Mike Poteshman EVP & CFO - Tupperware...

41

Mike Poteshman EVP & CFO September 2015

Transcript of Mike Poteshman EVP & CFO - Tupperware...

Mike Poteshman

EVP & CFO

September 2015

2

FORWARD LOOKING STATEMENTS

We are making some forward looking statements today that use words

like “outlook” or “target” or similar predictive words. Such forward

looking statements involve risks and uncertainties detailed in our recent

periodic reports as filed in accordance with the Securities and

Exchange Act of 1934. These risks and uncertainties may cause actual

results to differ materially from our statements today.

Visit www.tupperwarebrands.com or download our Investor Relations app

3

THIRD QUARTER 2015 SALES UPDATE*

Trending toward the high-end of the +4 to +6% local currency sales increase range

Seeing expected sequential improvement in Indonesia, France and Italy

Continued strong year-over-year growth in Argentina, Brazil, China, Tupperware Mexico and South Africa

*As of September 2, 2015

WHY INVEST

Our Business Model

is our Competitive

Advantage

Opportunities for

Above Average

Growth

Diversified Portfolio

for Sustainable

Performance

Significant

Return of Capital to

Shareholders

WE’RE A MULTI-LOCAL BUSINESS

Approx. 3,700 Unit Managers

Approx. 61,000 Demonstrators

Belgium Manufacturing & Warehouse

Tours Manufacturing

Tupperware Germany

Est. 1962

Headquarters in Frankfurt/Main

Logistics center in Eppertshausen

128 Distributors

Each controls a specific geography

Approximately 260 Team Leaders

Average German

Distributor has about

2 Team Leaders

(Sub-Distributors)

30 Managers

475 Consultants

Sales by Distributor

varies by geography

DISTRIBUTOR STRUCTURE GERMANY

6

Our BusinessModel

ASPIRATIONAL BRAND &

INCREDIBLE PRODUCTS

GPS (DEMONSTRATION)

SOLID BUSINESS FUNDAMENTALS

OPPORTUNITY

8

POWER OF OUR BRAND

The well known, aspirational Tupperware

brand along with the channel is powerful

because:

• Relatively low product line competition

• In our category, low channel competition

• Allows maintenance of a strong gross

margin along with innovation & unique

features & benefits

• Ability to sell flanker & subcategories

INNOVATIVE & DEMONSTRABLE PRODUCT

COOKWARE &

CUTLERY

BAKING &

OVENWARE

KITCHEN

TOOLS &

GADGETS

MICROWAVE

WATER &

ON THE GO

TABLETOP &

SERVING KITCHEN

PREP

FOOD CONSERVATION

Approximately

25% of Sales

each year

comes from

new products

introduced in

the last two

years

Around

100 new

concepts

normally in the

innovation

pipeline

9

Allows High

Price Point

Selling

Creates

Edutainment

Demonstration

unlocks

F & B

RELATIONSHIP-BASED SELLING THE POWER OF THE DEMONSTRATION

A group selling situation or party is

held every

1.3 sec

Rent Advertising

Personal Sales Opportunity Career Opportunity

11

Part-time

Extra Income

Full-time

Career

Demonstrator

Unit Manager

Team Leader (Sub-Distributor)

Distributor

REAL & COMPELLING SALES FORCE OPPORTUNITY

RECRUIT

TRAIN

MOTIVATE

CONTACT

COMPETITION

RECOGNITION

ENABLING SUCCESS THROUGH DIRECT TO CONSUMER FUNDAMENTALS

13

OUR BUSINESS MODEL OFTEN OFFSETS NEGATIVE EXTERNALS

• Earnings Opportunity resonates in a softer

employment environment

Unemployment

• Predominately a Push versus a Pull

business

• Messages through our Sales Force around

saving money -- tips to avoid food

waste/spoilage, promote cook at home, store

bulk purchases

Difficult

Consumer Spending

Environment

• We own the shelf

• Price with consumer inflation Inflation

28%

33% 13%

11%

15% 36%

20%

15%

24%

5%

14

2014 SEGMENT SALES AS % OF TOTAL

DIVERSIFIED GLOBAL PORTFOLIO

2006 SEGMENT SALES AS % OF TOTAL

Emerging Markets 44% of Sales Emerging Markets: 66% of Sales, 12.7% CAGR*

Established Market: 34% of Sales, (1.6)% CAGR*

*CAGR from 2006 to 2014

15

NINE MARKETS OVER $100M

Brazil

Fuller Mexico

Indonesia

$200M +

China

France

Germany

Malaysia & Singapore

TW Mexico

TW U.S. & Canada

$100M +

DIVERSIFIED GLOBAL PORTFOLIO

16

Key Sales & Profit Currencies

• Euro

• Indonesian rupiah

• Mexican peso

• Brazilian real

• Malaysian ringgit

• Chinese renminbi

92% of 2014 sales and 100% of net

profit from outside the U.S.

