Morgan Stanley Conference Handout.ppt - AEP.com · Morgan Stanley Utilities Conference Handout New...

34

1 Morgan Stanley Utilities Conference Handout New York, NY March 7, 2013

Transcript of Morgan Stanley Conference Handout.ppt - AEP.com · Morgan Stanley Utilities Conference Handout New...

1

Morgan Stanley Utilities Conference Handout

New York, NYMarch 7, 2013

2

Investor Relations Contacts

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995

Bette Jo RozsaManaging DirectorInvestor Relations

Julie SherwoodDirector

Investor Relations614-716-2663

Sara MaciochAnalyst

Investor Relations614-716-2835

This presentation contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. Although AEP and each of its RegistrantSubsidiaries believe that their expectations are based on reasonable assumptions, any such statements may be influenced by factors that could cause actual outcomesand results to be materially different from those projected. Among the factors that could cause actual results to differ materially from those in the forward-lookingstatements are: the economic climate and growth in or contraction within and changes in market demand and demographic patterns in our service territory, inflationary ordeflationary interest rate trends, volatility in the financial markets, particularly developments affecting the availability of capital on reasonable terms and developmentsimpairing our ability to finance new capital projects and refinance existing debt at attractive rates, the availability and cost of funds to finance working capital and capitalneeds, particularly during periods when the time lag between incurring costs and recovery is long and the costs are material, electric load, customer growth and the impactof retail competition, particularly in Ohio, weather conditions, including storms and drought conditions, and our ability to recover significant storm restoration costs throughapplicable rate mechanisms, available sources and costs of, and transportation for, fuels and the creditworthiness and performance of fuel suppliers and transporters,availability of necessary generating capacity and the performance of our generating plants, our ability to recover increases in fuel and other energy costs through regulatedor competitive electric rates, our ability to build or acquire generating capacity, and transmission lines and facilities (including our ability to obtain any necessary regulatoryapprovals and permits) when needed at acceptable prices and terms and to recover those costs (including the costs of projects that are cancelled) through applicable ratecases or competitive rates, new legislation, litigation and government regulation including oversight of nuclear generation, energy commodity trading and new orheightened requirements for reduced emissions of sulfur, nitrogen, mercury, carbon, soot or particulate matter and other substances or additional regulation of fly ash andsimilar combustion products that could impact the continued operation and cost recovery of our plants and related assets, evolving public perception of the risksassociated with fuels used before, during and after the generation of electricity, including nuclear fuel, a reduction in the federal statutory tax rate could result in anaccelerated return of deferred federal income taxes to customers, timing and resolution of pending and future rate cases, negotiations and other regulatory decisionsincluding rate or other recovery of new investments in generation, distribution and transmission service and environmental compliance, resolution of litigation, our ability toconstrain operation and maintenance costs, our ability to develop and execute a strategy based on a view regarding prices of electricity, coal, natural gas and otherenergy-related commodities, prices and demand for power that we generate and sell at wholesale, changes in technology, particularly with respect to new, developing oralternative sources of generation, our ability to recover through rates or market prices any remaining unrecovered investment in generating units that may be retired beforethe end of their previously projected useful lives, volatility and changes in markets for electricity, natural gas, and other energy-related commodities, changes in utilityregulation, including the implementation of ESPs and the transition to market and expected legal separation for generation in Ohio and the allocation of costs withinregional transmission organizations, including PJM and SPP, our ability to successfully manage negotiations with stakeholders and obtain regulatory approval to terminatethe Interconnection Agreement, changes in the creditworthiness of the counterparties with whom we have contractual arrangements, including participants in the energytrading market, actions of rating agencies, including changes in the ratings of our debt, the impact of volatility in the capital markets on the value of the investments held byour pension, other postretirement benefit plans, captive insurance entity and nuclear decommissioning trust and the impact on future funding requirements, accountingpronouncements periodically issued by accounting standard-setting bodies and other risks and unforeseen events, including wars, the effects of terrorism (includingincreased security costs), embargoes, cyber security threats and other catastrophic events

3

Table of Contents

Topic PageCompany Overview/Strategy 4Transmission 11Competitive Operations 14Financial 21

4

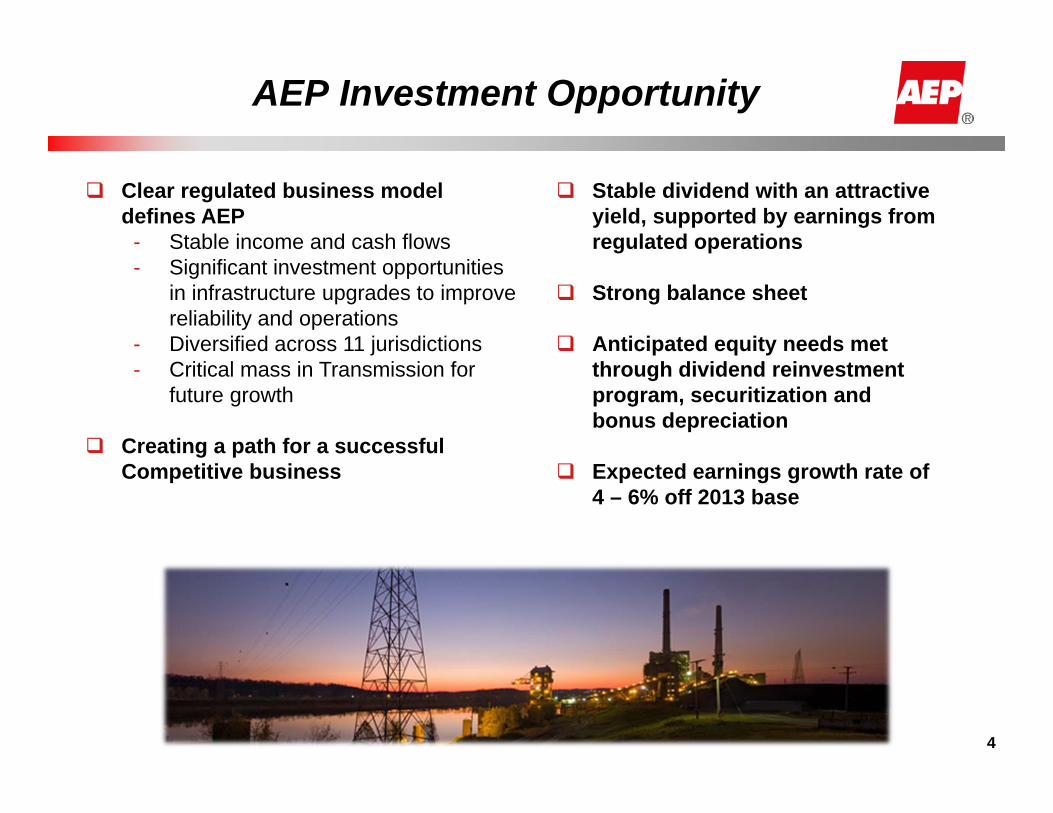

AEP Investment Opportunity

Clear regulated business model defines AEP

- Stable income and cash flows- Significant investment opportunities

in infrastructure upgrades to improve reliability and operations

- Diversified across 11 jurisdictions- Critical mass in Transmission for

future growth

Creating a path for a successful Competitive business

Stable dividend with an attractive yield, supported by earnings from regulated operations

