Next Plc JPMorgan 24.4.2012

52

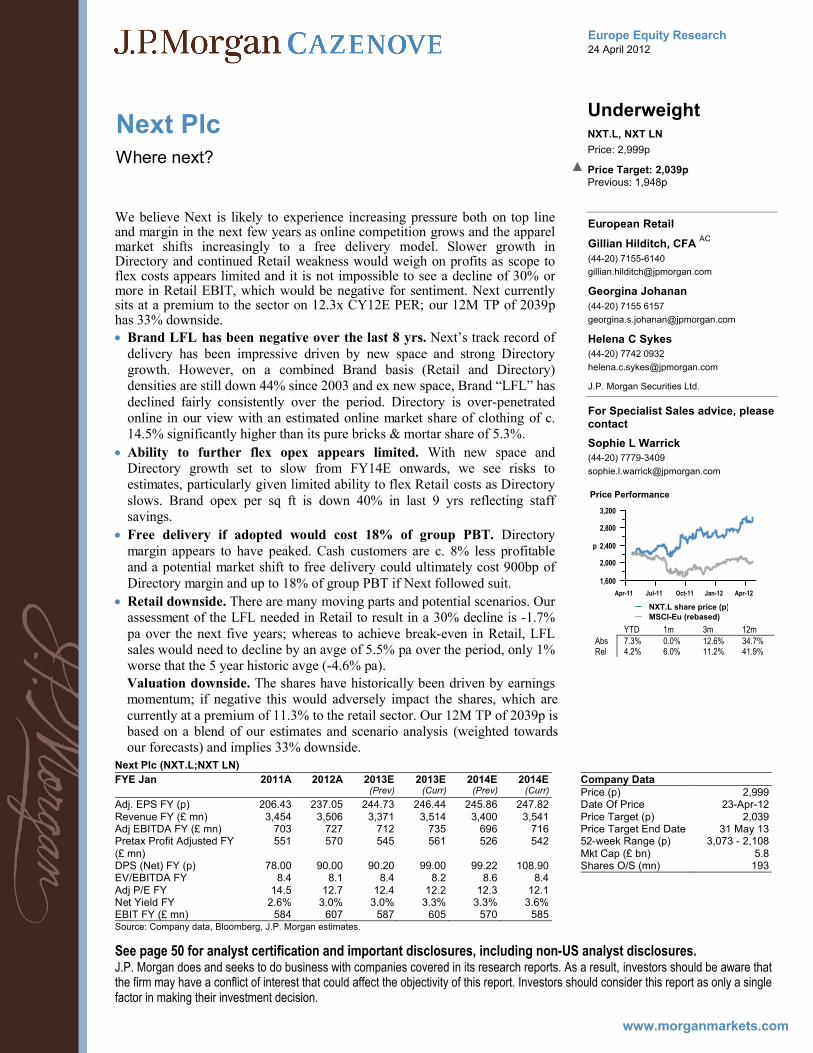

www.morganmarkets.com Europe Equity Research 24 April 2012 Next Plc Underweight NXT.L, NXT LN Where next? ▲ Price: 2,999p Price Target: 2,039p Previous: 1,948p European Retail Gillian Hilditch, CFA AC (44-20) 7155-6140 [email protected] Georgina Johanan (44-20) 7155 6157 [email protected] Helena C Sykes (44-20) 7742 0932 [email protected] J.P. Morgan Securities Ltd. For Specialist Sales advice, please contact Sophie L Warrick (44-20) 7779-3409 [email protected] YTD 1m 3m 12m Abs 7.3% 0.0% 12.6% 34.7% Rel 4.2% 6.0% 11.2% 41.9% Next Plc (NXT.L;NXT LN) FYE Jan 2011A 2012A 2013E (Prev) 2013E (Curr) 2014E (Prev) 2014E (Curr) Adj. EPS FY (p) 206.43 237.05 244.73 246.44 245.86 247.82 Revenue FY (£ mn) 3,454 3,506 3,371 3,514 3,400 3,541 Adj EBITDA FY (£ mn) 703 727 712 735 696 716 Pretax Profit Adjusted FY (£ mn) 551 570 545 561 526 542 DPS (Net) FY (p) 78.00 90.00 90.20 99.00 99.22 108.90 EV/EBITDA FY 8.4 8.1 8.4 8.2 8.6 8.4 Adj P/E FY 14.5 12.7 12.4 12.2 12.3 12.1 Net Yield FY 2.6% 3.0% 3.0% 3.3% 3.3% 3.6% EBIT FY (£ mn) 584 607 587 605 570 585 Source: Company data, Bloomberg, J.P. Morgan estimates. Company Data Price (p) 2,999 Date Of Price 23-Apr-12 Price Target (p) 2,039 Price Target End Date 31 May 13 52-week Range (p) 3,073 - 2,108 Mkt Cap (£ bn) 5.8 Shares O/S (mn) 193 See page 50 for analyst certification and important disclosures, including non-US analyst disclosures. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 1,600 2,000 2,400 2,800 3,200 p Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Price Performance NXT.L share price (p) MSCI-Eu (rebased) We believe Next is likely to experience increasing pressure both on top line and margin in the next few years as online competition grows and the apparel market shifts increasingly to a free delivery model. Slower growth in Directory and continued Retail weakness would weigh on profits as scope to flex costs appears limited and it is not impossible to see a decline of 30% or more in Retail EBIT, which would be negative for sentiment. Next currently sits at a premium to the sector on 12.3x CY12E PER; our 12M TP of 2039p has 33% downside. Brand LFL has been negative over the last 8 yrs. Next’s track record of delivery has been impressive driven by new space and strong Directory growth. However, on a combined Brand basis (Retail and Directory) densities are still down 44% since 2003 and ex new space, Brand “LFL” has declined fairly consistently over the period. Directory is over-penetrated online in our view with an estimated online market share of clothing of c. 14.5% significantly higher than its pure bricks & mortar share of 5.3%. Ability to further flex opex appears limited. With new space and Directory growth set to slow from FY14E onwards, we see risks to estimates, particularly given limited ability to flex Retail costs as Directory slows. Brand opex per sq ft is down 40% in last 9 yrs reflecting staff savings. Free delivery if adopted would cost 18% of group PBT. Directory margin appears to have peaked. Cash customers are c. 8% less profitable and a potential market shift to free delivery could ultimately cost 900bp of Directory margin and up to 18% of group PBT if Next followed suit. Retail downside. There are many moving parts and potential scenarios. Our assessment of the LFL needed in Retail to result in a 30% decline is -1.7% pa over the next five years; whereas to achieve break-even in Retail, LFL sales would need to decline by an avge of 5.5% pa over the period, only 1% worse that the 5 year historic avge (-4.6% pa). Valuation downside. The shares have historically been driven by earnings momentum; if negative this would adversely impact the shares, which are currently at a premium of 11.3% to the retail sector. Our 12M TP of 2039p is based on a blend of our estimates and scenario analysis (weighted towards our forecasts) and implies 33% downside.

-

Upload

maverick227 -

Category

Documents

-

view

108 -

download

1

Transcript of Next Plc JPMorgan 24.4.2012

www.morganmarkets.com

Europe Equity Research24 April 2012

Next PlcUnderweightNXT.L, NXT LN

Where next?▲

Price: 2,999p

Price Target: 2,039pPrevious: 1,948p

European Retail

Gillian Hilditch, CFA AC

(44-20) 7155-6140

Georgina Johanan

(44-20) 7155 6157

Helena C Sykes

(44-20) 7742 0932

J.P. Morgan Securities Ltd.

For Specialist Sales advice, please contact

Sophie L Warrick

(44-20) 7779-3409

YTD 1m 3m 12mAbs 7.3% 0.0% 12.6% 34.7%Rel 4.2% 6.0% 11.2% 41.9%

Next Plc (NXT.L;NXT LN)

FYE Jan 2011A 2012A 2013E(Prev)

2013E(Curr)

2014E(Prev)

2014E(Curr)

Adj. EPS FY (p) 206.43 237.05 244.73 246.44 245.86 247.82Revenue FY (£ mn) 3,454 3,506 3,371 3,514 3,400 3,541Adj EBITDA FY (£ mn) 703 727 712 735 696 716Pretax Profit Adjusted FY (£ mn)

551 570 545 561 526 542

DPS (Net) FY (p) 78.00 90.00 90.20 99.00 99.22 108.90EV/EBITDA FY 8.4 8.1 8.4 8.2 8.6 8.4Adj P/E FY 14.5 12.7 12.4 12.2 12.3 12.1Net Yield FY 2.6% 3.0% 3.0% 3.3% 3.3% 3.6%EBIT FY (£ mn) 584 607 587 605 570 585Source: Company data, Bloomberg, J.P. Morgan estimates.

Company DataPrice (p) 2,999Date Of Price 23-Apr-12Price Target (p) 2,039Price Target End Date 31 May 1352-week Range (p) 3,073 - 2,108Mkt Cap (£ bn) 5.8Shares O/S (mn) 193

See page 50 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

1,600

2,000

2,400

2,800

3,200

p

Apr-11 Jul-11 Oct-11 Jan-12 Apr-12

Price Performance

NXT.L share price (p)MSCI-Eu (rebased)

We believe Next is likely to experience increasing pressure both on top line and margin in the next few years as online competition grows and the apparel market shifts increasingly to a free delivery model. Slower growth in Directory and continued Retail weakness would weigh on profits as scope to flex costs appears limited and it is not impossible to see a decline of 30% or more in Retail EBIT, which would be negative for sentiment. Next currently sits at a premium to the sector on 12.3x CY12E PER; our 12M TP of 2039p has 33% downside.

Brand LFL has been negative over the last 8 yrs. Next’s track record of delivery has been impressive driven by new space and strong Directory growth. However, on a combined Brand basis (Retail and Directory) densities are still down 44% since 2003 and ex new space, Brand “LFL” has declined fairly consistently over the period. Directory is over-penetrated online in our view with an estimated online market share of clothing of c. 14.5% significantly higher than its pure bricks & mortar share of 5.3%.

Ability to further flex opex appears limited. With new space and Directory growth set to slow from FY14E onwards, we see risks to estimates, particularly given limited ability to flex Retail costs as Directory slows. Brand opex per sq ft is down 40% in last 9 yrs reflecting staff savings.

Free delivery if adopted would cost 18% of group PBT. Directory margin appears to have peaked. Cash customers are c. 8% less profitable and a potential market shift to free delivery could ultimately cost 900bp of Directory margin and up to 18% of group PBT if Next followed suit.

