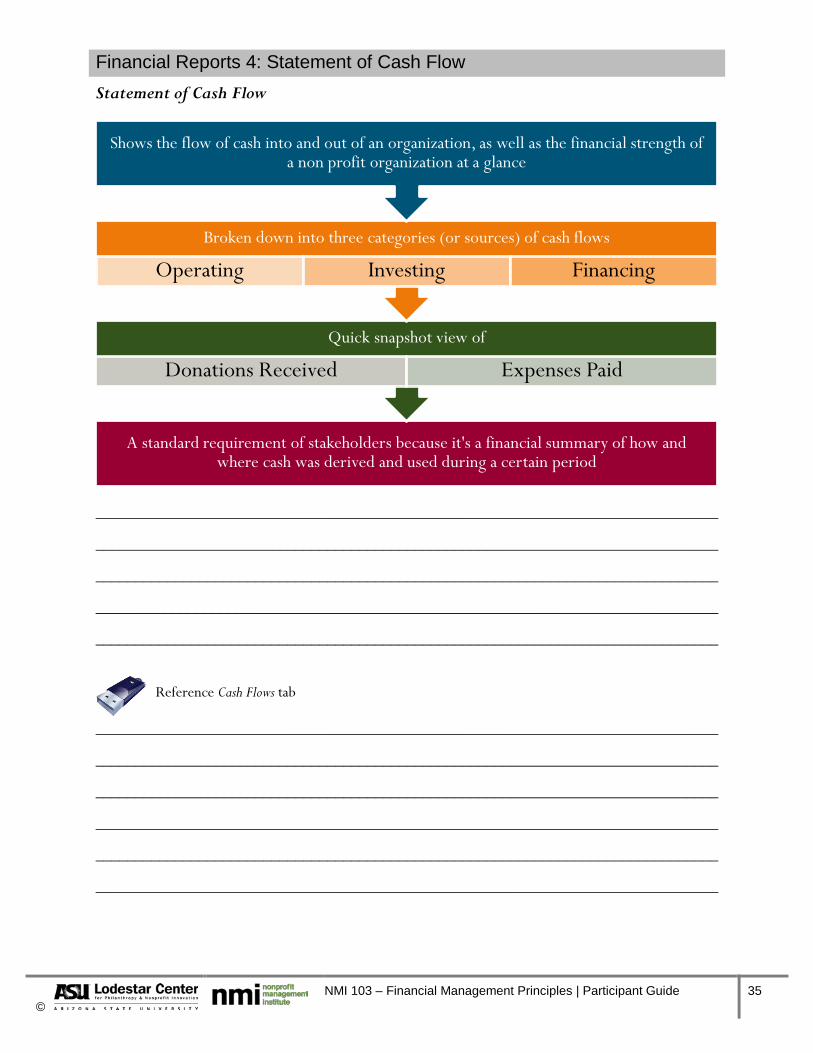

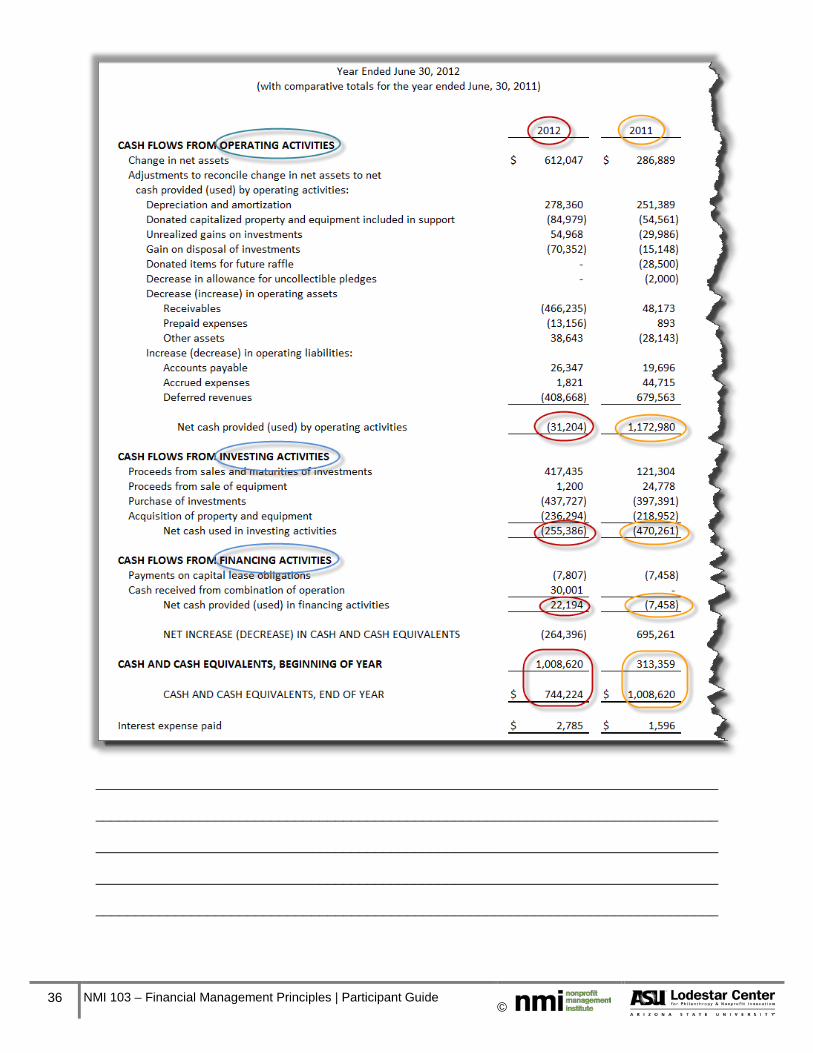

Financial Reports 4: Statement of Cash Flow Statement of Cash Flow

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Reference Cash Flows tab

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

A standard requirement of stakeholders because it's a financial summary of how and where cash was derived and used during a certain period

Quick snapshot view of

Donations Received Expenses Paid

Broken down into three categories (or sources) of cash flows

Operating Investing Financing

Shows the flow of cash into and out of an organization, as well as the financial strength of a non profit organization at a glance

© NMI 103 – Financial Management Principles | Participant Guide 35

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

36 NMI 103 – Financial Management Principles | Participant Guide ©

Financial Reports: Accountants Report and Footnotes

Footnotes

Example Footnotes

Open Rivera Organization Accountant Footnotes document

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

The final section of a standard set of external financial statements

Provide added valuable info about an organization’s financial status that can influence the overall judgment about its future

“Footnotes” or “notes of disclosure” explain things the numbers can’t

© NMI 103 – Financial Management Principles | Participant Guide 37

Types of Accountant’s Reports

A report issued by an outside CPA when that CPA has taken information, provided by management, and put it into the form of a financial statement. The CPA does not do any testing of the information provided and, accordingly, does not express an opinion or provide any assurance of the accuracy of the financial information provided.

A report issued by an outside independent CPA when that CPA has done some limited testing of the financial information. The report does not express an opinion on the accuracy of the financial information, but rather states whether or not any misstatements came to their attention during the limited testing.

A report issued by an outside independent CPA when that CPA has done sufficient testing of the financial information to be able to render an opinion about whether or not the financial information fairly represents the financial position of the organization in all material respects when the financial statements are taken as a whole.

A specialized report issued by an outside Independent CPA when that CPA has done sufficient testing to render an opinion about whether or not the organization complied with the terms of a federal grant or contract.

Audit Report Normally Covers

Statement of Financial Position

Statement of Activities

Statement of Functional Expense

Statement of Cash Flows

Related Footnotes

Supplemental Schedules

38 NMI 103 – Financial Management Principles | Participant Guide ©

Types of Audit Opinions

