More looking to buy...Singapore. Last December, Allgreen Properties bought Royalville for $478...

16

Transcript of More looking to buy...Singapore. Last December, Allgreen Properties bought Royalville for $478...

More looking to buy homes in 2018

The Homebuyers’ Sentiment Survey, jointly conducted by EdgeProp and Knight Frank Singapore, sheds light on how people feel about the local residential market.

See our Cover Story on Pages 5 to 7.

PROPERTY PERSONALISED

Visit EdgeProp.sg to nd properties, research market trends and read the latest news The week of January 8, 2018 | ISSUE 812-34

MCI (P) 136/08/2017 PPS 1519/09/2012 (022805)

Gig economyWeWork expands in Singapore, Southeast

Asia EP4

Done DealsToh Tuck area sees increase in buying

interest EP8&9

Gains and LossesUnit at The Marq sold

at $4.9 mil lossEP10

Deal WatchConservation terraced

house on Kim Yam going for $2.78 mil EP11

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

View of Bukit Merah from Alexandra Road

EP2 • EDGEPROP | JANUARY 8, 2018

Low Keng Huat launches Kismis Residences and TRANQUILIA @ KismisSingapore-listed property development and construc-

tion company Low Keng Huat (Singapore) officially

launched Kismis Residences (above) and TRANQUILIA

@ Kismis on Jan 5, according to ERA Realty, which is

jointly marketing both projects with OrangeTee & Tie.

Located near Toh Tuck Road, the two freehold pro-

jects are jointly developed by Low Keng Huat and pri-

vately held developer Wenul Development.

Kismis Residences, located on Lorong Kismis, com-

prises 31 terraced houses: Eight are corner lots and

23 are intermediate units.

According to ERA Realty, each five-floor unit has

five en-suite bedrooms, an entertainment room in the

basement with a separate entrance, an attic, a jet pool

at the roof terrace, as well as a car porch. The built-

up area of each unit is between 4,700 and 5,500 sq ft.

Each corner lot is priced between $5.003 million

and $5.282 million; and each intermediate lot is priced

between $4.155 million and $4.464 million.

Meanwhile, TRANQUILIA @ Kismis, which is lo-

cated at the junction of Eng Kong Road and Lorong

Kismis, comprises seven strata terraced houses. Each

unit has a strata area of 4,359 to 5,597 sq ft. Prices

range between $3.521 million and $4.255 million.

“Over the soft launch period in December 2017,

we managed to secure buyers for 11 of the 22 units

released for sale at both projects,” says Eugene Lim,

key executive officer at ERA Realty.

City Towers makes fourth collective sale attempt with $355 mil reserve priceCity Towers (top, centre) on Bukit Timah Road has

been put up for collective sale on Jan 4. This is the

fourth such attempt for the owners at City Towers,

says M Singh, chairman of the City Towers collective

sale committee.

The reserve price of the property is $355 million,

including a development charge of about $3.505 mil-

lion for the intensification of land use, according to

marketing agent Colliers International. This works out

to $1,633 psf per plot ratio, comparable to the $1,840

psf ppr land rate garnered by the nearby Crystal Tower

in December, notes Colliers.

Built in the 1960s, the 17-storey development occu-

pies a 104,531 sq ft site. Under the 2014 Master Plan, the

site is zoned “Residential”, with a gross plot ratio of 2.1.

Based on the total gross floor area of 219,516 sq ft,

the site could be redeveloped into a 24-storey residen-

tial block with 190 units, assuming that each unit is

an average of 1,098 sq ft and subject to authorities’

approval, says Colliers.

City Towers comprises 77 apartments and maison-

ettes, a penthouse and a retail unit. If the collective

sale is successful, each residential owner could receive

between $2.45 million and $10.17 million, depend-

ing on the size of their units, according to Colliers.

The tender exercise closes on Feb 7.

Sixth Avenue Centre up forcollective sale at $90.5 milSixth Avenue Centre (top, right) at Bukit Timah was

launched for collective sale on Jan 3. The guide price

for the freehold, mixed-use redevelopment site is

$90.5 million, including a development charge of

about $526,000, according to marketing agent Sav-

ills Singapore. This works out to a land cost of about

$2,022 psf ppr.

The existing development comprises seven retail

units and 18 residential units on a 15,009 sq ft site.

Under the 2014 Master Plan, the site is zoned “Com-

mercial and Residential”, with a gross plot ratio of

3.0. This means the property has an allowable gross

floor area of 45,028 sq ft.

According to Savills, Sixth Avenue Centre can be

redeveloped into a project comprising a retail com-

ponent with 18,011 sq ft of GFA, as well as 35 apart-

ments with a total GFA of 27,017 sq ft — subject to

authorities’ approval. This is assuming an average

size of 753 sq ft for each apartment.

Sixth Avenue Centre is located within walking dis-

tance of Royalville and the residential Government

Land Sales (GLS) site on Fourth Avenue, says Suz-

ie Mok, senior director of investment sales at Savills

Singapore. Last December, Allgreen Properties bought

Royalville for $478 million ($1,960 psf ppr) and the

Fourth Avenue site for $553 million ($1,540 psf ppr).

The tender closes on Jan 31.

Kovan Apartments launched forcollective sale at $33 milKovan Apartments on Kovan Road was launched for

collective sale on Jan 3. According to marketing agent

Savills Singapore, the guide price for the property is

$33 million. Savills estimates the development charge

required to develop the site to its maximum allowable

plot ratio at $2.57 million. Taking this into account,

the price works out to $1,199 psf ppr.

Located 700m from the Kovan MRT station, the

21,193 sq ft site is near amenities such as Heartland

Mall and Kovan Market and Food Centre. The exist-

ing development is a four-storey residential block of

16 units.

Under the 2014 Master Plan, the site is zoned

“Residential”, with a plot ratio of 1.4. This means

the site can be redeveloped into a project with

a GFA of about 29,670 sq ft. This in turn works

out to be 27 units, assuming each unit is an ave-

rage of 1,075 sq ft. The tender closes on Feb 5.

— Compiled by Angela Teo

PROPERTY BRIEFS

EDITORIALEDITOR | Cecilia ChowHEAD OF RESEARCH | Feily Sofi anDEPUTY EDITOR | Lin ZhiqinWRITERS | Angela Teo, Timothy TayDIGITAL WRITER | Fiona Ho

COPY-EDITING DESK | Elaine Lim, Evelyn Tung, Chew Ru Ju, Shanthi MurugiahPHOTO EDITOR | Samuel Isaac ChuaPHOTOGRAPHER | Albert ChuaEDITORIAL COORDINATOR | Yen TanDESIGN DESK | Tan Siew Ching, Christine Ong, Monica Lim, Tun Mohd Zafi an Mohd Za’abah

ADVERTISING + MARKETING ADVERTISING SALES

DIRECTOR, COMMERCIAL OPERATIONS | Cowie TanASSOCIATE ACCOUNT DIRECTOR | Diana LimACCOUNT MANAGER |James Chua

CIRCULATIONDIRECTOR | Victor TheEXECUTIVE | Malliga Muthusamy, Ashikin Kader

CORPORATE CHIEF EXECUTIVE OFFICER | Bernard Tong

PUBLISHERThe Edge Property Pte Ltd150 Cecil Street #13-00Singapore 069543Tel: (65) 6232 8688Fax: (65) 6232 8620

PRINTERKHL Printing Co Pte Ltd57 Loyang DriveSingapore 508968Tel: (65) 6543 2222Fax: (65) 6545 3333

PERMISSION AND REPRINTSMaterial in The Edge Property may not be reproduced in any form without the written permission of the publisher

We welcome your commentsand criticism: [email protected]

Pseudonyms are allowed but please state your full name, address and contact number for us to verify.

| BY ANGELA TEO |

Based on flash estimates released by URA on Jan 2, the private residential property index rose one point to 138.6 in 4Q2017, up 0.7% q-o-q. Property prices rose 1% in 2017, marking the first y-o-y increase in prices since 2013. Prices fell 3.1% y-o-y in 2016, 3.7% y-o-y in 2015 and 4% y-o-y in 2014.

Lee Nai Jia, head of research at Edmund Tie & Co (ET&Co), attributes the full-year increase in private residential property prices to, among other factors, the easing of cooling measures, bullish bids for Government Land Sales (GLS) and collective sale sites, as well as the stronger economic outlook towards year-end.

Prices of non-landed private residential properties in the Core Central Region (CCR) saw the strongest growth, rising 1.6% q-o-q in 4Q2017, compared with a 0.1% increase in 3Q2017.

“According to caveats lodged with URA,

some projects that contributed to the price growth in 4Q2018 were Martin Modern, Gramercy Park and Sophia Hills, which saw median prices rise q-o-q by 8.3%, 4.0% and 1.8%, respectively,” comments Tricia Song, head of research for Singapore at Colliers International.

Meanwhile, prices in the Rest of Central Region (RCR) and the Outside Central Region (OCR) recorded lower q-o-q increases of 0.2% and 0.6%, respectively, in 4Q2017, compared with 0.5% and 0.8% in 3Q2017.

It was the same for landed property prices, which rose 0.6% q-o-q in 4Q2017, versus 1.2% in 3Q2017.

Colliers’ Song notes that overall private residential property prices for 2017 are 10.3% below the 2013 peak. “We expect overall private home prices to rise 5% in 2018, barring unforeseen events,” she says.

According to URA, flash estimates were calculated based on transaction prices given in contracts submitted for stamp duty

payment as well as developer sales data until mid-December.

Meanwhile, based on flash estimates released by HDB on Jan 2, the resale price index for public housing fell from 132.8 points in 3Q2017 to 132.6 in 4Q2017, translating into a 0.2% decrease in prices versus a 0.7% decline in 3Q2017.

According to Eugene Lim, key executive officer of ERA Realty, resale prices of HDB flats saw a 1.5% y-o-y decline in 2017. Lim attributes this to, among other factors, a reported announcement by Minister for National Development Lawrence Wong in March that not all ageing HDB flats will undergo the Selective En-Bloc Redevelopment Scheme.

HDB will offer about 3,600 new flats in the first Build-to-Order exercise this year, which is slated for launch in February. The flats will be located in Tampines, Woodlands, Choa Chu Kang and Geylang.

URA and HDB will release the full and updated set of real estate statistics on Jan 26.

Jan 26.

Private-home prices up 1% in 2017 after three years of decline

Prices of non-landed private residential properties in CCR rose 1.6% in 4Q2017

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

SAVI

LLS

SIN

GAP

ORE

COLL

IERS

ERA

REAL

TY

E

EDGEPROP | JANUARY 8, 2018 • EP3

EP4 • EDGEPROP | JANUARY 8, 2018

GIG ECONOMY

WeWork expands in Singapore and Southeast Asia| BY CECILIA CHOW |

New York-based WeWork, the

largest co-working space

provider in the world,

opened its Singapore flag-

ship space, WeWork Beach

Centre, on Dec 1, with an official

launch party on Dec 14. The space,

which occupies the first three floors

of Beach Centre on Beach Road, has

more than 690 desks and is already

almost filled up.

