Nanofilm Technologies International

17

C O N F I D E N T I AL Nanofilm Technologies International Limited Nanofilm Technologies International 1H 2021 Results Announcement 16 August 2021

Transcript of Nanofilm Technologies International

C O N F I D E N T I A L

Nanofilm Technologies International Pte LtdNanofilm Technologies International Limited

Nanofilm Technologies International1H 2021 Results Announcement

16 August 2021

Nanofilm Technologies International Limited

Results Overview1H 2021

18 18

23.7%18.5%

-50.0%

-30.0%

-10.0%

10.0%

30.0%

50.0%

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

1H 2020 1H 2021

PATMI (S$m)Margin (%)

2 | C O N F I D E N T I A L

Source: Company information(1) Adjusted EBITDA is reconciled from profit before income tax by adding back depreciation, amortization, net finance expenses, other professional fees, and other exceptional items(2) Refers to profit attributable to equity holders of the Company

PATMI –Down 3% YoY

Adjusted EBITDA –Flattish YoY

Revenue –24% YoY growth

64 76

3 2 11

19 78 97

-

20

40

60

80

100

120

140

1H 2020 1H 2021

AMBU NFBU IEBU

33 33

42.7%34.4%

-50.0%

-30.0%

-10.0%

10.0%

30.0%

50.0%

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

1H 2020 1H 2021

Adjusted EBITDA (S$m)Margin (%)

0%

(S$m) (S$m) (S$m)

(1) (2)

YoY (%) 41% 24% 63% 0% 62% -3%

1H2021 Top Line Growth Despite Supply Chain Disruptions

41 45

52.6%46.1%

-50.0%

-30.0%

-10.0%

10.0%

30.0%

50.0%

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

1H 2020 1H 2021

Gross Profit (S$m)Margin (%)

Gross Profit –9% YoY growth(S$m)

43% 9%

1H2021 growth ledby AMBU and IEBUdespite severe globalchip shortage

Partially offset bydecline in revenuefrom NFBU

Lowered margins impacted by costs totalling S$5.4m associated with newShanghai Plant 2 and equipment qualification costs, as well as higher newproduct introduction costs involving new projects yet to contributemeaningfully to revenue

Also partially impacted by product mix, where projects of lower averagemargins were executed in 1H2021

3 5 10

12 5

7 2

3 20 27

26.0% 28.3%

-

5

10

15

20

25

30

35

Total opex as % of revenue (%)

37 52

47.4%53.9%

-

10

20

30

40

50

60

70

80

90

100

D&A 2.3 3.0% 3.4 3.5%

R&D & Engineering (1) 4.6 5.9% 6.6 6.8%

Administrative (2) 10.0 12.9% 12.2 12.6%

Selling & Distribution (3) 3.3 4.2% 5.2 5.3%

3 | C O N F I D E N T I A L

Higher Expenses in Preparation for New Capacity & Peak PeriodExpenditure – Increase in % proportion to revenue primarily due to new Shanghai Plant 2, NPI(4) projects and indirect labour increases in line with business expansion plan

(in S$m)

Source: Company information(1) R&D & Engineering expense excludes Depreciation & Amortisation expenses(2) Administrative expense excludes Depreciation & Amortisation expenses(3) Selling & Distribution expense excludes R&D & Engineering and Depreciation & Amortisation expenses(4) NPI refers to New Product Introduction

1H 2020 1H 2021S$m % of revenue S$m % of revenue

Cost of Sales 37.0 47.4% 52.1 53.9%

(in S$m)

4 | C O N F I D E N T I A L

Cash conversion cycle(3)Trade payables turnover period(1)

Trade receivables turnover period(2)Inventory turnover period(1)

58 88

-

20

40

60

80

100

120

140

160

2020 1H 2021

121 97

-

20

40

60

80

100

120

140

160

2020 1H 2021

81 77

-

20

40

60

80

100

120

140

160

2020 1H 2021

144

86

-

20

40

60

80

100

120

140

160

2020 1H 2021

(in days) (in days)

(in days) (in days)

Source: Company information(1) Computed by multiplying the amount of inventories (trade payables) at the end of each period by the number of calendar days in the period and dividing the resulting figure by the cost of sales (cost of

inventories consumed and consumables used) in respect of that period(2) Computed by multiplying the amount of trade receivables at the end of each period by the number of calendar days in the period and dividing the resulting figure by the total revenue in respect of that

period(3) Sum of inventory turnover period and trade receivables turnover period less trade payables turnover period

Working Capital Changes Tracking Business Season

199 189

3 8

150

160

170

180

190

200

Total cash Current debt Non-currentdebt

Net cash

5 | C O N F I D E N T I A L

Source: Company information(1) Includes Construction-in-progress(2) Other capex spend includes office equipment, tools and supplies, and motor vehicles(3) Negative working capital denotes positive cash flows

Strong operating cash flowNet cash balance post repayment of S$40m loan as of 30 June 2021

(in S$m)

