Navigating investment in Vietnam's logistics and ...

55

Webinar | 14 October 2021 Navigating investment in Vietnam's logistics and industrial real estate sector

Transcript of Navigating investment in Vietnam's logistics and ...

Webinar | 14 October 2021

Navigating investment in Vietnam's logistics and industrial real estate sector

Agenda

1 Investments into IPs, warehouse

and logistics

2 Tax incentives

3 Land use and sub-lease

4 Merger control

5 Renewable Energy

6 Financing and security

7 Intellectual property protection

8 Q&A

Chung Seck

Partner

Corporate/M&A

+84 28 3520 2633

Manh Hung Tran

Partner

Intellectual Property+84 24 3936 9398

Thanh Hai Nguyen

Special Counsel

Energy & Projects+ 84 24 3936 9606

Tuan Minh Le

Associate

Antitrust/Competition+ 84 28 3520 2695

Our speakers

Hien Bui

Senior Consultant

Real Estate+84 28 3520 2663

Thuy Van Pham

Special Counsel

Finance & Project+84 28 3520 2703

Thanh Hoa Dao

Special Counsel

Tax & Trade+84 28 3520 2642

Thanh Le

Senior Associate

Corporate/M&A+84 28 3520 2681

1

Investments into IPs, warehouse and logistics

OverviewForeign investment into Vietnam in Warehouse services (Logistics)

According to the report from Ministry of Planning and Investment, logistics is one of the top ten

industries attracting most foreign direct investment capital accounting for approx. USD 5.7 billion

(as of September 2021).

According to the Vietnam Logistics Business Association, logistics industry in Vietnam accounts

for 20 to 25% of GDP, with the sector projected to grow by roughly 12% every year.

Typical foreign real estate investment structure are:

■ Greenfield investment; or

■ Brownfield investment (M&A).

Market access

Most of these projects are engaged in 2 business activities:

■ Real estate business, owner – owned or leased land use rights. Details: Warehouse for rent.

(VSIC 6810).

■ Warehousing and commodity storage. Details: warehousing and commodity storage services.

(VSIC 5210).

Vietnam international treaties will be applied first to look for any foreign ownership restrictions. If

the Schedule is silent, the authorities will refer to sector-specific Vietnamese regulations if the

foreign investors wish to engage in activities that are not committed.

Market access

For real estate business:

Real Estate business is not committed

by international treaties, but the Real

Estate Business Law provides the

activities that foreign invested company

(with no foreign ownership limitation) can

provide certain services, including "build

and sublease construction works (công

trình) in an IP.

For logistic services:

Vietnamese government has removed

market access restrictions for most

logistic services (e.g. warehousing

services) in its domestic laws. The

applicable domestic law for this area is

Decree 163/2017/ND-CP on the

provision of logistics services.

Investment StructureGreenfield investment (without bidding or auctioning)

Project Company

Project/

Property

Offshore

Vietnam

Foreign Investor

Vietnam

Government /

IP developer

100%

Leases or

allocates land to

Project Company

for development

of project

STEP

1

STEP

2

STEP

3

Identifying and acquiring land;

Obtaining approval for investment

project in Vietnam and setting up

Vietnamese subsidiary for implementing

the approved project; and

Obtaining approval for

construction of the project.