Global tech company HP Inc and

cloud communications company

Twilio as well as start-ups such as

restaurant booking app Chope, dig-

ital insurance app PolicyPal and dig-

ital wealth manager StashAway are

WeWork members, and located at

WeWork Beach Centre.

A second WeWork co-working

space will open at 71 Robinson Road

in the CBD early this year. It will be

its largest — with more than 1,000

desks across three floors. The third

WeWork office will occupy 40,000

sq ft of space across two floors (lev-

els 4 and 5) of Funan’s office block

and will have more than 700 desks.

It is scheduled to open in early 2019.

The co-working or collaborative

work space at Funan is a “co-crea-

tion” between WeWork and Capita-

Land Mall Trust.

Growing footprintTurochas “T” Fuad, managing direc-

tor of WeWork Southeast Asia, was

the founder of Spacemob, which We-

Work acquired last August as part of

its US$500 million ($664 million) ex-

pansion in Southeast Asia and South

Korea. Spacemob, a Singapore-based

co-working operator, was founded by

Fuad in early 2016. It received US$5.5

million in seed funding from Temasek

Holdings’ venture capital arm Vertex

Ventures and Alpha JWC Ventures in

November that year.

Besides appointing Fuad as man-

aging director of WeWork Southeast

Asia, the company has also absorbed

his team of 20 at Spacemob. For now,

Spacemob continues to operate its

co-working space at 8 Claymore Hill

and Ascent on Science Park Drive in

Singapore as well as in Jakarta. “At

the moment, the Spacemob locations

are still operating,” says Fuad. “All the

The reception and lounge area of WeWork Beach Centre

The pantry and communal area at WeWork Beach Centre

members will also be able to access

the WeWork locations.”

The opening of WeWork Beach

Centre last month marked the group’s

200th location and its entry into the

20th country. The expansion is the

latest in Asia for WeWork as it grows

its footprint of co-working spaces to

new markets beyond the US. Last Au-

gust saw Japan’s SoftBank Group Corp

and its Vision Fund invest US$4.4

billion in WeWork. This includes

US$500 million for a WeWork pro-

ject in China and a joint venture in

Japan. Another US$500 million has

been earmarked for expansion into

Southeast Asia and South Korea.

WeWork’s first landing point in

Asia was in Hong Kong two years

ago, says Fuad. It has two locations

there currently, with several more in

the pipeline.

In Southeast Asia, it is looking

at expanding into key cities, name-

ly Bangkok, Jakarta, Kuala Lumpur

and Ho Chi Minh City. “We’re look-

ing at the first-tier cities,” says Fuad.

Beyond co-workingHowever, Fuad says, “At WeWork, we

don’t see ourselves as just a co-work-

ing space operator. We are commu-

nity builders.” The company devel-

ops technology and designs spaces

including lighting and furnishing

that can be plugged into WeWork

spaces around the world. Today, it

has more than 300 member compa-

nies with more than 175,000 mem-

bers globally. The company also

uses heat maps to track how spaces

are being used, and then leverages

its R&D data when it designs future

WeWork spaces. “It’s about econo-

mies of scale, not just space optimi-

sation,” Fuad notes.

WeWork was co-founded by Adam

Neumann and Miguel McKelvey and

launched in 2010. The company is

valued at US$20 billion and is one

of the top office tenants in New York

City. It is set to become one of the

biggest private tenants of office space

in London, according to a Bloomb-

erg report last month.

“A lot of companies, including

those from China and India, are

looking at flexible office space ar-

rangements,” says Fuad. “We’re look-

ing at how we can support them.”

That has led to the provision of

its “Powered by We” services. It will

help companies manage and operate

their office premises in the WeWork

style and with the WeWork vibe,

says Fuad. WeWork’s R&D team will

speak to employees of the company

to find out how they use their space

and what they would like to have,

the number of meeting rooms, phone

conference booths, privacy and com-

munal space required. WeWork will

then provide customised solutions to

the specific needs of the company at

their respective spaces. According to

Fuad, “Powered by We”, which was

launched last year, now accounts for

about 20% of the company’s business.

Co-livingThe company has also expanded into

co-living with WeLive. There are now

three WeLive co-living spaces locat-

ed in New York, Washington DC and

Seattle. “The misconception is that

co-living is like a high-end dormito-

ry,” says Fuad. “However, WeLive has

apartments with three or even four

bedrooms. There will be one level

of shared facilities for residents. It’s

also ideal to have WeLive and We-

Work in the same building.”

According to Fuad, there is a pos-

sibility of launching WeLive in Asia.

“WeLive is a much broader concept

than a typical serviced apartment op-

eration. Likewise, WeWork provides

more than just co-working or serviced

office space. We build communities.”

Regardless of what WeWork calls

itself, with a US$20 billion valuation,

it is now ranked among the most

highly valued private US tech uni-

corns after Airbnb and Uber.

Fuad: At WeWork, we don’t see ourselves as just a co-working space operator. We are community builders. One of the many office suites at WeWork Beach Centre

PICT

URES

: SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

E

EDGEPROP | JANUARY 8, 2018 • EP5

COVER STORY

| BY ZHIQIN LIN |

At least one in two people plan to buy a home, and

more are looking to buy this year than in the past.

Of the 611 respondents to the EdgeProp-Knight Frank

Homebuyers’ Sentiment Survey, 55.6% said they

were looking to purchase a residential property in

Singapore in the next 12 months.

The survey was jointly conducted by EdgeProp and Knight

Frank Singapore in 4Q2017. In the previous survey conducted

in 2016, 51.2% of the 500 respondents said they were on the

lookout for a residential property in Singapore (see Chart 1).

A key reason for the increase in homebuying interest is re-

cord land bid prices in government land sales (GLS) and collec-

tive sales, which have “created an expectation of higher prices

within the next year or so, prompting buyers to take positions

as soon as they can before the new price level can actualise”,

says Alice Tan, director and head of consultancy and research

at Knight Frank Singapore.

According to figures released by URA on Jan 2, prices of pri-

vate residential property rose 0.7% in 4Q2017, following a sim-

ilar increase in 3Q2017. “For the whole of 2017, prices have in-

creased by 1%, compared with the 3.1% decline in 2016,” says

URA. Given that prices are beginning to rebound, it is likely that

more people would be prompted to buy before prices rise further.

Another reason is “the release of pent-up demand from pro-

spective homebuyers over the past four years, built up since

the seventh round of cooling measures and the total debt ser-

vicing ratio [TDSR] ruling implemented in 2013”, according

to Tan. An indication of pent-up demand would be the trans-

action volume for private residential properties in Singapore,

which plummeted sharply between 2012 and 2014 but has

since been on an uptrend (see Chart 2).

A good proportion of those looking to buy in the next 12

months are already property owners. At least 58.5% indicat-

ed that they already owned one, while 15.9% said they owned

multiple properties. Most of those looking to buy said the prop-

erty would be for their own use or renting out, with a smaller

proportion of respondents indicating other reasons such as for

their children, as a future retirement home or for capital gains.

Potential homebuyers who do not currently own a property are

more likely to be owner-occupiers, while those who already

own properties are likely to be rental investors (see Chart 3).

Preference for condos in prime districtsPerhaps owing to the high proportion of investors among the

respondents, the results indicated a preference for private con-

dominiums and apartments, with 65.6% of the respondents

selecting that as their preferred property type. This is followed

More looking to buy homes

The Homebuyers’ Sentiment Survey, jointly conducted by EdgeProp and Knight Frank Singapore, sheds light on how people feel about the local residential market

CONTINUES NEXT PAGE

More people are looking to buy in 2018 Transaction volume of private residential properties in Singapore

Chart 1 Chart 2

%100

90

80

70

60

50

40

30

20

10

0

40000

35000

30000

25000

20000

15000

10000

5000

0

Respondents felt confident about Singapore’s politicalleadership, its economy and the residential property market

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

Looking to buy

Not looking to buy

Previous survey Latest survey

2009 2010 2012 2014 20162011 2013 2015 2017Note: While a larger proportion of respondents in the latest survey indicated they were looking to buy in the next 12 months, the questions were phrased differently in the surveys, which may have resulted in different interpretations by respondents Note: 2017 data is year-to-date as at 3Q2017

Resale

Subsale

New sale

URA

REAL

IS, K

NIG

HT F

RAN

K RE

SEAR

CH

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, K

NIG

HT F

RAN

K RE

SEAR

CH, E

DGEP

ROP

Units

EP6 • EDGEPROP | JANUARY 8, 2018

COVER STORY

by HDB flats at 15% and executive condos at 9.1%, with the

remainder split between landed houses, strata-landed proper-

ties and shophouses. HDB flats and ECs are subject to a five-

year Minimum Occupation Period and rules for resale and rent-

al, which make them less favoured as investment properties.

Tan says most respondents preferred the prime districts when

buying a condo, regardless of where they currently reside. She

notes that the propensity to move to the prime

districts is highest for residents who current-

ly live in the suburbs, with only 13.8% pre-

ferring to stay put and 56.3% preferring to

buy a property in the prime districts.

Meanwhile, 54.9% of those who have

homes in the city fringe would also like to

move to the prime districts and 40.8% said

they wanted to remain in the city fringe.

An overwhelming 76.9% of respondents

with homes in the prime districts indicat-

ed a preference to continue to stay there.

Among the respondents, 51.9% and 47.5%

showed a strong preference for two- and

three-bedroom units respectively. On the

other hand, one-, four- and five-bedroom

units are favoured by 21.9%, 20.9% and

9.8% of respondents respectively. Fifty-nine

per cent of those who favoured one-bed-

room units also chose the prime districts as

their preferred location. Meanwhile, those

who preferred two-, three- and four-bed-

room units showed a preference for the city

fringe, with 68.5%, 65.5% and 53.9% say-

ing they would buy property in this loca-

tion, respectively. Of the respondents who

said they would like to buy a five-bedroom

unit, 56.7% chose the suburbs as their pre-

ferred location (see Chart 4).

This trend of buyers’ preference for smaller

units in and larger units away from the prime

districts could be due to concerns about af-

fordability. Properties in the prime districts

tend to be the priciest, followed by those in

the city fringe and the suburbs. Based on

URA caveat data as at Jan 2, average trans-

acted prices in 2017 for private non-landed

residential properties are $2.7 million ($1,956

psf) in the Core Central Region (CCR); $1.7

million ($1,463 psf) in the Rest of Central

Region (RCR); and $1.2 million ($1,158 psf) in the Outside Cen-

tral Region (OCR), which are also referred to as the prime dis-

tricts, city fringe and suburbs, respectively.

Prices of non-landed private residential properties in CCR

rose 1.6% in 4Q2017, while prices in RCR and OCR rose 0.2%

and 0.6%, respectively. According to Tan, prices in CCR fell by

10.8% between 2013 to the trough in 2Q2017.

