Monetary unions among developing and emerging markets: how many currencies does africa need?

22

Thorvaldur Gylfason 50 TH ANNIVERSARY CELEBRATION OF THE CENTRAL BANK OF NIGERIA, 4- 6 MAY 2009

description

Monetary unions among developing and emerging markets: how many currencies does africa need?. 50 TH ANNIVERSARY CELEBRATION OF THE CENTRAL BANK OF NIGERIA, 4-6 MAY 2009. Thorvaldur Gylfason. Pan-continental africa. - PowerPoint PPT Presentation

Transcript of Monetary unions among developing and emerging markets: how many currencies does africa need?

Thorvaldur Gylfason

50TH ANNIVERSARY CELEBRATION OF

THE CENTRAL BANK OF NIGERIA, 4-6

MAY 2009

Despite Africa’s great diversity of culture and languages, many Africans identify themselves as Africans first, then as Congolese, Kenyans, Nigerians, South Africans, etc.Most Europeans, North Americans, and Asians

have it the other way round: country first, then continent

Yet, national boundaries within Africa are generally less open than those within EuropeVarious restrictions on trade and migrationRestrictions need to be relaxed to spur growth National currencies constitute a trade restrictionNational currencies constitute a trade restriction

In view of the success of the EU and the euro, economic and monetary unions appeal to many Africans and others with increasing force

Consider four categoriesExisting monetary unionsDe facto monetary unionsPlanned monetary unions Previous – failed! – monetary unions

CFA franc14 African countries

CFP franc3 Pacific island states

East Caribbean dollar8 Caribbean island states

Picture of Sir W. Arthur Lewis, the great Nobel-prize winning development economist, adorns the $100 note

Euro, more recent16 EU countries plus 6 or 7 others

Thus far, clearly, a major success in view of old conflicts among European nation states, cultural variety, many different languages, etc.

Australian dollar Australia plus 3 Pacific island states

Indian rupee India plus Bhutan (plus Nepal)

New Zealand dollar New Zealand plus 4 Pacific island states

South African rand South Africa plus Lesotho, Namibia, Swaziland –

and now Zimbabwe Swiss franc

Switzerland plus Liechtenstein US dollar

US plus Ecuador, El Salvador, Panama, and 6 others

East African shilling (2009) Burundi, Kenya, Rwanda, Tanzania, and

Uganda Eco (2009)

Gambia, Ghana, Guinea, Nigeria, and Sierra Leone (plus, perhaps, Liberia)

Khaleeji (2010) Bahrain, Kuwait, Qatar, Saudi-Arabia, and

United Arab Emirates Other, more distant plans

Caribbean, Southern Africa, South Asia, South America, Eastern and Southern Africa, Africa

