![MS Hiremath Ppt[1]](https://static.fdocuments.net/doc/165x107/54762ce1b4af9ffd628b458e/ms-hiremath-ppt1.jpg)

MS II UNIT MATERIAL MANAGEMENT PPT

21

-

Upload

chaitanya-prasad -

Category

Education

-

view

241 -

download

7

Transcript of MS II UNIT MATERIAL MANAGEMENT PPT

Unit -IV

a) Materials Management: Objectives, Need for

Inventory control, EOQ, ABC Analysis, Purchase

Procedure, Stores Management and Stores

Records.

Materail refer to inputs into the production process most of

which are embodied in the finished goods being manufactured.

It may be raw materail, work in progress, finished gods, spare

parts and components etc.

Definition:Materials management is the process of planing, organising

and controlling the materails in a given organisation.

In government organsiations it is beetr known as “Supply

Management”

In armed forces it refers to this as “Logistics Management”

Materials is the broad term which includes Inventory +

Stores

Inventory refers to all the idle physical stocks which have

economic value.

Stores includes materials, supplies, and finished goods not

required immediately for use.

“Inveotory control is a scientific method of providing the right

type of material at the right time in the right quantities and at

right price to sustain the given production schedule”

To support the production department with right

kind of material at right time

To minimise the wastage in production process

To avoid accumulation of work in progress

To ensure economy of costs by processing economic

order quantities

To increase the profitability of the organisation

Maintain stores record to ensure continuos stock taking

Classify, in a comprehensive manner, the items of invntory and codify the same

Formulate a clear cut purhcase procedures

Set stock levels for different levels

Monitor each category of the stocks through ABC anlysis

Minise the cost of each order by determining EOQ

Replenish the stock as and when required

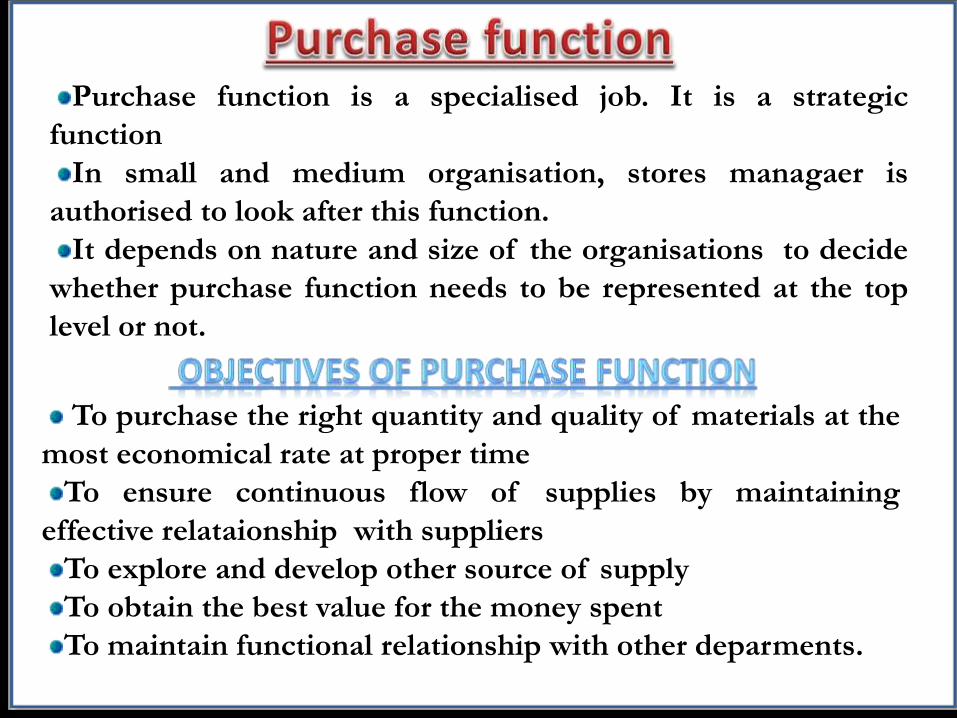

Purchase function is a specialised job. It is a strategic

function

In small and medium organisation, stores managaer is

authorised to look after this function.

