N-RIP stage 2

46

National Renewables Infrastructure Plan National Renewables Infrastructure Plan Stage 2 Report from Scottish Enterprise and Highlands and Islands Enterprise July 2010

Transcript of N-RIP stage 2

National Renewables Infrastructure Plan

National Renewables Infrastructure Plan Stage 2 Report from Scottish Enterprise and Highlands and Islands Enterprise

July 2010

2National Renewables Infrastructure Plan Stage 2 Report | Contents

Contents

Stage 2 Report - Executive Summary .......................................................... 3

1. Introduction .............................................................................................. 5

2. N-RIP – Industry Collaborative Approach ............................................. 6

3. Market Interest in Port Clusters/Groups .............................................. 7

4. First Phase Site Investment Cases ......................................................... 8

5. Planning Processes ............................................................................... 11

6. N-RIP Funding Approach ....................................................................... 13

7. N-RIP Total Site Capacity – Potential Economic Impact .................... 17

8. Wave and Tidal - Port Infrastructure Needs ....................................... 19

9. Conclusions and Recommendations .................................................... 24

Appendices .................................................................................................... 26

3National Renewables Infrastructure Plan Stage 2 Report | Executive Summary

Executive Summary

The purpose of the National Renewables Infrastructure Plan (N-RIP) is to support the development of a globally competitive offshore renewables industry based in Scotland. Scotland has a unique opportunity to become the home to much of this industry, from design through manufacturing, to pioneering new approaches to installation and operations and maintenance. Scotland’s key strengths are:

• Scottish based companies with expertise and skills in subsea engineering and installation borne out of years of experience of working in the North sea and globally;

• A vibrant innovation support system that is driving industry research and component development and device testing;

• A skills development infrastructure that can quickly grow the skilled workforce needed to serve this industry as it develops; and

• Existing port and harbour infrastructure that could be used and a port industry keen to engage with the

renewables sector.

The Scottish Government’s Renewables Action Plan,

published in June 2009, instigated the development

of an investment plan to support appropriate

infrastructure for the emerging offshore wind, wave

and tidal energy industries. The Energy Advisory Board,

co-chaired by the First Minister, has also tasked the

Scottish Government, through the N-RIP project, to

take an active leadership role in building a coherent

Scotland-wide proposal. The Scottish Government and

its economic development agencies are resolute in their

commitment to capitalising on these opportunities.

Offshore renewables is a significant business

opportunity for a range of organisations including

project developers, utilities, supply chain firms and port

and harbour asset owners. Private sector bodies will

have a key role to play in developing detailed investment

proposals for site developments. Scotland’s public

sector economic development bodies are already taking

a pro-active approach to working with the private sector

to make things happen and accelerate progress.

The challenge goes beyond specific site development

– it is about creating clusters of economic activity

throughout the supply chains around our key locations.

This process will require significant public sector

investment and in the current fiscal climate, it will be

critical to ensure that existing funding mechanisms are

well targeted and all efforts are made to utilise other

funding sources including United Kingdom wide and

European Union programmes. Public sector support

has already enabled vital infrastructure development

for offshore renewables as highlighted in the case

studies outlined in the report – consideration of future

investment proposals will be treated as high priority

activity.

This N-RIP report forms a key element of the Route Map that the Offshore Wind Industry Group is developing, which identifies the broad range of key steps needed to support the growth of this industry in Scotland. It is based on joint analysis by industry and government bodies of the infrastructure required to make Scotland the home for offshore renewables.

Offshore Wind - this report sets out the investment that port owners estimate they would need to make to fully develop the eleven first phase sites identified in the Stage 1 N-RIP Report for use for Offshore Wind manufacturing. This excludes the provision of buildings where these would be required. These total infrastructure costs can be approached in phases at each site.

Total investment for all sites of £223m would create a set of clustered port sites which could support an offshore wind sector manufacturing 750 complete offshore wind units a year. For Scotland’s economy the direct economic impact of this manufacturing site potential alone would support in the region of 5180 jobs and create an annual economic impact of £294.5m year on year.

4National Renewables Infrastructure Plan Stage 2 Report | Executive Summary

different stages in project developments, initially vessels undertaking environmental assessment work, and to support small scale demonstration deployments. The delivery of the Pentland Firth and Orkney Waters commercial scale leasing programme from 2016 will require development of port infrastructure proposals alongside development of the technology and deployment techniques.

The Crown Estate will shortly commission work to detail the “Build Out” story of the Pentland Firth and Orkney Waters leasing programme by November 2010 in partnership with Scottish Government, HIE (Highlands and Islands Enterprise) and Local Authorities. This will be used to help further collective understanding of opportunities and to help construct business cases for investment.

• The strategic importance of the development of the

sites for economic growth should be recognised in

the next review of the National Planning Framework.

Any support by the public sector will have to be

prioritised and the assessment of priorities for support,

if a case is shown, will be based on the impact any

development would have on supporting the growth of

the offshore wind industry in Scotland. Stage 3 of N-RIP

will consist of these discussions with individual site

owners.

Key to Government decision making, on any support to

port owners, is recognition that to secure industry use

sites will need to be ready by 2013/14 and earlier for

some users. 2014/15 is currently seen to be the key year

in which installation will begin for Round 3 and Scottish

Territorial Waters (STW) sites. Funding decisions by

Government triggered by site owners’ business cases

will recognise the importance of ensuring investment is

made early enough to secure users.

Wave and Tidal Infrastructure

The requirements of the wave and tidal industry for

port infrastructure are still evolving, reflecting the

stage of development the sector is at, with technology

and resulting deployment practices yet to achieve

standardisation. It is however clear from EMEC

(European Marine Energy Centre) and developers that

there will be a need for a range of ports to service

The Report:

• Outlines the emerging market view of groupings of port locations acting as complementary clusters with an emphasis on early opportunities on the East Coast.

• Sets out the planning and consenting processes that will be progressed in tandem with an assessment of investment approaches.

• Indicates the next steps that will be taken in considering public funding support.

Four key conclusions have been reached by the Delivery Group:

• As this industry develops there is a stock of sites in Scotland that could potentially meet industry needs for a broad range of uses. Decisions to invest will be led by the port owners.

• Based on market interest, catalytic public sector support through part funding initial investment with the private sector may be needed to make ready some sites in the right timescale for them to be used by the industry.

• That based on offshore project developer feedback and Scottish Development International’s enquiry stream most interest is being shown in sites in the Forth/Tay cluster and Moray Firth cluster at present. The sites where the interest is strongest should be the focus for initial investment.

The purpose of the National Renewables Infrastructure Plan (N-RIP) is to support the development of a globally competitive offshore renewables industry based in Scotland. Scotland has a unique opportunity to become the home to much of this industry, from design through manufacturing, to pioneering approaches to installation and operations and maintenance. Scotland’s key strengths are:

• Scottish based companies with expertise and skills in subsea engineering and installation borne out of years of experience of working in the North sea and globally;

• A vibrant innovation support system that is driving industry research and component development and device testing;

• A skills development infrastructure that can quickly grow the skilled workforce needed to serve this industry as it develops; and

• Existing port and harbour infrastructure that could be used and a port industry keen to engage with the renewables sector.

This report details progress on the actions set out in the N-RIP Stage 1 report in relation to the provision of sites at port locations for offshore wind industry use and further analysis of the need for additional locations to be developed to support the wave and tidal sector, primarily the delivery of the Pentland Firth and Orkney Waters commercial scale leasing round.

This report is the result of collaborative analysis by industry and government bodies of the infrastructure required to make Scotland the home for offshore renewables. As part of this analysis, there is recognition that the market views the sites identified in the Stage 1 report as potential regional groups or clusters. These can support complementary manufacturing and construction/installation uses, with potential operations and maintenance uses either at the same locations or other nearby locations.

For Offshore Wind industry development this report sets out:

• An estimate of infrastructure investment required at each of the identified first phase sites to make them fit to support a range of assumed uses.

• Key planning and consenting processes that will need to be completed to enable sites to be developed in a manner consistent with sustainable development.

• The scale of offshore wind supply chain manufacturing that could be supported from the development of all the first phase sites and impact of that to Scotland’s economy.

• A proposed approach for the public sector to adopt in assessing the need for public sector pump-priming investment alongside funding from the asset owner. Some triggered investment will stimulate activity, other investment will be driven by occupier location decisions.

