mkljq - Oil & Gas UKoilandgasuk.co.uk/wp-content/uploads/2015/07/EY-Review-of-the-UK... · regions...

92

Review of the UK oilfield services industry January 2016

Transcript of mkljq - Oil & Gas UKoilandgasuk.co.uk/wp-content/uploads/2015/07/EY-Review-of-the-UK... · regions...

Review of the UK oilfield services industryJanuary 2016

29

45

41

35

17

23

Contents

Review of the UK oilfield services industry January 2016

01 Introduction 1

02 Overview 5

The UK oilfield services sector by supply chain category

03 Reservoirs 17

04 Wells 23

05 Facilities 29

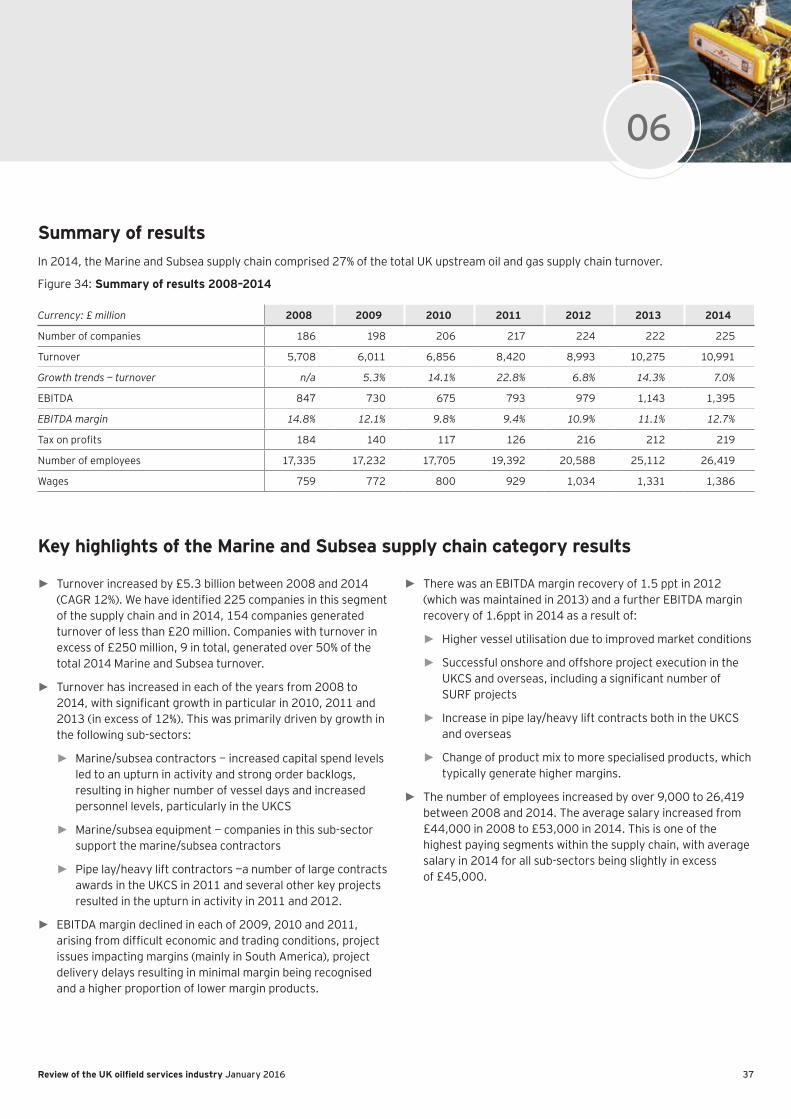

06 Marine and Subsea 35

07 Support and Services 41

08 Comparison with the Norwegian oilfield services sector 45

09 Methodology and key assumptions 50

A

Appendix A: Reservoirs supply chain segment sub-sectors 52

B Appendix B: Wells supply chain segment sub-sectors 56

C Appendix C: Facilities supply chain segment sub-sectors 62

D Appendix D: Marine and Subsea supply chain segment sub-sectors 70

E Appendix E: Support and Services supply chain segment sub-sectors 76

32 subsectors

>1500 companies

Wells

Support and Services M

arine and Subsea

FacilitiesReservoirs

Review of the UK oilfield services industry January 2016

Welcome to EY’s fifth annual review of the UK oilfield services (OFS) industry. In this report, we review the 2014 trading performance of UK registered companies in this hugely diverse oilfield services marketplace and discuss the impact the oil price decline has had, and is expected to have, on their performance in both the UK and global markets.

UK upstream oil and gas supply chain2014 2015 and 2016 trends

Generating £41bn turnover

3% turnover growth from 2013 to 2014

EBITDA margin flat at 10%

38% of 2014 turnover is generated from export activity

Balance sheet restructuring

Consolidation

Cost reductions

Improving liquidity

Internatonalisation

Production efficiencies

Standardisation

Technological solutions and innovation

Introduction 01

1Review of the UK oilfield services industry January 2016

UK OFS: Fit for the future?

The current oil and gas market is one of the most challenging ever. The oil price has fallen from a high of around US$115/bbl in 2014 to below US$30/bbl for the first time in over a decade with exploration and production (E&P) companies having significantly reduced capital expenditure budgets in response. Alongside any rise in the oil price, price volatility will also need to reduce before the sector can make informed investment decisions and gain confidence that any price recovery is sustainable. In the meantime, UK OFS companies need to take action to survive in this new market. Although there was 3% turnover growth in 2014, the slowest growth rate for five years, turnover is expected to decline significantly in both 2015 and 2016, putting pressure on cash flows and capital structures.

The oil price decline has resulted in many projects being delayed or cancelled; margin pressure on both capital projects and operation and maintenance contracts; and a lack of visibility over future orders, creating stress across the UK upstream supply chain. The companies most severely affected to date have been those with asset heavy businesses and those exposed to capital projects (e.g., seismic, drilling and vessel owners). A number of companies have been partially protected in 2014 and 2015 as they have been focused on either more robust production activities (as opposed to capital projects) or working through pre-existing backlog. However, there are major uncertainties around replenishment of backlog and general activity levels in 2016.

As around 40% of the turnover generated by UK OFS companies is from overseas markets, those companies with specialist products and services that can be exported

Barry Fraser

Executive Director Transaction Advisory Services

are seeing lower UK demand being partly compensated by activity in international markets. Although overall exports were flat in 2014, certain markets such as the Middle East have been less impacted, while others such as North America have been harder hit.

The UK OFS sector is responding to the low oil price environment by making itself more resilient through implementing cost reductions; driving efficiencies in project delivery; changing how it engages with customers and targeting sectors out with upstream oil and gas. Although the actions taken to date have made many companies stronger, further action is required. Companies are also focused on working capital, cash management and are examining capital structures. Stakeholders need to take a medium rather than short term view on market recovery in order to support these businesses.

Consolidation is inevitable and many of the best value-generating deals have been done during previous downturns. This is a great opportunity to add both technological solutions and geographical presence as well as delivering a step change in cost reduction through effective integration and economies of scale. Companies need to act now to avoid being left behind.

It is a challenging period for the oil and gas market, however there are world leading capabilities within the UK supply chain providing hope for the future. Companies that proactively look for opportunities to improve their resilience, engage with their stakeholders and make targeted, strategic acquisitions could find themselves emerging from the current downturn leaner, stronger and well placed to capitalise on the recovery.

2 Review of the UK oilfield services industry January 2016

Introduction continued

3Review of the UK oilfield services industry January 2016

01

Viewpoint: Oil and Gas Authority

When the Oil and Gas Authority was in its earliest stages of formation, few predicted the scale and duration of the current downturn. Our focus is to maximise economic recovery (MER) from the basin, and whilst we don’t regulate the service sector, we are one of its strong supporters. A successful supply chain is essential to MER UK and to the continued significant value of the OFS industry domestically and internationally. The service sector can also play a vital role in helping identify and deliver sustainable, cost-effective and efficient solutions for the longer term.

The prospect of prolonged tough market conditions and the resultant impact on the sector is a cause for concern. Strong leadership and collaboration, in the spirit of the Wood Review, are vital to effect rejuvenation of the basin. We’ve been working very closely with industry (operators and the service sector) and governments with good collaboration in industry boards, such as the Supply Chain and Exports Board. By working together we will see a transformation in the way operators and contractors interact, fostering greater trust and co-operation. Despite this downturn, I hope the industry will rally and fully recognise the value and importance of the OFS sector to the basin’s future.

Andy Samuel Chief Executive Oil and Gas Authority

Viewpoint: Oil & Gas UK

This report highlights the importance of the UK’s oilfield services sector to our economy, in applying its world-leading expertise serving the North Sea and through its growing export business.

Whilst the UK offshore oil and gas sector is adapting rapidly to the low oil price, driving greater efficiencies throughout its operations, it is imperative the supply chain — as the heart of the industry — continues to be promoted and be nurtured through this cycle and beyond.

While times are undoubtedly tough, we are confident that the industry can survive this downturn. In 2015, we welcomed the first rise in oil and gas production for over 15 years, and, with 20 billion barrels of oil and gas estimated to potentially still be available in UK waters and global demand for the products and services developed at the cutting edge of the North Sea showing no sign of waning, there is still plenty to play for.

