Yammer: The Enterprise Social Network - All Service Social Media Conference - February 2011

Upload

national-enterprise-networkCategory

view

684download

1

Paul McEldon NEN Chairman

Welcome and introductions

Sue Hayes Managing Director, Barclays Business Banking

Headline sponsor’s address

The Rt Hon Lord Young Prime Minister’s Adviser on Enterprise

Keynote speaker

Frances Brindle Director of Audiences, British Library

The Rt Hon Michael Fallon MP Minister of State for Business and Energy

Ministerial address

Refreshments and networking break

Andrew Devenport CEO, The Prince’s Youth Business International (YBI)

Why networks are important

Andrew Devenport, Chief Executive,

Youth Business International

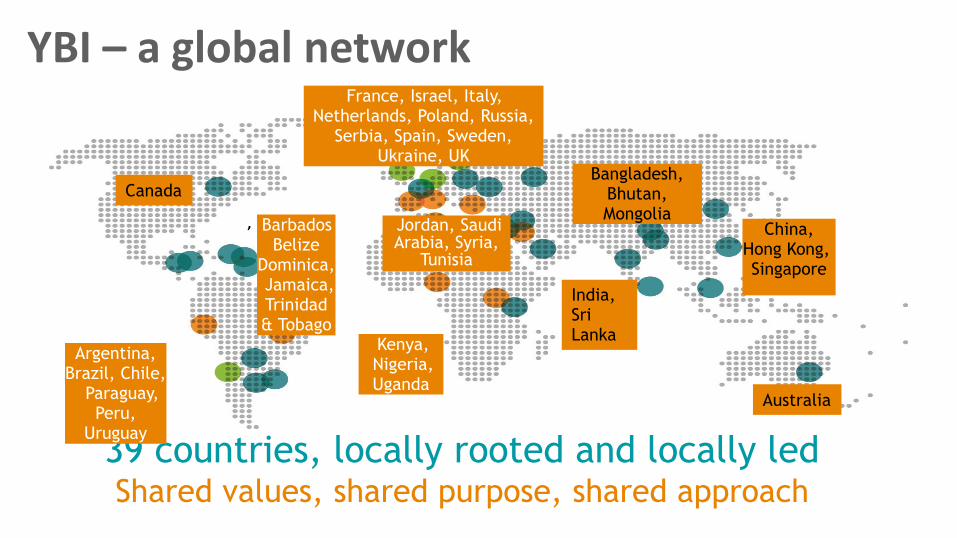

YBI – a global network

39 countries, locally rooted and locally led Shared values, shared purpose, shared approach

,

Barbados Belize

Dominica, Jamaica, Trinidad & Tobago

Canada

Argentina, Brazil, Chile, Paraguay,

Peru, Uruguay

France, Israel, Italy, Netherlands, Poland, Russia,

Serbia, Spain, Sweden, Ukraine, UK

Jordan, Saudi Arabia, Syria,

Tunisia

Kenya, Nigeria, Uganda

India, Sri Lanka

Bangladesh, Bhutan, Mongolia

China, Hong Kong, Singapore

Australia

The power of a network

Global Entrepreneurship

Week 2013 We want current and aspiring entrepreneurs to take a step forward in their plans – whether that’s starting a business, seizing a new opportunity or finding out more about careers in enterprise. www.gew.org.uk

#GEWfwd

Real life entrepreneurs

Rekha Mehr Business owner: Pistachio Rose

www.pistachiorose.co.uk

@pistachiorose / @rekhamehr

Mark Earnden Business owner: Mark Earnden

www.markearnden.com

@markearnden

Phil Pethybridge Business owner: Neon Street and Your Music Business

www.neonstreet.net / www.yourmusicbusiness.co.uk @ppethybridge / @neonstreet / @ymbuk

Phil Pethybridge

Industry: ‘Build audiences and maximise income’ Education: 'Support young musicians to develop sustainable careers’

Real life entrepreneurs

Q&A

Lunch and networking

Annual General Meeting

NEN Members only

Justin Urquhart-Stewart Co founder, Seven Investment Management

NOVEMBER 2013

NATIONAL •ENTERPRISE •NETWORK

NOVEMBER 2013

GLOBAL GROWTH - •EFFECT •ON UK?

GREEN SHOOTS •OR ADVANCED •MOULD

30

31

Green Shoots or Advanced Mould?