For Wave and Tidal industry development this report sets out:

• Early assessment of infrastructure needs to support wave and tidal energy projects, with a focus on the Pentland Firth and Orkney Waters commercial scale leasing round.

5National Renewables Infrastructure Plan Stage 2 Report | Introduction

1. Introduction

6National Renewables Infrastructure Plan Stage 2 Report | N-RIP – Industry Collaborative Approach

2. N-RIP – Industry Collaborative Approach

The N-RIP process aims to establish how port owners can provide sites for offshore renewables use in the locations that the industry favours, and in a way that fits with the principles of sustainable development and the timescales for use that the industry requires.

There are two main elements to progressing the

readiness of these locations for use:

• Suitability for use - ensuring that the potential use

of the site for this industry is appropriate bearing in

mind the need to ensure sustainable development

and that the environmental impacts of the

development are considered and taken on board in

the planning and design phase of the development.

This requires each site to progress through the

range of appropriate consenting processes; and

• Asset owners making the investment required in site

infrastructure to make them ready for use.

A Strategic Environmental Assessment for the plan

has been undertaken, which will assist in the further

actions on planning and consenting. It is for site

owners to decide when to take forward their consenting

processes in accordance with their plans to move to

industry readiness. Joint working with the site owners

has enabled key investment needs for all the first phase

sites to be identified and these are set out in Section 4.

The development of N-RIP has followed a collaborative approach with a range of industry stakeholders and is an ongoing process. The ongoing role of Scottish Government and its Enterprise Agencies is to enable the supply chain, offshore renewables (wind, wave and tidal) developers and port asset owners to understand each others requirements as these evolve and change as the industry matures. Scottish Government and the wider public sector will have a key role to play as a strategic and local partner in relation to planning and consenting. In addition N-RIP recognises that in some cases there may be a role to be played from an economic growth perspective in supporting asset owner investment in infrastructure. This may be particularly necessary in the early years of industry development to ensure that the supply chain gains confidence to invest in Scotland.

This report has been prepared with support from a Delivery Group made up of industry and other stakeholders (Membership listed at Appendix 1). Their input has ensured that the conclusions set out in Section 9 reflect the current state of industry thinking. As part of the process all the leaseholders in Scottish Waters (Round 3 and Scottish Territorial Waters) have had the opportunity to express views on the potential uses and development of the sites. The responses received have informed the analysis set out in this report. In addition, discussions with wave and tidal developers successful in the Pentland Firth and Orkney Waters leasing programme have informed the wave and tidal section of the report.

An offshore wind installation workshop was held in June 2010 attended by key stakeholders including developers, port owners, installation and oil and gas contractors. From this there will be further discussions on evolving approaches to efficient installation. The N-RIP Stage 1 report indicated that operations and maintenance would require two different types of supporting port infrastructure – local support bases for regular maintenance and hub locations for specialist services which would service a broader spread of offshore wind locations. To enable Scottish engagement between ports, developers and supply chain companies about both opportunities, an Operations and Maintenance Ports Stakeholder Session will be held in September.

7National Renewables Infrastructure Plan Stage 2 Report | Market Interest in Port Clusters/Groups

3. Market Interest in Port Clusters/Groups

As the collaborative discussion between industry, ports and government has developed over the Stage 2 process, the value of viewing the sites as regional groups that can have complementary roles has become apparent. This approach is supported by emerging market interest and observations of industry practice in other locations.

Previous and current approaches to offshore wind

manufacturing and installation have followed this

cluster approach whereby one location acts as a

staging/logistics port, manufacturing is sourced from

other locations and storage can be located in a third

location.

In northern Germany the development of the Offshore

Wind industry is also seeing this complementary use

approach develop with Bremerhaven, Cuxhaven and

Emden having different elements of the offshore wind

supply chain located adjacent to their ports.

Viewing the various locations as clusters could provide

three benefits for supply chain companies:

• The cluster approach can be a lower cost option than

some of the single site options in other competing

regions - the potential for clustered manufacturing

uses to locate in a port grouping is seen as an

attractive alternative to investing in one single site

at significant cost. Although the supply chain is not

physically on one site, sea connections mean that

moving elements between sites and assembly/

installation locations is practical.

• Each cluster will have access to a range of different

local labour markets.

• Companies locating in the regional cluster, whilst

collaborating on some projects for some developers,

will have more access to load out quaysides so that

they are able to serve a wider range of customers.

To date these groupings and port uses have emerged

around local offshore wind opportunities. The existence

of, and progress on Scottish Water sites can make

these groups of locations attractive to the supply chain.

Whilst remote manufacturing is possible, companies in

the supply chain do see the benefit of locating near to an

active offshore wind market.

In Scotland locations at ports for offshore wind

manufacturing fall into three broad geographic clusters

and within these there is also potential for installation

uses and operations and maintenance:

• Forth/Tay

• Moray Firth

• West Coast

In addition a fourth, existing, subsea cluster exists

focussed on Aberdeen and Peterhead and these

locations amongst others are used by companies which

will bring expertise to offshore wind installation and operations and maintenance processes. Some offshore wind manufacturing is also thought possible in this area.

A fifth cluster of sites exists which could service the marine sector supporting the Pentland Firth and Orkney Waters commercial scale leasing round.

It is not envisaged that these will operate as closed groups – rather that concentrations of uses may develop – with components coming from locations outwith the group. What is clear however is that Scotland can offer sites in these five clusters with capacity to act as industry hot spots.

The map at Appendix 2 shows the clusters for offshore wind and also indicates the marine area involved in the Pentland Firth and Orkney Waters commercial scale leasing round.

8National Renewables Infrastructure Plan Stage 2 Report | First Phase Site Investment Cases

4. First Phase Site Investment Cases

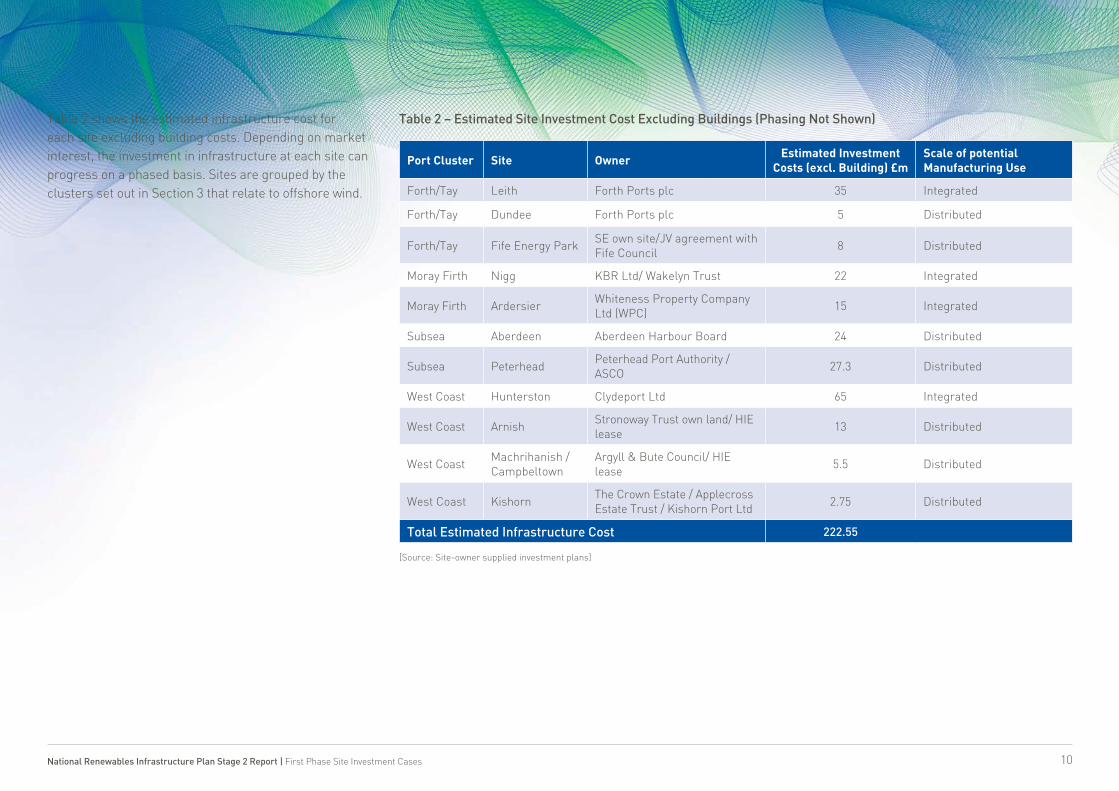

The N-RIP Stage 1 report indicated that Scottish Enterprise (SE) and Highlands and Islands Enterprise (HIE) would work with the first phase sites to identify investment in site infrastructure required to make the sites ready for use by the offshore wind supply chain. The potential of each site is set out in Appendix 3. Investment required at each site represents the site owner’s perspective on what is needed based on current industry requirements and potential uses at their location. Some locations outwith the first phase site group have also engaged with SE and HIE and have also shared their view of total investment required at their sites.

