NATIONAL BANK OF GREECE Strategic Planning & Research · NATIONAL BANK OF GREECE Strategic Planning...

33

NATIONAL BANK OF GREECE Strategic Planning & Research July 2012 Paul Mylonas General Manager Strategy & International Operations, Chief Economist for the Group Andreas Athanasopoulos General Manager Retail Banking

Transcript of NATIONAL BANK OF GREECE Strategic Planning & Research · NATIONAL BANK OF GREECE Strategic Planning...

NATIONAL BANK OF GREECE

Strategic Planning & Research

July 2012

Paul Mylonas

General Manager Strategy &

International Operations,

Chief Economist for the Group

Andreas Athanasopoulos

General Manager Retail Banking

2

While small and medium-sized enterprises (SMEs) are a vital component of the Greek business sector,

knowledge of their structure and dynamics is limited.

This survey aims at filling part of that gap. In view of the lack of published data, this analysis is based

mainly on data drawn from a sample of almost 1,000 enterprises.

Both the structure of our questionnaire and the construction of the business confidence indices were

based on European Commission and OECD harmonized questionnaire standards, in order to: i) achieve

maximum reliability and predictability of indices; and ii) enable comparability with confidence indices

for the business sector as a whole in Greece (such as IOBE indices) and Europe (e.g., those of the EC).

This survey will be carried out each semester so as to form a clear picture of the SMEs’ course over time

(as reflected in the business confidence index).

In this phase of the survey, a cross-section comparison of the indices offers some useful insights into

the growth potential, as well as the inherent challenges faced by SMEs:

Very small enterprises appear to be weakening and this business segment is contracting.

The main problem for SMEs at present is their lack of access to credit, largely reflecting the

substantial reduction in trade credit.

However, using an ordered probit model, we discern a subset of SMEs that remains healthy and

oriented mainly to external markets and new products.

Accordingly, policy regarding SMEs needs to be structured around three core targets:

Reducing operating costs

Enhancing liquidity

Enhancing sales

In brief

Table of contents

3

Introduction: SMEs’ position in the market

NBG’s Survey of Greek SMEs

Methodology

Key findings

Variations by size and sector

The outlook for Greek SMEs

SMEs with growth prospects

Policy directions

Annex: Survey ID

5

Small and medium-sized enterprises* in Greece account for a

greater part of the business sector, as compared with other

European countries (60% of turnover, versus 40% on average

in Europe). Note that this difference arises from the higher

share held by firms with turnover below €2 million in Greece

(40% versus 19% in Europe). SMEs have a strong presence in

trade and construction, and a weaker presence in industry.

Greek SMEs are of smaller scale than in Europe (with average

turnover of c. €200,000 versus €400,000 in Europe). The

greatest difference in size is found in manufacturing, where

European SMEs are triple the size of their Greek

counterparts.

In light of the above, a picture emerges of a deeply fragmented

sector, which is dominated by very small firms. Nevertheless,

we should stress that the small business segment (turnover

<€1 million) has been contracting over time, as it accounted

for ¼ of the business sector in 2007 compared with ⅓ in

2002.

Introduction to the survey:

SMEs dominate the Greek business sector

* For the purposes of our survey, we define SMEs as enterpriseswith turnover of less than €10 million. Note

that firms of this size are defined as “small” by the European Commission (2003/361/EC) in the context of

similar analyses.

0,20,1

0,3

0,10,2

0,6

0,2

0,6

0,30,4

0

0,2

0,4

0,6

0,8

milio

n €

Average turnover of SMEs

Greece EU (27)

Source: Eurostat

* The data refer to companies with less than 50employees, which to a large extent report a turnover of lessthan €10 million (which is our definition ofSMEs).

34%

69% 58%68%

60%

19%

49% 46%61%

40%

0%

20%

40%

60%

80%

100%

% turn

over

SMEs in the business sector

Greece EU (27)

Source: Eurostat

* The data refer to companies with less than 50employees, which to a large extent report a turnover of lessthan €10 million (which is our definition ofSMEs).

Half of SMEs turnover derives from small firms and half from

medium-sized firms

6

The approximately 750,000 SMEs in Greece generate turnover of around €150 billion.

4/5 of SMEs are sole proprietorships, which account for a corresponding share of the total domestic

business sector (compared with just ½ of the business sector in Europe).

Although sole proprietorships comprise the majority of SMEs, the greater share of turnover (over 60%) is

produced by companies of various legal status (SA, limited partnership, limited liability, etc.).

Number of SMEs

747,800 firms

Sole proprietorships

79%

Companies

21%

Small

78%

Medium

1%

Small

18%

Medium

3%

* For the purposes of the survey, small enterprises are those reporting turnover of less than €1 million and medium-sized

enterprises are those reporting turnover of between €1 million and €10 million.

Turnover of SMEs

€150 billion

Sole proprietorships

38%

Companies

62%

Small

32%

Medium

6%

Small

18%

Medium

44%

* For the purposes of the survey, small enterprises are those reporting turnover of less than €1 million and medium-sized

enterprises are those reporting turnover of between €1 million and €10 million.

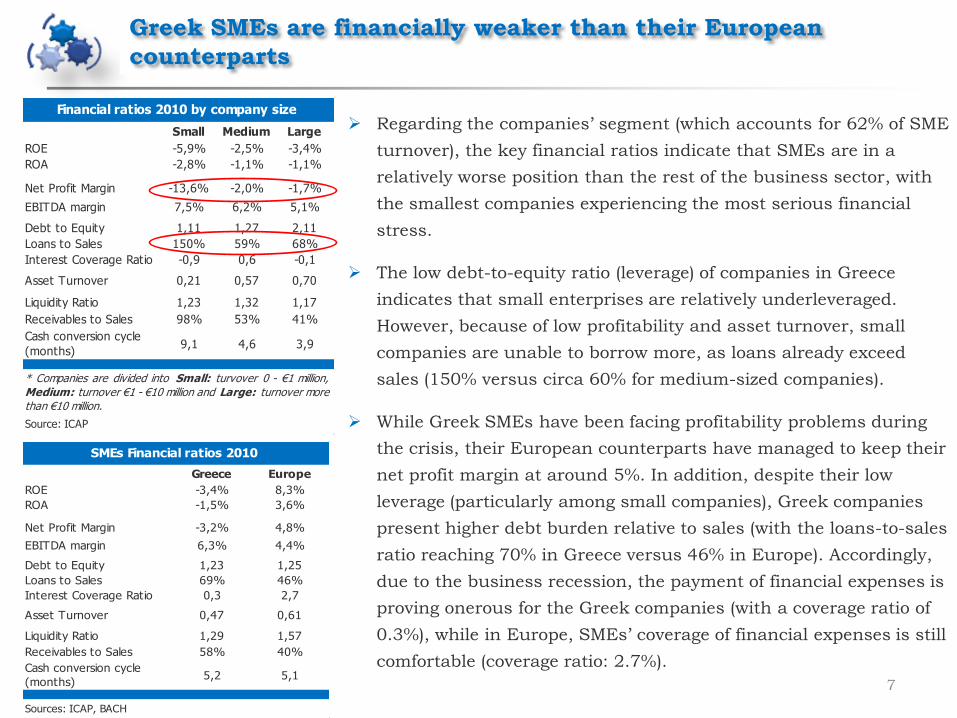

Greek SMEs are financially weaker than their European

counterparts

7

Regarding the companies’ segment (which accounts for 62% of SME

turnover), the key financial ratios indicate that SMEs are in a

relatively worse position than the rest of the business sector, with

the smallest companies experiencing the most serious financial

stress.

The low debt-to-equity ratio (leverage) of companies in Greece

indicates that small enterprises are relatively underleveraged.

However, because of low profitability and asset turnover, small

companies are unable to borrow more, as loans already exceed

sales (150% versus circa 60% for medium-sized companies).

While Greek SMEs have been facing profitability problems during

the crisis, their European counterparts have managed to keep their

net profit margin at around 5%. In addition, despite their low

leverage (particularly among small companies), Greek companies

present higher debt burden relative to sales (with the loans-to-sales

ratio reaching 70% in Greece versus 46% in Europe). Accordingly,

due to the business recession, the payment of financial expenses is

proving onerous for the Greek companies (with a coverage ratio of

0.3%), while in Europe, SMEs’ coverage of financial expenses is still

comfortable (coverage ratio: 2.7%).

