Beyond classical growth theory Human capital, Endogenous growth Growth and development.

Natural Disasters in a Two-Sector Model of

Endogenous Growth∗

Masako Ikefuji† Ryo Horii‡

January 3, 2008

Abstract

This paper studies sustainability of economic growth considering the riskof natural disasters caused by pollution in an endogenous growth model withphysical and human capital accumulation. We consider an environmental taxpolicy, and show that economic growth is sustainable only if the tax rate on thepolluting input is increased over time and that the long-term rate of economicgrowth follows an inverted V-shaped curve relative to the growth rate of theenvironmental tax. The social welfare is maximized under a positive steady-state growth in which faster accumulation of human capital compensates theproductivity loss due to declining use of the polluting input.Keywords: natural disasters, human capital, endogenous depreciation, eco-nomic growth.JEL Classification Numbers: O41, O13, E22.

∗We are grateful to Kazumi Asako, Koichi Futagami, Tatsuro Iwaisako, Kazuo Mino, Takumi

Naito, Tetsuo Ono, Yoshiyasu Ono, Makoto Saito, Yasuhiro Takarada, and seminar participants at

Fukushima University, Nagoya University, Osaka University, and Toyama University for their helpful

comments and suggestions. This study is partly supported by JSPS Grant-in-Aid for Scientific

Research (No. 16730097). All remaining errors are naturally our own.

†Fondazione Eni Enrico Mattei, Corso Magenta, 63, 20123 Milano, Italy. E-mail:

‡Graduate School of Economics, Tohoku University, Kawauchi 27-1, Aoba-ku, Sendai 980-8576,

Japan. E-mail: [email protected]

1

1 Introduction

Natural disasters have a large impact on economic activity primarily through de-

struction of capital stock. For example, National Oceanic and Atmospheric Admin-

istration (NOAA, 2005) estimates that Hurricane Katrina, occurred on August 2005

in the Gulf of Mexico, caused over 100 billion dollars’ worth of damage mainly on

physical capital. This magnitude of destruction might seem unusual, but the losses

caused by landfalling hurricanes in the United States in the previous year, 2004, were

also considerably large—approximately 45 billion dollars, as reported by NOAA. This

magnitude of damage is not negligible even in comparison to the whole size of the

U.S. physical capital stock.

Despite various forms of preventive efforts, the occurrence of natural disasters is

not declining but in a growing trend.1 The long-term consequence of the increased

possibility of such disasters critically hinge on whether their occurrences are purely

exogenous phenomena to the economic system, or they are caused for some part by

economic activity. That is, if the latter is true, economic growth itself creates a threat

to economic activity, making the sustainability of economic growth questionable.

Recent meteorological research shows that, unfortunately, the latter argument is

likely to be true. For example, it is clearly stated in the Intergovernmental Panel on

Climate Change third assessment report (IPCC, 2001) that “Emissions of greenhouse

gas and aerosols due to human activities have a great impact on global climate

change.” Global warming, or more specifically, increasing sea surface temperature,2

1In Hoyois et al. (2005), the global number of reported disasters is 1.55 times higher in 2000-

2004 period than in 1995-1999 period, and the number of reported extreme temperature disasters,

floods, and people affected by disasters are almost 2 times, 1.74 times, and 1.33 times higher,

respectively. A disaster in the database must be fulfilled at least one of the following criteria: 10

or more people reported killed; 100 people reported affected; declaration of a state of emergency;

call for international assistance.

2The tropical sea surface temperature in the North Atlantic shows a large upswing in the last

decade. Emamuel (2005) argues such a upswing is related to the El Nino and reflects the effect of

global warming.

2

is in turn suspected to increase hurricane frequency and intensity (Emamuel, 2005;

Webster et al., 2005).

Those observations suggest that there is a two-way causality between economic

activities and the occurrence of natural disasters. This paper investigates the sustain-

ability of economic growth in the presence of this two-way causality, by introducing

the endogenous risk of natural disasters into a Uzawa-Lucas type of endogenous

growth model. Following the literature (e.g., Copeland and Taylor, 1994; Bovenberg

and Smulders, 1995; Stokey, 1998), we assume that polluting inputs such as fossil

fuels are necessary for economic activities and those inputs are subject to an envi-

ronmental tax.3 Differently from earlier studies, however, this paper examines the

case in which the use of polluting inputs raises the probability that capital stocks

are destroyed by natural disasters. Agents make saving decisions taking into account

the possibilities of loss of asset due to natural disasters.

Using the model, we show that the economic growth is, in fact, not sustainable

if the (per-unit) tax rate on polluting inputs is kept constant. Intuitively, under the

constant tax rate, firms are willing to use increasing amounts of polluting inputs as

the economy grows. However, as increased use of polluting inputs raises the risk of

natural disasters, it reduce incentive agents to invest in capital stock since they face

a higher possibilities of asset loss. Thus, even in the long run, capital stock cannot

exceed a constant threshold under a constant tax rate.

To overcome this limitation, we next consider a time-varying tax on polluting in-

puts. If the per-unit tax rate is raised over time, private firms owing a Cobb-Douglas

production technology will increase the use of other inputs, including human cap-

ital, relative to polluting inputs. As a result, the use of polluting inputs can be

bounded above, making the economic growth sustainable. It is also shown that the

growth rate of environmental tax has both positive and negative effects on economic

growth. The faster the rate at which the environmental tax is increased, the lower is

3Copeland and Taylor (1994) and Stokey (1994) assumed that there are a continuum of technol-

ogy generating a different level of pollution. However, the technology can be written with capital

and the total level of pollution as inputs.

3

the asymptotic amount of pollution and therefore the lower is probability of disasters.

This gives households more incentive to save, which promotes growth. However, the

increased cost of using polluting input faced by private firms reduces their produc-

tivity at each date, which has a negative effect on growth. Due to those opposite

effects, the rate of economic growth rate is shown to follow an inverted V-shaped

curve relative to the growth rate of environmental tax.

Having shown that the sustained growth is feasible, this paper then examine

whether it is desirable or not. This question may seem trivial, but in a AK-growth

model with pollution Stokey (1998) shows that, even when production technology

allows sustained growth, it is theoretically possible that agents prefer a no-growth

state with a good environment.4 Contrary to Stokey’s analysis, we show that the

social welfare is maximized on a steady-state growth path, where the environmental

tax is raised at a positive rate, although this does not coincide with the growth

maximizing path.

The difference of our result from Stokey’s stems not from our assumption that the

use of polluting input only affects the risk of natural disasters without directly affect-

ing consumer’s utility.5 Rather, it comes from the our two-sector specification that

the growth is driven both by physical and human capital accumulation. This paper’s

analysis shows that sustained growth with a Cobb-Douglas technology is feasible

under a limited use of polluting input because human capital stock is accumulated

much faster than the rate at which output is increased. In fact, provided that human

capital stock has lower degree of vulnerability to disasters, as suggested by Skidmore

4Stokey (1998) assumed additive separable preference for consumption and pollution in which

the marginal utility from consumption is declining whereas the marginal disutility from pollution is

increasing. Then, as consumption increases due to capital accumulation, reducing pollution becomes

more important than increasing consumption. She shows that further growth is not optimal at a

high level of capital stock.

5In section 5, we examine the case in which pollution directly causes disutility to consumers, in

addition to raising the risk of disasters. It is shown that a positive steady-state growth is compatible

to welfare maximization even in this case.

4

and Toya (2002), the risk raises incentives for more investment in human capital

stock relative to physical capital stock.

To our best knowledge, this study is a first attempt to examine the consequences

of natural disasters in an endogenous growth model. This does not mean, of course,

that our study is independent from the previous literature. In fact, great attention

has been paid to the sustainability of economic growth in the literature of growth

theory, by noticing that the finite nature of natural environment may potentially

restrict sustainability of economic growth. With regard to the finiteness of natu-

ral resources, Aghion and Howitt (1998), Scholz and Ziemes (1999), Schou (2000),

Grimaud and Rouge (2003), and Agnai, Gutierrez and Iza (2005) examined sus-

tainability of economic growth in endogenous growth models with non-renewable

resources.6

Complementary to those studies, Stokey (1998) and Uzawa (2003) examined sus-

tainability focusing on emission of pollutants. Since the global atmosphere is finite,

the negative effects from pollutants will become unacceptably serious when the us-

age of polluting input increases without bound. Therefore, both Stokey (1998) and

Uzawa (2003) concludes that, without exogenous technological change, it is opti-

mal for the economy to converge to a no-growth steady state. Their conclusions

are different from ours because they consider only accumulation of physical capital,

whereas we consider both human and physical capital. In this respect, our study is

more related to a two sector model developed by Bovenberg and Smulders (1995),

where accumulation of knowledge is explicitly incorporated. Specifically, Bovenberg

and Smulders (1995) assumed that the amount of pollution cannot be increased in

the long-run and showed that, if output can grow at the same rate as that of physical

and human capital for a constant level of pollution,7 sustained growth is both feasible

6For example, Grimaud and Rouge (2003) analyzed sustainability of economic growth intro-

ducing a non-renewable natural resource into a Schumpeterian endogenous growth model. They

showed that whether both optimal and equilibrium growth is positive at the steady-state depends

on the value of the subjective discount rate relative to the productivity of R&D.