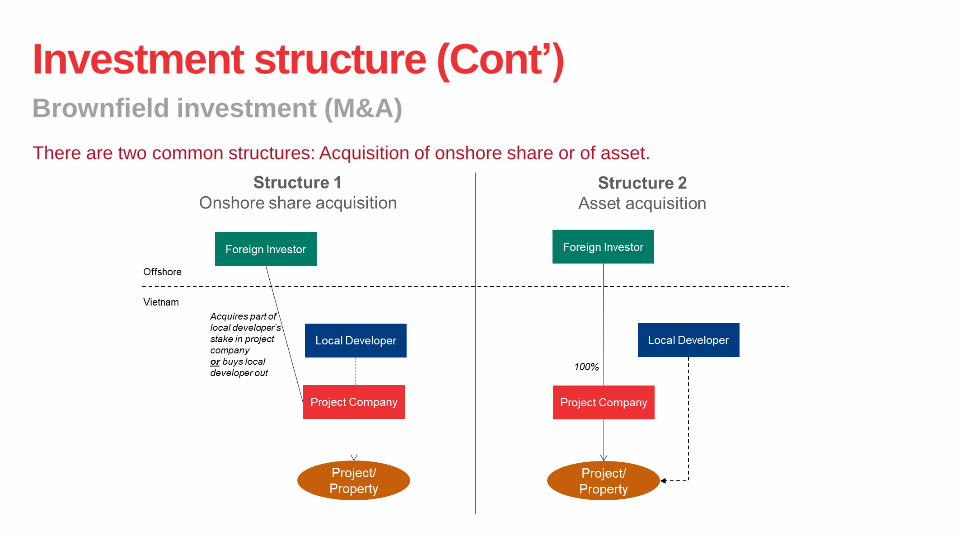

Investment structure (Cont’)Brownfield investment (M&A)

There are two common structures: Acquisition of onshore share or of asset.

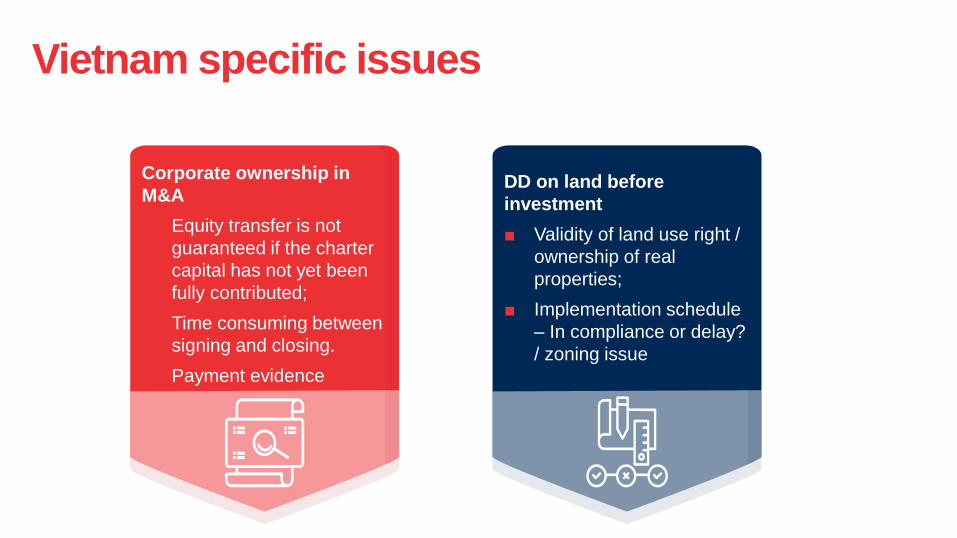

Vietnam specific issues

DD on land before

investment

■ Validity of land use right /

ownership of real

properties;

■ Implementation schedule

– In compliance or delay?

/ zoning issue

Corporate ownership in

M&A

Equity transfer is not

guaranteed if the charter

capital has not yet been

fully contributed;

Time consuming between

signing and closing.

Payment evidence

2

Tax incentives

Overview of CIT incentives

Reduced CIT rates

10%, 15% or 17%

CIT exemption 50% CIT reduction

CIT incentives include preferential CIT rate, exemption and reduction

Overview of CIT incentivesCIT incentives are granted to a project, not to a legal entity

Expanded projectsNew investment

projects

Restructured

projects

Overview of CIT incentives

■ Location: economic parks, high-tech parks, industrial parks, geographical

areas with harsh or especially harsh socio-economic conditions.

■ Business activities: high-tech industries, scientific research and

technological development, infrastructure development, software product

production, supporting industries, renewable energy, etc.

