Middle East PointofView - Deloitte · Middle East In the Middle East since No place like home...

54

Middle East In the Middle East since No place like home Homegrown Asset management in the Middle East Mixin’ it up Commercialization of sports venues “Ebony, ivory…” Harmony in Islamic Banking National resources Mining Big Data Point of View Published by Deloitte & Touche (M.E.) and distributed to thought leaders across the region. Fall 2015

Transcript of Middle East PointofView - Deloitte · Middle East In the Middle East since No place like home...

Middle East

In the MiddleEast since

No place like home

HomegrownAsset management in the Middle East

Mixin’ it upCommercialization ofsports venues

“Ebony, ivory…”Harmony in Islamic Banking

National resourcesMining Big Data

Point of ViewPublished by Deloitte & Touche (M.E.)and distributed tothought leadersacross the region.

Fall 2015

2 | Deloitte | A Middle East Point of View | Fall 2015

Fall 2015Middle East Point of ViewPublished by Deloitte & Touche (M.E.)

Read ME PoV on your iPad. Download ME PoV app.

www.deloitte.com/middleeast

Deloitte | A Middle East Point of View | Fall 2015 | 3

A word from theeditorial team

Have you ever wondered what it would be like not tohave a home to go to? After a long, hard day at work or a trip away, do you ever ponder the difficulty of nothaving a place to, as Paul Young* so eloquently put it,“lay down [your] hat?”

Yet for centuries people have left their homes or havebeen driven out as a result of wars and occupations, or out of a desire for a place that could provide perhaps more safety, autonomy and security, a new roof over one’s head: a place of one’s own, a new place to call home.

The essential idea of “home” is a nuance that waftsthrough this issue of Middle East Point of View, in both senses of identity and space, in the macro andmicroeconomic sense and in the literal and figurativesense. In some of the articles included, it is the notion of bringing the outside in, of importing ideas andgrowing them locally that is considered, while in others, it is about improving one’s environment and making it an even better place.

In Going local by Umair Hameed, Benjamin Collette and Francois Gilles, and Mixin’ it up by JoaquinMartinez, asset management products and thecommercialization of sports venues, respectively, are notions that are imported and then homegrown. A similar idea runs through the article on accrualaccounting by Mohammad Jallad and Faisal Darras(Accrual accounting is for the public sector too) in which they offer a perspective on the subject for Arab countries.

Big Data, mining a national resource by EmmanuelDurou is also about using a local resource, data, tosupport governments in their national vision. In Living in perfect harmony, it is, in contrast, a notion exportedfrom the Arab world, that of Islamic banking, that isunder scrutiny. Bhavin Shah and Saad Qureshi say thatdespite the substantial growth of the sector in recentyears, it would benefit from a more consistent andharmonized approach in order to penetrate globalmarkets.

In Journey to Excellence by Tarek Nahle, Joana AbouJaoude and Raquelle Azar, the concept of improvingone’s space is examined through their article onexcellence standards and e-initiatives that “haveimproved service quality [and] customer experience.”

As social media becomes the new standard, companiesneed to learn how to attract and use that power fortheir own benefit, says Elissar Hajj in her article Like it or not, here I am. In trying to harness the people power of “Social,” Hajj advises company leaders to ask not “how social are my employees” but how “social is my company?”

Talking of which, make sure not to miss us on all thesocial networks to stay updated on the hot issuesmaking the business rounds in the region.

ME PoV editorial team

* English singer and musician

4 | Deloitte | A Middle East Point of View | Fall 2015

In this issue

Going local Asset management in the Middle East Umair Hameed, Benjamin Collette and Francois Gilles

Living in perfect harmonyBhavin Shah and Saad Qureshi

Mixin’ it upCommercialization opportunities in GCC sports venuesJoaquin Martinez

Big DataMining a national resource Emmanuel Durou

6

14

18

22

Contents

Deloitte | A Middle East Point of View | Fall 2015 | 5

30

36

42

Table of contents

Like it or not, here I amSocial media and the workplaceElissar Hajj

Journey to ExcellenceTarek Nahle, Joana Abou Jaoude and Raquelle Azar

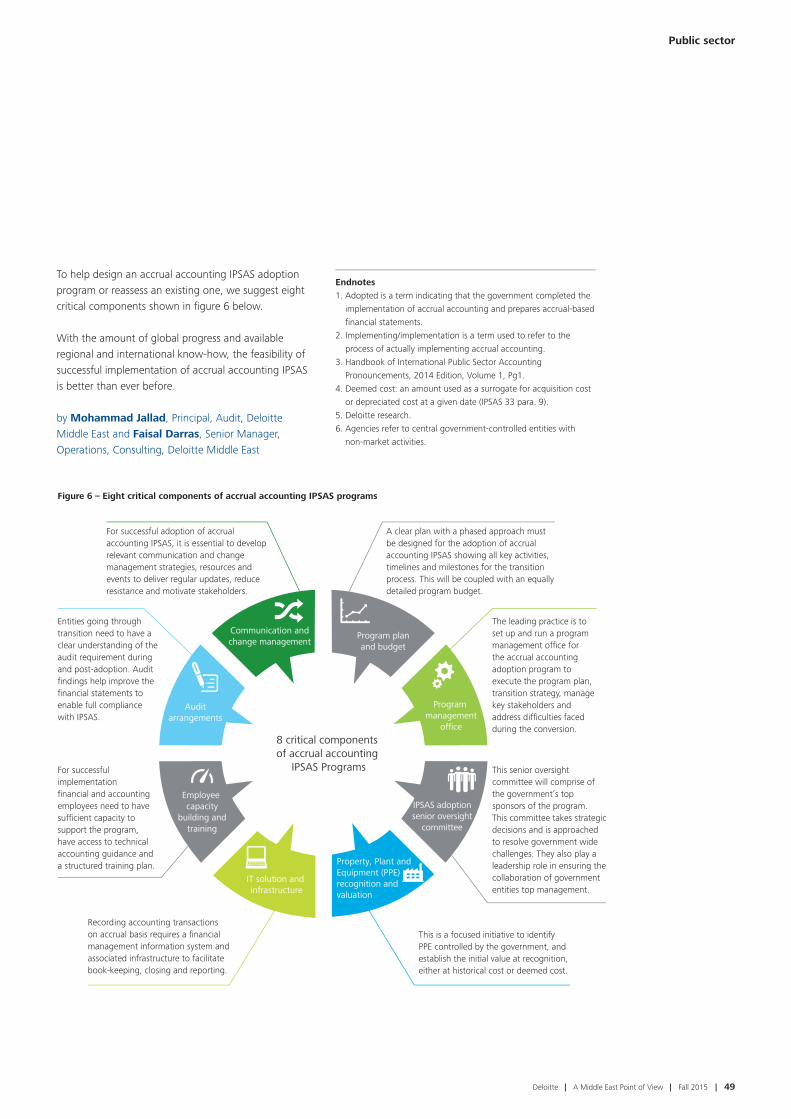

Accrual accounting is for the public sector tooA perspective for Arab central governmentsMohammad Jallad and Faisal Darras

Going localAsset management in the Middle East

Deloitte | A Middle East Point of View | Fall 2015 | 7

Asset management

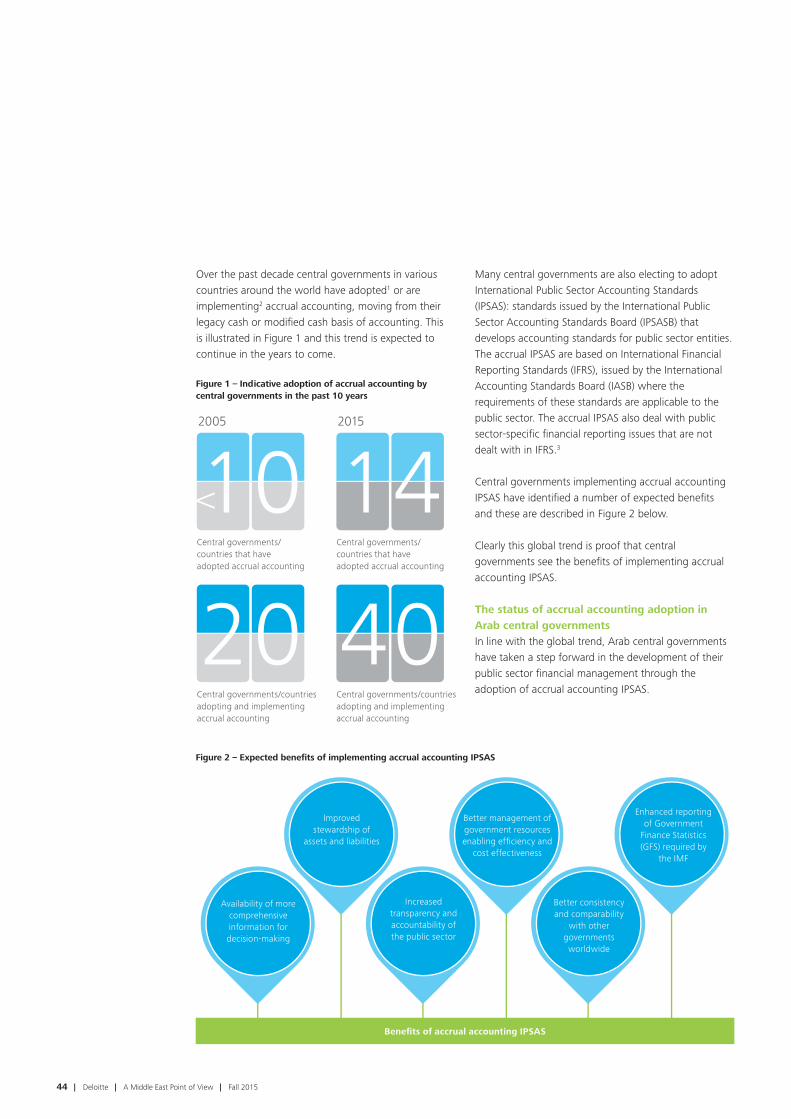

The Middle East economies have grown stronglyin the past few years and are increasing theirefforts at diversificationMiddle East growth has picked up strongly following thefinancial crisis of 2008-2009, driven to a large extent bygrowth in the Gulf Cooperation Council (GCC) countries.The GCC region’s real GDP growth rate averaged 5.2percent from 2010 to 2014, outperforming mostdeveloped countries throughout this period.1

Most GCC countries have benefited from high oil pricesover the past decade, which contributed to significantwealth creation for both institutional and privateinvestors. Oil revenue still represents the majority of

the region’s GDP, but the countries are making efforts to diversify their economies. The United Arab Emirates(UAE) and other countries in the region have launcheddevelopment plans (e.g. Abu Dhabi Vision 2030, QatarNational Vision 2030, UAE Vision 2021) to developother sectors such as aviation, tourism, transportation,and financial services.

