Mutual Funds in India - Building a better working world - …(Mutual Funds in India: Being future...

48

Mutual Funds in India Being future ready September 2015

Transcript of Mutual Funds in India - Building a better working world - …(Mutual Funds in India: Being future...

Mutual Funds in India

Being future ready

September 2015

2 | Mutual Funds in India: Being future ready

3Mutual Funds in India: Being future ready |

ContentsExecutive summary ..................................................................................................4

Overview ...................................................................................................................6

Global scenario ........................................................................................................12

Asset Management Companies ...............................................................................16

Distribution landscape ............................................................................................28

Investors’ perspective .............................................................................................36

Conclusion ..............................................................................................................42

4 | Mutual Funds in India: Being future ready

Executive summary

Mutual Funds in India: Being future ready |

0.3 45.6470.0

1,218.1

5,051.5

4,173.0

6,139.8 5,922.5 5,877.0

7,025.0

8,252.0

10,828.0

FY65 FY87 FY93 FY03 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

1964–87: UTI was the sole player

Source: AMFI.

1993: Private sector

mutual fund regulations came into existence

1987: Several public sector entities entered the industry

2003: UTI bifurcated into

Undertaking in charge of assured return schemes

2014: The MF market surpassed INR10b for the

1996: Formulation of SEBI (Mutual Fund) Regulations 1996 under which the industry currently functions

2006-2008: Several large

market

Mutual fund assets under management (INRb)

•

•

to investors

•

•

•

•

| Mutual Funds in India: Being future ready

Overview

Mutual Funds in India: Being future ready |

Regulator

InvestorsStakeholders

Distributors

AssetManagement

Companies

Principal stakeholders in the industry

| Mutual Funds in India: Being future ready

Mutual fund industry: a promising future

Financial Express

Low penetration provides for strong potential

Source: Investment Company Factbook, 2015 and IMF, World Economic Outlook Database, April 2015

9%

7%

17%

22%

40%

42%

49%

91%

111%

India

Mexico

Japan

Korea

UK

Brazil

France

US

Australia

AUM to GDP ratio (2014)

