Mortgage-Backed Securitization in the United Kingdom: The … · 2020-01-03 · mortgage market...

36

Mortgage-Backed Securitization in the United Kingdom: The Background Michael Pryke University of London Tim Freeman Baring Brothers & Co., Limited Abstract This article examines the changes that have taken place in the United Kingdom’s residential mortgage markets since the 1980s and the specific role of mortgage-backed securitization in generating change. The article sets out the nature of securitization, its development during the boom and slump in mortgage market activity in the United Kingdom, the types of financing vehicles that have been used, and the ways the risks involved in this financing technique have been assessed, mediated, and priced. The article concludes by discussing the likely development of this market in the United Kingdom. While future developments will be heavily influenced by investors’ require- ments on yields and the expansion of a liquid market, funding restrictions and competition for market share among traditional mortgage suppliers, the higher return on capital achievable through securitization, and the nature of the recovery in residential mortgage business will strongly influence further issues of mortgage-backed securitization in the United Kingdom. The changing housing finance market At the start of the 1980s the U.K. mortgage finance market was funded through a “specialist circuit of housing finance” (Building Societies Association 1988, 75) dominated by building societies that depended on retail savings instruments for their finance. The relationship between mortgagor and lender was compara- tively uncomplicated, and housing finance risk was contained within this housing-related circuit. Mortgage interest rates were shielded from wider macroeconomic fluctuations by the limited competition for retail funds. The whole circuit, moreover, was “unresponsive” to mortgagors; rates were set by lenders and not immediately responsive to other market rate changes (Boléat and Coles 1987, 110). For the lenders, this cozy environment was to change in the 1980s. Housing Policy Debate • Volume 5, Issue 3 307 © Fannie Mae 1994. All Rights Reserved.

Transcript of Mortgage-Backed Securitization in the United Kingdom: The … · 2020-01-03 · mortgage market...

Mortgage-Backed Securitization in the United Kingdom: The Background 307

Mortgage-Backed Securitization in the UnitedKingdom: The Background

Michael PrykeUniversity of London

Tim FreemanBaring Brothers & Co., Limited

Abstract

This article examines the changes that have taken place in the UnitedKingdom’s residential mortgage markets since the 1980s and the specific roleof mortgage-backed securitization in generating change. The article sets outthe nature of securitization, its development during the boom and slump inmortgage market activity in the United Kingdom, the types of financingvehicles that have been used, and the ways the risks involved in this financingtechnique have been assessed, mediated, and priced. The article concludes bydiscussing the likely development of this market in the United Kingdom.

While future developments will be heavily influenced by investors’ require-ments on yields and the expansion of a liquid market, funding restrictionsand competition for market share among traditional mortgage suppliers, thehigher return on capital achievable through securitization, and the nature ofthe recovery in residential mortgage business will strongly influence furtherissues of mortgage-backed securitization in the United Kingdom.

The changing housing finance market

At the start of the 1980s the U.K. mortgage finance market wasfunded through a “specialist circuit of housing finance” (BuildingSocieties Association 1988, 75) dominated by building societiesthat depended on retail savings instruments for their finance.The relationship between mortgagor and lender was compara-tively uncomplicated, and housing finance risk was containedwithin this housing-related circuit. Mortgage interest rates wereshielded from wider macroeconomic fluctuations by the limitedcompetition for retail funds. The whole circuit, moreover, was“unresponsive” to mortgagors; rates were set by lenders and notimmediately responsive to other market rate changes (Boléatand Coles 1987, 110). For the lenders, this cozy environment wasto change in the 1980s.

Housing Policy Debate • Volume 5, Issue 3 307© Fannie Mae 1994. All Rights Reserved.

308 Michael Pryke and Tim Freeman

By the mid-1980s a new lending rate pattern had emerged fol-lowing increased competition in the domestic mortgage market.Consequently, mortgage rates moved closer to the costs of whole-sale finance (table 1). U.K. mortgage rates became pegged not toretail funding, but to a level higher than the marginal cost ofwholesale funds, a cost gauged in relation to the London Inter-bank Offered Rate (LIBOR) (Gilbody 1988). This situation inturn made the mortgage market more attractive both to the U.K.retail banks and to a growing number of foreign banks, both ofwhich could mix retail and wholesale finance to fund their mort-gage business. A later challenge came with the entry of the so-called centralized lenders in the mid-1980s, which had no accessto retail funds. Their entry was facilitated by the deregulation ofpersonal financial services in 1986 and made economically fea-sible by the increased margin between the rate that mortgagorscould be charged for mortgage finance and LIBOR, the bench-mark for the cost of wholesale funds (table 1).

Table 1. The Changing Cost of Funds, 1976–1992 (percent)

BuildingBuilding Society Shares Society

Mortgage 3-MonthYear Net Gross Rates LIBOR Base Rate

1976 7.02 10.80 11.08 14.37 11.111977 6.98 10.58 11.05 6.66 8.941978 6.46 9.64 9.55 12.44 9.041979 8.45 12.07 11.94 17.06 13.681980 10.34 14.77 14.92 14.84 16.321981 9.19 13.13 14.01 15.75 13.271982 8.80 12.57 13.30 10.50 11.931983 7.27 10.39 11.03 9.34 9.831984 7.74 11.06 11.84 9.95 9.681985 8.69 12.41 13.47 12.24 12.251986 7.75 10.92 12.07 10.95 10.901987 7.42 10.16 11.61 9.70 9.741988 6.87 9.16 11.05 10.31 10.091989 9.03 12.04 13.70 13.89 13.851990 9.62 12.83 15.12 14.77 14.771991 8.21 10.94 12.93 11.53 11.701992 6.63* 8.84 10.82 9.63 10.00

Source: Data from Bank of England Quarterly Bulletin 1980, 1984; Housing Finance1991, 1992; Financial Statistics 1991, 1993.* Second quarter.

The centralized lenders are new in the sense that their lendingactivities are financed entirely through the wholesale markets.What is also of interest is that they have formed the beginningsof a secondary mortgage market in the United Kingdom, asdiscussed later in this article.

Mortgage-Backed Securitization in the United Kingdom: The Background 309

All these challenges—those from the banks and the specialistlenders as well as that forced on building societies with thedisintegration of their own cartel—have in different ways signifi-cantly altered the source and forms of housing finance instru-ments in the United Kingdom—both saving and lendingproducts. Regulatory change and further competition have pro-moted the transfusion of a mixture of wholesale funds into whathad been an exclusively retail-sourced housing finance circuit.Not only has the supply of housing finance expanded across arange of lenders, but the price of funds now relates to the gen-eral finance market rather than simply to the supply of retailfunds.

Overall, the mortgage market has changed from one with anundersupply of funds in the 1970s to one with intense competi-tion to provide mortgage finance, particularly pronounced at thepeak of the last boom in 1988. Building societies, however, stilldominate the housing finance markets; for example, they ac-counted for 60 percent of total outstanding mortgages at the endof 1990 (table 2). The challenge from the banks is reflected inthe growth of their mortgage advances, from £593 million in1980 to £10,894 million at the height of the recent house priceboom. To a lesser degree, growing competition has come from thecentralized lenders (which fall within the “Other FinancialInstitutions” heading in table 2) and accounted for only7.7 percent of outstanding mortgages in the second quarter of1992.

The influence of the centralized lenders, however, should not beinterpreted in purely quantitative terms. Although their share ofthe volume of mortgage business was small, these lenders intro-duced much change into the U.K. housing finance market, chieflythrough their main funding process: mortgage-backed secu-ritization (MBS). MBS is a process that enhances the attributesof domestic mortgages so that they equate with other capitalmarket investment media in terms of risk and return. Securitiesbacked by domestic mortgages are sold to investors through thecapital markets.

While expanding the supply of housing finance internationally,MBS also involved quite new sets of risks and costs and frag-mented the process of mediation of housing finance. These effectscontrast with those of the “new” financing instruments used bythe traditional suppliers throughout the 1980s, which did notgreatly alter the mediation of housing finance. The mechanismsfor origination, servicing, and funding of loans, for example,remained very much intact within the role of the traditionalhousing finance supplier.

