Netcents Protocol for Inexpensive Znternet Puyments · 2020-04-07 · NetCents Protocol for...

99

Netcents Protocol for Inexpensive Znternet Puyments Tomi J. Poutanen A thesis subrnitted in confonnity with the requirementsfor the degree of Masrers of Applied Science Graduate Deparnent of Electrical and Cornputer Engineering University of Toronto O Copyright by Tomi Poutanen, 1997 1

Transcript of Netcents Protocol for Inexpensive Znternet Puyments · 2020-04-07 · NetCents Protocol for...

Netcents Protocol for Inexpensive

Znternet Puyments

Tomi J. Poutanen

A thesis subrnitted in confonnity with the requirements for the degree of

Masrers of Applied Science

Graduate Deparnent of Electrical and Cornputer Engineering

University of Toronto

O Copyright by Tomi Poutanen, 1997

1

Nationai Library m*m ofCanada Bibliothèque nationale du Canada

Acquisitions and Acquisitions et Bibliographic Services services bibliographiques

395 Wellington Street 395. rue Wellington OüawaON KIAON4 Ottawa ON K I A ON4 Canada Canada

The author has ganted a non- L'auteur a accordé une licence non exclusive licence dowing the exclusive permettant à la National Library of Canada to Bibliothèque nationale du Canada de reproduce, loan, distri'bute or sell reproduire, prêter, distn'buer ou copies of this thesis in microform, vendre des copies de cette thèse sous paper or electronic formats. la forme de microfiche/nlm, de

reproduction sur papier ou sur format électronique.

The author retains ownership of the L'auteur conserve la propriété du copyright in this thesis. Neither the droit d'auteur qui protège cette thèse. thesis nor substantial extracts fiom it Ni la thèse ni des extraits substantiels may be printed or othenvise de celle-ci ne doivent être imprimés .

reproduced without the author's ou autrement reproduits sans son permission. autorisation.

NetCents Protocol for Inexpensive Internet Payments

Tomi J. Poutanen

Masters of Applied Science, 1997

Graduate Department of Elecmcal and Computer Engineering

University of Toronto

NetCents is a lightweight. flexible and secure protocol for electronic commerce over the internet.

It is designed to support purchases ranging in value from a fraction of a penny to several dollars,

with an emphasis on micropayments. It is based on decentralized verifkation of electronic

currency at a vendor's server with offline payment capture and policing. This is accomplished with

floating scrips, or signed containers of electronic currency, that are passed from vendor to vendor.

No custorner trust is required, but the system does place a certain amount of trust in vendors, for

exarnple, to guard against double spending, and therefore requires a probabilistic verification

scheme to limit vendor fraud to unprofitable levels. The protocol can be extended to support fully

anonymous payments. An online arbiter is implemented that will ensure proper delivery of

purchased goods and that can senle most customer/vendor disputes.

Acknowledgements

I offer my sincerest gratitude to Prof. Heather Hinton for her patience, support and vast expertise in

the field and to Prof. Michael Stumm for his inspiration and insight.

A lot of my early work was discussed with Anthony Cheng, who always provided me with valuable

feedback and motivation to punue the concept funher.

Caught In The Web, Inc. granted me access to their equipment in order to conducting my research

and develop the prototype system.

Lastly, to my wife, Susan. who's support and patience never wavered.

Thank you all.

Table of Contents

2.3 Cryptographie F ~ ~ ~ t i ~ n ~ ~ w . w w ~ ~ o ~ ~ w a w w o ~ ~ ~ ~ ~ ~ ~ - - ~ ~ ~ m - - ~ ~ ~ ~ a - ~ - ~ ~ - - ~ ~ w ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ l O

2.3.1 One-Way Funcuons ........... . .............. . .... ...... ............................. ........................... . ...................... 10 2.3.2 Hash Functions .......................................................................... -- ............................................... 1 1

2.3.3 Secret-Key Cryptography ............................................................................................... 1 1

2.3.4 hblicKeyCryptography ....................................................................................................... 12

2.3.5 Digital Signatures ............................................................................ - .......................... - .......... 12 2.3.6 Digital Certificates and Certification Authoritics ..................................................................... 13

2.4 Hybrid Payment Sy~t~m~~..~~~~~~~.~~~..~..~~.~~~~~,,~~~.~~~~~~.~~.~~~~..~---~.~.---~~~~~~~.l3 2.4.1 Account B a ~ d Payment Systems .................................................................................... 13

2-4.2 Encryptul Credit Card Protocois ............................. - . . . . . . . . . . . .......................................... 14

2 Current Electrooic Payment Systems,,,,,-------*~.-.*------15

2 . Online Payment Rotocols ...................................................................... . ................ 16

....................................................................................................................... 2.5.2 Offline Payment Protocols 2 1

2.5.3 MiIlicent ................................................................................................................................................... 27

2.6 Comparative Evaluation of Existing Payment Protocoh- ....w----w.-.,..w..-HII.mmH.. 3 .............................................................................................................................. 2.6.1 Evaluation Criteria 2 8

3 Netcents Protocol .....e................................................................................................................ 31

3.1 Motivation for the Netcents Protocol ..mo.-*.,-..*.mw....~wrn...*.rn.ww..ae..mw......o..w* ....w..a.m.no.w.aJ1

3.2 Overview ~ - . ~ - ~ ~ - - ~ ~ . W 1 ~ I I o ~ - n ~ ~ - ~ w w ~ ~ ~ ~ o w w m r ~ ~ ~ ~ ~ - ~ ~ ~ ~ w o - - ~ - ~ ~ ~ ~ ~ ~ ~ w ~ o m ~ ~ ~ m ~ ~ ~ w w ~ ~ ~ ~ ~ H ~ * ~ ~ ~ * * - H ~ ~ ~ - J l

3 3 Pr0to~01 ~ ~ ~ ~ O H W ~ ~ O ~ O ~ ~ O H ~ ~ ~ ~ W M ~ ~ ~ ~ ~ ~ ~ H H . H ~ ~ ~ ~ ~ O ~ ~ O . H ~ W ~ ~ ~ W ~ ~ H ~ ~ ~ H ~ O ~ H ~ ~ t . ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ O ~ ~ ~ ~ ~

Participants ............................................................................................................................................... 33

.................................................................................................................................... Hierarchy of Trust 34

Cornrnon Data Structures ..................................................................................................................... 3 5

............................................................................................... Customer-Issuing Authori ty Transactions 3 6

............................................................................................................ Customer-Vendor Transactions 3 7

.................................................................................................................. Scrip Relocation Transactions 38

.............................................................................................................. Payment Against Multiple Scrip 40

Policy for Medium and Large Scale Transactions ....... ... .... ... ........ .. . 4 1

................................................................ Vendor-Acquirer-Issuing Authority Offline Batch Processing 41

..................................................................................................................... User to User Fund Transfers 42

.................................................................................................................................... Online Arbitration 42

...................................................................................................... ....................... Anonymous Scrip ... 43

........................................................................................................................................... Blinding Sites 44

........................................................................................................................................ Vendor Policing 45

Vendor Tamperproof Hardware ..................... ..., .................................................................................. 47

................................................................................................................................ Currency Conversion 48

5.3 Vendor ~erver...~.~.........~~~.~

8 Discussion .................................................................................................................................. 61

8.1 The NetCents Protocol As a Universal Internet Payment Scheme ... 61

8.3 Currency Conversion ...................................... -.62

9 Conclusion and Future Work .................................................................................................. 65

................................................................. 9.2 FufUm Work ....- 0.68

....................................................................................................................... 9.2.1 Online Shopping Behavior 68

........................................................................................................................................ 9.2.2 Wide sale tests 68

................................................................................................................................. 9.2.3 Distribution Policies 68

................................................................................................................................. 9.2.4 Scrip fund allotment 69

9.2.5 Explore Other Signature Schemes.. ............. .... ................................................................................ 69

.................................................................................... 9.2.6 Further support for arbitracion. certified delivery 70

9.2.7 Analysis of Tamperprwf Hardware ......................................................................................................... 70

9.2.8 Inregration with SET ........................................................................................................................... 7 1

Appendix B O RSA ............................................................................................................................ 83

List of Figures

Figure 1 : Flow of scnp and electronic payrnent orders in NetCents ................... .... ................. 32