Strong balance sheet

Anticipated equity needs met through dividend reinvestment program, securitization and bonus depreciation

Expected earnings growth rate of 4 – 6% off 2013 base

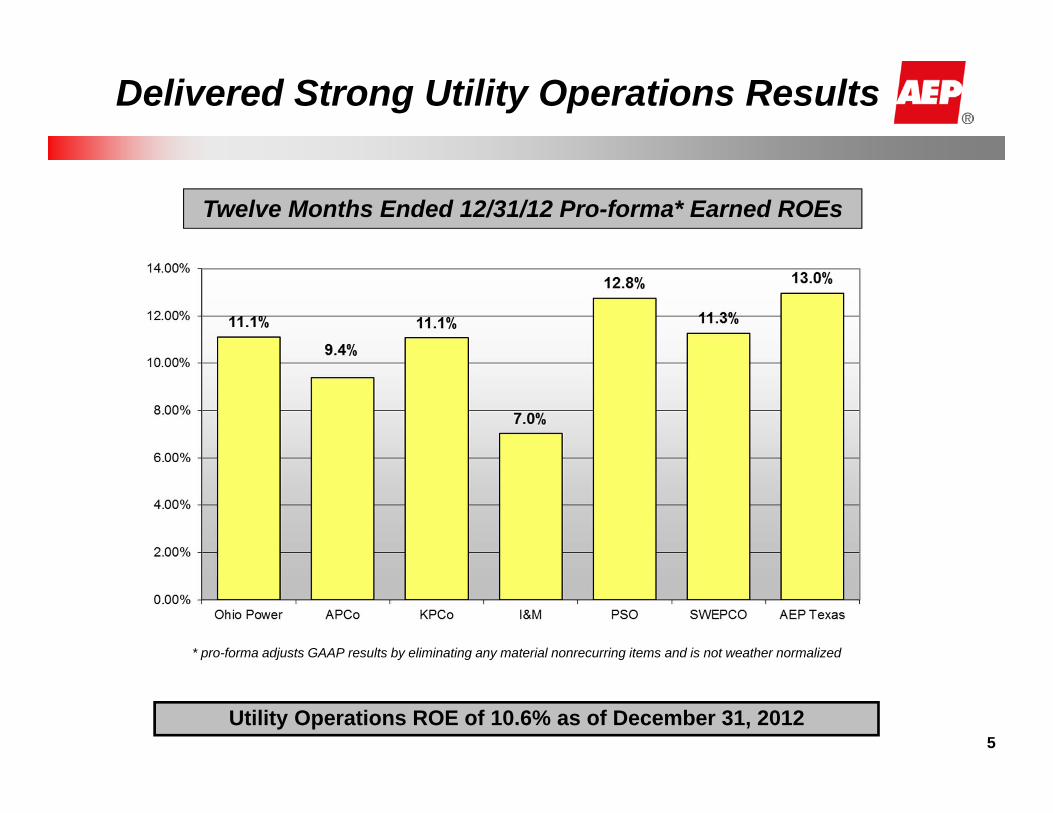

Twelve Months Ended 12/31/12 Pro-forma* Earned ROEs

* pro-forma adjusts GAAP results by eliminating any material nonrecurring items and is not weather normalized

Utility Operations ROE of 10.6% as of December 31, 2012

Delivered Strong Utility Operations Results

5

6

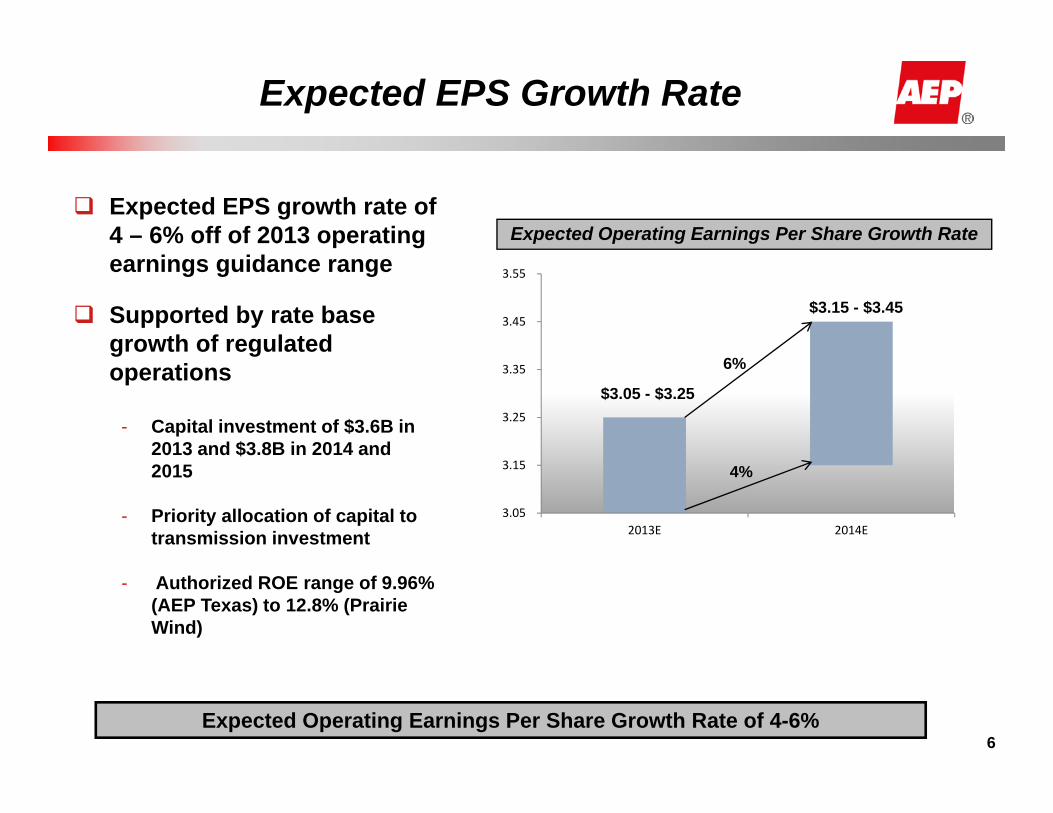

Expected EPS Growth Rate

Expected Operating Earnings Per Share Growth Rate of 4-6%

3.05

3.15

3.25

3.35

3.45

3.55

2013E 2014E

4%

6%

$3.05 - $3.25

$3.15 - $3.45

Expected Operating Earnings Per Share Growth Rate Expected EPS growth rate of

4 – 6% off of 2013 operating earnings guidance range

Supported by rate base growth of regulated operations

- Capital investment of $3.6B in 2013 and $3.8B in 2014 and 2015

- Priority allocation of capital to transmission investment

- Authorized ROE range of 9.96% (AEP Texas) to 12.8% (Prairie Wind)

7

$0.7

$1.4

$2.1

$2.4

$4.8

$7.5

$4.4

$2.8$1.3

$0.6

$0.4

$1.0

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

2013E 2014E 2015E

$ in

bill

ions

Wires CompaniesTX Wires and Ohio Power Wires Rate recovery via trackers (OH) or TCOS (TX)ROEs range from 9.96% to 11.49%

