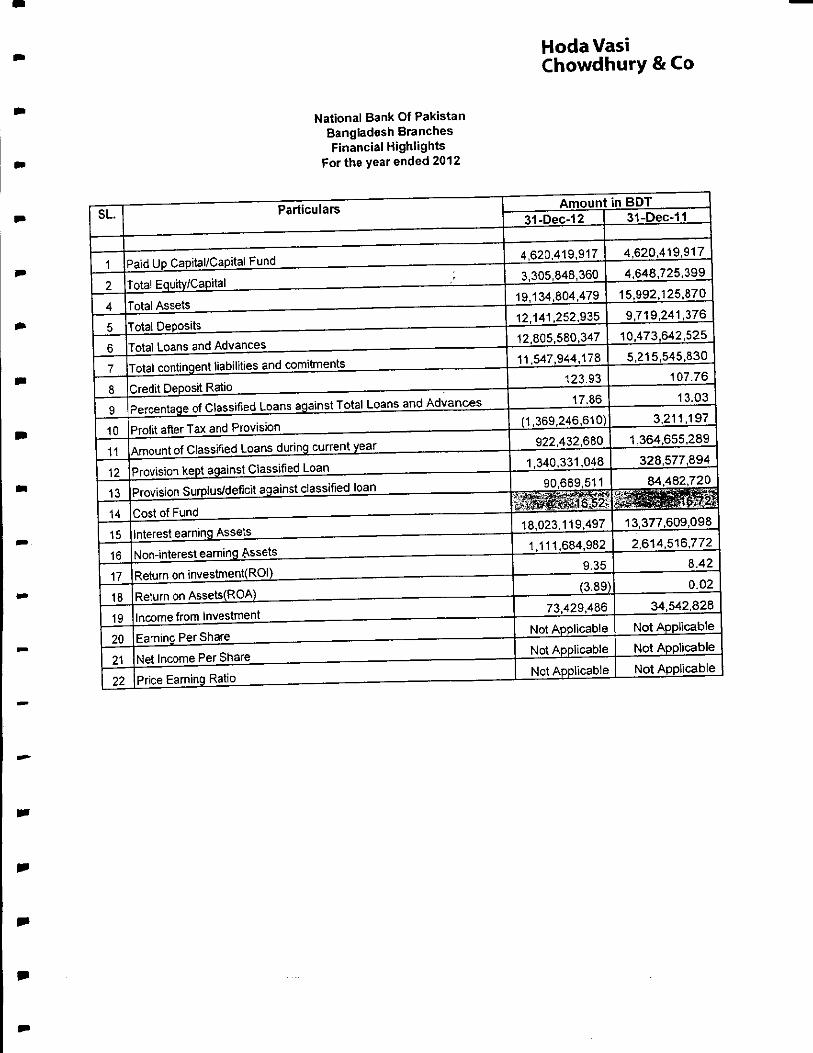

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHESnbp-bd.com/files/160215090244NBP Audited Report...

44

Hoda Vasi Chowdhury & Co NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES Audited Financial Statements For the year ended 31 December 2012

Transcript of NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHESnbp-bd.com/files/160215090244NBP Audited Report...

Hoda VasiChowdhury & Co

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES

Audited Financial StatementsFor the year ended 31 December 2012

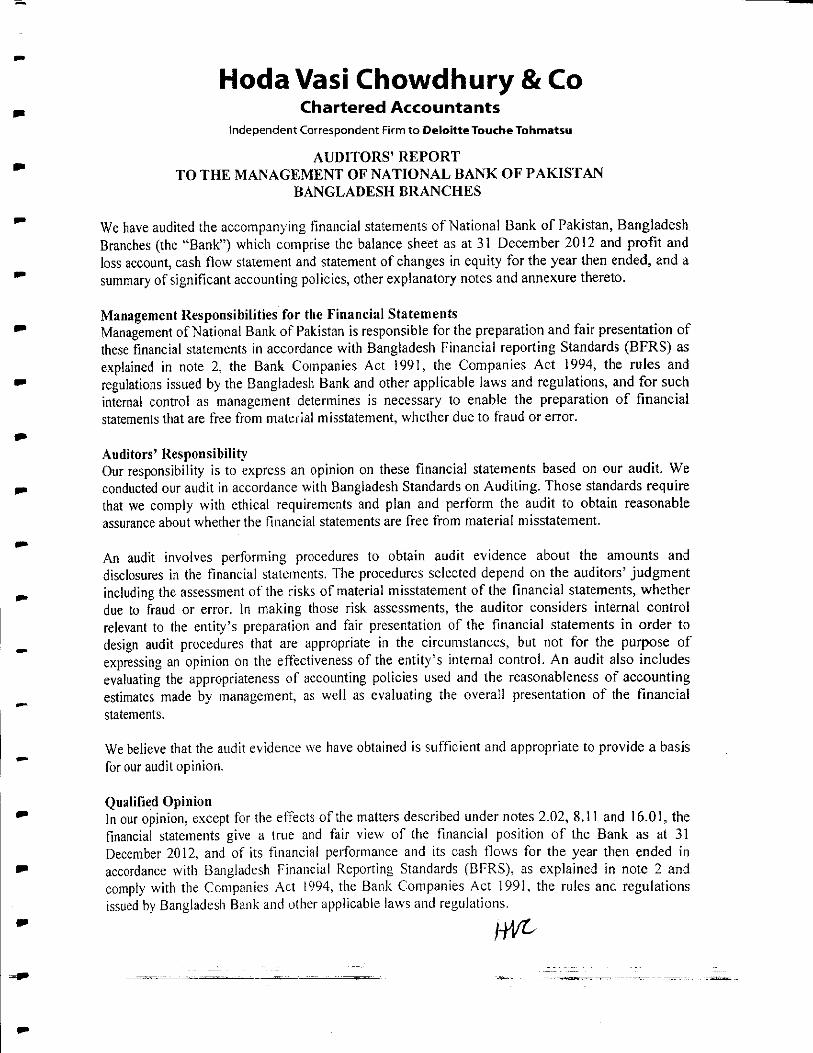

Hoda Vasi Chowdhury & Co Chartered Accountants

Independent Correspondent Firm to Deloitte Touche Tohmatsu

AUDITORS' REPORT TO THE MANAGEMENT OF NATIONAL BANK OF PAKISTAN

BANGLADESH BRANCHES

We have audited the accompanying financial statements of National Bank of Pakistan, BangladeshBranches (the "Bank") which comprise the balance sheet as at 31 December 2012 and profit andloss account, cash flow statement and statement of changes in equity for the year then ended, and asummary of significant accounting policies, other explanatory notes and annexure thereto.

Management Responsibilities for the Financial StatementsManagement of National Bank of Pakistan is responsible for the preparation and fair presentation ofthese financial statements in accordance with Bangladesh Financial reporting Standards (BFRS) asexplained in note 2, the Bank Companies Act 1991, the Companies Act 1994, the rules andregulations issued by the Bangladesh Bank and other applicable laws and regulations, and for suchinternal control as management determines is necessary to enable the preparation of financialstatements that are free from material misstatement, whether due to fraud or error.

Auditors' ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with Bangladesh Standards on Auditing. Those standards requirethat we comply with ethical requirements and plan and perform the audit to obtain reasonableassurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control

relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial

statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Qualified Opinion In our opinion, except for the effects of the matters described under notes 2.02, 8.11 and 16.01, the financial statements give a true and fair view of the financial position of the Bank as at 31 December 2012, and of its financial performance and its cash flows for the year then ended in accordance with Bangladesh Financial Reporting Standards (BFRS), as explained in note 2 and comply with the Companies Act 1994, the Bank Companies Act 1991, the rules and regulations issued by Bangladesh Bank and other applicable laws and regulations.

Hoda Vasi Chowdhury & Co

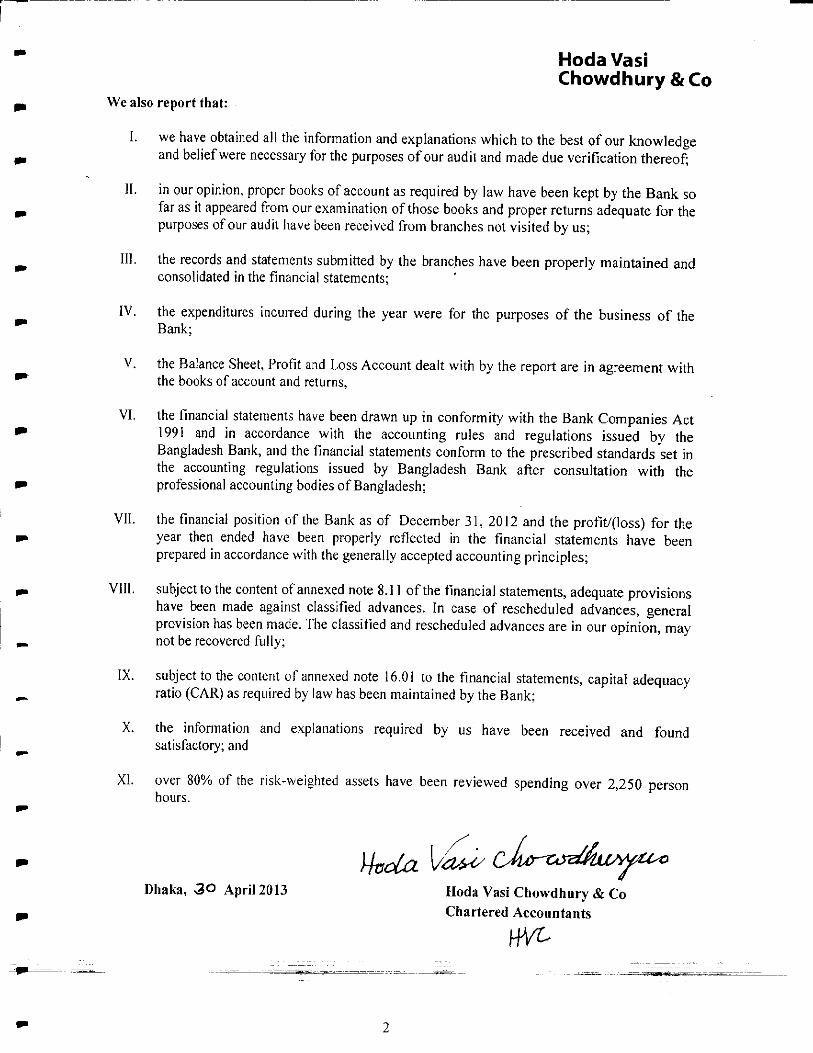

We also report that:

I. we have obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit and made due verification thereof;

II. in our opinion, proper books of account as required by law have been kept by the Bank so far as it appeared from our examination of those books and proper returns adequate for the purposes of our audit have been received from branches not visited by us;

III.the records and statements submitted by the branches have been properly maintained and consolidated in the financial statements;

IV.the expenditures incurred during the year were for the purposes of the business of the Bank;

V. the Balance Sheet, Profit and Loss Account dealt with by the report are in agreement with the books of account and returns,

VI. the financial statements have been drawn up in conformity with the Bank Companies Act 1991 and in accordance with the accounting rules and regulations issued by the Bangladesh Bank, and the financial statements conform to the prescribed standards set in the accounting regulations issued by Bangladesh Bank after consultation with the professional accounting bodies of Bangladesh;

VII. the financial position of the Bank as of December 31, 2012 and the profit/(loss) for the year then ended have been properly reflected in the financial statements have been prepared in accordance with the generally accepted accounting principles;

VIII. subject to the content of annexed note 8.11 of the financial statements, adequate provisions have been made against classified advances. In case of rescheduled advances, general provision has been made. The classified and rescheduled advances are in our opinion, may not be recovered fully;

IX. subject to the content of annexed note 16.01 to the financial statements, capital adequacy ratio (CAR) as required by law has been maintained by the Bank;

X. the information and explanations required by us have been received and found satisfactory; and

XL over 80% of the risk-weighted assets have been reviewed spending over 2,250 person hours.

nvoia. Va^y cJio-^o^tuAytc^

Dhaka, 3 April 2013Hoda Vasi Chowdhury & Co

Chartered Accountants

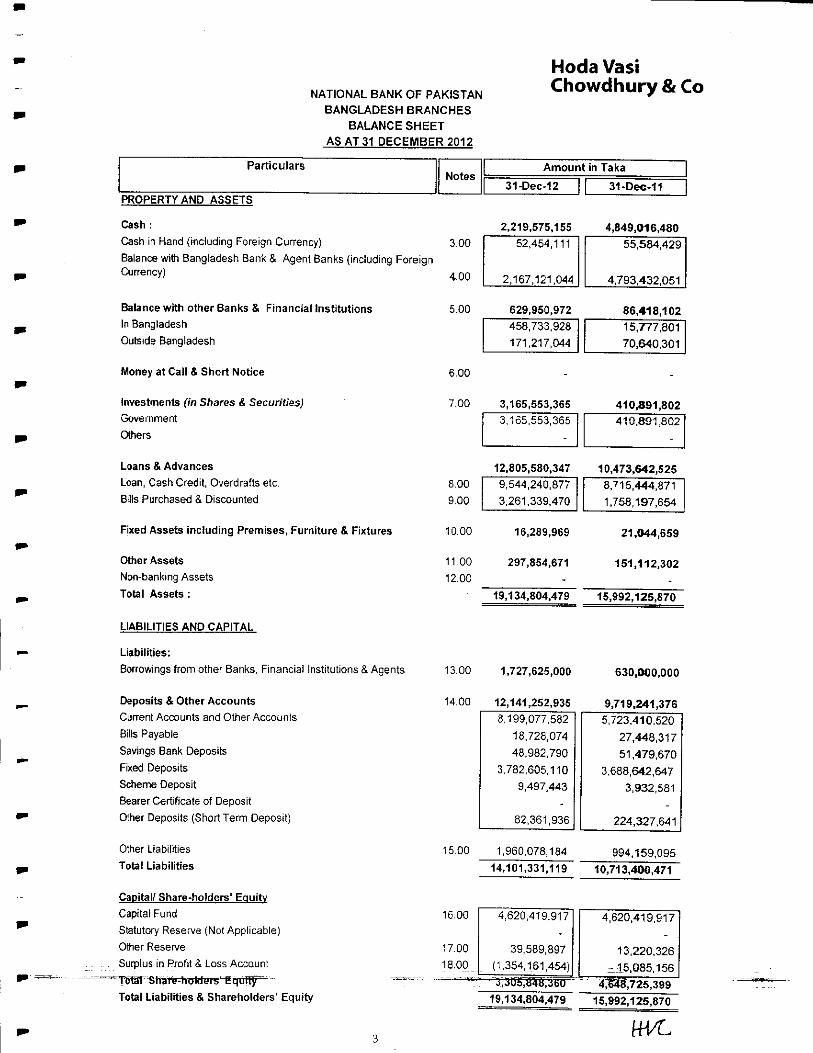

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES

BALANCE SHEET AS AT 31 DECEMBER 2012

Hoda VasiChowdhury&Co

ParticularsNotes

PROPERTY AND ASSETS

Cash: Cash in Hand (including Foreign Currency)

Balance with Bangladesh Bank & Agent Banks (including Fore Currency)

Balance with other Banks & Financial Institutions In Bangladesh

Outside Bangladesh

Money at Call & Short Notice

Investments (in Shares & Securities) Government

Others

Loans & Advances Loan, Cash Credit, Overdrafts etc.

Bills Purchased & Discounted

Fixed Assets including Premises, Furniture & Fixtures

Other Assets Non-banking Assets

Total Assets :

LIABILITIES AND CAPITAL

Liabilities: Borrowings from other Banks, Financial Institutions & Agents

Deposits & Other Accounts Current Accounts and Other Accounts

Bills Payable

Savings Bank Deposits

Fixed Deposits Scheme Deposit

Bearer Certificate of Deposit

Other Deposits (Short Term Deposit)

Other Liabilities

Total Liabilities

Capital/ Share-holders' Equity Capital Fund

Statutory Reserve (Not Applicable)

Other Reserve

Surplus in Profit & Loss Account

"T^^^^SrraTO^hoWCTS^qtmr"-^*>=~

Total Liabilities & Shareholders' Equity

3.00

4.00

5.00

6.00

7.00

8.009.00

10.00

11.0012.00

16,289,969

297,854,671

21,044,659

151,112,302

19,134,804,479 15,992,125,870

ttVL

Amountin

31-Dec-12|[

2,219,575,155

52,454,111

2,167,121,044

629,950,972458,733,928

171,217,044

Taka

31-Dec-11

4,849,016,480

55,584,429

4,793,432,051

86,418,10215,777,801

70,640,301

3,165,553,365 410,801,802

9,544,240,877

3,261,339,4708,715,444,871

1,758,197,664

13.00

14.00

15.00

16.00

17.00

18.00

1,727,625,000

12,141,252,9358.199,077,582

18,728,074

48,982,7903,782,605,110

9,497,443

82,361,936

1,960,078,184

14.101,331,119

4,620,419,917

39,589,897(1,354,161,454)3,305,878,360

19,134,804,479

630,000,000

9,719,241,3765,723,410.520

27,448,317

51,479,670

3,688,642,647

3,932,581

224,327,641

994,159,095

10,713,400,471

4,620,419,917

13,220,326

-15,085,156

15,992,125,870

Hoda VasiChowdhury & Co

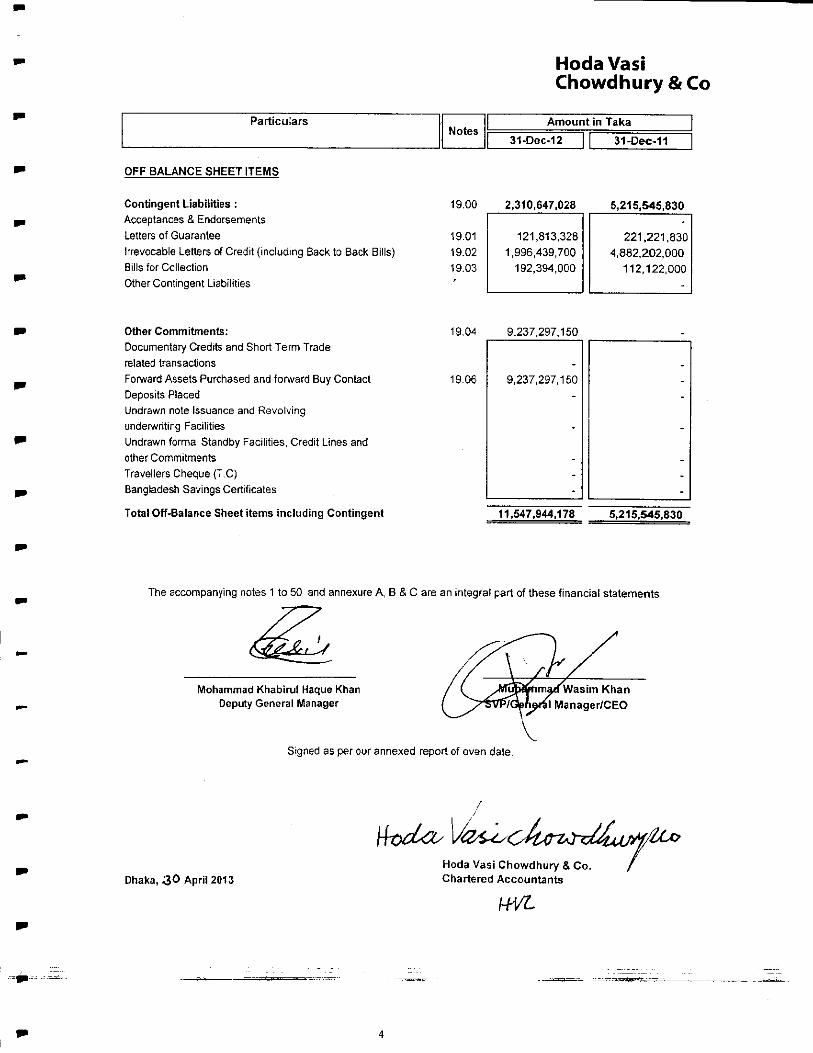

nParticularsNotes

Amount in Taka31-Dec-12 | f 31-Dec-11

OFF BALANCE SHEET ITEMS

Contingent Liabilities:Acceptances & EndorsementsLetters of GuaranteeIrrevocable Letters of Credit {including Back to Back Bills)Bills for CollectionOther Contingent Liabilities

19.00 2,310,647,028 ^,215,545,830

19.01 121,813,3281,996,439,700

192,394,000

221,221,8304,882,202,000

112,122,000

Other Commitments:Documentary Credits and Short Term Traderelated transactionsForward Assets Purchased and forward Buy ContactDeposits PlacedUndrawn note Issuance and Revolvingunderwriting FacilitiesUndrawn formal Standby Facilities, Credit Lines andother CommitmentsTravellers Cheque (T.C)Bangladesh Savings Certificates

Total Off-Balance Sheet items including Contingent

19.049,237,297,150

9,237,297,150

11,547,944,1785,215,545,830

The accompanying notes 1 to 50 and annexure A, B & C are an integral part of these financial statements.

