MIDDLE EAST NATIONAL ENERGY COMPANY...

24

www.meed.com MIDDLE EAST NATIONAL ENERGY COMPANY REVIEW Sponsored by

Transcript of MIDDLE EAST NATIONAL ENERGY COMPANY...

www.meed.com

MIDDLE EAST NATIONAL ENERGY COMPANY REVIEW

Sponsored by

2014

01 NOC Cover v2.indd 1 29/10/2013 10:11

vvwz

Recognising quality construction projects in the GCC

Join these iconic award winning projects and ensure your team get the

recognition they deserveEntry Deadline: 30 January 2014

ENTER NOW

www.meedawards.com

Burj Khalifa, UAEWinner of the GCC MEED Quality Project of the Year 2011

Winner of the GCC Building Project of the Year 2011

Pearl GTL, QatarWinner of the GCC MEED Quality Project of the Year 2012

Winner of the GCC Oil & Gas Project of the Year 2012

Dubai International Airport – Concourse A, UAEWinner of the GCC MEED Quality Project of the Year 2013

Winner of the GCC Transport Project of the Year 2013

In association with:

2014

‘‘“We are extremely excited to have won the MEED Quality Project of the Year 2013 and the GCC Transport Project of the Year for the Dubai International Airport – Concourse A. It has been an amazing experience to have our whole project team and partners recognised for all of the hard work put into the project by all team members.”

‘‘

Suzanne Al-Anani, CEO, Dubai Aviation Engineering Projects (DAEP)

For more information contact: Jibraan Abdul | E: [email protected] | T: +971 (0) 4 3902707 | www.meedawards.com

www.meed.com National oil companies 2013 | MEED | 3

CO

VER

: IAN

NAY

LOR

/ILL

US

TRAT

ION

WEB

. PH

OTO

GR

APH

: SH

UTT

ERS

TOC

K

Overview

3 Overview

6 Algeria’s Sonatrach

7 Bahrain Petroleum Company

8 Egypt’s EGPC, Egas and Ganope

9 National Iranian Oil Company

10 Iraq’s national oil companies

12 Kuwait Petroleum Corporation

13 Libya’s National Oil Corporation

14 Petroleum Development Oman

15 Qatar Petroleum

17 Saudi Aramco

19 Syrian Petroleum Company

20 Tunisia’s Etap

21 Abu Dhabi National Oil Company

CONTENTS

CONTACTSMEED HEAD OFFICEAl-Thuraya Tower 1, 20th Floor, Offi ce 2004, Dubai Media City, PO Box 25960, Dubai, UAETel +971 (0)4 390 0045Fax +971 (0)4 368 8025Email: fi [email protected]

EDITORIAL Editorial Director Richard Thompson +971 (0)4 433 1426richard.thompson@Editor (MEED magazine)Elizabeth Bains +971 (0)4 433 1423elizabeth.bains@Supplements EditorAustyn Allison +971 (0)4 374 8191austyn.allison@Production Editor Ken Campbell +971 (0)4 375 5012ken.campbell@Sub Editor Ananda Shakespeare +971 (0)4 433 1422ananda.shakespeare@Sub Editor Sneha Abraham +971 (0)4 433 2807sneha.abraham@Art Editor Martin Staniszewski +971 (0)4 375 7988martin.staniszewski@Contributors Nancy el-Khory, Marianne Makdisi, Peter Salisbury

ADVERTISEMENT SALES Head of AdvertisingGary Povey +971 (0)4 390 0046/gary.povey@Head of SupplementsVictoria James +971 (0)4 375 1621/+971 (0)56 644 5227victoria.james@Saudi Arabia Enquiries Ali Jaber +966 (0)1 479 7692/+971 (0)50 455 9153ali.jaber@Sales Support and Europe EnquiriesMonica D’Souza +971 (0)4 390 0698Monica.dsouza@

CUSTOMER SERVICESRetention and Client Relations ManagerMariam Mahmood +971 (0)4 375 5606 mariam.mahmood@

MEED SUBSCRIPTION SERVICES Tel +44 (0)1858 438 837 Fax +44 (0)1858 461 [email protected]

TOP RIGHT GROUP HEAD OFFICEThe Prow, 1 Wilder Walk, London W1B 5AP, UKTel +44 (0)20 7715 6000 For a full list of reader services, editorial and advertising contacts visit www.meed.com

All rights reserved © 2013 MEED Media FZ LLC, An EMAP Service – part of Top Right Group Printed by Headley Brothers Ltd, UKRegistered as a newspaper with the Post Offi ceISSN 0047-7238

Member of the Audit Bureau of Circulation

Two and a half years on from the Arab uprisings of 2011, and fi ve years since the global fi nancial crisis started to

bite, the Middle East and North Africa (Mena) region retains its geopolitical signifi cance. There are many reasons why the region is so important to the international political system and the global economy, but at the crux lies the one thing it has in abundance, and which keeps the global economy moving: energy.

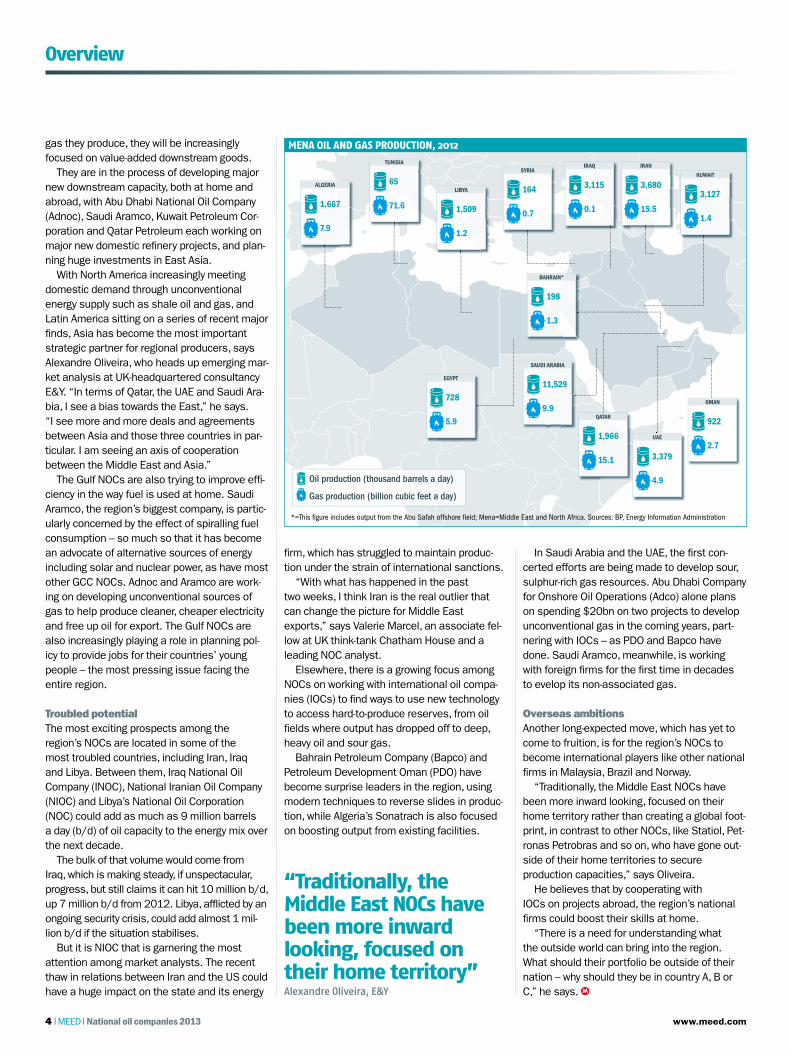

The Mena region is home to 54.4 per cent of the world’s oil and 40.5 per cent of gas reserves, according to the UK’s BP, and produces a 35 per cent of global oil supply.

The Gulf, the most resource-rich area in the region, accounts for 45 per cent of oil reserves and about a quarter of all oil produc-tion worldwide.

As the global economy moves back into gear and demand for oil and gas continues to increase – rising above 90 million barrels a day (b/d) for the fi rst time in 2013 and likely to

A NEW ERA FOR MENA NATIONAL OIL COMPANIES

top 100 million b/d within the next decade, according to the Paris-based International Energy Agency (IEA) – and oil prices remain steady around the $100 a barrel mark, regional hydrocarbons output will be crucial to making sure that the world remains well supplied.

At the heart of efforts to maintain and increase output will be the region’s national oil companies (NOCs). And while the world’s dependency on Mena oil is changing, the way NOCs operate is also shifting.