For each of the sites there is the potential for a

phased investment leading to the full development of

the site and site owners are engaging with industry

to understand the degree of market interest in their

location.

Confidence to Invest - For site owners generally, their

confidence to invest grows with increasing levels of

certainty that the offshore wind industry will move

forward on the development of offshore wind farms

under The Crown Estate’s Round 3 leases and Scottish

Territorial Water leases. For each particular site the

owners are engaging with companies in the supply

chain and gauging the level of interest in using their

port for this industry.

Although each site has different infrastructure

investment needs, the investment relates to three

generic types of expenditure that is required to make

the locations fit for their potential industry use:

Enabling Infrastructure Investment – This is

investment in a range of basic elements of the site to

make them fit for use by the offshore wind industry.

• Quayside Infrastructure - This includes creation,

renewal and strengthening of quaysides for load out

of equipment. This will be required in sites to enable

both a construction/installation use and to support

load out from manufacturing locations which are

not used for direct installation. The weight bearing

requirements and quantum of quayside required

will depend on the use and assumptions of potential

uses have been made for each site.

• Improving Water Depth at Quayside – depending

on installation or delivery vessels that are utilised

during the lifetime of the industry some of the first

phase locations may require dredging to ensure that

vessels are able to load up from the quayside.

• Land Remediation – a range of the first phase sites

require the available land to be made ready for

fabrication buildings.

• Land Reclamation – for some sites part of the

phased infrastructure development may involve the

reclamation of land to create larger areas for use.

• Demolition/Site Clearance – on some sites existing but redundant buildings will need to be cleared to enable development.

• Utilities Upgrade – dependent on use there will be a need to upgrade basic utilities to some of the sites.

• Site Access – some sites require internal access to be improved/created to enable movement within the site. In addition there is a need to ensure that those components which are not being moved by sea are able to access the site by land.

Manufacturing Facilities – some of the first phase sites have existing fabrication sheds which users may be able to occupy, however, in the main, it is assumed that new fabrication facilities will be required to meet these new specialist requirements. Different uses require different building sizes, layouts, weight bearing capacities and eaves height. Whilst there are elements of user requirements that will be bespoke to individual company processes four main facility types can be modelled:

• Jacket production facility

• Nacelle production facility

• Blade production facility

• Tower manufacture facility

9National Renewables Infrastructure Plan Stage 2 Report | First Phase Site Investment Cases

For sites identified as having the scale required for integrated manufacturing in N-RIP Stage 1 a combination of these facilities could be accommodated. For those sites identified for distributed manufacturing at least one of these uses could be housed in the location. In addition cable manufacturing facilities will be required and will have a different layout to those listed above. There is also potential for Scotland to host substation platform fabrication and monopile production at these sites.

Based on knowledge of existing buildings and costed designs of particular types of facility, a generic benchmark cost for these types of facilities is set out. This is indicative and a guide to the order of building costs envisaged. The costing relates to a shell building only. In addition, there will be a range of internal fit out costs and external site costs driven by the particular users needs. Table 1 below sets out these benchmark costs.

Table 1 - Estimated building costs.

[Source: SE Estimates of shell building costs based on indicative floor areas]

Manufacturing Building TypeIndicative Cost (shell building)

Jacket production facility £10m

Nacelle production facility £10m

Blade production facility £25m

Tower manufacture facility £10m

A range of options are available for the procurement of these new facilities – user procured, asset owner procured and third party developer procured. Each of these instances leads to different beneficiaries from the revenue streams arising from the manufacturing use.

Bespoke Equipment/Facility Requirements - The third element of infrastructure investment is to support particular users’ requirements. This relates to craneage/lifting equipment, load out quayside configuration and bespoke plant and equipment required by the particular manufacturing process – for example steel casting, gear box testing plant.

It is difficult to predict these elements at this stage as they are directly related to the user and their requirements. A range of approaches to financing these elements are available and these would be considered with any user by the asset provider.

10National Renewables Infrastructure Plan Stage 2 Report | First Phase Site Investment Cases

[Source: Site-owner supplied investment plans]

Port Cluster Site OwnerEstimated Investment

Costs (excl. Building) £mScale of potential Manufacturing Use

Forth/Tay Leith Forth Ports plc 35 Integrated

Forth/Tay Dundee Forth Ports plc 5 Distributed

Forth/Tay Fife Energy ParkSE own site/JV agreement with Fife Council

8 Distributed

Moray Firth Nigg KBR Ltd/ Wakelyn Trust 22 Integrated

Moray Firth ArdersierWhiteness Property Company Ltd (WPC)

15 Integrated

Subsea Aberdeen Aberdeen Harbour Board 24 Distributed

Subsea PeterheadPeterhead Port Authority / ASCO

27.3 Distributed

West Coast Hunterston Clydeport Ltd 65 Integrated

West Coast ArnishStronoway Trust own land/ HIE lease

13 Distributed

West CoastMachrihanish / Campbeltown

Argyll & Bute Council/ HIE lease

5.5 Distributed

West Coast KishornThe Crown Estate / Applecross Estate Trust / Kishorn Port Ltd

2.75 Distributed

Total Estimated Infrastructure Cost 222.55

Table 2 shows the estimated infrastructure cost for each site excluding building costs. Depending on market interest, the investment in infrastructure at each site can progress on a phased basis. Sites are grouped by the clusters set out in Section 3 that relate to offshore wind.

Table 2 – Estimated Site Investment Cost Excluding Buildings (Phasing Not Shown)

11National Renewables Infrastructure Plan Stage 2 Report | Planning Issues

5. Planning Processes

A key element of making sites ready for industry use is securing planning consents so that sites can be developed for occupiers to meet the timescales for supplying the industry. During Stage 2 of N-RIP development there has been ongoing engagement with planning authorities about the potential uses on the 11 sites. Asset owners have also considered the other consents that would be required and the extent to which their existing consents and permitted development rights will support the potential uses.

Planning approvals will be key milestones that will further build confidence amongst

potential users. Scotland’s planning system was recently modernised to make it best

able to support the sustainable development of Scotland’s economy in a manner

that respects responsibility to the environment. A key element, prior to approval that

gives potential occupiers confidence is an agreed timetable of milestones leading to a

planning consent decision. The N-RIP supports an ongoing strategic dialogue between

the site owners and the public sector at national and local level to progress planning

and consenting processes for sites. This will ensure that decisions about the suitability

of development of the sites for offshore manufacturing and associated uses can be

made in a timescale that meets industry needs.

For each site this timeline of planning/consenting milestones is being developed and

site owners are taking forward their discussions with planning and consenting bodies

to progress the necessary steps.

The Delivery Group view the sites identified as being of strategic importance to the

development of Scotland’s economy and conclude that this should be recognised in the

next review of the National Planning Framework.

A strategic environmental assessment (SEA) has been undertaken of the N-RIP, in accordance with the Environmental Assessment (Scotland) Act 2005. The purpose of the SEA is to identify significant environmental effects arising from the N-RIP and to consider means of mitigating such effects. An integral part of the SEA has been consultation with SNH, SEPA and Historic Scotland. The SEA has focused on the immediate and medium-term sites identified in the N-RIP Stage 1 report. The results, set out in the Environmental Report for this Stage 2 report, identify key issues which can be addressed by the N-RIP as well as providing early identification of environmental issues (and solutions) which could arise during project planning and consenting processes.

The SEA has identified key issues relating to port improvement, renewable manufacture/assembly, and operations and maintenance activities.