Oil revenues have allowed the countries in the region toinvest heavily in infrastructure projects that today form a solid base for the development of a more diversifiedeconomy. However, the recent fall in oil prices couldchallenge near-term growth and investments.

Asset management

8 | Deloitte | A Middle East Point of View | Fall 2015

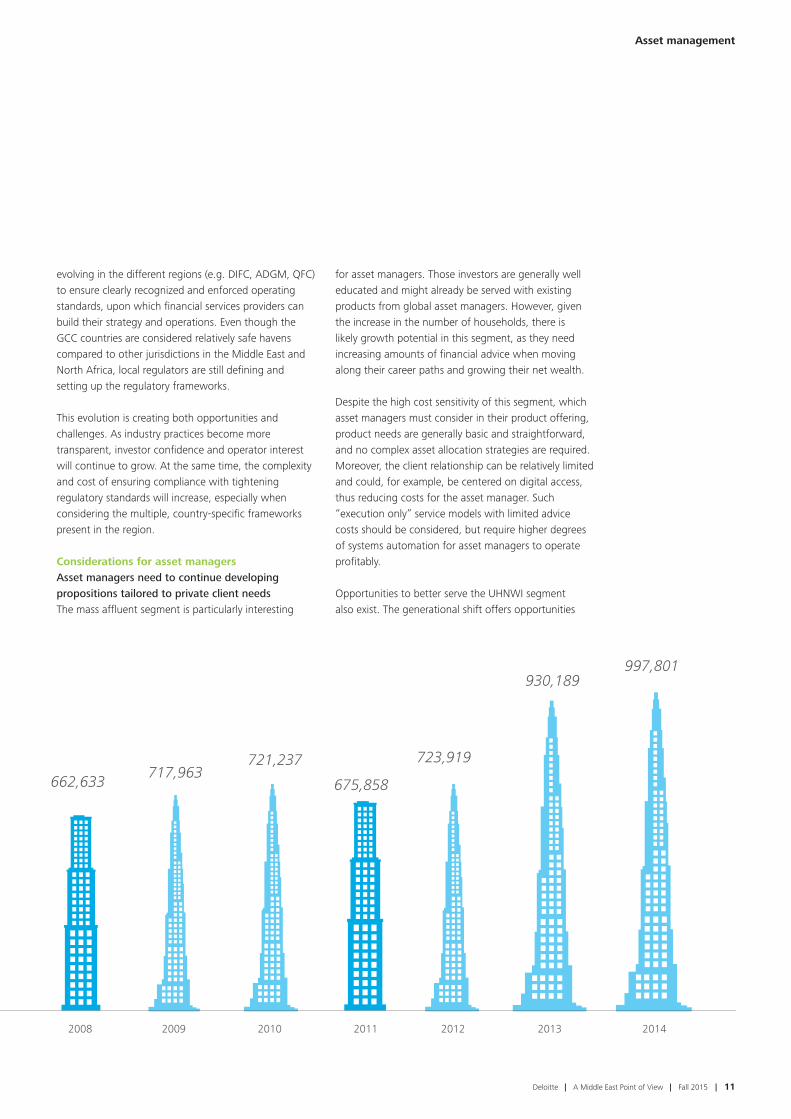

The Middle East asset management industry isgaining in maturity and is no longer a purelyinstitutional businessThe total wealth pool in the region today amounts to approximately US$5.2 trillion and local Sovereign Wealth Funds (SWFs) represent almost 50 percent ofthis wealth. The remaining wealth is split between other institutional investors such as local pension funds, as well as mass affluent investors and Ultra High Net Worth Individual (UHNI) investors in the non-professional segment. The growth in local wealthresults from global capital markets growth as well as the strong growth of GDPs in the region.

International as well as local asset managers haverecognized the importance of the region in terms ofpotential asset collection and have started to increasetheir local activities over the past decade. Historically,asset management activities in the Middle East havefocused on SWFs and other institutional investors.

Recently, however, we have seen asset managersincrease their range of investment funds in the regionthat are addressed to private investors. Particularly inanticipation of the opening of the Saudi Arabian stockmarket to foreign investors, there has been an increaseof almost 10 percent in the number of investment funds operating in Saudi Arabia in 2014. There is alsoincreased interest in the distribution of Undertakings forCollective Investment in Transferable Securities (UCITS)structures into the Middle East region, reflected in theincreasing number of UCITS approved for distribution inthe various countries.

The mass affluent segment shows one of thestrongest relative growth rates in private wealthThe mass affluent segment shows the strongest growthin wealth from 2009 to 2013, with a Compound AnnualGrowth Rate (CAGR) exceeding 15 percent. Thissegment is composed of Western, Asian, and otherexpatriates who tend to keep their home bankingservices providers and asset managers when movinginto the region and tend not to invest large portions of their wealth in the region. While historically thissegment may have suffered from a home market bias in terms of asset management choices, the length ofexpatriates’ stay in the region is increasing, and isexpected to encourage local investment choices.2 Themass affluent segment also recorded an increase in the number of households over the past five years,indicating the creation of a financially stable middle class in the region, which supports the long-termeconomic development of the region in general.

HNWI and UHNWI investors represent the largestsegment of non-professional investors in the region interms of wealth, and have shown continued growthover the past few years. The majority of investors in thissegment are GCC nationals. The generational shift in thissegment raises questions of how to align the traditionalvalues of the current generation with the new, moremodern perspectives of the younger generation, and the impact on their investment behavior.

International as well as local assetmanagers have recognized theimportance of the region in terms ofpotential asset collection and havestarted to increase their local activitiesover the past decade

Deloitte | A Middle East Point of View | Fall 2015 | 9

The current generation’s investments are characterizedby highly liquid, low-risk assets with emphasis on capitalprotection. On the other hand, the younger generationhas a more aggressive investment approach with higherexpected returns, shorter time horizons, and seekswealth generation rather than wealth preservation. Thisnew generation of investors also shows an increasedinterest in professionalizing their private portfolios interms of asset allocation and diversification. This createsopportunities for asset managers to provide professionalsolutions to those investors. Furthermore, GCC investorstend to appreciate tangible assets such as realestate–“Property gets sick but it never dies” is acommonly used proverb to explain the lure of suchassets for local investors.3

Most assets in the UHWNI segment are held offshore, in part due to the lack of actively managed investmentopportunities with a good track record in the region. We observe a low penetration of private wealth byprofessional asset management products. In 2012,roughly US$56 billion of the total US$2.2 trillion wealthpool in the region was captured by professional assetmanagement products locally (i.e. investment fundsand/or discretionary mandates.) This is also due to thefact that many wealthy families have their own wealthadvisor to ensure discretion and are not linked toprofessional advisors. However, both professional and non-professional investors have shown increasedinterest in Shari’a-compliant structures as well asregional investment products, but the demandsignificantly outpaces the supply of such products,indicating the strong growth potential for assetmanagers.

Regional financial centers continue to emerge withthe ambition to enter the top tier of global financialcentersThe financial industry in the Middle East has seen stronggrowth over the past decade. Today, four Middle Easternfinancial centers appear in the top 35 as per the Global

Financial Centers Index 2015, namely Qatar (26th), Dubai (29th), Riyadh (31st), and Abu Dhabi (32nd). Inconsequence, global banks and asset managers haveconstantly increased their presence in the region andlocal banks have been expanding into non-interestincome activities such as asset management to reducetheir exposure to the highly competitive core bankingactivities.

Despite this increased activity, we still observe certainareas for improvement in the financial centers, whichlimit the ability of industry players to commit to on-the-ground investments and increased activity. These areasfor improvement include capital markets liquidity andthe development of robust regulatory and legalframeworks.

While still small, the local capital markets areshowing progressively more sophistication andliquidityThe market capitalization of the GCC stock markets was about US$1 trillion in December 2014, with Saudi Arabia accounting for almost 50 percent withUS$480 billion. While market capitalization hasincreased steadily over the past decade, regionalmarkets are still limited in terms of asset classes and

While market capitalization has increasedsteadily over the past decade, regionalmarkets are still limited in terms of assetclasses and investor groups such aspension funds, insurance companies, and large investment companies

Asset management

investor groups such as pension funds, insurancecompanies, and large investment companies. These are important elements of a sound financial system that eventually support the development and growth of the overall economy.

Some of the local capital markets have been closed toforeign direct investments (FDI) and are now slowlybeing opened to foreign investors, which will ultimatelyincrease liquidity. The opening of the Saudi Arabianstock market to qualified foreign investors, in the first

half of 2015, is widely considered a milestone in thedevelopment of the regional stock markets and likely toincrease the liquidity in the Tadawul, the Saudi Arabianstock index. Also, the increased presence of GCC indicesin global emerging market indices (e.g. Qatar’s increasedweight in the MSCI Emerging Markets index) is expectedto have a positive impact on the capital markets’liquidity in the region.4

Gradual sophistication of the capital markets is also likely to promote the development of the domesticeconomy with increased availability of financial productspotentially helping fuel growth of the private sector,especially the SMEs that have restricted access to capitalmarkets and are often limited to traditional sources offunding.

Legal and regulatory regimes are gradually evolvingtoward global standardsThe stability of the regulatory and legal environments is a requirement for the development of the assetmanagement industry. Regulatory frameworks are

The stability of the regulatory and legalenvironments is a requirement for thedevelopment of the asset managementindustry

GCC market capitalization evolution (in current US$ million)

1,000,000

800,000

600,000

58,474

2001 2002 2003 2004 2005 2006 2007

91,018

182,692

364,801

744,037

641,603

1,001,584

400,000

200,000

10 | Deloitte | A Middle East Point of View | Fall 2015

Deloitte | A Middle East Point of View | Fall 2015 | 11

evolving in the different regions (e.g. DIFC, ADGM, QFC)to ensure clearly recognized and enforced operatingstandards, upon which financial services providers canbuild their strategy and operations. Even though theGCC countries are considered relatively safe havenscompared to other jurisdictions in the Middle East andNorth Africa, local regulators are still defining andsetting up the regulatory frameworks.

This evolution is creating both opportunities andchallenges. As industry practices become moretransparent, investor confidence and operator interestwill continue to grow. At the same time, the complexityand cost of ensuring compliance with tighteningregulatory standards will increase, especially whenconsidering the multiple, country-specific frameworkspresent in the region.

Considerations for asset managersAsset managers need to continue developingpropositions tailored to private client needsThe mass affluent segment is particularly interesting

for asset managers. Those investors are generally welleducated and might already be served with existingproducts from global asset managers. However, giventhe increase in the number of households, there is likely growth potential in this segment, as they needincreasing amounts of financial advice when movingalong their career paths and growing their net wealth.