7They focused on the case in which the production function exhibits constant rate to scale

5

and optimal.

While their conclusions are similar to ours, the settings in the model differs in two

respects. First, we does not assume that pollution cannot increase in the long run,

but show that a path in which pollution increases without bound is not chosen in

equilibrium since it reduces the incentive to save of consumers, who face increasingly

high possibility of asset losses due to disasters. Second, we consider a more natural

setting in which the production function exhibits constant return to scale with respect

to all production factors—including polluting inputs. This means that, if the amount

of pollution is fixed, the production function faces decreasing returns to scale (DRS).

We show that, even under this more severe condition, sustained growth is both

feasible and desirable since the DRS can be overcome by accumulating human capital

more rapidly than the rate of economic growth.

The rest of the paper is organized as follows. Section 2 presents the model

and proves that growth cannot be sustained under a constant tax rate on polluting

inputs. The steady-state growth with an increasing environmental tax is analyzed in

Section 3. The social planners’s problem is examined in Section 4 so as to investigate

the desirability of sustained growth. Section 5 considers an extension of the model

in which pollution harms the utility of consumers as well as increases the risk of

disasters. Section 6 concludes.

2 The Model

This section presents a model of natural disasters and economic growth. In the first

subsection, the risk of natural disasters is introduced into a two-sector growth model

based on Uzawa (1965) and Lucas (1998). In the second subsection, the behavior of

households and firms is examined. The third subsection summarizes the equilibrium

(CRS) with respect to Kt and (HtPt), where Pt represents the level of pollution. This means that,

if all production factors Kt, Ht and Pt, are doubled, the output is more than doubled; i.e., the

production function exhibits increasing returns to scale with respect to Kt, Ht and Pt. In contrast,

we maintain a standard setting in which output is CRS with respect to all production factors.

6

conditions. The final subsection proves that sustained growth is not possible when

the environmental tax rate is kept constant.

2.1 The risk of natural disasters

In the model, output is produced by a constant-returns-to-scale production technol-

ogy using physical capital Kt, human capital Ht, and polluting input Pt such as fossil

fuels that emits pollutants or greenhouse gases. The production function is given by:

Yt = F (Kt, utHt, Pt) = AKαt (utHt)

1−α−βP βt , (1)

where ut ≥ 0 is the time share devoted to production of goods, α ∈ (0, 1/2) is a

constant share of physical capital,8 and β ∈ (0, 1− α) is that of the polluting input.

Note that production function (1) exhibits constant returns to scale with respect to

all inputs including Pt. Output is either consumed or added to physical capital stock.

Since we focus on the risk of natural disasters, we ignore the extraction cost and/or

production cost of polluting inputs and finite nature of natural resources. The risk

of natural disasters on capital stock is assumed to be inevitable and to depend on

the amount of pollution.

Specifically, suppose that economy consists of continuum of local areas. Let qt be

the arrival rate of natural disasters per unit of time at each area:

qt = q + qPt, (2)

where q and q are positive constants. Equation (2) says that the arrival rate raises

as the amount of aggregate polluting inputs increases, as in the case of hurricanes

and fossil fuels. When a natural disaster occurs at an area, it causes damage to

physical capital. For example, if natural disasters occur at an area where the existing

aggregate physical capital stock is Kt, the expected loss of physical capital is ϕKt,

where ϕ > 0 is the average damage to physical capital stock. Note that, for various

8We assume α < 1/2 for simplicity of the stability analysis. In a model where human capital is

considered explicitly, this assumption seems quite reasonable.

7

reasons, a natural disaster harms human capital stock as well.9 Similarly to ϕ, define

ψ > 0 as the average damage to human capital stock. The damage on human capital

measured in relative to the size of the existing stock is typically smaller than the

damage on physical capital, which implies that ϕ would be smaller than ψ.

For simplicity, each area is assumed to be small enough and the occurrence of

natural disasters in one area is assumed not to be correlated to others.10 By the

law of large numbers with (2), the aggregate damage to physical capital stock and

human capital stock are respectively:

qt · ϕKt = (ϕq + ϕqPt)Kt, (3)

qt · ψHt = (ψq + ψqPt)Ht. (4)

Let δK and δH be the constant rates of depreciation of physical capital stock and

human capital stock, respectively. Then, similarly to Lucas (1988), the resource

constraints for physical and human capital stocks are written as:

Kt = F (Kt, utHt, Pt) − Ct − (δK + ϕPt)Kt, (5)

Ht = B(1 − ut)Ht − (δH + ψPt)Ht, (6)

where δK ≡ δK + ϕq, ϕ ≡ ϕq, δH ≡ δH + ψq, ψ ≡ ψq, and Ct, B, and 1 − ut are

the aggregate consumption, the constant productivity of human capital accumula-

tion, and the fraction of time devoted to production of human capital, respectively.

Equations (5) and (6) shows that the risk of natural disasters effectively augments

the depreciation rates of physical and human capital stocks, in proportion to the use

of polluting input.

9The death toll in Katrina rose to over 1000 (NOAA, 2005) and the number of the injured was

much more. In addition, many education institutions are forced to remain closed for extended

periods of time and a large number of data and documents storing valuable knowledge are lost after

the disasters pass.

10This assumption is not realistic when considering large scale disasters. Without it, the law of

large numbers does not apply, and disasters cause short-term fluctuations. However, since we are

focusing on long-term behavior of the economy, analysis of such fluctuations are out of the scope

of this paper.

8

Observe that, unlike standard endogenous growth models, the right hand sides of

equations (5) and (6) are not homogenous of degree one in terms of quantities. This

implies that balanced growth that exhibits a homothetic expansion is not feasible,

reflecting the finiteness of natural environment.

2.2 The market economy

Since firms do not take into consideration the externality that the use of polluting

inputs increases the risk of natural disasters, the market equilibrium does not cor-

respond with the solution of the social planner’s problem. The followings consider

explicitly the market economy where per-unit tax τt, in terms of final goods, is levied

on the use of polluting inputs. The government balances its budget at each moment

and equally distribute the tax revenue Tt = τtPt among households in a lump-sum

fashion.

Households

The economy is populated by a unit mass of infinitely lived homogeneous house-

holds. Each household owns physical capital stock, kt, and human capital stock, ht.

However, due to natural disasters, they are faced with the risk of damages to both

types of capital stock. The insurance market is assumed to be complete. Under

this assumption, it is optimal for households to take out insurance that cover the all

losses associated with natural disasters. Since their expected damages to physical

capital stock and human capital stock are qtϕkt and qtψht, respectively, the budget

9

constraint of households can be written as:11

kt = rtkt + wtutht − (δK + ϕPt)kt − ct + Tt, (7)

ht = B(1 − ut)ht − (δH + ψPt)ht, (8)

where rt, wt, and ct denote the real interest rate, the real wage rate, and the amount

of consumption, respectively. Note that the cost associated with depreciation and

insurance is paid by the owner of the capital.

The utility function of the representative household is given by:∫ ∞

0

c1−θt − 1

1 − θe−ρtdt, (9)

where θ > 1 is the inverse of the elasticity of intertemporal substitution and ρ is the

rate of time preference. We assume B − δH > ρ so that households have enough

incentive to investment in human capital. Given the time paths of rt, wt, Pt, τt and

Tt, each household maximizes (9) subject to the constraints (7) and (8). From the

first-order condition for maximization problem, we obtain the Keynes-Ramsey Rule:

−θct

ct

= ρ + ϕPt + δK − rt. (10)

This condition is similar to that obtained in the original Uzawa-Lucas model, except

that the depreciation rate is augmented by the risk of natural disasters, ϕPt.

The shadow price of human capital relative to that of physical capital is wt/B,

which equals to the market price of human capital measured by physical capital

stock. Hence, the arbitrage condition between human capital investment and physical

capital investment is given by:

wt

wt

= rt − (ϕ − ψ)Pt − (δK − δH) − B. (11)

11Equations (7)-(8) implicitly assume that damaged human capital is compensated in the form of

human capital. Obviously, a more realistic setting is that this compensation is done in the form of

goods. Nonetheless, as long as the amount of compensation in terms of goods is calculated using the

appropriate price of human capital, wt/B, the equilibrium outcomes do not change in the aggregate

level.

