Investor Presentation STS Group AG Investor Presentation ...

Upload

shivamnigam9Category

view

229download

1

June 2014 Investor Presenta2on

TSX: IRL AIM: MIRL BVL: MIRL

A Opportunity in La.n America

2

Forward Looking Statements This presenta,on is for informa,onal purposes only and may not be reproduced or distributed to any other person or published, in whole or in part, for any purpose. This presenta,on does not cons,tute an admission document, lis,ng par,culars, prospectus, offering memorandum or an offer to sell or a solicita,on to buy securi,es of Minera IRL Limited (the “Company”) and should not be relied on in connec,on with a decision to purchase or subscribe for any such securi,es. No reliance may be placed for any purpose whatsoever on the informa,on contained in this presenta,on or the completeness or accuracy of such informa,on. No representa,on or warranty, express or implied, is given by or on behalf of the Company nor advisors including, but not limited to, Canaccord Genuity Limited (“Canaccord Genuity”) nor their respec,ve shareholders, directors, officers or employees nor any other person as to the accuracy or completeness of the informa,on or opinions contained in the presenta,on. None of the Company or advisors shall be liable for any claims, expenses, damages (including direct, indirect, special or consequen,al damages), loss of profits, or opportuni,es arising from the use of or reliance on the informa,on contained in this presenta,on. The shares of the Company have not been and will not be registered under the United States Securi,es Act of 1933, as amended (“Securi,es Act”) or state securi,es laws and may not be offered or sold in the United States or to or for the account or benefit of U.S. persons (as such terms are defined in Regula,on S under the Securi,es Act) except pursuant to certain exemp,ons. The distribu,on of this presenta,on in certain jurisdic,ons may be restricted by law and therefore persons into whose possession this presenta,on comes should inform themselves about and observe any such restric,ons. Any such distribu,on could result in a viola,on of the law of such jurisdic,on. In par,cular, this presenta,on should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in par,cular, should not be distributed to persons with an address in the United States of America, Australia, the Republic of South Africa, the Republic of Ireland, Japan or in any other country outside the United Kingdom where such distribu,on may lead to a breach of any legal or regulatory requirement. Accordingly, subject to certain excep,ons, the shares of the Company may not, directly or indirectly, be offered or sold within Australia, Canada, Japan, South Africa or the Republic of Ireland or offered or sold to a resident of Australia, Japan, South Africa or the Republic of Ireland. This presenta,on is distributed in the United Kingdom only to persons who are approved persons or exempted persons within the meaning of the Financial Services and Markets Act 2000, or any Order made there under (including, without limita,on, persons falling within either ar,cle 19 (Investment Professionals) or ar,cle 49 (High Net Worth Companies) of the Financial Services and Markets Act 2000 (Financial Promo,on) Order 2005) and, if permi^ed by applicable law, for distribu,on outside the United Kingdom to professionals or ins,tu,ons whose ordinary business involves them engaging in investment ac,vi,es. It is not intended to be distributed or passed on, directly or indirectly, to any other class or persons in the United Kingdom and persons of any descrip,on other than as described in this paragraph should not rely or act upon this presenta,on and the accompanying verbal presenta,on. This presenta,on and its contents and accompanying verbal presenta,on are confiden,al and are being supplied to you solely for your informa,on and may not be reproduced, further distributed to any other person or published, in whole or in part, for any purpose. This Presenta,on may contain forward-‐looking statements rela,ng to the business and financial outlook of the Company which are based on the current expecta,ons, es,mates and projec,ons of the Company. When used in this Presenta,on, the words “an,cipate”, “expect”, “will”, “intend”, “es,mate”, “forecast”, “planned” and similar expressions are intended to iden,fy forward-‐looking statements or informa,on. Forward-‐looking statements include, but are not limited to, the es,mate of mineral reserves and resources, the ,ming and amount of es,mated future produc,on, costs and ,ming of development of new deposits, permi`ng ,me lines and expecta,ons regarding metal recovery rates. Forward-‐looking statements are necessarily based upon a number of es,mates and assump,ons that, while considered reasonable by management, are inherently subject to significant business, economic and compe,,ve uncertain,es and con,ngencies. The Company cau,ons that such forward-‐looking statements involve known and unknown risks, uncertain,es and other factors that may cause the actual financial results, performance or achievements of the Company to be materially different from its es,mated future results, performance or achievements expressed or implied by those forward-‐looking statements and the forward-‐looking statements are not guarantees of future performance. The Company does not intend and does not assume any obliga,on, to update or revise any forward-‐looking statements whether as a result of new informa,on, future events or otherwise, except as required by law. There can be no assurance that forward-‐looking statements will prove to be accurate, as actual results and future events could differ materially from those an,cipated in such statements. Accordingly, readers should not place undue reliance on forward-‐looking statements due to the inherent uncertainty therein. Canaccord Genuity, which is authorised and regulated by the Financial Services Authority, is advising the Company and will not be responsible to anyone other than the Company for providing the protec,ons afforded to customers of Canaccord Genuity. Any other person should seek their own independent legal, investment and tax advice as they see fit. Canaccord Genuity’s responsibili,es as the Company’s Nominated Adviser under the AIM Rules will be owed solely to the London Stock Exchange plc and not to the Company, to any of its directors or any other person in respect of a decision to subscribe for or acquire shares or other securi,es in the Company. Canaccord Genuity has not authorised the contents of, or any part of, the Presenta,on and no representa,on or warranty, express or implied, is made by it as to any of its contents.