• A number of the sites at ports and harbours, particularly on the east coast, are adjacent to or in the environs of sites designated for their nature conservation value. These include European sites (Special Protection Area and/or Special Area of Conservation) and nationally important sites (Sites of Special Scientific Interest). In areas where these sites are present, port improvements have the potential to affect their interests. Examples include; land reclamation and/or land clearance resulting in habitat loss as a result of land take; and construction activity and noise which could result in disturbance of species.

• The SEA has assumed that quays will require strengthening, which will entail piling. This can affect biodiversity interests, for example, noise disturbance to birds; noise and vibration disturbance to cetaceans (whales, dolphins, porpoises) and migratory fish. Effects on the latter can include acoustic barriers to movement and displacement from habitat. Piling is also likely to disturb residential neighbours, where present.

12National Renewables Infrastructure Plan Stage 2 Report | Planning Issues

• Dredging will need to be considered at those ports and harbours which cannot currently accommodate vessels of the required draft. Dredging is likely to result in increased turbidity, with consequent effects on fish, light penetration and smothering of sediments. Sedimentation patterns along the coast could be affected which could affect bird feeding areas. Increased vessel movements could also affect sedimentation patterns.

Mitigation has been considered using the mitigation hierarchy of avoid, reduce, remedy and/or offset. Measures include:

• avoid land reclamation that would encroach on biodiversity interests;

• use alternative extant land where habitat losses may result from reclamation and/or land clearance;

• undertake construction work (particularly piling) at times of the year appropriate for the species in question.

Measures for the mitigation of these adverse effects will need to be integrated into port and harbour planning and design. Consultation with organisations with responsibility for the environment at an early stage of project development is key to successful mitigation of adverse effects.

These issues will be addressed through the N-RIP, as required or by the site owner as they progress their approach.

13National Renewables Infrastructure Plan Stage 2 Report | N-RIP Funding Approach

6. N-RIP Funding Approach

The investment decision for a site owner is based on their assessment of future revenues arising from the use of their site by this industry. There are a range of beneficiaries from this investment who are seen to be potential partners in the process.

For developers who hold The Crown Estate leases, investment that creates efficient installation bases can reduce installation costs and risks. Investment that attracts manufacturers will help to create a strong and innovative Scottish based supply chain which will drive down costs through design innovation and increased competition.

For manufacturing supply chain companies (turbines, towers, jackets, blades, cables), practical locations that have modern fit for purpose quayside and load out capacity are at a premium in the UK and a finite resource around the North Sea. Investment by Scottish port owners, with support from the public sector where appropriate will expand the range of potential locations.

For port and fabrication location asset owners, investment in infrastructure will facilitate the use of their facilities by the industry and thereby drive lease payments and port income. Port income will relate to installation processes where items will be brought into the quayside and then loaded out (requiring in and out handling) and manufacturing uses where there will be a load out port charge. Where ports are used for operation and maintenance there is the potential for long term port fees for regular small vessel uses and planned maintenance uses.

Asset owners and any public sector pump-priming decisions on investment will need to weigh this range of potential beneficiaries and consider how each may contribute to the investment needed and the revenue streams arising from investment. Funding support by the public sector will be focused on securing a sustainable economic impact.

14National Renewables Infrastructure Plan Stage 2 Report | N-RIP Funding Approach

Table 3 - Approach to Funding Route Map

A route map has been developed to provide clarity to all beneficiaries – port or asset owners, manufacturers, developers or operators – on the approach N-RIP is suggesting for accessing public sector support for projects. This is shown as table 3 opposite.

A critical first step for site owners is to decide that the potential use of their site for this industry is a key part of their business plan.

The route map provides a step by step process for any individual infrastructure proposal. N-RIP sites are at varying stages of this process. It gives an indication of the activities anticipated and the role that public sector key players will play – be they HIE, SE, Local Authorities or other Government bodies – as well as port and asset owners and the wider renewables investment market.

.

Development Feasibility Port owners to explore potential short, medium and long term site uses and identify the scope and indicative costs of any associated works required to enable development

t

SE/HIE/SDI engagement Initial engagement between port owner and SE/HIE to establish potential development, and identify any support that may be required from SE/HIE/SDI for engagement with the market

t

Market engagementInitial exploratory discussions with potential port users (including manufacturers and developers) to better understand the commercial options/opportunities, potentially facilitated by SE/HIE/SDI

t

Feasibility update Update feasibility assessment to reflect market discussions and establish indicative investment requirements

t

Market interest Establish clear and specific market interest (be it manufacturing, installation or O&M) and an understanding of the scale, nature and timing of the proposed infrastructure development

t

Detailed Business Plan Based on this interest/proposition, port/asset owner to develop a detailed Business Plan that clearly articulates the business proposition and investment requirements

t

Business Plan Review Public Sector review of the Business Plan to assess robustness of the proposed commercial structure and financial arrangements

t

Establish support need Establish and agree with port/asset owner the structure, level, timing and source of public sector support (if any)

Private investment Finance raised by private company on corporate or project basis

Formal submission Port/Asset owner to submit formal business plan/application for support to the appropriate public sector approver/provider

t

Support agreed Financial support arrangement agreed

Yes No

15National Renewables Infrastructure Plan Stage 2 Report | N-RIP Funding Approach

Investment Options - It is expected that finance for port infrastructure development would be raised principally by private companies either on a corporate or project basis. However as identified in the Approach to Funding route map outlined above, it is also anticipated that there may in some instances be a case for financial support from the public sector. Some of the financial delivery structures that could be envisaged for support of this kind are outlined below. Appendix 4 identifies some of the potential sources of funding and financing that could be called upon to support the projects.

Potential delivery structures - Support from the public sector can be channelled in a number of ways. Depending on the nature of the investment required, any funding gap identified and there being sufficient market interest, SE and HIE would consider a range of approaches to supporting investment. In addition partnership with Local Authorities could bring other potential approaches forward.

In general terms the approaches would include:

• Joint Venture – this could either be for a specific site or building, or a more broadly structured joint approach where there is a sharing of risk and return agreed.

• Public Financed Loan – provision of finance as a repayable loan on agreed commercial terms.

• Equity Investment – the public sector may become an equity investor on a commercial basis in an asset owner enabling investment to take place.

• Direct Investment – in some instances there might be value in a direct public sector investment that would require ownership of the asset in question. The public sector would then manage the asset in a manner that complies with state aid requirements.

• Regional Selective Assistance – this is available in certain locations and may support the investment required.

The appropriate approach will vary for different types of asset investment and will need to be suitable for the existing asset ownership structure. Risk and uncertainty in relation to revenues ensuing from the investment will also be a key factor in determining the best approach. Where any public sector support is considered it will need to comply with state aid regulations and support sustainable economic growth objectives.

Two case studies showing how Scottish Government, its economic development agencies and the wider public sector have supported the development of infrastructure and facilities that assist the development of the offshore renewables industry are set out on the following page:

16National Renewables Infrastructure Plan Stage 2 Report | N-RIP Funding Approach

Support to Jacket Manufacturer – BiFab

In spring 2010 BiFab was offered £2m of Regional Selective Assistance by Scottish Government and a £4m commercial loan from Scottish Enterprise to help finance a new Jacket production facility at Energy Park Fife, Methil.

At the same time Scottish and Southern Energy Plc (SSE) purchased a 15% stake in BiFab for a total consideration of £11m to further enhance the company’s competitiveness. In addition, SSE secured an agreement with BiFab for the supply of a minimum of 50 jacket substructures per annum commencing around 2014 for a period of 10 to 12 years. BiFab currently has around 350 employees at their Methil facilities producing 40 structures per year. It is anticipated that the company will more than treble its annual production to 130 structures a year helped by the Scottish Enterprise and SSE investment.

BiFab’s jacket production facility is located at Energy Park Fife. This location has already attracted £23m of public sector investment from Scottish Enterprise, Fife Council and the European Union to develop infrastructure on the site and support company growth.

BiFab also operates a facility at Arnish, currently employing 70 people and fabricating components and sub assemblies for the renewables sector. HIE has invested £15million in the Arnish facility over the last 10 years creating a multi-user site with a strong renewables focus.

Support to Tower Manufacturer - Campbeltown/Machrihanish

In early 2010 Welcon Towers, a subsidiary of Skykon began a £25m investment at Machrihanish backed by £9.2m of Regional Selective Assistance and £5.6m from Highlands and Islands Enterprise. The new buildings will modernise production at the plant and enable the manufacture of larger turbine tower sections for both the onshore and offshore renewables market. The investment safeguards 100 existing jobs and Skykon aims to increase the workforce to 300 over the next two years.

