Mobile payments landscape in Zimbawe | Beyond 2015

17

Evolys Digital is changing the way we do business in Zimbabwe for the better. Already their clients are benefiting fro m their wealth of knowledge in deploying mobility solutions for businesses big and small. Whether its mobile aggregation services USSD, Bulk SMS and mobile marketing, or mobile apps (android, iOS, Blackberry) Evolys Digital is the best company in Zimbabwe to deploy such services at the least possible cost to your business. They add value to business in Zimbabwe. Evolys Business. doing business better Mobile Payments in Zimbabwe : Consumer perspectives & Growth opportunities

-

Upload

evolys-digital -

Category

Mobile

-

view

162 -

download

1

Transcript of Mobile payments landscape in Zimbawe | Beyond 2015

Evolys Digital is changing the way we do business in Zimbabwe for the better. Already their clients are benefiting fro m their wealth of knowledge in deploying mobility solutions for businesses big and small. Whether its mobile aggregation services USSD, Bulk SMS and mobile marketing, or mobile apps (android, iOS, Blackberry) Evolys Digital is the best company in Zimbabwe to deploy such services at the least possible cost to your business. They add value to business in Zimbabwe. Evolys Business. doing business better

Mobile Payments in Zimbabwe :

Consumer perspectives & Growth opportunities

This document allows you to see the potential and opportunities that exist in the mobile payments space in Zim-babwe, and its effect on emerging businesses and existing ones. It illus-trates how the biggest influencer in technology and mobile payments are changing and shaping the mobility eco-

system in Zimbabwe and beyond.

doing business better

Why You Should Read This Document

Evolys Digital is changing the way we do business in Zimbabwe for the better. Already their clients are benefiting fro m their wealth of knowledge in deploying mobility solutions for businesses big and small. Whether its mobile aggregation services USSD, Bulk SMS and mobile marketing, or mobile apps (android, iOS, Blackberry) Evolys Digital is the best company in Zimbabwe to deploy such services at the least possible cost to your business. They add value to business in Zimbabwe. Evolys Business. doing business better

ContentsIntroduc�on....................................................4

Mobile Money Transfers................................5

Mobile Money Gaining Momentum...............6

At a Glance.....................................................7

Zimbabwe by 2020........................................8

M- Co�erce.................................................9

Remi�ance Poten�al in Zimbabwe................10

Where to go next?.......................................14

Open Money.................................................15

Evolys digital is changing the way people send, spend and receive money in Zimbabwe. It is the next generation in digital technology with services such as Evolys Digital, Evolys Business and Evolys Payments (Swypeup Register) are changing businesses all over Zimbabwe. Now we can safely say goodbye to Ecocash, Telecash and The ATM

Introduction

Money has been a central part of society for as long as we've had societies. It has connected cities, countries, cultures and people

Until now, money has been about dollars and rands, yens and euros, a physical method of exchange. But thanks to mobile tech-nology the way we send, spend and receive money is changing fast, mobile payments are gaining momentum and the benefits are clear, the potential too.

Yet today more than three quarters of all payments in Zimbabwe are still made in cash.

Services such as Ecocash (Econet), OneWallet (NetOne), Telecash (Telecel), Nettcash and Swypeup have received popular appeal from the public as they control over 60% of the mobile wallets active sub-scribers.

Already, there are over 5 million users of m-payments in Zimbabwe and the possibilities are endless.

The Evolys Business

Maurine MunyaviHead of Business Developments

Creating anOpen Money SocietyBringing finance and telecom together to empower people and businesses everywhere.