...................... .....................................................-....... Figure 2: NetCents hierarchy of min .... 34

........... Figure 3: Electronic Payrnent Order processing .. .............................................................. 36

Figure 4: Basic Netcents Transaction ..................... .... ....................................................... 37

Figure 5 : Scnp Relocation Transactions .................... .. ................................................................ 38

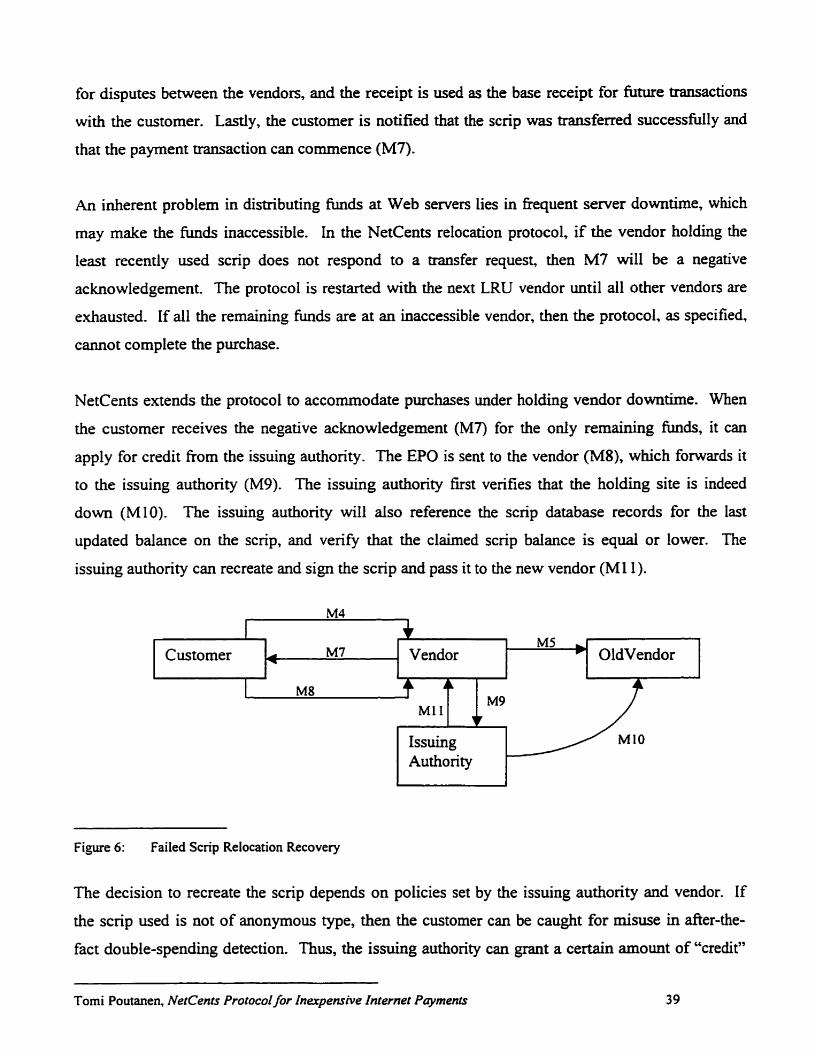

............................................................. Figure 6: Failed Scnp Relocation Recovery ................... .. 39

Figure 7: Offline Payrnent Capture Transactions ....................................................................... 42

........................... ........................................................... Figure 8: Odine Arbiter Transactions .. 43

Figure 9: Purchase of Anonyrnous Cash ......................... .. ........................................................... 44

Figure 10: Average payment latency to the fiequency of requests for various hit rates ................ 59

vii

List of Tables

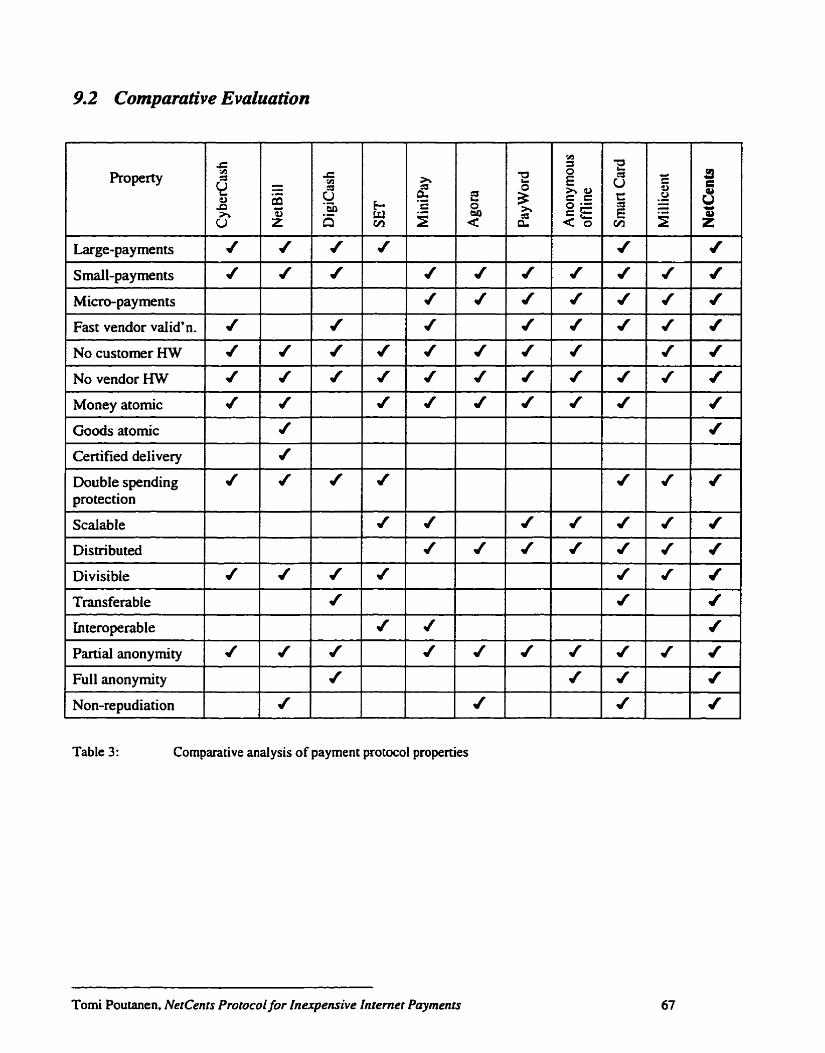

Table 1 : Comparative analysis of payment protocol properties

Table 2: Netcents vendor server performance

Table 3: Comparative analysis of payrnent protocol properties

viii

1 Introduction

I . I Motivation

With the rapid growth of the Internet, there has k e n great expectation of a new marketplace, with

systerns that would facilitate electronic commerce. However, the expectations have greatly

exceeded the reality - no standard electronic currency exists, and profitable Intemet ventures have

been far and between. The concept of physicai, hand carried cash does not lend itself well to the

electronic medium. Electronic currency has the potential to be easily duplicated, forged, or stolen.

Methods of tracing electronic currency infringe on the anonymity of the spender. the anonymity of

the spender, however, ensures the untracability of the currency.

In this work we present a novel protocol that is inexpensive, secure, scalable, and can handle the

societal issues associated with electronic commerce. This research originated from the need of a

universal electronic payment mechanism for the Intemet that meets the security properties of real

world currency as we have corne to expect, and yet remains low cost to dlow micropayments and

scalable to a world wide basis. No current payment scheme meets the above requirements,

typically trading security for cost or vice versa. The difficulty stems from the ease at which

electronic bit patterns can be duplicated. Unlike hard coins and bills, which are protected from

duplication by the cost of the metal and starnping machine or by elaborate watermarking and

holograms, electronic data can be copied and retransmitted readily. A central server is typically

required to validate each transaction and to guard against double spending. This raises the cost of

the protocol, introduces a central bottleneck and a single point of failure, and increases the latency

of a payment. The scalability at a low cost of such systems is questionable, due to the distributed

nature of the Internet,

The Internet presents a new mode1 for commerce that necessitates low per transaction costs.