The Local Authority, Argyll & Bute Council with assistance from the European Regional Development Fund are making an investment of £12million in Campbeltown harbour which will facilitate the export of larger tower sections and improve the capability of Campbeltown to respond to future Operations & Maintenance opportunities.

Case Studies

17National Renewables Infrastructure Plan Stage 2 Report | N-RIP Total Site Capacity – Potential Economic Impact

7. N-RIP Offshore Wind – Potential Direct Manufacturing Economic Impact

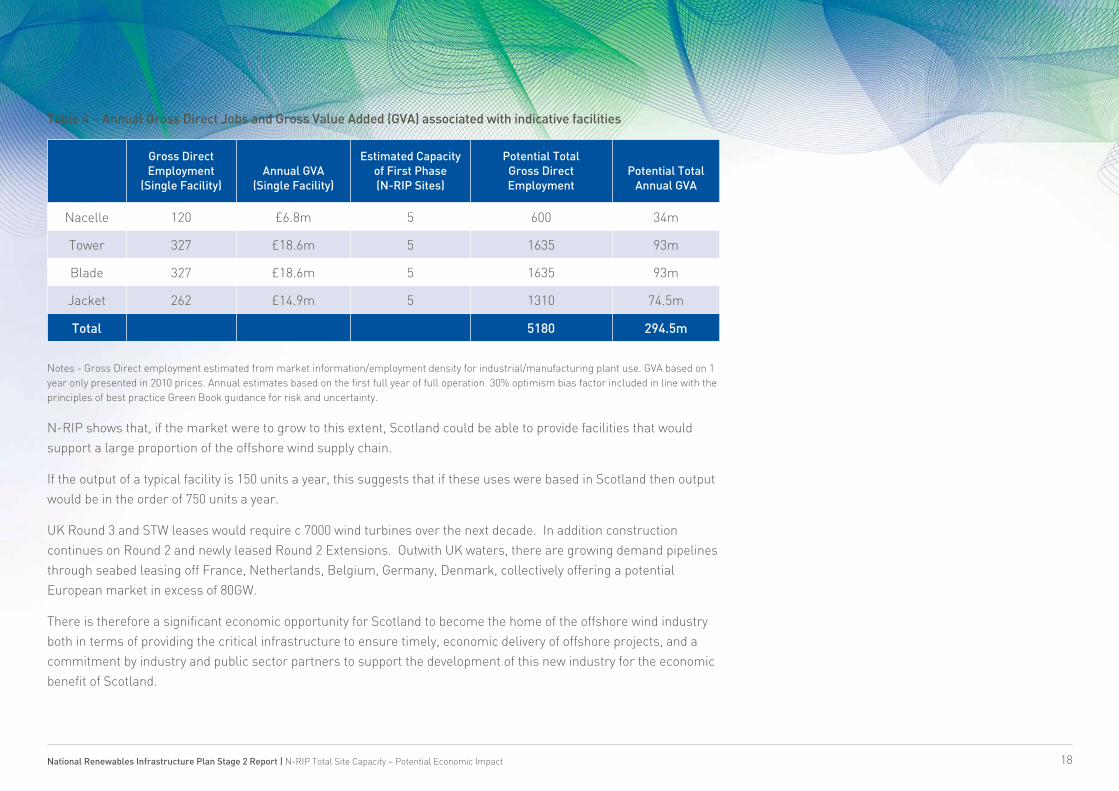

N-RIP aims to ensure that Scotland can offer a range of locations that can be developed in a sustainable fashion. To understand the scale of potential economic impact that would arise if sites are developed for manufacturing use, a high level economic impact model has been developed. This model sets out gross indicative direct manufacturing jobs only.

Alongside this, Scotland can expect to see significant additional economic impact arising from the design and development processes for offshore wind, construction/installation phases and from the associated ongoing operation and maintenance of the installed offshore wind arrays. In addition to these direct benefits and the benefits from other core aspects of the industry there will be potential significant indirect and induced benefits to other sectors such as transportation, material suppliers, service suppliers such as Health and Safety support and vessel suppliers.

As this industry is still evolving exact direct employment in each type of facility is difficult to predict. However, based on estimates derived from discussions with supply chain companies and relating this to employment densities for other similar industries it is possible to broadly estimate potential direct employment for different kinds of manufacturing use. As the industry develops, it will be possible to predict the potential impact with greater certainty. For example, some manufacturers have indicated an intention to potentially scale up production to a three shift working pattern which would lead to greater direct employment and increased annual output. This, displacement and local parameters have not been factored into the current model.

Based on the capacity of the sites it is estimated that Scotland could accommodate at least five plants for each of the following manufacturing uses – nacelle, tower, blade, jacket. Many of the sites have the potential to serve a range of uses depending on the environmental impact of these different processes. Table 4 (page 18) gives a broad estimate of the potential gross direct employment from that scale of use in Scotland.

18National Renewables Infrastructure Plan Stage 2 Report | N-RIP Total Site Capacity – Potential Economic Impact

Notes - Gross Direct employment estimated from market information/employment density for industrial/manufacturing plant use. GVA based on 1 year only presented in 2010 prices. Annual estimates based on the first full year of full operation. 30% optimism bias factor included in line with the principles of best practice Green Book guidance for risk and uncertainty.

N-RIP shows that, if the market were to grow to this extent, Scotland could be able to provide facilities that would support a large proportion of the offshore wind supply chain.

If the output of a typical facility is 150 units a year, this suggests that if these uses were based in Scotland then output would be in the order of 750 units a year.

UK Round 3 and STW leases would require c 7000 wind turbines over the next decade. In addition construction continues on Round 2 and newly leased Round 2 Extensions. Outwith UK waters, there are growing demand pipelines through seabed leasing off France, Netherlands, Belgium, Germany, Denmark, collectively offering a potential European market in excess of 80GW.

There is therefore a significant economic opportunity for Scotland to become the home of the offshore wind industry both in terms of providing the critical infrastructure to ensure timely, economic delivery of offshore projects, and a commitment by industry and public sector partners to support the development of this new industry for the economic benefit of Scotland.

Gross Direct Employment

(Single Facility)Annual GVA

(Single Facility)

Estimated Capacity of First Phase (N-RIP Sites)

Potential Total Gross Direct Employment

Potential Total Annual GVA

Nacelle 120 £6.8m 5 600 34m

Tower 327 £18.6m 5 1635 93m

Blade 327 £18.6m 5 1635 93m

Jacket 262 £14.9m 5 1310 74.5m

Total 5180 294.5m

Table 4 – Annual Gross Direct Jobs and Gross Value Added (GVA) associated with indicative facilities

19National Renewables Infrastructure Plan Stage 2 Report | Wave and Tidal - Port Infrastructure Needs

8. Wave and Tidal - Port Infrastructure Needs

Scotland’s lead in the development of the wave and tidal energy sector is demonstrated by the establishment of the European Marine Energy Centre in Orkney, the only grid connected, UKAS accredited, wave and tidal test facility in the world for fullscale testing, combined with arguably the best financial support in the world with enhanced Renewables Obligations Certificates (ROCs) (5 ROCs for Wave and 3 ROCs for Tidal), capital investment in R&D demonstrated by the recent WATERS £13million awards and the £10million Saltire Prize. This activity and encouraging environment has lead to the world’s first commercial scale leasing round and the development of a new consenting regime, with Marine Scotland to enable it.

In comparison with the offshore wind sector, the wave and tidal energy sector is, however, in the early stages of development. At present, there are a number of prototype devices being tested to move towards proving that marine energy converters can produce electricity at a competitive rate.

As part of N-RIP Stage 2, further consultations were undertaken, following Round 1 lease option awards in the Pentland Firth and Orkney waters and building on those undertaken by HIE in November and December 2009. A list of those consulted is attached as Appendix 5. Any assumptions made at this point in time are likely to be subject to considerable change as the technology and sector develops over the next five years.

As indicated in the N-RIP Stage 1 Report any infrastructure to support the Pentland Firth and Orkney Waters leasing area is the most immediate need. Other lease option awards for the Saltire Prize and any other future leasing rounds would need analysis when locations for these become clear. Currently there is a leasing process underway for a site in the Inner Sound in the Pentland Firth. Award of this site is expected later in 2010. The areas currently with options for lease for development are highlighted in Figure 1 on the next page.