November 13 32

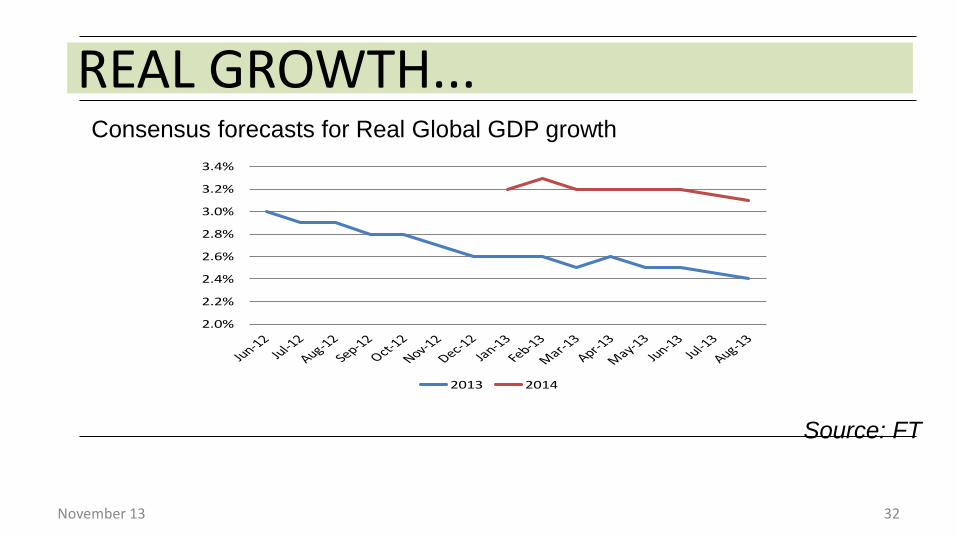

REAL GROWTH...

Source: FT

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%

3.4%

2013 2014

Consensus forecasts for Real Global GDP growth

THE TAPIR & THE PANDA

33

Vs.

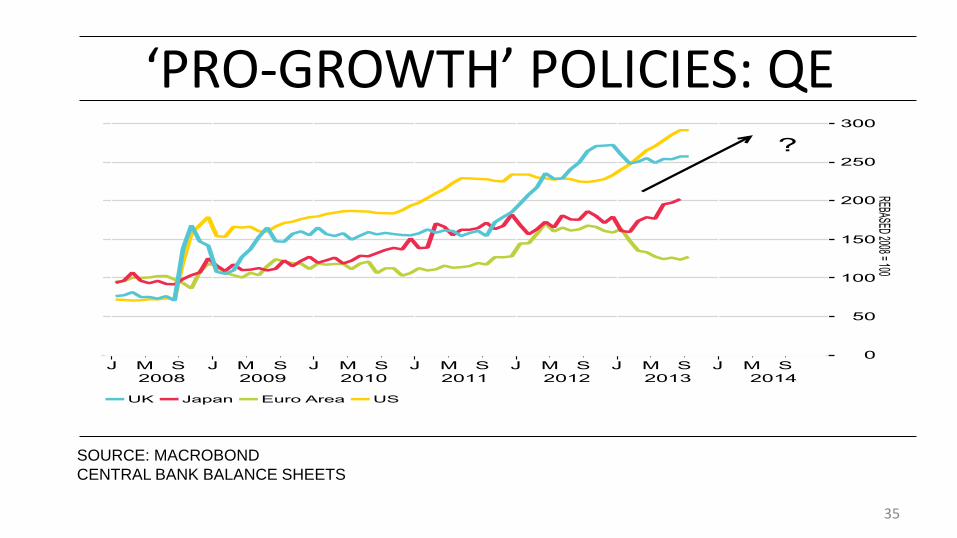

BUT COMING OFF THE STIMULANTS....

‘PRO-GROWTH’ POLICIES: QE

SOURCE: MACROBOND

CENTRAL BANK BALANCE SHEETS

35

USA - HOW TO KICK THE CAN......

36

UNDERSTANDING THE “FISCAL CLIFF” PUT IN BETTER PERSPECTIVE

U.S. Tax Revenue: $2,170,000,000,000

Fed Budget: $3,820,000,000,000

New debt: $1,650,000,000,000

National debt: $16,699,000,000,000

Recent Budget cuts: $38,500,000,000

UNDERSTANDING THE “FISCAL CLIFF” NOW LET’S REMOVE EIGHT ZEROS & PRETEND IT’S A HOUSEHOLD BUDGET...

Annual Family Income: $21,700

Money the family spent: $38,200

New debt on the Credit Card: $16,500

Outstanding Balance on that Card: $166,990

Total Budget cuts so far: $38.5

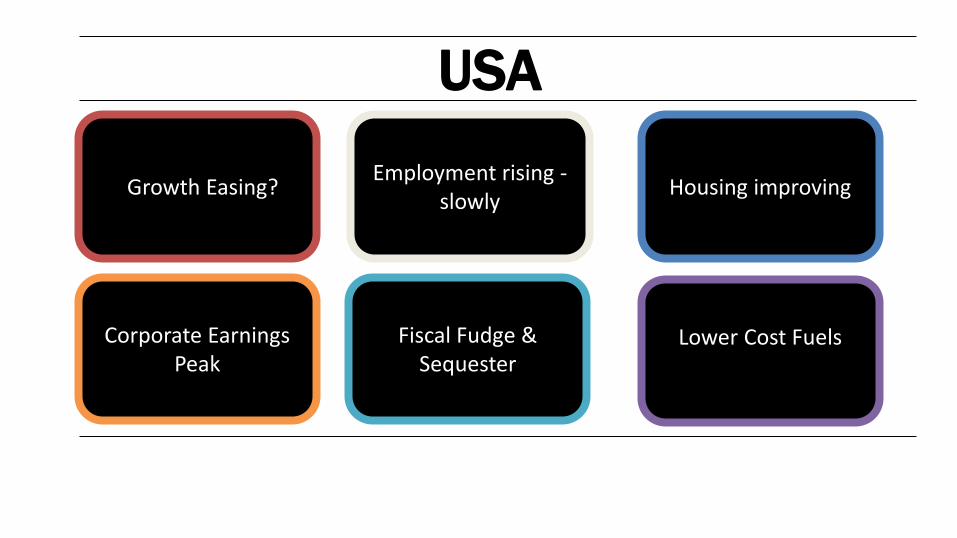

USA

Growth Easing?