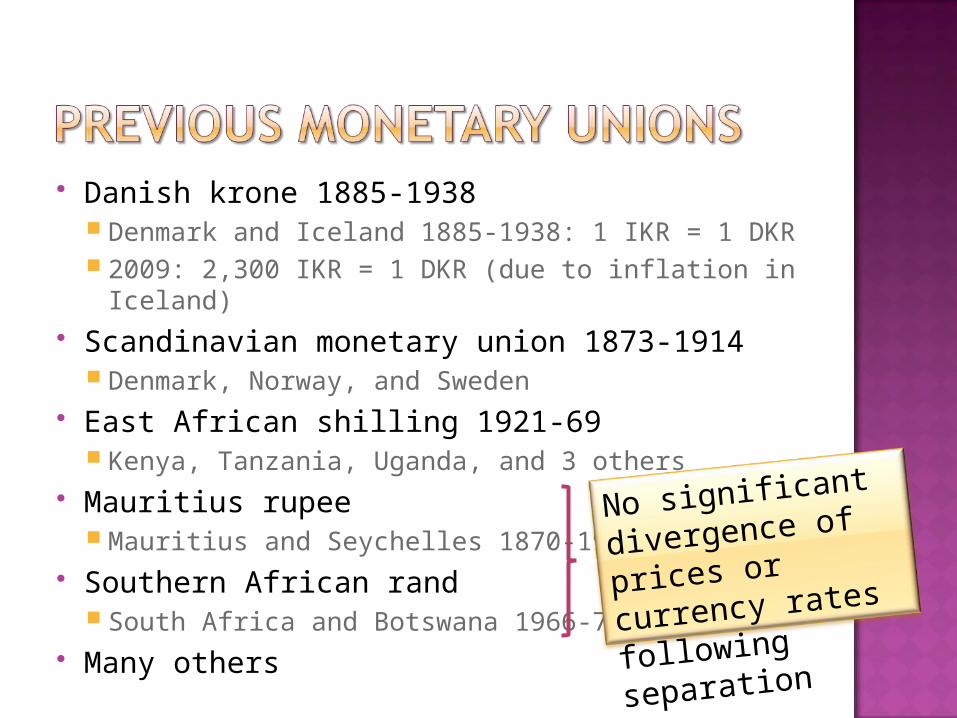

Danish krone 1885-1938 Denmark and Iceland 1885-1938: 1 IKR = 1 DKR 2009: 2,300 IKR = 1 DKR (due to inflation in

Iceland) Scandinavian monetary union 1873-1914

Denmark, Norway, and Sweden East African shilling 1921-69

Kenya, Tanzania, Uganda, and 3 others Mauritius rupee

Mauritius and Seychelles 1870-1914 Southern African rand

South Africa and Botswana 1966-76 Many others

No significant

divergence of

prices or currency

rates following

separation

CentripetalCentripetal tendency to joinjoin monetary unions, thus reducing number of currencies To benefit from stable exchange rates stable exchange rates at the

expense of monetary independence CentrifugalCentrifugal tendency to leaveleave monetary

unions, thus increasing number of currenciesTo benefit from monetary independence monetary independence often,

but not always, at the expense of exchange rate stability

With globalization, centripetal tendencies appear stronger than centrifugal onesWhat does this mean for Africa?

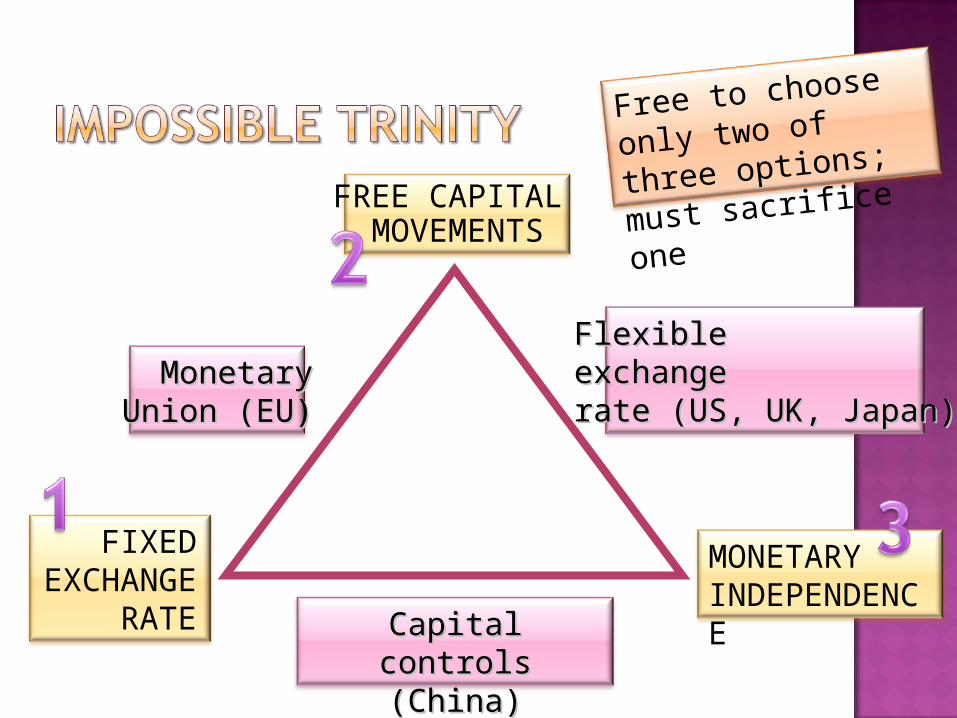

FREE CAPITAL MOVEMENTS

FIXEDEXCHANGE

RATE

MONETARYINDEPENDENCE

MonetaryMonetaryUnion (EU)Union (EU)

