Navigating a Mature Bull Market - Microsoft · 2018-09-28 · Navigating a Mature Bull Market. ......

28

Ned Davis Research Group Generate Alpha. Identify Risk. Choose Ned Davis Research. ED CLISSOLD, CFA Chief U.S. Strategist September 2018 Navigating a Mature Bull Market

Transcript of Navigating a Mature Bull Market - Microsoft · 2018-09-28 · Navigating a Mature Bull Market. ......

Ned DavisResearch

Group

Generate Alpha. Identify Risk.Choose Ned Davis Research.

ED CLISSOLD, CFAChief U.S. Strategist

September 2018

Navigating a Mature Bull Market

Please see important disclosures at the end of this report. NED DAVIS RESEARCH GROUP i

TABLE OF CONTENTSNDR Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Fundamental. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2-5

Macro . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6-12

Sentiment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13-15

Technical . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16-20

Bottom Line. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21-22

NDR House Views . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

NED DAVIS RESEARCH GROUP 1Please see important disclosures at the end of this report.

NED DAVIS RESEARCH GROUP APPROACH

EXPECTATIONS:How the market SHOULD BE acting

TIMING:How the market

IS acting

Macro

Sentiment

Fundamental

Technical

Idea

NED DAVIS RESEARCH GROUP 2Please see important disclosures at the end of this report.

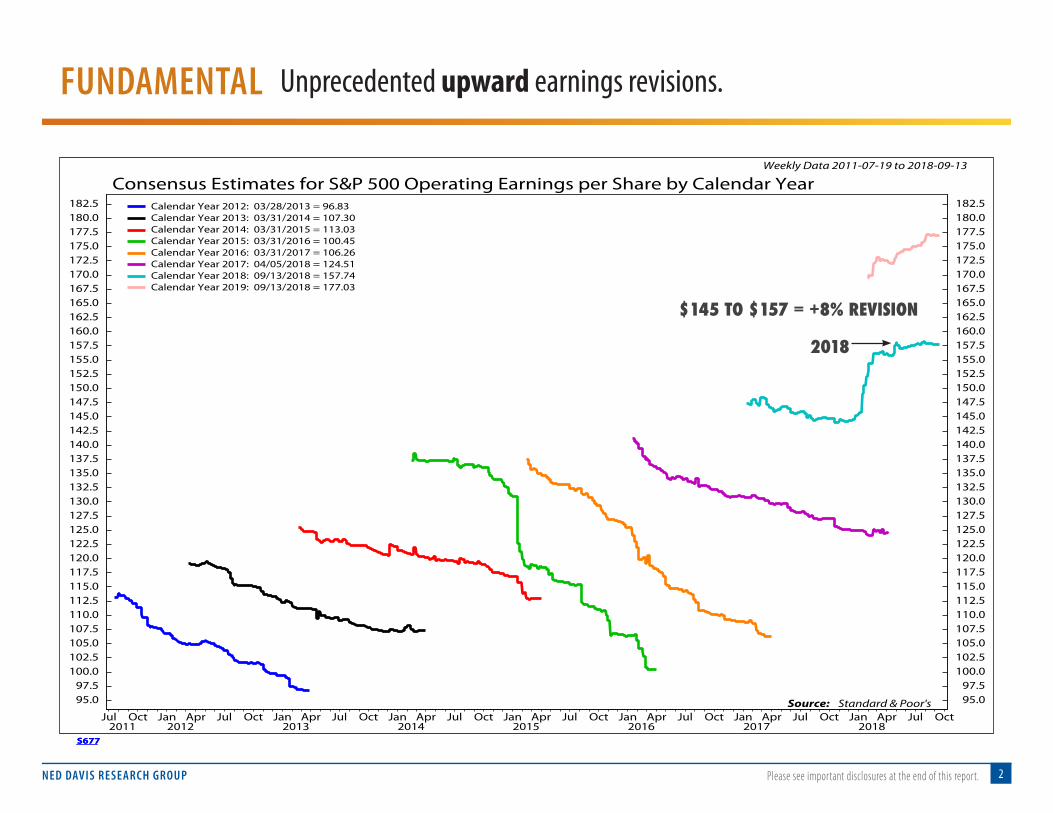

Unprecedented upward earnings revisions.FUNDAMENTAL

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S677

Consensus Estimates for S&P 500 Operating Earnings per Share by Calendar YearWeekly Data 2011-07-19 to 2018-09-13

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S677

Consensus Estimates for S&P 500 Operating Earnings per Share by Calendar YearWeekly Data 2011-07-19 to 2018-09-13

2011Jul Oct

2012Jan Apr Jul Oct

2013Jan Apr Jul Oct

2014Jan Apr Jul Oct

2015Jan Apr Jul Oct

2016Jan Apr Jul Oct

2017Jan Apr Jul Oct

2018Jan Apr Jul Oct

95.097.5

100.0102.5105.0107.5110.0112.5115.0117.5120.0122.5125.0127.5130.0132.5135.0137.5140.0142.5145.0147.5150.0152.5155.0157.5160.0162.5165.0167.5170.0172.5175.0177.5180.0182.5

95.097.5

100.0102.5105.0107.5110.0112.5115.0117.5120.0122.5125.0127.5130.0132.5135.0137.5140.0142.5145.0147.5150.0152.5155.0157.5160.0162.5165.0167.5170.0172.5175.0177.5180.0182.5Calendar Year 2012: 03/28/2013 = 96.83

Calendar Year 2013: 03/31/2014 = 107.30Calendar Year 2014: 03/31/2015 = 113.03Calendar Year 2015: 03/31/2016 = 100.45Calendar Year 2016: 03/31/2017 = 106.26Calendar Year 2017: 04/05/2018 = 124.51Calendar Year 2018: 09/13/2018 = 157.74Calendar Year 2019: 09/13/2018 = 177.03

Source: Standard & Poor's

2018

$145 TO $157 = +8% REVISION

NED DAVIS RESEARCH GROUP 3Please see important disclosures at the end of this report.

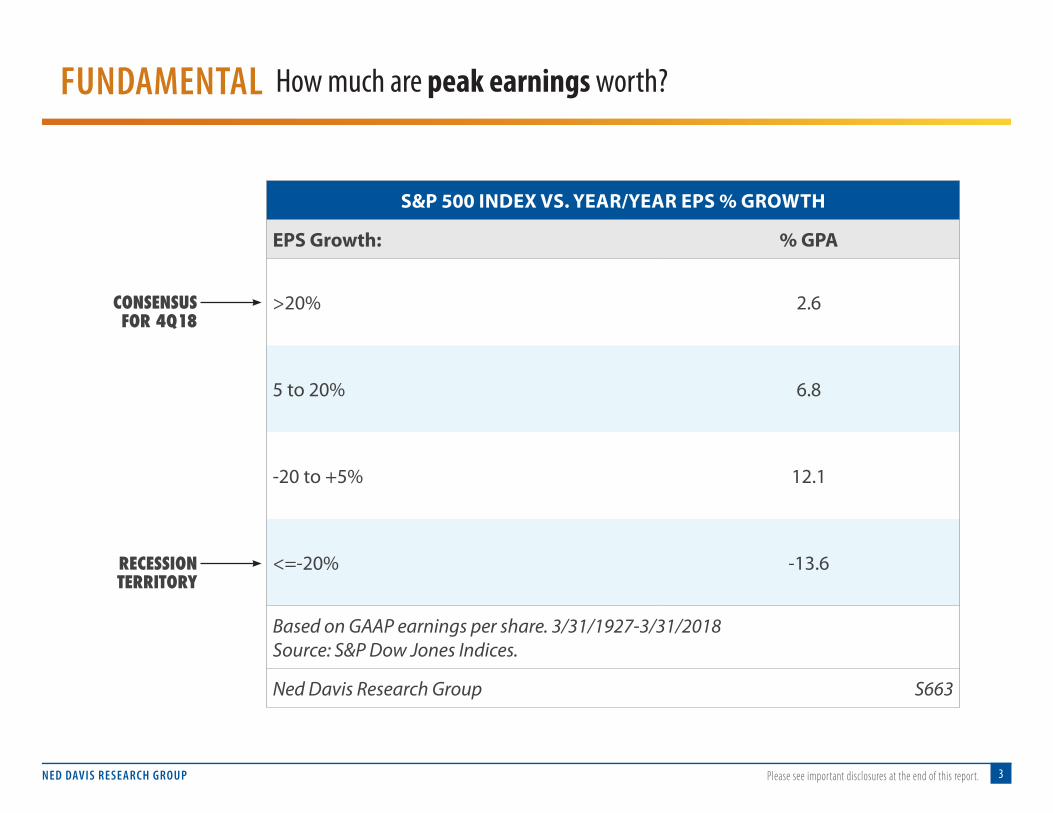

FUNDAMENTAL How much are peak earnings worth?

S&P 500 INDEX VS. YEAR/YEAR EPS % GROWTH

EPS Growth: % GPA

>20% 2.6

5 to 20% 6.8

-20 to +5% 12.1

<=-20% -13.6

Based on GAAP earnings per share. 3/31/1927-3/31/2018Source: S&P Dow Jones Indices.