Corporate Earnings Peak

Fiscal Fudge & Sequester

Housing improving Employment rising -

slowly

Lower Cost Fuels

GAME CHANGER?

US DEFICIT REDUCTION

42

A DIVIDED VIEW – Can He Do It?

EUROZONE

The Future of the Euro

German election? A decade ago 12% umplymt

Company Valuations

Austerity & Growth? ECB

buying bonds

Low Confidence

MERKEL’S DIRECTION FOR CYPRUS

45

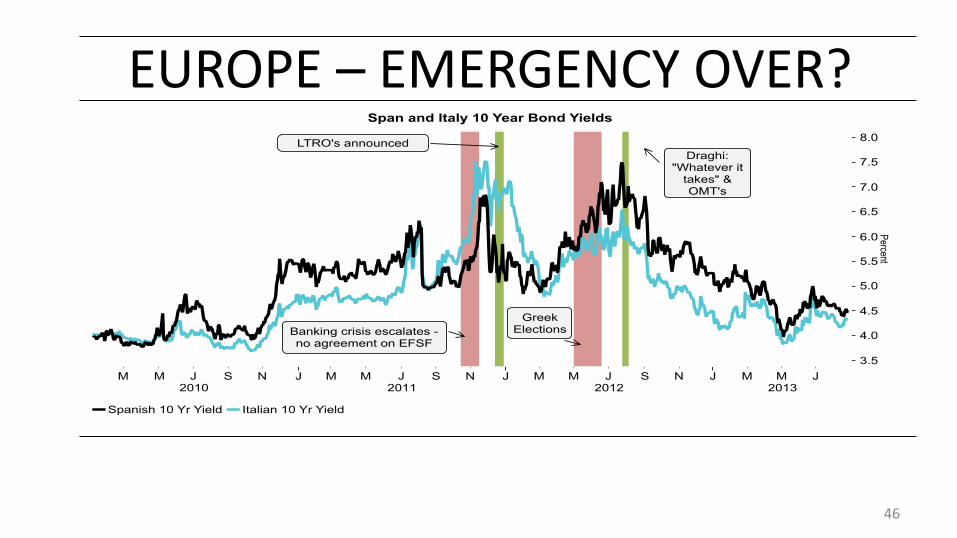

EUROPE – EMERGENCY OVER?

46

FRANCE AND GERMANY - A UNITED APPROACH?

47

Ezone Current A/c balances

November 13

“For the use of authorised intermediaries only. This document must not be

distributed to retail clients.” See notes on p25

48

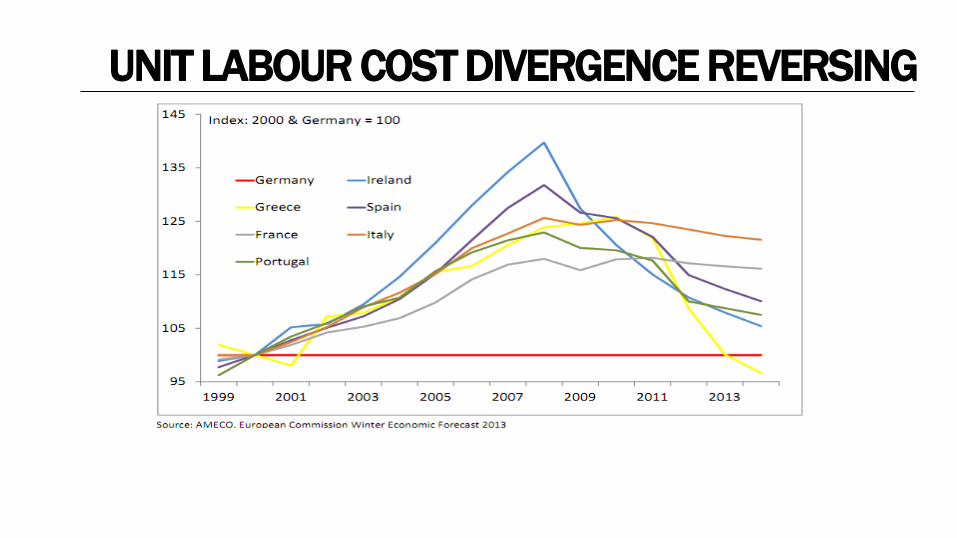

UNIT LABOUR COST DIVERGENCE REVERSING

GERMANY NEEDS EUROPE

SOURCE: MACROBOND

50

•Exports 40% to EuroZone, 31% to rest of Europe, 6% to China and 7% to USA!

EUROPE – WINDOW OF OPPORTUNITY?

