mPOS is dead. Long live SmartPOS.

17

www.barracloughandco.com is dead. Long live SmartPOS Geoffrey Barraclough 1

-

Upload

geoffrey-barraclough -

Category

Technology

-

view

118 -

download

1

Transcript of mPOS is dead. Long live SmartPOS.

www.barracloughandco.com

is dead. Long live SmartPOSGeoffrey Barraclough

1

www.barracloughandco.com

Strategy | Proposition Development | Insight Experts in Retail Technology & Payments

2

www.barracloughandco.com

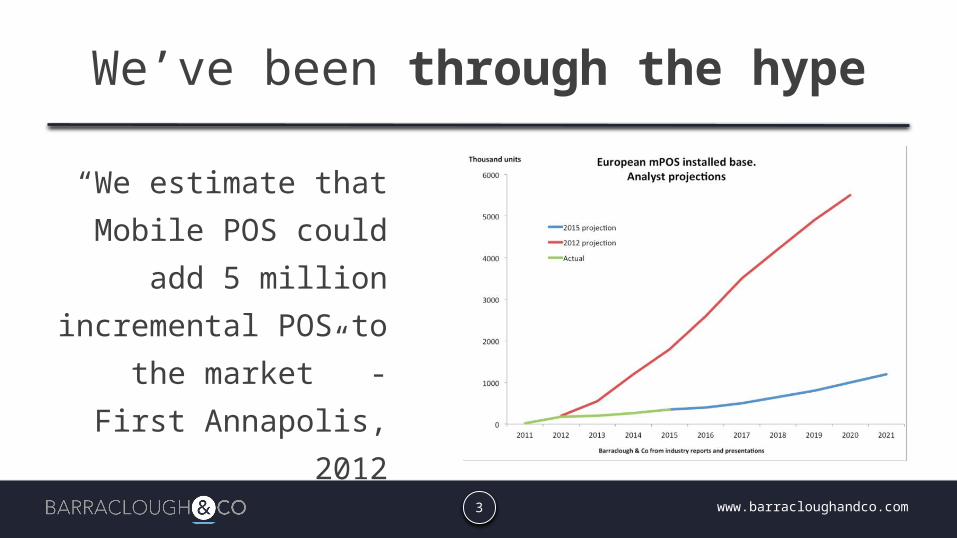

We’ve been through the hype

“We estimate that

Mobile POS could add

5 million incremental

POS to the market” -

First Annapolis, 2012

3

www.barracloughandco.com

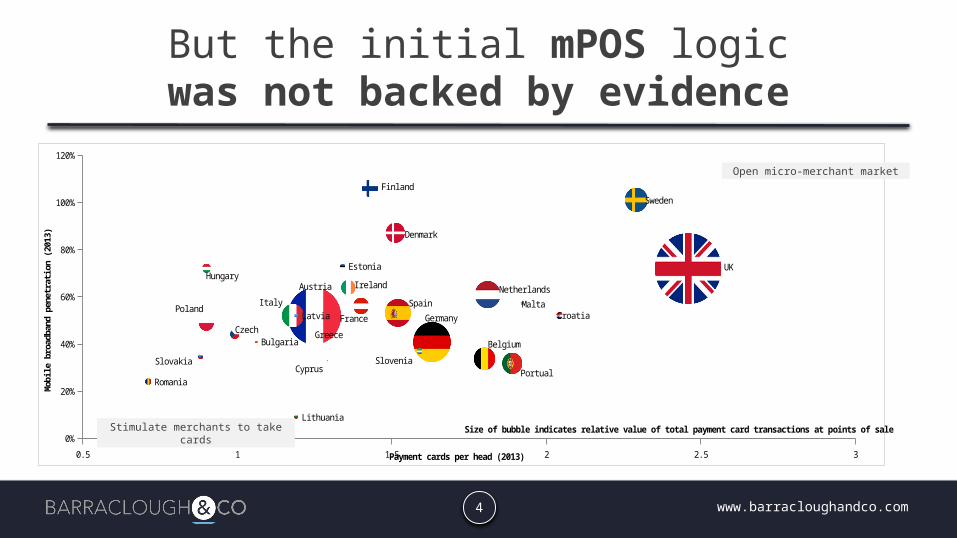

0.5 1 1.5 2 2.5 3

0%

20%

40%

60%

80%

100%

120%

BelgiumBulgariaCzech

Denmark

Germany

Estonia

Ireland

Greece

Spain

France CroatiaItaly

Cyprus

Latvia

Lithuania

Hungary

Malta

NetherlandsAustria

Poland

PortualRomania

SloveniaSlovakia

Finland

Sweden

UK

Size of bubble indicates relative value of total payment card transactions at points of sale

Payment cards per head (2013)

Mobile b

roadband p

enetr

ati

on (

2013)

