Money market

49

-

Upload

mallikarjuna-tr -

Category

Education

-

view

297 -

download

0

Transcript of Money market

As per RBI definit ions “ A market for shor t terms f inancial assets that are close substitute for money, facil itates the exchange of money in primary and secondary market”.

The money market is a mechanism that deals with the lending and borrowing of shor t term funds (less than one year).

A segment of the f inancial market in which f inancial instruments with high l iquidity and very shor t maturit ies are traded.

I t doesn’t actually deal in cash or money but deals with substitute of cash l ike trade bil ls, promissory notes & government papers which can conver ted into cash without any loss at low transaction cost.

I t includes all individual, institution and intermediaries.

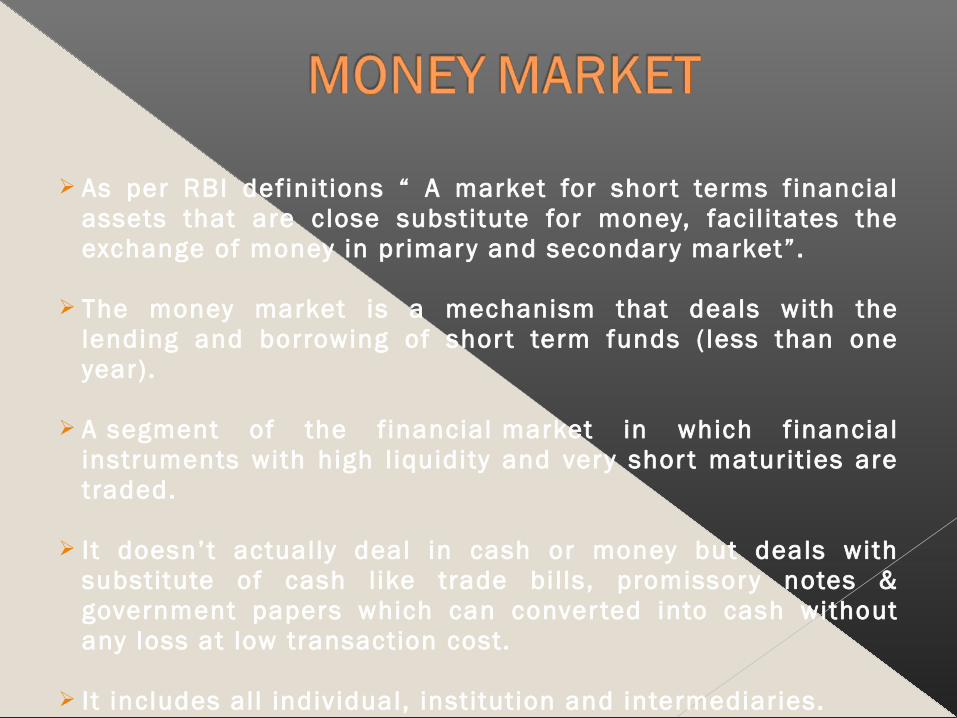

It is a market purely for short-terms funds or financial assets called near money.

It deals with financial assets having a maturity period less than one year only.

In Money Market transaction can not take place formal like stock exchange, only through oral communication, relevant document and written communication transaction can be done.

Transaction have to be conducted without the help of brokers.

It is not a single homogeneous market, it comprises of several submarket like call money market, acceptance & bill market.

The component of Money Market are the commercial banks, acceptance houses & NBFC (Non-banking financial companies).

To provide a parking place to employ short term surplus funds.

To provide room for overcoming short term deficits.

To enable the central bank to influence and regulate liquidity in the economy through its intervention in this market.

To provide a reasonable access to users of short-term funds to meet their requirement quickly, adequately at reasonable cost.

o Development of trade & industry.o Development of capital market.o Smooth functioning of commercial banks.o Effective central bank control.o Formulation of suitable monetary policy.o Non inflationary source of finance to

government.

I :- ORGANISED STRUCTURE 1. Reserve bank of India. 2. DFHI (discount and finance house of India).

3. Commercial banks i. Public sector banks SBI with 7 subsidiaries Cooperative banks 20 nationalised banks ii. Private banks Indian Banks Foreign banks4. Development bank IDBI, IFCI, ICICI, NABARD, LIC, GIC, UTI etc.

II. UNORGANISED SECTOR 1. Indigenous banks 2 Money lenders 3. Chits 4. Nidhis

III. CO-OPERATIVE SECTOR 1. State cooperative i. central cooperative banks Primary Agri credit societies Primary urban banks 2. State Land development banks central land development banks Primary land development banks

Money Market consists of a number of sub-markets which collectively constitute the money market. They are:

Call Money MarketCommercial bills market or discount marketAcceptance market Treasury bill market

A variety of instrument are available in a developed money market. In India till 1986, only a few instrument were available. They were•Treasury bills •Money at call and short notice in the call loan market.•Commercial bills, promissory notes in the bill market.