Despite the high cost sensitivity of this segment, whichasset managers must consider in their product offering,product needs are generally basic and straightforward,and no complex asset allocation strategies are required.Moreover, the client relationship can be relatively limitedand could, for example, be centered on digital access,thus reducing costs for the asset manager. Such“execution only” service models with limited advicecosts should be considered, but require higher degreesof systems automation for asset managers to operateprofitably.

Opportunities to better serve the UHNWI segment also exist. The generational shift offers opportunities

Asset management

2008

662,633

2011

675,858

2009

717,963

2010

721,237

2012

723,919

2013

930,189

2014

997,801

12 | Deloitte | A Middle East Point of View | Fall 2015

for asset managers to establish connections with the new generation and their specific need forprofessional advice.

This could also be used as a foot in the door to establisha link to the current generation, by understanding theirinvestment needs and translating them into easy-to-understand investment propositions. UHNWI havehistorically been one of the most favored client segmentfor asset managers due to the high margins linked tothis client base. However, competition in this segmentis intense and it may be difficult to convince clients witha long-term relationship with existing Single- or Multi-Family Offices (SFO/MFO) to enter into new wealthmanagement relationships.

Besides the macro segmentation of the non-professionalinvestors, asset managers should consider thedemographic composition of the different countries and markets. Even though GCC nationals dominate the UHNWI segment, expatriates are also representedand have different investment habits that should beconsidered by offering specially tailored products to thissub-segment. The same rule applies to the mass affluentand retail segments, where expatriates from the Asiancountries can wield increasing investment power.

Low oil prices will have an impact in the short termthough the long-term potential of the industry lookspromisingThe recent drop in oil prices has impacted GCC marketcapitalization and impeded liquidity with some of theregional governments resorting to debt, in order tomeet funding shortfalls. However, given customerinterest and a strong government drive to develop thesector through initiatives such as the new Abu DhabiGlobal Markets, intended to become operational in2016, give further indication that asset management ispoised for growth in the longer term.

The changing regulatory landscape needs to beclosely monitoredThe increasing number of regulatory regimes in theregion, that aim to define a framework for assetmanagers and financial services providers to operate in, creates opportunities for those players to positionthemselves in the market in the appropriate way.However, as those regimes are still under developmentand most likely subject to further amendments, assetmanagers need to implement regulatory watchprocesses to closely monitor the evolution of theregulatory regimes applicable to their entities and assess their impact on their existing business models.New or changing legal requirements may just represent additional workload (e.g. additional reporting requirements), but may also offer newbusiness opportunities to asset managers (e.g. creationor permission of new product classes) into which they(quickly) need to tap if they want to benefit from themomentum created by such amendments or new laws.

Digital channels have become a keyselling point of a complete assetmanagement value proposition and go beyond the provision of accountstatements in electronic format

Deloitte | A Middle East Point of View | Fall 2015 | 13

On-the-ground sales teams are not sufficient tobuild long-standing relationshipsGlobal asset managers often limit their presence to localsales teams or representative offices in order to managethe assets in the global financial centers. However,establishing relationships with wealthy investors in theregion is a long-term project and such relationships arebuilt over several years with regular face-to-face contact.We think that this is one of the reasons why global assetmanagers have failed to capture more of the availablewealth into their asset management products.

Asset managers have to rethink both theirdistribution and product strategiesThe increasing wealth–and thus investment potential–ofmass affluent investors and the new generation ofUHNWI investors require asset managers to rethink theirdistribution strategies and product offerings.

Digital channels have become a key selling point of acomplete asset management value proposition and gobeyond the provision of account statements inelectronic format. The digital channel should offer acomplete service with information and transactionexecution features as well as advising features and a link to the relationship manager. It should also bepossible to switch between interaction channels without any problems (e.g. from mobile applications to face-to-face advice in a branch.)

This increased wealth also has an impact from a productpoint of view, as the increased reallocation of assets in the region should be captured in local products tofurther boost economic development and local financialmarket liquidity. The success of local products (e.g.Sukuks and other Shari’a-compliant structures as well as local Real Estate Investment Trusts) indicates that

there is a strong demand to invest in the region and todo this using local structures. If asset managers cansuccessfully respond to that demand by creatinginnovative products, it will eventually lead to a greaterdiversity in asset pools and thus allow the financialcenters to increase their maturity and their contributionto overall economic development.

by Umair Hameed, Director, Monitor Deloitte MiddleEast, Benjamin Collette, Partner, Deloitte Luxembourgand Francois Gilles, Director, Deloitte Luxembourg

Endnotes1. Institute of International Finance.2. Invesco Middle East Asset Management Study 2013.3. Ibid.4. http://www.khaleejtimes.com/biz/inside.asp?xfile=/data/uae

business/2014/September/uaebusiness_September177.xml§ion=uaebusiness

This increased wealth also has animpact from a product point of view, as the increased reallocation of assets in the region should be captured in local products to further boosteconomic development and localfinancial market liquidity

Asset management

Deloitte | A Middle East Point of View | Fall 2015 | 15

Despite its substantial growth in recent years,Islamic banking is facing challenges when itcomes to deeper global market penetration.The solution, say these authors, is moreconsistency and harmonization.

Living inperfectharmony

Islamic banking

16 | Deloitte | A Middle East Point of View | Fall 2015

The growth of Islamic banking has outstripped that ofconventional banking in recent years with total Islamicbanking assets crossing the US$1.5 trillion mark in 2013.The widely held expectation that this superior growthrecord will continue is understandable given thatapproximately one-sixth of the world’s population isMuslim–most of which is based in the Middle East andAsia. Taking note of the demand, a number of westerncountries have recently started allowing Islamic banks tooperate in their respective jurisdictions. The UK becamethe first leading western country to issue a governmentSukuk (Islamic bond.) The first full-fledged Islamic bankin Germany was launched earlier this year; whileJapanese regulators are considering issuing regulationsthat will allow Japanese banks to provide Islamic financeproducts in Japan.

Yet, despite the increased interest, Islamic bankingpenetration in non-Muslim countries has been slow asIslamic banks find it difficult to expand into differentjurisdictions and face regulatory and Shari’acomplications in terms of approvals. Islamic banks arealso finding it challenging to cope with the evolvingglobal banking environment and making appropriaterules and regulations to cope with these changes whilestill remaining competitive with their conventionalcounterparts. Additionally, the industry lacks consistencyin product structures and investment practices thatadversely affects its credibility, reputation, perceptionand regulation capabilities.

The challengeIslamic banks are essentially governed by their Shari’aboards–the religious scholars that deem a productShari’a-compliant, or not. But the challenge is that thereis no central authority promulgating Shari’a law, and theunderstanding of what is hence permissible and what is not varies among Islamic scholars and jurisdictions.The rapid growth of Islamic banking over the years has resulted in the introduction of complex bankingproducts and structures, which now require Shari’aharmonization at a global level. At present, thatharmonization is lacking. For example, the Islamiccontract of Tawwaruq or Commodity Murabaha is onlyallowed by certain scholars. Similarly Bai-al-dain, or saleof debt, although disallowed by the majority of Muslimscholars, is allowed by some scholars in Malaysia.Recently a prominent Shari’a scholar concluded thatapproximately 85 percent of Sukuks in the market fallshort of basic Shari’a principles.

While conventional banks have harmonized andapproved regulatory standards that banks around theworld follow, making it easier for them to expand andconduct operations in different countries, there are noapproved standards per se for Islamic banks; they followthe conventional banking regulations.

But because Islamic banking differs from conventionalbanking, it is difficult for Islamic banks to completelyfollow these global conventional standards. Forinstance, the capital structure in Islamic banks isdifferent from that of conventional banks. Because ofthe prohibition of interest, Islamic banks mobilize andutilize funds using Shari’a-compliant instruments orcontracts that are not used by conventional banks andhence their capital structure primarily consists of Tier 1capital only, while only a handful of Islamic banks haveTier 2 capital. Another differentiation between the twobanking models is the bank’s ownership of the asset: inIslamic banking contracts like Murabaha, Islamic bankshave to own the asset for a period of time, a practicethat is not required in conventional banking practices.

The challenge is that there is no centralauthority promulgating Shari’a law, andthe understanding of what is hencepermissible and what is not varies amongIslamic scholars and jurisdictions

Deloitte | A Middle East Point of View | Fall 2015 | 17

Industry responseThe industry realizes this challenge and certain countriesand governments have fostered the development of theIslamic banking sector. Countries like Malaysia, Bahrain,and Oman have developed separate legal and regulatoryframeworks for Islamic banks to follow, while Qatar hasaimed to separate Islamic banking from conventionalbanking by banning Islamic windows withinconventional branches in the country. Other countries,like the United Arab Emirates (UAE) and Turkey, havebeen focusing on promoting the Islamic bankingindustry and are becoming centers of excellence. Yetdespite these improvements, these countries have beenworking in isolation rather than collectively to addressthese issues. As a result, the industry still lacks a clearstrategy and direction to help achieve its potential.

Nevertheless, the industry has taken certain steps; theIslamic Development Bank (IDB) recently echoed theneed for a Global Shari’a advisory board that offersgreater uniformity to the Islamic finance industry. Also,the Association of Shari’a Advisors in Islamic Finance(ASAS) was officially registered in 2011 with theobjective of establishing a global entity to ensureprofessionalism among Shari’a advisors and experts in Islamic Finance. The aim of the Association is to“develop Malaysia as a reference center for Islamicfinancial transactions” and the country is working on the development of human capital in Islamic financeand is establishing the necessary Shari’a, legal,regulatory and supervisory frameworks. The success of such associations will rest heavily on individualgovernments and local regulators to enforce thestandards within their jurisdictions.

ConclusionIt is imperative for the Islamic banking industry to focuson the development of products that foster marketintegration and attract investors and entrepreneurs tothe risk-return characteristics of the product rather thanconcentrating only on its Shari’a compliance. Islamicbanks need to invest in the research and thedevelopment of new products that are acceptable by a“Global Shari’a Board.” At the moment, there is a

dilemma as Shari’a opinion is diversified, leading tosituations where one school of thought may approve aproduct or service as being Shari’a-compliant only for itto be rejected by another school of thought. A big steptowards achieving harmony would be to set up a centralboard at a global level with representation from alldifferent schools of thought.