Peak productionBy 2020, the Gulf’s oil and gas producers will almost without exception have reached produc-tion capacity targets that they currently have no intention of surpassing.

As North America moves towards energy independence, those same NOCs will be paying more and more attention to East Asia, which continues to be the main driver of global demand. To extract more value from the oil and

03-04 Intro.indd 3 29/10/2013 10:10

www.meed.com4 | MEED | National oil companies 2013

Overview

“Traditionally, the Middle East NOCs have been more inward looking, focused on their home territory”Alexandre Oliveira, E&Y

gas they produce, they will be increasingly focused on value-added downstream goods.

They are in the process of developing major new downstream capacity, both at home and abroad, with Abu Dhabi National Oil Company (Adnoc), Saudi Aramco, Kuwait Petroleum Cor-poration and Qatar Petroleum each working on major new domestic refi nery projects, and plan-ning huge investments in East Asia.

With North America increasingly meeting domestic demand through unconventional energy supply such as shale oil and gas, and Latin America sitting on a series of recent major fi nds, Asia has become the most important strategic partner for regional producers, says Alexandre Oliveira, who heads up emerging mar-ket analysis at UK-headquartered consultancy E&Y. “In terms of Qatar, the UAE and Saudi Ara-bia, I see a bias towards the East,” he says. “I see more and more deals and agreements between Asia and those three countries in par-ticular. I am seeing an axis of cooperation between the Middle East and Asia.”

The Gulf NOCs are also trying to improve effi -ciency in the way fuel is used at home. Saudi Aramco, the region’s biggest company, is partic-ularly concerned by the effect of spiralling fuel consumption – so much so that it has become an advocate of alternative sources of energy including solar and nuclear power, as have most other GCC NOCs. Adnoc and Aramco are work-ing on developing unconventional sources of gas to help produce cleaner, cheaper electricity and free up oil for export. The Gulf NOCs are also increasingly playing a role in planning pol-icy to provide jobs for their countries’ young people – the most pressing issue facing the entire region.

Troubled potentialThe most exciting prospects among the region’s NOCs are located in some of the most troubled countries, including Iran, Iraq and Libya. Between them, Iraq National Oil Company (INOC), National Iranian Oil Company (NIOC) and Libya’s National Oil Corporation (NOC) could add as much as 9 million barrels a day (b/d) of oil capacity to the energy mix over the next decade.

The bulk of that volume would come from Iraq, which is making steady, if unspectacular, progress, but still claims it can hit 10 million b/d, up 7 million b/d from 2012. Libya, affl icted by an ongoing security crisis, could add almost 1 mil-lion b/d if the situation stabilises.

But it is NIOC that is garnering the most attention among market analysts. The recent thaw in relations between Iran and the US could have a huge impact on the state and its energy

fi rm, which has struggled to maintain produc-tion under the strain of international sanctions.

“With what has happened in the past two weeks, I think Iran is the real outlier that can change the picture for Middle East exports,” says Valerie Marcel, an associate fel-low at UK think-tank Chatham House and a leading NOC analyst.

Elsewhere, there is a growing focus among NOCs on working with international oil compa-nies (IOCs) to fi nd ways to use new technology to access hard-to-produce reserves, from oil fi elds where output has dropped off to deep, heavy oil and sour gas.

Bahrain Petroleum Company (Bapco) and Petroleum Development Oman (PDO) have become surprise leaders in the region, using modern techniques to reverse slides in produc-tion, while Algeria’s Sonatrach is also focused on boosting output from existing facilities.

In Saudi Arabia and the UAE, the fi rst con-certed efforts are being made to develop sour, sulphur-rich gas resources. Abu Dhabi Company for Onshore Oil Operations (Adco) alone plans on spending $20bn on two projects to develop unconventional gas in the coming years, part-nering with IOCs – as PDO and Bapco have done. Saudi Aramco, meanwhile, is working with foreign fi rms for the fi rst time in decades to evelop its non-associated gas.

Overseas ambitionsAnother long-expected move, which has yet to come to fruition, is for the region’s NOCs to become international players like other national fi rms in Malaysia, Brazil and Norway.

“Traditionally, the Middle East NOCs have been more inward looking, focused on their home territory rather than creating a global foot-print, in contrast to other NOCs, like Statiol, Pet-ronas Petrobras and so on, who have gone out-side of their home territories to secure production capacities,” says Oliveira.

He believes that by cooperating with IOCs on projects abroad, the region’s national fi rms could boost their skills at home.

“There is a need for understanding what the outside world can bring into the region. What should their portfolio be outside of their nation – why should they be in country A, B or C,” he says.

MENA OIL AND GAS PRODUCTION, 2012

ALGERIA

IRAN

BAHRAIN*

OMAN

KUWAIT

QATAR

SAUDI ARABIA

UAE

IRAQSYRIA

EGYPT

LIBYA

TUNISIA

1,667

3,680

198

922

3,127

1,966

11,529

3,379

3,115164

728

1,509

65

7.9

15.5

1.3

2.7

1.4

15.1

9.9

4.9

0.10.7

5.9

1.2

71.6

*=This fi gure includes output from the Abu Safah offshore fi eld; Mena=Middle East and North Africa. Sources: BP, Energy Information Administration

Gas production (billion cubic feet a day)

Oil production (thousand barrels a day)

03-04 Intro.indd 4 29/10/2013 10:10

Visit the Jotachar JF750 team at Adipec 2013 Hall 12, Stand number 12166 beside the Media Hub

Next generation Epoxy Passive Fire Protection

• Reduces installation cost • No cost of mesh • No cost for installing mesh • Reduced labour costs

Saves time. Saves money.• Faster project completion• Potential single coat application• Fewer installation days• Less man hours

jotun.com

www.meed.com6 | MEED | National oil companies 2013

Algeria

BackgroundSonatrach began life 50 years ago as Algeria’s first state-owned energy com-

pany, taking control of the small stakes the gov-ernment had in the country’s oil fields, which were operated by French and American firms, and helping to establish the North African state as the first liquefied natural gas (LNG) exporter in the world.

Following the Arab-Israeli war of 1967, Sonat-rach nationalised the country’s refining and export facilities, later taking over a minimum stake of 51 per cent of Algeria’s oil and gas fields – a process that at one stage meant France’s Total was the only major international oil com-pany (IOC) operating in the country.

From the mid-1980s onwards, Sonatrach began to work with IOCs on a number of major projects, including a series of huge gas produc-tion and export schemes that have helped to make Algeria one of the world’s most important gas exporters. The country is home to the world’s eighth-largest gas reserves, but gas pro-duction has been in decline since 2005.

Sonatrach has been hit by both scandal and tragedy in recent years. In 2010, the company’s longtime chief executive officer Mohamed Meziane was abruptly sacked and charged with corruption.

A deadly terrorist attack in 2013 on the firm’s In Amenas facility then led to questions being asked about security at its production sites.

Role in Algeria’s economyOil and gas exports are crucial to Algeria’s econ-omy, accounting for more than 98 per cent of all exports, and hence the majority of the country’s foreign currency reserves. More than two thirds of all government revenues come from the hydrocarbons sector.

Much of Algeria’s non-oil growth is driven by state spending, making the money earned by Sonatrach doubly important.

The firm is also Algeria’s primary economic brand. It is the biggest company in Algeria and Africa, earning revenues of $58bn in 2011. Sonatrach employs about 120,000 workers, the vast majority of whom are Algerians.

Role in the global economyAlgeria was the world’s sixth-largest exporter of natural gas in 2012, and the 15th-biggest oil exporter. The bulk of its oil and gas is sold to European markets, meaning Sonatrach is a par-

SonAtrAch Algeria’s state-owned energy giant plans to invest $80bn by 2016

Founded: 1963CEO: Abdelhamid ZerguineTel: (+213) 2 154 8011Web: www.sonatrach.com

AlgeriA gDP by Sector, 2012

MAjor hyDrocArbonS ProjectS

AlgeriA oil AnD gAS Sector, 2012

Source: African Development BankSource: BP

BP=British Petroleum; LNG=Liquefied natural gas. Source: MEED Projects

Mining

Public administration, education, health and social work, community, social and personal services

389

8

10 %11 16

Construction

Agriculture, hunting, forestry and fishing

Wholesale and retail trade, hotels and restaurants

Manufacturing 4 Finance, real estate and business services 3

Electricity, gas and water 1

Transport, storage and communication

Oil production (thousand barrels a day)

1,667

Gas production (billion cubic feet a day)

7.9

Scheme Client TypeCost ($m) Status

Gassi Touil Integrated LNG Project: Arzew LNG plant

Sonatrach Gas export 4,500 Under commissioning

Gassi Touil Integrated LNG Project: Upstream package

Sonatrach Gas export 2,800 Under commissioning

Arzew Fertiliser Complex Sonatrach/Bahwan Group Petrochemicals 2,400 Under commissioning

In Salah Gas Compression Project: Southern gas fields

Sonatrach/BP/Statoil Gas production 1,200 Under review

ticularly important partner for the eurozone coun-tries and plays a key role in maintaining the bal-ance of the global gas market.