310 Michael Pryke and Tim Freeman

Tab

le 2

. S

up

ply

of

Lo

an

s fo

r H

ou

se P

urc

ha

se:

Net

Ad

va

nce

s a

nd

Ba

lan

ces

Ou

tsta

nd

ing

,19

80–1

992

(mil

lio

n £

)

Insu

ran

ceO

ther

Oth

erB

uil

din

gL

ocal

Com

pan

ies

and

Fin

anci

alP

ubl

icS

ocie

ties

Au

thor

itie

sP

ensi

on F

un

dsB

ank

sIn

stit

uti

ons

Sec

tor

Tot

ala

Net

adv

ance

s du

rin

g pe

riod

1980

5,72

245

426

459

3—

341

7,28

219

816,

331

269

882,

448

—35

39,

308

1982

8,14

755

56

5,07

8—

356

14,1

4219

8310

,928

–306

126

3,53

122

540

14,3

1919

8414

,572

–195

250

2,04

348

0–4

217

,108

1985

14,7

11–5

0220

14,

223

491

6019

,194

1986

19,5

41–5

0635

64,

804

2,56

854

26,8

2319

8715

,076

–433

772

10,0

363,

956

4929

,466

1988

23,7

20–3

2944

710

,894

5,23

914

440

,110

1989

24,0

02–2

3030

7,16

93,

028

134

34,1

3319

9024

,140

–322

124

6,41

12,

324

–100

32,5

7719

9120

,567

–370

–223

4,80

62,

159

–435

26,4

94

Bal

ance

s ou

tsta

ndi

ng

1980

42,6

963,

809

2,03

02,

880

—1,

026

52,4

4119

8149

,019

3,08

02,

118

5,67

3—

1,37

961

,269

1982

57,1

524,

635

2,12

410

,751

—1,

737

76,3

9919

8368

,056

4,32

92,

250

14,8

45—

1,77

891

,258

1984

82,5

864,

134

2,50

016

,888

480

1,73

710

7,84

519

8597

,213

3,63

22,

700

21,1

1197

11,

798

126,

454

1986

116,

640

3,12

63,

135

25,9

163,

539

1,85

215

0,66

919

8713

1,44

72,

693

3,90

435

,949

7,49

51,

901

175,

894

Mortgage-Backed Securitization in the United Kingdom: The Background 311

Tab

le 2

. S

up

ply

of

Lo

an

s fo

r H

ou

se P

urc

ha

se:

Net

Ad

va

nce

s a

nd

Ba

lan

ces

Ou

tsta

nd

ing

,19

80–1

992

(mil

lio

n £

) (c

onti

nu

ed)

Insu

ran

ceO

ther

Oth

erB

uil

din

gL

ocal

Com

pan

ies

and

Fin

anci

alP

ubl

icS

ocie

ties

Au

thor

itie

sP

ensi

on F

un

dsB

ank

sIn

stit

uti

ons

Sec

tor

Tot

ala

Bal

ance

s ou

tsta

ndi

ng

(con

tin

ued

)

1988

155,

167

2,36

44,

504

45,3

3714

,227

2,04

522

6,74

119

8915

2,54

22,

134

4,51

679

,193

17,4

132,

179

257,

977

1990

176,

682

1,81

24,

640

85,6

7723

,555

2,07

529

4,44

219

9119

7,24

91,

442

4,40

790

,374

25,7

681,

641

320,

881

1992

b20

4,87

71,

189

4,23

493

,182

25,3

861,

545

330,

466

Sou

r ce :

Dat

a fr

om H

ous i

ng

Fin

anc e

, 19

91,

No.

9;

1992

, N

o. 1

6.N

ote :

Abb

ey N

atio

nal

plc

was

cla

ssif

ied

as a

ban

k f

r om

th

ird

quar

ter

1989

.a B

ecau

se s

ome

info

r mat

ion

fr o

m t

he

orig

inal

tab

le i

s om

itte

d, n

ot a

ll t

otal

s ar

e ex

act.

b S

econ

d qu

arte

r .

312 Michael Pryke and Tim Freeman

What is more, MBS exposes certain characteristics of the U.K.housing finance system, such as the prepayment of mortgages, tofresh scrutiny so that risks historically internal to the U.K.housing finance circuit now have to be calculated and priced atcompetitive rates.

With such points in mind, this article is an attempt to set out theworking of MBS in the United Kingdom to date and to explorethe feasibility of expanding its use to include the traditionalhousing finance suppliers in the United Kingdom, the buildingsocieties.

From traditional to more complex systems ofintermediation

The traditional system

Under the traditional system of mortgage finance, the process oftransferring funds from savers to borrowers was extremelysimple, using a single intermediary (figure 1). In this context therole of the intermediary, the building society, was to maintain apositive margin between the source of funds and the use of fundsto cover cost.

Figure 1. Simple Intermediation

Intermediary

Source of funds Use of funds

Retail savingsFirst residential

mortgages

The purpose of the intermediary was to provide an effectivechannel for savers’ surpluses to meet borrowers’ deficits. Thisstyle of intermediation embraced the assessment of credit anddefault risk, liquidity and maturity risk, and interest rate risk.Furthermore, building societies performed all three basic hous-ing finance functions: origination, servicing (i.e., collecting,accounting, and enforcement of the mortgage instrument), and

Mortgage-Backed Securitization in the United Kingdom: The Background 313

funding of the loan. As this suggests, the special circuit offinance operated to exclude many of the potential risks.

These three main risk-bearing functions were dealt with by thesimplicity and the narrow range of both savings and mortgageinstruments. In particular, savings instruments and variable-rate mortgages meant that there was little difficulty in matchingthe rates required by savers to those charged to borrowers. Onthe other hand, there was little incentive to minimize the costs ofintermediation. Moreover, liquidity and maturity risk wereminimized, as prepaid sums could be reinvested in new mort-gages at equivalent rates. The conservative nature of this regimealso limited default risk.

The changed pattern of intermediation

Modern intermediation has resulted from deregulation (leadingto increased competition from a wide range of institutions) andinnovations in information technology. These changes have madespecialization in different activities more possible while allowingthe transfer of risks between sectors. Modern intermediariesmay access a vast array of funds, while at the same time offeringa fuller range of mortgage products and reducing the costs ofintermediation (figure 2).

The opening up of the U.K. housing finance market has producedan environment in which the specialist circuit has been inte-grated into wider macroeconomic change and in which mortgagerates need not now be linked directly with specific costs of fundsbut may instead relate to aggregate costs of retail and wholesalefunds or a mix of wholesale instruments. But this new environ-ment has introduced new risk. The need to develop means ofboth reducing and transferring risks has thus become apparent.Because of competition among lenders to maintain or increasemarket shares, risks (such as default among marginal borrow-ers) all increase substantially. Similarly, the wider range ofinstitutional lenders means that their requirements in terms ofmaturity, and particularly certainty about their maturity, arequite different from those of a traditional retail lender.

Developments on all these fronts, however, have so far beenrelatively slow. Most funds that have not come from the retailmarket have been raised by building societies and banks throughtraditional wholesale market transactions.

314 Michael Pryke and Tim Freeman

Fig

ure

2.