Capex spend on infrastructure and equipment paving wayfor long-term growth

(in S$m)

20 19

12 15

3 2

1H 2020 1H 2021

Equipment Land, Building & Renovation Others

30

49

(1)

(20)

4

4

1H 2020 1H 2021

Net OCF Working Capital Interest & Taxes

34

32

OCF before WC, interest

& taxes

(in S$m)

(1) (2)(1)

Strong Operating Cash Flow GenerationNet cash balance, well positioned to fund growth opportunities

(3)

Nanofilm Technologies International Limited

Segmental Information1H 2021

Source: Company information, numbers may not tie due to rounding (refer to results announcement)(1) Company also provides customised operating software, training, spare-parts, customer service and after-sales support to IEBU customers(2) Adjusted EBITDA is reconciled from profit before income tax by adding back depreciation, amortization, net finance expenses, other professional fees, and other exceptional items(3) Nanofabrication BU is a start up that was acquired in 2018(4) Based on Frost & Sullivan’s forecast of the growth in the global market size for nanoproducts to US$7.8 billion in 2023 (IMR)

7 | C O N F I D E N T I A L

Advanced Materials BU(“AMBU”)

Provides mission critical surfacesolutions based on vacuum coatingtechnologies and processes acrossmultiple industries & value chains

Nanofabrication BU(“NFBU”)(3)

Part of our value chain integrationand positions us to capture thenanoproducts (US$8bn) TAMopportunity(4)

Industrial Equipment BU(“IEBU”)

Manufactures turnkey equipmentsystems for AMBU and for sale toselected customers(1)

6476

20

30

40

50

60

70

80

90

1H 2020 1H 2021

3 2-

5

10

15

20

25

30

1H 2020 1H 2021

1119

-

5

10

15

20

25

30

35

40

45

50

1H 2020 1H 2021

Delivering Sustainable Growth Synergistic Technological Pillar Growing Order Book

29 28

45.9%37.2%

1H 2020 1H 2021

(in S$m)

(in S$m)

Rev

enue

Adju

sted

EB

ITD

A(2)

0 (1)

7.3%

-54.3%

1H 2020 1H 2021

4 6

33.8% 31.1%

1H 2020 1H 2021

Adjusted EBITDA Margin (%)

Focused on Execution to Deliver Sustainable Growth

64 76

29 28 -

10

20

30

40

50

60

70

80

90

100

1H 2020 1H 2021Revenue Adjusted EBITDA

8 | C O N F I D E N T I A L

Continuing increase in adoption of our surface solutions The increase of 18% YoY was driven by increased revenue contributions from 3C and

Automotive sub-segments Growth was still achieved despite supply chain disruptions caused by the global chip shortage 1H2021 EBITDA impacted by costs associated with equipment qualification costs incurred for

new Shanghai Plant 2, increase in NPI costs involving new projects yet to reach massproduction status and product mix changes

(in S$m)

Source: Company information

YoY growth18%

AMBU: Growth Achieved Despite Supply Chain Bottlenecks

EBITDA Margins46%

EBITDA Margins37%

Key Operating Data: AMBU

9 | C O N F I D E N T I A L

Source: Company information(1) Based on number of coating equipment at the end of the financial year/period which are utilised to fulfil revenue generating customer orders only, excludes coating equipment used for R&D activities(2) In-line coating equipment consists of several coating equipment and the capacity of an in-line coating equipment is approximately 4.5 coating equipment(3) Utilisation rate is calculated by dividing the average number of operating hours of our coating equipment and in-line coating system by the number of hours in a day (i.e. 24 hours)

Key performance indicators for AMBU

1H 2020

Equipment utilisation: Our long-term target optimal utilisation rate is ~80% with remaining un-utilizedtime catering for sufficient cycle switch between different customer projects execution, for maintenanceand unforeseen breakdowns

With the TOP of new Shanghai Plant 2 in Feb 2021, coating equipment has been progressivelyinstalled in 1H2021 and qualified in preparation for production. Given the increase in coatingequipment, the utilisation was 61% in 1H 2021, down from 73% in 1H 2020

Coating equipment (no.)(1) 122 186

In-line coating equipment (no.)(2) 4 4

Equipment utilisation (%)(3) 73% 61%

1H 2021

320

(1)(3)

(1)

1

3

5

7

9

1H 2020 1H 2021Revenue Adjusted EBITDA

NFBU: End-of-Life Project Impacted Revenue

10 | C O N F I D E N T I A L

(in S$m)

Source: Company information

48% YoY drop in the topline due to end of life of projects coupled with delay in securing new projects