StrategySonatrach plans to spend $80bn between 2012 and 2016, much of that on exploration for new upstream gas production and on using enhanced production techniques to maintain and increase output from existing facilities. The company also hopes to revamp its refineries at Skikda, Arzew and Algiers.

Overseas ambitionsSonatrach is well on its way to becoming an international player, with investments in France, Portugal, Spain and Peru, mainly in gas trans-portation infrastructure and power plants. It is also exploring for oil and gas in Africa; the com-pany has concessions in Libya, Mali, Mauritania and Tunisia.

“Sonatrach is well on its way to becoming an international player, with investments in France, Portugal, Spain and Peru”

06 AlgeriaSUBBED.indd 6 29/10/2013 10:09

www.meed.com National oil companies 2013 | MEED | 7

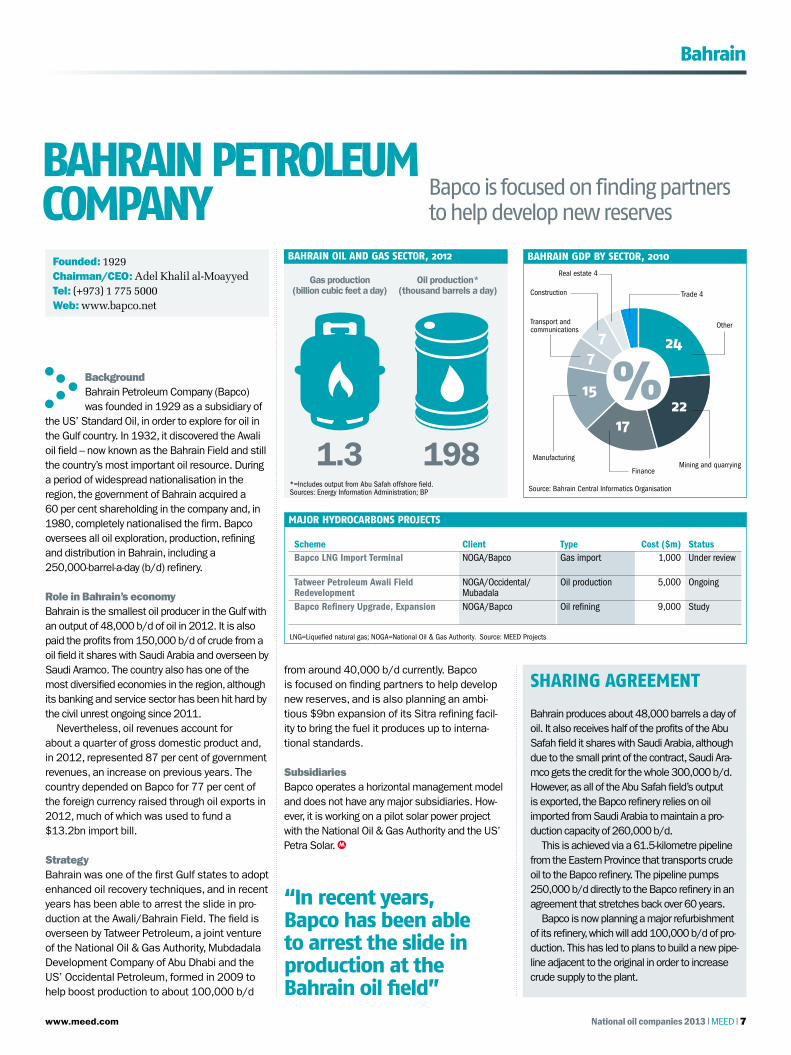

BackgroundBahrain Petroleum Company (Bapco) was founded in 1929 as a subsidiary of

the US’ Standard Oil, in order to explore for oil in the Gulf country. In 1932, it discovered the Awali oil field – now known as the Bahrain Field and still the country’s most important oil resource. During a period of widespread nationalisation in the region, the government of Bahrain acquired a 60 per cent shareholding in the company and, in 1980, completely nationalised the firm. Bapco oversees all oil exploration, production, refining and distribution in Bahrain, including a 250,000-barrel-a-day (b/d) refinery.

Role in Bahrain’s economyBahrain is the smallest oil producer in the Gulf with an output of 48,000 b/d of oil in 2012. It is also paid the profits from 150,000 b/d of crude from a oil field it shares with Saudi Arabia and overseen by Saudi Aramco. The country also has one of the most diversified economies in the region, although its banking and service sector has been hit hard by the civil unrest ongoing since 2011.

Nevertheless, oil revenues account for about a quarter of gross domestic product and, in 2012, represented 87 per cent of government revenues, an increase on previous years. The country depended on Bapco for 77 per cent of the foreign currency raised through oil exports in 2012, much of which was used to fund a $13.2bn import bill.

StrategyBahrain was one of the first Gulf states to adopt enhanced oil recovery techniques, and in recent years has been able to arrest the slide in pro-duction at the Awali/Bahrain Field. The field is overseen by Tatweer Petroleum, a joint venture of the National Oil & Gas Authority, Mubdadala Development Company of Abu Dhabi and the US’ Occidental Petroleum, formed in 2009 to help boost production to about 100,000 b/d

Bapco is focused on finding partners to help develop new reserves

Bahrain Petroleum ComPany

Bahrain

Founded: 1929Chairman/CEO: Adel Khalil al-MoayyedTel: (+973) 1 775 5000 Web: www.bapco.net

Bahrain GDP By seCtor, 2010

major hyDroCarBons ProjeCts

Bahrain oil anD Gas seCtor, 2012

Source: Bahrain Central Informatics Organisation*=Includes output from Abu Safah offshore field. Sources: Energy Information Administration; BP

LNG=Liquefied natural gas; NOGA=National Oil & Gas Authority. Source: MEED Projects

Other

Mining and quarryingFinance

24

22

77

15 %17

Transport and communications

Construction

Real estate 4

Manufacturing

Trade 4

Oil production*(thousand barrels a day)

198

Gas production (billion cubic feet a day)

1.3

Scheme Client Type Cost ($m) StatusBapco LNG Import Terminal NOGA/Bapco Gas import 1,000 Under review

Tatweer Petroleum Awali Field Redevelopment

NOGA/Occidental/Mubadala

Oil production 5,000 Ongoing

Bapco Refinery Upgrade, Expansion NOGA/Bapco Oil refining 9,000 Study

from around 40,000 b/d currently. Bapco is focused on finding partners to help develop new reserves, and is also planning an ambi-tious $9bn expansion of its Sitra refining facil-ity to bring the fuel it produces up to interna-tional standards.

SubsidiariesBapco operates a horizontal management model and does not have any major subsidiaries. How-ever, it is working on a pilot solar power project with the National Oil & Gas Authority and the US’ Petra Solar.

“in recent years, Bapco has been able to arrest the slide in production at the Bahrain oil field”

Bahrain produces about 48,000 barrels a day of oil. It also receives half of the profits of the Abu Safah field it shares with Saudi Arabia, although due to the small print of the contract, Saudi Ara-mco gets the credit for the whole 300,000 b/d. However, as all of the Abu Safah field’s output is exported, the Bapco refinery relies on oil imported from Saudi Arabia to maintain a pro-duction capacity of 260,000 b/d.

This is achieved via a 61.5-kilometre pipeline from the Eastern Province that transports crude oil to the Bapco refinery. The pipeline pumps 250,000 b/d directly to the Bapco refinery in an agreement that stretches back over 60 years.

Bapco is now planning a major refurbishment of its refinery, which will add 100,000 b/d of pro-duction. This has led to plans to build a new pipe-line adjacent to the original in order to increase crude supply to the plant.

sharing agreement

07 Bahrain.indd 7 29/10/2013 10:08

www.meed.com8 | MEED | National oil companies 2013

Egypt

BackgroundAlthough not widely considered a major oil and gas player, Egypt is one of the biggest

producers in the Middle East and North Africa region that is not part of oil producers group Opec. It is also the second-biggest producer of gas in Africa and the continent’s largest refiner.