Small Medium Large

ROE -5,9% -2,5% -3,4%

ROA -2,8% -1,1% -1,1%

Net Profit Margin -13,6% -2,0% -1,7%

EBITDA margin 7,5% 6,2% 5,1%

Debt to Equity 1,11 1,27 2,11

Loans to Sales 150% 59% 68%

Interest Coverage Ratio -0,9 0,6 -0,1

Asset Turnover 0,21 0,57 0,70

Liquidity Ratio 1,23 1,32 1,17

Receivables to Sales 98% 53% 41%

Cash conversion cycle

(months)9,1 4,6 3,9

Source: ICAP

Financial ratios 2010 by company size

* Companies are divided into Small: turvover 0 - €1 million,Medium: turnover €1 - €10 million and Large: turnover more than €10 million.

Greece Europe

ROE -3,4% 8,3%

ROA -1,5% 3,6%

Net Profit Margin -3,2% 4,8%

EBITDA margin 6,3% 4,4%

Debt to Equity 1,23 1,25

Loans to Sales 69% 46%

Interest Coverage Ratio 0,3 2,7

Asset Turnover 0,47 0,61

Liquidity Ratio 1,29 1,57

Receivables to Sales 58% 40%

Cash conversion cycle

(months)5,2 5,1

Sources: ICAP, BACH

SMEs Financial ratios 2010

8

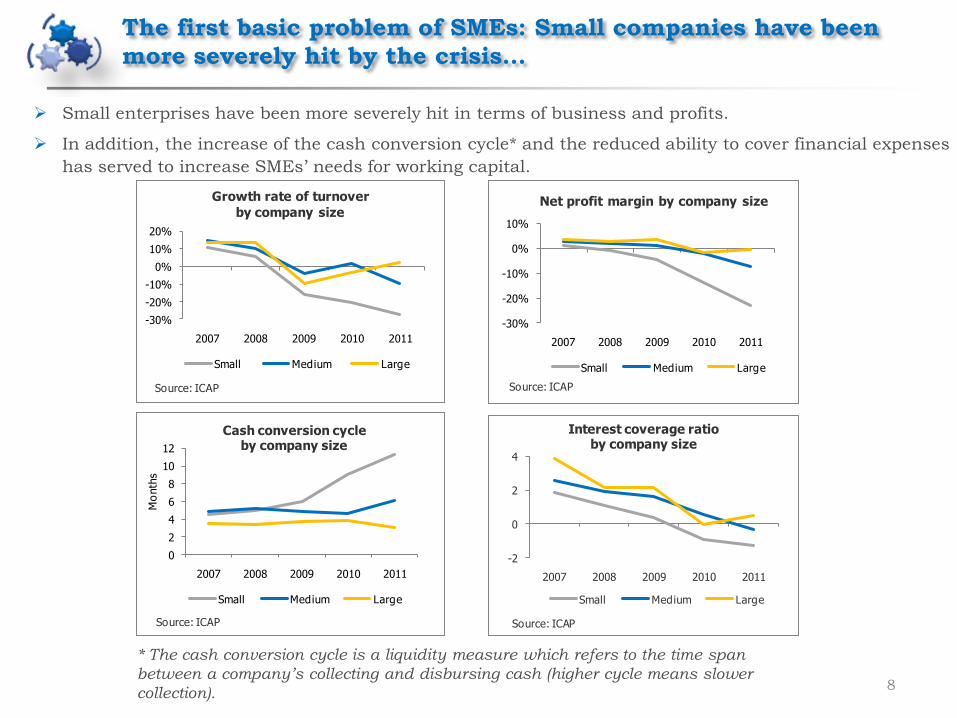

Small enterprises have been more severely hit in terms of business and profits.

In addition, the increase of the cash conversion cycle* and the reduced ability to cover financial expenses

has served to increase SMEs’ needs for working capital.

The first basic problem of SMEs: Small companies have been

more severely hit by the crisis…

-30%

-20%

-10%

0%

10%

20%

2007 2008 2009 2010 2011

Growth rate of turnover

by company size

Small Medium Large

Source: ICAP

-30%

-20%

-10%

0%

10%

2007 2008 2009 2010 2011

Net profit margin by company size

Small Medium Large

Source: ICAP

-2

0

2

4

2007 2008 2009 2010 2011

Interest coverage ratio by company size

Small Medium Large

Source: ICAP

0

2

4

6

8

10

12

2007 2008 2009 2010 2011

Mo

nth

s

Cash conversion cycleby company size

Small Medium Large

Source: ICAP

* The cash conversion cycle is a liquidity measure which refers to the time span

between a company’s collecting and disbursing cash (higher cycle means slower

collection).

9

While the ratio of operating costs to sales is lower in small

companies, this advantage is fully offset by the impact of anti-

economies of scale. Therefore, in the three-year period 2008-

2010, although small companies managed to post an operating

profit margin of around 11.5%, fixed cost charges acted as a

brake on profitability by almost 18 percentage points, thereby

generating net losses (-6.4% for the same period).

The first reason for the high fixed costs at small companies

(and, accordingly, the wide gap between operating profit margin

and net profit margin) is the low asset turnover (0.3 for small

enterprises, 0.6 for medium-sized enterprises, and 0.7 for larger

firms). This parameter is reflected in the high ratio of

depreciation to sales (20% in very small companies versus circa

5% in large companies).

High fixed costs reduce significantly the flexibility of small

companies, thus making them more vulnerable under

conditions of falling demand.

… mainly due to anti-economies of scale…

Small Medium Large

Net Profit Margin -6,4% 0,3% 1,6%

EBITDA margin 11,3% 8,4% 7,5%

Margin Gap (net - ebitda) -17,7% -8,1% -5,9%

Asset Turnover 0,27 0,57 0,70

Source: ICAP (average 2008-2010)

Financial ratios by company size

0%

5%

10%

15%

20%

25%

(0 -

0,1

]

(0,1

-0,5

]

(0,5

-1]

(1 -

2,5

]

(2,5

-5]

(5 -

10]

(10 -

50]

>50

Dep

reci

atio

n to

sal

es

Turnover (million €)

Depreciation expenses by company size

Source: ICAP (average 2008-2010)

LargeSMEs

10

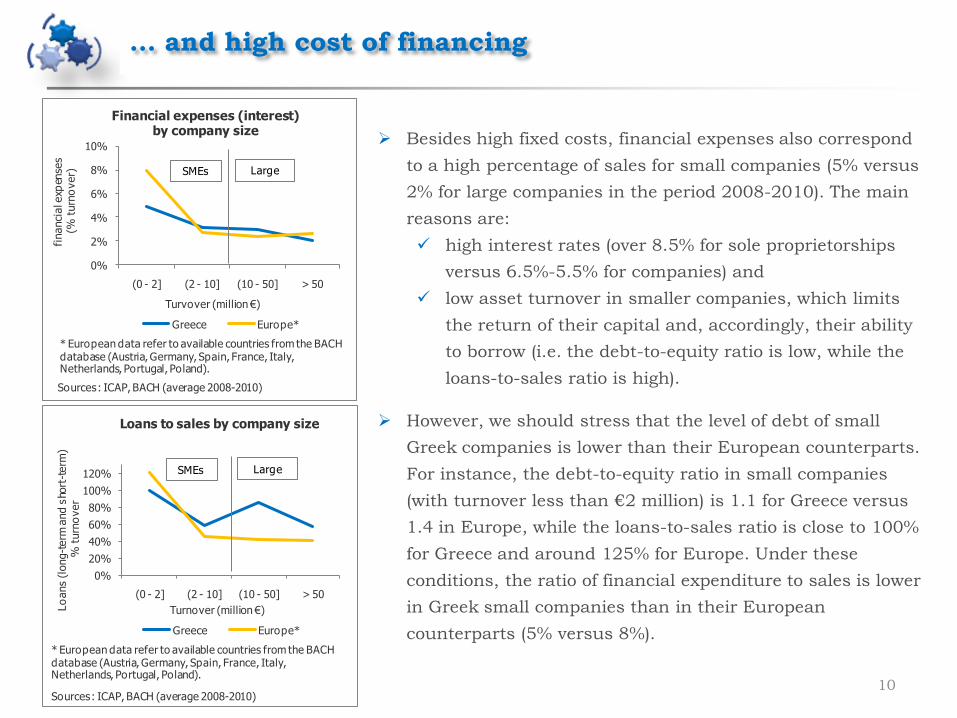

Besides high fixed costs, financial expenses also correspond

to a high percentage of sales for small companies (5% versus

2% for large companies in the period 2008-2010). The main

reasons are:

high interest rates (over 8.5% for sole proprietorships

versus 6.5%-5.5% for companies) and

low asset turnover in smaller companies, which limits

the return of their capital and, accordingly, their ability

to borrow (i.e. the debt-to-equity ratio is low, while the

loans-to-sales ratio is high).