For harmonizing standards and structures, the industrydoes encourage ijtihad in the global community through international conferences and convocations.Organizations such as the Islamic Financial ServicesBoard (IFSB) and the Accounting and AuditingOrganisations for Islamic Financial Institutions (AAOIFI)have been formed to recommend principles and industry best practices at global levels. However, theseorganizations unfortunately have no binding powers to implement their standards on the industry and theymerely develop recommendations. If Islamic banking is to achieve its potential, it needs to be supported by governments and regulators. Most importantly, all aspects of Shari’a compliance need to be properlydefined; ultimately the harmonization of Shari’acompliance is a critically important component toensuring the stability, which is intrinsic to the Islamicfinance model.

by Bhavin Shah, Director, Forensic, Deloitte CorporateFinance Limited and Saad Qureshi, Manager, Forensic,Deloitte Corporate Finance Limited (regulated by theDubai Financial Services Authority)

The harmonization of Shari’a complianceis a critically important component toensuring the stability, which is intrinsic to the Islamic finance model

Islamic banking

Deloitte | A Middle East Point of View | Fall 2015 | 19

Mixin’ it upCommercialization opportunitiesin GCC sports venues

Sports venue operators have become increasinglycreative in their efforts to identify additional revenuestreams by capitalizing on the needs of the localcommunity and market. In this article we explore whichopportunities are available in the Middle East regionand steps to introduce these complementary activitiesas part of the sports venue’s value proposition.

The Gulf Cooperation Council (GCC) region has theopportunity to develop broader attractive and sustainablecommercial offers at sport venues. Traditionally theregional sports venue operators (e.g. sports clubs andsport governing bodies) have focused their efforts oncustomary sporting events. The region has recently startedto explore other commercial opportunities not related tosporting events such as business and cultural events,restaurants facilities, rental of commercial spaces andother retail opportunities.

Operators are facing significant challenges to exploit thesenew commercial opportunities. The common challenges

include operational and logistical complexities, lack ofsuitably qualified and experienced professionals andincompatibility of traditional European approaches tosupplemental revenue generation with local factors suchas climatic conditions and cultural norms. Early selectionand planning of the commercial uses are key to addresssome of these challenges.

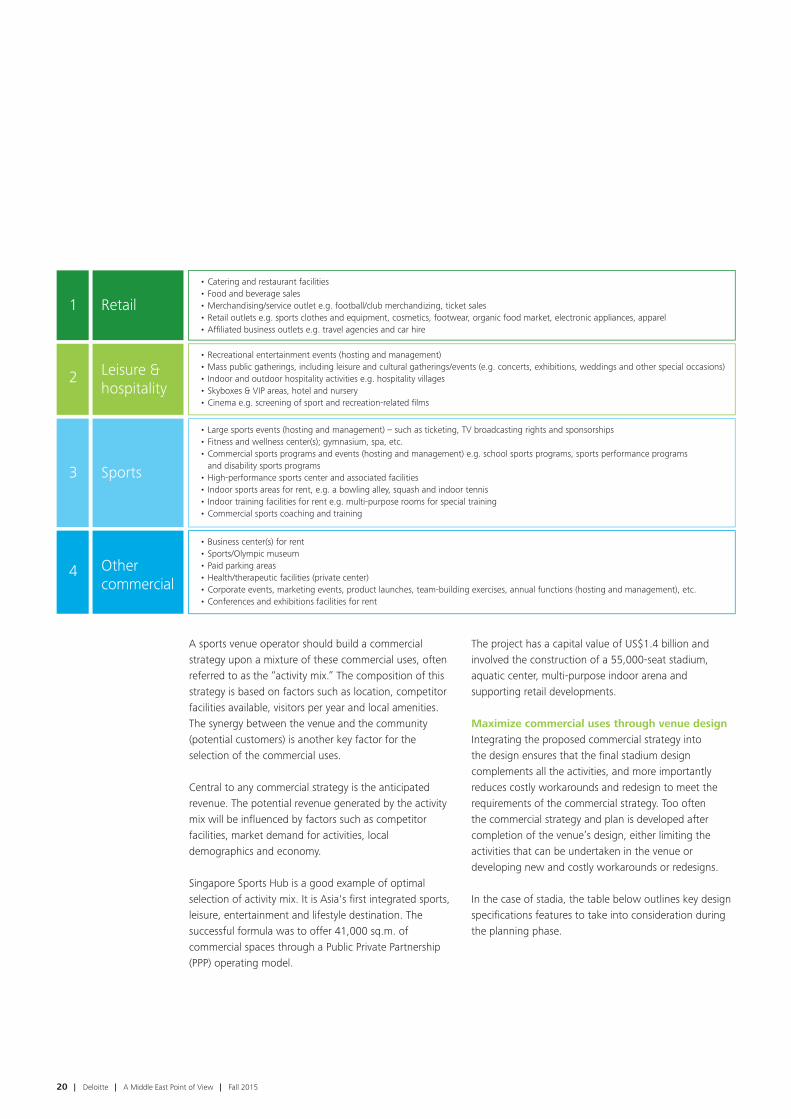

Commercial uses available and selectionThe commercial uses available can be classified into four categories: retail, leisure and hospitality, sports andother commercial. Table 1 lists a selection of the typicalcommercial uses for sports venues for each category.

Sports

Retail1

2

3

4

• Catering and restaurant facilities• Food and beverage sales• Merchandising/service outlet e.g. football/club merchandizing, ticket sales• Retail outlets e.g. sports clothes and equipment, cosmetics, footwear, organic food market, electronic appliances, apparel • Affiliated business outlets e.g. travel agencies and car hire

• Recreational entertainment events (hosting and management)• Mass public gatherings, including leisure and cultural gatherings/events (e.g. concerts, exhibitions, weddings and other special occasions)• Indoor and outdoor hospitality activities e.g. hospitality villages• Skyboxes & VIP areas, hotel and nursery • Cinema e.g. screening of sport and recreation-related films

• Large sports events (hosting and management) – such as ticketing, TV broadcasting rights and sponsorships• Fitness and wellness center(s); gymnasium, spa, etc.• Commercial sports programs and events (hosting and management) e.g. school sports programs, sports performance programs and disability sports programs• High-performance sports center and associated facilities• Indoor sports areas for rent, e.g. a bowling alley, squash and indoor tennis• Indoor training facilities for rent e.g. multi-purpose rooms for special training• Commercial sports coaching and training

• Business center(s) for rent• Sports/Olympic museum• Paid parking areas • Health/therapeutic facilities (private center)• Corporate events, marketing events, product launches, team-building exercises, annual functions (hosting and management), etc. • Conferences and exhibitions facilities for rent

Leisure &hospitality

Sports

Othercommercial

20 | Deloitte | A Middle East Point of View | Fall 2015

A sports venue operator should build a commercialstrategy upon a mixture of these commercial uses, oftenreferred to as the “activity mix.” The composition of thisstrategy is based on factors such as location, competitorfacilities available, visitors per year and local amenities.The synergy between the venue and the community(potential customers) is another key factor for theselection of the commercial uses.

Central to any commercial strategy is the anticipatedrevenue. The potential revenue generated by the activitymix will be influenced by factors such as competitorfacilities, market demand for activities, localdemographics and economy.

Singapore Sports Hub is a good example of optimalselection of activity mix. It is Asia's first integrated sports,leisure, entertainment and lifestyle destination. Thesuccessful formula was to offer 41,000 sq.m. ofcommercial spaces through a Public Private Partnership(PPP) operating model.

The project has a capital value of US$1.4 billion andinvolved the construction of a 55,000-seat stadium,aquatic center, multi-purpose indoor arena andsupporting retail developments.

Maximize commercial uses through venue design Integrating the proposed commercial strategy into the design ensures that the final stadium designcomplements all the activities, and more importantlyreduces costly workarounds and redesign to meet therequirements of the commercial strategy. Too often the commercial strategy and plan is developed aftercompletion of the venue’s design, either limiting theactivities that can be undertaken in the venue ordeveloping new and costly workarounds or redesigns.

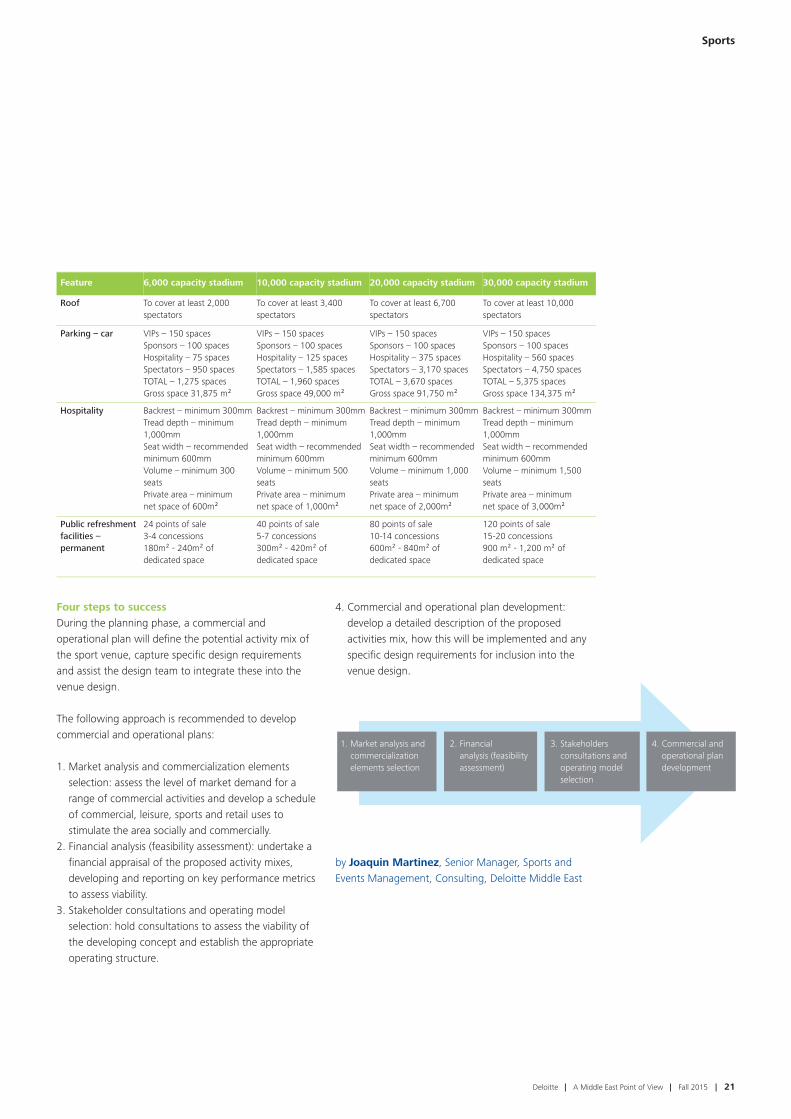

In the case of stadia, the table below outlines key designspecifications features to take into consideration duringthe planning phase.