It depends on nature and size of the organisations to decide

whether purchase function needs to be represented at the top

level or not.

To purchase the right quantity and quality of materials at the

most economical rate at proper time

To ensure continuous flow of supplies by maintaining

effective relataionship with suppliers

To explore and develop other source of supply

To obtain the best value for the money spent

To maintain functional relationship with other deparments.

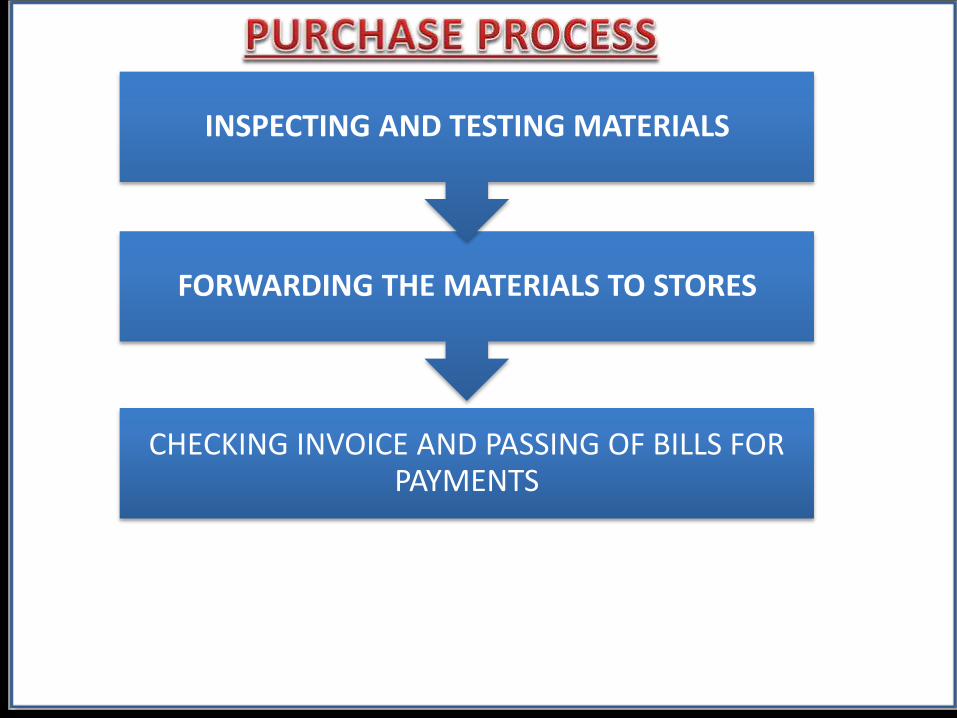

CHECKING INWARD INVOICE

RECEIVING OF MATERIALS ALONG WITH THE INVOICE

PLACING PURCHASE ORDER

NEGOTIATING OVER THE PURCHASE PRICE AND TERMS OF SUPPLY

OPENING OF TENDERS AND PREPATION OF STATEMENT

ISSUING OF TENDERS AND OBTAINING QUOTATION

EXPLORING THE SOURCE OF SUPPLY

REQUISITIONING FOR PURCHASING