Mohammad Khabirul Haque Khan Deputy General Manager

Signed as per our annexed report of even datt

\\t>dasVau.

Dhaka, 3<> April 2013Hoda Vasi Chowdhury & Co.Chartered Accountants

HVL

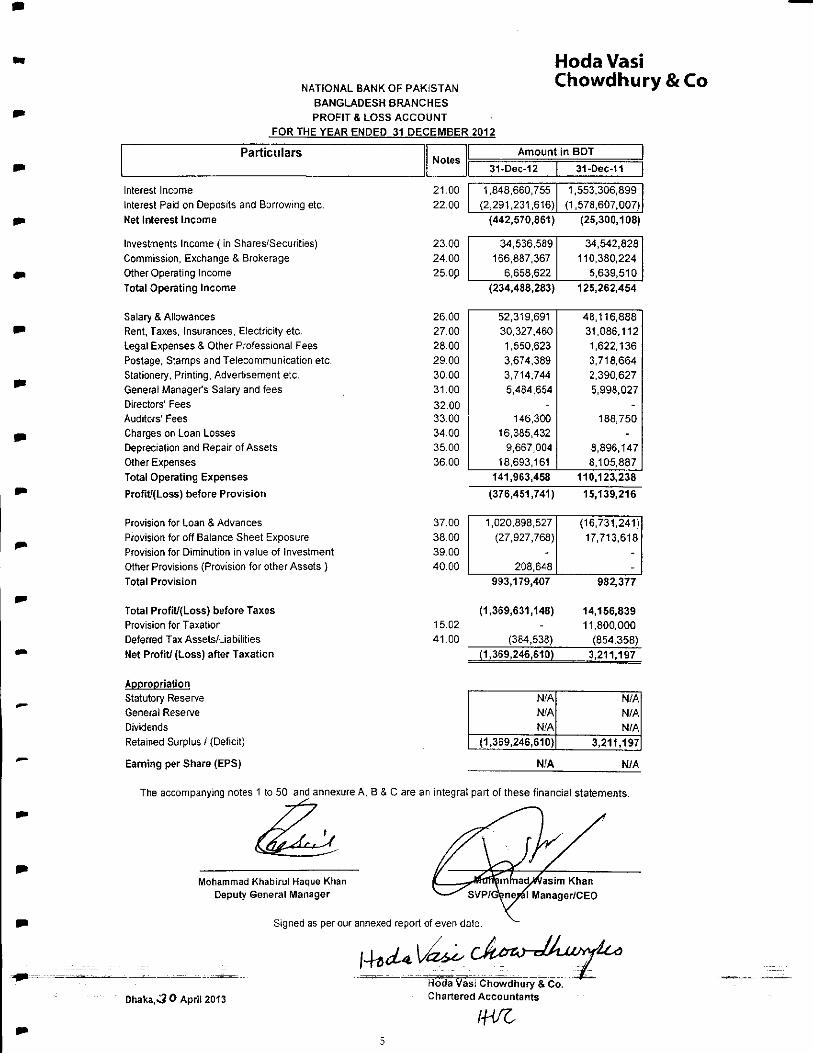

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES PROFIT & LOSS ACCOUNT

FOR THE YEAR ENDED 31 DECEMBER 2012

Hoda VasiChowdhury&Co

Net Interest Income

Investments Income (in Shares/Securities)Commission, Exchange & BrokerageOther Operating IncomeTotal Operating Income

Salary & AllowancesRent, Taxes, insurances, Electricity etc.Legal Expenses & Other Professional FeesPostage, Stamps and Telecommunication etc.Stationery, Printing, Advertisement etc.General Manager's Salary and feesDirectors' FeesAuditors' FeesCharges on Loan LossesDepreciation and Repair of AssetsOther ExpensesTotal Operating Expenses

Profit/{Loss) before Provision

Provision for Loan & AdvancesProvision for off Balance Sheet ExposureProvision for Diminution in value of InvestmentOther Provisions (Provision for other Assets )Total Provision

(442,570,861) (25,300,108)

(234,488,283) 125,262,454

141,963,458 110,123,238

(376,451,741)15,139,216

993,179,407 982,377

Total Profit/(Loss) before TaxesProvision for TaxationDeferred Tax Assets/LiabilitiesNet Profit/ (Loss) after Taxation

AppropriationStatutory ReserveGeneral ReserveDividendsRetained Surplus / (Deficit)

Earning per Share (EPS)

(1,369,631,148) 14,156,83915.02-11,800,00041.00(384,538)(854,358)

(1,369,246,610) 3,211,197

The accompanying notes 1 to 50 and annexure A, B & C are an integral part of these financial statements.

Mohammad Khabirul Haque Khan Deputy General Manager

Signed as per our annexed report of even daie.

Dhaka, JO April 2013

'rHoda Vasi Chowdhury & Co. Chartered Accountants

iwc

Particulars

InterestIncomeInterestPaidonDepositsandBorrowingetc.

Notes

21.0022.00

AmountinBDT

31-Dec-12

1,848,660,755(2,291,231,616)

31-Dec-11

1,553,306,899(1,578,607,007)

23.0024.0025.0P

34,536,589166,887,367

6,658,622

34,542,828110,380,224

5,639,510

26.0027.0028.0029.0030.0031.0032.0033.0034.0035.0036.00

52,319,69130,327,4601,550,6233,674,3893,714,7445,484,654

146,30016,385,432

9,667,00418,693,161

48,116,88831,086,1121,622,1363,718,6642,390,6275,998,027

188,750

8,896,1478,105,887

37.0038.0039.0040.00

1,020,898,527(27,927,768)

-208,648

(16,731,241}17,713,618

N/AN/AN/A

(1,369,246,610)

ill

3,211,197

Hoda VasiChowdhury & Co

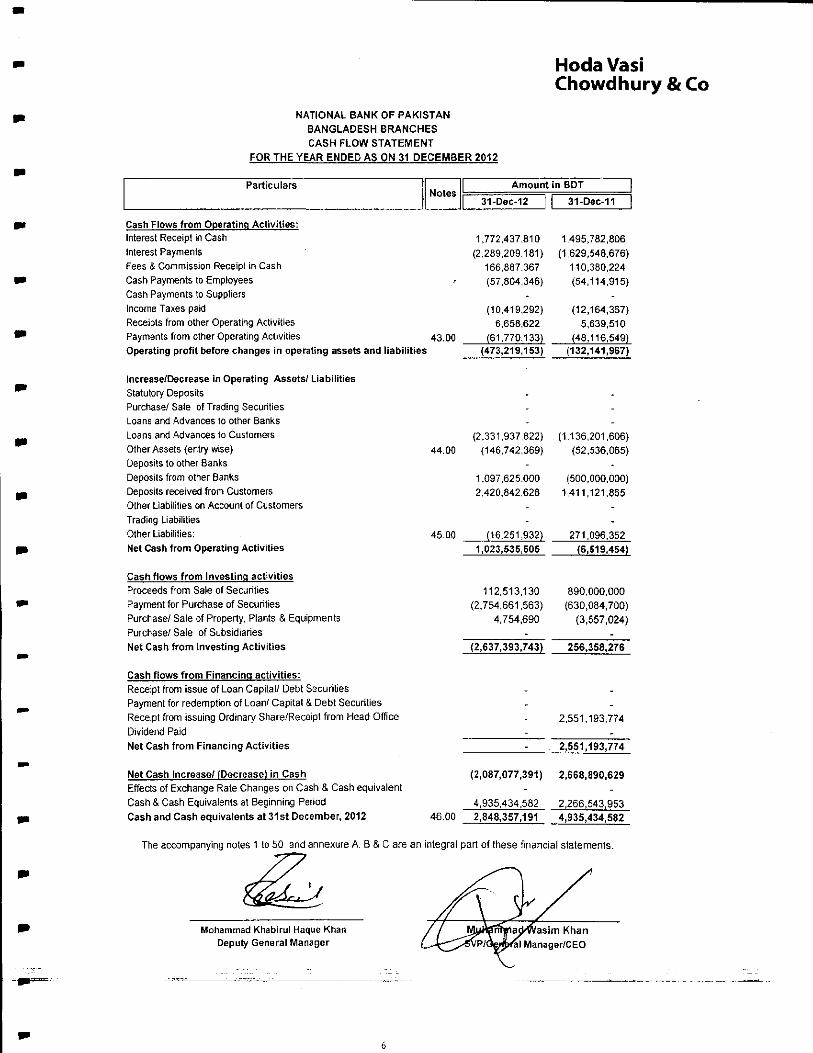

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES CASH FLOW STATEMENT

FOR THE YEAR ENDED AS ON 31 DECEMBER 2012

Particulars Amount in BDT31-Dec-11I

Cash Flows from Operating Activities:Interest Receipt in CashInterest PaymentsFees & Commission Receipt in CashCash Payments to EmployeesCash Payments to SuppliersIncome Taxes paidReceipts from other Operating ActivitiesPayments from other Operating Activities43,00Operating profit before changes in operating assets and liabilities

Increase/Decrease in Operating Assets/ LiabilitiesStatutory DepositsPurchase/Sale of Trading SecuritiesLoans and Advances 10 other BanksLoans and Advances to CustomersOther Assets {entry wise)Deposits to other BanksDeposits from other BanksDeposits received from CustomersOther Liabilities on Account of CustomersTrading LiabilitiesOther Liabilities:Net Cash from Operating Activities

1,772,437.810(2,289,209181)

166,887,367 (57.804,346)

(10,419,292) 6,658,622

(61,770,133)

1.495,782,806(1629,548,676)

110,380,224 (54,114,915)

(12,164,387) 5,639,510

(48,116,549)(473,219,153) (132,141,967)

Cash flows from Investing activitiesProceeds from Sate of SecuritiesPayment for Purchase of SecuritiesPurchase/ Sale of Property, Plants & EquipmentsPurchase/Sale of SubsidiariesNet Cash from Investing Activities

Cash flows from Financing activities:Receipt from issue of Loan Capital/ Debt SecuritiesPayment for redemption of Loan/ Capital & Debt SecuritiesReceipt from issuing Ordinary Share/Receipt from Head OfficeDividend PaidNet Cash from Financing Activities

Net Cash Increase/ (Decrease) in CashEffects of Exchange Rate Changes on Cash & Cash equivalentCash & Cash Equivalents at Beginning PeriodCash and Cash equivalents at 31st December, 2012

(2,331.937,822) (1,136,201,606)44.00 (146,742,369)(52.536.065)

1,097,625.000 (500,000,000)2,420,842628 1,411,121,865

(16,251.932)

112,513,130890,000,000(2,754,661,563)(630,084,700)

4,754,690(3,557,024)

(2,637,393,7437256,358,277"

2,551,193,774

(2,087,077,391) 2,668,890,629

4,935,434,582 2,266,543,95346 00 2,848,357,191 4,935,434,582

The accompanying notes 1 to 50 and annexure A. B & C are an integral part of these financial statements.

Mohammad Khabirul Haque Khan Deputy General Manager

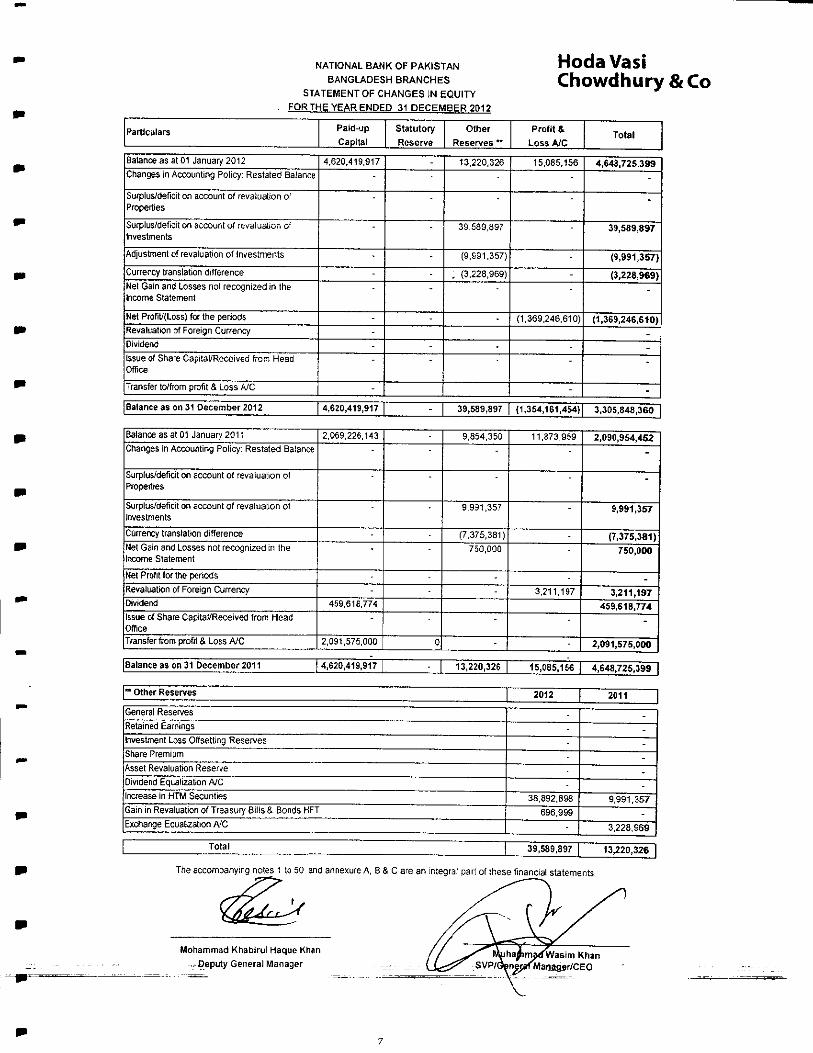

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES

STATEMENT OF CHANGES IN EQUITYFOR THE YEAR ENDED 31 DECEMBER 2012

Hoda VasiChowdhury &Co

The accompanying notes 1 to 50 and annexure A, B & C are an integral part of these financial statements.

Mohammad Khabirul Haque Khan -Deputy General Manager

Particulars

Balanceasat01January2012ChangesinAccountingPolicy:RestatedBalance

Surplus/deficitonaccountofrevaluationofProperties

Surplus/deficitonaccountofrevaluationofInvestments

AdjustmentofrevaluationofInvestments

CurrencytranslationdifferenceNetGainandlossesnolrecognizedintheIncomeStatement

NetProfit/(Loss)fatheperiodsRevaluationofForeignCurrencyDividendIssueofShareCapital/ReceivedfromHeadOffice

Transferto/fromprofit&LossA/C

Paid-upCapital

4,620,419,917

|Balanceason31December2012|4,620,419,917

StatutoryReserve

-

OtherReserves"

13.220,326

39,589,897

(9.S91.357)

,(3,228,969)

39,589,897

Balanceasat01January2011ChangesinAccountingPolicy:RestatedBalance

Surplus/deficitonaccountofrevaluationolProperties

Surplus/deficitonaccountofrevalualionofInvestmentsCurrencytranslationdifferenceNetGainandLossesnotrecognizedintheIncomeStatementNeiProfitfortheperiodsRevaluationofForeignCurrencyDividendIssueofShareCapital/ReceivedfromHeadOfficeTransferfromprofit&LossA/C

2,069.226,143

459,616,774

2,091,575,000

|8alanceason31December2011 4,620,419,917

|@OtherReserves

0

9,854,350

8,991,357

(7,375,381)750,000

Profit&LossA/C

15,085,156

(1.369,246,610)

(1,354,161,454)

Total

4,648,725,399

39,589,897

(8,991,357)

(3,228,969)

(1,369,246,610)

--

3,305,848,360

11,873,959

3,211,197

@|13,220,326|15,085,156

GeneralReservesRetainedEarningsInvestmentLossOffsettingReservesSharePremiumAssetRevaluationReserveDividendEqualizationA/CIncreaseinHTMSecuritiesGaininRevaluationofTreasuryBills&BondsHF TExchangeEcualizationA'C

Total

2012

38,892,898696,999

39,589,897

2,090,954,452

-

9,991,357

(7,375,381)750,000

3,211,197459,618,774

2,091,575,000

4,648,725,399

2011

-

9,991,357

3.228,969

13,220,326|

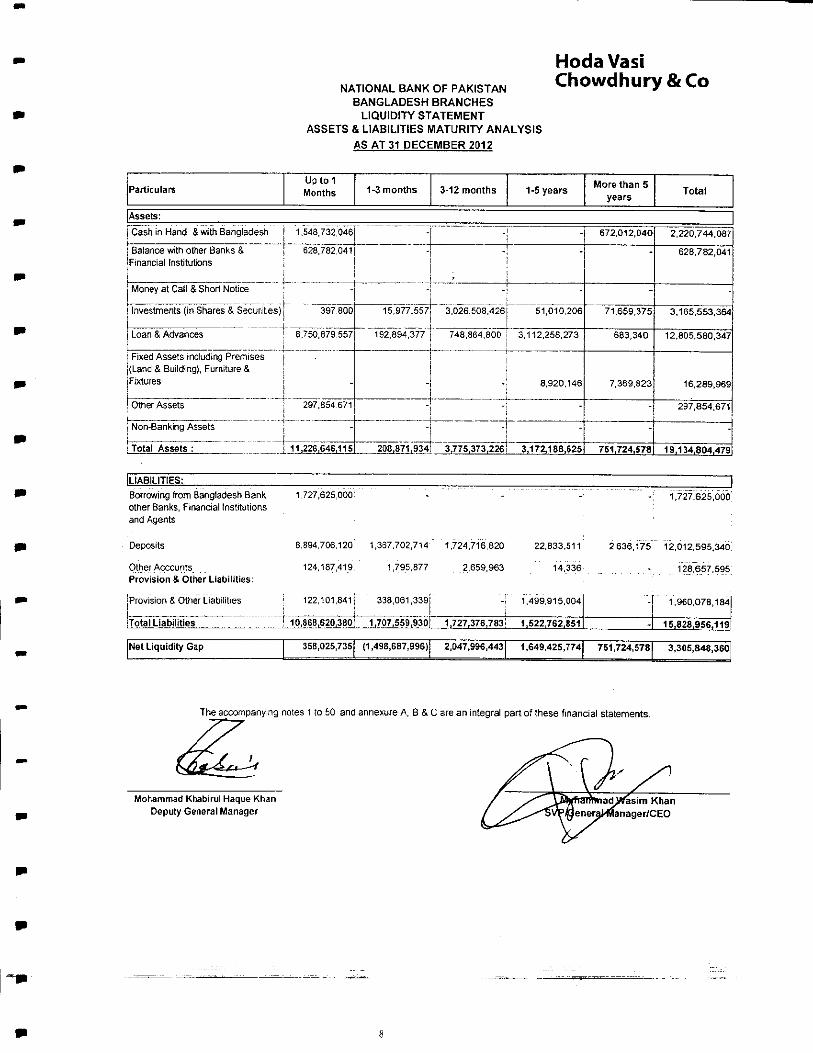

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES

LIQUIDITY STATEMENTASSETS & LIABILITIES MATURITY ANALYSIS

AS AT 31 DECEMBER 2012

HodaVasiChowdhury & Co

Borrowing from Bangladesh Bank,other Banks, Financial Institutionsand Agents

Other AccountsProvision & Other Liabilities:

8,894,706,120 1,367,702,714 1,724,716,820

124,187,419.1,795,8772,659,963

22.B33.5112,636.175 12,012.595,340

14.336-128,657.595

The accompanying notes 1 to 50 and annexure A, B & C are an integral part of these financial statements.

