NEW GMA STUDY OUTSOURCING SALES - ASMC …asmcfoundation.org/OutsourcingSalesMarketing.pdfHow CPG...

13

FORUM 75 M I D -F A L L 2007 I S S U E O UTSOURCING IS AN AREA IN WHICH CPG IS ROUTINELY OBSERVED TO LAG OTHER SECTORS. But in one key function, sales and marketing, CPG manufac- turers are expert outsourcers: They have relied for many years on food brokers –– today preferably known as sales and marketing agencies. Now, according to an 18-month GMA study, “Outsourcing is In!”, financed by the ASMC Foundation and conducted by iCRM, the pace of sales and marketing outsourcing is picking up. Why? “First,” says Thomas W. Gruen, Ph.D., University of Colorado (Colorado Springs), a study author who presented the findings on October 2 at GMA ’s MSM Conference, “most ... CPG companies believe that sales and marketing agencies perform transactional services at somewhere around 30 to 50 percent lower than direct sales teams.” How? By spreading overheads and operating costs over multiple prod- ucts and manufacturers: “Scale advantages from the syndicated sales model –– back room support, HR, the general ability to spread over- heads and operating costs across multiple companies all add up.” SALES & MARKETING SALES & MARKETING AGENCIES ARE THE SWISS ARMY KNIFE OF CPG –– in the field, they are the manufacturer’s head and hands, its “go to” implementation guys and gals, its connection from the top of the customer organization to the floor of the store. Today, shifting mar- ket forces are rapidly leading even more manufacturers to employ this implementation ‘tool’ at an ever-faster rate: According to a new GMA study unveiled at the recent MSM conference, sales agency market representation will have grown 10-15 percent in 2007 alone, and by 2010 will represent a full $213 billion –– almost double the 2005 level. HERE’S WHY. OUTSOURCING NEW GMA STUDY: ©iStockphoto.com/James Steidl/Elissa Hari-Curtis

Transcript of NEW GMA STUDY OUTSOURCING SALES - ASMC …asmcfoundation.org/OutsourcingSalesMarketing.pdfHow CPG...

FORUM 75M I D - F A L L 2 0 0 7 I S S U E

OUTSOURCING IS AN AREA IN

WHICH CPG IS ROUTINELY

OBSERVED TO LAG OTHER

SECTORS. But in one key function,sales and marketing, CPG manufac-turers are expert outsourcers: Theyhave relied for many years on foodbrokers –– today preferably knownas sales and marketing agencies.

Now, according to an 18-monthGMA study, “Outsourcing is In!”,

financed by the ASMC Foundationand conducted by iCRM, the paceof sales and marketing outsourcing ispicking up.

Why? “First,” says Thomas W. Gruen,Ph.D., University of Colorado(Colorado Springs), a study author whopresented the findings on October 2at GMA’s MSM Conference, “most ...CPG companies believe that salesand marketing agencies perform

transactional services at somewherearound 30 to 50 percent lower thandirect sales teams.”

How? By spreading overheads andoperating costs over multiple prod-ucts and manufacturers: “Scaleadvantages from the syndicated salesmodel –– back room support, HR,the general ability to spread over-heads and operating costs acrossmultiple companies all add up.”

SALES &MARKETING

SALES & MARKETING AGENCIES ARE THE SWISS ARMY KNIFE OF CPG –– in the field, they arethe manufacturer’s head and hands, its “go to” implementation guys and gals, its connectionfrom the top of the customer organization to the floor of the store. Today, shifting mar-ket forces are rapidly leading even more manufacturers to employ this implementation ‘tool’at an ever-faster rate: According to a new GMA study unveiled at the recent MSMconference, sales agency market representation will have grown 10-15 percent in 2007 alone, andby 2010 will represent a full $213 billion –– almost double the 2005 level. HERE’S WHY.

OUTSOURCINGNEW GMA STUDY:

©iS

tock

phot

o.co

m/

Jam

es S

teid

l/El

issa

Har

i-Cur

tis

FORUM76 M I D - F A L L 2 0 0 7 I S S U E

50

25

75

100

50250

75 100

Percent of CPG Revenues Outsourced

...55% of companies outsource 65% of revenues

PERC

ENT

OF R

EVEN

UES

PERCENT OF COMPANIES OUTSOURCING

50

25

75

100

05025 75 100

Percent of Brands Outsourced

...60% of companies outsource 80% of their brands PE

RCEN

T OF

BRA

NDS

PERCENT OF COMPANIES OUTSOURCING

5025 75 100

Percent of Customers Outsourced

50

25

75

100

0

...50% of companies outsource 65% of their customers

PERC

ENT

OF C

USTO

MER

S

PERCENT OF COMPANIES OUTSOURCING

Costs are lower also because salesagencies are better able to cope withthe peaks and valleys of work forcedemand, especially for non-routineretail projects.

But today, cost savings are not the onlybenefit, according to CPG suppliersmoving rapidly to deploy sales agen-cies more widely. Intense competitionand shifting market forces are drivingCPG companies to turn increasingly tosales agencies for more efficient andeffective retail account servicing.

“Even companies that do not outsourcetheir sales and marketing acknowledge... superior capabilities by SMAs to pro-vide more frequent retail coverage,”Gruen notes.

More and more, the study finds, sen-ior CPG executives are recognizingsales agencies as an effective tool forimproving marketing productivity

and reduce the margin pressurescaused by retail price erosion, risingwages and escalating fuel costs.