Now, in addition to the above the following new instrument are available:

Commercial papers. Certificate of deposit. Inter-bank participation certificates. Repo instrument Banker's Acceptance Repurchase agreement/Reverse Repo Money Market mutual fund

Call / Notice Money Market: The bank with deficit fund make a call for bank

with surplus fund in a Call / Notice Money Market Benefit received in terms of call rate range

between 7.50-9.70 Call money Market- funds are transacted on

overnight basis. Notice money market- Funds are transacted for

the period between 2days to 14 days. Participants: Individuals , commercial Banks,

stock brokers financial institution and cooperative banks

Advantages of Call / Notice Money Market:1. Highly liquidity 2.Safe and cheap3. Highly profitability 4.To meet SLRDisadvantages of Call / Notice Money Market:1.Uneven Development 2.Volatality in call money rates.

Treasury bill market: Just like commercial bill which represents commercial debt, Treasury bill represents short-term borrowing of government(center and state) These were first issued in India in 1917. Meaning : It is a promissory note issued by the government under the discount for a specified period, the government promises bearer to pay the specified amount mentioned on the due date.91 days Treasury bill – 4% discount rate 182 days Treasury bill364 days Treasury bill issued on auction base (cut off rate)

There are two types of treasury bills

1.Ordinary bill

2. ‘Ad hoc’ bill

Operations and Participants: The date of Auction and the last date of submission of

tenders are notified by RBI through the press release. On the next working day of date of auction , the accepted

bids with the prices are displayed The successful bidders have to collect letter of acceptance

from the RBI and deposits the same amount along with cheque within 24 hours.

Participants: RBI and SBI, Commercial bank, state government, DFHI, financial institutions like UTI, LIC, IDBI and etc.

Advantages of T-Bills:1. Safety2. Liquidity3. Ideal short term investment4. Ideal fund management 5. CRR and SLR6. Source of short term fund7. Hedging facility.Disadvantages of T-Bills:1. Poor yield2. Absence of competitive bills3. Absence of active trading

Commercial papers:An unsecured, short-term debt instrument issued by a

corporation, typically for the financing of accounts receivable, inventories and meeting short-term liabilities. Maturities on commercial paper rarely range any longer than 270 days. The debt is usually issued at a discount, reflecting prevailing market interest rates.

Issuers: all private sector company, public sector units, NBFC’s and etc

Investors: Individuals banks ,corporates and also NRI’s

Features :1. Short term money market instruments.2. Unsecured corporate debt.3. Issued at discount.4. Issued directly by company to investors or through

merchant bankers/ Banks.Advantages:1. Simplicity2. High returns3. Flexibility4. Easy to raise long term funds.5. Movement of funds.Disadvantages:1. Unsecured corporate debt

Certificate Of Deposit – CD’sA certificate of deposit is a promissory note issued by a bank.

It is a time deposit that restricts holders from withdrawing funds on demand. Although it is still possible to withdraw the money, this action will often incur a penalty.

Issuers: Banks, FI’s and etc.Investors: Individuals , corporates , NRI’s and etc.Features: 1. Issued at discount2. Stamp duty3. Freely transferable after 45 days4. Repayable on fixed date without grace days

Repo Instrument - Repurchase Repo Rate is the interest rate at which the Reserve Bank of

India lends money to the banks to meet their short-term needs. Banks have to provide security for such loans

Banks borrow funds from RBI to bridge the gap between

loans demand and money supply.

Example: Suppose SBI Bank has a loan demand of Rs. 100, while the bank has only Rs. 80 in its system. In this scenario, SBI will borrow Rs. 20 from RBI at current Repo Rate and will bridge the gap.

Reverse Repo RateReverse Repo Rate is the rate at which the banks park their surplus money with RBI.

Example: Suppose SBI Bank has a loan demand of Rs. 80, while the bank has Rs. 100 in its system. In this scenario, SBI will park Rs. 20 in RBI at current Reverse Repo Rate.

The current Repo rate is 7.50% and Reverse Repo Rate is 6.50%.

CDs are short-term borrowings in the form of Stance Promissory Notes having a maturity of not less than 15 days up to a maximum of one year.

CD is subject to payment of Stamp Duty under Indian Stamp Act, 1899 (Central Act)

They are like bank term deposits accounts. Unlike traditional time deposits these are freely negotiable instruments and are often referred to as Negotiable Certificate of Deposits

Like most time deposit, funds can not withdrawn before maturity without paying a penalty.

