new horizons: creating value, enabling livelihoods€¦ · Sustainable Development forum project...

56

new horizons: creating value, enabling livelihoods final report opportunities in microfinance for the UK financial services sector

Transcript of new horizons: creating value, enabling livelihoods€¦ · Sustainable Development forum project...

new horizons:creating value,enabling livelihoods

final report

opportunities in microfinance

for the UK financial services sector

11883 FFF microfinance report_v2 12/6/07 10:59 Page 1

2

acknowledgements

Forum for the Future would like to thank all the individuals who contributed to this project through providinginterviews or participating in the workshop in October 2006.

This project has been supported by:

The Defra support came through funding from the Implementation Fund of the World Summit on Sustainable Development

forum project team

Alice Chapple [email protected]

Vedant Walia [email protected]

Sven Remer Research intern

list of abbreviations

AECI-ICO – Spanish development finance

ATM – Automatic Teller Machine

BOMFS – Blue Orchard Microfinance Securities

BOLD – Blue Orchard Loans for Development

CGAP – Consultative Group to Assist the Poor (microfinance resource centre hosted at the World Bank)

CDO – Collateralised Debt Obligation

DFID – Department for International Development

EBRD – European Bank for Reconstruction and Development

FMO – Netherlands Development Finance Company

IFC – International Finance Corporation

KfW – German development finance (part of KfW Bankengruppe)

LIBOR – London Inter-bank Borrowing Rate

OPIC – Overseas Private Investment Corporation

MFI – Microfinance Institution

MIV – Microfinance Investment Vehicle

NGO – Non-Governmental Organisation

SRI – Socially Responsible Investment

June 2007

All dollar figures ($) used in this report refer to United States Dollars.

11883 FFF microfinance report_v2 12/6/07 10:59 Page 2

executive summary

The majority of poor people across the world have no access to formal financial services such as credit, savings, insurance and payment products that help to grow incomes, accumulate wealth and manage risk. Microfinance has emerged as a successful bottom up intervention that has demonstrated that the poor can be served viably. Despite increasing global attention – including the 2006 Nobel peace prize to Mohamed Yunus and Grameen Bank of Bangladesh – the microfinance sector is highly fragmented and lacks the necessary capacity and capital to meet the massive latent demand for financial services. At best, the industry is currently only meeting about 10-20 percent of a total potential demand of US$ 300 billion. This is mainly demand for credit; provision of other products such as insurance and remittances is even lower.

Commercial involvement in microfinance is increasing. Financial institutions have tended to enter this space in the past because of a desire to engage the local community, to build their brand, to deflect criticism or simply as part of their charitable activities. In some cases, this has evolved into a recognition that microfinance can be profitable and can open up a massive new untapped market segment, and created fertile conditions for innovation and experimentation. From large international banking groups through to boutique microfinance investment management houses, commercial players are looking at ways to provide capital and deliver financial services through employing new techniques, technologies and business models.

This wave of innovation is emerging rapidly and starting to fundamentally alter microfinance by bringing it into contact with the financial, technical and managerial resources of the wider financial sector. However, this is still at an early stage and the opportunity – and necessity – for further innovation by mainstream financial institutions, including those based in the UK, is immense. For those examining microfinance through a commercial lens, this report sets out innovations that are transforming the industry landscape in three main areas.

In capital markets and investment, a number of new vehicles have emerged to channel private and public capital to microfinance institutions. They are growing fast, with about a US$ 2 billion portfolio in 2006, but have several challenges to overcome in order to become viable commercial investment propositions. Most tend to focus on short-term foreign currency debt to a narrow set of elite microfinance institutions. There are no standard performance metrics, transparency is poor and most do not offer market rate returns, forcing them to rely on donors and social investors. To expand the investor base and create new funding solutions, increasingly sophisticated mainstream financial techniques are being adopted in microfinance.

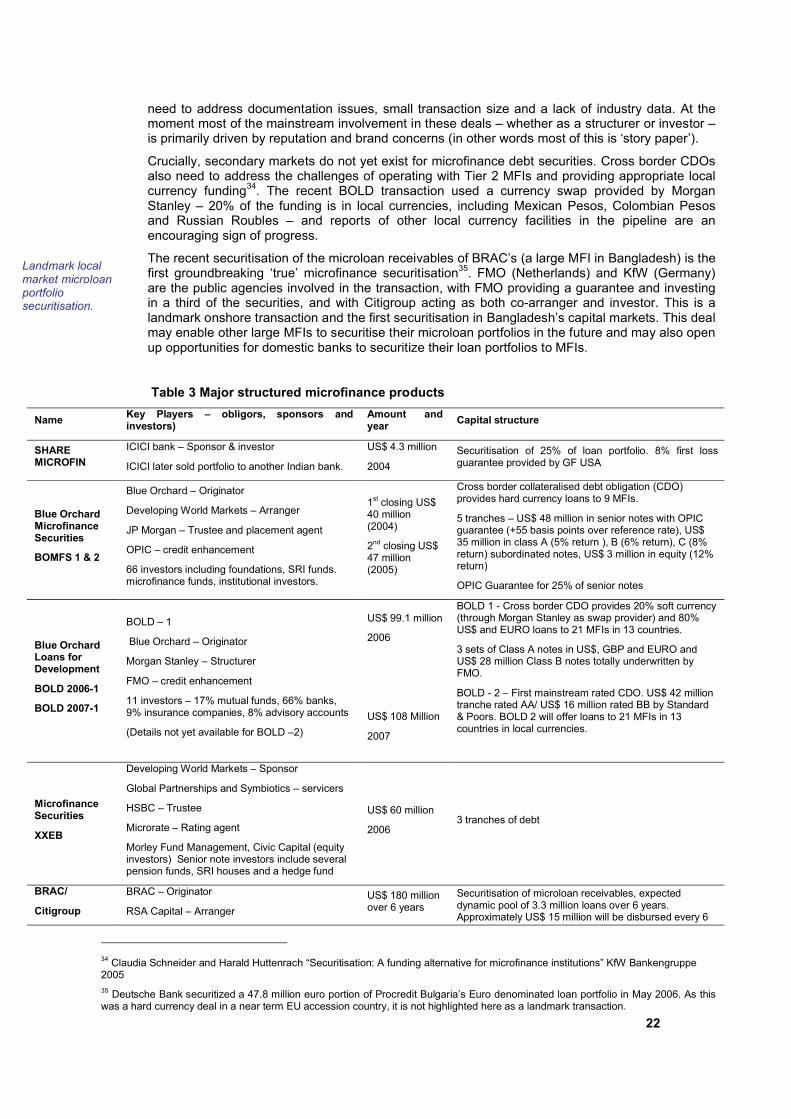

Groundbreaking transactions have introduced new capital structures that enable a wider range of international commercial investors to invest in senior layers of debt, while social investors and development agencies purchase the more risky junior layers. Over US$ 500 million of structured microfinance paper has been issued since 2004. Analysts expect a similar amount to be issued by the end of 2007, driven by larger deal sizes, the involvement of major institutions such as Morgan Stanley to structure and place the securities, helped by moves from rating agencies such as Standard and Poor’s to develop rating methodologies. Structured finance instruments such as collateralised debt obligations are a growing part of the capital mix but need to address concerns about liquidity, lack of a performance record, poor data availability and the need to offer local currency funding.

Equity investment in microfinance institutions only makes up about 17 percent of a total broadly defined US$ 30 billion microfinance portfolio (including state financed schemes through agricultural banks). High risk, a lack of exit opportunities and little publicly listed equity make investment difficult but the landscape is changing rapidly. In April 2007 alone, Compartamos floated a third of its equity in Mexico in a US$ 407 million issue, 85 per cent of which was successfully placed in the international equity market by Credit Suisse, and Sequoia Capital, a prominent American venture capital firm, invested US$ 6.5 million in a for-profit Indian microfinance start-up.

Institutions are also exploring new ways of developing and delivering financial services. Most commercial players cannot directly serve low-income clients due to inappropriate products and business models for low-margin, high volume microfinance markets.

Microfinance institutions tend to focus on credit – often using the Grameen model of group lending – and lack the capacity to offer an optimal suite of financial products designed for low-income

2

clients. Commercial players, in collaboration with microfinance institutions, are exploring opportunities to develop a wider range – particularly critical products such as life and general insurance, remittances and dedicated agricultural finance and risk management.

Delivery channels that can bring appropriate products to target client groups cost-effectively are being developed to expand product range and availability. Banks and insurers are partnering with microfinance institutions to develop products which are then distributed through the institution’s field network or using the institution to originate and service loans or insurance policies. Innovative business models built on agent banking – through a network of community level microentrepreneurs – are being enabled through technologies such as smartcards and networked point-of-sale devices. New transformative technological innovations around technology enabled banking and payment services are pushing the boundaries and could radically lower transaction costs and increase efficiency. Low cost mobile banking is already being offered in many parts of Africa and pilot projects to revolutionise the remittances market through using a mobile-enabled platform could have significant pro-poor benefits.

Microfinance institutions are key intermediaries but require significant technical assistance to professionalise, scale operations and be able to absorb commercial debt and equity capital. This needs to happen both at an institutional level – transferring best practice in governance, operations, liquidity management and credit methodologies to name a few – as well as a systemic level, where rating methodologies, performance standards and supporting regulatory environments are critical.

Concerns about the commercialisation of the industry undermining its traditional focus on helping the poor should not be ignored. There is still a very important role for philanthropic funds to reach the poorest segments and provide added social services. The future could include a much more hybrid industry with a varied capital mix and the best use of resources – allocating commercial capital to the most profitable and robust areas and reserving donor funds for more difficult operating environments and for leveraging private funding.

