Network of California Community College Foundations Webinar – UPMIFA June 30, 2009.

18

Network of California Community College Foundations Webinar – UPMIFA June 30, 2009

-

Upload

brielle-naish -

Category

Documents

-

view

215 -

download

0

Transcript of Network of California Community College Foundations Webinar – UPMIFA June 30, 2009.

Network of California Community College

Foundations

Webinar – UPMIFA

June 30, 2009

Non-Profit Endowments: MasteringStaff Position FAS 117-1

Uniform Law Commission, Uniform Prudent Management of Institutional Funds Act

(“UPMIFA”) and FSP FAS 117-1

Barry C. Hawkins, Shipman & Goodwin LLP, [email protected]

Introduction 1. UPMIFA (2006) Replaces UMIFA (1972)

(which was the law in 48 states) as the primary source of law governing the investment, management and expenditure of donor generated dollars.

2. Economic Impact: A. 1.4 Trillion Dollars in 2004 B. 5.2% of G.D.P. in the U.S. C. Employment Significance D. Types of NPO’s and Endowment Funds

Common Misconceptions 1. Board restricted or quasi-endowment

“This money is set aside for investment and is to be used for the construction of a new library after it reaches $10,000,000.”

2. Pooled investments vs. separate use, restrictions.

3. Creditor reliance, borrowing capacity and insolvency risk. The types of donor restrictions are highly significant to those who read and rely upon the financial reports of any NPO.

Legal Obligations of the Board of an NPO

1. Prudently manage and invest the funds to maximize the return of assets (at least for endowment funds).

2. Spend a portion of “return on investment” for current needs of the NPO and retain the balance in investments to provide for future needs, being mindful of inflation and the long term viability of an endowment fund.

3. Abide by the restrictions imposed by the donors on a separate fund by fund basis.

4. Follow state law (UMIFA/UPMIFA) which supplies standards if not specified by donor.

Examples of Endowment Restrictions

1. “This money should be kept intact and the income from it is for Bowdoin College.”

True endowment – No use restriction 2. “This money should be kept intact and the income from it is for

the purchase of books for the Bowdoin College Library.”True endowment, combined with use restriction

3. “This money should be kept intact for the period of 10 years, during which the income from it should be used only for the purchase of books for the Bowdoin College Library, and thereafter the money may be used for the general use of Bowdoin College.”

Endowment for a term of years, and thereafter the money has no time or use restriction.

Almost any combination is possible in this highly flexible concept of restriction.

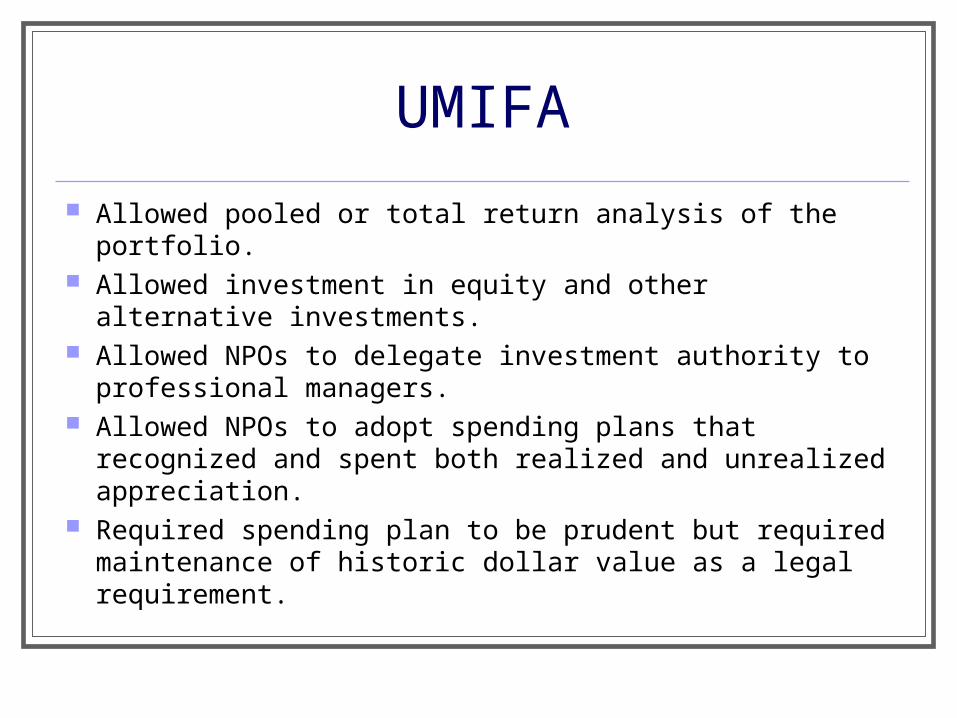

UMIFA

Allowed pooled or total return analysis of the portfolio. Allowed investment in equity and other alternative

investments. Allowed NPOs to delegate investment authority to

professional managers. Allowed NPOs to adopt spending plans that recognized

and spent both realized and unrealized appreciation. Required spending plan to be prudent but required

maintenance of historic dollar value as a legal requirement.

The Creation Process for UPMIFA

1. 2001 Study Committee – Uniform Law Commission 2. The prior adoption of Uniform Prudent Investor Act in 46

states clearly indicated need to extend modern trust standards to NPOs organized as corporations.

3. Drafting Committee 2002-2006 A. Timing B. Process

4. Since July 2006, UPMIFA has been adopted in 35 jurisdictions, a near record pace, with 10 more adoptions in process and expected in the next two months. Six of the remaining eight jurisdictions are likely to have such legislation in 2010, leaving only Pennsylvania and Puerto Rico without UPMIFA. Neither of them ever adopted UMIFA.

The New LawWhat Does UPMIFA Do?