Today, in many operational areas,limits on available resources withinthe context of a rapidly moving andever-changing business landscape areprompting CPG companies to focusmore on their core capabilities andoutsource those functions that canbe better performed by others.

Outsourcing to sales agencies is con-sidered by a growing number ofCPG companies large and small tobe a viable option for streamliningand improving the sales and market-ing processes –– indeed, even toserve some accounts at all.

Non-traditional specialty retailers,for example, are increasingly includ-ing CPG food products as part oflifestyle offerings. Often, these

accounts could not be efficientlyserved by a CPG company’s directsales force.

The emergence of an expanded scopeof merchandise in non-grocery retailers,such as dollar stores and specialty life-style stores including Barnes & Noble,Best Buy, Home Depot, Victoria’s Secretand Toys “R” Us, is another factorprompting more CPG companies toseek support from sales agencies.

Servicing such an emerging mix in non-traditional channels through a directsales force can be difficult even for bigCPG companies with deep pockets.

Finally, the expansion of mega-retail-ers into new geographies, new cate-gories, new formats and new pricepositioning is compelling CPG com-panies to devise ways of participat-ing more actively with retailer-defined tasks and objectives.

PREVALENCE OF OUTSOURCING: CPG Manufacturer Use of Sales & Marketing Agencies

ON THE UPSWING: Expected CPG Sales

Outsourced to Sales Agencies 2005 2006 2007 2008 2009 2010

116133

153176

194213

250

200

150

50

100

0

CPG

SALE

S $B

SOURCE OF ALL CHARTS: “Outsourcing is In! How CPG Companies Enhance Performance, Reduce Costs & Increase ROI Through OutsourcingSales and Marketing,” 2007, GMA/FPA, ASMC Foundation and iCRM.

NEW GMA STUDY: OUTSOURCING SALES &MARKETING

FORUM 77M I D - F A L L 2 0 0 7 I S S U E

AS CPG MANUFACTURERS SEEK MORE SOPHISTICATION, EFFICIENCIES OF SHARED COSTS

New Services Come to the Fore

Ben Fischer President-Sales AgencyCROSSMARK

ONE OF OUR CORE BELIEFS IS THAT

VALUE IS A RELATIVE THING.Different-sized manufacturers get

different value out of different services for differentreasons. So, our approach is to work with eachmanufacturer to understand the unique needs thatoffer them the greatest opportunity to create value.

This could be everything from headquarter cover-age to retail coverage to project-based work versuscontinuity-based work. It could mean that a differ-ent store base has greater value to one client, oreven to one brand inside a client portfolio, thananother store base.

Today, we’re doing ROI-based modeling to under-stand which activities creates a quantifiable dollarreturn to our clients. At the same time, some thingsaren’t necessarily an ROI calculation. Some thingsadd value not because they make money per se,but because they help build a brand or establish abetter business partnership with a key retailer.

The information we can gather and bring to bearfor manufacturer and retailer alike is one of ourgreatest strengths. We have access to 75,000SKUs, everything from the candy and gum on thefront end all the way to meat in the back.

So we can understand which stores provide a man-ufacturer’s profit –– or could. For example, a storemay be selling a lot of some product –– but not afair share of a given manufacturer’s brand.Obviously, this visibility creates an opportunity.

Or, stores that seem similar in every way often turnout, when we analyze the data, to perform very

differently in terms of a given product or brand.

Traditionally, as a manufacturer you have wantedto be in all of a given chain’s stores –– yet whenwe analyze the data we have, we often find that,say, only 40 percent of this chain’s stores createany profit for you. Which means you might bebetter served spending your money at a differentretailer, one with a more profitable store mix, or ahigher percentage of stores that perform well foryou.

If you look at the world through that kind of lens,it greatly changes your thinking and your results.Every day, as the results of these kinds of analyticsare applied to micromarketing and store clustering,it becomes clearer and clearer that this is the future.

MANUFACTURERS AREN’T THE ONLY BENEFICIARIES ofthese new capabilities; retailers gain, too. Forexample, different activity drives different results indifferent stores. Each store almost has its ownunique behavior pattern. A display at the front ofone store may not increase sales at the same rate asa display at the front of another store.

The more of such information you see, the moreyou realize it isn’t just about product mix –– it’s wherethe products are placed, what time of year, in which stores.

This might seem obvious –– but how do youknow where, when, which? As a model, applying theright activities to the right store is quite complex,actually.

So we have focused on building in a lot morespeed and flexibility. As an example, we call onevery Kroger store for one client in a 32-hour win-dow –– we hit 2,000 stores between Tuesdaymorning at 8 a.m. and Wednesday afternoon at 5p.m. This gives us a snapshot that almost no retail-

What are today’s sales agencies doing to keep up with the growing needs of manufacturers andretailers for more and better services? Here’s what “Outsourcing Is In!” steering committee membersand their services heads told us ...

■ Continues on page 84

FORUM78 M I D - F A L L 2 0 0 7 I S S U E

SUCH HAVE PRESSURES INTENSIFIED THAT

EVEN THE LARGEST CPG COMPANIES,those that have traditionally useddirect sales teams –– Kraft, GeneralMills and Procter & Gamble, forexample — are now considering ormoving to sales outsourcing.