4

doing business better

5

active

doing business better

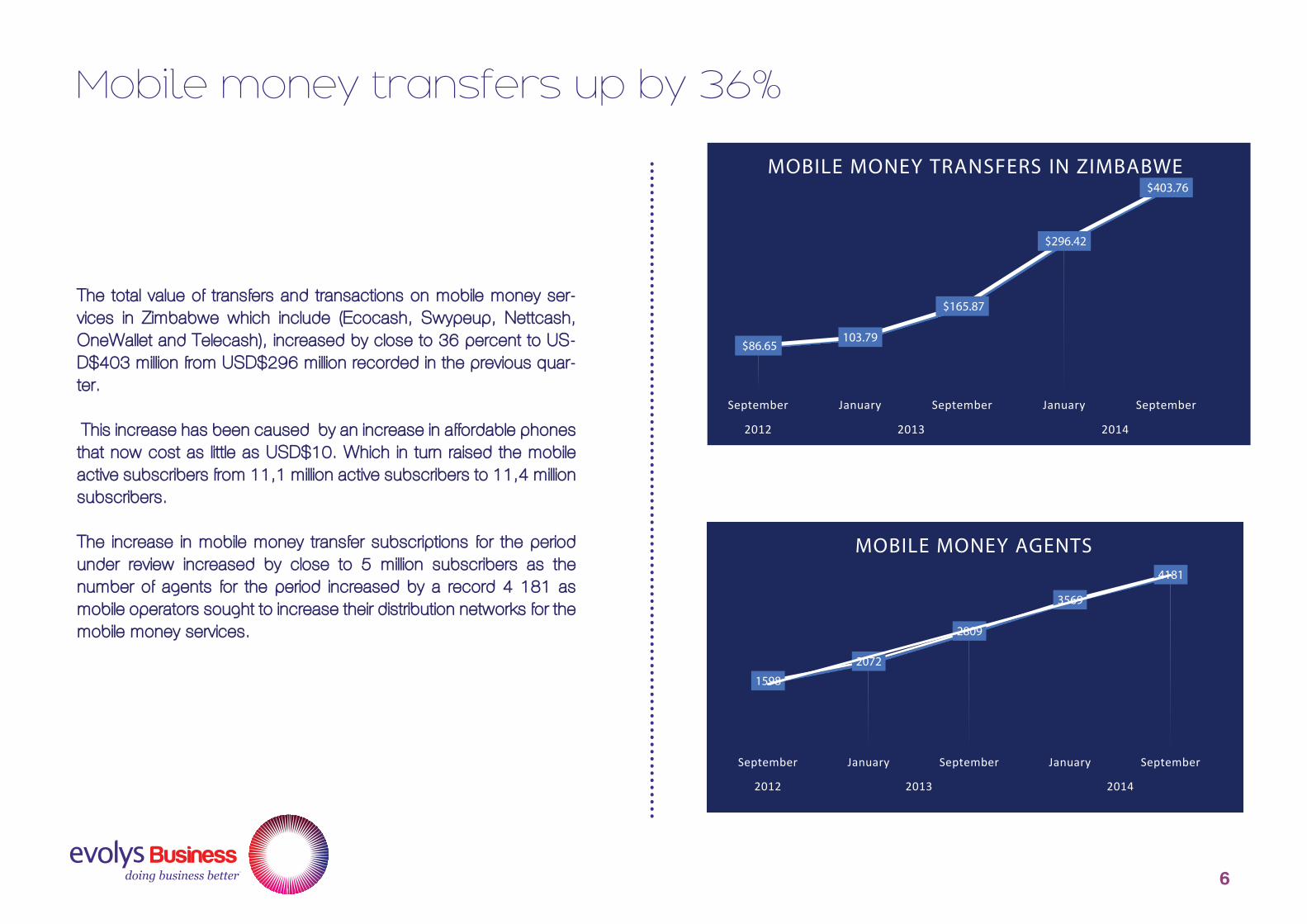

The total value of transfers and transactions on mobile money ser-vices in Zimbabwe which include (Ecocash, Swypeup, Nettcash, OneWallet and Telecash), increased by close to 36 percent to US-D$403 million from USD$296 million recorded in the previous quar-ter.

This increase has been caused by an increase in affordable phones that now cost as little as USD$10. Which in turn raised the mobile active subscribers from 11,1 million active subscribers to 11,4 million subscribers.

The increase in mobile money transfer subscriptions for the period under review increased by close to 5 million subscribers as the number of agents for the period increased by a record 4 181 as mobile operators sought to increase their distribution networks for the mobile money services.