20National Renewables Infrastructure Plan Stage 2 Report | Wave and Tidal - Port Infrastructure Needs

Figure 1: Map of development sites under the Pentland Firth and Orkney Waters Leasing Round

21National Renewables Infrastructure Plan Stage 2 Report | Wave and Tidal - Port Infrastructure Needs

For the purposes of this report the time periods have been divided into three periods:

• 2010-2015 – immediate needs being for deployment of devices at EMEC and other testing facilities, before moving on to the deployment of small scale arrays, both at sites identified under the Pentland Firth and Orkney Waters leasing round, as well as any other future leasing rounds, and at other locations identified by developers themselves. Up to 50MW is planned for deployment on known sites, including those in the Pentland Firth and Orkney Waters leasing area in this initial five years period, the bulk of this likely in 2015.

• 2016-2020 – assuming the continuing progression of technology development and subject to the necessary grid infrastructure being in place, the industry should be moving towards deployment of arrays of over ten devices using established installation techniques. 1,150MW (plus the Inner Sound, anticipated to be 200MW to 500MW) is planned on known sites during this period, primarily in the Pentland Firth and Orkney Waters leasing area. Further the Saltire Prize is aimed to incentivise at least two years commercial production of electricity from wave and tidal technologies by June 2017.

• 2020 onwards – operations and maintenance of installed devices.

Figure 2 below illustrates the aggregate installation proposed under lease agreements for the Pentland Firth and Orkney Waters leasing round. These dates for capacity installation are the deadlines under lease agreements and so deployment will potentially anticipate this schedule.

Figure 2 – Wave and Tidal Build Out Timescales

22National Renewables Infrastructure Plan Stage 2 Report | Wave and Tidal - Port Infrastructure Needs

From developer discussions consideration has been given to the infrastructure needs at these stages:

2010 – 2015: Short-term activity

EMEC sites

Deployment at EMEC will accelerate over the next two years with ten devices due to be installed. Existing sites are being expanded and two “nursery” sites being developed. Demand from developers for increased shoreside facilities and light industrial capabilities in support of R&D activity is currently being addressed with the development at Hatston, and proposals for development on land at Lyness.

The Pentland Firth and Orkney Waters Leasing Round sites

Developer discussions have focused on specific requirements for survey work and installation of small arrays, and have highlighted following observations:

Survey work

• Type of vessels that may be used for this work are multi-cats (20metres in length) and small workboats (10metres in length)

• Volume of Activity: developers’ timelines show survey activity for at least two seasons per site.

• Location: Stromness is likely to be used for the largest number of sites given sailing times and specialist workforce location. Hatston and Kirkwall Harbours could also be used for northerly sites, and Scrabster Harbour and Gills Bay providing mainland facilities for the Pentland Firth. Wick is already hosting survey work boats for offshore wind, and depending on which companies win the Environmental Impact Assessment contracts, White Head (Loch Eriboll) may be used.

Installation of small arrays

• Cable laying activities will continue to be serviced out of existing facilities at this small volume.

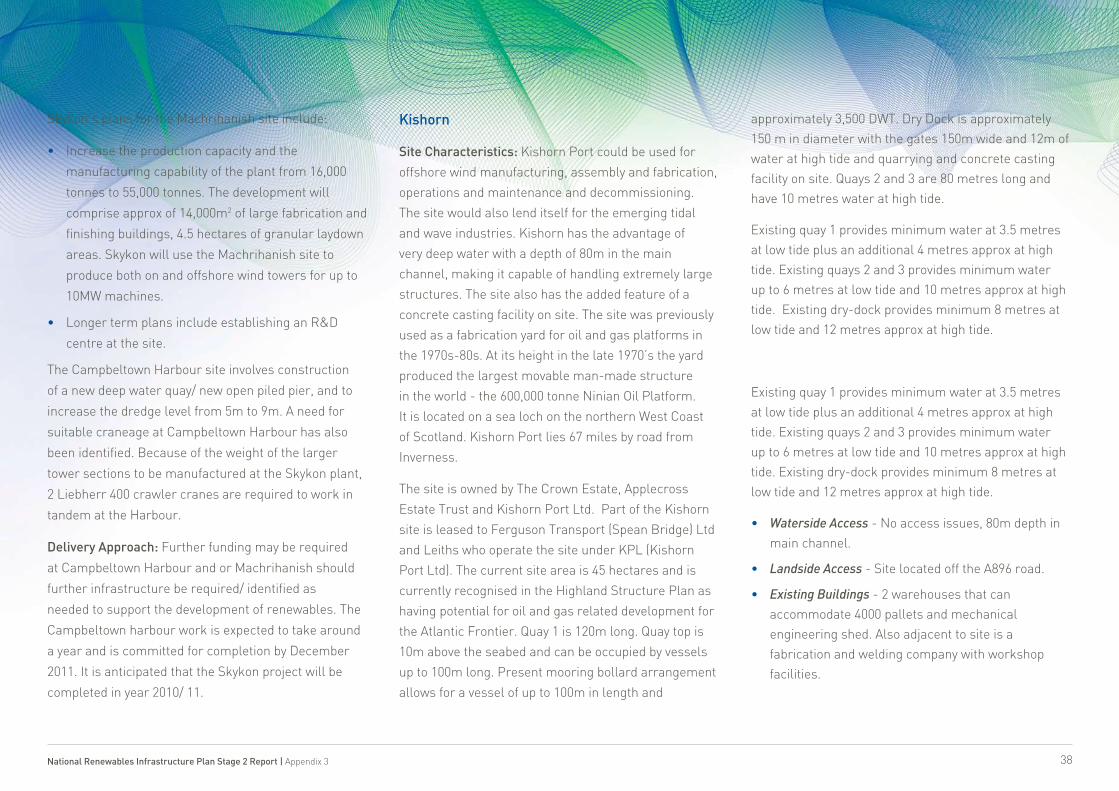

• Devices: there are three methods of installation used, influenced to some extent by the port facilities available as well as by the type of device.

– The Pontoon and small quay model - where the device is towed from the fabrication site to a deployment site with wet storage and then using pontoons for final adjustments.

– Quayside and cranes model - devices are delivered on a vessel to a quayside for assembly and adjustments, and deployed from the quay.

– Deployment direct from the fabrication site onto a vessel.

To ensure that port infrastructure is not a constraint on the development of this industry during its test and demonstration phase dialogue will continue with lease holders as they develop their technology and deployment methods.

2016-2020 – Medium term activity

Beyond five years the volume proposed to be deployed rises sharply with considerable associated port infrastructure required. The exact specifications for that infrastructure are not yet established but will be clarified as the technology progresses and financial commitments to grid infrastructure, device manufacture and support vessels are made.

2020 onwards – Long term activity

Operation and maintenance facilities will, for economic and operation reasons, need to be provided near the deployment sites with four hours sailing being given as the ideal maximum by some developers. A three to five year maintenance cycle is envisaged by most of the developers consulted which will create requirements over decades for the port facilities to service this. Further it is expected that additional leasing rounds will be in construction phase.

23National Renewables Infrastructure Plan Stage 2 Report | Wave and Tidal - Port Infrastructure Needs

Planned port developments to support Medium and Longer Term Activity

All ports in both Caithness and Orkney that could host or are already hosting deployment activity have development plans with at least guideline costs for expansion of existing facilities. Lead times vary, but three years to delivery, including obtaining planning permissions and financing should be allowed for, and hence developer input on requirements for larger scale deployments scheduled from 2017 onwards will need to be determined by 2012-2013 at the latest and work needs to begin by 2014 at the latest.

Therefore, some decisions on port development and use may have to be made before there is any specific certainty in the market in order to meet the deployment timetables as they are currently planned.

Providing deepwater quay space and cranes at deployment sites will increase the number of technologies that will be successfully able to deploy, to include those that have not designed around minimal infrastructure.

Quay space and cranes at deployment sites could enable manufacture and fabrication to happen further afield from the lease sites as devices can be transported over a greater distance by barge than wet towing. Moving on from this, delivery to deployment sites in batches will create a greater need for laydown areas at both fabrication and deployment sites.

The N-RIP Stage 2 analysis indicates that a range of locations could support wave and tidal installation, fabrication and ongoing operations and maintenance. There will in time be a need for locations to support these uses, both in the initial Pentland Firth and Orkney Waters leasing area, and other areas that may be leased in future around the Scottish coast. These potential locations are shown in Appendix 6.