Multiple factors are driving this trend,Gruen states: “Besides the cost advan-tage –– that minimum 30- to 50-per-cent savings –– there is the flexiblework force; as a CPG company’s busi-ness goes up and down, the SMA hasthe ability to adjust accordingly. “

In-market expertise is another strongappeal. “Local market knowledge,sell-through promotions, relation-ships inside the customers, relation-ship continuity all make for greater

effectiveness,” Gruen observes.

“Finally, there’s the marketing capa-bilities –– the frequent retail cover-age, effective shelf performance, sec-ondary selling and new-item cut-ins,the ability to generate a greater‘share of voice’ with the customer.”

CPG COMPANY RESPONDENTS EXPRESS

SIGNIFICANT INTEREST IN INCREASING

THEIR MARKET COVERAGE primarily tothe fast-evolving multi-channel world.

Even in more traditional supermarketchannels, high-value stores accountfor 60 percent of all commodities’actual cash value, while independentsand smaller customers offer greateropportunities to increase actual cashvalue and margins.

For reasons of scale and local market

presence, sales agencies are consideredby ever more sales executives to bebetter positioned than direct salesteams to service these customers.Several CPG sales vice presidents whohave made a transition or partial tran-sition addressed GMA MSM confer-ence attendees in a video accompany-ing Gruen’s presentation; all reportgreat satisfaction with the move.

States Tim Snelling, vice present-salesfor Kimberly-Clark, “What led us touse sales and marketing agencies isthe effectiveness they offer at retail, inthe small accounts. And the efficien-cies –– in some areas, a sales agencycan provide services for us at a cost ofsales well below what we can do forourselves.”

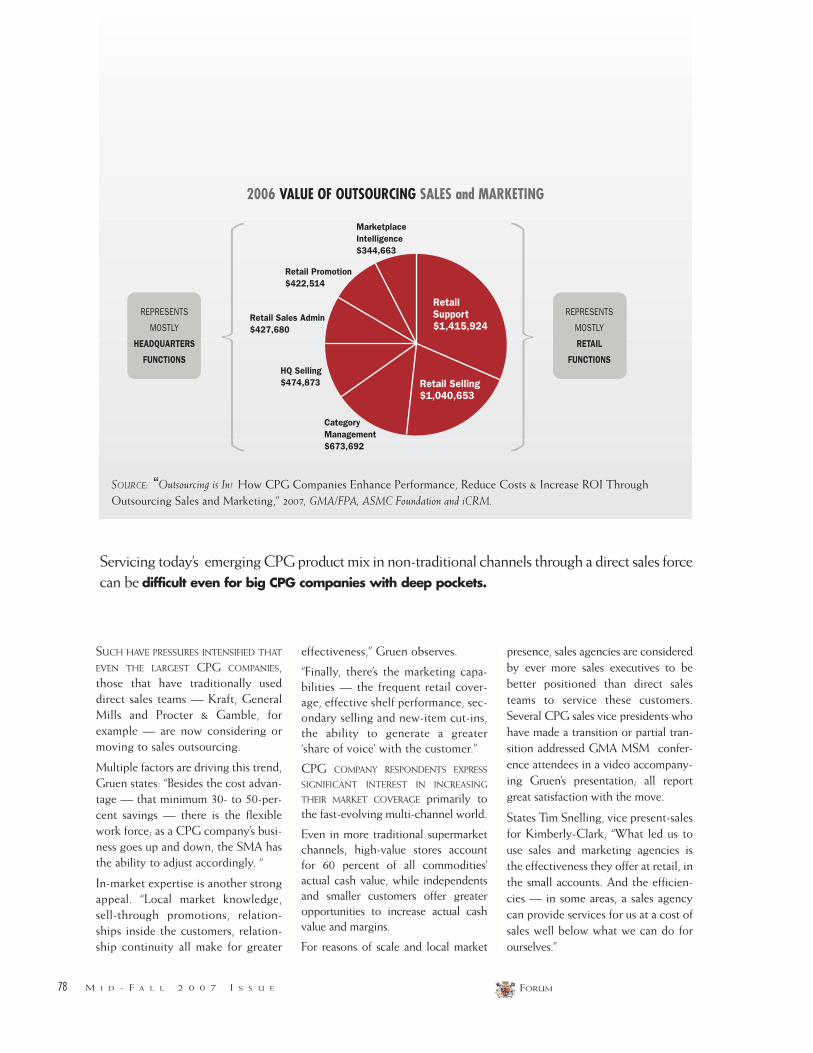

2006 VALUE OF OUTSOURCING SALES and MARKETING

Marketplace Intelligence$344,663

Retail Support$1,415,924

Retail Selling$1,040,653

Category Management$673,692

HQ Selling$474,873

Retail Sales Admin$427,680

Retail Promotion$422,514

REPRESENTS

MOSTLY

HEADQUARTERS

FUNCTIONS

REPRESENTS

MOSTLY

RETAIL

FUNCTIONS

Servicing today’s emerging CPG product mix in non-traditional channels through a direct sales forcecan be difficult even for big CPG companies with deep pockets.

SOURCE: “Outsourcing is In! How CPG Companies Enhance Performance, Reduce Costs & Increase ROI ThroughOutsourcing Sales and Marketing,” 2007, GMA/FPA, ASMC Foundation and iCRM.