6

Mobile money transfers up by 36%

$86.65 103.79

$165.87

$296.42

$403.76

September January September January September

2012 2013 2014

MOBILE MONEY TRANSFERS IN ZIMBABWE

1598

2072

2809

3569

4181

September January September January September

2012 2013 2014

MOBILE MONEY AGENTS

doing business betterMobile Moneyis gaining momentum

* GSMA MMU Mobile Money Tracker 25th March 2014** Source: GSMA MMU State of the Industry Report 2013

228*

4,9M**Registered Accounts

~6M*Active users by

June 2016 –day period

225*Live deployments

in emerging markets August

2015

3**Deployments have

more than 1M active mobile money users

14Of deployments

are by Banks

4,9M

11,4Mmobile phone users in

the Zimbabwe

mobile money accounts

7,8Mpeople lack bank

accounts in Zimbabwe

50Mreal-time transactions

handled per day

ZimbabweBy 2020…

17 MSmartphone

Subscriptions

30 MMobile Subscriptions

X 20Mobile Data

Traffic growth

16 MMobile

Broadband Subscriptions Source: Evolys Digital Mobility Report, 2014

doing business better

-03-25 | Page 2

-

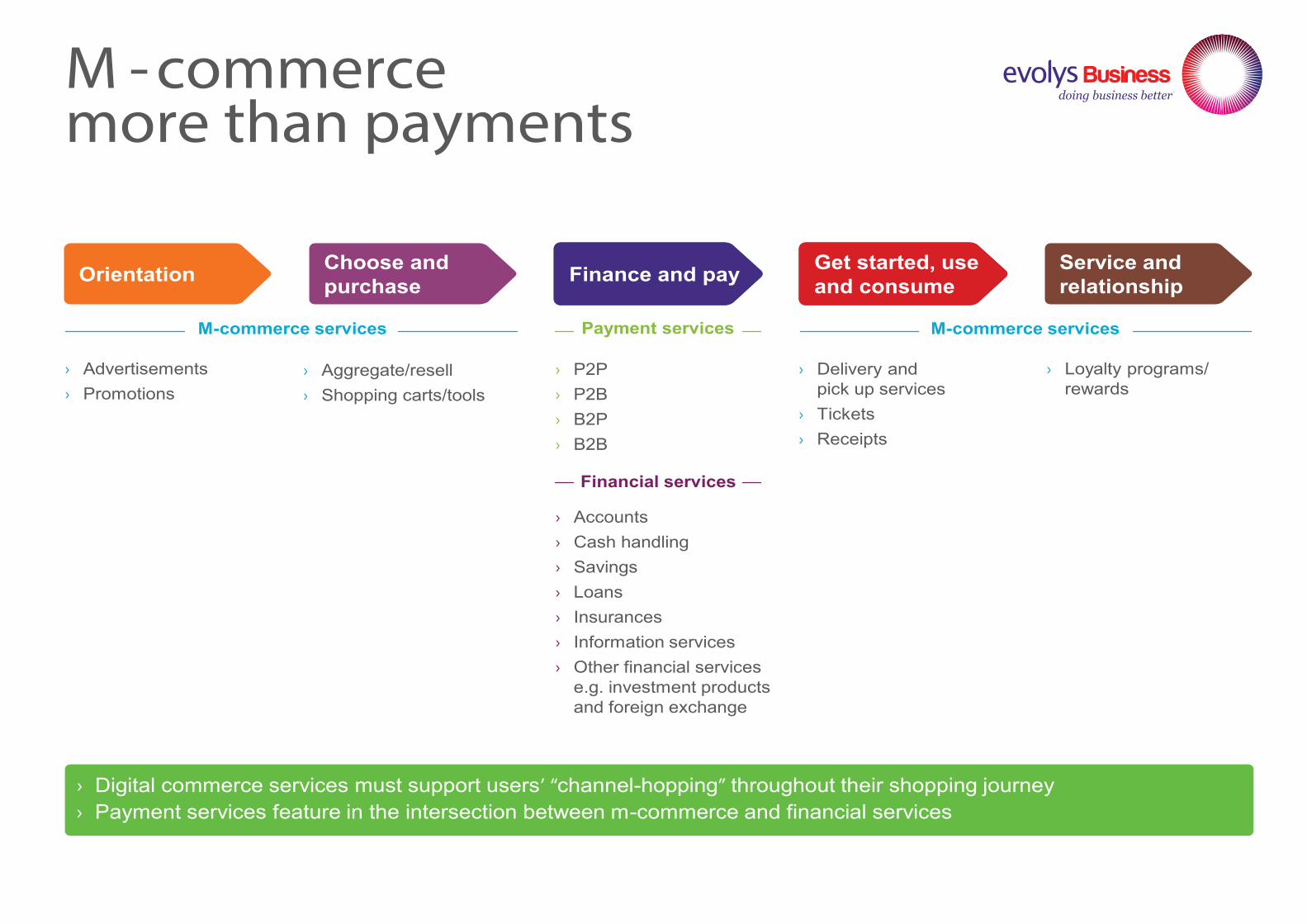

M - commerce more than payments

Orientation

M-commerce services

Financial services

Payment services

Choose and purchase Finance and pay Get started, use

and consumeService and relationship

› Advertisements› Promotions

› Aggregate/resell› Shopping carts/tools

› P2P› P2B› B2P› B2B

› Accounts› Cash handling› Savings› Loans› Insurances› Information services› Other financial services

e.g. investment products and foreign exchange

› Digital commerce services must support users’ “channel-hopping” throughout their shopping journey› Payment services feature in the intersection between m-commerce and financial services