3

A PorDolio of Golden Opportuni2es

Corihuarmi Mine

2013A: 25k oz Au 2014E: 21k oz Au Open pit mining

Heap leach Explora2on Upside

Production Developing Mines Exploration

The Cash Generator Flagship Project

Addi2onal Upside

Ollachea Project

Es2mate 100k oz pa over first 9 years of produc2on Underground mining

CIL 10.6m tonnes @ 4.0g/t Feasibility Complete Explora2on Upside

Don Nicolas JV

Es2mate 26k oz Au pa (net) Open pit mining

CIL 1.2m tonnes @ 5.1g/t Fully Permiaed Project Explora2on Upside

First Produc2on in Q2 2015

PorDolio

Escondido Michelle Chispas Bethania Quilavira Cecilia

Paula Andrea Goleta

Microondas Frontera JV Huaquirca JV

Deseado Massif

Drill program underway to extend

mine life Construc2on Permit expected in June 2014

Our Next Mine

Construc2on underway

& fully funded

4

2014 Corporate Strategy

u Permit and finance the Ollachea Mine ² ESIA is approved, Construc,on Permit expected in June 2014 ² Goal of arranging project financing in June 2014

u Complete construc2on of Don Nicolas Mine joint venture (51%) ² $80 million of construc,on financing in place ² Project development underway ² Commission mill in Q1 2015 ² First produc,on expected in Q2 2015

u Extend the life of the Corihuarmi Mine again ² Cayhua Ridge and Ely expected to extend mine life beyond late 2015 ² Other near-‐mine explora,on opportuni,es

u Maintain financial discipline while pursuing mine financing ² Limit discre,onary spending during permi`ng and financing phases

5

* Resident of Perú + Resident of South America

Diego Benavides* President Minera IRL SA Corporate lawyer with Peruvian mining experience in legal and business transac,ons

Courtney Chamberlain* Execu6ve Chairman Metallurgical Engineer with more than 45 years of worldwide mining experience in senior execu,ve posi,ons

Donald McIver* VP Explora6on Geologist with 28 years experience in Africa and La,n America

Trish Kent* Internal Consultant Interna,onal experience in public, investor and community rela,ons

Francis O’Kelly+ Internal Consultant Mining engineer with more than 40 years experience in mining and banking in the Americas

Bill Hogg VP Project Development Mechanical engineer and project manager with more than 36 years professional experience, specializing in gold leach projects

John Velásquez* General Manager Corihuarmi Gold Mine Process engineer, 22 years experience in Peru’s mining industry

Stuart Smith Technical Manager Metallurgical engineer, specializing in gold extrac,ve technologies, with more than 24 years of worldwide experience

Brad Boland Chief Financial Officer More than 16 years of interna,onal financial experience in resource industries

Page 5

An Experienced Management Team

6

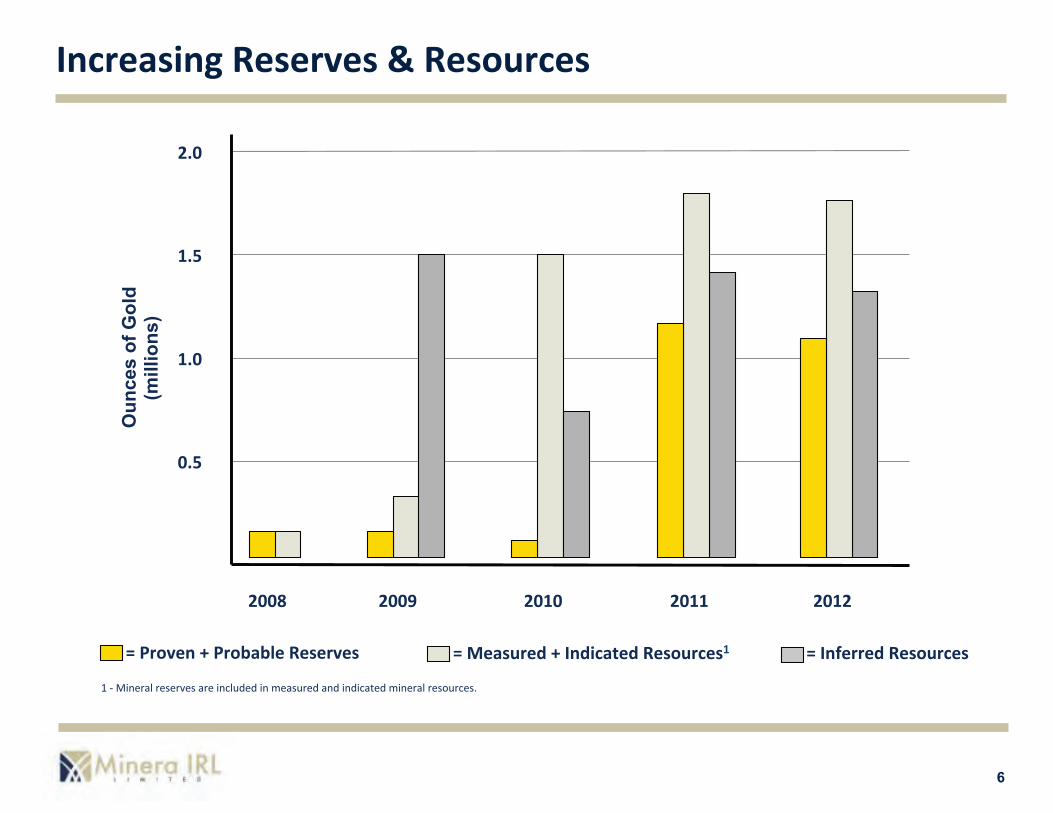

Increasing Reserves & Resources

= Measured + Indicated Resources1 = Inferred Resources = Proven + Probable Reserves

2008 2009 2010

0.5

1.0

1.5

2.0 O

unce

s of

Gol

d

(mill

ions

)

2011 2012

1 -‐ Mineral reserves are included in measured and indicated mineral resources.