As for the impact, he says: “We do notfeel we made any tradeoffs with the cus-tomer or regarding our internal organi-zation, or sacrificed anything with ouraccounts because they are no longerserved by a direct Kimberly-Clarkemployee. Today, our representativesare members of our sales team throughthe agency –– and, again, we havegained efficiencies.”

States Vanessa Maskal, vice president-sales for B&G Sales, “We use SMAs forboth headquarter and retail executionthroughout our market area.

“Because we have a diverse portfolio ofretail brands, we need local marketexpertise to effectively communicatewith our customers, and service theirneeds and our brands properly.”

For this reason, Maskal explains, B&Ghas chosen to use what it believes is thebest sales agency by market, rather thancontracting with one national service:

“It’s important to us that the key sellingpeople at headquarters have the localknowledge and the skills to effectivelyaccomplish our objectives.”

Overall, she notes, “Our success withSMAs has been to maximize our salesefforts by market area, while minimiz-ing costs –– while at the same time pro-viding our customers with the bestinformation and resources possible bymarket area.”

MERGERS ARE ANOTHER INFLUENTIAL FAC-TOR cited by CPG companies who usesales and marketing agencies.

Says Lou Tursi, vice president-con-sumer sales for Church & Dwight, “Inrecent years, our company hasacquired a lot of businesses. Having abroker partner gives you instanta-neous selling teams to sell those newproducts. This makes it simple for usto acquire a business, and almostseamlessly be able to take it to mar-ket.”

FORUM 79M I D - F A L L 2 0 0 7 I S S U E

NEW GMA STUDY: OUTSOURCING SALES &MARKETING

MANAGING THE OUTSOURCING RELATIONSHIP:Key Collaborative Dimensions / Activities / Parameters

■ Periodic meetings to review progress and achievements

■ Collaborative governance with joint development of strategies, plans,

systems, processes and competencies

■ Continuous improvement process planning and implementation by both

parties

■ Independent responsibilities undertaken by company executives and sales

agencies to manage the relationship

■ Established processes for reviewing results

■ Ongoing transparency of sales agency activities and results

■ Continuous visibility (including web-enabled reporting tools)

■ Alignment of each party’s sales administration process to avoid

duplication of activities and errors

■ Well-defined roles and responsibilities of sales agencies vis-a-vis CPG

internal sales teams

■ Variable models –– dedicated or syndicated teams, according to client need

2006 VALUE DERIVED by CPG COMPANIESFrom OUTSOURCING to SALES and MARKETING AGENCIES

SMAs REPRESENTSAVINGS in pure cost terms of$4.8 Billion

ADDITIONAL INDUSTRY SAVINGS if 100% Outsourced to SMAs$4.1 Billion

FORUM80 M I D - F A L L 2 0 0 7 I S S U E

Merchandising is still another advan-tage Tursi cites: “(Our sales agents) areincredible at helping us place merchan-dise. Their merchandising results areunbelievable! As an example, on ourCrest Spin Brush, this year –– 2007 ––we will place about 158,000 displays.”

Finally, he cites technology advan-tage: “Our sales agents stay up on allthe latest technologies in the industry,and keep us abreast of what’s going onwith each.”

Outsourcing Trends Quantified

SALES AGENCIES, THE STUDY FOUND,NOW REPRESENT ABOUT 54 PERCENT of allUS CPG company retail sales rev-enues, equivalent in 2006 to $133 bil-lion in actual cash value of commodi-ty revenues for CPG companies.

Given the trends of increased out-sourcing, the level of market represen-tation by sales agencies grew 15 per-cent from 2005 to 2006, and is expect-

ed to grow by another 10 to 15 per-cent for 2007 and beyond.

Thus, by 2010, sales and marketingagencies would represent $213 billion— almost double the 2005 level — inCPG sales to the retail channels.

The additional gain in SMA represen-tation of CPG revenues will comelargely from three sources:

■ shifts from direct sales to agencies;

■ growth in new categories such as

CASE STUDY: Rapid and Effective Cut-In of 31 New Items

NEW GMA STUDY: OUTSOURCING SALES &MARKETING

■ Cut-in 31 new pet food items in more than2,000 stores of a major retailer

■ Visit 70 percent of stores in the first week

■ Ensure new shelf tags are in place

■ Pack out shelf

■ Complete reset

The sales agency handled the followingsteps:

■ Received project request from CPG firm

■ Identified required stores for project

■ Built stores list and project plan

■ Sent project plan to field

■ Assigned field labor and executed project

■ Pulled reports daily to ensure timelyexecution

■ Sent reports to client weekly

IMPACT OF SMA’S WORK:

■ Number of stores in project: 2,164

■ Number of stores completed: 2,055

■ Two-week completion rate: 95 percent

Pet Food

■ Out-of-Stocks Corrected: 831

■ Voids Corrected: 396

■ Tags Replaced: 1,475

Litter

■ Out-of-Stocks Corrected: 25

■ Voids Corrected: 6

■ Tags Replaced: 1,475

■ ROI Ratio Impact: $233.33 to every $1

The following case illustrates how an SMA firm successfully managed a large new product introduction for aCPG firm. In a two-week period, the sales agency had to:

FORUM 81M I D - F A L L 2 0 0 7 I S S U E

organics and naturals;

■ significant growth of such channels asdollar stores and lifestyle stores.

Sales and marketing agencies cur-rently represent 67 percent, or morethan two-thirds, of all CPG brands.They cover 63 percent, or nearlytwo-thirds, of all retail customers.Study results show that 55 percent ofCPG companies outsource more than65 percent of their retail sales dollars.Sixty percent of companies outsource80 percent of their brands to salesagencies.