Automated processes can serve customers with electronic goods and services at a fraction of the

cost of material goods or human services. This insignificant variable cost of sales, and the huge

potential market 0 together will drive individuai prices down to unprecedented levels.

miniscule communication cost, custornized information withdrawal and direct marketing

The

will

-- - - - -- - - - - - - -

Tomi Poutanen, NetCents Protocol for Inexpensive Intenter Payrnents

enable traditional news and entertainment media to be decomposed and sold by section or article.

Individual information requests can be charged for, as is the case for stock quotes. background

information, knowledge base searches, etc.

This research has resulted in a novel payrnent protocol, named NetCents, that is both secure and

low cost, and is scalable to a world-wide reach with multiple currencies, and issuing authorities (or

mints). NetCents is a payment protocol that hnctions offline, without the need to contact a central

server. Thus, the cost and payment latency are kept at check, and scalability is not hindered.

1.2 Electronic Commerce and the htemet

Electronic fund transfers have been around well before the advent of the World Wide Web

0. However, until recently al1 electronic monetary transfers have been of significant value,

and handled via dedicated private networks. At fint, financial institutions used private

communication channels to wire money orders between one another. This quickly expanded to

include large commercial trading partnea, enabling companies to transfer funds amongst

themselves with a bank as an intermediary, and the term electronic commerce was coined.

Electronic commerce was formalized into a set of clearly defined standards, named Electronic Data

Interchange (EDO, which defined typical business transactions such as purchase ordea, invoices,

account balances, etc. [GE97].

Consumers were introduced to the world of cash alternatives in the form of credit cards, and later

debit cards. More recently, prepaid smart car& have started to surface in restricted uses. Smart

cards offer the only low-cost payment solution that scales down to sub-dollar level payments. This

is due to its reliance on the tarnper resistance of the smart card, and thus, a central server need not

be contacted at every transaction. The ability to accommodate low value transactions is of great

importance since in the current US. marketplace, there are many more purchases of value below

$10 than there are transactions of greater value [GS97].

Tomi Poutanen, Netcents Profocof for Inexpensive Interner Payments

Payment mechanisms over the Intemet are at their infancy, and no clear protocol has emerged as

dominant. At stake is a cut in al1 online purchases, which are expected to reach US $6 billion by

the year 2000 [GS97]. Current schemes reflect those of debit card systems, where a cenual bank is

contacted to authonze the payment. Much hope is placed on the recently released Secure

Electronic Transfer (SET) protocol developed by Visa, MasterCard and a consortium of the most

powemil cornputer software and hardware vendon. It aims to enable secure credit card purchases

over the Internet [SET97]. Unfortunately. SET will suffer many of the same costs associated with

the real world use of credit cards; namely, the reliance on available central serves and the cost of

diable and secure communication channels. SET, like credit card payments, does not cover the

full range of payment amounts, and is not suitable for payments below five dollars. An Internet

micropayment system is required to handle payments below those handled by the online debit

based systems or SET. This dissertation deals with an electronic substitute for cash to handle small

to medium valued purchases of electronic content over the Intemet.

I .3 Electronic Payment Protocols Payment mechanisms face an enormous arnount of attention and scrutiny due to the intrinsic

associated value of the transactions. A new payment system will only be accepted if it can be

uusted. To be twted, it needs to be fully documented and open to public scrutiny, much like

current cryptographic protocols. Payment protocols need to be provably secure against attacks.

The security is usually built on top of a cryptographic primitive, and the security will hold as long

as the cryptographic function holds. Security by hidden, unpublicized means or "security by

obscurity" is not suficient and is vulnerable to the vast hacker community.

It is imperative that the protocol is formally specified since it is likely to be irnplemented by a

number of independent software developers. Proper interoperability between independently

developed payment systems is crucial in overall system security, and it is important to clearly

define the required operation in every case. The formal SET specification alone is over 1000 pages

long!

Torni Poutanen, Netcents Protocof for Inexpensive Inrenier Paymenrs

1.4 Micropayment Protocols A rnicropayment refen to a transaction of low monetary value, comparable to a payment with

pocket change. The value of micropayments is typically below one dollar, and ranges down to

fractions of pennies. At the onset of the Intemet, this class of payment protocols received most of

the publicity and research, and it was predicted to revolutionize traditional markets and kick-start

online econornies. The payment protocol that dominated the micro-levei transactions was expected

eventuaily to also dominate the larger valued transactions. It was widely believed that online

content would be sold at extremely low prices at a "per view" cost, such that anyone owning a

homepage could charge a penny for, Say, a poem, or an online magazine could charge per article

read instead of the entire publication. Unfominately, despite al1 the great promise, the field of

micropayments has ken the slowest to materialize, due io the technical dificulties involved in

supporting such a system.

The underiying dificulty in implementation is due to the ease of duplicating electronic bit patterns.

Real coins are protected from duplication by the cost of the metal and the cost of the machinery,

and bills contain hard to produce watermarks, holograrns, etc. However, an electronic coin cm

simply be copied, or retransmitted for future payments, in an assault called double spending. To

guard against double spending, every payment needs to be authorized by the institution that issued

the coin [Ch95, CTS95, BelCo951. This is called an online payment scheme since the issuing bank

is invoived in every transaction. This presents serious scalability, reliability and usability

shortcornings, by introducing a central bottleneck, a single point of failure, and increased payment

latency. It also raises the cost of the transaction, and imposes a minimum cost per transaction, as

the issuing bank is faced with the real cost of authorking each transaction.

Schemes that do not rely on a central semer to guard against double spending are called offline

payment protocols WSh96, HSW96, GaSi96, HeYo961. Typicaily, these protocols are credit

based, since there is no hard protection mechanism to prevent a user from double spending, and

spending more than the balance in their account. Double spending is detected at the time of the

clearing process, when the merchants tum in the received coins to their respective banks. Once

double spending is detected, the malicious user is penalized and expelled. Though offiine protocols

have received a lot of attention from researchers and cryptographers, no offline payment systems

Tomi Pou tanen, Net Cents Protocol for Inexpensive Intemet Payments

exist in the general public use. This is due to the inherent risk of introducing a payment system to

the Intemet where hackers are abundant and wide-scale malicious colluding is easy.

1.5 The Thesis In this thesis we perform an in-depth analysis of existing and proposed payment protocols,

including the much heralded SET standard. W e identify a list of desirable attributes for an online

payment system, and propose a novel payment protocol, dubbed NetCents, that fulfills the

requirements. The motivation for the research was to create a novel payment protocol that is

secure, low cost, distributed and scalable and that works well on the unreliable Internet

communication network. We also wanted it to be anonymous and interoperable across many

financial institutions and various currencies.

We provide a formai specification and a working implementation of the protocol, which correctly

verifies Our performance assumptions. The prototype implementation was also used to analyze the

security and robustness of the system by deliberately attempting to break it. This was

accomplished by attempting to subvert the protocol using compted or deleted messages.

NetCents provides the necessary requirements for an effective online economy: low cost,

scalability, and adequate security, privacy and non-repudiation. Security is based on standard

public key encryption algorithms. It provides the anonymity of cash, yet the buyer can dispute a

purchase effectively to an online arbiter.

The key innovation of NetCents is its use of floating scrips. A floating scrip is a signed container

of electronic cumncy passed from one vendor to another, such that it remains active at only one

vendor at a time. A scrip has a monetary value, or balance, associated with it, dong with a unique

public and private key. Initially the bank assigns a certain balance to the scrip, which is decreased

as the user makes online purchases at various vendors. A vendor accumulates signatures of the

scrip at declining balances, and collects the difference in balance from the bank, by presenting

signed pre-purchase and post-purchase balances of the scrip. For example, presenting a vendor

with two signatures of the scrip at balances of 30 cents and 25 cents constitutes a five cent

Tomi Poutanen, Netcents Protocoi for Inexpensive Intemet Payrnents 5

payment. The vendor locally verifies the signatures to prevent customer fraud, such as double

spending. Since a scnp is active at only one vendor at a time, catching double spending is trivial.

Steps are built into the NetCents protocol to detect vendor fraud, and measures are taken to limit

fraud to unprofitable levels. Vendor fraud control is built into the system and can be demonstrated

not to be profitable. The distributed operation of the protocol removes the bank as a central

bottleneck and single point of failure, and lowers the end-to-end transaction latency.