SOURCE: BANK CREDIT ANALYST

51

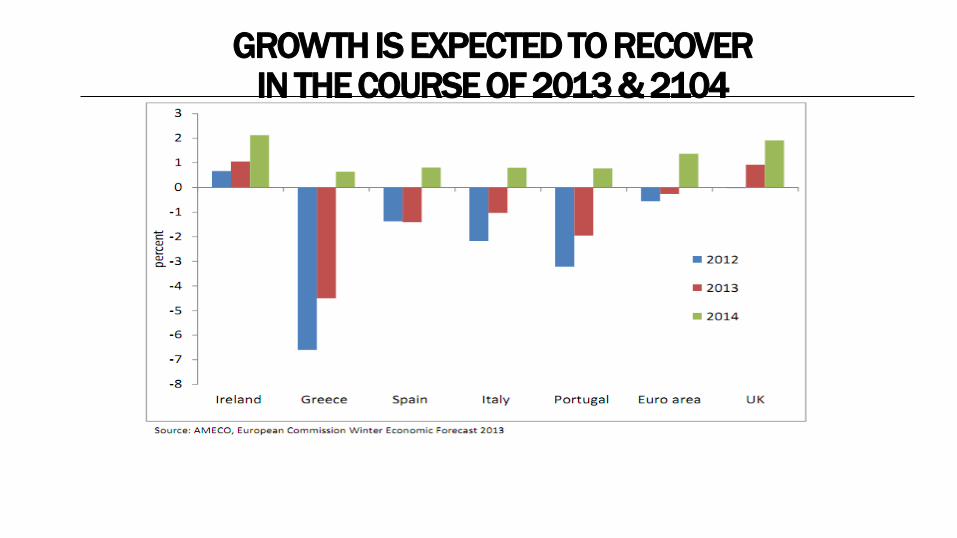

GROWTH IS EXPECTED TO RECOVER IN THE COURSE OF 2013 & 2104

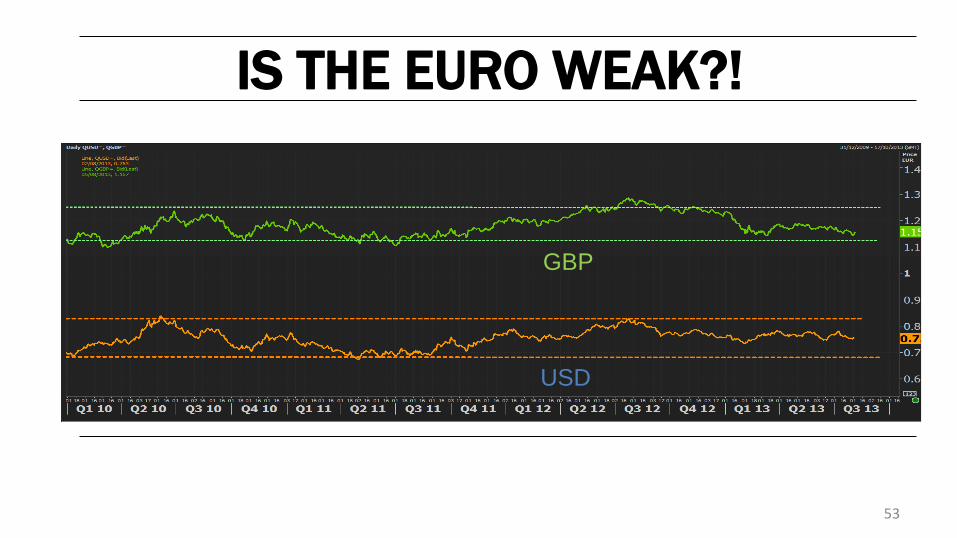

IS THE EURO WEAK?!

53

GBP

USD

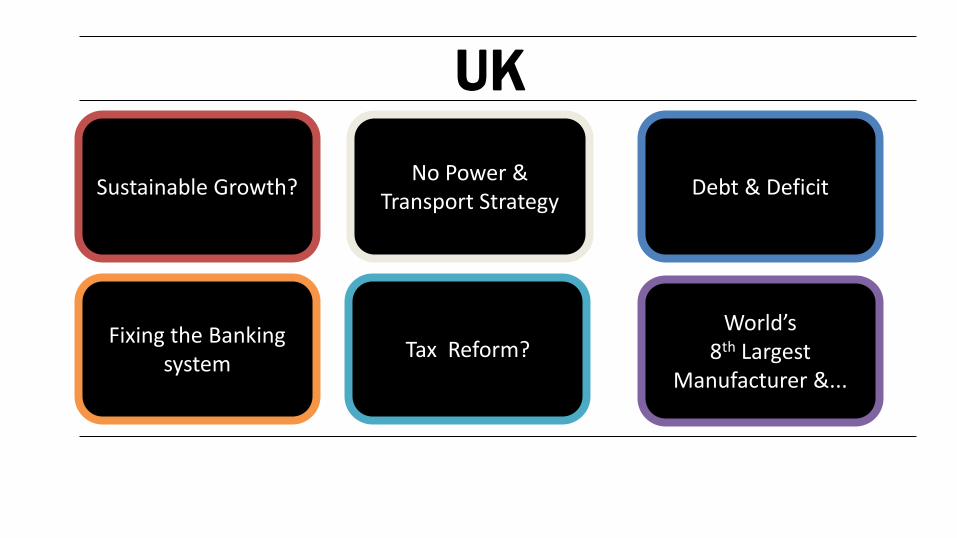

UK

Sustainable Growth?

Fixing the Banking system

Tax Reform?

Debt & Deficit No Power &

Transport Strategy

World’s 8th Largest

Manufacturer &...

55

Confident in our Leaders?