Aggregate Value of Outsourcing

CPG COMPANIES DERIVE AN ECONOMIC

VALUE OF MORE THAN $4.8 BILLION

ANNUALLY by outsourcing to sales andmarketing agencies, the study indi-cates. Adjusted modestly for per-ceived sales agency effectivenesscompared with direct sales teams, thisvalue reflects net cost savings accruedvia outsourcing by CPG companies.

An additional net value contributionof $4.1 billion to the CPG industry ispossible from outsourcing the 46 per-cent of CPG sales revenues not cur-rently handled by sales agencies. IfCPG companies did outsource all thesales and marketing functions cur-rently performed by direct salesteams, sales agencies would gain addi-tional professional services revenuesin excess of $2.3 billion.

CPG companies and their sales agen-cies would gain further, the study sug-gests, by making collaborative effortsto increase sales agency effectivenessand success in achieving CPG compa-ny marketing objectives. Respondents

indicate that sales agency perform-ance can be improved in several areas,including:

■ promotional effectiveness

■ customer service processes

■ entry into new markets

Satisfaction Levels Vary

DESPITE THE CLEAR TREND TO GREATER

SALES AND MARKETING OUTSOURCING,satisfaction levels among those whouse agencies varies –– curiously, withthose who do the least outsourcingalso expressing the least satisfactionwith it. The question, in classic chick-en-and-egg fashion, is: Are these compa-nies doing less outsourcing because they’re lesssastisfied –– or less satisfied because they’redoing less outsourcing?

“We spent quite a bit of time in recentweeks trying to tease out some ofthese differences between overallresponses, respondents who out-source just a little bit, and respon-dents who outsource most of theirsales and marketing work,” says TomGruen.

To do so, researchers examined sevenareas:

■ retail support and merchandising

■ retail selling

■ marketplace intelligence / monitor-ing

■ category management

■ headquarters selling

■ retail sales administration

■ retail promotion management

OUTSOURCING PENETRATION: Highest Among Small Companies,Followed by Large Companies, with Medium in Middle

Revenue Brands Customers

80%

70%

60%

50%

40%

20%

30%

10%

0%

90%

EXTE

NT O

F OU

TSOU

RCIN

G

MediumSmall Large

Sales and marketing agenciescurrently represent a full

67 percent –– more than twothirds –– of all CPG brands.

The study found that the lowest-leveloutsourcers rated sales and marketingagency capabilities at two on a six-point scale –– hardly a vote of confi-dence. Conversely, high and medi-um-level outsourcing CPG compa-nies rated SMAs at over four on a six-point scale.

Observes Tom Gruen, “What we’reseeing are real differences betweenthe perceived capabilities, based onthe degree to which respondents out-source.

“From this, it’s reasonable to concludethat CPGs who practice little or nooutsourcing may be missing opportu-nity to enhance performancethrough higher SMA utilization.

“In other words, ‘Try it! You might like it!’After all, the people who are using

SMAs are finding their capabilities tobe very strong across all seven areas.”