“With prices for some private homes in CCR hitting attrac-

tively low levels in 2017, demand for value-for-money buys

naturally increased, along with rising optimism, following the

collective sales boom that began in May 2017,” says Tan. In

3Q2017, the transaction volume in CCR rose 85.1% y-o-y, re-

flecting the return of interest, she adds.

Sweet spot for pricesMost respondents preferred to buy properties priced from

$800,000 to $1 million, followed by those in the $1 million-to-$1.2

million price bracket. In the previous survey, the most pop-

ular price bracket was $1 million to $1.5

million, chosen by 41.9% of respondents;

28.1% chose the $500,000-to-$1 million

price bracket (see Charts 5 and 6).

According to Tan, the shift in preferred

price quantum could be due to a larger pro-

portion of respondents preferring a unit size

of 701 to 900 sq ft, the approximate size for

two-bedroom units, this year. More respon-

dents preferred three-bedroom units in the

previous survey.

In 2017, most of the transactions for

private non-landed residential properties

were in the $1 million-to-$1.5 million price

bracket, according to URA caveat data as

at Jan 2. The proportion of transactions in

this price bracket also rose 2.3 percentage

points from 2016. There appears to be a

shift in homebuyer’s preference from 2016

to 2017, showing a propensity to purchase

pricier properties, based on the proportion

of transactions in each price bracket. This

might be due to the type of units available

for sale in the market and the prices set by

sellers (see Chart 7).

ABSD biggest hurdle for buyersOf the 611 respondents in the latest survey,

44.4% said they did not plan to buy a resi-

dential property in the next 12 months and

the biggest hurdles holding them back were

the additional buyer’s stamp duty (33.6%),

preference for other types of investments

(30.3%) and uncertain economic and job

prospects (27.7%). A small proportion of

16.6% also felt that prices might decline

further (see Chart 8).

Delving deeper into the macro factors that

weigh on potential homebuyers’ minds, it

appears that people are most worried about

their job prospects and the global economy. At least 14.2% of

respondents said they had “poor” and “very poor” confidence

for their job prospects and 8.7% expressed low confidence in

the global economy (see Chart 9).

This could point to a “mismatch in market confidence ver-

sus current price recovery and home price affordability in Sin-

gapore, as many Singaporeans do not think that their future

job prospects and salary expectations match future housing

prices in Singapore”, says Tan.

“This can also be inferred from the price expectations of

Respondents most worried aboutjob prospects and global economy

Tan: Record land bid prices have created an expectation of higher prices, prompting buyers to take positions as soon as they can

Tee Khoon: Those not affected by collective sales may also be spurred to consider purchasing soon, as they foresee prices going up

FROM PREVIOUS PAGE

PICT

URES

: SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

Most of those looking to buy in the next 12 months are either owner-occupiers or rental investors

Top fi ve preferred unit types Top fi ve reasons for not intendingto buy within the next 12 months

The $1 million-to-$1.5 million price bracket accounted for most of thetransactions in 2017

Chart 3 Chart 4 Chart 8

Chart 7

80

70

60

50

40

30

20

10

0

60

50

40

30

20

10

0

35

30

25

20

15

10

5

0

25

20

15

10

5

0

Do not currently own property

Own one property

Own multiple properties

Note: Values do not total 100%, as respondents could choose more than one reason Note: Values do not total 100%, as respondents could choose more than one unit-type Note: Values do not total 100%, as respondents could choose more than one reason

Note: Based on URA caveat data for private non-landed residential property as at Jan 2

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, E

DGEP

ROP

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, K

NIG

HT F

RAN

K RE

SEAR

CH

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, K

NIG

HT F

RAN

K RE

SEAR

CHUR

A, E

DGEP

ROP

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, K

NIG

HT F

RAN

K RE

SEAR

CH

%

%

Perc

enta

ge o

f res

pons

es

Perc

enta

ge o

f res

pons

esPe

rcen

tage

of t

rans

actio

ns

I intend to move in I intend to rent it out

Most respondents would preferto buy properties priced from $800,000 to $1 mil

Chart 5 and 6

45

40

35

30

25

20

15

10

5

0

45

40

35

30

25

20

15

10

5

0

Note: The questions were phrased differently in the surveys and respondents were able to select up to two choices in the latest survey but only one in the previous survey. Values do not total 100%, as respondents could choose more than one price bracket.

%

%

Perc

enta

ge o

f res

pons

esPe

rcen

tage

of r

espo

nses

$800

,001

to

$1,0

00,0

00

$1,0

00,0

01 to

$1

,200

,000

$1,2

00,0

01 to

$1

,500

,000

$1,5

00,0

01 to

$1

,800

,000

$1,8

00,0

01 to

$2

,000

,000

$2,0

00,0

01 to

$2

,500

,000

$2,5

00,0

01 to

$3

,000

,000

Abov

e $3

,000

,000

$800

,001

to$1

,000

,000

$1,0

00,0

01 to

$1,2

00,0

00

$1,5

00,0

01 to

$1,8

00,0

00

$1,8

00,0

01 to

$2,0

00,0

00

$2,0

00,0

01 to

$2,5

00,0

00

$2,5

00,0

01 to

$3,0

00,0

00

$1,2

00,0

01 to

$1,5

00,0

00

$800

,000

and

be

low

Abov

e $3

,000

,000

Belo

w

$0.5

mil

$1 m

il to

$1

.5 m

il

$2 m

il to

$2

.5 m

il

$0.5

mil

to

$1 m

il

$1.5

mil

to

$2 m

il

$2.5

mil

to

$3 m

il

$3 m

il to

$3

.5 m

il

$3.5

mil

to

$4 m

il

$4 m

il to

$4

.5 m

il

Mor

e th

an

$5 m

il

Latest survey

Previous survey

38.6

10.0

25.9

5.9

31.8

8.0

15.5

5.1

2.3

8.3

41.9

1.8

28.1

1.8

13.4

0.5 0.5 1.4

2016 2017

Waiting forremoval of ABSD

Prefer otherasset classes

Uncertaineconomic and job prospects

Prices maydecline further

Market is currenty

unsuitable for investment

33.6

27.730.3

16.6 14.8

51.9

%

47.5

21.9 20.9

9.8

2-bedroom 3-bedroom 1-bedroom 4-bedroom 5-bedroom

74.7%

29.9

56.8

37.731.5

53.7

EDGEPROP | JANUARY 8, 2018 • EP7

COVER STORY

non-landed private residential units, with an increasing pro-

portion of respondents thinking that prices will increase more

than 3% a year in the medium to long term [see Chart 10].”

Their worries notwithstanding, people still felt confident

about Singapore’s political leadership, economy and the resi-

dential property market, with 58.4%, 51.4% and 52.3% of res-

pondents indicating a “good” and “excellent” confidence for

these factors, respectively.

Homebuyers’ sentiment might improve furtherOn Dec 13, the Ministry of National Development warned of

“a large potential supply of around 20,000 units from awarded

en-bloc sale and GLS sites that have not yet been granted plan-

ning approval, on top of the around 18,000 unsold units that

already have planning approval. Moreover, more than 30,000

existing private housing units remain vacant”.

Despite the high vacancy rate, an increasing proportion of

survey respondents think that rents will increase, and at a fast-

er pace of growth, in the longer term (see Chart 11).

In his 2018 New Year message, Prime Minister Lee Hsien

Loong said: “Last year, our economy grew 3.5%, more than

double our initial forecast. Incomes have gone up across the

board, especially for low and middle earners.”

Figures released by the Ministry of Trade and Industry on

Jan 2 show that Singapore’s GDP grew 3.1% y-o-y in 4Q2017

and the full-year growth, estimated at 3.5%, is higher than

the 2% growth in 2016.

“Despite stronger economic performance in 2017 versus 2016,

consumer sentiment remains fairly cautious amid rising infla-

tion,” says Tan. She notes that prospects in the job market have

remained tepid, with limited growth in overall employment, and

income growth could be uneven across various occupations and

income groups. “Nonetheless, the prospect of better conditions

this year may fuel interest for residential property,” she adds.

Another factor that could lead to more homebuyers en-

tering the market would be the spate of successful collective

sales. Those whose homes have been sold through such sales

will require replacement accommodation, says Tan Tee Khoon,

exe cutive director and head of residential project marketing

at Knight Frank Singapore. “Those not affected by collective

sales may also be spurred to consider purchasing soon, as they

foresee prices going up.”

Vista Park was put up for sale by tender on Nov 17, with

an asking price of $350 million. On Dec 14, Oxley Holdings an-

nounced its acquisition of Vista Park for $418 million ($1,096

psf per plot ratio). This follows its purchase of Apartment 8,

a freehold property on Meyappa Chettiar Road in Potong Pa-

sir, for $21.53 million. Oxley, which has been an active buyer

of collective sale sites, has nine residential projects with more

than 4,000 units in the pipeline for launch.

“[More people would] expect price increases across the

board, including for HDB flats in sought-after locations, when

they read news of aggressive land bids from the recent collec-

tive sale and government land sale sites,” says Tee Khoon. E

People are most worried aboutjob prospects

Chart 9

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, K

NIG

HT F

RAN

K RE

SEAR

CH

Confidence level in Singapore Residential Properties

Confidence level in Job Prospects

Confidence level in Singapore Economy

Confidence level in Singapore Political Leadership

Confidence level in Global Economy

Excellent Good Fair Poor Very poor

More people expect prices and rents to rise, and at a faster pace of growth, in the longer term

Charts 10 and 11

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

EDG

EPRO

P-KN

IGHT

FRA

NK

HOM

EBUY

ERS’

SEN

TIM

ENT

SURV

EY, K

NIG

HT F

RAN

K RE

SEAR

CH

Perc

enta

ge o

f res

pons

es

Perc

enta

ge o

f res

pons

es

Prices will continue falling

Prices will increase slightly: 1% to 3% a year

Prices will increase: more than 3% a year

Prices will remain relatively stable

Next 12 months Next 24 months Beyond 24 months Next 12 months Next 24 months Beyond 24 months

Rents will continue falling

Rents will increase slightly: 1% to 3% a year

Rents will increase: more than 3% a year

Rents will remain relatively stable

EP8 • EDGEPROP | JANUARY 8, 2018

Singapore — by postal districtLOCALITIES DISTRICTSCity & Southwest 1 to 8Orchard/Tanglin/Holland 9 and 10Newton/Bukit Timah/Clementi 11 and 21Balestier/MacPherson/Geylang 12 to 14East Coast 15 and 16Changi/Pasir Ris 17 and 18Serangoon/Thomson 19 and 20West 22 to 24North 25 to 28