■ Scale of an investment project in the manufacturing sector: investment

capital, revenues, number of employees.

CIT incentives are determined based on the following criteria:

Criteria for enjoying CIT incentives

CIT incentives applicable to real estate business and logistics services

Real estate business: leasing service is not entitled to CIT incentives. There would be CIT

incentives depending on the location of a project

Warehouse/logistics projects: only location based CIT incentives applied.

Location-based CIT incentives

LocationReduced CIT

rateCIT Exemption

50% CIT

Reduction

New investment projects located in economic

parks, high-tech parks or geographical areas

with especially harsh socio-economic conditions

10% for 15

years

4 years Subsequent 9

years

New investment projects located in areas with

harsh socio-economic conditions

17% for 10

years

2 years Subsequent 4

years

New investment projects in industrial parks other

than those located in areas with advantageous

socio-economic conditions

N/A (standard

CIT rate

applied)

2 years Subsequent 4

years

3

Land use andsub-lease

Industrial land classification and land use of IP developer

Classification of industrial land under the

Land Law 2013

Industrial land can be located inside

Industrial Park ("IP") or outside IP

Type of industrial land (i.e. annual land,

upfront land)

Type of IPs under Decree 82 of 2018

(Industrial Park, Export Processing Zone,

Eco - Industrial Park)

Establishment of IP

IP land sub-lease and land use of IP tenant

Conditions required for IP developer to sub-lease

the land in IPTerm of the sub-lease

What is leasable land area in IP Land use purpose/ zoning

Who are eligible Tenants of IP Rights and obligations of IP Tenants

When to enter into the Land Reservation

Agreement and the Land Lease Agreement

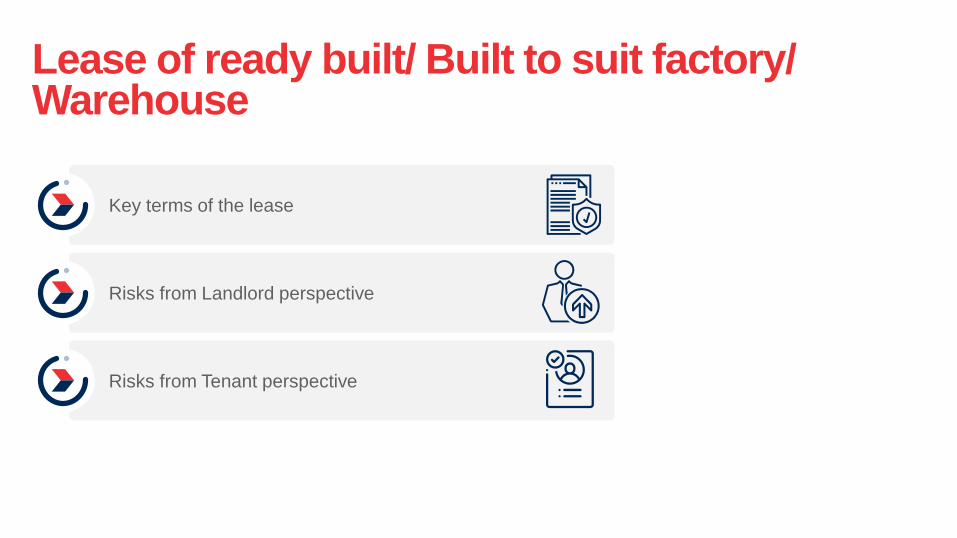

Lease of ready built/ Built to suit factory/ Warehouse

Key terms of the lease

Risks from Landlord perspective

Risks from Tenant perspective

Practical issues and common questions

IP land type

■ Can IP Tenant convert its sub-lease

annual land into sub-lease upfront

land?

Zoning

■ Can industrial production land in IP be

converted into logistics/ warehouse

land?

IP land acquisition

■ Can foreign invested company (FIE)

receive industrial land use rights

transfer by another IP Tenant or buy

factory/ warehouse from IP developer/

another IP Tenant?