Retail downside. There are many moving parts and potential scenarios. Our assessment of the LFL needed in Retail to result in a 30% decline is -1.7% pa over the next five years; whereas to achieve break-even in Retail, LFL sales would need to decline by an avge of 5.5% pa over the period, only 1% worse that the 5 year historic avge (-4.6% pa).

Valuation downside. The shares have historically been driven by earnings momentum; if negative this would adversely impact the shares, which are currently at a premium of 11.3% to the retail sector. Our 12M TP of 2039p is based on a blend of our estimates and scenario analysis (weighted towards our forecasts) and implies 33% downside.

2

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Table of ContentsInvestment thesis .....................................................................3

Summary Points......................................................................................................3

Where Next? .............................................................................6

One Brand, one dream – does it matter where the sales come from?...............................................................................7

Next sales densities fall even on the combined business ...........................................7

Both new space and Directory are key for Brand sales growth..................................8

Directory has been the main driver of sales and profit in the last year .......................9

The switch to offering cash with order has provided a short-term boost …..............10

….., but Next is already over-penetrated online......................................................11

The growth in cash customers encourages cannibalization of the UK store customers.............................................................................................................................13

Overall market share in clothing appears to be stagnant..........................................13

Profit per sq ft has also been falling .......................................................................14

Scope to further cut costs appears limited ..............................................................15

Directory margin could have peaked....................................17

Growth in less profitable cash customers to outpace credit account holders ............17

Move to free delivery could reduce Group PBT by 18%.........................................19

How likely is free delivery?...................................................................................24

Could free delivery grow Next Directory sales? .....................................................25

Outlook for FY13E and beyond .............................................26

FY13E Guidance...................................................................................................26

FY13E assumptions ..............................................................................................27

FY14E assumptions ..............................................................................................28

FY15E assumptions ..............................................................................................28

EBIT margin analysis in more detail......................................................................30

Cash flow and Balance sheet analysis ....................................................................33

Scenario analysis; risks lie to the downside .......................35

P&L cost base has little opportunity for incremental flex .......................................35

Retail break-even scenario.....................................................................................37

Alternative Retail downside scenario.....................................................................38

Valuation .................................................................................40

ROICs...................................................................................................................40

Share price versus earnings revisions.....................................................................40

Valuation versus peers...........................................................................................44

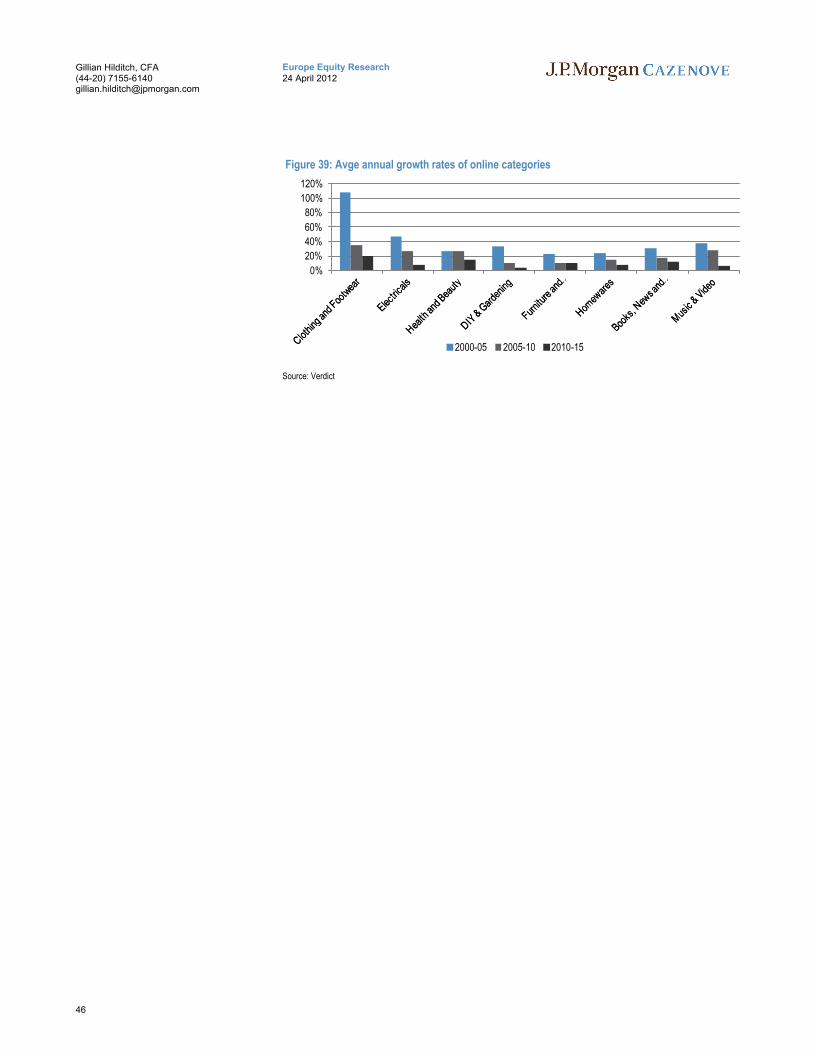

Appendix – online clothing growth.......................................45

Online clothing growth has outperformed the rest of online…................................45

Valuation Methodology and Risks ........................................47

3

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Investment thesis

Summary Points

Next’s track record of delivery throughout the downturn has been impressive; reflected in the share price outperformance.

EPS 4 year CAGR +9.2% between 2008 and 2012.

Shares +39% in 2011, an outperformance of 50% vs. the sector.

Growth has been driven by safe haven status and strong performance in Directory

Directory performance reflects structural growth in the market BUT as a first mover Next’s is over penetrated online and looks set to lose share going forward.

Next has a 14.5% share of the online clothing market, significantly higher than its 5.3% share of the bricks and mortar market. Risk of a loss in share is weighted to the downside.

New Space and Directory are key for Brand sales growth.

The average growth in Brand sales over the past 5 years has been +1.6% pa despite an average space contribution of +3% and an average contribution from Directory of +2% to total Brand growth.

Cash customers have been a key driver of Directory Growth.

Of 9.7% growth in active customers in FY12 (to Jan), 6.3% came from the increase in cash customers.

BUT has tempted those “hold-out” Next Retail customers who did not like having to order on credit and is therefore encouraging cannibalization of store customers.

Figure 1: Next vs. FTSE 350 General Retailers Relative Performance

Source: Bloomberg

Figure 2: Next Active Customers vs. ASOS Active Customers

Figure 3: Brand sales growth yoy % less weighted space contribution

Source: Company Data, JPMC estimates

Figure 4: Cash with Order Customers vs. Credit Customer

Source: Company Data, JPMC estimates

0.9

1.1

1.3

1.5

1.7

1.9

Jan 11

Feb 11

Mar 11

Apr 11

May 11

Jun 11

Jul 11

Aug 11

Sep 11

Oct 11

Nov 11

Dec 11

Next:FTSE 350 General Retailers Relative

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brand sales growth less weighted space contribution

4

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Directory margin could have also peaked.

Free delivery becoming increasingly prevalent.

Growth in less profitable cash customers/ increasing international mix (we estimate that account customers are at least 8% more profitable on average).

Increasing international mix (margin on international customers c.350bps below UK customers).

Free Delivery could impact the Directory margin by 900 bps and reduce Group PBT by 18%.

Moving to free delivery would mean that Next loses £3.99 of income generated from customer delivery charges on an estimated 15m parcels pa at present -generating a one time hit of £59m.

Combined with likely increased average order frequency and an incremental channel shift this equates to lost margin of c.900bps (over a 2-3 year timeframe). This compares to the cost to Asos of 1300bps from a shift to free shipping (although it has a greater proportion of international sales which will be more expensive).

Next’s sales densities have been falling even on a combined basis.

Combined (i.e. Retail & Directory) sales densities have fallen by 44% from a peak of £953 per sq ft in 2003 to £533 in 2012.

We estimate cumulative underlying Brand LFL decline of -7.7% over the 8 years to 2012.

Cost cutting is important to mitigate this pressure; scope to further cut costs appears limited.

Management has achieved aggressive efficiencies in underlying costs. Per sq ft Brand opex has fallen by 40% in the 9 years to 2012 and Brand FTE’s have halved to 4.1, which is lower than most peers.

Figure 5: Service Income

Source: Company Data, JPMC estimates

Table 1: Potential Impact on Group PBT if Current Paid For Deliveries Were Free

Source: JPMC estimates

Figure 6: Combined Brand Sales Densities

Source: Company Data, JPMC estimates

Figure 7: Next Brand Employees per '000 sq ft

Source: Company Data

Directory sales inc VAT and grossed up for returns £2160m

Collected in store (inc VAT) £432m 20%

Delivered by courier £1728m 80%

Sales delivered by courier with free delivery £259m 15%

Sales where delivery charge paid by the customer £1469m 85%

Directory customers (m) 3.0

Average spend per customer pa £721

Average order value £100

Implied average order frequency pa 7x

Implied no. of parcels (m) pa - total 22

Implied no. of parcels (m) pa - delivery paid by customer 15

Standard delivery charge £3.99

Current income generated from customer delivery charge £59m

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

0

200

400

600

800

1000

1200

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

E

2014

E

Combined sales density £ sq ft (LHS) Space growth yoy % chge (RHS)

0

1

2

3

4

5

6

7

8

9

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Next Brand employees per 000 sq ft

