Monetary Systems and Macro Policy - American UniversityMonetary Systems and Macro Policy Slides for...

67

Macroeconomic Policy Monetary Systems and Macro Policy Slides for KOMIF Ch08 (KOMIE Ch19) Alan G. Isaac American University 2017-11-30 Alan G. Isaac Monetary Systems and Macro Policy

Transcript of Monetary Systems and Macro Policy - American UniversityMonetary Systems and Macro Policy Slides for...

Macroeconomic Policy

Monetary Systems and Macro PolicySlides for KOMIF Ch08 (KOMIE Ch19)

Alan G. Isaac

American University

2017-11-30

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Preview

Goals of macroeconomic policies

Persistent current account deficitsMonetary standards

Gold standardInternational monetary system during 1918-1939Bretton Woods system: 1944-1973Collapse of the Bretton Woods system

International effects of U.S. macroeconomic policies

Problems of macro policy coordination

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Macroeconomic Goals

Internal Balancefull employment (Yf)price stability or low inflation

External Balancecurrent account in "normal" rangebalance of payments “equilibrium”

official international reserves staticcurrent account (plus capital account) matches the non-reservefinancial account

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

The European Stability Mechanism (ESM)

Institutional support to fight internal imbalances.

established September 2012

role: safeguard and provide instant access to financial assistanceprogrammes eurozone states in financial difficulty

a maximum lending capacity: EUR 500 billion.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

European Monetary Fund

In 2017, the European Commission (EC) proposed to turn the ESMinto European Monetary Fund (EMF) by 2019.

role: act as a lender of last resort in banking crises.

role: bailouts? (Germany=no, France=yes)

independent (like ESM) or subordinate to EC?

aid may be conditional

goals appear to be more sovereignty (vs IMF) and more ECpower

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

European Minister of Economy and Finance?

put one person in charge of policing respect for eurozone budgetrules, and forging deals between governments on everything fromeconomic reforms to crisis bailouts.

would combine the existing posts of EU economy commissionerand eurogroup president

set an overall fiscal stance for the euro area

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Deviations from Internal Balance

unemploymentresource wasteother social costs (crime, health)

overemploymentunsustainableputs pressure on prices

high inflationreduces value of price signalscomplicates planning by households and businesses

unanticipated Inflationredistributes income

from creditors to debtorsfrom worker to employers

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Costs of Recession

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Suicide and the Great Recession

sharp increase in middle-aged suicides around 2007http://www.sciencedirect.com/science/article/pii/S074937971400662X

middle-aged suicide reasons often: job, financial, and legalproblems

Great Recession is associated with at least 10000 additionaleconomic suicides between 2008 and 2010.http://connection.ebscohost.com/c/articles/98001212/economic-suicides-great-recession-europe-north-america

austerity measures imposed in Greece in 2011 "marked thebeginning of significant, abrupt and sustained increases in totalsuicide." http://bmjopen.bmj.com/content/5/1/e005619.short?g=w_open_current_tab

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Benefits of Nonzero Current Accounts

gains to intertemporal trade:

a current account deficit country may be cushioning a temporarynegative shock

a current account surplus country may be finding more productiveuses abroad for its savings

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Deviations from External Balance

large CA surplusmay induce protectionist sentiment abroad

large CA deficitmay induce protectionist sentiment at homecreates questions of solvency if sustained

creditors cease lendingfinancial crisis

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

IIP and Total National Income (Y)

Part of national income is measured in the BoP accounts as “primaryincome” (net factor income from abroad). Let r be the rate of return onthe net international investment position (IIP).

Y = GDP+ r · IIP

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Absorption Approach to Current Account

Recall the absorption approach to the current account.