Under the auspices of the Pentland Firth and Orkney Waters Delivery Group, comprising The Crown Estate, the Scottish Government, HIE, Local Authorities and the developers, work to refine these locations and investment opportunities will be undertaken as developer requirements become clear in the next phase of work.

24National Renewables Infrastructure Plan Stage 2 Report | Conclusions and Recommendations

9. Conclusions and Recommendations

Scotland has a unique opportunity to become the home to much of the offshore renewables industry, from design through manufacturing, to pioneering new approaches to installation and operations and maintenance.

Scotland’s key strengths are;

• Scottish based companies with expertise and skills in subsea engineering and installation borne out of years of experience of working in the North sea and globally;

• A vibrant innovation support system that is driving industry research and component development and device testing;

• A skills development infrastructure that can quickly grow the skilled workforce needed to serve this industry as it develops; and

• Existing port and harbour infrastructure that could be used and a port industry keen to engage with the renewables sector.

The Scottish Government and its economic development agencies are resolute in their commitment to capitalising on these opportunities. Public sector support has already enabled vital infrastructure development for offshore renewables as highlighted in the case studies outlined in the report – consideration of future investment proposals will be treated as high priority activity.

This N-RIP report forms a key element of the Route Map that the Offshore Wind Industry Group is developing which identifies the broad range of key steps that are needed to ensure the growth of this industry in Scotland. It is based on joint analysis by industry and government bodies of the infrastructure required to make Scotland the home for offshore renewables.

Four key conclusions have been reached by the Delivery Group on offshore wind;

• As this industry develops there is a stock of sites in Scotland that could potentially meet industry needs for a broad range of uses. Decisions to invest will be led by the port owners.

• Based on market interest, catalytic public sector support through part funding initial investment with the private sector may be needed to make ready some sites in the right timescale for them to be used by the industry.

• That based on offshore project developer feedback and Scottish Development International’s enquiry stream most interest is being shown in sites in the Forth/Tay cluster and Moray Firth cluster at present. The sites where the interest is strongest should be the focus for initial investment.

• The strategic importance of the development of the sites for economic growth should be recognised in the next review of the National Planning Framework.

Total investment for all sites of £223m would create a set of clustered port sites which could support an offshore wind sector manufacturing 750 complete offshore wind units a year. For Scotland’s economy the gross direct economic impact of this manufacturing site potential alone would support in the region of 5180 jobs and create an annual economic impact of £294.5m year on year.

Any support by the public sector will have to be prioritised and the assessment of priorities for support if a case is shown will be based on the impact any development would have on supporting the growth of the Offshore Wind industry in Scotland.

Key to government decision making, on any support to port owners, is recognition that to secure industry use sites will need to be ready by 2013/14 and earlier for some users. 2014/15 is currently seen to be the key year in which installation will begin for Round 3 and STW sites. Funding decisions by Government triggered by site owners’ business cases will recognise the importance of ensuring investment is made early enough to secure users.

25National Renewables Infrastructure Plan Stage 2 Report | Conclusions and Recommendations

Wave and Tidal Infrastructure

The report concludes that there will be a need for investment by port owners in various locations to make sites ready for this industry in the future. The specifics of the port infrastructure required in the medium term for large scale deployment will be developed by the Pentland Firth and Orkney Waters Delivery Group with knowledge from the port sector and proposals for potential port development informing the development of deployment and operations and maintenance plans. SDI will continue to market the investment potential of port facilities servicing this sector.

The Crown Estate will shortly commission work to detail the “Build Out” story of the Pentland Firth and Orkney Waters leasing programme by November 2010 in partnership with Scottish Government, HIE and Local Authorities. This will be used to help further collective understanding of opportunities and to help construct business cases for investment.

26

Appendices

Appendix 1............................................N-RIP Delivery Group Membership

Appendix 2 .................................................................Port Cluster Mapping

Appendix 3..........................................N-RIP First Phase Sites Information

Appendix 4..................................................................... Sources of Finance

Appendix 5.................................. Wave and Tidal Stage 2 Consultation List

Appendix 6 ............................................Wave and Tidal potential locations

National Renewables Infrastructure Plan Stage 2 Report | Appendices

27National Renewables Infrastructure Plan Stage 2 Report | Appendix 1

Appendix 1 - N-RIP Delivery Group Membership

Paul Lewis (co-chair) ..........................................................................................Scottish Enterprise

Andrew Jamieson (co-chair) .....................................Scottish Renewables Forum/Scottish Power

Allan MacAskill ...............................................................................................SeaEnergy Renewables

Colin Hood (Andrew Donaldson) ...................................................... Scottish and Southern Energy

Keith Anderson (Jason Martin) ............................................................ Scottish Power Renewables

Colin Parker .................................................................................................Aberdeen Harbour Board

Euan Jamieson ......................................................................................................................Clydeport

Alan Burns .........................................................................................................................Forth Ports

Alasdair Rankin ....................................................................................................... The Crown Estate

Mike Kydd .......................................................................... (chair) North Scotland Industries Group

Robin Presswood ........(chair) Scottish Local Authorities Economic Development Group/(SLAED)

Rod Johnstone .............................................................................................Scrabster Harbour Trust

Calum Davidson .............................................................................Highlands and Islands Enterprise

Audrey MacIver..............................................................................Highlands and Islands Enterprise

Tom Lamb ...................................................................................Scottish Development International

Colin Grant ....................................................................................Highlands and Islands Enterprise

Tony Rose ..........................................................................................................Scottish Futures Trust

Jamie Hume .................................................................................................The Scottish Government

Alex Reid ......................................................................................................The Scottish Government

Adrian Gillespie ....................................................................................................Scottish Enterprise

Euan Dobson .........................................................................................................Scottish Enterprise

28National Renewables Infrastructure Plan Stage 2 Report | Appendix 2

Appendix 2 - Port Cluster Mapping

29National Renewables Infrastructure Plan Stage 2 Report | Appendix 3

Appendix 3 - N-RIP First Phase Sites Information

FORTH/ TAY CLUSTER

Leith

Site Characteristics: Leith is a strong location for large scale manufacturing, installation activities and operations and maintenance for the renewables industry. The port is owned and operated by Forth Ports PLC. In total Leith Docks comprises a total water area of 100 hectares and a total land area of 158 hectares. The current masterplan designates 150 acres for renewable activities. Additional land may be available within the docks and offsite at adjoining industrial areas.

• Waterside Access - There is an impounded dock with water depths of 9.75m – 7.20m depending on berths. Entrance to port is via a lock which is 259m long and 31.6m wide between floating fenders and depth over outer sill at MHWS 12.293m. Forth Ports are assessing requirements going forward to construct an outer tidal berth with heavy lift capacity.

• Landside Access - Leith Docks is on the southern shore of the Forth Estuary downstream of the Forth Bridges on the northern boundary of Edinburgh. Transport connections are good with road access to A1, M8 and M9, rail connected to main East Coast line via sidings and Edinburgh Airport is 12km from port.

• Existing Buildings - A range of existing industrial buildings may be available.

• Quayside Length/Weight Bearing - Minimum of 1800m of quaysides available all with heavy lift capability

• Planning - Port facility carries permitted development powers for certain port related uses.

Potential Offshore Renewables Infrastructure Role: Leith can support large scale manufacturing, installation activities and operations and maintenance

Market Use and Interest: The port currently supports a wide range of shipping activities including offshore oil and gas support. Leith is also home for research, development and manufacture of the Pelamis wave to energy marine device. A biomass powered electrical and thermal generating plant is proposed and is progressing through a consent process.

Infrastructure Development Requirement: Facilities to client’s specification can be put in place. Base industrial and marine assets with exception of proposed outer berth already exist.

Delivery Approach: Making the site ready, depending on client requirements and scale and complexity of facility would take between12-36 months. Outer berth development has a 36-month lead-time. Feasibility studies are ongoing.

Dundee

Site Characteristics: The Port of Dundee currently

offers 60 acres of development land for the renewables

sector, all in the ownership of Forth Ports. If there was

a need there may be potential to extend this through

the reclamation of additional land at the east end of

the existing Port boundary (c 20 acres). Outwith the

port estate, two principal sites have been identified

to support Renewables development in the city –

Claverhouse and Linlathen, both owned by Dundee City

Council and within 3 miles of the port, offer 140 and 240

acres available for immediate development. There is

also a number of private sector owned sites within the

area.