› Delivery and pick up services

› Tickets› Receipts

› Loyalty programs/rewards

M-commerce services

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 7

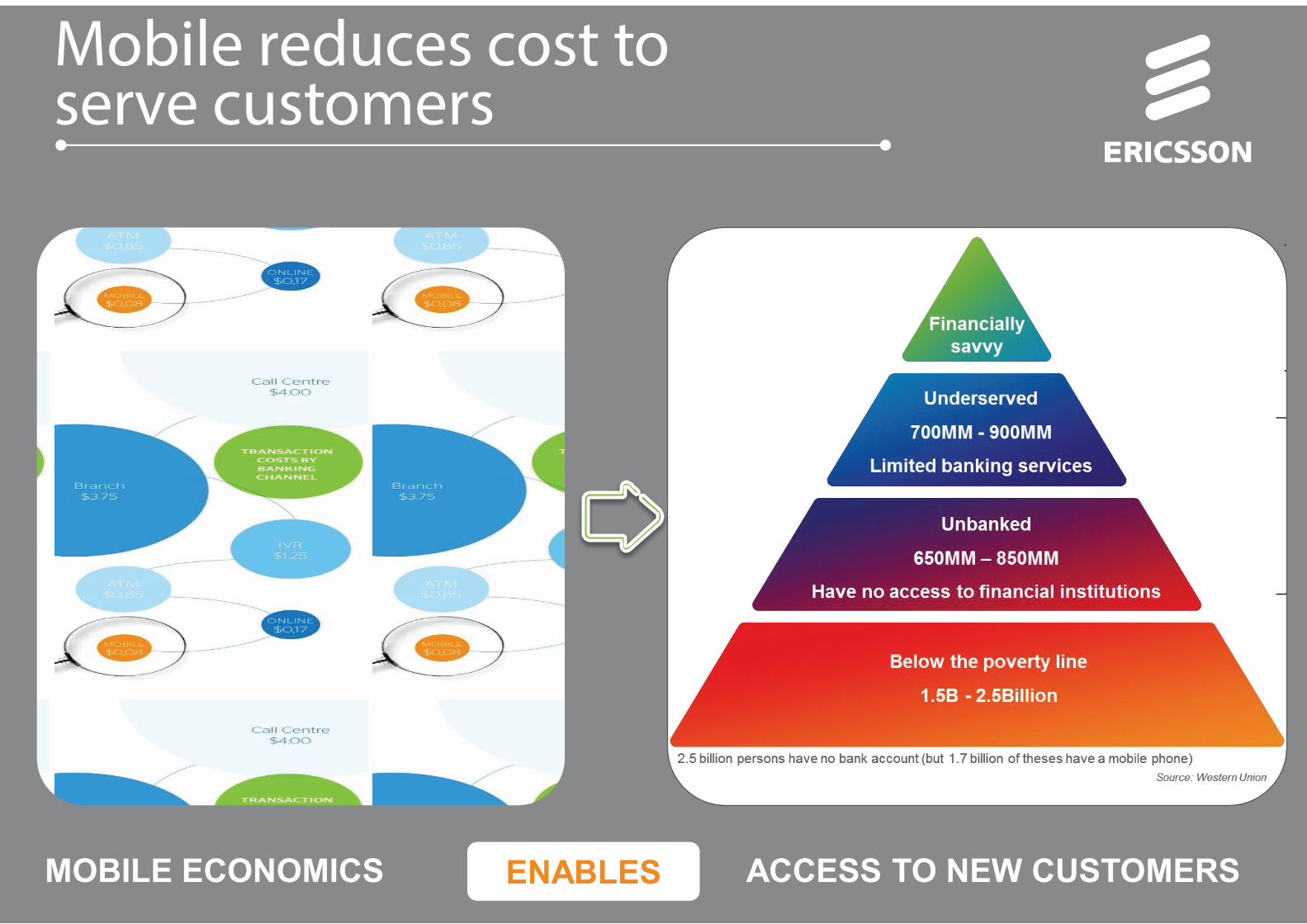

Mobile reduces cost to serve customers

MOBILE ECONOMICS ACCESS TO NEW CUSTOMERSENABLES

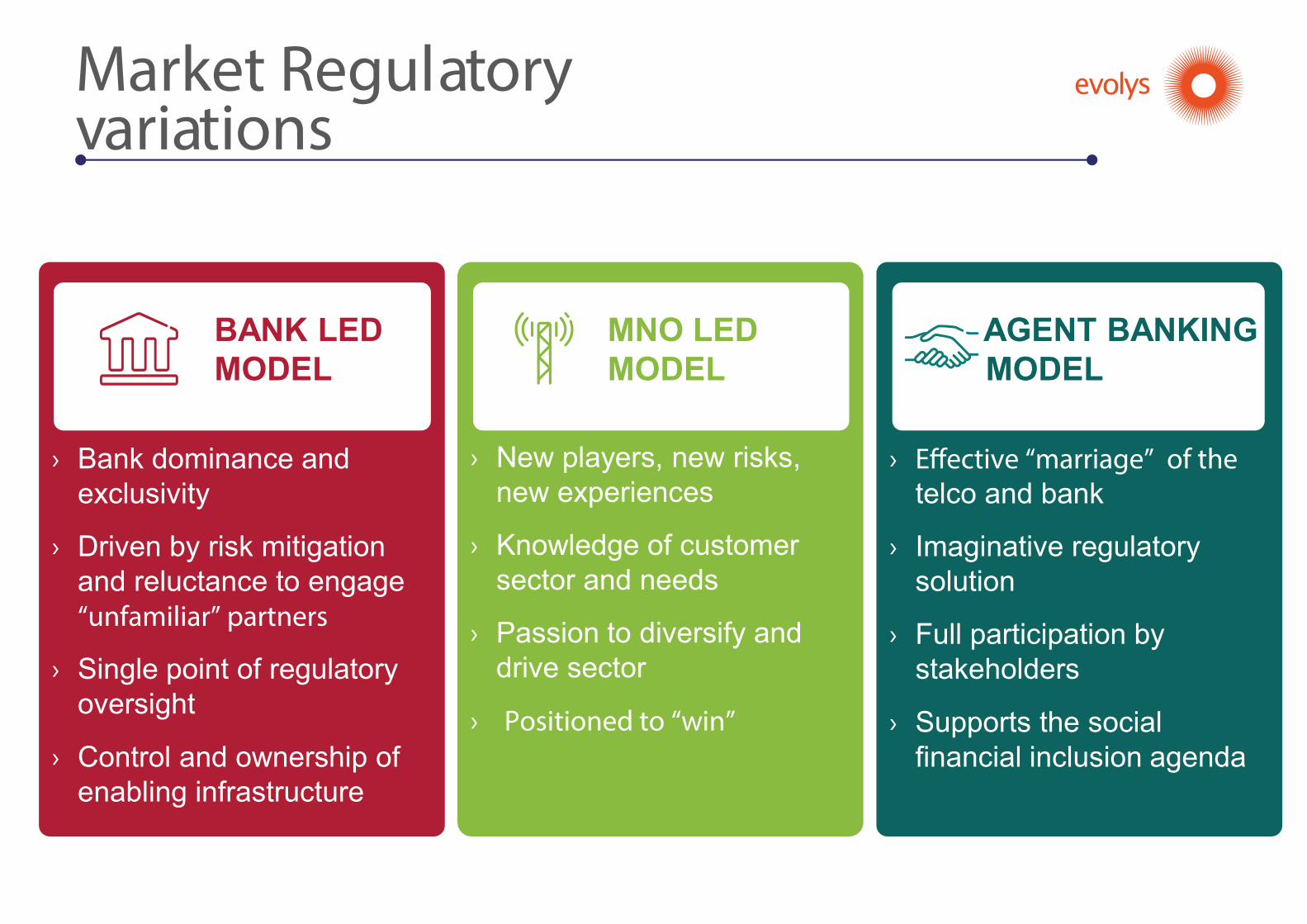

Market Regulatory variations

WALLET PLATFOR

M› Bank dominance and

exclusivity

› Driven by risk mitigation and reluctance to engage “unfamiliar” partners

› Single point of regulatory oversight

› Control and ownership of enabling infrastructure

WALLET PLATFOR

M› E�ective “marriage” of the

telco and bank

› Imaginative regulatory solution

› Full participation by stakeholders

› Supports the social financial inclusion agenda

WALLET PLATFOR