All of the country’s oil exploration and produc-tion operations are overseen by Egypt General Petroleum Company (EGPC), while a separate state-run firm, Egypt Natural Gas Holding Com-pany (Egas), created in 2001, is in charge of gas exploration and production. In 2003, the Oil Minis-try set up the South Valley Development Com-pany, since renamed Ganoub el-Wadi (Ganope), to promote oil and gas exploration and development activities in Upper Egypt.

EGPC was created in 1956 and was known at the time as the General Corporation of Petroleum Affairs. It was given its current name in 1976. The company ramped up oil production in the 1970s and 1980s, with output peaking at 920,000 bar-rels a day (b/d) in 1993-94. Since then, it has worked with international oil companies (IOCs) to stabilise output, using the addition of natural gas liquids to help maintain production levels. Egas has been the success story of the past decade, overseeing a huge increase in gas production from practically nothing in the early 2000s to 5.9 billion cubic feet a day in 2012.

Role in Egypt’s economyThe Egyptian economy is relatively diversified, as is the government’s revenue base. EGPC accounted for an estimated 2.5 per cent of eco-nomic output in Egypt in 2010 and 2011, while the money earned by the company represented about 12 per cent of government revenues. Nev-ertheless, the national oil companies (NOCs) play an important part in keeping the economy afloat. EGPC and Egas provide most of the oil and gas

used to produce hugely subsidised fuel and elec-tricity for Egyptians, which would be unaffordable to the government if the energy was imported. Oil and gas exports have also historically been the main source of the foreign currency used to stabi-lise the Egyptian pound and pay the country’s massive import bill. Subsidies place an enor-mous strain on EGPC, which oversees much of the country’s refining infrastructure and must organise fuel imports when necessary.

Role in the global economyEgypt consumes much of the oil it produces, but its gas is exported, via the Arab gas pipeline and as liquefied natural gas, to markets in Europe and Asia. However, rising domestic gas consumption – mainly for electricity – is denting its status as a supplier to the international market.

Egypt’s NOCs play a significant role in the trans-portation of oil. The Suez-Mediterranean (Sumed) pipeline, a joint venture of EGPC, Abu Dhabi

EGPC, EGas and GanoPE Egypt’s national oil companies help

keep the country’s economy afloat

Founded: 1956 (EGPC); 2001 (Egas); 2004 (Ganope)Chairman: Tarek el-Molla (EGPC); Taher Abdel Rahman (Egas); Sherif Ismail Mohamed (Ganope)Tel: (+202) 2 706 5445Web: www.petroleum.gov.eg

EGYPt GdP bY sECtor, 2012

Major hYdroCarbons ProjECts

EGYPt oil and Gas sECtor, 2012

GDP=Gross domestic product. Source: African Development BankSource: BP

BP=British Petroleum. Source: MEED Projects

Extractive industries

Agriculture, forestry and fishing

16

1510

95

10%14

15

General government services

Finance and insurance

Transportation, communication and information

Manufacturing

Social services 4ConstructionElectricity, water and sanitation 2

Wholesale, retail trade and real estate ownership

Oil production (thousand barrels a day)

728

Gas production (billion cubic feet a day)

5.9

Scheme Client TypeCost ($m) Status

West Nile Delta Development Project: North Alexandria Development

BP/RWE Dea Oil production 9,000 Study

Tahrir Petrochemicals Complex Egyptian Hydrocarbon Company

Petrochemicals 4,250 Under construction

Mostorod New Refinery Citadel Capital Refining 3,700 Under construction

Ain Sokhna Refinery Project Ain Sokhna Refining & Petroleum Company

Refining 3,400 On hold

National Oil Company and Kuwaiti investors, car-ries 2.35 million b/d of oil between the Red Sea and the Mediterranean.

StrategyEgypt’s political system is in flux, and although its NOCs were able to continue operations throughout 2011 and 2012, it is hard to know whether strate-gies adopted before the overthrow of President Hosni Mubarak will be maintained.

SubsidiariesEGPC oversees a number of joint-venture compa-nies with IOCs and most of the country’s major refiners. Key subsidiaries include General Petro-leum Company, Suez Oil Processing Company. Cairo Petroleum Refining Company, El-Nasr Petro-leum Company, Alexandria Petroleum Company, Egyptian Petrochemicals Holding Company, Amerya Petroleum Refining Company and Assuit Petroleum Refining Company.

08 EgyptSUBBED.indd 8 29/10/2013 10:08

www.meed.com National oil companies 2013 | MEED | 9

BackgroundIran’s state-run oil company traces its roots back to the early 20th century,

when William Knox D’Arcy was awarded the coun-try’s first oil exploration concession. Oil was dis-covered in 1908, by which time the UK’s Burmah Oil held most of the rights to the concession. In 1935, the Burmah subsidiary Anglo-Persian Oil Company was renamed Anglo-Iranian Oil Com-pany, and in 1951 the company was nationalised by then Prime Minister Mossadegh – an action that led to his ousting in a 1953 coup d’etat.

Overall oil production in Iran peaked at 6.6 mil-lion barrels a day (b/d) in 1976, but fell after the 1979 Islamic Revolution. National Iranian Oil Company (NIOC) can currently produce about 3.8 million b/d, but production fell to an esti-mated 3.7 million b/d in 2012.

Iran’s South Pars Field forms the world’s largest offshore gas reservoir along with Qatar’s North Field, and is developed by NIOC subsidiaries.

Role in Iran’s economyThe hydrocarbons sector accounted for about 27 per cent of all economic output in Iran in the fiscal year 2011/12, but made up 60 per cent of all government revenues. Tehran has been work-ing on a series of plans to wean the government off its oil dependence, and revenues have dropped substantially in recent years as US and EU sanctions have bitten into production levels.

Role in the global economyIran was once one of the biggest oil producers in the world, and still has the world’s third-largest oil reserves and third-largest gas reserves. But mis-management since 1979 and, more recently, the impact of sanctions have limited output. NIOC has struggled to buy equipment and hire contractors on international markets. But the fact remains that under the right circumstances, it could produce in excess of 4 million b/d.

The sanctions imposed on Iran in recent years have curtailed oil output

NatioNal iraNiaN oil CompaNy

iran

Founded: 1901 (Anglo-Persian Oil Com-pany); 1935 (Anglo-Iranian Oil Company); 1951 (National Iranian Oil Company)CEO: Roknoddin JavadiTel: (+98) 21 6162 2211-3Web: www.nioc.ir

iraN GDp by seCtor, 2011/12

major hyDroCarboNs projeCts

iraN oil aND Gas seCtor, 2012

GDP=Gross domestic product. Source: Central Bank of IranSources: Energy Information Administration; BP

EPC=Engineering, procurement and construction; NIOEC=National Iranian Oil Engineering & Construction Company; PIDMCO=Petrochemical Industries Development Management Company. Source: MEED Projects

ServicesOil

44

115

13 %27

Agriculture

Manufacturing and mining

ConstructionOil production (thousand barrels a day)

3,680

Gas production (billion cubic feet a day)

15.5

Scheme Client Type Cost ($m) StatusSouth Pars Gas Field Development: Phases 19-21

Pars Oil and Gas Company Gas production 9,000 On hold due to funding problems

South Pars Gas Field Development: Phases 17-18

Pars Oil and Gas Company Gas production 2,500 Commissioning planned for 2014

South Pars Gas Field Development: Phases 22-24

Pars Oil and Gas Company Gas production 3,500 Commissioning

West Ethylene Pipeline PIDMCO Gas 5,501 Commissioning

Neka-to-Jask Pipeline NIOEC Oil transport 3,000 EPC contract awarded

StrategyNIOC has been hamstrung in recent years in its ability to competitively tender major projects to non-Iranian companies, and was further squeezed by sanctions imposed by the EU in late 2012. It has nevertheless been working on a series of projects to expand oil and gas production. In late 2012, NIOC formed a Strategic Studies Centre at Iran’s Institute for International Energy Studies.

SubsidiariesKey NIOC subsidiaries include Iranian Offshore Oil Company, which produces oil and gas from the off-shore South Pars field; Central Iranian Oil Fields Company, which is in charge of oil and gas explo-ration and production in central Iran; National Ira-nian South Oil Company; Pars Oil and Gas Com-pany; National Iranian Oil Terminals Company; National Iranian Drilling Company; and National Iranian Tanker Company.

With sanctions restricting international engineer-ing firms from operating in Iran’s oil and gas sec-tor, NIOC has become increasingly reliant on Khatam al-Anbia – an engineering contractor con-trolled by the Iranian Revolutionary Guard Corps.