10

In (11), the left hand side implies the rate of change in the relative shadow price of

human and physical capital while the right hand side implies the difference between

the marginal return to investment in physical capital and human capital. Note that

this condition must be satisfied in the long run. If it is not, the solution would be

either ut = 0 or ut = 1 for all agents, and therefore one of the two kinds of aggregate

capital stock approaches zero due to depreciation. However, it raises the shadow

price of the unaccumulated type of capital stock, which is at odds with the decision

of agents that they do not invest in that type of capital stock. The transversality

conditions (TVCs) for physical capital stock and human capital stock, respectively,

are

limt→∞

ktc−θt e−ρt = 0, and (12)

limt→∞

ht(wt/B)c−θt e−ρt = 0, (13)

where c−θt and (wt/B)c−θ

t represent shadow prices of physical and human capital.

Firms

There are a continuum of firms producing final goods in competitive market. We

consider a representative firm maximizing its profit. The firm pays the wages for

labor input, the rental rate for physical capital input, and the environmental tax as

well. Given factor prices rt, wt and τt, the profit maximization problem is:

maxKt,Nt,Pt

F (Kt, Nt, Pt) − rtKt − wtNt − τtPt,

where Nt ≡ utHt is the amount of human capital employed by the firm. The first-

order conditions for this problem are rt = αYt/Kt, wt = (1 − α − β)Yt/Nt, and

τt = βYt/Pt. Substituting the profit maximizing polluting input, Pt = βYt/τt, into

production function (1), the output can be written as:

Yt =(Aτ− β

1−β

)K bα

t N1−bαt , (14)

where A ≡ ββ/(1−β)A1/(1−β) and α ≡ α/(1 − β). When written in the form of (14),

it becomes clear that the environmental tax lowers the effective total factor pro-

ductivity, Aτ−β/(1−β). Using this notation, the first order conditions are expressed

11

as

rt = αYt

Kt

= αAτ− β

1−β

t

(Kt

Nt

)bα−1

, (15)

wt = (1 − α − β)Yt

Nt

= (1 − α − β)Aτ− β

1−β

t

(Kt

Nt

)bα

. (16)

2.3 Equilibrium conditions

In this economy, the equilibrium path is characterized by the motions of aggregate

physical capital stock Kt, aggregate human capital stock Ht, aggregate labor supply

ut, aggregate consumption Ct, and the use of polluting input Pt. This subsection

summarizes the equilibrium conditions for those variables.

Note that, since the population is homogenous and normalized to unity, Kt = kt,

Ht = ht, Ct = ct, and ut = Nt/Ht hold in equilibrium. Substituting factor prices

(15) and (16) as well as the lump-sum transfer Tt = τtPt into the budget constraint

of households (7) yields the evolution of physical capital stock:

Kt

Kt

=Yt

Kt

− Ct

Kt

− (δK + ϕPt). (17)

From the production function of human capital (8), the evolution of aggregate human

capital stock is given as:

Ht

Ht

= B(1 − ut) − (δH + ψPt). (18)

Substituting factor prices (15) and (16) into the arbitrage condition (11), we obtain

the evolution of labor supply ut:

− β

1 − β· τt

τt

+ α(Kt

Kt

− Ht

Ht

− ut

ut

)= α

Yt

Kt

+ (ψ − ϕ)Pt − (δK − δH) − B. (19)

The dynamics of consumption is given by the Keynes-Ramsey Rule (10) where rt is

replaced by (15):

−θCt

Ct

= ρ − αYt

Kt

+ δK + ϕPt. (20)

Finally, from the firm’s f.o.c. (see the previous subsection), the amount of polluting

input is determined by:

Pt = βYt/τt. (21)

12

The equilibrium dynamics is determined by equations (17)-(21), exogenously given

time path of τt, initial levels of K0 and H0, and the TVCs (12) and (13).

Note that the TVCs can be simply stated using equilibrium conditions. From

(17) and (20), the growth rate of ktc−θt e−ρt is (1 − α)(Yt/Kt) − (Ct/Kt). Similarly,

from (10), (11) and (18), the growth rate of ht(wt/B)c−θt e−ρt is −But. Therefore, a

sufficient condition for the TVC is that those growth rates are negative in the long

run:

(12), (13) ⇐ limt→∞

(1 − α)(Yt/Kt) − (Ct/Kt) < 0, limt→∞

ut > 0. (22)

Condition (22) implies that the TVCs are satisfied when more than fraction 1 − α

of output is consumed and the fraction of time used for production is positive. For

later use, we also present necessary conditions for the TVC which are slightly weaker

than (22):

(12) ⇒ limt→∞

(1 − α)(Yt/Kt) − (Ct/Kt) ≤ 0, (23)

(13) ⇒ limt→∞

ut/ut ≥ 0. (24)

Condition (24) implies that, if the fraction of time used for production converges

toward zero, it must do so very slowly. That is, if limt→∞ ut/ut < 0, the attrition

rete of ht(wt/B)c−θt e−ρt, which is But, decreases toward zero very rapidly (i.e., ex-

ponentially). In that case ht(wt/B)c−θt e−ρt cannot reach zero in the long run, and

therefore the TVC (13) is violated.12

2.4 Sustainability under a constant tax rate

Observe, from (21), that pollution increases in proportion to output Yt if the gov-

ernment do not change the environmental tax rate. Since the increasing usage of

polluting inputs makes natural disasters more and more frequent, it seems that eco-

12Let V h(t) ≡ log(ht(wt/B)c−θt e−ρt). Then (13) is equivalent to limt→∞ V h(t) = −∞. Note

that, for arbitrary T > 0, limt→∞ V h(t) = V h(T )−B∫ ∞

Tu dt. The first term is finite. In addition,

when limt→∞ ut/ut < 0, the integral of the second term is also finite. Therefore the TVC is violated

if limt→∞ ut/ut < 0.

13

nomic growth is not sustainable under such a static environmental policy. This

subsection formally proves that this insight is correct.

Proposition 1 If the per-unit tax on polluting input is constant, then economic

growth is not sustainable in the sense that aggregate consumption cannot grow in the

long run.

Proof: The proof goes via reductio ad absurdum. When the government sets a con-

stant environmental tax rate (i.e., τt = τ0 for all t), the Keynes-Ramsey Rule (20)

can be rewritten, from (21), as:

−θCt

Ct

= ρ + δK −(

α − ϕβ

τ0

Kt

)Yt

Kt

.

This equation states that, if consumption grow in the long-run (i.e., Ct → ∞ as

t → ∞), the sign of the value in the parentheses must be positive. Hence, Kt

must be bounded above by a constant value τ0α/ϕβ (i.e., limt→∞ Kt < τ0α/ϕβ).

To interpret this result, observe that that, from (14) and (15), the rental price of

physical capital is rt = αYt/Kt and therefore the last term of represents marginal

rate of return of holding capital net of insurance cost ϕPt = ϕβYt/τ0. As physical

capital accumulates, the insurance cost increases in relative to interest rate due to

increased risk of natural disasters. Since this lowers the incentive to save, the stock of

physical capital should not become too large in order to maintain sustained growth.

This raises another question, however, of maintaining output growth under a lim-

ited size of physical capital. From (14), the positive growth rate of output requires

the positive growth rate of human capital stock devoted to production due to the

supremum of Kt. That is, limt→∞ Nt ≥ 0 must hold in order to support increas-

ing consumption. Under a constant environmental tax rate equation, (19) can be

rewritten as:

α(Kt

Kt

− Nt

Nt

)= α

Yt

Kt

+ (ψ − ϕ)Pt − (δK − δH) − B.

Consider the behavior of both hands of the above equation in the long-run. The left

hand side implies the growth rate of wage, which eventually becomes negative value,

14

−αNt/Nt. Conversely, the right hand is given by:(α − ϕβ

τ0

Kt

)Yt

Kt

− δK + ψPt − B + δH ,

which is the difference between the marginal rate of return on both types of capital

stock. From the condition for the positive growth rate of consumption derived above,

the sign of the value in the parentheses must be positive, and thus, the value of the

right hand side goes to infinity as Yt → ∞. These results imply that the equality in

(19) fails to hold, and therefore Ct and Yt cannot grow in the long run. ¥The proof of proposition clarifies that, under a constant environmental tax rate,

economic growth is not sustainable since agents lose the incentive to save when output

and the risk of natural disasters increases to a certain level. The risk of disasters

rises proportionally with output, and this follows from the fact that firms face a

constant tax rate on the polluting input Pt (see equation 21). This result provides

an anticipation that, in order to sustain economic growth, it might be necessary to

increase the rate of environmental tax increased over time so as to prevent the risk

of disasters to rise excessively when output grows. In the remaining of the paper, we

consider such a time-varying tax policy.

3 Sustainable Growth

This section examines the possibility of long-run growth under a time-varying tax

policy. In the literature of endogenous growth, long-term analysis is usually done by

focusing on balanced growth paths, which is sometimes called steady-state growth

paths, where the growth rates of all variables are constant. However, in the present

model, the economy do not typically have a steady-state growth path primarily

because the introduction of the endogenous risk of natural disasters (and therefore

the endogenous effective depreciation rate of capital) makes the structure of the

model intrinsically non-homothetic. Nonetheless, it does not rule out the possibility

that, under an appropriate tax policy, the economy converges, or asymptotes, to a

steady-state growth path as will be examined in this section.

