New Opportunities for Operators in the Blended Reality Era

21

New Opportunities for Operators in the Blended Reality Era Sheridan Nye, Senior Analyst Lawrence Lundy, Consultant ICT 9 September 2014 © 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

-

Upload

frost-sullivan -

Category

Technology

-

view

598 -

download

3

Transcript of New Opportunities for Operators in the Blended Reality Era

New Opportunities for Operators in the Blended Reality Era

Sheridan Nye, Senior Analyst

Lawrence Lundy, Consultant

ICT

9 September 2014

© 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

2

Today’s Presenter

• Regularly provide guest analysis for Bloomberg, BBC, and CNBC focusing on

mobile, social and web.

• Extensive research and consulting experience across a broad range of industries

including: ICT, healthcare, financial services, telecoms & media, and public & third

sector.

• Core interest in convergence opportunities, disruptive innovation and business

model evolution

@lawrencelundy

Lawrence Lundy, ICT Consultant

Frost & Sullivan

@uk.linkedin.com/in/lawrencelundy

3

Today’s Presenter

• Over a decade of research and analysis expertise in the ICT industry.

• Specialising in Connected Industries markets and mobile operator

strategy in Europe.

• Interests in ICT as a catalyst for socio-economic change.

Sheridan Nye, Senior Analyst

Frost & Sullivan

Follow me on:

@sheridannye

@uk.linkedin.com/pub/sheridan-nye

4

Focus Points

Key questions addressed in this webinar

What disruptive technologies are challenging border between digital & physical worlds?

How can MNOs prepare for the resulting Blended Reality era?

How can the mobile operator remain relevant in the next decade?

5

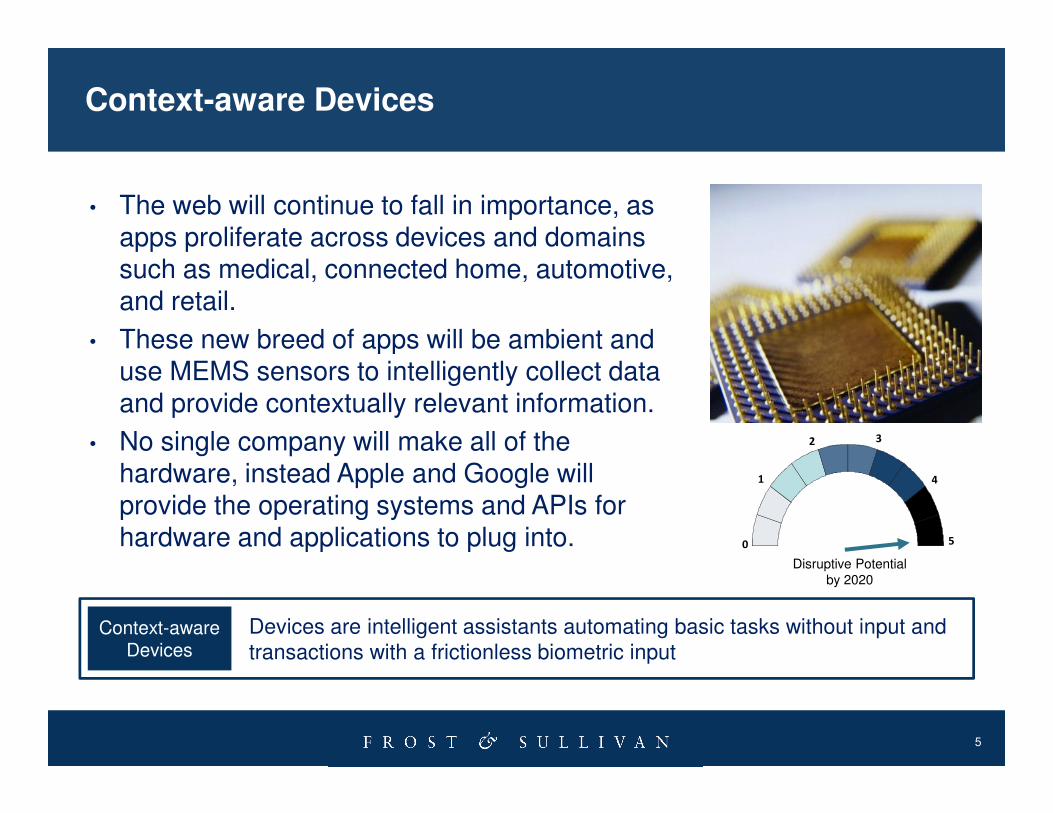

Context-aware Devices

• The web will continue to fall in importance, as apps proliferate across devices and domains such as medical, connected home, automotive, and retail.