Mo

der

n I

nte

rmed

iati

on

Inte

rmed

iary

Wh

oles

ale

Ret

ail

Pu

blic

ly t

r ade

d

CD

sE

ur o

bon

dsS

ecu

r iti

zati

onC

omm

erc i

al p

aper

Neg

otia

ble

bon

ds

Pr i

vate

pla

c em

ent

Loa

ns

from

ban

ks

Sec

ur i

tiza

tion

Tim

e de

posi

ts

Low

in

ter e

st

Tr a

nsa

c tio

nR

egu

lar

savi

ngs

Sav

e as

You

Ear

n(S

AY

E)

Hig

h i

nte

r est

Ter

m a

c cou

nts

Use

of

fun

ds

Com

mer

cial

mor

tgag

es a

nd

mis

c ell

aneo

us

Inve

stm

ents

in

r eal

est

ate

Un

sec u

r ed

loan

s

For

eign

cu

r ren

cyL

ink

edIn

tere

st o

nly

Rep

aym

ent

Yen

Sw

iss

fran

cE

uro

pean

Cu

r ren

cyU

nit

U.S

. do

llar

Deu

tsch

mar

kC

anad

ian

dol

lar

Du

tch

flo

r in

En

dow

men

tpe

nsi

on u

nit

Fir

st r

esid

enti

alm

ortg

ages

Sou

rce

of f

un

ds

Oth

er r

esid

enti

alm

ortg

ages

Sec

ond

c har

ge l

oan

sN

on-o

wn

er-o

c cu

pied

Hou

sin

g A

ssoc

iati

ons

Mortgage-Backed Securitization in the United Kingdom: The Background 315

Nevertheless, the way centralized lenders operate and the waythey link with other agents suggest a degree of disintermediationwithin the housing finance markets in the areas of origination,servicing, and funding of mortgages. The underlying financinginstruments appear more complex, while the position of themortgagor may appear to be more risk laden as a result. Thepath into owner occupation now takes the mortgagor from alargely domestic environment into one in which internationalbanking and capital markets are accessed either to supplement(in the case of building societies) or to replace (in the case ofcentralized lenders) retail funds.

The new funding framework is not simply linking the mortgagorand originator indirectly with capital market investors; it is alsointroducing a new subset of specialist roles for such agents asadministrators, credit enhancers, pool insurers, and issuers. Theremainder of this article provides an overview of these changesand a tentative description of their influence on the provision offinance for owner occupation.

The form of mortgage-backed securitization in theUnited Kingdom

MBS in the United Kingdom has grown out of methods of financ-ing housing markets in the United States (e.g., see Ball 1990;Mortgage-Backed Securities 1988). All in all, the types of changein the housing markets in the United States over the past decadeor so demonstrate that traditional retail funding and originatingmethods are not an immutable framework (Gabriel 1987), some-thing that is becoming clearer in the United Kingdom.

The characteristics of mortgage-backed securitization

Securitization, broadly defined, increasingly is a characteristic ofbank credit in international financial markets (Bank for Interna-tional Settlements 1986; Developments 1989). The growth of thesecuritization of mortgages in the United Kingdom encompassesboth the conversion of mortgages into tradable financial instru-ments and the growth of negotiable instruments, such asfloating-rate notes (FRNs). From the mid-1980s, FRNs tended tosupplant bank loans as a form of borrowing and encouraged thegrowth of disintermediation in the financial markets, as inves-tors and borrowers traded directly with one another (Bank forInternational Settlements 1986).

316 Michael Pryke and Tim Freeman

The broad function of securitization is to package and marketdebt primarily in the capital markets. Securitization is a way tosubstitute tradable instruments for direct borrowing from finan-cial institutions. A mortgage-backed issue generally will take theform of an FRN, floated at a margin above LIBOR with interestpayable quarterly. Against these securities, variable-rate,nonamortizing (residential) mortgages are offered as security.Mortgage payments are usually based on interest only, with theprincipal payable on maturity of the mortgage.

The securitization of mortgages involves either the creation of apass-through security, in which interest and principal are“passed through” to the holders of the securities or certificates,or the issue of mortgage-backed bonds, which in effect are debtobligations collateralized by mortgages (see Baring Brothers1989a, 1989b, 1992; Mortgage-Backed Securities 1988).

Development of the U.K. mortgage-backed securities market

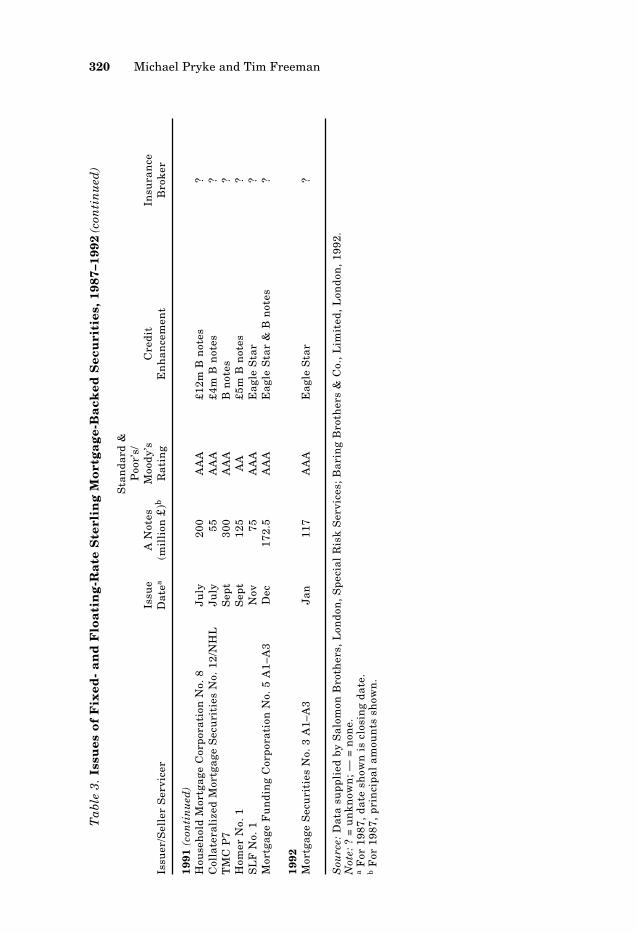

To date, more than £14 billion of mortgage-backed securitieshave been issued publicly in the United Kingdom, with an esti-mated further £3 billion to £5 billion placed privately. Thisvolume represents about 80 public issues, the vast majority ofwhich have been floating-rate rather than fixed-rate bonds,mostly backed by variable-rate domestic mortgages (table 3).

The U.K. MBS market effectively began in 1987 with the issue ofabout £1 billion of mortgage-backed securities. The annualvolume of issuance had grown to £3.2 billion in 1988, but fewnew issuers were coming to the market by the end of that year.Market activity slowed to £2.6 billion in 1989 and £2.3 billion in1990. These decreases in new issues reflected in part the sharplyreduced activity in the U.K. residential mortgage market and inpart the decreased margin between mortgage rates and LIBOR,which made securitization economically less attractive as amethod of funding mortgage lending (figure 3).

With MBS at a low level during 1991 and 1992, total issuancehad grown to £12 billion by the end of February 1993. Thisfigure must be compared with a total residential mortgage mar-ket of around £320 billion, 80 percent of which is originated bybuilding societies and major banks. Although it has developedvery rapidly, the U.K. MBS market remains very small com-pared with the estimated £1,000 billion or more of finance raisedthrough securitization in the United States.

Mortgage-Backed Securitization in the United Kingdom: The Background 317

Tab

le 3

. Is

sues

of

Fix

ed-

an

d F

loa

tin

g-R

ate

Ste

rlin

g M

ort

ga

ge-

Ba

cked

Sec

uri

ties

, 19

87–1

992

Sta

nda

rd &

Poo

r’s/

Issu

eA

Not

esM

oody

’sC

redi

tIn

sura

nce

Issu

er/S

elle

r S

ervi

cer

Dat

ea(m

illi

on £

)bR

atin

gE

nh

ance

men

tB

rok

er

1987

NH

L F

irst

Fu

ndi

ng

Cor

pora

tion

plc

/T

he

Nat

ion

al H

ome

Loa

ns

Cor

pora

tion

plc

Feb

24

50A

AA

Su

n A

llia

nce

?T

MC

Mor

tgag

e S

ecu

riti

es N

o. 1

plc

/T

he

Mor

tgag

e C

orpo

rati

onM

arch

31

200

AA

Su

n A

llia

nce

?H

MC

Mor

tgag

e S

ecu

riti

es p

lc/

Hou

seh

old

Mor

tgag

e C

orpo

r ati

on p

lcJu

ly 1

615

0A

AA

Su

n A

llia

nc e

?T

MC

Mor

tgag

e S

ecu

r iti

es N

o. 2

plc

/T

he

Mor

tgag

e C

orpo

r ati

onA

ug

2610

0A

AE

agle

Sta

r?