M› New players, new risks,

new experiences

› Knowledge of customer sector and needs

› Passion to diversify and drive sector

› Positioned to “win”

BANK LEDMODEL

MNO LEDMODEL

AGENT BANKINGMODEL

Mobile Payments and NFC | Ericsson Internal | 2014-03-25 | Page 8

Remittance opportunity

› Inflows coming into Zimbabwe

› Pan-Africa estimated to be large

› Price levels vary

$91M

Source: Evolys Business Consulting

5-25%

Slide title 44

Text and bullet level minimum 24

Bullets level 2minimum 20

Characters for Embedded font: !"#$%&'()*+, -./0123456789 :;<=>?@ABCDEFGHIJKLMNOPQRSTUVWXYZ[ \]^_`abcdefghijklmnopqrstuvwxyz{|}~¡¢£¤¥¦ §¨©ª«¬®¯ °±²³ ´¶·¸ ¹º»¼½ÀÁÂÃÄÅÆÇÈËÌÍÎÏÐÑÒÓÔÕÖ×ØÙÚÛÜÝÞßàáâãäåæçèéêëìíîïðñòóôõöøùúûüýþÿĀāĂăąĆćĊċČĎďĐđĒĖėĘęĚěĞğĠġĢģĪīĮįİıĶķĹĺĻļĽľŁłŃńŅņŇňŌŐőŒœŔŕŖŗŘřŚśŞşŠšŢţŤťŪūŮůŰűŲųŴŵŶŷŸŹźŻżŽžƒȘșˆˇ˘˙˚˛˜˝ẀẁẃẄẅỲỳ –—‘’‚“”„†‡•…‰‹›⁄€ ™ĀĀĂĂĄĄĆĆĊĊČČĎĎĐĐĒĒĖĖĘĘĚĚĞĞĠĠĢĢĪĪĮĮİĶĶĹĹĻĻĽĽŃŃŅŅŇŇŌŌŐŐŔŔŖŖŘŘŚŚŞŞŢŢŤŤŪŪŮŮŰŰŲŲŴŴŶŶŹŹŻŻȘș−≤≥fifl

ΆΈΉΊΌΎΏΐΑΒΓΕΖΗΘΙΚΛΜΝΞΟΠΡΣΤΥΦΧΨΪΫΆΈΉΊΰαβγδεζηθικλνξορςΣΤΥΦΧΨΩΪΫΌΎΏ

ЁЂЃЄЅІЇЈЉЊЋЌЎЏАБВГДЕЖЗИЙКЛМНОПРСТУФХЦЧШЩЪЫЬЭЮЯАБВГДЕЖЗИЙКЛМНОПРСТУФХЦЧШЩЪЫЬЭЮЯЁЂЃЄЅІЇЈЉЊЋЌЎЏ������ҐҐәẁẂẃẄẅỲỳ№

Do not add objects or text in the footer area

Where do we go next?

Transfer Store Grow

Capture daily retail spend

Bring local context

Inter- operability

It’s time for Money to Change When money is open, the way we send, spend, and receive money will change forever.

All rights reserved

Evolys Business Solu�onsemail: [email protected]: www.evolysbusiness.comtwi�er: www.twi�er.com/evolysdigitalfaceb�k: www.faceb�k.com/evolysdigital