The UK financial sector can play an important catalytic role in microfinance. Banking and insurance groups with a global footprint can be active through local subsidiaries – provide funding, product development and technical assistance – and leverage their global presence and expertise to transfer learning and successful models. Institutions with a global footprint such as HSBC, Standard Chartered and Barclays are increasingly offering wholesale services to microfinance institutions though local subsidiaries. London’s capital markets’ depth, expertise and access to investors can be harnessed to increase the flow of commercial capital to microfinance. Some capital market transactions have been arranged and placed in London with mainstream players such as Morley Fund Management and Standard Life investing. However, with industry-wide collaboration backed by public and non-profit agencies, there is a considerable amount more that can be done within a formalised and integrated strategy.

Some may be concerned about accusations of profiting from the poor. This is a misrepresentation provided that institutions take a long-term view and invest in developing the capacity to meet unmet needs for financial services in a way that adds value for both the client and the provider. On the basis of this analysis, it seems some commercial organisations are starting to do just that but it remains to be seen whether this can be transferred across the industry as a whole.

Microfinance and the mainstream finance sector have just started to engage. Systematic integration of microfinance as a mature financial sub-sector is just one of many future scenarios. The industry will need to work with both public and private stakeholders to build on its considerable success by creating strong foundations for future growth. At the same time, microfinance cannot deliver a magic solution. Efforts to improve socio-economic conditions for the world’s poor have to tackle a large and formidable range of issues. However, for the individual microentrepreneur or household, and within the growing agendas of base of the pyramid markets and enterprise solutions to poverty, microfinance plays a critical role. The UK financial sector can help propel the sector to maturity.

3

introduction

Access to financial services is very difficult for low-income groups in the developing world. Microfinance has proven to be a successful model for viably providing credit and other financial services to the poor. This report presents the findings of a project to examine opportunities for the UK financial services sector to contribute to expanding access to finance. The project was undertaken by Forum for the Future with support from the City of London Corporation, Gresham College and Defra, as part of a follow on process to the London Principles project1.

Objectives

This report explores the potential and need for commercial involvement in microfinance and provides examples of commercially oriented innovations in products, processes or market mechanisms by which mainstream financial institutions have increased access to financial services to the poor. After assessing the case for commercial involvement, it examines three areas in more detail:

The current and potential role of commercial investment and capital markets

Initiatives to develop new products, technologies and business models

The need for technical assistance to develop and integrate the microfinance sector

This project focuses on access to finance for low-income groups that are not served by formal financial services – individuals, microentrepreneurs or group borrowers. It does not address wider questions regarding the macroeconomic barriers to investment in developing countries, or broader development finance issues.

1 The London Principles promote banking, insurance and investment for sustainable development and were launched at the Johannesburg Earth Summit in 2002. A progress review in 2005 identified progress on enabling access to finance and risk management products for the poor in developing countries as a key area of future action. Phase II of the London Principles has two workstreams on access to finance for developing countries (this project) and access to finance for environmental technologies. See www.forumforthefuture.org.uk for more information.

4

1 global financial exclusion and microfinance

Globally, about 2.5 billion people do not have access to basic financial

services. As a broad generalisation, the percentage of the population with

access to financial services in poorer developing economies is about the

same as the percentage excluded from financial services in richer

industrialised countries. Financial exclusion is not just a simple measure of

access to bank accounts. The access frontier approach developed by

Finmark in South Africa uses a ladder of different levels of access – those

who have access to banking but do not use it, those who are users of other

formal non-bank services, those who use informal services only and those

who use no financial services at all1.

Figure 1. Global map of financial inclusion

High 7.5 - 10 Upper 5 -7.5 Medium 2.5 -5 Low 0 - 2.5 No data

Source: Maplecroft 2007

This map is based on World Bank data used to develop a Financial Inclusion Index with eight separate components. Countries are scored on an index of 1 to 10, with 10 being high access to financial services and 1 being little or no access. Data coverage is patchy and not all countries were analysed on the full set of metrics. See ‘Global Map of financial inclusion’ at http://maps.maplecroft.com/ for more information.

5

‘Unbanked’ people are forced to rely on a narrow range of expensive and risky informal services. This constrains their ability to participate in economic exchanges, increase their incomes and contribute to economic growth. Improving access to financial services for underserved groups in the developing world can have strong development impacts, particularly at an individual or community level. It empowers the poor to establish livelihoods, improve (and smoothen) incomes, build assets and act as a buffer against high exposure to economic shocks. Informal activities to manage risk – selling assets, reducing consumption, and taking on expensive informal loans – are inefficient, not cost-effective and often have damaging effects on livelihoods and quality of life.

The formal financial sector was not interested in a low-income market perceived as miniscule, highly risky and with very poor returns. Around three decades ago, the ‘microfinance’ model emerged as a bottom up intervention to provide finance for the poor. Grameen Bank in Bangladesh pioneered the idea that the impoverished have skills that are underutilized, are surprisingly low credit risks, and can be served profitably.

1.1 the microfinance model

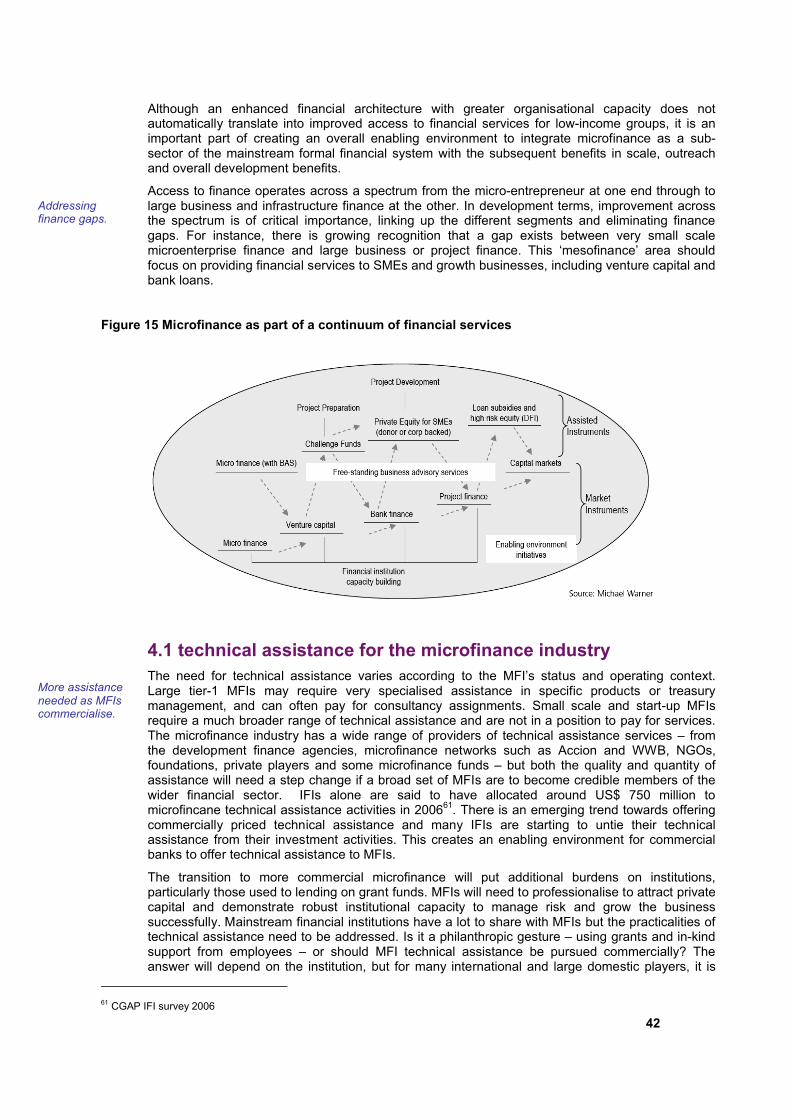

Microfinance broadly refers to the provision of credit and other financial services to low-income clients, usually in small increments with affordable service charges. Microcredit – the provision of small loans usually under $100-200 without formal collateral – is the most well known form of microfinance product but it also extends to savings, insurance, payment transfer and remittance services. Microfinance products are provided by a variety of financial intermediaries. Microfinance Institutions (MFIs) may vary in terms of size, legal structure and vision, and exist in many forms –such as credit unions, non-bank financial institutions, co-operative banks and, often, NGOs. Some other financial actors such as state-owned postal, development and agricultural banks are also active in microfinance. Some of the key differences between microfinance and mainstream finance models are outlined in the table below.

Table 1 Main differences between mainstream finance and microfinance

Product range Lending model Organisational status

Mainstream finance

Comprehensive product portfolio but based on higher value transactions.

Competitive transaction costs and interest rates.

Mostly built on collateral based lending. Use of sophisticated credit scoring systems.

Individual and enterprise lending.

Formal regulated institutions, with a wide variety of local, national and international entities.

Use strong management information, technology and risk management systems.

Microfinance

Limited products concentrated on credit but increasingly offering other services. Uses low value, high volume model.

Very high costs due to transaction-intensive business model.

No need for collateral. Group lending dominates, but increasingly lending to individual and enterprise clients.

MFIs use group lending to utilise social collateral. Short loan cycle (6-12 months) with weekly payments.

Diverse range from small NGOs restricted to lending services through to formal bank status.

Most use little or no technology, have rudimentary information systems and lack financial sophistication.

Many MFIs depend on leveraging social collateral, usually through lending to organised groups, mainly consisting of women who are seen as more productive users of the loans and better credit risks. MFIs charge interest rates that might sound high in a mainstream context— the average global rate is about 35-40 % annually — to cover the high administration costs incurred through originating and servicing small loans, often in rural areas with weekly payment collection. In this context though, it is important to note that although MFIs may charge rates of 30 to 70% to cover their costs, these interest rates are still significantly lower than the 300% to 3,000% annual rates that many borrowers were previously paying to informal money lenders.

