MSME Sector in India - Current Financing Landscape for MSMEs - Part - 16

Upload

fate-foundationCategory

view

456download

2

1

Financing opportunities available to

MSMEs in Sterling Bank Plc.

THE MSME SEGMENT AS DEFINED BY CBN

CBN for the purpose of the N220B MSMEDFscheme defined a Small and Medium ScaleEnterprise (SME) as an enterprise that hasasset base (excluding land) of betweenN5million - N500 million and labor force ofbetween 11 and 300.

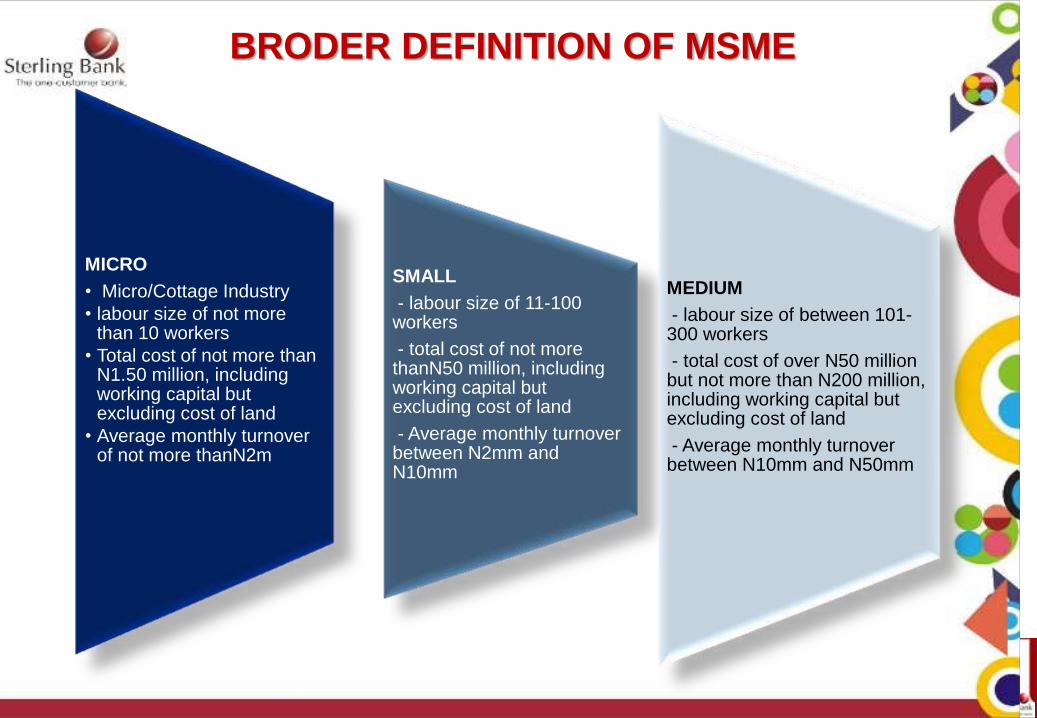

BRODER DEFINITION OF MSME

MICRO

• Micro/Cottage Industry

• labour size of not more than 10 workers

• Total cost of not more than N1.50 million, including working capital but excluding cost of land

• Average monthly turnover of not more thanN2m

SMALL

- labour size of 11-100 workers

- total cost of not more thanN50 million, including working capital but excluding cost of land

- Average monthly turnover between N2mm and N10mm

MEDIUM

- labour size of between 101-300 workers

- total cost of over N50 million but not more than N200 million, including working capital but excluding cost of land

- Average monthly turnover between N10mm and N50mm

Financing Opportunities Available for

MSMEs in Nigerian Commercial Banks

Given that MSMEs are considered to be the backbone of

economic growth in all countries and the fact that they

constitute 97.2% of the companies in Nigeria, Commercial

Banks however little, have overtime supported MSMEs

financial need via different products which broadly fall into

Overdraft to finance working capital

Term loans for business expansion

Leases for asset acquisition

Stock financing

Invoice discounting etc.

4

Financing Opportunities Available for

MSMEs in Sterling Bank Plc

5

To enable the bank meet the needs of MSMEs (Micro,

Small and Medium Enterprises) in the country, it

developed a holistic and integral framework of value-add

offerings that will inspire, nurture, mentor and manage

specific MSME types from micro to medium.

This product is called the SUPA Business Proposition

which comes in three variants.

The SUPA Offerings

Features of the SUPA Account Types (ZERO AMF accounts)

Target Market Micro Small Medium

Monthly

turnoverN4million N20million N100million

Minimum

opening and

daily account

balance

N15,000 N25,000 N50,000

Other features

Free SMS & Email Alerts, Mobile

Banking, Internet Banking, Mobile

Payments, Free Debit Card

(Verve Debit Cards only)

Free SMS & Email Alerts,

Mobile Banking, Internet

Banking, Mobile Payments,

Free Debit Cards (Verve upon

default and Visa Debit Card on

request)

Free SMS & Email Alerts,

Mobile Banking, Internet

Banking, Mobile Payments,

Free Debit Cards (Verve upon

default and Visa Debit Card on

request)

Monthly flat

chargeN1,000 N2,500 N5,000

Our SUPA offering:

Financial

Unsecured overdraft

• One year facility of up to N2.5mm with a 30 day clean upcycle

Secured Overdraft

• One year facility of up to N25mm with a 90 day clean upcycle

Term / Time loan

• Up to N20mm available over a tenor of up to 48months for asset acquisition and business expansion.