The company has been awarded several phases of Iran’s key South Pars offshore gas field development. South Pars phases 13 and 14 were awarded to Khatam al-Anbia in 2011 after UK/Dutch Shell and Spain’s Repsol YPF were given an ultimatum on moving forward with the projects. Khatam al-Anbia was established during the 1980-88 Iran-Iraq war to help with the Islamic Republic’s reconstruction and has since diversified into a mechanical engineering, energy, mining and defence contractor.

Khatam al-anbia

09 Iran.indd 9 29/10/2013 10:08

www.meed.com10 | MEED | National oil companies 2013

BackgroundUntil the 1970s, Iraq’s oil industry was dominated by Iraq Petroleum Company

(IPC), a consortium of US and UK oil majors, which had been granted an effective monopoly over oil and gas exploration in Iraq in the 1920s. In 1964, the then government in Bagh-dad set up a state-run firm, Iraq National Oil Company (INOC), to explore for and produce oil. In 1972, the decision was made to nationalise IPC-run assets, transferring them to the new state firm.

A year later, the concession of the Basra Petroleum Company (BPC), an IPC subsidiary, was partly nationalised, a process that was completed in 1975.

INOC pushed oil production to 3.5 million bar-rels a day (b/d) over the next five years, expand-ing the country’s oil reserves. The ruinous Iran-Iraq war of the 1980s, followed by more than a decade of economic sanctions after Saddam Hussein’s 1990 decision to invade Kuwait, placed huge strain on INOC’s ability to operate, however, and by the time of the US invasion in 2003, much of the company’s infrastructure was hugely outdated.

Iraq’s natIonal oIl companIes The profile of Iraq’s state oil firms in

international markets is growing fast

Iraq

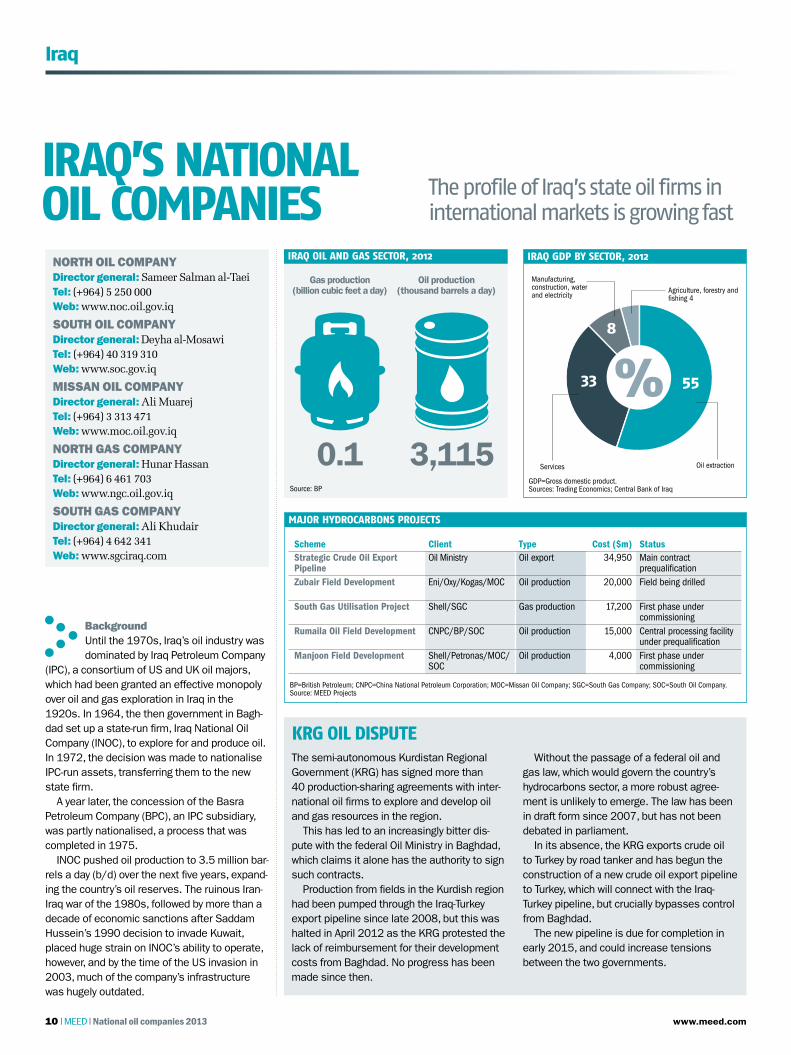

North oil CompaNyDirector general: Sameer Salman al-Taeitel: (+964) 5 250 000 Web: www.noc.oil.gov.iq

South oil CompaNy Director general: Deyha al-Mosawitel: (+964) 40 319 310Web: www.soc.gov.iq

miSSaN oil CompaNyDirector general: Ali Muarejtel: (+964) 3 313 471 Web: www.moc.oil.gov.iq

North GaS CompaNyDirector general: Hunar Hassantel: (+964) 6 461 703Web: www.ngc.oil.gov.iq

South GaS CompaNyDirector general: Ali Khudairtel: (+964) 4 642 341 Web: www.sgciraq.com

Iraq GDp by sector, 2012

major hyDrocarbons projects

Iraq oIl anD Gas sector, 2012

GDP=Gross domestic product. Sources: Trading Economics; Central Bank of IraqSource: BP

BP=British Petroleum; CNPC=China National Petroleum Corporation; MOC=Missan Oil Company; SGC=South Gas Company; SOC=South Oil Company. Source: MEED Projects

Oil extraction

55

8

33 %Services

Manufacturing, construction, water and electricity

Agriculture, forestry and fishing 4

Oil production (thousand barrels a day)

3,115

Gas production (billion cubic feet a day)

0.1

Scheme Client Type Cost ($m) StatusStrategic Crude Oil Export Pipeline

Oil Ministry Oil export 34,950 Main contract prequalification

Zubair Field Development Eni/Oxy/Kogas/MOC Oil production 20,000 Field being drilled

South Gas Utilisation Project Shell/SGC Gas production 17,200 First phase under commissioning

Rumaila Oil Field Development CNPC/BP/SOC Oil production 15,000 Central processing facility under prequalification

Manjoon Field Development Shell/Petronas/MOC/SOC

Oil production 4,000 First phase under commissioning

The semi-autonomous Kurdistan Regional Government (KRG) has signed more than 40 production-sharing agreements with inter-national oil firms to explore and develop oil and gas resources in the region.

This has led to an increasingly bitter dis-pute with the federal Oil Ministry in Baghdad, which claims it alone has the authority to sign such contracts.

Production from fields in the Kurdish region had been pumped through the Iraq-Turkey export pipeline since late 2008, but this was halted in April 2012 as the KRG protested the lack of reimbursement for their development costs from Baghdad. No progress has been made since then.

Without the passage of a federal oil and gas law, which would govern the country’s hydrocarbons sector, a more robust agree-ment is unlikely to emerge. The law has been in draft form since 2007, but has not been debated in parliament.

In its absence, the KRG exports crude oil to Turkey by road tanker and has begun the construction of a new crude oil export pipeline to Turkey, which will connect with the Iraq- Turkey pipeline, but crucially bypasses control from Baghdad.

The new pipeline is due for completion in early 2015, and could increase tensions between the two governments.

KRG oil dispute

10-11 Iraq.indd 10 29/10/2013 10:07

www.meed.com National oil companies 2013 | MEED | 11

“Iraq remains deeply unstable and the business environment continues to be incredibly complex”

IRAQ

TURKEY

SYRIA

JORDAN

SAUDI ARABIA

KUWAIT

IRAN

Samawah

BaghdadBaghdad

Kirkuk

Sulaimaniya

Erbil

Baiji

Karbala

Tikrit

HadithaKhanaqin

Baquba

Kut

Mosul

Basra

Faw

Baghdad

IRAQ OIL FIELDSIn 1987, INOC was merged with the Oil Minis-try, which in turn spun off INOC’s subsidiaries into standalone companies. The most impor-tant subsidiaries were South Oil Company (SOC), which took over the operations of BPC and oversaw the Rumaila fi eld, one of Iraq’s most important oil deposits, along with export facilities; and North Oil Company, which over-saw oil production in the north of Iraq, including another major fi eld, Sulimaniya. Other impor-tant companies included the state refi ner North Refi ning Company, North Gas Company and South Gas Company, which oversaw develop-ment of the country’s gas resources.