Standard Auditors Report

How an Actual Auditors Report Might Read Explanation of Sections of the Auditors Report

Independent Auditor's Report 1. Title

Independent

To the Board of Directors of XYZ Organization 2. Addressee

Group that hires auditor, generally not management

We have audited the accompanying statement of financial position of XYZ Organization (a non-profit organization) and the related statements of activities, functional expenses, and cash flows for the years then ended.

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and

3. Introductory paragraph

We have audited

List financial statements

Indicated management's responsibility

U

nqua

lifi

ed

Qua

lifi

ed

Unqualified - The financial statements present fairly, in all material respects, the financial position of the organization in accordance with the method of accounting chosen by management.

Qualified - The financial statements present fairly, in all material respects, the financial position of the organization in accordance with the method of accounting chosen by management with the exception of certain enumerated departures.

Dis

clai

mer

Disclaimer - The auditor states that s/he could not form an opinion on the financial statements.

Adverse – The financial statements are materially misstated and do not conform with the method of accounting chosen by management.

Adv

erse

© NMI 103 – Financial Management Principles | Participant Guide 39

maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Our responsibility is to express and opinion on these financial statements based on or audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

4. Scope paragraph

Generally Accepted Audit Standards (U.S.)

Reasonable assurance statements are free of material misstatement

Not an examination of the internal control system/environment

Examining on a test basis evidence supporting amounts and disclosures

Assessing accounting principles used and significant estimates made, as well as evaluating overall presentation

Audit provides a reasonable basis for our opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of XYZ Organization as of June 30, 2013, and the changes in its net assets and its cash flows for the year then ended in conformity with accounting principles generally accepted in the

5. Opinion paragraph

In our opinion

Present fairly, in all material respects (or not – read this paragraph carefully!)

In conformity with U.S. generally accepted

40 NMI 103 – Financial Management Principles | Participant Guide ©

United States of America.

accounting principles (or not, material departures will be noted – read carefully!)

Name and signature of auditors 6. Signature

Firm

November 20, 2013 7. Date

- Date financials are available to be published

Source: from Scottsdale Training and Rehabilitation Services, I

Source: from Scottsdale Training and Rehabilitation Services, Inc.