Impact analysis studies are frustrated by the difficulty of identifying causality. Numerous studies have documented improvements at individual, household and enterprise levels as microloans have not only enabled productive entrepreneurial activity but also offered new ‘consumption’ opportunities for education, nutrition or healthcare. But an exhaustive survey of existing impact assessments found that positive impacts could only be attributed to specific contexts shaped by the

Improving access to finance can have powerful economic and social benefits.

Grameen Bank pioneered microloans in the 1970/80s.

Unsecured microcredit dominates but other financial products are emerging.

High costs due to transaction intensive model leads to high interest rates.

.

Proven impact at community level but difficult to extrapolate.

.

6

type of services offered, client profiles and regional environment2. Microfinance works in specific cases but more research is underway to create a robust and credible evidence base that is valid on a broader scale.

Microfinance is not a magic solution to poverty, nor is it an automatic enabler of higher living standards. As a successful and scaleable bottom up solution it offers an alternative to the top down aid models of the past but does not tackle the important structural and macroeconomic drivers behind development such as infrastructure, legal systems, trade policy, governance and investment climate amongst others. Critics point to the simple fact that Bangladesh is the most successful microfinance country – both in symbolic terms as well as actual penetration with a US$ 995 million portfolio on loan to 9.2% of the total population – yet still ranks 137 out of 177 countries on human development indicators3. Other criticisms refer to microloans fuelling only immediate consumption but not improving productive economic activity and the risk of over-indebtedness exacerbated by high interest rates.

Ultimately, initiatives designed to develop and deepen financial sectors in developing countries will enhance the overall climate for delivering financial services to the poor. Successful microfinance depends on an enabling environment, some of which is industry-specific – such as interest rate caps, financial regulation or foreign investment rules – but also relies on general rule of law, functioning societies with microentrepreneurial opportunities and a range of other social and economic factors.

microfinance has been growing rapidly

Microfinance has been building momentum over the last 20 years that has accelerated in recent years – given a high profile boost by the 2005 UN Year of Microcredit and the Award of the 2006 Nobel Peace prize to Grameen founder Mohammed Yunus – and is now taking the first steps towards becoming a mature financial sub-sector. It is growing rapidly and now has thousands of MFIs, millions of borrowers, billions of dollars in loan portfolios, and numerous donors and investors. The exact scale of the industry is difficult to estimate reliably given conflicting data sources that use different methodologies and definitions and the disparity of the sector with weak information systems.

Figure 1 The microfinance industry is expanding rapidly

26.9

41.654.8

66.6

19.3

7.6 12.213.8

3164

1567

2186

2572

2931

1065925

618

0

10

20

30

40

50

60

70

80

90

100

1997 1998 1999 2000 2001 2002 2003 2004

Nu

mb

er o

f cl

ien

ts m

illio

n

0

500

1000

1500

2000

2500

3000

3500

Nu

mb

er o

f M

FIs

Poorest clients Total Number of MFIs

Despite increasing commercialisation and the successful use of commercial funds from banks and investors by some MFIs, the sector is still heavily reliant on public and private donors to provide grants and subsidised loans. CGAP has a broad estimate of the total global microloan portfolios

2 Nathaneal Goldberg “Measuring the Impact of Microfinance: Taking stock of what we know” Grameen Foundation USA 20053 UNDP Human Development Report 2006

Scaleable bottom up intervention but not a magic solution to poverty.

.

Grameen Nobel Prize raises profile.

. .

.

Substantial growth in scale but difficult to estimate size accurately.

.

Source: Microcredit Summit Campaign Report 2005. Note these figures are inflated by the addition of 2 very large Indian traditional women’s savings and credit groups that account for 31 million borrowers and also includes 16 million from government run programmes. Source: Accion 2006

7

outstanding at about US$ 15 billion4. This is a very rough estimate that includes the loans made by state owned banks, agricultural and postal banks. Another estimate puts the amount of microfinance assets at about US$ 11 billion in 2005, forecast to grow to US$ 20 billion by 20085.

an elite band of MFIs dominate a fragmented sector

The size and reach of MFIs varies widely. On the one hand, there are the ‘top-tier’ or ‘tier-1’ MFIs, that have significant scale, established track records, highly professional operations, healthy finances and, often, many of the characteristics of commercial banks. Over the past 10 to 15 years, a number of leading MFIs have developed an excellent track-record as financial entities which compares favourably with mainstream financial institutions. This exclusive MFI club – which consists of around 75 to 100 organisations – contains the most commercial performers of the industry which share similar characteristics such as high growth rates, a solid product portfolio, strong profitability (return on equity in the 20s is common), low portfolio at risk (average default rates of 3%), strong Management Information Systems, excellent diversification and access to commercial funding sources. As some studies report, many top MFIs outperform local bank peers in terms of return on equity6. However, increasing professionalisation also introduces the potential for ‘mission drift’ as larger MFIs may be tempted to go upmarket and reduce their focus on poorer clients. Established networks of MFIs spread best practices and offer technical assistance, increased visibility, and public validation for established and emerging MFIs alike.7

A study found explosive organic growth in tier-1 commercial MFIs across all regions. Based on a sample of 71 MFIs between 2004 and 2006, total assets grew by 191% to US$ 6.7 billion, total equity by 122% to US$ 791 million, loan portfolios by 231% to US$ 4.8 billion and number of borrowers by 73% to 4 million8. Projecting the trends and organic growth rate forward results in strong asset and portfolio growth to about US$ 36 billion in loans to 23 million borrowers by 20119. However, this is a mechanistic projection that does not take account of several variables and assumes growth rates can continue at the same pace. The underlying assumptions of the scenarios include expansion of the number of elite MFIs, greater involvement of commercial capital, rapidly increased efficiency and much higher leverage. This also requires US$ 2.4 billion worth of external equity investment by 2011.

On the other hand, the remaining 98% of all MFIs below tier-1 vary dramatically from one another, in terms of business models, scale and financial health. Most MFIs face significant challenges, particularly 10:

o A lack of internal capacity: Most MFIs have rudimentary business processes, poor managerial capacity and a lack of technology systems. Their growth often stops once a programme reaches several thousand clients. Adequate internal operating capacity includes improvements in areas such as information technology infrastructure, internal controls, new product development, and human resources, all of which are costly to acquire.

o A capital gap: Many MFIs have limited options to mobilise capital. Most rely on a limited pool of donor and grant funds, and the majority are restricted from taking deposits and recycling them into loans as is common in the formal banking sector. They must either sell some of the debt on their balance sheets or otherwise secure substantial new funds in order to expand their lending activity. When MFIs only rely on philanthropic or subsidised funding, there is rarely enough money to make the necessary investments in key areas to create an operation that is well run and has the ability to grow on a sustainable basis.

4 “Foreign investment in microfinance: debt and equity from quasi-commercial investors” Consultative Group to Assist the Poor, Focus Note 25, January 20045 Source Celent 6 Jennifer Isern and David Porteous “Commercial banks and microfinance: evolving models of success” Consultative Group to Assist the Poor, Focus Note 28, June 20057 Examples of MF Networks are: Women’s World Banking, Opportunity International, Accion, FINCA, The Microfinance Network, Grameen8 Elisabeth Rhyne and Brian Busch “The Growth of Commercial Microfinance 2004-2006’ Council of Microfinance Equity Funds, September 2006 9 Ibid10 Source: Unitus

Tier1 MFIs are profitable but only represent 2% of the sector.

.

Spectacular growth in Tier-1 MFIs since 2004…

.

…if trends continue will grow 6x to meet 12% of demand by 2011

.

8

Figure 2 Small scale MFIs dominate the industry

1.2 meeting demand for financial services

The main providers of funding have been local domestic sources – government grants, domestic investors and mobilised savings – and foreign donors. However, domestic funding from government sources can be very limited in low-income states and most MFIs are legally unable to mobilise savings. Donors have more flexibility in providing grants and subsidised loans, but have a limited amount of capital available and have many competing areas for development investment such as education or healthcare.

The industry is still unable to scale to meet the latent demand for financial services amongst the world’s poor. Estimates suggest that 80% of the working poor (more than 400 million families) are still without access to microfinance services. At current growth rates, the gap will not be closed for decades11. Only 55 million of the poorest families out of 250 million have access to microcredit. With an expansion of the definition of the poor, only 80 million out of about 600 million families have access to credit. This indicates, at best, about a 10-20 percent market penetration. When considering loans, the industry is doing an even worse job at meeting demand. Total demand for micro-loans is estimated at US$ 300-500 billion while supply is only US$ 15 to 30 billion12.

Microfinance is growing rapidly from a very small base but the potential demand is forecast to stay on a continued upward trend because predicted global population increases to around 9 billion by 2050 will mostly be in lower income (and microfinance target) segments in the developing world.

11 Source; Unitus 12 Source: McKinsey, CGAP estimates

Source: Grameen Foundation 2004, Unitus 2006

Domestic funding sources dominate…

.

… but industry only meeting a fraction of total demand.

.