5

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

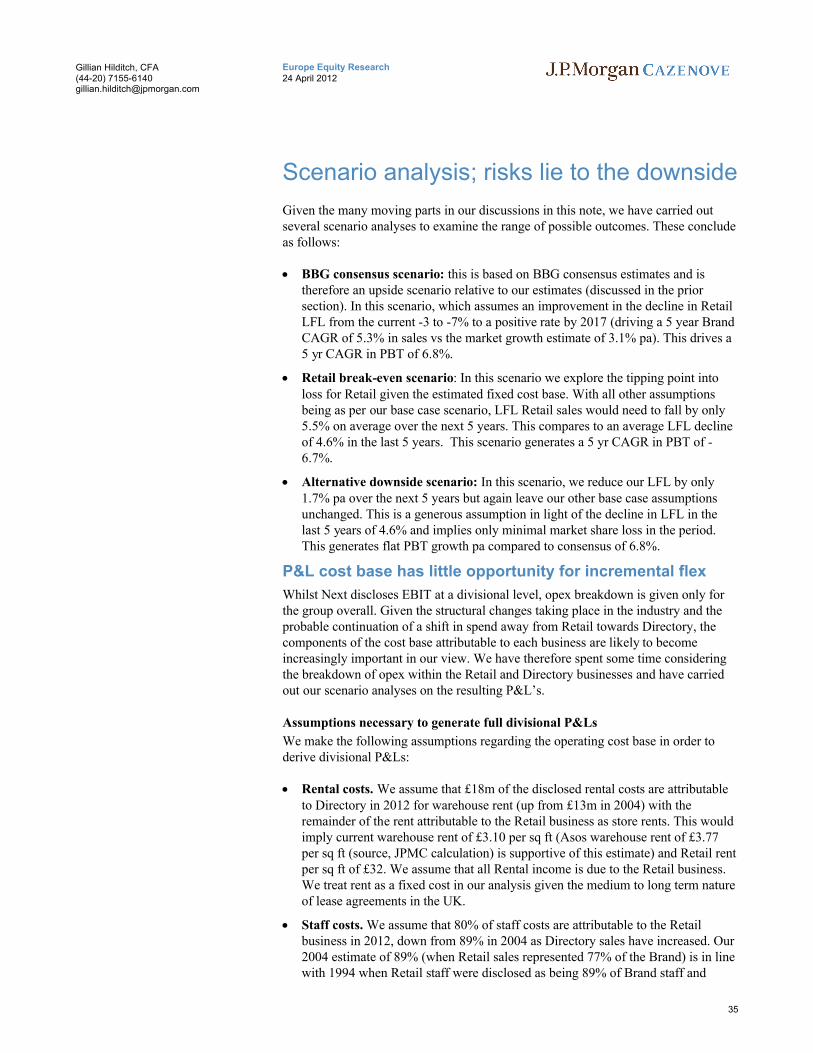

Our scenario analysis gives a range of outcomes; risks lie to the downside.

Worst case scenario; to reach the tipping point into Retail loss, Next LFL Retail sales would need to fall by 5.5% on average over 5 years.

A 30% fall in Retail EBIT would result if LFL Retail sales declined by only -1.7% on average over 5 years.

PBT expected to fall by 3% pa over the next 3 years

This includes a fall of -1.6% in FY13E, towards the bottom of management’s guidance range (-2% to +7%).

3-year EPS CAGR (including the buyback) +1.6% (FY13E +4.0%)

Valuation; Next is the most expensive stock within the peer group.

Premium rating (CY12E PER of 12.3x) and PEG of 4.4x.

Discounted profit model returns a value of £16.76 per share.

Price target updated to 2039p based on a blend of scenarios.

Table 2: Scenario Summary Table

Retail LFL 5yr avrg

Brand Sales 5yr

CAGRPBT 5yr

CAGR

Base Case 0.2% 5.3% 6.8%Alternative Downside -1.7% 1.7% 0.0%Worst Case -5.5% 0.6% -6.7%

Source: JPMC Estimates.

Figure 8: JPMC annual growth rate estimates.

Source: JPMC Estimates, Bloomberg

Figure 9: EPS CAGR CY11-13 vs. CY12 P/E

Source: Bloomberg, JPMC ests

Table 3: Probability weighted discounted economic profit

Implied value Probability

BBG base case 32.87 20%

Retail break even 14.67 15%

30% downside in Retail 21.57 15%

JPMC base case 16.76 50%

Implied equal weighted implied value (p) 20.39

Source: J.P. Morgan estimates, Company data.

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Retail LFL (avrg) Brand LFL (avrg) PBT (CAGR)

2008-2012 2013-2015

Home Retail

Kingfisher

M&S

Next

Inchcape

Debenhams

Dunelm

Howdens

Halfords

Kesa

Mothercare

WH Smith

Dixons

H&M

Inditex

R² = 0.4368

-40%

-30%

-20%

-10%

0%

10%

20%

30%

5x 10x 15x 20x 25x 30x 35x 40x

EP

S C

AG

R C

Y1

1-1

3

P/E CY12

Asos PER 33.7x

6

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Where Next?

Top performance in 2011 driven by safe haven status and Directory enthusiasm

Next was the best performing stock in UK General Retail in 2011. The shares rose by 36% on an absolute basis and 49% on a relative basis as investors chose to back the security of a well regarded management team and a share buyback programme over the uncertainties of self help programmes or macro recovery stories elsewhere in the sector. However, it was not just about looking for a safe haven. Investor enthusiasm also appeared to be stimulated by the strong growth delivered by the Directory business and Directory's potential to offset the moribund Retail business and perhaps even deliver a “growth” angle for what had hitherto seemed at best to be a stable story.

However, it seems that this enthusiasm has been carried forward into the current year with estimates and the valuation implying that Directory can continue to perform at this high rate of growth and offset the impact of a deteriorating Retail business indefinitely. We disagree with such a view for a number of reasons

Firstly, Next argues frequently that given the cannibalization of the Retail business by Directory, we should look at the business as one combined entity: Next Brand. However, when we do so, we can see that the metrics still look less than appealing

Secondly, we believe that Directory growth has been driven by several one-off factors in the last couple of years and that Next’s first mover online advantage leaves it little room to manouevre as competition online increases, especially given it is already over-penetrated online.

Thirdly and importantly, we believe that Directory margin has peaked and that looking forward there are a number of pressures on margin including but not limited to negative mix effects from growth in cash customers and the potential introduction of free delivery.

Fourthly, we believe that this view ignores the pressures being placed upon the retail business, where management's scope to further reduce costs in our view looks to be limited.

In this note we aim to examine what we consider to be the main pressure points within the Next business, looking at the business on both a combined Brand basis as well as breaking the P&L down into its component parts to examine its ability to flex to meet a lower sales environment.

7

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

One Brand, one dream – does it matter where the sales come from?

The positive argument in favour of investing in Next’s shares is based on the theory that it does not matter where the sales come from provided combined Brand sales are growing. However, our take is that such a view ignores several key factors:

Growth in the combined Brand sales (ie Retail + Directory) has been driven by new space growth and ex this new space, Brand sales have been falling on a “LFL” basis

Sales densities for the combined business have been falling consistently over time

Directory has been the main driver of group sales and profitability in recent years and has been cannibalizing the retail business

The more recent sales growth in Directory has been coming from cash customers, who are less profitable and who have come, we believe, from the Retail business

The two different channels, Retail and Directory have different cost structures, even though there is some cross-subsidisation of, for example, returns

Brand EBIT per sq ft has fallen by 29% over the last decade despite the substantial improvement Next has delivered in gross margins

Opex as a % of sales (for the combined business) has risen by 450bp over the last 10 years, despite considerable efforts by management to trim costs

A persistent decline in sales densities in Retail will eventually lead to a tipping point in terms of the fixed cost base of the Retail business leading to declines in Retail profit

Next sales densities fall even on the combined business

While we accept management’s argument that the two businesses should be examined as one entity and indeed that is how we look at multi-channel businessesfor other retailers, we equally believe that we cannot ignore the strains on store metrics of a falling sales base. This is discussed in more depth later in this report, but first examining the combined businesses as one, we see that perhaps, contrary to commonly held belief, the combined sales densities for Next Retail and Directory have been falling since 2003 (Figure 10) ie the growth in Directory is not outweighing the decline in Retail on a square footage basis. We estimate that the cumulative LFL decline in Brand sales has been -7.7% over the 8 years to 2012.

Brand sales densities (Next Retail and Next Directory

combined) have fallen by 44%

from their peak in 2003

8

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Figure 10: Next Brand sales densities

£ sq ft

Source: J.P. Morgan estimates, Company data.

Both new space and Directory are key for Brand sales growth

Part of the decline in sales densities can be attributed to the decision by Next to open larger space stores, which do dilute density and also to the decision to roll out Home stores which also generate lower sales densities, but this does not explain the entirety of the reduction as even as space growth has slowed, densities have continued to fall (Figure 11).

Figure 11: Space change vs change in combined sales density

Source: J.P. Morgan estimates, Company data.

0

200

400

600

800

1000

1200

Combined sales density £ sq ft

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

E

2014

E

Space growth Change in combined sales density

9

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Figure 12: Next Brand sales and %ge chge yoy

Source: J.P. Morgan estimates, Company data.

Figure 12 looks at the absolute sales within Next Brand and the rate of growth being delivered and we can see that growth has decreased dramatically since 2002. The average growth in Brand sales over the last five years has been 2% pa despite the addition of 6.6% average new space per annum and growth in Directory. From this, we can see that, despite the headline grabbing growth in Directory, new space has been crucial for the growth of the Next Brand (Figure 13). Without it, sales would have been negative for the combined group in five of the last six years.

Figure 13: Brand sales growth yoy % less weighted space contribution

Source: J.P. Morgan estimates, Company data.

Directory has been the main driver of sales and profit in the last year

Next’s Directory business has grown its sales by 12.4% pa over the comparable period and with c. 80% online penetration of the Directory sales base, we estimate that its fate is inexorably tied to that of the online clothing market. Growth in Directory in the past has been fuelled by two principal factors: an increase in the number of active customers and an increase in the number of pages.