Audit Opinion, June 30, 2013

www.starsaz.org

© NMI 103 – Financial Management Principles | Participant Guide 41

42 NMI 103 – Financial Management Principles | Participant Guide ©

© NMI 103 – Financial Management Principles | Participant Guide 43

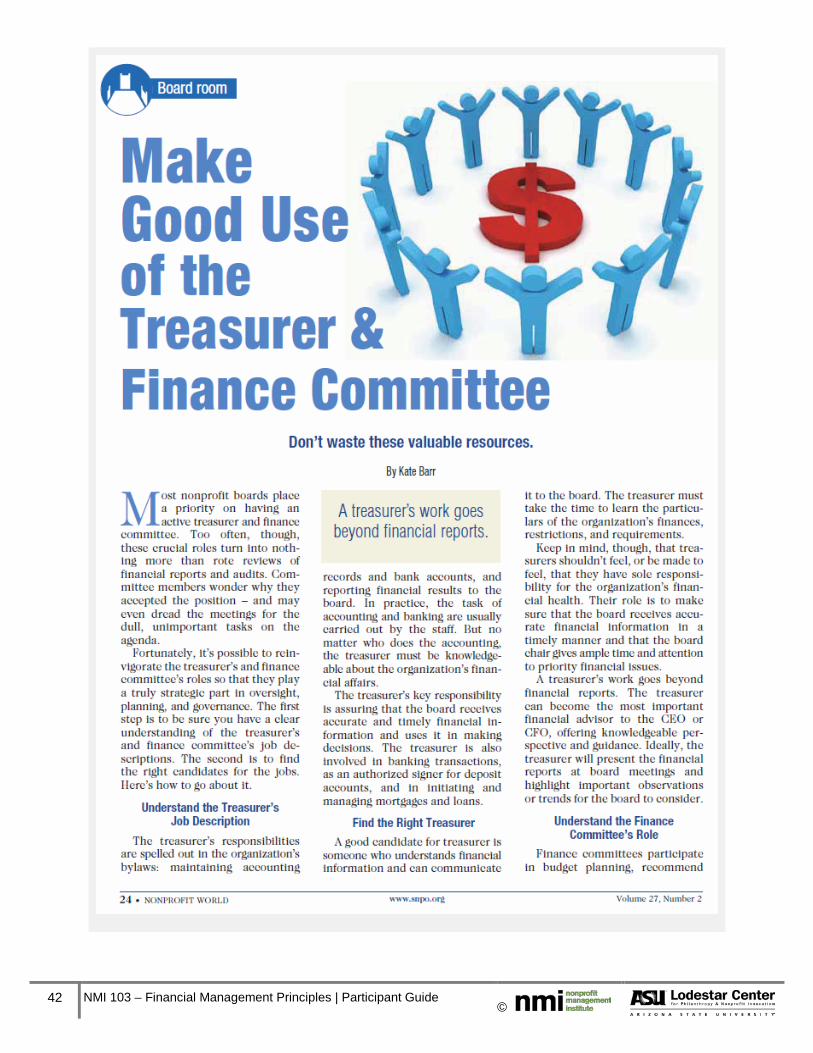

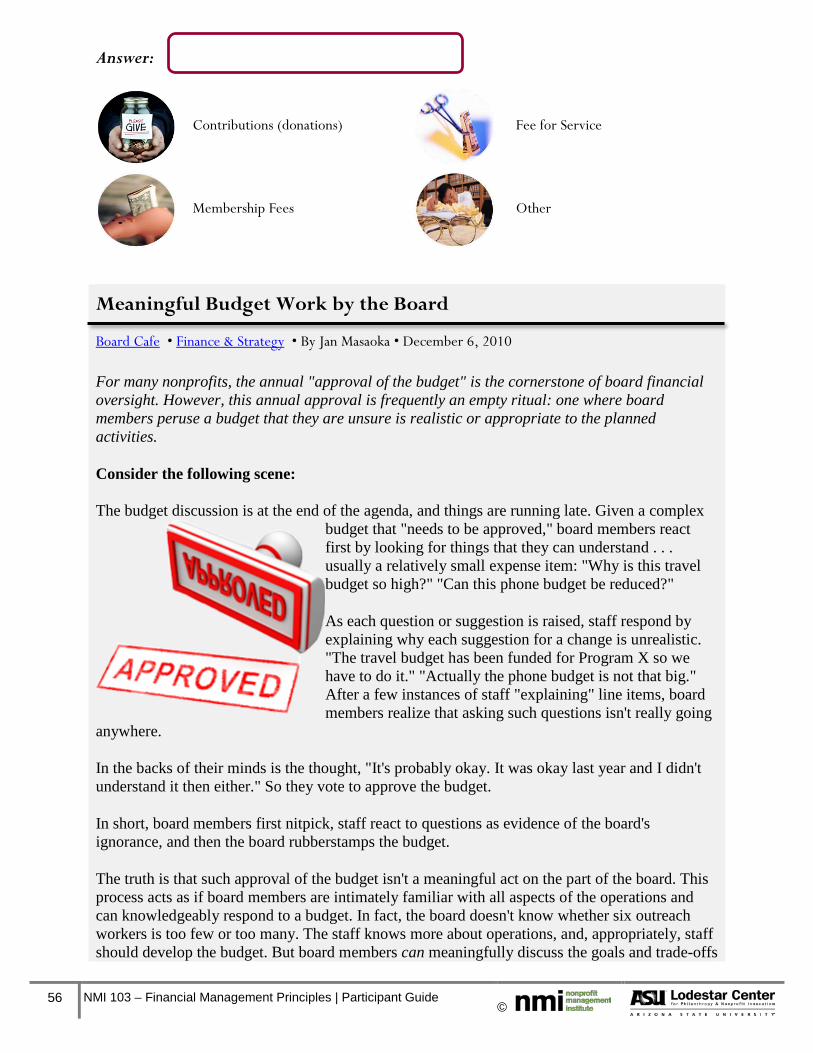

Make Good Use of the Treasurer & Finance Committee

Author: Kate Barr, Nonprofits Assistance Fund Originally appeared in Nonprofit World, 2009 Accessed 10/28/11 www.snpo.org

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Understand the Treasurer’s Job Description

• Must be knowledgeable about the organization’s financial affairs • Assures the board receives accurate and timely financial information and uses it in

making decisions • Signer for deposit accounts • Initiates and manages mortgages and loans

Find the Right Treasurer

• Board receives accurate financial information in a timely manner • Board chair gives ample time and attention to priority financial issues • Important observations and trends are highlighted for the board