CA = Y −A

Substituting our previous expression for Y , and recalling thatA = C + I +G, we get:

CA = GDP+ r · IIP− (C + I +G)

Recalling that NX = GDP− (C + I +G), this becomes:

CA = NX+ r · IIP

This is just our decomposition of the current account into twocomponents: the “balance or trade” and “net factor payments”.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Intertemporal Budget Constraint

Ignoring capital gains and losses for the moment:

IIPt+1 = IIPt +CAt

= IIPt +NXt + r · IIPt

IIPt+1 = (1+ r)IIPt +NXt

Recall CA = NX+ r · IIP.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Adjacent Periods

We have found a relationship between any two adjacent periods:

IIPt+1 = (1+ r)IIPt +NXt

For example:IIP1 = (1+ r)IIP0 +NX0

This last equation implies:

IIP0 =1

1+ r

(IIP1 −NX0

)

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Adjacent Periods (Continued)

So we have

IIP0 =IIP1 −NX0

1+ r

Similarly,

IIP1 =IIP2 −NX1

1+ r

Together these imply

IIP0 =−NX0

1+ r− NX1

(1+ r)2 +IIP2

(1+ r)2

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Implication of the Intertemporal Budget Constraint

Suppose all debts are eventually repaid. Then we must have

IIP0 =−∞

∑t=0

1(1+ r)t+1 NXt

This means that a country starting with positive IIP can run deficits intothe future, but that a country starting with negative IIP must runsurpluses in the future.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Deflating by GDP

We can rewrite this as a proportion of GDP. Define:

iip = IIP/GDP

nx = NX/GDP

(1+g) = GDPt+1/GDPt

Then we can write:

iip0 =−∞

∑t=0

(1+g)t

(1+ r)t+1 nxt

=− 11+g

∞

∑t=0

(1+g1+ r

)t+1

nxt

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Representing the Infinite Sum

Is there a “sustainable” BoP deficit? Suppose we run n̄x forever. Then

iip0 =− 11+g

∞

∑t=0

(1+g1+ r

)t+1

n̄x

Assume r > g > 0, so that this summation makes sense and

11+g

∞

∑t=0

(1+g1+ r

)t+1

=1

1+ r

∞

∑t=0

(1+g1+ r

)t

=1

1+ r

(1

1− 1+g1+r

)

=1

1+ r

(1

r−g1+r

)=

1r −g

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Sustaintable Balance of Trade

Under the assumption that r > g, we have found that:

iip0 =−n̄xr −g

Solving this for the sustainable balance of trade we get:

n̄x = (r −g)iip0

So a country with a positive iip0 can in principle run a negativebalance of trade forever. (Just negative enough that does notcontinually run up iip.)

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Implied Current Account

In period 0, the corresponding current account (as a fraction of GDP) is

ca0 = n̄x+ r · iip0

= (r −g)iip0 + r · iip0

= g · iip0

Thus if an indebted country is growing, it can continuously run a smallcurent account deficit, paying back just enough to keep iip constant.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Example: New Zealand

From 1992-2012, NZ has had:

(CA/GDP)<0 every year

(IIP/GDP) around -0.7

nominal GDP growth around 0.05

Assuming r=0.06, we have

m̄x =−(r −g)iip0

=−(0.06−0.05)(−0.7)

= 0.007

This 0.7% of GDP is in fact the average ratio of NZ’s exports to GDPover the same period.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Gold Standard, Revisited

The gold standard from 1870–1914 and after 1918 hadmechanisms that prevented flows of gold reserves (the balance ofpayments) from becoming too positive or too negative.

Prices tended to adjust according the amount of gold circulating inan economy, which had effects on the flows of goods andservices: the current account.Central banks influenced financial asset flows, so that thenon-reserve part of the financial account matched the currentaccount in order to reduce gold outflows or inflows.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Price-Specie-Flow Mechanism

CA > 0-> gold earned from exports flows into the country-> domestic prices rise; foreign prices fall-> domestic goods become relatively costly-> _CA and ^CA*

inflow of specietends to inflate prices� demand shifts toward foreign goods

outflow of specietends to deflate prices� demand shifts toward home goods

domestic price level rises or falls in response to gold (“specie”)inflows or outflows

relative price changes cause an adjustment in the flow of goods

More carefully: gold flows in when CA surplus exceeds thenon-reserve financial account

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Policy under the Price Specie Flow Mechanism

central banks actively influence financial capital flowsconstrained gold flows, especially outflowstried to match the non-reserve part of the financial account to thecurrent account

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Gold Standard, Revisited (cont.)