The average spend per customer is also a key factor, but as Figure 14 illustrates has fluctuated considerably over the last decade or so, tending to reflect the economic environment. For instance, it became negative in both 2005 and 2010/2011 as consumers retrenched in a more difficult environment.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

500

1000

1500

2000

2500

3000

3500

4000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Brand sales £m (LHS) y oy chge in Brand sales (%) (RHS)

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brand sales growth less weighted space contribution

Ex new space we estimate that

the Brand has delivered a

cumulative LFL decline of 7.7% over the last 8 years

c. 80% of Directory’s sales are now online; most levers for

growth appear fully utilised

10

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

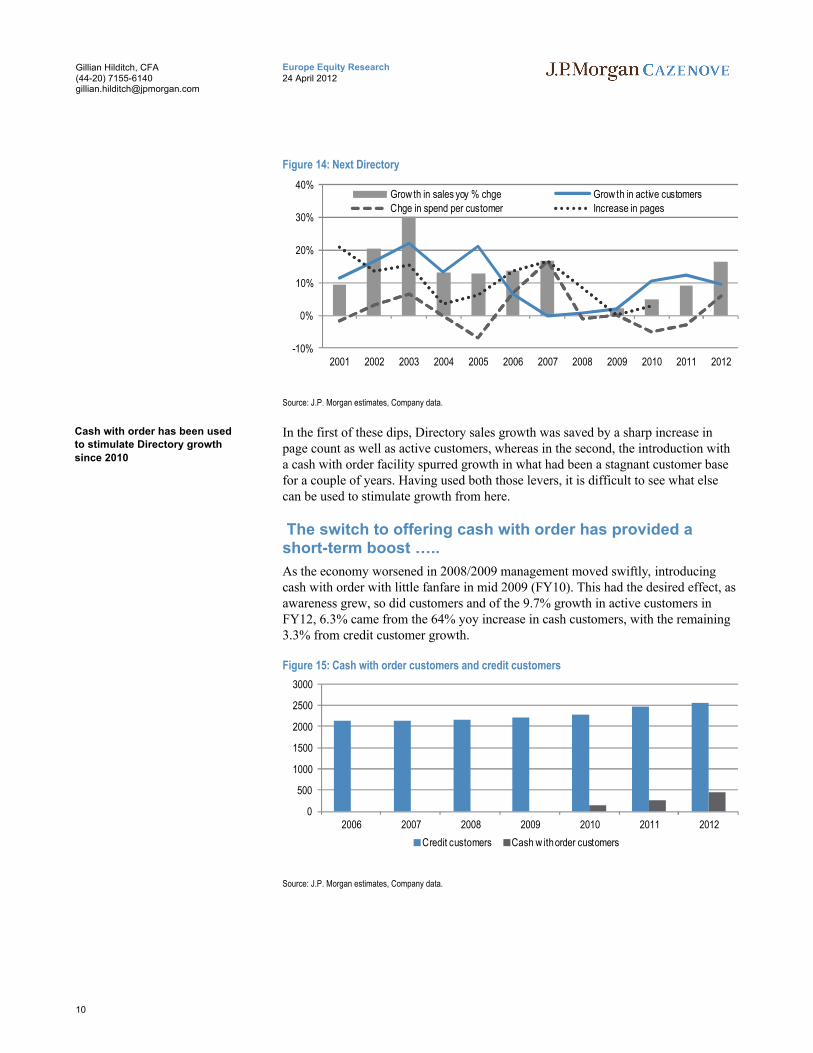

Figure 14: Next Directory

Source: J.P. Morgan estimates, Company data.

In the first of these dips, Directory sales growth was saved by a sharp increase in page count as well as active customers, whereas in the second, the introduction with a cash with order facility spurred growth in what had been a stagnant customer base for a couple of years. Having used both those levers, it is difficult to see what else can be used to stimulate growth from here.

The switch to offering cash with order has provided a short-term boost …..

As the economy worsened in 2008/2009 management moved swiftly, introducing cash with order with little fanfare in mid 2009 (FY10). This had the desired effect, as awareness grew, so did customers and of the 9.7% growth in active customers in FY12, 6.3% came from the 64% yoy increase in cash customers, with the remaining 3.3% from credit customer growth.

Figure 15: Cash with order customers and credit customers

Source: J.P. Morgan estimates, Company data.

-10%

0%

10%

20%

30%

40%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Grow th in sales yoy % chge Grow th in active customers

Chge in spend per customer Increase in pages

0

500

1000

1500

2000

2500

3000

2006 2007 2008 2009 2010 2011 2012

Credit customers Cash w ith order customers

Cash with order has been used to stimulate Directory growth

since 2010

11

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

….., but Next is already over-penetrated online

Our analysis suggests that Next’s share of online clothing is unsurprisingly higher than it is in the overall clothing market. This reflects its early entry into this market with an incumbent high customer base through Directory. This market share has been declining as new entrants expand online.

Over time as all its main competitors build their online offering, we believe Next’s online share should trend towards the market share level it achieves of the overall market, especially once we bear in mind that the level of competition and choice on line will ultimately be greater than that in the physical store base which is naturally limited by geographic boundaries. Next's credit offering could provide some competitive advantage, however, by allowing it to maintain a higher share than it would otherwise, but we think it fair to say that further growth in online share seemsunlikely and the risk of a loss in share is weighted to the downside.

Figure 16 illustrates the growth both in Next's active customer base and in that of Asos over time and demonstrates we believe that Next’s first mover advantage is being eroded as other online retailers grow.

Figure 16: Next Directory Active Customers vs. ASOS

Source: Company Data

Figure 17: Market Share: Directory vs. Retail

Source: J.P. Morgan estimates, Company Data, Verdict

0

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011

Next '000s ASOS '000s

0%

5%

10%

15%

20%

25%

30%

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

Next Directory Next Retail

Next’s market share online is

more than twice that of its bricks

& mortar market share

We believe that Next’s online

share should trend down over

time

12

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

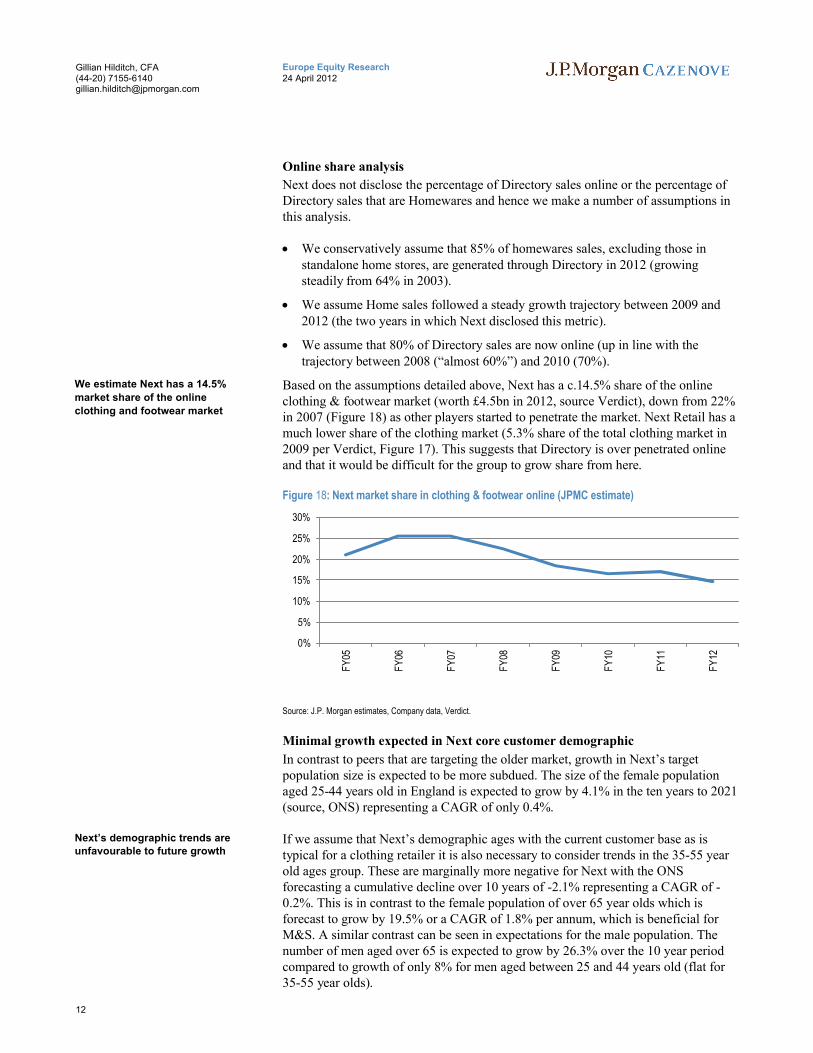

Online share analysis

Next does not disclose the percentage of Directory sales online or the percentage of Directory sales that are Homewares and hence we make a number of assumptions in this analysis.

We conservatively assume that 85% of homewares sales, excluding those in standalone home stores, are generated through Directory in 2012 (growing steadily from 64% in 2003).

We assume Home sales followed a steady growth trajectory between 2009 and 2012 (the two years in which Next disclosed this metric).

We assume that 80% of Directory sales are now online (up in line with the trajectory between 2008 (“almost 60%”) and 2010 (70%).

Based on the assumptions detailed above, Next has a c.14.5% share of the online clothing & footwear market (worth £4.5bn in 2012, source Verdict), down from 22% in 2007 (Figure 18) as other players started to penetrate the market. Next Retail has a much lower share of the clothing market (5.3% share of the total clothing market in 2009 per Verdict, Figure 17). This suggests that Directory is over penetrated online and that it would be difficult for the group to grow share from here.

Figure 18: Next market share in clothing & footwear online (JPMC estimate)

Source: J.P. Morgan estimates, Company data, Verdict.

Minimal growth expected in Next core customer demographic

In contrast to peers that are targeting the older market, growth in Next’s target population size is expected to be more subdued. The size of the female population aged 25-44 years old in England is expected to grow by 4.1% in the ten years to 2021 (source, ONS) representing a CAGR of only 0.4%.

If we assume that Next’s demographic ages with the current customer base as is typical for a clothing retailer it is also necessary to consider trends in the 35-55 yearold ages group. These are marginally more negative for Next with the ONS forecasting a cumulative decline over 10 years of -2.1% representing a CAGR of -0.2%. This is in contrast to the female population of over 65 year olds which is forecast to grow by 19.5% or a CAGR of 1.8% per annum, which is beneficial for M&S. A similar contrast can be seen in expectations for the male population. The number of men aged over 65 is expected to grow by 26.3% over the 10 year period compared to growth of only 8% for men aged between 25 and 44 years old (flat for 35-55 year olds).

0%

5%

10%

15%

20%

25%

30%

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

We estimate Next has a 14.5%

market share of the online

clothing and footwear market

Next’s demographic trends are unfavourable to future growth

13

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

The growth in cash customers encourages cannibalization of the UK store customers

So where, in a difficult consumer market, is this growth in Directory customers coming from? Without access to each customer’s personal details, it is naturally difficult to say definitively, but unsurprisingly our analysis of Next’s online market share and Directory share would seem to suggest that they are primarily coming from the Next Retail store base rather than representing incremental consumers. This is, we believe, undoubtedly the case when we think about the growth in the context both of Next's over-penetration online and of the recent boost provided by the switch to cash with order, which has tempted those "hold-out” Next Retail customers who did not like having to order on credit.

Figure 19: Next Online share change vs Next Directory share change (2009 on 2005)

Source: Verdict

That online is cannibalising store sales is not new news. For some years now the debate in retail has been around the transfer of sales from physical space to online and the impact that could potentially have on store metrics. Nowhere within clothing is that effect more marked than at Next, which has the most developed online business of any of the major apparel players.