Ned Davis Research Group S663

CONSENSUS FOR 4Q18

RECESSION TERRITORY

NED DAVIS RESEARCH GROUP 4Please see important disclosures at the end of this report.

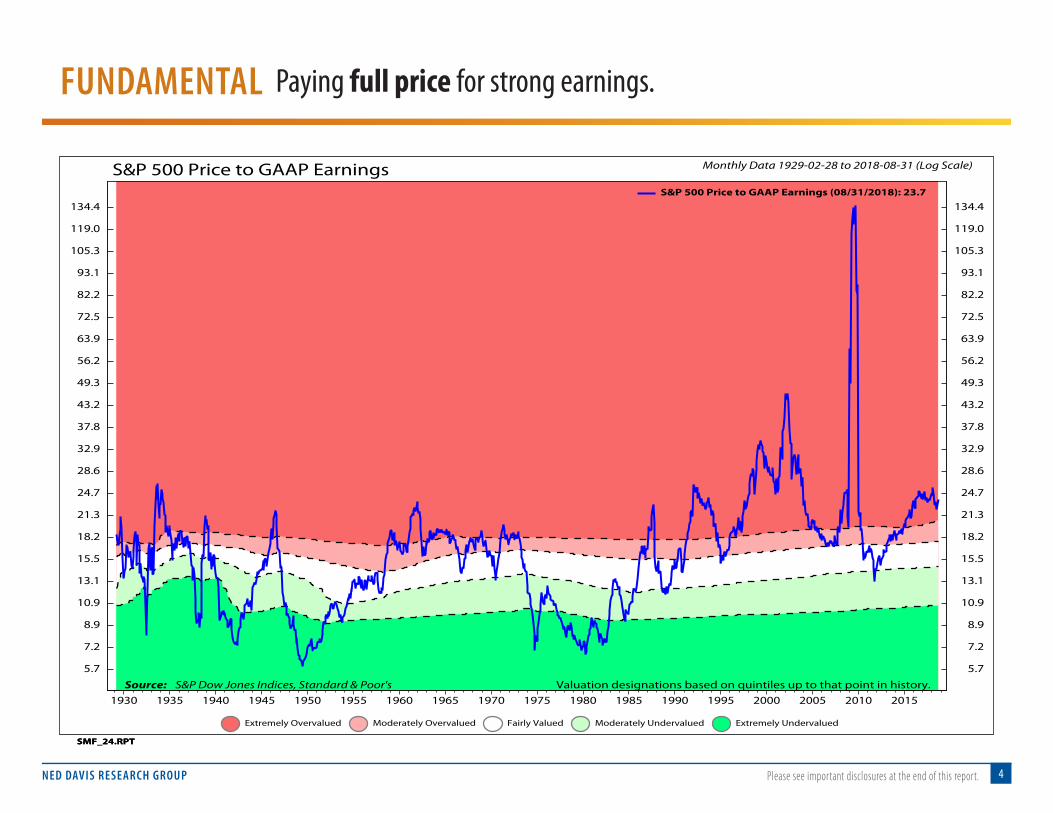

FUNDAMENTAL Paying full price for strong earnings.

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

SMF_24.RPT

S&P 500 Price to GAAP Earnings Monthly Data 1929-02-28 to 2018-08-31 (Log Scale)

Extremely Overvalued Moderately Overvalued Fairly Valued Moderately Undervalued Extremely Undervalued

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

SMF_24.RPT

S&P 500 Price to GAAP Earnings Monthly Data 1929-02-28 to 2018-08-31 (Log Scale)

Extremely Overvalued Moderately Overvalued Fairly Valued Moderately Undervalued Extremely Undervalued

1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

5.7

7.2

8.9

10.9

13.1

15.5

18.2

21.3

24.7

28.6

32.9

37.8

43.2

49.3

56.2

63.9

72.5

82.2

93.1

105.3

119.0

134.4

5.7

7.2

8.9

10.9

13.1

15.5

18.2

21.3

24.7

28.6

32.9

37.8

43.2

49.3

56.2

63.9

72.5

82.2

93.1

105.3

119.0

134.4S&P 500 Price to GAAP Earnings (08/31/2018): 23.7

Valuation designations based on quintiles up to that point in history.Source: S&P Dow Jones Indices, Standard & Poor's

NED DAVIS RESEARCH GROUP 5Please see important disclosures at the end of this report.