7

La2n American Countries with a History of Mining

Ollachea Development Project (95%) (Arranging Financing)

Don Nicolas Development Project (51%) (Development in Progress)

Corihuarmi Gold Mine (100%)

8

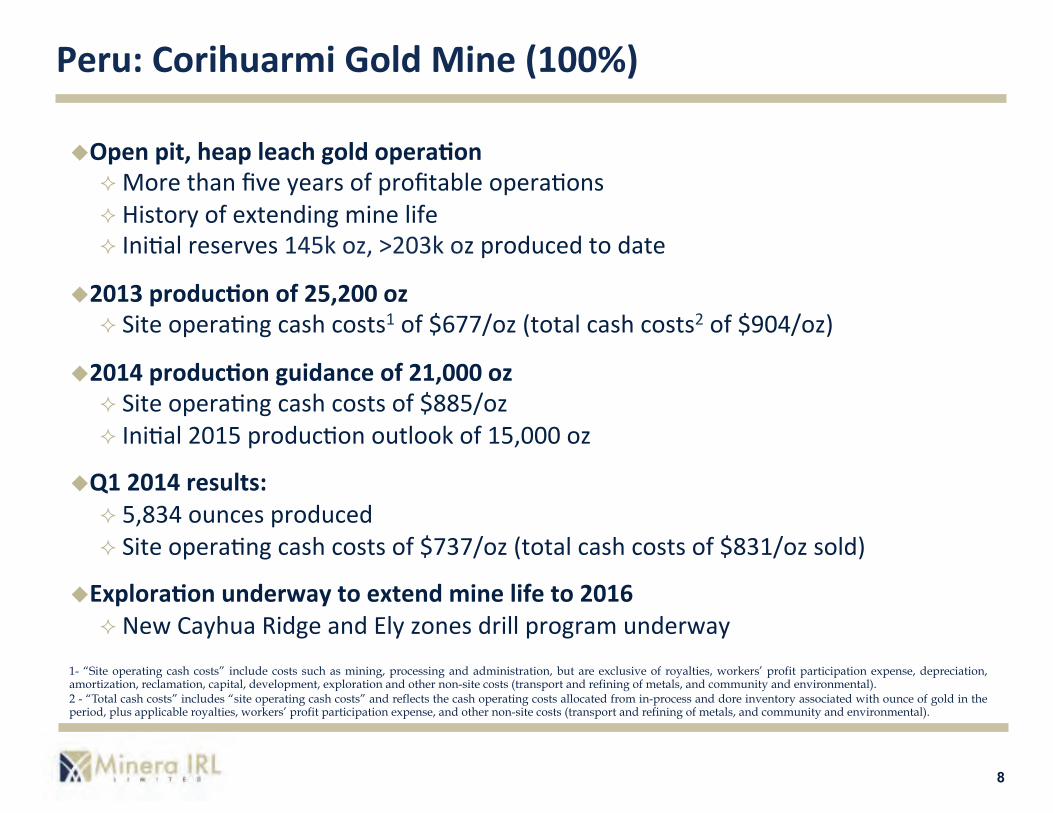

u Open pit, heap leach gold opera2on ² More than five years of profitable opera,ons ² History of extending mine life ² Ini,al reserves 145k oz, >203k oz produced to date

u 2013 produc2on of 25,200 oz ² Site opera,ng cash costs1 of $677/oz (total cash costs2 of $904/oz)

u 2014 produc2on guidance of 21,000 oz ² Site opera,ng cash costs of $885/oz ² Ini,al 2015 produc,on outlook of 15,000 oz

u Q1 2014 results: ² 5,834 ounces produced ² Site opera,ng cash costs of $737/oz (total cash costs of $831/oz sold)

u Explora2on underway to extend mine life to 2016 ² New Cayhua Ridge and Ely zones drill program underway

Peru: Corihuarmi Gold Mine (100%)

1- “Site operating cash costs” include costs such as mining, processing and administration, but are exclusive of royalties, workers’ profit participation expense, depreciation, amortization, reclamation, capital, development, exploration and other non-site costs (transport and refining of metals, and community and environmental). 2 - “Total cash costs” includes “site operating cash costs” and reflects the cash operating costs allocated from in-process and dore inventory associated with ounce of gold in the period, plus applicable royalties, workers’ profit participation expense, and other non-site costs (transport and refining of metals, and community and environmental).

9

Current produc,on

Produc,on

Expansion

Explora,on

Corihuarmi: Classic High Sulphida,on Epithermal System

10

ZONES OF EXPLORATION AND ZONES TO EXPLORE

CAYHUA RIDGE AREA

ELY

LAURA SUSAN PIT

DIANA PIT

DIANA EAST

CAYHUA SOUTH

N

New Explora2on Areas

Recent Explora2on Areas

Current Produc2on Areas

SCREE SLOPE

CAYHUA

DIANA & ELY PITS

EXTENSION

Corihuarmi: Produc2on and Explora2on Areas

11

u The Company’s flagship project and next mine in Peru ² Government approval of ESIA received in Q3 2013 ² Defini,ve Feasibility Study Op,miza,on completed in May 2014 ² Construc,on Permit expected in Q2 2014

u Robust Project Economics ² Average annual produc,on of more than 100,000 ounces during the first 9 years ² First quar,le low cash costs and manageable capex of $165 million

u Key Infrastructure In-‐place ² Paved highways, grid power, ports, airports, and a skilled workforce

u Strong Community Support ² 30-‐year surface rights agreement in place

u Significant Explora2on Upside ² DFS only considers the Minapampa Zone ² Concurayoc Zone hosts an inferred mineral resource of 0.9 million ounces ² Recent 320m drilling step-‐out confirmed on-‐strike and down dip poten,al

Peru: Ollachea Gold Project

1 – Based upon the November 29, 2012 Defini,ve Feasibility Study Technical Report

12

Ollachea: Key Infrastructure in Place

² Interoceanic Highway

² Grid power ($0.067 kW/h)