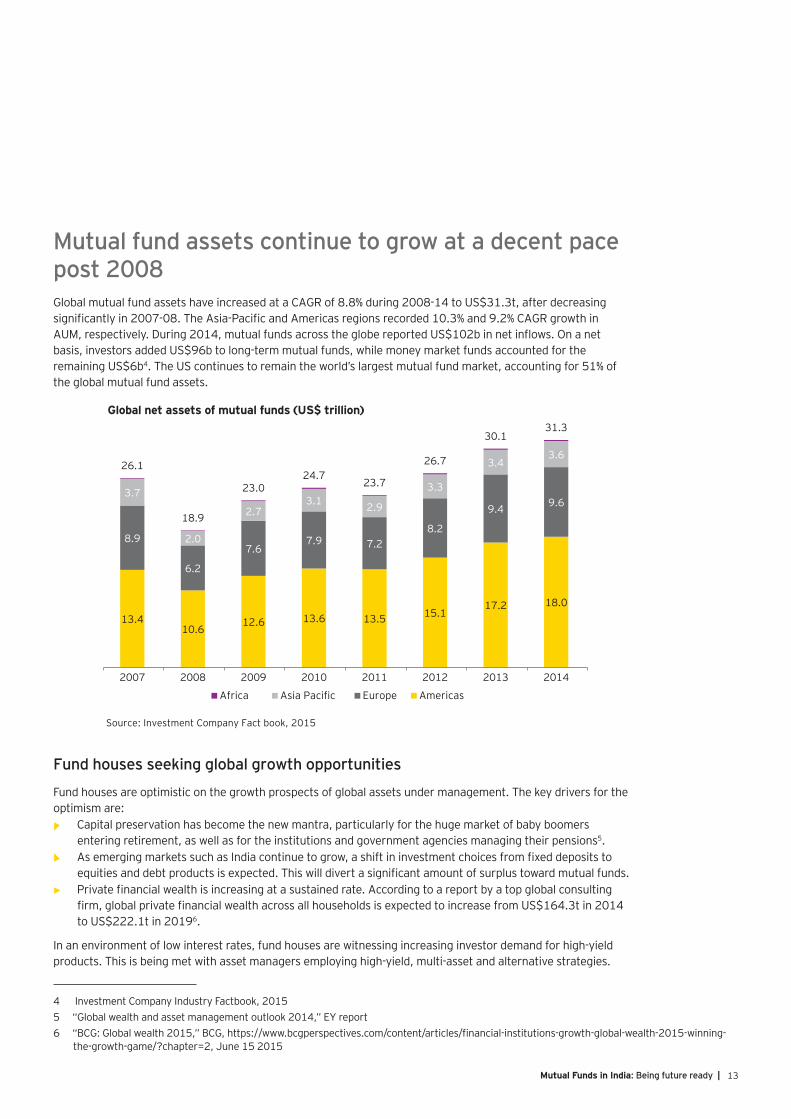

Promising macroeconomic environment: Indian mutual funds have outpaced global mutual funds in

terms of AUM growth.

savings (INR11.7 trillion) into capital markets Increasing investor awareness to augment mutual fund growth

Favourable demographics: Growing population with lower average age is expected to

increase number of mutual fund investors Tier II and Tier III cities promise growth opportunities

investments in equities and alternative investment funds

Conducive environment for product development:

Evolution of new products such as REITS

Growth in HNWIs to promote development of Portfolio Management schemes (PMS)

Conducive environment for product development:

Tax incentives for NPS Higher FDI limit for

pension sector TER relaxations to

promote AUM penetration in tier II and tier III cities

to promote investor

Government of India’s

inclusion to augment AUM growth as well

AUM to increase to INR20 trillion

by 2018

Mutual Funds in India: Being future ready |

Strong macroeconomic fundamentals lead strong recovery in Indian

Source: Investment Company Factbook , 2015 and AMFI

100120

87 105 113 109 123 138 144100

170128

206 194 189235 255

325

2006 2007 2008 2009 2010 2011 2012 2013 2014

AUM: Indian mutual funds vs. global mutual funds

Global MFs AUM Indian MFs AUMAUM based to 100

Favorable demographics

2

3

Source: United Nations, Department of Economic and Social Affairs, 18 March 2015

30% 20%

65% 68%

4% 10%1% 2%

0%20%40%60%80%

100%

2010 2050

0-14Age group in year 15-64 65-79 80+

Working age population(15-64 years)

| Mutual Funds in India: Being future ready

Recent industry trends Large AMCs have shown considerable improvement in terms

FY09 FY11 FY14

Revenue margin 0.62% 0.65% 0.70%

Cost margin 0.43% 0.38% 0.37%

PAT margin 0.16% 0.19% 0.24%

AUM (INRb) 572.4 783.0 916.2

Mutual Funds in India: Being future ready |

industry’s AUM

Category 31 March 2009 31 March 2012 31 March 2015

Major product schemes 94.94 94.22 94.33

Total 100.00 100.00 100.00

Metros continue to contribute the major proportion of AUM

Cities Per capita income in INR (2013-2014) % share in AUM (31 March 2015)

Chennai

| Mutual Funds in India: Being future ready

2

Mutual Funds in India: Being future ready |

Mutual fund assets continue to grow at a decent pace post 2008

4

Global net assets of mutual funds (US$ trillion)