Directory now represents 31% of Group sales and is more than half the size of Retail and is cannibalising the store base. Yet investors do not seem to be concerned by this trend, if the share price is any judge, and they have been right not to be over the last few years as the company has maintained profitability in the face of challenging economic conditions. However, we argue that this trend is unsustainable in the longer-term and there will inevitably be a point at which the metrics within the store base will move the wrong way.

Overall market share in clothing appears to be stagnant

We have disaggregated Next Home sales from its overall Brand sales to derive a clothing and footwear number, which we have then divided into the Verdict market value to derive an estimated market share for Next. This clearly is not perfect, but it provides we think a useful guide as to the trend in Next’s market share in recent years ex its growth in Home.

-1.00% -0.50% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00%

PrimarkSainsbury

Shop DirectTK Maxx

TescoPeacocksNew Look

AsdaArcadia Group

River IslandN Brown

H&MNext DirectorySports Direct

DebenhamsJohn LewisBonmarche

MatalanHouse of Fraser

Next RetailM&S

Figure 19: illustrates that the growth in Directory between

2005 and 2009 has come at the

expense of Retail

14

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Figure 20: Next Market share

Source: J.P. Morgan estimates, Verdict, Company data. Using Next Financial Years

Profit per sq ft has also been fallingUnderlying cost efficiencies have been unable to keep pace with falling sales

Brand sales densities have been falling since 2003, decreasing by 44% in total from £953 to £533 in 2012. This has been partially mitigated by an improving gross margin with COGS falling by 50% on a square foot basis over the period. However, despite aggressive efficiencies in underlying costs, the decline in opex per square foot has been unable to fully keep pace with the Brand LFL sales decline (we estimate -1% on average over the eight years to 2012) resulting in an overall fall in Brand EBIT per square foot of 28% from £130 in 2003 to £93 in 2012. This begs the question as to what happens when sales per square foot approach the point at which profit begins to move backwards. We explore this further in our scenario analysis

Figure 21: Retail EBIT per sq ft

Source: J.P. Morgan estimates Company data.

Figure 22: Next Brand EBIT per sq ft

Source: J.P. Morgan estimates, Company data.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2004 2005 2006 2007 2008 2009 2010 2011

Market Share (sales/ONS mkt value)

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Retail EBIT per sq ft

0

20

40

60

80

100

120

140

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brand EBIT per sq ft

The decline in sales densities

has been mitigated by strong growth in gross margin. Despite

aggressive reductions in costs,

the decline in opex sq ft has been unable to keep pace

15

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Scope to further cut costs appears limited

Next’s cost ratios at first glance appear high when examined against its peer group; however, this is a function of a falling sales base relative to more limited reductions in the cost base. In fact, management has controlled costs very tightly over the period.

Figure 23: Rental costs compared (last reported)

Source: J.P. Morgan estimates Company data. NB Next sales include Directory

Figure 24: Staff costs compared (last reported)

Source: J.P. Morgan estimates, Company data. NB staff costs for Next include Directory staff costs and Directory sales

Focusing on staff as % sales ignores the already efficient nature of Next’s staffing

While Next’s staff costs are high relative to peers (Figure 24), it has been making considerable efficiencies over time (Figure 25), which have allowed it to maintain its staff cost ratios at a fairly constant level of sales despite sales densities halving. This has been achieved through improved scheduling amongst other things, which has allowed Next to reduce staff intensity per 000 sq ft by 50% over the last seven years.

Management argues that staffing densities are an irrelevant measure as the most important metric to focus on is staff costs as a % of sales, as it is throughput of product per staff member that matters, not intensity of staff on the shop floor. While we can see some validity to this argument, we would, however, suggest that having a lower staffing ratio per 000 sq ft than peers may well mean that customers compare their ability to find a staff member when they want one unfavourably across retailers.

0.020.040.060.080.0

100.0120.0140.0

Rental Costs per sq ft

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%

Rent % sales

020406080

100120140160180

Staffing Costs Per Sq ft £

0%

5%

10%

15%

20%

25%

Staff % sales

Next has reduced staff per 000 sq ft by 50% over the last 7 years

Management argues that the most important metric to focus

on is staff costs as a % of sales

as it is throughput of product per staff member that matters,

not intensity on the shop floor

16

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

More importantly the already low level of staffing means in our view that the scope to make further efficiencies in this area is limited.

Figure 25: Brand staff costs – ratios have improved over time

Source: J.P. Morgan estimates, Company data.

Figure 26: Staff intensity has dropped

Source: J.P. Morgan estimates, Company data. NB this includes Directory staff, store staff per 000 sq ft is even lower

Furthermore, we would note that the above ratios are based on Brand staffing numbers (ie inclusive of Directory) and that Retail FTEs could now be as low as just over 3 per 000 square foot (down from over 7 in 2001) highlighting that whilst cost efficiencies have been aggressive, there is little scope for further savings. If we are correct in our estimate it would also imply store staffing levels only marginally above New Look (2.2 per 000 sq ft) which is well known for its focus on value ahead of customer service.

16.0%

16.5%

17.0%

17.5%

18.0%

18.5%

19.0%

19.5%

20.0%

2004 2005 2006 2007 2008 2009 2010 2011

Staff costs as % of sales

0

20

40

60

80

100

120

140

160

2001 2003 2005 2007 2009 2011

Brand staff costs per sq ft

0

1

2

3

4

5

6

7

8

9

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Next Brand employees per 000 sq ft

But the already efficient staff

base in our view shows that the

scope to make more efficiencies is limited

17

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Directory margin could have peaked

Whenever we discuss our concerns over the profit densities in the Retail business, bulls on Next point to the attractive margins in the Directory business. However, CEO Simon Wolfson made an intriguing comment at the FY results in March 2012 at which he remarked that “Directory margin has peaked”. This may well have been his usual caution, but we see two very concerning trends, which could well support this view.

Cash customers are growing faster than account customers. Cash customers order less and are less profitable than account holders. Every 10% shift in proportion of cash customers costs c. 80bps of Directory margin.

Free delivery is becoming increasingly prevalent in the market place. While Next is vehemently opposed to the introduction of free delivery as standard, if it were forced to do so as a defensive move then we estimate a c. 18% impact to group PBT

In addition, management expects international customers to grow by 70% in FY13 to 4.5%. These customers generate a margin of 20% (vs Directory average of 23.5%). Every 10% shift towards international costs c. 30bp of margin, so while not significant, it is not helpful, in our view

Growth in less profitable cash customers to outpace credit account holders

Cash customers spend less on average

In the first 2 years following the start of the downturn, sales per customer were relatively flat at £370 in 2008 and £371 in 2009. In 2010 sales per active customer fell by 5% to £352. This was driven by the introduction of cash with order where customer spend is significantly lower in part because they order less in value terms per order and in part because they order much less frequently. Whilst the differential has reduced it remains significant, we estimate in the region of 42% (spend in store is c.third of average Directory account customer spend and hence a differential in cash versus credit spend in the region of 30% to 45% seems reasonable).

In 2012 sales per customer grew by 6% to £364 per customer (albeit remaining below 2007 levels of £374). The increase is explained at least in part by an improved service offering in the year, and in particular the introduction of next day delivery as standard for orders before 9pm. However, it is not clear if the group’s initiatives generated incremental Brand sales, or rather encouraged an acceleration in the shift to Directory, with falling sales densities at a Brand level being supportive of the latter. Furthermore, the impact of the introduction of next day delivery clearly shows the impact of the service offering on customer behavior, highlighting the importance of being at least in line with peers on service with regards to delivery and returns.

Increasing proportion of cash customers will generate further margin dilution

Cash with order customers currently account for 14.6% of the Directory customer base but account for a lower proportion of sales (we estimate c.9%) due to a lower average spend (we estimate spend by cash customers is c.42% lower on average).

We estimate that cash with order

customers spend c. 42% less

than account customers

We believe increased

convenience of the service

proposition stimulated the transfer of Retail customers to

Directory

18

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Account customers are more profitable as a result of the service income they generate, effectively the interest income (25.99% APR) and charges on the credit provided by Next, less the bad debt charge. Between 2007 and 2009 (before the introduction on cash with order) the average benefit to the Directory margin as a result of the net service income was 8.3%, implying that account customers are more profitable than cash with order customers. This has been confirmed by management.Since the introduction of cash with order in 2010, Next has lost up to 180bp of margin. Whilst this was in part due to customers paying more quickly (in order not to incur interest and charges that they could ill afford given the difficult macro), weestimate that at the very least, every incremental 10% penetration of cash with order customers will have a dilutive impact on the Directory margin of c.80-90bps. Going forward we expect the growth in cash customers to continue to outpace accountcustomers (account customers +12% in the 2 years to 2012 versus cash customers +196%) as Retail customers who have traditionally paid by cash and have been reluctant to open an account migrate sales online.

Since 2010 cash customers have grown by 8.5% as a proportion of the total Directory customer base to 14.6% and management believes this could comfortably rise to 20% within the next 2 years. The trajectory to date suggests that this forecast could be conservative (and management accepts that in the long term cash penetration could be substantially higher, although it does not necessarily think it will be). Merely taking the 20% number given by management would imply an incremental 5.4% penetration, which would impact the Directory margin by c.40bps to 50bps.

Figure 27: Service income as % of Directory sales

Source: J.P. Morgan estimates, Company data.

0%

2%

4%

6%

8%

10%

12%

14%

2005 2006 2007 2008 2009 2010 2011 2012

Serv ice income as % of sales

We estimate that every 10% shift

towards cash customers costs c.