4

Merger control

Overview of Vietnam merger control rulesScope of applicability

Competition Law No.

23/2018/QH14

Mergers, Consolidations,

Acquisitions, Joint Ventures

(collectively referred to as an

"Economic Concentration")

Vietnam's merger control regulations

covers the following transactions

Definition of Acquisitions redefined

under Decree 35Legal Framework

■ Appointment/removal of majority of the Board, the Chairman of the Board of Members, the Director or General Director;

■ Decide on the amendment or supplementation to the Charter;

■ Decide on other important decisions of the Target

Decree No. 75/2019/ND-CP on

Penalties for Administrative

Violations

Decree No. 35/2020/ND-CP

Guiding the Implementation of

the Competition Law Other economic concentrations

as prescribed by law

Acquisition of over 50% charter

capital, or 50% total voting rights

of the acquired enterprise;

Acquisition of over 50% assets of

all or one business line of the

acquired enterprise;

Acquisition sufficient to gain the

following rights:

Overview of Vietnam merger control rulesMerger Prohibition and Notification Regime

Enterprises carrying out an

economic concentration

which causes or potentially

causes a "substantial

anti-competitive effect" in

the Vietnam market.

Article 33 Notification of

economic concentration

Enterprises which participate in an

economic concentration must

submit a file notifying the

economic concentration to the

National Competition Commission

("NCC") as stipulated in article 34

of this Law prior to carrying out the

economic concentration if [such

economic concentration] reaches

the threshold requiring notification

of economic concentration…

(1)

Mandatory Notification RegimeMerger Prohibition

Article 30 Prohibited

economic concentration

Overview of Vietnam merger control rulesMerger Notification Thresholds

General Thresholds Sectors Specific Thresholds

Threshold 1: The total Vietnam asset of any enterprise involved in the

concentration (on a consolidated group-wide basis) is VND 3,000 billion

(approx. USD 129 million) or more.

■ Credit Institutions

■ Insurance companies

■ Securities companies

Threshold 2: The total Vietnam turnover of any enterprise involved in the

concentration (on a consolidated group-wide basis) is VND 3,000 billion

(approx. USD 129 million) or more.

Threshold 3: The value of the economic concentration is VND 1,000 billion

(approx. USD 43 million) or more.

Threshold 4: The combined market share of the participating enterprises is

20% or more on the relevant market.

Overview of Vietnam merger control rulesNotification/Approval Timeline

Merger control

regime does not

apply

If no

Step 3: Notify the

NCC of the

transaction and

seek approval

If no

Mandatory

notification does not

apply

Step 4(a): Proceed

to complete the

transaction

No response from NCC

at end of time limit

Clearance decision

from the NCC Step 4(b): Cooperate

with NCC to provide

further information

Issue notice

of official

appraisal

Step 2: Are any notification thresholds

triggered? If yes, proceed to step 3

Step 1: Determine if proposed

transaction is an "economic

concentration" if yes, proceed to

step 2

NCC commences

Preliminary Review (30

days from the date of

receipt of a complete

filing)

NCC commences

Official Review (90++

days from date of

issuance of notice)

Overview of Vietnam merger control rulesEnforcement Trends

Administering authority:

■ Ministry of Industry and Trade ("MOIT")

■ Vietnam Competition and Consumer

Authority ("VCCA")

Statistics from 2019 to 2021

■ 125 merger notifications have been made to

the VCCA/MOIT

• 80% Acquisitions

• 11% Mergers

• 11% Joint Ventures

■ 90% Preliminary Review /

10% Official Review

■ 70% Onshore Transaction /

30% Offshore Transaction

5

Renewable Energy

Introduction

Corporate PPAs - Overview

Traditionally, electricity generated by a renewable power project is sold directly to

an electricity supplier who then trades the electricity on the wholesale market or

supplies it directly to its customers.