Since the invasion of Iraq, the Kurdish regional government in Erbil has taken over operations of its oil and gas assets in a move still contested by Baghdad, while a new state fi rm, Maysan Oil Company (MOC), has been spun off from SOC and a new fi rm, Midland Oil Company (also MOC), was set up to oversee the development of the country’s central oil fi elds. Maysan runs six relatively small fi elds along with the bigger Majnoon fi eld, which it operates in joint venture with SOC. The MOC spin-off was a pilot for a much bigger scheme to give each province of Iraq its own oil fi rm. Mid-land oversees the development of the major Mansuriya fi eld.

Between 2009 and 2013, the government of Iraq signed a series of deals with interna-tional oil companies (IOCs) to help develop its major oil fi elds. The UK’s BP brokered the most recent agreement in September 2013, to help revive the northern Kirkuk fi eld in partnership with North Oil Company; it had already won the right to work on the Rumaila fi eld, along with China National Petroleum Corporation (CNPC) and SOC, in 2009. CNPC won the right to develop the Halfaya fi eld along with France’s Total and Malaysia’s Petronas in the same 2009 bid round.

Petronas also won the right to develop the Majnoon fi eld with UK/Dutch Shell, which in turn is part of the consortium developing the West Qurna fi eld along with the US’ ExxonMobil, Russia’s Lukoil and Norway’s Statoil. The fi nal consortium developing a major fi eld, Al-Zubair, is made up of Italy’s Eni, Korea Gas Corpora-tion, the US’ Occidental Petroleum, Maysan and SOC.

In 2011, meanwhile, Shell and Japan’s Mitsubi-shi won a contract to capture and process gas from the Rumaila, West Qurna and Zubair fi elds. The deal was part of a programme to capture gas resources in partnership with South Gas Com-pany, as most gas produced in the country was being fl ared because of a lack of available infra-structure to process and make use of it.

Role in Iraq’s economyOil and gas earnings accounted for 93 per cent of government revenues and 45 per cent of all economic output in 2012, making the sector the single most important component of the national economy. Given that government spending currently accounts for 66.5 per cent of all investment in Iraq, oil and gas revenues consequently account for the bulk of growth-creating spending.

Role in the global economyAfter decades of waning signifi cance, Iraq and its national oil companies’ profi le in interna-tional energy markets is growing fast. Overall output at INOC-run fi elds has risen from 2.5 mil-lion b/d in 2009, when the last licences were awarded, to 3.7 million b/d in 2012. Oil Minis-ter Hussein al-Shahristani believes that Iraq could go on to produce 10 million b/d by the end of the decade, making the country one of

the most important oil producers in the world, and Opec’s second ‘swing’ producer.

Iraq has also been a source of focus for IOCs and international engineering companies, who had hoped to capitalise on the opening up of the oil market.

However, Iraq remains deeply unstable and the business environment continues to be incredibly complex. An oil law fi rst tabled in 2007 has yet to be passed by the country’s fractious parliament.

StrategyThe Oil Ministry hopes to increase oil output to 10 million b/d by 2020, while capturing increasing volumes of gas. The Paris-based International Energy Agency, however, has fore-cast that the national oil companies and their partners will produce 6.2 million b/d at most by the end of the decade, citing logistical and legal constraints.

The prospects for gas production remain bright, meanwhile, with the Shell/Mitsubishi consortium starting a processing plant with a capacity of 400 million cubic feet a day, due to be increased to 2 billion cubic feet a day. The gas is already being used to fuel a major new power plant, and the consortium is plan-ning to build a liquefi ed natural gas plant in the coming years, once domestic gas demand has been satisfi ed.

Oil pipeline

Provincial borders

Tanker terminal

Supergiant oil fi eld (5 billion barrels in reserves)

Oil fi eld

Sources: MEED; Iraq Oil Ministry

10-11 Iraq.indd 11 29/10/2013 10:07

www.meed.com12 | MEED | National oil companies 2013

Kuwait

Background Kuwait Petroleum Corporation (KPC) traces its history back to the early 1930s,

when Anglo-Persian Oil Company, known today as the UK’s BP, and Gulf Oil, now Chevrolet of the US, formed a joint venture to search for oil in the emir-ate. Named Kuwait Oil Company (KOC), the firm made its first discovery in 1938 at the giant Burgan field, which continues to be one of the country’s most important assets. In 1960, the government established its own refining and fuel trading firm, Kuwait National Petroleum Company (KNPC), which built a refinery at Shuaiba. In 1964, the govern-ment also started its first petrochemicals joint ven-ture, Petrochemical Industries Company (PIC).

In 1973, Kuwait bought out its partners to take full control of PIC, moving to nationalise KOC in 1975. In 1978 and 1980 the government nation-alised the two main oil refineries it did not own, at Mina al-Ahmadi and Mina Abdullah. In 1980, KPC was formed as a holding company to oversee operations at all of the country’s oil, gas, refining and petrochemicals firms.

Role in Kuwait’s economyAs the state oil producer, KPC is a hugely impor-tant player in the domestic economy. Oil and gas accounted for 94.5 per cent of all exports in 2012, providing the government with 76 per cent of its annual revenues and making up more than half of all economic output. KPC also provides cheap fuel and feedstocks, helping to make Kuwaiti busi-nesses more competitive internationally.

Role in the global economyKPC is the world’s eighth-largest producer of oil and a key member of the oil producers’ club Opec.

StrategyThe firm’s domestic ambitions, especially with respect to its ageing refineries, are tempered by the country’s volatile political scene, which has seen KPC struggle to get the parliamentary

approval it needs to move on major new projects. In 2013, the company was ordered to pay $2.2bn to the US’ Dow Chemical after a joint-venture plan failed five years earlier due to political infighting.

Nevertheless, KPC is still aiming for a produc-tion capacity of 4 million barrels a day by 2020. It also hopes to build a major new refinery at Al-Zour and overhaul its existing refineries to bring them

“KPC is the world’s eighth-largest producer of oil and a key member of the oil producers’ club Opec”

Kuwait PetrOleum COrPOratiOn Despite political infighting, the firm

has ambitious expansion plans

Kuwait GDP by SeCtOr, 2012

majOr hyDrOCarbOnS PrOjeCtS

Kuwait Oil anD GaS SeCtOr, 2012

GDP=Gross domestic product. Source: National Bank of KuwaitSource: BP

KNPC=Kuwait National Petroleum Company; Feed=Front-end engineering and design. Source: MEED Projects

Other

28

665

5 5

%19 24

Finance and business

Trade

Manufacturing

ConstructionTelecommunications

Agriculture

Utilities 2

Oil and gas

Oil production (thousand barrels a day)

3,127

Gas production (billion cubic feet a day)

1.4

Scheme Client TypeCost ($m) Status

Clean Fuels Project KNPC Refining 16,835 Bids due 24 Dec 2013

New Refinery Project KNPC Refining 14,388 Prequalification

Mina al-Ahmadi Gas Train 5 KNPC Refining 1,532 Feed

New North Liquid Petroleum Gas Tank Farm

KNPC Refining 1,367 Execution

Mina al-Ahmadi Gas Train 4 KNPC Refining 1,135 Execution

Mina al-Ahmadi Sulphur-Handling Facilities

KNPC Refining 899 Execution

Founded: 1980CEO: Nizar al-AdsaniTel: (+965) 1 858 585Web: www.kpc.com.kw

up to international standards. To increase its foot-print abroad, the company is building a new refin-ery in China with China Petroleum & Chemical Cor-poration (Sinopec). KPC’s subsidiary Kuwait Foreign Exploration Company (Kufpec) has recently taken on a new concession in Yemen and has spo-ken of its desire to expand production in south-east Asia. In March 2013, Kufpec agreed a $750m loan with a local bank to fund its activities.

ConcessionsUnder Kuwaiti law, it is more or less impossible for KPC to award exploration and production conces-sions to foreign companies. Negotiations over Enhanced Technical Service Agreements, which would work in a manner similar to production-sharing agreements, have stalled since the first deal was awarded to UK/Dutch Shell in 2011.

12 KuwaitSUBBED.indd 12 29/10/2013 10:06

www.meed.com National oil companies 2013 | MEED | 13

Libya

BackgroundLibya’s National Oil Corporation (NOC) is still one of the most important oil pro-

ducers in the Middle East and North Africa region, but it has been hard hit by the events of the past few years. A number of international oil compa-nies (IOCs) entered Libya during the 1950s to look for oil, with a series of major discoveries towards the end of the decade sparking excite-ment over the country’s potential.

After a coup that saw Libya’s then ruler King Idriss ousted, the country’s new ‘brother leader’ Muammar Gaddafi nationalised most of the country’s oil and gas assets, creating NOC to oversee the development of the hydrocarbons sector in 1970. NOC partnered with several Ital-ian and US firms over the course of the 1970s, but also continued the process of nationalisa-tion and renegotiation of existing deals.