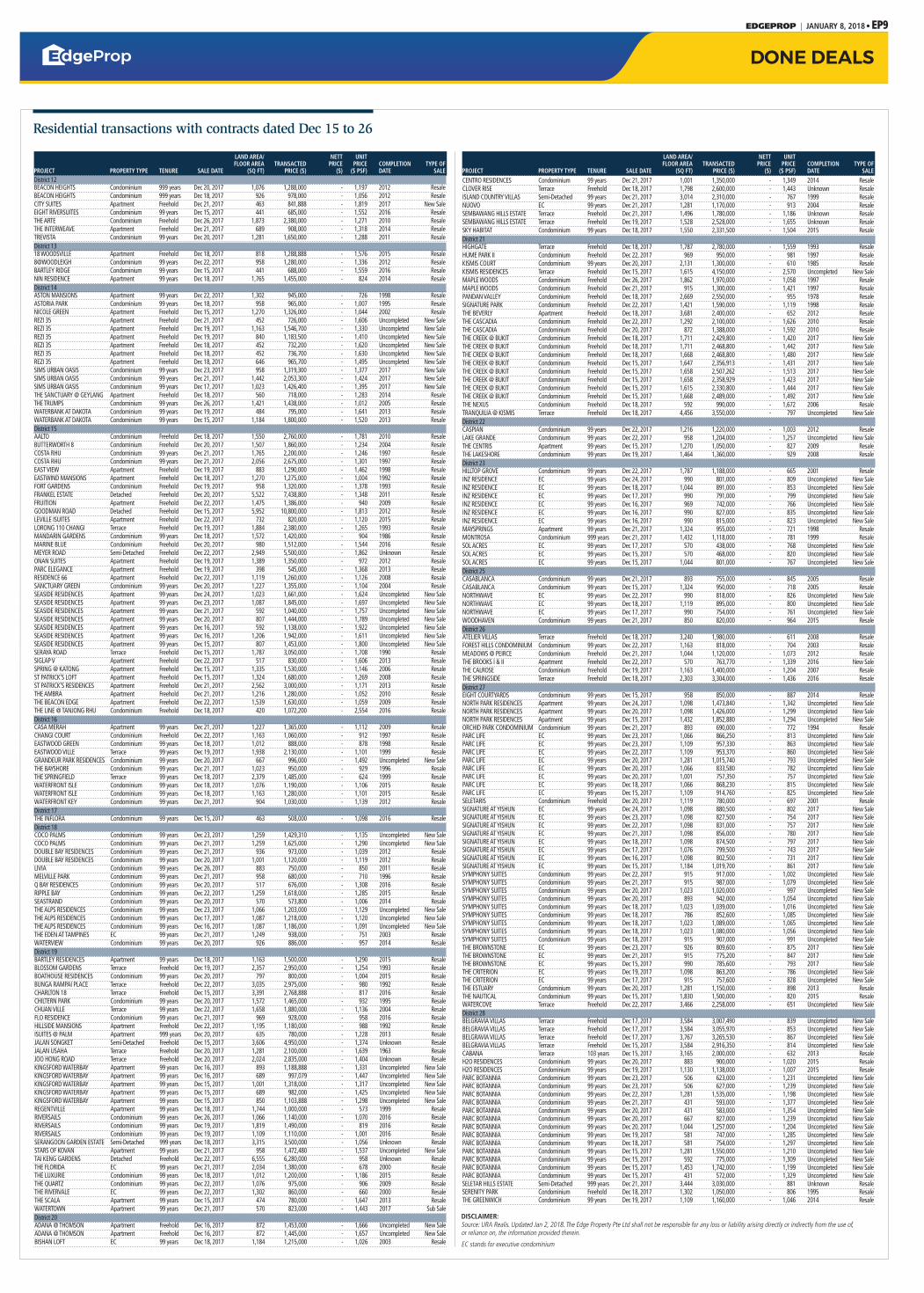

Residential transactions with contracts dated Dec 15 to 26

District 1 MARINA ONE RESIDENCES Apartment 99 years Dec 20, 2017 1,539 3,600,000 - 2,339 2017 New SaleTHE SAIL @ MARINA BAY Apartment 99 years Dec 19, 2017 1,184 2,400,000 - 2,027 2008 ResaleTHE SAIL @ MARINA BAY Apartment 99 years Dec 18, 2017 614 1,200,000 - 1,956 2008 ResaleDistrict 2 76 SHENTON Apartment 99 years Dec 18, 2017 592 1,186,000 - 2,003 2014 ResaleONZE @ TANJONG PAGAR Apartment Freehold Dec 22, 2017 1,141 2,821,800 - 2,473 2017 New SaleWALLICH RESIDENCE AT TANJONG PAGAR CENTRE Apartment 99 years Dec 23, 2017 614 2,020,000 - 3,292 2017 New SaleDistrict 3 ARTRA Apartment 99 years Dec 21, 2017 1,227 1,879,800 - 1,532 Uncompleted New SaleHIGHLINE RESIDENCES Condominium 99 years Dec 16, 2017 1,152 2,100,000 - 1,823 Uncompleted New SaleQUEENS Condominium 99 years Dec 22, 2017 1,184 1,380,000 - 1,165 2002 ResaleQUEENS Condominium 99 years Dec 15, 2017 1,184 1,380,000 - 1,165 2002 ResaleQUEENS PEAK Condominium 99 years Dec 16, 2017 775 1,309,000 - 1,689 Uncompleted New SaleREGENCY SUITES Apartment Freehold Dec 22, 2017 1,421 2,283,000 - 1,607 2008 ResaleTHE ANCHORAGE Condominium Freehold Dec 26, 2017 1,464 1,975,000 - 1,349 1997 ResaleTHE CREST Condominium 99 years Dec 22, 2017 1,539 2,827,000 - 1,837 2017 ResaleTHE CREST Condominium 99 years Dec 21, 2017 947 1,804,000 - 1,904 2017 ResaleTHE METROPOLITAN CONDOMINIUM Condominium 99 years Dec 15, 2017 1,367 1,930,000 - 1,412 2009 ResaleDistrict 4 HARBOUR SUITES Apartment Freehold Dec 21, 2017 527 850,000 - 1,612 2014 ResaleTHE INTERLACE Condominium 99 years Dec 26, 2017 1,066 1,350,000 - 1,267 2013 ResaleDistrict 5 DOVER PARKVIEW Condominium 99 years Dec 15, 2017 969 1,000,000 - 1,032 1997 ResaleFABER CREST Condominium 99 years Dec 18, 2017 1,744 1,460,000 - 837 2001 ResaleFABER DRIVE Detached Freehold Dec 15, 2017 8,493 8,200,000 - 966 1977 ResaleISLAND VIEW Condominium Freehold Dec 22, 2017 3,100 3,650,000 - 1,177 1984 ResaleLIIV RESIDENCES Apartment Freehold Dec 16, 2017 474 886,950 842,000 1,778 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 22, 2017 904 1,181,000 - 1,306 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 22, 2017 710 935,000 - 1,316 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 21, 2017 1,184 1,400,000 - 1,182 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 18, 2017 710 959,000 - 1,350 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 18, 2017 1,184 1,285,760 - 1,086 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 18, 2017 710 855,540 - 1,204 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 16, 2017 603 810,000 - 1,344 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 16, 2017 1,152 1,468,000 - 1,275 Uncompleted New SalePARC RIVIERA Condominium 99 years Dec 15, 2017 1,152 1,329,000 - 1,154 Uncompleted New SaleTAMAN MAS MERAH Semi-Detached Freehold Dec 20, 2017 3,240 2,800,000 - 866 Unknown ResaleTHE CLEMENT CANOPY Apartment 99 years Dec 18, 2017 1,109 1,657,000 - 1,495 Uncompleted New SaleTHE ORIENT Apartment Freehold Dec 23, 2017 1,130 1,960,000 - 1,734 2017 New SaleTHE PARC CONDOMINIUM Condominium Freehold Dec 15, 2017 1,292 1,580,000 - 1,223 2010 ResaleTHE TRILINQ Condominium 99 years Dec 21, 2017 1,109 1,412,000 - 1,274 2017 New Sale