NH

L S

econ

d F

un

din

g C

orpo

r ati

on p

lc/

Th

e N

atio

nal

Hom

e L

oan

s C

orpo

r ati

on p

lcO

c t 8

100

AA

AE

agle

Sta

r?

TM

C M

ortg

age

Sec

ur i

ties

No.

3 p

lc/

Th

e M

ortg

age

Cor

pora

tion

Oc t

30

100

AA

Eag

le S

tar

?N

HL

Th

ird

Fu

ndi

ng

Cor

pora

tion

plc

/T

he

Nat

ion

al H

ome

Loa

ns

Cor

pora

tion

plc

Nov

30

100

AA

B N

otes

?T

MC

Mor

tgag

e S

ecu

r iti

es N

o. 4

plc

/T

he

Mor

tgag

e C

orpo

rati

onN

ov 3

010

0A

AE

agle

Sta

r?

Dom

us

Mor

tgag

e F

inan

ce N

o. 1

plc

/C

hem

ical

Ban

k H

ome

Loa

ns

Lim

ited

Dec

410

0A

+S

un

All

ian

ce?

1988

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 2

Jan

14

175

AA

AJu

nio

r /S

enio

r—

Mor

tgag

e F

un

din

g C

orpo

rati

on N

o. 1

Feb

23

175

AA

Eag

le S

tar

Spe

c ial

Ris

k S

ervi

c es

Th

e M

ortg

age

Cor

pora

tion

No.

5M

arc h

112

5A

AA

Poh

jola

/Eag

le S

tar

Spe

c ial

Ris

k S

ervi

c es

Th

e M

ortg

age

Cor

pora

tion

No.

6M

arc h

11

100

AA

AP

ohjo

la/E

agle

Sta

rS

pec i

al R

isk

Ser

vic e

sR

esid

enti

al P

r ope

r ty

Sec

ur i

ties

No.

1/B

of

Irel

and

Apr

il 1

120

0A

AA

Sk

andi

a/P

ohjo

la/E

SS

pec i

al R

isk

Ser

vic e

sT

he

Mor

tgag

e C

orpo

rati

on N

o. 7

Apr

il 2

510

0A

AA

Poh

jola

/Eag

le S

tar

Spe

c ial

Ris

k S

ervi

c es

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 3

May

16

150

AA

AJu

nio

r /S

enio

r—

318 Michael Pryke and Tim Freeman

Tab

le 3

. Is

sues

of

Fix

ed-

an

d F

loa

tin

g-R

ate

Ste

rlin

g M

ort

ga

ge-

Ba

cked

Sec

uri

ties

, 19

87–1

992

(con

tin

ued

)

Sta

nda

rd &

Poo

r’s/

Issu

eA

Not

esM

oody

’sC

redi

tIn

sura

nce

Issu

er/S

elle

r S

ervi

cer

Dat

ea(m

illi

on £

)bR

atin

gE

nh

ance

men

tB

rok

er

1988

(co

nti

nu

ed)

Th

e M

ortg

age

Cor

pora

tion

No.

8M

ay 2

710

0A

AA

Poh

jola

/Eag

le S

tar

Spe

cial

Ris

k S

ervi

ces

MA

ES

Fu

ndi

ng/

CIB

CJu

ne

620

0A

AA

Han

sa/E

agle

Sta

rS

peci

al R

isk

Ser

vice

sR

esid

enti

al P

rope

rty

Sec

uri

ties

No.

2/B

of

Irel

and

Jun

e 30

200

AA

AH

ansa

/Eag

le S

tar

Spe

cial

Ris

k S

ervi

ces

Exc

lusi

ve F

inan

ce N

o. 1

/TS

BJu

ly 2

713

5A

AA

Han

sa/E

agle

Sta

rS

peci

al R

isk

Ser

vice

sT

he

Mor

tgag

e C

orpo

r ati

on N

o. 9

Au

g 1

200

AA

AP

ohjo

la/E

agle

Sta

rS

pec i

al R

isk

Ser

vic e

sM

ortg

age

Fu

ndi

ng

Cor

por a

tion

No.

2A

ug

411

5A

AA

/AA

Jun

ior /

Sen

ior +

ES

Spe

c ial

Ris

k S

ervi

c es

Th

e M

ortg

age

Cor

por a

tion

No.

10

Sep

t 1

200

AA

AP

ohjo

la/E

agle

Sta

rS

pec i

al R

isk

Ser

vic e

sN

atio

nal

Hom

e L

oan

s N

o. 4

Sep

t 20

100

AA

AJu

nio

r /S

enio

r—

Mor

tgag

e S

ecu

r iti

es N

o. 1

/FM

SO

c t 1

220

AA

A/A

AJu

nio

r /S

enio

r +E

SS

pec i

al R

isk

Ser

vic e

sM

ortg

age

Fu

ndi

ng

Cor

por a

tion

No.

3O

c t 8

120

AA

A/A

AJu

nio

r /S

enio

r +E

SS

pec i

al R

isk

Ser

vic e

sT

he

Mor

tgag

e C

orpo

rati

on N

o. 1

1O

c t 2

250

0A

AA

Poh

jola

/Eag

le S

tar

Spe

c ial

Ris

k S

ervi

c es

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 1

01O

c t 2

410

0A

AA

Jun

ior /

Sen

ior /

AIG

—

1989

Sec

ure

d R

esid

enti

al F

un

din

g N

o. 1

Mar

c h15

0A

AA

Jun

ior /

Sen

ior

—H

ouse

hol

d M

ortg

age

Cor

pora

tion

No.

102

Mar

c h10

0A

AA

Jun

ior /

Sen

ior /

AIG

—M

AE

S E

CP

No.

1/C

IBC

200

A1P

1E

agle

Sta

rS

pec i

al R

isk

Ser

vic e

sM

AE

S F

un

din

g N

o. 2

/CIB

CJu

ne

300

AA

AE

agle

Sta

r /H

ansa

/S

pec i

al R

isk

Ser

vic e

sH

anov

er R

eC

olla

ter a

lize

d M

ortg

age

Sec

ur i

ties

No.

1/N

HL

Jun

e21

0A

AA

Jun

ior /

Sen

ior

—G

race

chu

r ch

Mor

tgag

e F

inan

ce/B

arc l

ays

Jun

e17

5A

AA

Su

n A

llia

nce

Spe

c ial

Ris

k S

ervi

c es

TM

C P

IMB

S N

o. 1

Jun

e25

0A

AA

Eag

le S

tar /

Han

saS

pec i

al R

isk

Ser

vic e

sH

ouse

hol

d M

ortg

age

Cor

pora

tion

No.

4A

ug

150

AA

AJu

nio

r /S

enio

r—

Col

late

r ali

zed

Mor

tgag

e S

ecu

r iti

es N

o. 2

/NH

LS

ept

250

AA

AJu

nio

r /S

enio

r—

Mor

tgag

e S

ecu

r iti

es N

o. 2

/FM

SS

ept

150

AA

AE

agle

Sta

r /H

anov

er R

eS

pec i

al R

isk

Ser

vic e

sT

MC

PIM

BS

No.

2S

ept

250

AA

AS

un

/Roy

alS

pec i

al R

isk

Ser

vic e

sT

MC

PIM

BS

No.

3N

ov30

AA

AE

agle

Sta

r /C

apit

al R

eS

pec i

al R

isk

Ser

vic e

sT

MC

PIM

BS

No.