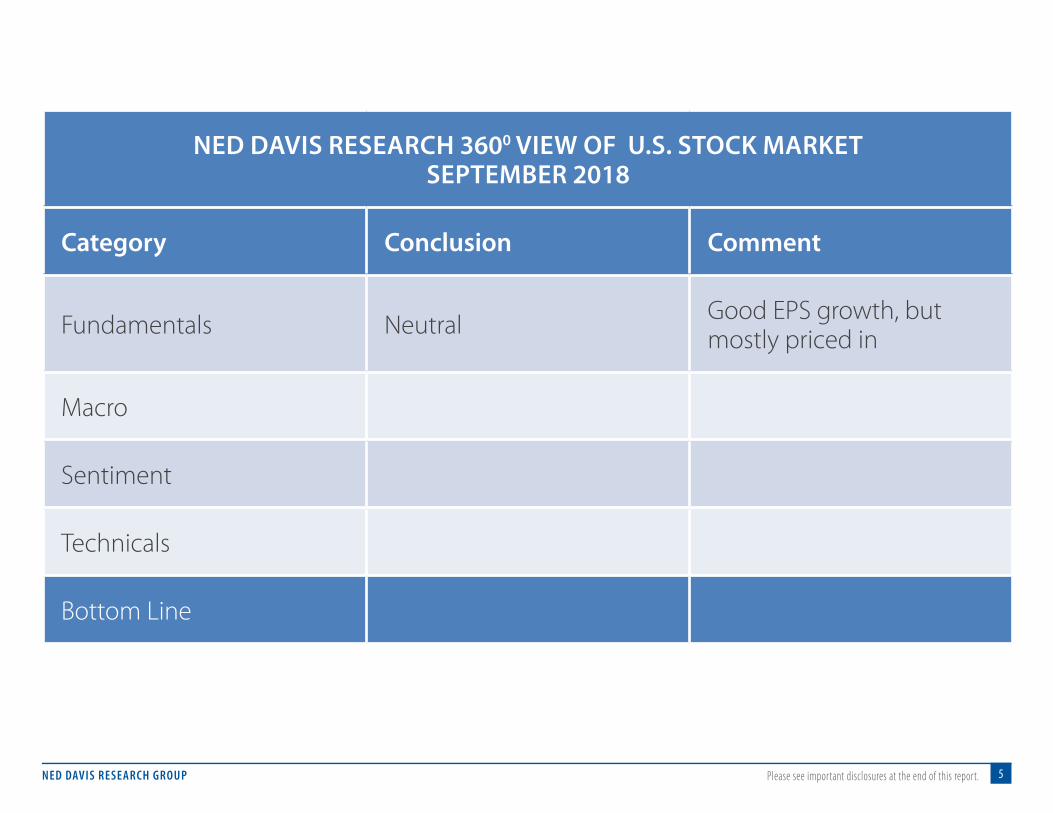

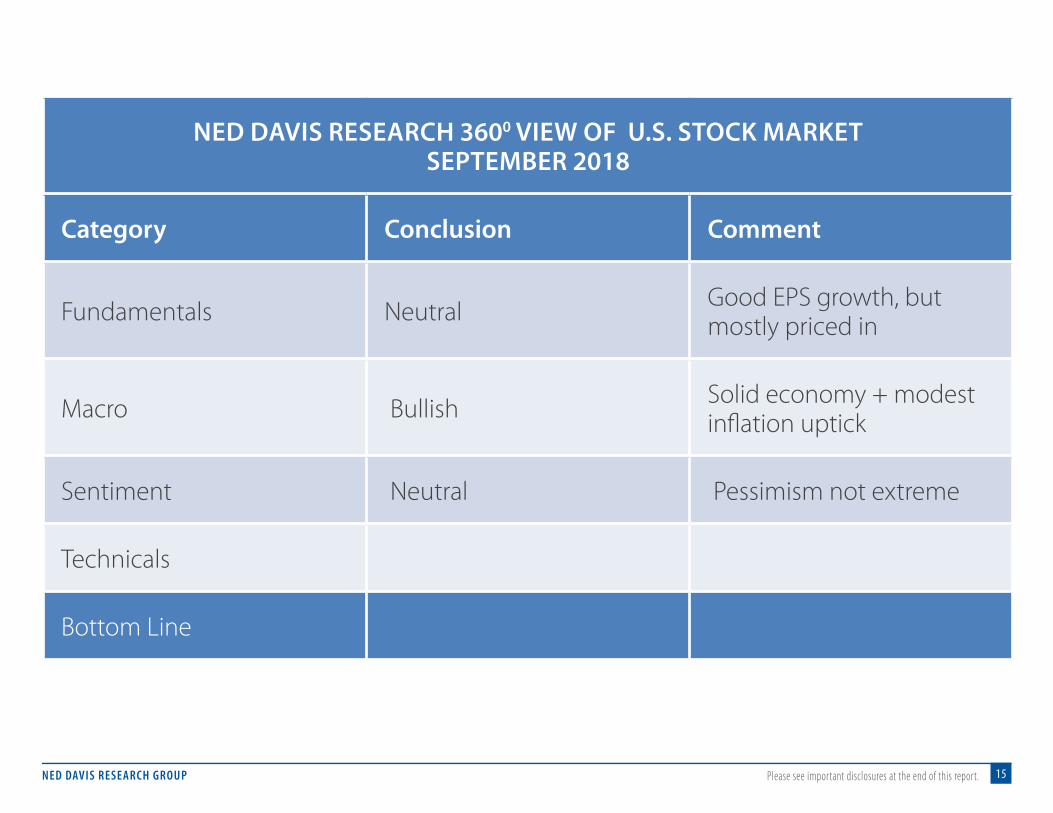

NED DAVIS RESEARCH 3600 VIEW OF U.S. STOCK MARKETSEPTEMBER 2018

Category Conclusion Comment

Fundamentals Neutral Good EPS growth, but mostly priced in

Macro

Sentiment

Technicals

Bottom Line

NED DAVIS RESEARCH GROUP 6Please see important disclosures at the end of this report.

Stocks cheap relative to bonds.MACRO

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

SMF_24.RPT

S&P 500 GAAP Earnings Yield less 10-Year Treasury Yield Monthly Data 1966-03-31 to 2018-08-31 (Log Scale)

Extremely Overvalued Moderately Overvalued Fairly Valued Moderately Undervalued Extremely Undervalued

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

SMF_24.RPT

S&P 500 GAAP Earnings Yield less 10-Year Treasury Yield Monthly Data 1966-03-31 to 2018-08-31 (Log Scale)

Extremely Overvalued Moderately Overvalued Fairly Valued Moderately Undervalued Extremely Undervalued

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

-4.8-4.7-4.6-4.5-4.3-4.2-4.0-3.9-3.7-3.5-3.3-3.1-2.9-2.6-2.4-2.1-1.8-1.6-1.2-0.9-0.6-0.20.20.61.11.52.02.53.13.74.34.95.56.26.9

-4.8-4.7-4.6-4.5-4.3-4.2-4.0-3.9-3.7-3.5-3.3-3.1-2.9-2.6-2.4-2.1-1.8-1.6-1.2-0.9-0.6-0.20.20.61.11.52.02.53.13.74.34.95.56.26.9S&P 500 GAAP Earnings Yield less 10-Year Treasury Yield (08/31/2018): 1.4

Valuation designations based on quintiles up to that point in history.Source: S&P Dow Jones Indices, Standard & Poor's

NED DAVIS RESEARCH GROUP 7Please see important disclosures at the end of this report.

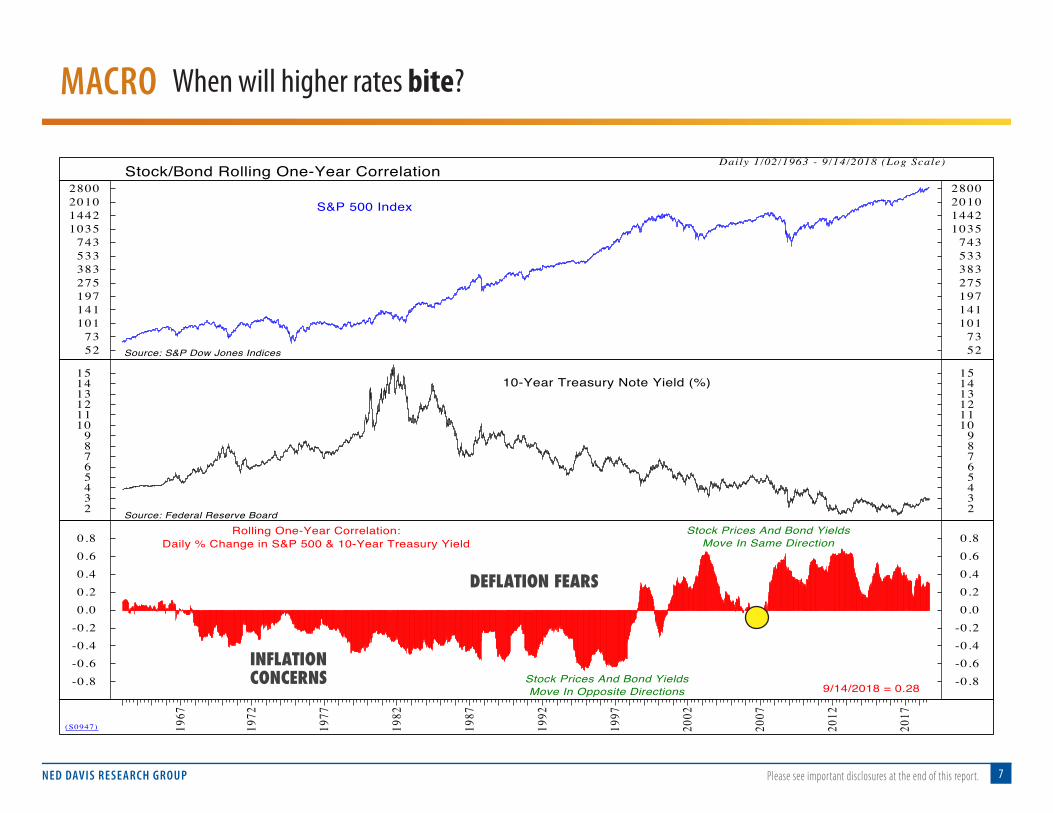

When will higher rates bite?MACRO

(S0947)

Daily 1/02/1963 - 9/14/2018 (Log Scale)

S&P 500 Index

Source: S&P Dow Jones Indices5273

101141197275383533743

1035144220102800

5273

101141197275383533743

1035144220102800

10-Year Treasury Note Yield (%)

Source: Federal Reserve Board23456789

101112131415

23456789

101112131415

9/14/2018 = 0.28

Rolling One-Year Correlation:Daily % Change in S&P 500 & 10-Year Treasury Yield

Stock Prices And Bond YieldsMove In Same Direction

Stock Prices And Bond YieldsMove In Opposite Directions

-0.8-0.6-0.4-0.20.00.20.40.60.8

-0.8-0.6-0.4-0.20.00.20.40.60.8

1967

1972

1977

1982

1987

1992

1997

2002

2007

2012

2017

Stock/Bond Rolling One-Year Correlation

Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved..www.ndr.com/vendorinfo/. For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

�

DEFLATION FEARS

INFLATION CONCERNS

NED DAVIS RESEARCH GROUP 8Please see important disclosures at the end of this report.

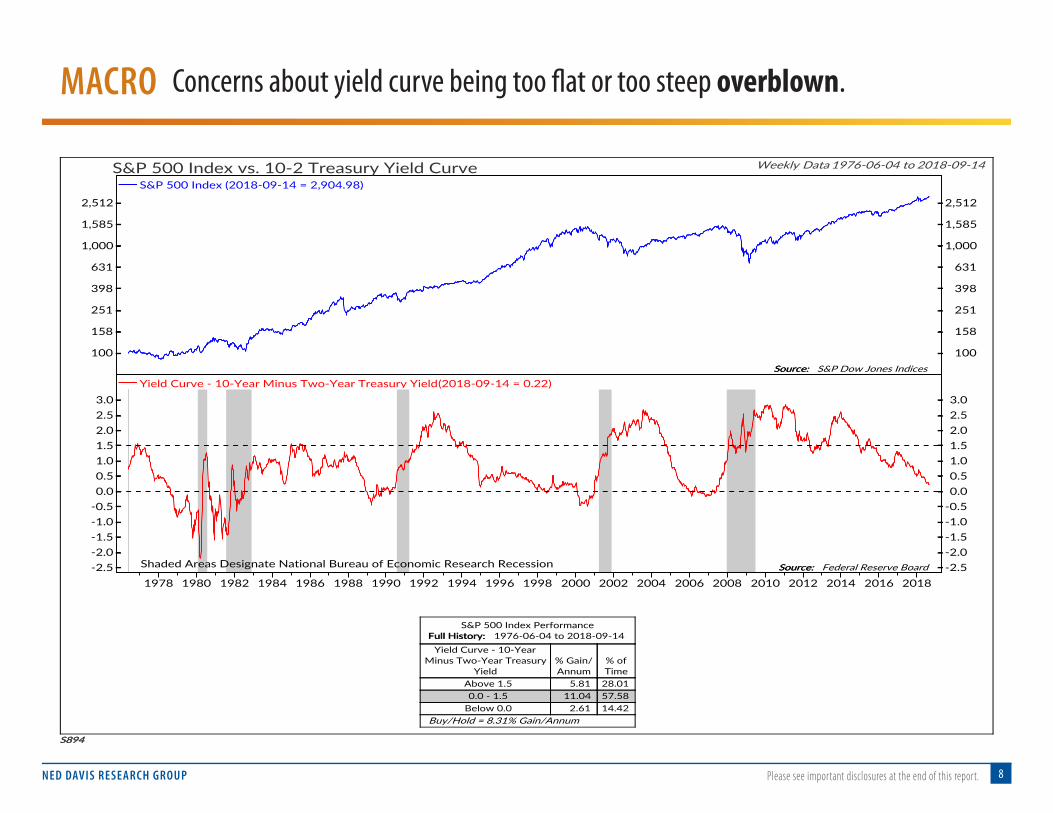

Concerns about yield curve being too flat or too steep overblown.MACRO

S894S894

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

100

158

251

398

631

1,000

1,585

2,512

100

158

251

398

631

1,000

1,585

2,512

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Source:Source: S&P Dow Jones Indices

Shaded Areas Designate National Bureau of Economic Research Recession Source:Source: Federal Reserve Board

Weekly Data 1976-06-04 to 2018-09-14S&P 500 Index vs. 10-2 Treasury Yield Curve

S&P 500 Index Performance

Full History:Full History: 1976-06-04 to 2018-09-14

Yield Curve - 10-Year

Minus Two-Year Treasury

Yield

% Gain/

Annum

% of

Time

Above 1.5 5.81 28.01

0.0 - 1.5 11.04 57.58

Below 0.0 2.61 14.42

Buy/Hold = 8.31% Gain/Annum

S&P 500 Index (2018-09-14 = 2,904.98)

Yield Curve - 10-Year Minus Two-Year Treasury Yield(2018-09-14 = 0.22)

NED DAVIS RESEARCH GROUP 9Please see important disclosures at the end of this report.

Deflationary forces have not disappeared.MACRO

NED DAVIS RESEARCH GROUP 10Please see important disclosures at the end of this report.

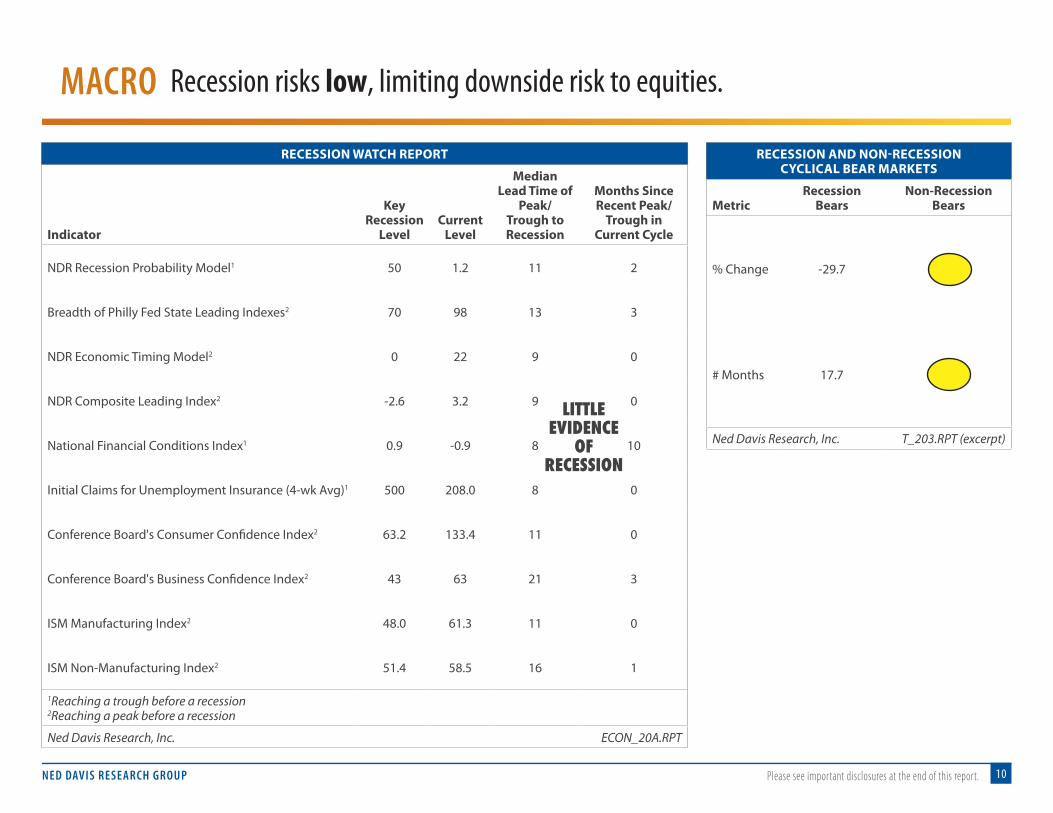

Recession risks low, limiting downside risk to equities.MACRO

RECESSION WATCH REPORT

Indicator

Key Recession

LevelCurrent

Level

Median Lead Time of

Peak/ Trough to Recession

Months Since Recent Peak/

Trough in Current Cycle

NDR Recession Probability Model1 50 1.2 11 2

Breadth of Philly Fed State Leading Indexes2 70 98 13 3

NDR Economic Timing Model2 0 22 9 0

NDR Composite Leading Index2 -2.6 3.2 9 0

National Financial Conditions Index1 0.9 -0.9 8 10

Initial Claims for Unemployment Insurance (4-wk Avg)1 500 208.0 8 0

Conference Board's Consumer Confidence Index2 63.2 133.4 11 0

Conference Board's Business Confidence Index2 43 63 21 3

ISM Manufacturing Index2 48.0 61.3 11 0

ISM Non-Manufacturing Index2 51.4 58.5 16 1

1Reaching a trough before a recession2Reaching a peak before a recession

Ned Davis Research, Inc. ECON_20A.RPT

RECESSION AND NON-RECESSION CYCLICAL BEAR MARKETS

MetricRecession

BearsNon-Recession

Bears

% Change -29.7 -18.0

# Months 17.7 6.8

Ned Davis Research, Inc. T_203.RPT (excerpt)

LITTLE EVIDENCE

OF RECESSION

NED DAVIS RESEARCH GROUP 11Please see important disclosures at the end of this report.

Economy needs more than the consumer.MACRO

Quarterly 3/31/1995 - 6/30/2018

(E65)

PCE 6/30/2018 = 2.55

Source: Bureau of Economic Analysis-2.0-1.00.01.02.03.04.05.0

-2.0-1.00.01.02.03.04.05.0

Gross Private Domestic Investment 6/30/2018 = 0.10

-6

-4

-2

0

2

4

-6

-4

-2

0

2

4

Net Exports 6/30/2018 = 1.17

-1.5-1.0-0.50.00.51.01.52.02.5

-1.5-1.0-0.50.00.51.01.52.02.5

Government 6/30/2018 = 0.41

-0.9-0.6-0.30.00.30.60.91.2

-0.9-0.6-0.30.00.30.60.91.2

1995 2000 2005 2010 2015

Percentage Point Contributions to GDP Growth

Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved..www.ndr.com/vendorinfo/. For data vendor disclaimers refer to www.ndr.com/copyright.htmlSee NDR Disclaimer at

�

BIGGEST DRIVER

NEEDED FOR ESCAPE VELOCITY

TRADE WAR RISK

TAX CUTS

NED DAVIS RESEARCH GROUP 12Please see important disclosures at the end of this report.

NED DAVIS RESEARCH 3600 VIEW OF U.S. STOCK MARKETSEPTEMBER 2018

Category Conclusion Comment

Fundamentals Neutral Good EPS growth, but mostly priced in

Macro Bullish Solid economy + modest inflation uptick

Sentiment

Technicals

Bottom Line

NED DAVIS RESEARCH GROUP 13Please see important disclosures at the end of this report.

SENTIMENT Pessimism never fell to wash out levels.

S574AS574A

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

631

794

1,000

1,259

1,585

1,995

2,512

631

794

1,000

1,259

1,585

1,995

2,512

30

35

40

45

50

55

60

65

70

75

80

30

35

40

45

50

55

60

65

70

75

80

Source:Source: S&P Dow Jones Indices

33.5 33.9

43.8

46.6

49.7

42.5

49.947.6

38.0

30.9

46.8

40.538.4

47.2

55.253.3

45.8

42.8

52.7

69.2

75.773.5

71.970.5

72.2

58.1

70.773.0

70.7 71.673.9 73.3

69.8

78.9Extreme Optimism (Bearish)

Extreme Pessimism (Bullish)Updates weekly on Wednesday mornings. Source:Source: Ned Davis Research, Inc.

Daily Data 1995-12-01 to 2018-09-13S&P 500 Index vs. NDR Crowd Sentiment Poll - Transitional Mode Basis

S&P 500 Index Performance

Full History:Full History: 1995-12-01 to 2018-09-13

NDR Crowd Sentiment Poll

is

% Gain/

Annum

% of

Time

Above 66.0 -3.29 25.03

57.0 - 66.0 From Above 1.97 18.22

57.0 - 66.0 From Below 21.22 19.05

Below 57.0 10.59 37.23

Buy/Hold = 7.11% Gain/Annum

S&P 500 Composite Index (2018-09-13 = 2904.18)

NDR Crowd Sentiment Poll (2018-09-13 = 67.4)

NED DAVIS RESEARCH GROUP 14Please see important disclosures at the end of this report.