9

Figure 3 Microfinance is unable to meet potential demand

Expanding the tier-1 and 2 base by building institutional capacity and seeding many more new professionally driven commercial MFIs will be essential to enable the industry to scale and improve absorptive capacity for both debt and equity capital. Otherwise, the current trend of focusing on a handful of tier-1 institutions by both private and public investors could have dangerous consequences – and leave the large and unwieldy majority of small scale, inefficient and unprofitable MFIs to stagnate and decline. There is increasing evidence that the donor and philanthropic community is crowding out private sector investment by allocating soft funds to strong tier-1 MFIs that can access commercial sources of capital13. This soft funding should instead be directed to weaker and less commercially appealing organisations, be used to leverage private sector funding and be invested in public goods and an enabling infrastructure for the microfinance industry.

the solution? Moving from donor to market capital

Philanthropic sources, foundations and governmental organisations mainly provided the significant sums initially needed to launch and grow microfinance over the last three decades. They ‘pushed’ capital into the sector because of its ability to create sustainable microenterprises using a successful lending model, but with little regard for the risk as to whether the capital would be returned and often with limited understanding of whether it had been well deployed. These philanthropic investors played an important role as risk-tolerant angel investors who helped capitalize a new industry, and they need to continue to play a critical role in many circumstances, particularly for the vast majority of small-scale tier-2 and below MFIs.

The main public agencies active in international funding for microfinance are the development finance institutions – both multilaterals such as the International Finance Corporation (IFC) and those from individual countries such as Kfw (Germany) and OPIC (United States). These institutions held a combined microfinance portfolio of US$ 2.2 billion in 2006. Just five agencies accounted for 75% - KfW (Germany), AECI-ICO (Spain), IFC (multilateral), OPIC (United States) and EBRD (multilateral)14. DFID, the UK government agency, promotes microfinance within a broader inclusive financial sector strategy. It allocated approximately £86 million between 2003-06 on microfinance activities moving away from directly funding MFIs to providing support for financial

13 Julie Abrams and Damian Van Staffenberg “Role reversal: Are public development institutions crowding out private investment in microfinance?” Microrate MFI Insights, February 200714 Source: CGAP IFI survey 2006

Philanthropic and public funding nurtured microfinance.

.

$300 b

Foreign debt16%

Domestic debt19%

Domestic equity12%

Domestic guarantee

1%Deposits

45%

Foreign equity

5%

Foreign guarantee

2%

~$30 billion Current supply

Potential demand

Total investment – 100%= ~$30 billion

Domestic $26 b

Foreign $4 b

~$300 billion

Source: CGAP, McKinsey estimates. This refers to a very broad estimate of the total microloan portfolio including government run institutions.

10

infrastructure, capacity building and its flagship Financial Deepening Challenge Fund – a £15 million pool managed by a private agency that is currently funding 28 projects in collaboration with private sector players15. DFID has also leveraged private money by providing a first loss position in a transaction arranged by Deutsche Bank.

An increasing number of industry experts argue, for microfinance to unleash its full potential, to operate at scale, and to create the economic virtuous cycle of development that builds the capital of the poorest communities, philanthropic and soft funding alone will not be sufficient. An estimated capital requirement of US$ 270 billion – 45 billion equity and 225 billion debt assuming a 5:1 leverage – will not come from donor funds or philanthropists. Total Official Development Assistance (ODA) – using the broadest measure including emergency assistance, debt relief, bilateral and multilateral funds – was about US$ 100 billion in 200516.

Commercial capital is needed at much greater scales in microfinance. The main potential providers are banks – either through provision of financial services to low-income clients directly or through dedicated subsidiaries and service companies or indirectly through wholesale services or outsourcing arrangements with MFIs17 – and domestic and international investors. The positive trends in the microfinance industry have not gone unnoticed in the mainstream financial community. An increasing number of domestic banks are ‘downscaling’ to seek new growth markets and large international banks are looking at strategic opportunities, initially driven by corporate social responsibility (CSR) concerns or regulatory requirements but increasingly moving to a commercial basis.

The other main group of potential commercial players is mainstream and socially responsible investors – and other actors in the investment value chain such as investment banks, raters and fund managers – who can allocate significant volumes if microfinance becomes a viable asset class.

In the medium term, the main portion of the capital requirement is likely to be provided by domestic sources – including mobilised savings, commercial bank loans, retained MFI earnings and domestic debt and equity investors – but this is only currently starting to happen in a few isolated cases with strong MFIs and active local capital markets. Domestic funding, particularly in low-income nations, is unlikely to be able to scale fast enough to meet demand without the injection of catalytic capital from international investors – particularly those who have a greater risk appetite than mainstream domestic investors. Ultimately, microfinance must become a segment of the formal financial sector, using as broad a mix of capital sources as mainstream banks, including a central role for mobilised savings.

Commercial involvement from international institutions can act as a catalyst to professionalise and scale the microfinance industry while providing value for mainstream participants. For MFIs, access to a much larger pool of more flexible risk capital – often at lower interest rates than commercial loans from domestic banks – options to leverage domestic funding, potential equity investment, market discipline, formalisation, an expanded product portfolio and technical assistance are all potential benefits.

Advantages for international commercial financial institutions will vary according to business objectives and strategic intent. For large global banking and insurance groups seeking mid to long term growth opportunities in emerging markets, early involvement in microfinance will provide market intelligence and access to a potentially massive future customer base. Some national commercial banks are downscaling while immediate opportunities for providing wholesale services to MFIs are being seized by both national and international players. The elite MFIs also offer valuable channels for developing and distributing new products such as insurance or remittance services.

The investment community can also benefit from examining the emerging opportunities in microfinance. Although microfinance investment is still embryonic and dominated by public and social agencies, it is possible to visualise some commercial opportunities that may be attractive for select institutions. Investment banking and asset management skills are increasingly being used to

15 Source: Hansard 27 January 2007: Column 2088W. Also see www.financialdeepening.org for more information. 16 Source OECD http://www.oecd.org/dataoecd/52/18/37790990.pdf17 Jennifer Isern and David Porteous “Commercial banks and microfinance: evolving models of success” Consultative Group to Assist the Poor, Focus Note 28, June 2005

But commercial capital is needed to scale.

.

Domestic sources unlikely to be sufficient in short term.

.

International investors can play a catalytic role.

.

Microfinance as a long-term strategy for international banks.

.

11

create investment propositions to appeal to a broad range of investors – from foundations and high net worth individuals through to socially responsible and mainstream institutional investors. Benefits may lie in new product opportunities, options to respond to increasing client interest in investments that deliver both commercial and social returns and the possibility of establishing microfinance as an uncorrelated asset class to mainstream market trends.

Recent positive media and political support for microfinance is also driving many institutions to reap some reputation and brand advantage by publicly declaring an interest and involvement in providing financial services to the poor.

A range of commercial institutions around the world are taking the first steps in innovating to realise these potential advantages, often in partnership with other commercial stakeholders, development agencies and MFIs. This report showcases this innovation and explains the significant challenges that remain to be resolved before microfinance becomes a part of the formal financial system. Before proceeding to this, we highlight the added momentum that may be provided by the financial services sector in the UK.

1.3 the potential role of the UK financial services sectorThe UK financial services sector – in collaboration with a range of other public and private actors –can play an important role in propelling the microfinance sector to maturity, improve product coverage and establish microfinance as an asset class. This can create the foundations for truly inclusive international financial markets that provide both commercial and developmental returns.

The UK financial services sector is a global economic powerhouse accounting for about 5% ofGDP and providing £17 billion to the UK’s balance of payments18. This includes major UK based multinational financial institutions with a global footprint from the banking, insurance and investment management sectors such as Barclays, HSBC, RBS and Aviva. In addition, London is the world’s leading international financial centre with the presence of hundreds of financial institutions, deep capital markets and a range of ancillary service providers such as legal and accountancy firms. Although not all actors in the UK financial services sector can potentially have a role to play in extending access to financial services amongst the world’s poor – for instance purely domestic players or those without significant developing country exposure – there are significant opportunities for the UK to apply its expertise.

Several institutions are already involved in microfinance to some extent, starting from a reputation and CSR focus but increasingly underpinned by a longer-term commercial vision. Moving on from a philanthropic motivation that involved giving grants and providing some technical assistance to MFIs, some international banks are now starting to explore partnership options, provide wholesale services to MFIs (usually through local subsidiaries), develop pilot projects and create targeted financial products such as remittances and microinsurance.

Wholesale loans to MFIs are probably the most widespread form of commercial engagement in microfinance. Loans to MFIs by a set of international banks were estimated to amount to between US$ 450 to 550 million in 2006 – a US$ 100 million increase over 200519. Most of this is offered through local subsidiaries, particularly in India where regulatory stipulations mean that banks have to allocate some lending to microfinance and priority rural lending areas.

Institutions have taken different approaches in their microfinance strategy. Some are building on a CSR platform to develop a targeted commercial approach with several strands – such as developing customised funding options including local currency funding, guarantee schemes, raising dedicated funds and capital market transactions; exploring strategic MFI partnerships; taking equity stakes in MFIs and developing tailored products – while others remain driven by CSR commitments with some isolated commercial initiatives. Some regional and domestic banks are also emerging as strong contenders in microfinance, for instance Egypt’s Banc du Caire, as they have local market knowledge and presence. However, ICICI bank in India is remarkable for the sophistication and scale of its microfinance business. ICICI (profiled in a case study on page 40)

18 UKTI https://www.uktradeinvest.gov.uk/ukti/fileDownload/fin_services_invest_uk.pdf?cid=38874619 See ING ‘A Billion to Gain: update 2006’ – the sample set includes 11 banks: ABN Amro, Barclays, Citigroup, Commerzbank, Deutsche Bank, Grupo Santander, HSBC, ING Group, Rabobank, Societe Generale, Standard Chartered. Data is estimated and self reported by the banks.

Some potential advantages for asset managers and investors.

.

Innovation is accelerating.

.

Only some parts of the UK financial sector can potentially play a role.

.

Microfinance given initial traction by CSR, but business-led approaches emerging.

International bank microfinance strategies vary.

12

has innovated in several areas and is a valuable case study for international banks looking at integrated microfinance strategies.