However, we should stress that the level of debt of small

Greek companies is lower than their European counterparts.

For instance, the debt-to-equity ratio in small companies

(with turnover less than €2 million) is 1.1 for Greece versus

1.4 in Europe, while the loans-to-sales ratio is close to 100%

for Greece and around 125% for Europe. Under these

conditions, the ratio of financial expenditure to sales is lower

in Greek small companies than in their European

counterparts (5% versus 8%).

… and high cost of financing

0%

2%

4%

6%

8%

10%

(0 - 2] (2 - 10] (10 - 50] > 50

financi

al e

xpen

ses

(% t

urn

over)

Turvover (million €)

Financial expenses (interest)by company size

Greece Europe*

Large

Sources: ICAP, BACH (average 2008-2010)

* European data refer to available countries from the BACH database (Austria, Germany, Spain, France, Italy, Netherlands, Portugal, Poland).

SMEs

0%

20%

40%

60%

80%

100%

120%

(0 - 2] (2 - 10] (10 - 50] > 50

Lo

ans

(long-t

erm

and

sho

rt-t

erm

)%

turn

over

Turnover (million €)

Loans to sales by company size

Greece Europe*

LargeSMEs

* European data refer to available countries from the BACH database (Austria, Germany, Spain, France, Italy, Netherlands, Portugal, Poland).

Sources: ICAP, BACH (average 2008-2010)

The second basic problem for SMEs: Reduced trade credit from

suppliers has disrupted their financing equilibrium

11

Suppliers’ reluctance to provide credit, combined with the

squeeze on equity (in part because of reduced earnings), has

generated a substantial liquidity gap among SMEs.

Trade credit (i.e. credit from suppliers) is a significant source of

funding for Greek SMEs (accounting for 23% of their external

financing versus 16% for European SMEs).

This significant liquidity gap has been largely covered by a

higher share of loans relative to total financing by SMEs, up by

7 percentage points during the past five years (from 26% to

33%). Specifically, refinancing of loans by SMEs has led to a

reduction in short-term liabilities to banks and an increase in

long-term borrowing (mainly in the form of corporate bonds

and syndicated loans). Before the crisis, companies preferred

borrowing to trade credit.

In addition, as a result of reduced liquidity, there are now

increased delays in payments to other creditors (such as

rents).

23% 16%

59% 67%

18% 18%

0%

20%

40%

60%

80%

100%

Greece Europe

Str

uct

ure

of Lia

bili

ties

External Financing of SMEs

Trade creditors Loans* Other creditors

Sources: ICAP, BACH

* Loans include long-term liabilities and

short-term payments of long-term loans

(mainly from banks).

-6%

-1%

7%

3%

-8%

-4%

0%

4%

8%

SMEs Large

Chang

e in

fi

nanci

ng

co

ntr

ibution

Change in financing sources(2006-2011)

Trade creditors Other creditors

Loans* Equity

Source: ICAP

Sample

13

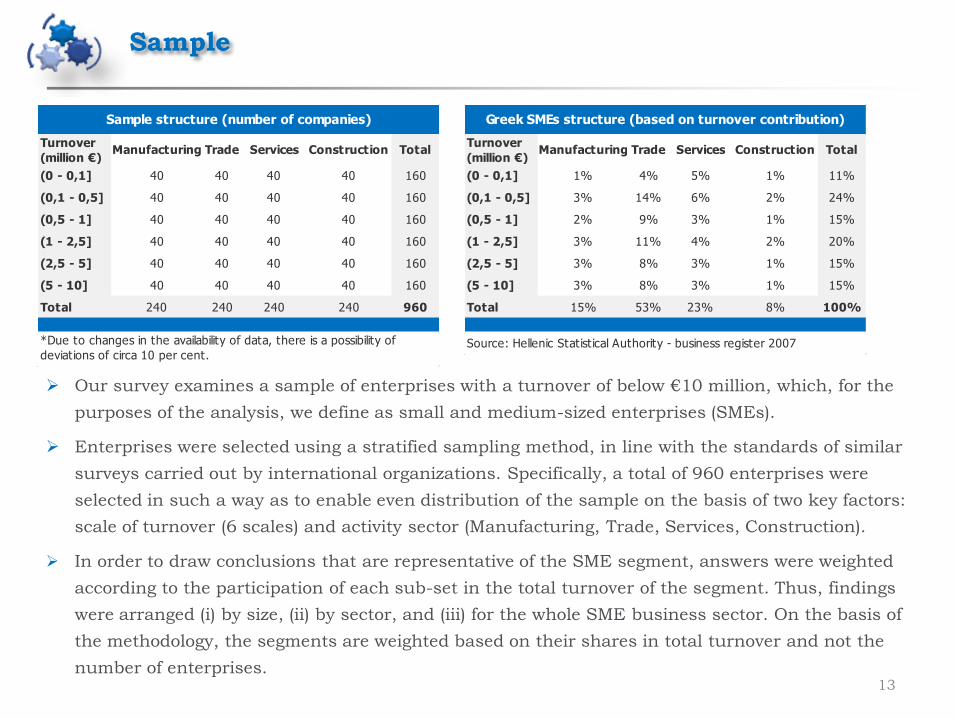

Our survey examines a sample of enterprises with a turnover of below €10 million, which, for the

purposes of the analysis, we define as small and medium-sized enterprises (SMEs).

Enterprises were selected using a stratified sampling method, in line with the standards of similar

surveys carried out by international organizations. Specifically, a total of 960 enterprises were

selected in such a way as to enable even distribution of the sample on the basis of two key factors:

scale of turnover (6 scales) and activity sector (Manufacturing, Trade, Services, Construction).

In order to draw conclusions that are representative of the SME segment, answers were weighted

according to the participation of each sub-set in the total turnover of the segment. Thus, findings

were arranged (i) by size, (ii) by sector, and (iii) for the whole SME business sector. On the basis of

the methodology, the segments are weighted based on their shares in total turnover and not the

number of enterprises.

Turnover

(million €)Manufacturing Trade Services Construction Total

(0 - 0,1] 40 40 40 40 160

(0,1 - 0,5] 40 40 40 40 160

(0,5 - 1] 40 40 40 40 160

(1 - 2,5] 40 40 40 40 160

(2,5 - 5] 40 40 40 40 160

(5 - 10] 40 40 40 40 160

Total 240 240 240 240 960

*Due to changes in the availability of data, there is a possibility of

deviations of circa 10 per cent.

Sample structure (number of companies)

Turnover

(million €)Manufacturing Trade Services Construction Total

(0 - 0,1] 1% 4% 5% 1% 11%

(0,1 - 0,5] 3% 14% 6% 2% 24%

(0,5 - 1] 2% 9% 3% 1% 15%

(1 - 2,5] 3% 11% 4% 2% 20%

(2,5 - 5] 3% 8% 3% 1% 15%

(5 - 10] 3% 8% 3% 1% 15%

Total 15% 53% 23% 8% 100%

Greek SMEs structure (based on turnover contribution)

Source: Hellenic Statistical Authority - business register 2007

Constructing a business confidence index

14

In order to construct a confidence index for SMEs, we included a number of basic questions

regarding the level of business activity in the previous and in the coming semester. The model for the

questions is based on the harmonized questionnaire recommended by the OECD and the European

Commission, thereby enhancing the predictability of the index.

The Index questions have 3 alternative answers: increase (+), no change (=), decrease (-), or above

normal (+), normal (=), below normal (-). To begin with, we convert the number of answers per

category (+,=,-) to percentages and then we calculate the net result by subtracting the (-) from the (+)

percentage. Last, the confidence index for each sector is the average of the net results for the

following questions:

For manufacturing: The level of orders, inventories, and future production trend.

For services: The business situation of the firm in the previous semester, past and future

demand trend.

For trade: Level of inventories, past and future demand.

For construction: Level of backlog, and future employment trend.

For the SME sector, the business confidence index has been estimated as a weighted average of its

subsectors (the weights being the shares of the sectors’ turnover in the economy).

By carrying out the survey on a regular 6-month basis we should be able to form a picture of SMEs’

course over time, as reflected in the index. To draw reliable conclusions, comparison will be made

between the current index level and its long-term average (so as to correct possible over-optimism or

over-pessimism bias).