56

Break Up & Float or Float & Break Up

UK PMI SERVICES

57

SOURCE:

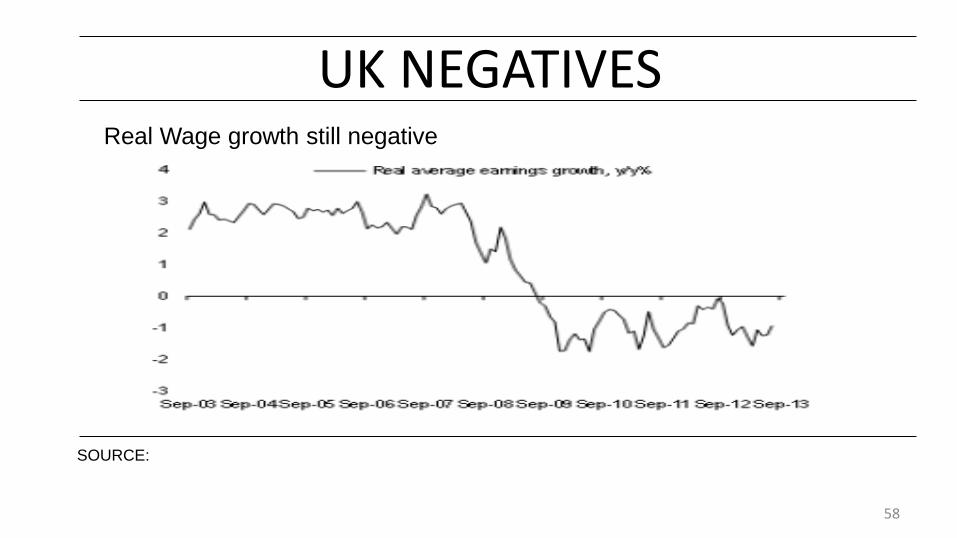

UK NEGATIVES

58

SOURCE:

Real Wage growth still negative

UNDERSTANDING our debt

Annual Family Income: £612

Money the family spent: £720

New debt on the Credit Card: £108

Outstanding Balance on that Card: £1,153

Total Budget cuts so far: £35

UK ISSUES

“Re-shoring” – Noodles

Cars more exports than domestic production

Steel • Blast furnaces

• Top end Sheffield steel

10th largest exporter

Non EU exports now higher than EU

– Rice Cookers to Asia!