Flexible Flexible exchange exchange rate (US, UK, Japan)rate (US, UK, Japan)

Capital controls Capital controls (China)(China)

Free to choose

only two of three

options; must

sacrifice one

If capital controls are ruled out in view of the proven benefits of free trade free trade in goods, services, labor, and also capital (four freedomsfour freedoms), …

… then long-run choice boils down to one between monetary independencemonetary independence (i.e., flexible exchange rates) vs. fixed ratesflexible exchange rates) vs. fixed rates Cannot have both!Cannot have both!

Either type of regime has advantages as well as disadvantages

Let’s quickly review main benefits and costs

BenefitsBenefits CostsCosts

Fixed Fixed exchange exchange ratesrates

Floating Floating exchange exchange ratesrates

BenefitsBenefits CostsCosts

Fixed Fixed exchange exchange ratesrates

Stability of Stability of trade and trade and investmentinvestment

Low inflationLow inflation

Floating Floating exchange exchange ratesrates

BenefitsBenefits CostsCosts

Fixed Fixed exchange exchange ratesrates

Stability of Stability of trade and trade and investmentinvestment

Low inflationLow inflation

InefficiencyInefficiency

BOP deficitsBOP deficits

Sacrifice of Sacrifice of monetary monetary independenceindependence

Floating Floating exchange exchange ratesrates

BenefitsBenefits CostsCosts

Fixed Fixed exchange exchange ratesrates

Stability of Stability of trade and trade and investmentinvestment

Low inflationLow inflation

InefficiencyInefficiency

BOP deficitsBOP deficits