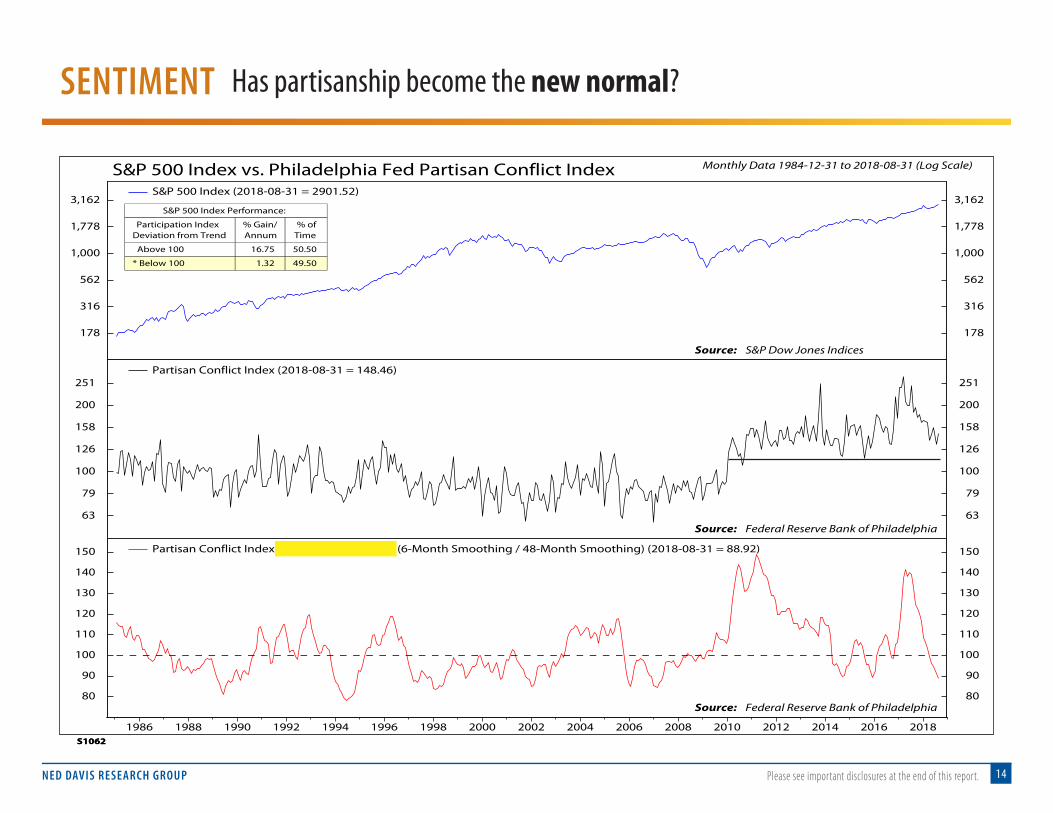

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S1062

S&P 500 Index vs. Philadelphia Fed Partisan Conflict Index Monthly Data 1984-12-31 to 2018-08-31 (Log Scale)

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S1062

S&P 500 Index vs. Philadelphia Fed Partisan Conflict Index Monthly Data 1984-12-31 to 2018-08-31 (Log Scale)

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

178

316

562

1,000

1,778

3,162

178

316

562

1,000

1,778

3,162S&P 500 Index (2018-08-31 = 2901.52)

S&P 500 Index Performance:

Participation IndexDeviation from Trend

% Gain/Annum

% ofTime

Above 100 16.75 50.50

* Below 100 1.32 49.50

Source: S&P Dow Jones Indices

63

79

100

126

158

200

251

63

79

100

126

158

200

251Partisan Conflict Index (2018-08-31 = 148.46)

Source: Federal Reserve Bank of Philadelphia

80

90

100

110

120

130

140

150

80

90

100

110

120

130

140

150Partisan Conflict Index Deviation from Trend (6-Month Smoothing / 48-Month Smoothing) (2018-08-31 = 88.92)

Source: Federal Reserve Bank of Philadelphia

SENTIMENT Has partisanship become the new normal?

NED DAVIS RESEARCH GROUP 15Please see important disclosures at the end of this report.

NED DAVIS RESEARCH 3600 VIEW OF U.S. STOCK MARKETSEPTEMBER 2018

Category Conclusion Comment

Fundamentals Neutral Good EPS growth, but mostly priced in

Macro Bullish Solid economy + modest inflation uptick

Sentiment Neutral Pessimism not extreme

Technicals

Bottom Line

NED DAVIS RESEARCH GROUP 16Please see important disclosures at the end of this report.

TECHNICAL Sell in May period even weaker in mid-term years.

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S01666

S&P 500 Cycle Composite for 2018 Daily Data 2017-12-29 to 2018-12-31

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S01666

S&P 500 Cycle Composite for 2018 Daily Data 2017-12-29 to 2018-12-31

2018Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019Jan

-4.0-3.5-3.0-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.53.03.54.04.55.05.56.06.57.07.58.08.59.09.5

10.010.511.011.512.012.5

-1.00

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

2018 Cycle CompositePlaces Equal Weight On:One-Year Seasonal CycleFour-Year Presidential Cycle10-Year Decennial Cycle

Trend Is More Important Than LevelBased on Daily Data 1/3/1928 - 12/31/2017

Lines represent cumulative year-to-date percent gains

S&P 500 Cycle Composite for 2018 (Scale Right)Actual S&P 500 Composite Through 2018-09-14 (Scale Left)

Source: S&P Dow Jones Indices

AVERAGE YEAR

2018

NED DAVIS RESEARCH GROUP 17Please see important disclosures at the end of this report.

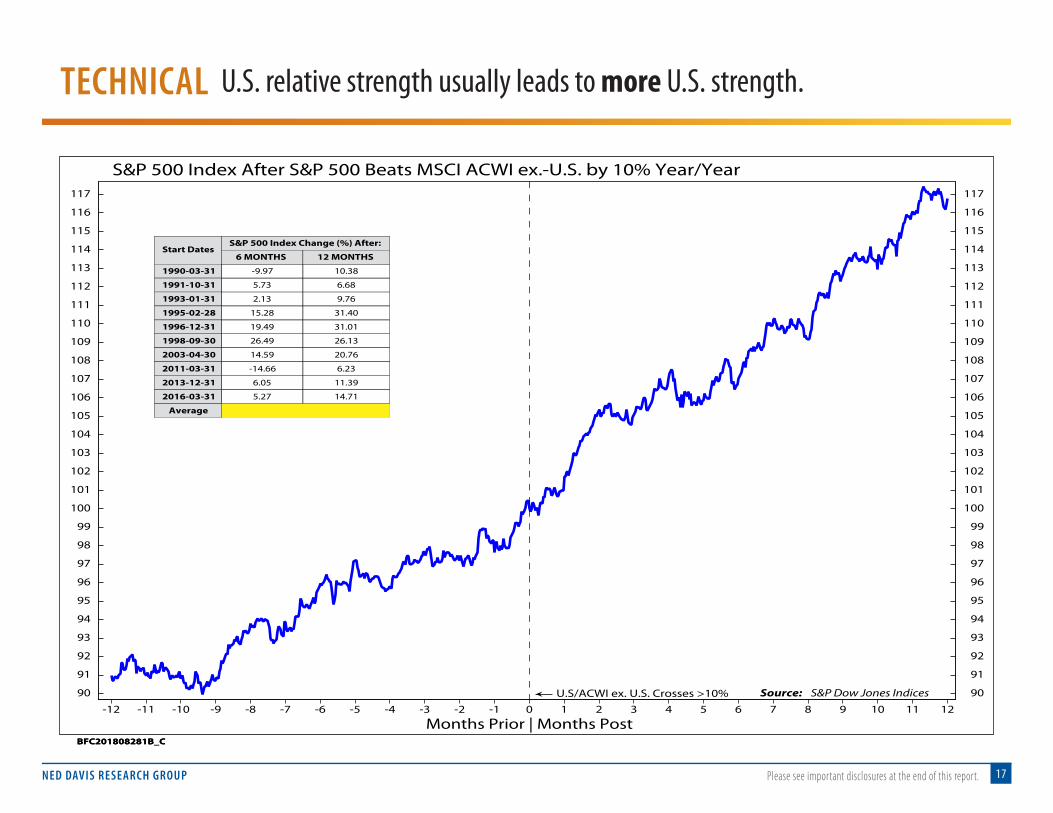

TECHNICAL U.S. relative strength usually leads to more U.S. strength.