Feature 6,000 capacity stadium 10,000 capacity stadium 20,000 capacity stadium 30,000 capacity stadium

Roof To cover at least 2,000spectators

To cover at least 3,400spectators

To cover at least 6,700spectators

To cover at least 10,000spectators

Parking – car VIPs – 150 spacesSponsors – 100 spaces Hospitality – 75 spaces Spectators – 950 spacesTOTAL – 1,275 spacesGross space 31,875 m²

VIPs – 150 spacesSponsors – 100 spaces Hospitality – 125 spaces Spectators – 1,585 spacesTOTAL – 1,960 spacesGross space 49,000 m²

VIPs – 150 spacesSponsors – 100 spaces Hospitality – 375 spaces Spectators – 3,170 spacesTOTAL – 3,670 spacesGross space 91,750 m²

VIPs – 150 spacesSponsors – 100 spaces Hospitality – 560 spaces Spectators – 4,750 spacesTOTAL – 5,375 spacesGross space 134,375 m²

Hospitality Backrest – minimum 300mmTread depth – minimum1,000mm Seat width – recommendedminimum 600mm Volume – minimum 300 seats Private area – minimum net space of 600m²

Backrest – minimum 300mmTread depth – minimum1,000mm Seat width – recommendedminimum 600mm Volume – minimum 500 seats Private area – minimum net space of 1,000m²

Backrest – minimum 300mmTread depth – minimum1,000mm Seat width – recommendedminimum 600mm Volume – minimum 1,000seats Private area – minimum net space of 2,000m²

Backrest – minimum 300mmTread depth – minimum1,000mm Seat width – recommendedminimum 600mm Volume – minimum 1,500seats Private area – minimum net space of 3,000m²

Public refreshmentfacilities –permanent

24 points of sale 3-4 concessions180m² - 240m² of dedicated space

40 points of sale 5-7 concessions300m² - 420m² of dedicated space

80 points of sale 10-14 concessions600m² - 840m² of dedicated space

120 points of sale 15-20 concessions900 m² - 1,200 m² ofdedicated space

Deloitte | A Middle East Point of View | Fall 2015 | 21

Four steps to success During the planning phase, a commercial andoperational plan will define the potential activity mix ofthe sport venue, capture specific design requirementsand assist the design team to integrate these into thevenue design.

The following approach is recommended to developcommercial and operational plans:

1. Market analysis and commercialization elementsselection: assess the level of market demand for arange of commercial activities and develop a scheduleof commercial, leisure, sports and retail uses tostimulate the area socially and commercially.

2. Financial analysis (feasibility assessment): undertake afinancial appraisal of the proposed activity mixes,developing and reporting on key performance metricsto assess viability.

3. Stakeholder consultations and operating modelselection: hold consultations to assess the viability ofthe developing concept and establish the appropriateoperating structure.

4. Commercial and operational plan development:develop a detailed description of the proposedactivities mix, how this will be implemented and anyspecific design requirements for inclusion into thevenue design.

by Joaquin Martinez, Senior Manager, Sports andEvents Management, Consulting, Deloitte Middle East

Sports

1. Market analysis and commercialization elements selection

2. Financial analysis (feasibility assessment)

3. Stakeholders consultations and operating model selection

4. Commercial and operational plan development

Deloitte | A Middle East Point of View | Fall 2015 | 23

Mining a national resource

Cyber Security

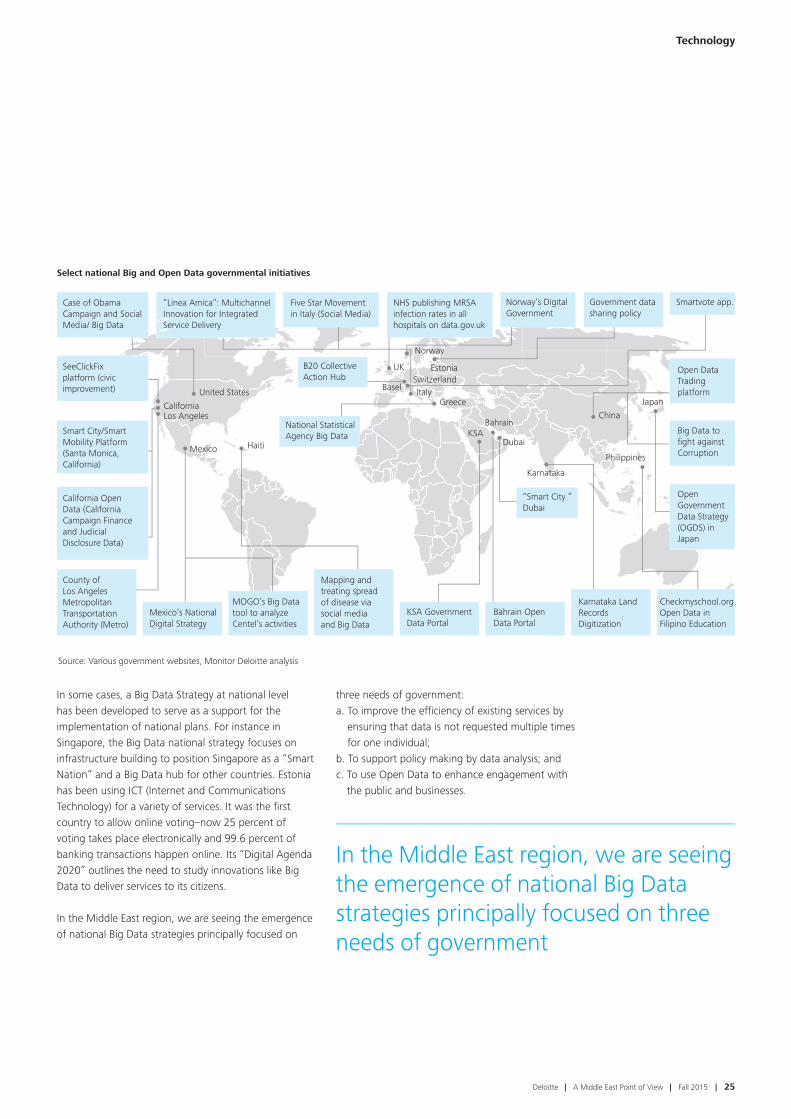

Since the Obama Administration announced the“Big Data Research and Development Initiative” in2012, a number of nations across the globe have setin motion their national Big Data plans. Improvingthe government’s ability to extract insights from alarge volume of information and complex data sets is also increasingly topping the national agendas ofgovernments in the Middle East.

Big Data

Technology

24 | Deloitte | A Middle East Point of View | Fall 2015

The regulatory debateBig Data usage, by private and public entities, is comingunder increasing scrutiny from regulators and policymakers, with data privacy clearly top of mind in terms of key concerns. While there are limited instances of“Big Data regulation” internationally it has become anincreasingly important theme for regulators within andwithout the Middle East region.

The challenge is twofold. First, how can the governmentleverage the massive amounts of data available withinits different entities to deliver better service, formulatemore predictive policies and reduce operationalinefficiencies? Secondly, how can regulators set up aregulatory framework that will encourage usage of BigData within the private sector and at the same timeprovide enough assurance for the citizens that their datais not being misused?

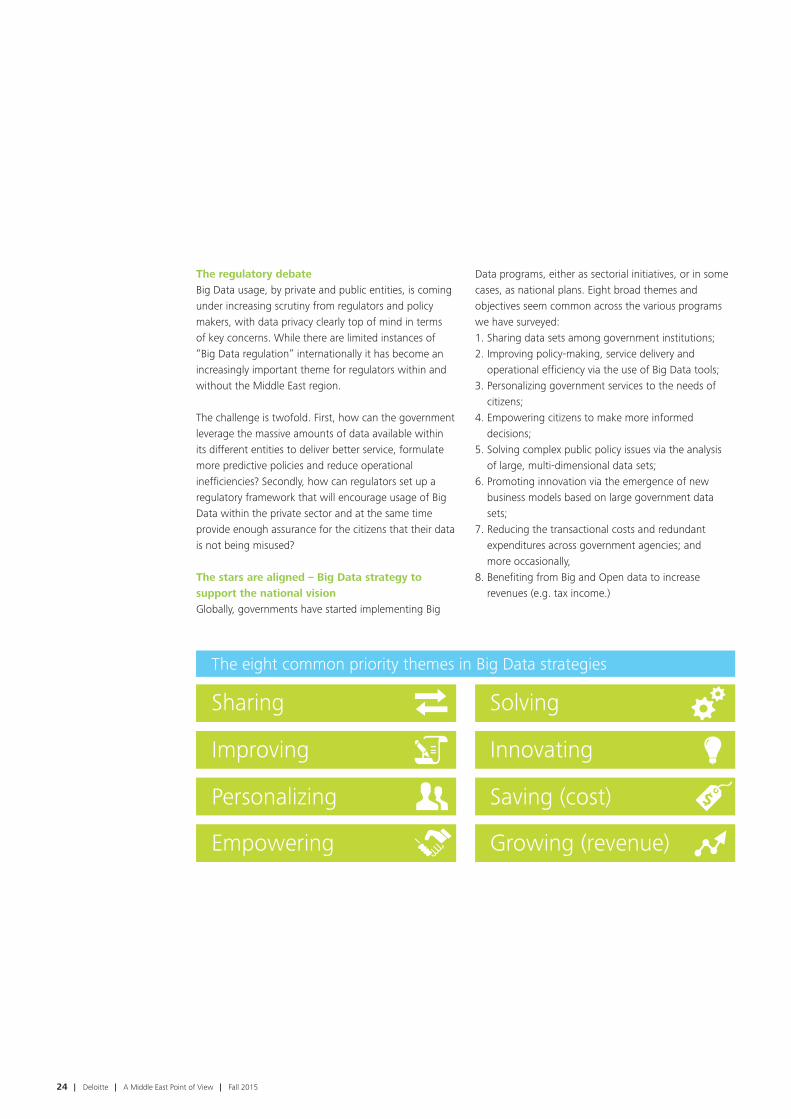

The stars are aligned – Big Data strategy tosupport the national visionGlobally, governments have started implementing Big

Data programs, either as sectorial initiatives, or in somecases, as national plans. Eight broad themes andobjectives seem common across the various programswe have surveyed: 1. Sharing data sets among government institutions; 2. Improving policy-making, service delivery and

operational efficiency via the use of Big Data tools; 3. Personalizing government services to the needs of

citizens; 4. Empowering citizens to make more informed

decisions; 5. Solving complex public policy issues via the analysis

of large, multi-dimensional data sets; 6. Promoting innovation via the emergence of new

business models based on large government datasets;

7. Reducing the transactional costs and redundantexpenditures across government agencies; and more occasionally,

8. Benefiting from Big and Open data to increaserevenues (e.g. tax income.)

Sharing

The eight common priority themes in Big Data strategies

Improving

Personalizing

Empowering

Solving

Innovating

Saving (cost)

Growing (revenue)

Select national Big and Open Data governmental initiatives

Source: Various government websites, Monitor Deloitte analysis

Case of Obama Campaign and Social Media/ Big Data

“Linea Amica”: MultichannelInnovation for IntegratedService Delivery

Five Star Movement in Italy (Social Media)

B20 Collective Action Hub

“Smart City ” Dubai

National Statistical Agency Big Data

NHS publishing MRSA infection rates in all hospitals on data.gov.uk

Norway’s Digital Government

Government data sharing policy

Smartvote app.