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE

VARSITY PARK CONDOMINIUM Condominium 99 years Dec 23, 2017 1,302 1,500,000 - 1,152 2008 ResaleDistrict 7 DUO RESIDENCES Apartment 99 years Dec 20, 2017 614 1,390,000 - 2,266 2017 Sub SaleDUO RESIDENCES Apartment 99 years Dec 19, 2017 1,927 3,923,367 - 2,036 2017 New SaleDUO RESIDENCES Apartment 99 years Dec 15, 2017 1,927 4,110,000 - 2,133 2017 New SaleDUO RESIDENCES Apartment 99 years Dec 15, 2017 1,927 4,160,000 - 2,159 2017 New SaleDUO RESIDENCES Apartment 99 years Dec 15, 2017 1,927 4,145,000 - 2,151 2017 New SaleDistrict 8 CITY SQUARE RESIDENCES Condominium Freehold Dec 15, 2017 1,206 1,780,000 - 1,476 2008 ResaleCITYLIGHTS Condominium 99 years Dec 19, 2017 678 1,150,000 - 1,696 2007 ResaleCITYLIGHTS Condominium 99 years Dec 15, 2017 1,421 1,900,000 - 1,337 2007 ResaleCLYDES RESIDENCE Apartment Freehold Dec 18, 2017 1,023 1,150,000 - 1,125 2005 ResaleFORTE SUITES Apartment Freehold Dec 19, 2017 678 1,401,600 - 2,067 2016 New SaleFORTE SUITES Apartment Freehold Dec 17, 2017 624 1,210,000 - 1,938 2016 New SaleFORTE SUITES Apartment Freehold Dec 16, 2017 624 1,301,538 - 2,085 2016 New SaleKERRISDALE Condominium 99 years Dec 22, 2017 1,259 1,250,000 - 993 2005 ResaleMERA SPRINGS Condominium Freehold Dec 20, 2017 1,044 1,428,000 - 1,368 2008 ResaleSTURDEE RESIDENCES Condominium 99 years Dec 24, 2017 947 1,591,000 - 1,680 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 23, 2017 947 1,577,000 - 1,665 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 23, 2017 947 1,550,000 - 1,636 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 23, 2017 1,302 1,984,000 - 1,523 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 19, 2017 1,044 1,676,200 - 1,605 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 16, 2017 947 1,532,720 - 1,618 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 15, 2017 947 1,537,000 - 1,623 Uncompleted New SaleSTURDEE RESIDENCES Condominium 99 years Dec 15, 2017 1,302 1,866,000 - 1,433 Uncompleted New SaleDistrict 9 2 RVG Apartment Freehold Dec 21, 2017 926 1,680,000 - 1,815 2006 ResaleGAMBIER COURT Apartment 99 years Dec 18, 2017 1,485 1,750,000 - 1,178 1999 ResaleHILLTOPS Condominium Freehold Dec 19, 2017 2,390 8,500,000 - 3,557 2011 ResaleRESIDENCES @ KILLINEY Apartment Freehold Dec 22, 2017 2,368 4,098,888 - 1,731 2012 ResaleRIVERGATE Apartment Freehold Dec 15, 2017 1,044 2,250,000 - 2,155 2009 ResaleRIVERIA GARDENS Apartment Freehold Dec 18, 2017 1,432 2,933,550 - 2,049 2010 ResaleROBERTSON EDGE Apartment 999 years Dec 20, 2017 904 1,400,000 - 1,548 2008 ResaleSAM KIANG MANSIONS Apartment Freehold Dec 19, 2017 1,281 2,000,000 - 1,561 1999 ResaleSCOTTS SQUARE Apartment Freehold Dec 19, 2017 624 2,394,200 - 3,835 2011 ResaleSOPHIA HILLS Condominium 99 years Dec 22, 2017 667 1,360,000 - 2,038 Uncompleted New SaleSOPHIA HILLS Condominium 99 years Dec 17, 2017 570 1,280,000 - 2,244 Uncompleted New SaleSOPHIA HILLS Condominium 99 years Dec 15, 2017 721 1,435,000 - 1,990 Uncompleted New SaleTHE MARQ ON PATERSON HILL Condominium Freehold Dec 20, 2017 3,089 10,280,000 - 3,328 2011 ResaleWILKIE 80 Apartment Freehold Dec 19, 2017 603 980,000 - 1,626 2010 ResaleDistrict 10 BALMORAL 8 Condominium Freehold Dec 20, 2017 3,757 3,750,000 - 998 2003 ResaleDUCHESS CREST Condominium 99 years Dec 20, 2017 936 1,330,000 - 1,420 1998 ResaleDUCHESS MANOR Condominium 999 years Dec 15, 2017 635 1,100,000 - 1,732 2005 ResaleGALLOP GREEN Condominium Freehold Dec 15, 2017 3,272 5,600,000 - 1,711 2002 ResaleGOODWOOD RESIDENCE Condominium Freehold Dec 21, 2017 9,666 17,000,000 - 1,759 2013 ResaleLEEDON RESIDENCE Condominium Freehold Dec 20, 2017 4,704 9,450,000 - 2,009 2015 ResaleLERMIT ROAD Detached Freehold Dec 18, 2017 17,373 28,300,000 - 1,629 1994 ResaleLOFT @ NATHAN Apartment Freehold Dec 21, 2017 441 838,000 - 1,899 2014 ResaleNATHAN RESIDENCES Apartment Freehold Dec 15, 2017 775 1,450,000 - 1,871 2013 ResaleNATHAN SUITES Condominium Freehold Dec 18, 2017 1,776 3,430,000 - 1,931 2014 ResaleONE JERVOIS Condominium Freehold Dec 20, 2017 990 1,710,000 - 1,727 2009 ResaleONE TREE HILL Semi-Detached Freehold Dec 15, 2017 4,402 9,350,000 - 2,125 Unknown ResaleONE TREE HILL RESIDENCE Apartment Freehold Dec 26, 2017 2,454 4,300,000 - 1,752 2008 ResalePARVIS Condominium Freehold Dec 21, 2017 1,991 3,880,000 - 1,948 2012 ResaleROCHALIE DRIVE Detached Freehold Dec 22, 2017 16,770 33,000,000 - 1,968 Unknown ResaleSIXTH AVENUE Terrace 999 years Dec 22, 2017 2,293 2,738,000 - 1,192 Unknown ResaleTANGLIN REGENCY Condominium 99 years Dec 18, 2017 1,292 1,700,000 - 1,316 1998 ResaleTHE ARC AT DRAYCOTT Apartment Freehold Dec 26, 2017 1,270 2,900,000 - 2,283 2008 ResaleTHE BOULEVARD RESIDENCE Apartment Freehold Dec 21, 2017 2,034 5,000,000 - 2,458 2005 ResaleTHE ELEMENT @ STEVENS Apartment Freehold Dec 21, 2017 1,324 1,950,000 - 1,473 2007 ResaleTHE TRIZON Condominium Freehold Dec 15, 2017 1,894 2,980,000 - 1,573 2012 ResaleTOMLINSON HEIGHTS Condominium Freehold Dec 18, 2017 4,047 10,500,000 - 2,594 2014 ResaleVILLAGE TOWER Condominium Freehold Dec 26, 2017 1,808 2,470,000 - 1,366 1983 ResaleDistrict 11 6 DERBYSHIRE Condominium Freehold Dec 22, 2017 829 1,834,022 - 2,213 2017 Resale6 DERBYSHIRE Condominium Freehold Dec 20, 2017 1,012 2,056,863 - 2,033 2017 Resale6 DERBYSHIRE Condominium Freehold Dec 19, 2017 474 1,138,804 - 2,404 2017 ResaleBO SENG AVENUE Detached Freehold Dec 15, 2017 5,059 7,750,000 - 1,533 1999 ResaleCAPITOL PARK Semi-Detached Freehold Dec 26, 2017 4,047 6,816,800 - 1,686 1989 ResaleCUBE 8 Condominium Freehold Dec 20, 2017 560 850,000 - 1,519 2013 ResaleEVELYN ROAD Semi-Detached Freehold Dec 20, 2017 2,400 4,600,000 - 1,919 1993 ResaleJALAN BAHASA Detached Freehold Dec 26, 2017 9,268 14,500,000 - 1,565 2015 ResaleJALAN BAHASA Detached Freehold Dec 19, 2017 9,806 15,300,000 - 1,561 2015 ResaleNEWTON IMPERIAL Apartment Freehold Dec 21, 2017 1,938 3,200,000 - 1,652 2011 ResaleSIME ROAD Detached Freehold Dec 18, 2017 5,587 8,560,000 - 1,533 2007 ResaleSOLEIL @ SINARAN Condominium 99 years Dec 18, 2017 1,722 2,700,000 - 1,568 2011 ResaleUNIVERSITY PARK Semi-Detached 99 years Dec 19, 2017 2,648 2,888,888 - 1,092 1997 ResaleWATTEN ESTATE Terrace Freehold Dec 18, 2017 1,765 4,500,000 - 2,549 Unknown ResaleZEDGE Apartment Freehold Dec 18, 2017 700 1,060,000 - 1,515 2010 Resale

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE

| BY ANGELA TEO |

On Dec 18, 2017, three penthouses

at The Creek @ Bukit on Toh Tuck

Road were sold, according to caveats

lodged with URA. Of the three, the

1,668 sq ft, four-bedroom penthouse

went for $2.47 million and achieved the high-

est price psf of $1,480. The other two were

four-bedders measuring 1,711 sq ft that fetched

$2.47 million ($1,442 psf) and $2.43 million

($1,420 psf).

The penthouses were sold just three days

after local developer and construction compa-

ny Chiu Teng Group moved five units at the

freehold project. Of the five units sold, four

were three-bedroom mansionettes located on

the ground floor and measuring between 1,615

sq ft and 1,658 sq ft. The other was a 1,668 sq

ft, four-bedroom penthouse.

Prices of the four maisonettes ranged from

$2.33 million ($1,444 psf) for a 1,615 sq ft unit

to $2.51 million ($1,513 psf) for a 1,658 sq ft

unit. The penthouse was sold for $2.49 mil-

lion ($1,492 psf), registering the second-high-

est price among the five units sold on Dec 15.

The eight transactions at The Creek @ Bukit

on Dec 15 and 18 brought the total number of

units sold at the project to 253 units (97%), ac-

cording to caveats on URA Realis as at Jan 2,

2018, leaving only seven units for sale.

According to URA caveat data as at Jan 2,

2018, 101 units at The Creek @ Bukit were

sold in 2017, compared with 43 in 2016, 25

in 2015 and 42 each in 2013 and 2014. The

Creek @ Bukit, a redevelopment of the for-

mer Green Lodge, was launched in Novem-

ber 2013.

Sales at the project have been growing since

Malaysian property group S P Setia clinched

the adjacent, 201,287 sq ft site on Toh Tuck

Road under the 1H2017 Government Land

Sales (GLS) programme, for $265 million

($939 psf per plot ratio) last April. The 99-

year leasehold project is set to be launched

as Daintree Residence in 1H2018, with an

estimated 327 units.

The Toh Tuck Road residential area has

been transformed over the years through col-

lective sale redevelopments. Besides The Creek

@ Bukit, another redevelopment of a collec-

tive sale site in the area is the 31-unit Kismis Residences. The recently launched project sits

on part of the site of the former Kismis Lodge,

according to ERA Realty, which is jointly mar-

keting the two collective sale redevelopments

with Orange Tee & Tie.

About 300m away from Kismis Residences,

the 43-unit Kismis View was launched for col-

lective sale by marketing agent JLL on Nov 22

at a reserve price of $102 million. The tender

for Kismis View will close on Jan 17.

An upcoming collective sale redevelopment

site within the Toh Tuck Road residential en-

clave is the 210-unit Goodluck Garden, which

is in the advanced stage of the collective sale

process, according to marketing agent Knight

Frank Singapore. E

Toh Tuck area sees increase in buying interest

DONE DEALS

The Toh Tuck Road residential area has been transformed over the years through collective sale redevelopments