4D

ec25

0A

AA

Su

n A

llia

nce

/Roy

alS

pec i

al R

isk

Ser

vic e

sT

empl

e C

our t

Mor

tgag

es N

o. 1

Dec

175

AA

AS

un

All

ian

ceS

pec i

al R

isk

Ser

vic e

s

Mortgage-Backed Securitization in the United Kingdom: The Background 319

Tab

le 3

. Is

sues

of

Fix

ed-

an

d F

loa

tin

g-R

ate

Ste

rlin

g M

ort

ga

ge-

Ba

cked

Sec

uri

ties

, 19

87–1

992

(con

tin

ued

)

Sta

nda

rd &

Poo

r’s/

Issu

eA

Not

esM

oody

’sC

redi

tIn

sura

nce

Issu

er/S

elle

r S

ervi

cer

Dat

ea(m

illi

on £

)bR

atin

gE

nh

ance

men

tB

rok

er

1990

Col

late

rali

zed

Mor

tgag

e S

ecu

riti

es N

o. 3

/NH

LF

eb21

6A

AA

Jun

ior/

Sen

ior

—B

ear

Ste

arn

s M

ortg

age

Sec

uri

ties

No.

1M

ar10

6A

AA

Eag

le S

tar/

Han

saS

peci

al R

isk

Ser

vice

sT

MC

PIM

BS

Tra

nch

e N

o. 5

Apr

il20

0A

AA

Su

n A

llia

nce

Spe

cial

Ris

k S

ervi

ces

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 5

Apr

il15

0A

AA

Jun

ior/

Sen

ior

—C

olla

ter a

lize

d M

ortg

age

Sec

ur i

ties

No.

4/N

HL

Jun

e20

0A

AA

Eag

le S

tar /

Han

saS

pec i

al R

isk

Ser

vic e

sC

olla

ter a

lize

d M

ortg

age

Sec

ur i

ties

No.

5/N

HL

July

250

AA

AS

un

All

ian

c eS

pec i

al R

isk

Ser

vic e

sH

ouse

hol

d M

ortg

age

Cor

por a

tion

No.

6A

ug

140

AA

AJu

nio

r /S

enio

r—

TM

C P

IMB

S T

r an

c he

No.

6S

ept

250

AA

AS

un

All

ian

c eS

pec i

al R

isk

Ser

vic e

sM

ortg

age

Sec

ur i

ties

No.

2/F

MS

Tap

Iss

ue

Sep

t50

AA

AE

agle

Sta

r /H

anov

er R

eS

pec i

al R

isk

Ser

vic e

sC

olla

ter a

lize

d M

ortg

age

Sec

ur i

ties

No.

6/N

HL

Sep

t22

5A

AA

Su

n A

llia

nc e

Spe

c ial

Ris

k S

ervi

c es

ST

AR

S N

o. 1

/Cit

iban

kN

ov47

5A

AA

Su

n A

llia

nc e

Spe

c ial

Ris

k S

ervi

c es

1991

Col

late

r ali

zed

Mor

tgag

e S

ecu

r iti

es N

o. 7

/NH

LJa

n30

0A

AA

Eag

le S

tar /

Han

over

Re

Spe

c ial

Ris

k S

ervi

c es

TM

C P

IMB

S T

ran

che

No.

7F

eb21

0A

AA

Su

n A

llia

nce

Spe

c ial

Ris

k S

ervi

c es

Col

late

r ali

zed

Mor

tgag

e S

ecu

r iti

es N

o. 8

/NH

LF

eb20

0A

AA

Su

n A

llia

nce

Spe

c ial

Ris

k S

ervi

c es

Tem

ple

Cou

r t M

ortg

ages

No.

2/A

1A

pril

75A

AA

Eag

le S

tar

?T

empl

e C

our t

Mor

tgag

es N

o. 2

/A 2

Apr

il75

AA

AE

agle

Sta

r?

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 7

May

100

AA

AE

agle

Sta

r?

Col

late

r ali

zed

Mor

tgag

e S

ecu

r iti

es N

o. 9

/NH

LM

ay60

AA

AT

rygg

Han

sa?

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 1

03M

ay12

5A

AH

MC

Mor

t N

otes

No.

7?

Col

late

r ali

zed

Mor

tgag

e S

ecu

r iti

es N

o. 1

0/N

HL

May

100

AA

AC

MS

9 A

3 N

otes

?C

olla

ter a

lize

d M

ortg

age

Sec

ur i

ties

No.

9/N

HL

May

40A

AA

—?

Mor

tgag

e F

un

din

g C

orpo

rati

on N

o. 4

May

100

AA

AE

agle

Sta

r?

Col

late

r ali

zed

Mor

tgag

e S

ecu

r iti

es N

o. 1

1/N

HL

Jun

e15

0A

AA

£10.

5m B

not

es?

320 Michael Pryke and Tim Freeman

Tab

le 3

. Is

sues

of

Fix

ed-

an

d F

loa

tin

g-R

ate

Ste

rlin

g M

ort

ga

ge-

Ba

cked

Sec

uri

ties

, 19

87–1

992

(con

tin

ued

)

Sta

nda

rd &

Poo

r’s/

Issu

eA

Not

esM

oody

’sC

redi

tIn

sura

nce

Issu

er/S

elle

r S

ervi

cer

Dat

ea(m

illi

on £

)bR

atin

gE

nh

ance

men

tB

rok

er

1991

(co

nti

nu

ed)

Hou

seh

old

Mor

tgag

e C

orpo

rati

on N

o. 8

July

200

AA

A£1

2m B

not

es?

Col

late

rali

zed

Mor

tgag

e S

ecu

riti

es N

o. 1

2/N

HL

July

55A

AA

£4m

B n

otes

?T

MC

P7

Sep

t30

0A

AA

B n

otes

?H

omer

No.

1S

ept

125

AA

£5m

B n

otes

?S

LF

No.

1N

ov75

AA

AE

agle

Sta

r?

Mor

tgag

e F

un

din

g C

orpo

r ati

on N

o. 5

A1–

A3

Dec

172.

5A

AA

Eag

le S

tar

& B

not

es?

1992

Mor

tgag

e S

ecu

r iti

es N

o. 3

A1–

A3

Jan

117

AA

AE

agle

Sta

r?

Sou

r ce :

Dat

a su

ppli

ed b

y S

alom

on B

r oth

ers,

Lon

don

, S

pec i

al R

isk

Ser

vic e

s; B

arin

g B

r oth

ers

& C

o.,

Lim

ited

, L

ondo

n,

1992

.N

ote :

? =

un

kn

own

; —

= n

one.

a F

or 1

987,

dat

e sh

own

is

c los

ing

date

.b

For

198

7, p

r in

c ipa

l am

oun

ts s

how

n.

Mortgage-Backed Securitization in the United Kingdom: The Background 321

Fig

ure

3.

Issu

e M

arg

ins

for

Pu

bli

c S

enio

r S

terl

ing

Mo

rtg

ag

e-B

ack

ed S

ecu

riti

es

Discounted Margin to Investor (basis points)

100 80 60 40 20 0 03

-Mar

-87

07-A

pr-8

831

-Mar

-89

14-S

ep-9

001

-May

-91

15-A

pr-9

230

-Oc t

-87

25-J

ul-

8816

-Mar

-90

29-J

an-9

106

-Sep

-91

27-S

ep-9

3

Lau

nch

Dat

e

Not

e : M

argi

ns

are

wei

ghte

d by

ave

rage

lif

e an

d si

ze o

f is

sue.

322 Michael Pryke and Tim Freeman

The U.K. market has, however, produced some interesting inno-vations during its short history. First, there have been three so-called arrears bonds. As the term implies, these issues packagemortgages that are typically at least six months in arrears. Highlevels of credit enhancement to produce triple A ratings from therating agencies have made these bonds readily salable to sophis-ticated investors. Another innovation worthy of mention was therepackaging of the slow-pay tranche of a two-tranche (fast-pay/slow-pay) FRN by a subsidiary of Household Mortgage Corpora-tion by way of a fixed-rate bond issue secured on the slow-paytranche of the FRN. The fast-pay tranche of the FRN and thefixed-rate bond were aimed at different investor bases, thusbroadening the investor base for the issue and so reducing itsoverall cost.