CHECKING INVOICE AND PASSING OF BILLS FOR PAYMENTS

FORWARDING THE MATERIALS TO STORES

INSPECTING AND TESTING MATERIALS

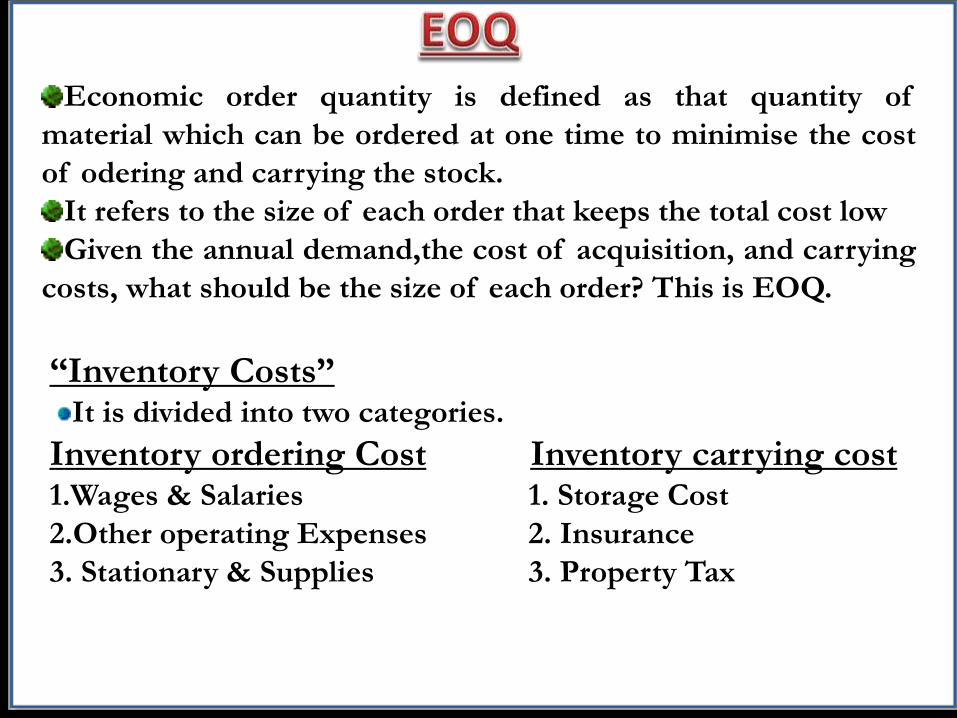

Economic order quantity is defined as that quantity of

material which can be ordered at one time to minimise the cost

of odering and carrying the stock.

It refers to the size of each order that keeps the total cost low

Given the annual demand,the cost of acquisition, and carrying

costs, what should be the size of each order? This is EOQ.

“Inventory Costs”It is divided into two categories.

Inventory ordering Cost Inventory carrying cost1.Wages & Salaries 1. Storage Cost

2.Other operating Expenses 2. Insurance

3. Stationary & Supplies 3. Property Tax

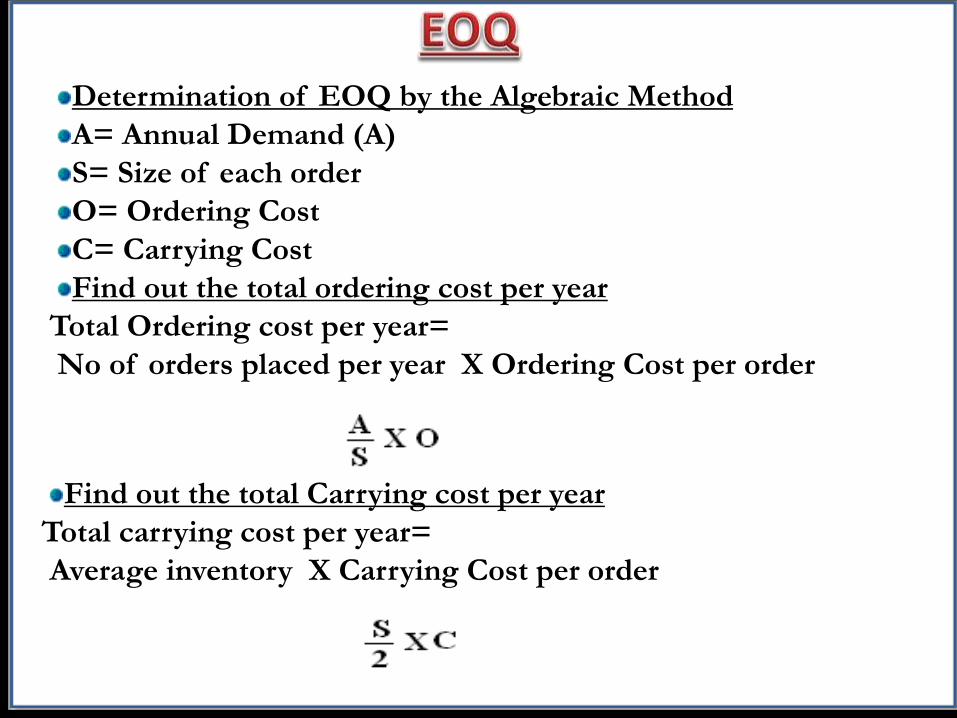

Determination of EOQ by the Algebraic Method

A= Annual Demand (A)