1. Prudence is adopted as the articulated standard for investment management and expenditure. UPIA standards for the trust world are extended to charitable corporations.

2. Elimination of HDV and substitution of multi-faceted prudence standards become the linchpin of legal authorization for endowment expenditures. A prudent spending policy must be adopted by each NPO.

3. Greatly improved standards for modifying or eliminating restrictions imposed by donors, which have become outmoded, wasteful or impracticable.

The Elimination of HDV As A “Bright Line” Restriction

Boards may now adopt spending policies that will go below (invade) HDV if it is prudent to do so.

The Standards to be considered:1. Duration and preservation of endowment fund2. Purposes of the institution and the fund3. General economic conditions4. The possible effect of inflation/depletion5. Expected total return from income and appreciation6. Other resources of the institution7. The investment policy of the institution

The key is to maintain long-term viability and short-term flexibility.

Other Possibilities Within Endowed Spending Authorization.

1. The bracketed 7% presumption of imprudence in Section 4d A. Available if bright line is still desired B. Limited acceptance C. Three-year rolling average determination D. No presumption of prudence below 7%

2. The small fund exception in comments A. under $2 million B. 60 days notification to regulator C. Will they know about the requirement?

Release Or Modification Of Restrictions

What is new? Clearer, more articulated language. Under UMIFA it was

unclear that would happen if a court released a restriction because it was impracticable or wasteful. Under UPMIFA modern cy pres and deviation concepts from trust law are mandated to NPOs.

Section 6(d) allows a new departure for small (less than $25,000), old (more than 20 years) – 60 days prior notice to

charitable regulator.

UPMIFAAccounting Rules And FSP FAS 117-1

1. Section 4A of UPMIFA specifies that unless donor specifically provides to the contrary in the gift instrument, the assets in an endowment fund are donor-restricted assets until they are appropriated for expenditure by the institution.

2. Note: This does not require the institution to determine what portion of the endowment is “permanently restricted,” which is an accounting concept, not a legal requirement.

3. Note: Legally, endowment funds are always restricted, either for time, purpose or for both, and become unrestricted only when appropriated for expenditure by the institution.

UPMIFAAccounting Rules And FSP FAS 117-1 (Cont.)

4. Reconciliation of FSP FAS 117-1 with Sect. 4a of UPMIFA? (a) They apply different concepts (b) The law (enactment of UPMIFA by state statute) trumps

a contrary interpretation by FASB

5. To the extent that FSP FAS 117-1 requires strict adherence to HDV or changing other asset classifications to “restore” HDV level, the two are essentially in conflict and cannot be reconciled.

UPMIFAAccounting Rules And FSP FAS 117-1 (Cont.)

6. What are the options available to a NPO? (a) Contest the FSP FAS 117-1 requirements, by court

action, persuasion or regulatory interpretation (b) Live with FSP FAS 117-1 by acting as though it governs

instead of statutory law and adopt a spending policy which identifies what portion of endowment the NPO believes it is obligated to retain permanently.

(c) Take concerted action to have FASB adopt a new classification scheme for non-profit accounting for endowment funds.

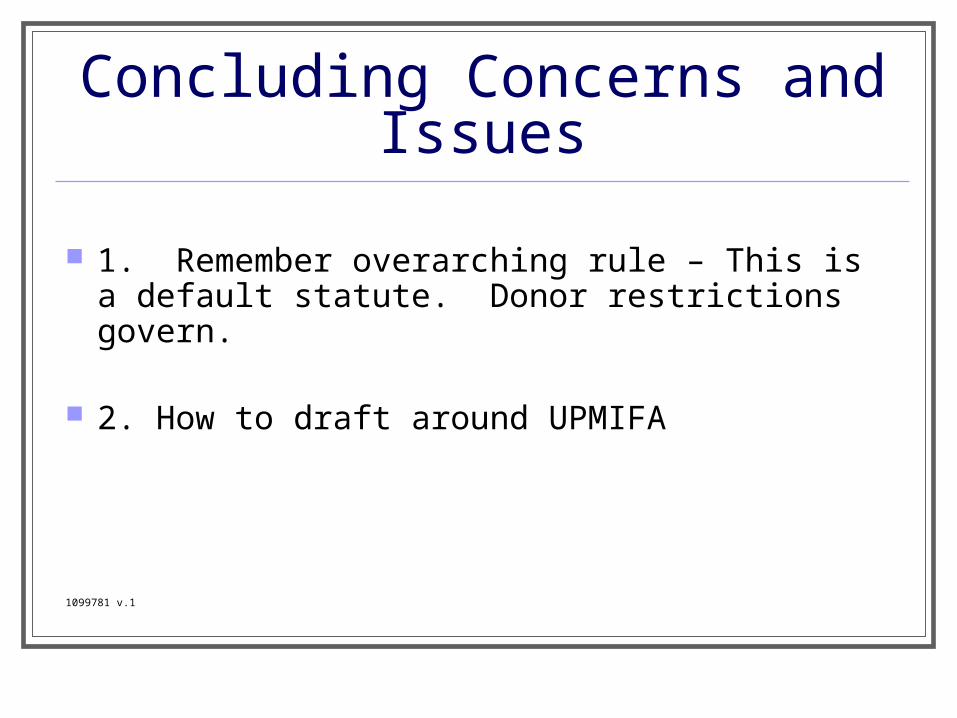

Concluding Concerns and Issues

1. Remember overarching rule – This is a default statute. Donor restrictions govern.

2. How to draft around UPMIFA

1099781 v.1

Network of California Community College

Foundations

Thank you!

Save the Date July 23rd webinar – Raising Money in Challenging Times

9:00am – 10:00amSpeaker: Lawrence Henze, Blackbaud

RSVP today: [email protected]