Corporate PPAs: Instead of buying electricity direct from utilities (EVN),

corporations are now purchasing electricity directly from generators under corporate

renewable PPAs.

Many Asian countries (including Vietnam) operate under the traditional monopoly

utility market structure.

Regulations therefore need to be navigated – the regulations drive the structure.

$ for

excess

power

/ FiT

Structure 1: Behind-The-Meter Corporate PPA structure for Onsite Rooftop Solar

SOLAR ENERGY PROJECTCORPORATE

CUSTOMER

ELECTRIC UTILITY

(EVN)

BEHIND THE METER PPA

Power

to cover

unserved

electricity

demand

Excess

power

Electricity (and RECs)

$ Electricity (and REC) price

$ for

power

ELECTRICITY SUPPLY

CONTRACT

Rooftop solar

RTS Corporate PPA

If the purchaser is not EVN (i.e.,

private consumer), PPA terms and

tariff are subject to parties' negotiation

in accordance with applicable laws

Utility PPA

If the purchaser is EVN,

PPA is subject to model

PPA issued by MOIT

On-site rooftop solar PPAs

■ Utility PPA vs. RTS Corporate PPA (FiT 2 Decision 13/MOIT Circular 18) for COD by 31 Dec 2020

■ Utility PPA vs. RTS Corporate PPA (Draft New PM Decision) for COD in 2021

Key terms Key Considerations in Rooftop Solar Corporate PPA

Pricing ■ Power price risk is top of the agenda.

■ Negotiable price: Parties have certain flexibilities to agree on a price and how to reflect in the PPA

pricing (e.g., incentive regimes, environmental attributes)

■ Price adjustment: Parties can negotiate cases in which the price can be adjusted. From a power

consumer's perspective, power purchase may not be a core business of power consumer.

Payment

options

■ Actual v. deemed generation: How to deal with excess energy? Who is responsible for paying to EVN if

any excess energy?

■ Power consumption risk – consumers may not be able to consume all power produced, but still have to

pay for it?

Contract term ■ Commencement delay: Whether any installation delay may need to trigger an event of default or

termination rights and entitle the power consumer with compensation (e.g., delay LD, penalty)?

■ Consistency with other project documents: Whether the contract term of the PPA is consistent with the

land/site/building lease agreement for rooftop/building/premises/site and the investment approvals of

the power consumer's businesses.

Key Contractual TermsOn-site Rooftop Solar Corporate PPA

Key terms Key Considerations in Rooftop Solar Corporate PPA

Qualification ■ Counterparty risk

■ The developer's qualification: Qualified and duly licensed to provide proposed relevant services and

activities (e.g., power generation, equipment installation, O&M and repair services, etc.):

■ Business lines registrations for power sellers

■ Capacity permits for installation, maintenance, and repairing rooftop solar rooftop system

System Size

and Capacity

■ Regulatory risk: restrictive regulations relating to the direct sale of power to corporations.

■ Licensing implications (related to 1 MW and 1.25MWp threshold if there are more than one location

and total size is larger than 1 MW and 1.25MWp).

Key Contractual TermsOn-site Rooftop Solar Corporate PPA

Structure 2: Synthetic Corporate DPPA

SOLAR OR WIND

GENCO / PROJECT COMPANY

EVN / Vietnam

Wholesale

Electricity

(Pool) Market

CORPORATE

POWER

CONSUMER

ELECTRIC UTILITY

(Power Corporation)

VIRTUAL PPA

"Contract-for-Differences"

(CfD)Electricity

(PPA output)

Wholesale

market spot

price

Electricity(Energy charge

+ DPPA charge)

price x load

Electricity

Wholesale spot price and

market charges

Whole market

spot priceRECs

Fixed price (electricity &

RECs) for PPA output

POWER SUPPLY

AGREEMENT

POWER PURCHASE

AGREEMENT

Tentative plan and schedule for DPPA pilot program

Within 15 working days from the date on which this proposed DPPA Circular comes into effect (which is

to be determined), the MOIT will announce the launch of the DPPA pilot program.