7

Regulated Business Growth Forecast

Cumulative Change in Regulated Net Property, Plant & Equipment (PP&E)

Vertically Integrated UtilitiesD and G rate adjustments via base rate cases with certain tracker mechanisms for nuclear, environmental and reliability investments T Rate recovery via trackers in TN, VA, MI. Others in base rates ROEs range from 10.0% to 10.9%

AEP Transmission Holdco(excluding unconsolidated JVs)Transcos: Rate recovery via FERC formula rates ROEs 11.49% (PJM) / 11.20% (SPP)

Note: 2013 annual regulated depreciation is $1.3B; Transmission JV investments, other than Transource, are not reflected above as the ventures are not consolidated on AEP’s financial statements

2012 Net Regulated PP&E = $33.9B6.9% CAGR in Net Regulated PP&E

Growth in regulated PP&E supports overall earnings growth of 4-6%

8

$6 - 8$5 - 7

$4 – 5

$ in billions

Environmental Transition Capital Plan2012-2020

Generation fleet will move to a more balanced portfolio while controlling costs, complying with environmental rules and benefitting our customers

65% of our current fleet capacity comes from coal generation

Anticipated coal capacity of 50% of the fleet by 2020

Estimated capital spend of $4 - $5 billion between now and 2020 to make these remaining coal plants compliant with current and proposed EPA regulations, including MATS, coal combustion residuals and 316(b) and effluent guidelines

Diligence in finding the lowest cost and low risk compliance options have resulted in more retirements, lower cost retrofits and reduced capital expenditures

Fleet Transformation

Repositioned Cost Profile

Organizational and process optimization evaluation, including five ‘deep dive’ areas of focus

- Finance & Accounting- Information Technology- Procurement/Supply Chain- Generation- Organizational Effectiveness

Aligned AEP’s employee benefits with other companies in the sector

Study reinforced resource allocations throughout the company to provide better customer service

Repositioned cost profile will sustainably absorb new operations and other expense increases

Utility Operations O&M well controlled

$2,874 $2,937 $2,675 $2,631

$553 $607$636 $754

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

2010A 2011A 2012A 2013E

$ in

mill

ions

Items withEarningsOffsets

Base UtilityO&M

Utility O&M Trend

9

10

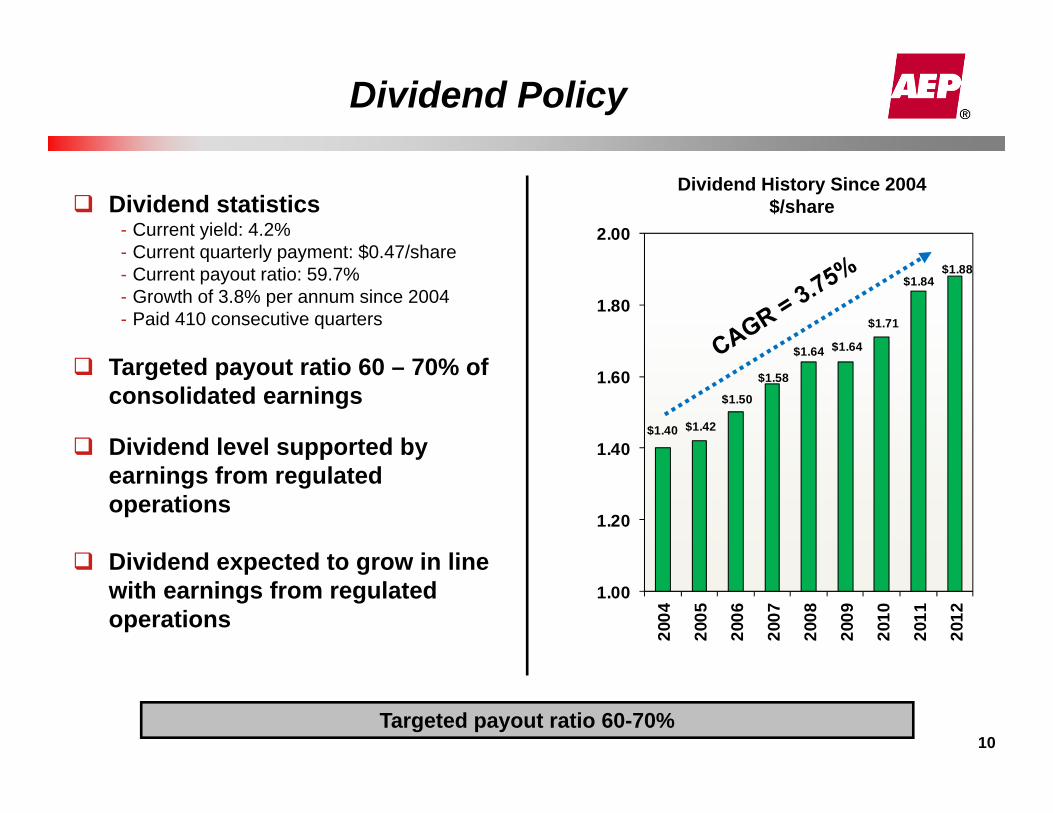

Dividend Policy

Dividend statistics- Current yield: 4.2%- Current quarterly payment: $0.47/share- Current payout ratio: 59.7%- Growth of 3.8% per annum since 2004- Paid 410 consecutive quarters

Targeted payout ratio 60 – 70% of consolidated earnings

Dividend level supported by earnings from regulated operations

Dividend expected to grow in line with earnings from regulated operations

Targeted payout ratio 60-70%

Dividend History Since 2004$/share

$1.40 $1.42

$1.50

$1.58

$1.64 $1.64

$1.71

$1.84 $1.88

1.00

1.20

1.40

1.60

1.80

2.00

2004

2005

2006

2007

2008

2009

2010

2011

2012

11

PJM SPP ERCOT TotalNew / Enhanced Stations 340 71 68 479

Transformation Capacity 17,900 MVA 2,500 MVA 1,300 MVA 21,700 MVA

New Transmission Lines 260 miles 175 miles 1,350 miles 1,785 miles

Rebuilt Transmission Lines 2,675 miles 425 miles 775 miles 3,875 milesCommunication and Control

Major Infrastructure Improvements

Rebuild or replace obsolete communication circuits and pilot wire protection, expand SCADA and add new equipment condition

Transmission Outlook

2013 – 2015 Earnings Forecast Based on Approved Projects

Post 2015 Investment Opportunities Drive Additional Future Earnings Growth

Largest transmission construction program in the country

*

Transmission ROEs and Incentives

Actual Project ROEs are a Function of the Base ROE PLUS Applicable Project Incentives

Transco & Operating Company ROEs are in the middle of the current range of ROEs in PJM and SPP

*includes 50 bps RTO adder

12

AEP has a track record of prudently requesting and receiving incentives that are commensurate with the risk of each project

Range of ROEs in PJM*AEP East OPCO& Transco ROEs

10.5% 12.4%11.49%

10.77%

Range of ROEs in SPP*AEP West OPCO& Transco ROEs

12.8%11.20%

Project/Joint Venture

Requested Incentives(ROE adder) Incentives Granted

TransourceMissouri

100 bps for Sibley-Nebraska City 0 bps for Iatan-Nashua project50 bps RTO adder for all projects