² Abundant water supply

² Skilled local workforce

² Modern telecommunica,ons

² Comfortable al,tude

² Established camp

² Matarani deep water port

² Lima’s Callao Bay deep water port

² Juliaca’s domes,c airport

² Lima’s interna,onal airport

13

Ollachea: Key Infrastructure in Place

Exis2ng 138 kV

power line

View overlooking the Minapampa outcrop and the loca2on of future upper mine facili2es

Minapampa ore body outcrop

Future plant loca2on behind ridge

14

Ollachea: Excellent Facili2es

15 Page 15

Ollachea: Strong Community Support

u Community of Ollachea is our partner: ² Strong community support ² 30-‐year surface rights agreement ² 5% par,cipa,ng interest in the mine

upon commercial produc,on

u Ollachea is the only community within the “area of direct influence” : ² Streamlines the permi`ng process

16

Ollachea: A Large Open-‐ended Orogenic Gold System

Community of Ollachea

Future Plant

Facili2es

Historical and recent explora2on results con2nue to demonstrate on-‐strike and down-‐dip poten2al

Mineralized Trend

Ore-‐grade Intercepts

1.2 km Explora2on Tunnel

Mineral Resources

LEGEND

Regional Fault trace

?

?

Minapampa

1.4M oz (M&I)

+0.3M oz (Inf)

17

Ollachea: Drilling Demonstrates Explora2on Upside

5.45 g/t Au over 9m

N

5.47 g/t Au over 11m

S

4.48 g/t Au over 20m

Minapampa Zone

Concurayoc Zone

1.2km “explora.on” tunnel

320 m step out

18

Ollachea: DFS Op2miza2on Highlights

u Completed in November 2012 by AMEC and Coffey Mining u Total gold produc2on: 930,000 ounces

² Average annual produc,on over 100,000 ounces for first 9 years ² Significant mine life extension poten,al iden,fied

u Average total cash cost of $587 per ounce1 ² A low-‐cost producer ² Pay back period of 3.7 years (aser tax)

u Sustaining total cash opera2ng cost of $646 per ounce2 ² Sustaining and closure costs of $51million over life of mine ($59 per ounce)

u Low ini2al capital cost of $165 million ($177 per ounce) ² Financeable for a junior

u Significant explora2on upside ² Recent explora,on results con,nue to demonstrate on-‐strike and down dip mineral

resource expansion poten,al

1 – As per the 4 June 2014 MIRL press release ,tled “Minera IRL Reports Posi,ve Ollachea Project Op,miza,on Results”. Also excludes the 1% gross revenue royalty due to Macquarie Bank. 2 – “Sustaining Total Cash Costs” are defined as “Total Cash Costs” plus “Sustaining Capital and Mine Closure” costs.

19

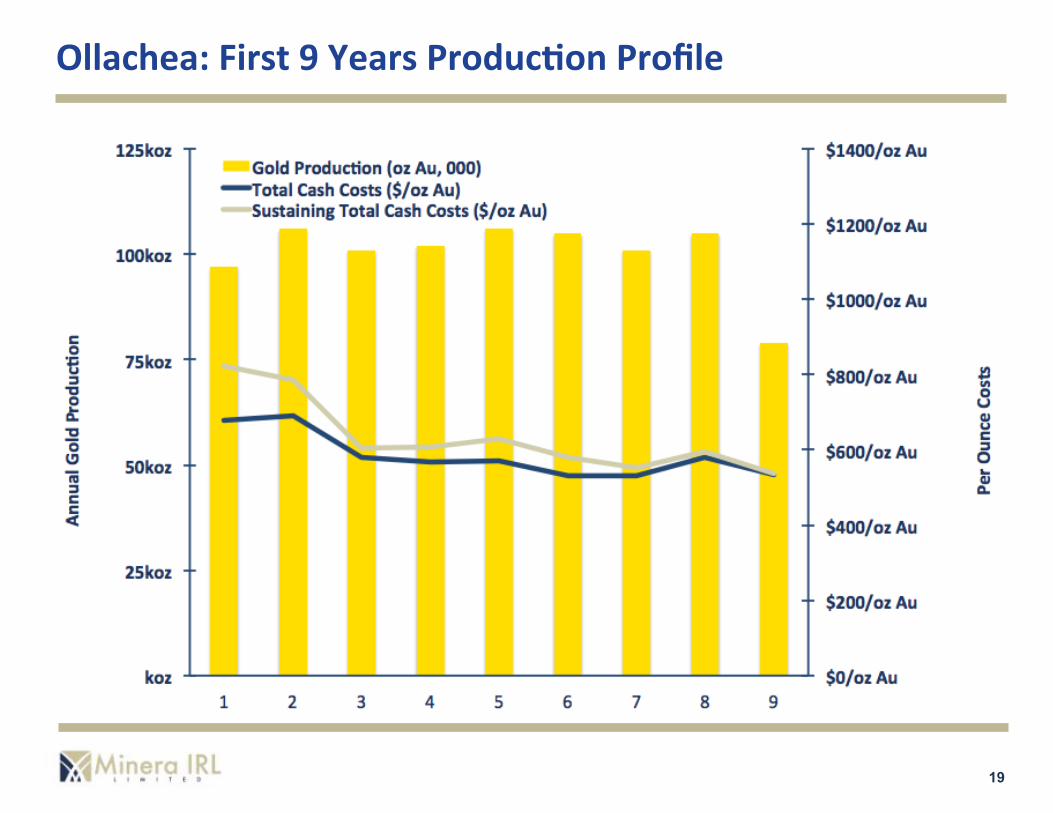

Ollachea: First 9 Years Produc4on Profile

20

Ollachea: Aver-‐Tax NPV1 (millions)

Discount Gold Price ($/oz)

Rate $1,100 $1,200 $1,300 $1,400 $1,500

0% $231 $289 $344 $399 $453

5% $135 $177 $218 $259 $299

7% $107 $144 $181 $217 $253

10% $72 $104 $135 $166 $197

IRR 20% 24% 28% 32% 35%

Payback 4.0 3.4 3.1 2.7 2.4

1 – Based upon the November 29, 2012 Technical Report that was op,mized and reported on 4 June 2014. Assumes a 100% equity basis and no considera,on has been provided for the Community of Ollachea’s 5% equity interest (to be earned upon commercial produc,on), the 1% gross revenue royalty due to Macquarie Bank, the final payment of $16 million to Rio Tinto for the purchase of Ollachea that is due in mid-‐2016, further project op,miza,on opportuni,es, or for mineral resources outside of the Minapampa Zone.