Within 15 working days from the date of announcing the launch of the DPPA pilot program, the MOIT

will open the pilot DPPA Program's portal and announce the Service Unit (which is selected by the

MOIT) that will assess the application dossier.

Within 45 working days from the date of MOIT's opening of the DPPA pilot program's electronic

information portal, GENCOs and CONSUMERS who wish to participate will be required to prepare and

submit registration applications to the MOIT portal.

Within 40 working days from the date of closing the DPPA pilot program's portal, the Service Unit will

evaluate and rank the application dossiers and send the MOIT a list of eligible GENCOs and

consumers.

Within five working days from the date of receiving the list from the Service Unit, ERAV will submit the

selection result to the head of the MOIT for announcement.

Preparation Phase (Draft MOIT Circular)1

Key eligibility criteria for

CONSUMER

Must be an existing industrial consumer purchasing power at 22 kV or higher

voltage level.

Must have committed to using renewable energy or its factories within supply

chain of its group have committed to using renewables.

Must have a CfD "in-principle agreement" with GENCO for purchase of power

from selected project.

Must commit that, for the first three years of participation in the DPPA pilot

program, the output to be purchased from GENCO within a year will be at

least 80% the total output consumed in such year as supplied by EVN/Power

Corporation.

6

Financing and Security

A

Financing

Types of loans

Types of loans

Onshore loan (such as loans from credit institutions, inter-companies loans, shareholder loans)

Offshore loan (such as loans from credit institutions, other

offshore lenders, and offshore shareholders)

Short-term loan

Middle-long term loan

(registration with the State Bank of Vietnam

in case of offshore loan)

Borrowing limits

FDI company

■ For middle-long term loans: Borrowing limits (include onshore and offshore) may not exceed

investment capital minus equity of borrower as mentioned in its Investment Registration

Certificate.

■ For short-term loan: Not subject to limitation.

Local company

■ No borrowing restriction imposed.

Borrowing purposesOffshore Loan

Offshore Loan

Offshore loan

Short-term loanFunding the working

capital

Middle and long-term loan

Implement the business plans or investment

projects of

The borrower

The borrower's subsidiaries

Refinance of foreign loans without increasing the borrowing cost

Borrowing purposes

Onshore Loan

Prohibited purposes:

■ For business investment activities in an industry or trade in which the law prohibits business.

■ To pay the expenses of or to satisfy financial requirements of transactions or other conduct prohibited by law.

■ To purchase or use goods or services in an industry or trade in which the law prohibits business investment.

■ To purchase gold bars.

■ To refinance its existing loan which was granted by its credit institution, except for a loan to make payment of

interest arising during the construction process, which were included in the estimated budget for building the

construction works approved by the competent body in accordance with law.

■ To refinance its existing loan which was granted by another credit institution or to refinance a foreign loan,

except for a refinanced loan satisfies all the following conditions:

• a financed loan to serve business activities;

• the term of the new loan does not exceed the residual term of the refinanced loan;

• the term for repayment of the refinanced loan has not yet been restructured.