First

Tie

r

Second

Tie

r BASKET OF GLOBAL CURRENCIES

• Home to 85% of the world’s population & 66% of sales in 2014

• Growing Middle Class

• Lower Employment of Women outside the home

• Direct Sales Channel Growth of 4-5% annually through 2019*

17

GROWTH OPPORTUNITIES: POWER OF THE EMERGING MARKETS

*Source: Euromonitor 17

GROWTH OPPORUNITIES

Technology Millennials Emerging

Middle

Class

Urbanization 3rd

Billion

LARGER ADDRESSABLE MARKET

Connected

Communities

18

Systematizing

What Works

Aligning

Our Message

Shifting

Our Mindset

STRENGTHEN

OUR CORE

LEVERAGE

OUR PURPOSE

SIMPLE • CONSISTENT • SCALABLE

EXTEND

OUR REACH

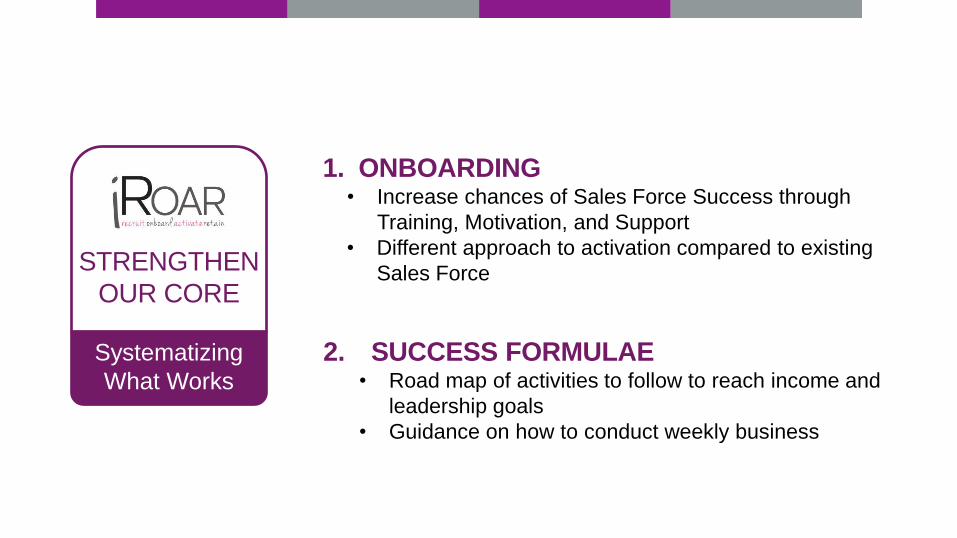

STRENGTHEN

OUR CORE

Systematizing

What Works

1. ONBOARDING • Increase chances of Sales Force Success through

Training, Motivation, and Support

• Different approach to activation compared to existing

Sales Force

2. SUCCESS FORMULAE • Road map of activities to follow to reach income and

leadership goals

• Guidance on how to conduct weekly business

21

Party happens around the world

every 1.3 Seconds

Predominately a Push Business

built on Relationships

OUR CORE WORKS

CREATE MORE OPPORTUNITY FOR

SALES FORCE & REACH MORE CONSUMERS

G U I D I N G P R I N C I P L E S

RESPECT SALES FORCE IN THE VALUE CHAIN

INSPIRE & NURTURE RELATIONSHIPS

PROMOTE DEMONSTRATION BASED SELLING

22

SHIFTING OUR MINDSET

FROM

REACH ONLY

THROUGH

PARTY & BROCHURE

TO

EXTENDING REACH TO

RELATIONSHIPS

BEYOND THE PARTY

23

NEW INITIATIVES TO

EXTEND OUR REACH

Close to consumers with updated look & feel to increase brand awareness

Drives contact with Sales Force & consumers

Urban penetration model

Party PLUS a few more

Test phase in TW U.S.