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

EDGEPROP | JANUARY 8, 2018 • EP9

Residential transactions with contracts dated Dec 15 to 26

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALEDistrict 12 BEACON HEIGHTS Condominium 999 years Dec 20, 2017 1,076 1,288,000 - 1,197 2012 ResaleBEACON HEIGHTS Condominium 999 years Dec 18, 2017 926 978,000 - 1,056 2012 ResaleCITY SUITES Apartment Freehold Dec 21, 2017 463 841,888 - 1,819 2017 New SaleEIGHT RIVERSUITES Condominium 99 years Dec 15, 2017 441 685,000 - 1,552 2016 ResaleTHE ARTE Condominium Freehold Dec 26, 2017 1,873 2,380,000 - 1,271 2010 ResaleTHE INTERWEAVE Apartment Freehold Dec 21, 2017 689 908,000 - 1,318 2014 ResaleTREVISTA Condominium 99 years Dec 20, 2017 1,281 1,650,000 - 1,288 2011 ResaleDistrict 13 18 WOODSVILLE Apartment Freehold Dec 18, 2017 818 1,288,888 - 1,576 2015 Resale8@WOODLEIGH Condominium 99 years Dec 22, 2017 958 1,280,000 - 1,336 2012 ResaleBARTLEY RIDGE Condominium 99 years Dec 15, 2017 441 688,000 - 1,559 2016 ResaleNIN RESIDENCE Apartment 99 years Dec 18, 2017 1,765 1,455,000 - 824 2014 ResaleDistrict 14 ASTON MANSIONS Apartment 99 years Dec 22, 2017 1,302 945,000 - 726 1998 ResaleASTORIA PARK Condominium 99 years Dec 18, 2017 958 965,000 - 1,007 1995 ResaleNICOLE GREEN Apartment Freehold Dec 15, 2017 1,270 1,326,000 - 1,044 2002 ResaleREZI 35 Apartment Freehold Dec 21, 2017 452 726,000 - 1,606 Uncompleted New SaleREZI 35 Apartment Freehold Dec 19, 2017 1,163 1,546,700 - 1,330 Uncompleted New SaleREZI 35 Apartment Freehold Dec 19, 2017 840 1,183,500 - 1,410 Uncompleted New SaleREZI 35 Apartment Freehold Dec 18, 2017 452 732,200 - 1,620 Uncompleted New SaleREZI 35 Apartment Freehold Dec 18, 2017 452 736,700 - 1,630 Uncompleted New SaleREZI 35 Apartment Freehold Dec 18, 2017 646 965,700 - 1,495 Uncompleted New SaleSIMS URBAN OASIS Condominium 99 years Dec 23, 2017 958 1,319,300 - 1,377 2017 New SaleSIMS URBAN OASIS Condominium 99 years Dec 21, 2017 1,442 2,053,300 - 1,424 2017 New SaleSIMS URBAN OASIS Condominium 99 years Dec 17, 2017 1,023 1,426,400 - 1,395 2017 New SaleTHE SANCTUARY @ GEYLANG Apartment Freehold Dec 18, 2017 560 718,000 - 1,283 2014 ResaleTHE TRUMPS Condominium 99 years Dec 26, 2017 1,421 1,438,000 - 1,012 2005 ResaleWATERBANK AT DAKOTA Condominium 99 years Dec 19, 2017 484 795,000 - 1,641 2013 ResaleWATERBANK AT DAKOTA Condominium 99 years Dec 15, 2017 1,184 1,800,000 - 1,520 2013 ResaleDistrict 15 AALTO Condominium Freehold Dec 18, 2017 1,550 2,760,000 - 1,781 2010 ResaleBUTTERWORTH 8 Condominium Freehold Dec 20, 2017 1,507 1,860,000 - 1,234 2004 ResaleCOSTA RHU Condominium 99 years Dec 21, 2017 1,765 2,200,000 - 1,246 1997 ResaleCOSTA RHU Condominium 99 years Dec 21, 2017 2,056 2,675,000 - 1,301 1997 ResaleEAST VIEW Apartment Freehold Dec 19, 2017 883 1,290,000 - 1,462 1998 ResaleEASTWIND MANSIONS Apartment Freehold Dec 18, 2017 1,270 1,275,000 - 1,004 1992 ResaleFORT GARDENS Condominium Freehold Dec 19, 2017 958 1,320,000 - 1,378 1993 ResaleFRANKEL ESTATE Detached Freehold Dec 20, 2017 5,522 7,438,800 - 1,348 2011 ResaleFRUITION Apartment Freehold Dec 22, 2017 1,475 1,386,000 - 940 2009 ResaleGOODMAN ROAD Detached Freehold Dec 15, 2017 5,952 10,800,000 - 1,813 2012 ResaleLEVILLE ISUITES Apartment Freehold Dec 22, 2017 732 820,000 - 1,120 2015 ResaleLORONG 110 CHANGI Terrace Freehold Dec 19, 2017 1,884 2,380,000 - 1,265 1993 ResaleMANDARIN GARDENS Condominium 99 years Dec 18, 2017 1,572 1,420,000 - 904 1986 ResaleMARINE BLUE Condominium Freehold Dec 20, 2017 980 1,512,000 - 1,544 2016 ResaleMEYER ROAD Semi-Detached Freehold Dec 22, 2017 2,949 5,500,000 - 1,862 Unknown ResaleONAN SUITES Apartment Freehold Dec 19, 2017 1,389 1,350,000 - 972 2012 ResalePARC ELEGANCE Apartment Freehold Dec 19, 2017 398 545,000 - 1,368 2013 ResaleRESIDENCE 66 Apartment Freehold Dec 22, 2017 1,119 1,260,000 - 1,126 2008 ResaleSANCTUARY GREEN Condominium 99 years Dec 20, 2017 1,227 1,355,000 - 1,104 2004 ResaleSEASIDE RESIDENCES Apartment 99 years Dec 24, 2017 1,023 1,661,000 - 1,624 Uncompleted New SaleSEASIDE RESIDENCES Apartment 99 years Dec 23, 2017 1,087 1,845,000 - 1,697 Uncompleted New SaleSEASIDE RESIDENCES Apartment 99 years Dec 21, 2017 592 1,040,000 - 1,757 Uncompleted New SaleSEASIDE RESIDENCES Apartment 99 years Dec 20, 2017 807 1,444,000 - 1,789 Uncompleted New SaleSEASIDE RESIDENCES Apartment 99 years Dec 16, 2017 592 1,138,000 - 1,922 Uncompleted New SaleSEASIDE RESIDENCES Apartment 99 years Dec 16, 2017 1,206 1,942,000 - 1,611 Uncompleted New SaleSEASIDE RESIDENCES Apartment 99 years Dec 15, 2017 807 1,453,000 - 1,800 Uncompleted New SaleSERAYA ROAD Terrace Freehold Dec 15, 2017 1,787 3,050,000 - 1,708 1990 ResaleSIGLAP V Apartment Freehold Dec 22, 2017 517 830,000 - 1,606 2013 ResaleSPRING @ KATONG Apartment Freehold Dec 15, 2017 1,335 1,530,000 - 1,146 2006 ResaleST PATRICK’S LOFT Apartment Freehold Dec 15, 2017 1,324 1,680,000 - 1,269 2008 ResaleST PATRICK’S RESIDENCES Apartment Freehold Dec 21, 2017 2,562 3,000,000 - 1,171 2013 ResaleTHE AMBRA Apartment Freehold Dec 21, 2017 1,216 1,280,000 - 1,052 2010 ResaleTHE BEACON EDGE Apartment Freehold Dec 22, 2017 1,539 1,630,000 - 1,059 2009 ResaleTHE LINE @ TANJONG RHU Condominium Freehold Dec 18, 2017 420 1,072,200 - 2,554 2016 ResaleDistrict 16 CASA MERAH Apartment 99 years Dec 21, 2017 1,227 1,365,000 - 1,112 2009 ResaleCHANGI COURT Condominium Freehold Dec 22, 2017 1,163 1,060,000 - 912 1997 ResaleEASTWOOD GREEN Condominium 99 years Dec 18, 2017 1,012 888,000 - 878 1998 ResaleEASTWOOD VILLE Terrace 99 years Dec 19, 2017 1,938 2,130,000 - 1,101 1999 ResaleGRANDEUR PARK RESIDENCES Condominium 99 years Dec 20, 2017 667 996,000 - 1,492 Uncompleted New SaleTHE BAYSHORE Condominium 99 years Dec 21, 2017 1,023 950,000 - 929 1996 ResaleTHE SPRINGFIELD Terrace 99 years Dec 18, 2017 2,379 1,485,000 - 624 1999 ResaleWATERFRONT ISLE Condominium 99 years Dec 18, 2017 1,076 1,190,000 - 1,106 2015 ResaleWATERFRONT ISLE Condominium 99 years Dec 18, 2017 1,163 1,280,000 - 1,101 2015 ResaleWATERFRONT KEY Condominium 99 years Dec 21, 2017 904 1,030,000 - 1,139 2012 ResaleDistrict 17 THE INFLORA Condominium 99 years Dec 15, 2017 463 508,000 - 1,098 2016 ResaleDistrict 18 COCO PALMS Condominium 99 years Dec 23, 2017 1,259 1,429,310 - 1,135 Uncompleted New SaleCOCO PALMS Condominium 99 years Dec 21, 2017 1,259 1,625,000 - 1,290 Uncompleted New SaleDOUBLE BAY RESIDENCES Condominium 99 years Dec 21, 2017 936 973,000 - 1,039 2012 ResaleDOUBLE BAY RESIDENCES Condominium 99 years Dec 20, 2017 1,001 1,120,000 - 1,119 2012 ResaleLIVIA Condominium 99 years Dec 26, 2017 883 750,000 - 850 2011 ResaleMELVILLE PARK Condominium 99 years Dec 21, 2017 958 680,000 - 710 1996 ResaleQ BAY RESIDENCES Condominium 99 years Dec 20, 2017 517 676,000 - 1,308 2016 ResaleRIPPLE BAY Condominium 99 years Dec 22, 2017 1,259 1,618,000 - 1,285 2015 ResaleSEASTRAND Condominium 99 years Dec 20, 2017 570 573,800 - 1,006 2014 ResaleTHE ALPS RESIDENCES Condominium 99 years Dec 23, 2017 1,066 1,203,000 - 1,129 Uncompleted New SaleTHE ALPS RESIDENCES Condominium 99 years Dec 17, 2017 1,087 1,218,000 - 1,120 Uncompleted New SaleTHE ALPS RESIDENCES Condominium 99 years Dec 16, 2017 1,087 1,186,000 - 1,091 Uncompleted New SaleTHE EDEN AT TAMPINES EC 99 years Dec 21, 2017 1,249 938,000 - 751 2003 ResaleWATERVIEW Condominium 99 years Dec 20, 2017 926 886,000 - 957 2014 ResaleDistrict 19 BARTLEY RESIDENCES Apartment 99 years Dec 18, 2017 1,163 1,500,000 - 1,290 2015 ResaleBLOSSOM GARDENS Terrace Freehold Dec 19, 2017 2,357 2,950,000 - 1,254 1993 ResaleBOATHOUSE RESIDENCES Condominium 99 years Dec 20, 2017 797 800,000 - 1,004 2015 ResaleBUNGA RAMPAI PLACE Terrace Freehold Dec 22, 2017 3,035 2,975,000 - 980 1992 ResaleCHARLTON 18 Terrace Freehold Dec 15, 2017 3,391 2,768,888 - 817 2016 ResaleCHILTERN PARK Condominium 99 years Dec 20, 2017 1,572 1,465,000 - 932 1995 ResaleCHUAN VILLE Terrace 99 years Dec 22, 2017 1,658 1,880,000 - 1,136 2004 ResaleFLO RESIDENCE Condominium 99 years Dec 21, 2017 969 928,000 - 958 2016 ResaleHILLSIDE MANSIONS Apartment Freehold Dec 22, 2017 1,195 1,180,000 - 988 1992 ResaleISUITES @ PALM Apartment 999 years Dec 20, 2017 635 780,000 - 1,228 2013 ResaleJALAN SONGKET Semi-Detached Freehold Dec 15, 2017 3,606 4,950,000 - 1,374 Unknown ResaleJALAN USAHA Terrace Freehold Dec 20, 2017 1,281 2,100,000 - 1,639 1963 ResaleJOO HONG ROAD Terrace Freehold Dec 20, 2017 2,024 2,835,000 - 1,404 Unknown ResaleKINGSFORD WATERBAY Apartment 99 years Dec 16, 2017 893 1,188,888 - 1,331 Uncompleted New SaleKINGSFORD WATERBAY Apartment 99 years Dec 16, 2017 689 997,079 - 1,447 Uncompleted New SaleKINGSFORD WATERBAY Apartment 99 years Dec 15, 2017 1,001 1,318,000 - 1,317 Uncompleted New SaleKINGSFORD WATERBAY Apartment 99 years Dec 15, 2017 689 982,000 - 1,425 Uncompleted New SaleKINGSFORD WATERBAY Apartment 99 years Dec 15, 2017 850 1,103,888 - 1,298 Uncompleted New SaleREGENTVILLE Apartment 99 years Dec 18, 2017 1,744 1,000,000 - 573 1999 ResaleRIVERSAILS Condominium 99 years Dec 26, 2017 1,066 1,140,000 - 1,070 2016 ResaleRIVERSAILS Condominium 99 years Dec 19, 2017 1,819 1,490,000 - 819 2016 ResaleRIVERSAILS Condominium 99 years Dec 19, 2017 1,109 1,110,000 - 1,001 2016 ResaleSERANGOON GARDEN ESTATE Semi-Detached 999 years Dec 18, 2017 3,315 3,500,000 - 1,056 Unknown ResaleSTARS OF KOVAN Apartment 99 years Dec 21, 2017 958 1,472,480 - 1,537 Uncompleted New SaleTAI KENG GARDENS Detached Freehold Dec 22, 2017 6,555 6,280,000 - 958 Unknown ResaleTHE FLORIDA EC 99 years Dec 21, 2017 2,034 1,380,000 - 678 2000 ResaleTHE LUXURIE Condominium 99 years Dec 18, 2017 1,012 1,200,000 - 1,186 2015 ResaleTHE QUARTZ Condominium 99 years Dec 22, 2017 1,076 975,000 - 906 2009 ResaleTHE RIVERVALE EC 99 years Dec 22, 2017 1,302 860,000 - 660 2000 ResaleTHE SCALA Apartment 99 years Dec 15, 2017 474 780,000 - 1,647 2013 ResaleWATERTOWN Apartment 99 years Dec 21, 2017 570 823,000 - 1,443 2017 Sub SaleDistrict 20 ADANA @ THOMSON Apartment Freehold Dec 16, 2017 872 1,453,000 - 1,666 Uncompleted New SaleADANA @ THOMSON Apartment Freehold Dec 16, 2017 872 1,445,000 - 1,657 Uncompleted New SaleBISHAN LOFT EC 99 years Dec 18, 2017 1,184 1,215,000 - 1,026 2003 Resale