16

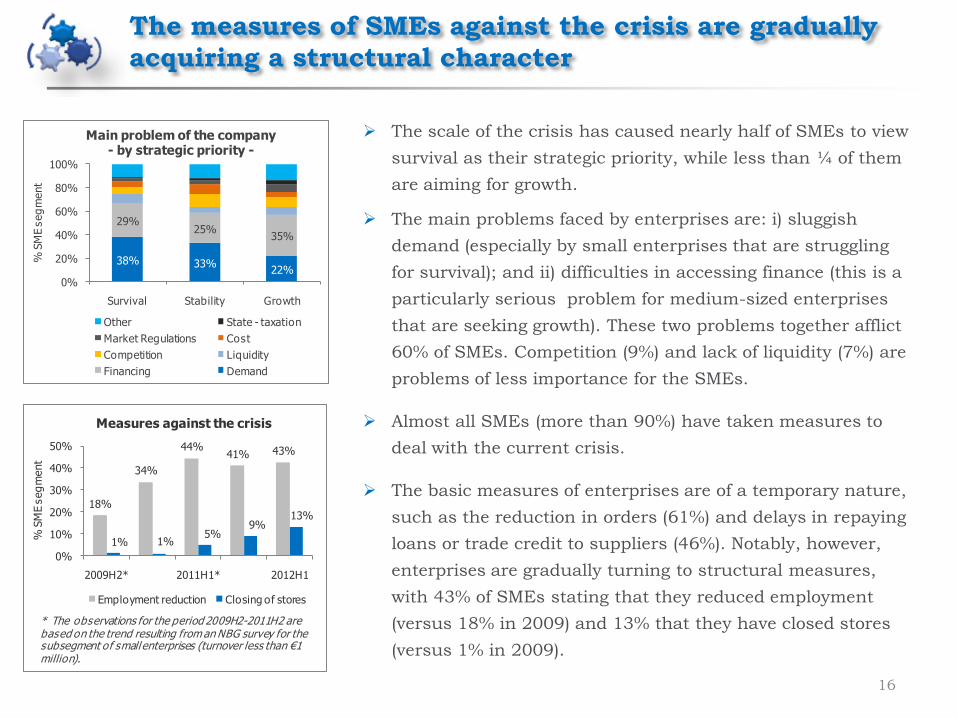

The scale of the crisis has caused nearly half of SMEs to view

survival as their strategic priority, while less than ¼ of them

are aiming for growth.

The main problems faced by enterprises are: i) sluggish

demand (especially by small enterprises that are struggling

for survival); and ii) difficulties in accessing finance (this is a

particularly serious problem for medium-sized enterprises

that are seeking growth). These two problems together afflict

60% of SMEs. Competition (9%) and lack of liquidity (7%) are

problems of less importance for the SMEs.

Almost all SMEs (more than 90%) have taken measures to

deal with the current crisis.

The basic measures of enterprises are of a temporary nature,

such as the reduction in orders (61%) and delays in repaying

loans or trade credit to suppliers (46%). Notably, however,

enterprises are gradually turning to structural measures,

with 43% of SMEs stating that they reduced employment

(versus 18% in 2009) and 13% that they have closed stores

(versus 1% in 2009).

The measures of SMEs against the crisis are gradually

acquiring a structural character

38% 33%22%

29%25%

35%

0%

20%

40%

60%

80%

100%

Survival Stability Growth

% S

ME s

eg

ment

Main problem of the company- by strategic priority -

Other State - taxation

Market Regulations Cost

Competition Liquidity

Financing Demand

18%

34%

44%41% 43%

1% 1%5%

9%13%

0%

10%

20%

30%

40%

50%

2009Η2* 2011Η1* 2012Η1

% S

ME s

eg

ment

Measures against the crisis

Employment reduction Closing of stores

* The observations for the period 2009Η2-2011Η2 are based on the trend resulting from an NBG survey for the subsegment of small enterprises (turnover less than €1 million).

Financing of working capital at SMEs is being hit by the

reduction in trade credit…

17

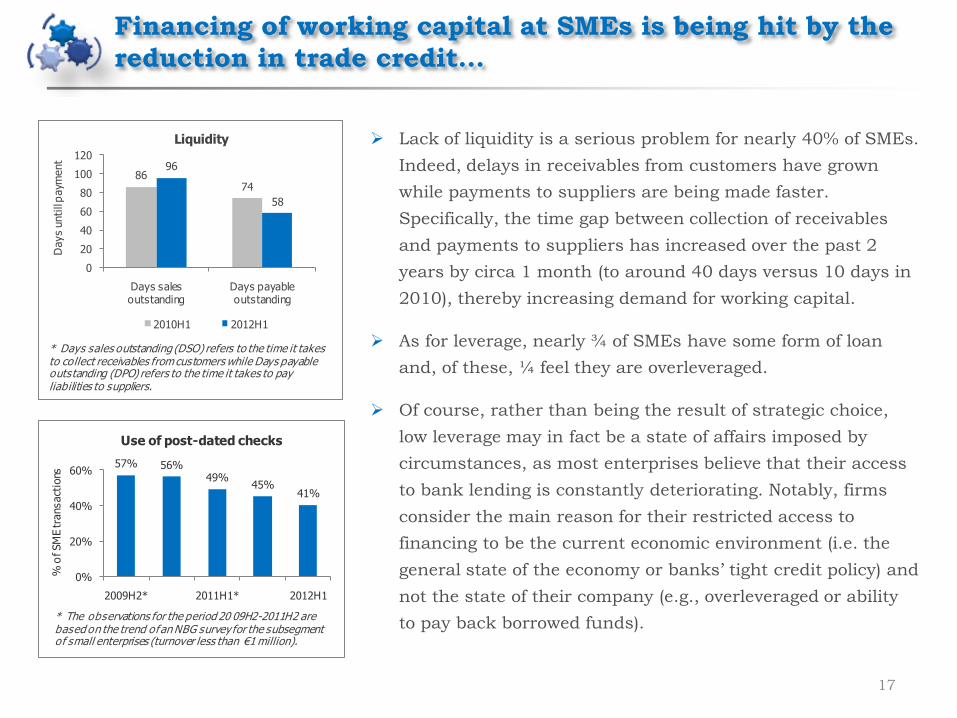

Lack of liquidity is a serious problem for nearly 40% of SMEs.

Indeed, delays in receivables from customers have grown

while payments to suppliers are being made faster.

Specifically, the time gap between collection of receivables

and payments to suppliers has increased over the past 2

years by circa 1 month (to around 40 days versus 10 days in

2010), thereby increasing demand for working capital.

As for leverage, nearly ¾ of SMEs have some form of loan

and, of these, ¼ feel they are overleveraged.

Of course, rather than being the result of strategic choice,

low leverage may in fact be a state of affairs imposed by

circumstances, as most enterprises believe that their access

to bank lending is constantly deteriorating. Notably, firms

consider the main reason for their restricted access to

financing to be the current economic environment (i.e. the

general state of the economy or banks’ tight credit policy) and

not the state of their company (e.g., overleveraged or ability

to pay back borrowed funds).

57% 56%49%

45%41%

0%

20%

40%

60%

2009Η2* 2011Η1* 2012Η1

% o

f SM

E tra

nsact

ions

Use of post-dated checks

* The observations for the period 20 09Η2-2011Η2 are based on the trend of an NBG survey for the subsegment of small enterprises (turnover less than €1 million).

8674

96

58

0

20

40

60

80

100

120

Days sales outstanding

Days payable outstanding

Days u

ntill p

aym

ent

Liquidity

2010Η1 2012Η1

* Days sales outstanding (DSO) refers to the time it takes to collect receivables from customers while Days payable outstanding (DPO) refers to the time it takes to pay liabilities to suppliers.