The NetCents protocol was designed to minimize the operational cost of the protocol. The bank is

only required for offline batch processing and customer services. The vendor overhead of

supporting the payment system is carefully minimized by offloading the majonty of the

computation load onto the purchaser. h the common case, payment verification is reduced to two

modular multiplications. Vendor communication costs are reduced by distributing the scnps in a

LRU fashion, in an attempt to exploit the users' tendency to shop repeatedly at the same locations.

I.6 Outline The next section presents a background to the field of electronic commerce. The section describes

desirable qudities of new payment systems, and formulates a method of evaluating and comparing

various systems. It also presents previously proposed payment protocols in detail, and shows how

these protocols have attempted to rneet the desired goals. Section 4 presents the new payment

protocol, NetCents. The section contains a natural language description of the protocol, complete

with illustrations. Appendix C has the formal specification of the protocol. Section 5 discusses the

secunty properties of the protocol. What sets this thesis apart from most payment protocol

specifications, is that a protocol impiementation was completed in order to test the performance

hypotheses. The developed system is described in section 6. and the performance results are

discussed in section 7. Section 8 discusses the scalability properties of the protocol and outlines a

possible worldwide implementation. Lastly, section 9 has general discussion about micropayments.

followed by the concluding remarks and an outline of future work in section 10.

Tomi Poutanen, NetCents Protocol for Inexpensive Intemet Paymenrs

2 Background and Prior Work

2.1 Fundamental Properties of Money

As researchers develop new electronic forms of money, it is important to keep fundamental

monetary properties in mind. The protocol that provides the most life-like payment mechanism

will have the greatest chance of being accepted by the Intemet population. Ideally, we would like a

system that is as painless to use as is cash in the form of coins and bills.

Coins and bills can be traded between any parties with in physicd contact, quickly and without the

need of expensive verification equiprnent. Coins and bills are divisible clown to the lowest

denomination, or one cent. Divisibility is redized through the use of change to a payrnent, with

different denominations, and is enabled by the ease of tradability of coins.

When cash is exchanged, there is typically limited anonymity. Merchants or observers may be able

to identify the buyer, or will at minimum be able to extract useful demographics such as gender,

race, age, time and location of purchase, etc. Disclosure to third parties is limited in practice by the

relative difficulty of physical (as opposed to data) surveillance. This independent and distributed

disclosure of limited identity with purchases is acceptable, since the transaction records are not

communicated to a central tracking server. A central tracking server would be detrimental to the

privacy requirements of shoppers, and their desire to not disclose their purchasing power.

However, there are a number of negative qualities of cash. Cash is an attractive target for theft

since it can be easily transferred and cannot be tracked in practice. Coins and bills are easily

misplaced and lost. There is the inconvenience of carrying cash, and the effort required to count

coins and bills to satisfy a payment. Interoperability between different currencies is cumbersome,

and requires detrimental exchange rates. Most significantly, there is the real cost of supporting

cash transactions. Not only does the consumer often pay to withdraw money from an automatic

teller, the merchani endures the cost of counting, auditing, storing and depositing the money, as

well as the cost and liability of miscounting money, and the possibility of robbery.

Tomi Poutanen, NetCenfs Protucol for Inexpensive Interner Payments

Alternative forms of money have been introduced to counter some of these deficiencies. These

payment systems include credit cards, debit cards, prepaid smart cards, and travelen' checks. Al1

systems charge the merchant a small fraction of the cost of the transaction. In retum, the merchant

can reduce the liabilities and costs associated with cash transactions, and they can extend their

target market by the easy accessibility to large amounts of money and the built in support for credit.

Unfortunately, credit and debit card transactions are intended for payments above five dollars only,

due to the high per transaction costs [GS97].

In the field of computerized transaction systems, a transaction should have four characteristics:

atomicity, consistency, isolation and durability [GR93]. These four properties are commonly

referred to as the ACID properties. The ACID properties have recently also k e n used evaluate

electronic payment systems [CST95, CHTY961.

Atomicity: A transaction either completes h l l y or not at dl. This is the most important

concept in electronic fund transfers, since Funds should be transferred as a

whole and should not be created or be destroyed.

Consistency: Al1 relevant parties must agree on al1 critical facts of the exchange.

Isolation: Transactions should not interfere with each other, and the result of a set of

overlapping transactions must be equivalent to some sequence of those

transactions executed in non-concurrent serial order.

Durability: Unexpected failures and computer shutdowns will not cormpt the data. The

system should be able to recover to the last consistent state.

J. D. Tygar further subdivided the definition of atomicity in the context of electronic commerce to

include the delivery of purchased goods as part of the evaluation of a payment transaction [Ty96].

This is especiaily relevant in the realm of Internet commerce, where communication channels are

not reliable. Certified delivery of electronic goods parallels the rise of a multi-billion dollar

industry in iracked, receipted couner delivery of documents and packages.

Tomi Poutanen, Netcents Protocol for Inexpensive Intemet Payments

Money atomicity:

Goods atomicity:

Cerüfkd delivery:

Transactions that feature atomic transfers of money are said to be

money atomic. The transaction either completes fully or not at dl. and

no money is created or destroyed.

Goods atomic transactions are money atomic and also ensure that the

consumer will receive goods if and only if the merchant is paid.

Goods atomic transactions provide an atomic swap of the electronic

goods and funds - sirnilar to the effect of the "cash on delivery"

parcels.

Protocols that are goods atomic and also allow the consumer and

merchant to prove exactly what was delivered satisfy certified delivery

requirements. If there is a dispute, this evidence can be shown to a

iudple to prove exactly what goods were delivered.

Using the above classification scheme and the desired monetary properties. we will compare

existing payment systems (section 3), and demonstrate the power of the proposed NetCents

protocol.

2.2 Government ReguIQfions on Payment Systems

Most countries have a long history of banking and credit agency laws that are set up to protect the

financial security of the consumer. Special rules are also defined to accommodate government

police and tax agencies, in order to detect embeulement, money laundering or tax evasion. The

laws have been defined for traditional payment mediums, such as electronic hinds transfers and

credit card transaction, and have not yet k e n modified to accommodate payments over the Intemet.

The following is a compendium of relevant American rules and regulations that apply when

designing an internet payment mechanism (Canadian laws are not as developed and restrictive as

the Amencan ones, but in order for a payment system to succeed acceptance by the Amencan

regulators is a must).

Tomi Poutanen, NetCents Protocol for Inexpensive Internet Paymenrs

Provide detailed transaction information at consumer's request (subpoena 12 USC

1829. Bank Secrecy Act) or to law enforcement (under subpoena 12 USC 3403.

Financial Privacy Act).

Store records of al1 transactions above $100 for a minimum of five years (12 USC

1829, Money Laundering Act).

Report d l transactions above $3000 to the govemment (12 USC 1829, Money

Laundenng Act).

Any currency system which is accessed by a card or similar device must protect the

consumer against fraud by assuming al1 losses over $50 resulting from the ioss of this

device (1 5 USC 1693, 12 USC 3403).

Regulation E is the rule goveming electronic fun& transfen, and is required by ail

credit issuing agencies, and it may well be enforced over the Intemet. It is intended as

a consumer protection rule to help guard against losing money €rom erron or fraud in

electronic fun& transfers. It requires written advance authorization for arrangements

to move money electronically. written receipts for every transfer, a written periodic

statement, giving the consumer the right to challenge any electronic funds transfer for a

period of 30 days from when they get the statement. Financial institutions have a duty

to investigate any challenges and respond within a short time (usually 10 days).

2.3 Cryptographie Functions We briefly outline some cryptographic primitives required for the understanding of current

payment protocols.

2.3.1 One-Way Functions One way functions form the basis of al1 cryptographic operations. and indicate a mathematical

operation that is easy to calculzts in one direction but hard to reverse. An example of a one way

function is the multiplication of two large primes. The product can easily be calculated but the

factors of the product are very hard to deduce. RSA public key encryption attains its secunty from

this specific one-way function [RSA79].

Tomi Poutanen, Netcents Protocol for Inexpensive Interner Payments

2.3.2 Hash Functions

A hash function is a one way operation that maps a variable length bit string into a fixed-length

value called the message digest. Traditional examples of hash functions are the check sum and

CRC32 operations. A gwd one-way, cryptographie hash hinction, H, has the foilowing three

qualities:

Given message M. it is easy to computer the hash, h. where h = H(M).