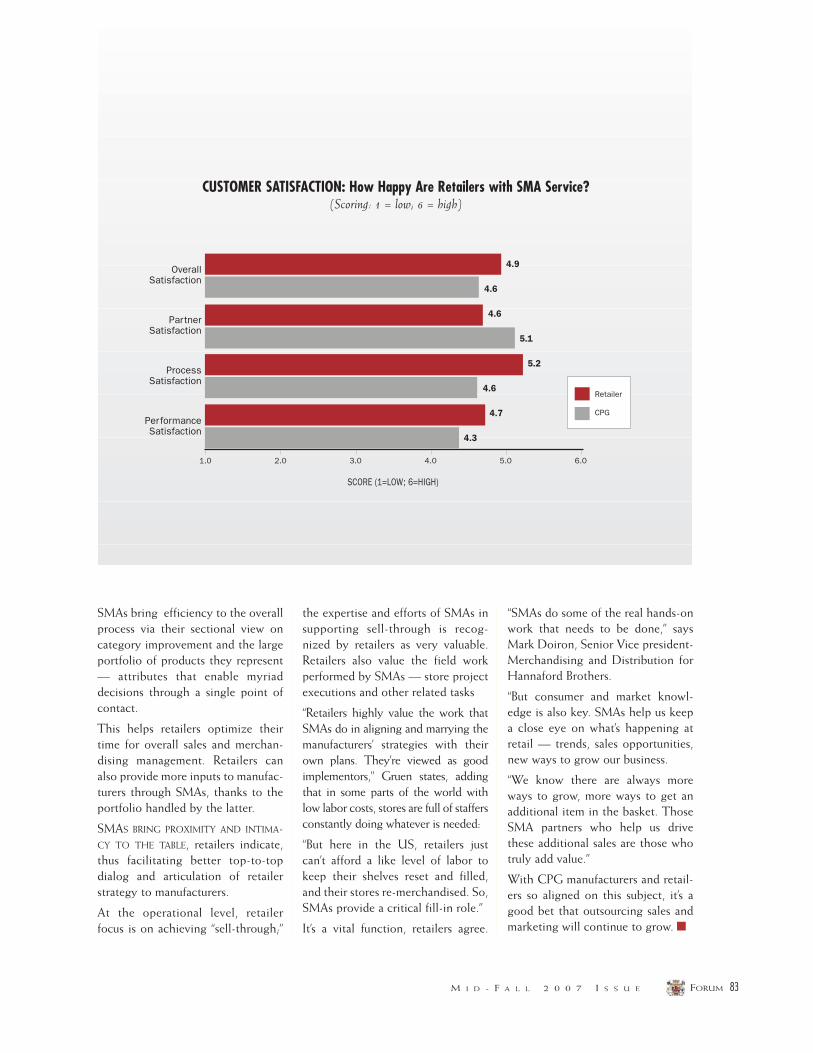

Retail Customer Satisfaction

Clearly, no matter how much sales andmarketing outsourcing saves the man-ufacturer, it won’t work for long if itdoesn’t work for the retail customer.Accordingly, researchers measuredretailer satisfaction against three criteria:

■ Partner satisfaction

■ Performance satisfaction and

■ Process satisfaction

“These,” Tom Gruen observes, “arewhat drives overall relationship con-tinuity and commitment to theorganization.”

HAPPILY FOR SMA USERS ON THE CPGSIDE, RETAILER SATISFACTION IS HIGH. “Inessence, the overall satisfaction rat-ing was almost five points on a six-point scale,” Tom Gruen adds.

Sales and marketing agencies areviewed as good partners, since theyand retailers share a common goal:retail sales. Retailers view SMAs asknowledgeable about customerprocesses, with appropriate relation-ships to accomplish necessary tasks.

FORUM82 M I D - F A L L 2 0 0 7 I S S U E

CPG User Perception: CAPABILITY RATINGS of Sales & Marketing Agencies(Ranked by low, medium and high users)

Retail SalesAdministration

HQSelling

CategoryManagement

MarketplaceIntel and

Monitoring

RetailSelling

Retail Supportand

Merchandising

RetailPromotion

Management

6.0

5.0

4.0

2.0

3.0

1.0

0

CAPA

BILI

TY R

ATIN

G (1

=LOW

; 6=H

IGH)

MediumOutsourcers

LowOutsourcers

HighOutsourcers

NEW GMA STUDY: OUTSOURCING SALES &MARKETING

FORUM 83M I D - F A L L 2 0 0 7 I S S U E

SMAs bring efficiency to the overallprocess via their sectional view oncategory improvement and the largeportfolio of products they represent— attributes that enable myriaddecisions through a single point ofcontact.

This helps retailers optimize theirtime for overall sales and merchan-dising management. Retailers canalso provide more inputs to manufac-turers through SMAs, thanks to theportfolio handled by the latter.

SMAS BRING PROXIMITY AND INTIMA-CY TO THE TABLE, retailers indicate,thus facilitating better top-to-topdialog and articulation of retailerstrategy to manufacturers.

At the operational level, retailerfocus is on achieving “sell-through;”

the expertise and efforts of SMAs insupporting sell-through is recog-nized by retailers as very valuable.Retailers also value the field workperformed by SMAs –– store projectexecutions and other related tasks

“Retailers highly value the work thatSMAs do in aligning and marrying themanufacturers’ strategies with theirown plans. They’re viewed as goodimplementors,” Gruen states, addingthat in some parts of the world withlow labor costs, stores are full of staffersconstantly doing whatever is needed:

“But here in the US, retailers justcan’t afford a like level of labor tokeep their shelves reset and filled,and their stores re-merchandised. So,SMAs provide a critical fill-in role.”

It’s a vital function, retailers agree.

“SMAs do some of the real hands-onwork that needs to be done,” saysMark Doiron, Senior Vice president-Merchandising and Distribution forHannaford Brothers.

“But consumer and market knowl-edge is also key. SMAs help us keepa close eye on what’s happening atretail –– trends, sales opportunities,new ways to grow our business.

“We know there are always moreways to grow, more ways to get anadditional item in the basket. ThoseSMA partners who help us drivethese additional sales are those whotruly add value.”

With CPG manufacturers and retail-ers so aligned on this subject, it’s agood bet that outsourcing sales andmarketing will continue to grow. ■

CUSTOMER SATISFACTION: How Happy Are Retailers with SMA Service?(Scoring: 1 = low; 6 = high)

PartnerSatisfaction

ProcessSatisfaction

OverallSatisfaction

PerformanceSatisfaction

Retailer

CPG

4.9

4.6

4.6

5.1

5.2

4.6

4.7

4.3

4.0 6.05.03.02.01.0

SCORE (1=LOW; 6=HIGH)

FORUM84 M I D - F A L L 2 0 0 7 I S S U E

CROSSMARK: ROI-BASED MODELING REVEALS NEW INSIGHTS,ENABLES SUPPLIERS, RETAILERS TO TAILOR SERVICE LEVEL TO NEED

New Services Come to the Fore

er ever has of just what its store con-ditions are in that small a window oftime. So we’re able to understand,say, overall readiness for the fall bak-ing season –– where the stores are interms of their preparedness, whetherdisplays of the relevant product are

up, are the price points correctly reflected.

Now, this kind of detail isn’t needed on every brandat every time of the year. But when you do need it–– during ice cream season, say, if you’re a toppingsmanufacturer –– frequency does matter, and it canbe very valuable.

We’ve also found, as we have measured back towhich activity produces which results, that in fact adisplay is not always a display. That is, while manyCPG companies think that if they can just get adisplay up in the stores, they’ll do well.