S= Size of each order

O= Ordering Cost

C= Carrying Cost

Find out the total ordering cost per year

Total Ordering cost per year=

No of orders placed per year X Ordering Cost per order

Find out the total Carrying cost per year

Total carrying cost per year=

Average inventory X Carrying Cost per order

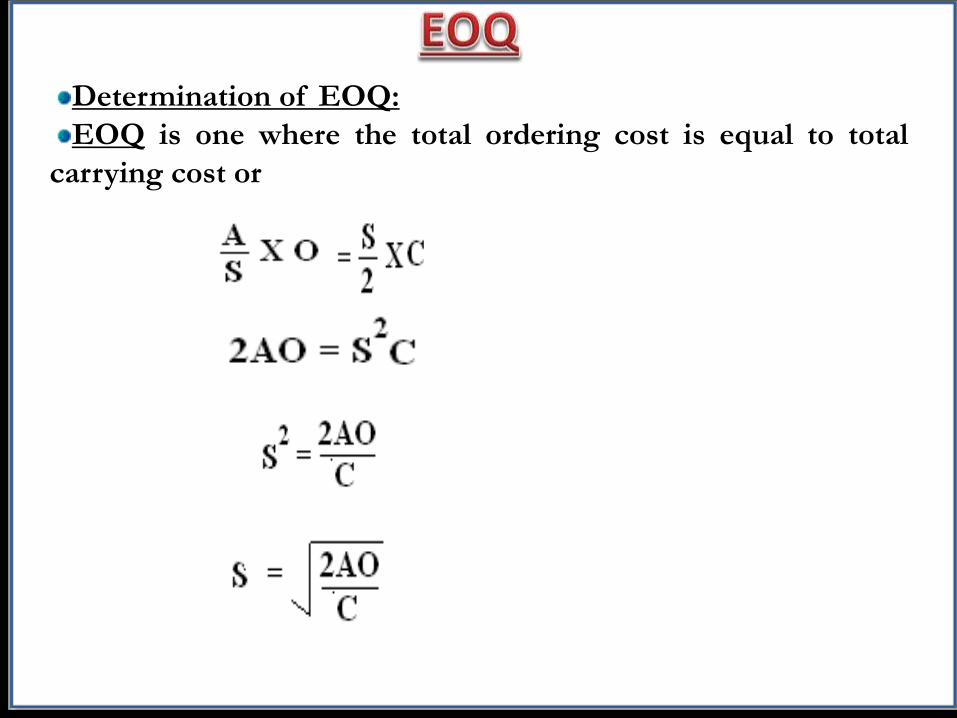

Determination of EOQ:

EOQ is one where the total ordering cost is equal to total

carrying cost or

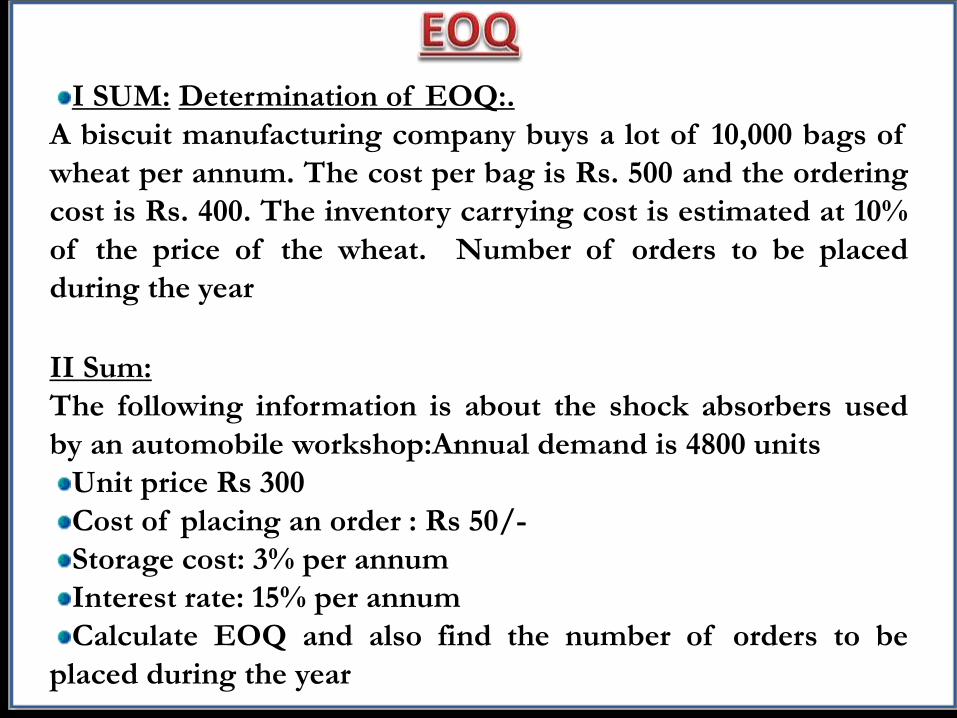

I SUM: Determination of EOQ:.

A biscuit manufacturing company buys a lot of 10,000 bags of

wheat per annum. The cost per bag is Rs. 500 and the ordering

cost is Rs. 400. The inventory carrying cost is estimated at 10%

of the price of the wheat. Number of orders to be placed

during the year

II Sum:

The following information is about the shock absorbers used

by an automobile workshop:Annual demand is 4800 units

Unit price Rs 300

Cost of placing an order : Rs 50/-

Storage cost: 3% per annum

Interest rate: 15% per annum

Calculate EOQ and also find the number of orders to be

placed during the year

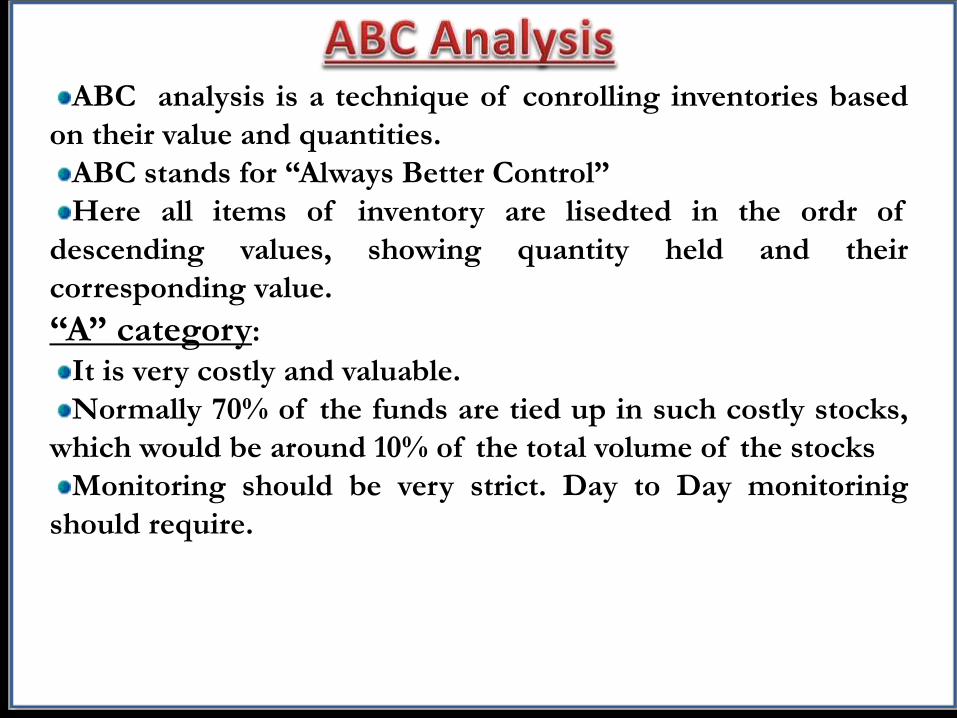

ABC analysis is a technique of conrolling inventories based

on their value and quantities.

