Multinational Business Finance 12th Edition Slides Chapter 12

Upload

ivy-manalangCategory

view

230download

0

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 1/26

4/19/12 JSGabinera

Click to edit Master subtitle styleAn Introduction

MULTINATIONAL BUSINESS FINANCE

11 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 2/26

4/19/12 JSGabinera

Why is International FinanceImportant?

22 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 3/26

4/19/12 JSGabinera

Why is International FinanceImportant?

v In previous finance courses you have beentaught about general finance concepts thatapply to domestic or local settings, BUT welive in an international world.

v Companies (and individuals) can raise funds,invest money, buy inputs, produce goods

and sell products and services overseas.

v With these increased opportunities comes

additional risks. We need to know how toidentify these risks and then how to control33 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 4/26

4/19/12 JSGabinera

The Multinational Enterprise(MNE)

v A multinational enterprise (MNE) is definedas one that has operating subsidiaries,branches or affiliates located in foreigncountries.

v The ownership of some MNEs is sodispersed internationally that they areknown as transnational corporations.

v The transnationals are usually managedfrom a global perspective rather than from44 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 5/26

4/19/12 JSGabinera

Multinational Business Finance

v While multinational business financeemphasizes MNEs, purely domesticfirms also often have significant

international activities:

v Import & export of products, components

and servicesv Licensing of foreign firms to conduct

their foreign business

v Exposure to foreign competition in the

domestic market55 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 6/26

4/19/12 JSGabinera

Types of MultinationalEnterprises

v Raw Material Seekers

Ø First type of MNEs

Ø Exploit raw materials found overseas

Ø Trading, mining and oil companiesv Market Seekers

Ø Post-WWII MNEs

Ø Expand production and sales into foreign markets

Ø Big name companies – IBM, McDonalds etc.

v Cost Minimisers

Ø More recent MNEs

Ø Seek out lowest production cost countries66 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 7/26