Most banks provide some form of technical assistance to MFIs but this can vary from ad hoc volunteer programmes run by bank employees through to systemic support packages. Technical assistance is usually offered as a philanthropic activity with much more potential to expand –especially through partnerships with international financial institutions, trade associations, MFI networks and government agencies.

Figure 4 Mapping microfinance activity for some international banking groups

*Note refers to commercial business units, both Citigroup and Rabobank Foundations are also significant philanthropic actors in microfinance. Source: adapted from Figure 6 in ‘A billion to gain- update’, ING Microfinance Support 2006. HSBC, ICICI added separately.

Stated Commitment

Actual Involvement

CSR orientation

Commercial orientation

ABN Amro is building a strong microfinance business through its local subsidiaries in Brazil and India, focusing on wholesale loans and services to MFIs but also investing in microfinance venture funds and pursuing strategic partnerships.

Barclays has a small microbanking service in Ghana but a large retail presence in South Africa through its subsidiary ABSA, which has 4.3 million low-income clients.

Citigroup has a dedicated Microfinance Group which works across the global business to develop commercial relationships with MFIs, develop products, create financing facilities and facilitate capital market transactions, particularly in local markets. It is pursuing a partnership model with MFIs. (see extended case study)

Deutsche Bank manages a number of global microfinance funds that offer tailored funding options for MFIs including guarantees, long term local currency funding through co-lending, letters of credit and credit default swaps.

HSBC is piloting projects to provide wholesale services to MFIs, including loans, transaction and remittance services. It aims to embed microfinance within local subsidiaries.

ICICI Bank pioneered the partnership model in India and is aggressively pursuing a multi-pronged microfinance strategy that includes product development, use of new technologies and a comprehensive technical assessment and seed capital programme. ICICI has innovated in launching new products including life and crop insurance and is piloting a new internet enabled rural agent banking model. (see extended case study)

Standard Chartered offers wholesale loans to MFIs in Africa and Asia. The current portfolio is around US$ 50 million but it is establishing a US$ 500 million facility to disburse funds over five years in Africa and Asia. It also has equity stakes in a couple of Asian MFIs.

Source: ING ‘A billion to gain: Update’ 2006, ICICI, Citigroup

Citigroup*

ICICI Bank

Deutsche Bank

Rabobank*

ING ABN Amro Barclays

Standard Chartered

CommerzbankHSBC

Societe Generale

Citigroup Foundation

Rabobank Foundation

13

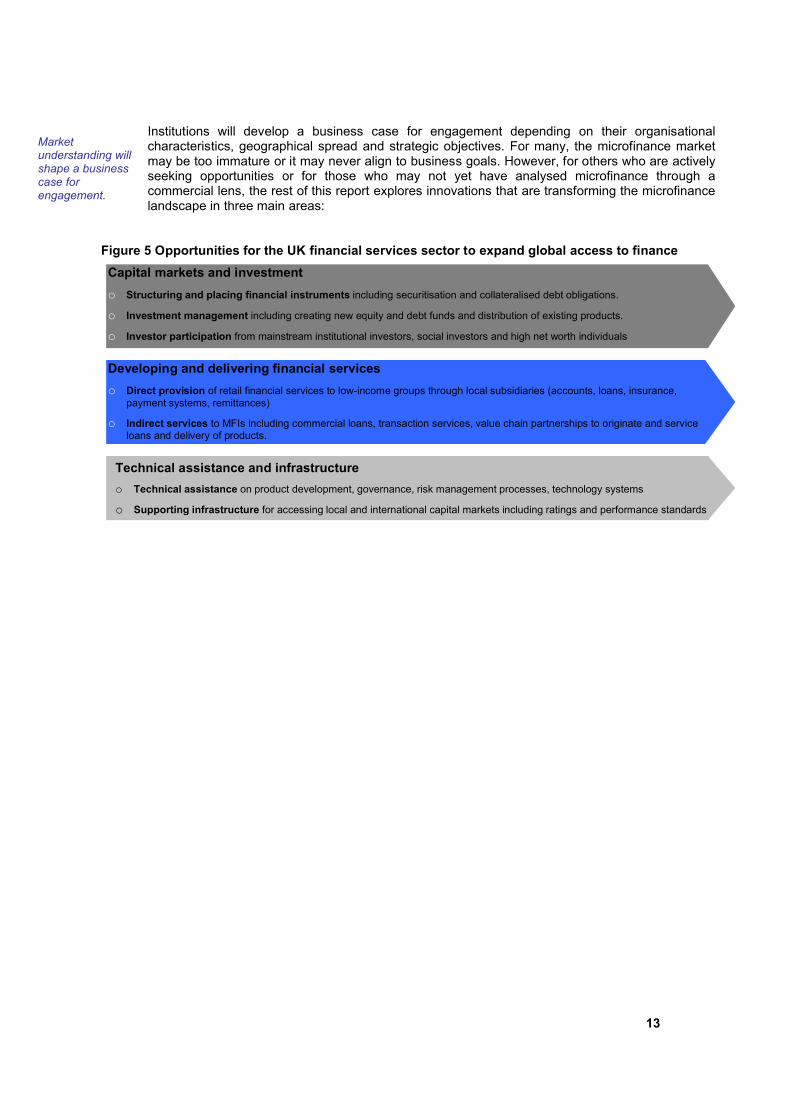

Institutions will develop a business case for engagement depending on their organisational characteristics, geographical spread and strategic objectives. For many, the microfinance market may be too immature or it may never align to business goals. However, for others who are actively seeking opportunities or for those who may not yet have analysed microfinance through a commercial lens, the rest of this report explores innovations that are transforming the microfinance landscape in three main areas:

Figure 5 Opportunities for the UK financial services sector to expand global access to finance

Market understanding will shape a business case for engagement.

Developing and delivering financial services

o Direct provision of retail financial services to low-income groups through local subsidiaries (accounts, loans, insurance, payment systems, remittances)

o Indirect services to MFIs including commercial loans, transaction services, value chain partnerships to originate and service loans and delivery of products.

Capital markets and investment

o Structuring and placing financial instruments including securitisation and collateralised debt obligations.

o Investment management including creating new equity and debt funds and distribution of existing products.

o Investor participation from mainstream institutional investors, social investors and high net worth individuals

Technical assistance and infrastructure

o Technical assistance on product development, governance, risk management processes, technology systems

o Supporting infrastructure for accessing local and international capital markets including ratings and performance standards

14

2 capital markets and investment

The demand for commercial capital in the microfinance industry is far greater

than current supply levels. As explained earlier, donor and philanthropic funds

are unable to meet the financing needs of MFIs. Mobilising savings is only an

option for a small portion of MFIs who are authorised to take deposits – and

particularly in many very low-income areas – this is not yet a viable and scaleable

source of capital. Only commercial funding – from international and domestic

sources – will be able to fill the gap. Nevertheless, donor funds will remain an

important component of the capital mix, especially for leveraging private

investment, seed capital for new MFIs, technical assistance and providing

finance for micro-loans for the extreme poor.

This section starts by examining emerging commercial investment opportunities

and exploring the growing force of microfinance investment vehicles before

focusing on debt and equity investment in more detail with some case studies.

A range of routes into commercial investment in microfinance have emerged in

recent years – for both mainstream commercial investors and social investors

looking for market returns. These include direct investments in MFIs or MFI

bonds or through microfinance investment vehicles such as dedicated debt and

equity funds, pooled guarantees and more esoteric structured instruments such

as collateralised debt obligations (CDOs). Venture capital style investing in start-

up MFIs is also gaining increased attention with a few small operators such as

Unitus and Aavishkar India. Accelerating growth and rapidly expanding the top

tier of MFIs will be essential to increase the sector’s capacity to absorb growing

amounts of capital.

15

Figure 6 Commercial investment in microfinance

Foreign investors include a broader mix of philanthropic and social investors, enabling a wider risk return profile and more flexibility in choosing investment options than purely commercial investors in most developing countries. Both international and domestic commercial investors have a much more conservative investment profile and will invest in a narrower range of low risk instruments –often through credit enhancement – or high quality MFIs. The large and growing multi-trillion dollar socially responsible investor segment in North America and Europe is potentially an attractive source of funds for the microfinance industry. However, the bulk of these funds are held in screened portfolios that exclude ‘sin stocks’ such as nuclear or tobacco but mainly invest in large corporate stocks. They may be more flexible than purely commercial investors but do not compromise on returns. Socially responsible funds run by institutions such as Morley in the UK and AXA in France have invested in microfinance securities, but only in relatively well structured and lower risk instruments.

Some of the larger institutional investors such as TIAA-CREF in the United States and ABP from the Netherlands have recently made significant allocations to microfinance but overall activity and interest in this space from pension funds is relatively low. Some mainstream financial institutions have also invested in the emerging structured instruments that can offer a range of risk-reward profiles to suit different investor types (discussed in more detail in the next section).

“Mainstream capital is not brave. It does not like going places where the rules are unclear or subject to multiple interpretations. It does not like to go where the expected returns are not calculated clearly and plausibly and where the risk is not fully detailed and explained”20.

Microfinance investment has only emerged in the last few years, and although it is growing rapidly, it is more of an umbrella term for a diverse range of investment approaches rather than a formalised investment thesis. It is a very young field with undefined metrics, poor performance measurement standards and insufficient disclosure. Liquidity is a concern as is the complete absence of any secondary markets for microfinance investments (apart from some ad hoc sales of microloan portfolios by ICICI to other banks in India, where demand is driven by priority sector

20 Jed Emerson and Josh Spitzer “Blended Value Investing: Capital Opportunities for Social and Environmental Impact” World Economic Forum March 2006

Microfinance institutions

Debt Funding

Commercial loans to MFIs made by international or domestic banks, MFI funds or international financial institutions.