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

BFC201808281B_C

S&P 500 Index After S&P 500 Beats MSCI ACWI ex.-U.S. by 10% Year/Year

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

BFC201808281B_C

S&P 500 Index After S&P 500 Beats MSCI ACWI ex.-U.S. by 10% Year/Year

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

U.S/ACWI ex. U.S. Crosses >10%

Months Prior | Months Post

Source: S&P Dow Jones Indices

Start DatesS&P 500 Index Change (%) After:

6 MONTHS 12 MONTHS

1990-03-31 -9.97 10.38

1991-10-31 5.73 6.68

1993-01-31 2.13 9.76

1995-02-28 15.28 31.40

1996-12-31 19.49 31.01

1998-09-30 26.49 26.13

2003-04-30 14.59 20.76

2011-03-31 -14.66 6.23

2013-12-31 6.05 11.39

2016-03-31 5.27 14.71

Average 7.04 16.85

NED DAVIS RESEARCH GROUP 18Please see important disclosures at the end of this report.

Breadth thrust elusive.TECHNICAL

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S45

Standard & Poor's 500 Stock Index Daily Data 1980-10-10 to 2018-09-14 (Log Scale)

© Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.See NDR Disclaimer at www.ndr.com/copyright.html For data vendor disclaimers refer to www.ndr.com/vendorinfo/

S45

Standard & Poor's 500 Stock Index Daily Data 1980-10-10 to 2018-09-14 (Log Scale)

NDR Multi-Cap Equity Series % of Stocks Above Their 10-Day Moving Averages

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

25

32

40

50

63

79

100

126

158

200

251

316

398

501

631

794

1,000

1,259

1,585

1,995

2,512

25

32

40

50

63

79

100

126

158

200

251

316

398

501

631

794

1,000

1,259

1,585

1,995

2,512

Event Date% Stocks

Above MA10

Days21

Days42

Days63

Days84

Days126

Days253

Days

1982-08-23 90.93 4.5 6.8 19.8 18.0 19.4 27.5 41.5

1984-08-03 91.02 1.1 1.6 0.1 3.2 0.3 10.0 17.4

1987-01-06 90.40 6.4 10.6 15.0 19.5 16.9 21.6 2.4

1991-02-06 91.68 1.9 4.7 4.3 5.7 6.0 9.1 15.6

1997-05-05 90.97 0.4 1.2 10.4 14.5 11.8 10.2 33.1

2002-10-21 90.73 1.0 -0.3 -1.7 -2.4 -5.7 2.1 14.5

2003-03-20 91.64 0.1 1.9 5.0 13.6 11.8 18.7 25.1

2004-04-01 92.01 0.2 -1.3 -0.6 -0.6 -2.9 -0.1 4.3

2004-05-26 90.44 1.9 1.7 -1.8 -0.9 -1.0 6.0 7.5

2007-03-21 91.77 0.3 3.4 6.3 5.4 6.9 6.5 -5.9

2008-11-04 92.64 -14.6 -16.0 -7.1 -15.9 -32.7 -9.8 6.1

2008-11-28 90.28 -1.8 -0.6 -7.9 -22.3 -9.5 5.4 23.7

2009-03-13 91.98 7.9 11.2 16.8 25.1 19.7 37.8 53.3

2009-10-14 90.25 -4.5 -0.4 2.0 5.2 0.3 9.2 7.7

2010-02-17 91.81 1.8 6.0 8.9 1.9 1.5 -0.6 21.5

2010-06-15 95.15 -6.6 -1.7 -3.2 0.5 5.6 11.2 13.5

Event Date% Stocks

Above MA10

Days21

Days42

Days63

Days84

Days126

Days253

Days

2010-07-13 96.02 1.7 -0.5 1.3 6.4 10.8 15.9 20.3

2010-09-02 93.77 3.3 4.3 9.5 12.1 16.7 21.2 7.7

2011-03-30 90.40 -1.0 2.7 1.3 -1.6 -2.7 -13.3 6.0

2011-07-01 96.07 -2.6 -6.4 -9.0 -15.5 -6.4 -6.1 2.6

2011-08-29 97.41 -3.1 -4.9 6.2 -1.4 3.3 12.9 16.6

2011-10-10 92.94 5.0 6.8 3.3 8.1 13.1 14.5 19.9

2011-11-30 93.65 -2.8 0.9 6.2 9.8 13.8 2.5 12.8

2011-12-27 91.93 2.1 4.0 8.4 11.1 10.9 5.2 12.7

2012-07-03 92.46 -0.1 -0.7 2.4 5.2 2.9 6.7 20.3

2012-11-23 90.34 0.6 1.2 6.7 6.2 10.9 17.8 27.9

2013-12-24 92.38 0.3 -2.8 0.6 0.9 2.0 6.8 13.9

2014-08-19 90.65 1.0 1.5 -4.8 3.0 1.6 5.8 2.7

2014-10-21 93.23 3.6 5.5 6.7 6.3 8.7 8.8 5.7

2015-10-09 91.48 3.0 3.2 1.6 -4.5 -8.1 2.3 6.0

2016-02-22 92.38 2.9 5.4 7.5 5.5 7.4 12.3 21.5

Stats show % change in S&P 500 N-Days after event

Combined statistics for all dates

Summary Item 10Days

21Days

42Days

63Days

84Days

126Days

253Days

Mean 0.44 1.58 3.68 3.93 4.29 8.98 15.42

Median 0.96 1.56 3.30 5.22 5.64 8.84 13.93

Number Up 22 20 23 22 23 26 30

Number Down 9 11 8 9 8 5 1

All Periods Mean 0.37 0.78 1.56 2.33 3.13 4.75 9.94

Arrows show initial dates when indicator rose above90% after falling to at least 10% in between.

Source: S&P Dow Jones Indices

0

25

50

75

0

25

50

75

Source: Ned Davis Research, Inc. 2018-09-14 = 58.8

2.5 YRS W/O BREADTH THRUST

NED DAVIS RESEARCH GROUP 19Please see important disclosures at the end of this report.

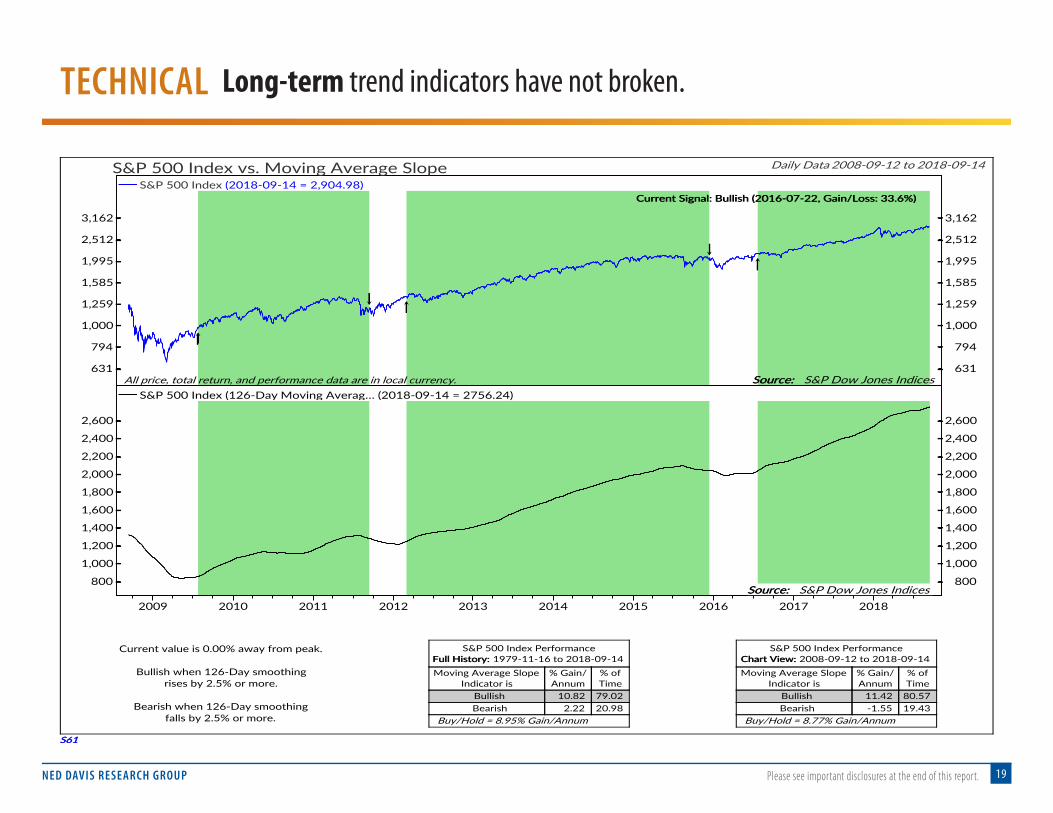

Long-term trend indicators have not broken.TECHNICAL

S61S61

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

631

794

1,000

1,259

1,585

1,995

2,512

3,162

631

794

1,000

1,259

1,585

1,995

2,512

3,162

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

Source:Source: S&P Dow Jones Indices

Current Signal: Bullish (2016-07-22, Gain/Loss: 33.6%)Current Signal: Bullish (2016-07-22, Gain/Loss: 33.6%)

All price, total return, and performance data are in local currency.