That is why coherent action is being taken to make companies stronger and more efficient. Oil & Gas UK’s industry-lead Efficiency Task Force will lead the drive for greater co-operation across the sector with the objective of transforming the UK continental Shelf into the most efficient basin in the world, supported by a yet stronger and growing oilfield services sector.

Michael Tholen Economics and Commercial Director Oil & Gas UK

4 Review of the UK oilfield services industry January 2016

5Review of the UK oilfield services industry January 2016

OverviewGlobal

► The oil price decline, which started in the second half of 2014, has continued in 2015, with prices averaging around US$50/bbl. The oil market is still being affected by concerns over reduced growth in Chinese demand and the expectations regarding the timing and magnitude of additional Iranian supply. If, as expected, there is a return of Iranian oil in the first half of 2016, this will add to the pressure on prices.

► At the OPEC meeting in December 2015, there was no action taken to either cut production or raise the production ceiling in anticipation of Iranian supply. OPEC is to revisit this at the next meeting in June 2016 (unless an emergency meeting is held before then), by which time there will likely be more clarity on the timing of Iran export resumption and the scale of additional potential volumes entering the market. As such, it is likely there will be at least another six months of the market determining prices.

► The oil production of major producers is currently strong and the high level of global crude stocks will act as a substantial barrier to any sustained increase in prices over the next 12 months. Although there are four civil wars or major conflicts underway across the Middle East and North Africa regions (Iraq, Yemen, Syria and Libya), these are unlikely to pose a major threat to oil supplies as global crude stocks should act as a buffer to any temporary supply disruptions.

► The decline in the oil price has led to a number of actions by operators including maximising revenue from existing operations, reducing operating costs where possible (e.g., headcount reductions) and deferring capital expenditure on new projects, especially those that are not close to completion.

► Although operational cost savings and asset sales should assist company finances whilst oil prices are weaker, lower capital expenditure will impact production in future years. The lack of available cash flow is likely to limit capital spending for a number of operators in 2016, even if there were to be a gradual improvement in oil price. In the majority of cases, the large cuts in upstream oil and gas capital expenditure in 2015 have not yet fed through to supply. However, when this does happen, it will play a major role in rebalancing the market.

► Even with the decline in the oil price, the long-term global demand for oil and gas remains. The International Energy Agency1 anticipates global energy demand to increase by 14% from 2014 to 2040. The impact of the large cuts in capital expenditure will influence the ability to meet annual production replacement needs in future years if the trend is not reversed in the near term.

02

1 World Energy Outlook, 2015

6 Review of the UK oilfield services industry January 2016

Overview continued

Figure 1: Top 100 listed OFS companies actual and forecast results 2011–16

Currency: US$ billion 2011 2012 2013 2014 2015E 2016E

Turnover 424 479 500 507 413 391

Turnover growth/(decline) trends n/a 12.9% 4.5% 1.3% (18.6%) (5.3%)

EBITDA 80 87 88 95 70 66

EBITDA margin 18.8% 18.3% 17.6% 18.8% 17.1% 16.8%

► For the top 100 listed OFS companies, we analysed the reported results from 2011 to 2014 and the forecast results (based on analyst’s expectations) for 2015 and 2016 and these are shown in Figure 1. As can be seen, turnover is forecast to decline by over 18% in 2015 and a further 5% in 2016, with EBITDA margins also being impacted. Given the rate reductions, project deferrals and cancellations, the EBITDA margin decline may be even more pronounced in 2015 and 2016.

► These trends support our view that the market outlook for OFS companies for the coming year looks increasingly challenging. E&P companies will continue to target service costs and try to renegotiate contracts, resulting in a further reduction in activity levels and additional margin erosion.

► Consolidation and strategic alliances were inevitable given market conditions as companies seek to offer innovative lower cost solutions to customers or to reduce their cost base by streamlining supply chains, lowering operating costs and implementing manufacturing processes improvements. Following on from the acquisition of Baker Hughes by Halliburton, which was announced in November 2014 (Australian and EU antitrust regulators decisions still to be announced, US antitrust regulators to assess further proposals provided by the companies as remedies offered to date are not sufficient to address its concerns — the time period for closing has been extended to no later than 30 April 2016 as a result of this), there have been a number of significant announcements during 2015 including:

► In March 2015, FMC Technologies and Technip signed an agreement to form an exclusive alliance and to launch a 50/50 joint venture to unite their skills and capabilities. The alliance aims to redefine the way subsea fields are designed, delivered and maintained to significantly reduce the cost of subsea field development and provide the technology to maximise well performance over the life of the field.

► In August 2015, Schlumberger and Cameron jointly announced they had entered into a definitive merger agreement. The merger is expected to bring significant cost synergies and is expected to close in the first quarter of 2016.

Viewpoint: Global market

The oil market remains oversupplied and indications are that this situation will continue for some time, with prices likely to be lower for longer. Together with the improving costs position of unconventionals, this is putting huge pressure on the owners of assets in higher cost basins to cut costs and improve performance to protect returns. The initial response of the industry was to cut or defer projects and force price reductions on to its supply chain. Whilst these are going to remain core responses, operators are now looking to standardise processes to further reduce costs. Given the relatively fragmented nature of the supply chain, we believe further consolidations are essential if OFS companies are to deliver both the costs savings required by customers and sustainable returns for their investors.

Within the overall market for OFS, the pressure will be highest on those assets which are inherently more expensive such as some deepwater and LNG projects. However, in every market the key to success will be the proven ability to deliver efficiencies and support the operators performance agenda in an extremely challenging environment.

Andy Brogan Global Oil & Gas Transaction Leader Transaction Advisory Services

7Review of the UK oilfield services industry January 2016

02

UK ► The United Kingdom Continental Shelf (UKCS) has a 50 year

pedigree in extracting oil and gas making it one of the most experienced regions in the world. It is a proven hydrocarbon basin and is well supported by an established offshore service industry. Aberdeen is recognised as a centre of excellence in the UK OFS supply chain, with world leading capability in areas such as subsea technology and services and many large global players have headquarters or regional head offices there. During 2014, despite a decline in the oil price, the UK OFS industry still achieved turnover growth of 3% from 2013, whilst maintaining EBITDA margins.

► The UK government published a new Energy Bill on 10 July 2015, which saw the establishment of the new Oil and Gas Authority (OGA) and the implementation of other recommendations from Sir Ian Wood’s strategic review of the UK North Sea published in 2014. The OGA has been given regulatory powers that aims to drive greater collaboration and productivity within the oil and gas industry, as well as attracting investment and creating jobs.

UKCS production ► Oil and gas production in the UKCS increased in 2015 for the

first time in 15 years, after years of production decline rates at maturing North Sea fields. There are several key fields which will commence production in 2015 to 2018, including Greater Laggan Area, Cygnus and Mariner (assuming no further delays) and the start-up of these fields, in addition to field redevelopments such as the Montrose Area Redevelopment, will support an increase in production from 2015 to 2018. BP also announced in August 2015 that it will spend US$1bn to increase output from oil fields off the eastern coast of Scotland (Eastern Trough Area Project (ETAP)), with the aim of securing the future of the field until 2030 and beyond.

► There have been a number of significant investments from new entrants in 2015 which shows there is still appetite to invest in the UKCS, even with the low oil price, including:

► Antin Infrastructure Partners acquisition of further equity in CATS, taking its total share to 99%

► Energy firm SSE’s acquisition of a minority stake in the Greater Laggan Area development

► North Sea Midstream Partners acquisition of FUKA and SIRGE gas pipelines and the St Fergus gas terminal

► Acquisition of the UK North Sea gas fields owned by DEA Group by Ineos.

► There are also still a number of significant developments in the UKCS, including the Laggan-Tormore development off the Shetland Islands noted above (one of the largest offshore oil

and gas projects in Europe, which involves the development of two gas and condensate fields) and the Culzean oil field development in the UK Central North Sea, which was approved by the OGA in September 2015. Culzean is a high pressure high temperature gas condensate field and is of immense importance to UK gas production as it is the largest single gas field sanctioned since East Brae in 1990, with production expected to start up in 2019.

► A number of other UK projects (e.g., small field or brownfield developments and expansions) have breakeven prices lower than the current oil prices due to the presence of existing infrastructure, reflecting the well-developed oil industry in the UKCS. However, falling prices could impact project economics for small to mid-scale developments and this could make the realisation of projects which have not reached final investment decision (FID) more difficult, as companies cut capital budgets and prioritise higher value-added projects elsewhere. A large portion of the remaining development projects in the UKCS could be delayed until either the costs are materially reduced or oil prices rise.

► In addition, reduced exploration activity is a worrying trend for the UKCS as new reserves fail to fully replenish produced reserves. Whilst there is high investment in terms of new developments (Oil & Gas UK’s Economic Report 2015 noted capital expenditure was £14.8 billion in 2014, the highest for the fourth consecutive year), there is a risk this won’t be sustained without further exploration activity and success. The OGA has identified this as a high priority area and the UK government has provided funding of £20 million for seismic surveys in untapped regions of the UKCS to try to stimulate exploration (data expected to be made freely available early in 2016). This in itself is unlikely to be sufficient and further incentives targeting exploration, such as the Norwegian regime where companies can claim an 80% rebate on exploration spending, are being called for but it is unlikely the UK Government would introduce a similar regime.