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE

CENTRO RESIDENCES Condominium 99 years Dec 21, 2017 1,001 1,350,000 - 1,349 2014 ResaleCLOVER RISE Terrace Freehold Dec 18, 2017 1,798 2,600,000 - 1,443 Unknown ResaleISLAND COUNTRY VILLAS Semi-Detached 99 years Dec 21, 2017 3,014 2,310,000 - 767 1999 ResaleNUOVO EC 99 years Dec 21, 2017 1,281 1,170,000 - 913 2004 ResaleSEMBAWANG HILLS ESTATE Terrace Freehold Dec 21, 2017 1,496 1,780,000 - 1,186 Unknown ResaleSEMBAWANG HILLS ESTATE Terrace Freehold Dec 19, 2017 1,528 2,528,000 - 1,655 Unknown ResaleSKY HABITAT Condominium 99 years Dec 18, 2017 1,550 2,331,500 - 1,504 2015 ResaleDistrict 21 HIGHGATE Terrace Freehold Dec 18, 2017 1,787 2,780,000 - 1,559 1993 ResaleHUME PARK II Condominium Freehold Dec 22, 2017 969 950,000 - 981 1997 ResaleKISMIS COURT Condominium 99 years Dec 20, 2017 2,131 1,300,000 - 610 1985 ResaleKISMIS RESIDENCES Terrace Freehold Dec 15, 2017 1,615 4,150,000 - 2,570 Uncompleted New SaleMAPLE WOODS Condominium Freehold Dec 26, 2017 1,862 1,970,000 - 1,058 1997 ResaleMAPLE WOODS Condominium Freehold Dec 21, 2017 915 1,300,000 - 1,421 1997 ResalePANDAN VALLEY Condominium Freehold Dec 18, 2017 2,669 2,550,000 - 955 1978 ResaleSIGNATURE PARK Condominium Freehold Dec 22, 2017 1,421 1,590,000 - 1,119 1998 ResaleTHE BEVERLY Apartment Freehold Dec 18, 2017 3,681 2,400,000 - 652 2012 ResaleTHE CASCADIA Condominium Freehold Dec 22, 2017 1,292 2,100,000 - 1,626 2010 ResaleTHE CASCADIA Condominium Freehold Dec 20, 2017 872 1,388,000 - 1,592 2010 ResaleTHE CREEK @ BUKIT Condominium Freehold Dec 18, 2017 1,711 2,429,800 - 1,420 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 18, 2017 1,711 2,468,800 - 1,442 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 18, 2017 1,668 2,468,800 - 1,480 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 15, 2017 1,647 2,356,913 - 1,431 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 15, 2017 1,658 2,507,262 - 1,513 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 15, 2017 1,658 2,358,929 - 1,423 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 15, 2017 1,615 2,330,800 - 1,444 2017 New SaleTHE CREEK @ BUKIT Condominium Freehold Dec 15, 2017 1,668 2,489,000 - 1,492 2017 New SaleTHE NEXUS Condominium Freehold Dec 18, 2017 592 990,000 - 1,672 2006 ResaleTRANQUILIA @ KISMIS Terrace Freehold Dec 18, 2017 4,456 3,550,000 - 797 Uncompleted New SaleDistrict 22 CASPIAN Condominium 99 years Dec 22, 2017 1,216 1,220,000 - 1,003 2012 ResaleLAKE GRANDE Condominium 99 years Dec 22, 2017 958 1,204,000 - 1,257 Uncompleted New SaleTHE CENTRIS Apartment 99 years Dec 15, 2017 1,270 1,050,000 - 827 2009 ResaleTHE LAKESHORE Condominium 99 years Dec 19, 2017 1,464 1,360,000 - 929 2008 ResaleDistrict 23 HILLTOP GROVE Condominium 99 years Dec 22, 2017 1,787 1,188,000 - 665 2001 ResaleINZ RESIDENCE EC 99 years Dec 24, 2017 990 801,000 - 809 Uncompleted New SaleINZ RESIDENCE EC 99 years Dec 18, 2017 1,044 891,000 - 853 Uncompleted New SaleINZ RESIDENCE EC 99 years Dec 17, 2017 990 791,000 - 799 Uncompleted New SaleINZ RESIDENCE EC 99 years Dec 16, 2017 969 742,000 - 766 Uncompleted New SaleINZ RESIDENCE EC 99 years Dec 16, 2017 990 827,000 - 835 Uncompleted New SaleINZ RESIDENCE EC 99 years Dec 16, 2017 990 815,000 - 823 Uncompleted New SaleMAYSPRINGS Apartment 99 years Dec 21, 2017 1,324 955,000 - 721 1998 ResaleMONTROSA Condominium 999 years Dec 21, 2017 1,432 1,118,000 - 781 1999 ResaleSOL ACRES EC 99 years Dec 17, 2017 570 438,000 - 768 Uncompleted New SaleSOL ACRES EC 99 years Dec 15, 2017 570 468,000 - 820 Uncompleted New SaleSOL ACRES EC 99 years Dec 15, 2017 1,044 801,000 - 767 Uncompleted New SaleDistrict 25 CASABLANCA Condominium 99 years Dec 21, 2017 893 755,000 - 845 2005 ResaleCASABLANCA Condominium 99 years Dec 15, 2017 1,324 950,000 - 718 2005 ResaleNORTHWAVE EC 99 years Dec 22, 2017 990 818,000 - 826 Uncompleted New SaleNORTHWAVE EC 99 years Dec 18, 2017 1,119 895,000 - 800 Uncompleted New SaleNORTHWAVE EC 99 years Dec 17, 2017 990 754,000 - 761 Uncompleted New SaleWOODHAVEN Condominium 99 years Dec 21, 2017 850 820,000 - 964 2015 ResaleDistrict 26 ATELIER VILLAS Terrace Freehold Dec 18, 2017 3,240 1,980,000 - 611 2008 ResaleFOREST HILLS CONDOMINIUM Condominium 99 years Dec 22, 2017 1,163 818,000 - 704 2003 ResaleMEADOWS @ PEIRCE Condominium Freehold Dec 21, 2017 1,044 1,120,000 - 1,073 2012 ResaleTHE BROOKS I & II Apartment Freehold Dec 22, 2017 570 763,770 - 1,339 2016 New SaleTHE CALROSE Condominium Freehold Dec 19, 2017 1,163 1,400,000 - 1,204 2007 ResaleTHE SPRINGSIDE Terrace Freehold Dec 18, 2017 2,303 3,304,000 - 1,436 2016 ResaleDistrict 27 EIGHT COURTYARDS Condominium 99 years Dec 15, 2017 958 850,000 - 887 2014 ResaleNORTH PARK RESIDENCES Apartment 99 years Dec 24, 2017 1,098 1,473,840 - 1,342 Uncompleted New SaleNORTH PARK RESIDENCES Apartment 99 years Dec 20, 2017 1,098 1,426,000 - 1,299 Uncompleted New SaleNORTH PARK RESIDENCES Apartment 99 years Dec 15, 2017 1,432 1,852,880 - 1,294 Uncompleted New SaleORCHID PARK CONDOMINIUM Condominium 99 years Dec 21, 2017 893 690,000 - 772 1994 ResalePARC LIFE EC 99 years Dec 23, 2017 1,066 866,250 - 813 Uncompleted New SalePARC LIFE EC 99 years Dec 23, 2017 1,109 957,330 - 863 Uncompleted New SalePARC LIFE EC 99 years Dec 22, 2017 1,109 953,370 - 860 Uncompleted New SalePARC LIFE EC 99 years Dec 20, 2017 1,281 1,015,740 - 793 Uncompleted New SalePARC LIFE EC 99 years Dec 20, 2017 1,066 833,580 - 782 Uncompleted New SalePARC LIFE EC 99 years Dec 20, 2017 1,001 757,350 - 757 Uncompleted New SalePARC LIFE EC 99 years Dec 18, 2017 1,066 868,230 - 815 Uncompleted New SalePARC LIFE EC 99 years Dec 15, 2017 1,109 914,760 - 825 Uncompleted New SaleSELETARIS Condominium Freehold Dec 20, 2017 1,119 780,000 - 697 2001 ResaleSIGNATURE AT YISHUN EC 99 years Dec 24, 2017 1,098 880,500 - 802 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 23, 2017 1,098 827,500 - 754 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 22, 2017 1,098 831,000 - 757 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 21, 2017 1,098 856,000 - 780 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 18, 2017 1,098 874,500 - 797 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 17, 2017 1,076 799,500 - 743 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 16, 2017 1,098 802,500 - 731 2017 New SaleSIGNATURE AT YISHUN EC 99 years Dec 15, 2017 1,184 1,019,700 - 861 2017 New SaleSYMPHONY SUITES Condominium 99 years Dec 22, 2017 915 917,000 - 1,002 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 21, 2017 915 987,000 - 1,079 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 20, 2017 1,023 1,020,000 - 997 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 20, 2017 893 942,000 - 1,054 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 18, 2017 1,023 1,039,000 - 1,016 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 18, 2017 786 852,600 - 1,085 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 18, 2017 1,023 1,089,000 - 1,065 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 18, 2017 1,023 1,080,000 - 1,056 Uncompleted New SaleSYMPHONY SUITES Condominium 99 years Dec 18, 2017 915 907,000 - 991 Uncompleted New SaleTHE BROWNSTONE EC 99 years Dec 23, 2017 926 809,600 - 875 2017 New SaleTHE BROWNSTONE EC 99 years Dec 21, 2017 915 775,200 - 847 2017 New SaleTHE BROWNSTONE EC 99 years Dec 15, 2017 990 785,600 - 793 2017 New SaleTHE CRITERION EC 99 years Dec 19, 2017 1,098 863,200 - 786 Uncompleted New SaleTHE CRITERION EC 99 years Dec 17, 2017 915 757,600 - 828 Uncompleted New SaleTHE ESTUARY Condominium 99 years Dec 20, 2017 1,281 1,150,000 - 898 2013 ResaleTHE NAUTICAL Condominium 99 years Dec 15, 2017 1,830 1,500,000 - 820 2015 ResaleWATERCOVE Terrace Freehold Dec 22, 2017 3,466 2,258,000 - 651 Uncompleted New SaleDistrict 28 BELGRAVIA VILLAS Terrace Freehold Dec 17, 2017 3,584 3,007,490 - 839 Uncompleted New SaleBELGRAVIA VILLAS Terrace Freehold Dec 17, 2017 3,584 3,055,970 - 853 Uncompleted New SaleBELGRAVIA VILLAS Terrace Freehold Dec 17, 2017 3,767 3,265,530 - 867 Uncompleted New SaleBELGRAVIA VILLAS Terrace Freehold Dec 15, 2017 3,584 2,916,350 - 814 Uncompleted New SaleCABANA Terrace 103 years Dec 15, 2017 3,165 2,000,000 - 632 2013 ResaleH2O RESIDENCES Condominium 99 years Dec 20, 2017 883 900,000 - 1,020 2015 ResaleH2O RESIDENCES Condominium 99 years Dec 19, 2017 1,130 1,138,000 - 1,007 2015 ResalePARC BOTANNIA Condominium 99 years Dec 23, 2017 506 623,000 - 1,231 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 23, 2017 506 627,000 - 1,239 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 22, 2017 1,281 1,535,000 - 1,198 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 21, 2017 431 593,000 - 1,377 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 20, 2017 431 583,000 - 1,354 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 20, 2017 667 827,000 - 1,239 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 20, 2017 1,044 1,257,000 - 1,204 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 19, 2017 581 747,000 - 1,285 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 18, 2017 581 754,000 - 1,297 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 15, 2017 1,281 1,550,000 - 1,210 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 15, 2017 592 775,000 - 1,309 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 15, 2017 1,453 1,742,000 - 1,199 Uncompleted New SalePARC BOTANNIA Condominium 99 years Dec 15, 2017 431 572,000 - 1,329 Uncompleted New SaleSELETAR HILLS ESTATE Semi-Detached 999 years Dec 21, 2017 3,444 3,030,000 - 881 Unknown ResaleSERENITY PARK Condominium Freehold Dec 18, 2017 1,302 1,050,000 - 806 1995 ResaleTHE GREENWICH Condominium 99 years Dec 19, 2017 1,109 1,160,000 - 1,046 2014 Resale