100 bps for Sibley-Nebraska City 0 bps for Iatan-Nashua project50 bps RTO adder for all projects

RITELine Overall risk adder of 200 bps 50 bps RTO adder100 bps Risk Adder

Prairie Wind 150 bps Risk Adder50 bps RTO adder

150 bps Risk Adder50 bps RTO adder

Pioneer 150 bps Risk Adder50 bps RTO adder

150 bps Risk Adder50 bps RTO adder

1313

Transmission Holdco Business Growth

Cumulative Transmission Holdco Net Property, Plant & Equipment

Note: 2013 annual depreciation is $9M; Transmission JV investments, other than Transource, are not reflected in PP&E above as the ventures are not consolidated on AEP’s financial statements; EPS represents AEPTHC, which includes all transcos and JVs

2010 Net PP&E = $50M124% CAGR in Net Transmission Holdco PP&E

Expected growth in EPS contribution closely tied to growing capital investment

$0.3

$0.7

$1.4

$2.2

$2.8

AEP Transmission Holdco(excluding unconsolidated JVs)

Transcos and TransourceRegulated by FERC

Revenue requirement reset annually based on prior year’s activity plus the current year’s projected plant-in-service balances, reducing regulatory lag

Transcos: ROEs 11.49% (PJM) 11.20% (SPP)

Transource: 86% ownership; capital investment begins in 2014

14

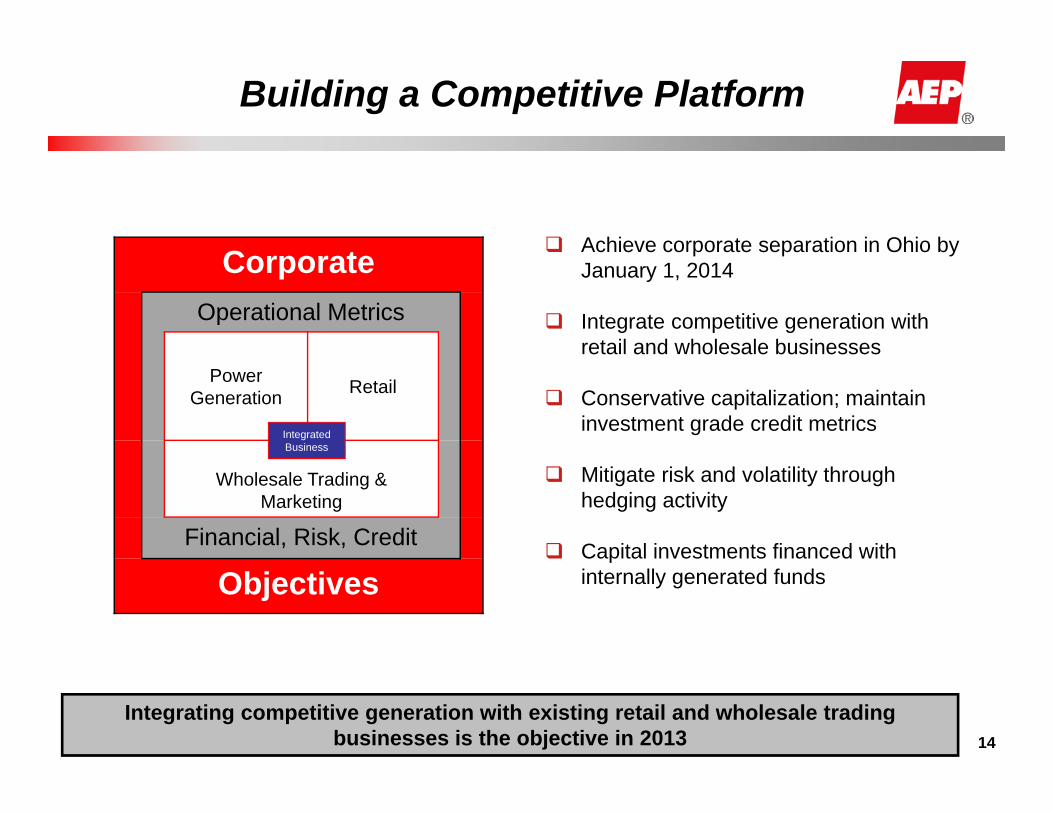

Building a Competitive Platform

Achieve corporate separation in Ohio by January 1, 2014

Integrate competitive generation with retail and wholesale businesses

Conservative capitalization; maintain investment grade credit metrics

Mitigate risk and volatility through hedging activity

Capital investments financed with internally generated funds

CorporateOperational Metrics

Power Generation Retail

Wholesale Trading & Marketing

Financial, Risk, Credit

Objectives

Integrated Business

Integrating competitive generation with existing retail and wholesale trading businesses is the objective in 2013

1515

AEP Generation Resources Footprint

AEP Generation Resources has the competitive advantage of fuel and operational diversity

Fuel Profile (2015)

Geographic Profile

8,876 MW

Capacity Profile (MW)

16

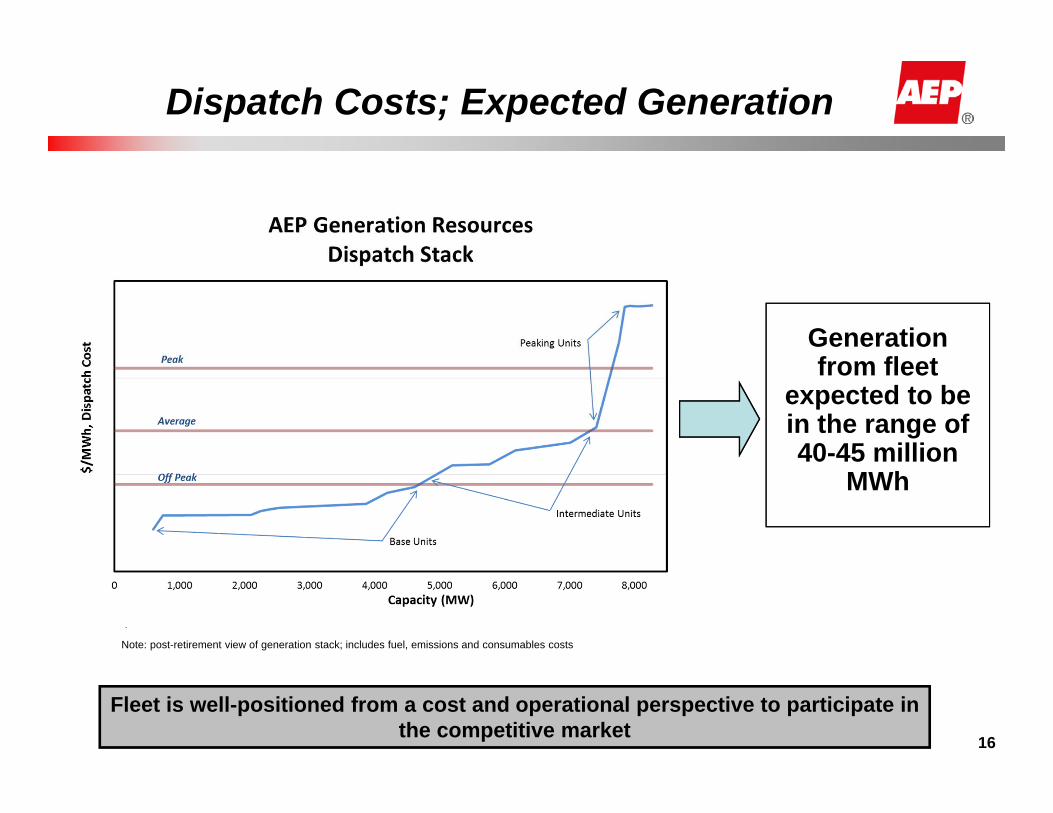

Dispatch Costs; Expected Generation

Fleet is well-positioned from a cost and operational perspective to participate in the competitive market