Given h, it is hard to cornpute an M such that H(M) = h.

Given MT it is hard to find another message, MT, such that H(M') = H(M)

Hash functions work by repeatedly applying one-way functions over the input data Stream. A

message digest is a value generated for a message (or document) that is unique to that message. It

is used to verify that the message has not been aitered. A cryptographically secure hash function,

as described above, certifies that the message digest cm only be produced if and only if the entire

message is known. Thus, the knowledge of a secret cm be communicated as a message digest

without revealing the secret itself. Two prominent hash functions have emerged as

cryptographically secure: MD5 [Ri921 and SHA [SHS93], with output Iengths of 128 and 160 bits

respectively. As a rough guide, hash operations are in the order of 10,000 times faster than RSA

public key encryption operations [RiSh96].

2.3.3 Secret-Key Cryptography

Secret-key cryptography, also known as symmetric cryptography, uses the sarne key to encrypt and

decrypt the message. Therefore, the sender and the recipient of a message must share a secret,

namely the key. A well known secret-key cryptography algorithm is the Data Encryption Standard

(DES). Symmetnc key cryptography is significantly faster than public key encryption or

decryption [Shi96]. Thus, long messages are typically encrypted by a symmetric key, which, in

Nrn, is encrypted using a public key operation.

Tomi Poutanen, NerCents Protocol for Inexpensive Internet Payrnents

2.3 -4 Public Key Cryptography Public-key cryptography uses two keys: one key to encrypt the message and the other key to

decrypt the message. The two keys are mathematically related so that data encrypted with either

key can only be decrypted using the other. These two keys are referred to as the key-pair, and

comprise of a public key and a pn'vare key. The user distributes the public key and keeps the

private key secret. Because of the relationship between the two keys, a message encrypted with

either one of the key pairs can only be decrypted with the other key. The public key is used to

transmit a message to a user, with the assurance that only the owner of the private key (or the user)

cm decode the message. The private key is used to decode received messages and to sign message

digests to prove the authenticity and source of a message or data file. This assurance is only

maintained if the user ensures that the private key is not disclosed to anyone else. The best known

public-key cryptography algorithm is USA (narned after its inventors Rivest, Shamir, and Adleman)

[RSA79].

2.3.5 Digital Signatures When combined with message digests. encryption using the pnvate key allows users to digitally

sign messages. When the digest of a message is encrypted using the sender's pnvate key and

appended to the original message, the result is known as the digital signature of the message.

Recipient of the digital signature c m be sure that the message really came from the sender. in trust

of the security in the two one-way functions. And, because changing even one character in the

message changes the message digest in an unpredictable way, the recipient can be sure that the

message was not changed after the message digest was generated.

In many applications, a signature is created only once, but the signature is verified repeatedly.

Such applications include the signature on digital certificates, or on downloaded software

components such as ActiveX controls. In a payment scheme it is also desirable to distribute the

computational burden to the buyers in an effort to minirnize the server load. In an RSA encryption

environment, this cm be accomplished by using srnail values as the public key exponent, such as 3,

17, or 65537, which take only 2, 5 and 17 rnodular multiplications respectively to exponentiate in

Tomi Poutanen, Netcents Prorocol for Inexpertsive Internez Payments

order to verify the authenticity of a signature [Shi96]. As a rough guide, signaiure verifcation is

about 100 times faster than signature generation WSh961.

2.3 .6 Digital Certificates and Certification Authorities Key distribution and hierarchy of trust are integral issues faced with secure, distributed system

designers. In a scalable environment, new secure communication channels are constantly created,

and new relationships between entities are constantly initiated. It is infeasible to trust every

identity at al1 times. Mead, a hierarchy of trust is used where trusted parties, called certification

authonties, sign facts about memben, such as name, IP address, public key, etc., into one

unforgeable digital certiticate. The certification authority is expected to perfom sufficient due

diligence on its client before signing the certificate. The public key c m be used to initiate a secure

communication channel, and to authenticate a signature.

2.4 H y W Payment Systems Hybnd Intemet payment systems, are transaction schemes that rely on traditional payment means to

facilitate online purchases.

2.4.1 Account Based Payment Systems The fiat instance of electronic commerce and online purchases came in the means of account based

systems. In account based systems, the user registea with a site, such as an online journal like

Wall Street Journal Interactive (wsj.com), and pays for an account using traditional means, such as

a postal mailed cheque, or a telephone cal1 to provide a credit card number. The account can serve

as a subscnption to a web site with prepaid access, or as a debit account for future purchases.

Amenca Online (AOL) has k e n using account based purchasing schemes even before the advent

of the m. AOL would track user purchases within the AOL framework and bill the member as

part of the monthly online charges.

Tomi Poutanen, NetCents Protocof for Inexpensive Interner Payments

With account based systems, no credit card numben are passed over the Intemet, and the cost of a

transaction is aggregated into a number of smaller transactions. This mechanism. however, has

serious drawbacks. This system does not lend itself to spur-of-the-moment purchases at distributed

Intemet content providen, due to cost and time involved in seaing up a customer-vendor

relationship. Due to the cost of setting up an account and the cost of the credit card transaction,

single, sub-dollar level purchases are completely infeasible, unless the cost of the payment cm be

aggregated over several future purchases. Another limitation is the lack of trust and arbitration:

there is no formal policing of prornised service for each account based site. Once the customer

deposits money into an account, they will have a difficult time withdrawing their balance.

2.4.2 Encrypted Credit Card Protocols As the Intemet matured and the use of encryption became cornmonplace, a number of companies

began offering online credit card purchasing systems. The idea was to transfer the credit card

number to the vendor in an encrypted form. and build a mechanism for the vendor to contact the

acquirer for authorization, and later clearing. Enabling technologies included SSL encryption

[Shi971 between the customer and vendor. vendor storefront applications with shopping baskets,

such as Net.Commerce, Merchant Server, Open Market or VenFone, and a gateway to traditional

credit card clearing systems, such as vPOS (virtual Point Of Sale terminal from VeriFone).

Again, per transaction costs imposed by current credit card systems prevent low valued

transactions. The usability of the system is hindered by the cumbersome need to key in the credit

card number and expiry date. This also opened the possibility of Trojan sites [TW96] that spoof

customers into thinking they are at a legitimate site by mimicking the content and URL as close as

possible. The most detrimental aspect of this mechanisrn is the accumulation of credit card

numbers by vendors. This database of valid credit card numbers is easily stolen by anyone who

could crack into the server, a frighteningly common occurrence.

Tomi Poutanen, Netcents Protocol for Inexpensive Internet Payrnents

2.5 Current Electronic Payment Systems In this section we describe the previous work in electronic commerce protocols and micro-payment

based protocols. We highlight the significant systems and efforts to date and describe the relevant

issues and mechanisms used in payrnent protocol design and implementation.

Payment protocols that are exclusively designed for electronic payments in a normal consumer to

merchant transaction can be categorized as either online or offline protocols. In an online protocol

a central payrnent authority is contacted to authorize the transaction. In an offline protocol, the

merchant verifies the payrnent using cryptographie techniques, and commits the payment to the

payrnent authority at a later time, such as late at night, in a batch process.

In general, online systems, if designed and implemented properly, secure the merchant and the

bank against customer fraud, since every payment is approved by the customer's bank. Customen,

however, may counter theft or loss of their electronic money, and rnay be cheated by merchants via

misrepresentation of goods or failed delivery. Typical national banking laws protect the customer

from fraud, and the credit agency or the issuing banking authonty is responsible for the cost of the

fraud.

However, an online authorkation system is expensive due to the necessity of a highly available and

responsive clearing system at the issuing authority. Offline systems were designed to lower the

cost of a transaction by delaying the clearing to a batch process. Offline systerns, however, suffer

from the ease at which electronic currency can be duplicated and spent repeatedly, termed double

spending. Thus, offline protocols concentrate on detecting and lirniting fraud, and in catching the

fraudulent Party. As a result, offline payrnent protocols are generally suitable for low value

transactions where accountability d e r the fact is sufficient to deter abuse. Online payrnent,

however, remains necessary for transactions that require prior restraint against pesons spending

beyond their available funds.