800bps of margin

Management believes that

penetration could in theory

comfortably exceed 20%

19

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

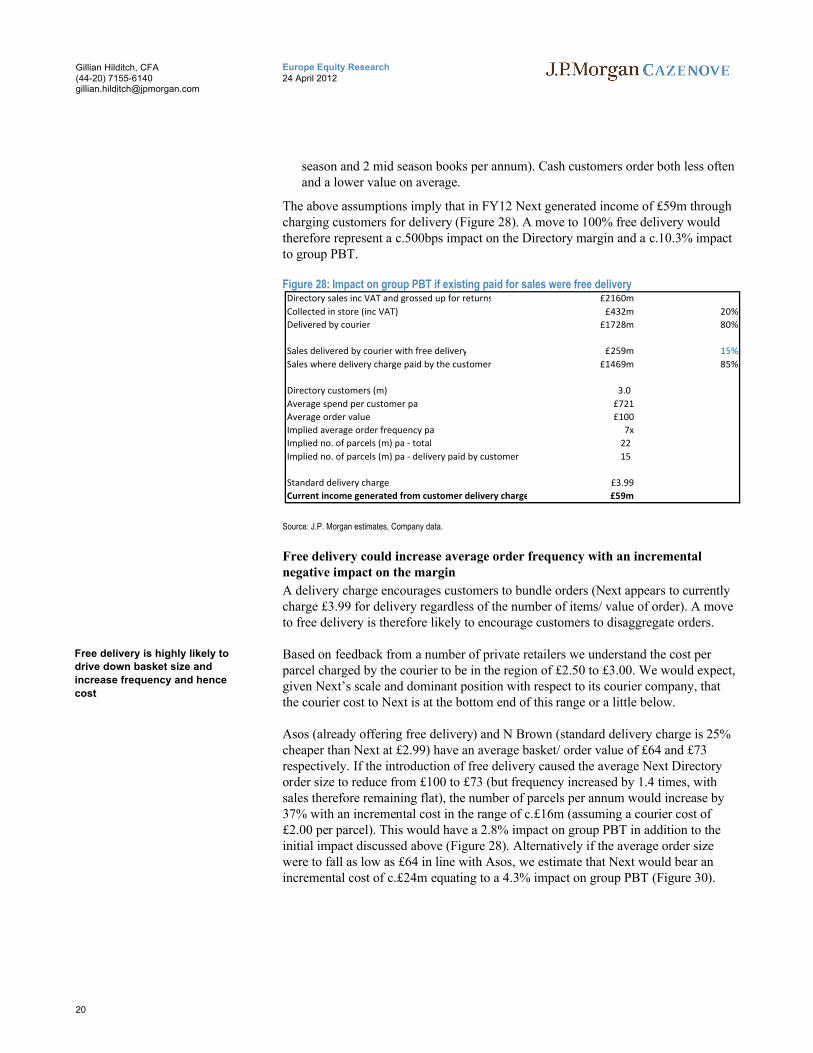

Move to free delivery could reduce Group PBT by 18%

We have carried out some analysis to estimate the potential margin dilution if Next were to move to a free shipping policy. We have made a number of assumptions in doing so; but the key impacts are:

Moving to free delivery on the remaining c. 85% of parcels adversely impacts Directory margin by 500bp equating to 20% of Directory EBIT and 10% of group PBT

Free delivery as standard is likely to increase frequency of purchase and reduce average order size, further impacting profit by up to 4.3%

Free delivery could encourage a faster channel shift away from Retail. This could cost c. 3.7% of PBT over a 3 year period

In aggregate we estimate that free delivery could cost c. 18% of group PBT over a 2-3 year time frame. This equates to lost margin of c. 900bp. This compares to the cost to Asos of 1300bp from a shift to free shipping,although Asos has a greater proportion of international sales, which will be more expensive.

Free delivery – negative impact of 900bp on Directory margin

At present Next charges for c. 85% of deliveries. The standard charge is in the region of £3.99 per order/ parcel. However, management does not disclose enough detail forus to calculate the number of order/ parcels shipped to customers per annum and hence we attempt to estimate this based on a number of assumptions.

We use the following information in our calculations:

20% of Directory sales are collected in store (company disclosed that 20% of Directory parcels are collected in store at the FY12 results).

15% of the Directory sales delivered by courier are already free (Next commented at the FY12 interim results that 20% of Delivery was effectively free and although management noted at the FY results that this had reduced, we use 15% as our best estimate).

There are 3 million Directory customers (as disclosed by Next at the FY results). This implies an average annual spend per customer in 2012 of £721 including VAT and grossed up for returns (excluding both returns and VAT average annual spend is £364).

We estimate a Directory returns rate of 41% (calculated from disclosure in the FY12 results and supported by management’s comments that Directory returns are in the high thirties).

We assume that the average standard delivery charge for paid for orders is £3.99 as per the website (this charge appears to be applied to all orders as standard regardless of product category or value).

We assume an average order value (inc VAT) of £100, implying an average order frequency of 7 times per annum. This is in line with management’s comments that account customers order over £100 of product 2-3 times a season (2 main

We estimate that free delivery

would negatively impact

Directory margin by 900bp

20

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

season and 2 mid season books per annum). Cash customers order both less often and a lower value on average.

The above assumptions imply that in FY12 Next generated income of £59m through charging customers for delivery (Figure 28). A move to 100% free delivery would therefore represent a c.500bps impact on the Directory margin and a c.10.3% impact to group PBT.

Figure 28: Impact on group PBT if existing paid for sales were free delivery

Source: J.P. Morgan estimates, Company data.

Free delivery could increase average order frequency with an incremental negative impact on the margin

A delivery charge encourages customers to bundle orders (Next appears to currently charge £3.99 for delivery regardless of the number of items/ value of order). A move to free delivery is therefore likely to encourage customers to disaggregate orders.

Based on feedback from a number of private retailers we understand the cost per parcel charged by the courier to be in the region of £2.50 to £3.00. We would expect,given Next’s scale and dominant position with respect to its courier company, that the courier cost to Next is at the bottom end of this range or a little below.

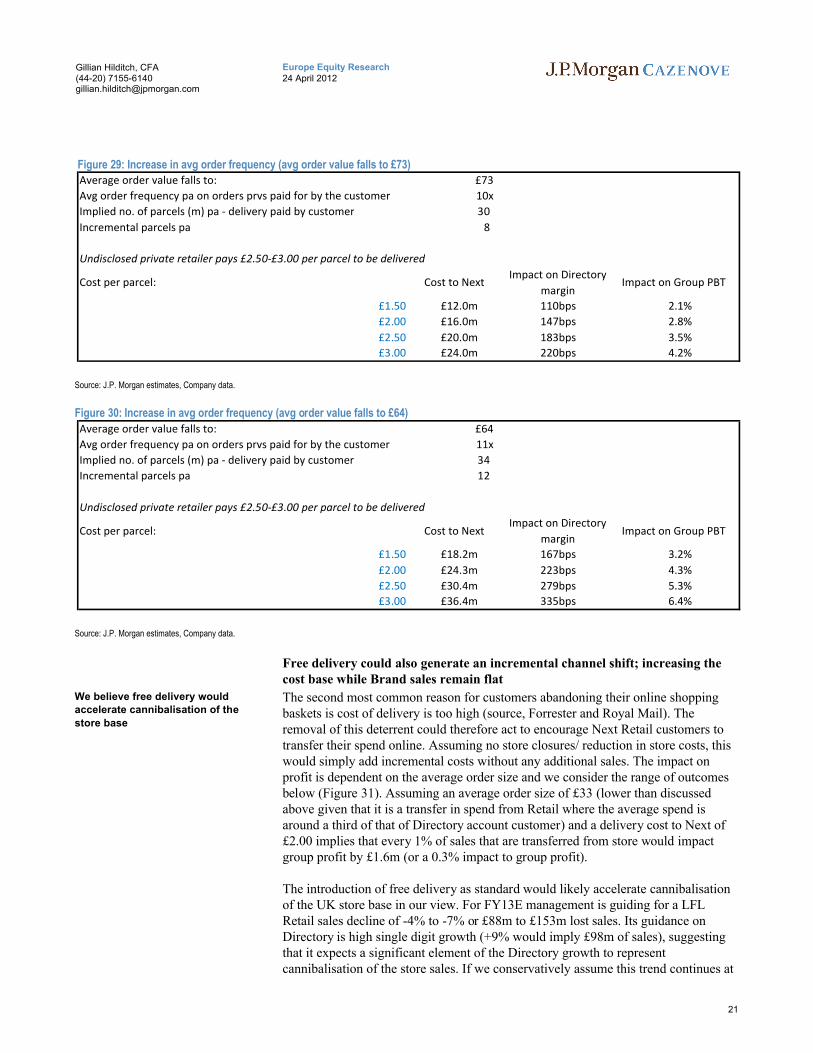

Asos (already offering free delivery) and N Brown (standard delivery charge is 25% cheaper than Next at £2.99) have an average basket/ order value of £64 and £73 respectively. If the introduction of free delivery caused the average Next Directory order size to reduce from £100 to £73 (but frequency increased by 1.4 times, with sales therefore remaining flat), the number of parcels per annum would increase by 37% with an incremental cost in the range of c.£16m (assuming a courier cost of £2.00 per parcel). This would have a 2.8% impact on group PBT in addition to the initial impact discussed above (Figure 28). Alternatively if the average order size were to fall as low as £64 in line with Asos, we estimate that Next would bear an incremental cost of c.£24m equating to a 4.3% impact on group PBT (Figure 30).

Directory sales inc VAT and grossed up for returns £2160m

Collected in store (inc VAT) £432m 20%

Delivered by courier £1728m 80%

Sales delivered by courier with free delivery £259m 15%

Sales where delivery charge paid by the customer £1469m 85%

Directory customers (m) 3.0

Average spend per customer pa £721

Average order value £100

Implied average order frequency pa 7x

Implied no. of parcels (m) pa - total 22

Implied no. of parcels (m) pa - delivery paid by customer 15

Standard delivery charge £3.99

Current income generated from customer delivery charge £59m

Free delivery is highly likely to drive down basket size and

increase frequency and hence

cost

21

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Figure 29: Increase in avg order frequency (avg order value falls to £73)

Source: J.P. Morgan estimates, Company data.

Figure 30: Increase in avg order frequency (avg order value falls to £64)

Source: J.P. Morgan estimates, Company data.

Free delivery could also generate an incremental channel shift; increasing the cost base while Brand sales remain flat

The second most common reason for customers abandoning their online shopping baskets is cost of delivery is too high (source, Forrester and Royal Mail). The removal of this deterrent could therefore act to encourage Next Retail customers to transfer their spend online. Assuming no store closures/ reduction in store costs, this would simply add incremental costs without any additional sales. The impact on profit is dependent on the average order size and we consider the range of outcomes below (Figure 31). Assuming an average order size of £33 (lower than discussed above given that it is a transfer in spend from Retail where the average spend is around a third of that of Directory account customer) and a delivery cost to Next of £2.00 implies that every 1% of sales that are transferred from store would impact group profit by £1.6m (or a 0.3% impact to group profit).