Shale ► In August 2015, the OGA announced the list of companies

which were to be awarded licences for 27 onshore blocks from the 14th Onshore Oil and Gas licensing round, which was the first for shale gas licensing. There are a number of challenges these companies will face including environmental, local and social opposition, as well as lack of technical knowledge. Uncertain geology and the time-consuming application process for hydraulic fracturing permits could temper shale gas efforts in the medium term and first commercial shale gas production will probably only occur in early 2020s and then only in minimal volumes.

8 Review of the UK oilfield services industry January 2016

UKCS operating costs ► In 2014, OFS companies started to address the rising costs

of operating in the UKCS, including cuts to contractor’s rates and redundancies. This has continued in 2015 due to the continued low oil price and a large number of companies have implemented pay freezes, further rounds of redundancies and warm or cold stacking equipment to address the decline in activity. A number of companies are proactively tackling the high cost base in the UKCS and a number of industry initiatives have been launched to try to improve efficiency and address the rising costs. This includes Wood Group which announced in September 2015 it is leading five new joint industry projects using the company’s extensive subsea experience to solve industry-wide challenges. These international projects, which will run between 2015 and 2018, will see Wood Group work with several oil and gas operators, contractors and regulators to improve quality, safety and competence across the sector and achieve significant savings in design and unplanned intervention costs.

► The OGA is also addressing rising costs in the UKCS and has a focused technology strategy to support a targeted 30%-40% efficiency improvement, with its priority technology themes being:

► Small pool development (technology to enable the development of more than 1 billion barrels of oil and gas from pools smaller than 50 million barrels of oil equivalent in place)

► Integrity and inspection (generate more than £1 billion additional revenue through the radical reduction of time dedicated to vessel inspection and managing corrosion under insulation)

► Well construction (reduce well construction costs by 50% to allow an extra c.50 wells to be drilled each year).

Fiscal regime ► UK North Sea tax receipts dropped to their lowest in 20

years in the 2014-2015 tax year, highlighting the challenges being faced by companies operating in the region in a lower commodity price environment. Low oil prices have led to a reduction in investing in sustaining production in the higher cost mature areas of the UKCS (e.g., planned shutdown of the Janice field).

► From January 2016, Petroleum Revenue Tax (PRT) will be reduced from 50% to 35% to support investment in maturing fields. This reduction in PRT aims to help to stimulate

brownfield investments on these fields, to help to maintain production at mature fields and by extension, helping to extend the life of infrastructure. The maintenance of this infrastructure for a longer period before decommissioning is critical, as this could incentivise the development and tie-ins of marginal nearby fields, whose smaller reserve size do not warrant a standalone development.

Viewpoint: UK OFS sector

The outlook for the UK sector continues to be extremely challenging, with expectations of an oil price recovery in the short term receding. Backlogs are being worked through, non-essential maintenance projects deferred, contract terms shortened and rates reducing. Companies have responded by implementing cost savings and have already cut discretionary spend, reduced headcount and re-engineered processes. The next step would be to consider longer term transformation projects such as operating model changes, standardising systems, business process outsourcing and the opportunities for consolidation and strategic acquisitions.

A particular challenge for management is how best to balance managing short-term cash flows through a period of volatility and change against the long-term health of their organisations, by continuing to invest in areas such as maintaining the skills base and technological innovation. Short term survival must always take precedence but history also suggests future leaders will recognise the importance of investing through the cycle and looking for opportunities to expand and develop.

There is evidence already of turnaround in certain operational indicators. Following the record investment levels of recent years and increased focus on production efficiency, the long term decline in UK production has begun to reverse. Similarly, unit operating expenditure per barrel has started to reduce after many years of increases. If these trends can be maintained into the medium-term, together with an upturn in exploration, the industry could yet emerge leaner and, with its long established international pedigree, well placed to capitalise on any recovery in the oil price.

Stuart White Director Transaction Advisory Services

Overview continued

9Review of the UK oilfield services industry January 2016

02

Viewpoint: Decommissioning

Decommissioning is a significant cost to the UK oil and gas industry and potentially the UK taxpayer, as the costs are tax deductible, which ought to result in a real focus on achieving cost-effective solutions. These cost efficiencies will only be delivered through integrated planning, tightly managed operating and capital expenditure and innovative engineering solutions. Industry will have to overcome a steep learning curve and adapt and implement lessons learned as quickly as possible; it will also need to co-operate to drive economies of scale, reduce risk and smooth demand over time.

The UK Government has long seen the need to encourage smaller, more agile operators into the sector to drive Maximising Economic Recovery (MER) and extend the life of fields. This M&A activity has experienced a decline in recent years, partly driven by uncertainty in decommissioning liabilities. The tax regime is also proving to be an obstacle with tax relief for retained decommissioning liabilities being uncertain, and there being no current mechanism to transfer an asset’s tax history. Industry is working with government to try and address these issues.

Derek Leith Partner EY UK Tax

Decommissioning ► There are over 600 offshore oil and gas installations in the

North Sea, 470 of which are in UK waters. These include sub-sea equipment fixed to the ocean floor, platforms, more than 10,000km of pipelines and around 5,000 wells. Many of these structures have been producing oil and gas for almost forty years and are now beyond the end of the lifespan for which they were designed. Under current regulatory requirements, over 90% of offshore structures will need to be completely removed from their marine sites and brought to shore for re-use, recycling or other means of disposal.

► Forecast spend on decommissioning continues to rise, and is currently estimated at $67bn by 2045 for the UKCS, which is a 13% increase in costs since August 20152. The UKCS actual spend on decommissioning passed £1 billion for the first time in 2014 and is likely to rise to around £1.5 billion in 2015 and to over £2 billion per annum by 20183 by which time over 50 fields will be either approaching or undergoing decommissioning.

► Decommissioning experience on the UKCS is currently limited to around ten large projects. As this is a new phase of activity for the OFS sector, initial solutions remain expensive and there is a need to significantly reduce costs and manage activity more effectively. Managing spend on decommissioning is one of the OGA’s priorities and its strategy is to reduce costs, increase efficiency, facilitate cooperation and technology innovation. The aim is that by integrating efforts, this will help reduce operating, equipment and service costs, downtime and overruns and limit non-productive activities.

► The scale of a number of the decommissioning projects to be undertaken on the UKCS over the next decade is unprecedented globally. The experience gained and any pioneering breakthroughs over the next decade could offer a competitive advantage to the UK OFS supply chain, as long as companies are able to adapt their business to offer support on decommissioning projects. This could create significant short term opportunities in the UK and export potential for these companies as demand for expertise will only continue to grow both domestically and globally.

2 Wood Mackenzie data3 Oil & Gas UK’s Economic Report, 2015

10 Review of the UK oilfield services industry January 2016

Overview continued

Summary of resultsFigure 2: Summary of results

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Number of companies 1,252 1,357 1,408 1,463 1,508 1,510 1,520

Reservoirs 712 851 848 1,092 1,219 1,355 1,244

Wells 5,752 5,605 5,652 6,360 7,298 7,776 8,020

Facilities 8,790 8,912 8,855 10,089 11,475 13,125 13,135

Marine and Subsea 5,708 6,011 6,856 8,420 8,993 10,275 10,991

Support and Services 3,904 4,201 4,711 5,578 6,297 7,254 7,554

Turnover 24,865 25,580 26,922 31,539 35,281 39,786 40,943

Growth trends — turnover n/a 2.9% 5.2% 17.2% 11.9% 12.8% 2.9%

EBITDA 2,785 2,727 2,605 2,870 3,535 4,066 4,195

Reservoirs 21.6% 16.0% 11.9% 14.8% 14.0% 18.1% 11.6%

Wells 13.2% 13.4% 12.7% 10.0% 12.0% 12.1% 15.0%

Facilities 7.0% 7.5% 8.2% 8.1% 8.6% 8.4% 6.3%

Marine and Subsea 14.8% 12.1% 9.8% 9.4% 10.9% 11.1% 12.7%

Support and Services 10.5% 10.5% 8.2% 8.4% 8.3% 8.7% 8.4%

EBITDA margin 11.2% 10.7% 9.7% 9.1% 10.0% 10.2% 10.3%

Tax on profits 620 527 465 486 677 608 674

Number of employees 108,284 106,504 106,666 113,652 122,903 133,701 140,965

Wages 4,594 4,761 4,864 5,275 5,873 6,737 7,234

The completeness of our data depends on the financial information disclosed in companies’ annual accounts submitted at Companies House. Consequently, our analysis is likely to be understated as opposed to overstated. For example, not all companies disclose headcount information and companies that file abbreviated accounts (those typically with less than £6.5 million turnover) do not disclose the financial information included in the above table.

Figure 3: 2014 revenue bandings

< £20mn

Num

ber o

f com

pani

es

% re

venu

e sh

are

2014 revenue share Number of companies

£20mn to£50mn

£50mn to£250mn

£100mn to£250mn

Over £250mn

297066173

1,182

0

200

400

600

800

1,000

1,200

1,400

0%5%

10%15%20%25%30%35%40%45%

11Review of the UK oilfield services industry January 2016

02

Key highlights ► During 2014, the UK OFS sector delivered another year

of growth across all the supply chain categories, except Reservoirs, albeit at a lower rate than the trend of recent years, primarily due to the decline in the oil price in the second half of 2014. Turnover increased by £16.1 billion between 2008 and 2014 (compound annual growth rate (CAGR) 9%)). Although there are over 1,500 companies in our sample, the 338 companies that generated turnover in excess of £20 million in 2014 accounted for over 90% of total 2014 revenue. The largest UK OFS companies typically operate across the whole supply chain and offer integrated solutions to their customers, whilst the smaller companies typically specialise in a specific sub-sector.