Price specie flow mechanismis the adjustment of prices as gold(“specie”) flows into or out of a country, causing an adjustment inthe flow of goods.

An inflow of gold tends to inflate prices.An outflow of gold tends to deflate prices.If a domestic country has a current account surplus in excess ofthe non-reserve financial account, gold earned from exports flowsinto the country—raising prices in that country and lowering pricesin foreign countries.Goods from the domestic country become expensive and goodsfrom foreign countries become cheap, reducing the currentaccount surplus of the domestic country and the deficits of theforeign countries.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Gold Standard, Revisited (cont.)

Thus, price specie flow mechanism of the gold standard couldautomatically reduce current account surpluses and deficits,achieving a measure of external balance for all countries.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Gold Standard, Revisited (cont.)

The “Rules of the Game” under the gold standard refer to anotheradjustment process that was theoretically carried out by centralbanks:

The selling of domestic assets to acquire money when gold exitedthe country as payments for imports. This decreased the moneysupply and increased interest rates, attracting financial inflows tomatch a current account deficit.

This reversed or reduced gold outflows.The buying of domestic assets when gold enters the country asincome from exports. This increased the money supply anddecreased interest rates, reducing financial inflows to match thecurrent account.

This revered or reduced gold inflows.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Gold Standard, Revisited (cont.)

Banks with decreasing gold reserves had a strong incentive topractice the rules of the game: they could not redeem currencywithout sufficient gold.

Banks with increasing gold reserves had a weak incentive topractice the rules of the game: gold did not earn interest, butdomestic assets did.

In practice, central banks with increasing gold reserves seldomfollowed the rules.

And central banks often sterilized gold flows, trying to prevent anyeffect on money supplies and prices.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Gold Standard, Revisited (cont.)

The gold standard’s record for internal balance was mixed.The U.S. suffered from deflation, recessions and financialinstability during the 1870s, 1880s, and 1890s while trying toadhere to a gold standard.The U.S. unemployment rate 6.8% on average from 1890–1913,but it was less than 5.7% on average from 1946–1992.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Interwar Years: 1918–1939

The gold standard was stopped in 1914 due to war, but after 1918was attempted again.

The U.S. reinstated the gold standard from 1919–1933 at $20.67per ounce and from 1934–1944 at $35.00 ounce, (a devaluationthe dollar).The UK reinstated the gold standard from 1925–1931.

But countries that adhered to the gold standard for the longesttime, without devaluing their currencies, suffered most fromreduced output and employment during the 1930s.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Bretton Woods System: 1944–1973

In July 1944, 44 countries met in Bretton Woods, NH, to design theBretton Woods system:

a fixed exchange rates against the U.S. dollar and a fixed dollar price ofgold ($35 per ounce).

They also established other institutions:

The International Monetary Fund

The World Bank

General Agreement on Trade and Tariffs (GATT), the predecessorto the World Trade Organization (WTO).

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

International Monetary Fund

The IMF was constructed to lend to countries with persistentbalance of payments deficits (or current account deficits), and toapprove of devaluations.

Loans were made from a fund paid for by members in gold andcurrencies.Each country had a quota, which determined its contribution to thefund and the maximum amount it could borrow.Large loans were made conditional on the supervision of domesticpolicies by the IMF: IMF conditionality.Devaluations could occur if the IMF determined that the economywas experiencing a “fundamental disequilibrium”.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

International Monetary Fund (cont.)

Due to borrowing and occasional devaluations, the IMF wasbelieved to give countries enough flexibility to attain an externalbalance, yet allow them to maintain an internal balance andstable exchange rates.