Guarantees for MFI loans using approaches such as pooled guarantee funds.

Bonds for domestic capital markets.

Structured instruments including securitisation for both national and international debt offerings.

Microfinance investment funds and vehicles

Debt only / Debt & Equity / Equity only / Venture Capital

Equity Funding

Socially responsible equity directly or through microfinance funds

Commercial equity directly or through microfinance funds. Little MFI listed equity or mainstream funds yet.

Social venture capital using venture model for early stage investment in MFIs

Debt funding

Equity funding

Range of investor profiles from social to commercial.

Microfinance investment is a young and undeveloped field.

Local commercial investors

Local commercial bank loans

International donor

International philanthropic

International socially responsible

International commercial

16

lending regulations) making it very difficult for investors to freely trade microfinance assets and exit investments rapidly as is the case in most mainstream asset classes.

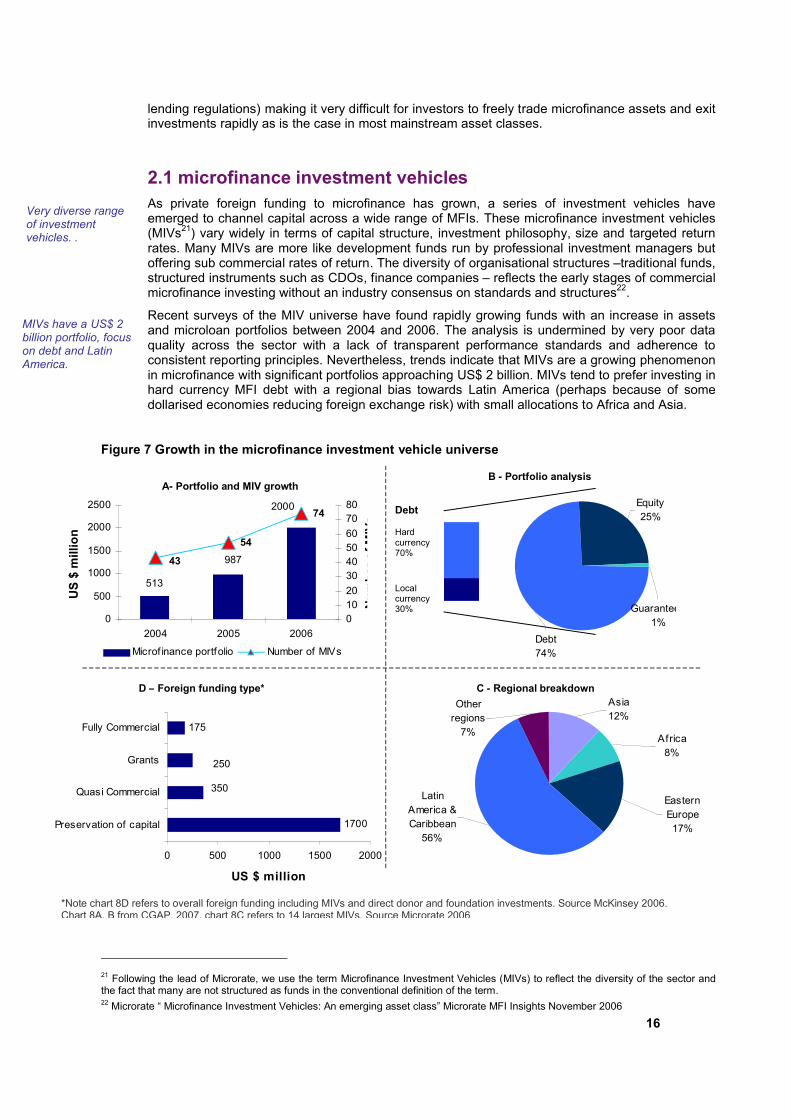

2.1 microfinance investment vehicles As private foreign funding to microfinance has grown, a series of investment vehicles have emerged to channel capital across a wide range of MFIs. These microfinance investment vehicles (MIVs21) vary widely in terms of capital structure, investment philosophy, size and targeted return rates. Many MIVs are more like development funds run by professional investment managers but offering sub commercial rates of return. The diversity of organisational structures –traditional funds, structured instruments such as CDOs, finance companies – reflects the early stages of commercial microfinance investing without an industry consensus on standards and structures22.

Recent surveys of the MIV universe have found rapidly growing funds with an increase in assets and microloan portfolios between 2004 and 2006. The analysis is undermined by very poor data quality across the sector with a lack of transparent performance standards and adherence to consistent reporting principles. Nevertheless, trends indicate that MIVs are a growing phenomenon in microfinance with significant portfolios approaching US$ 2 billion. MIVs tend to prefer investing in hard currency MFI debt with a regional bias towards Latin America (perhaps because of some dollarised economies reducing foreign exchange risk) with small allocations to Africa and Asia.

Figure 7 Growth in the microfinance investment vehicle universe

21 Following the lead of Microrate, we use the term Microfinance Investment Vehicles (MIVs) to reflect the diversity of the sector and the fact that many are not structured as funds in the conventional definition of the term. 22 Microrate “ Microfinance Investment Vehicles: An emerging asset class” Microrate MFI Insights November 2006

Very diverse range of investment vehicles. .

MIVs have a US$ 2 billion portfolio, focus on debt and Latin America.

Latin America & Caribbean

56%

Eastern Europe

17%

Africa8%

Asia12%

Other regions

7%

1700

175

250

350

0 500 1000 1500 2000

Preservation of capital

Quasi Commercial

Grants

Fully Commercial

US $ million

513

987

2000

54

74

43

0

500

1000

1500

2000

2500

2004 2005 2006

US

$ m

illio

n

01020

30405060

7080

Nu

mb

er o

f M

IVs

Microf inance portfolio Number of MIVs

C - Regional breakdown

B - Portfolio analysisA- Portfolio and MIV growth

D – Foreign funding type*

Guarantees1%

Debt74%

Equity25%

Local currency 30%

Hard currency 70%

Debt

*Note chart 8D refers to overall foreign funding including MIVs and direct donor and foundation investments. Source McKinsey 2006. Chart 8A, B from CGAP, 2007, chart 8C refers to 14 largest MIVs. Source Microrate 2006

17

Most MIVs are relatively small; 82% have less than US$ 20 million under management while only 8% have more than US$ 50 million. The top ten account for 65% of total investments23. The largest MIVs – ProCredit (a Germany based holding company for a group of 19 microfinance banks dominated by 10 banks in Eastern Europe with 5 in Africa and 4 in Latin America) and Oikocredit (a Dutch 30 year old privately owned cooperative society that offers investors a capped 2% dividend return) are mainly development MIVs but more commercially driven funds (Dexia or responsAbility) and CDOs are becoming increasingly important.

Figure 8 (a) Top ten microfinance investment vehicles (b) MIV investors by type

MIVs are still reliant on funding from social investors and international financial institutions. ‘Preservation of capital’ investment – where investors want to protect their principal but do not demand market returns – dominates overall foreign microfinance funding – directly or through MIVs. Socially Responsible Investors (SRI) are a growing force in private MIVs, accounting for about 47% of total investment – of which 70% comes from European investors – but this includes a wide variety of investment styles and return targets from near market rates through to minimal returns. Almost all MIVs (excluding the CDOs) offer subcommercial returns of around 1-3% rather than competitive market rate returns. The more mature MIVs that focus on debt offer returns of between 2.6% and 5.1% in US Dollars24.

Some MIVs are trying to expand their investor base by creating investment propositions that will attract a wider range of commercial investors. CDOs with credit-enhanced debt that can be purchased by conservative institutional investors are discussed in the next section. Another approach is to tap retail and high net worth investors, particularly those looking for social and commercial returns. Dexia Microcredit Fund is a Luxembourg registered SICAV (a type of open ended mutual fund) sponsored and distributed by Dexia, a large Belgian banking and investment group, and managed by BlueOrchard, a specialised Swiss microfinance investment firm. The fund offers investment in US Dollars, Swiss Francs and Euros. Since inception in 1998, the fund has grown to US$ 169 million in total assets with a top level 6.49% return in the last 12 months25. Credit Suisse, some other Swiss private banks and social venture capital firms sponsor the responsAbility global microfinance fund which invests directly in MFIs across the world as well as other MIVs with a focus on hard currency short to mid term MFI debt. The fund is Luxembourg registered and managed by Credit Suisse and has grown very rapidly. Since inception in 2003, it grew by 455% in 2005 and now has a total fund volume of US$ 96 million26. These registered funds can be

23 Xavier Reille and Ousa Saninkone “Microfinance Investment Vehicles” Consultative Group to Assist the Poor, Brief, April 2007. The data is based on two surveys in late 2006: a CGAP study on IFI microfinance portfolios and joint CGAP-MicroRate research on MIV trends24 Ibid. The data is based on the Symbiotic Microfinance Index available at www.symbiotics.ch 25 Dexia Microcredit Fund – February newsletter 26 Microrate “ Microfinance Investment Vehicles: An emerging asset class” Microrate MFI Insights November 2006, responsibility monthly report January 2007

Most MIVs do not offer market returns..

Rapid growth through tapping retail and high net worth investors.

3 90 .4

107

96

90 .7

8 1.2

6 0

5 2 .5

39 .8

19 9 .2

23 1.3

0 100 200 300 400 500

P ro Credit Ho lding A G

Oikocredit

Euro pean Fund fo r So utheast Euro pe

Dexia M icrocredit Fund

B lueOrchard Loans fo r Develo pment*

respo nsA bility glo bal micro finance fund

B lueOrchard M F Securit ies*

Develo ping World M arkets XXEB *

Glo bal Commerc ial M F Conso rtium

Grey Ghost Fund

US $ million

M ainstream Investo rs

17%

Develo pment Finance

Instituio ns 36%

So cially Responsible

Investo rs 47%

* Refers to collateralised debt obligations (CDOs). Source CGAP Microrate Survey 2005

18

distributed using traditional channels and follow mainstream fund management processes including daily or monthly pricing, have International Security Identification Numbers (ISIN) - a uniform identification system – and are usually sponsored by well established mainstream commercial institutions which provides credibility.