4/19/12 JSGabinera

Global Financial Management

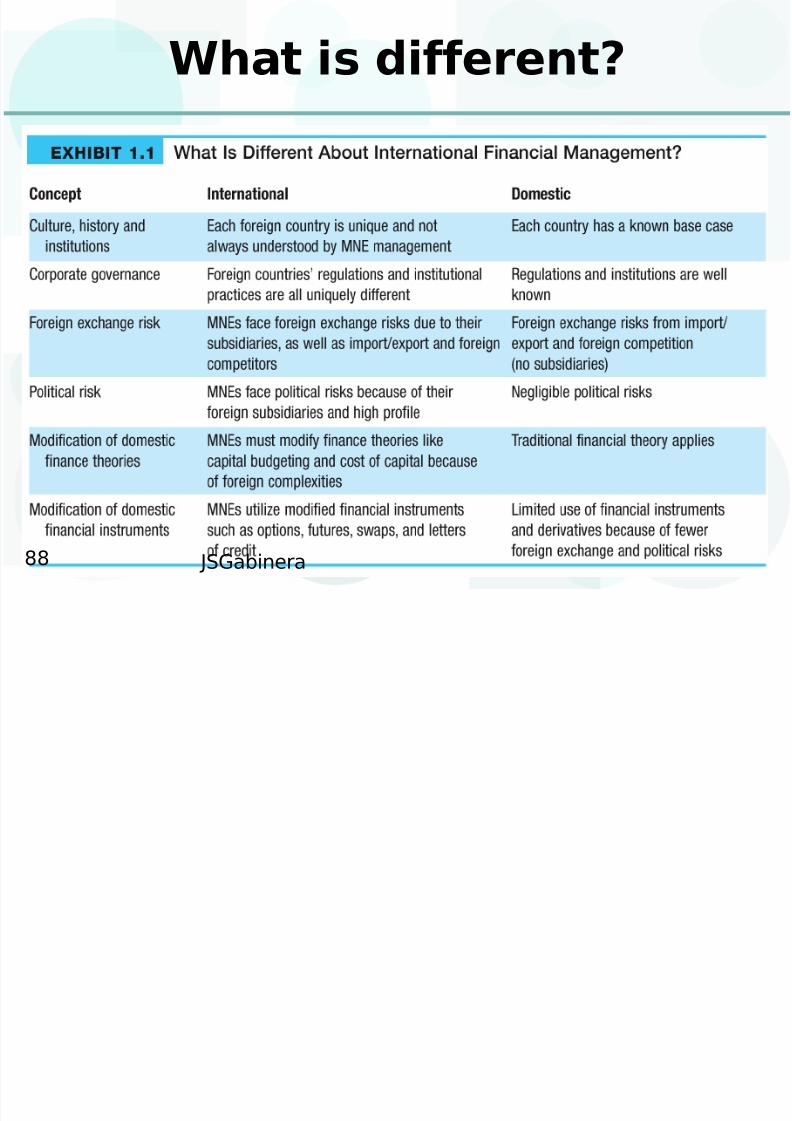

v There are significant differencesbetween international and domesticfinancial management:

v Cultural issues

v Corporate governance issues

v Foreign exchange risks

v Political Risk

v Modification of domestic finance theories

v Modification of domestic financialinstruments77 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 8/26

4/19/12 JSGabinera

What is different?

88 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 9/26

4/19/12 JSGabinera

Separation of Ownership fromManagement

v The U.S. and U.K. stock markets arecharacterized by widespreadownership of shares.

v Management owns only a smallproportion of stock in their own firms.

v In the rest of the world, ownership is

usually characterized by controllingshareholders. Typical controllingshareholders are:

1. Government (such as privatized99 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 10/26

4/19/12 JSGabinera

The Goal of Management

There are basic differences incorporate and investor philosophiesglobally.

In this context, the universal truths of finance become culturally determinednorms.

1010 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 11/26

4/19/12 JSGabinera

Shareholder WealthMaximization

In a Shareholder Wealth Maximizationmodel (SWM), a firm should strive tomaximize the return to shareholders, asmeasured by the sum of capital gains anddividends, for a given level of risk.

Alternatively, the firm should minimize thelevel of risk to shareholders for a given

rate of return.

1111 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 12/26

4/19/12 JSGabinera

Shareholder WealthMaximization

The SWM model assumes as a universaltruth that the stock market is efficient.

An equity share price is always correctbecause it captures all the expectations of return and risk as perceived by investors,quickly incorporating new information into

the share price.

Share prices are, in turn, the best

allocators of capital in the macro economy.1212 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 13/26

4/19/12 JSGabinera

Shareholder WealthMaximization

The SWM model also treats its definition of risk as a universal truth.

Risk is defined as the added risk that afirm’s shares bring to a diversifiedportfolio.

Therefore the unsystematic, or operationalrisk, should not be of concern to investors(unless bankruptcy becomes a concern)because it can be diversified.

1313 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 14/26

4/19/12 JSGabinera

Shareholder WealthMaximization

Agency theory is the study of how shareholderscan motivate management to accept theprescriptions of the SWM model.

Liberal use of stock options should encouragemanagement to think more like shareholders.

If management deviates too extensively from SWM

objectives, the board of directors should replacethem.

If the board of directors is too weak (or not at“arms-length”) the discipline of the capital marketscould effect the same outcome through a takeover.1414 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 15/26

4/19/12 JSGabinera

Shareholder WealthMaximization

Long-term value maximization can conflictwith short-term value maximization as aresult of compensation systems focused onquarterly or near-term results.

Short-term actions taken by managementthat are destructive over the long-termhave been labeled impatient capitalism.

This point of debate is often referred to afirm’s investment horizon (how long ittakes for a firm’s actions, investments and

operations to result in earnings).1515 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 16/26

4/19/12 JSGabinera

Shareholder WealthMaximization

In contrast to impatient capitalism is patient capitalism.