County of Los Angeles MetropolitanTransportation Authority (Metro)

Mexico’s National Digital Strategy

MOGO’s Big Data tool to analyze Centel’s activities

Mapping and treating spread of disease via social media and Big Data

KSA Government Data Portal

Bahrain Open Data Portal

Karnataka Land Records Digitization

Checkmyschool.orgOpen Data in Filipino Education

Open Data Trading platform

Big Data to fight against Corruption

Open Government Data Strategy(OGDS) in Japan

SeeClickFix platform (civic improvement)

Smart City/Smart Mobility Platform(Santa Monica, California)

California Open Data (CaliforniaCampaign Finance and JudicialDisclosure Data)

United States

Los Angeles

Mexico Haiti

California

ItalyBasel

UK

Norway

EstoniaSwitzerland

GreeceChina

Philippines

Japan

Dubai

Karnataka

BahrainKSA

Deloitte | A Middle East Point of View | Fall 2015 | 25

Technology

In some cases, a Big Data Strategy at national level has been developed to serve as a support for theimplementation of national plans. For instance inSingapore, the Big Data national strategy focuses oninfrastructure building to position Singapore as a “SmartNation” and a Big Data hub for other countries. Estoniahas been using ICT (Internet and CommunicationsTechnology) for a variety of services. It was the firstcountry to allow online voting–now 25 percent ofvoting takes place electronically and 99.6 percent ofbanking transactions happen online. Its “Digital Agenda2020” outlines the need to study innovations like BigData to deliver services to its citizens.

In the Middle East region, we are seeing the emergenceof national Big Data strategies principally focused on

three needs of government: a. To improve the efficiency of existing services by

ensuring that data is not requested multiple times for one individual;

b. To support policy making by data analysis; andc. To use Open Data to enhance engagement with

the public and businesses.

In the Middle East region, we are seeingthe emergence of national Big Datastrategies principally focused on threeneeds of government

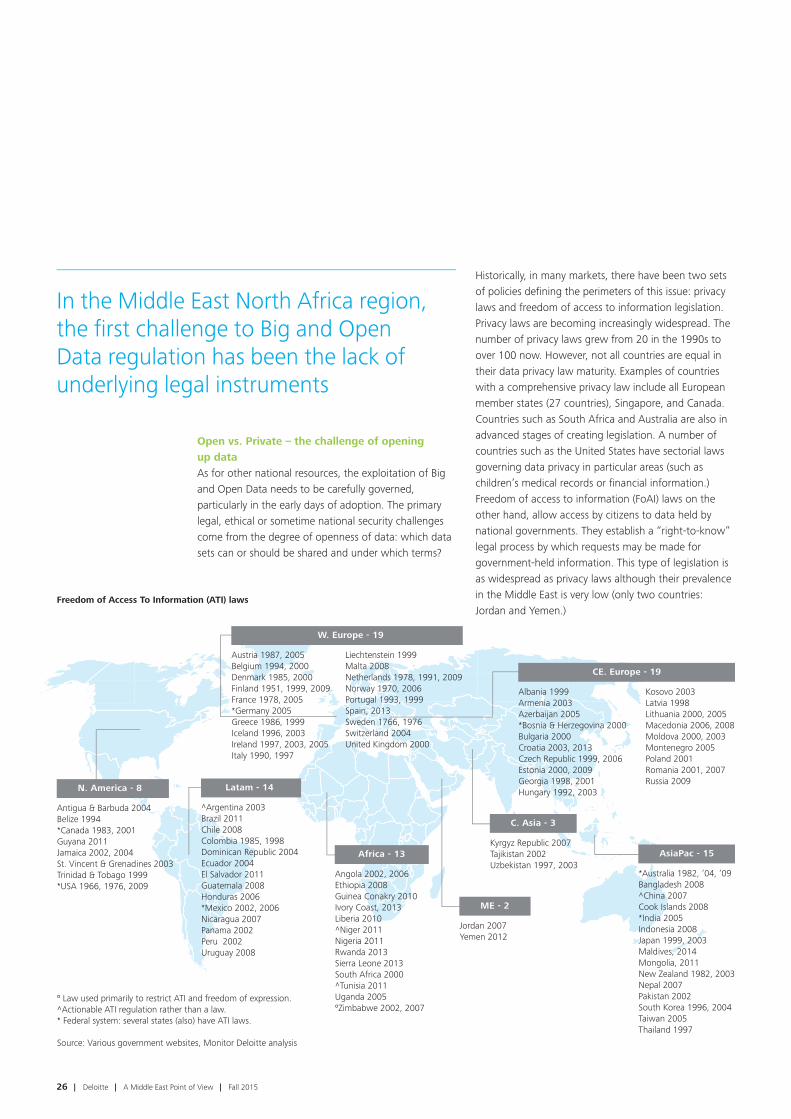

Freedom of Access To Information (ATI) laws

Antigua & Barbuda 2004Belize 1994*Canada 1983, 2001Guyana 2011 Jamaica 2002, 2004St. Vincent & Grenadines 2003Trinidad & Tobago 1999*USA 1966, 1976, 2009

º Law used primarily to restrict ATI and freedom of expression. ^Actionable ATI regulation rather than a law.* Federal system: several states (also) have ATI laws.

Source: Various government websites, Monitor Deloitte analysis

N. America - 8

^Argentina 2003Brazil 2011Chile 2008Colombia 1985, 1998Dominican Republic 2004Ecuador 2004El Salvador 2011Guatemala 2008Honduras 2006*Mexico 2002, 2006Nicaragua 2007Panama 2002Peru 2002Uruguay 2008

Latam - 14

Angola 2002, 2006Ethiopia 2008Guinea Conakry 2010Ivory Coast, 2013Liberia 2010^Niger 2011Nigeria 2011Rwanda 2013Sierra Leone 2013South Africa 2000^Tunisia 2011Uganda 2005ºZimbabwe 2002, 2007

Africa - 13

Austria 1987, 2005Belgium 1994, 2000Denmark 1985, 2000Finland 1951, 1999, 2009France 1978, 2005*Germany 2005Greece 1986, 1999Iceland 1996, 2003Ireland 1997, 2003, 2005Italy 1990, 1997

Liechtenstein 1999Malta 2008Netherlands 1978, 1991, 2009Norway 1970, 2006Portugal 1993, 1999Spain, 2013Sweden 1766, 1976Switzerland 2004United Kingdom 2000

W. Europe - 19

Albania 1999Armenia 2003Azerbaijan 2005*Bosnia & Herzegovina 2000Bulgaria 2000Croatia 2003, 2013Czech Republic 1999, 2006Estonia 2000, 2009Georgia 1998, 2001Hungary 1992, 2003

Kosovo 2003Latvia 1998Lithuania 2000, 2005Macedonia 2006, 2008Moldova 2000, 2003Montenegro 2005Poland 2001Romania 2001, 2007Russia 2009

CE. Europe - 19

Kyrgyz Republic 2007Tajikistan 2002Uzbekistan 1997, 2003

C. Asia - 3

Jordan 2007Yemen 2012

ME - 2

*Australia 1982, ‘04, ‘09Bangladesh 2008^China 2007Cook Islands 2008*India 2005Indonesia 2008Japan 1999, 2003Maldives, 2014Mongolia, 2011New Zealand 1982, 2003Nepal 2007Pakistan 2002South Korea 1996, 2004Taiwan 2005Thailand 1997

AsiaPac - 15

26 | Deloitte | A Middle East Point of View | Fall 2015

Open vs. Private – the challenge of opening up dataAs for other national resources, the exploitation of Bigand Open Data needs to be carefully governed,particularly in the early days of adoption. The primarylegal, ethical or sometime national security challengescome from the degree of openness of data: which datasets can or should be shared and under which terms?

Historically, in many markets, there have been two setsof policies defining the perimeters of this issue: privacylaws and freedom of access to information legislation.Privacy laws are becoming increasingly widespread. Thenumber of privacy laws grew from 20 in the 1990s toover 100 now. However, not all countries are equal intheir data privacy law maturity. Examples of countrieswith a comprehensive privacy law include all Europeanmember states (27 countries), Singapore, and Canada.Countries such as South Africa and Australia are also inadvanced stages of creating legislation. A number ofcountries such as the United States have sectorial lawsgoverning data privacy in particular areas (such aschildren’s medical records or financial information.)Freedom of access to information (FoAI) laws on theother hand, allow access by citizens to data held bynational governments. They establish a “right-to-know”legal process by which requests may be made forgovernment-held information. This type of legislation isas widespread as privacy laws although their prevalencein the Middle East is very low (only two countries:Jordan and Yemen.)

In the Middle East North Africa region,the first challenge to Big and Open Data regulation has been the lack ofunderlying legal instruments

Deloitte | A Middle East Point of View | Fall 2015 | 27

In contrast with data privacy laws, Open Data laws are still relatively few as their origins are more recent(post-2010) and include laws such as the 2014 Digitalaccountability and transparency act in the United States.In many cases, instead of full fledge laws, Open Datapolicies were developed, for instance the EC directive2003/98/EC on the re-use of public sector information,which took root in the FoAI laws mentioned above.

In the Middle East North Africa region, the firstchallenge to Big and Open data regulation has been the lack of underlying legal instruments. Privacy laws are being developed but do not always have a trackrecord of implementation and the limited number ofcountries with FoAI frameworks makes it even moredifficult to have Open Data laws or data sharing policiesin place. Overall the region still has a long way to go on data sharing as demonstrated by the current lowranking of most Middle East nations, with all GulfCooperation Council (GCC) countries ranked below the50th global rank in the Open Data Barometer. However,some interesting initiatives are underway across theregion–the UAE and Qatar have plans to launch orrevamp their open data portals and Saudi Arabia hasrecently launched a new Open Data portal(http://www.data.gov.sa/).

Managing data accessOpen data is however only one component in the vastrealm of applications of government Big Data. Sharinginformation among government institutions can alsolead to significant value creation across one of the eightthemes discussed above. Nevertheless, with largeamounts of data available but also scattered amongdifferent entities, it is critical to establish a structuredframework to collect, analyze and share the data.