15

Specifically, we seek to find a tax policy realizes an asymptotically steady-state

growth path, which is defined as follows.

Definition 1 An equilibrium path is said to be an asymptotic steady-state growth

path if the limiting values of the growth rates of output, inputs, and consumption all

exist and finite. That is, g∗ ≡ limt→∞ Yt/Yt, gK ≡ limt→∞ Kt/Kt, gH ≡ limt→∞ Ht/Ht,

gu ≡ limt→∞ ut/ut, gP ≡ limt→∞ Pt/Pt, and gC ≡ limt→∞ Ct/Ct are well-defined and

finite. Furthermore, an asymptotically steady-state growth path is said to be sustain-

able if gC is strictly positive.13

In the remaining of the paper, we focus on the sustainable, asymptotically steady-

state growth paths and refer them simply as steady-state growth paths unless it

causes any ambiguity. Note that the requirements for a sustainable, asymptotically

steady-state growth also restricts the asymptotic behavior of tax rate τt because

Pt = βYt/τt (equation 21) must be satisfied in the long run. In particular, for g∗ and

gP to be well-defined and finite, the asymptotic growth rate of tax rate

gτ ≡ limt→∞

τt/τt

must also be well-defined and finite. This means, in the long run, the per-unit tax

rate on the polluting input must be changed at a constant rate. The main task of

this section is to examine the dependence of long-term rate of economic growth g∗

on the (long-term) growth rate of environmental tax gτ . In the first subsection, we

13The notion of growth path presented here is essentially the same as the notion of a nonde-

generate, asymptotically balanced growth path proposed by Palivos et al. (1997, Definition 2). We

call it steady-state growth rather than balanced because an important property of the equilibrium

path which will be derived below is that it exhibits different growth rates among production inputs.

Correspondingly, the notion of sustainability in our definition is weaker than the notion of nonde-

generate growth by Palivos et al. (1997) in that we do not require every production input to grow

at positive rate. In fact, we show an important case of the analysis is that in which the growth rate

of one production input (namely, polluting input Pt) is negative and converges to zero. Even in

this case, the growth rates of output and consumption can be positive if the growth rates of other

inputs are positive and more than offset the declining use of a certain type of input.

16

present the conditions that must be satisfied on the steady-state growth path. In the

second and third subsections, we examine two different possibilities of steady-state

growth. The final subsection summarizes.

3.1 Conditions for Sustainable, Asymptotically Steady-State

Growth Path

We first show that, in the long run, the economy cannot grow faster than the growth

rate of environmental tax.

Lemma 1 On any asymptotically steady-state growth path, g∗ ≤ gτ .

Proof: in Appendix.

Intuitively, if production grows so fast that the usage of polluting input Pt = βYt/τt

become infinite in the long run, natural disasters occurs increasingly frequently. In

such a situation, however, both physical and human capital deteriorate at an accel-

erating rate, contradicting with the initial assumption that output can grow. One

implication of Lemma 1 is that sustainable steady-state paths (with g∗ > 0) are

obtained only when gτ > 0; i.e., only when the per-unit tax rate is increased expo-

nentially. This confirms the anticipation provided in the end of Section 2.4.

Another implication is that g∗ ≤ gτ leads to gP ≡ limt→∞ Pt/Pt ≤ 0 from (21).

Since the amount of polluting input Pt is nonnegative, this means that Pt converges to

a constant value in the long-run. We denote this asymptotic value by P ∗ ≡ limt→∞ Pt.

Note that P ∗ = 0 if Pt/Pt < 0. Even though we limit our attention to sustainable

growth paths, we should not rule out this possibility. It is true that output Yt is

zero if Pt = 0 given the Cobb-Douglas function (1) in which polluting inputs such

as fossil fuels are necessary; that is, a steady-state growth path in a conventional

sense with Pt = P ∗ = 0 is obviously inconsistent with sustainable growth. However,

we are considering asymptotically steady-state growth path in which Pt asymptotes

to P ∗, and therefore Pt does not necessarily coincide with P ∗ = 0 at any date.

Furthermore, limt→∞ Pt = 0 does not necessarily mean limt→∞ Yt = 0 since other

production factors in (1), namely Kt and Ht, can grow unboundedly.

17

We next show that these requirements and transversality conditions determine

the growth rates of ut, Kt, and Ct.

Lemma 2 On any sustainable, asymptotically steady-state growth path,14

(i) ut, zt ≡ Yt/Kt, and χt ≡ Ct/Kt are asymptotically constant.

(ii) gu = 0 and gK = gC = g∗.

Proof: in Appendix.

The result that physical capital and consumption grow in parallel with output

is a common property in models of endogenous growth (e.g., Lucas 1988, Palivos et

al. 1997). However, in our model, the growth rate of human capital is not the same

as output. Differentiating production function (14) logarithmically with respect to

time gives g∗ = − β1−β

gτ + αgK + (1 − α)(gu + gH), where we used Nt = utHt. This

equation implies that conditions for the steady-growth path (i.e, gK = g∗ and gu = 0)

are satisfied only when

gH = g∗ +β

1 − α − βgτ . (25)

Equation (25) says that, in a steady state growth path, human capital must accu-

mulate faster than physical capital and output, and the difference is larger when the

growth rate of environmental tax is higher.

To see why agents are willing to accumulate human capital faster in equilibrium,

observe that, as the tax rate on the polluting input is increased over time, the effective

productivity of private firms Aτ−β/(1−β) gradually falls (see equation 14). This means

that, if human capital is accumulated at the same speed as physical capital, output

can only grow slower than the speed of physical capital accumulation. As a result,

interest rate rt = αYt/Kt falls, which discourages agents from investing in physical

14Observe that property (ii) of Lemma 2 is a stronger statement than (i); i.e., property (i) holds

whenever gu ≤ 0, gK ≥ g∗, and gC ≤ gK . In the proof of the lemma on Appendix, we show that

all of gu ≤ 0, gK ≥ g∗, and gC ≤ gK must hold with equality since otherwise either transversality

conditions (their necessary condition are given by equations 23 and and 24) or sustainability (gC >

0) is eventually violated.

18

capital.15 This induces agents accumulate human capital relatively more rapidly than

physical capital. When human capital becomes increasingly abundant in relative to

physical capital, it can compensate the declining productivity so that the marginal

productivity of physical capital rt = αYt/Kt is kept constant (which is a necessary

condition for a steady-state growth).

Now we are ready to summarize the conditions that must be satisfied by any

sustainable, asymptotically steady-state growth path. For convenience, let us denote

asymptotic values by u∗ ≡ limt→∞ ut ∈ [0, 1], z∗ ≡ limt→∞ Yt/Kt ≥ 0, and χ∗ ≡

limt→∞ Ct/Kt ≥ 0. Substituting gu = 0, gK = gC = g∗ and (25) for (17)-(21), the

equilibrium conditions that must hold in the long run can be represented as follows.16

Evolution of Kt: g∗ = z∗ − χ∗ − (δK + ϕP ∗), (26)

Evolution of Ht: g∗ +β

1 − α − βgτ = B(1 − u∗) − (δH + ψP ∗), (27)

Arbitrage condition: − β

1 − α − βgτ = αz∗ − B + (ψ − ϕ)P ∗ − (δK − δH), (28)

Keynes-Ramsey rule: − θg∗ = ρ − αz∗ + (δK + ϕP ∗), (29)

Asymptotic pollution: P ∗

≥ 0 if g∗ = gτ (Case 1),

= 0 if g∗ < gτ (Case 2).

(30)

Given gτ > 0 set by the government, the five conditions, (26)-(30), determine five

unknowns, g∗, z∗, χ∗, u∗, and P ∗, in the asymptotically steady-state growth path.

In the following, we explicitly calculate the values for unknowns as a function of

gτ . Note that, however, there is a complementary slackness condition (30), and we

cannot know whether P ∗ = 0 or g∗ = gτ holds in advance. Thus we need to examine

two possible cases in turn, and then to determine which case actually occurs in

equilibrium under a particular tax policy.

15Recall that the rate of return from physical capital investment is rt − δK − ϕPt, whereas that

from human capital investment is B − δH − ψPt.

16Since ut = u∗ is constant, we use Nt/Nt = ut/ut + Ht/Ht = Ht/Ht in deriving the LHS of

(28).

19

3.2 Case 1: P ∗ ≥ 0 and g∗ = gτ

Let us first examine the possibility that the equilibrium long term rate of growth

coincides with the growth rate of environmental tax on the steady-state equilibrium

path. Substituting g∗ = gτ into (28) and (29), we obtain the asymptotic value of

polluting input:

P ∗ =1

ψ

[B − δH − ρ −

(θ +

β

1 − α − β

)gτ

], (31)

which is decreasing in gτ . Recall that, as shown by (30), the asymptotic value must

be nonnegative: P ∗ ≥ 0. From (31), we can see that the condition is satisfied if gτ

is within the following region:

gτ ≤ B − δH − ρ

θ + β1−α−β

≡ gmax, (32)

where gmax is positive from the assumption that B − δH > ρ. Hence, Case 1 (i.e.,

P ∗ ≥ 0 and g∗ = gτ ) is possible only if gτ ∈ (0, gmax].