The volatility of exchange rates during 1918–1939, caused bydevaluations and the vagaries of the gold standard, was viewed asa source of economic instability.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Bretton Woods System: 1944–1973

In order to avoid sudden changes in the financial account(possibly causing a balance of payments crisis), countries in theBretton Woods system often prevented flows of financial assetsacross countries.Yet, they encouraged flows of goods and services because of theview that trade benefits all economies.

Currencies were gradually made convertible (exchangeable)between member countries to encourage trade in goods andservices valued in different currencies.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Bretton Woods System: 1944–1973 (cont.)

Under a system of fixed exchange rates, all countries but the U.S.had ineffective monetary policies for internal balance.

The principal tool for internal balance was fiscal policy(government purchases or taxes).

The principal tools for external balance were borrowing from theIMF, restrictions on financial asset flows and infrequent changesin exchange rates.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Automatic Adustment: The Costs

When money is coined precious metalPrices tended to adjust according the amount of coin circulating inan economy

prices in turn affect international flows of goods and services (CA)Coinage Act of 1873

demonetized silver"Crime of 1873"Deflation despite increased gold supplies from 1849 CaliforniaGold Rush

demand grew faster than supply

1875-1896 saw CPI fall about 1% per year

1894 recession: U reached 18%Gold discoveries ended the deflation

big discoveries in South Africa and Alaska

Gold Standard Act of 1900

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Internal Balance: The II Curve

Suppose internal balance in the short run occurs when D=Yf

Yf = C(Y f −T )+ I +G+CA(EP ∗/P,Y f −T )

Consider a fiscal expansion starting at Y=Yf:

^G (or _Tx) � ^D � (Y>Yf)_E could restore internal balance in the short runthe II curve slopes down in (G,E)-space

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Internal Balance: The II Curve

E

G

II

E1

G1

Y > Yf

Y < Yf

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

External Balance: The XX Curve

Suppose external balance in the short run occurs when CA = X(e.g., CA=0)

CA(EP ∗/P,Y −T ) = X

Consider a fiscal expansion starting at CA=X:

^G (or _Tx) � ^D � ^Y � _CA^E could restore external balance in the short runthe XX curve slopes up in (G,E)-space

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

External Balance: The XX Curve

E

G

XX

E1

G1

CA > 0

CA < 0

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Four Zones of “Economic Discomfort”

E

G

XX

II

E1

G1

CA > 0

CA > 0

CA < 0

CA < 0Y > Yf

Y > Yf

Y < Yf

Y < Yf

Compare KOMIF Fig 8-2 (KOMIE 11 Fig 19-2)

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Macroeconomic Goals (cont.)

But under the fixed exchange rates of the Bretton Woods system,devaluations were supposed to be infrequent, and fiscal policywas supposed to be the main policy tool to achieve both internaland external balance.

But in general, fiscal policy can not attain both internal balanceand external balance at the same time.

A devaluation, however, can attain both internal balance andexternal balance at the same time.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

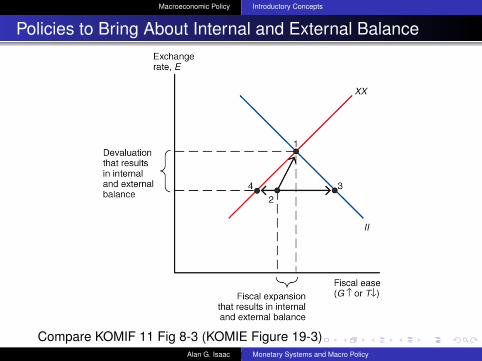

Policies to Bring About Internal and External Balance

Compare KOMIF 11 Fig 8-3 (KOMIE Figure 19-3)At point 2, the economy is below IIand XX: it experiences low outputand a low current account

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Policy constraints of the Bretton Woods system

fiscal policywas supposed to be the main policy tool

for both internal and external balance!but what about a situation of unemployment and CA deficit?!

may not be able to attain both internal balance and externalbalance

devaluationswere supposed to be infrequentcan reduce U and improve CA simultaneously

but what about a situation of overemployment and CA deficit?!