But in fact, some stores sell a lot more off of onekind of display, or a display in one location, thanthey do off another. We don’t always know, imme-diately, just why this is, but we do know that, incertain stores, this is how consumers shop.

Again, we know this because we’re in the stores fre-quently and we monitor the scan data. Then, thechallenge is to determine why this is the case in aparticular store. Was it the specific location within a par-ticular aisle? So we pick things up that create morequestions –– but isn’t it great that we now haveinformation to ask those questions?

Answering them, of course, takes good analyticswork –– another thing we have been focusing on.In fact, we now have one CPG company client thatgoes direct –– but has engaged us to provide ana-lytical services. The reason is our knowledge of andinsights into store level; some of our information isnow being used to help better direct this company’sown retail force.

We’re seeing more and more outsourcing in all areasoccurring across the CPG space, even includingR&D and brand marketing. Retailers, too, are begin-

ning to realize they need outside help at store level.

Wal-Mart, for example, has engaged us to do amajor frozen food reset.

This involved some 250,000 man hours in a five-week window –– all at night, so as not to disruptthe shopper. In some cases, this involved resettingas many as 300 freezer doors in a single night.We’d have 12 to 14 people show up at 10 p.m. on aMonday night, and by 6 a.m. Tuesday morning,the store was reset. Again, the process never inter-fered with the shopper.

This not only created value for Wal-Mart, but forevery manufacturer in the planogram.

ALL OF THESE CAPABILITIES REFLECTED AT RETAIL HAVE

SIMILAR IMPLICATIONS FOR HEADQUARTER. Theyenable manufacturer and retailer alike to betterunderstand which stores should have whichplanogram and what kind of retail coverage isneeded. There’s great value in retail coverage ––not only for its own sake, but as a headquarters toolin terms of the information it can generate, andfeed back up to management.

Often, manufacturers and retailers alike think thatretailers know which planograms they have inwhich stores, what the adjacencies are, and whatthe product mix is. But the reality is, things can anddo change fast in the stores, and it’s very difficultfor any retailer to keep up with these. Because we’rein these stores on a regular basis, we have moredata at our disposal. We can, for example, do aspace utilization study that will produce moreinformation than could be obtained any other way.

If used appropriately, for the manufacturer these arefabulous headquarter tools. And for the retailer, theefficiencies are huge: If every manufacturer wentdirect, just think of the number of category man-agers the retailer would have to hire to work withevery manufacturer’s representative.

In short, not only does the manufacturer gainthrough reduced costs, but the retailer gains greatefficiencies as well. ■

Ben Fischer CROSSMARK

■ Continued from page 77

NEW GMA STUDY: OUTSOURCING SALES &MARKETING

FORUM 85M I D - F A L L 2 0 0 7 I S S U E

ONE BIG THING WE’VE BEEN WORKING ON AND DOING

MORE AND MORE OF IS AN ORDER-TO-CASH SOLUTION.We developed this because, for years, we have hada core competency in customer service and trademanagement.

We have expanded our services in this arena becauseour clients were coming to us needing help. Theywere challenged in areas like vendor managedinventory, customer service, EDI processing anddata synchronization. With all the new trade man-agement packages out there, they were spending alot of money to get up to speed on these things.

But because we serve so many clients, we have to beup to speed on everything. So, a lot of people werecoming to us and saying, Can you do this for us?

Basically, what we do encompasses everything fromthe time the order is placed or created (if we’redoing VMI for them), all the way to collecting thecash. Our services include customer service, EDIprocessing, order management, data sync, deduc-tion management, and more.

DEDUCTION MANAGEMENT HAS BEEN HUGE. As we allknow, some clients have looked at their strategicretail customers and decided, We’d like to make thatsales call. But when they started to do that, they sud-denly realized they had been resourcing from us allof their admin services related to that retailer.

So, we have often gotten these back –– deductionmanagement and order processing, for example.Manufacturers realize we can simply be a lot moreefficient than they can be. After all, while they maybe processing 1,000 orders a month, we process100,000 –– and efficiency results from that kind ofvolume. It’s simple math.

IT’S EXCITING FOR ME THAT WE HAVE BUILT SUCH A

GREAT CORE COMPETENCY that we can say to ourclients: Yes! We can make you more efficient.

As for trade promotion management, another high-interest service, we have two processes. Some

clients come to us and say: We don’t want to touch anyof this. Do the whole thing for us, start to finish. Then wehave other clients who say: We want this particular sys-tem, perhaps because they’re running SAP and theywant its trade package or some other package. Butthey don’t want to manage it.

Of course, this requires ongoing communicationwith the client and its sales force. For example,we’re working on a project right now with oneCPG client, and have staffed a position there tomanage trade promotion and deductions on a majorretailer. We are in constant contact with their salesteam; we work with them on a day-to-day basis, weunderstand what deals they’re offering.

In most cases, retailers require contracts to be writ-ten, and so we also do the contracts. That way,we’re right in the loop; we know what is supposedto happen. The benefit to the client: Whether it’s adirect sales team or our sales team, the team can sell.They’re not spending their time doing admin work.

There have also been situations where companiessimply have not had people in given locations to dothis. Because we’re all over the country, maybe theywant the admin support to do the contracts andtrade management, but they want them to be wherea person is located. And because we’re strategicallylocated around the big retailers, we usually have ateam in that city.