• Waterside Access - The port offers around 1800m of

quayside in a sheltered riverside location with access

to the North Sea unrestricted by either air draft or

vessel width. The water depth along the quay is up

to 9.5m, with a range of quayside load capacities

up to 7 Te/m². The port also offers a full range of

commercial port services including cargo handling

and quayside craneage.

• Landside Access - Improvements are underway with

the construction of a road bridge and reconfigured

road layout at Stannergate providing direct abnormal

load access to Scotland’s trunk road network in

2011. There is also the potential for a rail freight

terminal within the port estate.

30National Renewables Infrastructure Plan Stage 2 Report | Appendix 3

• Existing Buildings - There are a number of existing industrial buildings within the port available for use, along with a range of warehouse, office and open storage areas.

• Planning - Port facility carries permitted development powers for certain port related uses. A supportive approach from local planners exists. The feasibility of the future potential land reclamation extension of the port is under consideration.

Potential Offshore Renewables Infrastructure Role: There is potential for a major turbine manufacturing facility and a tower manufacturing facility to co-locate on the site, with capacity for a number of supply chain operations within the existing site. A detailed developer requirement for an Operation and Maintenance facility has been incorporated into the planning of the site.

Market Use and Interest: The Port of Dundee is a strong regional port handling a wide range of bulk agricultural and forest products and providing servicing and supply to the oil and gas industry. The port currently hosts a refinery and various fabrication and engineering uses, with a proposed Biomass generation facility currently progressing consent with a potential operational date of 2014.

An extensive range of interests from the renewables sector have been received for the port including turbine manufacture, tower manufacture and operations and maintenance.

Infrastructure Development Requirement: As the

port enjoys the benefits of being a fully commercially

operating facility, the principal infrastructure

requirements are specific to the particular

requirements of occupiers. While the detail varies to a

degree, the requirements principally relates to large

scale bespoke industrial buildings with associated load

out areas and appropriate land storage.

The potential expansion of the port estate through

land reclamation is a further potential future phase

dependent on demand.

Delivery Approach: Indicative costings for large end

user buildings and load out areas have been formulated

and can be adapted depending on the specifics of the

operation. The co-location of two such facilities on the

port has been identified as technically and commercially

feasible. Supply chain opportunities could potentially

utilise existing buildings on the port.

Costs for the land reclamation have not yet been

finalised, and will be dependent on opportunity cost

of available, suitable fill material and consenting

processes.

Development on the existing port estate is not likely to

be subject to any abnormal milestones. The specific

requirement for planning consent or utilisation of

permitted development powers will be determined

based on the specifics of proposed development. The

design and construction of any facility is not considered

overly complex, and the implementation is deliverable

within twelve months of a decision, subject to lead times

remaining broadly as current.

Energy Park, Fife/Methil

Site Characteristics: Energy Park, Fife at Methil can

accommodate a range of offshore renewables supply

chain companies. BiFab is already located in Energy

Park Fife and is a major player in the manufacturing

of jackets for offshore wind turbines. Located on the

former Kvaerner oil fabrication yard at Methil, the 54

hectare Energy Park is a joint venture between Scottish

Enterprise and Fife Council. The site has two quaysides

extending to a total of 340m and is adjacent to Methil

Harbour owned and operated by Forth Ports as well as

the Methil Docks Business Park, together creating the

larger Fife Energy Zone. There is also the opportunity

for additional off-site land, in close proximity to the

quayside.

SE owns the site but there is a joint venture agreement

with Fife Council. Currently c 14 hectares of land is

available on site. Land reclamation is a possibility but

this has still to be investigated in detail. Further land

exists at Methil Docks Business Park, Forth Ports land

at Methil and in other nearby Strategic Land Allocations.

31National Renewables Infrastructure Plan Stage 2 Report | Appendix 3

• Waterside Access - Energy Park - Quayside 1: -9.0m OD (planned), Quayside 2: -9.0m OD (planned). Some weather/tidal restrictions on quayside use during winter.

• Landside Access - common user access to quayside.

• Existing Buildings - On site there is existing 32,000 sqft building (owned by DSNL) of which c9,000 sqft is let. BiFab currently occupies 290,000 sqft of accommodation on site made up of three fabrication buildings, a paint/blast shed and storage buildings.

• Quayside Length/Weight Bearing - Quay 1 – length 180 m, Quay 2 – length 160 m. 200kN/sqm or patch loads of up to 600 kN/sqm can be accommodated.

• Planning - Currently classed under MET 16 of the Draft Mid-Fife Local Plan which states that it is to be used for renewable energy assembly, fabrication and research & development.

Potential Offshore Renewables Infrastructure Role: BiFab are a major player in the manufacturing of jackets for offshore wind turbines. It is anticipated that the remaining site(s) will go to companies in the supply chain.

Market Use and Interest: Interest to date from the remaining site(s) has come predominantly for supply chain companies that would have a complementary use to existing BiFab use. For some interests looking for manufacturing sites the remaining space has to date been deemed too small.

Infrastructure Development Requirement: Scottish Enterprise with Fife Council support is currently progressing quayside repairs/upgrades, new mooring facilities to accommodate multiple users and development of the site to support BiFab expansion.

Delivery Approach: Scottish Enterprise is progressing investment in the site at present and dependent on market interest there is the potential to extend the developable site area through creating a new level area by removal of the bing at the west side of the site. Within the wider Methil area there is the potential to develop other sites and Scottish Enterprise with Fife Council and Forth Ports are developing a strategic approach to the growth of a Fife Energy Zone focussed at Methil.

MORAY FIRTH CLUSTER

Nigg

Site Characteristics: Nigg is a 96.14 Hectare (238 acre) facility, formerly a fabrication yard, with 4.35 Ha. dry dock, large fabrication/warehouse buildings, 725 m of quayside with load-out areas up to 1000 tonnes and draught up to 9.5m. Strategically placed on the Moray Firth and accessible 24/7 at all states of wind and tide. Extensive deep water, sheltered anchorage and diverse local support facilities. Further adjacent development land of 240 Ha exists. 26.99 Ha. of the site is an oil terminal facility currently leased to Ithaca Ltd. Tankers of up to 160,000 tonnes dwt. can be handled at the jetty.

The majority of the site is owned by KBR Ltd, with the dock and load-out area leased to KBR until 2031 by the Wakelyn Trust. Adjacent is the undeveloped “Cromarty Petroleum” site, some 240 Ha. DSM has recently purchased this land from Dow Chemicals.

Quayside totals 725 m, water depths from 4.5 to 9.5 metres LAT, up to 13.7 metres MHWS. Load out pad can take up to 1,000 tonnes.

• Waterside Access - Access to dry dock via slipway

• Existing Buildings - Buildings currently on site comprise:- Fabrication - 17,000 m²; Assembly 17,000 m²; Warehousing 22,000 m².

• Planning Status - current planning status allows use as a fabrication yard. The Development Masterplan adopted by The Highland Council in November 2009 as supplementary planning guidance envisages use as a multi-user site for fabrication, renewable energy device manufacture and petrochemical structure decommissioning. Included in the Development Masterplan is the adjacent “Cromarty Petroleum” site.

Potential Renewables Infrastructure Role: The Nigg site is suitable for integrated manufacturing on a large scale, particularly if the proximal site is brought into use. Invergordon, approximately 10 miles away by road, 5 miles by sea, has a comprehensive and well-established engineering supply chain, developed to service the offshore petrochemicals industry.

32National Renewables Infrastructure Plan Stage 2 Report | Appendix 3

This includes fabrication facilities, towage, stevedoring, craneage, haulage, etc, centred around excellent port facilities supporting a substantial oil rig IRM business.

Market Use & Interest: The Nigg Yard is mainly on a care and maintenance basis at present. A limited amount of fabrication work, mostly subsea structures, is being undertaken. The turbines for the Beatrice offshore wind project were assembled and loaded out from Nigg.

Extensive interest has been expressed in using the Nigg Yard for renewables manufacture, and a proposal by the yard’s current owners KBR to use it for monopile and jacket manufacture was being developed for evaluation by the parent company, but they have now decided not to go ahead with this. The Development Masterplan envisages the yard being developed as a multi-user site, with a variety of engineering activities to support a spread of industries, including renewables.