Understand the Finance Committee’s Role

• Participates in budget planning • Recommends fiscal policies • Discusses financial statements in detail • Helps staff and board think through financial questions and develop opinions

A finance committee isn’t needed if the board as a whole can understand the financial information, provide guidance, and make financial decisions efficiently.

While finance committee members need to understand financial reports, don’t assume that only accountants, bankers, and businesspeople are qualified. Financial language can be learned.

44 NMI 103 – Financial Management Principles | Participant Guide ©

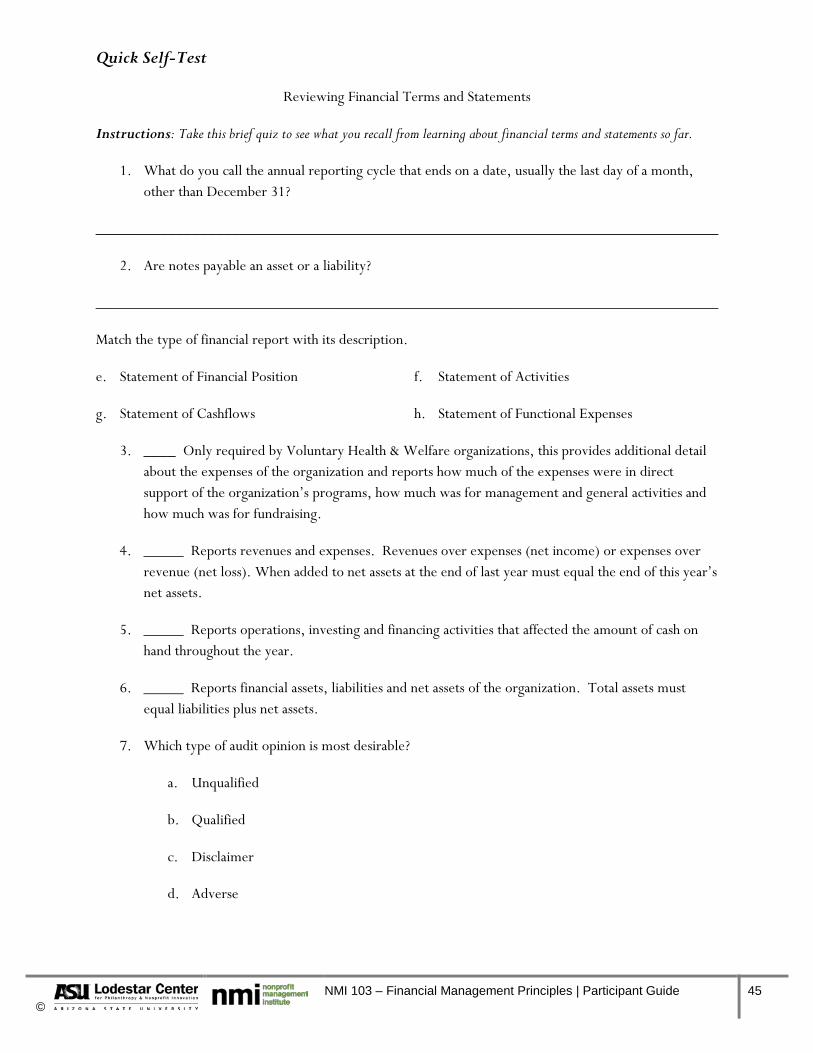

Quick Self-Test

Reviewing Financial Terms and Statements

Instructions: Take this brief quiz to see what you recall from learning about financial terms and statements so far.

1. What do you call the annual reporting cycle that ends on a date, usually the last day of a month, other than December 31?