Using g∗ = gτ , we obtain the asymptotic values of other variable from (26)-(29):

z∗ =1

α(θgτ + δK + ϕP ∗ + ρ) , (33)

χ∗ =1

α

((θ − α)gτ + (1 − α)(δK + ϕP ∗) + ρ

), (34)

u∗ =1

B

(B − (δH + ψP ∗) − 1 − α

1 − α − βgτ

). (35)

Substituting (31) into (33)-(35) and using gτ ∈ (0, gmax], it can be confirmed that

z∗ > 0, χ∗ > 0, u∗ ∈ (0, 1), and (1 − α)z∗ − χ∗ < 0. The last two inequalities

imply that the sufficient condition for the transversality condition, given by (22), is

satisfied. In addition, we show in Appendix that the steady-state growth path is

saddle stable given that the impacts of disasters on human capital (ψ) is relatively

small compared to that on physical capital (ϕ). The following lemma states the

obtained results.

Lemma 3 A sustainable, asymptotically steady-state growth path with P ∗ ≥ 0 and

g∗ = gτ exists if and only if gτ ∈ (0, gmax]. It is characterized by g∗ = gτ and (31)-

(35), and satisfy equilibrium conditions (26)-(30) and the transversality conditions.

20

In addition, if ψ/ϕ < (1 − 2α)/(1 − α − β), this equilibrium path is locally saddle

stable.

Proof: Stability is examined in Appendix.

We assume parameters satisfy ψ/ϕ < (1 − 2α)/(1 − α − β) in the remaining of the

paper.

3.3 Case 2: P ∗ = 0 and g∗ < gτ

Next, we examine the possibility that the amount of polluting input asymptotically

converges toward zero on the steady-state growth path. Substituting P ∗ = 0 for (28)

and (29) yields the steady-state growth rate:

g∗ =1

θ

(B − δH − ρ − β

1 − α − βgτ

). (36)

Contrary to Case 1 in which g∗ = gτ , equation (36) shows that the long-term rate of

growth is decreasing in gτ . Recall that, for the amount of polluting input Pt = βYt/τt

to converge toward zero as assumed, growth rate g∗ must be lower than gτ . Equation

(36) shows that, for condition g∗ < gτ to be satisfied, the rate of environmental tax

must be raised faster than gmax, where gmax is defined in (32). However, equation (36)

also implies that economic growth cannot be sustained when gτ is too high: g∗ ≤ 0

if gτ ≥ glim ≡ (1 − α − β)β−1(B − δH − ρ). Therefore, a sustainable, asymptotically

steady-state with P ∗ = 0 obtains only if gτ ∈ (gmax, glim), for which range of policies

g∗ ∈ (0, gτ ) holds.

Substituting P ∗ = 0 and (36) into (26)-(29), we obtain the asymptotically steady-

state values for other variables:

z∗ =1

α

(B + δK − δH − β

1 − α − βgτ

), (37)

χ∗ =( 1

α− 1

θ

)(B − δH − β

1 − α − βgτ

)+

1 − α

αδK +

ρ

θ, (38)

u∗ =1

Bθ

[(θ − 1)

(B − δH − β

1 − α − βgτ

)+ ρ

]. (39)

From gτ ∈ (gmax, glim), it can be confirmed that z∗ > 0, χ∗ > 0, (1−α)z∗−χ∗ < 0, and

u∗ ∈ (0, 1), implying that transversality condition (22) is satisfied. In addition, we

21

show in Appendix that this steady-state growth path is saddle stable. The following

lemma states the results.

Lemma 4 A sustainable, asymptotically steady-state growth path with P ∗ = 0 and

g∗ < gτ exist if and only if gτ ∈ (gmax, glim). It is characterized by P ∗ = 0 and (36)-

(39), and satisfy equilibrium conditions (26)-(30) and the transversality conditions.

In addition, this equilibrium path is locally saddle stable.

Proof: Stability is examined in Appendix.

3.4 Summary

Lemma 3 and Lemma 4 shows that there are two possible patterns of sustained

growth. Observe that those two possibilities are mutually exclusive—that is, under

a given time path of environmental tax at most one lemma is applicable. Therefore,

the sustainable, asymptotically steady-state growth path is always unique; it is char-

acterized by Lemma 3 if gτ ∈ (0, gmax], and by Lemma 4 if gτ ∈ (gmax, glim). The

following proposition states the main result.

Proposition 2 A sustainable, asymptotically steady-state growth path exists if and

only if the per-unit tax on polluting input is raised over time so that its asymptotic

growth rate, gτ , is strictly positive and less than glim ≡ (1− α− β)β−1(B − δH − ρ).

When it exists, it is unique and saddle stable. The long-term rate of economic growth

follows an inverted-V shape against gτ ∈ (0, glim), and it is maximized at gτ = gmax ≡

(B − δH − ρ)(θ + β1−α−β

)−1.

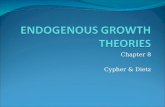

Figure 1 illustrates how asymptotic growth rate of environmental tax, which is

an exogenous policy variable, affects growth rates of other variables as well as the

level of pollution in the long run.17 This result can be interpreted as follows.

17Figure 1 is derived as follows. gC and gK are the same as g∗, which is given by g∗ = gτ for

gτ ∈ (0, gmax) and (36) for gτ ∈ (gmax, glim). Given g∗, gH and gP are determined by (25) and

gP ≡ Pt/Pt = g∗−gτ (recall equation 21). Finally P ∗ is given by (31) for gτ ∈ (0, gmax) and P ∗ = 0

for gτ ∈ (gmax, glim).

22

g¿

gmax

glim

gH

gK = gC = g¤

gP

P ¤P

gmax

g¿

0

Figure 1: Growth rate of environmental tax and the sustainable, asymptotically

steady-state growth. The upper panel shows the relationship between the growth rate of envi-

ronmental tax (gτ ) and that of human capita (gH), physical capital (gK), output (g∗), and pollution

(gP ). The lower panel shows the level to which the level of pollution converges to in the long run

(Pt → P ∗). Parameters: α = .3, β = .2, θ = 2, ρ = .05 B = 1, ψ = .005, ϕ = .01, δH = .09, and

δK = .1.

When the environmental tax rate is asymptotically constant (i.e., gτ = 0), the

asymptotic growth rates of all endogenous variables are zero, which means that the

economy settles to a no-growth steady state. In this steady state, the amount of

pollution converges to P ∗ = (B − δH − ρ)/ψ ≡ P , which causes the probability of

natural disasters (i.e., the risk of losing their physical and human capital) so high

that agents loses incentive to save. Interestingly, observe that the asymptotic level

of Pt does not depend on the level of the environmental tax rate, τt, as long as it

is constant. Nonetheless, since Yt = τtPt/β from (21), a higher tax rate induces the

economy to converges to a higher output level by influencing the equilibrium path

in transition.

When the government raises the per-unit tax rate on polluting inputs at an

exponential rate (gτ > 0), the asymptotic level of Pt can be kept below P so that

economic growth may be maintained without bound. When gτ in increased within

23

the range of (0, gmax], the long-run amount of pollution P ∗ decreases, and so does the

risk of natural disasters. The reduced risk of natural disasters encourages agents to

accumulate capital at a faster speed. As a result, the growth rate of physical capital

gK increase in parallel with gτ (i.e., gK = gτ ). The growth rate of human capital, gH ,

also increases with gτ , and more rapidly than physical capital. (Recall the discussion

in Section 3.1 for why agents are willing to do so.) This makes possible sustained

growth under asymptotically constant use of polluting input.

However, accelerating the rise of tax rate does not necessarily enhance economic

growth because it also has a negative effect on growth through limiting the use of

Pt, which is a necessary input for the Cobb-Douglas production process. Specifically,

when the environmental tax rate is raised so rapidly that gτ exceeds gmax, the use

of polluting inputs Pt is continually reduced, converging asymptotically to zero level

(Pt → P ∗ = 0). In this case, a further acceleration of gτ no longer can reduce the

asymptotic probability of natural disasters (because is is already at the lowest level),

but only accelerates the fall of the effective productivity of private firms Aτ−β/(1−β).

As a result, g∗ is no longer increasing in parallel with gτ , but decreasing in gτ . An

extreme case is that of gτ ≥ glim, for which case, even though the risk of natural

disasters is a the lowest level, the fall of the effective productivity Aτ−β/(1−β) is

so fast that it cannot be compensated by a faster accumulation of human capital,

resulting in zero or negative growth.