Source:Source: S&P Dow Jones Indices

Daily Data 2008-09-12 to 2018-09-14S&P 500 Index vs. Moving Average Slope

Current value is 0.00% away from peak.

Bullish when 126-Day smoothing

rises by 2.5% or more.

Bearish when 126-Day smoothing

falls by 2.5% or more.

S&P 500 Index Performance

Full History:Full History: 1979-11-16 to 2018-09-14

Moving Average Slope

Indicator is

% Gain/

Annum

% of

Time

Bullish 10.82 79.02

Bearish 2.22 20.98

Buy/Hold = 8.95% Gain/Annum

S&P 500 Index Performance

Chart View:Chart View: 2008-09-12 to 2018-09-14

Moving Average Slope

Indicator is

% Gain/

Annum

% of

Time

Bullish 11.42 80.57

Bearish -1.55 19.43

Buy/Hold = 8.77% Gain/Annum

S&P 500 Index (2018-09-14 = 2,904.98)

S&P 500 Index (126-Day Moving Averag… (2018-09-14 = 2756.24)

NED DAVIS RESEARCH GROUP 20Please see important disclosures at the end of this report.

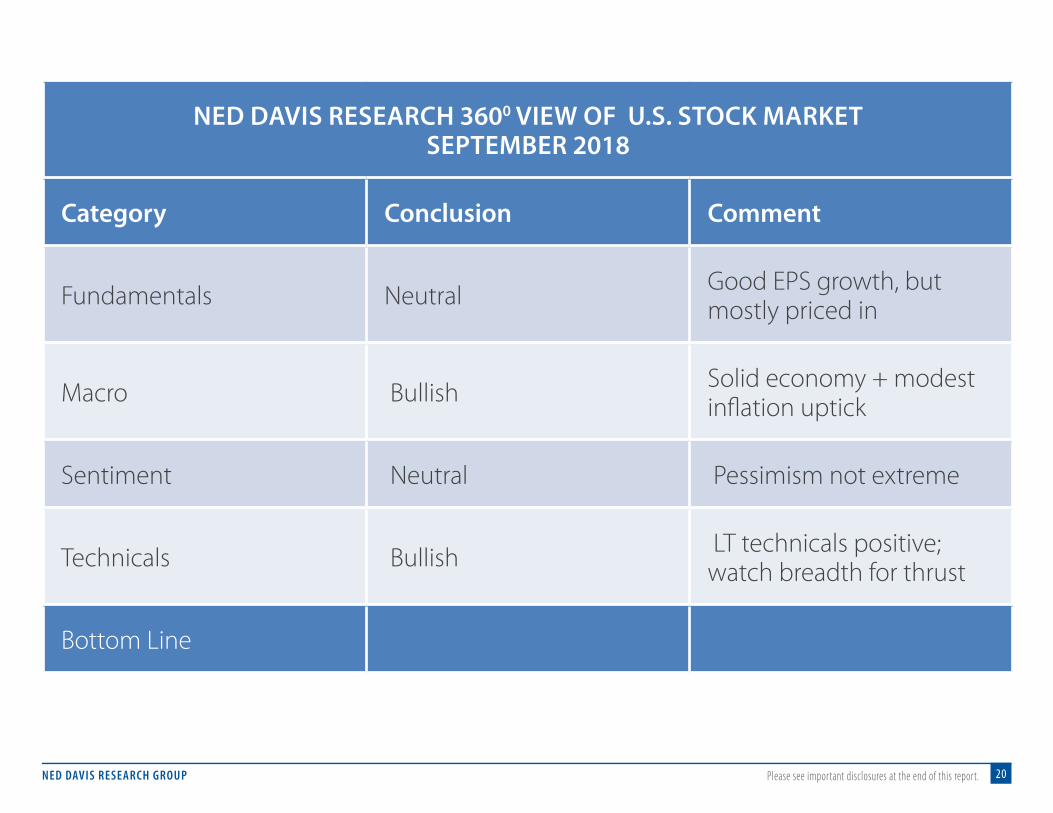

NED DAVIS RESEARCH 3600 VIEW OF U.S. STOCK MARKETSEPTEMBER 2018

Category Conclusion Comment

Fundamentals Neutral Good EPS growth, but mostly priced in

Macro Bullish Solid economy + modest inflation uptick

Sentiment Neutral Pessimism not extreme

Technicals Bullish LT technicals positive; watch breadth for thrust

Bottom Line

NED DAVIS RESEARCH GROUP 21Please see important disclosures at the end of this report.

Watch long-term technicals and interest rates.BOTTOM LINE

NDR U.S. STOCK MARKET MODEL

LONG TERM

SHORT TERM

NED DAVIS RESEARCH GROUP 22Please see important disclosures at the end of this report.

NED DAVIS RESEARCH 3600 VIEW OF U.S. STOCK MARKETSEPTEMBER 2018

Category Conclusion Comment

Fundamentals Neutral Good EPS growth, but mostly priced in

Macro Bullish Solid economy + modest inflation uptick

Sentiment Neutral Pessimism not extreme

Technicals Bullish LT technicals positive; watch breadth for thrust

Bottom Line Bullish Positive technicals deciding factor

NED DAVIS RESEARCH GROUP 23Please see important disclosures at the end of this report.

Q & A

Ned DavisResearch

Group

NED DAVIS RESEARCH GROUP 24Please see important disclosures at the end of this report.

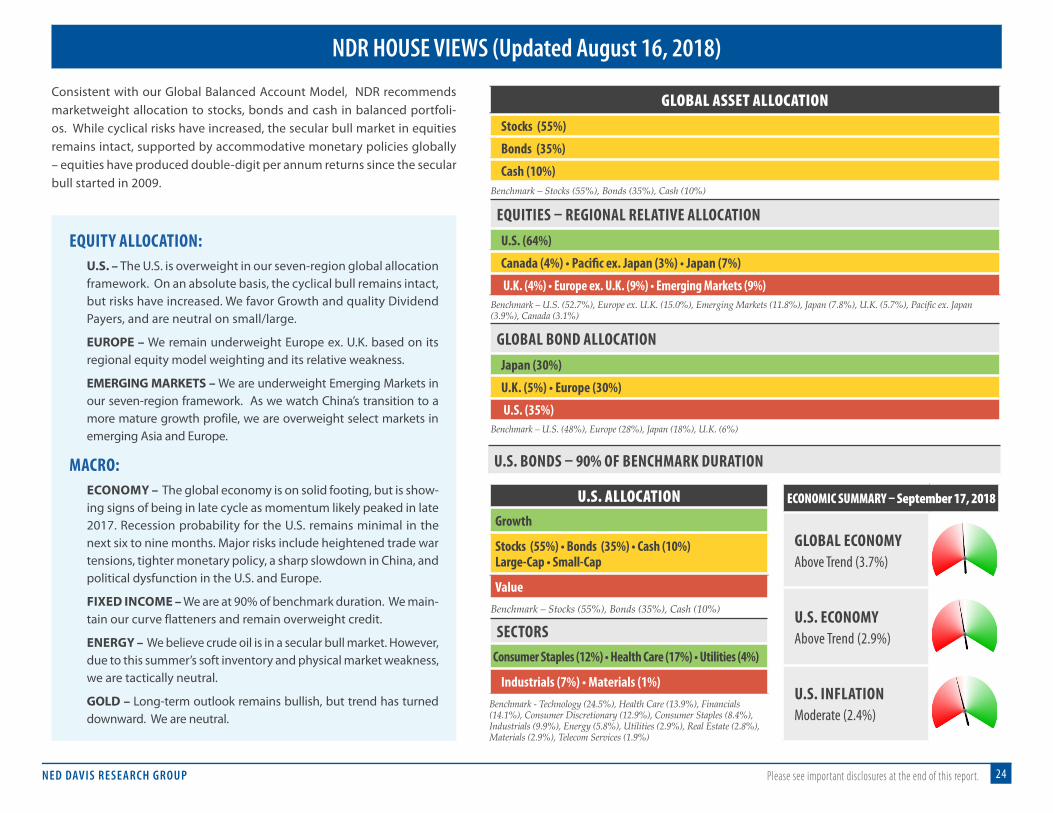

Consistent with our Global Balanced Account Model, NDR recommends marketweight allocation to stocks, bonds and cash in balanced portfoli-os. While cyclical risks have increased, the secular bull market in equities remains intact, supported by accommodative monetary policies globally – equities have produced double-digit per annum returns since the secular bull started in 2009.

EQUITY ALLOCATION: U.S. – The U.S. is overweight in our seven-region global allocation framework. On an absolute basis, the cyclical bull remains intact, but risks have increased. We favor Growth and quality Dividend Payers, and are neutral on small/large.

EUROPE – We remain underweight Europe ex. U.K. based on its regional equity model weighting and its relative weakness.

EMERGING MARKETS – We are underweight Emerging Markets in our seven-region framework. As we watch China’s transition to a more mature growth profile, we are overweight select markets in emerging Asia and Europe.