______________________________________________________________________________

2. Are notes payable an asset or a liability?

______________________________________________________________________________

Match the type of financial report with its description.

e. Statement of Financial Position f. Statement of Activities

g. Statement of Cashflows h. Statement of Functional Expenses

3. ____ Only required by Voluntary Health & Welfare organizations, this provides additional detail about the expenses of the organization and reports how much of the expenses were in direct support of the organization’s programs, how much was for management and general activities and how much was for fundraising.

4. _____ Reports revenues and expenses. Revenues over expenses (net income) or expenses over revenue (net loss). When added to net assets at the end of last year must equal the end of this year’s net assets.

5. _____ Reports operations, investing and financing activities that affected the amount of cash on hand throughout the year.

6. _____ Reports financial assets, liabilities and net assets of the organization. Total assets must equal liabilities plus net assets.

7. Which type of audit opinion is most desirable?

a. Unqualified

b. Qualified

c. Disclaimer

d. Adverse

© NMI 103 – Financial Management Principles | Participant Guide 45

Contribution versus Exchange Transactions Contribution versus Exchange Transactions

Classifying something as an “exchange” or a “contribution” (i.e. a donation) can be tricky

Accountants must sometimes sift through the facts to get a description and classify the transaction properly as “exchange” or “contribution”

Contribution Transactions Defined

Exchange Transactions Defined

A unique attribute of nonprofit accounting that could include contributions (i.e. donations) of

• Money • Stock • Valuables: car, horse,

jewelry, artwork

People will have no expectation for getting anything in return for their contribution, except a good feeling for helping the cause and forwarding your organization’s mission

When an organization provides goods or services in exchange for money

Recorded differently from contributions (i.e. donations)

• Revenue is only recorded when the goods or serviced are delivered

46 NMI 103 – Financial Management Principles | Participant Guide ©

Exchange Transaction – Classic Example: Mental Health Treatment

Performance of a behavioral health service to a segment of the population

By law or by agreement, the unit of government (e.g. county or state) is obligated to serve this population

However…

Government asks a nonprofit with expertise to perform the services

Government pays the nonprofit an agreed upon amount

Nonprofit submits proof that they have performed the service

Nonprofit is paid

No element of contribution to the nonprofit for the payment

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Your Turn: Contribution or Exchange?

Scenario 1:

The US Parks Service agrees to fund a Museum’s study of the rare plants in a section of the Grand Canyon National Park.

The research staff spends 18 months in the field and lab follow-up work to identify 10 new types of rare plants in that section of the park.

At the study’s end, the Museum staff writes a report on their findings which is made available to the Park Service as well as to the general public. The Park Service is pleased.

The Museum did valuable research and had a “grant” of $10,000.

The Museum staff’s expenses are included in the operating budget of the Museum.

Is this a contribution or exchange transaction?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 47

Scenario 2:

The US Park Service needs people to build trails, so they hire clients of “Green Tree,” a nonprofit organization, to work for $10 per hour.

The money is paid to “Green Tree” for trail building services.

Payments are made on this arrangement every two weeks. When the project is completed, the Park Service will pay “Green Tree” a larger lump sum.

Is this a contribution or exchange transaction?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