Onshore Loan

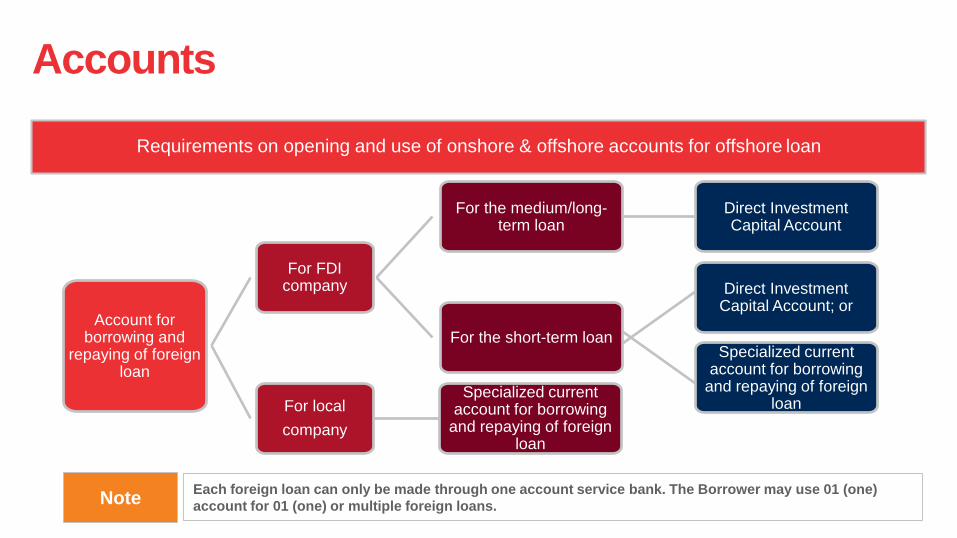

Accounts

Account for borrowing and

repaying of foreign loan

For FDI company

For the medium/long-term loan

Direct Investment Capital Account

For the short-term loan

Direct Investment Capital Account; or

Specialized current account for borrowing

and repaying of foreign loanFor local

company

Specialized current account for borrowing

and repaying of foreign loan

Each foreign loan can only be made through one account service bank. The Borrower may use 01 (one)

account for 01 (one) or multiple foreign loans.Note

Requirements on opening and use of onshore & offshore accounts for offshore loan

Accounts

SpecificRequirements on opening and use of onshore & offshore accounts for offshore loan (continue)

Offshore foreign currency account require the SBV’s approval: granted on a case by case basis

The application dossiers for issuance of the license for opening and use of offshore foreign

currency account shall be submitted to the SBV, together with the application dossier for

registering the foreign loan.

Offshore Loan

■ Fees payable to the offshore lenders in relation to the offshore loan (either bilateral or

syndicated loans) are not subject to Vietnamese law. The popular fees relating to the offshore

loans are:

■ Payment of fees are only made after registration of the foreign facility/loan with the SBV.

■ SBV only registers ascertainable fees as at the time of application.

Fees that can be collected relating to onshore and offshore loans

Agency feeSecurity

agency feeCommitment

feeUpfront fee

Arrangement fee

Fees that can be collected relating to onshore and offshore loans

Onshore Loan

■ Onshore lenders are permitted by law to collect certain fees relating to their provisions of

onshore loans, including:

Commitment fee (one off payment) can be calculated and accrued from the effective date of

the facility/loan agreement to the first drawdown date.

With regard to onshore syndicated loans: agents can collect fees/remuneration arising from

their implementation of agency roles such as facility agency fee, security agency fee,

arrangement fee, paying agency fee.

Prepayment fee/premium

Standby credit line fee

Arrangement fee relating to

syndicated loans

Commitment

fee

B

Security

Common Security Package

Priority can be preserved by voluntary registration with the

National Registration Agency of Secured Transactions (NRAST).

Mortgage or pledge of:

■ LUR, assets attached to LUR

(including future assets)

■ equipment and machinery

■ equity/shares

■ receivables from contracts,

insurances, bank accounts

■ other assets in line with

Vietnamese laws

Notarization and mandatory registration of the mortgages of LUR

and assets attached to LUR with the LUR Registration Offices,

aircrafts with Civil Aviation Authority of Viet Nam (CAAV) and

vessels with sea vessel registration authorities of Vietnam. The

security over listed shares must be registered with Vietnam

Securities Depository and Clearing Corporation (VSDCC),

including block the trading of the listed shares.

Mortgage of LUR and assets attached to LUR can only be

granted to onshore lenders (including onshore branches of

foreign lenders). Upfront land rental needs to be made before the

mortgage.

Mortgage of land for companies in IPs

■ Companies in IPs sign the

sub-lease land agreement with

IP Developer, who leased the

land from the

State/Government.