The introduction of free delivery as standard would likely accelerate cannibalisation of the UK store base in our view. For FY13E management is guiding for a LFL Retail sales decline of -4% to -7% or £88m to £153m lost sales. Its guidance on Directory is high single digit growth (+9% would imply £98m of sales), suggesting that it expects a significant element of the Directory growth to represent cannibalisation of the store sales. If we conservatively assume this trend continues at

Average order value falls to: £73

Avg order frequency pa on orders prvs paid for by the customer 10x

Implied no. of parcels (m) pa - delivery paid by customer 30

Incremental parcels pa 8

Undisclosed private retailer pays £2.50-£3.00 per parcel to be delivered

Cost per parcel: Cost to NextImpact on Directory

marginImpact on Group PBT

£1.50 £12.0m 110bps 2.1%

£2.00 £16.0m 147bps 2.8%

£2.50 £20.0m 183bps 3.5%

£3.00 £24.0m 220bps 4.2%

Average order value falls to: £64

Avg order frequency pa on orders prvs paid for by the customer 11x

Implied no. of parcels (m) pa - delivery paid by customer 34

Incremental parcels pa 12

Undisclosed private retailer pays £2.50-£3.00 per parcel to be delivered

Cost per parcel: Cost to NextImpact on Directory

marginImpact on Group PBT

£1.50 £18.2m 167bps 3.2%

£2.00 £24.3m 223bps 4.3%

£2.50 £30.4m 279bps 5.3%

£3.00 £36.4m 335bps 6.4%

We believe free delivery would accelerate cannibalisation of the

store base

22

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

the lower end of the range (that is, 4% of Retail sales shift into Directory per annum) and that these sales are free delivery this implies a c.1.2% negative impact on group profit per annum (that is 4x the 0.3% impact discussed above). Over 3 years therefore this would reduce PBT in the region of 3.6%.

Figure 31: Impact if sales are transferred from Retail to Directory

Source: J.P. Morgan estimates, Company data.

Experience of Asos highlights risk of margin dilution

All of this, of course is theoretical, but we do have a real life example to look at in Asos, which has been a leader relative to other UK retailers in developing its service offering to consumers. Both delivery and returns are now free for UK customers. Initially both delivery and returns were charged for and Asos formally moved to free delivery in the UK in April 2010. However, in the years prior to this it had been increasingly moving towards this point with an increasing number of promotional free delivery offers. Over this period the group moved from making a small profit on delivery receipts of £1.9m in 2008, to a loss of £21.9m in 2011, representing an impact on the group operating margin of 9.5% (marginally inflated by the impact of free global shipping in one quarter of 2011). In 2013 this is expected to move to a loss of £85m on a sales base of £676m (this compares to Next Directory’s sales of £1.1bn), representing 13% of sales. This gives some context to our assumptions above and provides us with some comfort on the assumptions.

Free returns is much less significant - 94% of returns are free already

The Directory business has a returns rate in the high 30s. Customers make 59% of their returns through stores at no tangible delivery cost to Next (whilst there is a cost of processing a return in store, a processing cost would also have been incurred had the goods been returned directly to the warehouse and this is therefore simply an allocation issue in our view). Returns are free for Next cardholders and therefore we estimate that Next already incurs the delivery charge for a further 35% of returns. This leaves only 6% of returns where the cost is currently incurred by the customer. Assuming a cost of c.£2.00-2.50 to Next per parcel and an average return value of £41 (given the 41% returns rate and assumed average order value of £100) would imply a c.0.4% impact to group earnings if free returns were implemented. Given that 85% of the Directory customer base (that is, account customers) are already eligible for free returns, we would not anticipate a significant change in the

Retail sales £2191m

1% transfer of Retail sales (ex VAT) £22m

1% transfer of Retail sales (inc VAT) £26m

Avg order size £33 £64 £73 £100

Implied no. of parcels (m) 0.8 0.4 0.4 0.3

Undisclosed retailer pays £2.50 to £3.00 per parcel

Incremental cost:

£1.50 £1.2m £0.6m £0.5m £0.4m

£2.00 £1.6m £0.8m £0.7m £0.5m

£2.50 £1.9m £1.0m £0.9m £0.6m

£3.00 £2.3m £1.2m £1.1m £0.8m

Free shipping is expected to

cost Asos c.13% of sales in FY13E, up from zero in 2008

Free returns are not expected to

have a significant impact as

virtually all returns are already free.

23

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

percentage going through store if a blanket free returns policy was introduced and hence we would not expect the impact to be material.

Given the high proportion of free returns already in place, we would not expect a move to free delivery/ returns to significantly change the returns rate.

Reduced production and print costs could partially offset the impact – but high risk

Despite customers paying c.£4 for a Next Directory, each book costs the company c.£12 to produce and deliver, generating a loss therefore of around £8 per book. Each year there are 4 editions of the catalogue (Christmas, Autumn/Winter, Spring/Summer and Summer). Of the almost 3 million Directory customers we assume 2.3m buy a copy of the book, implying a maximum cost, and therefore maximum potential saving, in the region of £72m, representing 12.6% of PBT.

However, there are two reasons why any potential saving is likely to be some way below this level. Firstly there are costs associated with the production of the Directory that would continue to be incurred regardless of the size of the print run (all the photography for example is also necessary for displaying the product on the website). We estimate that the delivery cost is c.£4 of the full £12 cost per book. In 2000 we estimate that print costs were c.£4.20 per book (based on active customernumbers and disclosure that print costs represented 6% of Directory sales at the time). Given the threefold increase in customers since then we would expect the current print cost per book to be at a lower level. However, this implies current photography costs in the region of £36m (ie c. 50% of the total cost) and therefore a maximum potential saving of £36m (representing 6.3% of PBT).

Secondly, whilst the number of catalogues is likely to decline over time as Next customers become increasingly comfortable with using the internet to browse rather than simply to order, at present management view it as a key sales driver and there is therefore a risk that any sharp deterioration in catalogue distribution could negatively impact the top line to a significant degree.

We estimate the Big Book production and print costs are

c.12.6% of PBT annually

Scope to cut these is limited as we estimate c. 50% are fixed

In addition, the adverse impact on sales of withdrawal of the Big

Book would be in our view

significant

24

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

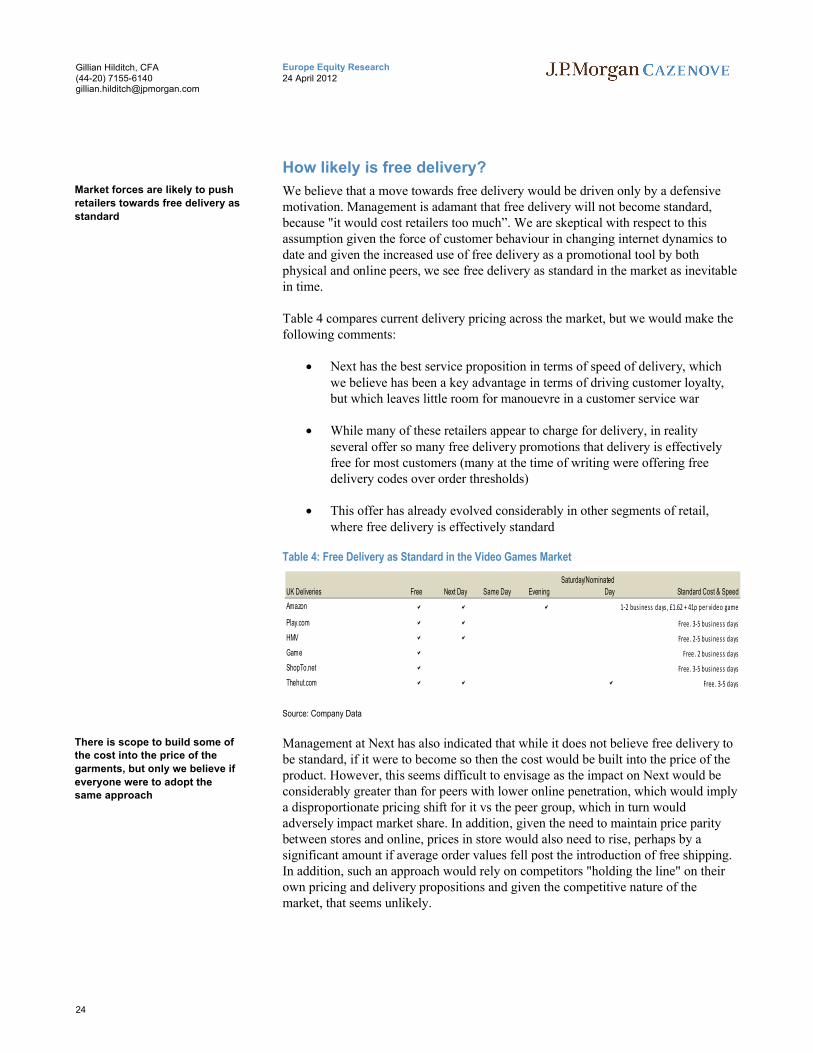

How likely is free delivery?

We believe that a move towards free delivery would be driven only by a defensive motivation. Management is adamant that free delivery will not become standard, because "it would cost retailers too much”. We are skeptical with respect to this assumption given the force of customer behaviour in changing internet dynamics to date and given the increased use of free delivery as a promotional tool by both physical and online peers, we see free delivery as standard in the market as inevitable in time.

Table 4 compares current delivery pricing across the market, but we would make the following comments:

Next has the best service proposition in terms of speed of delivery, which we believe has been a key advantage in terms of driving customer loyalty, but which leaves little room for manouevre in a customer service war

While many of these retailers appear to charge for delivery, in reality several offer so many free delivery promotions that delivery is effectively free for most customers (many at the time of writing were offering free delivery codes over order thresholds)

This offer has already evolved considerably in other segments of retail, where free delivery is effectively standard

Table 4: Free Delivery as Standard in the Video Games Market

Source: Company Data

Management at Next has also indicated that while it does not believe free delivery to be standard, if it were to become so then the cost would be built into the price of the product. However, this seems difficult to envisage as the impact on Next would be considerably greater than for peers with lower online penetration, which would imply a disproportionate pricing shift for it vs the peer group, which in turn would adversely impact market share. In addition, given the need to maintain price parity between stores and online, prices in store would also need to rise, perhaps by a significant amount if average order values fell post the introduction of free shipping. In addition, such an approach would rely on competitors "holding the line" on their own pricing and delivery propositions and given the competitive nature of the market, that seems unlikely.

UK Deliveries Free Next Day Same Day Evening

Saturday/Nominated

Day Standard Cost & Speed

Amazon 1-2 bus iness days , £1.62 + 41p per vide o game

Play.com Free . 3-5 bus iness days

HMV Free . 2-5 bus iness days

Game Free . 2 bus iness days

ShopTo.net Free . 3-5 bus iness days

Thehut.com Free . 3-5 days

Market forces are likely to push

retailers towards free delivery as

standard

There is scope to build some of the cost into the price of the

garments, but only we believe if

everyone were to adopt the same approach

25

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Table 5: Comparison of free delivery options in the UK

Source: J.P. Morgan estimates, Company data.