ABC stands for “Always Better Control”

Here all items of inventory are lisedted in the ordr of

descending values, showing quantity held and their

corresponding value.

“A” category:It is very costly and valuable.

Normally 70% of the funds are tied up in such costly stocks,

which would be around 10% of the total volume of the stocks

Monitoring should be very strict. Day to Day monitorinig

should require.

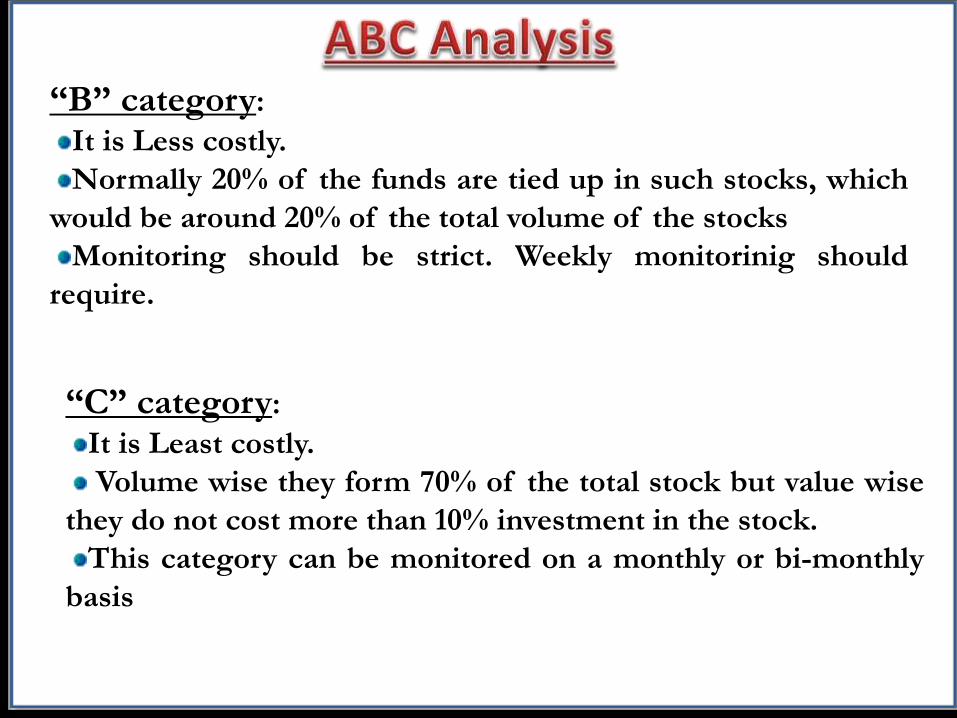

“B” category:It is Less costly.

Normally 20% of the funds are tied up in such stocks, which

would be around 20% of the total volume of the stocks

Monitoring should be strict. Weekly monitorinig should

require.

“C” category:It is Least costly.

Volume wise they form 70% of the total stock but value wise

they do not cost more than 10% investment in the stock.