Sharing data within government entities or between thepublic and private sectors has promoted the creation ofinnovative products and services. This becomesincreasingly of value when developing smart cities, sincesmart city services will require automated interactionsbetween public and private sector companies throughstandard data interfaces. For example when Londonreleased its maps of the tube to the public, new onlineand mobile applications were created by entrepreneursto improve the usage of the tube.

The flipside to sharing data this freely is security.Countries are often struggling to strike the balancebetween improving services and exposing the country to threats unintentionally. It is well-known that multiplestreams of open data can be overlaid to deducepotentially sensitive information. For example, it may be possible to deduce the destination and movement of oil supplies via ships from oil production data andport vessel movement data.

Technology

Open data is however only onecomponent in the vast realm ofapplications of government Big Data.Sharing information among governmentinstitutions can also lead to significantvalue creation.

28 | Deloitte | A Middle East Point of View | Fall 2015

Prevention, as the old adage recommends, is better than a cure. Governments can mitigate these risks byadequately whetting the data through a consistent andcoherent framework. It starts with putting the databroadly in buckets that mark it as open or closeddepending on the national or institutional policy.Buckets that are classified as potential for Open Datathen need to be assessed for consumption by the publicby ensuring that sensitive private or national data isrendered anonymous, or removed. The data shouldideally then go through at least one more round ofchecks by qualified data scientists that look at the risksof releasing the data sets. The broad selectionframework should be tailored to the government’spolicies.

Regulating data monetizationAnother issue that needs to be considered whenaddressing the regulatory framework of Big and OpenData is the price tag of data. The general consensus isthat Open Data is free to access and use, but not allorganizations are willing to give away their data for free.Organizations often consider their data to be part of

their Intellectual Property and are reluctant to foregoadditional revenues for the cause of open data. Telecomcompanies are a case in point as they typically sit on avariety of structured (call data, geo-location data) andunstructured data (web browsing logs, social mediaposts, app usage patterns, etc.) that has high valuewhen analyzed. For example, retailers are usually willingto pay for information that tells them the density andprofile of customers in the vicinity of their locationduring different times of the day. However, these andother types of geo-location data are very useful inproviding public services as well. In Sierra Leone,telecom data has been used to predict day-to-dayoutbreaks of Ebola and take preventative action tocontain the disease. This natural tension betweenopening data and monetizing it will need to be carefullythought through by governments in the region as theyweigh the potential costs and benefits of a free versus apay model for data access.

Capability building: data scientists are the newunicorns! With an increasing role as Big Data regulators andpromoters, a key challenge for governments in theregion will be capability building. Big Data is bringingabout a new breed of roles and job positions both in the core business and in the Information Technology (IT)departments of public and private organizations.

The analysis of real-time structured and unstructureddata requires not only sophisticated systems but alsonew resources that did not exist several years ago. The presence of data owners, governors and stewardsamong others is as much part of the sophisticated

Another issue that needs to beconsidered when addressing theregulatory framework of Big and OpenData is the price tag of data

Deloitte | A Middle East Point of View | Fall 2015 | 29

system as the mining tools, business intelligenceapplications, and server and network infrastructure. The emerging positions and roles are becoming moredifficult to fill due to the increasing need to have bothbusiness and technical knowledge and skills. Moreover,the limited existence of skilled professionals currently inthe industry’s workforce hinders effective knowledgeand skill transfer. This is eventually leading to increasedreliance on contractors and consultants, which in turnchallenges organizations in terms of skill retention andfuture capability building.

Going forward, it will be crucial for governments toinvest in building their capabilities around Big Data ifthey want to achieve tangible results from their Big Datastrategy. Although this will involve significant investmentin capturing and retaining key talents, it will alsodemand stronger awareness of Big Data and itsoperations among the government leadership as well asHuman Resource managers and talent specialists. Theprofiles required for the realization of national Big Datastrategies are not only sophisticated but also often aunique blend of skills (e.g. Physician crossed with Dataspecialist.) Data Scientists are the new unicorns of thetalent pool.

by Emmanuel Durou, Partner, Technology, Media andTelecommunications, Monitor Deloitte

Going forward, it will be crucial forgovernments to invest in building theircapabilities around Big Data if they want to achieve tangible results fromtheir Big Data strategy

Technology

Like it or not,here I amSocial media and the workplace

The figure of 1 billion active users a day as at end-August of this year, i.e. 1 in 7 of the world’s populationnow on Facebook may not be striking per se, exceptwhen compared to the figure of 1 in 9 of the world’spopulation who don’t even have access to clean water.We know that social media has changed the way thatpeople think and operate, but what do they seek out ofthis daily engagement and how can companies harnessthat drive to their own advantage?

Social media

The changing world of “Social”Social media has been changing the destiny of nationsin the last decades, eradicating entire countries’ politicalsystems, and creating the momentum for drasticchanges in entire regions. A photo or video going viralcan affect people’s perception of events, such as somephotos that have ignited outrage over the deaths ofthousands of desperate refugees and promptinghitherto blindsided countries to aid in what had provento be one of the largest humanitarian crises of thiscentury. Such stories of fundamental worldwidemobilization are a crystal clear revelation of the powerof social media channels and their impact on changingthe status quo.

Social media and enterprise social networks:identical or fraternal twins? Figures on social media platforms such as Twitter,Instagram and LinkedIn are on an exponential rise,illustrating social media’s high penetration rate as itincreasingly becomes part and parcel of people’s dailylives. But what is it that makes these platforms sosuccessful and what are people seeking from such daily engagement? Is it the technology itself or thenetworking and relationship-building part? Theknowledge-sharing one? Or is it the fear of missing out?

And do these same needs apply when it comes tohaving people use internal social media networks,referred to as Enterprise Social Networks (ESN), at theworkplace? How long will it take ESN to potentiallyoutshine their “public” twin and meet their objectives offostering collaboration, communication and knowledge-sharing among employees? Are external social mediaplatforms and enterprise social networks identical, orfraternal, twins?

Building the case for internal communicationsToday’s business leaders seek a highly engagedworkforce to support them in achieving their businessgrowth strategies at a faster pace. Hence the need andcall for action for a social media strategy that lays outplatforms, known as ESN, targeted at the firm’s internalaudiences as a primary communications tool for noting,deciding and acting on information relevant to carryingout the work and increase productivity.

Adopting ESN technologies in the workplace has been on the rise since 2011, according to DeloitteTelecommunications, Media and Technology yearlypredictions. While many enterprises have alreadyadopted ESN, many of these companies struggle torecruit users and advocates, or to engage with them.What is it that makes such companies struggle inbuilding the case for proper internal communicationsand to what extent have businesses been going social in their strategies, shifting from a social media strategyto a social business strategy?

Defined as “the set of visions, goals, plans, andresources that align social media initiatives with businessobjectives,” a social media strategy lays out thechannels, platforms, and tactics to support publishing,listening, and engagement. Such had been the hope ofmany a company that has sought to emulate, throughits enterprise social network, the success that theexternal social media platforms are witnessing. Withtime, more emphasis has been placed on the business

32 | Deloitte | A Middle East Point of View | Fall 2015

Defined as “the set of visions, goals,plans, and resources that align socialmedia initiatives with businessobjectives,” a social media strategy laysout the channels, platforms, and tacticsto support publishing, listening, andengagement

Social media

than on the media, changing the platform from “socialmedia” to “social business.” Social business is moreabout the integration of social media and socialmethodologies and processes into the organization andits day-to-day practices to build relationships and sparkconversations within and without the organization, tocreating value and driving impact to clients, talent andthe business alike.

Finding the ideal balance for social engagement There is not one best way to engage employees socially,be it in the frequency of posts, or content, or drivingconversations. What matters is finding the ideal balancefor social engagement, taking into account that even ifinternal communications are addressed to internalaudiences, they do not necessarily encompasseveryone’s varying interests i.e. they are not a one-stopshop. Internal audiences’ interests vary widely in largeorganizations. These audiences are being spread indifferent geographies, are connected to different sets ofclients, sometimes have different language preferences,and are of different leadership levels. Differentaudiences respond in different ways. What works forone category of talent may not work for anothercategory of talent. And no, there are no magic buttonsthat internal communicators can click to secure socialfollowing and interaction, or to spark conversations and increase their social engagement rates.

If internal communicators never post, they will surelynever get interactions per post. But what they do postalso matters. Much depends on the quality of posts,how relevant the messaging is, how catchy the designis, the added-value that the conversation is bringing,how it is tied to people’s performance, and how itmakes processes and procedures more efficient andstreamlined.

Today’s companies and their chief marketing officers,chief communicators, and chief internal communicatorsare looking for new levels of employee engagement and

advocacy, in more agile companies, able to move fast to face the challenges of inevitable change. Leaders inthese companies are required more and more, to betterarticulate a social business vision and strategy that goes beyond the scope and responsibility of brand,communication, marketing and, more specifically,internal communication experts’ field of expertise. It requires working in a hybrid matrix that is theorganizational platform to support cross-functionalcollaboration and cooperation and bridge the gapbetween the client and talent experience, getting themcloser towards reaching the company’s overarchingbusiness goals.

Strategy, not technology, drives digitaltransformationSuccessful social business initiatives require leadershipand behavioral changes. They hit at the core ofcompanies’ cultures and require that enterprisesembrace innovation and collaboration. Leaders of suchenterprises are not necessarily tech savvy, but they areadvocates of technology, with a clear understanding of the potential impact that adopting innovation and

Today’s companies and their chiefmarketing officers, chief communicators,and chief internal communicators arelooking for new levels of employeeengagement and advocacy, in more agile companies, able to move fast toface the challenges of inevitable change

Deloitte | A Middle East Point of View | Fall 2015 | 33

34 | Deloitte | A Middle East Point of View | Fall 2015

technology has on their businesses, as well as retainingand engaging talent. As such, social business and digitalfluency do not demand mastery of the technology.Instead, they require the ability to articulate the value of social and digital technologies to the organization'sfuture and scale it up for wider use among constituents.

A recent report conducted by Deloitte and MIT SloanManagement Review, entitled Strategy, Not Technology,drives Digital Transformation reveals that 80 percent of employees across all generations want to work for adigitally-enabled company or digital leader. In addition,more than 75 percent of respondents from digitallymature companies agree that their organizations providethe necessary skills to capitalize on digital trends.Among low maturity entities, the number drops to 19 percent.

Findings from Deloitte’s fourth annual global survey of more than 4,800 business executives across 27industries and 129 countries, reveal that the ability to digitally transform and reimagine a business isdetermined in large part by a clear digital strategysupported by leaders who foster a culture to changeand reinvent their organizations. Accordingly, it isstrategy, and not technology, that drives digitaltransformation in companies. It seems that manycompanies have been putting too much emphasis onthe technology itself that they have missed the criticaland most important factor behind successful behavioralchange that is mainly driven by leadership commitmentand the setting and implementation of a sound digitalstrategy.