Tomi Poutanen. NerCenrs Protocol for lnexpensive internet Payments

2.5.1 Online Payment Protocols

2.5.1.1 CyberCash

CyberCash (h~~lwww.cvbercash.com~ is the North American de facto standard for low-value

transaction electronic payments. CyberCash is also based on one of the most basic forms of

payment protocol: A payment is made by a client signing a iransfer request (of a fixed monetary

value) to the merchant. The rnerchant submits this signed request to the bank for authorization of

payment. Depending on the availability of fun& in the buyer's account, the bank will reply to the

merchant with a signed authorization or refusal.

The scalability of the CyberCash protocol is doubtful since it relies on the availability of a single

online bank, and only supports one currency per wallet. CyberCash, in its present fom, is not

goods atomic. It does not provide the mechanisms for dispute resolution by an independent online

arbiter. Furthermore, the protocol is not anonyrnous in nature, allowing the issuing bank to track

every purchase. Most significantly, however, CyberCash is not cheap. The systern restricts

payments to a minimum of 25 cents, for which arnount it charges the merchant an authorization fee

of 8 cents (or 32 percent). Although this fraction diminishes as the value of the transaction

increases, it still makes the cost of the protocol relatively expensive for sub-dollar payments.

Despite the numerous deficiencies and the high cost of the protocol, CyberCash has established

itself as the standard small-valued, online payment vehicle in North America by aggressive

marketing and the formation of strategic alliances. It is accepted in a number of high-volume, big-

ticket sites such as espn.com, wsj.com, and the Internet NewsStand. Despite its comparative

success, CyberCash reported less than $70,000 in revenue frorn its online payment scheme in Q1

1997. This bleak financial performance signifies the lack of acceptance of online electronic

payment protocols to date.

2.5.1.2 NetBill

Carnegie Mellon researchers Cox, Tygar and Sirbu defined a payrnent system. NetBill [ n S 9 5 ] ,

that fulfills the goods atomic payment requirements. NetBiil also adds signed pnce quotes and

sales agreements. which can later be used by an arbiter to resolve disputes. The protocol is based

- -

Tomi Poutanen, NetCents Protocol for Inexpensive intemet Payments

on Kerberos [SNS88] tickets to authenticate users and to provide credentials such as age or a

membership that may make her eligible for a discount. The key contribution of NetBill is its

certified gwds delivery mechanism. In the protocol, the goods are delivered to the buyer in

encrypted format as part of the payment negotiation format Only once the goods have been hilly

delivered will the client software sign and send the electronic payment order (EPO) to the

merchant. The merchant, in mm, forwards the EPO to the NetBill server. dong with the key to

unlock the encrypted goods. The NetBill server will authenticate the purchase against the buyer's

account. and reply with a confirmation to the merchant. As the final step in the protocol, the

merchant provides the buyer with the key to unlock the go&. Failing to do so, the buyer can

retrieve the key from the bank. By combining the payment clearing process with the delivery of the

purchased goods' decryption keys to the bank, the protocol ensures that the buyer will only be

charged if she can retrieve the keys to unlock the goods, regardless of communication failure with

the merchant. The delivery of goods is cerùfied as long as the buyer can communicate with either

the merchant or the bank.

The drawback of the certified delivery protocol is the addition of extra messages, and the

significant increase in the amount of encryption used. Although the protocol is useful for single

download applications, such as downloads of files or single news articles, it is not suitable for many

Intemet applications, such as access to the entire site, Iive feeds and interactive applications. and

downloads of time-sensitive information. Furthemore, encrypting the entire Web page and its

multimedia elements in one packet will strip the Web browser of its progressive rendering

capabilities.

In early 1997, CyberCash announced that it had licensed the NetBill certified delivery mechanism

to be incorporated into its CyberCarh and CyberCoin payment system.

2.5.13 DigiCash

Introduced in 1995 by Danish cryptographer and privacy advocate David Chaum, DigiCash was the

first functioning Intemet payment system [Ch95]. The major differentiator to DigiCash is its

completely anonymous nature, which is accomplished via the use of blind signatures [Ch821 (see

Appendix C). DigiCash lets the user create coins which the bank signs using the blinded signature

Tomi Poutanen, Netcents Protocol for Inexpensive Interner Payments 17

algorithm. The bank must accept coins that it has signed, and its main online function is to guard

against double spending.

Although DigiCash is cryptographically sound, it lacks the sophistication required of a scaleable.

worldwide payment system. DigiCash requires a centralized server to validate payments, which

creates a central boaleneck. Fiaws in the DigiCash protocol have been shown io lead to an

inconsistent state violating the money atomic definition [CST95]. If transfer of DigiCash tokens

from customer to merchant is interrupted then it is possible that both or neither party may believe

that it has legitimate access to the tokens. The protocol is also not goods-atomic, nor do the

messages support non-repudiation to support an online arbiter.

The use of cryptographic coins also presents a problem. To validate a payment, a bank must

perform public key operations for every coin submitted. and must search through al1 previously

validated coins for double spending. For exarnple, a payment of 4 cents would arnount to 4 public

key operations and searches. Thus, the protocol is significantly more expensive to support than

CyberCash.

There is also the issue of possessing the correct change for a purchase. Only a bank can issue

change, and thus may need to be contacted by the custorner prior to a transaction. This further

complicates the protocol and introduces points of failure, latency and cost to a transaction.

The initial enthusiasm gmered by the system at its infancy has mostly tampered off, and the

system has not been able to attract big-ticket, high volume merchants. The fact that DigiCash is not

based in North America has, undoubtedly, played a significant part in its struggles to gain

acceptance. North Amencan users have complained about intolerably long transaction latency and

low reliability as the central semer is contacted to authorize the payment. On the other hand,

DigiCash seems to be surviving in Europe where it has announced strategic partnerships with a

number of European banks in order to locdize into different currencies.

Torni Poutanen. NerCents Prorocol for Inexpensive Internet Paymenrs

25.1.4 SET - Secure Eiectronic Transfer

The much-heralded protocol for enabling secure credit card transactions over the Intemet has at last

k e n finalized as the SET 1.0 standard [SET97], and is only now seeing wide scale field testing

before public rollout. It was devised by a large industry consortium and charnpioned by Visa and

Mastercard, who saw the need for a solid extension to the Intemet before an alternate payment

scheme becarne the de-facto standard. The protocol replaces the failed attempts of the STT

[SïT96] protocol defined by Visa and Microsoft. We will borrow much of the vocabulary used by

SET and credit card systems. The customer's credit card is issued by an issuing authoriîy, or

simply an issuer. Many different issuen can supply the same brand of credit card. The vendor

collects credit card numbers and signatures, and contacts his credit card payment agency, the

acquirer, for authorization of the payment. The acquirer, in tum, contact's the credit card holder's

issuing authority via a secure, private network, called an interchange network, to clear the payment

and to transfer funds.

What sets SET apart from other online payment schemes is its secunty, scalability and robust

design. The protocol is based on the RSA encryption protocol and utilizes 1024 bit public keys,

and a 2048 bit root key. The trust relationship is hierarchicai, al1 stemming from one root key.

This enables multiple certification authorities, issuing authorities, and acquiren (merchant payment

agencies), facilitating wide scalability.

Unlike the original STï specification and the many predating credit card payment protocols, the

SET protocol is completely removed from any association with credit card numbers. Instead it is

merely an extension to the card issuer's services, and functions much like other online protocols do.

Where it differs from the normal online message passing sequence, is that the merchant's acquirer

uses traditional pnvate networks to contact the buyer's issuing authority to authorize the payment.

Though proven through years of service in the existing credit card infrastructure, these interchange

networks add a real per transaction cost. Currently interchange network service companies charge

between 5 to 10 cents [GS97] for timely and secure message passing between acquirers and issuen,

whether it be a credit card or a debit card transaction.

Tomi Poutanen, NetCents Protocof for Inexpensive Interner Payments

SET introduces a new application of digital signatures, narnely the concept of dual signatures. A

dual signature is generated by creating the message digest of two messages, concatenating the

digests together, computing the message digest of the result and encrypting this digest with the

signer's private signature key. The signer must include the message digest of the other message in

order for the recipient to verify the dual signature. A recipient of either message cm check its

authenticity by generating the message digest on its copy of the message, concatenating it with the

message digest of the other message (as provided by the sender) and computing the message digest

of the result. If the newly generated digest matches the decrypted dual signature. the recipient can

trust the authenticity of the message.