21

Ollachea: Expected Timeline to Produc2on

2010 2011 2012 2013 2014 2015

In-‐fill & Extension Drilling

Pre-‐Feasibility Study

30-‐year Surface Agreement

Defini2ve Feasibility Study

“Explora2on” Drive (1.2km)

ESIA Report Prepara2on

Final Public Review of ESIA

ESIA Review Period

ESIA Approval

Construc2on Financing

Construc2on Permiwng

Mine Construc2on

Produc2on

✓ ✓ ✓ ✓ ✓ ✓

✓ ✓

✓

22

Ollachea Financing Opportuni2es

u Senior Project Debt Facility ² Term sheet received for up to $120 million (inclusive of exis,ng debt facili,es) ² Nego,a,ons expected to be concluded in Q2 2014

u Mezzanine Debt ² Subordinate to senior debt

u Sale of Produc2on Royalty ² Upfront cash payment

u Precious Metals Stream ² Upfront cash payment plus ongoing cash payments ,ed to produc,on

u Strategic or Joint Venture Partner ² Up to a 49% interest

u Off take agreement ² Cash or debt in exchange for a selling gold at a slight discount to spot

u Gold Loan ² Credit agreement that is repaid from produc,on

u Equity ² Expected to be the last piece of the financing strategy

23

u Santa Cruz has always been a mining-‐friendly jurisdic2on ² Several precious metals mines in opera,on, others under development

u The project is under construc2on now ² Construc,on commenced in Q1 2014 ² Construc,on planned to be complete in Q1 2015 ² First produc,on expected in Q2 2015

u The project is fully financed by joint venture partner ² $45 million in common and preferred equity, $35 million bridge loan facility

u Strong community support ² 10-‐year Social License Agreement with the communi,es of Jaramillo and Fitzroy

u Robust project economics ² Simple open-‐pit mining with low opera,ng costs and mine capex

u Key infrastructure in place ² Paved roads, airports, gas pipeline, and water

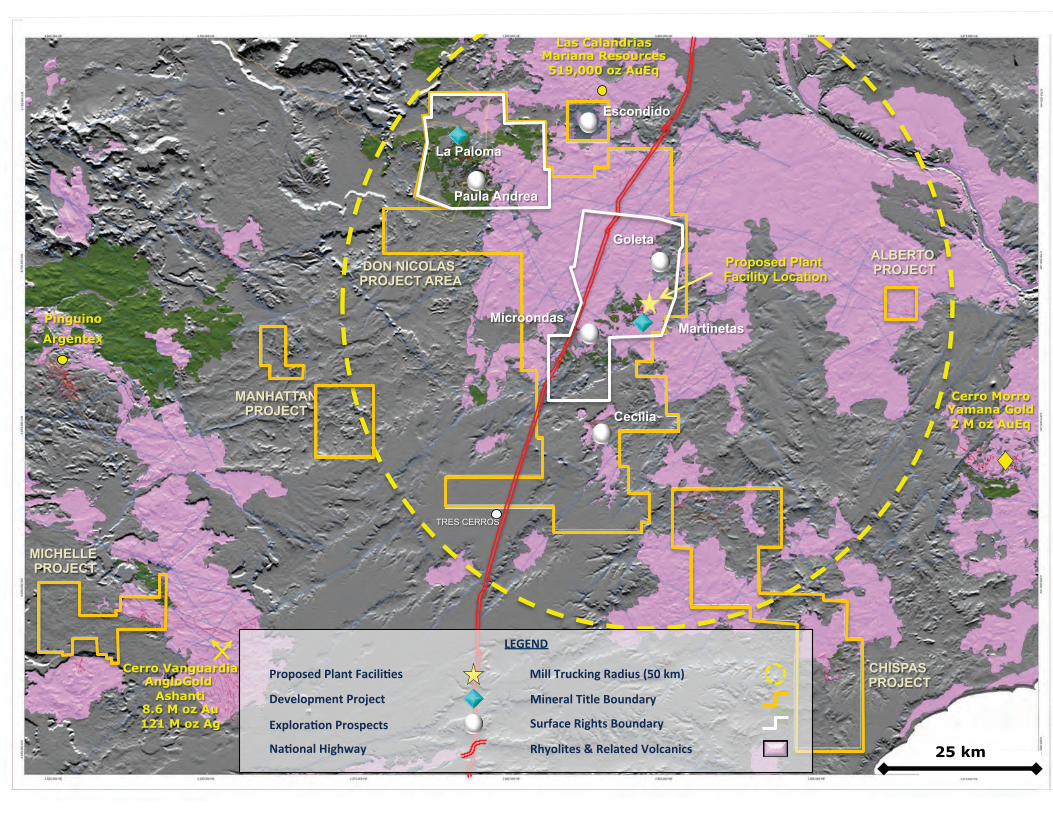

u Large 2,583 km2 explora2on package on Deseado Massif

Argen2na: Don Nicolas Gold Project (51% ownership)