Generation from fleet

expected to be in the range of 40-45 million

MWh

Note: post-retirement view of generation stack; includes fuel, emissions and consumables costs

1717

Business As Usual (BAU) -Transition - Market

Capacity

SSO Load

Fuel Clause

Off-system Energy

2013 20142015

2016

BAU

BAU

10% slice of system auction

(Q3 ‘13-May ‘14)

FRR Capacity

revenue per ESP

60% slice of system auction

(Jun-Dec)

Per ESP

No SSO obligation

100% slice of system auction

FRR Capacity

revenue per ESP

Jan-May June-Dec

PJM RPM

Market

Excess energy sold in

retail and wholesale markets

All energy sold in

retail and wholesale markets

No SSO obligation

Blue – represents market exposureRed – According to ESP order from PUCO

PJM RPM

Market

All energy sold in

retail and wholesale markets

All energy sold in

retail and wholesale markets

Recovered through market sales

Recovered through market sales

Per ESP

FRR Capacity

revenue per ESP

1818

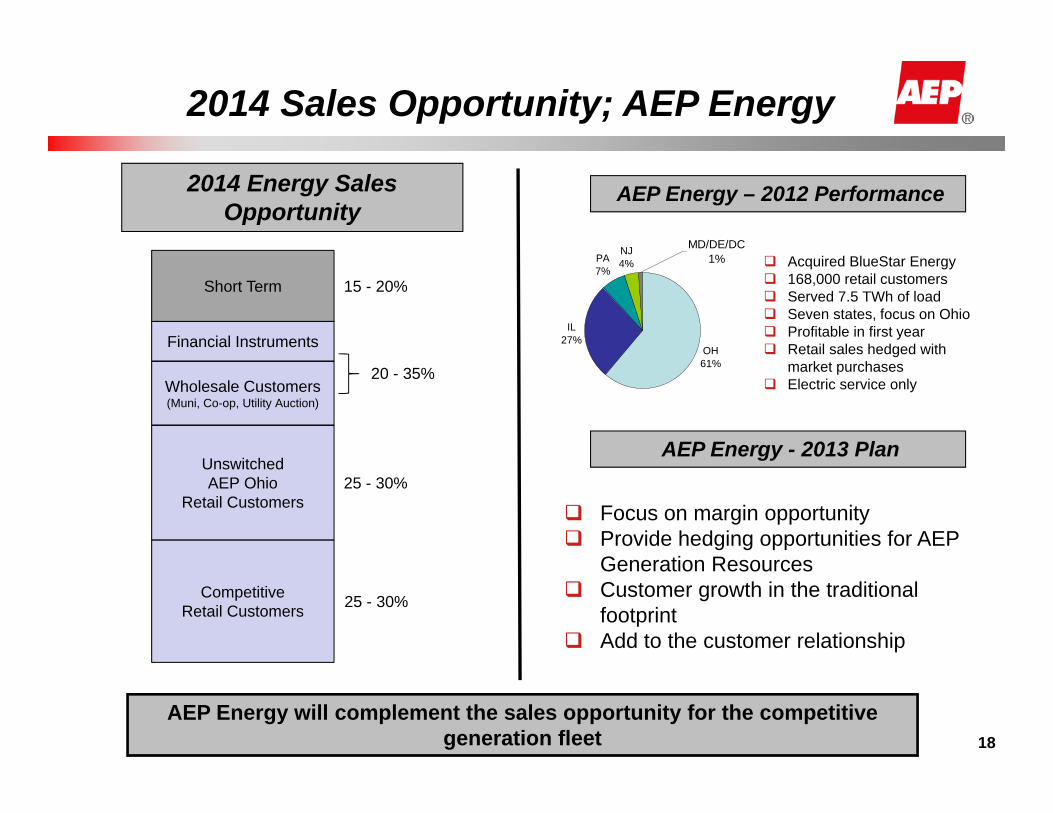

2014 Sales Opportunity; AEP Energy

AEP Energy – 2012 Performance

AEP Energy will complement the sales opportunity for the competitive generation fleet

IL27%

PA7%

NJ4%

OH61%

MD/DE/DC1% Acquired BlueStar Energy

168,000 retail customers Served 7.5 TWh of load Seven states, focus on Ohio Profitable in first year Retail sales hedged with

market purchases Electric service only

AEP Energy - 2013 Plan

Focus on margin opportunity Provide hedging opportunities for AEP

Generation Resources Customer growth in the traditional

footprint Add to the customer relationship

2014 Energy Sales Opportunity

Competitive Retail Customers

UnswitchedAEP Ohio

Retail Customers

Wholesale Customers (Muni, Co-op, Utility Auction)