13.410.6

12.6 13.6 13.5 15.117.2 18.0

8.9

6.2

7.67.9 7.2

8.2

9.4 9.63.7

2.0

2.73.1 2.9

3.3

3.43.6

26.1

18.9

23.024.7

23.7

26.7

30.131.3

2007 2008 2009 2010 2011 2012 2013 2014

Africa

Source: Investment Company Fact book, 2015

Asia Paci c Europe Americas

Fund houses seeking global growth opportunities

• �

• �

• �

| Mutual Funds in India: Being future ready

Technological and regulatory forces changing the game

Importance of big data analytics

Emergence of robo-advisors8

The Economic Times

PressReader

• Rational advice

• Lower cost

• Smaller ticket size

Advantages of Robo-advisor

Rationaladvice

Lowercost

Highertransparency

Small ticketsize

Advantages

Shortage of

advisors

Mutual Funds in India: Being future ready |

Economic Times

ETF.com

•

• Greater transparency

Increasing regulatory scrutiny11

• Scale becomes even more crucial

• Growing importance of risk culture and governance

•

• Reduced dependence on traditional distribution channels

| Mutual Funds in India: Being future ready

3

Mutual Funds in India: Being future ready |

Competitive landscape: a highly concentrated industry

Key particulars Domestic AMCs Foreign AMCs

4

i

Cost ratio ii

•

•

•

•

•

The Financial Express

| Mutual Funds in India: Being future ready

39.5%49.5%

35.0% 16.5%

6.6%5.7%

17.4%25.1%

1.4% 3.2%

Outperformers Underperformers

Others Bonds

0.19% 0.14%

• Smaller AMCs

•

income

•

Mutual Funds in India: Being future ready |

Key trends

Beyond top 15 cities: cities of future growth

cities

Strong potential

Business Standard

mydigitalfc.com

Distribution of ultra-HNI wealth in India

Source: Top of the Pyramid 2015, Kotak Wealth ManagementNote: Ultra HNIs are households with over INR250 million of wealth

56% 44%

Metros Non-metros

| Mutual Funds in India: Being future ready

AMCs cash in on rising equity markets by launching new products

Increasing dependency on offshore investors and other sources of income22

23

MF Utility

The Times of India

Business Standard

mydigitalfc.com

Business Standard

Mutual Funds in India: Being future ready |

LiveMint

Business Standard

Business Standard

High focus on investor awareness: going beyond FAQs and seminars

24

•

•

manner

•

A phase of consolidation

investment horizon27

22 | Mutual Funds in India: Being future ready

Challenges faced by AMCs

•

•

Business Standard

400

500

600

700

800

900

1000

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

FY09

Source: Company reports, EY analysis

FY11 FY12 FY14

PAT as a % of AUM Cost as a % of AUM AAUM (INRb) (RHS)

23Mutual Funds in India: Being future ready |

Business Standard

Weak distribution network

Ground realities in B15 cities restrict growth

•

•

•

•

Non-bank-sponsored small and mid-sized AMCs at a disadvantage29

24 | Mutual Funds in India: Being future ready

Way forward: all-inclusive strategy needed to achieve success in B-15 cities Customize business strategies based on scale of operations

• The New Entrants

• The Marathoners

• The Big Five

• The Strugglers

Leverage existing distribution channels to expand network

Expand branches in tier-2 and tier-3 towns

Develop an effective

digital strategy

Focus on training and development

of existing talent

AMCs Strategic imperatives

The new entrants •

The marathoners •

strategy

•

The strugglers •

Mutual Funds in India: Being future ready |

cities

How UTI made it to small cities and towns?

Cities Per capita income in INR (2013-2014) % share in AUM (31 March 2015)

Business Standard

| Mutual Funds in India: Being future ready

New players can begin only with a B2C distribution network

31

34

Enhance collaboration with R&T agents to improve customer service standards

Quantum Mutual Fund website

Mutual Funds in India: Being future ready |

Forbes India

Times of India

Nature of complaints received by top 15 AMCs during FY15

9.4%

72.6%

17.9%

Source: AMFI, Company reports

Non-commercialtransaction

Commercialtransaction

Others

Tap the huge potential of the SME sector

32

33

| Mutual Funds in India: Being future ready

4

Mutual Funds in India: Being future ready |

Mutual fund distribution is still dominated by third party distributors, with direct channels preferred mainly by institutional investors