Within SET, dual signatures are used to link an order message sent to the merchant with the

payment instructions containing account information sent to the acquirer. When the merchant

sen& an authorization request to the acquirer, it includes the payment instructions sent to it by the

cardholder and the message digest of the order information. The acquirer uses the message digest

from the merchant and cornputes the message digest of the payment instructions to check the dual

signature. The dual signature is used to blind the merchant from any account and payrnent

instructions sent as part of the payment.

SET is not a lightweight protocol. Cryptographie functions are readily used, in terms of setting up

a secure channel, verifying certificates and signing messages. In total, up to a dozen public key

operations can transpire to authorize one transaction. This adds payment latency and further drives

up the per transaction cost. Coupled with the interchange network charges and the risk based cost

of maintaining a credit account, then the cost of SET payments will make sub dollar valued

transactions unfeasible.

SET was obviously designed with emphasis on security, and it lacks many of the desirable features

of other, far simpler payment protocols. SET, like real world credit card payrnent systems, does not

provide for user anonymity against the issuer. SET does not provide non-repudiation [SET97], and

does not have certified delivery of purchased goods. It would seem that SET was designed with

traditionai purchases in rnind such as cataiog sales, where a couner Company certifies the delivery

of goods.

Tomi Poutanen. NerCenrs Protocol for Inexpensive hternet Payments

2.5 -2 Offline Payment Protocols

2.5.2.1 Mini-Pay

Though IBM is heavily involved with SET, it concedes that SET is not suitable for micro-

payments. Thus, they have proposed a low-cost, offline payment scheme narned Mini-Pay

[HeYo96]. A Mini-Pay user requests a daily signed certificate containing the user's issuing

authority, her public key, and her offline purchasing limit. The offline limit is the maximal amount

of purchases per day that the buyer c m do, before an online confirmation for the issuing authority

is required.

The buyer makes a purchase by signing a Mini-Pay payment order. If the total arnount of

purchases for the day is lower that the offline lirnit, then the purchase is fulfilled instantly.

Othenvise, the issuing authority is contacted to authonze the payment and issue a new offline limit.

At fixed periods, the seller would aggregate al1 the payment orders received frorn al1 buyers. and

would send thern as a single, signed deposit message to his online financial institution for clearing.

In al1 offline systems, this clearing period is typically set at low-load periods, such as laie at night,

in order to minirnize the communication cost and computational impact on the rest of the system.

An offline clearing process greatly reduces the costs of implementing and running a bank, since this

relaxes the high availability, and fast responsiveness requirements.

2.5.2-2 Agora

Independently developed from Mini-Pay, Agora is a closely sirnilar offline payment protocol

developed at the Bell Laboratones [GaSi96J. Agora extends the simple Mini-Pay system by adding

an enhanced fraud protection protocol, oniine arbitration and user ID revocation. Fraud control is

introduced by requesting online authorization from the buyer's issuing authority when the buyer

exceeds an offline credit limit (as in Mini-Pay) and at some low random probability. The random

probability mirron the purchasing rate of the consumer. The bank will revoke a customer ID when

the customer either exceeds her credit limit, or when the purchasing rate exceeds some preset rate.

This restriction is imposed due to the belief that a thief would go on an electronic shopping spree

Tomi Poutanen, Net Cents Protocol for Inexpensive Interner Payments 2 1

with a stolen wallet. Revocation is accomplished by a broadcast of the customer ID to dl of the

merchants in the system.

Online arbitration is necessary aven the current lack of stability within the Internet. If the buyer

fails to receive the purchased goods, then an online arbiter is contacted with a signed item price

with a hash, and the corresponding signed purchase order. The arbiter verifies the signatures and

contacts the merchant. The merchant is obliged to resend the item to the arbiter. Failing to do so

will cause the arbiter to repudiate the transaction by sending the bank a copy of the signed purchase

order. Unfominately, adding non-repudiation adds the extra computation overhead of two costly

public key operations for the merchant.

A clairn to fame for both Agora and Mini-Pay is the minimal cost when measured in terms of

communication overhead. When the online bank is not contacted for authorization, then the

protocols can be hilly piggybacked on typical HTTP-Get request and reply messages (four

messages in total). The authors of Agora, in particular, argue that the cost of a payment protocol

should be measured in the number of messages more than in computational complexity.

Although both protocols are certainly low-cost, they have major shortcomings based on the

customer's ability to double spend. Online issuing authorities will need to perform a rigid due

diligence of the users before signing them on, such as is done by credit card cornpanies or by

financial institutions. This need increases initialization costs and reduces competition in willing

issuing authorities, thus ultimately driving up the cost of the system. There is also the question of

who pays in case of fraud. In Mini-Pay, the merchant will not receive payment, in Agora it is not

specified. Either way, a high level of fraud will drive up the cost of the system. Furthermore, there

is also the real possibility of theft of the customer wallet. In case of credit card theft, the issuing

authority is required to pay for dl of the fraud according to law, a law that would likely be

extended to cover online purchases.

Tomi Poutanen, NetCenrs Protocol for Inexpensive Interner Payments

Neither protocol is fully anonymous, due to the after-the-fact policing requirements. Thus, the

bank is able to collect a complete purchasing profile of their customers - a highly undesirable

characteristic of online micro-payment level purchases.

Even when a customer is found to double spend, how do you stop hem? Mini-Pay requires a daily,

signed certificate from the issuing authority. Thus, the criminal is free to spend at their hearts

content for one fidl day. Agora atternpts to correct this problem by implementing a revocation

protocol. However, the revocation aigorithm has real scalability problems. In a worldwide

implementation with millions of online merchants, how do you broadcast revocation messages to

al1 of them in a timely fashion? The criminal may still attempt to make several additional

purchases before the revocation message is received from the bank. Furthermore, imposing a

probabilistic purchasing rate notification scheme is dangerous. By bad chance, a customer making

several purchases within a short penod of time may have al1 of her purchases relayed to the bank,

and will quickly exceed her allowed purchasing rate. This, in mm, would tngger the massive

revocation broadcast. The probabilistic purchasing rate notification scheme aside, a preset offline

credit limit makes it possible for a criminal to double spend up to the offline limit at each and every

merchant on the system.

The above faults in offline payment systems make them only suitable for low-cost, non-tangible

electronic content with no barter value. It is especially hard to implement online lottery or

garnbling sites, software downloads, or shipped goods delivery. Content such as pay news sites,

online stock quotes and games, however, are suitable. It cm be argued that an online pay site does

not lose any revenue from criminal use of the payrnent protocol. since the cost of providing the

service is negligible. Chances are that the criminal would not have paid for the service anyway.

However, if the fraudulent use is abundant, then there is a reai cost of the protocol above the per

transaction costs imposed by the payment system.

2.522 PayWord, micro-iKP and Mlprp

The lightest payment protocols are not based on public key cryptography due to its inherent

computational cost. Payrnent systems like PayWord [RiSh96], Micro Payment Transfer Protocol

(MPTP) [HalB95] and micro-LW mSW96] are al1 based on the repeated use of one way functions.

Tomi Poutanen, NetCents Protocol for Inexpensive Intemet Payments

Like Agora and MiniPay, these protocols do not protect against double spending at different

merchants. The merchants merely venfy the validity of the coins, and the issuing authonty will

detect double spending at the time of the offiine clearing.

The three protocols are built on the concept of chains of cryptographie hashes, similar to MD5

[Riv92]. A hash chah consists of a randorn seed, X, and a set of coins, where co = X, ci = hâsh(ci_

,). The buyer initiates a set of transactions with a merchant by presenting a signed tuple (v, n, c,),

where n is the number of coins the user agent expects to spend at the merchant, and v is the vendor.