► In terms of revenue, Facilities and the Marine and Subsea supply chain categories dominate, which reflects the mature state of the UKCS. The expertise developed over the last 40 years or so has allowed UK entities to become world-leading and export their services and products on a global basis.

► There has been year-on-year growth in turnover between 2008 and 2014. However, the growth of over 10% in each of 2011, 2012 and 2013, driven both by activity in the UKCS and overseas, was not repeated in 2014. The decline in the oil price has affected growth rates in all supply chain segments, with the Reservoirs segment being first hit and worst affected with a 8% revenue decline in 2014 as a result of the E&P companies significantly reducing investment in exploration activity. In addition, given the mature nature of the UK market and the challenges it faces in areas such as cost competitiveness, it is worrying that, after delivering year on year growth in exports from 2008, export sales were flat in 2014.

► EBITDA margin varies across the supply chain segments, with Wells achieving the highest margin in 2014. EBITDA margin declined from 2009 to 2011 mainly as a result of pricing pressure from customers, salary increases due to the shortage of skilled personnel in the sector and unrealised supply chain savings. During 2012 and 2013, this decline was somewhat reversed as costs were recovered from customers. EBITDA margin was flat in 2014 but in order to address the impact of the decline in the oil price, companies had started to implement cost saving strategies to reduce their cost base. This continued in 2015 as companies faced lower activity levels and a reduction in contract rates.

► The key trends by supply chain category are as follows:

► Reservoirs has seen a 8% turnover decline in 2014 and a 6 percentage points (ppt) EBITDA margin reduction as a result of pricing pressures following the decline in investment in exploration activity. We would expect further turnover and EBITDA declines in 2015 as the divisional results for the nine months to September 2015 for the listed parents of the top five companies in this segment show a reduction of 22% in turnover and 27% in EBITDA. Backlogs for these listed companies have reduced by over 32%, which creates further uncertainty for 2016.

► Wells turnover growth has continued in 2014, with a 3% improvement, due to a number of new assets operating in the UKCS and a higher level of product sales and provision of services. EBITDA margin also improved due to high margin rig activity and lower levels of vessel downtime. However, we would not expect to see this trend continue in 2015 as the results from the listed parents of the top five companies for the nine months to September 2015 show a decline of over 20% in turnover and 28% in EBITDA, mainly due to additional discounting on existing contracts and a decline in rig activity. In addition, backlogs have shown a 44% reduction for these listed companies, which suggest a further decline in 2016.

► Turnover for Facilities was flat in 2014 due to a reduction in the number of major projects and a sharp decline in sales of certain products, offset by an increase in activity levels for a number of specialist services. EBITDA margin declined by 2 ppt in 2014 primarily as a result of additional costs on a major construction project in Shetland. The decline in turnover of the listed parents of the top five companies for the six months to June 2015 was not as severe as for other segments of the supply chain (c 10%) as these companies are partially protected by the long term operations and maintenance contracts they operate under and this should also offer some protection for these companies in 2015 and 2016.

12 Review of the UK oilfield services industry January 2016

► Our analysis of the number of employees is based on employee headcount disclosed within individual company’s annual accounts filed at Companies House. The total number of employees in our analysis will be understated as a consequence of:

► Not all companies disclose employee numbers

► A number of offshore employees are employed by overseas entities and, as such, are excluded from our analysis as they do not submit annual accounts at Companies House

► Individual contractors involved in the UK upstream oil and gas industry are excluded

► EY’s Fuelling the next generation — A study of the UK upstream oil and gas workforce published in December 2014 identified the OFS workforce (based on information provided directly by the OFS companies either through interview or questionnaire) to be approximately 250,000, including around 50,000 contract staff.

► Based on our analysis from annual accounts, the number of employees increased by 32,681 to 140,965 between 2008 and 2014 and the average salary increased from £42,000 in 2008 to £51,000 in 2014 (CAGR 3%), whereas average salaries in the UK across all industries over the same period increased by less than CAGR 2% (ONS Labour Market Statistics). This partly reflects the skilled nature of the work in the OFS sector and the many organisations globally competing for the same talent pool but also indicates an inflated cost base. However, given the pay freezes, pay cuts and redundancies which started in the latter half of 2014 and continued in 2015, these actions are likely to impact on 2015 average salaries and numbers of employees.

Overview continued

► Marine and Subsea turnover increased by 7% in 2014 and EBITDA margin improved by 2 ppt due to higher vessel utilisation, successful project execution and change of product mix. However, due to a decrease in activity and reduced vessel utilisation globally, there has been a 15% reduction in turnover for the listed parents of the top five companies for the nine months to September 2015, although EBITDA margins are flat as there has been a focus on cost reduction and fleet management. Although UK companies will have some protection due to a number of large capital projects in the UKCS which are set to continue in 2015, reduced vessel utilisation and reduction in capital projects globally will impact UK companies. In addition, the backlog reduction of 18% from the listed parents is likely to result in additional turnover declines in 2016.

► Support and Services turnover only increased by 4% in 2014, following double digit growth in each of the preceding four years. There were a number of companies in this segment which were severely impacted by the cost savings initiatives implemented as a result of the low oil price as customers cut discretionary spend and delayed non-essential spend. As the majority of the top five customers do not have listed parents, there is no financial information available in relation to 2015 trends. However, these companies are expected to follow the overall global listed trends and see further turnover decline in both 2015 and 2016.

13Review of the UK oilfield services industry January 2016

02

Geographic analysis of turnover

Figure 4: Analysis of turnover between UK and exports

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

UK 14,170 13,806 14,221 17,274 20,218 24,089 25, 276

Exports 10,695 11,774 12,701 14,265 15,064 15,697 15,668

Turnover 24,865 25,580 26,922 31,539 35,281 39,786 40,943

Exports as a percentage of turnover 43% 46% 47% 45% 43% 39% 38%

Figure 5: UK and export turnover 2008-14

0

5,000

10,000

15,000

20,000

25,000

30,000

2008 2009 2010 2011 2012 2013 2014

£mn

UK Exports

Figure 6: UK and export turnover CAGR 2008-14

0%2%4%6%8%

10%12%14%

Under£50mn

£50mn to£100mn

£100mn to£250mn

Over£250mn

UK Exports

► There was a significant increase in UK turnover in each of 2011, 2012 and 2013, reflecting the increase in spend in the UKCS in this period (there was an increase in capital expenditure of some £2.5 billion in 2011, £3.4 billion in 2012 and £3 billion in 20134. Growth slowed in 2014 as a result of the impact of oil price decline which particularly affected the reservoirs and facilities supply chain categories.

► Export turnover increased year-on-year between 2008 and 2013 and represents around 40% of total turnover, reflecting the internationalisation of the UK OFS sector and the demand for the specialist skills the companies in our analysis provide in the global arena. With the ramp up in activity in the UKCS in 2011 to 2013, exports as a percentage of turnover has reduced slightly in recent years and this trend continued in 2014 as some of the overseas markets which UK OFS companies operate in were also impacted by the declining oil price.

► Export growth from 2008 to 2014 was highest in companies with annual turnover of less than £50 million. Typically, this is because the smaller companies tend to be niche players in a particular sub-sector and the higher export growth reflects the global demand for such specialist skills. Large players often also have a local subsidiary presence in key overseas locations, which are excluded from our analysis as they do not submit annual accounts at Companies House. Given the maturity of UKCS, the cuts to capital expenditure programmes and the emphasis on reducing operating costs by E&P companies, there will be an increased focus on generating revenues from export activity for a number of UK companies in locations which are still experiencing growth, such as the Middle East.

4 Oil & Gas UK’s 2014 Activity Survey

14 Review of the UK oilfield services industry January 2016

15Review of the UK oilfield services industry January 2016

03–07

15

The UK oilfield services sector by supply chain category

16 Review of the UK oilfield services industry January 2016

17Review of the UK oilfield services industry January 2016

03Reservoirs

18 Review of the UK oilfield services industry January 2016

Reservoirs

Figure 7: UK upstream oil and gas supply chain sub-sectors

Supply chain categories: Reservoirs Wells Facilities Marine and Subsea Support and

Services

Tier 2:

Main contractors and consultants

► Seismic data acquisition and processing contractors

► ►Well services contractors

► ►Drilling contractors ► Well engineering consultancies

► ►Engineering, operation, maintenance and decommissioning contractors

► Engineering consultants

► ►Structure and topside design and fabrication

► ►Marine/Subsea contractors

► Heavy lift/Pipe lay contractors

► Floating production storage units

► ►Catering/facility management

► ►Sea/air transport ► ►Warehousing/logistics

► ►Communications ► ►Recruitment ► ►Training ► ►Health, safety and environmental services

► ►Energy consultancies

► ►IT Hardware/software

Tier 3:

Products and services suppliers

Components

Sub-contractors and sub-suppliers

► ►Geosciences consultancies

► Data interpretation consultancies

► ►Seismic instrumentation

► ►Drilling and well equipment design and manufacture

► ►Laboratory services

► ► ►Machinery/plant design and manufacture

► ►Engineering support contractors

► ►Specialist engineering services

► Specialist steels and tubulars

► ►Inspection services

► ►Subsea manifold/riser design and manufacture

► ►Marine/subsea equipment

► ►Subsea inspection services

Figure 8: Analysis of Reservoirs turnover and EBITDA margin by sub-sector

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Seismic data acquisition and processing contractors

415 528 498 668 720 779 599

Geosciences consultancies 91 115 146 170 217 206 223

Data interpretation consultancies 132 132 134 150 177 238 275

Seismic instrumentation 74 77 70 104 104 132 146

Turnover 712 851 848 1,092 1,219 1,355 1,244

Seismic data acquisition and processing contractors

22.1% 16.3% 8.4% 13.1% 12.4% 19.2% 9.1%

Geosciences consultancies 21.1% 13.5% 13.4% 11.7% 12.0% 12.0% 12.9%

Data interpretation consultancies 20.7% 16.2% 23.0% 22.7% 23.5% 22.1% 15.9%

Seismic instrumentation 21.2% 17.9% 12.2% 19.3% 13.3% 14.1% 12.2%

EBITDA margin 21.6% 16.0% 11.9% 14.8% 14.0% 18.1% 11.6%

19Review of the UK oilfield services industry January 2016

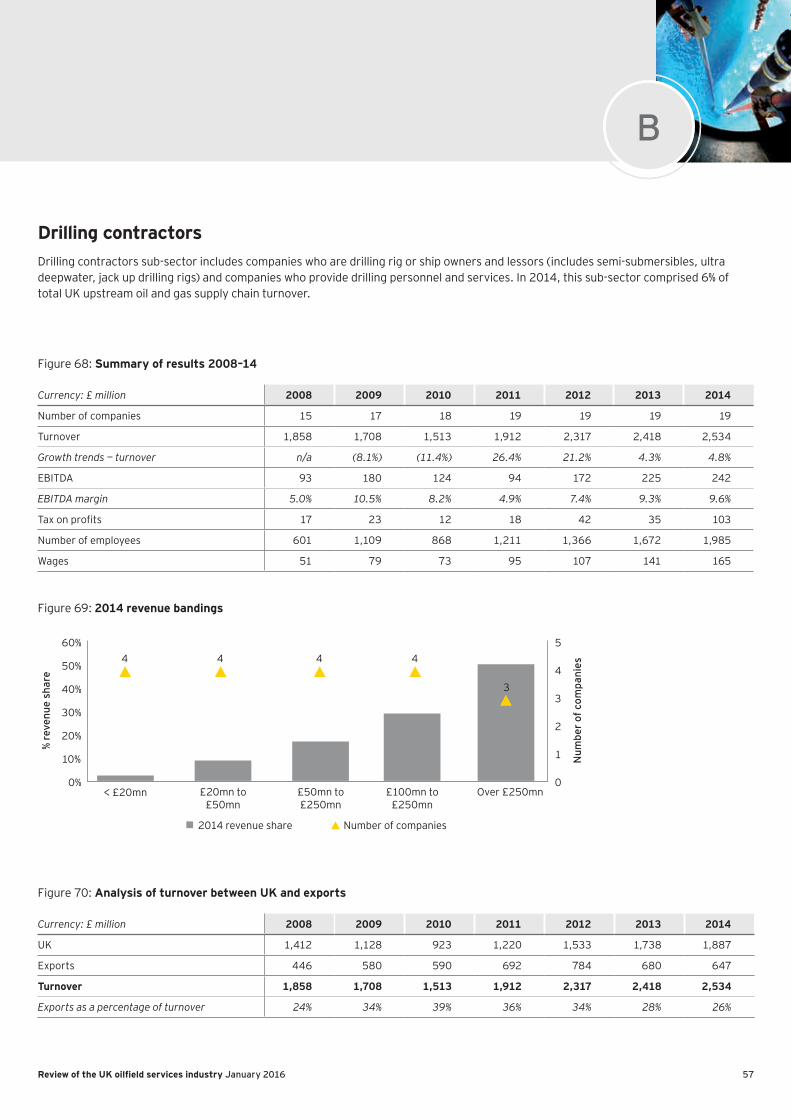

Summary of resultsIn 2014, the Reservoirs supply chain comprised 3% of the total UK upstream oil and gas supply chain turnover.

Figure 9: Summary of results 2008–2014

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Number of companies 74 80 84 84 84 84 84

Turnover 712 851 848 1,092 1,219 1,355 1,244

Growth trends — turnover n/a 19.5% (0.4%) 28.8% 11.6% 11.2% (8.2%)

EBITDA 154 136 100 162 171 245 145

EBITDA margin 21.6% 16.0% 11.9% 14.8% 14.0% 18.1% 11.6%

Tax on profits 46 21 18 28 30 43 23

Number of employees 3,379 3,904 4,059 4,314 4,983 5,323 5,896

Wages 141 165 182 205 242 271 287

Key highlights of the Reservoirs supply chain category results

► Turnover increased by £0.5 billion between 2008 and 2014 (CAGR 10%). We have identified 84 companies in this segment of the supply chain and in 2014, 67 companies generated turnover of less than £20 million. The largest 7 companies generated over 50% of the total 2014 Reservoirs turnover.

► There was a significant upturn in turnover in each of 2011, 2012 and 2013 as the industry continued its search for new hydrocarbon resources in regions featuring deeper waters, harsher environments, extreme reservoir depths and complex geologies. This had increased the need for better seismic analysis and companies were also reappraising many existing fields using 3D seismic, resulting in better quality information.

► However, there was a 8% decline in turnover in 2014 as a result of the fall in the oil price and oil companies significantly reducing investment in exploration activity. This has led to intense competition for work among seismic companies, which has had a detrimental impact on pricing.

► EBITDA margin was negatively impacted in 2010 by the cessation of exploration activity in the Gulf of Mexico following the Macondo incident in April 2010. This resulted in the number of vessels working in the Gulf of Mexico reducing significantly, with the majority of the excess capacity being absorbed by West Africa and Europe at lower margins.

► Since 2010, EBITDA margins have started to recover and in 2013, Reservoirs generated the highest EBITDA margin as compared to the other supply chain categories, primarily as a result of the skilled nature of the work and the increase in 3D seismic. However, this trend was reversed in 2014 and EBITDA margin declined by 6 ppt. This was a result of the pricing pressures faced by Reservoir companies as a result of the decline in investment in exploration activity, partly offset by cost saving initiatives implemented by a number of the companies.

► The number of employees increased by over 2,500 between 2008 and 2014 and the average salary increased from £42,000 in 2008 to £49,000 in 2014 (CAGR 3%), reflecting the skilled nature of the work.

03

20 Review of the UK oilfield services industry January 2016

Reservoirs continued

Geographic analysis of Reservoirs turnover

Figure 11: UK and export turnover 2008-14

0

200

400

600

800

1,000

2008 2009 2010 2011 2012 2013 2014

£mn

UK Exports

Figure 12: UK and export turnover CAGR 2008-14

0%

10%

20%

Under £50mn £50mn to£100mn

£100mn to£250mn

UK Exports

► UK turnover increased year-on-year from 2008 to 2013, driven by the increase in seismic analysis in the UKCS and reappraisal of existing fields. However, this trend was reversed in 2014 due to the impact of the decline in the oil price, which has resulted in a significant reduction in investment in exploration activity in the UKCS.

► Reservoirs exports as a percentage of turnover is the highest amongst all the supply chain categories. This is driven by the specialist nature of the services and the ease to which they can be transferred and utilised on a global basis.

► In 2012 and 2013, the reduction in exports as a percentage of turnover was driven by two of the largest companies in this segment significantly increasing the level of seismic work undertaken in the UKCS. In 2014, exports as a percentage of turnover has increased as, although global exploration activity has reduced in response to the oil price, it has done so at a slower rate than in the UKCS.

► As can be seen in Figure 12, export growth was highest for companies with turnover under £50 million due to a number of companies within this revenue banding, which operated solely in the UKCS in 2008, expanding their activities overseas from 2009 onwards. In 2014, more than 50% of the turnover for a number of these entities was generated from exports, which demonstrates the extent of the expansion.

Figure 10: Analysis of turnover between UK and exports

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

UK 244 279 310 384 547 580 497

Exports 468 573 538 708 671 775 747

Turnover 712 851 848 1,092 1,219 1,355 1,244

Exports as percentage of turnover 66% 67% 63% 65% 55% 57% 60%

21Review of the UK oilfield services industry January 2016

Key trends in Reservoirs

► Where available, we have analysed the divisional results of the listed parents of the top five companies in the Reservoir supply chain category. As can be seen from Figure 14, there has been a steep decline in both turnover and EBITDA for 9m2015 against 9m2014. However, EBITDA margin has only reduced by 1.6 ppt as companies have been reducing costs, resizing their fleets and implementing efficiency measures. As backlog has declined by nearly 33%, it would appear the revenue decline will continue into 2016.

► As noted above, in the global Reservoir supply chain category, there has been falling backlogs, intense pricing pressure (including decreases in contract rates for already signed exploration commitments) and oversupply of vessels. Although there has been a reduction in streamer vessels from 2013 to 2015 of around 20% (including those which are cold-stacked), the decrease in demand over the same period was around 30%, resulting in a continued oversupply. This suggests further capacity reductions are required.