Resultant negative adjusted EBITDA of S$0.9m in 1H2021

YoY drop48%

EBITDA Margins7%

EBITDA Margins-54%

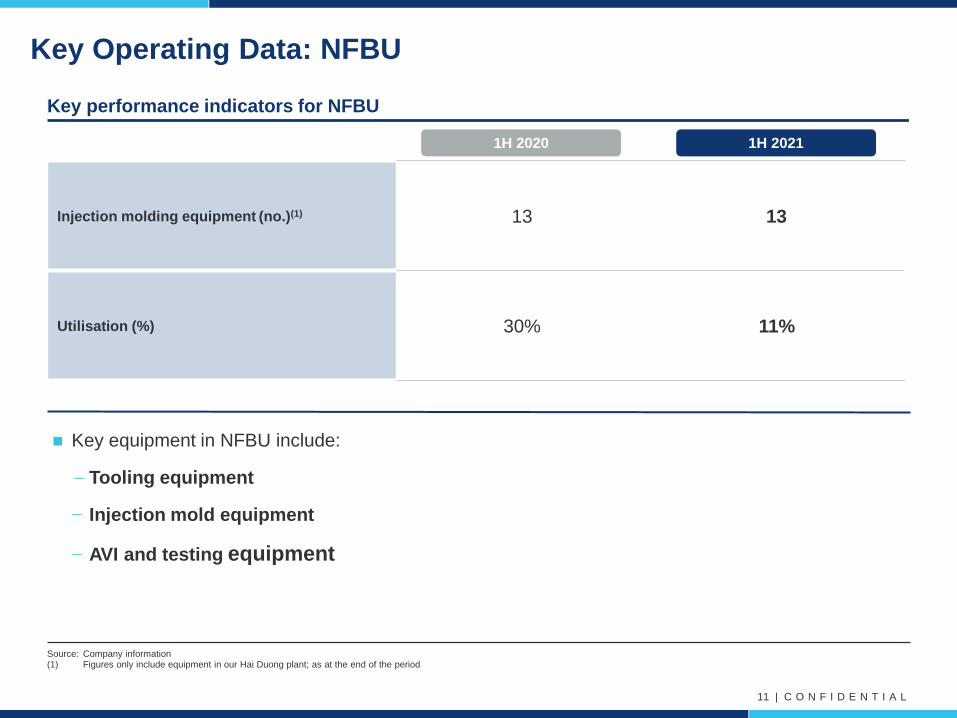

Injection molding equipment (no.)(1) 13 13

Utilisation (%) 30% 11%

11 | C O N F I D E N T I A L

Source: Company information(1) Figures only include equipment in our Hai Duong plant; as at the end of the period

Key performance indicators for NFBU

1H 2020 1H 2021

Key equipment in NFBU include:

−Tooling equipment

− Injection mold equipment

− AVI and testing equipment

Key Operating Data: NFBU

IEBU: Higher Demand with Returning & New Capex Spend from Customers

12 | C O N F I D E N T I A L

11

19

4 6-

5

10

15

20

25

30

1H 2020 1H 2021Revenue Adjusted EBITDA

(in S$m)

YoY growth came in at 81% driven by an increase in external sales of customized industrial equipmentto customers

Adjusted EBITDA of S$5.9m in 1H2021, up from S$3.5m (or 67%) in 1H2020

Source: Company information

YoY growth81%

EBITDA Margins34%

EBITDA Margins31%

13 | C O N F I D E N T I A L

Source: Company information(1) Includes in-line coating equipment, figures as at the end of the period

Key performance indicators for IEBU

In 1H 2021, IEBU continued to build for the production needs of the AMBU while the sales of coatingequipment remain selective to industries where coating services business model may not be feasible

During the period, IEBU saw an increase in external sales in line with the return of capex and newcapex spend from customers, particularly in the glass lens mold and precision engineering industries

Equipment produced (no.)(1) 23 16

Equipment sold (no.) 4 6

Equipment used internally (no.) 19 10

1H 2020 1H 2021

Key Operating Data: IEBU

Nanofilm Technologies International Limited

Outlook

Continue to increase sales to existing customers and grow

customer base

Leverage synergies across business segments to offer

customers integrated solutions

Ramp-up demonstrated share gains in new markets

Opportunistically enter new markets leveraging easily

adaptable nature of technology

Advanced Materials Market size 2023E: US$24.3bn(1)

Capturing greater share in Established End-Markets Future New Areas

Precision Engineering / HPLC Pumps / Valves

Printing and Imaging

Biomedical

3Cs

IoT Optics

Vertical & Horizontal Integration

Take-off in Recently Established End-Markets

FATP, Module / End Component New Applications• Automotive

• Fuel Cell –Sydrogen

• Optical lens

• Optical sensors

• FMCG

Automotive

Optical Lens Medical Lens & Devices

Value Chain Integration - Components TAM 2023E: US$423bn(1)

Optical Sensors

Source: Frost & Sullivan, Company Information.(1) Based on Frost & Sullivan’s forecast in its IMR

17 | C O N F I D E N T I A L

Outlook: Well-Positioned for Multiple Avenues of GrowthLeveraging Core Enabling Technologies in End-Market Applications and Value Chains of Strategic Partners to Achieve Sustainable Long-Term Growth

FMCG Personal grooming

Fuel Cell –Sydrogensuccessfully launched from Nanofilm

Nanofilm Technologies International Limited

Thank You