Industry-wide efforts to improve transparency and develop a standard set of disclosure guidelines, led by CGAP, are underway. Although still at a draft stage, the proposed guidelines include a set of robust performance metrics, valuation procedures, cost structures and a classification scheme.

2.2 debt funding for MFIsDebt is clearly the preferred method of foreign funding for MFIs. After donated funds, debt makes up the bulk of capital that has flowed to MFIs and is considered less risky for the investor. With many investors still unsure of the potential of equity investment at this early stage of the industry, debt instruments are the best way to become familiar with an MFI’s operations and management. Furthermore, debt ensures a regular flow of interest income. Most MFIs are not structured as joint stock companies, preventing them from issuing equity. However, debt funding has also seen the most innovation in products and processes. Moving beyond commercial loans or lines of credit to a select handful of MFIs, a number of recent innovations have pushed the envelope in debt funding for MFIs by adapting structuring techniques from mainstream capital markets such as securitization or creating innovative loan guarantee structures. However, the emerging asset class of MFI debt faces significant challenges in expanding outreach, creating appropriate products, and managing risk.

Most of the foreign debt investment is going to a small number of Tier 1 MFIs with funds increasingly competing to lend to elite institutions who might be able to attract domestic investors or mobilise savings27. Increasing competition and declining yields encourages these regulated MFIs to increase domestic financing of their liabilities, as this is seen as less expensive than debt. This does not necessarily mean that these MFIs want the absolute amount of their foreign borrowings to decline. But it does suggest that, in the future, the regulated MFIs that have absorbed most of the foreign debt may need less of it as a proportion of total liabilities28. In contrast, the vast majority of unregulated Tier 2 and below MFIs are not structured to take equity investment, and they are generally prohibited from taking public savings. Few domestic banks lend to those Tier 2 MFIs – and if so, often only for a mortgage on the MFIs’ property and only at very expensive rates.

Smaller MFIs offer a huge opportunity for foreign debt – and in some cases equity – investment. At the same time, Tier 2 and below MFIs also present a risky proposition for debt investors. Their legal structure does not include owners that banks can hold accountable in case of default. Arguably most critical however is the lack of collateral. Tier 2 MFIs don’t have an asset base apart from an unsecured microloan portfolio, which is hard to evaluate given poor information quality. Credit enhancement and pooling for risk diversification may help overcome some of these barriers.

Another frequently raised concern about efficient debt funding for MFIs relates to foreign exchange risk. Around 70% of foreign investment in MFIs is in hard currency - whilst most of an MFI’s loans and other assets tend to be denominated in local currency. Since MFIs operate in developing countries where the risk of currency depreciation is highest, they are vulnerable to risk that has at least three components: 1) devaluation or depreciation risk, 2) convertibility risk, and 3) transfer risk. While some instruments do exist for some MFIs to hedge against foreign exchange risk29, evidence indicates that most MFIs that take on foreign debt are heavily focused on the apparent interest rate advantage. But they are not alert to the fact that a foreign loan with a lower nominal interest rate may be more costly in real terms. Some risk management and hedging instruments are available but are often too expensive meaning that FX risks are currently not managed well. Sophisticated initiatives that can offer local currency funding are slowly emerging but have yet to scale effectively and be used by the majority of MFIs. The TCX facility being developed by IFC,

27 “Foreign investment in microfinance: debt and equity from quasi-commercial investors” Consultative Group to Assist the Poor, Focus Note 25, January 200428 Ibid29 Possible methods to ‘hedge’ against exchange risk could involve, for instance, e.g. 1) Conventional instruments (Forward contracts and futures, Swaps, Options; 2) Back-to-Back Lending, 3) Letters of Credit, 4) Local Currency Loans Payable in Hard Currency with a Currency Devaluation Account, 5) Self-imposed Prudential Limits, 6) Indexation of Loans to Hard Currency.

Debt dominates foreign investment , but innovation is increasing.

Investment concentrated in elite MFIs, who need it least.

Tier-2 MFIs are higher risk but offer massive opportunities.

Foreign exchange risk is not managed.

19

Kfw and FMO is an example of efforts in this space as are currency swaps used by Morgan Stanley and the emergence of local currency microfinance funds such as Minlam Asset Management and LOCFUND.

Innovations are emerging in both onshore funding (where the transaction is based solely in domestic jurisdictions) and offshore funding (where the transaction is across national borders and is often based in an attractive tax domicile such as Luxembourg). Bonds, guarantees and syndicated loan facilities are some of the main onshore innovations.

local currency bonds

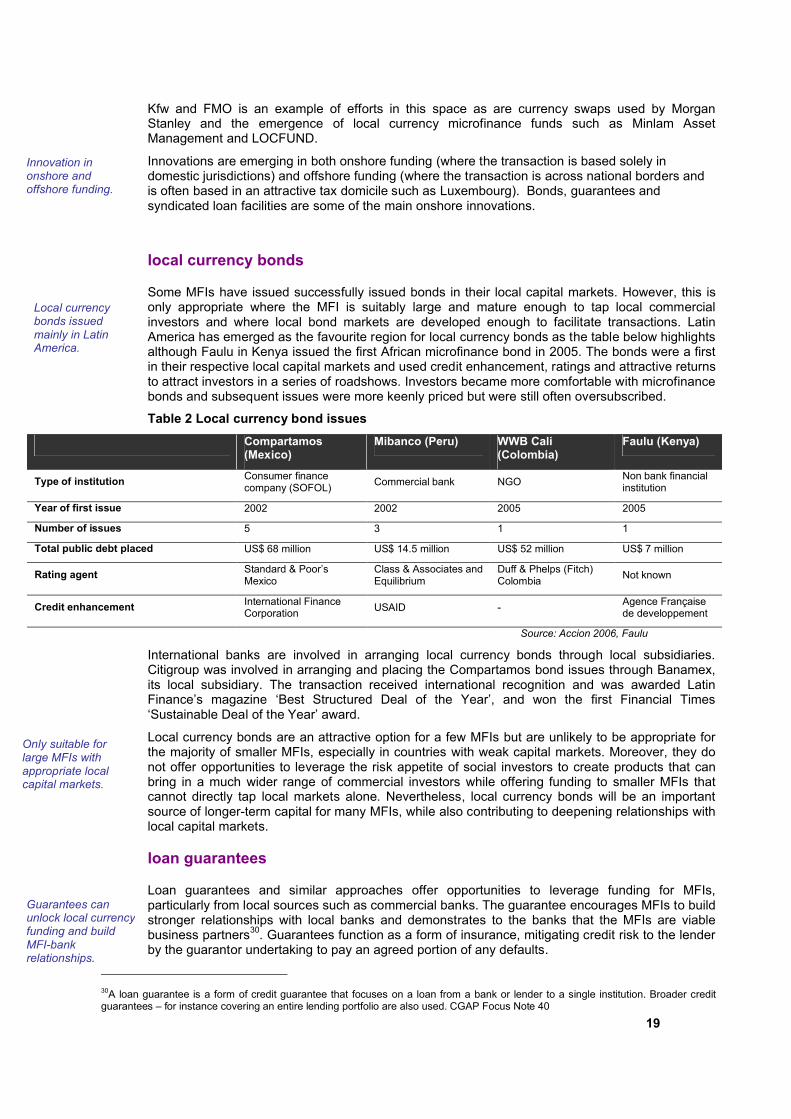

Some MFIs have issued successfully issued bonds in their local capital markets. However, this is only appropriate where the MFI is suitably large and mature enough to tap local commercial investors and where local bond markets are developed enough to facilitate transactions. Latin America has emerged as the favourite region for local currency bonds as the table below highlights although Faulu in Kenya issued the first African microfinance bond in 2005. The bonds were a first in their respective local capital markets and used credit enhancement, ratings and attractive returns to attract investors in a series of roadshows. Investors became more comfortable with microfinance bonds and subsequent issues were more keenly priced but were still often oversubscribed.

Table 2 Local currency bond issues

Compartamos (Mexico)

Mibanco (Peru) WWB Cali (Colombia)

Faulu (Kenya)

Type of institution Consumer finance company (SOFOL)

Commercial bank NGONon bank financial institution

Year of first issue 2002 2002 2005 2005

Number of issues 5 3 1 1

Total public debt placed US$ 68 million US$ 14.5 million US$ 52 million US$ 7 million

Rating agent Standard & Poor’s Mexico

Class & Associates and Equilibrium

Duff & Phelps (Fitch) Colombia

Not known

Credit enhancement International Finance Corporation

USAID -Agence Française de developpement

Source: Accion 2006, Faulu

International banks are involved in arranging local currency bonds through local subsidiaries. Citigroup was involved in arranging and placing the Compartamos bond issues through Banamex, its local subsidiary. The transaction received international recognition and was awarded Latin Finance’s magazine ‘Best Structured Deal of the Year’, and won the first Financial Times ‘Sustainable Deal of the Year’ award.