This focuses on long-term SWM.

Many investors, such as Warren Buffet,

have focused on mainstream firms thatgrow slowly and steadily, rather thanlatching on to high-growth but riskysectors.

1616 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 17/26

4/19/12 JSGabinera

Corporate Wealth Maximization

In contrast to the SWM model, continentalEuropean and Japanese markets arecharacterized by a philosophy that acorporation’s objective should be to

maximize corporate wealth (the CWMmodel).

In this context, a firm should treat

shareholders on a par with other corporateinterest groups, such as management,labor, the local community, suppliers,creditors and even the government.

1717 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 18/26

4/19/12 JSGabinera

Corporate Wealth Maximization

The definition of corporate wealth is muchbroader than just financial wealth (cash,marketable securities and lines of credit).

Corporate wealth includes technical,market and human resources.

This measure goes beyond financialreports to include the firm’s marketposition, employee knowledge base andskill sets, manufacturing processes,

technological proficiencies, marketing and1818 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 19/26

4/19/12 JSGabinera

Corporate Wealth Maximization

The CWM model does not assume thatequity markets are either efficient orinefficient.

In fact, market efficiency does not matteras the firm’s financial goals are notexclusively shareholder-oriented.

This model assumes that long-term “loyal”shareholders should influence corporatestrategy, not transient portfolio investors.1919 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 20/26

4/19/12 JSGabinera

Corporate Wealth Maximization

The CWM model assumes that total risk,operating and financial risk, does count.

In the CWM model, it is a corporateobjective to generate growing earningsand dividends over the long run with asmuch certainty as possible given the firm’s

mission statement and goals.

Risk is measured more by product marketvariability than by short-term variation inearnings and share price.2020 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 21/26

4/19/12 JSGabinera

Corporate Wealth Maximization

Although the CWM model avoids theimpatient capitalism as seen in the SWM, ithas its own flaw in that management istasked with meeting the demands of

multiple stakeholders.

This leaves management without a clear

signal about the tradeoffs, whichmanagement tries to influence throughwritten and oral disclosures and complexcompensation systems.

2121 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 22/26

4/19/12 JSGabinera

Failures in CorporateGovernance

There are clear examples of thefailure of Corporate Governance inthe United States:

Enron – lack of full disclosure of off-B/Sdebt

WorldCom – capitalizing costs thatshould have been expensed

2222 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 23/26

4/19/12 JSGabinera

Failures in CorporateGovernance

In each case, prestigious auditing firmsmissed the violations or minimized them,presumably because of lucrative consultingrelationships or other conflicts of interest.

In addition, security analysts urgedinvestors to buy the shares of firms they

knew to be highly risky (or even close tobankruptcy).

Top executives themselves wereresponsible for mismanagement and still2323 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 24/26

4/19/12 JSGabinera

Regulation of CorporateGovernance

The corporate regulatory “pyramid”in the United States is as follows:

US Congress

Securities and ExchangeCommission (SEC)

New York Stock2424 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 25/26

4/19/12 JSGabinera

The Sarbanes-Oxley Act

This act was passed by the US Congress,and signed by President George W. Bushduring 2002 and has three majorrequirements:

CEOs of publicly traded companies must vouchfor the veracity of published financial statements

Corporate boards must have audit committeesdrawn from independent directors

Companies can no longer make loans tocorporate directors

Penalties have been spelled out for variouslevels of failure.

2525 JSGabinera

8/4/2019 Multinational Business Finance Chapter 1

http://slidepdf.com/reader/full/multinational-business-finance-chapter-1 26/26

4/19/12JSGabinera

Governance, Rights, and theFuture

Clearly, there has been substantialreflection on business in the earlydays of the 21st century.

Issues such as sustainabledevelopment, environmentalism and

corporate social responsibility areemerging as concerns for society,and of course management as

businesses look toward the future2626 JSGabinera