The cost of MBS in the United Kingdom has varied considerablyas the market has developed. In the early days of the market,new issues showed a yield to investors of about 25 to 30 basispoints over LIBOR—slightly higher than the yield on similardebt issued by building societies. The initial investor base con-sisted mostly of banks, but as corporations gradually began torecognize the high credit quality of mortgage-backed securitiesand to invest the high liquidity they then had, yields to investorsfell gradually to a low of just 18 basis points over LIBOR in mid-1989. This yield compared favorably with debt costs achieved bybuilding societies at that time.

Several factors combined over the next two years to push yieldsback up to a high of 75 to 80 basis points over LIBOR: (1) asharp reduction in corporate liquidity, leaving the banks onceagain the predominant investor base; (2) uncertainty overwhether for bank investors mortgage-backed securities wouldretain a 50 percent risk asset weighting or move to a 100 percentweighting in line with European Community proposals; and (3)growing uncertainty over the credit quality of U.K. mortgagelending that, although not affecting the performance of anymortgage-backed securities, raised price expectations. The subse-quent resolution of the regulatory treatment of mortgage-backedsecurities in favor of a 50 percent risk asset weighting, togetherwith the dearth of new issues, has brought secondary marketyields back to 20 to 25 basis points over LIBOR. This remains10 to 12 basis points higher than the yield offered by similarbuilding society paper.

While a few early issues of mortgage-backed securities weredouble A rated, it has become market practice to credit-enhanceissues to produce a triple A rating at launch. Some issues have

Mortgage-Backed Securitization in the United Kingdom: The Background 323

been subsequently downgraded because of the downgrading ofthe insurance companies providing credit enhancement. How-ever, no issues have been downgraded because of the perfor-mance of the underlying mortgage pool, and there have been nodefaults in payment of principal or interest, even on the juniornote tranches of those issues using a credit enhancement struc-ture based on senior and junior notes.

Integration in a securitized environment

Integral to the gradual move away from a retail-dominatedsystem of raising funds toward direct access to the capital mar-kets is the enhancement of the attributes of a domestic mortgageso that it equates with other capital market investment media(Drake and Llewellyn 1987, 2; Simpson 1988, 11).

Once the securitized mortgages are sold, they are no longer heldin the originator’s portfolio. Any future transactions in themtake place in the secondary mortgage market. Ownership of thenotes, which gives rights to the income and principal from theunderlying mortgages, may be traded any number of times(depending on the depth of the market). Perhaps it should bereiterated that under securitization the mortgage itself is notsold; securitization is simply a process by which tradable notesare issued in relation to a specific pool of mortgages that pass onto an investor (indirectly via the issuing vehicle) interest andprincipal from the mortgagor. A pure secondary market transac-tion would see the actual mortgage traded among financialinstitutions as part of a package of mortgages by transfer of thelegal interest in the mortgages; here the legal rights to themortgages are bought and sold.

More recently, secondary market activity has increased. Bothforms of MBS inevitably involve the appraisal of the perceivedriskiness of the underlying pool of mortgages. The next sectionoutlines this process of “credit rating.”1

Credit rating mortgage-backed securities

The market in securities backed by mortgages has embracedprivate sector capital market agents for two reasons: (1) toappraise the risks associated with the securitization vehicle and

1 For further information, see Baring Brothers 1989a, 1989b, 1992; Moody’s1988; Standard & Poor’s 1989.

324 Michael Pryke and Tim Freeman

the underlying assets (the process of credit rating), and(2) through a range of insurance instruments, to cushion inves-tors from these risks (the process of credit enhancement). Theneed for assessment agencies arises also for historical reasons.

In the past, outside parties were not needed to assess the qualityof lending undertaken by originators (mainly building societies)because the originator and holder of a mortgage were usually thesame organization. With the rise of securitization, however,lending policies—which cover such areas as loan-to-value ratiosand loan-to-income ratios—are now open to scrutiny, as areother aspects of the mortgage business, such as prepaymentsthat were, in a sense, internal to the old regime of housing fi-nance. Under an increasingly “unbundled” (Follain and Zorn1990) financing system, prepayments may now be seen as aproblem for outside investors as they attempt to assess thepredictability of the income flow on their investment. (Similarly,the requirements of the secondary markets are now shaping bothlending policies and products.)

Five areas for risk assessment

There are five features of the U.K. mortgage market that haveparticular bearing on the risk assessment and rating of mort-gages to be pooled and then securitized.

Variable rates. The first feature is that mortgage rates in theUnited Kingdom are variable, not set in accordance with anagreed index. Instead, rates are determined by individual orga-nizations. Competition among originators in setting and chang-ing mortgage rates tends to produce a general unity of movementin interest rates.

Further advances and substitutions. Second, other uncertaintiesare introduced through the effect of further advances and substi-tutions. Mortgage loans may be increased to finance home im-provements or non-mortgage-related consumption. This actionraises the chances of credit losses because of the increased loan-to-value ratio and liquidity shortfalls. These uncertainties maybe accounted for by bringing them into the initial calculations forcredit loss and liquidity shortfall under a worst-case scenario. Amaximum advance figure may provide some assurance as to thefull extent of first mortgages plus subsequent advances.

Repayment terms. A third area of uncertainty is mortgage repay-ment terms. The mortgagor’s ability to meet interest and principal

Mortgage-Backed Securitization in the United Kingdom: The Background 325

repayments will vary across different mortgage products. Inimportant ways, the interest-principal systems alter risk assess-ment and, to some extent, shift risk from the mortgagor andmortgaged property alone to other parties involved in the pro-cess. For instance, with an endowment-type policy the mortgagoris under an obligation to pay interest to the lender in addition topaying a premium on the endowment policy (the means for re-paying the principal). If, as is often the case, the endowmentpolicy provider is a separate party, the overall rating of themortgage pool must then broaden to include the insurer. That is,the insurer’s ability to pay the policy on maturity must be takeninto account in assessing overall risk.

Loan administration. Fourth, loan administration forms animportant part of the overall MBS transaction. Loan administra-tion is often a responsibility delegated (through power of attor-ney) by the note trustee, so that the administrator acts in manyrespects (although not wholly) independently in areas such assubstitutions and further advances.

Transfers. Fifth, transfers of mortgages over land may be legalor equitable assignments. The rating process will be concernedparticularly with the security offered to the note holder by equi-table interests in land.

New intermediaries, new specializations, new risks

The benefits of securitization—such as a more reactive supply ofmortgage finance and a greater scope for widening the range ofmortgage products available to the public—bring with them newproblems related to the correct pricing of risk, new forms ofintermediary, and renewed liquidity.

Existing housing risk must be reallocated and new financialmarkets distributed among the agents—the mortgagor, theoriginator, the lender, the administrator, the insurers, the issu-ers, and the bondholders—who form this new structure for hous-ing finance (figure 4).

An example of securitization

The relationship between the originators, the issuer, the funders,and the eventual note holders under securitization is presentedin figure 5. The borrowers are brought into the process throughthe marketing and sales activity of a range of agreed originators

326 Michael Pryke and Tim Freeman

Figure 4. Disintermediation and the Unbundling of Activities inSecuritization

Changes and New Roles

Increasing range and sophistication, costs of20 to 30 basis points over LIBOR for normalvariable-rate mortgages; more prosaic mortgagesare costlier to get through the rating process butcan be taken off balance sheet throughsecuritization.

Organization actually sells the mortgage; mayrange from traditional society or specialistmortgage bank to insurance company; use ofinformation technology to categorize and assessweighted average recovery and default rates.

May act for a nonhousing market specialist, suchas an insurance company; may deal in mortgagesfor public placing or private transaction; respon-sible for processing and quality control ofmortgages and may be responsible for makingoriginal offer, further advances, and dealing witharrears and further advances.*

Need only be mentioned in legal documentation;shielded from housing market by originator andadministrator; margin between LIBOR andmortgage rate attracted funders (particularlyforeign banks) in 1988; building societies ac-quired seasoned mortgage packages, paying 120basis points over par for such pools around 1988.Centralized lenders (unlike societies) rely totallyon LIBOR-related funds.