Early results:

• 1 – 3 additional guests on average

• guests spend 2x the typical online order

24

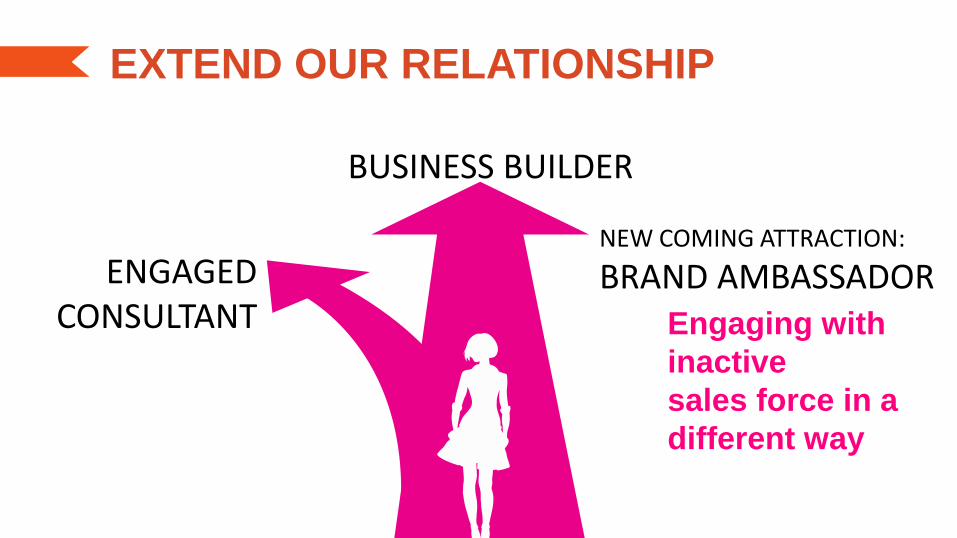

ENGAGED CONSULTANT

NEW COMING ATTRACTION:

BRAND AMBASSADOR

BUSINESS BUILDER

Engaging with

inactive

sales force in a

different way

EXTEND OUR RELATIONSHIP

26

VALUE

STRONG RECORD of

GROWTH and of RETURNING

27

Local currency sales*

growth each year

2007–2014

*See GAAP to non-GAAP sales reconciliation for reported sales growth

SOLID HISTORY of GROWTH

5% to 9% Today’s value of $10,000

invested in Tupperware

in January 2007 to

December 2014 vs. $17k

in the S&P 500*

$40,000

28

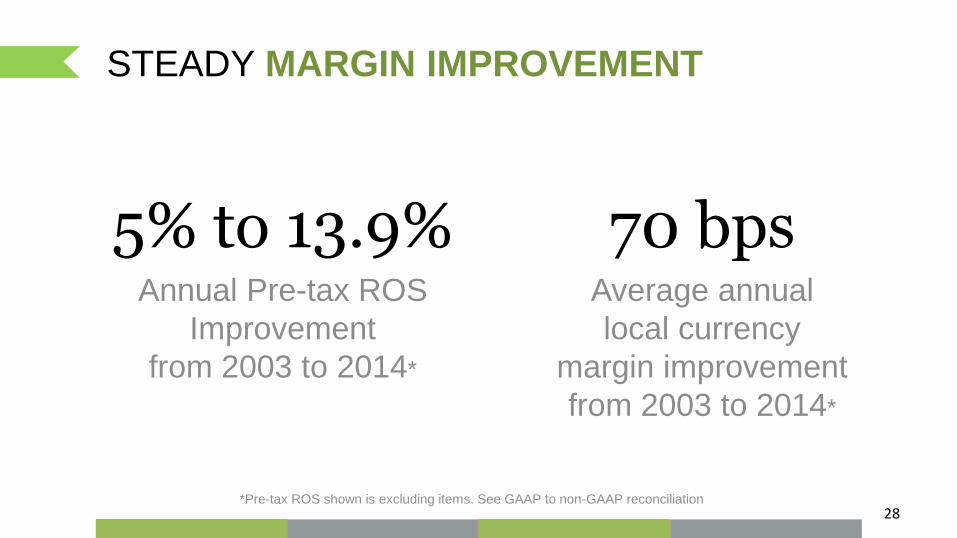

Annual Pre-tax ROS

Improvement

from 2003 to 2014*

5% to 13.9%

*Pre-tax ROS shown is excluding items. See GAAP to non-GAAP reconciliation

Average annual

local currency

margin improvement

from 2003 to 2014*

70 bps

STEADY MARGIN IMPROVEMENT

$0

$50

$100

$150

$200

$250

$300

2009 2010 2011 2012 2013 2014 2015*

$M

illio

ns

Net Cash Flow before Financing Activities (Free Cash Flow) GAAP Net Income

29 *High end of guidance range provided in July 22, 2015 Earnings Release.

**Impact of changes in foreign currency versus prior year are updated monthly and posted on: http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm

GAAP Net Income includes

impact of non-cash

purchase accounting asset

impairment charges

GAAP Net Income

includes

impact of Venezuelan

devaluations from

balance sheet items

CASH PRODUCER FREE CASH FLOW (as reported)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

1996 -2009

2010 2011 2012 2013 2014 2015

+20%

Announce 50% Payout

target on EPS ex. items

YIELD

4.9%*

+20%

+72% +10% EVEN

30

STEADY DIVIDENDS AND REPURCHASED ~20% OF SHARES SINCE 2007

*Yield based on August 17, 2015 closing stock price of $55.55

21.3 MILLION

SHARES (50.3 million outstanding)

For $1.3 BILLION

ANNUAL DIVIDENDS SHARE REPURCHASES

2007-2014

31

OUTLOOK

Third Quarter 2015 Guidance

2015 Full Year Guidance

USD Sales* (11)% to (10)% (11)% to (10)%

GAAP EPS** $0.57 – $0.62 $3.77– $3.87

GAAP Pre-tax ROS 7.9% – 8.4% 11.4 – 11.6%

Local Currency Sales +4% to 6% +4 to 5%

EPS, excluding items*** $0.69– $0.74 $4.42 – $4.52

Pre-tax ROS, excluding items 9.0% – 9.4% 12.8% – 13.0%

FX Impact on EPS comparison, excluding items ($0.22) ($1.22)

*Outlook as of the July 22, 2015 earnings release. Venezuelan operating activity was translated at 50 bolivars/$ in January 2015, and at the Simadi rate for

February 2015 through June 2015. Expect to use the Simadi rate, which was approximately 200 as of July 20, 2015 to translate future operating activity

**Excludes any second half Orlando land transactions

***GAAP to non-GAAP reconciliation attached to 2Q 2015 earnings release

2016 initial sales guidance to be released in October

Double Digit EPS Growth driven by:

· Local Currency Sales: +6% to 8% · Emerging markets about 10%

· Established markets low single digit

· Pre-Tax ROS, excluding items:

· 50 bps improvement per year into the mid- to high-teens

· Some offset from tax rate:

· Going to 27-28% over time

· CAPEX $70 - $80 million a year

· Share repurchases

LONG-TERM OUTLOOK

32

APPENDIX

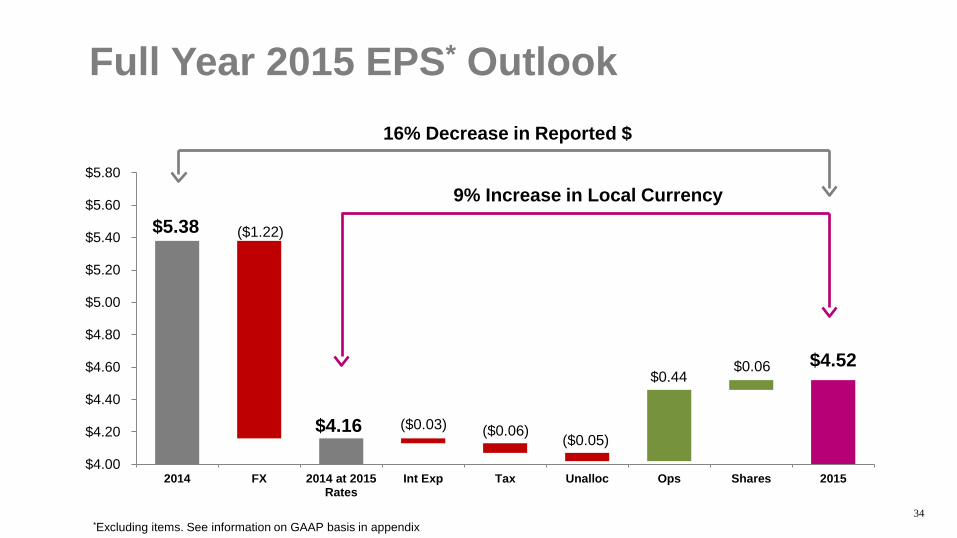

Full Year 2015 EPS* Outlook

34

$5.38 ($1.22)