Could free delivery grow Next Directory sales?

It is possible that free delivery could drive incremental sales. This has been the case with Asos but we would argue that it had a first mover advantage as well as no significant incumbent store base to cannibalise.

Furthermore, Next already has significant penetration of its customer profile base (ABCD1 women in the 25-44 year old age bracket). Assuming that the majority of the almost 3 million Directory customers are women implies 41% penetration in this age bracket alone (7.2 million, 25-44 year old women in the UK, source ONS), and in practice will be higher than this given that the Next demographic is focused on ABC1’s. Furthermore this excludes any Next Retail customers that do not shop through Directory. This implies an even higher penetration in their core customer demographic. Hence, in our view, incremental Next Brand customer growth in the UK is unlikely from here and we would not expect to see a material impact on Brand sales as a result of free delivery.

UK Deliveries Free Next Day Same Day Evening

Saturday

/Nominated Day Standard Cost & Speed

Free Standard Delivery

Rachets

ASOS £3.95. Within 3 working days On orders over £70

Debenhams Free. 2-4 working days

Next £3.99. Next Day

Marks & Spencer £3.50. Up to working 5 days

H&M £3.90. Within 4-6 working days

Zara £3.95. Within 3-5 working days

John Lewis £3.00. Within 4 working days On orders over £30

Ted Baker £4.50. Within 2-5 working days

House of Fraser £3.00. Within 3-5 working days On orders over £50

River Island £3.95. Within 5-7 working days

Very.com £3.95. Next Day

Boohoo.com £3.99. Within 4 working days

Warehouse £2.99. Within 5 working days On orders over £55

Topsop £4.00. Within 2-4 working days

French Connection £3.95. Within 3 to 5 working days On orders over £75

Free delivery a defensive stance;

incremental Brand customers unlikely given existing

penetration

26

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Outlook for FY13E and beyond

We are looking for PBT at Next to fall by an average of 3% per annum over the next three years (to 2015E). This includes a fall of 1.6% in FY13E, at the bottom of management's guidance range (Table 6).

FY13E Guidance

Management’s guidance for FY13E is outlined in Table 6: .

Table 6: Management guidance for H1 and FY 2013

Low-scenario High scenarioH1 guidanceLFL Retail sales -7% -4%Total Retail sales -3% 0%Directory sales +9% +12%Brand sales +1% +4%

FY13 guidanceBrand sales +1% +4%PBT £560m £610mPBT growth -2% +7%Buyback (% of shares) +4% +4%EPS growth +3% +12%

Source: Company reports.

Total Brand sales are expected to increase by +1% to +4% with high single digit growth expected from Directory (H1 guidance is +9% to +12%). Assuming 9% growth for Directory, would imply a FY change in Retail sales of between +1% and -3% (H1 guidance is 0 to -3%), which given an expected space contribution of 4% (60% conversion) implies an expected LFL of between -3% and -7%.

Bought in gross margins are expected to be flat with manufacturing costs and selling prices level yoy. No significant changes to markdown are expected; hence, gross margins are expected to remain flat.

Annual LFL inflation in the cost base is expected to be £36m driven by wage inflation of 2.5% and underlying increases in rent and rates. Management expects to offset £28m of this cost pressure with cost savings.

Management has also indicated that we should expect a £28m interest charge, £8m of profit from international and £25m of profit from sourcing.

Implementing management’s guidance, results in a modest upgrade to our PBT estimate for FY13E from £545m to £561m. This puts us at the bottom of the range of guidance and 5% below BBG consensus of £590m. This appears to be primarily due to our assumptions on margin as we are only 1% below BBG consensus on sales. These assumptions are discussed in more depth below.

Management guidance implies

an FY13E LFL of between -4% and -7%

27

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

FY13E assumptions

Q1 likely to be difficult

Next is due to report its Q1 IMS on 2 May. We expect LFL Retail sales to have declined by 9% which, while a deterioration on a headline basis (Q4 FY12 -3.2%), represents a broad maintenance of the underlying run-rate on a comparative that is c.650bps tougher. In line with management’s FY guidance we expect a contribution from new space in the region of +4% resulting in a decline in total Retail sales of -5% (expected new space contribution to total Brand sales +2.7%). In the Directory business we also assume that the underlying trend continues (2-year growth rate +26%) implying Q1 sales +11% yoy.

Retail sales data and commentary for Q1 has to date been marginally more positive than over the last 6 months. John Lewis has reported strong performances with fashion being up mid to high single digit on average. M&S sales, whilst disappointing, were the result of the group under potentialising and M&S data actually suggested that the consumer environment was stable to marginally more positive. The warm weather in March also provided a boost. Overall therefore it appears that underlying trends in the consumer environment are largely unchanged since Next released its FY results in mid-March and as such we do not expect any material changes to FY guidance (JPMCe FY13E PBT c. 5% below consensus).

FY sales growth bolstered by strong Directory

Within the Retail business we expect square footage to grow by c.6% in FY13 and contribute 4% to top line growth (60% conversion), in line with the guidance. At this stage management expects around half of the space to be in standalone home stores. We forecast a FY13 LFL of -5.5% at the mid-point of the implied guided range (-4% to -7%). Overall therefore we expect sales in the Retail business to decline by -1.5%. We expect Directory growth to continue to be impressive at +9% (guidance is for high single digit growth) driven by in part by the ongoing annualisation of the “offers” tab and in the main by a continued shift in spend from Retail, through both growth in cash customers and an increase in account customer spending online rather than via cash in store. In line with management guidance we also assume an incremental £20m from international online sales (taking the total to £50m) which contributes 1.8% to total Directory growth of +9%. Overall therefore this implies total growth in Brand sales of +2%, within the range of management guidance of +1% to +4%. We would note however, that given the new space contribution, this implies a negative underlying Brand LFL of -0.7% (or -1.3% excluding international online).

FY margin in both businesses under pressure

We assume that the gross margin in both divisions remains flat yoy given no material change expected by management in bought in gross margin or the level of markdown yoy. We expect the Retail EBIT margin to decline by 100bps yoy (discussed in detail below) which, combined with the negative top line performance, results in EBIT of £297m, a yoy decline of 8.2%. We expect Directory EBIT margin to fall by 60bps yoy (discussed in detail below), generating growth of only 6.2% yoy in Directory profits (despite the more impressive top line performance).

Contribution from new space is

expected to be 4% pa

Gross margins expected to

remain flat

28

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

We model international and sourcing profit and interest in line with guidance as detailed above. Combined with a share option charge of £17m (flat yoy) we expect PBT of £561m, a decline of -1.6% yoy, at the bottom of the guided range of -2% to +7%.

FY14E assumptions

Sales trend unchanged in Retail, but Directory slows to +5%

In FY14E we expect top line trends within the Retail division to remain broadly unchanged with space growth of +4.3% and Retail LFL of -6% resulting in an overall decline in Retail sales of -1.7%. However, we anticipate that the extent of mitigation caused to the overall decline in Brand sales reduces as the rate of Directory growth slows. We forecast Directory growth of only 5% in FY14, implying LFL Brand sales of -2.1% (total Brand sales +0.6%).

Pressure persists on margin

We have little visibility on gross margins out to CY13, however, we see little reason for the sourcing environment to move in the retailers’ favour (with Chinese wages for example continuing to experience double digit increases). With any improvement in the aggressively promotional environment that currently persists likely to be offset, we assume gross margins remain flat. We assume a continued decline in both the Retail and Directory EBIT margins, by 110bps and 60bps respectively (discussed in more detail below). With the other largest elements of PBT (share option charge and interest) being unchanged yoy this results in FY14E PBT of £542m (-3.5% yoy).

FY15E assumptions

We expect sales trends in both the Retail and Directory business to be unchanged versus FY14 with Retail sales falling by 2% in total (space +4% and LFL -6%) and Directory growth of +5%. This results in total Brand sales rising by only +0.6% and a negative Brand LFL of -1.9%.

In line with FY14 at this stage we assume flat gross margins in both divisions in FY15 and that the EBIT margin will fall by 130bps and 50bps in Retail and Directory respectively. With the share option and interest charge remaining unchanged yoy we forecast FY15E PBT of £521m, a yoy decline of -3.8%.

29

Europe Equity Research24 April 2012

Gillian Hilditch, CFA(44-20) [email protected]

Table 7: Summary P&L

Source: Company Data, JPMC ests

Table 8: Summary Cashflow

Summary Cash Flow (£m) 2009 2010 2011 2012E 2013E 2014E 2015E

Gross cash flow (post tax & interest) 439.9 491.5 507.9 576.2 556.3 541.7 526.2Change in working capital -39.8 46.8 -76.6 -69.2 -56.1 -13.7 -13.8Operating cash flow 400.1 538.3 431.3 507 500.1 528 512.3Cashflow from investing -134.4 -96.2 -138.1 -70.2 -115 -115 -115Dividends paid -106.5 -108.5 -129.6 -135.1 -140.8 -146.8 -153Cashflow from financing -51.3 -107.3 -290.3 -330.2 -240 -240 -240Change in cash 107.9 226.3 -126.7 -28.5 4.3 26.2 4.3Opening Net Cash -740.5 -628.6 -400.1 -530.4 -574.7 -570.4 -544.3Other 4 2.1 -3.6 -15.8 0 0 0Closing Net cash/(debt) -628.6 -400.1 -530.4 -574.7 -570.4 -544.3 -540

Source: Company Data, JPMC ests

Y/E January 2009 2010 2011 2012 2013E 2014E 2015E

£m

Retail Sales 2197.2 2274.2 2222.1 2191.4 2158.5 2120.9 2078.3

Retail LFL -7.1% 0.3% -4.0% -5.7% -5.5% -6.0% -6.0%

Retail Space 4.5% 3.2% 3.0% 4.3% 4.0% 4.3% 4.0%

Retail Growth -2.6% 3.5% -1.0% -1.4% -1.5% -1.7% -2.0%

Retail EBIT 288.6 324.0 328.8 323.7 297.2 268.1 236.2

EBIT Margin 13.1% 14.2% 14.8% 14.8% 13.8% 12.6% 11.4%

Directory Sales 816.4 873.2 935.5 1088.7 1186.7 1246.0 1308.3

Directory Sales Growth 2.1% 7.0% 7.1% 16.4% 9.0% 5.0% 5.0%