Integrating social and digital strategiesThe success of such a strategy as outlined above clearlyrequires an alignment between the strategic businessgoals of a company and its organizational arrangementi.e. the support that enables the execution of a socialmedia strategy.

While the use of external social media platforms andsocial media strategies of companies have shownincreasing success, with the ability to target clientsbased on their preferences and needs, the use of ESN in companies requires a wider look at the evolution of the firms into better social businesses, and theintegration of the social aspect of the business with thedigital one. Internal communicators need to shift theirfocus from working on social media platforms in silos to developing a consistent and integrated contentstrategy that supports a cohesive digital and socialstrategy. Social media platforms should enhance talentexperience and knowledge-sharing, while driving morebusiness integration of mobile applications and intranetsas well as social media channels and platforms.

While the use of external social mediaplatforms and social media strategies of companies have shown increasingsuccess, with the ability to target clientsbased on their preferences and needs,the use of ESN in companies requires a wider look at the evolution of the firms into better social businesses

Deloitte | A Middle East Point of View | Fall 2015 | 35

What happens in Rome goes on Facebook, whathappens at work, stays at work!Do employees post on internal social media platformswith the same frequency and enthusiasm that they poston Facebook, LinkedIn or Twitter? In reality, people useexternal social media platforms differently than they useinternal ones. With a socially extrovert generation Y sokeen on taking everything in their social life out to thepublic out of peer and social pressure, it becomes morechallenging to differentiate ways of interacting withinexternal and internal social media platforms. Thischallenge requires companies to define the boundariesand draw the horizons of social media activity, laying outgovernance and risk structures that can alter as talent,as well as companies’ social and digital maturity,increases.

Fraternal twins have, after all, many things in common,yet many differences still do set them apart. Whetherexternal and internal social media platforms are identicalor fraternal twins, is not in itself the question anymore.What matters is that they are surely twins, yet withdifferent mindsets, and different expectations arise out of each one.

If what happens in Rome goes on Facebook, whathappens at work, stays at work, even if it is bound to go “social.” Business leaders should not necessarily ask“how social are my employees?” but “how social anddigital is my business?”

by Elissar Hajj, Senior Manager, Brand andCommunications, Deloitte Middle East

If what happens in Rome goes onFacebook, what happens at work, stays at work, even if it is bound to go“social.” Business leaders should notnecessarily ask “how social are myemployees?” but “how social and digital is my business?”

Social media

36 | Deloitte | A Middle East Point of View | Fall 2015

Journey toExcellence

Operational excellence

Deloitte | A Middle East Point of View | Fall 2015 | 37

The excellence agenda in the Gulf countries isincreasingly changing the context in which governmentsoperate and serve their citizens. The United ArabEmirates (UAE), for example, is seeking to position itseconomy among the most successful economies of the world by 2030. The UAE government is setting its Excellence Programs as a key priority in order toimprove their overall performance, quality and customer experience and become more competitive.

To this end, several initiatives were set up in the 1990s,such as excellence awards, recognition programs,excellence standards and e-government initiatives thathave improved service quality, efficiency, customer

experience and most importantly, competitiveness.Excellence awards in the UAE are being awarded to entities demonstrating a consistent engagement to good practices and promoting sustainableorganizational excellence across the emirate.

Most of the excellence awards and frameworks in theUAE are based on the European Foundation of QualityManagement (EFQM), which is a practical, non-prescriptive framework that provides a holistic view ofthe organization and allows leaders to understand thecause and effect between their actions and the resultsthey can achieve.

38 | Deloitte | A Middle East Point of View | Fall 2015

The EFQM Excellence framework is based on ninecriteria, five of which are ‘enablers’ (what theorganization does) and four are ‘results’ (what theorganization achieves.) The five enablers are leadership,people, strategy, partnership and resources andprocesses, products and services.

Objectives of “excellent” public sectororganizationsExcellence has several objectives that are embedded inthe economic and social visions of the public sector.These are: achieving balanced results, adding value forcustomers, creating a sustainable future, nurturing talentand developing competencies, managing with agility,harnessing creativity and innovation, and leading withintegrity.

Organizations perceive excellence as their ability toreach their fullest potential using their human, financialand physical resources. These organizations aresuccessfully able to meet their mission and visionstatements by planning and achieving balanced resultsthat meet and exceed the short- and long-termexpectations of their stakeholders.

A modern yet “excellent” public sector organization is one that identifies, categorizes and prioritizes itscustomers. In fact, this activity allows for a betterunderstanding of customers’ needs and expectationsthat the organization has to consistently understand,anticipate, fulfill, meet or even exceed by striving to be innovative and create value for them.

Increasingly, governments are asked to think ofsustainability. When making an impact, a public sectororganization needs to ensure that it does so in the long-term while advancing the economic, environmental andsocial conditions in the ecosystem it operates in.

The public sector has come to be known for itsbureaucracy and rigidity. However some governmententities have proven their agility and ability to effectivelymanage change. In fact, they respond in an effectiveand efficient manner to opportunities and threats andare able to adapt to increasingly demanding citizens.

Over time, “excellent” public sector organizations havesuccessfully demonstrated their ability to build onlessons learned to derive continuous improvements.Furthermore, they have built an environment thatnurtures and harnesses creativity and innovation, acrucial element for leading with vision and makingthings happen. Additionally, it nurtures a culture inwhich people are empowered, rewarded and recognizedfor the balanced achievement of both personal andorganizational goals.

Excellence in the public sectorWe have identified the following enablers to becommon among the most efficient public sectors acrossthe globe.

LeadershipEvery organization requires strong leadership. An“excellent” organization requires leadership that shapesand helps achieve its vision. Leaders act as role modelsmainly in their ability to adapt to the various situationstheir organization faces. Additionally, they have thecapacity to adopt change and always be ready toembrace it. While leadership is only one of the enablers,it definitely is a key success factor for other enablers aswell. In fact, leaders are a great source of inspiration tomove organizations forward and to ensure that peopleare building on any potential failures and extractinglessons learned.

The public sector has come to be knownfor its bureaucracy and rigidity. Howeversome government entities have proventheir agility and ability to effectivelymanage change.

Deloitte | A Middle East Point of View | Fall 2015 | 39

Public sector leaders have a great task to demonstratepossibilities and opportunities. They have the power aswell to create the future. As the prominent sociologistPeter Drucker rightly said, “the best way to predict thefuture is to create it.” In fact, they are those who designgovernments’ strategies and lead their successfulimplementation.

StrategyAn “excellent” organization does not have a strategyonly. It implements it and ensures that it is beingrefreshed regularly. “Excellent” organizations in the UAEhave ensured the alignment of their strategy with theirkey stakeholders’ needs and expectations and, mostimportantly, with the emirate’s strategy.

A strategy is not only a vision, a mission and a set ofmeasurable initiatives that are documented. Excellentorganizations have the ability and, perhaps moreimportantly, the agility to implement what they aim to achieve and to adapt to the changing dynamics ofthe ecosystem in which they operate. In its multi-yearinitiative, Gov2020, Deloitte identified drivers of changethat shape public sector strategies. Those include, in anutshell, the demography, the economy, the society, andthe technology. Those drivers will introduce mega shiftsin governments’ strategies by 2020.

PeopleExcellence frameworks, particularly the EFQM model,put employees at the heart of excellence. They defineclearly how the people criteria can be fulfilled byorganizations. People existed long before organizationsdid and without them, organizations would not havebeen built and would not have lasted.

From an excellence standpoint, the people factor is akey enabler that consists of empowering, involving,recognizing and rewarding employees and nurturing an organizational culture. Accordingly, organizations are invited to build the competencies that will allowpeople to produce the required results. “Excellent”organizations aim to harmonize between their goals andinterests as well as their people thanks to systems that

are well orchestrated around attraction, recruitment,selection, retention, development, deployment andremuneration. In Deloitte’s Human Capital Trends 2015report, Middle East respondents (primarily from thepublic sector) said that the highest interest fororganizations is to “reinvent” how people are beingmanaged. There is a great appetite to modernize theHuman Resources (HR) function and to introduce newconcepts that have been successful elsewhere in theworld such as employee self-service (rather than dataentry), HR data analytics, and HR business partners.

Partnership and resourcesFrom an EFQM perspective, partnership and resourcesare essential to an organization’s excellence agenda. Infact, they enable its strategy and the effective realizationof its processes. Additionally, they ensure that theorganization has the impact it hopes to have based ongood relationships with those partners and on theoptimal allocation of its available resources.

Partners are typically customers, the wider society, keysuppliers, and non-governmental organizations thatgenerally do not seek profit and share common interestsand objectives with the organization. An “excellent”organization identifies, categorizes and prioritizespartners and seeks to build a long-lasting or sustainablerelationship with them as this is mutually beneficial from

Operational excellence

Over time, “excellent” public sectororganizations have successfullydemonstrated their ability to build onlessons learned to derive continuousimprovements. Furthermore, they havebuilt an environment that nurtures andharnesses creativity and innovation.

40 | Deloitte | A Middle East Point of View | Fall 2015

various perspectives, namely cost and reputation.Excellent organizations reassess the status and priority of those relationships regularly as they may changedepending on the need of the organization, the stage of its maturity, its growth, and the context in which itoperates. Moreover, excellent organizations areinterested in those types of relationships as they areaware that there are things that they cannot achieve on their own or that can be achieved in a better wayshould they enter in a form of partnership with anotherorganization. It is crucial to plan the exchange ofexperiences, knowledge and services to achieve addedvalue for both parties, in order to support thedevelopment and institutional performance.

From a resources perspective, the one key remains the organization’s financial capabilities. An “excellent”organization is aware of those capabilities thanks toparameters and measures that are constantly updatedsuch as cash flow, turnover, cost benefit analysis, andothers. There are others as well that indicate theorganization’s capability to plan for the future and makedecisions around certain investments. The second keyresource consists of assets and facilities. An “excellent”organization manages those resources in a sustainablefashion. In fact, assets are typically managed by“excellent” organizations using methodologies and

tools that aim to increase productivity, reducethroughput times, and enhance standardization.

“Excellent” organizations are not only keen on how bestto utilize resources (particularly fixed assets). In fact, theyare increasingly conscious about the society and theenvironment. Furthermore, public sector organizationsrecognize their societal responsibilities. Some adoptstandards or frameworks that help them put things intocontext and gain control (e.g. ISO 14000, EcoManagement Audit Scheme). However, “excellent”organizations go beyond that from a corporate socialresponsibility perspective.