Accusations of terrorism levelled against the Gaddafi regime saw the US impose sanctions on Libya, which came to include a ban on Ameri-can companies working in the country. This led to an exodus of many of NOC’s most important partners. The state firm responded by offering the concessions to non-US companies.

Stronger sanctions imposed during the 1990s made the operating environment even tougher. However, a thaw in relations between Tripoli and Washington in the early 2000s saw several IOCs return to the country, with oil pro-duction rising for six successive years, to 1.8 million barrels a day in 2008.

The 2011 uprising in Libya caused oil produc-tion to collapse and placed considerable strain on NOC. Its longtime chairman, Shokri Ghanem, defected and a number of executives fled the country when the Gaddafi regime fell. Some progress was made in restoring production over the course of 2012, but growing insecurity in 2013 has left output virtually frozen and has caused a number of IOCs to question the wis-dom of continued participation in the sector.

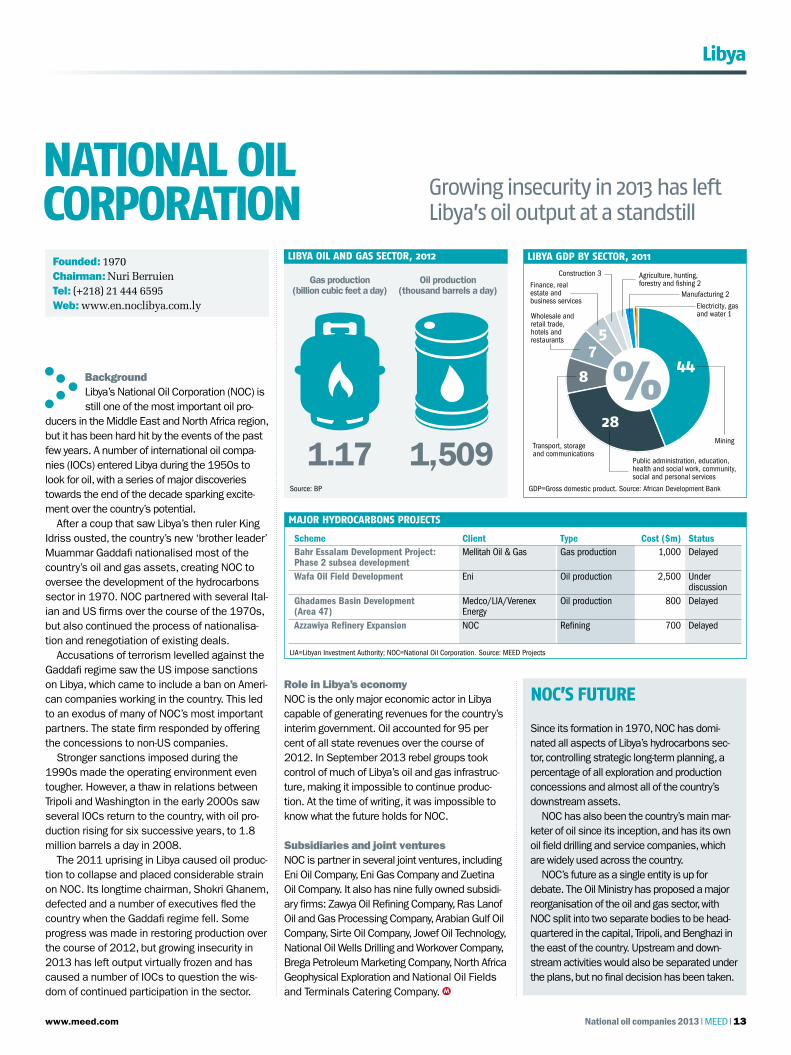

Growing insecurity in 2013 has left Libya’s oil output at a standstill

NatioNaL oiL CorporatioN

Founded: 1970Chairman: Nuri BerruienTel: (+218) 21 444 6595 Web: www.en.noclibya.com.ly

Libya GDp by seCtor, 2011

Major hyDroCarboNs projeCts

Libya oiL aND Gas seCtor, 2012

GDP=Gross domestic product. Source: African Development BankSource: BP

LIA=Libyan Investment Authority; NOC=National Oil Corporation. Source: MEED Projects

Mining

4475

8 %28

Wholesale and retail trade, hotels and restaurants

Finance, real estate and business services

Construction 3

Transport, storage and communications

Agriculture, hunting, forestry and fishing 2

Manufacturing 2

Electricity, gas and water 1

Public administration, education, health and social work, community, social and personal services

Oil production (thousand barrels a day)

1,509

Gas production (billion cubic feet a day)

1.17

Scheme Client Type Cost ($m) StatusBahr Essalam Development Project: Phase 2 subsea development

Mellitah Oil & Gas Gas production 1,000 Delayed

Wafa Oil Field Development Eni Oil production 2,500 Under discussion

Ghadames Basin Development (Area 47)

Medco/LIA/Verenex Energy

Oil production 800 Delayed

Azzawiya Refinery Expansion NOC Refining 700 Delayed

Role in Libya’s economyNOC is the only major economic actor in Libya capable of generating revenues for the country’s interim government. Oil accounted for 95 per cent of all state revenues over the course of 2012. In September 2013 rebel groups took control of much of Libya’s oil and gas infrastruc-ture, making it impossible to continue produc-tion. At the time of writing, it was impossible to know what the future holds for NOC.

Subsidiaries and joint venturesNOC is partner in several joint ventures, including Eni Oil Company, Eni Gas Company and Zuetina Oil Company. It also has nine fully owned subsidi-ary firms: Zawya Oil Refining Company, Ras Lanof Oil and Gas Processing Company, Arabian Gulf Oil Company, Sirte Oil Company, Jowef Oil Technology, National Oil Wells Drilling and Workover Company, Brega Petroleum Marketing Company, North Africa Geophysical Exploration and National Oil Fields and Terminals Catering Company.

Since its formation in 1970, NOC has domi-nated all aspects of Libya’s hydrocarbons sec-tor, controlling strategic long-term planning, a percentage of all exploration and production concessions and almost all of the country’s downstream assets.

NOC has also been the country’s main mar-keter of oil since its inception, and has its own oil field drilling and service companies, which are widely used across the country.

NOC’s future as a single entity is up for debate. The Oil Ministry has proposed a major reorganisation of the oil and gas sector, with NOC split into two separate bodies to be head-quartered in the capital, Tripoli, and Benghazi in the east of the country. Upstream and down-stream activities would also be separated under the plans, but no final decision has been taken.

NOC’s future

13 LibyaSUBBED.indd 13 29/10/2013 10:06

www.meed.com14 | MEED | National oil companies 2013

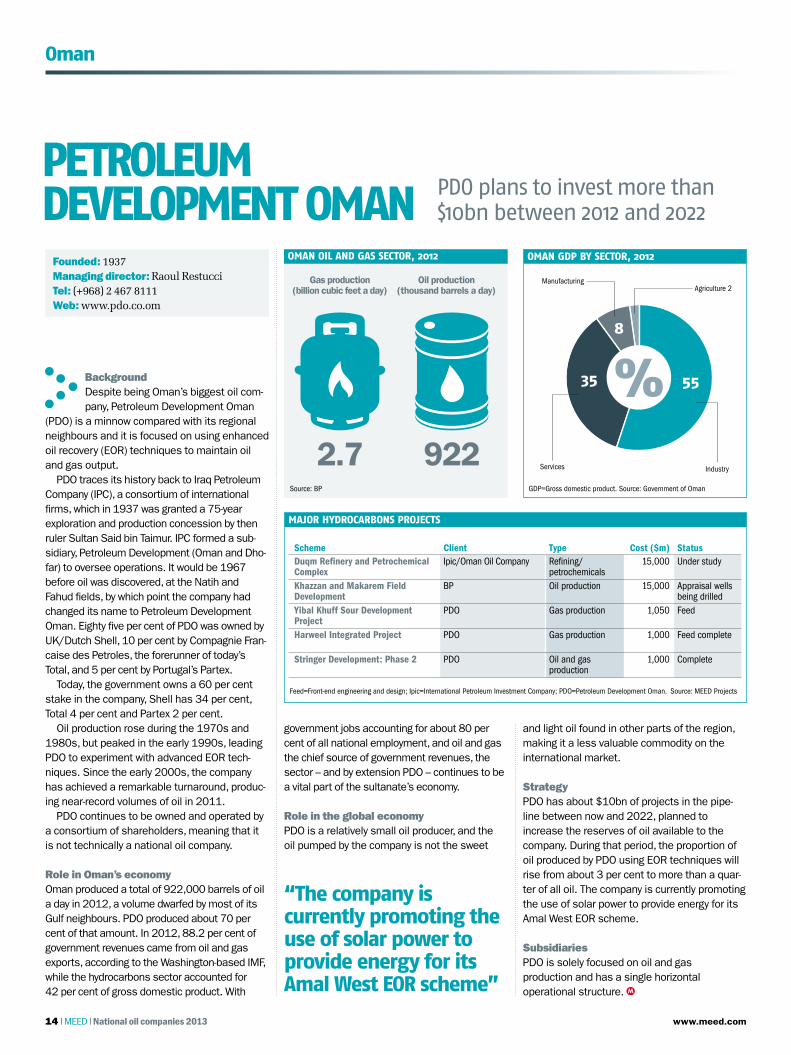

BackgroundDespite being Oman’s biggest oil com-pany, Petroleum Development Oman

(PDO) is a minnow compared with its regional neighbours and it is focused on using enhanced oil recovery (EOR) techniques to maintain oil and gas output.