Mohammad Khabirul Haque Khan Deputy General Manager

ParticularsUptoiMonths 1-3months 3-12months 1-5years Morethan5

yearsTotal

Assets:CashinHand&withBangladesh

BalancewithotherBanks&FinancialInstitutions

MoneyatCail&ShortNotice

Investments(inSharesSSecurit.es)

Loan&Advances

FixedAssetsincludingPremises(Land&Building),Furniture&Fixtures

OtherAssets

Non-BankingAssets

TotalAssets:

1,548,732,046

628.782,0411"!-)-.

"|"@

i8,750,879.557

297.854671

11,226,646,115

51,010,206

1S2.S94.377]748.864,800j3,112.258,273

!|1";

j@!208,871,934f3,775,373,226:3,172,188,625

672,012,040

71,659,375

683,340

7,369,823

751,724,578

2,220,744,087

628,782,041

3,165,553,364

12,805,580,347

16,289,969

297,854,671

19,134,804.479

Provision&OtherLiabilities

.TotalLiabilities

NetLiquidityGap

122,101,841

10,86^620^80

35B.025.735

338,061,339

_1,707,559,930

(1,498,687,996)

1,727,376,783

2,047,996,443

1.499,915.004

1,522,762,851

1,649,425,774

"-

-

751,724,578

1,960,078,184

15,828,956.119

3,305,848,360

Hoda VasiChowdhury & Co

NATIONAL BANK OF PAKISTAN BANGLADESH BRANCHES

NOTES TO THE FINANCIAL STATEMENTFOR THE YEAR ENDED 31 DECEMBER 2012

1.00 Status and nature of business:

a)Status of the Bank:

National Bank of Pakistan ("NBP) was established under the National Bank of Pakistan Ordinance, 1949 and is listed on all the stock exchanges in Pakistan. It's registered and head office is situated at I.I. Chundriger Road, Karachi. It commenced banking operation in Bangladesh at Dhaka since August 1994, Chittagong branch since 15 April 2004, Sylhet branch since March 2008 and Gulshan Branch since April 2008 (hereinafter referred as the "Bank").

b)Nature of Business

The Principal activities of the Bank in Bangladesh are to provide all kinds of commercial banking services to its customers.

2.00Significant Accounting Policies and basis of preparation of financial statements:

2.01Basis of Preparation of the Financial Statement:

The financial statements of the Bank are made up to 31 December 2012 and are prepared under the historical cost convention, except investment in certain types of government securities which are stated at fair value, in accordance with the "First Schedule (Section-38) of the Bank Companies Act 1991 as amended by the Bangladesh Bank vide BRPD circular number 14 dated 25 June 2003 and other Bangladesh Bank circulars, International Financial Reporting Standards (IFRS) adopted by the Institute of Chartered Accountants of Bangladesh (ICAB) as Bangladesh Financial Reporting Standards ("BFRS") and other laws and rules applicable in Bangladesh.

In case the requirement of provisions and Circulars issued by Bangladesh Bank differ with those of other regulatory authorities and accounting standards, the provisions and Circulars issued by Bangladesh Bank shall prevail. The major such difference is in relation to the provision for loans and advances which is mentioned below.

As per BAS 39, an entity should start the impairment assessment by considering whether objective evidence of impairment exists for financial assets that are individually significant. For financial assets which are not individually significant, the assessment can be performed on an individual or collective (portfolio) basis.

As per the Bangladesh Bank BRPD Circular no. 14 & 15 dated 23 September 2012 and BRPD Circular no. 19 dated 27 December 2012, a general provision at 0.25% to 5% under different categories of unclassified loans (standard/ SMA loans) should be maintained regardless of objective evidence of impairment. Specific provision for sub standard loans, doubtful loans and bad losses should be provided at 20%, 50% and 100% respectively for loans and advances depending on the duration of overdue. Also, a general provision at 1% should be provided for all off-balance sheet exposures. Such

-- provision policies are not specificaltyJoJine with those prescribed by BAS 39.

Hoda VasiChowdhury & Co

2.02 Going Concern

The Bank has recorded a net loss after provision and tax ot ik i,jo,<:<tD,oiu ^ui i.profit of Tk 3,211,197) for the year ended 31 December 2012 and has a regulatory capitalshortfall of Tk 909,215,605 as at balance date. The ability of the Bank to continue itsbusiness activity is dependent on successful recovery of loans and advances, increasingbusiness volumes necessary to achieve profitable operations, the success of commercialand strategic initiatives already been taken, and continued financial and liquidity supportof the overseas network of the Bank as well as its head office.

Accordingly, the management of the Bank have prepared the financial statements on the going concern assumption. The head office of the' Bank has already remitted USD 11.50 million on 4 February 2013 as further injection of capital. Overseas networks of NBP have already provided on balance sheet funding support to the tune of USD 68.5 million and JPY 4,000 million respectively. The Bank is also rigorously following-up recovery of its overdue/past due balances and successfully rescheduled a number of such loans and ^niiartciri ciihGtantial amount of cash as down-payment.

2.03Consolidation

A Separate set of records for consolidating trie statement of affairs and income and expenditure of the branches were maintained at the Dhaka branch of the Bank based on which these financial statements have been prepared.

2.04Foreign currency transaction:

Foreign currency transactions are converted into equivalent Taka using the ruling exchange rates on the dates of respective transactions as per BAS-21-"The effects of Changes in Foreign Exchange Rates". Foreign currencies balances held in US dollar are @@itort intn Taka at mid rate of the bank on the closing date of every week.

(b)

Foreign Currency transactions are converted into Taka currency at tne excnangerates prevailed on the dates of such transactions.

Assets and Liabilities outstanding on 31 December 2011 in foreign currencyhauo hApn mnverted into Taka currency at the following rates:

! Country Currency Mid rate

2.05 Gains and Losses of transactions:

Gains and losses of transactions are dealt with through exchange account in profit and loss account except Balance held with Bangladesh Bank in Foreign Currency against Capital Fund. No loss/gain effect has been considered against capital fund held with

Ranntadesh Bank

10

U.S.AU.S.A

U.K

JAPANEUROPE

USD-1=(Cash)USD-1=(Others)

JPY-1=

EURO-1=

Regular80.5080.50

130.16460.9400

106.2331

Hoda VasiChowdhury & Co

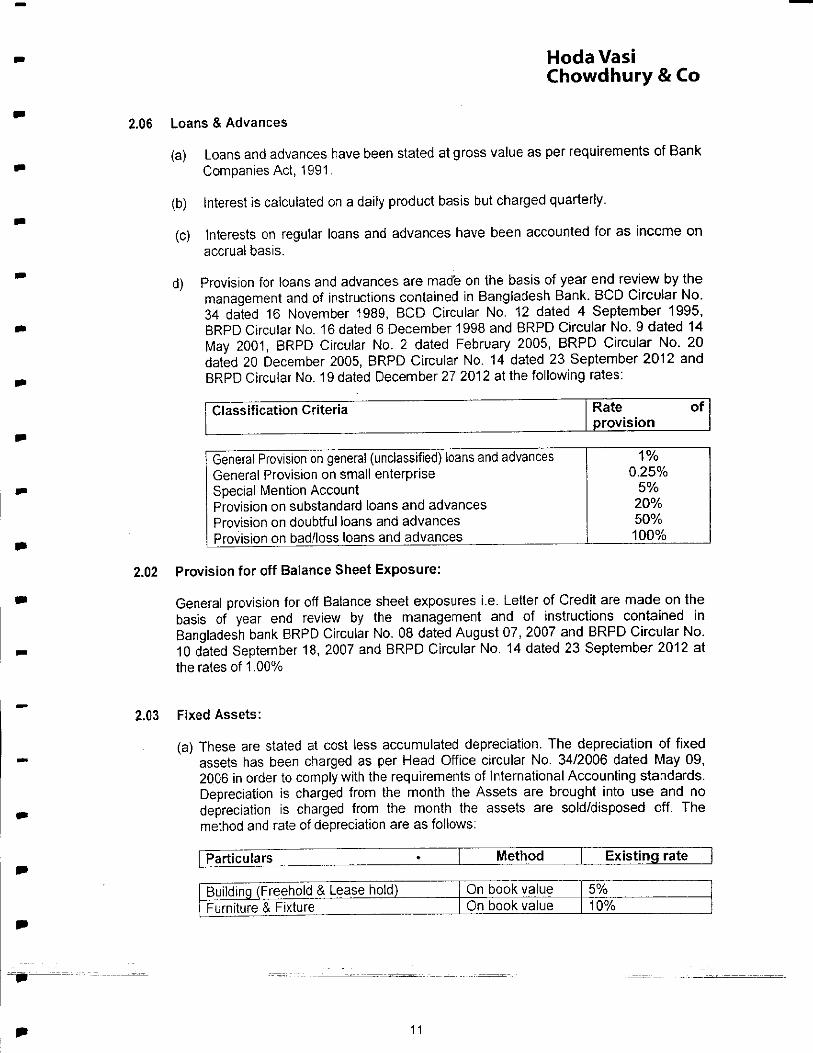

2.06 Loans & Advances

(a)Loans and advances have been stated at gross value as per requirements of Bank Companies Act, 1991.

(b)Interest is calculated on a daily product basis but charged quarterly.

(c)Interests on regular loans and advances have been accounted for as income on accrual basis.

d) Provision for loans and advances are made on the basis of year end review by the management and of instructions contained in Bangladesh Bank. BCD Circular No. 34 dated 16 November 1989, BCD Circular No. 12 dated 4 September 1995, BRPD Circular No. 16 dated 6 December 1998 and BRPD Circular No. 9 dated 14 May 2001, BRPD Circular No. 2 dated February 2005, BRPD Circular No. 20 dated 20 December 2005, BRPD Circular No. 14 dated 23 September 2012 and BRPD Circular No. 19 dated December 27 2012 at the following rates:

Classification Criteria Rateprovision

of

General Provision on general (unclassified) loans and advancesGeneral Provision on small enterpriseSpecial Mention AccountProvision on substandard loans and advancesProvision on doubtful loans and advances

Provision on bad/loss loans and advances

1%0.25%

5% 20% 50%100%

2.02 Provision for off Balance Sheet Exposure:

General provision for off Balance sheet exposures i.e. Letter of Credit are made on the basis of year end review by the management and of instructions contained in Bangladesh bank BRPD Circular No. 08 dated August 07, 2007 and BRPD Circular No. 10 dated September 18, 2007 and BRPD Circular No. 14 dated 23 September 2012 at the rates of 1.00%

2.03 Fixed Assets:

(a) These are stated at cost less accumulated depreciation. The depreciation of fixed assets has been charged as per Head Office circular No. 34/2006 dated May 09, 2006 in order to comply with the requirements of International Accounting standards. Depreciation is charged from the month the Assets are brought into use and no depreciation is charged from the month the assets are sold/disposed off. The method and rate of depreciation are as follows:

Particulars Method Existingrate

Building(Freehold&Leasehold)Furniture&Fixture

OnbookvalueOnbookvalue

5%10%

Hoda VasiChowdhury&Co

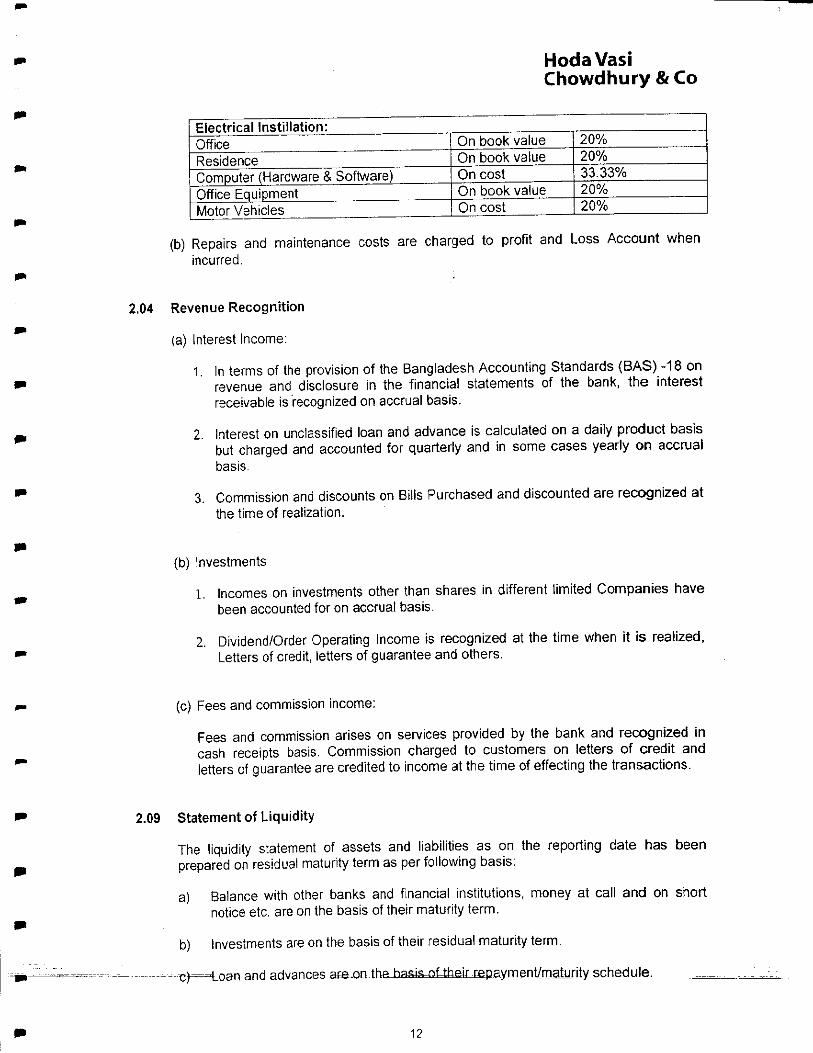

(b) Repairs and maintenance costs are charged to profit ana loss Accouni wnen

2.04 Revenue Recognition

(a) Interest Income:

1.In terms of the provision of the Bangladesh Accounting Standards (BAS) -18 on revenue and disclosure in the financial statements of the bank, the interest receivable is recognized on accrual basis.

2.Interest on unclassified loan and advance is calculated on a daily product basis but charged and accounted for quarterly and in some cases yearly on accrual

basis.

3.Commission and discounts on Bills Purchased and discounted are recognized at thus timo nf reali7atinn.

(b) Investments

1.Incomes on investments other than shares in different limited Companies have been accounted for on accrual basis.

2.Dividend/Order Operating Income is recognized at the time when it is realized, I ptters of credit, letters of guarantee and others.

(c) Fees and commission income:

Fees and commission arises on services provided by the bank and recognized in cash receipts basis. Commission charged to customers on letters of credit and letters of quarantee are credited to income at the time of effecting the transactions.

2.09 Statement of Liquidity

The liquidity statement of assets and liabilities as on the reporting date has been prepared on residual maturity term as per following basis:

a)Balance with other banks and financial institutions, money at call and on short notice etc. are on the basis of their maturity term.

b)Investments are on the basis of their residual maturity term.

@ -- c>=Loan and advances are-on the_basJs=QLtbiuepayment/maturity schedule.

OfficeResidenceComputer(Hardware&Software)

MotorVehicles

OnbookvalueOnbookvalueOncostOnbookvalueOncost

20%20%33.33%20%20%

Hoda vasi Chowdhury & Co

d)Fixed assets are on the basis of their useful lives.

e)Other assets are on the basis of their adjustment.

f)Borrowings from other banks, financial institutions and agents as per their maturity/

repayment term

g)Deposits and other accounts are on the basis of their maturity term and behavioral

past trend.

h) Other long term liability on the basis of their maturity term.

i) Provisions and other liabilities are on the basis of their settlement.

2.10Cash Flow Statement

Cash Flow Statement is prepared principally in accordance with BAS 7 "Cash Flow Statement" and the cash flow from the operating activities have been presented under direct method as prescribed by the Securities and Exchange Rules 1987 and considering the provisions of Paragraph 18 (b) of BAS-7 which provides that "Enterprises are Encouraged to Report Cash Flow from Operating Activities using the

Direct Method".

2.11Statement of Changing in Equity

Statement of Changing in Equity has been prepared in accordance with BAS- 1 /'Presentation of Financial Statements" and under the guidelines of Bangladesh Bank BRPD Circular No.14 dated June 25, 2003.

2.12Taxation

(i) Current Tax

Provision for Income Tax has been made @ 42.50% as prescribed in the Financial Act, 2012 of accounting profit made by the bank after considering some of the taxable add backs of income and disallowances of expenditures.

(ii) Deferred Tax:

Deferred tax liabilities are the amounts of income taxes payable in future periods in respect of taxable temporary differences. Deferred tax assets are the amount of income taxes recoverable in future periods in respect of taxable temporary differences. Deferred tax assets and liabilities are recognized for the future tax consequences of timing differences arising between the carrying values of assets, liabilities, income and expenditure and their respective tax basis. Deferred tax assets and liabilities are measured using tax rates and tax laws that have been enacted or substantially enacted at the balance sheet date. The impact on the account of changes in the deferred tax assets and liabilities has also been recognized in the profit and loss account. Disclosures of Deferred Tax have been made on the basis of the instructions contained in Bangladesh Bank. BRPD Circular No. 11 dated 12 nQootnhor9ni1

13

Hoda VasiChowdhury & Co

2.13 Deposits and Other Accounts:

Deposits and other accounts include bills payable and have been analyzed in terms ofthe maturity grouping showing separately other deposits are inter-bank deposits.

2.14 Investment

Value of investment has been enumerated as follows:

2.15 Reconciliation of inter-bank/inter-branch account

Books of account with regard to inter-bank (in Bangladesh and outside Bangladesh) are subsequently reconciled.

2.16 Provision for liabilities:

A provision is recognized in the balance sheet when the bank has a legal or constructive obligation as a result of a past event and it is provable that an outflow of economic benefit will be required to settle the obligations, in accordance with the Bangladesh Accounting Standard (BASJ-37 -Provision, Contingent Liabilities and contingent Assets.

2.17 Retirement benefits to the employments:

(a) Provident Fund

Contributory provident fund benefit is given to the staff of the bank who complete consecutive five years of his/her service of the bank. This amount is payable only at the time of retirement or realize from the bank. Incase the employee whishes to get realize or dismissed by the bank before completion of service, he/she will get only his/her contribution towards provident fund account. The registration of provident fund with NBR is under process.

(b) Gratuity/pension fund:

Pension fund is given only to those employees at the time of his/her retirement or realize from the bank who have complete consecutive 5 years service with the bank. He /she will receive his/her 5 times of the last drown basic, provision in respect of which, is made annually covering all its permanent employees. Actuarial valuation of gratuity scheme had been made to access the adequacy of the liabilities provided for the scheme as per BAS-19 "Employee Benefits".