– Financial/Professional trade exports £55bn

–420,000 new business start ups

DAMAGED •NOT •DOOMED

61

GOVERNMENT DEFICIT

UK ANNUAL GOVERNMENT BORROWING

2011 = £94 billion

SOURCE: DATASTREAM

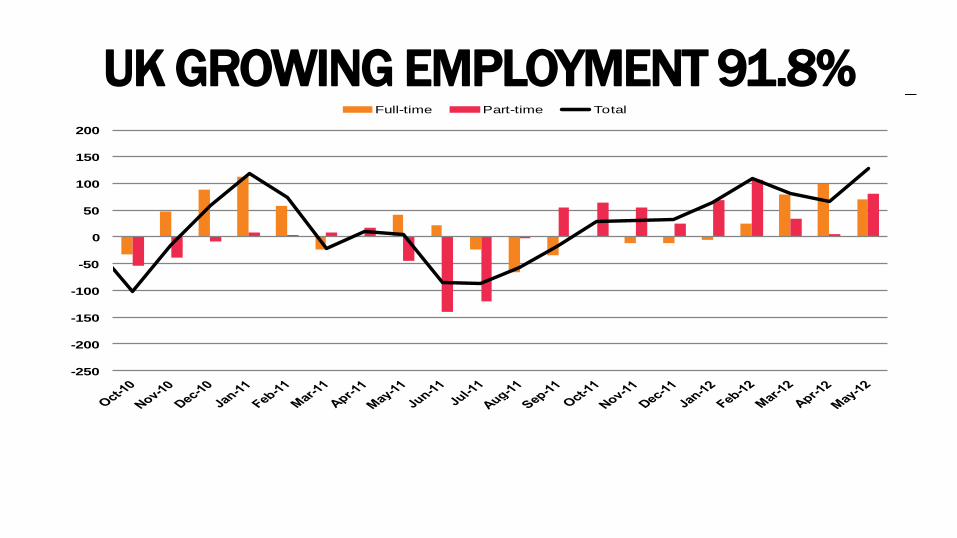

UK GROWING EMPLOYMENT 91.8%

-250

-200

-150

-100

-50

0

50

100

150

200

Full-time Part-time Total

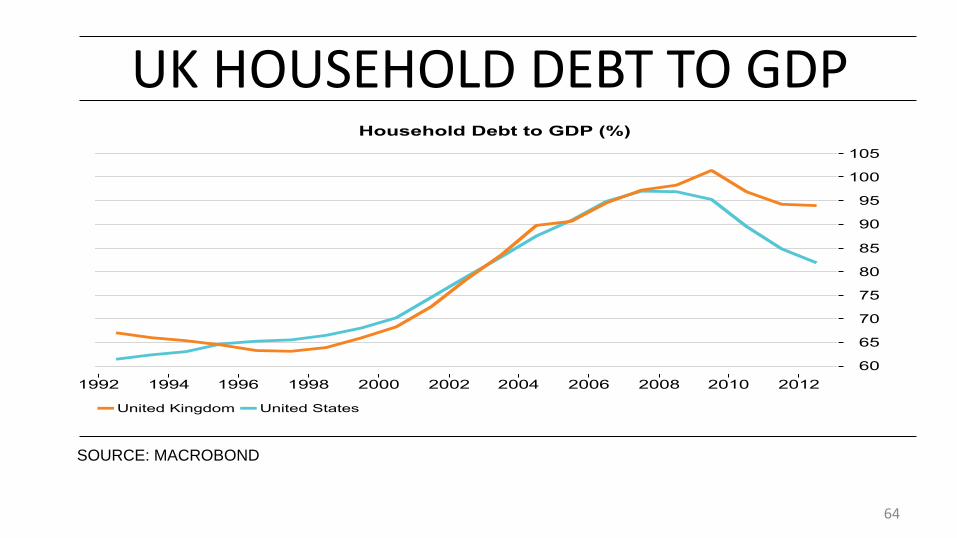

UK HOUSEHOLD DEBT TO GDP

SOURCE: MACROBOND

64

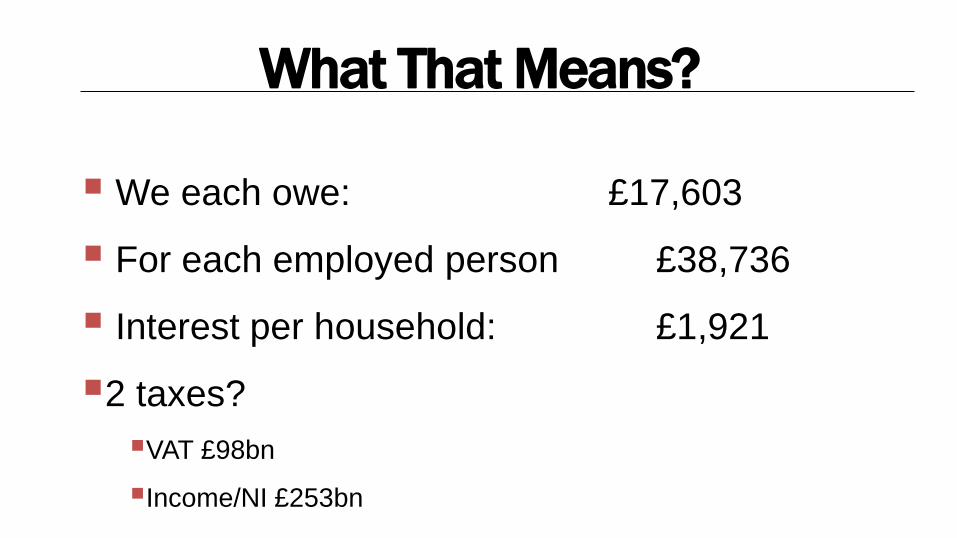

What That Means?

We each owe: £17,603

For each employed person £38,736

Interest per household: £1,921

2 taxes?

VAT £98bn

Income/NI £253bn

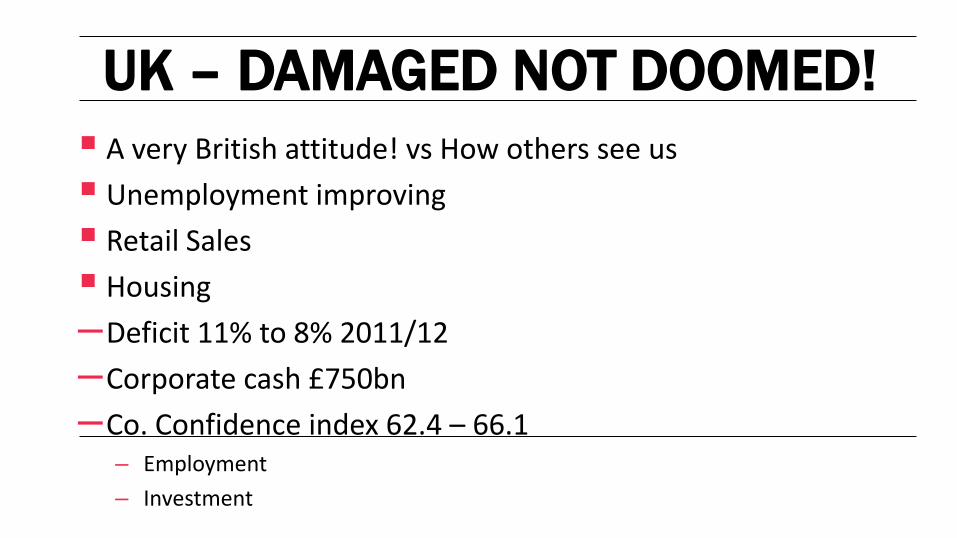

UK – DAMAGED NOT DOOMED!

A very British attitude! vs How others see us

Unemployment improving

Retail Sales

Housing

–Deficit 11% to 8% 2011/12

–Corporate cash £750bn

–Co. Confidence index 62.4 – 66.1 – Employment

– Investment

DYNAMIC ACTIONS?

Tax modernisation – 14,000 pages

Stamp Duty?