SO THAT’S HOW IT HAS GROWN: clients have come tous and said: Will you do this for us? And we have.

Only recently have we started to market it. In thepast year, we have begun to bring a great manyclients onto it, at many different levels. Some wantto outsource their customer service completely, andsave themselves 25 to 50 percent. Others want todo it on a lesser scale, transitioning some smallercustomers while retaining the strategic customer.

The feedback we have been getting is exciting forus –– we have been able improve the customer’sbottom line. ■

ADVANTAGE SALES & MARKETING: ORDER-TO-CASH SERVICESFREE CPG CLIENTS TO FOCUS ON SELLING, RETAILER RELATIONSHIPS

Sonny King, CEO and Sandy Yob, Vice President-Administration

FORUM86 M I D - F A L L 2 0 0 7 I S S U E

Ritchie DavisVice-President of Operations SELLETHICS MARKETING GROUP

AS DR. THOMAS GRUEN AND DR.DANIEL CORSTEN POINTED OUT IN

THEIR STUDY OF OUT-OF-STOCKS,there are many factors that come into play, includ-ing warehouse inventory, accurate store ordering,and proper shelf allocation.

As an industry, we did not have the insight 10 or 15years ago that we have today. If we did, we wouldprobably find that out-of-stocks weren’t as much ofa problem, but inventory carrying costs probablywere a problem.

Cash flow was negatively affected due to excessiveinventory levels. But at least the product made it tothe store and, more than likely, made it to its spoton the shelf because of more full-time stockers.

Since very few retailers had effective measuring sys-tems back then, they didn’t understand the costsassociated with these high shelf availability rates.But here we are today, with out-of-stocks costingmany retailers around $800 a week per store.

This doesn’t include the loss of customer satisfac-tion, considering roughly 31 percent of customersvisit a competitive store to purchase the out-of-stock item. If I were a retailer, I would have to askmyself, What other of my competitors’ items are making theirway into my customer’s basket?!

WITH KNOWLEDGE COMES RESPONSIBILITY. With allof the information at our fingertips our industryshould be able to make great strides towardsimproving service levels throughout the productsales cycle while at the same time provide retailers

with efficient and effective inventory levels. Weknew that as a broker we could not affect every-thing in the product’s cycle but that we could makea very positive difference at the shelf.

With this in mind, we spent the last few yearsdeveloping proprietary software that would notonly help our clients but also help retailers to betterunderstand store conditions.

This year, we placed over 300 laptops in the fieldwith our new software (SellEthics Retail Solutions) andthe results have been outstanding. The mostimpressive component of the software is that aretail associate can put in a retailer’s store number,and only those products authorized for that specificstore are shown on their screen.

Having this feature puts us in a great position asmore and more retailers pursue store specific prod-uct mixes to meet the unique needs of their con-sumers at each individual store.

Our program also allows our retail representativesaccess to display images, planograms, productimages, sales sheets and manufacturer question-naires, so they can more effectively work each storeand educate the retailer and our principals on vari-ous opportunities that exist.

With a click of a button, the retail rep can show astore’s grocery manager or scan analyst all productsthat were out-of-stock, missing a tag, or void alto-gether. With store employees being as busy as theyare, you can imagine how helpful this quick accessis to them.

We have already partnered with retailers to assistthem with improving store conditions on their pri-vate label items. The reporting aspect of the systemgives buyers, category managers, and store ops per-sonnel insight into what is really happening at store

SELLETHICS MARKETING GROUP: PROPRIETARY SOFTWARE SHOWSSTORE CONDITIONS, AUTHORIZED PRODUCT, OUT-OF-STOCKS, MORE

New Services Come to the Fore

FORUM 87M I D - F A L L 2 0 0 7 I S S U E

■ Joel BarhamPresident and Chief Executive OfficerSELLETHICS MARKETING GROUP

[email protected]: (704) 847-4450 ext: 111

■ Ben FischerPresident, Sales [email protected]: (469) 814-1174

■ Robert HillPresident and Chief Operating OfficerACOSTA SALES & MARKETING COMPANY

[email protected]: (904) 296-4281

■ Sonny KingChief Executive OfficerADVANTAGE SALES AND MARKETING

[email protected]: (949) 797-2920

■ Chip O'Hare President and Chief Executive OfficerJOHNSON, O'HARE COMPANY, [email protected]: (978) 663-9000

■ Peter SingerPresident and Chief Executive OfficerTHOMAS, LARGE & SINGER [email protected]: (905) 754-3440

Special thanks from GMA/FPA and the GMA FORUM to the ‘Outsourcing Is In!’ Steering Committee:

level and what needs to be done to better servetheir customer base. This has made a tremendousimpact on our organization as we are better ableto understand on a strategic level where our retailpartners are headed and how we can better servethem through our associates and principals.

The more insight we receive from industry stud-ies like the Comprehensive Guide to Retail Out-of-StockReduction, conducted by the GMA/FMI/NACDS,the more encouragement we receive for the direc-tion we are headed as a company.

Every organization should constantly evaluate theproducts and services they offer to ensure theyare of value to the market.

More and more, we see that manufacturers canbenefit greatly from outsourcing retail services.We want to take it a step further. We want tomake sure that we aren’t just considered a cost-effective option to performing retail services butinstead, the best return on investment. ■

NEW GMA STUDY: OUTSOURCING SALES &MARKETING