Financial Instruments

Short Term

25 - 30%

25 - 30%

20 - 35%

15 - 20%

19

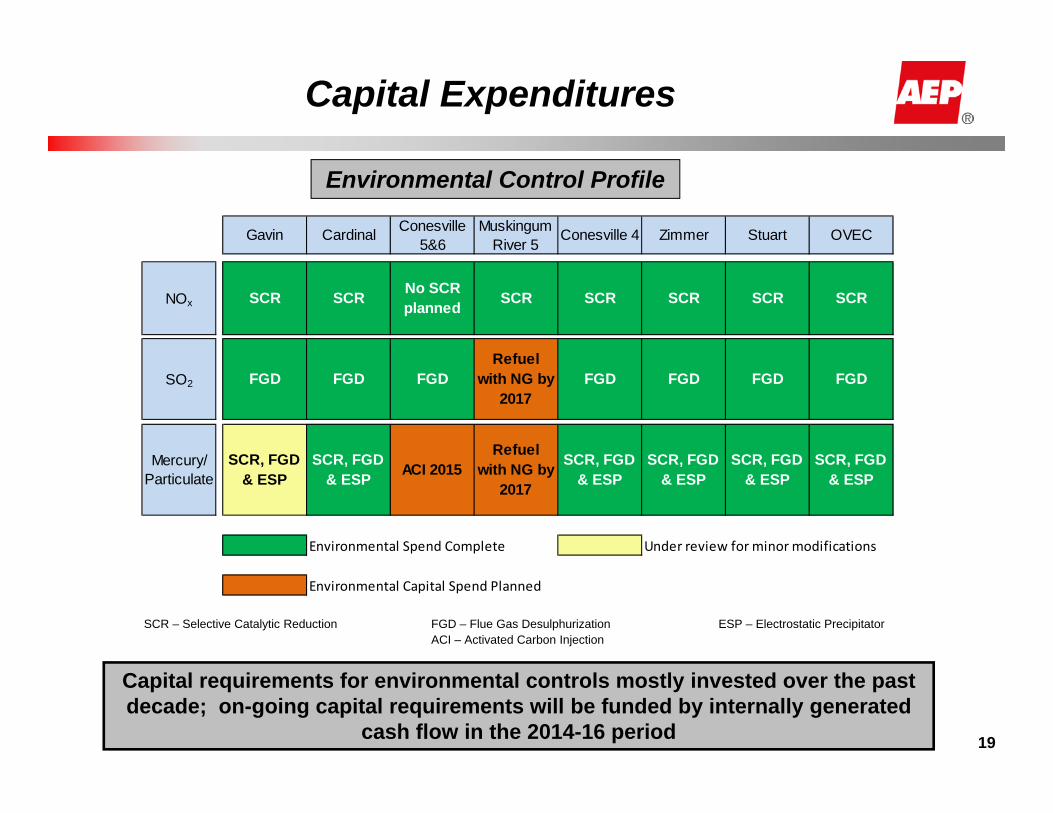

Capital requirements for environmental controls mostly invested over the past decade; on-going capital requirements will be funded by internally generated

cash flow in the 2014-16 period

Capital Expenditures

Environmental Control Profile

SCR – Selective Catalytic Reduction FGD – Flue Gas Desulphurization ESP – Electrostatic PrecipitatorACI – Activated Carbon Injection

Gavin Cardinal Conesville 5&6

Muskingum River 5

Conesville 4 Zimmer Stuart OVEC

NOx SCR SCR No SCR planned SCR SCR SCR SCR SCR

SO2 FGD FGD FGDRefuel

with NG by 2017

FGD FGD FGD FGD

Mercury/ Particulate

SCR, FGD & ESP

SCR, FGD & ESP ACI 2015

Refuel with NG by

2017

SCR, FGD & ESP

SCR, FGD & ESP

SCR, FGD & ESP

SCR, FGD & ESP

Environmental Spend Complete Under review for minor modifications

Environmental Capital Spend Planned

20AEP Generation Resources will be conservatively financed

Financing AEP Generation Resources

Debt 35% - 40%

Equity 60% - 65%

Total $3.1B

Expected Initial Capitalization

Closed on 27-month $1B bank loan to fund Ohio Power maturities this year

Expect AEP Generation Resources to be capitalized conservatively; company will look investment grade but will not be rated initially

Initial debt financing will be an inter-company loan from the parent; permanent financing will take place in the 2014/15 timeframe

Liquidity backstop provided through $3.5B in AEP core credit facilities; recently extended expiration dates into 2016/17 timeframe

21

2013 Operating Earnings Guidance

2013 Operating Earnings Guidance Range: $3.05 - $3.25 per share

2012A 2013E

22

Detailed Operating Earnings Guidance

2012A: $3.09 2013E: $3.05 - $3.25

($ millions) ($ millions)

UTILITY OPERATIONS:Gross Margin:

1 East Regulated Integrated Utilities 65,819 GWh 2,991 66,842 GWh 3,116 2 Ohio Companies 50,294 GWh 2,456 48,481 GWh 2,207 3 West Regulated Integrated Utilities 42,234 GWh 1,396 42,473 GWh 1,539 4 Texas Wires 29,039 GWh 642 28,785 GWh 659 5 Off-System Sales 324 311 6 Transmission Revenue - 3rd Party 500 595 7 Other Operating Revenue 506 552 8 Utility Gross Margin 8,815 8,979

9 Operations & Maintenance (3,311) (3,385) 10 Depreciation & Amortization (1,734) (1,694) 11 Taxes Other than Income Taxes (827) (855) 12 Interest Expense (882) (906) 13 Other Income & Deductions 139 62 14 Income Taxes (683) (787) 15 Utility Operations Operating Earnings 1,517 1,414

16 Transmission Operations Operating Earnings 44 67 NON-UTILITY OPERATIONS:

17 AEP River Operations 15 35 18 Generation & Marketing 7 24

19 Parent & Other Operating Earnings (86) (5)

20 OPERATING EARNINGS 1,497 1,535

American Electric PowerFinancial Results for 2012 Actual Vs 2013 Guidance

2012 Actual 2013 GuidancePerformance Driver Performance Driver

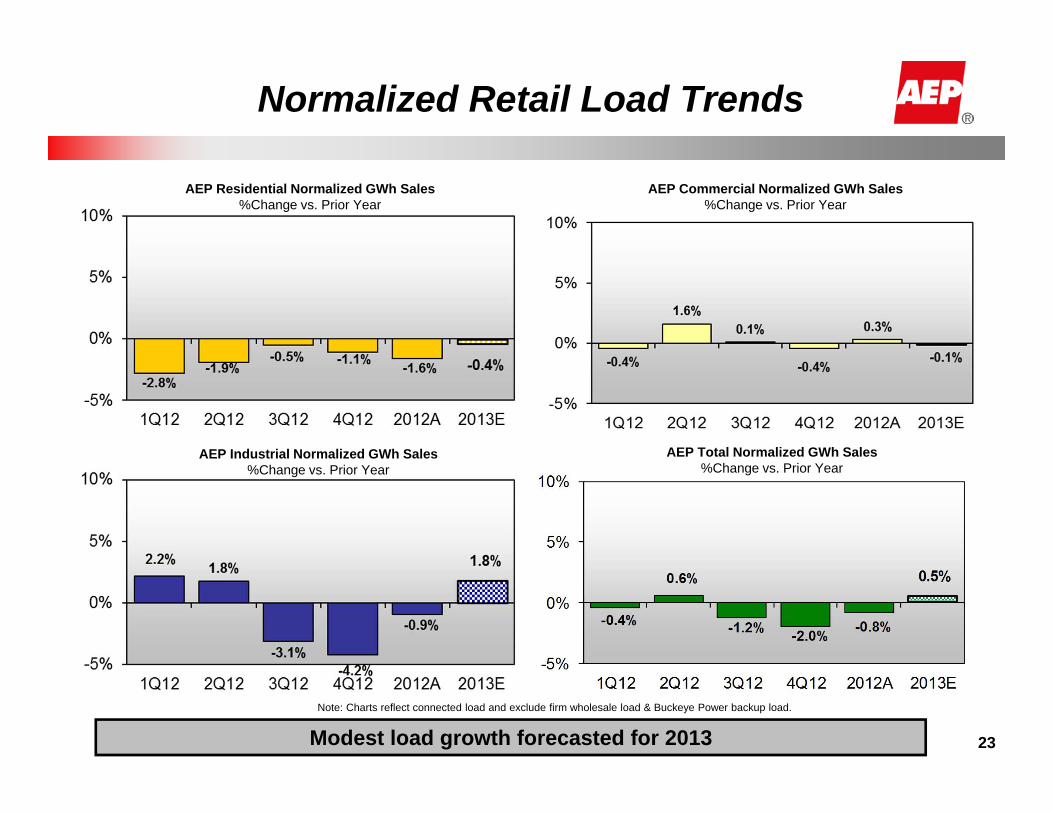

-0.4%

0.6%

-1.2% -2.0% -0.8%

0.5%

-5%

0%

5%

10%

1Q12 2Q12 3Q12 4Q12 2012A 2013E

Normalized Retail Load Trends

AEP Residential Normalized GWh Sales%Change vs. Prior Year

AEP Commercial Normalized GWh Sales%Change vs. Prior Year

AEP Industrial Normalized GWh Sales%Change vs. Prior Year

AEP Total Normalized GWh Sales%Change vs. Prior Year

Note: Charts reflect connected load and exclude firm wholesale load & Buckeye Power backup load.