CD’s have specific maturity date, interest rate and it can be issued in any denomination.

CDs are discounted instruments and are issued at a discounted price and redeemed at par value.

The main advantage of CD is their safety.

CDs can be issued by all scheduled commercial banks except RRBs – Regional Rural Banks

Minimum period 15 days Maximum period 1 year Minimum Amount Rs 1 lac and in multiples of Rs.

1 lac CDs are transferable by endorsement/approval. CD are used to maintain CRR & SLR. CDs are to be stamped

Commercial Paper (CP) is an unsecured money market instrument issued in the form of a promissory note. CP is a short term unsecured loan issued by a corporation typically financing day to day operation.

CP is very safe investment because the financial situation of a company can easily be predicted over a few months.

Only company with high credit rating issues CP’s. Who can issue Commercial Paper (CP)

Highly rated corporate borrowers, primary dealers (PDs) and satellite dealers (SDs) and all-India financial institutions (FIs)

a) The tangible net worth of the company, as per the latest audited balance sheet, is not less than Rs. 4 crore;

b) The working capital (fund-based) limit of the company from the banking system is not less than Rs.4 crore and the borrowable account of the company is classified as a Standard Asset by the financing bank/s.

CP can be issued for maturities between a minimum of 15 days and a maximum upto one year from the date of issue.

If the maturity date is a holiday, the company would be liable to make payment on the immediate preceding working day.

CP is issued to and held by individuals, banking companies, other corporate bodies registered or incorporated in India and unincorporated bodies, Non-Resident Indians (NRIs) and Foreign Institutional Investors (FIIs).

Issued to whom

RBI uses Repo and Reverse repo as instruments for liquidity adjustment in the system

It helps banks to invest surplus cash

It helps investor achieve money market returns with sovereign risk.

It helps borrower to raise funds at better rates

An SLR surplus and CRR deficit bank can use the Repo deals as a convenient way of adjusting SLR/CRR positions simultaneously.

Repo rate or repurchase rate is the rate at which banks borrow money from the central bank (read RBI for India) for short period by selling their securities (financial assets) to the central bank with an agreement to repurchase it at a future date at predetermined price.

It is similar to borrowing money from a money-lender by selling him something, and later buying it back at a pre-fixed price.

Reverse repo rate is the rate of interest at which the central bank borrows funds from other banks for a short duration. The banks deposit their short term excess funds with the central bank and earn interest on it.

Reverse Repo Rate is used by the central bank to absorb liquidity from the economy. When it feels that there is too much money floating in the market, it increases the reverse repo rate, meaning that the central bank will pay a higher rate of interest to the banks for depositing money with it.

The call money market is an integral part of the Indian Money Market, where the day-to-day surplus funds (mostly of banks) are traded. The loans are of short-term duration 1 day. The money that is lent for one day in this market is known as "Call Money", and if it exceeds one day (but less than 15 days) it is referred to as "Notice Money". The money that is lend for more than 14 days is referred to “Term Money”

Banks borrow in this market for the following purposeTo fill the gaps or temporary mismatches in funds To meet the CRR & SLR mandatory requirements as stipulated by the Central bank To meet sudden demand for funds arising out of large outflows.

(T-bills) are the most marketable money market

security. They are issued with three-month, six-month

and one-year maturities. T-bills are purchased for a price that is less than

their par(face) value; when they mature, the government pays the holder the full par value.

T-Bills are so popular among money market instruments because of affordability to the individual investors.

Consumer finance in the most basic sense of the word refers to any kind of lending to consumers.

One of the best ways to get the unsecured loans is through the consumer finance.

Television Washing Machine Air Conditioner DVD/VCD players Refrigerator Computers/laptops And other consumer durables

Seasonal Demand Demand in Rural India Consumer Awareness & Preference for new

models Attractive consumers loan schemes Growth of Media Use of Internet by Market Functionaries

Growth of GDP Opportunities in Rural Market Schemes of Banks & Financial Institutions Increasing Consumer Awareness

It’s a home loan that enables you to convert a portion of your home equity into tax-free funds without having to sell your home, give up title, or take on a new monthly payment.

Instead of making monthly mortgage payments, your mortgage pays you. That’s the “reverse” part of a reverse mortgage.

On borrower’s death or leaving the house property permanently, loan is repaid along with accumulated interest, through sale of the house property

SCB/Heirs can prepay the loan with interest. Mortgage on property can be released FM announced in 2007-08 Union Budget NHB issued Guidelines on May 31, 2007

RML seeks to monetize the house as an asset and specifically the owner’s equity in the house

Senior Citizen borrowers (SCB) mortgage the house property to a Public Lending Institution (PLI), who then makes periodic payments to borrowers during the latter’s lifetime

SCB not required to service the loan and hence no EMIs – Principal or Interest!