Local currency bonds are an attractive option for a few MFIs but are unlikely to be appropriate for the majority of smaller MFIs, especially in countries with weak capital markets. Moreover, they do not offer opportunities to leverage the risk appetite of social investors to create products that can bring in a much wider range of commercial investors while offering funding to smaller MFIs that cannot directly tap local markets alone. Nevertheless, local currency bonds will be an important source of longer-term capital for many MFIs, while also contributing to deepening relationships with local capital markets.

loan guarantees

Loan guarantees and similar approaches offer opportunities to leverage funding for MFIs, particularly from local sources such as commercial banks. The guarantee encourages MFIs to build stronger relationships with local banks and demonstrates to the banks that the MFIs are viable business partners30. Guarantees function as a form of insurance, mitigating credit risk to the lender by the guarantor undertaking to pay an agreed portion of any defaults.

30A loan guarantee is a form of credit guarantee that focuses on a loan from a bank or lender to a single institution. Broader credit guarantees – for instance covering an entire lending portfolio are also used. CGAP Focus Note 40

Guarantees can unlock local currency funding and build MFI-bank relationships.

Local currency bonds issued mainly in Latin America.

Only suitable for large MFIs with appropriate local capital markets.

Innovation in onshore and offshore funding.

20

Although guarantees are not always appropriate for all MFIs or countries and can sometimes be more expensive and less catalytic than intended, they can be powerful tools for leveraging guarantor capital, enabling local currency funding with low FX risk and overcoming regulatory hurdles to foreign investment31. Guarantees are a small but growing part of the microfinance capital mix – accounting for 2% of the estimated US$ 4 billion foreign investment. Although development finance agencies are the main guarantors, some private initiatives have emerged in recent years.

local lending facilities

Some international banks, with Citigroup probably doing most to innovate in this area, are also pursuing an alternative funding strategy by developing syndicated loan and local currency funding facilities. A US$ 100 million term facility supported by a US$70 million guarantee by OPIC (a US government agency that provides guarantee services) will enable funding to a broader set of tier 1 and 2 MFIs through Citigroup’s global branch network.

Other banks such as HSBC, ABN Amro and Standard Chartered also intend to mainly channel funding through local subsidiaries.

structured products

A recent development in microfinance debt funding is using mainstream financial structuring techniques to create products that enable MFIs to tap domestic or international debt markets. Structured finance techniques such as securitisation – which pools assets together and transfers them to a special purpose vehicle, which then issues securities backed by these assets to

31 CGAP focus note 40

Case – International guarantee schemes

Pooled guarantee schemes that use international investors to back local currency loans to MFIs by domestic commercial banks are increasingly being used as an effective way to enable MFIs to raise capital without having to make direct investments.

Some early initiatives used philanthropic investors to pledge assets in a special account that were in turn used to offer standby letters of credit (SBLOC) and other guarantee mechanisms to MFIs. Deutsche Bank’s Microcredit Development Fund used donated capital from private bank clients to set up a revolvinf fund that offered subsidised loans to MFIs to improve their balance sheet position (not for on-lending to MFI clients) and thus attract local capital.

Grameen Foundation USA’s Growth Guarantee programme uses donor-guarantors who pledge a minimum of US$ 1 million for 5 years to Citibank in the USA. The money is held in an agreed portfolio, the donors still earn returns and the pledges are pooled by Citibank to issue SBLOCs to domestic banks in the MFI’s country. This SBLOC can be used to guarantee a commercial loan, provide a first loss cushion or other forms of support.

Deutsche Bank’s Global Commercial Microfinance Consortium (GCMC) – which closed in November 2005 with US$ 75 million in committed capital – is an innovative transaction that uses structuring techniques to create different tranches with different risk-reward characteristics suitable for a range of investors and offers very flexible funding options for MFIs across the world. It is essentially a structured product (covered in the next section) but is discussed here due to its use of guarantee mechanisms.

The consortium’s sophisticated capital structure leverages credit enhancement by public agencies and social investors to create a debt tranche of US$ 60 million senior five-year notes (offering a return of LIBOR +1.25%) cushioned by three equity tranches totalling US$ 15 million (US$ 5.5 million class B equity offering 12% return, US$ 8 million class A equity offering 8%). A US$ 1.5 million first loss position was taken by the UK Department for International Development and USAID guarantees 25% (US$ 15 million) of the senior notes. Foundations and social investors bought the equity tranches while commercial investors like AXA, Merrill Lynch, State Street and Standard Life purchased the notes.

GCMC offers MFI flexible funding options including co-lending with domestic banks, use of deposits, SBLOCs and credit default swaps. This enables MFIs to build relationships with banks, leverage GCMC funding to attract local capital and reduces conventional hard currency debt loans with the associated foreign exchange risk.

These forms of innovative funding solutions for MFIs have a lot of potential for replication and scalability. By focusing on both investor needs (risk-return, credit enhancement) and MFI needs (flexible funding, improve commercial links, local currency) these structures can add significant value.

Source: Case study information adapted from WEF Blended Value Investing 2006

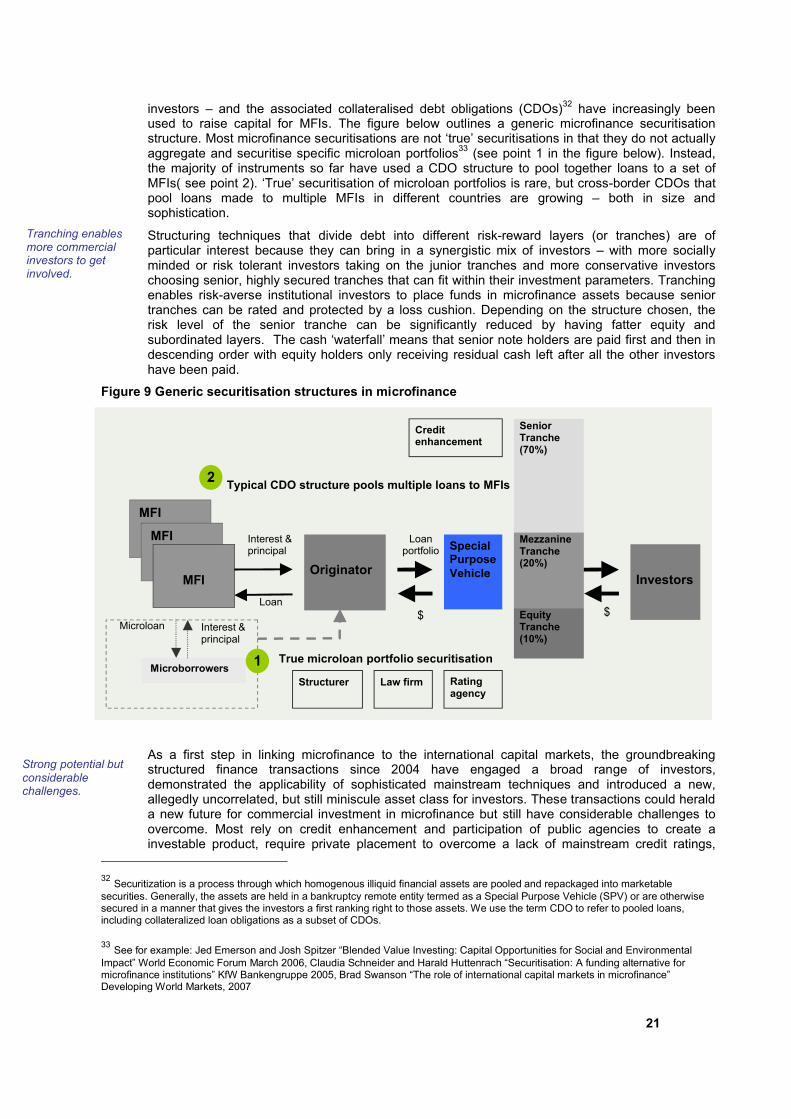

Microfinance securitisation uses a collateralised debt obligation (CDO) structure.

21

investors – and the associated collateralised debt obligations (CDOs)32 have increasingly been used to raise capital for MFIs. The figure below outlines a generic microfinance securitisation structure. Most microfinance securitisations are not ‘true’ securitisations in that they do not actually aggregate and securitise specific microloan portfolios33 (see point 1 in the figure below). Instead, the majority of instruments so far have used a CDO structure to pool together loans to a set of MFIs( see point 2). ‘True’ securitisation of microloan portfolios is rare, but cross-border CDOs that pool loans made to multiple MFIs in different countries are growing – both in size and sophistication.

Structuring techniques that divide debt into different risk-reward layers (or tranches) are of particular interest because they can bring in a synergistic mix of investors – with more socially minded or risk tolerant investors taking on the junior tranches and more conservative investors choosing senior, highly secured tranches that can fit within their investment parameters. Tranching enables risk-averse institutional investors to place funds in microfinance assets because senior tranches can be rated and protected by a loss cushion. Depending on the structure chosen, the risk level of the senior tranche can be significantly reduced by having fatter equity and subordinated layers. The cash ‘waterfall’ means that senior note holders are paid first and then in descending order with equity holders only receiving residual cash left after all the other investors have been paid.

Figure 9 Generic securitisation structures in microfinance

As a first step in linking microfinance to the international capital markets, the groundbreaking structured finance transactions since 2004 have engaged a broad range of investors, demonstrated the applicability of sophisticated mainstream techniques and introduced a new, allegedly uncorrelated, but still miniscule asset class for investors. These transactions could herald a new future for commercial investment in microfinance but still have considerable challenges to overcome. Most rely on credit enhancement and participation of public agencies to create a investable product, require private placement to overcome a lack of mainstream credit ratings,

32

Securitization is a process through which homogenous illiquid financial assets are pooled and repackaged into marketable securities. Generally, the assets are held in a bankruptcy remote entity termed as a Special Purpose Vehicle (SPV) or are otherwise secured in a manner that gives the investors a first ranking right to those assets. We use the term CDO to refer to pooled loans, including collateralized loan obligations as a subset of CDOs.

33See for example: Jed Emerson and Josh Spitzer “Blended Value Investing: Capital Opportunities for Social and Environmental