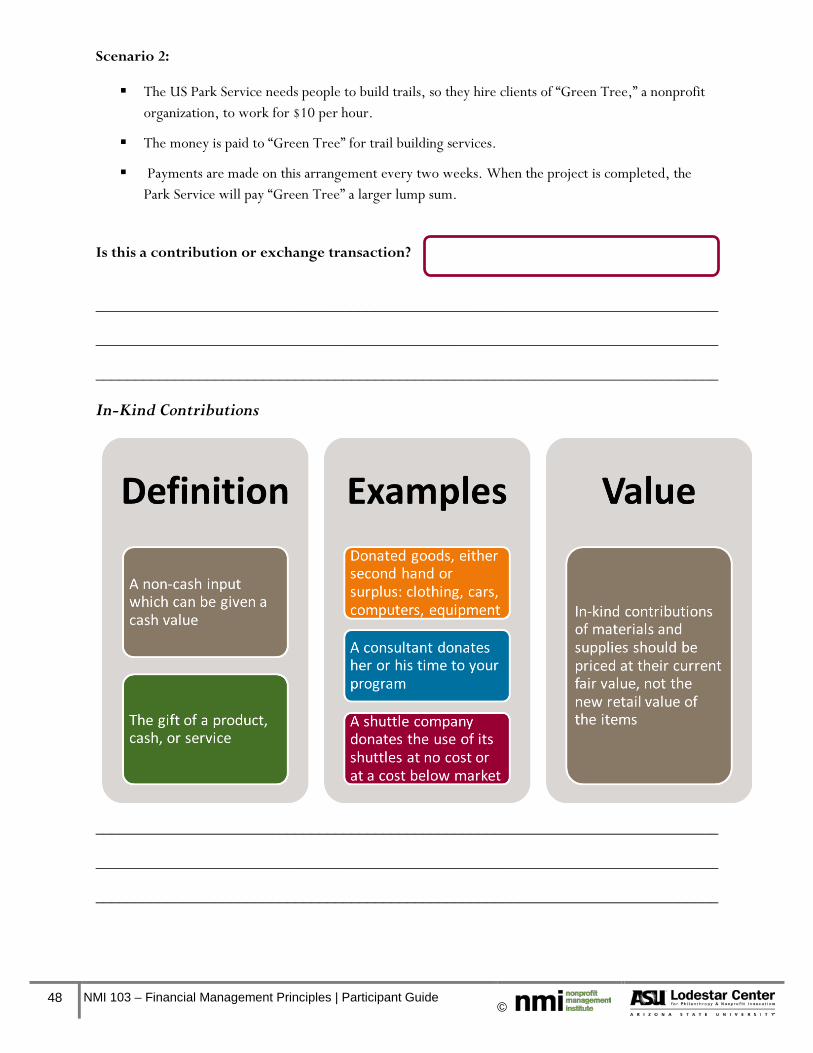

In-Kind Contributions

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

48 NMI 103 – Financial Management Principles | Participant Guide ©

Valuing In-Kind Contributions

“By law, non-profit organizations cannot provide a donor with the dollar value of an In-kind gift. Such valuations when applicable, relative to “fair market value” of In-Kind gifts, need to be professionally assessed and certified elsewhere—if they can be—and that is the responsibility of the donor. This certification subsequently needs to be resolved with the professionals and others who prepare the donor’s tax forms—whose work in turn will need to be reconciled with IRS regulations. In instances where time and service are donated, no tax break whatsoever is allowed, as the IRS Publication 526 clearly states, ‘You cannot deduct the value of your time or services. . . .’”

(“In-Kind Gifts: How to Acknowledge and Recognize Them,” by Tony Poderis, http://www.raise-funds.com/2008/in-kind-gifts-how-to-acknowledge-and-recognize-them/, accessed 5/14/2012)

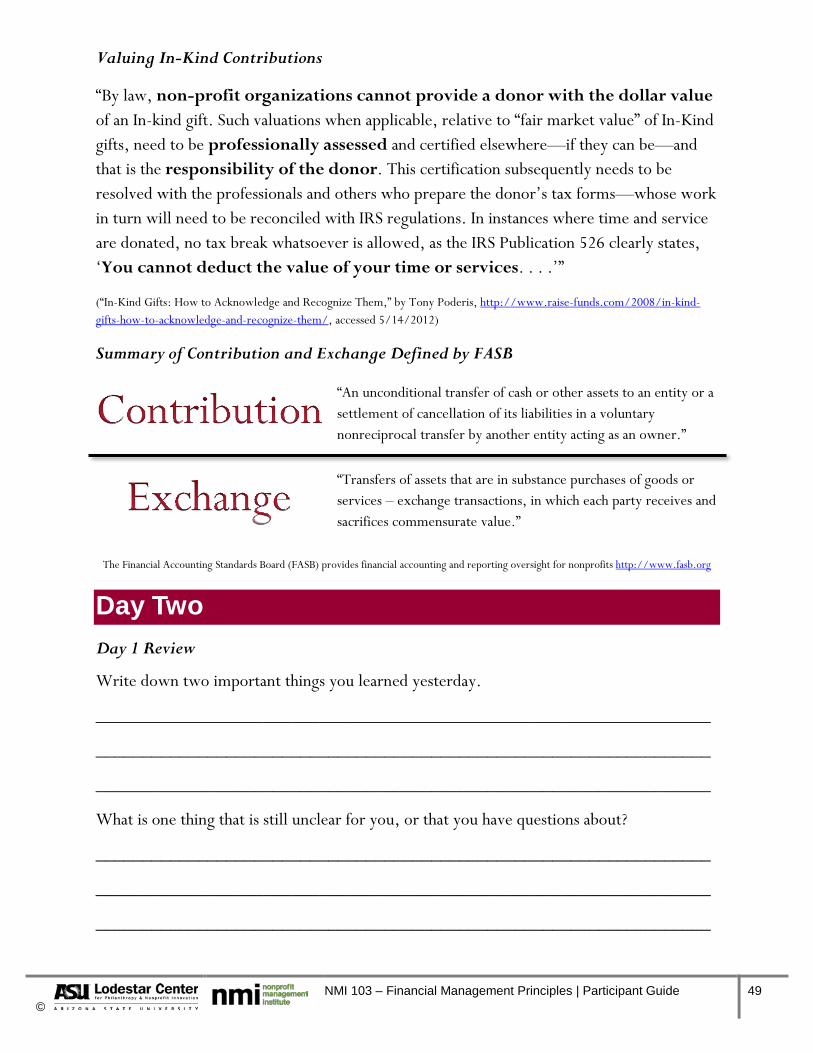

Summary of Contribution and Exchange Defined by FASB

“An unconditional transfer of cash or other assets to an entity or a settlement of cancellation of its liabilities in a voluntary nonreciprocal transfer by another entity acting as an owner.”