4 Welfare

The previous section established that sustained growth is feasible by raising the

rate of environmental tax rate over time. It is yet to shown, however, such an

environmental policy is desirable in terms of welfare. This section investigates the

social planner’s problem so as to derive the welfare-maximizing environmental policy,

and compares it with the growth maximizing policy derived in the previous section.

24

The social planner maximizes (9) subject to the following constraints:

Kt = F (Kt, utHt, Pt) − Ct − (δK + ϕPtKt), (40)

Ht = B(1 − ut)Ht − (δH + ψPtHt). (41)

From the first-order conditions for optimality, it can be confirmed that the dynamics

of Kt, Ht, and Ct, and the arbitrage condition between two types of capital stocks are

exactly the same as (17)-(20), which are parts of market equilibrium conditions. Since

the social planner takes into consideration the externality of polluting emissions, that

is, the risk of natural disasters, it chooses the amount of polluting input according

to the following rule:

Pt = βYt

(ϕKt + ψHt ·

(1 − α − β)Yt

ButHt

)−1

. (42)

Equation (42) says that the use of polluting input should be determined so that its

marginal product (βYt/Pt) is equal to the marginal disadvantage of using polluting

inputs. The marginal disadvantage is given by the expression in the large parenthesis,

which is the sum of increases in damage to physical capital stock and in damage to

human capital stock, both measured in terms of final goods (in particular, (1 − α −

β)Yt/(ButHt) is the shadow price of human capital in terms of final goods).

Recall that, in the market economy, firms choose Pt according to (21); i.e., Pt =

βYt/τt. This means that if the tax rate at each date is determined by

τ optt = ϕKt + ψ

(1 − α − β)Yt

But

, (43)

then the optimality condition for Pt, equation (42), is satisfied. Recall again that

other conditions for social optimum is the same as that for the market equilibrium.

Therefore, if the government set the environmental tax rate by following rule (43),

then the market equilibrium path completely traces the social optimal path.18

18Generally speaking, even when they look similar, a time-varying policy (a function only of time

such as considered in the previous section) and a policy rule (a function of state variable such

as equation equation 43) may result in different outcomes if agents behaves strategically. Such a

difference is studied in the literature of differential games: the difference between the open-loop

equilibrium and the Markovian equilibrium. However, in the present model, all agents are price

takers and therefore both policies results in the same outcome.

25

Although it may be convenient in practice to follow a policy rule than calculating

the time path of tax rate at the outset, equation (43) is not so informative about

the equilibrium path that result from such a policy. Equation (43) implies that τt

is function of Kt, Yt, and ut. However, Kt, Yt, and ut are endogenously determined

depending the future path of τt that is expected by consumers. That is, the welfare

maximizing path is given as a solution to a dynamic fixed point problem.

Since it is excessively difficult to solve this problem directly, we limit our attention

to sustainable, asymptotically steady-state growth paths and examine whether there

is a path that satisfies optimality condition (42) within this family of paths. Note

that on any sustainable, asymptotically steady-state growth path, both the LHS and

the RHS of condition (42) asymptotes to constants. Specifically,

P ∗ = β

(ϕ

1

z∗ +ψ(1 − α − β)

Bu∗

)−1

(44)

must hold in the long run, where P ∗, z∗ and u∗ represents the asymptotic values of Pt,

zt ≡ Yt/Kt and ut. We know from Proposition 2 that, whenever the equilibrium path

asymptotes to a sustainable steady-state growth path, the asymptotic growth rate of

the optimal tax rate, goptτ ≡ limt→∞ τt/τt, is well defined and that gτ ∈ (0, glim). In

addition, P ∗, z∗ and u∗ are determined as a function of gτ . Therefore, we examine

whether there exist a value of gτ within (0, glim) such that (44) holds.

Figure 3 plots the RHS and the LHS of equation (44) against gτ . The actual

amount of asymptotic pollution (the LHS) is positive but decreasing in gτ for gτ ∈

(0, gmax), and it is zero for gτ ≥ gmax. On the other hand, the optimal amount of

asymptotic pollution (the RHS) is positive for all gτ > 0. The both curves are are

continuous in gτ . In addition, it can be shown that the intercept of the RHS is lower

than that of the LHS whenever ρ or β is sufficiently small.19 Therefore, unless both β

and ρ are large, the two curves have an intersecting point within gτ ∈ (0, gmax), which

19Observe from (31), (33) and (35) that P ∗ = (B − δH − ρ)/ψ ≡ P , z∗ = (δK + ϕP + ρ)/α and

u∗ = ρ/B when gτ = 0. Substituting these into both sides of (44) and rearranging terms shows

that the prerequisite is satisfied if and only if β < (αϕ/(δK + ϕP + ρ) + ψ(1 − α − β)/ρ)P , which

is satisfied whenever ρ or β is sufficiently small.

26

g¿glim

P ¤

P

gmax0

gopt¿

Actual (LHS)P ¤

Optimal (RHS)P ¤

Figure 2: Determination of the optimal growth rate of environmental tax. The figure

plots the RHS and the LHS of condition (44) against gτ . The asymptotic growth rate of optimal

environmental tax is goptτ , is given by the intersection, which is lower than the growth maximizing

rate, gmax. The parameters are the same as in Figure 1.

represents the growth rate of optimal tax rate, goptτ . Note that, since gopt

τ ∈ (0, gmax),

the long-term rate of economic growth g∗ coincides with goptτ , and therefore it is

positive. The following proposition states the obtained result.

Proposition 3 Suppose that the welfare of consumers is given by (9) and that either

discount rate or or the share of polluting input is sufficiently low. Then among

sustainable, asymptotically steady-state growth paths, there exists a unique optimal

growth path with strictly positive rate of economic growth. The asymptotic growth

rate of optimal per-unit tax, goptτ , is positive but slower than the growth maximizing

rate, gmax.

Thus the above analysis shows that the sustained growth implemented by raising

the environmental tax rate is not only feasible but also desirable. It is also notable,

however, that the optimal policy does not coincide with the growth maximizing policy

since goptτ < gmax. That is, if the government care about welfare it should employ

milder policy for protecting environment than when growth is their only concern.

This result may seem at odds with the usual growth vs. environment arguments, but

its reasoning is similar to the modified golden rule argument familiar to economists.

27

Although an aggressive environmental policy that aims to eliminate the emission of

pollutants in the long run (i.e., P ∗ = 0) may maximize the economic growth rate in

the very long run, the cost in the form of reduced effective productivity that must

be incurred in the transition can overwhelm the benefit that cannot be reaped until

far future.

5 Disutility of Pollution

Our result that the sustained growth is both feasible and desirable is in contrast to

the previous literature. Notably, Stokey (1998) has shown that even when sustained

growth is feasible, it is not desirable when production of goods emits pollutants that

harm the utility of consumers. The difference of the results of course comes from

the setting of models. More specifically, our model significantly differs from Stokey

(1998) in two aspects; (i) we are considering human capital accumulation differently

from Stokey’s AK model; (ii) so far pollutants are assumed to cause disasters but do

not directly give disutility.

In this subsection, we clarify that the critical reason behind the difference in the

results is not (ii) but (i). To this end, we present an extended model in which agents

suffer from not only damages to capital stocks caused by natural disasters but also

disutility of pollution. Suppose that consumers has an utility function of∫ ∞

0

(c1−θt − 1

1 − θ− P 1+γ

t

1 + γ

)e−ρtdt, γ > 0. (45)

The only difference of (45) from (9) is that it includes a disutility term P 1+γt /(1+γ),

which is isoelastic and convex with respect to the use of polluting input Pt. Since

function (45) is separable with respect to ct and Pt, behavior of all agents, who takes

Pt as given, does not change. That is, the equilibrium outcome is exactly the same

as in analyzed in sections 2 and 3.

Let us examine how the planner’s problem is affected. Under resource constraints

(40) and (41), the planner maximizes function (45). Then, the optimality condition

28

with respect to polluting input becomes

Pt = βYt

(ϕKt + ψHt ·

(1 − α − β)Yt

ButHt

+P γ

t

C−θt

)−1

. (46)

When compared to (42), there is an additional marginal cost of polluting input that

comes from disutility.

Similarly to the previous section, we again limit our attention to sustainable,

asymptotically steady-state growth paths. In the long run, condition (46) implies

that

P ∗ = β

(ϕ

z∗+

ψ(1 − α − β)

Bu∗ +(χ∗)θ

(z∗)θlimt→∞

P γt Y θ−1

t

)−1

. (47)

The value of the RHS critically depends on the behavior of P γt Y θ−1

t . Note that, from

Pt = βYt/τt, its asymptotic growth rate is γgP +(θ−1)g∗ = (γ+θ−1)g∗−γgτ . Using

the fact that g∗ is a function of gτ , we can show that there is gτ ∈ (gmax, glim) such

that the asymptotic growth rate of P γt Y θ−1

t is strictly positive when gτ ∈ (0, gτ ) and

it is strictly negative when gτ ∈ (gτ , glim). This means that the RHS of (47) is zero

for gτ ∈ (0, gτ ) and strictly positive when gτ ∈ (gτ , glim). Therefore, as illustrated

in Figure , condition (47) holds for all gτ ∈ (gmax, gτ ). Whenever the asymptotic

growth rate of per-unit tax is between gmax and gτ , it is optimal to reduce the use of

polluting input toward zero in the long run, and Pt actually converges toward zero.