But the initial mPOS logicwas not backed by evidence

Stimulate merchants to take cards

Open micro-merchant market

4

www.barracloughandco.com

Yet the trends are positive

RegulationInterchange

Rise of the tablets

Big retail moblises

5

www.barracloughandco.com

8 Reasons whymPOS doesn’t work for micro-

merchants

1

2

3

4

5

6

7

8

Business Case doesn’t work

Products not integrated

Prices too high

Initial use cases were implausible

Card machines aren’t hard to get

Cash is resilient

Micro-merchants don’t know they need this

Finding the right partners is hard

6

www.barracloughandco.com

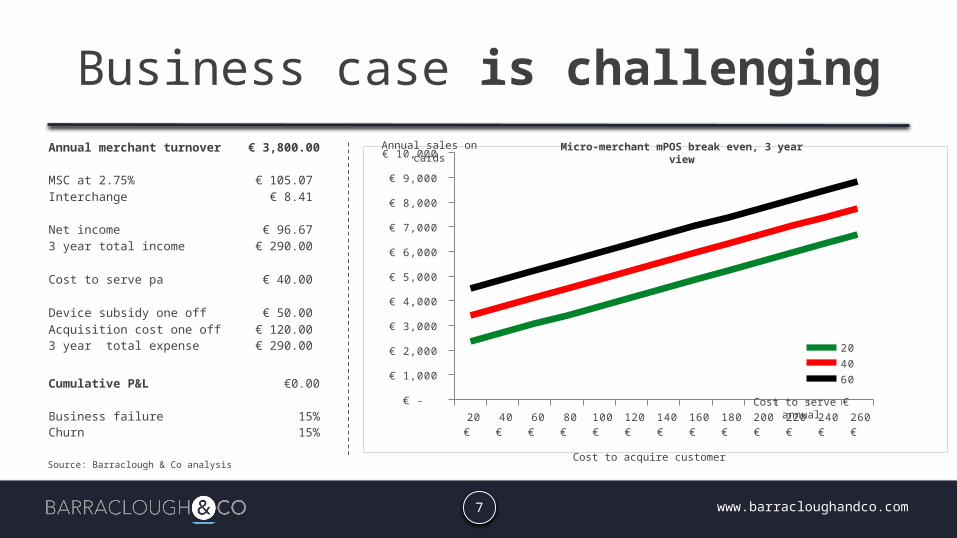

Business case is challenging

20 € 40 € 60 € 80 € 100 €

120 €

140 €

160 €

180 €

200 €

220 €

240 €

260 €

€ -

€ 1,000

€ 2,000

€ 3,000

€ 4,000

€ 5,000

€ 6,000

€ 7,000

€ 8,000

€ 9,000

€ 10,000

204060

Cost to serve € annual

Micro-merchant mPOS break even, 3 year view

Annual merchant turnover € 3,800.00

MSC at 2.75% € 105.07 Interchange € 8.41

Net income € 96.67 3 year total income € 290.00

Cost to serve pa € 40.00

Device subsidy one off € 50.00 Acquisition cost one off € 120.00 3 year total expense € 290.00