… while financing of investments is hampered mainly by

low earnings

18

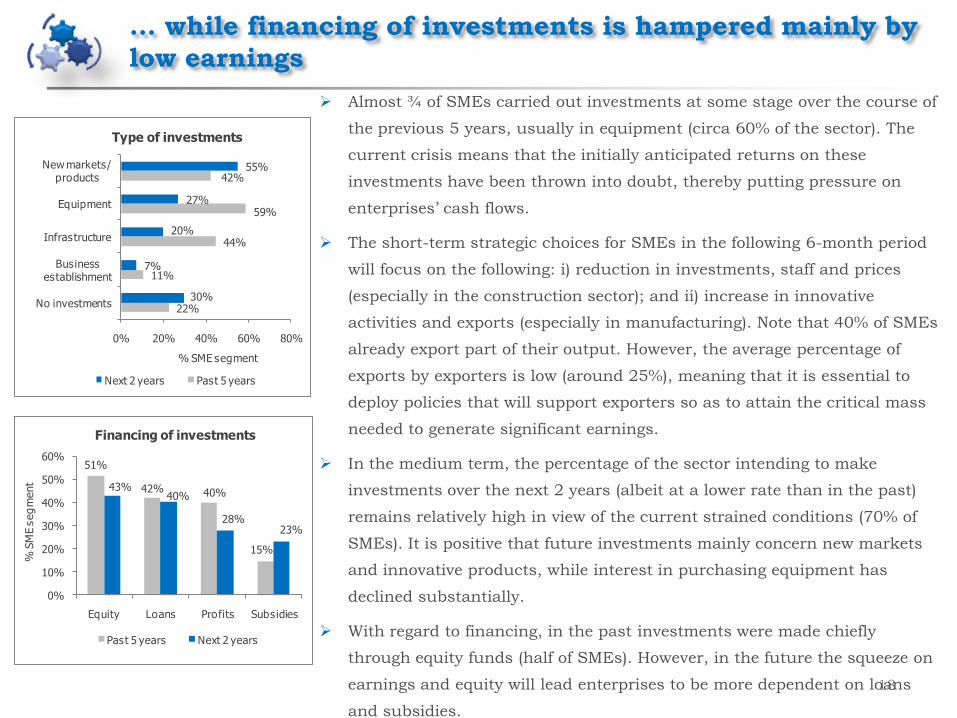

Almost ¾ of SMEs carried out investments at some stage over the course of

the previous 5 years, usually in equipment (circa 60% of the sector). The

current crisis means that the initially anticipated returns on these

investments have been thrown into doubt, thereby putting pressure on

enterprises’ cash flows.

The short-term strategic choices for SMEs in the following 6-month period

will focus on the following: i) reduction in investments, staff and prices

(especially in the construction sector); and ii) increase in innovative

activities and exports (especially in manufacturing). Note that 40% of SMEs

already export part of their output. However, the average percentage of

exports by exporters is low (around 25%), meaning that it is essential to

deploy policies that will support exporters so as to attain the critical mass

needed to generate significant earnings.

In the medium term, the percentage of the sector intending to make

investments over the next 2 years (albeit at a lower rate than in the past)

remains relatively high in view of the current strained conditions (70% of

SMEs). It is positive that future investments mainly concern new markets

and innovative products, while interest in purchasing equipment has

declined substantially.

With regard to financing, in the past investments were made chiefly

through equity funds (half of SMEs). However, in the future the squeeze on

earnings and equity will lead enterprises to be more dependent on loans

and subsidies.

22%

11%

44%

59%

42%

30%

7%

20%

27%

55%

0% 20% 40% 60% 80%

No investments

Business establishment

Infrastructure

Equipment

New markets/ products

% SME segment

Type of investments

Next 2 years Past 5 years

51%

42% 40%

15%

43%40%

28%23%

0%

10%

20%

30%

40%

50%

60%

Equity Loans Profits Subsidies

% S

ME s

eg

ment

Financing of investments

Past 5 years Next 2 years

Business confidence index

20

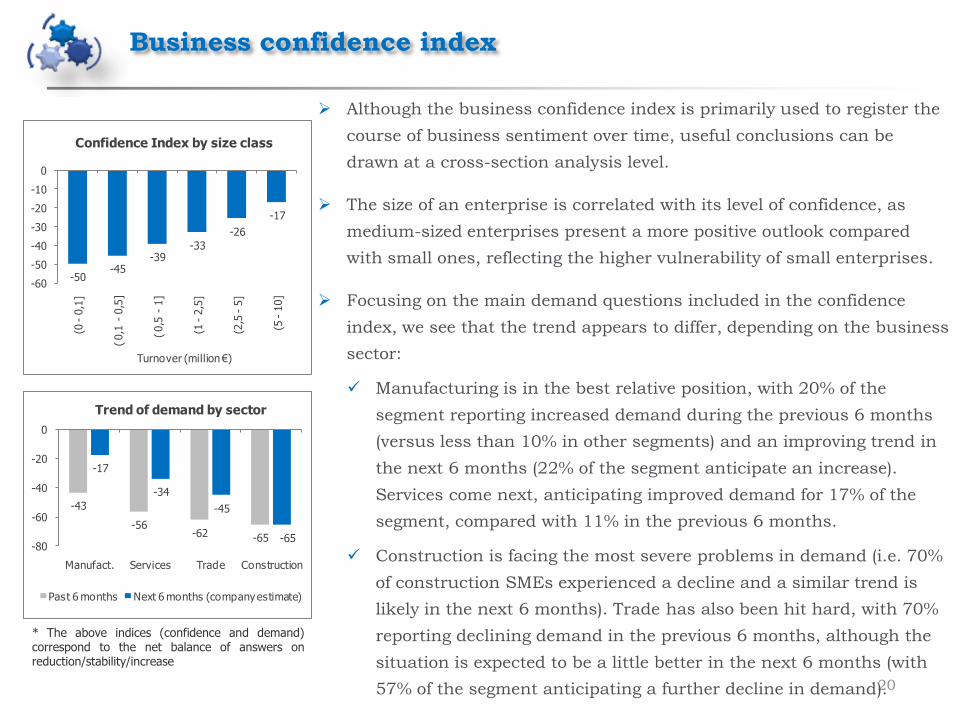

Although the business confidence index is primarily used to register the

course of business sentiment over time, useful conclusions can be

drawn at a cross-section analysis level.

The size of an enterprise is correlated with its level of confidence, as

medium-sized enterprises present a more positive outlook compared

with small ones, reflecting the higher vulnerability of small enterprises.

Focusing on the main demand questions included in the confidence

index, we see that the trend appears to differ, depending on the business

sector:

Manufacturing is in the best relative position, with 20% of the

segment reporting increased demand during the previous 6 months

(versus less than 10% in other segments) and an improving trend in

the next 6 months (22% of the segment anticipate an increase).

Services come next, anticipating improved demand for 17% of the

segment, compared with 11% in the previous 6 months.

Construction is facing the most severe problems in demand (i.e. 70%

of construction SMEs experienced a decline and a similar trend is

likely in the next 6 months). Trade has also been hit hard, with 70%

reporting declining demand in the previous 6 months, although the

situation is expected to be a little better in the next 6 months (with

57% of the segment anticipating a further decline in demand).

* The above indices (confidence and demand)correspond to the net balance of answers onreduction/stability/increase

-50-45

-39-33

-26

-17

-60

-50

-40

-30

-20

-10

0

(0 -

0,1

]

( 0,1

-0,5

]

( 0,5

-1]

(1 -

2,5

]

(2,5

-5]

(5 -

10]

Turnover (million €)

Confidence Index by size class

-43

-56-62 -65

-17

-34

-45

-65-80

-60

-40

-20

0

Manufact. Services Trade Construction

Trend of demand by sector

Past 6 months Next 6 months (company estimate)