Sacrifice of Sacrifice of monetary monetary independenceindependence

Floating Floating exchange exchange ratesrates

EfficiencyEfficiency

BOP BOP equilibriumequilibrium

BenefitsBenefits CostsCosts

Fixed Fixed exchange exchange ratesrates

Stability of Stability of trade and trade and investmentinvestment

Low inflationLow inflation

InefficiencyInefficiency

BOP deficitsBOP deficits

Sacrifice of Sacrifice of monetary monetary independenceindependence

Floating Floating exchange exchange ratesrates

EfficiencyEfficiency

BOP BOP equilibriumequilibrium

Instability of Instability of trade and trade and investmentinvestment

InflationInflation

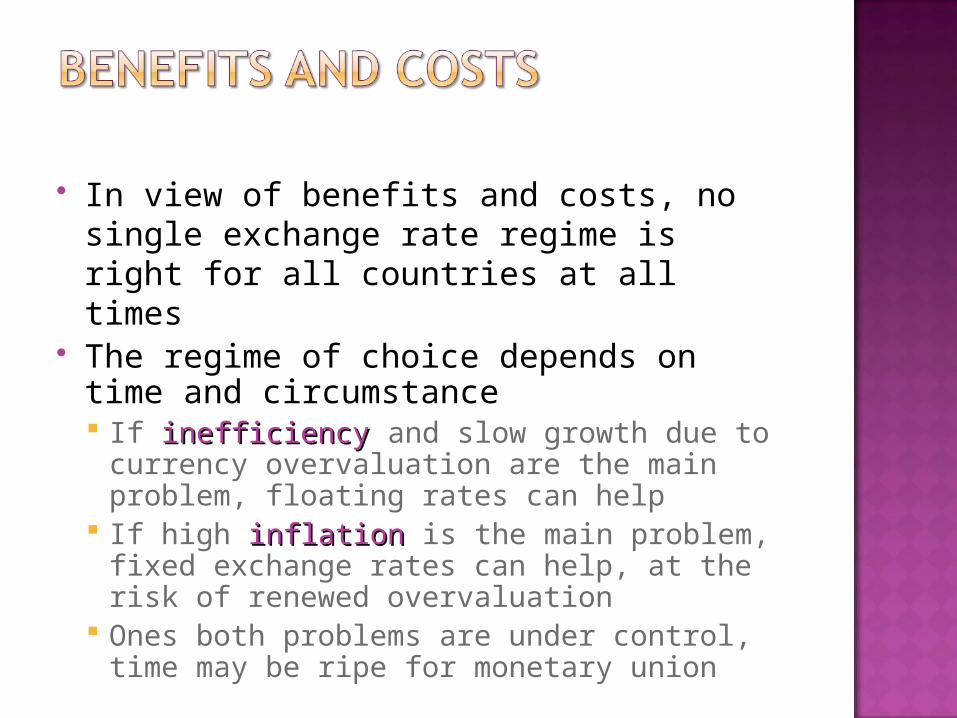

In view of benefits and costs, no single exchange rate regime is right for all countries at all times

The regime of choice depends on time and circumstance If inefficiencyinefficiency and slow growth due to

currency overvaluation are the main problem, floating rates can help

If high inflationinflation is the main problem, fixed exchange rates can help, at the risk of renewed overvaluation

Ones both problems are under control, time may be ripe for monetary union

The real exchange rate always floats Through nominal exchange rate adjustment

or price changes Even so, it does make a difference how

countries set their nominal exchange rates because floating takes time

Currency misalignments can persist Hence, a wide spectrum of options,

from absolutely fixed rates anchored through monetary unions to completely flexible exchange rates

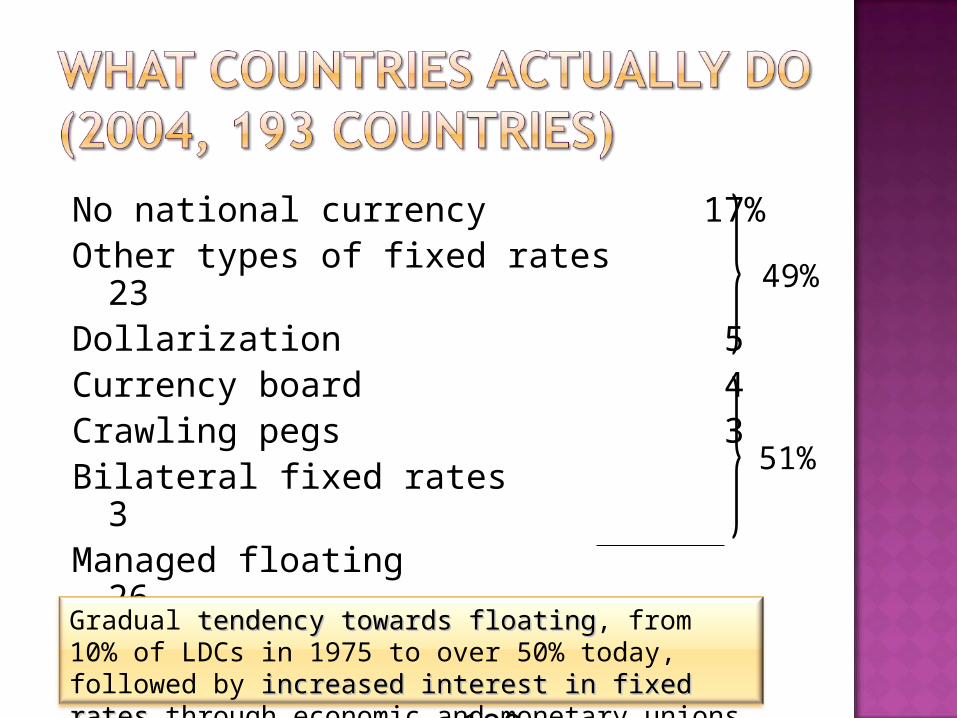

What do countries do?