UK ► Oil and gas exploration and appraisal in the UKCS is declining

as companies choose to focus on development activities rather than invest in exploration, or to move out of the mature North Sea altogether. The number of exploration and appraisal wells drilled in the UKCS has decreased from 105 in 2008 to 24 for the nine months to 30 September 2015, and exploration success for 2010 to 2014 was only 27%. There are a number of key challenges which are affecting the UKCS including:

► The high cost environment which de-incentivises new exploration in the UKCS

► The small size of many remaining opportunities — the UKCS is a mature basin and with a few notable exceptions, most of the remaining resources and new discoveries are small in size and cannot justify a standalone development.

► We would expect the 2015 results for the companies in the Reservoir supply chain category to follow the listed company turnover and EBITDA margin trends, assuming these companies have been proactive to address the decline in activity in 2015 by reducing their cost base. If not, the EBITDA margin decline could be more extensive.

► To try and address falling exploration activity, the OGA is supporting a £20 million UK government funded seismic project to acquire new high-quality broadband 2D data from

► The oil price decline is driving reductions in capital programmes and cost control by E&P companies, which has already led to delays or cancellations of exploration programmes. As can be seen from Figure 13, global seismic spending has historically correlated directly to oil price fluctuations.

Figure 13: Seismic spending versus average oil price

—

20

40

60

80

100

120

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2008 2009 2010 2011 2012 2013 2014 2015E

US$

US$

mn

Global seismic spending Oil price (Brent average)

Figure 14: Listed Reservoir companies results for the period from January 2015 to September 2015 (9m2015) versus the period from January 2014 to September 2014 (9m2014)

Currency: US$ million

9m2015 9m2014 Variance Variance %

Turnover 10,263 13,201 (2,938) (22.3%)

EBITDA 2,748 3,746 (998) (26.6%)

EBITDA margin 26.8% 28.4% (1.6) n/a

Backlog* 2,561 3,806 (1,245) (32.7%)

03

*where disclosed

03

Viewpoint: Reservoirs

Reservoirs is the segment most severely affected by the decline in the oil price since 2014; the results of the listed companies in this segment in 2015 suggest this will continue into 2016. Asset heavy companies reliant on acquisition are likely to be more affected than those focused on processing and data interpretation.

The decline in the number of exploration and appraisal wells drilled in the UKCS, together with the low success rate, was already a worrying trend for the UKCS and the reduced investment in exploration activity by E&P companies will only exacerbate this. The OGA, with financial support from the UK Government, is taking steps to try to address this; however, by itself, this is unlikely to be sufficient and further incentives to stimulate exploration may be required.

Celine Delacroix Executive Director Transaction Advisory Services

Review of the UK oilfield services industry January 201622

the Rockall Trough and Mid-North Sea High area. Operations began in mid-July 2015, with three vessels in the field acquiring data over an area of 220,000km (roughly the land mass of the UK). We understand survey operations are progressing to schedule and the data will be made freely available to the industry early in 2016.

► There are a number of other actions the OGA is planning to try to revitalise exploration activity (and related success) in the UKCS including:

► Management of geophysical data from operators to make sure high-quality data is made available to industry in a timely manner

► Providing industry with an in-depth evaluation of regional prospectivity and yet-to-find resources.

Reservoirs continued

23Review of the UK oilfield services industry January 2016

04Wells

24 Review of the UK oilfield services industry January 2016

Wells

Figure 15: UK upstream oil and gas supply chain sub-sectors

Supply chain categories: Reservoirs Wells Facilities Marine and Subsea Support and

Services

Tier 2:

Main contractors and consultants

► ►Seismic data acquisition and processing contractors

► ►Well services contractors

► ►Drilling contractors ► Well engineering consultancies

► ►Engineering, operation, maintenance and decommissioning contractors

► Engineering consultants

► ►Structure and topside design and fabrication

► ►Marine/Subsea contractors

► Heavy lift/Pipe lay contractors

► Floating production storage units

► ►Catering/facility management

► ►Sea/air transport ► ►Warehousing/logistics

► ►Communications ► ►Recruitment ► ►Training ► ►Health, safety and environmental services

► ►Energy consultancies

► ►IT Hardware/software

Tier 3:

Products & services suppliers

Components

Sub-contractors and sub-suppliers

► ►►Geosciences consultancies

► ►Data interpretation consultancies

► ►Seismic instrumentation

► ►Drilling and well equipment design and manufacture

► ►Laboratory services

► ► ►Machinery/plant design and manufacture

► ►Engineering support contractors

► ►Specialist engineering services

► Specialist steels and tubulars

► ►Inspection services

► ►Subsea manifold/riser design and manufacture

► ►Marine/subsea equipment

► ►Subsea inspection services

Figure 16: Analysis of Wells turnover and EBITDA margin by sub-sector

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Well services contractors 2,309 2,321 2,477 2,409 2,617 2,719 2,884

Drilling contractors 1,858 1,708 1,513 1,912 2,317 2,418 2,534

Well engineering consultancies 96 49 65 213 167 154 187

Drilling and well equipment design and manufacture

1,375 1,374 1,444 1,660 1,976 2,312 2,243

Laboratory services 113 154 154 164 219 173 171

Turnover 5,752 5,605 5,652 6,360 7,298 7,776 8,020

Well services contractors 15.0% 13.7% 12.6% 10.7% 12.0% 10.5% 11.7%

Drilling contractors 5.0% 10.5% 8.2% 4.9% 7.4% 9.3% 9.6%

Well engineering consultancies 6.8% 5.6% 3.1% 7.5% 5.4% 5.9% 11.5%

Drilling and well equipment design and manufacture

20.6% 15.9% 17.5% 14.8% 17.5% 17.5% 25.3%

Laboratory services 26.6% 21.8% 16.9% 13.4% 15.6% 10.6% 18.3%

EBITDA margin 13.2% 13.4% 12.7% 10.0% 12.0% 12.1% 15.0%

04

25Review of the UK oilfield services industry January 2016

Summary of resultsIn 2014, the Wells supply chain comprised 20% of the total UK upstream oil and gas supply chain turnover.

Figure 17: Summary of results 2008–2014

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Number of companies 177 194 200 206 207 210 211

Turnover 5,752 5,605 5,652 6,360 7,298 7,776 8,020

Growth trends — turnover n/a (2.6%) 0.9% 12.5% 14.7% 6.6% 3.1%

EBITDA 761 752 717 635 876 943 1,202

EBITDA margin 13.2% 13.4% 12.7% 10.0% 12.0% 12.1% 15.0%

Tax on profits 176 148 128 120 159 123 189

Number of employees 20,023 19,410 19,456 20,344 20,945 23,050 23,018

Wages 865 909 942 1,000 1,089 1,217 1,307

Key highlights of the Wells supply chain category results

► Turnover increased by £2.3 billion between 2008 and 2014 (CAGR 6%). We have identified 211 companies in this segment of the supply chain and in 2014, 155 companies generated turnover of less than £20 million. The largest 7 companies generated 50% of the total 2014 Wells turnover.

► The increased complexity of the type of field which is now being developed (e.g., brownfield work on older depleting fields or wells under deep water, some with high temperature and high pressure) has driven growth in this segment.

► Turnover increased in 2011, 2012 and 2013 primarily due to an increase in the number of drilling rigs and ships operating in the UKCS, an increase in contract day rates, higher vessel utilisation, an increase in personnel levels and an increase in the level of export activity from drilling and well equipment design and manufacture companies.

► Turnover growth continued in 2014 due to a number of new vessels operating in the UKCS (e.g., semi-submersible rigs, ultra-premium harsh environment jack up rigs), as well as an increase in product sales and provision of services. However, there were a number of companies that felt the impact of the oil price decline and had a reduction in turnover as a result of having to renegotiate contract extensions at lower rates or had a contraction in the overall volume of business.

► EBITDA margin declined in 2011 due to pricing pressure from customers and cost increases in the UKCS. There was a 2ppt EBITDA margin recovery in 2012 due to increased rig rates in the North Sea (Oil & Gas UK 2013 Activity Survey cited a 40% increase in semi-submersible and 66% increase in jack-up rig rates) and this was sustained in 2013. There was a further 3ppt EBITDA increase in 2014 primarily due to increase in rig activity (which generates very high EBITDA margins), reduced vessel downtime and lower repair costs incurred by the drilling contractors.

► The number of employees increased by nearly 3,000 between 2008 and 2014 and the average salary increased from £43,000 in 2008 to £57,000 in 2014 (CAGR 5%), reflecting the lack of available skilled and experienced workers, particularly in Drilling5.

5 EY’s Fuelling the next generation — A study of the UK upstream oil and gas workforce

26 Review of the UK oilfield services industry January 2016

Wells continued

Geographic analysis of Wells turnover

Figure 19: UK and export turnover 2008-14

0

1,000

2,000

3,000

4,000

5,000

2008 2009 2010 2011 2012 2013 2014

£mn

UK Exports

Figure 20: UK and export turnover CAGR 2008–14

0%

2%

4%

6%

8%

10%

12%

14%

Under£50mn

£50mn to £100mn

£100mnto £250mn

Over£250mn

UK Exports

► UK turnover decreased in 2010 due to a reduction in the number of drilling units operating in the UKCS. UK turnover increased in each of 2011, 2012, 2013 and 2014, primarily due to an upturn in UK activity by well services and drilling contractors. The increase in spend was reinforced by Oil & Gas UK’s 2012, 2013, 2014 and 2015 Activity Surveys which state that for the UKCS:

► Exploration and appraisal well spending was £1.4 billion, £1.7 billion, £1.6 billion and £1.1 billion in 2011, 2012, 2013 and 2014 respectively

► There was an increase in capital spend of some £2.5 billion in 2011 (up to £8.5 billion), £3.4 billion in 2012 (up to £11.4 billion), £3.0 billion in 2013 (up to £14.4 billion) and £0.4 billion in 2014 (up to £14.8 billion).