Items

GovernmenttreasuryPortfolioGovernmenttreasuryPortfolio

bill

bill

and

and

Bonds

Bonds

under

under

HTM

HFT

Applicableaccountingvalue

AtamortizedCostBasis

ValuedatMarkedtomarketonWeeklybasis

a

HodaVasiChowdhury & Co

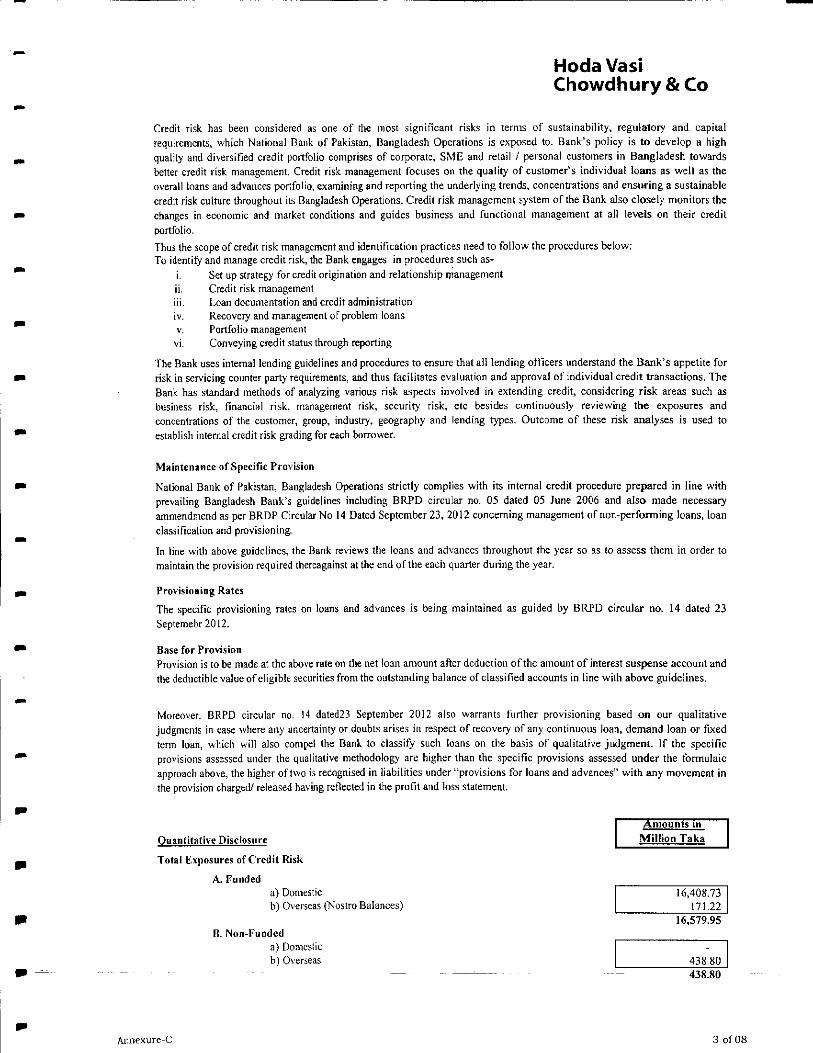

2.18 Risk management

The risk of the National bank of Pakistan is defined as the possibility of losses, financialor otherwise. The risk management of the bank covers 6 (six) crore risk areas ofbanking i.e. Credit Risk Management, Foreign Exchange Risk Management, AssetLiability Management, Prevention of money Laundering and through the establishmentof Internal Control and Compliances. The prime objective of the risk management is thatthe Bank takes well calculative business risks while safeguarding the banks capital, itsfinancial resources and profitability from various risks. In this context, the bank tooksteps to implement the guidelines of Bangladesh bank as under.

(a) Credit risk management:

Credit risk is one of the major risks faced by the bank. This can described as potential loss arising from the failure of counterparty to perform as per contractual agreement with the bank. The failure may result from unwillingness of the counterparty or decline in his/her financial condition. Therefore bank's credit risk management activities have been designed to address all these issues.

The bank has segregated duties of the officers/executives involved in credit related activities. Credit approval, administration, monitoring and recovery function have been segregated.

(b) Foreign Exchange Risk Management

Foreign exchange risk is defined as the potential change in earnings arising due to change in market prices. The foreign exchange risk of the bank is the minimal as all the transaction are carried out on behalf of the customers against underlying L/C commitments and other remittance requirements. No dealing on banks account was conducted during the year.

Treasury department independently conducts the transactions and back office of treasury is responsible for verification of the deals and passing of their entries in the books of account. All foreign exchange transaction are valued at Market to Market rate as determined by Bangladesh Bank at the month-end. All Nostro Accounts are reconciled on monthly basis and outstanding entry beyond 30 days is reviewed by the management for its settlement.

(c) Assets Liability Management

The Asset Liability Committee (ALCO) of the bank monitors market risk and liquidity risks of the bank. The market risk is defined as potential change in earnings due to change in rate of interest, foreign exchange rates which are not of trading nature. Asset Liability Committee (ALCO) reviews liquidity requirement of the bank, the maturity of assets and liabilities, deposit and lending, pricing strategy and the liquidity contingency plan. The primary objective of the ALCO is to monitor and avert significant volatility in Net Interest Income (NIL), investment value and exchange earnings.

Hoda VasiChowdhury & Co

(d) Prevention of money Laundering

Money laundering risk is defined as the loss of reputation and expenses incurredas penalty for being negligent in prevention in money laundering. For mitigating therisks, the bank has a designated Chief Compliance officer who independentlyreviews the transactions of the accounts to verify suspicious transactions. Manualsfor prevention of money laundering have been established and transaction profilehas been introduced. Training has been continuously given to all the category ofofficers and executives for developing awareness and skill for identifyingsuspicious activities.

(e) Internal Control and compliances

Operational loss may arise from error and fraud due to lack of internal control and compliance. Management through Internal Control and compliance division undertakes the review of the operational and compliance of statutory requirement.

(f) Information Communication Technology

ICT risk management is embedded in internal control and Compliance Policy of the Bank which are widely used for managing the union between business process and information system effectively. However this control emphasizes both business and technological regulation and monitoring which in turn support business requirement and governance and at the same time ensure that ICT risk are properly identified and managed. According to Central Bank ICT Guideline, the Bank ICT policies have been prepared and reviewed on regular basis based on which operating procedures for all ICT functions are carried out, Besides, in other to assure the appropriate usage of resources and information, the Bank IT Audit Policy ensures that the IT systems are properly protected and is free from unauthorized access illegal tempering and malicious actions and all these actions are continuously monitored and supervised by Banks IT auditor.

2.19 General

(a)The expenses, irrespective of capital or revenue nature, accrued/due but not paid have been provided for in the books of the bank.

(b)J/Vherever considered necessary previous year's figures have been rearranged for the purpose of comparison.

(c)Figures appearing in these financial statements have been rounded off to the nearest Taka.

16

Hoda VasiChowdhury & Co

Amount in BDT

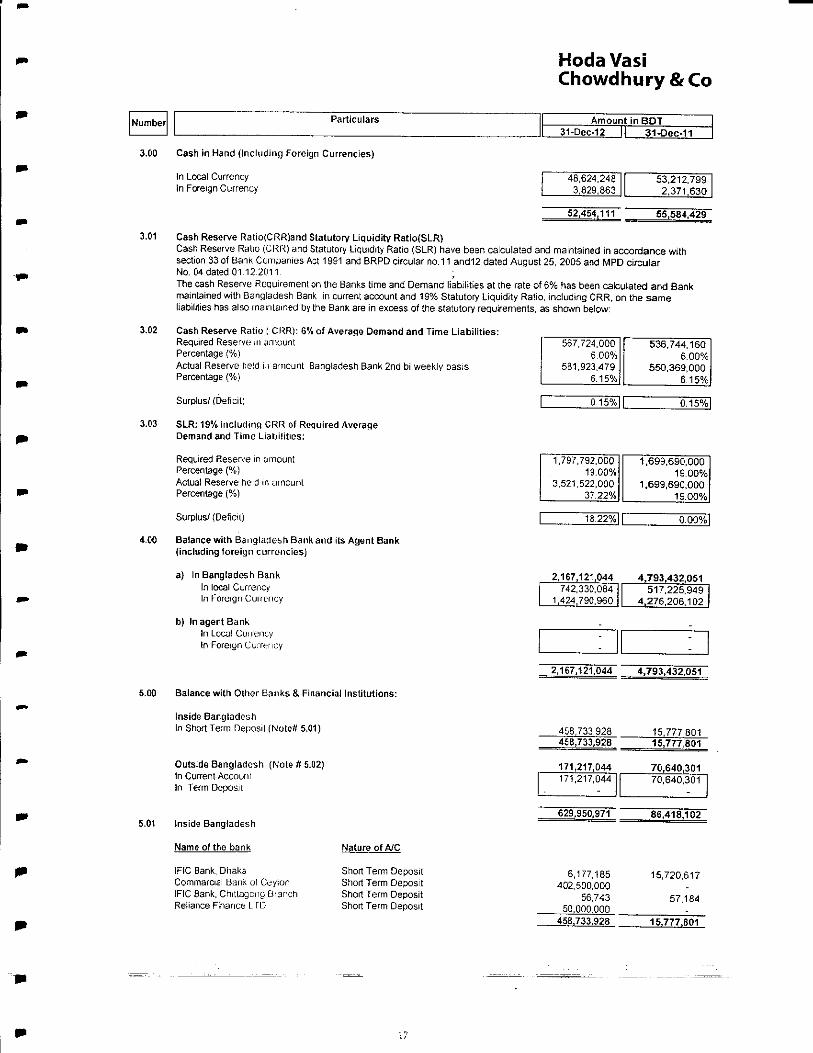

Cash in Hand (Including Foreign Currencies)

In Local CurrencyIn Foreign Currency

48,624.248 I 3.829.863 I

52,454,111

53,212.799 2,371.630

oi5%ir 0.15% I

Cash Reserve Ratio(CRR)and Statutory Liquidity Ratio(SLR)Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) have been calculated and maintained in accordance withsection 33 of Bank Companies Act 1991 and BRPD circular no. 11 and12 dated August 25, 2005 and MPD circularNo. 04 dated 01 12.2011;The cash Reserve Requirement on the Banks time and Oemand liabilities at the rate of 6% has been calculated and Bankmaintained with Bangladesh Bank in current account and 19% Statutory Liquidity Ratio, including CRR, on the sameliabilities has also maintained by the Bank are in excess of the statutory requirements, as shown below:

Cash Reserve Ratio | CRR): 6% of Average Demand and Time Liabilities:Required Reserve in amountI 567,724,000 11 536,744,161Percentage (%)5.00% 6.00'Actual Reserve held in amount Bangladesh Bank 2nd bi weekly basis531,923,479 550,369,001Percentage (%)|6,15%j| 6.15'

Surplus/ (Deficit;|0.15%| |Q.15'

SLR: 1S% includinct CRR of Required AverageDemand and Time Liabilities:

Required Reserve in amount 1,797,792,0001,699,690,001Percentage (%) 19.00%ig!u0(Actual Reserve held in amount 3,521,522,0001,699,690,00(Percentage (%)j 37.22%11ig|oo<;

Surplus/ (Deficit)|18.22%| |Q.QQ1-

Balance with Bangladesh Bank and its Agent Bank(including foreign currencies)

a)In Bangladesh Bank2,167,121,044 4,793.432.051 In local Currency742,330,084 j I 517.225,94J In Foreign Currency| 1,424790,960 j | 4,276,206,10;

b)In agent Bank. In Local Cunency I I II~

In Foreign Currency j|

18.22% | P Q.00%1

2,167,121,0444.793,432,051 742733008411 517.225,949 I

1,424790,960 II 4,276,206,102 1

5.00 Balance with Other Banks & Financial Institutions:

Inside BangladeshIn Short Term Deposit (Note# 5.01)

Outside Bangladesh (Note ft 5.02)In Current AccountIn Term Deposit

Inside Bangladesh

Name of the bank

IRC Bank, DhakaCommardal Ban* of CeylonIFIC Sank, Chitlagong BranchReliance Finance L TD

Short Term DepositShort Term DepositShort Term DeposiiShort Term Deposit

6,177,185402,500,000

56.743 50,000,000

15,720,617

57,184

15,777.B01~

567,724,0006,00%

581,923,4796.15%

536,744,1606.00%

550.369,000615%

1,797,792,000II19.00%

3.521,522,000

1,699,690,00019.00%

1.699,690,00019.00%

458,733,928458,733,928

171,217,044171,217,044II

629,950,971

15.777,80115,777,801

70,640,30170,640,301

86,418,102

Hoda VasiChowdhury & Co

Amount in BPT

5.02 Outside Bangladesh

Name of the Bank Name of the Branches

80,219182,013

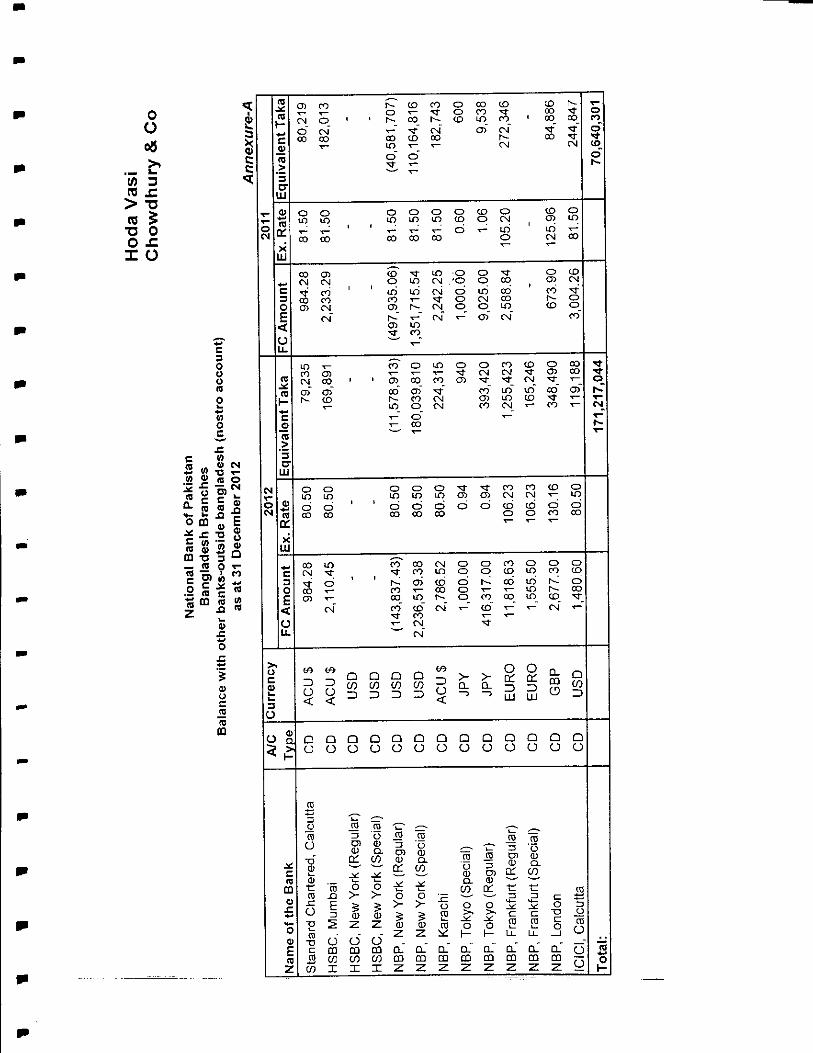

Annexure -A may kindly be seen for details of currency-wise amount and exchange rate.

Maturity Groupinq of Balance withOther Banks and Financial Institutions

Repayable on DemandWith a residual maturity of:Not more than 3 MonthsOver 3 months but not more than 1 YearOver 1year but not moie than 3 YearsMore than 3 years

5.04 Segregation of Balance with other Banks and Financial institutions 6.00Money at call & Short Notice

6.01Classification of money at call & short notice Commercial banks (Noic; # 6.01.0") Financial Institutions (Public & Private)

6.01.01 Commercial Barks a)Leading on Cull

b)Placement on Perm basis

Maturity Grouping ol Money at call & short noticeRepayable on denandWith a residua] maturity of:Upto 1 monthMore than 1 month bul less than 3 monthsMore than 3 month but less than 1 yearMore than 1 month but less :han 2 years

investment in Shares & Securitiesi. Government Secuniies (Note 7.01J

a)Held for Trade b)Held for Matuiity

ii. Bondsin. Sharesiv. Debenturesv Others Investmentsvi. Goldvii. O:hers (Prise Gone!).

3,165,155,565410,391,402 93,159,147

3,071,996,418410,391,402

397,800500,4003,165,553,365 410,891,802

StandardCharteredHSBC

NBP(OEP)

NBP(Special)NBPNBP(Regular)NBP(Special)NBP{Exchangeposition)NBPNBP

CalcuttaMumbaiNewYorkNewYorkBahrainBahrainNewYorkMewYorkKarachiTokyoTokyoFrankfurtFrankfurt(Special)LondonMumbai

(11,578,913)180,039,810

224,315940

393,4201.255,423

165.246348,490119,188

171,217,044

(40,581.707)110,164.816

182,7439,538

600272.346

84,886244,847

70,640,301

452,500,000

629,950,971 86,418,102

:

-

Hoda VasiChowdhury &Co

31-DeiAmount in I

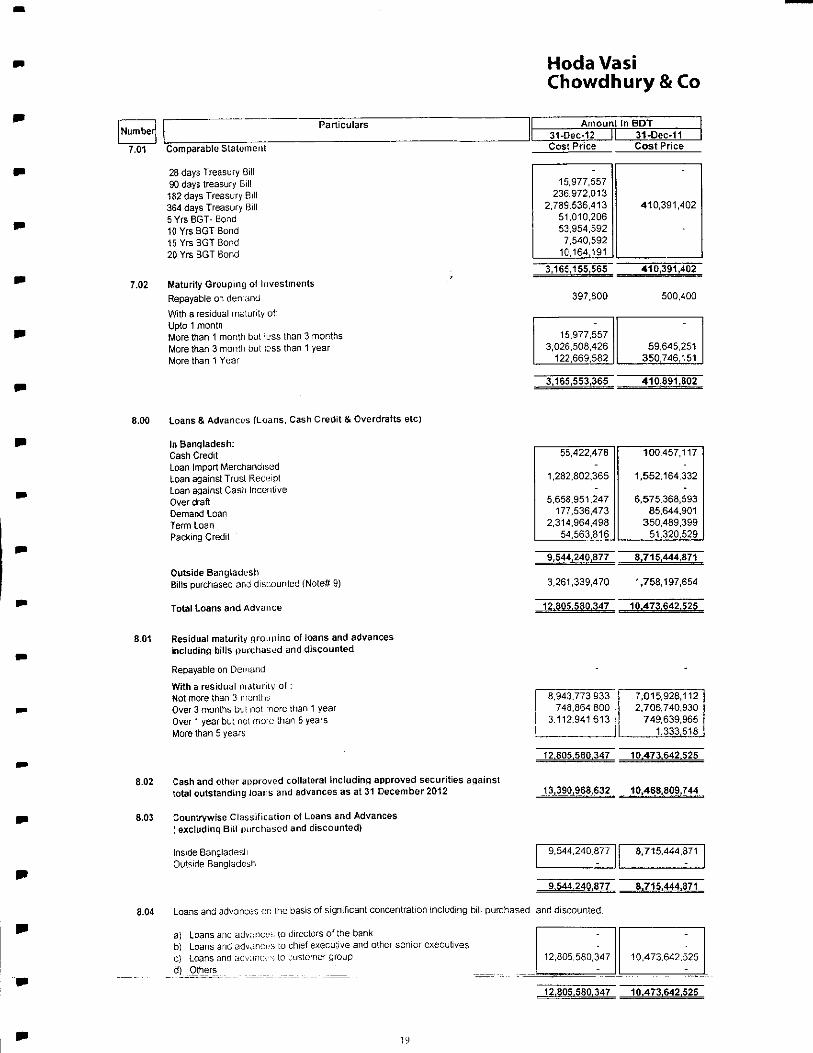

Comparable Statement

28 days Treasury Bill 90 days treasury Bill182 days Treasury Bill364 days Treasury Bill5 Yrs BGT- Bond10 Yrs BGT Bond15 Yrs BGT Bond20 Yrs BGT Bond

Maturity Grouping of InvestmentsRepayable on demandWith a residual maturity olUpto 1 monthMore than 1 month but less than 3 monthsMore than 3 month but less than 1 yearMore than 1 Year

8.00 Loans & Advances (Luans, Cash Credit & Overdrafts etc)

397,800

15,977.5573,026.508,426

122,669,582 59,645,251

350,746,151

In Bangladesh:Cash CreditLoan Import MerchandisedLoan against Trusl ReceiptLoan against Cash IncentiveOver draftDemand LoanTerm LoanPacking Credit

Outside BangladeshBills purchased and discounted (Notefl 9)

Total Loans and Advance

3,261,339,470 1,758,197,654

12.805.580,347 10.473.642.525

Residual maturity grouping of loans and advanceincluding bills purchased and discounted

Repayable on DemandWith a residual maturity of:Not more than 3 monthsOver 3 months but not nore than 1 yearOver 1 year bul not moru than 5 yearsMore than 5 years

Cash and other approved collateral including approved securities atotal outstanding loans and advances as at 31 December 2012