• These new breed of apps will be ambient and use MEMS sensors to intelligently collect data and provide contextually relevant information.

• No single company will make all of the hardware, instead Apple and Google will provide the operating systems and APIs for hardware and applications to plug into.

Context-aware Devices

Devices are intelligent assistants automating basic tasks without input and

transactions with a frictionless biometric input

0

1

2 3

4

5

Disruptive Potential

by 2020

6

Health Monitoring

2020

Every person with a smartphone will have a personal health record that is

shared with their healthcare professional and with trusted aggregators to

enable predictive healthcare

• The smartphone will fundamentally disrupt the healthcare industry as it exists in 2014; moving from a reactive infrastructure to a 4P solution -predictive, preventative, personalized and participatory.

• Sensors in smartphones and smartwear will reduce inefficiencies in the system and enable preventative care, reducing the demand on hospitals and elderly care.

• Low cost devices enables healthcare to be delivered cheaply in populations improving medical care and diagnosis.

0

1

2 3

4

5

Disruptive Potential

by 2020

7

Biometric Transactions

2020Biometrics will be pervasive and provide ambient computing for

authentication and data sharing

• Biometric authorization will take place on the smartphone and will include fingerprint and iris or voice, limiting the need to include biometrics on other hardware.

• A wearable device without a display with biometrics will also serve as frictionless authentication for transactions. E.g. wristband, ring

• Primary use cases will be identification to enable transactions/automatic processes -smart home applications such as locks, room profiles, driver profiles

0

1

2 3

4

5

Disruptive Potential

by 2020

8

Display Advancements

2020Graphene-based rollable screens are dominant in high-end smartphones,

and tablets with pico projectors replace TV usage.

• A variety of displays will be available and act as a differentiator for ODMs, some will offer pico projectors, others 3D screens, and others bendable screens.

• Rollable screens will be the breakthrough technology that will expand the screen real estate on a smartphone and make tablets less appealing.

• Graphene offers the potential for unbreakable, transparent and extremely thin devices, this is likely to be utilised in smartwear especially smart wristbands.

0

1

2 3

4

5

Disruptive Potential

by 2020

9

Eyewear

2020

Augmented reality displays will not be widely adopted in the consumer

space but will be standard across retail, healthcare, military, and education

verticals.

• Eyewear will offer a secondary and more immediate display than the smartphone, augmented reality applications will proliferate.

• Head-mounted displays will not achieve market penetration in the consumer space, but will become standard in specific industries such as emergency services, healthcare, and education.

• Virtual reality will be the next gaming/entertainment platform. VR headsets will also make there way into the enterprise for training, teleconferencing and as virtual collaboration spaces.

0

1

2 3

4

5

Disruptive Potential

by 2020

10

Profits will be generated by services based on data

• Businesses will need to collect data to

improve their own services AND share data to enable meta-level insight

• Winner-takes-all dynamics based on

machine learning and network effects

• Access model over ownership model &

decentralization/peer-to-peer trends

• Housing - Airbnb

• Transport & Logistics - Uber

• Entertainment – Netflix, Spotify

• Finance - Coinbase, TransferWise

• Education – Coursera, Udacity

• Healthcare – Turntable Health,

Predilytics

1

2

3

Business Models in 2020

Competitive advantage is trust

Businesses battle to build data-driven platforms offering VAS

A personal data market will exist enabling people to sell their data

11

Focus Points

Key questions addressed in this webinar

What disruptive technologies are challenging borders between digital & physical worlds?

How can MNOs prepare for the resulting Blended Reality era?

How can the mobile operator remain relevant in the next decade?

12

The Blended Reality Era: Quantified & Automated

2020Disruption always means reallocation of market power. By 2020, 75%of S&P 500 might be unknown to us today. 1

• Dematerialization of products & services has been underway for at least two decades.

• Next comes smarter, smaller & more flexible devices & displays. Also task-oriented, invisible & disposable devices.

• Affordability extends dematerialization to new contexts. Changes how people interact with each other and with markets.

• High level of public awareness due to this dematerialization of experience & identity

Average lifespan of S&P

500 company only 15yrs1.

1Richard Foster, Yale, 2012

13

Have We Been Here Before?

2020-25Challenge: to anticipate when conditions will be right for technological potential to go mainstream.

The 2001-3 dot.com crash

• Unsustainable investments in supporting infrastructure

• Build it and they will come!

• Regulatory ‘shocks’

• Dodgy accounting

• Expectations too high (and too fast!)

• Result was over-capacity, swiftly followed by drastic market correction.