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Tinbergen’s Rule

Consistent, determinate policy systems require an equal numberof targets and instrumentsreflects a mathematical fact

for a (linear, independent) equation system to have a uniquesolution.

need an equal number of variables and equations

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Macroeconomic Goals (cont.)

Under the Bretton Woods system, policy makers generally usedfiscal policy to try to achieve internal balance for political reasons.Thus, an inability to adjust exchange rates left countries facingexternal imbalances over time.

Infrequent devaluations or revaluations helped restore externaland internal balance, but speculators also tried to anticipate them,which could cause greater internal or external imbalances.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

External and Internal Balances of the U.S.

The collapse of the Bretton Woods system was caused primarilyby imbalances of the U.S. during the 1960s and 1970s.

The U.S. current account surplus became a deficit in 1971.Rapidly increasing government purchases increased aggregatedemand and output, as well as prices.Rising prices and a growing money supply caused the U.S. dollarto become overvalued in terms of gold and in terms of foreigncurrencies.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

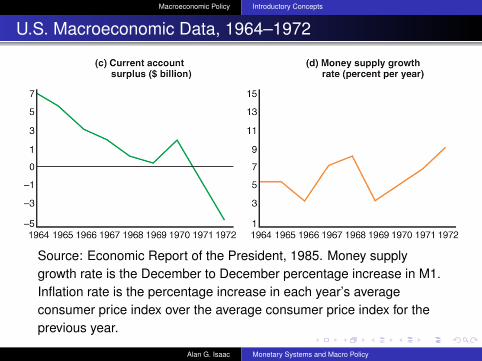

U.S. Macroeconomic Data, 1964–1972

Source: Economic Report of the President, 1985. Money supplygrowth rate is the December to December percentage increase in M1.Inflation rate is the percentage increase in each year’s averageconsumer price index over the average consumer price index for theprevious year.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

U.S. Macroeconomic Data, 1964–1972

Source: Economic Report of the President, 1985. Money supplygrowth rate is the December to December percentage increase in M1.Inflation rate is the percentage increase in each year’s averageconsumer price index over the average consumer price index for theprevious year.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Problems of a Fixed Exchange Rate, Revisited

Another problem was that as foreign economies grew, their needfor official international reserves grew to maintain fixed exchangerates.But this rate of growth was faster than the growth rate of the goldreserves that central banks held.

Supply of gold from new discoveries was growing slowly.Holding dollar denominated assets was the alternative.

At some point, dollar denominated assets held by foreign centralbanks would be greater than the amount of gold held by theFederal Reserve.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Problems of a Fixed Exchange Rate, Revisited (cont.)

The Federal Reserve would eventually not have enough gold:foreigners would lose confidencein the ability of the FederalReserve to maintain the fixed price of gold at $35/ounce, andtherefore would rush to redeem their dollar assets before the goldran out.

This problem is similar to what any central bank may face when ittries to maintain a fixed exchange rate.If markets perceive that the central bank does not have enoughofficial international reserve assets to maintain a fixed rate, abalance of payments crisis is inevitable.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Triffin’s Dilemma

1960 Robert Triffin testifies before US CongressUS stops BoP deficit

-> international community loses largest source of additions toreserves-> resulting shortage of liquidity

-> could pull the world economy into contraction

-> undermine systemUS deficits continue

number of dollars will eventually exceed US gold stock

erode confidence in the value of the U.S. dollar

-> dollar no longer be accepted as the world’s reserve currency

-> undermine system

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Bretton Woods collapse

Collapse of the Bretton Woods systemoften blamed on US imbalances in 1960s and 1970s.

US current account went int deficit in 1971.increased aggregate demand and output, rising inflation

Rapidly increasing government purchases due to Vietnam WarUS dollar became over-valued in terms of gold and in terms offoreign currencies.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Collapse of the Bretton Woods System

The U.S. was not willing to reduce government purchases orincrease taxes significantly, nor reduce money supply growth.These policies would have reduced aggregate demand, outputand inflation, and increased unemployment.

The U.S. could have attained some semblance of external balanceat a cost of a slower economy.