This category can be monitored on a monthly or bi-monthly

basis

Category Value(%) Volume(%) Degrees of Control

A 70 10 Strict

B 20 20 Moderate

C 10 70 Low

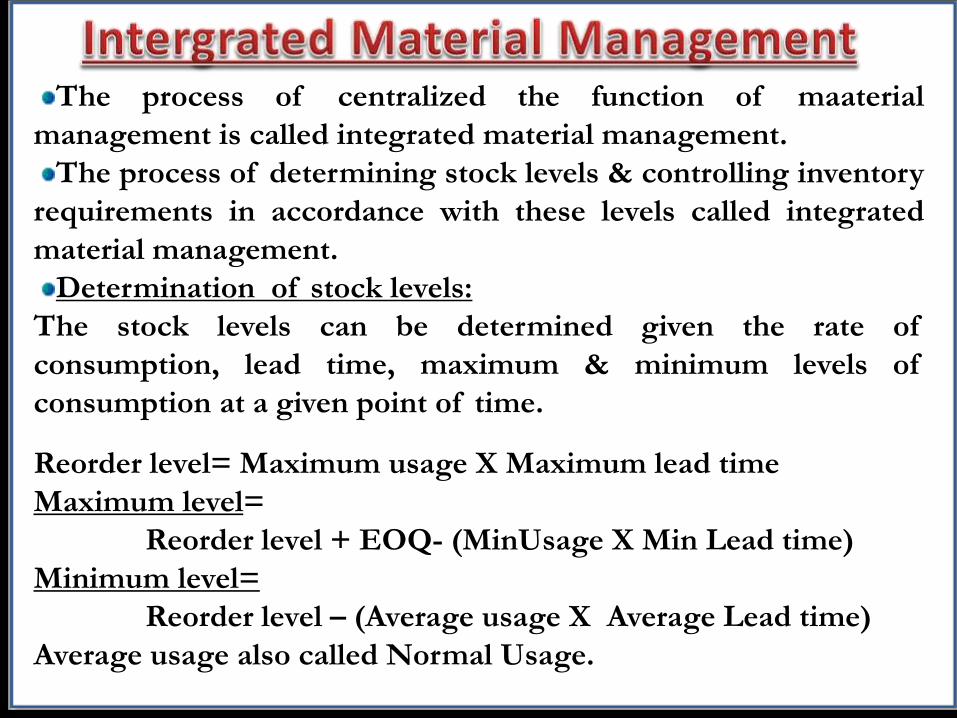

The process of centralized the function of maaterial

management is called integrated material management.

The process of determining stock levels & controlling inventory

requirements in accordance with these levels called integrated

material management.

Determination of stock levels:

The stock levels can be determined given the rate of

consumption, lead time, maximum & minimum levels of

consumption at a given point of time.