Guardian, August 2014

14

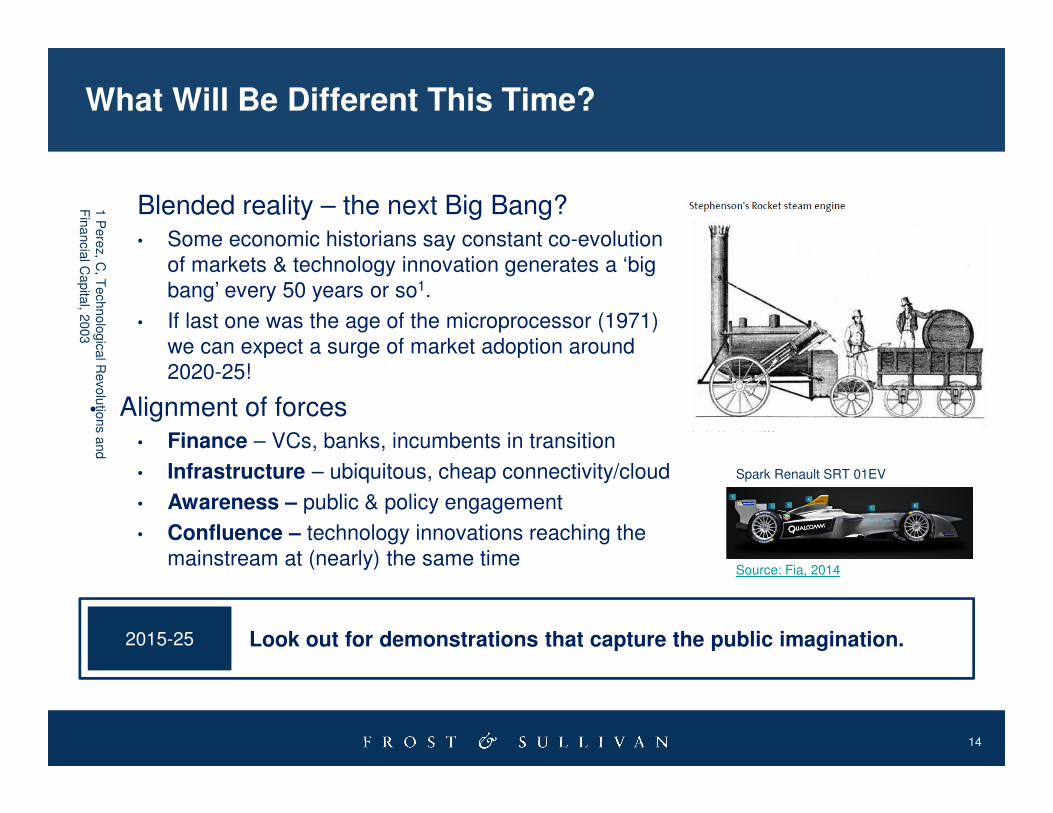

What Will Be Different This Time?

2015-25 Look out for demonstrations that capture the public imagination.

Blended reality – the next Big Bang?• Some economic historians say constant co-evolution

of markets & technology innovation generates a ‘big

bang’ every 50 years or so1.

• If last one was the age of the microprocessor (1971)

we can expect a surge of market adoption around

2020-25!

• Alignment of forces• Finance – VCs, banks, incumbents in transition

• Infrastructure – ubiquitous, cheap connectivity/cloud

• Awareness – public & policy engagement

• Confluence – technology innovations reaching the

mainstream at (nearly) the same time

Spark Renault SRT 01EV

Source: Fia, 2014

1 P

ere

z, C

, Technolo

gic

al R

evolu

tions a

nd

Fin

ancia

l Capita

l, 2003

15

Operators are moving in multiple directions

2015-20Seeking sources of innovation, building up defenses through scale and fighting to remove barriers such as unfavourable regulation.