A devaluation, however, could have avoided the costs of lowoutput and high unemployment and still have attained externalbalance (an increased current account and official internationalreserves).

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Collapse of the Bretton Woods System (cont.)

The imbalances of the U.S., in turn, caused speculation about thevalue of the U.S. dollar, which caused imbalances for othercountries and made the system of fixed exchange rates harder tomaintain.

Financial markets had the perception that the U.S. economy wasexperiencing a “fundamental disequilibrium” and that adevaluation would be necessary.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Collapse of the Bretton Woods System (cont.)

First, speculation about a devaluation of the dollar causedinvestors to buy large quantities of gold.

The Federal Reserve sold large quantities of gold in March 1968,but closed markets afterwards.Thereafter, individuals and private institutions were no longerallowed to redeem gold from the Federal Reserve or other centralbanks.The Federal Reserve would sell only to other central banks at$35/ounce.But even this arrangement did not hold: the U.S. devalued itsdollar in terms of gold in December 1971 to $38/ounce.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Collapse of the Bretton Woods System (cont.)

Second, speculation about a devaluation of the dollar in terms ofother currencies caused investors to buy large quantities offoreign currency assets.

A coordinated devaluation of the dollar against foreign currenciesof about 8% occurred in December 1971.Speculation about another devaluation occurred: Europeancentral banks sold huge quantities of European currencies in earlyFebruary 1973, but closed markets afterwards.Central banks in Japan and Europe stopped selling theircurrencies and stopped purchasing of dollars in March 1973, andallowed demand and supply of currencies to push the value of thedollar downward.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

International Effects of U.S. Macroeconomic Policies

Recall from chapter 17, that the monetary policy of the countrywhich owns the reserve currency is able to influence othereconomies in a reserve currency system.

In fact, the acceleration of inflation that occurred in the U.S. in thelate 1960s also occurred internationally during that period.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

International Effects of U.S. Macroeconomic Policies (cont.)

Source: Organization for Economic Cooperation and Development.Figures are annual percentage increases in consumer price indexes.Inflation rates in European economies relative to that in the US.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Effect on Internal and External Balance of a Rise in theForeign Price Level, P*

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Inflation Rates in European Countries, 1966–1972 (percentper year)

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

International Effects of U.S. Macroeconomic Policies (cont.)

Evidence shows that money supply growth rates in othercountries even exceeded the rate in the U.S.This could be due to the effect of speculation in the foreignexchange markets.

Central banks were forced to buy large quantities of dollars tomaintain fixed exchange rates, which increased their moneysupplies at a more rapid rate than occurred in the U.S.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Table 18-2: Changes in Germany’s Money Supply andInternational Reserves, 1968–1972 (percent per year)

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Summary

1 Internal balance means that an economy enjoys normal outputand employment and price stability.

2 External balance roughly means a stable level of officialinternational reserves or a current account that is not too positiveor too negative.

3 The gold standard had two mechanisms that helped to preventexternal imbalances

Price specie flow mechanism: the automatic adjustment of prices asgold flows into or out of a country.Rules of the game: buying or selling of domestic assets by centralbanks to influence flows of financial assets.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Summary (cont.)

4 The Bretton Woods agreement in 1944 established fixedexchange rates, using the U.S. dollar as the reserve currency.

5 The IMF was also established to provide countries with financingfor balance of payments deficits and to judge if changes in fixedrates were necessary.

6 Under the Bretton Woods system, fiscal policies were used toachieve internal and external balance, but they could not do bothsimultaneously, so external imbalances often resulted.

Alan G. Isaac Monetary Systems and Macro Policy

Macroeconomic Policy Introductory Concepts

Summary (cont.)

7 Internal and external imbalances of the U.S.—caused by rapidgrowth in government purchases and the money supply—andspeculation about the value of the U.S. dollar in terms of gold andother currencies ultimately broke the Bretton Woods system.

8 High inflation from U.S. macroeconomic policies was transferredto other countries late in the Bretton Woods system.

Alan G. Isaac Monetary Systems and Macro Policy