34

Type of distributors Description

•

•

•

•

•

•

Distributors vs. direct: investor-wise Distributors vs. direct: category-wise

0%

20%

40%

60%

80%

100%

Retail Institutions HNIs Corporates

Direct Distributor

0%

20%

40%

60%

80%

100%

Money Market ETFs Equity Debt

Direct Distributor

Source: AMFI Note: Data as of July 2015

| Mutual Funds in India: Being future ready

Key trends

Commission income from MF distribution on the rise; private banks dominate top spots

Distribution commission (INRb)

Source: AMFI, consolidated data on commission and expenses paid to distributors

18.83 23.89 26.03

Commission growth: 36% (CAGR)

47.29

FY12 FY13 FY14 FY15

Mutual Funds in India: Being future ready |

Times of India

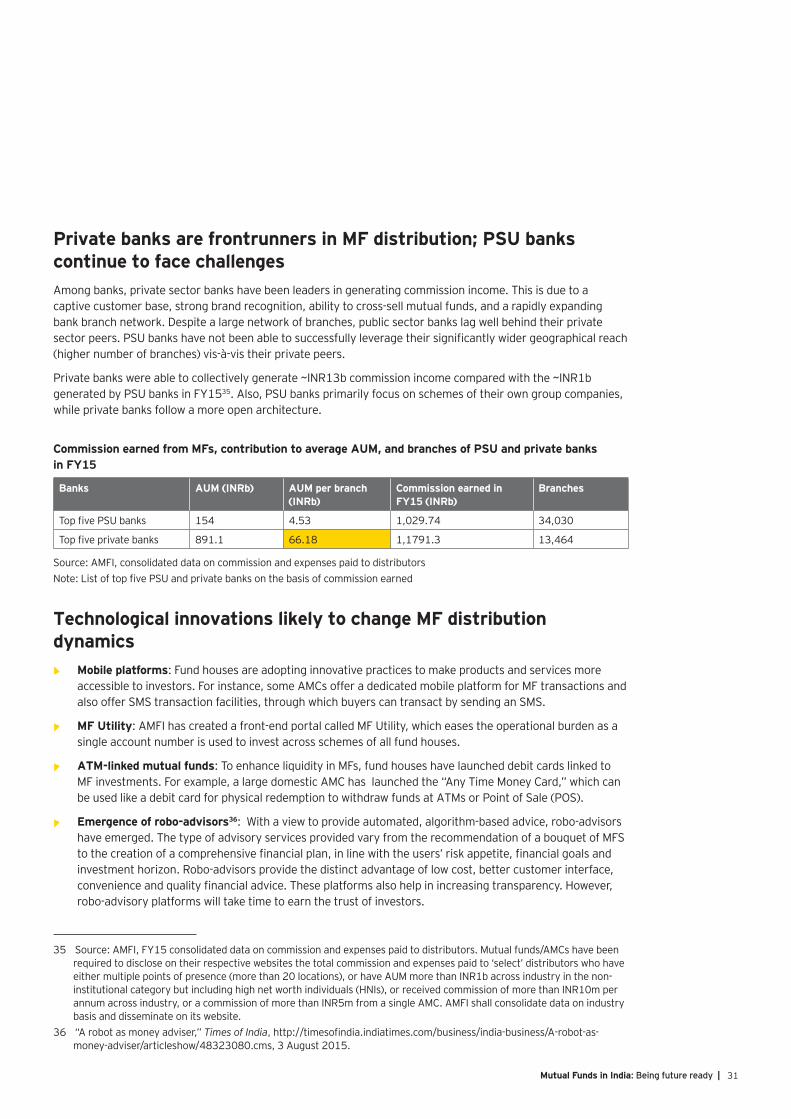

Private banks are frontrunners in MF distribution; PSU banks continue to face challenges

in FY15

Banks AUM (INRb) AUM per branch (INRb)

Commission earned in FY15 (INRb)

Branches

Technological innovations likely to change MF distribution dynamics• Mobile platforms

• MF Utility

• ATM-linked mutual funds

• Emergence of robo-advisors36

32 | Mutual Funds in India: Being future ready

Challenges faced by distributorsAdvisors lean toward other investment products due to cap on commissions in MFs

Way forward

33Mutual Funds in India: Being future ready |

Financial Times

Revisiting the client service model

Right balance between.....