Product differentiation

Market entry to drive demand

Incremental improvement

Customer segmentation

Deeper engagement• SMEs• Automotive• Public safety• Retail

• Lower cost• Higher quality• Customization• Pricing & multi-play

bundling

• Home, Work, Transportation, Lifestyles of the Future

• NaaS innovation platform• Telecom Big Data

New use cases• Network resilience

through diversity • LTE air-to-ground• M-banking alliances• Managed security

16

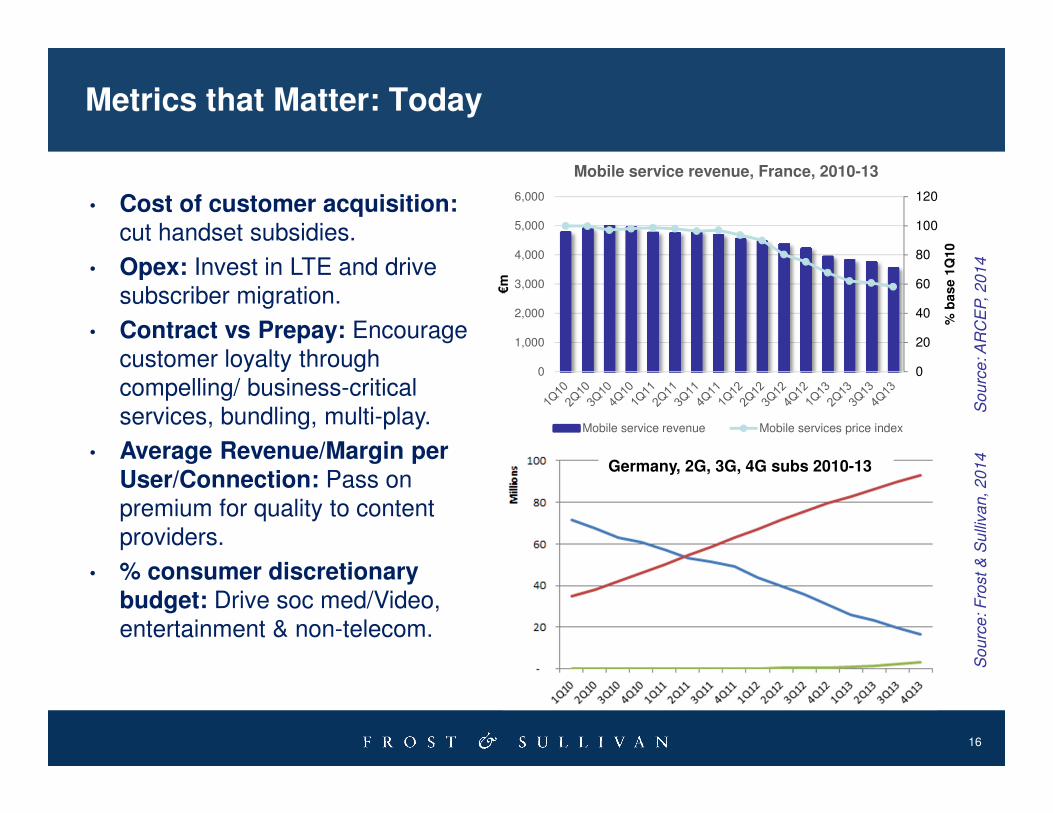

Metrics that Matter: Today

• Cost of customer acquisition:cut handset subsidies.

• Opex: Invest in LTE and drive

subscriber migration.

• Contract vs Prepay: Encourage customer loyalty through

compelling/ business-critical

services, bundling, multi-play.

• Average Revenue/Margin per User/Connection: Pass on

premium for quality to content providers.

• % consumer discretionary budget: Drive soc med/Video, entertainment & non-telecom.

0

20

40

60

80

100

120

0

1,000

2,000

3,000

4,000

5,000

6,000

% b

ase 1

Q10

€m

Mobile service revenue, France, 2010-13

Mobile service revenue Mobile services price index

So

urc

e: A

RC

EP, 2

01

4

Germany, 2G, 3G, 4G subs 2010-13

So

urc

e: F

rost

& S

ulli

va

n, 2

01

4

17

Metrics that Matter: 2020

2020-25Traditional ‘gateways’ like access networks will be less effective.

Sustainable competitive advantage relies on opening up.

Today’s assets won’t be tomorrow’s

• Spectrum – reuse, sharing, dynamic

• Brand – lost to OTT/digital natives

• Customers – profiles not relationships

• Market power – new market giants focus of regulator attention

• Metrics• Reach & number of partners

• Extent of network virtualization

• Diversity of access network infrastructure

• Resources –scale, scope, and agile corporate culture

Blended reality blurs the

borders of the

organization

18

Next Steps

Develop Your Visionary and Innovative SkillsGrowth Partnership Service Share your growth thought leadership and ideas or

join our GIL Global Community

Join our GIL Community NewsletterKeep abreast of innovative growth opportunities

19

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

What would you like to see from Frost & Sullivan?

20

https://twitter.com/FS_ITVision

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter (ICT)

http://www.facebook.com/FrostandSullivan

https://www.linkedin.com/groups/Future-Growth-Opportunities-in-ICT-4876870

http://www.slideshare.net/FrostandSullivan

21

For Additional Information

Edyta Grabowska

Corporate Communications

ICT

+48 (0) 22 48 16 203

Sheridan Nye

Senior Analyst

ICT

+44 (0)207 343 8350

Lawrence Lundy

Consultant

ICT

+44 (0)207 343 8322

Adrian Drozd

Research Director

ICT

+44 (0) 1865 398 699