■ Companies in IPs has the

LURC for its sub-leased land.

■ it has obtained the LURC for its leased land;

■ it has paid fully the sub-lease land rental to the IP

developer, and the IP developer also has paid fully

land lease rentals over the whole land it leased to the

Government. If the IP developer or has not fully paid

the lease rental, then companies in IPs can only

mortgage its assets on land to the bank.

Conditions for companies in IPs to mortgage its sub-

leased land:

7

Intellectual Property protection in Vietnam

Intellectual property protection in VietnamIP Registration

Common types of intellectual property (IP): trademark, patent, industrial design, copyrights, trade

secrets

Vietnam follows the first-to-file system (for patent, design and trademark).

■ Consequences of not filing or untimely filing:

• Patent / Design: Loss of novelty

• Pirated filing / Squatting (especially trademark)

• Lack of effective basis for brand protection against infringement

• Risk becoming an infringer yourself

Almost IP protection only has territorial effects it is necessary to obtain local registrations,

instead of relying on those obtained in other countries.

Intellectual property protection in VietnamIP Registration - Takeaways

IP is an asset, not a cost – IP filings and management are investments with substantial return-on-

investment as you expand your business in Vietnam.

If IP does not become your legitimate asset, it will really become a huge cost:

■ Costs for defending yourself against infringement claims of parties that have establish the

right first

■ Costs for negotiating and buying back the IP from squatters

■ Costs for negotiating and entering related arrangements such as coexistence agreements,

license agreements so that you can use the IP in Vietnam

Intellectual property protection in VietnamIP Commercialization

IP commercialization takes up many forms – most common: technology transfer, IP license,

franchising

Guarantee the validity and effectiveness of your arrangements in Vietnam:

■ Must be registered to have effect:

• Technology transfer agreements: at the

Ministry of Science and Technology

• Patent / Design license agreements: at

the Intellectual Property Office of

Vietnam

■ Registration not mandatory, but strongly

recommended:

• Trademark license agreement – some

Vietnamese authorities still request the

registration (such as Customs

agencies, tax agencies, some courts):

at the Intellectual Property Office of

Vietnam.

Our resources

Global Private M&A GuideA practical tool covering key aspects of the

legal and regulatory M&A framework in nearly

40 countries

Global Public M&A GuideA guide to some of the key legal

considerations associated with public M&A

transactions across the globe.

Global Guide to Take-Private TransactionsA comparison of the key features and requirements applicable

to take-private deals in a numbers of jurisdictions around the

globe, including indicative timelines.

Vietnam's New Investment LandscapeA dedicated investment updates covering a range of

issues including our views the legislative changes and

what businesses should look out for.

Guide to IPOsAn overview of the key stages of the process,

and an indicative timeline. A who's who as

regards the IPO deal team. Practical tips to help

achieve a successful IPO.

Asia Pacific Business Renewal SeriesBased on a custom survey of 800

respondents, this series spans four main areas

of business: Supply Chains, New M&A

Landscape, Digital Transformation and ESG.

bakermckenzie.com

This presentation has been prepared for clients and professional associates of Baker & McKenzie. Whilst every effort

has been made to ensure accuracy, this presentation is not an exhaustive treatment of the area of law discussed and no

responsibility for any loss occasioned to any person acting or refraining from action as a result of material in this

presentation is accepted by Baker & McKenzie.

Baker & McKenzie (Vietnam) Ltd., a limited liability company, is a member firm of Baker & McKenzie International, a

global law firm with member law firms around the world. In accordance with the common terminology used in

professional service organisations, reference to a "partner" means a person who is a partner, or equivalent, in such a law

firm. Similarly, reference to an "office" means an office of any such law firm. This may qualify as "Attorney Advertising"

requiring notice in some jurisdictions. Prior results do not guarantee a similar outcome.

© 2021 Baker & McKenzie (Vietnam) Ltd.