25 25 km

TRES CERROS

DON NICOLAS PROJECT AREA

MICHELLE PROJECT

CHISPAS PROJECT

ALBERTO PROJECT

MANHATTAN PROJECT

Pinguino

Argentex

Las Calandrias Mariana Resources 519,000 oz AuEq

Cerro Vanguardia AngloGold

Ashanti 8.6 M oz Au 121 M oz Ag

La Paloma

Martinetas

Cecilia

Paula Andrea

Proposed Plant Facility Location

LEGEND

Na2onal Highway

Mill Trucking Radius (50 km)

Rhyolites & Related Volcanics

Mineral Title Boundary

Surface Rights Boundary

Development Project

Explora2on Prospects

Proposed Plant Facili2es

Escondido

Goleta

Microondas

Cerro Morro Yamana Gold 2 M oz AuEq

26

Don Nicolas: Defini2ve Feasibility Study Highlights

u Completed in February 2012 by Tetra Tech u Total gold produc2on: 181,000 ounces (90,500 ounces net)

² Average annual gold produc,on of 52,400 ounces (26,200 net ounces) ² Aser-‐tax IRR of 23% and NPV1 of $22 million ² Ini,al mine life of 3.6 years, significant mine life extension poten,al ² Reserves represent only 42% of measured and indicated resources

u Average total cash cost of $578 per ounce1 ² A low-‐cost producer, rapid 2-‐year payback period

u Sustaining total cash opera2ng cost of $640 per ounce2 ² Sustaining capital cost of $7.3 million over life of mine ($40 per ounce) ² Closure costs of of $4.0 million ($22 per ounce)

u Low ini2al capital cost of $56 million ($306 per ounce) ² Construc,on capital provided by joint venture partner

u Substan2al upside through engineering and explora2on ² Evalua,ng the economics of an accompanying heap leach opera,on ² 2,583 km2 prospec,ve land package with several high-‐priority drill targets

1 – Based upon February 14, 2012 Technical Report u,lizing a gold price of $1,250 per ounce and a silver price of $25 per ounce. Assumes 100% ownership and 100% equity financing.

27

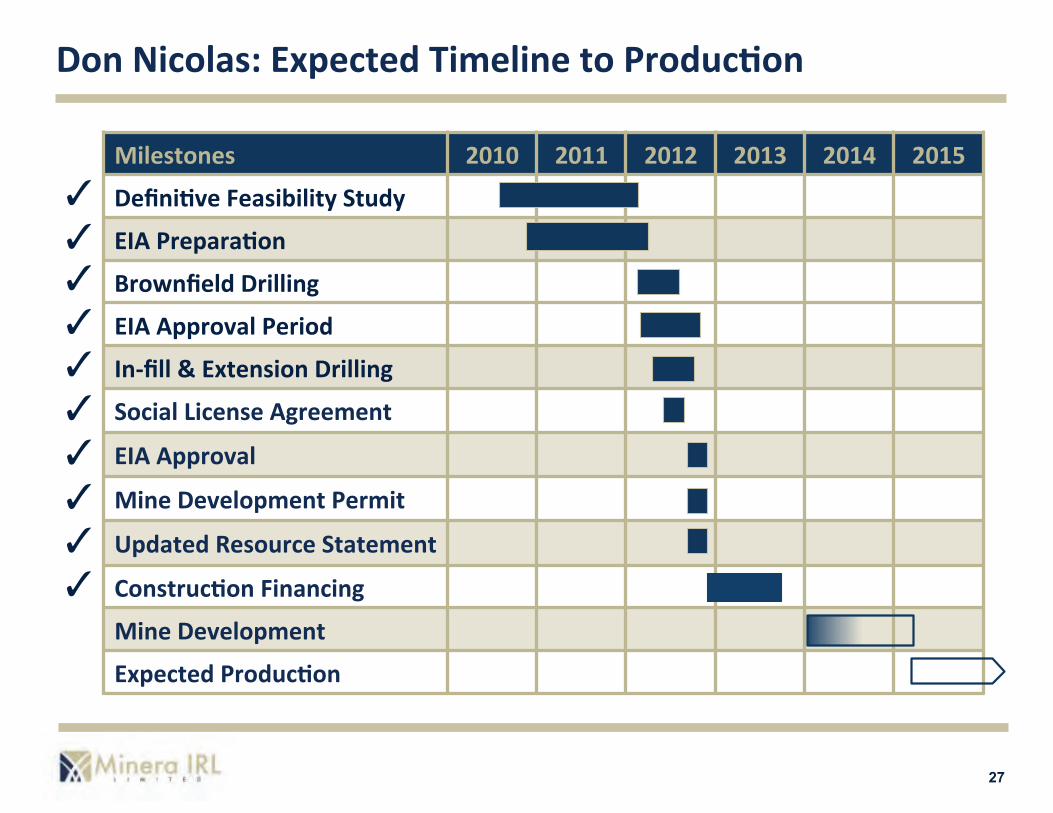

Don Nicolas: Expected Timeline to Produc2on

Milestones 2010 2011 2012 2013 2014 2015

Defini2ve Feasibility Study

EIA Prepara2on

Brownfield Drilling

EIA Approval Period

In-‐fill & Extension Drilling

Social License Agreement

EIA Approval

Mine Development Permit

Updated Resource Statement

Construc2on Financing

Mine Development

Expected Produc2on

✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

28

Financial Posi2on and Capital Structure

Shares Outstanding1 228,868,605 Stock Op2on Plan2 Debt Facility Op2ons3

12,170,000 18,786,525

Fully Diluted 259,825,130

Recent Share Price C$0.17 Market Capitaliza2on C$39 million

Cash & Equivalents4 ~US$6.4 million Debt Facility1,5 US$30 million

1 – As at 31 March 2014 2 – The weighted-‐average strike price is £0.668 per share purchase op,on 3 – The weighted-‐average strike price is US$1.06 per share purchase op,on 4 – As at 31 March 2013 5 – The Macquarie Debt Facility is currently fully drawn and matures on 30 June 2014

29

Appendix: Equity Research and Major Shareholders

Mineral IRL is formally covered by the equity research analysts listed above. Any opinions, es=mates, or forecasts regarding Minera IRL’s performance made by these analysts are theirs alone and do not represent opinions, forecasts, or predic=ons of Minera IRL or its management. Minera IRL does not by its reference above, or distribu=on, imply its endorsement of or concurrence with such informa=on, conclusions, or recommenda=ons.