Mortgageproducts

Funders

Administration/mortgagecompany

Originators

Mortgage-Backed Securitization in the United Kingdom: The Background 327

Figure 4. Disintermediation and the Unbundling of Activities inSecuritization (continued)

* As Rose and Haney (1990) pointed out, referring to the U.S. markets,smaller mortgage companies are unable to distribute the costs of close scru-tiny of originators over a deep mortgage portfolio. In an increasingly competi-tive market in the United Kingdom (and in the United States), the ability toreduce such management and quality control risks is likely to influence thecomposition of mortgage funders, originators, and administrators and thecorrelation of their functions. These changes may also lead particular marketparticipants to concentrate on certain market segments.

Investment banks—the key agents in arrangingmoney and capital market finance.

The security has to be designed to attractinvestors; FRNs and fixed-rate notes throughwhich investors receive principal and interestgenerated on mortgage products must be suffi-cient to cover coupon on bonds; MBS are one ofthe highest yielding quality sterling instrumentscurrently available, yielding around 25 to 30basis points over LIBOR at end of 1990; however,MBS are subject to high reinvestment risk; endof 1990, 50 percent banks, 30 to 40 percentmoney market funds, around 20 percent corpora-tions and a few long-term institutions; no realprimary or secondary market in the U.K. to date;unpredictable average life deters investors.

Leadmanagers

Investors

328 Michael Pryke and Tim Freeman

Fig

ure

5.

An

Ex

am

ple

of

a M

ort

ga

ge

Co

mp

an

y’s

Str

uct

ure

an

d F

un

din

g

Mor

tgag

e co

mpa

ny

issu

esm

ortg

age

fun

ds t

o bo

rrow

er(s

)(i

n)d

irec

tly

Bor

row

ers

Ori

gin

ator

s/m

ortg

age

c om

pan

y

Ori

gin

ator

s m

ay i

ncl

ude

ban

ks,

mor

tgag

e fi

nan

ceco

mpa

nie

s, i

nsu

ran

ce c

ompa

-n

ies,

per

son

al f

inan

c e c

ompa

-n

ies:

th

ese

may

hav

e a

r epr

esen

tati

ve o

n m

ortg

age

c om

pan

y’s

boar

d of

dir

ecto

r sS

ervi

c es

and

adm

inis

ter s

mor

tgag

eF

un

din

gso

ur c

es

1–6

Inte

r est

rat

e m

anag

emen

tpo

ssib

le t

hr o

ugh

sou

r cin

gva

r iet

y of

mar

ket

s (s

ee k

ey)

Spe

c ial

-pu

rpos

eve

hic

le (

SP

V)

Sec

ur i

ty o

npa

r i p

ass u

bas

isF

inan

c in

g an

d sy

stem

sm

anag

emen

t; m

ain

bu

sin

ess;

fin

anc i

ng

and

r efi

nan

c in

glo

ans

secu

red

agai

nst

r esi

den

tial

pr o

per t

y by

fir

stle

gal m

ortg

age

Tru

st d

eben

ture

floa

tin

g c h

arge

over

all

ass

ets

ofm

ortg

age

com

pan

yT

rust

ees

Mortgage-Backed Securitization in the United Kingdom: The Background 329

Fig

ure

5.

An

Ex

am

ple

of

a M

ort

ga

ge

Co

mp

an

y’s

Str

uct

ure

an

d F

un

din

g (c

onti

nu

ed)

Insu

rer

Inve

stm

ent

ban

k

Man

agem

ent

advi

ce,

for

exam

ple,

abo

ut

rati

ng

proc

ess

and

issu

e pr

ice

for

secu

riti

es

Poo

l in

sura

nce

poli

cy

KE

Y1.

Loc

al a

uth

orit

ies

2.E

ur o

c om

mer

c ial

pap

er3.

Mon

ey m

ark

ets:

sh

ort-

ter m

deb

tan

d c u

r ren

c y4.

Ban

ks:

com

mer

c ial

cr e

dit

lin

es,

r evo

lvin

g c r

edit

, syn

dic a

ted

loan

s5.

Mu

ltio

ptio

n f

acil

itie

s6.

Sec

ur i

tiza

tion

Win

s m

anda

te t

o pl

ace

issu

e in

mar

ket

s; a

lso

desi

gns

SP

V; u

nde

r -w

r ite

s de

al; m

ay a

lso

act

as t

r ust

ee

12

34

Issu

es

For

pu

blic

iss

ues

, r a

tin

gpr

oces

s is

nec

essa

ry

Dis

trib

uti

on o

f n

otes

in

c api

tal m

ark

ets

Sec

ur i

tiza

tion

th

r ou

ghsu

bsid

iary

com

pan

ies

(pu

blic

an

d pr

ivat

eis

sues

)

Sou

r ce :

Ada

pted

fr o

m M

ortg

age

Fu

ndi

ng

Cor

pora

tion

(19

88).

330 Michael Pryke and Tim Freeman

who have contracted with the mortgage company and sometimeshave representation on its board. The mortgages are passed onto the mortgage company, which services and administers themeither directly or through a specialist administrator under con-tract. The mortgage administrator is responsible for making themortgage offer. As shown in the figure, the mortgages are often“warehoused” before securitization, making use of a range ofbanking market facilities. The security for these loans is held bythe trustee on a pari passu basis.

The range of agents involved in the U.K. MBS market is not verydifferent from that in the United States. One significant differ-ence, however, is in the use of trustees in the U.K. market. Thereare two types of trustees: those who hold the mortgage and othersecurity on behalf of note holders and those who hold the sharecapital of the companies issuing the mortgage-backed securities.In the latter instance, this role arises from the Bank of Englandand Building Societies Commission requirements that in order toachieve, for regulatory purposes, an off-balance-sheet treatmentof mortgage assets securitized, the bank or building societyoriginator should have no proprietary interest in the issuingcompanies.

The key agents involved in arranging finance, from both thebanking and capital markets for centralized lenders, are theinvestment banks. The investment banks are involved in theMBS market in the capacity of lead manager and underwriter ofthe issues. They are involved in the design and structuring of thespecial-purpose vehicle (SPV), advising the mortgage companyon the constitution of the portfolio, on the rating process, and onthe legal structure. For the mortgage company, the concern willbe the amount of capital available to it and its required returnon the whole issue, from design through selling the bonds.

The lead manager will be in contact with perhaps half a dozenpotential issuers to try to establish when they will reach a criti-cal volume of originated new mortgages; typically they will“warehouse off” these mortgages, before securitization, on thestrength of some form of banking facility. When a critical mass isreached, the mortgage company will want to sell these mort-gages into an SPV. The SPV will then issue a security that will,in a sense, take care of the funding for the remaining life of themortgages. All potential lead managers will be looking for thatcritical date and the mandate for the bond issue. It is then thatthe structuring and working together with the issuer will takeplace. If an issuer returns to the same lead bank, then new ideascan be incorporated readily into an existing structure.

Mortgage-Backed Securitization in the United Kingdom: The Background 331

Once the mandate has been won and the issue launched, the leadbank will have, say, £100 million of debt on its balance sheet,which it will want to remove as quickly as possible. If the man-date has been won on a competitive basis, the lead manager’smargin will be very close to what the investors will be preparedto pay for the notes. With FRNs, price does not change as muchas in the fixed-rate market because FRNs adjust with everycoupon period, so the extent to which they can diverge fromcurrent market rates is limited to the issue of new bonds withinthe coupon period and the extent to which the coupon on thatdebt is superseded by events. This movement is small comparedwith the divergence that may appear in a fixed-rate market.