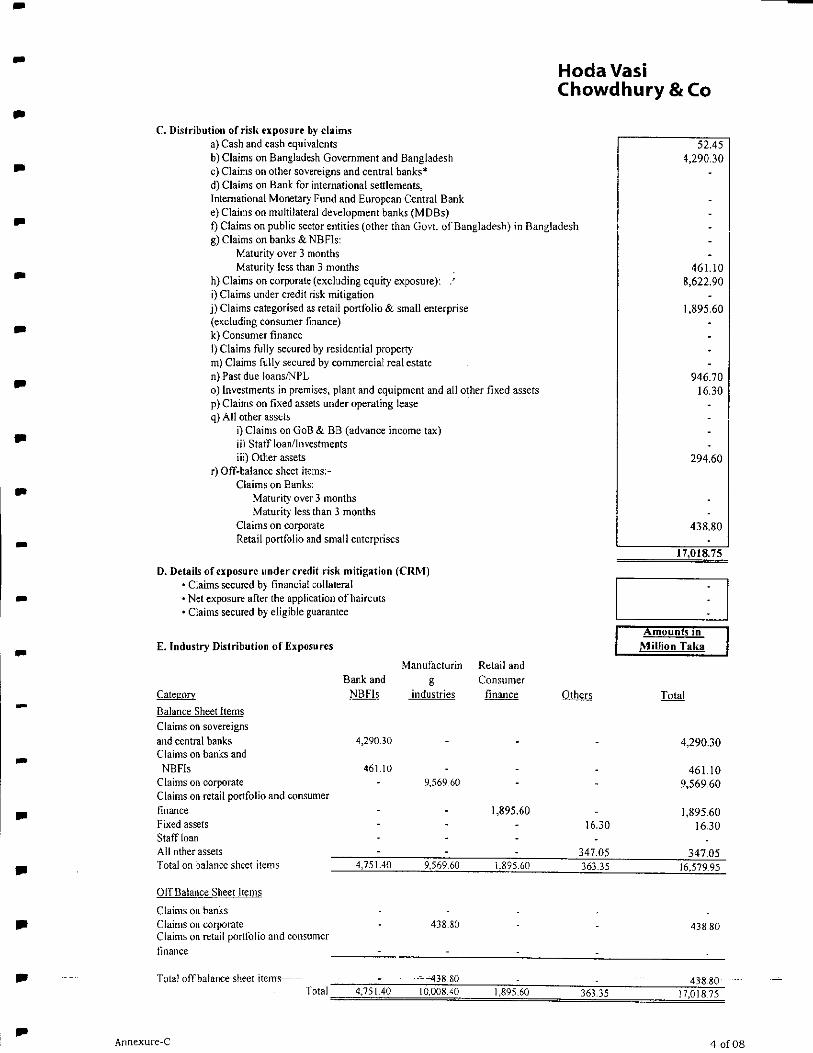

8.03 Countrywise Classification of Loans and Advances [ excluding Bill purchased and discounted)

Inside BangladeshOutside Bangladesh

Loans and advances an the basis of significant concentration including bi

a)Loans and advances to directors of the bankb)Loans and advancub to chief execu;ive and other senior executivesc)Loans and advances to customer group .

d).Others_ _ __

15.977,557236,972,013

2.789,536,41351,010.20653,954,5927,540,592

10,164,191

410,391,402

5,658,951,247177,536,473

2,314.964,49854,563.816

6,575368,59385,644,901

350,489,39951,320,529

3,112,9416131,333,518

Hoda VasiChowdhury &Co

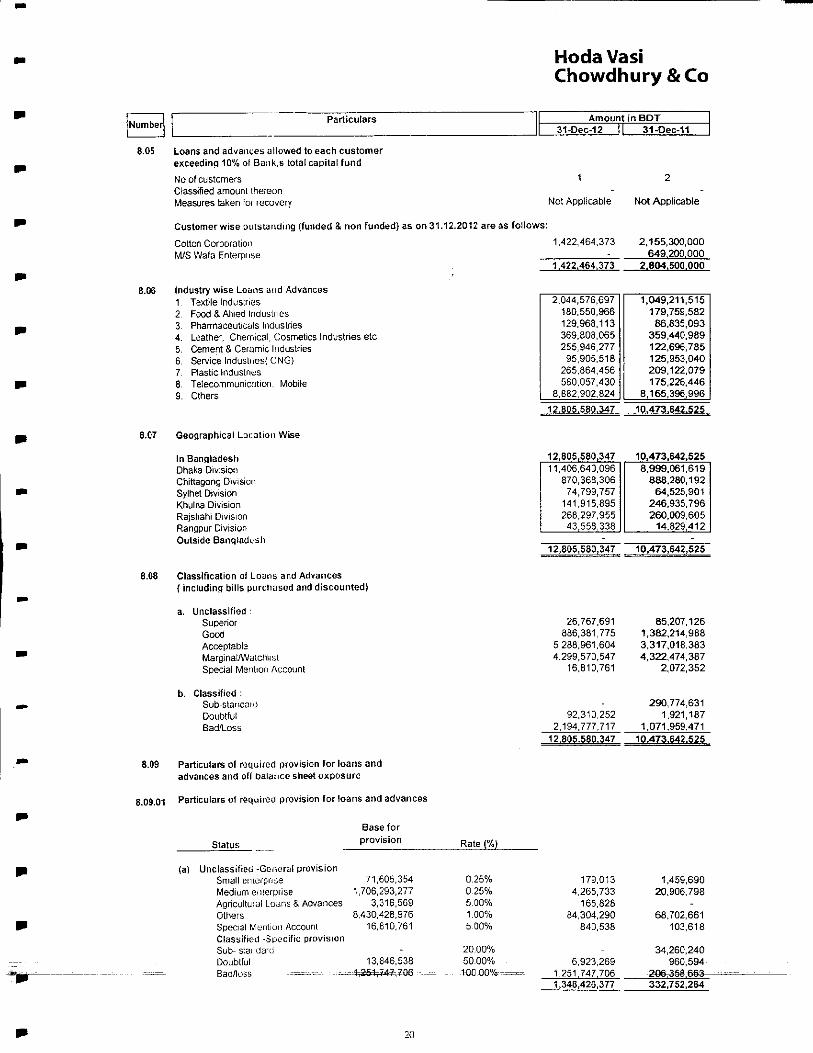

Loans and advances allowed to each customerexceeding 10% ol Bank.s total capita! fund

No of customersClassified amount thereonMeasures taken for recoveryH

Customer wise outstanding (funded & non funded) as on 31.12.2012 are as follows:

Cotton Corporation

M/S Wafa Enterprise

Industry wise Loans and Advances1Textile Industries2.Food & Allied industries3.Pharmaceuticals Industries4.Leather, Chemical, Cosmetics Industries etc5.Cement & Ceramic Industries6.Service Industries) CNG)7.Plastic Industries8.Telecommunication. Mobile9.Others

12

Not Applicable Not Applicable

2,155,300,000 649,200.000

1.422.464.373 2.8O4.500.000

12.805.580,347 10.473,642.525

8.07 Geographical Location Wise

In Bangladesh Dhaka Division Chittagong Division Sylhet Division Khulna Division Rajshahi Division Rangpur Division Outside Bangladesh

12,805,58D,347 10,473,642,525

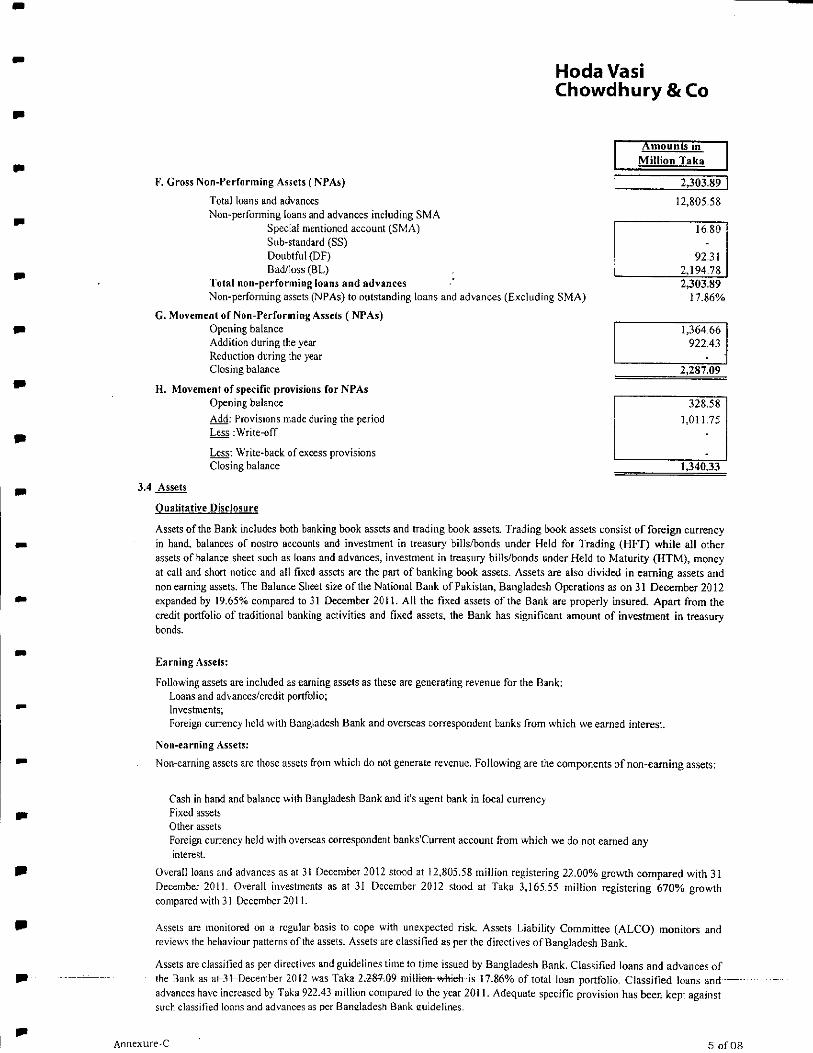

Classification oi Loans and Advances{including bills purchased and discounted)

a.Unclassified : Superior Good Acceptable Marginal/Walctilist Special Mention Account

b.Classified : Sub-stancotd Doubtful Bad/Loss

26,767,691 886,381,775

5,288,961,6044,299,57D.547

16,810.761

92,310,2522.194,777,717

85,207.1261,382,214,9883,317,018,3834,322,474,387

2,072,352

290,774,631 1,921,187

1,071,959,47112.805.580.347 10.473.642.525

8.09 Particulars of required provision for loans and advances and oil balance sheet exposure

8.09.01 Particulars of required provision for loans and advances

Particulars AmountinBDT31-Dec-12II31-Dec-11

2,044,576,697180.550,966129.968,113369,808.065265,946,27795,905,518

265,864,456580,057,430

8,882,902,824

1.049,211,515179,759,582

86,835,093359,440,989122,696,785125,953,040209,122,079175.226.446

8,165,396,996

12,805,580,34711,406,643,096

870,368,30674,799,757

141,915.895268,297,95543,558,338

10,473,642,5258,999.061,619

888,280,19264,525,901

246,935,796260,009.605

14,829.412

Status

(3)Unclassified-GeneralprovisionSmallenterpriseMediumenterptiseAgriculturalLoans&AdvancesOthersSpecislMentionAccounIClassified-SpecificprovisionSub-standardDoubtfulBad/loss--=^--.--v-@-_

Baseforprovision

71,605,3541,706,293,277

3,316,5696,430.428,976

16,610,761

13,846,538

Rate(%l

0,25%025%5,00%1.00%500%

20.00%50.00%

-10000%----=--

179.0134,265,733

165,82884,304.290

84D.538

6,923,269

1,348,420,377

1,459,69020,906,798

68,702,661103,618

34,260,240960,594

332,752,264

Hoda VasiChowdhury & Co

Amount in BDT

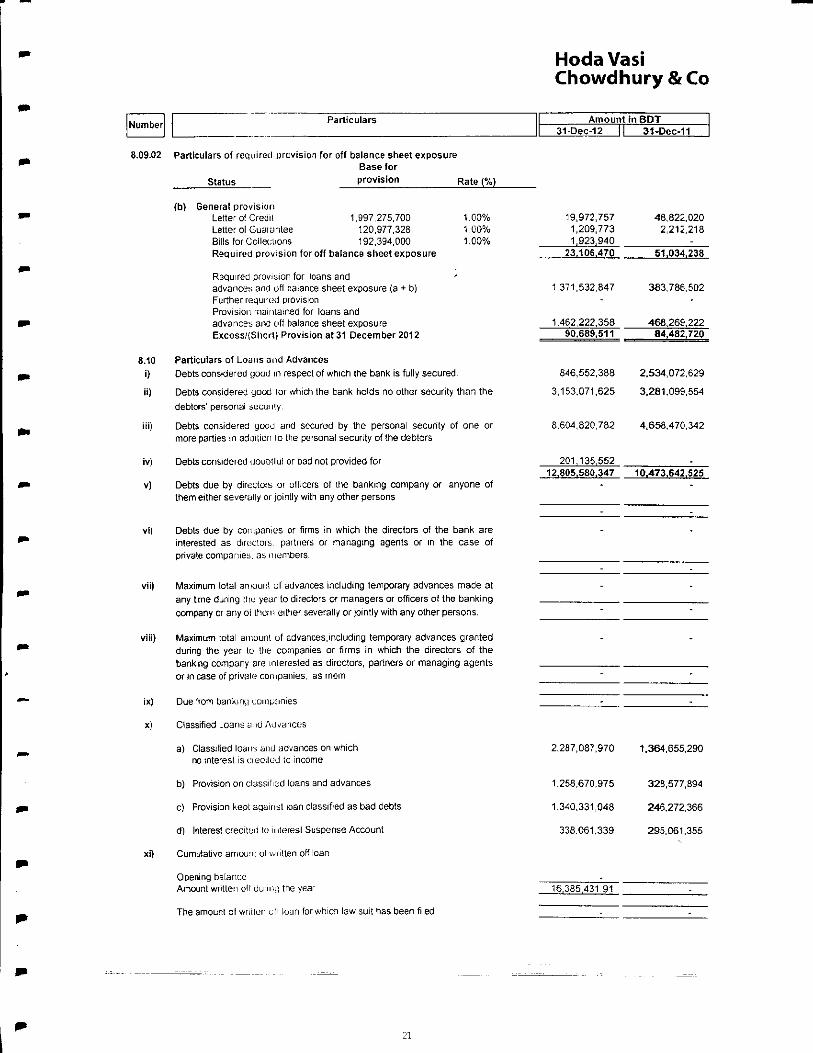

Particulars of required provision for off balance sheet exposure Base for

StatusprovisionRate (%)

(b) Genera! provision Letter of Credil1,997,275,700 Letter olGuaiuntee120,977,328 Bills for Collections192,394,000 Required provision for off balance sheet exposure

Required provision for loans and advances and off balance sheet exposure (a + b) Further requred provision Provision maintained for loans and advances and oft balance sheet exposure Excess/(Shorlj Provision at 31 December 2012

8.10 Particulars of Loans and Advances i) Debts considered good in respect of which the bank is fully secured.

ii) Debts considered good tor which the bank holds no other security than the debtors' personal secunly.

iti) Debts considered good and secured by the personal security of one or more parties in adoilioi i lo the personal security of the debtors

iv) Debts considered uouotlul or bad not provided for

v) Debts due by directors or officers of [he banking company or anyone of them either severally or jointly with any other persons

vi| Debts due by companies or firms in which the directors of the bank are interested as directors partners or managing agents or in the case of private companies, as members.

vii) Maximum total amount of advances including temporary advances made at any tme during the year to directors or managers or officers of the banking company or any oi them either severall/ or jointly with any other persons.

viii) Maximum total amount of advancesjncluding temporary advances granted during the year lo the companies or firms in which the directors of the banking company are interested as directors, partners or managing agents or in case of private companies, as mem

ix) Due from banking companies

x) Classified Loans yno Auvances

a} Classified loans and advances on which no interest is ci edited tc income

b)Provision on classified loans and advances

c)Provision kepi against loan classified as bad debts

d)Interest credited to n iteresl Suspense Account

xi) Cumulative amount of wiillen off loan

Opening balance Amount written off during the year

2,267,087,9701,364,655,290

1,258,670,975328,577,894

1,340,331,048246,272,366

338,061,339295.061.355

The amount of wntien n for which law suit has been filed

1.00%1.00%1.00%

19,972,7571,209,7731,923,940

48,822,0202,212,218

23.106.470

1,371.532,847

1,462,222,35890,689,511

846,562,388

3.153,071,625

8,604,820,782

201,135,55212,805,580,347

51.034.238

383,786,502

466,269,22284,482,720

2.534,072,629

3.261,099,554

4,658,470,342

10.473.642.525

HodaVasiChowdhury & Co

31-Dec-12Amount in BDT

31-Dec-11

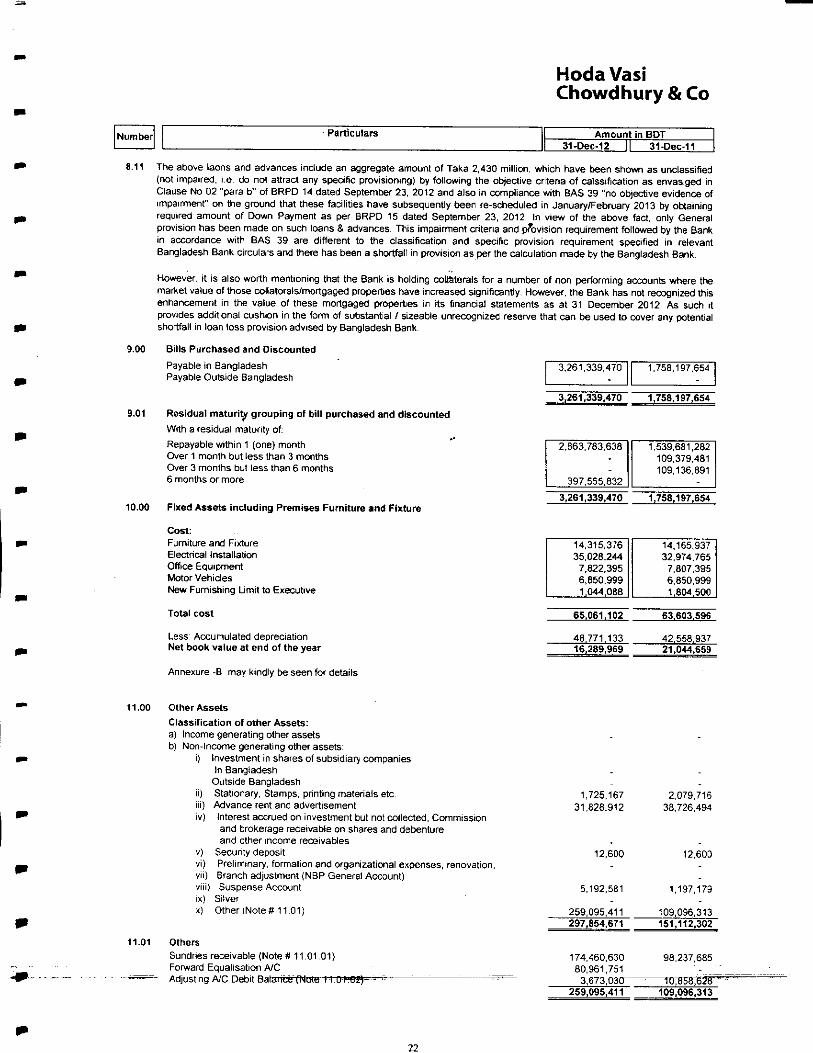

The above laons and advances include an aggregate amount of Taka 2,430 million, which have been shown as unclassified(not impaired, i.e. do nol attract any specific provisioning) by following the objective criteria of calssification as envasiged inClause No 02 "para b" of BRPD 14 dated September 23, 2012 and also in compliance with BAS 39 "no objective evidence ofimpairment" on the ground that these facilities have subsequently been re-scheduled in January/February 2013 by obtainingrequired amount of Down Payment as per BRPD 15 dated September 23, 2012. In view of the above fact, only Generalprovision has been made on such loans & advances. This impairment criteria and provision requirement followed by the Bankin accordance with BAS 39 are different to the classification and specific provision requirement specified in relevantBangladesh Bank circulars and there has been a shortfall in provision as per the calculation made by the Bangladesh Bank.

However, it is also worth mentioning that the Bank is holding collaterals for a number of non performing accounts where themarket value of those collatorals/mortgaged properties have increased significantly. However, the Bank has not recognized thisenhancement in the value of these mortgaged properties in its financial statements as at 31 December 2012. As such itprovides additional cushion in the form of substantial / sizeable unrecognized reserve that can be used to cover any potentialshortfall in loan loss provision advised by Bangladesh Bank.