19.3%&8.7%&

4.0%&3.4%&3.0%&3.0%&

2.5%&2.1%&2.0%&

Rio&Tinto&Miton&Asset&Management&

CIMINAS&MIRL&ExecuCve&Team&

RBC&Global&Asset&Management&Fratelli&Investments&Macquarie&Group&

Shairco&Black&Rock&Investment&Management&

Dmitry Kalachev Michael Parkin Mar@n PoAs

Peter Rose Humberto León Cailey Barker

30

A PorDolio of Golden Opportuni2es

Corihuarmi Mine

2013A: 24k oz Au 2014E: 21k oz Au Open pit mining

Heap leach Explora2on Upside

Production Developing Mines Exploration

The Cash Generator Flagship Project

Addi2onal Upside

Ollachea Project

Es2mate 100k oz pa over first 9 years of produc2on Underground mining

CIL 10.6m tonnes @ 4.0g/t Feasibility Complete Explora2on Upside

Don Nicolas JV

Es2mate 26k oz Au pa (net) Open pit mining

CIL 1.2m tonnes @ 5.1g/t Fully Permiaed Project Explora2on Upside

First produc2on in Q2 2015

PorDolio

Escondido Michelle Chispas Bethania Quilavira Cecilia

Paula Andrea Goleta

Microondas Frontera JV Huaquirca JV

Deseado Massif

Construc2on Permit expected in June 2014

Our Next Mine

Construc2on underway

& 100% funded

Drill program underway to extend

mine life

31

Ollachea DFS Op2miza2on Summary ($1,300 Au)

Item $M1

Mining Site Development Process Plant Ancillary Buildings Tailings System Indirect and Owners Cost Con,ngency

43.7 3.9

58.4 3.9 5.7

31.4 17.6

Ini2al Project Capital 164.7

Sustaining Capital Closure Costs

51.1 4.2

Total LOM Capital Cost 220.0

Capital Cost Breakdown

Item $/t Ore1 $/oz1,2

Mining Processing Site G&A

$23.5/t $21.5/t $4.3/t

$243/oz $222/oz $44/oz

Site Cash Opera2ng Costs3 $49.3/t $509/oz

Royal,es, Taxes, Selling Costs $78/oz

Total Cash Costs4 $587/oz

Sustaining and Closure Costs $59/oz

Sustaining Total Cash Costs5 $646/oz

Ini,al Project Capital $177/oz

Total Project Cash Costs6 $823/oz

Operating Cost Breakdown

1 -‐ Costs are in Q3 2012 millions of US dollars, except for unit costs which are in US dollars. Assumes US$1,300 per ounce gold price. 2 -‐ Some amounts may not compute due to the effects of rounding or trunca,on. Per ounce amounts are derived by dividing the gross amount for each item by the total number of ounces expected to be produced in the Ollachea DFS. 3 -‐ “Site opera,ng cash costs” include costs such as mining, processing and administra,on, but are exclusive of royal,es, workers’ profit par,cipa,on cost, deprecia,on, amor,za,on, reclama,on, capital, development, explora,on and other non-‐site costs (transport and refining of metals, and community and environmental). 4 -‐ “Total cash costs” includes “site opera,ng cash costs” and reflects the cash opera,ng costs allocated from in-‐process and dore inventory associated with ounce of gold in the period, plus applicable royal,es, workers’ profit par,cipa,on cost, and other non-‐site costs (transport and refining of metals, and community and environmental). This amount excludes the 1% gross revenue royalty due to Macquarie Bank. 5 -‐ “Sustaining Total Cash Costs” are defined as “Total Cash Costs” plus “Sustaining Capital and Mine Closure” costs. 6 – “Total Project Cash Costs” are defined as “Sustaining Total Cash Costs” plus “Ini,al Project Capital”. This measure excludes all sunk costs.

32

Ollachea: Permiwng Process and Progress

Baseline Studies Feasibility Study Impact Analysis & Management Plan

Submission of ESIA Report (December 2012)

ESIA Approval Received (September 2013)

Construc2on Permit Expected in June 2014

✓

Complete ESIA Document Components

1st Official Community Workshop

(February 2012)

2nd Official Community Workshop

(November 2012)

Final Community Workshop (May 2013)