“Transfers of assets that are in substance purchases of goods or services – exchange transactions, in which each party receives and sacrifices commensurate value.”

The Financial Accounting Standards Board (FASB) provides financial accounting and reporting oversight for nonprofits http://www.fasb.org

Day Two Day 1 Review

Write down two important things you learned yesterday.

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

What is one thing that is still unclear for you, or that you have questions about?

__________________________________________________________________

__________________________________________________________________

__________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 49

Internal Controls

Internal Controls Defined

Author: Patricia A. O’Malley, CPA. http://www.rubino.com. Copyright 2011 Greater Washington Society of CPAs Educational Foundation.

Accessed 10/21/11.

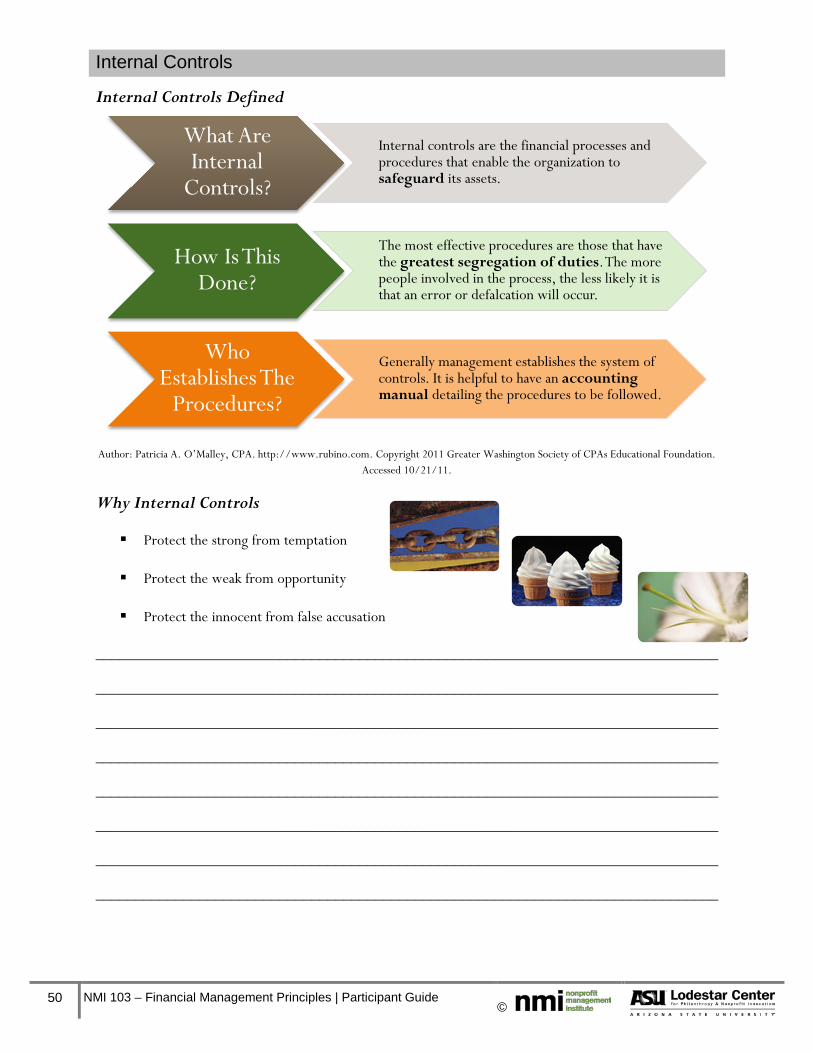

Why Internal Controls

Protect the strong from temptation

Protect the weak from opportunity

Protect the innocent from false accusation

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

What Are Internal

Controls?

Internal controls are the financial processes and procedures that enable the organization to safeguard its assets.

How Is This Done?

The most effective procedures are those that have the greatest segregation of duties. The more people involved in the process, the less likely it is that an error or defalcation will occur.

Who Establishes The

Procedures?

Generally management establishes the system of controls. It is helpful to have an accounting manual detailing the procedures to be followed.

50 NMI 103 – Financial Management Principles | Participant Guide ©

Once Upon Internal Control – Southside Community Church Cartoon Part 1Video

Instructions: While watching this video, list all of the internal controls you hear described

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Which Internal Controls Did you Detect?

Quickly compare your list with a partner’s. Compile one list of shared internal controls and be prepared to share your list with the group.