Cumulative P&L €0.00

Business failure 15%Churn 15%

Annual sales on cards

Cost to acquire customerSource: Barraclough & Co analysis

7

www.barracloughandco.com

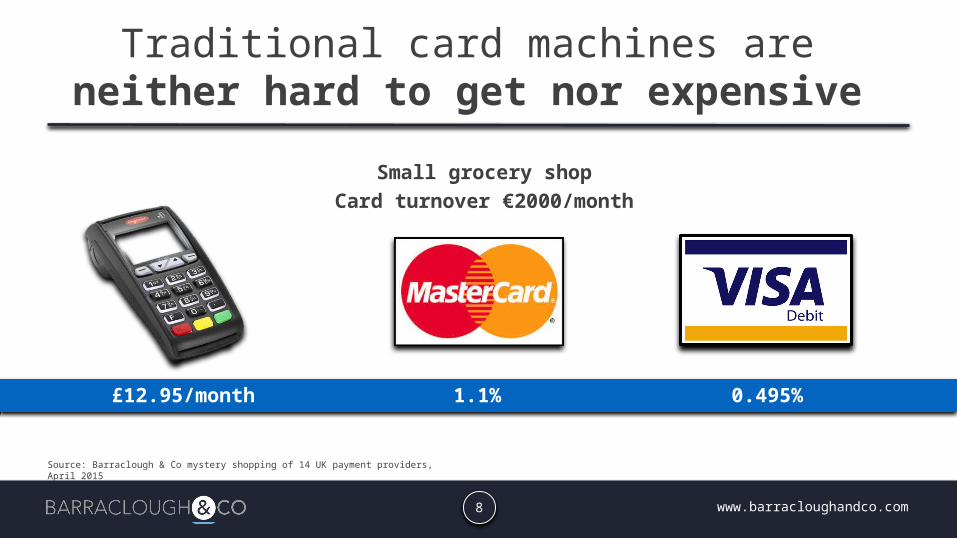

Traditional card machines areneither hard to get nor expensive

Small grocery shopCard turnover €2000/month

£12.95/month 1.1% 0.495%

Source: Barraclough & Co mystery shopping of 14 UK payment providers, April 2015

8

www.barracloughandco.com

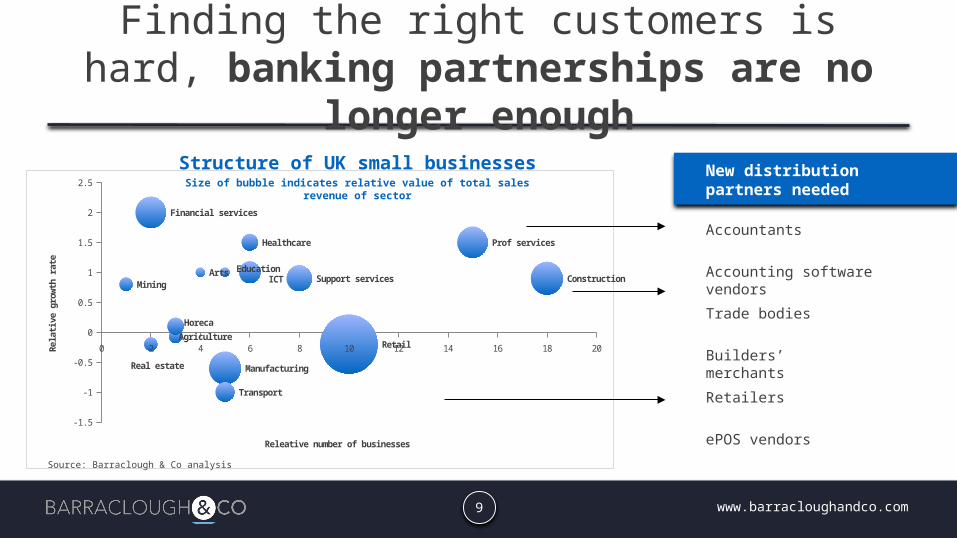

Finding the right customers is hard, banking partnerships are no longer

enough

0 2 4 6 8 10 12 14 16 18 20

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

Agriculture

Mining