No national currency 17%Other types of fixed rates 23Dollarization 5Currency board 4Crawling pegs 3Bilateral fixed rates 3Managed floating 26Pure floating 19 100

51%

49%

Gradual tendency towards floatingtendency towards floating, from 10% of LDCs in 1975 to over 50% today, followed by increased interest in fixed ratesincreased interest in fixed rates through economic and monetary unions

Governments sometimes prefer fixed exchange rates so they can try to keep their national currencies overvalued To keep foreign exchange cheap To retain power to ration scarce foreign

exchange To make GNP in dollars look larger than it is

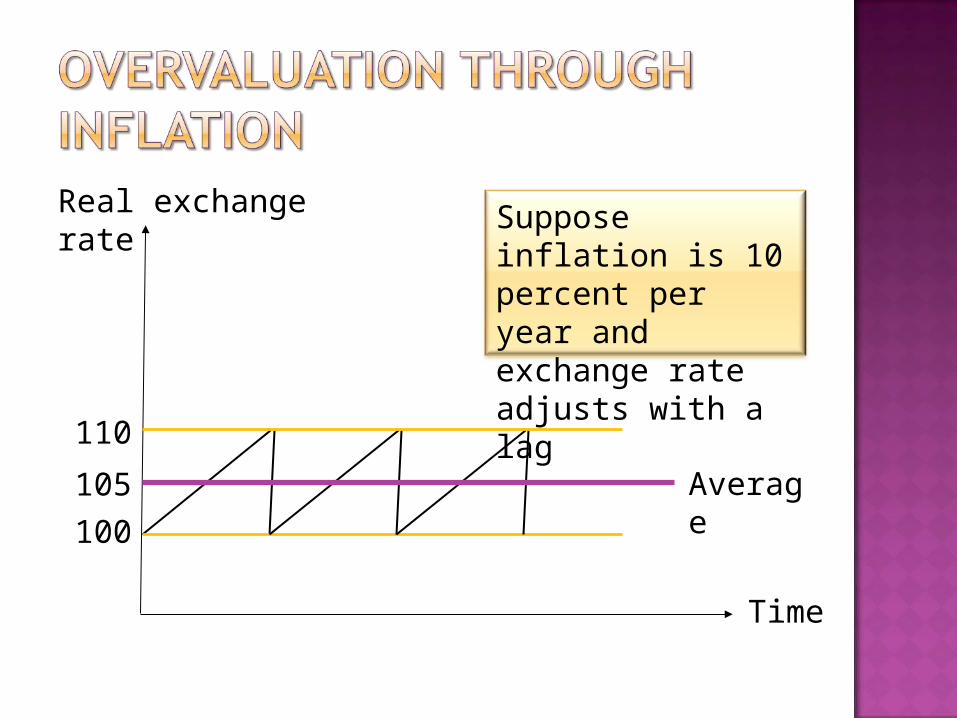

Another reason for persistent overvaluation, and thereby also sluggish trade and slow growth Inflation! Show by simple numerical example

Time

Real exchange rate

100

110105

Average

Suppose inflation is 10 percent per year and exchange rate adjusts with a lag

Time

100

120

Real exchange rate

110 Average

So, increased

inflation

increases real

exchange rate

as long as as long as

nominal nominal

exchange rate exchange rate

adjusts with a adjusts with a

laglag

Suppose inflation rises to 20 percent per year

Many African countries’ history of inflation, overvaluation, and slow growth is stark reminder that one of the keys to successful entry into monetary union is making sure that initial exchange rate at point of entry is not too highnot too high

European countries on euro zone’s doorstep – Baltic countries, Sweden, Iceland – face same challenge

Thank youThese slides can be viewed on my

website:

www.hi.is/~gylfason