($0.03) ($0.06) ($0.05)

$0.44 $0.06 $4.52

$4.00

$4.20

$4.40

$4.60

$4.80

$5.00

$5.20

$5.40

$5.60

$5.80

2014 FX 2014 at 2015Rates

Int Exp Tax Unalloc Ops Shares 2015

16% Decrease in Reported $

9% Increase in Local Currency

$4.16

*Excluding items. See information on GAAP basis in appendix

Return On Sales*

35

Third Quarter 2015

Guidance

2015 Full Year Guidance

2014 Pretax ROS 10.2% 13.9%

Translation FX (115) bp (135) bp

2014 Pretax ROS (constant currency) 9.0% 12.6%

LC Operating Margin Improvement 35 bp 45 bp

Net interest expense (11) (11)

Other, rounding 12 10

2015 Pretax ROS (high end guidance)** 9.4% 13.0%

*Venezuelan operating activity was translated at 50 bolivars/$ in January 2015, and at the Simadi rate for February 2015 through June 2015.

Expect to use the Simadi rate, which was approximately 200 as of July 20, 2015 to translate future operating activity.

***GAAP to non-GAAP reconciliation attached to 2Q 2015 earnings release

$0

$1

$2

$3

$4

$5

$6

$7

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2009 2010 2011 2012 2013 2014 2015*

Sales Diluted EPS Adjusted Diluted EPS36

Sales

$million

Diluted EPS includes

impact of non-cash

purchase accounting asset

impairment charges

EPS

$Dollar

*High end of guidance range provided in July 22, 2015 Earnings Release.

Impact of changes in foreign currency versus prior year are updated monthly and posted on: http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm

Diluted EPS includes

impact from balance sheet

items of Venezuelan

devaluations

CONSISTENTLY GROWING SALES & EPS

37

Non-GAAP FINANCIAL RECONCILIATION

2003 2004 2005 2006 2007 2008 2009 2010*

Net Income (GAAP) 47.9 86.9 85.4 94.2 116.9 161.4 175.1 221.2

Adjustments:

Gains on disposal of assets including insurance recoveries (3.6) (13.1) (4.0) (12.3) (11.8) (24.9) (21.9)

Re-engineering and other restructuring costs 6.9 7.0 14.3 7.6 9.0 9.0 8.0 10.0

Debt refinancing costs associated with Sara Lee acquisition 29.1

Acquired intangible asset amortization 1.8 25.0 13.6 11.9 5.1 3.8

Purchase accounting intangibles and goodwill impairment 11.3 9.0 28.1

Cumulative effect of accounting change 0.8

Costs associated with implementing 2007 credit agreement 9.6

Income tax impact of adjustments (2.4) 2.5 (36.9) (4.9) (7.4) 3.3 1.7 (4.0)

Net Income (Adjusted) 48.8 83.3 90.5 109.6 141.2 169.7 196.1 231.0

* High end of 2010 outlook provided in July 19, 2010 Earnings Release

38

2010 2011 2012 2013 2014 Q1 2015 Q2 2015 Q3 2015* 2015*

Net Income (GAAP) $225.6 $218.3 $193.0 $274.2 $212.0 $29.5 $62.0 $31.3 $194.8

ADJUSTMENTS:

Gains on disposal of assets including insurance

recoveries** (0.2) (3.8) (7.9) (0.7) (2.7) (0.6) (10.8) -- (11.4)

Re-engineering and other restructuring costs 7.6 9.6 22.1 9.3 13.4 16.2 1.5 2.9 23.5