Manufacturing

Construction

Retail

Transport

Horeca

ICT

Financial services

Real estate

Prof services

Support servicesEducation

Healthcare

Arts

Releative number of businesses

Rela

tive g

row

th r

ate

Structure of UK small businesses New distribution partners needed

ePOS vendors

Accountants

Builders’ merchants

Size of bubble indicates relative value of total sales revenue of sector

Trade bodies

Retailers

Accounting software vendors

Source: Barraclough & Co analysis

9

www.barracloughandco.com

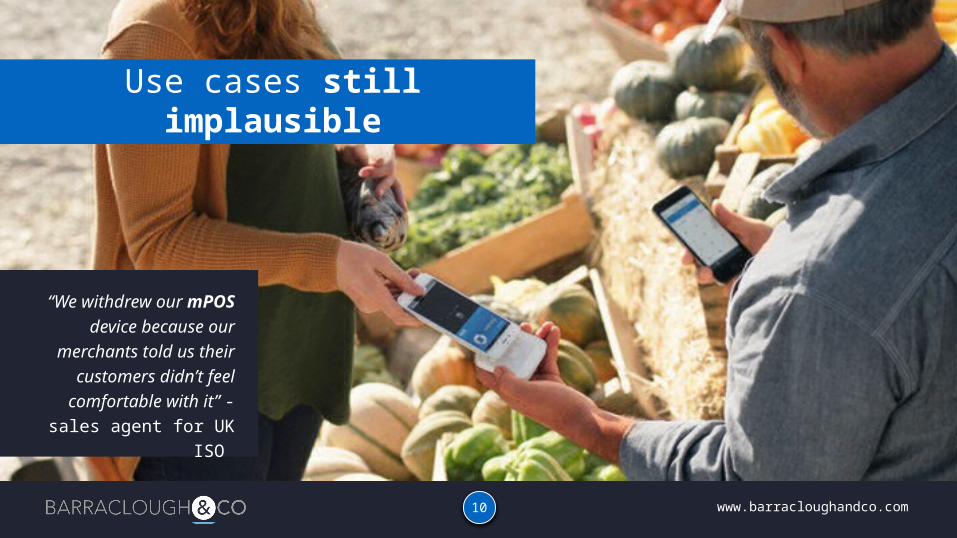

Use cases still implausible

“We withdrew our mPOS device because our merchants told us their customers didn’t