However, this does not necessarily mean that every tax policy with gτ ∈ (gmax, gτ )

is optimal, because (47) is merely a necessarily condition for (46). A more strong

condition is that both the LHS and the RHS of (46) falls toward zero at the same

speed. When gτ ∈ (gmax, gτ ), the asymptotic growth rate of the RHS of (46) is

−(γ + θ − 1)g∗ + γgτ (the negative of the growth rate of P γt Y θ−1

t ). As shown in

Figure , it coincides with the growth rate of Pt, which is g∗ − gτ , if and only if

gτ = goptτ ≡ (γ + θ)(1 − α − β)(B − δH − ρ)

θ(1 + γ)(1 − α − β) + β(γ + θ)∈ (gmax, gτ ).

Thus the following proposition obtains.

Proposition 4 Suppose that the welfare of consumers is given by (45). Then among

sustainable, asymptotically steady-state growth paths, there exists a unique optimal

29

g¿glimgmax0

¡gP

eg¿

bgopt¿

g¿

P ¤

Actual

Optimal

Actual

Optimal

Figure 3: Optimal growth rate of environmental tax when disutility of pollution is

accounted for. The upper panel plots the asymptotic levels of RHS and the LHS of condition

(46), whereas the lower panel depicts thier asymptotic growth rates. The asymptotic growth rate of

optimal environmental tax is goptτ , is higher than the growth maximizing rate, gmax. The parameters

are the same as in Figure 1 and γ = .2.

growth path with strictly positive rate of economic growth. The asymptotic growth

rate of optimal per-unit tax, goptτ , is higher than the growth maximizing rate, gmax.

The main result is that the desirability of sustained growth does not change even

when disutility of pollution is introduced into the model. However, the desirable

speed at which the environmental tax is increased is now higher than the growth

maximizing speed, gmax. This implies that, if pollution affects the utility of agents

directly, the emission of pollutant should be eliminated in the long run even at the

cost of accepting a slower (although positive) rate of economic growth.

6 Concluding Remarks

The sustainability of economic growth has been analyzed in a two-sector model of

endogenous growth, taking into account the risk of natural disasters. Polluting inputs

30

are necessary for production, but they intensify the risk of natural disasters. In this

setting, we obtained following results.

First, the long-run economic growth can not be sustained if the private cost of

using the polluting input is kept constant.20 Since, for simplicity, we do not con-

sider the cost associated with extracting resources or the finiteness of those inputs,

this result implies that the environmental tax rate should be increased over time.

However, it should be noted that if the private cost changes for some ignored rea-

sons, the environmental tax rate must be adjusted to absorb those changes. More

substantially, a next step in the research agenda would be to integrate the analysis

of natural disasters with the studies of finiteness of natural resources, although it is

beyond the scope of this first endeavor.

Second, the rate of the economic growth rate follows the inverted V-shaped curve

relative to the growth rate of the environmental tax. When the rate of environ-

mental tax is initially slow growing, its acceleration will reduce the long-run level of

emission and the risk of natural disasters, which enhances the incentive to save and

hence promotes economic growth. When the rate of environmental tax is already

fast growing, the amount of polluting input at the steady state is fairly small so that

further acceleration of environmental tax excessively impair the productivity of pri-

vate firms, which works against economic growth. Therefore, the economic growth

can be maximized with choice of the most gradual increase in environmental tax rate

that minimizes the amount of pollution in the long-run.

Third, the sustained growth, realized by ever increasing tax rate on polluting

inputs, is not only feasible but also desirable. Although economic growth ceteris

paribus induces private firms to use more polluting input, an appropriate environ-

mental policy can lead firms to use more of human capital (e.g., by investing in

alternative technology), which decreases their reliance on polluting inputs. The op-

20When the damage to physical capital stock is much larger than that to human capital stock

(i.e., ϕ >> ψ), the steady-state value of P ∗ is rather large (see Equation 31). In this case, the speed

of convergence to the steady state is slow, the economic growth declines gradually, and amount of

pollution increases during the transition to the steady state.

31

timal speed at which the environmental tax rate is increased is lower than the growth

maximizing speed if pollution only causes disasters, while it is higher when direct

disutility from pollution is accounted for.

Appendix

A Proof of Lemma 1

Suppose that g∗ > gτ (i.e., limt→∞ Yt/Yt > limt→∞ τt/τt). Then, Pt = βYt/τt → ∞.

From (18) and ut ≤ 1, this means Ht/Ht ≤ B − δH − ψPt → −∞. It con-

tradicts with the definition of the asymptotically steady-state growth, in which

gH ≡ limt→∞ Ht/Ht is finite.

B Proof of Lemma 2

On the asymptotically steady-state growth path, in which Ht/Ht and Pt are asymp-

totically constant, equation (18) implies that ut must also be asymptotically constant.

It means that the growth rate of ut is zero or negative (i.e., in the case of ut → 0),

but from (24) we know that the TVC for human capital accumulation is satisfied

only when the growth rate of ut is nonnegative. Therefore gu = 0. Next, since Ct/Ct

and Pt are asymptotically constant, equation (20) implies that the value of Yt/Kt

must also be constant in the long run. This means that the growth rate of Yt/Kt

is zero or negative. However, if Yt/Kt → 0, equation (17) says Kt/Kt < 0, which

means that Yt = (Yt/Kt) · Kt → 0. With output converging to zero, the sustainable

steady-state growth path, where gC ≥ 0, is clearly in contradiction. Therefore, the

growth rate of Yt/Kt must be zero; i.e., gK = g∗. Finally, given that Kt/Kt and

Yt/Kt are asymptotically constant, equation (17) in turn imply Ct/Kt must also be

asymptotically constant. Recall that that the TVC for physical capital (23) requires

Ct/Kt must not be smaller than (1−α)(Yt/Kt), which converges to a strictly positive

constant as shown above. Therefore, the growth rate of Ct/Kt must not be negative

but zero; i.e., gC = gK = g∗.

32

C Stability of the equilibrium path around the steady-state

growth path

In this subsection, we establish the stability of the equilibrium path stated in Lemma

3 and Lemma 4. The equilibrium path is characterized by a four-dimensional dy-

namics system of Kt, Ht, ut, Ct, where the laws of motion for those variables are

given by (17)-(20).21 In this dynamic system, Kt and Ht are predetermined state

variables, whereas ut and Ct are jumpable. Therefore, the system is both stable and

determinate when it has a stable manifold of dimension two.

For convenience we transform this system into another four-dimensional system

of ut, χt, zt, Pt. where χt ≡ Ct/Kt, z ≡ Yt/Kt and Pt ≡ βYt/τt. This transformed

system is equivalent to the original system since Kt, Ht, ut, Ct can be represented

in terms of ut, χt, zt, Pt.22 Therefore, saddle-stability (and determinacy) can be

established by confirming that this transformed system has a two dimensional stable

manifold. Using (14) and (17)-(21), we can write the dynamics of the system as

ut = ut

(But − χt + βzt + ΛPt +

1 − α − β

α(B + δK − δH) − β

αgτ

), (48)

χt = χt

(χt −

θ − α

θzt +

θ − 1

θϕPt −

ρ

θ+

θ − 1

θδK

), (49)

zt = zt

(−(1 − α − β)zt + ΛPt +

1 − α − β

α(B + δK − δH) − β

αgτ

), (50)

Pt = Pt

(−χt +

α + (1 − α − β)β

1 − βzt + ΩPt +

1 − α − β

αB − α + β

αgτ

+(1 − 2α − β)δK − (1 − α − β)δH

α

)(51)

where Λ and Ω are constants defined by Λ ≡ (1 − α − β)(ϕ − ψ)/α and Ω ≡

((1 − 2α − β)ϕ − (1 − α − β)ψ) /α.

21Note that, by making use of (14), (21) and Nt = utHt, Yt and Pt appearing in the LHS of (17)-

(20) can be expressed in terms of Kt,Ht, ut and τt, where the motion of τt is given exogenously by

the government.

22Equivalence is confirmed by that the inverse transformation is well defined. Specifically, Kt =

τtPt/(βzt), Ct = τtPtχt/(βzt), and Ht =(τ1/(1−β)−bα/A

)1/(1−bα)

zbα/(1−bα)t Pt/(βut).

33

We first examine the stability of the steady state equilibrium path for the case

of gτ ∈ (0, gmax]. As examined in Section 3.2, the (asymptotic) steady state of

the transformed system, denoted by u∗, χ∗, z∗, P ∗, is given by (31) and (35)–(33).