3/5 Year Start Up Holiday? – National insurance

– Employment

– Investment relief

– Infrastructure Projects & Bonds

– House building

– Peer To Peer Lending Initiatives

SOURCE: BANK OF ENGLAND

68

THE LONG AND WINDING ROAD ...the Bank of England concurs:

INFLATION LIKELY TO STAY LOW IN THE MID-TERM

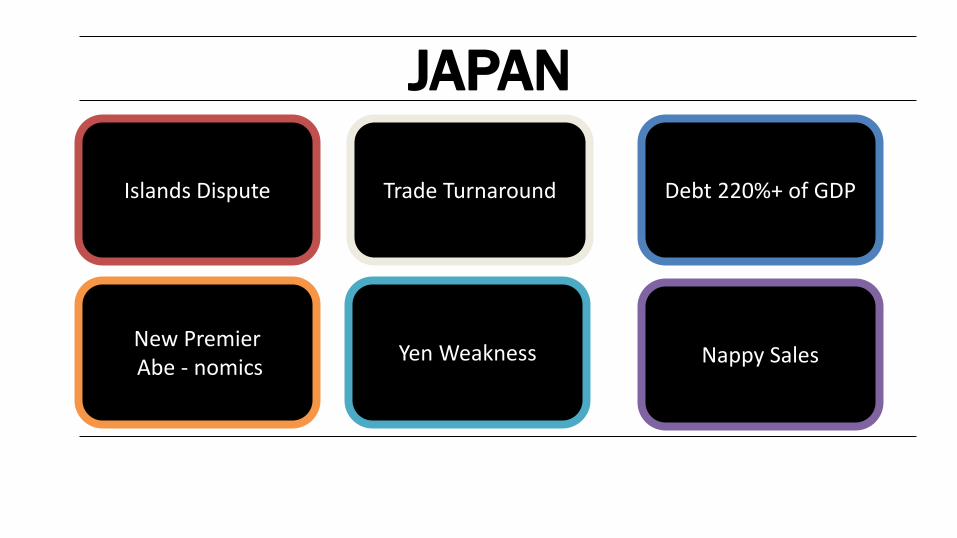

JAPAN

Islands Dispute

New Premier Abe - nomics

Yen Weakness

Debt 220%+ of GDP Trade Turnaround

Nappy Sales

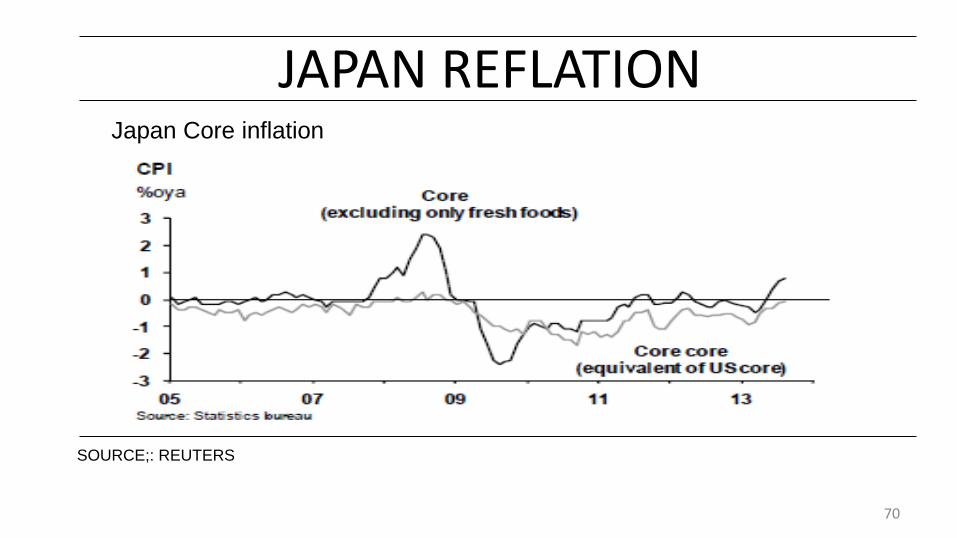

JAPAN REFLATION

SOURCE;: REUTERS

70

Japan Core inflation

BROKEN BRICS?

China Change of Life

Brazil Valuations?

South Africa Political issues

Russia Rule of law?