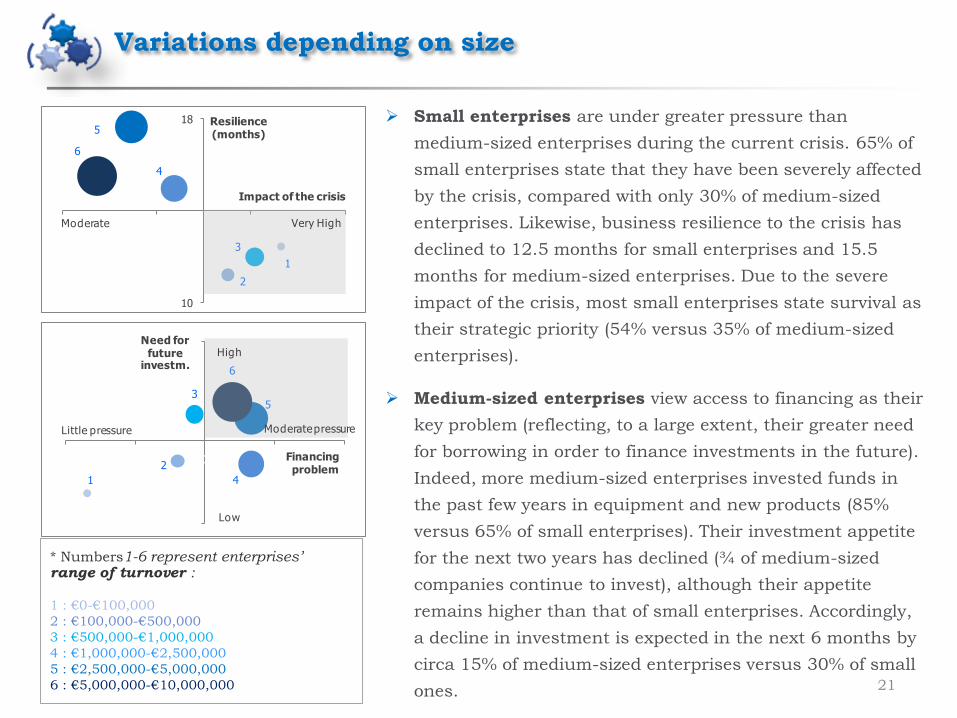

Variations depending on size

21

Small enterprises are under greater pressure than

medium-sized enterprises during the current crisis. 65% of

small enterprises state that they have been severely affected

by the crisis, compared with only 30% of medium-sized

enterprises. Likewise, business resilience to the crisis has

declined to 12.5 months for small enterprises and 15.5

months for medium-sized enterprises. Due to the severe

impact of the crisis, most small enterprises state survival as

their strategic priority (54% versus 35% of medium-sized

enterprises).

Medium-sized enterprises view access to financing as their

key problem (reflecting, to a large extent, their greater need

for borrowing in order to finance investments in the future).

Indeed, more medium-sized enterprises invested funds in

the past few years in equipment and new products (85%

versus 65% of small enterprises). Their investment appetite

for the next two years has declined (¾ of medium-sized

companies continue to invest), although their appetite

remains higher than that of small enterprises. Accordingly,

a decline in investment is expected in the next 6 months by

circa 15% of medium-sized enterprises versus 30% of small

ones.

* Numbers1-6 represent enterprises’ range of turnover :

1 : €0-€100,000

2 : €100,000-€500,000

3 : €500,000-€1,000,000

4 : €1,000,000-€2,500,000

5 : €2,500,000-€5,000,000

6 : €5,000,000-€10,000,000

1

2

35

4

6

0,6

0,9

10% 20% 30% 40% 50%

Need for future

investm.

Financing problem

Moderate pressure

Low

High

Little pressure

1

2

3

5

4

6

10

18

6,0 7,0 8,0 9,0

Resilience(months)

Impact of the crisis

Very HighModerate

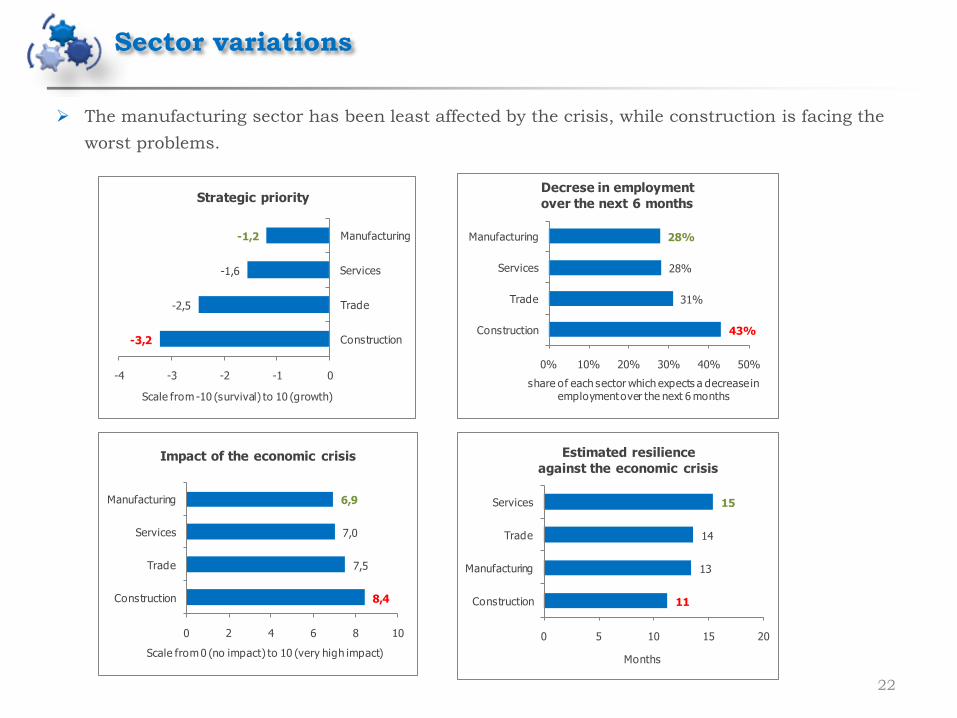

22

The manufacturing sector has been least affected by the crisis, while construction is facing the

worst problems.

Sector variations

43%

31%

28%

28%

0% 10% 20% 30% 40% 50%

Construction

Trade

Services

Manufacturing

share of each sector which expects a decrease in employment over the next 6 months

Decrese in employment

over the next 6 months

-3,2

-2,5

-1,6

-1,2

-4 -3 -2 -1 0

Construction

Trade

Services

Manufacturing

Scale from -10 (survival) to 10 (growth)

Strategic priority

8,4

7,5

7,0

6,9

0 2 4 6 8 10

Construction

Trade

Services

Manufacturing

Scale from 0 (no impact) to 10 (very high impact)

Impact of the economic crisis

11

13

14

15

0 5 10 15 20

Construction

Manufacturing

Trade

Services

Months

Estimated resilience

against the economic crisis

23

Construction is facing severe liquidity problems (with the gap between days sales outstanding

and days payable outstanding reaching 50 days), while industry has greater needs for

investment funds.

Sector variations

64%

69%

70%

76%

0% 20% 40% 60% 80% 100%

Construction

Services

Trade

Manufacturing

share of each sector which has investment needs

Investment needs

Past 5 years Next 2 years

6,9

5,9

5,8

5,6

0 2 4 6 8 10

Construction

Manufacturing

Services

Trade

Scale from 0 (no problem) to 10 (great problem)

Liquidity problem

70

58

65

54

130

102

98

87

0 50 100 150

Construction

Services

Manufacturing

Trade

Days

Days untill payment

Days sales outstanding (receivables)

Days payable outstanding (trade creditors)

5,0

5,0

4,2

4,1

0 2 4 6 8 10

Trade

Manufacturing

Construction

Services

Scale from 0 (no loan) to 10 (overleverage)

Debt problem

24

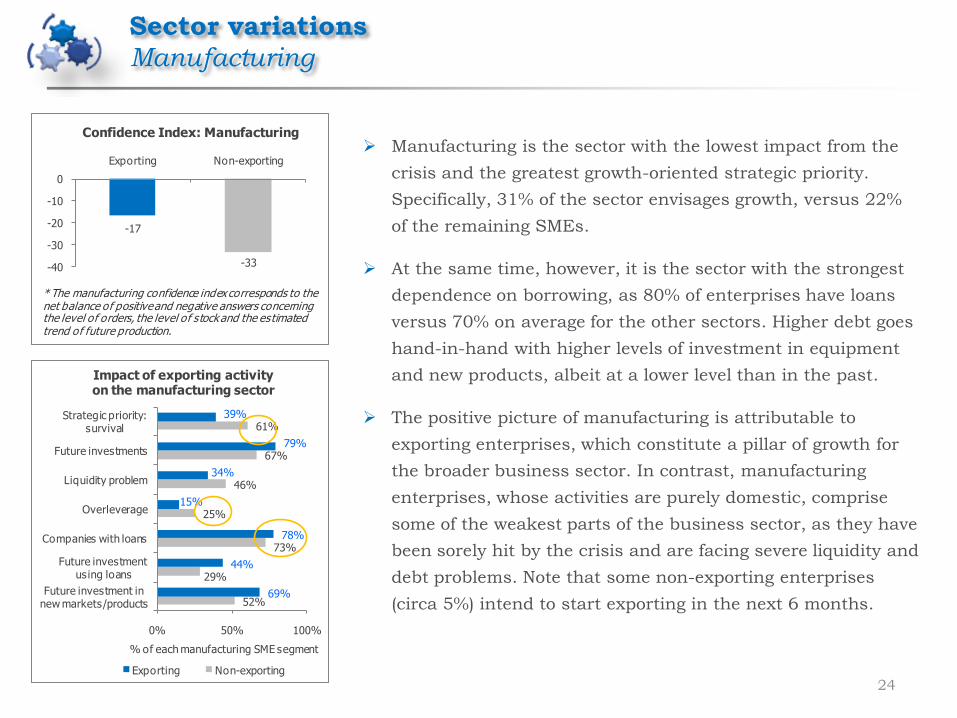

Manufacturing is the sector with the lowest impact from the

crisis and the greatest growth-oriented strategic priority.