Modest load growth forecasted for 2013 23

Identified Load Increases

Shale gas expansion is a fundamental positive for the AEP territory24

Jurisdiction IndustryMonthly GWh

ImpactDate of

ExpansionOhio Power Gas Transmission 7.7 Mar-13

Coating Services 9.0 Mar-13Gas Transmission 10.3 May-13Gas Transmission 15.3 Jul-13Gas Transmission 15.3 Sep-13Gas Transmission 7.7 Oct-13

Wheeling Power Gas Transmission 31.0 Mar-13Coal Mining 5.5 Apr-13Gas Transmission 3.0 Apr-13Gas Transmission 9.3 Jul-13Coal Mining 8.0 Jul-13Gas Transmission 3.0 Aug-13

TCC Steel 4.3 Jul-13PSO Gas Transmission 11.2 Oct-13

Gas Transmission 8.5 Oct-13

Expected Monthly Addition 149.0

2013Expansions

25

2012 and 2013 Capital & Equity Contributions

Incremental capital allocated to transmission and regulated utility investment opportunities

$ in millions

2013E: $3.6B2012A: $3.1B

New Generation spend decreasing 88%

Environmental spend increasing 126%

$ in millions

Excluding AFUDCExcluding AFUDC

Transco/JV spend increasing 48%

Nuclear spend increasing 42%

26

2013 Capital by Operating Company

Note: Ohio Power includes $136M related to Amos 3 and Mitchell plants to be transferred from Ohio Power to APCo and KPCo

27

2013 Key Assumptions & Sensitivities

Sensitivities OSS Assumptions, net of sharing

26,715 GWH

33,600 GWH

Sensitivity EPS

Retail Sales 0.5% +/- 0.04

Customer Switching in Ohio (net of capacity deferral) 4.0% +/- 0.03

Wholesale Market Prices $1 MWh +/- 0.03

O&M Expense (excludes O&M w ith offsets) 1.0% +/- 0.04

2013 Effective Tax rate @ 35.8% 1.0% +/- 0.05

Note: A $7.5M change in pre-tax earnings equals $0.01/share.

AD Hub ATC Price - $32.50

Henry Hub NG Price - $3.53

28

MATS Environmental Investments & Retirements

Projected Plant Retirements through 2016Potential Environmental Investments

ACI – Activated Carbon InjectionDSI – Dry Sorbent InjectionFGD – Flue Gas DesulfurizationSCR – Selective Catalytic Reduction

Operating Company Plant MW

Potential Type of retrofit

AEP Ohio(1) Conesville 5 & 6 800 ACIMuskingum River 5(2) 578 Refuel with Natural GasGavin 1 & 2 2,640 ACI

APCO Clinch River 1(3) 242 Refuel with Natural GasClinch River 2(3) 242 Refuel with Natural Gas

I&M Tanners Creek 4(4) 482 Refuel with Natural GasRockport(5) 2,620 DSI, SCR

KPCO Big Sandy 1(6) 278 Refuel with Natural Gas

PSO Oklaunion 101 FGD upgrade, ACINortheastern 3(5) 470 ACI, DSI, Baghouse

SWEPCO Welsh 1 528 ACI, DSI, BaghouseWelsh 3 528 ACI, DSI, BaghousePirkey 580 ACIDolet Hills 262 ACI, BaghouseFlint Creek(5) 264 FGD, ACI

TNC Oklaunion 377 FGD upgrade, ACIGrand Total MW 10,992

(1) Assumes investment is able to clear the market(2) Existing Coal Plant 585MW(3) Existing Coal Plant 235MW(4) Existing Coal Plant 500MW(5) Subject to regulatory and other approvals(6) Pending outcome of RFP process

Operating Company Plant MW

Expected Retirement

APCO Glen Lyn 5 95 2015Glen Lyn 6 240 2015Clinch River 3 235 2015Sporn 1 150 2015Sporn 3 150 2015Kanawha River 1 200 2015Kanawha River 2 200 2015Total MW 1,270

I&M Tanners Creek 1 145 2015Tanners Creek 2 145 2015Tanners Creek 3 205 2015Total MW 495

AEP Ohio Muskingum River 1-4 840 2015Picway 5 100 2015Sporn 2-4 300 2015Kammer 1-3 630 2015Beckjord 53 2015Total MW 1,923

KPCo Big Sandy 2 800 2015Total MW 800

SWEPCO Welsh 2 528 2014Total MW 528

PSO Northeastern 4 460 2016Total MW 460

Total Retirements = 5,476MW

29

Pension & OPEB Liabilities Well Managed

75% 74%

82%

88%

92%

70%

80%

90%

100%

2008 2009 2010 2011 2012

Qualified Pension Liability Funding

OPEB Assets and Liabilities

$1,000

$1,500

$2,000

$2,500

Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12

OPEB AssetsOPEB Liability

OPEBs Funded Status at December 31, 2012 is 90.8%

Contributions(in millions) $500 $450 $200

In addition to balance sheet deleveraging, significant funds were committed to improve the funded status of pension liabilities

Discount rate for 2013 is 3.95% for both pension and OPEB; assumed rate of return on assets is 6.50% for pension and 7.00% for OPEB

Modified post employment medical benefits for current employees, resulting in a reduction in the OPEB liability of $460M, or 21%

Expect combined pension and OPEB costs (O&M and capital) to decrease by about $60M pre-tax from 2012 to 2013

$ - $ -

Pension and OPEB funding and expense requirements significantly reduced

30

Forecasted Cash Flows and Financial Metrics

Cash needs are met through debt capital, securitization, bonus depreciation and the Dividend Reinvestment Plan

A:B:

Bonus Depreciation $ 952M

Securitization $1,192MOH distribution assets ($320M)WV ENEC ($422M)OH deferred fuel ($450M)

DRP/401k $ 300M

3-Year Total $2,444M

Cash inflowsfinance capital investment:

A:

B:

C:

C:

$ in millions 2013 2014 2015

Cash from Operations - Excluding Bonus Depreciation Impact 3,038 3,580 3,500

Bonus Depreciation Impact 792 160 -

Cash from Securitization 742 450 -

Capital & JV Equity Contributions (3,600) (3,800) (3,800)

Other Investing Activities (180) (280) (215)

Common Dividends @ $1.88/share (916) (921) (926)

Excess (Required) Capital (124) (811) (1,441)

Financing ($ in millions) 2013 2014 2015

Excess (Required) Capital (124) (811) (1,441)

Debt Maturities (Senior Notes, PCRBs) (1,649) (995) (1,155)

Securitzation Amortizations (280) (350) (330)