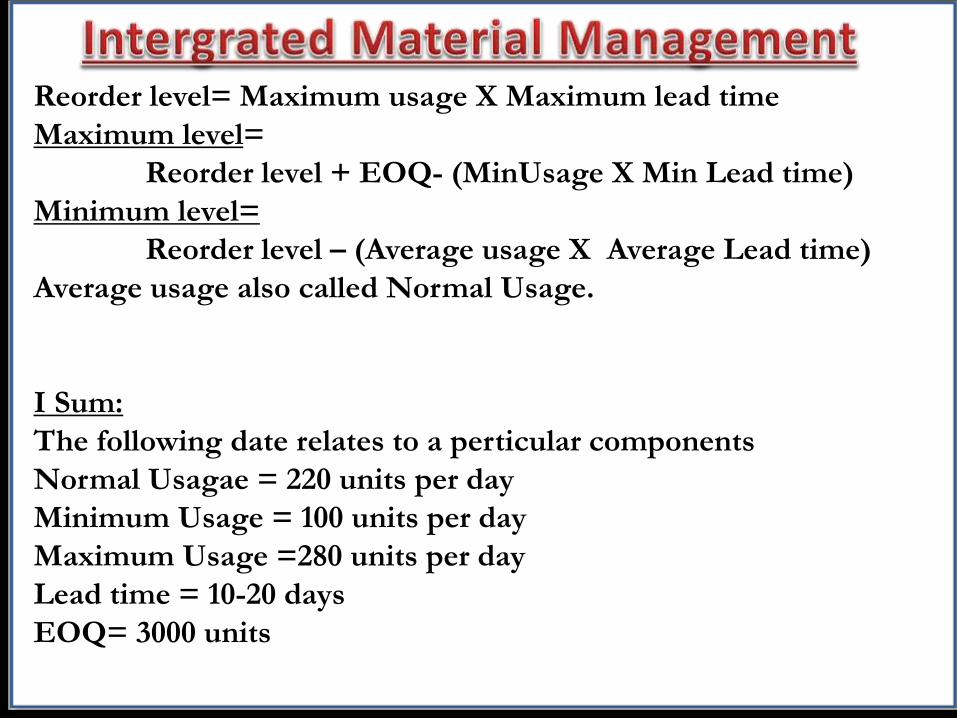

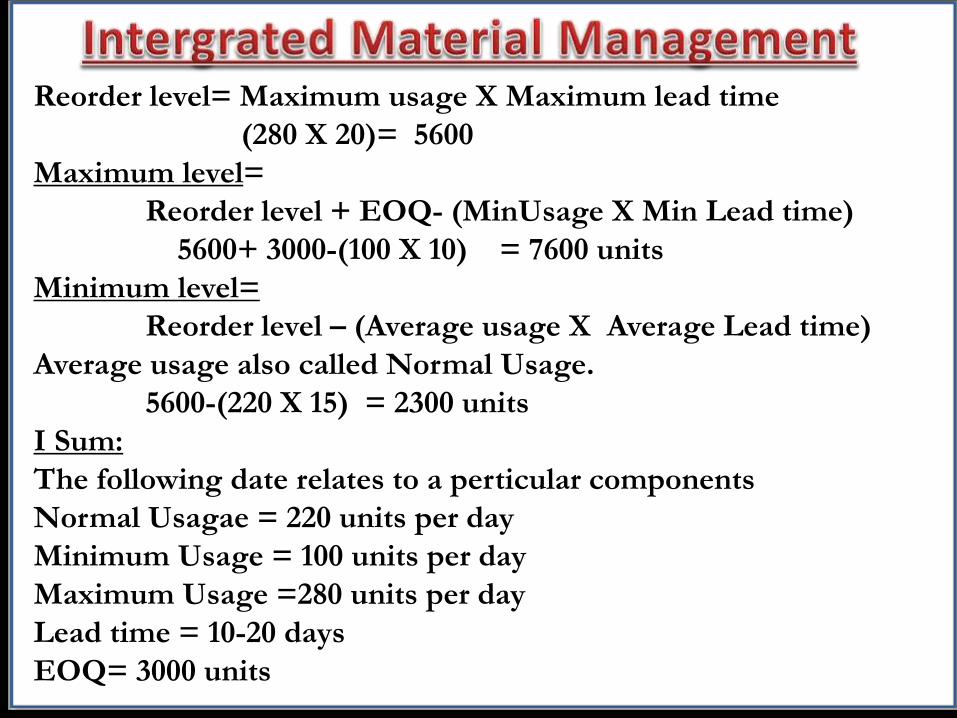

Reorder level= Maximum usage X Maximum lead time

Maximum level=

Reorder level + EOQ- (MinUsage X Min Lead time)

Minimum level=

Reorder level – (Average usage X Average Lead time)

Average usage also called Normal Usage.

Reorder level= Maximum usage X Maximum lead time

Maximum level=

Reorder level + EOQ- (MinUsage X Min Lead time)

Minimum level=

Reorder level – (Average usage X Average Lead time)

Average usage also called Normal Usage.

I Sum:

The following date relates to a perticular components

Normal Usagae = 220 units per day

Minimum Usage = 100 units per day

Maximum Usage =280 units per day

Lead time = 10-20 days

EOQ= 3000 units

Reorder level= Maximum usage X Maximum lead time

(280 X 20)= 5600

Maximum level=

Reorder level + EOQ- (MinUsage X Min Lead time)

5600+ 3000-(100 X 10) = 7600 units

Minimum level=

Reorder level – (Average usage X Average Lead time)

Average usage also called Normal Usage.

5600-(220 X 15) = 2300 units

I Sum:

The following date relates to a perticular components

Normal Usagae = 220 units per day

Minimum Usage = 100 units per day

Maximum Usage =280 units per day

Lead time = 10-20 days

EOQ= 3000 units

HML: High, Medium, Low

SDE: Scares, Difficult, Easy to Obtain

FSN: Fast moving, Slow moving, Non moving

VED: Vital, Essential, Desirable

XYZ: High, Medium, Low

SOS: Seasonal & Off Seasonal