► Export turnover has increased year-on-year from 2008 to 2013, driven primarily by the drilling and well equipment design and manufacture sub-sector and the well services contractors. However, exports as a percentage of turnover declined in 2014 as the overall growth was primarily a result of new vessels operating in the UKCS and overseas activity for well services contractors reduced.

► Whereas drilling contractors generate a large portion of turnover from the UK (c.70%) as they tend to use the UK entities primarily to lease units in the UKCS, drilling and well equipment design and manufacture companies typically service the global market, with 69% of the turnover in this sub-sector in 2014 being exports.

► As the UKCS is a mature basin, many of the companies in this segment (excluding drilling contractors which typically use local entities for overseas activity) have focused on expanding overseas for their growth strategies. This is highlighted as CAGR export growth exceeds CAGR UK growth across most of the revenue bandings (see Figure 20, and is particularly evident in companies with less than £50 million turnover which typically have the more specialised niche offerings.

Figure 18: Analysis of turnover between UK and exports

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

UK 3,110 2,840 2,538 2,951 3,320 3,739 4,078

Exports 2,642 2,765 3,115 3,408 3,977 4,037 3,942

Turnover 5,752 5,605 5,652 6,360 7,298 7,776 8,020

Exports as percentage of turnover 46% 49% 55% 54% 55% 52% 49%

*where disclosed

27Review of the UK oilfield services industry January 2016

Key trends in Wells

► However, EBITDA margin has only reduced by 1.8 ppt as companies have been managing their cost base and improving drilling efficiency in this period of lower activity. In addition, despite companies focusing on controlling their cost base, they are also still developing technologies to improve customers’ returns in a lower oil price world to ensure they remain competitive.

► Where available, we have analysed backlog and this has shown a decline of over 44% for 9m2015 against 9m2014, suggesting the revenue decline will continue at least into 2016, given the oil price is not predicted to increase significantly, if at all, over the next twelve months.

UK ► In 2014, capital expenditure in the UKCS was £14.8 billion, the

highest on record, but this was partially due to cost over-runs and project slippage on some of the large developments. It is expected to fall sharply in 2015 and very little new investment is expected to be sanctioned whilst the oil price is low (Oil & Gas UK’s 2015 Activity Survey).

► Drilling activity has been declining in the UKCS (see Figure 23), particularly in relation to exploration and appraisal wells due to the poor exploration results over the last four years.

Figure 23: Drilling activity on UKCS from 2008 to 2015

050

100150200250300

2008 2009 2010 2011 2012 2013 2014 Q1–Q32015

Num

ber o

f wel

ls

Exploration, appraisal and development wells

Source: OGA

► We would expect 2015 results for the companies in the Wells supply chain segment to decline due to the reduction in rig activity, with UK companies at greater risk due to the reduced competitiveness of the UKCS at lower oil prices as compared to some other basins.

► The Wells supply chain category is very reactive to oil price volatility, which has a direct impact on drilling activity. Any reduction in drilling activity has a knock-on effect on day rates that companies can charge for rigs and also results in excess supply sitting idle or being warm or cold stacked. As can be seen from Figure 21, the worldwide rig count has decreased steadily from December 2014 to November 2015 as a result of the decline in oil prices and the related reduction in activity.

Figure 21: Worldwide rig count for January 2014 to November 2015

0500

1,0001,5002,0002,5003,0003,5004,000

Jan

14Fe

b 14

Mar

14

Apr

14

May

14

Jun

14Ju

l 14

Aug

14

Sep

14O

ct 1

4N

ov 1

4D

ec 1

4Ja

n 15

Feb

15M

ar 1

5A

pr 1

5M

ay 1

5Ju

n 15

Jul 1

5A

ug 1

5Se

p 15

Oct

15

Nov

15

Worldwide rig count

Num

ber o

f rig

s

Source: Baker Hughes Incorporated

Figure 22: Listed Wells companies results for the period from January 2015 to September 2015 versus the period from January 2014 to September 2014

Currency: US$ million

9m2015 9m2014 Variance Variance %

Turnover 32,630 41,070 (8,440) (20.6%)

EBITDA 5,640 7,843 (2,204) (28.1%)

EBITDA margin 17.3% 19.1% (1.8) n/a

Backlog* 8,020 14,341 (6,321) (44.1%)

► We have analysed the divisional results of the listed parents of the top five companies in the Wells supply chain category. As can be seen from Figure 22, there has been a steep decline in both turnover and EBITDA for 9m2015 against 9m2014. This is a result of a combination of persistent pricing pressure due to oversupply in the global markets, additional discounting on existing contracts and continuing decline in rig activity.

04

04

Viewpoint: Wells

At present, the well construction phase typically involves a number of OFS companies and there is a significant amount of time lost due to either waiting on another supplier or slippages resulting in scheduling issues. This needs to be addressed to optimise end-to-end well construction, which could be achieved by:

► establishing an overall co-ordinator to effectively manage the project schedule

► collaboration and joint venture agreements (which we are already seeing in the sector

► standardisation of design to reduce the number of bespoke elements and associated manufacturing costs.

Together, this could reduce construction time and cost, which is imperative given the current oil price and to increase the attractiveness of the UKCS. Furthermore, production efficiencies have to be found and technologies to increase the lifespan of wells must be an area of focus for companies in this part of the supply chain.

Andrew Deane Director Advisory

28 Review of the UK oilfield services industry January 2016

► The OGA also recognises the issues facing this part of the supply chain and has actions to take accountability for the management of well data from operators to make sure high-quality data is made available to industry in a timely manner. It has already completed a rigorous analysis of failed wells in the Moray Firth and Central North Sea between 2003 and 2013, and presented its results at the Oil &Gas UK conference. Its findings highlighted the opportunity for significant improvement in fundamental technical work to avoid drilling poor quality prospects and it aims to implement a rigorous pre- and post-drill evaluation quality assurance process with operators as one measure to address this.

Wells continued

29Review of the UK oilfield services industry January 2016

05Facilities

30 Review of the UK oilfield services industry January 2016

Facilities

Figure 24: UK upstream oil and gas supply chain sub-sectors

Supply chain categories: Reservoirs Wells Facilities Marine and Subsea Support and

Services

Tier 2:

Main contractors and consultants

► ►Seismic data acquisition and processing contractors

► ►Well services contractors

► ►Drilling contractors ► Well engineering consultancies

► ►Engineering, operation, maintenance and decommissioning contractors

► Engineering consultants

► ►Structure and topside design and fabrication

► ►Marine/Subsea contractors

► Heavy lift/Pipe lay contractors

► Floating production storage units

► ►Catering/facility management

► ►Sea/air transport ► ►Warehousing/logistics

► ►Communications ► ►Recruitment ► ►Training ► ►Health, safety and environmental services

► ►Energy consultancies

► ►IT Hardware/software

Tier 3:

Products & services suppliers

Components

Sub-contractors and sub-suppliers

► ►►Geosciences consultancies

► ►Data interpretation consultancies

► ►Seismic instrumentation

► ►Drilling and well equipment design and manufacture

► ►Laboratory services

► ► ►Machinery/plant design and manufacture

► ►Engineering support contractors

► ►Specialist engineering services

► Specialist steels and tubulars

► ►Inspection services

► ►Subsea manifold/riser design and manufacture

► ►Marine/subsea equipment

► ►Subsea inspection services

Figure 25: Analysis of Facilities turnover and EBITDA margin by sub-sector

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Engineering, operation, maintenance and decommissioning contractors

4,245 4,042 3,968 4,675 5,176 5,709 5,390

Engineering consultants 195 234 259 288 350 394 482

Structure and topside design and fabrication 251 383 351 455 650 646 857

Machinery/plant design and manufacture 1,972 2,140 2,067 2,210 2,533 2,709 2,797

Engineering support contractors 778 767 792 875 1,030 1,206 1,180

Specialist engineering services 508 533 610 650 829 1,107 1,303

Specialist steels and tubulars 487 441 435 545 435 813 609

Inspection services 355 372 374 391 472 541 517

Turnover 8,790 8,912 8,855 10,089 11,475 13,125 13,135

Engineering, operation, maintenance and decommissioning contractors

3.7% 3.9% 6.3% 6.4% 6.6% 6.4% 0.7%

Engineering consultants 9.6% 6.8% 3.9% 3.9% 4.2% 2.9% 3.8%

Structure and topside design and fabrication 10.0% 8.8% 5.4% 7.3% 6.2% 8.0% 8.5%

Machinery/plant design and manufacture 11.4% 13.2% 13.3% 12.1% 12.8% 12.7% 12.2%

Engineering support contractors 7.6% 6.3% 5.7% 6.4% 6.9% 7.6% 7.2%

Specialist engineering services 7.9% 6.1% 7.7% 7.7% 10.2% 10.3% 11.1%

Specialist steels and tubulars 6.1% 5.6% 5.2% 6.0% 6.5% 5.6% 5.4%

Inspection services 16.4% 19.3% 15.6% 16.9% 16.5% 14.9% 17.3%

EBITDA margin 7.0% 7.5% 8.2% 8.1% 8.6% 8.4% 6.3%

05

31Review of the UK oilfield services industry January 2016

Summary of resultsIn 2014, the Facilities supply chain comprised 32% of the total UK upstream oil and gas supply chain turnover.