Impact of Venezuelan bolivar devaluation from

balance sheet positions 4.2 42.4 9.3 1.7 -- 11.1

Swap impairment and debt cost write-off 19.8

Acquired intangible asset amortization 3.9 2.9 2.1 4.8 11.9 2.7 2.6 2.7 10.6

Purchase accounting intangibles and goodwill

impairment 4.3 36.1 76.9

Income tax impact of adjustments (3.3) (9.6) (4.8) (3.5) (2.4) (5.9) 3.9 0.4 (0.9)

Net Income (Adjusted) $237.9 $273.3 $281.4 $288.3 $274.6 $51.2 $60.9 $37.3 $227.7

Adjusted ROS 13.9% 13.9% 14.1% 14.1% 13.9 % 11.8% 13.8% 9.4% 13.0%

Average number of diluted shares (millions) 61.4 61.4 56.4 53.1 51.0 50.3 50.4 50.4 50.3

*High end of guidance range provided in January 22, 2015 Earnings Release.

Impact of changes in foreign currency versus prior year are updated monthly and posted on: http://ir.tupperwarebrands.com/foreign-exchange-impact.cfm

**Excludes any second half 2015 Orlando land tranactions

Non-GAAP FINANCIAL RECONCILIATION

39

2009 2010 2011* 2012 2013 2014 2015**

Sales $2,128 $2,300 $2585 $2,584 $2,672 $2,606 $2,344

Reported Sales Growth (2)% 8% 12% 0% 3% (2)% (10)%

Local Currency Sales Growth 6% 6% 9% 5% 6% 5% 5%

*2011 had 53 weeks compared with 52 weeks in 2010

**2015 assumes the high-end of local currency sales growth

2009 THROUGH 2015 FULL YEAR GUIDANCE REPORTED AND LOCAL CURRENCY SALES

* 2011 included 53 weeks.

**High end of guidance range included in July 22, 2015 earnings release.

VENEZUELA FX IMPACT IN 2014 AND 2015

40

1H – 2014

Q3 – 2014

Q4 – 2014

FY 2014

Q1 – 2015

Q2 – 2015

Q3 – 2015(1)

FY 2015(1)

Total Company Percentage Point Impact on Sales from Changes in Rate

(0.7pp) (3.5pp) (3.4pp) (2.1pp) (4.7pp) (3.3pp) (0.7pp) (2.3pp)

Translation Impact of Changes in Rate on Diluted EPS Comparison ($0.04) ($0.10) ($0.08) ($0.21) ($0.13) ($0.13) ($0.01) ($0.28)

Re-measurement Impacts on Net Monetary Assets for 1H – 2014 and gain on conversion of bolivars to U.S. dollars (Q3 - 2014) (2)

($0.51) $0.09 ($0.08)(3) ($0.50) ($0.11)(4) ($0.01) N/A N/A

Transaction Impacts on cost of sales at Stronger Rates than Sales (2) ($0.12) ($0.23) $0.01(3) ($0.35) ($0.03)(4) ($0.02) (4) ($0.02) (4) ($0.06) (4)

(1) The bolivar to U.S. dollar exchange rate used in translating the Company’s first quarter 2014 operating activity was 6.3 bolivars to the U.S. dollar, was 10.8 bolivars to the U.S. dollar in

the second quarter and was 50.0 in the second half of 2014 and in January 2015. In February 2015, the Venezuelan government launched an overhaul of its foreign currency exchange

structure for obtaining U.S. dollars, eliminating the SICAD 2 auction process and introducing the Marginal Currency System, or Simadi, which was approximately 200 bolivars to the U.S.

dollar as of July 20, 2015. The Company's outlook used the Simadi rate to translate its February through June 2015 operating activity and expects to use it to translate future operating

activity. (2) The pretax expense impact from amounts on the balance sheet when the bolivar devalued are included in the U.S. GAAP earnings per share and return on sales data above, but not in

the data excluding items. (3) Reflects tax recognized on an annualized basis under U.S. GAAP. (4) With the change to the Simadi exchange rate there was a negative profit impact related to net monetary assets and inventory of $9.3 million and $1.8 million in the first and second

quarters of 2015 respectively. The change in rate in February 2015 also triggered $13.5 million write-off of long-term fixed assets in the first quarter of 2015. As of the end of June 2015,

there is $25.5 million in Cumulative Translation Adjustments and $8.6 million in net assets related to Venezuela.

Mike Poteshman

EVP & CFO

September 2015