An investment bank, acting as the lead manager, will be remu-nerated through a combination of underwriting fees paid on theamount of the issue and the difference between the price atwhich the lead manager buys the issue and the price at whichnotes are sold to investors. The remuneration of a lead manageris therefore a combination of a fixed (underwriting fee) and avariable “profit” (or loss) on the sale of notes, depending on thelead manager’s correct judgment of the investor base.

The lead manager is responsible for putting together the docu-mentation and working out the final structure with the mortgagecompany. Together, the lead manager and the issuer approachthe rating agencies—Moody’s or Standard & Poor’s—to obtainwhat is usually a triple A rating in the U.K. MBS markets.

In this example, the issuing company (or SPV) is owned by atrust with charitable status. The trustee ownership of the sharesof the SPV is designed to achieve an off-balance-sheet treatmentof the transaction from the originator’s point of view, and thetrust has charitable status for tax purposes. In practice, anyprofits arising within the SPV are stripped out by the originatorbefore payment of a nominal dividend on the shares of the SPV,which eventually flows through to the beneficiaries of the trust.At the end of the securitization process, any mortgages remain-ing within the SPV are typically repurchased by the originatingcompany (though the originator has no obligation to do so).

Before securitization, there are several ways to finance a mort-gage portfolio. Often the mortgages will be warehoused on thebalance sheet of the mortgage company and funded in the con-ventional wholesale (or retail) money markets with capitalprovided in accordance with the mortgage company’s regulatoryor banking covenant requirements. On occasion, however, evenat this warehousing stage, the mortgage portfolio may be

332 Michael Pryke and Tim Freeman

financed by, for example, a nonrecourse banking facility securedon the mortgages and credit-enhanced by agency pool insuranceor overcollateralization.

Before securitization, the mortgages are financed through theshort-term money markets (figure 5). The syndicated loan is anonrecourse facility and is secured through a fixed charge overthe pool of mortgages. The mortgage company uses credit en-hancement to secure this facility. In this example, mortgages areinsured through pool insurance. When the mortgages aresecuritized, the fixed charge is postponed through an immediatedischarge of the fixed charge and its immediate re-creation infavor of the trustee.

Pricing and investment market problems

Among the originators, lenders, issuers, and bondholders inparticular, MBS is a form of credit-risk transference. With theinclusion of rating agencies, the potentially volatile creditworthi-ness of parties—notably the mortgagors, the lenders, and theoriginators—may be countered by obtaining an investmentquality rating. Yet at the same time that this structure enablesfinancial market intermediaries to distribute risk, the growth inthe number of parties would seem to make the whole structuremore open to nonhousing macroeconomic fluctuations. Questionsarise therefore about how the price paid to each agent for bear-ing different types of risk is arrived at and how these risks aredefined. Are they defined, for instance, predominantly in termsof housing-related risks, related more to weakest link intermedi-ary risk? Or are they defined mainly in terms of interest rateand investment (or reinvestment) risks? Some of the mainproblems that have arisen in the pricing of these securities andtheir full acceptance as capital market paper are set out infigure 6.

Of the public issues, about £8 billion remains outstanding, re-flecting the relatively short life of these securities. Put slightlydifferently, their early redemption, or quick repayment, in acontext of limited new issues, makes them attractive to inves-tors. In this context, it is worth pointing out that the amortiza-tion profile of mortgage-backed securities broadly follows theredemption rate of the underlying domestic mortgages. Thispattern has influenced approaches to assessing yields and theattraction of the notes to investor groups.

Mortgage-Backed Securitization in the United Kingdom: The Background 333

Figure 6. Problems in Pricing and the Investment Market

1. “Engineered illiquidity” arises from the division of mortgage pools amongdifferent classes of investors, such as with three-tier fast-, medium-, andslow-pay collateralized notes (see Stadler and Jinkins 1990). Subdividingan already thin market makes establishing a secondary market even moredifficult and thus hinders efficient distribution.

2. Information flows—the securitization framework involves more protractedlinks between a large number of housing and nonhousing agents. Informa-tion from and about these agents now needs to be brought into the riskassessment process. Poor flow of information—much of which is in house—means that risks are less easy to identify, attribute, and price.

3. Transfer of risk—although securitization offers a great opportunity totransfer risk, the question arises whether mortgage securities can bepriced correctly in an immature market where information related tohousing finance and competition is not always clear and available. Defaultrisk and liquidity are two obvious examples of areas where existingpricing theory is inadequate (see Cooper 1986, 11).* The price paid forbearing default and illiquidity risk cannot easily be read off mortgage-backed pricing sheets.

4. Lack of large and regular volume of new issues reduces the possibility ofstandardizing notes and the benefits of market responsiveness suchstandardization would bring.

5. The uncertainty underlying the redemption date on mortgage-backed FRNsmeans that, despite their triple A rating, the securities trade at a widermargin than building society FRNs, although both relate to the U.K.domestic property markets.

6. Regulatory uncertainty surrounding the Bank of England’s solvency ratioand the Building Societies Commission’s categorization of mortgage-backed securities under its new liquid asset requirements leads to investoruncertainty and a widening of discounted spreads.

7. Widening discounted spreads in the primary market and (even greater)discounted spreads in the secondary market make it less economical tosecuritize because it substantially decreases the margin between domesticmortgage rates and the total costs of securitization.

8. Nonimmediate market factors stem from the protracted relations character-istic of a credit-wary mortgage-backed world in which downgrading ofagents seemingly unrelated to particular issues adversely affects the MBSmarket. For example, the downgrading of Alliance and Leicester from Aabto A by Moody’s led to a retreat by potential investors in society andmortgage-backed FRNs.

9. Who bears the costs of securitization? Centralized lenders are eventuallypassing on to the mortgagor the costs of selling bonds, as the lender mustshow a return that is approximate to the costs of the securitized portfolio.The larger the proportion of mortgages securitized, the less able the lenderis to substitute for cheaper funds from the rest of its wholesale portfolio orfrom retail sources. The limited liability spectrum of centralized lenders isa cost borne by the mortgagor.

334 Michael Pryke and Tim Freeman

Figure 6. Problems in Pricing and the Investment Market(continued)

10. Rating works on a weakest link principle, which leads to overinsurance,benefiting the note holder but hurting the consumer.

11. Insurance cover for MBS in the United Kingdom is provided through poolinsurance or less often through senior-junior structures. The primarymarket has been dominated by three U.K. insurers, two of which haverecently been downgraded by Moody’s, thus eliminating them from theprimary market. The dominant position of the insurers tends to affect theprice of insurance coverage. Prices have risen because it has become moredifficult to spread risk across the insurance market. This has occurreddespite the very limited number of calls on pool insurance. These influ-ences have skewed the market toward overinsurance, which then hasfuture effects on pricing and placement in the secondary market as well asintroducing a moral hazard risk.

12. Agency costs—the securitization of mortgages seems to provide relativelyefficient transactions and marketability of otherwise illiquid assets,without necessarily doing anything to isolate and then reduce, or satisfac-torily disperse, risk.

13. Issues must be perfectly matched; security offered to investor should matchthat offered to borrower; possible to restructure cash flows to investoreither through swaps and hedging activity, funded by the originator, or bypassing cash flows directly to investor in vanilla form. Uncertainty of cashflow and life of issue adds to costs of securitization, in region of 4 to 5basis points, as return in shorter time is more secure than one over alonger period. A, or senior, notes may be traded in secondary market afterissue; B, or junior, notes tend not to be traded.

14. Nonstandard mortgages—with growing market competition, there has beena rise in nonvanilla (i.e., nonendurable mortgages with 75 percent loan-to-value ratio), which raises nonstandard default risk and the need for creditenhancement.

15. Reinvestment risk will differ depending on structure of the securities.Reinvestment risk is very much linked to prepayment risk; as it is impos-sible to establish when cash will come through from borrowers or whatinterest rates will be at the time of prepayment, the term structure ofinterest rates may well have altered between acquisition of bond andprepayment. The term structure—the relationship between expected yieldon bonds of different maturities—may thus expose investors to interestrate risk (if rates have fallen). Hedging to cover this type of risk raisescosts of issue.