DONE DEALS

DISCLAIMER:Source: URA Realis. Updated Jan 2, 2018. The Edge Property Pte Ltd shall not be responsible for any loss or liability arising directly or indirectly from the use of, or reliance on, the information provided therein.

EC stands for executive condominium

GAINS AND LOSSES

EP10 • EDGEPROP | JANUARY 8, 2018

Unit at The Marq sold at $4.9 mil loss

E

Top 10 gains and losses from Dec 15 to 26, 2017

URA,

EDG

EPRO

P

Most profi table deals PROJECT DISTRICT AREA (SQ FT) SOLD ON (2017) SALE PRICE ($ PSF) BOUGHT ON PURCHASE PRICE ($ PSF) PROFIT ($) PROFIT (%) ANNUALISED PROFIT (%) HOLDING PERIOD (YEARS)

1 Goodwood Residence 10 9,666 Dec 21 1,759 June 9, 2010 1,560 1,920,000 13 2 7.5

2 Pandan Valley 21 2,669 Dec 18 955 Aug 17, 1999 472 1,290,000 102 4 18.4

3 Village Tower 10 1,808 Dec 26 1,366 Oct 2, 2006 708 1,190,000 93 6 11.2

4 Island View 5 3,100 Dec 22 1,177 July 22, 2009 806 1,150,000 46 5 8.4

5 City Square Residences 8 1,206 Dec 15 1,476 May 9, 2005 563 1,101,520 162 8 12.6

6 Signature Park 21 1,421 Dec 22 1,119 Nov 26, 2004 467 927,000 140 7 13.1

7 Rivergate 9 1,044 Dec 15 2,155 Dec 29, 2006 1,277 916,920 69 5 11.0

8 Parvis 10 1,991 Dec 21 1,948 Dec 30, 2009 1,495 903,390 30 3 8.0

9 Balmoral 8 10 3,757 Dec 20 998 Feb 28, 2002 793 804,843 27 2 15.8

10 Nicole Green 14 1,270 Dec 15 1,044 Feb 27, 2003 486 709,200 115 5 14.8

PROJECT DISTRICT AREA (SQ FT) SOLD ON (2017) SALE PRICE ($ PSF) BOUGHT ON PURCHASE PRICE ($ PSF) LOSS ($) LOSS (%) ANNUALISED LOSS (%) HOLDING PERIOD (YEARS)

1 The Marq on Paterson Hill 9 3,089 Dec 20 3,328 Sept 17, 2012 4,920 4,920,000 32 7 5.3

2 Newton Imperial 11 1,938 Dec 21 1,652 July 2, 2013 2,021 714,760 18 4 4.5

3 The Trizon 10 1,894 Dec 15 1,573 June 25, 2012 1,795 420,300 12 2 5.5

4 Residences @ Killiney 9 2,368 Dec 22 1,731 Aug 19, 2009 1,853 289,499 7 1 8.3

5 The Cascadia 21 872 Dec 20 1,592 Jan 25, 2013 1,844 220,000 14 3 4.9

6 St Patrick’s Residences 15 2,562 Dec 21 1,171 Nov 30, 2012 1,254 211,888 7 1 5.1

7 The Arc At Draycott 10 1,270 Dec 26 2,283 July 11, 2007 2,430 186,100 6 1 10.5

8 Seletaris 27 1,119 Dec 20 697 Dec 19, 2013 831 150,000 16 4 4.0

9 The Centris 22 1,270 Dec 15 827 Feb 18, 2013 945 150,000 13 3 4.8

10 Varsity Park Condominium 5 1,302 Dec 23 1,152 May 9, 2013 1,228 100,000 6 1 4.6

Note: Computed based on URA caveat data as at Jan 2 for private non-landed houses transacted between Dec 15 to 26, 2017. The profit-and-loss computation excludes transaction costs such as stamp duties.

PROJECT DISTRICT AREA (SQ FT) SOLD ON (2017) SALE PRICE ($ PSF) BOUGHT ON PURCHASE PRICE ($ PSF) LOSS ($) LOSS (%) ANNUALISED LOSS (%) HOLDING PERIOD (YEARS)DISTRICT SOLD ON (2017) BOUGHT ON LOSS ($) ANNUALISED LOSS (%)

Non-profi table deals

| BY TIMOTHY TAY |

The highest recorded loss in the week of

Dec 15 to 26, 2017 was from the sale of

a four-bedroom unit at the ultra-luxu-

ry condominium The Marq on Pater-son Hill. The seller bought the 3,089

sq ft unit from the developer for $15.2 million

($4,920 psf) in 2012. He sold it for $10.28 mil-

lion ($3,328 psf) on Dec 20 and incurred a $4.92

million (32%) loss, or an annualised loss of 7%

over a five-year holding period. According to a

property agent who declined to be named, the

seller is a Singaporean who has units in other

ultra-luxury projects in Singapore.

The first tranche of units sold at The Marq

when the project was launched in June 2007

was priced from $3,600 psf, but prices quick-

ly escalated to $5,262 psf by September that

year. The highest absolute price achieved at the

luxury condo is $31.4 million ($5,100 psf), for

a 6,157 sq ft unit transacted in July 2007. The

Marq also holds the record for the highest price

psf to date — $6,840 psf, for a 3,003 sq ft unit

on the 20th floor, which was bought by a for-

eigner for $20.54 million.

Only one other unit changed hands at The

Marq last year — a 6,232 sq ft mid-level unit

at The Signature Tower, which went for $21.8

million ($3,498 psf), according to a caveat

lodged in April 2017. The unit was last sold

for $26.4 million ($4,242 psf) in July 2007.

Completed in 2011, The Marq offers 66 units

in two 24-storey towers. At the Premier Tower,

a typical four-bedroom unit is around 3,000 sq

ft; at the Signature Tower, it is above 6,000 sq

ft and comes with a 15m lap pool. The Marq

on Paterson Hill was hailed as the foremost ul-

tra-luxury condo when it was launched a dec-

ade ago. It was developed by SC Global De-

velopments, which also developed Sculptura

Ardmore, where a super penthouse of 10,300 sq

ft sold for over $60 million, or $6,000-plus psf.

Over the past quarter, other freehold ul-

tra-luxury condos such as The Nassim and The

Ritz-Carlton Residences as well as Sculptura

The Marq on Paterson Hill. Find the most affordable listing in the project at edgepr.link/TheMarqOnPatersonHill

Ardmore have seen sales ranging from $3,171

to $4,171 psf, says Dominic Lee, PropNex Re-

alty head of the luxury team. Even the 99-year

leasehold luxury condos in integrated develop-

ments such as Wallich Residence at Tanjong Pa-

gar have seen prices hit a high of $4,000 psf.

Lee is optimistic that the residential market

will be more buoyant this year, but cautions

that over-exuberance could lead to the recovery

being short-lived. While local buyers account

for the majority of the transactions in the lux-

ury condo segment, he sees interest from for-

eign buyers returning, fuelling the rise in prices.

Meanwhile, the most profitable deal re-

corded in the week of Dec 15 to 26 was for

the sale of a penthouse at the luxury condo

Goodwood Residence, off Bukit Timah Road. The 9,666 sq ft unit on the 12th floor of one

of the blocks was purchased for $15.08 mil-

lion ($1,560 psf) in 2010 and sold for $17 mil-

lion ($1,759 psf), according to a caveat lodged