MACRO: ECONOMY – The global economy is on solid footing, but is show-ing signs of being in late cycle as momentum likely peaked in late 2017. Recession probability for the U.S. remains minimal in the next six to nine months. Major risks include heightened trade war tensions, tighter monetary policy, a sharp slowdown in China, and political dysfunction in the U.S. and Europe.

FIXED INCOME – We are at 90% of benchmark duration. We main-tain our curve flatteners and remain overweight credit.

ENERGY – We believe crude oil is in a secular bull market. However, due to this summer’s soft inventory and physical market weakness, we are tactically neutral.

GOLD – Long-term outlook remains bullish, but trend has turned downward. We are neutral.

ECONOMIC SUMMARY – September 17, 2018

GLOBAL ECONOMYAbove Trend (3.7%)

U.S. ECONOMYAbove Trend (2.9%)

U.S. INFLATIONModerate (2.4%)

U.S. BONDS – 90% OF BENCHMARK DURATION

U.S. ALLOCATIONGrowth

Stocks (55%) • Bonds (35%) • Cash (10%) Large-Cap • Small-Cap

ValueBenchmark – Stocks (55%), Bonds (35%), Cash (10%)

SECTORSConsumer Staples (12%) • Health Care (17%) • Utilities (4%)

Industrials (7%) • Materials (1%)Benchmark - Technology (24.5%), Health Care (13.9%), Financials (14.1%), Consumer Discretionary (12.9%), Consumer Staples (8.4%), Industrials (9.9%), Energy (5.8%), Utilities (2.9%), Real Estate (2.8%), Materials (2.9%), Telecom Services (1.9%)

NDR HOUSE VIEWS (Updated August 16, 2018)

GLOBAL ASSET ALLOCATIONStocks (55%)

Bonds (35%)

Cash (10%)Benchmark – Stocks (55%), Bonds (35%), Cash (10%)

EQUITIES – REGIONAL RELATIVE ALLOCATIONU.S. (64%)

Canada (4%) • Pacifi c ex. Japan (3%) • Japan (7%)

U.K. (4%) • Europe ex. U.K. (9%) • Emerging Markets (9%)Benchmark – U.S. (52.7%), Europe ex. U.K. (15.0%), Emerging Markets (11.8%), Japan (7.8%), U.K. (5.7%), Pacific ex. Japan (3.9%), Canada (3.1%)

GLOBAL BOND ALLOCATIONJapan (30%)

U.K. (5%) • Europe (30%)

U.S. (35%)Benchmark – U.S. (48%), Europe (28%), Japan (18%), U.K. (6%)

Ned DavisResearch

Group

Chief U.S. Strategist

Ed Clissold, CFA, is the Chief U.S. Strategist for Ned Davis Research Group. He and his team are responsible for the firm’s U.S. equity, style, sector and equity theme analysis. They do so via a combination of a top-down analysis of the macroeconomic and fundamental environments and a bottom-up analysis of factors specific to the asset class, market cap, style, sector, or theme. He and his team also provide in-depth macro research on fundamental topics such as earnings, dividends, and cash flow.

Ed writes several U.S. Strategy publications, which provide an intermediate-term outlook on U.S. markets via a combination of top-down and bottom-up analyses. He also writes a quarterly Benchmarks report, which analyzes the attribution of returns across asset classes, sectors, market cap, and styles.

Ed’s market commentary is often quoted in The Wall Street Journal, Barron’s, and other financial publications.

Ed has held a number of other positions since joining the firm in 2002, including Global Equity Strategist, Senior Global Analyst in the Global Asset Allocation group, and Analyst in the Custom Research Services department. Previously, Ed worked at Strong Capital Management and as a Market Strategist at J.C. Bradford & Co.

Ed is a CFA charterholder, a magna cum laude graduate in Economics from Transylvania University, and has earned his Masters in Business Administration in Finance, with distinction, from Indiana University (Kelley).

ED CLISSOLD, CFA

@edclissold

www.linkedin.com/in/edclissold

Important Information and Disclaimers

VENICE600 Bird Bay Drive West Venice, FL 34285(941) 412-2300

NEW YORK1120 Avenue of the Americas6th fl oorNew York, NY 10036(646) 810-7270

BOSTON745 Atlantic AveBoston, MA 02110(617) 279-4860

ATLANTA400 Northridge RoadSuite 515Atlanta, GA 30350(678) 303-0097

SAN FRANCISCO50 California StreetSuite 1500San Francisco, CA 94111(415) 277-5477

LONDON29 Ludgate HillLondonEC4M 7NX+44 (0) 20 7779-8682

HONG KONG38/F Hopewell Centre183 Queen’s Road EastWanchai+852 3416 6676

NED DAVIS RESEARCH GROUPsales @ndr.comwww.ndr.com(800) 241-0621

Ned Davis Research, Inc. (NDR), any NDR affi liates or employees, or any third-party data provider, shall not have any liability for any loss sustained by anyone who has relied on the information contained in any NDR publication. In no event shall NDR, any NDR affi liates or employees, or any third-party data provider, be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profi ts and opportunity costs) in connection with any use of the information contained in this document even if advised of the possibility of such damages.

The data and analysis contained in NDR’s publications are provided “as is” and without warranty of any kind, either expressed or implied. The information is based on data believed to be reliable, but it is not guaranteed. NDR DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

NDR’s reports refl ect opinions of our analysts as of the date of each report, and they will not necessarily be updated as views or information change. All opinions expressed therein are subject to change without notice, and you should always obtain current information and perform due diligence before trading. NDR or its affi liated companies or their respective shareholders, directors, offi cers and/or employees, may have long or short positions in the securities discussed in NDR’s publications and may purchase or sell such securities without notice.

NDR uses and has historically used various methods to evaluate investments which may, at times, produce contradictory recommendations with respect to the same securities. When evaluating the results of prior NDR recommendations or NDR performance rankings, one should also consider that NDR may modify the methods it uses to evaluate investment opportunities from time to time, that model results do not impute or show the compounded adverse eff ect of transaction costs or management fees or refl ect actual investment results, that other less successful recommendations made by NDR are not included with these model performance reports, that some model results do not refl ect actual historical recommendations, and that investment models are necessarily constructed with the benefi t of hindsight. Unless specifi cally noted on a chart, report, or other device, all performance measures are purely hypothetical, and are the results of back-tested methodologies using data and analysis over time periods that pre-dated the creation of the analysis and do not refl ect tax consequences, execution, commissions, and other trading costs. For these and for many other reasons, the performance of NDR’s past recommendations and model results are not a guarantee of future results.

Using any graph, chart, formula, model, or other device to assist in deciding which securities to trade or when to trade them presents many diffi culties and their eff ectiveness has signifi cant limitations, including that prior patterns may not repeat themselves continuously or on any particular occasion. In addition, market participants using such devices can impact the market in a way that changes the eff ectiveness of such devices. NDR believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision and suggests that all market participants consider diff ering viewpoints and use a weight of the evidence approach that fi ts their investment needs. Any particular piece of content or commentary may or may not be representative of the NDR House View, and may not align with any of the other content or commentary that is provided in the service. Performance measures on any chart or report are not intended to represent the performance of an investment account or portfolio, as some formulas or models may have superior or inferior results over diff ering time periods based upon macro-economic or investment market regimes. NDR generally provides a full history of a formula or model’s hypothetical performance, which often refl ects an “all in” investment of the represented market or security during “buy”, “bullish”, or similar recommendations. This approach is not indicative of the intended usage of the recommendation in a client’s portfolio, and for this reason NDR does not typically display returns as would be commonly stated when reporting portfolio performance. Clients seeking the usage of any NDR content in a simulated portfolio back-test should contact their account representative to discuss testing that NDR can perform using the client’s specifi c risk tolerances, fees, and other constraints.

NDR’s reports are not intended to be the primary basis for investment decisions and are not designed to meet the particular investment needs of any investor. The reports do not address the suitability of any particular investment for any particular investor. The reports do not address the tax consequences of securities, investments, or strategies, and investors should consult their tax advisors before making investment decisions. Investors should seek professional advice before making investment decisions. The reports are not an off er or the solicitation of an off er to buy or to sell a security.

Further distribution prohibited without prior permission. Full terms of service, including copyrights, terms of use, and disclaimers are available at https://www.ndr.com/web/ndr/terms-of-service. For data vendor disclaimers, refer to www.ndr.com/vendorinfo.

Copyright 2018 (c) Ned Davis Research, Inc. All rights reserved.

Founded in 1980, Ned Davis Research Group is a leading independent research fi rm with clients around the globe. With a

range of products and services utilizing a 360° methodology, we deliver award-winning solutions to the world’s leading

investment management companies. Our clients include professionals from global investment fi rms, banks, insurance

companies, mutual funds, hedge funds, pension and endowment funds, and registered investment advisors.

Generate alpha. Identify risk. Choose Ned Davis Research. Macro

Sentiment

Fundamental

Technical

Idea

360° APPROACH