Specifically, 31% of the sector envisages growth, versus 22%

of the remaining SMEs.

At the same time, however, it is the sector with the strongest

dependence on borrowing, as 80% of enterprises have loans

versus 70% on average for the other sectors. Higher debt goes

hand-in-hand with higher levels of investment in equipment

and new products, albeit at a lower level than in the past.

The positive picture of manufacturing is attributable to

exporting enterprises, which constitute a pillar of growth for

the broader business sector. In contrast, manufacturing

enterprises, whose activities are purely domestic, comprise

some of the weakest parts of the business sector, as they have

been sorely hit by the crisis and are facing severe liquidity and

debt problems. Note that some non-exporting enterprises

(circa 5%) intend to start exporting in the next 6 months.

Sector variations

Manufacturing

-17

-33-40

-30

-20

-10

0

Exporting Non-exporting

Confidence Index: Manufacturing

* The manufacturing confidence index corresponds to the net balance of positive and negative answers concerning the level of orders, the level of stock and the estimated trend of future production.

52%

29%

73%

25%

46%

67%

61%

69%

44%

78%

15%

34%

79%

39%

0% 50% 100%

Future investment in new markets/products

Future investment using loans

Companies with loans

Overleverage

Liquidity problem

Future investments

Strategic priority: survival

% of each manufacturing SME segment

Impact of exporting activity on the manufacturing sector

Exporting Non-exporting

25

The trade sector presents an uneven picture. To begin with, there

are three main kinds of trade: wholesale, retail, and motor

vehicles.

Wholesale traders are in a better position, as they are supported

by their export business and present the highest confidence index,

the higher resilience in the face of the crisis, and the least financial

problems. Retail trade has been hit mainly in terms of liquidity and

demand, while motor vehicle trade is in the worst position (versus

the entire business sector), its main problems being excessive debt

and low access to financing in the past year.

The relatively better position of wholesale trade is related, to some

extent, to the structural characteristics of the sector. Specifically,

Greek wholesale traders with a turnover less than €10 million:

are on average larger than small and medium retail traders

(€0.6 million versus €0.2 million) – which offers them greater

negotiating power;

account for a significant portion of the aggregate wholesale

trade segment (50% of the segment in Greece versus 30% in

Europe);

achieve higher operating profit margins than the European

average (8.5% versus 7% on average in the past 5 years).

Sector variations

Trade

-46-44

-34

-50

-40

-30

-20

-10

0

Retail Cars Wholesale

Confidence Index: Trade

* The trade confidence index corresponds to the net balance of positive and negative answers concerning the level of stock and the trend of past and future demand.

38%

25%

13%

45%

66%

67%

56%

48%

76%

44%

53%

17%

23%

37%

0% 50% 100%

Payment delays

Future investment using loans

Exporting activity

Overleverage

Liquidity problem

Future investments

Strategic priority: survival

% of each trade SME segment

Variations between trade segments

Wholesale Retail Motor vehicles

26

The service sector presents the highest resilience in the face of

the crisis (15.5 months versus 11 in construction and 13.5 in

other sectors) and the lowest level of debt (37% of the sector has

no debt whatsoever).

There are significant variations between various types of

services:

Freelancers/sole proprietors present the best picture, as

they have been least affected by the crisis. They are also the

only ones who still anticipate growth in the first half of

2012, with a focus mainly on innovative activity. Transport

also exhibits high resilience against the crisis (19 months

at the beginning of 2012). This segment is mainly

supported by its export performance. The hotel segment is

also in relatively good condition, investing mainly in

infrastructure and equipment usually backed by equity

funds.

Restaurants, however, are facing severe debt problems

(affecting 46% of restaurants versus just 12% for services

overall) and liquidity problems (affecting 60% of the

segment versus 37% for services overall).

Sector variations

Services

61%

8%

32%

46%

60%

68%

72%

96%

28%

79%

28%

0% 25% 50% 75% 100%

Exporting activity

Overleverage

Liquidity problem

Future investments

Strategic priority: survival

% of each services SME segment

Variations between services

segments

Freelancers Hotels Restaurants

Transport Other

-65

-54

-52

-34

-33

-70 -55 -40 -25 -10

Restaurants

Other

Hotels

Transport

Freelancers

Confidence Index: Services

* The services confidence index corresponds to the net balance of positive and negative answers concerning the business s ituation and the trend of past and future demand .

27

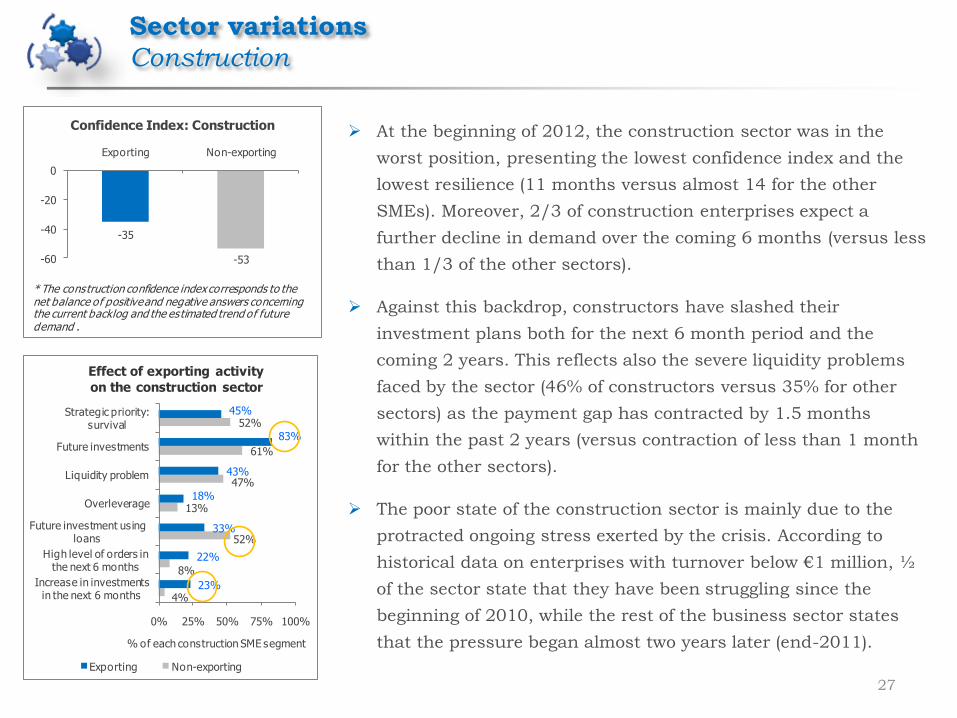

At the beginning of 2012, the construction sector was in the

worst position, presenting the lowest confidence index and the

lowest resilience (11 months versus almost 14 for the other

SMEs). Moreover, 2/3 of construction enterprises expect a

further decline in demand over the coming 6 months (versus less

than 1/3 of the other sectors).

Against this backdrop, constructors have slashed their

investment plans both for the next 6 month period and the

coming 2 years. This reflects also the severe liquidity problems

faced by the sector (46% of constructors versus 35% for other

sectors) as the payment gap has contracted by 1.5 months

within the past 2 years (versus contraction of less than 1 month

for the other sectors).

The poor state of the construction sector is mainly due to the

protracted ongoing stress exerted by the crisis. According to

historical data on enterprises with turnover below €1 million, ½

of the sector state that they have been struggling since the

beginning of 2010, while the rest of the business sector states

that the pressure began almost two years later (end-2011).

Sector variations

Construction

-35

-53-60

-40

-20

0

Exporting Non-exporting

Confidence Index: Construction

* The construction confidence index corresponds to the net balance of positive and negative answers concerning the current backlog and the estimated trend of future demand .