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

© NMI 103 – Financial Management Principles | Participant Guide 51

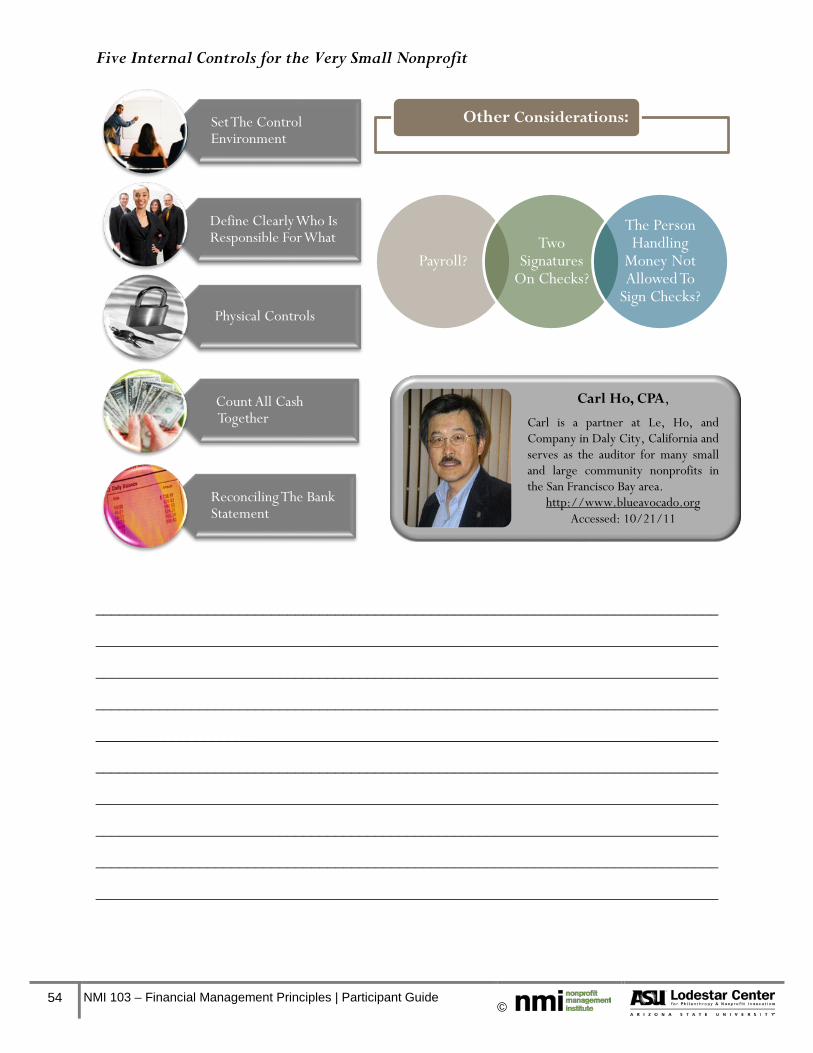

Five Internal Controls for the Very Small Nonprofit

Finance & Strategy • By Carl Ho, CPA • January 6, 2010 •

Segregation of duties, checks & balances . . . difficult to implement in the organization that has perhaps three or fewer staff, or only a few active board members in an all-volunteer organization. We asked CPA Carl Ho, who works with dozens of small nonprofits, what would be the five most important, most do-able controls for small groups:

1. The first and most important consideration is to set the control environment, that is, to let everyone know, from the top down, that there are policies in place and everyone has to follow the policies. In so many organizations the top person makes exceptions for himself or herself about policies, which sets a sloppy or even unethical tone. Then other people don't think they have to follow procedures, either, and they start cutting corners. The top person can't ask for reimbursement for anything for which they don't have a receipt. The management team members must all use time sheets themselves, get approval for travel expenses, have their credit cards scrutinized.

Emphasize the importance of ethics and controls at staff meetings, and demonstrate that everyone follows the rules, all the time.

2. Define clearly who is responsible for what. It's very common in small organizations, where not as much needs to be written down, for people to say, "I thought she was going to check the invoice." For example, with invoices: who is responsible for checking the math? Who is responsible for approving the invoice to be paid?

3. Physical controls. Lock it up. Computers should be locked to desks, and they should be protected with passwords. Put checks in a locked drawer. Among other abuses, there are too many cases where someone comes in and takes checks from the middle of the checkbook.

4. If there's cash involved -- such as at a fundraiser or box office at a performance -- have two people count all the cash together.

5. Reconciling the bank statement is a very crucial step. It's very unlikely that someone is going to steal from you and run away forever. Reconciling the bank statement means that embezzlement can't go on for very long.

Ideally someone other than the bookkeeper (or whoever handles the money) reconciles the bank account from an unopened statement. That's a strong check on the person who handles the money. But in a small nonprofit there may not be a bookkeeper, and there may be only one person who does everything. In these instances someone else, such as a board member, should receive the unopened bank statement, and look it over before giving it to the bookkeeper or the sole staff person.

There are several controls that are commonly recommended but that you haven't mentioned. Could you comment on them? For example:

52 NMI 103 – Financial Management Principles | Participant Guide ©

Payroll? Payroll controls at small organizations are actually easy because everybody knows everybody, so it's harder to create fictitious employees and pay them. The one area for attention is approval of timesheets for people working on an hourly basis. In these cases someone -- who knows what work they did -- should review and approve timesheets.

Two signatures on checks, or on large checks? This is okay as a policy, as long as you know that banks don't enforce this policy, nor can you hold them liable for a check that goes through with only one signature. Two signatures is a good policy so that someone sees the big checks, but it's more about setting the right tone than about preventing theft.