Bills Purchased and DiscountedPayable in BangladeshPayable Outside Bangladesh

9.01 Residual maturity grouping of bill purchased and discounted With a residual maturity of: Repayable within 1 (one) month Over 1 month but less than 3 months Over 3 months but less than 6 months 6 months or more

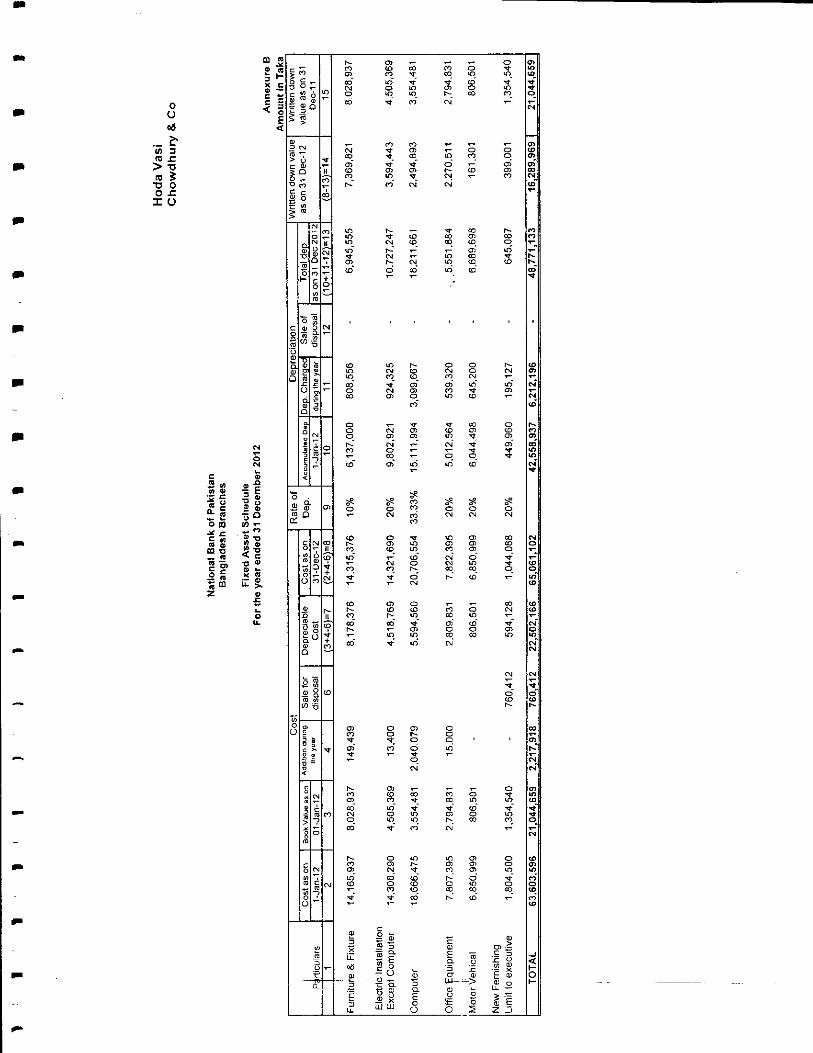

10.00 Fixed Assets including Premises Furniture and Fixture

Cost: Furniture and Fixture Electrical Installation Office Equipment Motor Vehicles New Furnishing Limit to Executive

Total cost

Less: Accumulated depreciation Net book value at end of the year

Annexure -B may kindly be seen for details

3,261.339,470 | 1.758,197,654 |

3,261,339,4701,758,197,654

Other AssetsClassification of other Assets:a)Income generating other assetsb)Non-Income generating other assets:

i) Investment in shares ol subsidiary companies In Bangladesh

Outside Bangladesh ii) Stationary, Stamps, printing materials etc. iii) Advance rent and advertisement iv) Interest accrued on investment but not collected, Commission

and brokerage receivable on shares and debenture and other income receivables

v) Security deposit vi) Preliminary, formation and organizational expenses, renovation, vii) Branch adjustment (NBP General Account) viii) Suspense Account ix) Silver x) Other(Note# 11.01)

OthersSundries receivable (Note # 11.01-01)Forward Equalisation A/C_Adjusting A/C Debit Batarice:(Note~'iHOl".OS) '^^ @=

1,725,1672,079,71631,828.91238,726,494

5.192,581

259,095,411

174,460,630 80.961,751

3,673,030"

1.197,179

109,096,313

2,863,783,638

397,555,832

1539.681,282109,379,481109,136,891

14.315,37635,028.244

7,822,3956,650,9991.044,088

14.165,93732,974,765

7,807,3956,650.9991,604.500

65.061.102

48.771.13316,289.969

63.603.596

42.558.93721,044,659

Hoda VasiChowdhury & Co

Particulars Amount in BDT

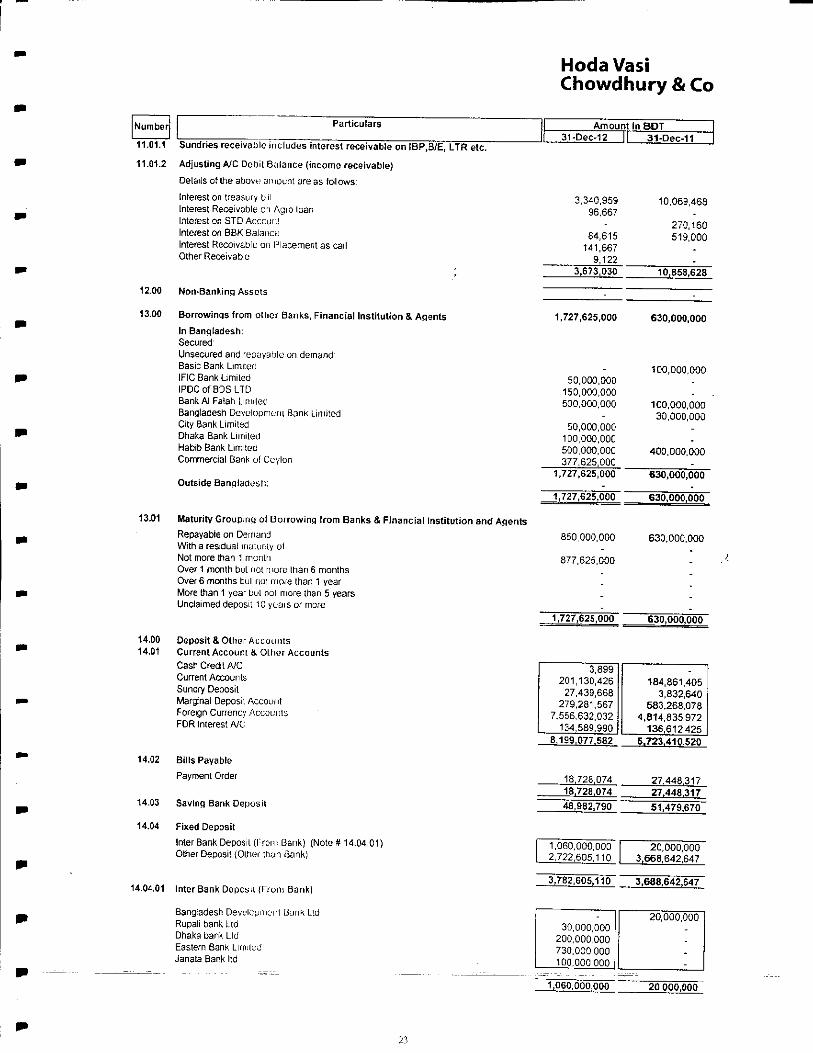

11.01.1Sundries receivable includes interest receivable on IBP,3/E, LTR etc.

11.01.2Adjusting A/C Debit Balance (income receivable)

Details of the above.1 amount are as follows Interest on treasury bll Interest Receivable ci Agio loan Interest on STD Account Interest on BBK Balance Interest Receivable! on Placement as call Other Receivabe

12.00 Non-Banking Assets

13.00 Borrowings from other Banks, Financial Institution & Agents

In Bangladesh: Secured Unsecured and repayable on demand: Basic Bank Limited IFIC Bank Limited IPDCofBOSLTD BankAl Faiah Limited Bangladesh Development Bank Limited City Bank Limited Dhaka Bank Limited Habib Bank Limited Commercial Bank ol Ceylon

Outside Bangladesh:

Maturity Grouping of Borrowinq from Banks & Financial Institution and AgentsRepayable on DemandWith a residual maturity ofNot more than 1 monlhOver 1 month bul not more lhan 6 monthsOver6 months bul no: more than 1 yearMore than 1 year bul not more than 5 yearsUnclaimed deposit 10 yeais or more

14.04 Fixed Deposit Inter Bank Deposit (lLroru Bank) (Note # 14.04.01) Other Deposit (Other than Bank)

14.04.01 Inter Bank Deposit (From Bank)

Bangiadesh Devulcymonl Bunk Lid Rupati bank Ltd Dhaka bank Lid Eastern Bank Limiluci Janata Bank ltd

1.060,000,0002,722,605.110

20,000,0003.668.642,547

3,782,605.1103,688.642,647

1,060,000.000

14.0014.01

14.02

14.03

Deposit&OtherAccountsCurrentAccount&OtherAccountsCashCreditA/CCurrentAccountsSundryDepositMarginalDepositAccountForeignCurrencyAccountFDRInterestA/C

BillsPayablePaymentOrder

SavingBankDeposit

3.340,95996,667

84,615141,667

9,1223,673,030

1,727,625,000

50,000,000150,000,000600,000,000

50,000,000100,000,000500,000,000377,625,000

1,727,625,000

1,727,625,000

10,069,468

270,160519,000

10,858,628

630,000,000

100,000,000

100,000.00030,000,000

400.000,000

630,000,000

630,000,000

3,899201,130,426

27,439,668279,281,567

7,556,632,032134,589,990

184,861,4053,832,640

583,268,0784,814.835972

136,612,4258.199.077,582

18,728,07418,728,07448,982,790

5.723.410,520

27,448,31727,448,31751,479,670

30,000,000200,000,000730,000,000100,000,000

20,000,000

Hoda VasiChowdhury & Co

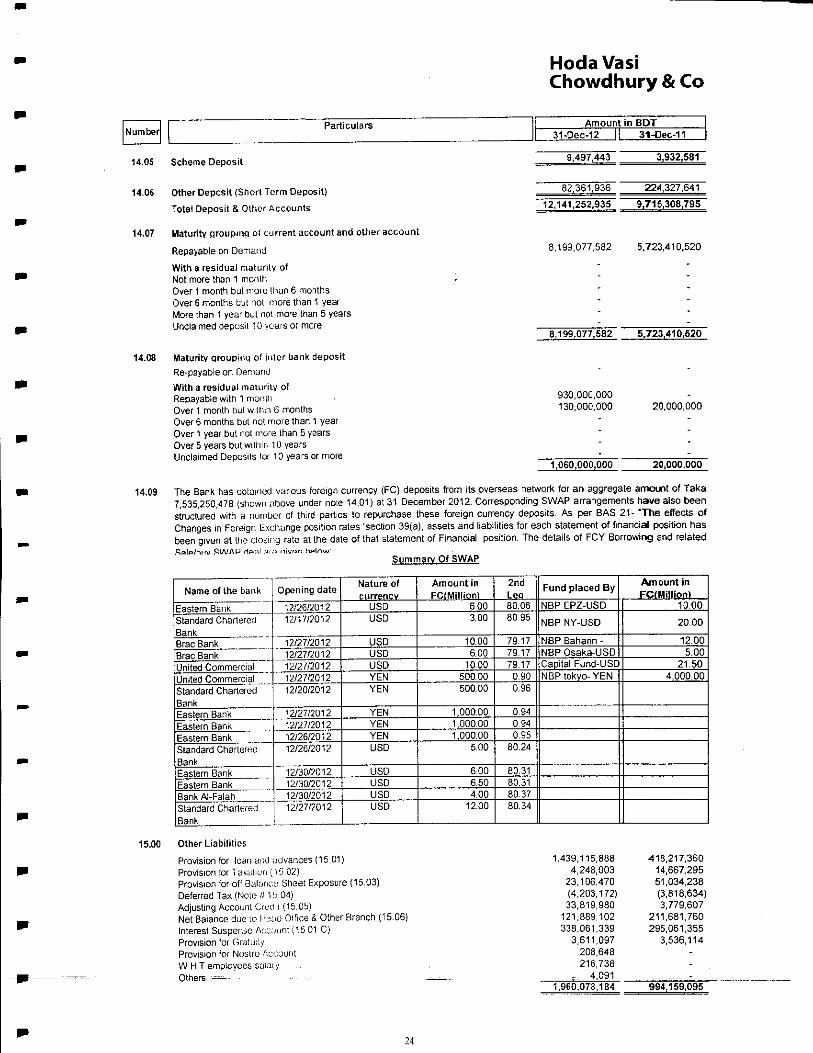

14.05Scheme Deposit

14.06Other Deposit (Short Term Deposit)

Total Deposit & Older Accounts

14.07Maturity grouping oi current account and other account

Repayable on Demand

With a residual maturity of Not more than 1 month Over 1 month but more than 6 months Over 6 months but not more than 1 year More than 1 year but not more than 5 years Unclaimed deposit 10 vears or mere

14.08Maturity grouping cl inter bank deposit Re-payable on Demand With a residual maturity of Repayable with 1 monih Over 1 month but within 6 months Over 6 months but not more than l year Over 1 year but not more than 5 years Over 5 years but within 10 years Unclaimed Deposits for 10 years or more

Amount in BDT31-Oec-12 II 31-0ec-11

8,199,077.582 5.723,410.520

8,199,077,5825.723,410,520

930,000,000130,000,00020,000,000

1,060,000,00020,000,000

The Bank has obtained various foreign currency (FC) deposits from its overseas network for an aggregate amount of Taka7.535,250,478 (shown isbove under note 14.01) at 31 December 2012. Corresponding SWAP arrangements have also beenstructured with a number of third parties to repurchase these foreign currency deposits. As per BAS 21- "The effects ofChanges in Foreign lExchunge position rates 'section 39(a), assets and liabilities for each statement of financial position hasbeen given at the closing rate at the date of that statement of Financial position. The details of FCY Borrowing and relatedBal(*/Kitu SWAP HPt,l aii> niuran halnw

Summary Of SWAP

15.00 Other Liabilities Provision for loan and advances (15.01) Provision for Taxain." i (15 02} Provision for off Balance Sheet Exposure (15.03) Deferred Tax (Note it 1 :i 04) Adjusting Account Croon (15.05) Net Balance due to lk:ad Olfice & Other Branch (15.06) interest Suspense Accjunt (15 01 C) Provision 'or Gratu:ly Provision 'or Noslro Account W H.T employees saiai y

Others ~@@@.@--_

1,439,115,888 4,248,003

23,106,470 (4,203,172) 33,819,980

121,889,102 338,061,339

3,611,097 208,648 216,738

- 4.091

413,217,360 14,667,295 51,034,238 (3.818,634) 3,779,607

211,681,760295,061,355

3,536,114

1,960,073,184

9,497,443

82,361,93612,141,252,935

3,932,581

224,327,6419,715,308,795

Nameofthebank

EasternBankStandardChartered

3racBankBraeBankJnitedCommercialJnitedCommercialStandardCharteredBankEasternBank"asternBankEasternBankStandardCharleredBankEasternBankEasternBankBankAl-FalahStandardCharleredBank

Openingdate

12/26/201212/17/2012

12/27/201212/27/201212/27/201212/27/201212/20/2012

12/27/201212/27/201212/26/201212/26/2012

12/30/201212/30/201212/30/201212/27/2012

Natureof

USDUSD

USDUSDUSDYENYEN

YENYENYENUSD

USDUSDUSDUSD

AmountinFCIMillionl

6003.00

10.006.00

10.00500.00600.00

1,000.001.000001,000.00

5.00

6006.504.00

12.00

2ndLeo80.068095

79.1779.1779.17

0.900.96

0940940.95

80.24

803180.3180.3780.34

FundplacedBy

NBPEPZ-USD

NBPNY-USD

NBPBaharin-NBPOsaka-USDCapitalFund-USDNBPtokvo-YEN

AmountinFCIMillionl

10.00

20.00

12.005.00

21.504.000.00

Hoda VasiChowdhury & Co

Amount in BDTHE

1,011.753,154

89,639,466 9,145.374

74,435,22815.204,236

98,784.8401,340.331,048

89,639,466328,577,894

295,061,355 42,999,984

234,501,850 60,559,505

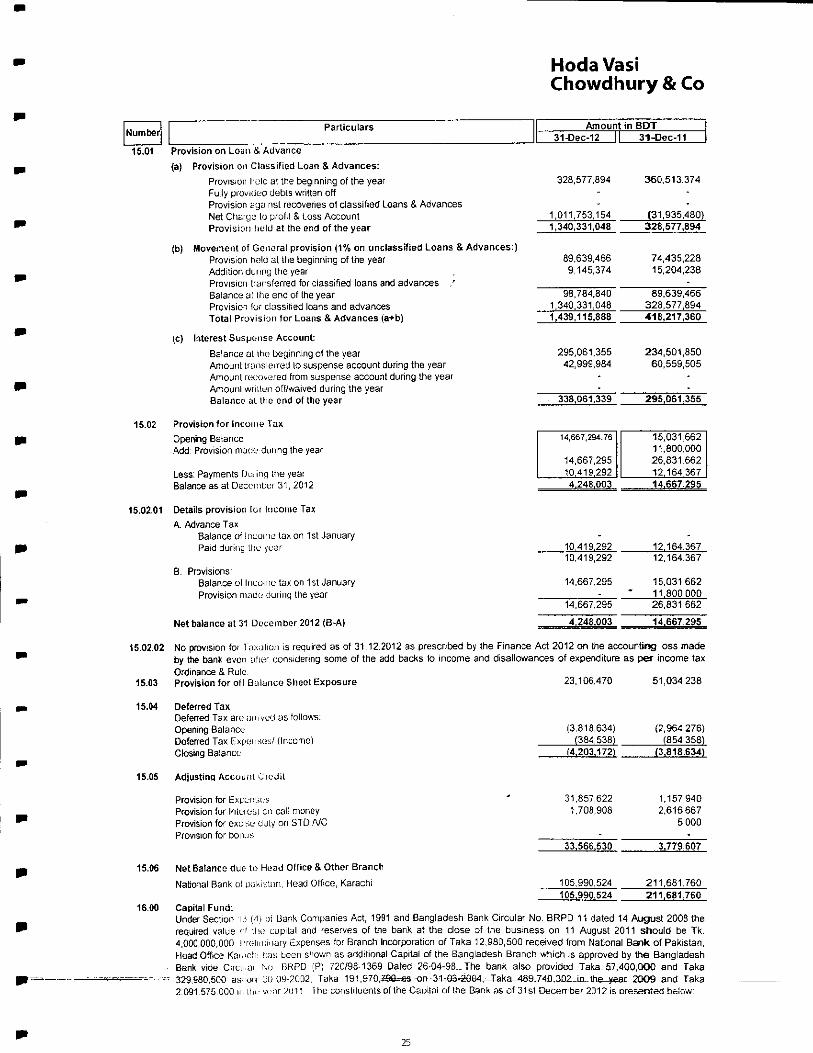

15.01Provision on Loan & Advance (a)Provision on Classified Loan & Advances:

Provision hole at the beginning of the year328,577,894 360,513,374 Fully provided debts written off Provision uyansl recoveries of classified Loans & Advances Net Chaiyi; to profit & Loss Account1,011.753,154(31,935,480> Provision Held at the end of the year1,340,331,048 328,577,894

(b)Movement of General provision (1% on unclassified Loans & Advances:) Provision held at the beginning of the year89,639,466 74,435,228 Addition during the year ,9,145.374 15.204,238 Provision transferred for classified loans and advances ,'- Balance at the end of the year98,784,840 89.639,466 Provision lur classified loans and advances1,340.331,048 328,577,894 Total Provision for Loans & Advances (a+b)1,439,115,888 418,217,360

(c)Interest Suspense Account: Balance at the beginning of the year295,061,355 234,501,850 Amount transierred lo suspense account during the /ear42,999,984 60,559,505 Amount recurred from suspense account during the year Amounl wnUun off/waived during the year-@ Balance at the end of the year338,061,339 295,061,355

15.02Provision for income Tax Opening BalanceI 14,667,294.76 [I 15,031,662 Add: Provision made during the year11,800,000

14,667,29526,831,662 Less: Payments Dm ing Ihe yearI 10,419,292 11 12,164,367 Balance as at December 31, 20124.248,003 14,667,295

15.02.01Details provision Fur Income Tax A.Advance Tax

Balance of inconu tax on 1st January Paid during thu year10,419.29212.164,367

10,419.29212,164,367 B.Provisions:

Balance ol income tax on 1st January14,667,295 15.031,662 Provision made during the year-" 11 800 000

14,667,29526,831,662

Net balance at 31 December 2012 (B-A)A.2.4.8-00314,667,295

15.02.02No provision foi Taxalion is required as of 31.12.2012 as prescribed by the Finance Act 2012 on the accounting loss made by the bank even after considering some of the add backs lo income and disallowances of expenditure as per income tax Ordinance & Rule

15.03Provision lor oil Balance Sheet Exposure23,106,470 51,034,238

15.04Deferred Tax Deferred Tax areunived as follows: Opening Balance13,818,634) (2,964,276) Deferred Tax Expenses/ (Income)(384,538) (854,358) Closing Balancef4.203.172) (3.818,634)

15.05Adjusting Account Credit

Provision for Expenses '31,857,622 1,157,940 Provision for Intae:,! on call money1,708,908 2,616,667 Provision for excise duly on STD A/C5,000 Provision for bonus-.