✓ ✓ ✓ ✓ ✓

✓

✓

Public Par,cipa,on Plan Execu,ve Summary Completed Document

✓

✓

✓

✓

33

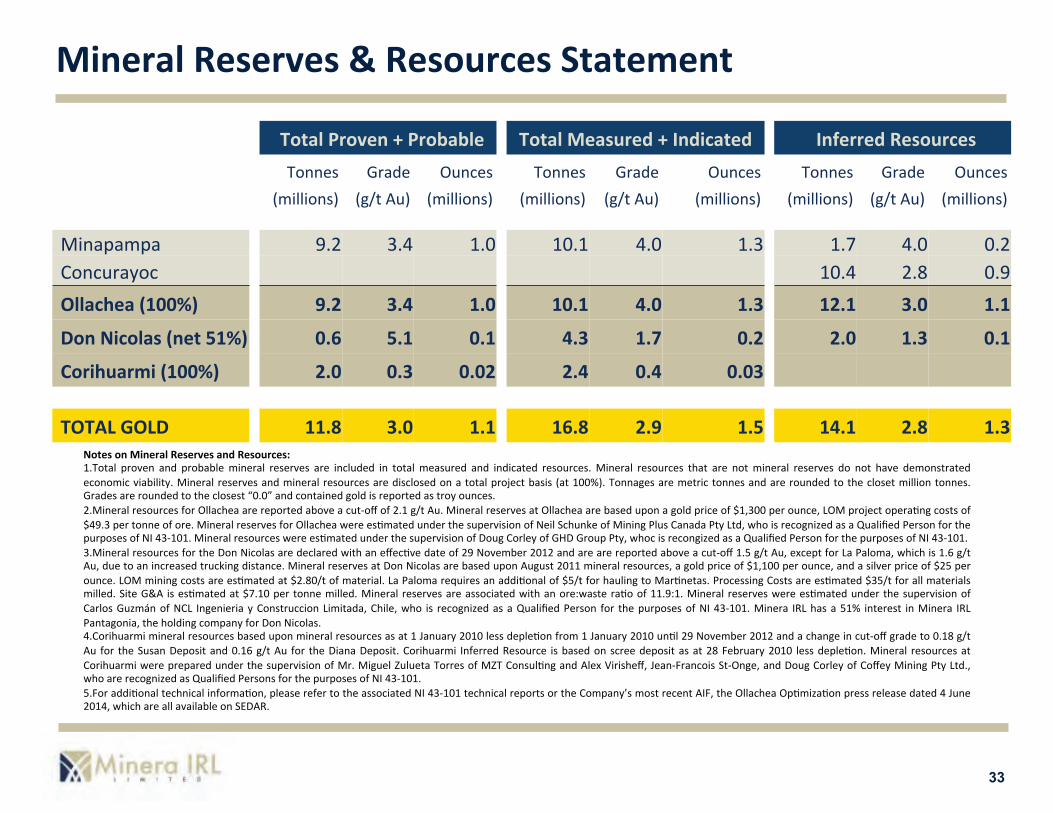

Mineral Reserves & Resources Statement

Total Proven + Probable Total Measured + Indicated Inferred Resources Tonnes Grade Ounces Tonnes Grade Ounces Tonnes Grade Ounces

(millions) (g/t Au) (millions) (millions) (g/t Au) (millions) (millions) (g/t Au) (millions)

Minapampa 9.2 3.4 1.0 10.1 4.0 1.3 1.7 4.0 0.2 Concurayoc 10.4 2.8 0.9 Ollachea (100%) 9.2 3.4 1.0 10.1 4.0 1.3 12.1 3.0 1.1

Don Nicolas (net 51%) 0.6 5.1 0.1 4.3 1.7 0.2 2.0 1.3 0.1

Corihuarmi (100%) 2.0 0.3 0.02 2.4 0.4 0.03

TOTAL GOLD 11.8 3.0 1.1 16.8 2.9 1.5 14.1 2.8 1.3 Notes on Mineral Reserves and Resources: 1. Total proven and probable mineral reserves are included in total measured and indicated resources. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Mineral reserves and mineral resources are disclosed on a total project basis (at 100%). Tonnages are metric tonnes and are rounded to the closet million tonnes. Grades are rounded to the closest “0.0” and contained gold is reported as troy ounces. 2. Mineral resources for Ollachea are reported above a cut-‐off of 2.1 g/t Au. Mineral reserves at Ollachea are based upon a gold price of $1,300 per ounce, LOM project opera,ng costs of $49.3 per tonne of ore. Mineral reserves for Ollachea were es,mated under the supervision of Neil Schunke of Mining Plus Canada Pty Ltd, who is recognized as a Qualified Person for the purposes of NI 43-‐101. Mineral resources were es,mated under the supervision of Doug Corley of GHD Group Pty, whoc is recongized as a Qualified Person for the purposes of NI 43-‐101. 3. Mineral resources for the Don Nicolas are declared with an effec,ve date of 29 November 2012 and are are reported above a cut-‐off 1.5 g/t Au, except for La Paloma, which is 1.6 g/t Au, due to an increased trucking distance. Mineral reserves at Don Nicolas are based upon August 2011 mineral resources, a gold price of $1,100 per ounce, and a silver price of $25 per ounce. LOM mining costs are es,mated at $2.80/t of material. La Paloma requires an addi,onal of $5/t for hauling to Mar,netas. Processing Costs are es,mated $35/t for all materials milled. Site G&A is es,mated at $7.10 per tonne milled. Mineral reserves are associated with an ore:waste ra,o of 11.9:1. Mineral reserves were es,mated under the supervision of Carlos Guzmán of NCL Ingenieria y Construccion Limitada, Chile, who is recognized as a Qualified Person for the purposes of NI 43-‐101. Minera IRL has a 51% interest in Minera IRL Pantagonia, the holding company for Don Nicolas. 4. Corihuarmi mineral resources based upon mineral resources as at 1 January 2010 less deple,on from 1 January 2010 un,l 29 November 2012 and a change in cut-‐off grade to 0.18 g/t Au for the Susan Deposit and 0.16 g/t Au for the Diana Deposit. Corihuarmi Inferred Resource is based on scree deposit as at 28 February 2010 less deple,on. Mineral resources at Corihuarmi were prepared under the supervision of Mr. Miguel Zulueta Torres of MZT Consul,ng and Alex Virisheff, Jean-‐Francois St-‐Onge, and Doug Corley of Coffey Mining Pty Ltd., who are recognized as Qualified Persons for the purposes of NI 43-‐101. 5. For addi,onal technical informa,on, please refer to the associated NI 43-‐101 technical reports or the Company’s most recent AIF, the Ollachea Op,miza,on press release dated 4 June 2014, which are all available on SEDAR.

34

For addi2onal informa2on, please contact: Brad Boland

Chief Financial Officer Tel: +1 (416) 907-‐7363

Jeremy Link Business Development Tel: +1 (416) 907-‐7363 [email protected]