4%

8%

52%

13%

47%

61%

52%

23%

22%

33%

18%

43%

83%

45%

0% 25% 50% 75% 100%

Increase in investments in the next 6 months

High level of orders in the next 6 months

Future investment using loans

Overleverage

Liquidity problem

Future investments

Strategic priority: survival

% of each construction SME segment

Effect of exporting activity

on the construction sector

Exporting Non-exporting

SMEs with growth prospects

Companies with a generally healthy profile

29

Our survey confirms that the SME sector (mainly small

enterprises) has been severely hit by the ongoing crisis.

However, we should stress that 1 out of 4 SMEs stated in the

survey that they envisage growth in the years ahead.

More importantly, these enterprises generally present a healthy

profile and accordingly the growth prospects stated by these

firms reflect more than just optimism. In other words, they

present features that can support their growth prospects:

Low impact of the crisis

Limited need for crisis measures (such as employment

reduction, closing of stores and reduction of orders)

Limited liquidity problems

Small-scale payment delays

Only a slight increase in days sales outstanding

Favourable purchase terms with suppliers

Growth strategy in respect of investments, hirings,

innovative activities, and outward-looking policies for the

next 6-month period. 27%

5%

64%

3%

61%

57%

69%

50%

23%

82%

17%

28%

17%

24%

0% 25% 50% 75% 100%

Increase in innovation in the next 6 months

Increase in employment in the next 6 months

Future investments

No measure against the cris is

Payment delays (to banks or creditors)

Liquidity problem

Very high impact of the cris is

% SME segment

Characteristics of enterprises with

different strategic priorities

Growth Survival

26%11% 8%

38%

38%25%

36%51%

67%

0%

20%

40%

60%

80%

100%

Growth Stability Survival

% S

ME s

eg

ment

Demand trend estimates for enterprises with different

strategic priorities

Increase in demand for the next 6 months

Stability in demand for the next 6 months

Decrease in demand for the next 6 months

30

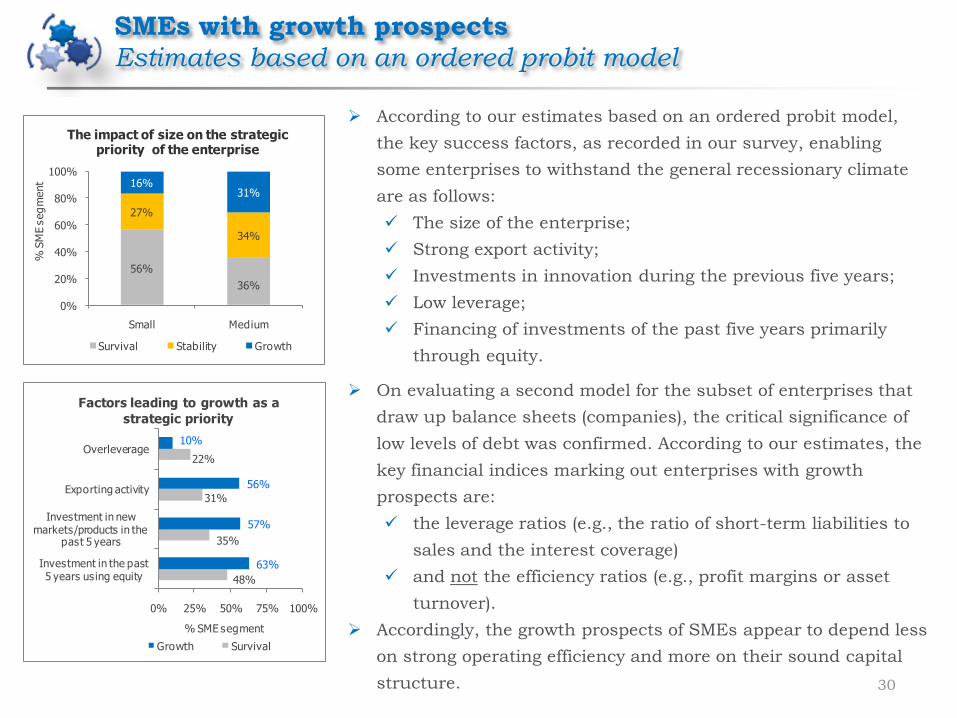

According to our estimates based on an ordered probit model,

the key success factors, as recorded in our survey, enabling

some enterprises to withstand the general recessionary climate

are as follows:

The size of the enterprise;

Strong export activity;

Investments in innovation during the previous five years;

Low leverage;

Financing of investments of the past five years primarily

through equity.

On evaluating a second model for the subset of enterprises that

draw up balance sheets (companies), the critical significance of

low levels of debt was confirmed. According to our estimates, the

key financial indices marking out enterprises with growth

prospects are:

the leverage ratios (e.g., the ratio of short-term liabilities to

sales and the interest coverage)

and not the efficiency ratios (e.g., profit margins or asset

turnover).

Accordingly, the growth prospects of SMEs appear to depend less

on strong operating efficiency and more on their sound capital

structure.

SMEs with growth prospects

Estimates based on an ordered probit model

56%

36%

27%

34%

16%31%

0%

20%

40%

60%

80%

100%

Small Medium

% S

ME s

eg

ment

The impact of size on the strategic priority of the enterprise

Survival Stability Growth

48%

35%

31%

22%

63%

57%

56%

10%

0% 25% 50% 75% 100%

Investment in the past 5 years using equity

Investment in new markets/products in the

past 5 years

Exporting activity

Overleverage

% SME segment

Factors leading to growth as a

strategic priority

Growth Survival

31

The main measures deployed by SMEs to deal with the crisis should focus on reducing their operating

costs. To this end, the following moves may provide impetus:

Organization of SMEs into broader clusters of enterprises belonging to the same business

segment or the same supply chain for a specific product. Such a strategy generates cost sharing

opportunities for marketing, research, and even basic infrastructures.

Provision of incentives for mergers with a view to gaining the necessary size for enterprises to

operate efficiently.

Second, it is crucial that liquidity in SMEs is enhanced. This may be achieved through the following:

Leveraging available EU support mechanisms (NSRF, EIB) for targeted provision of liquidity (e.g.,

to enterprises that export or promote innovation).

Creating equivalent credit tools, such as letters of credit (L/Cs) to international investment

agencies, so as to continue to import raw materials without having to pay in cash.

Last, significant assistance to SMEs could be provided by measures aimed at boosting sales, mainly

by promoting outward-looking strategies:

To focus on exports, SMEs need appropriate training, know-how and financial aid.

The development of a national export strategy could help support such firms, especially by

establishing a well-recognized and reputable national brand.

Policy directions

32

Company: TNS ICAP

Methodology: Quantitative research in the form of Computer Aided Telephone Interviewing - C.A.T.I.,

using a 20-minute structured questionnaire

Sample: A total of 960 interviews:

480 enterprises with annual turnover up to EUR 1 million (freelancers, sole proprietorships,

unlimited companies, limited partnerships, limited liability companies, SAs)

480 enterprises with annual turnover between EUR 1 million and 10 million (unlimited companies,

limited partnerships, SAs, limited liability companies)

Geographical coverage: Athens, Thessaloniki, Heraklion, Ioannina, Kavala, Larissa, Patras

Sampling: multi-stage, stratified, non-proportional sampling for sector and turnover size in each of the

two sets of samples

Statistical error: in each of the two sets of samples of 480 enterprises the maximum statistical error is

estimated at +/- 4.5% at a 95% confidence level

Period of survey: 8/3/2012 - 4/5/2012

Survey framework: The survey was carried out in line with ESOMAR and SEDEA (Association of Greek

Market and Opinion Research Companies) codes of conduct and the quality control requirements set by

PESS (Quality Control in Data Collection). A total of 48 researchers and 3 reviewers with experience

and know-how in business surveys participated in the field research.

Annex: Survey ID

Strategic Planning & Research Division

Survey of Greek SMEsJuly 2012

Analysts:

Fragiska Voumvaki

+30 210-3341549

e-mail: [email protected]

Maria Savva

+30 210-3341646

e-mail: [email protected]

Athanasia Koutouzou

+30 210-3341528

e-mail: [email protected]

This report is provided solely for the information of professional investors who are expected to make their own investment

decisions without undue reliance on its contents. Under no circumstances is it to be used or considered as an offer to sell, or a

solicitation of any offer to buy. Any data provided in this bulletin has been obtained from sources believed to be reliable.

Because of the possibility of error on the part of such sources, National Bank of Greece does not guarantee the accuracy,

timeliness or usefulness of any information. The National Bank of Greece and its affiliate companies accept no liability for any

direct or consequential loss arising from any use of this report.