33.566.5303.779,607

15.06Net Balance due to Head Office & Other Branch National Bank of pakistnn, Head Office, Karachi105,990,524211.681,760_

) Capital Fund: Under Section i< Mi requited value '_if Hit 4,000,000,000. I'roln Head Office Kai.'c!,! Bank vide CircLi.ai

2.091 575 000 u: Iht-

oi liank Companies Act, 1991 and Bangladesh Bank Circular No. BRPD 11 dated 14 August 2008 the capital and reserves of the bank at the close of the business on 11 August 2011 should be Tk.

unary Expenses for Branch Incorporation of Taka 12,980,500 received from National Bank of Pakistan, us been shown as additional Capital of the Bangladesh Branch which is approved by the Bangladesh

so I3RPD (P) 720/93-1369 Dated 26-04-98._ The bank also provided Taka, 57,400,000 and Taka3O-O9-2O02. Taka 191.97P.79Q-as -on -31-O3-PQ04, Taka 4&9 ,-740,-302 in the year 20O9 and Takany.trArt-\ Ihe constituents of the Capital of the Bank as of 31st Decerrber 2312 is oresented bfcicw:

14,667,294.76

14,667,29510,419.292

15,031,66211,800,00026,831,66212.164,367

10,419.29210,419.292

14,667,295

14,667,295

4.248.003

12.164,367

15.031,66211.800,00026,831,662

14.667.295

13,818,634)(384,538)

(4.203.172)

31,857,6221,708,908

33.566.530

105,990,524105.990,524

(2,964,276)(854,358)

(3.818.6341

1,157,9402,616,667

5,000

3.779.607

211.681,760211.681.760

Hoda VasiChowdhury & Co

Amount in BDT

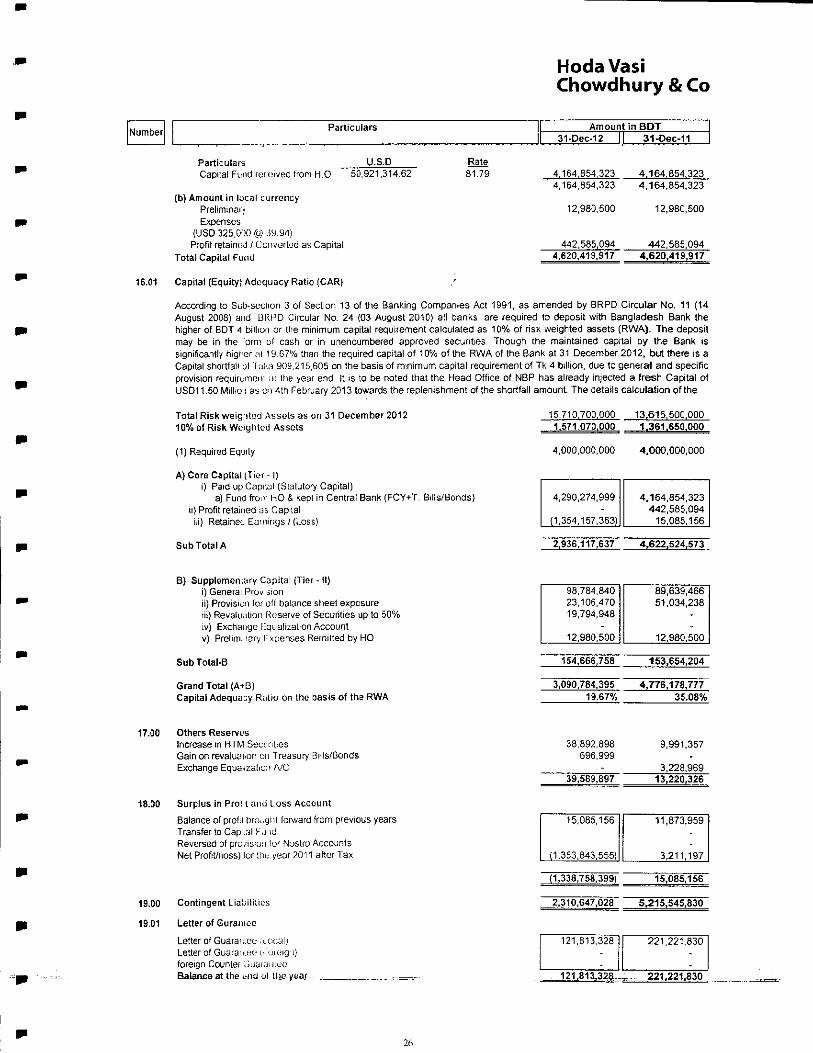

ParticularsU.S.DCapital Fund received from HO 50,921,314

(b) Amount in local currency Preliminaiy Expenses

(USD 325,000 fti? 39.94) Profit retained / Ccnverted as Capital

Total Capital Fund

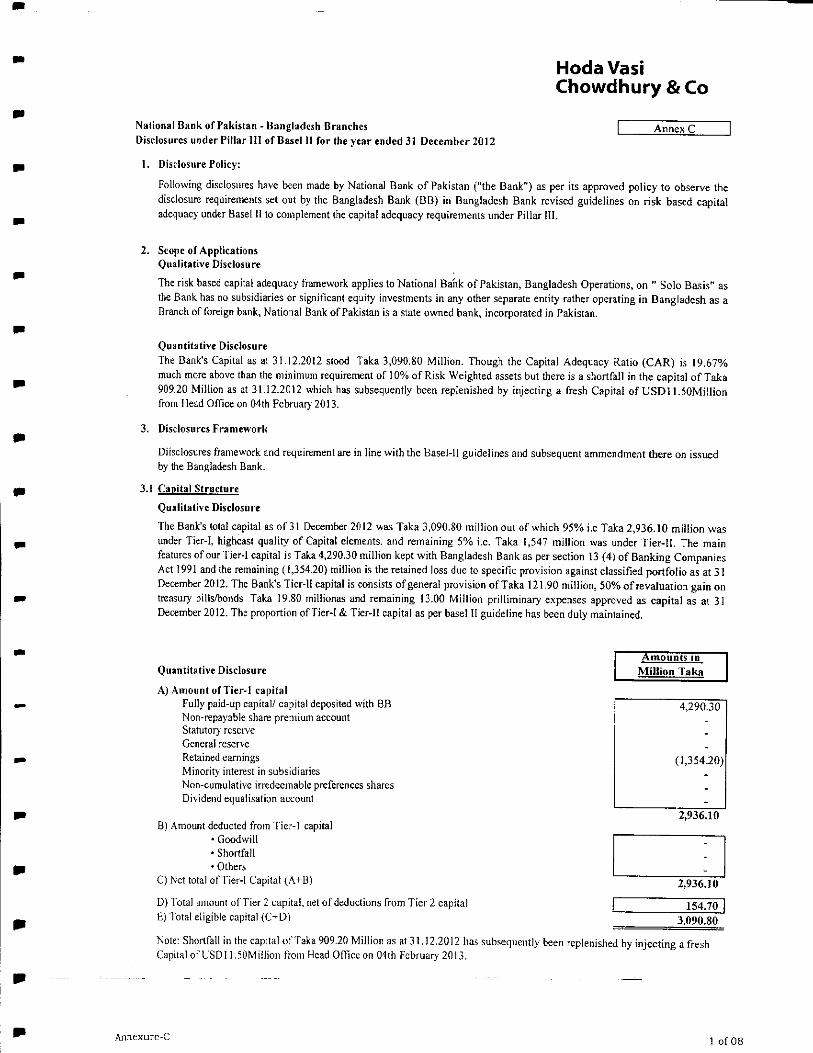

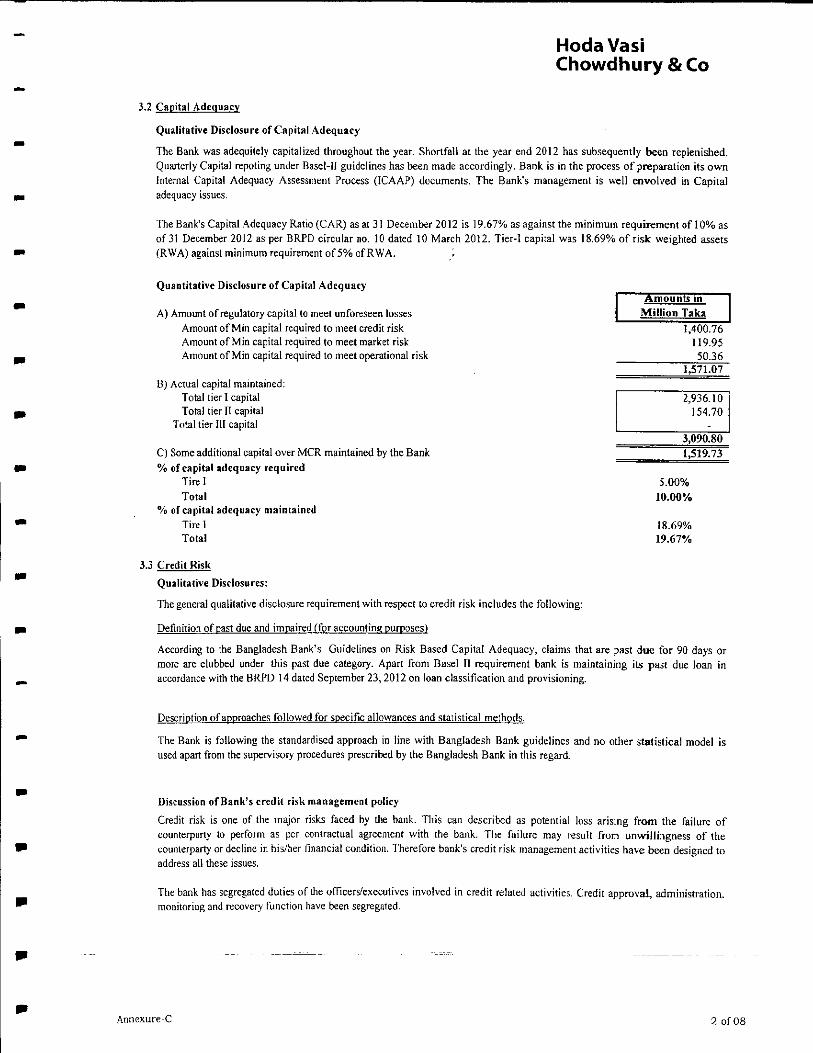

16.01 Capital (Equity} Actocjuacy Ratio (CAR)

4,164,854,3234.164,654,3234,164,854,3234.164.854,323

12,980,50012,980,500

442.585,094442,585,0944,620,419,9174,620,419,917

According to Sub-seciion 3 of Section 13 of the Banking Companies Act 1991, as amended by BRPD Circular No. 11 (14August 2008} and BRPD Circular No. 24 (03 August 2010) all banks are required to deposit with Bangladesh Bank thehigher of BDT 1 billion or the minimum capital requirement calculated as 10% of risk weighted assets (RWA). The depositmay be in the torm of cash or in unencumbered approved securities. Though the maintained capital by the Bank issignificantly higfer ;u 19 67% than the required capital of 10% of the RWA of the Bank at 31 December 2012, but there is aCapital shortfall of 'fLii-.a 909,215,605 on the basis of minimum capital requirement of Tk 4 billion, due to general and specificprovision requiruneni ;jt the year end It is to be noted that the Head Office of NBP has already injected a fresh Capita! ofUSD11.50 Million as en 4th February 2013 towards the replenishment of the shortfall amount. The details calculation of the

Total Risk weighted Assets as on 31 December 201210% of Risk Weighted Assets

(1) Required Equity

A) Core Capital (Tier-1) i) Paid up Capital (Statutory Capital)

a) Fund froiv HO & kept in Central Bank (FCY+T. Bills/Bonds) ii) Profit retained Lis Capital

iii) Retainer Earnings/(Loss)

Sub Total A

15,710.700.000 13.615.500.000 1.571.070.000 1.361.650.000

4,000,000,000

2,936,117,6374,622,524,573

B) Supplementary Capital (Tier - II) i) Genera! Provision ii) Provision (or off balance sheet exposure lii) Revaluation Reserve of Securities up to 50% iv) Exchange Equalization Account v) Preliminary Expenses Remitted by HO

Sub Total-B

Grand Total (A+B)Capital Adequacy Ratio on the basis of the RWA

17.00 Others Reserves Increase in HTM Securities Gain on revaluaiion on Treasury Bills/Bonds Exchange Equalization A/C

18.00 Surplus in ProM and Loss Account Balance ol profit brought forward from previous years Transfer to Cap.ial K.jnd Reversed of provision lor Nostro Accounts Net Profit/doss) lor (he year 2011 after Tax

19.00Contingent Liabilities

19.01Letter of Guramoe

Letter of Guarantee- ,icn;alj Letter of GuaraniL-e u orc;ig i) foreign Counlei iJuuKjiuee Balance at the .-nci 1 Utoyaa

38,892,8989,991,357 696.999

:3,228,969

4,290,274,999

(1,354,157.363)

4.164,854,323442,585,094

15.085.156

12.980,500 12.980.500

154,665,758

3,090,784,39519.67%

153,654,204

4,776,178.77735.08%

39,589,897 13.220,326

15,085,156

(1,353,843,555)

11,873,959

3,211.197

(1,338,758,399) 15,085,156

2,310,647,028 5.215,545,830

121,813,328

121.813^328-

221,221.830

Hoda VasiChowdhury & Co

mount in BDT31-Dec-12 II 31-Dec-H

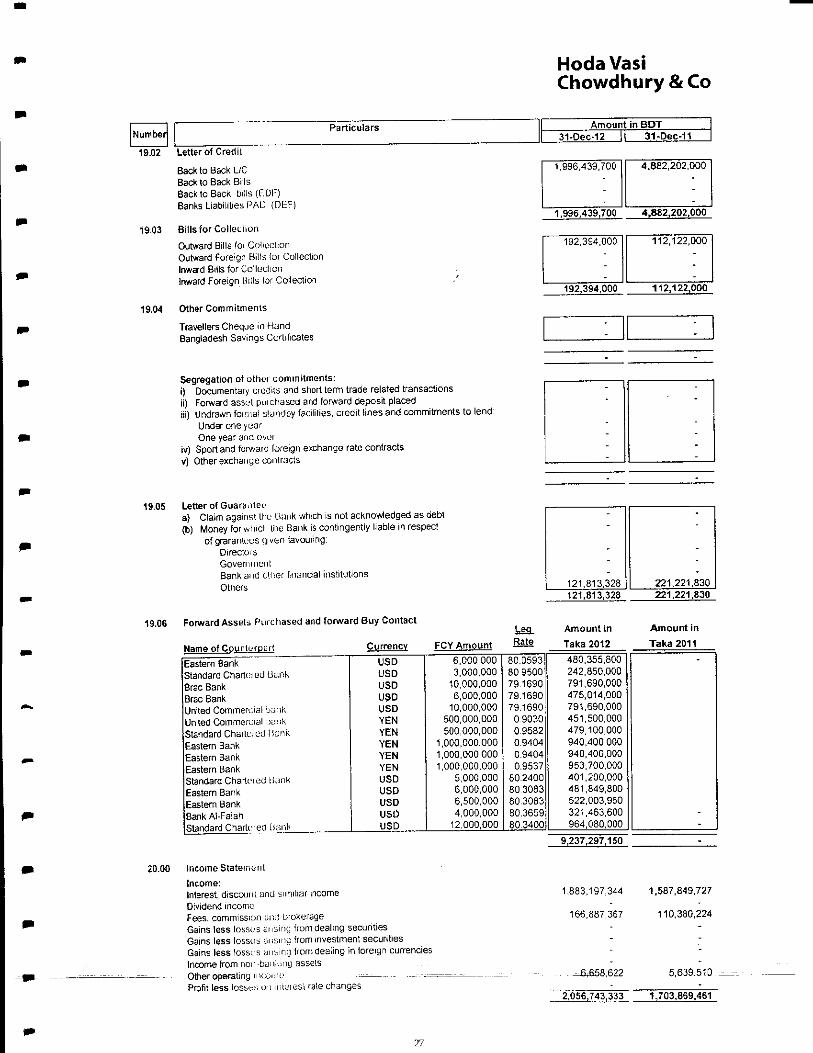

19.02Letter of Credit

Back to Back L/C Back to Back Bills Back to Back bills (F.DF) Banks Liabilities PAD (DEF)

19.03Bills for Collection Outward Bills fo< Collection Outward Foreign Bills (or Collection Inward Bills for Collection Inward Foreign Dills (or Collection

19.04Other Commitments

Travellers Cheque m Hand Bangladesh Savings Certificates

Segregation of other commitments:i) Documentary audits and short term trade related transactionsii) Forward ass^-t purchased and forward deposit placediii) Undrawn foinia! sUndby facilities, credit lines and commitments to lend:

Under one year One year and ovur

iv) Sport and forward foreign exchange rate contractsv) Other exchange contracts

Letter of Guaraiitei-a) Claim against the1 Bank which is not acknowledged as debt(b) Money forwhicf ihe Bank is contingently liable in respect

of graranli;(.;s given favouring: Directors Government Bank and clher Financial institutions Others

19.06 Forward Assets Purchased and forward Buy Contact

1,996,439,700 4.882,202.000

192,394,000112,122,000

Leg.Rate Taka 2012

'Eastern BankStandard Chartc-ied BankBrae Bank Brsc Bank United Commercial bank United Commercial :kimK Standard Charged Bank Eastern Bank Eastern Bank Eastern Bank Standard Chartei ed Hank Eastern Bank Eastern Bank Bank Ai-Falah Standard CharL^eajsynj^

USDUSDUSDUSDUSDYENYENYENYENYENUSDUSDUSDUSDUSD

6,000,000 3,000,000

10,000,000 6,000,000

10,000,000 500,000,000 500,000,000

1.000,000,0001,000,000,0001,000,000,000

5,000,000 6,000,000 6,500,000 4,000,000

12,000,000

80.059380950079.169079.169079.1690

09030 09582 0.9404 09404 0.9537

80.240080 308380.308380.3659

480,355,800242,850,000791,690,000475,014,000791,690,000451,500,000479,100,000940,400,000940,400,000953,700,000401.200.000481,849,800522,003,950321.463,600964,080,000

9,237,297,150

20.00 Income Statement Income: Interest, discount and simitiar income Dividend income Fees, commission and brokerage Gains less losses ansmc from dealing securities Gains less losses un:;mc from investmenl securities Gains less tossus anting from dealing in foreign currencies Income from non-bani.iiig assets

=@@@ - Other operating income?.@.. ... -^ Profit less losic:; on n lUJiissi rale changes