• Also covers invoice discounting, contract and LPO Financing

7

OUR VALUE –ADD

OFFERINGS

e-Solution for inventory management, daily business operations and book-keeping

Access to the MSME Capacity Building Workshop Academy

Access to Business Advisory services Helpdesk

Access to Market Arena

Meet the Executive Program to empower aspiring entrepreneurs

8

N220 BILLION CBN MICRO, SMALL & MEDIUM

ENTERPRISES DEVELOPMENT FUND

(MSMEDF)

To enable both Banks existing SMEs and

prospects access the MSMEDF funds in order to increase their productivity, output, employment and

engender inclusive growth.

The fund is spread as follows: 60% (Women), 30% 30% (Others) and 10% (For

new businesses).

For asset growth and attractive income accruing

to the Bank

To enhance and improve the Bank’s access to

increased long term and low cost liquidity to support

the our SME Business.

To grow the Bank’s customer base in this critical sector of the

economy

ELIGIBILITY CRITERIA

Only SMEs in Manufacturing, Agricultural Value Chain activities, Renewable energy/Energy efficient product and Technologies, Educational Institutions and income

generating Enterprises as advised by CBN

The fund is not to be used to re-finance existing facilities

The fund is for SMEs with Asset base of =N=5M -=N=500M (excluding land and buildings)and monthly business turnover of between N2M –

N50M.

Must be an account Holder with the Bank

Must have convincing business plans with a concise profit/loss projections

Employer of between 11 and 200 verifiable staff

TERMS & CONDITIONS

Single Obligor Limit

• Minimum of N5 Million per customer

• Maximum of N50 Million per customer

• For working capital purpose: customer can only access 50% of average monthly credit turnover of the customer over a period of 12 months account statement

Tenor

• Maximum of 3 years for SME Working Capital

• Maximum of 5 years for SME term loan

• Moratorium of 12months

Pricing and Other Conditions

• All in pricing of 9%

• Funds must be disbursed within 5 days of receipt from CBN

• Max. 70% of the average monthly positive net credit turnover of the customer (over a period of 12 months account statement with the Bank or any other Bank) shall be required to service the loan rentals.

13

4

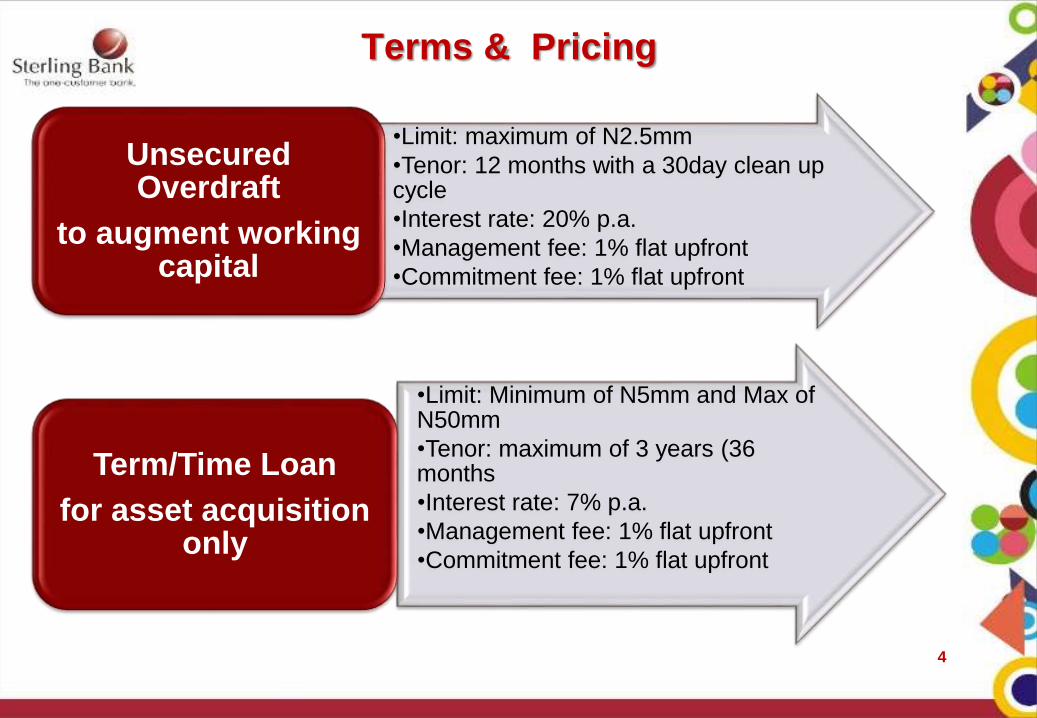

Terms & Pricing

•Limit: maximum of N2.5mm

•Tenor: 12 months with a 30day clean up cycle

•Interest rate: 20% p.a.

•Management fee: 1% flat upfront

•Commitment fee: 1% flat upfront

Unsecured Overdraft

to augment working capital

•Limit: Minimum of N5mm and Max of N50mm

•Tenor: maximum of 3 years (36 months

•Interest rate: 7% p.a.

•Management fee: 1% flat upfront

•Commitment fee: 1% flat upfront

Term/Time Loan

for asset acquisition only

4

Other Financing Opportunities

Cluster financing

Sterling Alternative Finance

Thank You!

![MSME Financing and Development Project [MSMEFDP]](https://static.fdocuments.net/doc/165x107/616a293811a7b741a34f777a/msme-financing-and-development-project-msmefdp.jpg)