Interim Credit Facility 1,000 - -

Equity (DRP/401k) 100 100 100

Debt Capital Market Needs (New) (953) (2,056) (2,826)

Financial Metrics 2013 2014 2015

Debt to Capitalization Target

FFO/Total Debt Target

Mid 50s

Mid -to- upper teens

31

AEP’s Financial Strength

AEP Corporate Credit Ratings

S&P Moody's FitchBBB (Stable) Baa2 (Stable) BBB (Negative)

Balance sheet remains stable at mid-50% debt to capitalization ratio

12/31/2012

4.5x

18.7%

4.6x

19.9%

Credit Metrics

Debt to Capitalization 55.3% 55.2%

12/31/2011 FFO to Interest

Coverage

FFO to Debt

On February 13, 2013, AEP: Repriced, upsized by $250 million and

extended by one year the previous $1.5 billion core credit facility due June 23, 2015

Repriced and extended by one year the previous $1.75 billion core credit facility due July 26, 2016

Obtained a 27-month $1 billion unsecured delayed draw term loan facility for Ohio Power / AEP Generation Resources transition

Liquidity increased and extended

$‐

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

2015 2016 2017

$ in m

illions

Year of Facility Expiration

Previous Renewed (as of 2/13/13) Ohio Transition Facility

Liquidity Summary

New

Long-term Debt Maturity Profile

32

Year 2013 2014 2015 2016 2017

AEP, Inc. - - - - $550AEP Generating Company - $45 - - -Appalachian Power $470 $204 $500 $65 $250Indiana Michigan Power $98 $308 $265 $182 -Kentucky Power - - - - $325Ohio Power $856 $404 $86 $350 -Public Service of Oklahoma - $34 - $150 -Southwestern Electric Power - - $304 - $250Texas Central Company * $143 - $250 $192 $349Texas North Company $225 - - - -Total $1,792 $995 $1,405 $939 $1,724

* Includes $892 million of amortizing Texas Securitization Bonds based upon scheduled final payment date

Includes mandatory tenders (put bonds)

Data as of December 31, 2012

($ in millions)

33

Credit Metrics

Trailing Twelve Months 12/31/2012

FFO Interest Coverage FFO to Debt

GAAP Debt to Capitalization

Senior Unsecured

Credit Ratings*

American Electric Power Company 4.56 19.9% 55.2% Baa2/BBB-/BBB

Appalachian Power Company 4.34 17.0% 55.9% Baa2/BBB/BBB

Indiana Michigan Power Company 4.53 21.4% 53.4% Baa2/BBB/BBB

Kentucky Power Company 3.79 18.1% 54.0% Baa2/BBB/BBB

Ohio Power Company 5.23 24.0% 46.0% Baa1/BBB/A-

Public Service Company of Oklahoma 5.84 28.3% 50.9% Baa1/BBB/BBB+

Southwestern Electric Power Company 5.26 26.7% 50.3% Baa3/BBB/BBB

AEP Texas Central Company 4.77 23.0% 82.1%** Baa2/BBB/A-

AEP Texas North Company 4.82 20.1% 55.6% Baa2/BBB/A-* Moody’s/S&P/Fitch ** Includes securitization debt

34

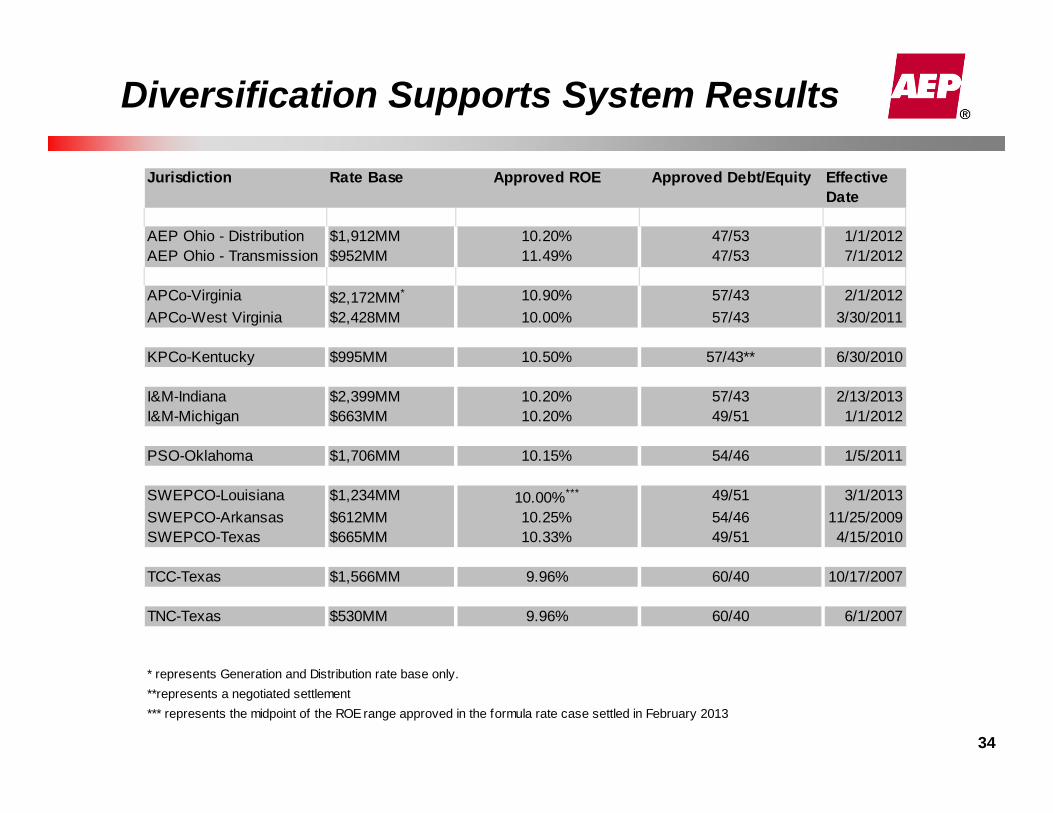

Diversification Supports System Results

Jurisdiction Rate Base Approved ROE Approved Debt/Equity Effective Date

AEP Ohio - Distribution $1,912MM 10.20% 47/53 1/1/2012AEP Ohio - Transmission $952MM 11.49% 47/53 7/1/2012

APCo-Virginia $2,172MM* 10.90% 57/43 2/1/2012APCo-West Virginia $2,428MM 10.00% 57/43 3/30/2011

KPCo-Kentucky $995MM 10.50% 57/43** 6/30/2010

I&M-Indiana $2,399MM 10.20% 57/43 2/13/2013I&M-Michigan $663MM 10.20% 49/51 1/1/2012

PSO-Oklahoma $1,706MM 10.15% 54/46 1/5/2011

SWEPCO-Louisiana $1,234MM 10.00%*** 49/51 3/1/2013SWEPCO-Arkansas $612MM 10.25% 54/46 11/25/2009SWEPCO-Texas $665MM 10.33% 49/51 4/15/2010

TCC-Texas $1,566MM 9.96% 60/40 10/17/2007

TNC-Texas $530MM 9.96% 60/40 6/1/2007

* represents Generation and Distribution rate base only.

*** represents the midpoint of the ROE range approved in the formula rate case settled in February 2013**represents a negotiated settlement