Applying a first-order Taylor expansion of equations (48)–(51) around this steady-

state yields ut

χt

zt

Pt

≃

u∗B −u∗ βu∗ Λu∗

0

0 J1

0

ut − u∗

χt − χ∗

zt − z∗

Pt − P ∗

, (52)

where

J1 ≡

χ∗ − θ−α

θχ∗ (θ−1)ϕ

θχ∗

0 −(1 − α − β)z∗ Λz∗

−P ∗ α+β(1−α−β)1−β

P ∗ ΩP ∗

.

We want to show that the Jacobian matrix of (52) has two positive and two negative

eigenvalues. From the block-triangular structure of the matrix, one eigenvalue is

u∗B > 0, and the other three are given by the eigenvalues of the submatrix J1. The

characteristic equation for J1 is

−λ3 + TrJ1λ2 − BJ1λ + DetJ1 = 0, (53)

where

TrJ1 =

θ + β − α

α− (1 − 2α)ϕ

αψ

(θ +

β

1 − α − β

)gτ +

β

αδK +

α + β

αρ

+

(1 − 2α)ϕ

αψ− 1 − α − β

α

(B − ρ − δH),

MJ1 =χ∗ − θ−α

θχ∗

0 −(1 − α − β)z∗+

−(1 − α − β)z∗ Λz∗

α+β(1−α−β)1−β

P ∗ ΩP ∗+

χ∗ (θ−1)ϕθ

χ∗

−P ∗ ΩP ∗,

= −1 − α − β

α

(ϕ − ψ)(z∗ − χ∗) +

αϕχ∗

θ(1 − α − β)

−1 − α − β

α· z∗

P ∗

(θ − α)gτ + (1 − α)δK + (1 − 2α)ϕP ∗ + ρ

,

DetJ1 =ψ(1 − α − β)

θz∗χ∗P ∗,

34

where MJ1 denotes the sum of the principal minors of J1. We determine the sign of

the real parts of the roots of (53) based on Theorem 1 of Benhabib and Perli (1994).

Theorem 1 (Benhabib-Perli) The number of roots of the polynomial in (53) with

positive real parts is equal to the number of variations of sign in the scheme

−1 TrJ1 − MJ1 +DetJ1

TrJ1

DetJ1.

Under the assumption that ψ/ϕ < (1−2α)/(1−α−β), we have TrJ1 > 0,23 MJ1 < 0,

and DetJ1 > 0. Thus the above theorem implies that there is only one eigenvalue

with positive real parts in the matrix J1. Combined with Bu∗ > 0 obtained before,

we have two positive eigenvalues in total. This completes the stability analysis for

that case of gτ ∈ (0, gmax] (and therefore the proof of Lemma 3).

Turning to the case of gτ ∈ (gmax, glim], the (asymptotic) steady state of the

transformed system for this case is given by P ∗ = 0 and (37)–(39) in Section 3.3. The

Taylor expansion of equations (48)–(51) around this steady-state yields essentially

the same expression as (52), with the only difference that submatrix J1 is replaced

by

J2 =

χ∗ · · · · · ·

0 −z∗(1 − α − β) · · ·

0 0 g∗ − gτ

,

where g∗ is the asymptotic growth rate of output, which is defined by (36). Since

J2 is a triangular matrix, its eigenvalues are simply given by its diagonal elements.

Observe that g∗ − gτ represent the asymptotic growth rate of Pt = βYt/τt. As

discussed in Section 3.3, it is negative in this case (i.e., when gτ ∈ (gmax, glim)).

Therefore, J2 has one positive eigenvalue (χ∗) and two negative ones (−z∗(1−α−β)

and g∗ − gτ ). This completes the stability analysis for that case of gτ ∈ (gmax, glim)

and the proof of Lemma 4.

¥

23This can be confirmed by noting that TrJ1 is linear in gτ and confirming TrJ1 > 0 at both

gτ = gmax and gτ = 0.

35

Reference

Aghion, P., Howitt, P.: Endogenous Growth Theory, MIT Press, Cambridge, MA.

(1998)

Agnani, B., Gutierrez, M.-J., Iza, A.: Growth in overlapping generation economies

with non-renewable resources, 50, 387-407 (2005)

Benhabib, J., Perli, R.: Uniqueness and indeterminacy: on the dynamics of endoge-

nous growth. Journal of Economic Theory, 63, 113-142 (1994)

Bovenberg, A.L., Sumlders, S.: Environmental quality and pollution-augmenting

technological change in a two-sector endogenous growth model. Journal of Public

Economics, 57, 369-391 (1995)

Copeland, B. R., Taylor, M. S.: North-South trade and the environment. Quarterly

Journal of Economics 109, 755-787 (1994)

Emanuel, K.: Increasing destructiveness of tropical cyclones over the past 30 years.

Nature 436, 686-688 (2005)

Grimaud, A., Rouge, L.: Non-renewable resources and growth with vertical inno-

vations: optimum, equilibrium and economic policies. Journal of Environmental

Economics and Management 45, 433-453 (2003)

Hoyois, P., Below, R., Guha-Sapir G.: World Disasters Report 2005. Annex 1,

Disaster Data. Geneva. International Federation of Red Cross and Red Crescent

Societies.

IPCC (2001): Summary for Policymakers, A Report of Working Group I of the

Intergovernmental Panel on Climate Change.

Lucas Jr., R. E.: On the mechanics of economic development. Journal of Monetary

Economics 22, 3-42 (1988)

36

National Climatic Data Center: Technical Report 2005-01. U.S. Department of

commerce, National Oceanic and Atomospheric Administration

Parivos, T., Wang, P., Zhang, J.: On the existence of balanced growth equilibrium.

International Economic Review, 38, 205-224 (1997)

Scholz, C. M., Ziemes, G.: Exhaustible resources, monopolistic competition, and

endogenous growth. Environmental and Resource Economics, 13, 169-185 (1999)

Schou, P.: Polluting Non-renewable resources and growth. Environmental and Re-

source Economics, 16 211-227 (2000)

Skidmore, M., Toya, H.: Do natural disasters promote long-run growth? Economic

Inquiry 40, 664-687 (2002)

Stokey, N. L.: Are there limits to growth? International Economic Review 39, 1-31

(1998)

Uzawa, H.: Optimal technical change in an aggregative model of economic growth.

International Economic Review 6, 18-31 (1965)

Uzawa, H.: Economic theory and global warming, Cambridge, UK: Cambridge

University Press (2003)

Webster, P. J., Holland, G. J., Curry, J. A., Chang, H.-R.: Changes in Tropical

Cyclone Number, Duration, and Intensity in a Warming Environment. Science 309,

1844-1846 (2005)

37

7 Referee Appendix

Optimization of the Household (Section 2.2)

The current value Hamiltonian for the maximization problem is:

H =c1−θt − 1

1 − θ+νt (rtkt − (δK + ϕPt)kt + wtutht − ct + Tt)+µt (B(1 − ut)ht − (δH + ψPt)ht) ,

where νt and µt are the shadow prices associated with the accumulation of physical

capital and human capital, respectively. The optimality conditions are

νt = c−θt , (54)

µt =wt

Bνt, (55)

νt

νt

= ρ + ϕPt + δK − rt, (56)

µt

µt

= ρ − νt

µt

wtut − B(1 − ut) + δH + ψPt. (57)

The transversality conditions for physical capital stock and human capital stock,

respectively, are

limt→∞

ktνte−ρt = 0, and

limt→∞

htµte−ρt = 0,

Substituting (55) into (57) yields

µ

µ= ρ − B + δH + ϕPt. (58)

From (54) and (56), the the Keynes-Ramsey Rule is

−θct

ct

= ρ + ϕPt + δK − rt.

Differentiating logarithmically with respect to time in (55) and using (56) and (58),

we obtain the arbitrage condition between human capital investment and physical

capital investment:

wt

wt

= rt − (ϕ − ψ)Pt − (δK − δH) − B.

38

Optimization of the Social Planner (Section 4)

The current value Hamiltonian is

H =C1−θ

t − 1

1 − θ+νo

t [AKαt (utHt)

1−α−βP βt −Ct−(δK+ϕPt)Kt]+µo

t [B(1−ut)Ht−(δH+ψPt)Ht],

where νot and µo

t are the planner’s shadow prices associated with the accumulation

of physical capital and human capital, respectively. The necessary conditions for

optimality

Hc = c−θt − νo = 0, (59)

Hu = νot (1 − α − β)

Yt

ut

− µotBHt = 0, (60)

HP = νot β

Yt

Pt

− νot ϕKt − µo

tψtHt = 0, (61)

νot

νot

= ρ −(

αYt

Kt

− (δK + ϕPt)

)= 0, (62)

µot

µot

= ρ − νot

µot

(1 − α − β)Yt

Ht

−(B(1 − ut) − (δH + ψtPt)

)= 0, (63)