feel comfortable with it” - sales agent for UK ISO

10

www.barracloughandco.com

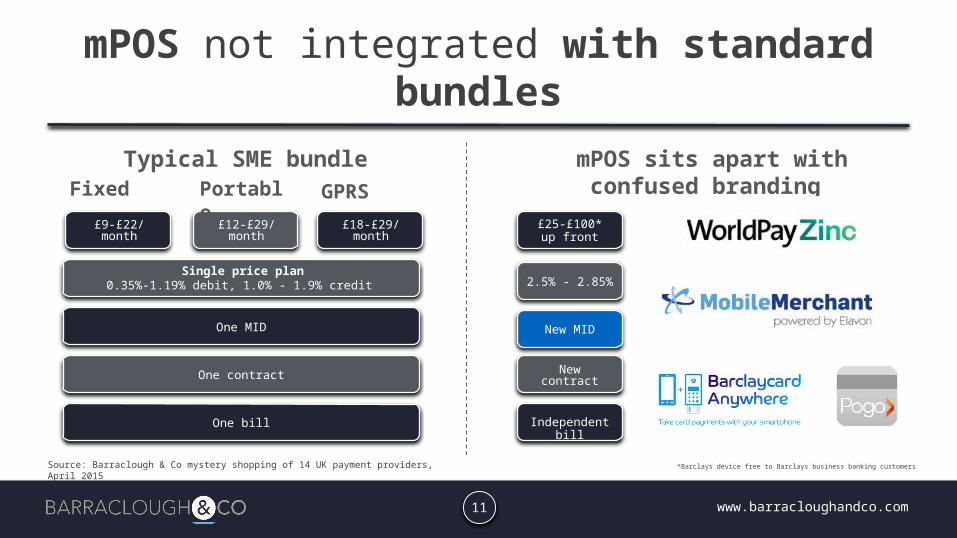

Single price plan0.35%-1.19% debit, 1.0% - 1.9% credit

One MID

One contract

£9-£22/month

Fixed Portable

GPRS

mPOS not integrated with standard bundles

£12-£29/month

£18-£29/month

£25-£100* up front

New MID

2.5% - 2.85%

New contract

One bill Independent bill

Typical SME bundle mPOS sits apart withconfused branding

*Barclays device free to Barclays business banking customersSource: Barraclough & Co mystery shopping of 14 UK payment providers, April 2015

11

www.barracloughandco.com

A platform for transformation

The best thing about mPOS is not…the m….or the POS…

it’s a state of mind (and an operating system)

13

www.barracloughandco.com

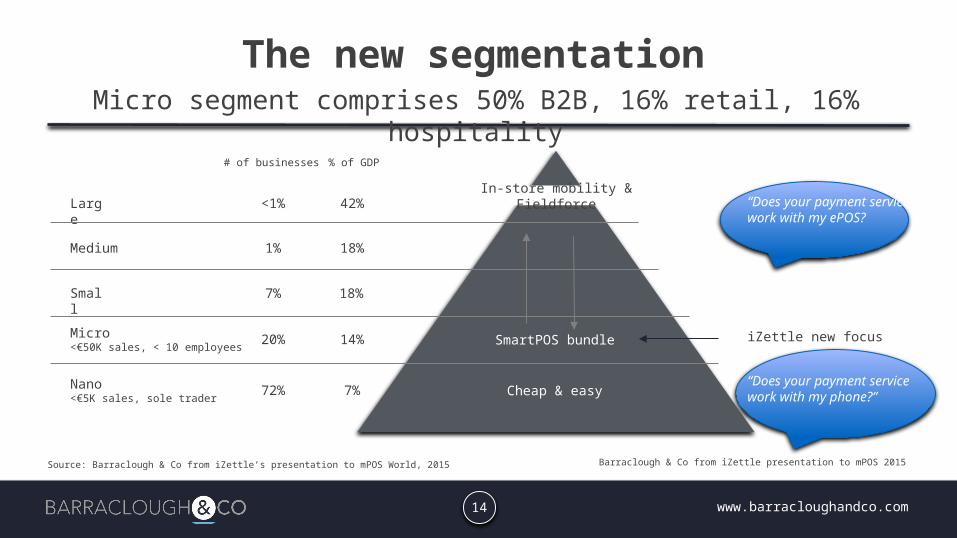

The new segmentationMicro segment comprises 50% B2B, 16% retail, 16% hospitality

Barraclough & Co from iZettle presentation to mPOS 2015

14

Source: Barraclough & Co from iZettle’s presentation to mPOS World, 2015

# of businesses % of GDP

Large

Medium

Small

Micro <€50K sales, < 10 employees

Nano<€5K sales, sole trader

<1%

1%

7%

20%

72%

42%

18%

14%

7%

18%

iZettle new focusSmartPOS bundle

In-store mobility & Fieldforce

Cheap & easy “Does your payment service work with my phone?”