Scheme Senior Citizens –Old Age Dependency

Increase in Longevity and Low Mortality Rising Cost of Good Health Care No proper Social Security Systems Regular Income flow + Pensions (?) Biggest Savings / Asset / Wealth Increase in residential house prices

Senior Citizen of India – above 60 years age Married Couples as joint borrowers Should be owner of a self-acquired, self

occupied residential property (house or flat) located in India, with clear title of ownership

Property should be free from burden Residual life of property be at least 20 years Borrowers should use the property as

permanent primary residence

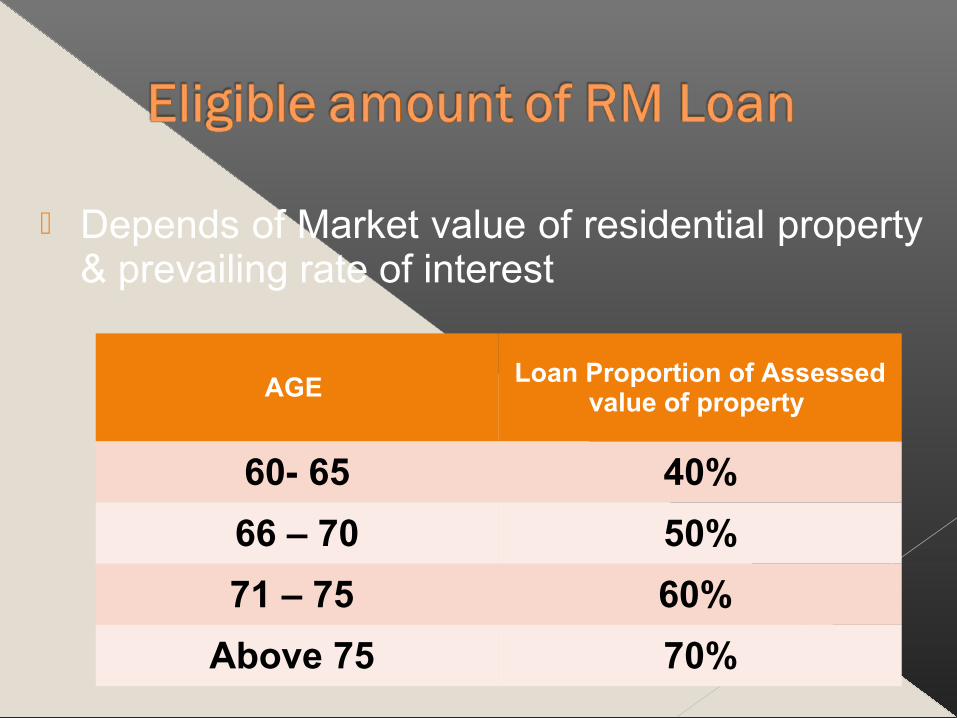

Depends of Market value of residential property & prevailing rate of interest

AGE Loan Proportion of Assessed value of property

60- 65 40%

66 – 70 50%

71 – 75 60%

Above 75 70%

Integration of unorganized sector with the organized sector

Widening of call Money market Introduction of innovative instrument Offering of Market rates of interest Promotion of bill culture Entry of Money market mutual funds Setting up of credit rating agencies Adoption of suitable monetary policy Establishment of DFHI Setting up of security trading corporation of India

ltd. (STCI)

Purchasing power of your money goes down, in case of up in inflation.

Absence of integration. Absence of Bill market. No contact with foreign Money markets. Limited instruments. Limited secondary market. Limited participants.

The money market specializes in debt securities that mature in less than one year.

Money market securities are very liquid, and are considered very safe. As a result, they offer a lower return than other securities.

The easiest way for individuals to gain access to the money market is through a money market mutual fund.

T-bills are short-term government securities that mature in one year or less from their issue date.

T-bills are considered to be one of the safest investments.

A certificate of deposit (CD) is a time deposit with a bank.

Annual percentage yield (APY) takes into account compound interest, annual percentage rate (APR) does not.

CDs are safe, but the returns aren't great, and your money is tied up for the length of the CD.

Commercial paper is an unsecured, short-term loan issued by a corporation. Returns are higher than T-bills because of the higher default risk.

Banker’s acceptance (BA) are negotiable time draft for financing transactions in goods.

Repurchase agreement (repos) are a form of overnight borrowing backed by government securities.