1,883,197,344

166,887,367

- fi,fiSB,622

221,221.830

Amount inTaka2011

1,587,849,727

110.380,224

5,639,510 ^-_

2,056,743,3331.703,869,461

1,996,439,700 4,882,202,000

192,394,000 112,122,000

121,813,328 221,221,830

Hoda VasiChowdhury &Co

Amount in BDT

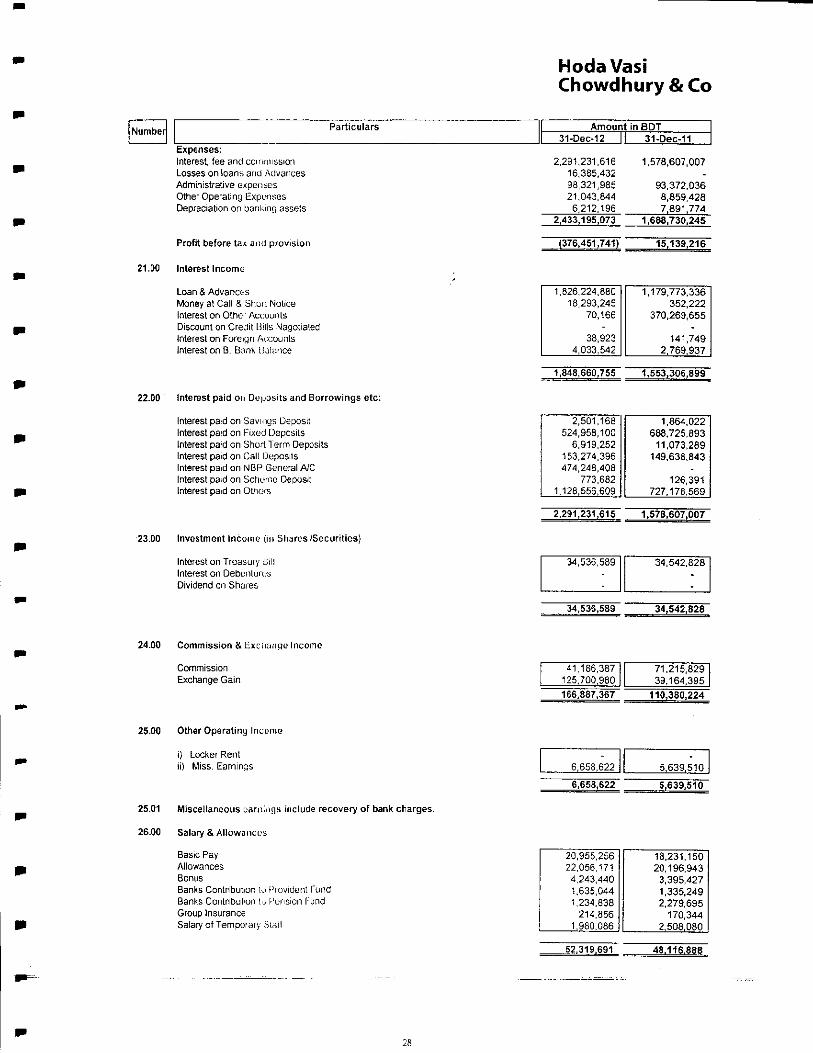

Expenses:Interest, lee and commissionLosses on !oans> and AdvancesAdministrative expensesOther Operating ExpunsesDepreciation on banking assets

Profit before ta< and provision

21.00 Interest Income

Loan & Advances Money at Call & Shon Nolice Interest on Other Aixounls Discount on Credit Bills Nagotialed Interest on Foreign Accounts Interest on B. Bank Balance

22.00 " Interest paid on Deposits and Borrowings etc:

Interest paid on Savings Deposit Interest paid on Fixed Deposits Interest paid on Short Term Deposits Interest paid on Call Deposits Interest paid on NBP General A/C Interest paid on Scheme Deposit Interest paid on Othois

Investment Income [in Shares /Securities)

Interest on Treasury UtllInterest on DebenluresDividend on Shares

24.00 Commission & Exc

CommissionExchange Gai

31-Dec-12

2,291,231,616 16,385,432 98,321,985 21,043.844

6,212,1962,433,195,073

1,578,607,007

93,372,036 8,859,428 7,891,774

25.00 Other Operating Income

i) Locker Rentii) Miss. Earnings

25.01 Miscellaneous earnings include recovery of bank charges.

26.00 Salary & Allowances

Basic Pay Allowances Bonus Banks Contribution lu Hrovident Fund Banks Contribution !@; Pension Fund Group Insurance Salary of Temporary Staff

38,9234,033,542

141,7492.769,937

2,501,168524,958,100

6,919,252153,274,396474,248,408

773,6821,128,666,609

1,864,022688,725,893

11,073,289149,638,843

126,391727,178,569

34,536,589

|125,700,98011_

166,887,367

34,542,828

71.215,829|39,164,395|

110,380,224

20,955,25622,056,1714,243,4401,635,0441,234.838

214,8561,980.086

18,231,15020.196,943

3,395,4271,335,2492,279,695

170,3442,508.080

Hoda VasiChowdhury & Co

Amount in BDT

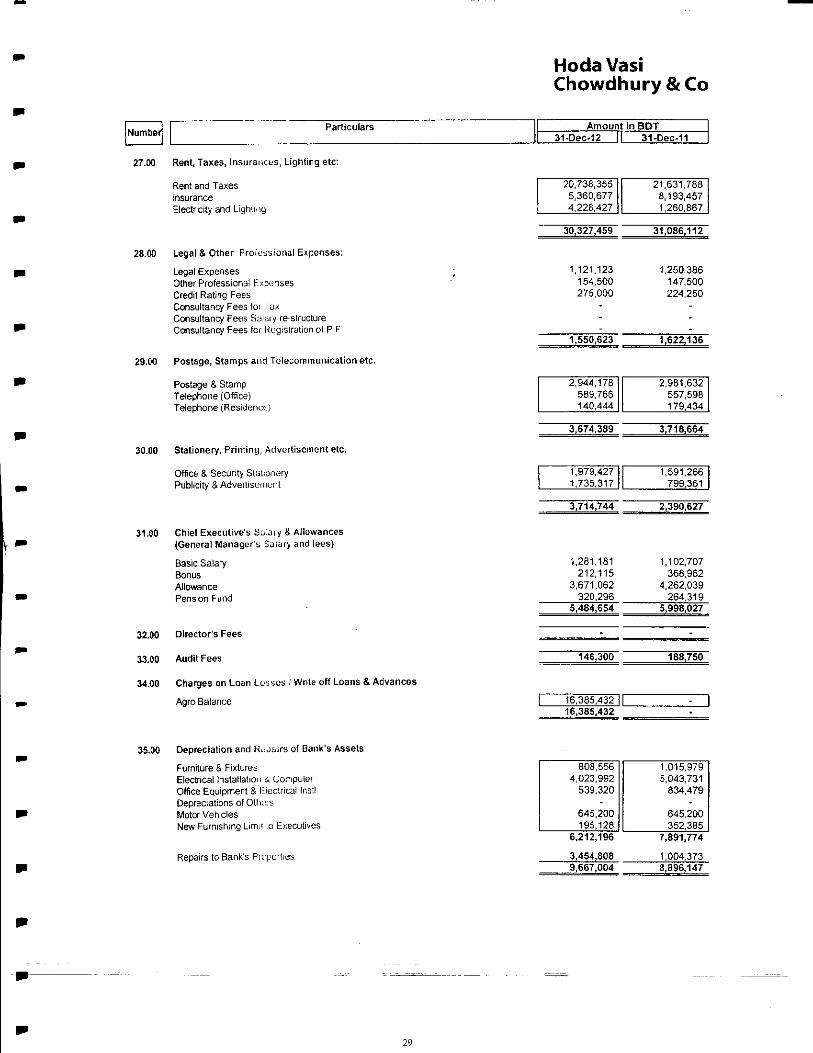

27.00 Rent, Taxes, Insurances, Lighting etc:

Rent and Taxes insurance Electricity and Lighlmy

28.00 Legal & Other Proioasional Expenses:

Legal Expenses Other Professional Expanses Credit Rating Fees Consultancy Fees for Tax Consultancy Fees Salaiy re-slructure Consultancy Fees for Kugistration of P F

29.00 Postage, Stamps and Telecommunication etc.

Postage & Stamp Telephone (Office) Telephone (Residence)

30.00 Stationery, Printing, Advertisement etc.

Office & Security StationeryPublicity & Advertisement

31.00 Chief Executive's S^ry & Allowances (General Manager's Salary and fees)

Basic Salary Bonus Allowance Pension Fund

32.00 Director's Fees

33.00 Audit Fees

34.00 Charges on Loan Losses i Write off Loans & Advances

Agro Balance

1,261,181 212,115

3.671,062 320,296

1,102,707 368,962

4,262,039 264,319

35.00 Depreciation and Repairs of Bank's Assets

Furniture & FixtLres Electrical Installation & computer Office Equipment & Heclrical Instl Depreciations of Otrios Motor Vehicles New Furnishing Limit io Executives

Repairs to Bank's Pic

6,212,196

3,454,8089,667,004

7,891,774

1,004,373

20,738,3555,360,6774,228,427

21,631,7888,193,4571,260.867

1,121,123154,500276,000

1,250,386147,500224,250

1,550,623 1,622,136

2,944,178589,766140,444

2,981,632557,598179,434

3,674,389 3,718,664

1,979,4271,735,317

3,714,744

I1,591.266I799,361

2,390,627

5,484,654

146,300

I16.385,4321116,385,432

5,998,027

-

188,750

-I

645.200195,128

645,200352,385

Hoda VasiChowdhury &Co

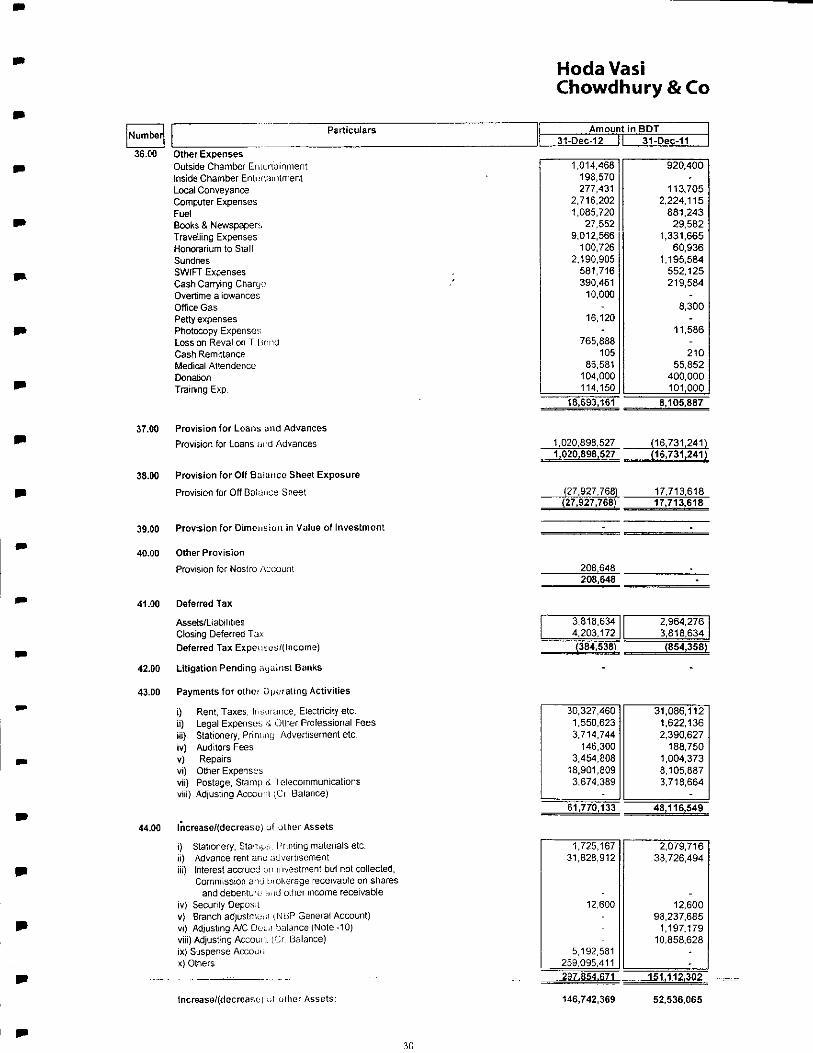

36.00

37.00 Provision for Loans und Advances Provision for Loans ;.i d Advances

38.00 Provision for Olf Balance Sheet Exposure

Provision for Off Balance Sheet

39.00 Provision for Dimension in Value of Investment

40.00 Other Provision Provision for Nostro Account

41.00 Deferred Tax

Assets/Liabilities Closing Deferred Tax Deferred Tax Expcni(.'S/(liicome)

42.00 Litigation Pending jujuitist Banks

43.00 Payments for othci Operating Activities

i)Rent, Taxes, Insurance, Electricity etc. ii)Legal Expenses >k Other Professional Fees iii)Stationery, Prinnmj, Advertisement etc. iv)Auditors Fees v)Repairs vi)Other Expenses vii)Postage, Stamp & I elecommunications viii)Adjusting Account (Ci Balance)

44.00 lncrease/(decreaso) uf other Assets

i) Stationery, Starry. Punting materials etc. ii) Advance rent unc advertisement iit) Interest accrued un investment but not collected,

Commission arvj brokerage receivable on shares and debenture- .ji id other income receivable

iv) Security Deposit v) Branch adjustment (NUP General Account} vi) Adjusting A/C Dol.i balance (Note -10) viii) Adjust'ng Accouiu (Cr Balance) ix) Suspense Accoun! x) Others

3,818.634 I4.203,172 |

2,964,27613,818,634 I

lncrease/(decrcast'j o\ oilier Assets:

IParticulars]|[._.IIOther ExpensesOutside Chamber EntertainmentIInside Chamber Entufiamtment*ILocal Conveyance|Computer Expenses|FuelIBooks & Newspaper;,|Travelling Expenses|Honorarium to Staff]Sundries|SWIFT Expenses-|Cash Carrying Chary;:@'|Overtime allowancesIOffice GasIPetty expensesIPhotocopy Expense;;|Loss on Reval on T.LsondICash Remittance|Medical Attendencu!DonationITraining Exp.I

IAmount in BDT1I 31-DEC-12 II 31-Dec-11 I

r 1,014,4681I198,670 |I277,431 |I2,716,202 |I1.085,720 I

27,552 |9,012.566 I

100,726!I2,190,905 |I581,716 |j390,461 |I10,000 |I - II16,120 II @ II765,888 |I105l

86,581 |104,000 I

I114.150 |

I920,400 |I- II113,705 |I2,224,115 II881,243 |I29.582 II1,331,665 |I60,936 |I1,195,584 |I552,125 |I219,584 |I- II8,300 |I@ II11,586!I- II210 II55.852 II400.000 |I101,000 I

1,020,898,5271,020,898,527

(27,927,768)(27,927,768)

208,648208,648

8,105,887

(16,731,241)(16,731,241)

17,713,61817,713,618

30,327,4601.550,6233.714,744

146,3003,454,808

18,901,8093,674,389

31,086,1121.622,1362,390,627

188,7501,004,3738,105,8873.718,664

1,725,16731,828,912

12,600

5,192,581259,095.411

2,079,71638,726,494

12,60098,237.685

1,197,17910,858,628

Hoda VasiChowdhury & Co

Amount in BDT

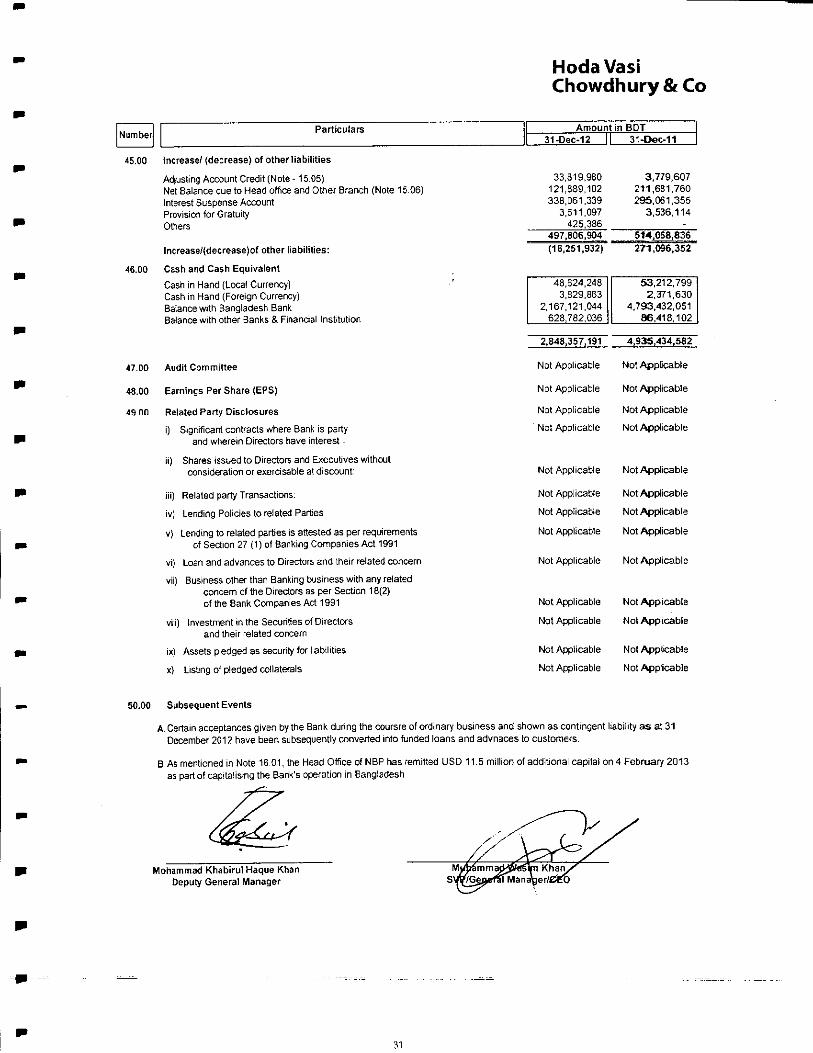

45.00 Increase/ (decrease) of other-liabilities

Adjusting Account Credit (Note -15.05) Net Balance due to Head office and Other Branch (Note 15.06) Interest Suspense Account Provision for Gratuity Otters

lncrease/(decrease)of other liabilities:

46.00 Cash and Cash Equivalent Cash in Hand (Local Currency) Cash in Hand (Foreign Currency) Balance with Bangladesh Bank Balance with other Banks & Financial Institution

47.00 Audit Committee

48.00 Earnings Per Share {EPS)

49 00 Related Party Disclosures

i) Significant contracts where Bank is party and wherein Directors have interest -

ii) Shares issued to Directors and Executives without consideration or exercisable at discount:

iii) Related party Transactions:

iv) Lending Policies to related Parties

v) Lending to related parties is attested as per requirements of Section 27 (1) of Banking Companies Act 1991

vi) Loan and advances to Directors and their related concern

vii) Business other than Banking business with any related concern of the Directors as per Section 18(2) of the Bank Companies Act 1991

viii) Investment in the Securities of Directors and their related concern

ix) Assets pledged as security for I abilities

x) Listing of pledged collaterals

33,819,980121,889,102338,061.339

3,611,097 425.386

3.779,607211,681,760295,061,355

3,536,114

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not ApplicableNot Applicable

Not ApplicableNot Applicable

Not ApplicableNot Applicable

Not ApplicableNot Applicable

Not ApplicableNot Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

Not Applicable

50.00 Subsequent Events

A,Certain acceptances given by the Bank during the coursre of ordinary business and shown as contingent liability as at 31 December 2012 have been subsequently converted into funded loans and advnaces to customers.

B.As mentioned in Note 16.01, the Head Office of NBP has remitted USD 11.5 million of additional capital on 4 February 2013 as part of capitalising the Bank's operation in Bangladesh

Mohammad Khabirul Haque Khan Deputy General Manager

497,806,904(16,251,932)

48,624,248II3,329,663

2,167.121.044628,762,036I!

2,848,357,191

514,058,836271,096,352

53,212,7992,371,630

4,793,432,05186,418.102

4,935,434,582

I O

|m5 IS

TO>TO

@DO

0o

@o

50

cc@a:

8

NO

urrency|

u

o

Taka|

cval

qui

UJate1

Li

c3OE

Li

nH

c@

>qui

LU

*2TO

XLU

C30

<oLL

ah-

theBank

"o

oECOz

219|

oCO

LO81.

COCMTfo>

mCOCMO>"N-

LOdCO

COCM^tCO

ACUS

ao

cutta|

Sal

Chartered,(

C.2C/)

013|

CNCO

.CO

O)CNCOCMcm'

O)COaito

moCO

o

cm"

ACUS|

QO

umbai

2(Jen(AI

1

USD

QO