Figure 26: Summary of results 2008–2014

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

Number of companies 457 497 514 524 537 539 543

Turnover 8,790 8,912 8,855 10,089 11,475 13,125 13,135

Growth trends — turnover n/a 1.4% (0.6%) 13.9% 13.7% 14.4% 0.1%

EBITDA 613 665 727 814 985 1,105 822

EBITDA margin 7.0% 7.5% 8.2% 8.1% 8.6% 8.4% 6.3%

Tax on profits 159 146 139 167 197 131 144

Number of employees 53,085 50,658 49,723 52,752 57,436 59,414 61,971

Wages 2,229 2,247 2,238 2,359 2,618 2,922 3,111

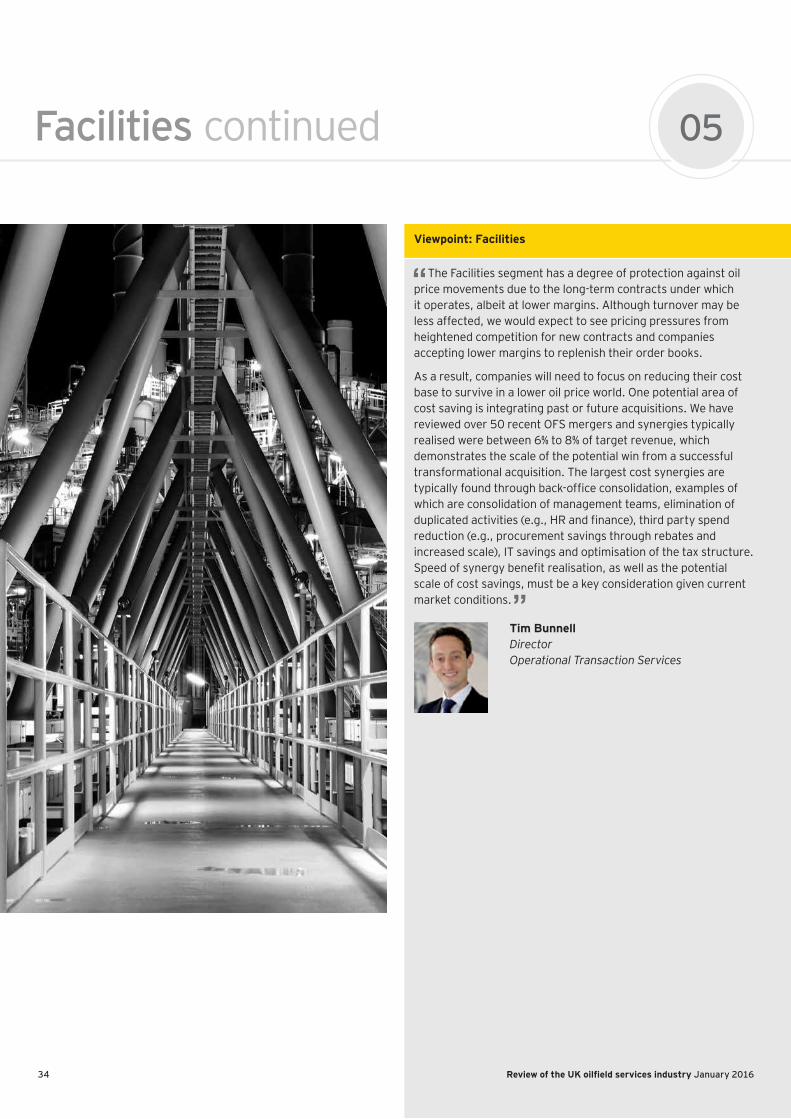

Key highlights of the Facilities supply chain category results ► Large construction works are typically carried out overseas,

usually in lower cost geographies. The UK companies in our analysis are typically involved in either an engineering role, construction of topside equipment including modules, or the operations and maintenance of the facilities.

► Turnover increased by £4.3 billion between 2008 and 2014 (CAGR 7%). We have identified 543 companies in this segment of the supply chain and in 2014, 425 companies generated turnover of less than £20 million. Companies with turnover in excess of £100 million, 32 in total, generated 60% of the total 2014 Facilities turnover.

► Turnover did not fluctuate significantly between 2008 and 2010 but there was a significant upturn in each of 2011, 2012 and 2013. There was an increase in activity in all sub-sectors in the Facilities supply chain but in particular from engineering, operation, maintenance and decommissioning contractors, driven by:

► Increased investment in the UKCS (2013 capital spend was the highest for more than three decades at £14.4 billion)

► Increase in UKCS brownfield activity in 2011 to 2013. As the UKCS is a mature region, substantial modifications and upgrades of installations are required by the ageing infrastructure to assist with extending the productive life of fields

► Operating expenditure rising from £7.0 billion in 2011 to £8.9 billion in 2013.

► Turnover growth in 2014 was minimal primarily due to: ► A reduction in activity in engineering, operation,

maintenance and decommissioning contractors as 2013 included a number of major projects that moved offshore and achieved first oil/gas in the second half of 2013 which were not repeated in 2014 and large construction projects coming to an end

► A reduction in activity in Specialist steels and tubulars due to Oil Country Tubular Goods (OCTG) demand declining in the UKCS and overseas due to the political situation in certain locations (e.g., Algeria and Egypt) offset by

► A large increase in activity levels for a number of specialist engineering services companies.

► EBITDA margin did not fluctuate significantly between 2008 and 2013 because a large number of the major players operate under multi-year contracts, which allows companies to manage their cost base in line with forecast activity levels. Wage increases were typically being passed on to the end customer in line with contractual terms. However, this also implies that the contractor pay cuts announced by a number of OFS companies in this supply chain category will also be passed on to the end customer.

► EBITDA margin declined by 2ppt in 2014 primarily as a result of the engineering, operation, maintenance and decommissioning contractors sub-sector EBITDA margin declining from 6.4% in 2013 to 0.7% in 2014. This was a result of a significant loss provision which had to be recorded in relation to a gas plant project in Shetland, construction of which is expected to be completed in 2015.

► The number of employees increased by over 8,800 between 2008 and 2014 and the average salary increased from £42,000 in 2008 to £50,000 in 2014 (CAGR 3%), There is a significant fluctuation between average salaries across the sub-sectors within Facilities, with employees involved in the more specialised niche sub-sectors typically receiving higher salaries. The number of employees increased by 2,500 from 2013 to 2014 against a backdrop of flat overall turnover.

32 Review of the UK oilfield services industry January 2016

Facilities continued

Geographic analysis of Facilities turnover

Figure 28: UK and export turnover 2008-14

0

2,000

4,000

6,000

8,000

10,000

2008 2009 2010 2011 2012 2013 2014

£mn

UK Exports

Figure 29: UK and export turnover CAGR 2008-14

0%

5%

10%

15%

Under£50mn

£50mnto £100mn

£100mnto £250mn

Over£250mn

UK Exports

► There was a significant upturn in UK turnover in 2011, 2012 and 2013 which resulted primarily from the engineering, operation, maintenance and decommissioning contractors sub-sector due to the increase in brownfield activity in the UKCS and the structure and topside design and fabrication sub-sector due to a number of large EPC contracts in the UKCS. There was minimal growth in 2014 as noted above due to large projects in 2013 not repeating.

► Export turnover increased year-on-year from 2008 to 2013, driven primarily by the machinery/plant design and manufacture and specialist engineering services sub-sectors as a result of targeted growth from overseas markets.

► Whereas engineering, operation, maintenance and decommissioning contractors (and related Tier 3 supporting sub-sectors) generate a large portion of turnover from both UKCS capital projects and long-term operations and maintenance contracts, machinery/plant design and manufacture companies service the global market, with over 50% of turnover in this sub-sector being from exports.

► As can be seen in Figure 29, there was significant export growth for companies with less than £50 million turnover. These companies (primarily in machinery/plant design and manufacture, engineering consultants, inspection services and specialist engineering services sub-sectors) tend to have specialised equipment or services and use this technical expertise to grow and expand by exporting into the global market. For companies with turnover between £100 million and £250 million in 2014, these also had significant export growth primarily driven by the growth and expansion within the specialist engineering services sub-sector.

Figure 27: Analysis of turnover between UK and exports

Currency: £ million 2008 2009 2010 2011 2012 2013 2014

UK 5,869 5,713 5,692 6,604 7,527 8,910 8,925

Exports 2,921 3,199 3,164 3,485 3,949 4,215 4,210

Turnover 8,790 8,912 8,855 10,089 11,475 13,125 13,135

Exports as percentage of turnover 33% 36% 36% 35% 34% 32% 32%

*where disclosed

33Review of the UK oilfield services industry January 2016

Key trends in Facilities

Figure 31: UKCS operating expenditure by region

0

5,000

10,000

15,000

20,000

25,000