India flat

Turkey On the Cusp

THE NEW LEADERSHIP

A SOUTH CHINA SEA SORE

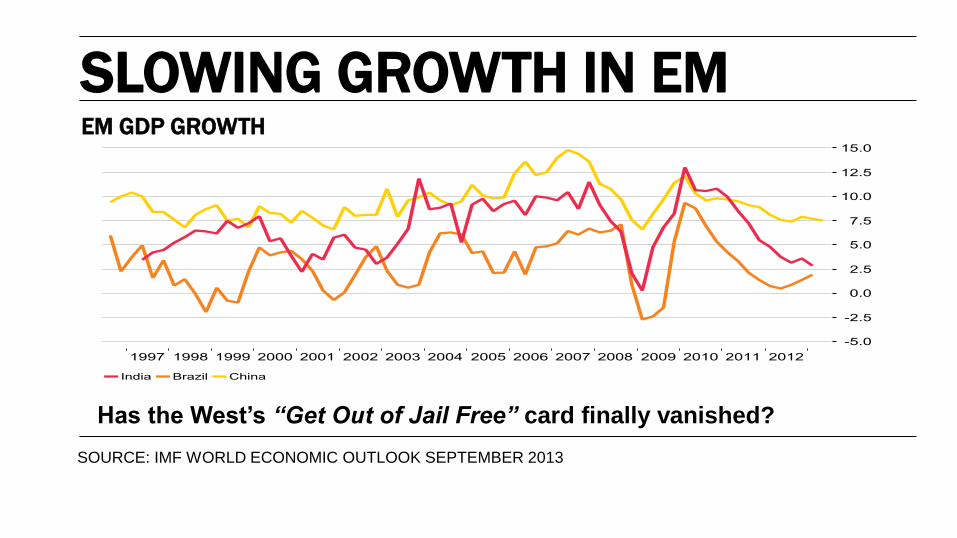

EM GDP GROWTH

Has the West’s “Get Out of Jail Free” card finally vanished?

SOURCE: IMF WORLD ECONOMIC OUTLOOK SEPTEMBER 2013

SLOWING GROWTH IN EM

November 13 75

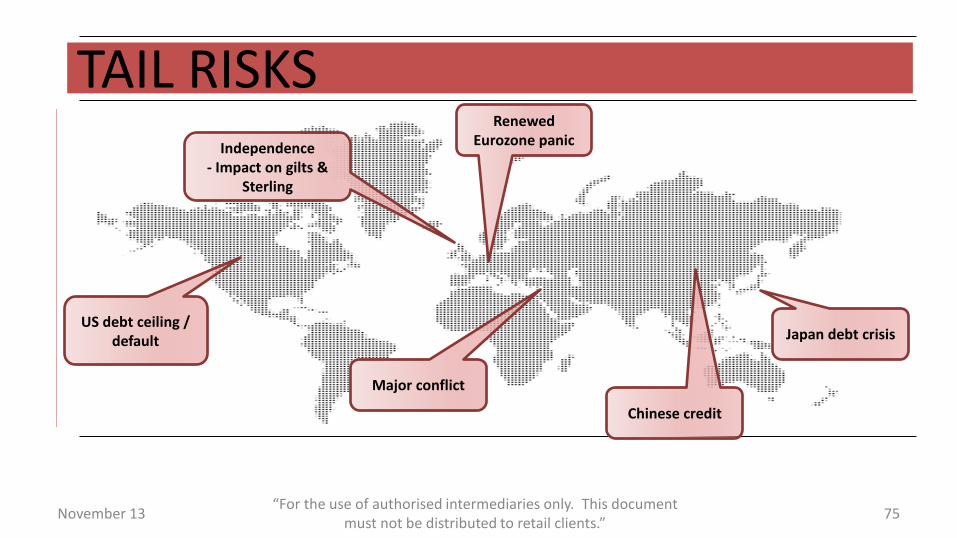

TAIL RISKS

Japan debt crisis

Renewed Eurozone panic

Major conflict

Chinese credit

“For the use of authorised intermediaries only. This document must not be distributed to retail clients.”

Independence - Impact on gilts &

Sterling

US debt ceiling / default

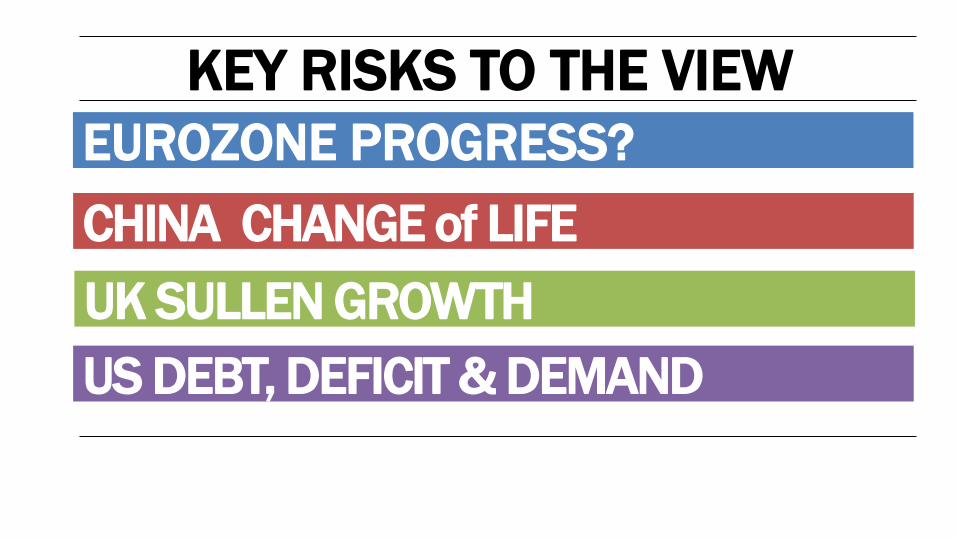

KEY RISKS TO THE VIEW

EUROZONE PROGRESS?

CHINA CHANGE of LIFE

UK SULLEN GROWTH

US DEBT, DEFICIT & DEMAND

YOU ARE NEEDED NOW

JUSTIN A URQUHART STEWART

THANK YOU

Dr Nicola Millard Customer Experience Futurologist, BT

Paul McEldon NEN Chairman

Closing the 2013 Conference

Thank you for your participation today –

please join us for networking drinks!