The vendor identifier, v, is included in the purchase order, in order to prevent malicious framing by

a vendor by simply spending the sarne coin at more than one other vendor in a double spending

attack. The coins are presented in descending order. For example, a payment of three coins (or

three cents) is accomplished by simply presenting the merchant with c,3. The merchant verifies

that c, = ha~h(hash(hash(c,.~ ))), which is computationally simple. The process is repeated for

future payments until n is exhausted. This process arnortizes the cost of one public key signature

verification over multiple payments, and substitutes the comparatively inexpensive hash function

for repeated purchases. The secunty lies in the difficulty of reversing the one way hash function,

and only the buyer can determine the proper payrnent bit-strings.

The micro-iKP actually signs each individual payment with a "highly efficient but specialized

signature scheme", in order to provide non-repudiation of payments. Details of the specialized

signature scheme are not given, and a normal signature scheme would increase the cost of the

system to the level of other offline payment schemes. PayWord and MPTP do not support non-

repudiation, and none of the three protocols are fully anonymous.

MicroMint is an extension to PayWord [RiSh96] that completely eliminates public key

cryptography. It bas lower security but even higher speed. A coin in MicroMint is a bit-string

whose validity can be checked by anyone, but which is hard to produce. The coins are represented

by k-way hash-function collisions. a computationally difficult problem to solve, but once solved,

cm produce many subsequent coins repeatedly. Just as for a red mint, a

scale" allows him to produce large quantities of such coins at very low cost

scale forgery attempts cm only produce coins at a cost exceeding their vaiue.

broker's "economy of

per coin, while small-

However, MicroMint

Tomi Poutanen. Netcents Prorocol for Inexpensive Interner Payments

suffea from the lack of trust in new cryptographic primitives, and in the lack of non-repudiation.

The lack of non-repudiation is especially troublesome for an offline scheme, as it leaves open the

possibility of purely malicious framing. Stolen coins or coins received as payment can be reissued

repeatedly. Thus, a broker cannot legally prove who is guilty of duplicating coins and will not be

able to pursue a cheater in court, but can only drop a suspected cheater from its system. Whether

such a system can operate in practice remains to be seen, and would seem to be highly risky in

nature.

25.23 Anoaymous Oftliae Payment Schemes

DigiCash Internet payment system demonstrated a relatively simple anonymous online protocol

using blind signatures. However, it requires every spent coin to be authorized by the issuing

authority that guards against double spending of coins. OMine protocols require after-the-fact

detection of double spending, and thus must be able to identify double spenders in order to penalize

them accordingly. Chaum et al introduced a remarkable offline payment protocoi which is

anonymous, yet allows the bank to detect and trace a "repeat spender" [CFN88]. If a customer uses

a coin only once, then her privacy is protected unconditionally. But if she reuses a coin, the bank

c m trace it to her account and can prove that she has used it twice.

The mechanism is based on a concept called one-show blind signatures. The use of the protocol

ensures that a certified public key, which has been issued by the bank in a blinded way, can be

traced to the party that it has been issued to ifand only ifmore than one signature is computed with

respect to the key. The mechanism consists of letting the bank certify the public key of a user in

such a way that the user cm perfectly blind the public key and the certificate thereon, but not part

of the corresponding secret key. The signature scheme employed by the user must be such that one

signature does not reveal this part of the secret key, whereas two signatures do. The mathematics

of the protocol are extensive and, as such, beyond the scope of this dissertation.

So far, no anonymous, ofTline payment system has been introduced into the marketplace. This can

be attributed to the lack of trust in the new cryptographic primitives, and its added computational

cost and complexity. A coin is represented by a number of independent, signed tokens, and thus,

the storage, communication and verification costs d l increase significantly. The bank, in

Tomi Poutanen, Net Cents Protucol for Inexpensive Interner Payments 25

paiticular, will face a heavy burden in creating and verifying the coins, and will most likely need to

define a per-transaction or a percoin cost. Since the protocols are coin based they face many of

the sarne problems as DigiCash: lack of divisibility of coins; the need for exact change; the cost of

the iterative validation of al1 coins independently per transaction; and the lack of offline

transferability of coins.

There has k e n a lot of ment research into the field of anonymous offline protocols that propose

new schemes that attempt to overcome the above limitations [CP93, Fe93, EC94, SPC951. Tholigh

incremental improvements are king made, the solutions are still much more complex than online

or other offline protocols.

23.2.4 sinart car& Smart cards ofier a promising solution to the double spending problem faced by offline protocols.

Physical car& are tightly packaged devices comprising of a microcontroller, memory and an y 0

pon. The packaging is designed to ensure that the microcontroller and the memory cannot be

tarnpered with, without breaking the entire system. There are several protocols that have been

defined on the basis of tamper resistance of smart cards pr95], [ChPe92]. A number of smartcard

solutions are currently in trial, such as those of Mondex in Ontario, or the Visa-Chip cards, with the

hope that they can serve as replacement for cash for low valued purchases.

In the Intemet realm, the obvious drawback of the smart card scheme is the requirement of a smart

card reader on every cornputer. In section 4.3.1 1 we will outline the use of tamper resistant devices

as an extension to the NetCents protocol to guard against malevolent merchants. However, unlike

the offline use of smart cards, only the merchants need be equipped with tarnper resistant devices,

in order to ensure provable system security.

The existence of tmly tamper resistant devices is a hotly debated topic [GSTY96], with every

significant "tamper resistant" consumer device having been cracked, from pay-TV chips, to pre-

paid long distance smart cards, to the Clipper chip, and to the venerable Dallas DS5002FP Secure

Microcontroller [AnKu96]. The fear is that if a universdly accepted payment system is dependent

on the tamper resistance of a smart card, then it will have to withstand tremendous scrutiny and

Tomi Poutanen, NetCents Prorocol for Inexpensive Interner Payments

relentless intrusion attempts. If the security is bmken in such a way that false car& can be

reproduced or altered in an automated and rapid succession, then the system would collapse and, at

minimum, al1 existing cards would have to be replaced.

2.5.3 Millicent Digital Equipment's Millicent [DEC95, Man951 is close in nature to our proposed NetCents

protocol. Millicent, like NetCents, does not fa11 into either the online or the oMine category, but

rather is a distributed allocation of fun& to merchants, who locally authonze payments. In brief,

both are automated account based systems.

Millicent introduces a scrip, which is a digital money that is honored by a single vendor. In

Millicent's plan, a customer will have their electronic credit distributed at various site accounts on

the Intemel with a comrnon management interface - in effect, prepaying for access to a vendor, as

in an account based scheme. On the first visit to an online merchant, the customer needs to ask her

issuing authority for a signed scnp specific to the merchant. The scrip is transported to the

merchant, who will subsequently authorize payments from the customer against that scrip. A scrip

is analogous to a prepaid calling carci, or a debit card specific to one merchant.

Once the scrip is fully used, the customer asks the broker to transmit additional hnds in scrip to the

merchant. When the funds are required elsewhere, the balance of the scrip can be redeemed by the

broker on request by the customer. The protocol was designed on the assumption that online

consumers, as in the real world, tend to shop repeatedly at the same merchants. If this assumption

holds, then indeed the protocol is inexpensive to the issuing authority due to its limited and mainly

offline involvement.

However, if a customer does not tend to revisit online merchants (since physical location is of no

importance in Cybeapace), then this protocol becornes even more expensive than the online

protocols. The fun& are can only be redeemed by the broker, which must first request the scrip

and signed balance from the vendor, it must venfy the signature, and lady it needs to create and

Tomi Poutanen, NetCents Protocol for Inexpensive Internet Puymenrs

sign a new scrip. As with online payment protocols, this will result in longer payrnent latencies and

a single point of failure.

The movement of fun& is especially troublesome when a custorner balance nears zero, and the

number of scrips approaches one. At this point, fund transfers become common, requiring broker

involvement to redeem existing scrip and sign new ones.

Millicent does not use public key encryption, but uses shared keys with cryptographie hashes.

Though this operation is substantially faster than public key cryptography, it implies that non-

repudiation cannot be assured, and an online arbiter cannot be implemented. Shared keys also

introduce communication overhead between the issuing authority and the account holder when

creating and re-issuing scrips. Furthemore, the protocol is not fully anonymous. since the broker

handles the customer's account transfen and scrip creation.

2.6 Comparative Evaluation of Existing Payrn ent Prorocok

2.6.1 Evaluation Criteria The payment protocols are compared with respect to the following properties and attributes.