“Does your payment service work with my ePOS?

www.barracloughandco.com

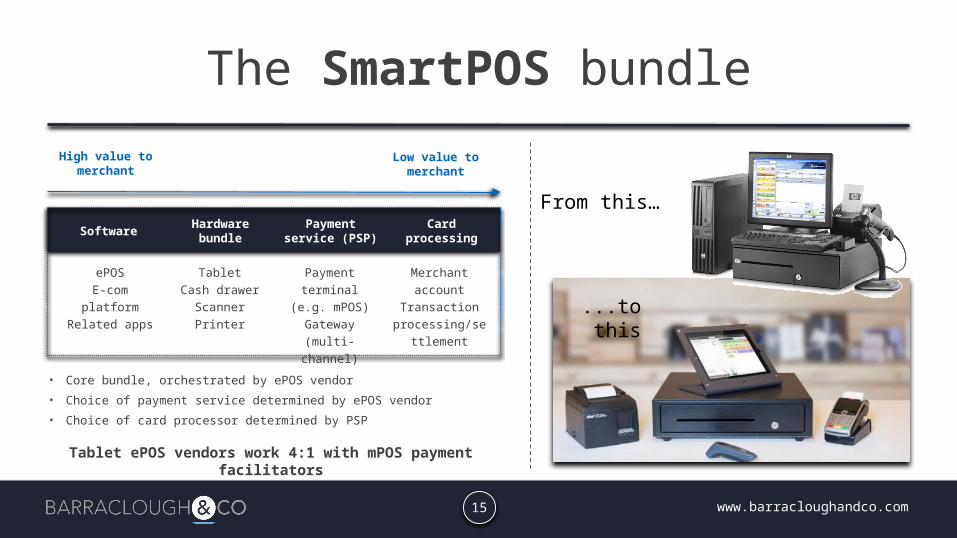

The SmartPOS bundle

From this…

Tablet ePOS vendors work 4:1 with mPOS payment facilitators

Hardware bundle

TabletCash drawer

ScannerPrinter

Software

ePOSE-com platformRelated apps

Payment service (PSP)

Payment terminal

(e.g. mPOS)Gateway

(multi-channel)

Card processing

Merchant account

Transaction processing/sett

lement

High value to merchant

Low value to merchant

• Core bundle, orchestrated by ePOS vendor

• Choice of payment service determined by ePOS vendor

• Choice of card processor determined by PSP

15

...to this

www.barracloughandco.com

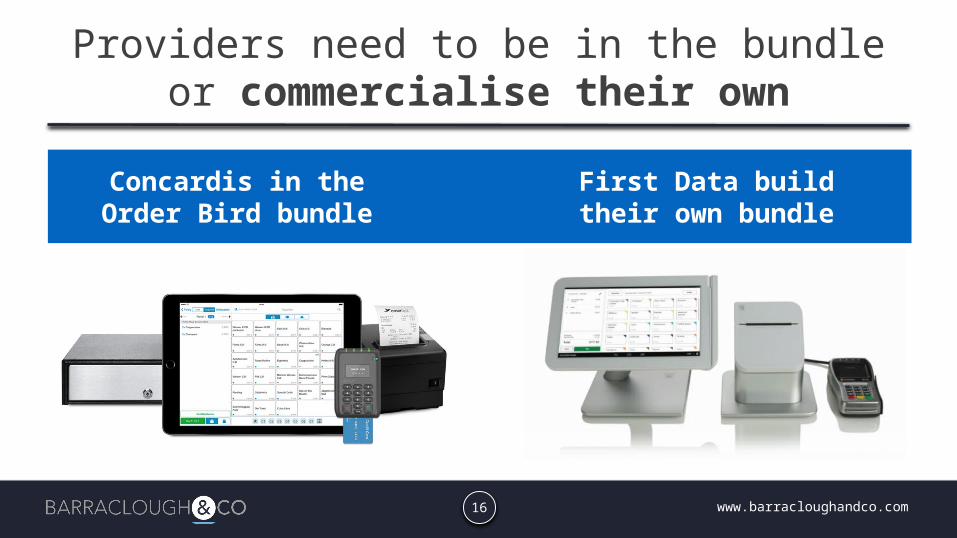

Providers need to be in the bundle or commercialise their own

Concardis in theOrder Bird bundle

First Data buildtheir own bundle

16

www.barracloughandco.com

Strategy | Proposition Development | Insight Experts in Retail Technology & Payments

17

18

www.barracloughandco.com

Thank You