Safeguard ofinvestorinterest

Economicallyviable model

for distributors

Fee-based model

Country-wise Distribution approach37

UK

US

The Netherlands

Singapore

South Africa

34 | Mutual Funds in India: Being future ready

Commission model

Book size of INR12 million

INR20,000 per month

revenue

600 clients

Target 12 clients per day

Distributor needs to maintain a book size of INR12 million in order to earn INR20,000 per month

Considering a 1% upfront commission and a 1% trail commission, the distributor will earn INR240,000 per annum or INR20,000 per month

Distributor needs to tap 600 clients to maintain the required book size, assuming that average ticket size per client is INR20,000

Distributor has to target at least 2,400 clients per year (assuming 25% conversion rate), i.e., he has to target at least 12 clients a day (assuming 200 working days in a year)

Source: EY analysis

Mutual Funds in India: Being future ready |

the right direction

Deploying advanced analytics techniques to expand distribution reach

| Mutual Funds in India: Being future ready

Mutual Funds in India: Being future ready |

Wealth of individuals continues to rise; mutual fund

class segment39

•

•

39.6m

2.6m

0.182m

23.6m

1.3m

0.076m

(US$10,000-US$100,000)

UHNI(>US$1m)

(2004)

The wealth pyramid

(2014)

HNI(US$0.1–US$1m)

Key trends

six years

| Mutual Funds in India: Being future ready

AUM by investor class (%)

Source: AMFI

50.9% 45.9%

4.6%

1.2%

1.2%1.4%

22.0%28.6%

21.3% 22.9%

Mar-09 Mar-15

Retail HNIs FIIs Banks/FIs Corporates

paid off

Increased familiarity with mutual fund terminologies (%)41

Source: Nielsen survey, 2014

32

25

29

26

24

23

25

40

37

36

34

33

31

29

Advisory fees

Lock-in period

Redemption

Entry load

Portfolio

NAV

NFO

2013 2014

Mutual Funds in India: Being future ready |

Changing investment approach: products matter more than the manufacturer42

Investment approach

41%

59%

First choose the AMC and then the best schemeChoose the suitable scheme irrespective of the AMC

Source: Nielsen survey, 2014

Historical performance of the fund is an important metric that determines investor’s choice43

Deciding factors while choosing an investment product (% of respondents)

40

38

38

35

31

Historical performance of the scheme

Source: Nielsen survey, 2014

Historical performance of the AMC

Recommendation of sales agent

Safety of fund

Ratings published by MF research

| Mutual Funds in India: Being future ready

Way forward

penetration

low-reward option44

Mint

Mutual Funds in India: Being future ready |

66

Source: Nielsen survey, 2014

42

25 2415 13 11 9 8

Life

Insu

ranc

e

Livemint

Reasons for not investing in mutual funds (% of respondents)

1915 14

86

Low rate of return

Source: Nielsen survey, 2014

Lack of moneyto invest

Very risky Lack of surplusincome

Low understanding

42 | Mutual Funds in India: Being future ready

43Mutual Funds in India: Being future ready |

investors

distributors

Asset management companies (AMCs)

44 | Mutual Funds in India: Being future ready

Contacts:

Acknowledgement

Abizer Diwanji Murali Balaraman

Rahul Shah

Parag Jani

Kirti Shenoi

Jayanta Kumar Ghosh

Communication

Nikhaar Mathur

Mutual Funds in India: Being future ready |

Notes:

| Mutual Funds in India: Being future ready

About Cafemutual

Ahmedabad2nd

Bengaluruth th

th

th

Chandigarhst

Chennaith th

Hyderabad

Kochith

Kolkata

3rd

Mumbaith

th

NCR

th

4th th

Puneth

Ernst & Young LLPEY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016

© 2015 Ernst & Young LLP. Published in India. All Rights Reserved.

EYIN1509-103

ED None

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

JG

EY refers to the global organization, and/or one or more of the independent member firms of Ernst & Young Global Limited