PDO traces its history back to Iraq Petroleum Company (IPC), a consortium of international firms, which in 1937 was granted a 75-year exploration and production concession by then ruler Sultan Said bin Taimur. IPC formed a sub-sidiary, Petroleum Development (Oman and Dho-far) to oversee operations. It would be 1967 before oil was discovered, at the Natih and Fahud fields, by which point the company had changed its name to Petroleum Development Oman. Eighty five per cent of PDO was owned by UK/Dutch Shell, 10 per cent by Compagnie Fran-caise des Petroles, the forerunner of today’s Total, and 5 per cent by Portugal’s Partex.

Today, the government owns a 60 per cent stake in the company, Shell has 34 per cent, Total 4 per cent and Partex 2 per cent.

Oil production rose during the 1970s and 1980s, but peaked in the early 1990s, leading PDO to experiment with advanced EOR tech-niques. Since the early 2000s, the company has achieved a remarkable turnaround, produc-ing near-record volumes of oil in 2011.

PDO continues to be owned and operated by a consortium of shareholders, meaning that it is not technically a national oil company.

Role in Oman’s economyOman produced a total of 922,000 barrels of oil a day in 2012, a volume dwarfed by most of its Gulf neighbours. PDO produced about 70 per cent of that amount. In 2012, 88.2 per cent of government revenues came from oil and gas exports, according to the Washington-based IMF, while the hydrocarbons sector accounted for 42 per cent of gross domestic product. With

government jobs accounting for about 80 per cent of all national employment, and oil and gas the chief source of government revenues, the sector – and by extension PDO – continues to be a vital part of the sultanate’s economy.

Role in the global economyPDO is a relatively small oil producer, and the oil pumped by the company is not the sweet

Petroleum DeveloPment oman PDO plans to invest more than

$10bn between 2012 and 2022

oman

Founded: 1937Managing director: Raoul RestucciTel: (+968) 2 467 8111Web: www.pdo.co.om

oman GDP by Sector, 2012

major hyDrocarbonS ProjectS

oman oil anD GaS Sector, 2012

GDP=Gross domestic product. Source: Government of OmanSource: BP

Feed=Front-end engineering and design; Ipic=International Petroleum Investment Company; PDO=Petroleum Development Oman. Source: MEED Projects

Industry

55

8

35 %Services

ManufacturingAgriculture 2

Oil production (thousand barrels a day)

922

Gas production (billion cubic feet a day)

2.7

Scheme Client Type Cost ($m) StatusDuqm Refinery and Petrochemical Complex

Ipic/Oman Oil Company Refining/petrochemicals

15,000 Under study

Khazzan and Makarem Field Development

BP Oil production 15,000 Appraisal wells being drilled

Yibal Khuff Sour Development Project

PDO Gas production 1,050 Feed

Harweel Integrated Project PDO Gas production 1,000 Feed complete

Stringer Development: Phase 2 PDO Oil and gas production

1,000 Complete

and light oil found in other parts of the region, making it a less valuable commodity on the international market.

StrategyPDO has about $10bn of projects in the pipe-line between now and 2022, planned to increase the reserves of oil available to the company. During that period, the proportion of oil produced by PDO using EOR techniques will rise from about 3 per cent to more than a quar-ter of all oil. The company is currently promoting the use of solar power to provide energy for its Amal West EOR scheme.

SubsidiariesPDO is solely focused on oil and gas production and has a single horizontal operational structure.

“the company is currently promoting the use of solar power to provide energy for its amal West eor scheme”

14 Oman.indd 14 29/10/2013 10:06

www.meed.com National oil companies 2013 | MEED | 15

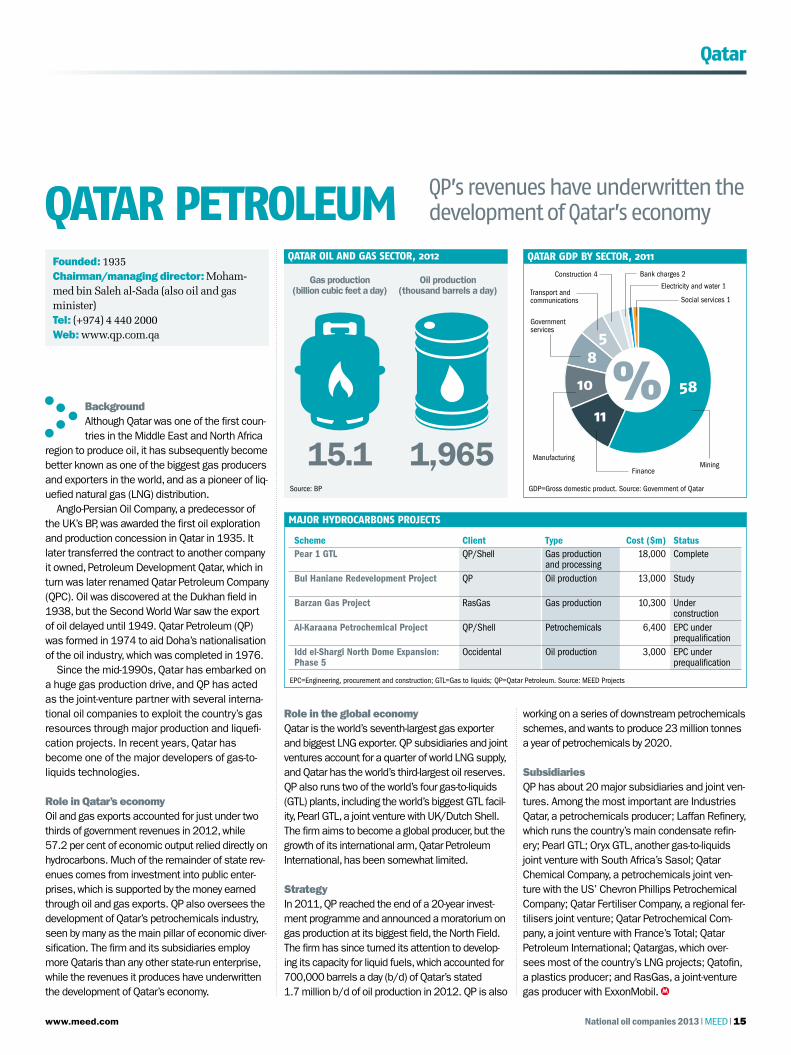

BackgroundAlthough Qatar was one of the first coun-tries in the Middle East and North Africa

region to produce oil, it has subsequently become better known as one of the biggest gas producers and exporters in the world, and as a pioneer of liq-uefied natural gas (LNG) distribution.

Anglo-Persian Oil Company, a predecessor of the UK’s BP, was awarded the first oil exploration and production concession in Qatar in 1935. It later transferred the contract to another company it owned, Petroleum Development Qatar, which in turn was later renamed Qatar Petroleum Company (QPC). Oil was discovered at the Dukhan field in 1938, but the Second World War saw the export of oil delayed until 1949. Qatar Petroleum (QP) was formed in 1974 to aid Doha’s nationalisation of the oil industry, which was completed in 1976.

Since the mid-1990s, Qatar has embarked on a huge gas production drive, and QP has acted as the joint-venture partner with several interna-tional oil companies to exploit the country’s gas resources through major production and liquefi-cation projects. In recent years, Qatar has become one of the major developers of gas-to-liquids technologies.

Role in Qatar’s economyOil and gas exports accounted for just under two thirds of government revenues in 2012, while 57.2 per cent of economic output relied directly on hydrocarbons. Much of the remainder of state rev-enues comes from investment into public enter-prises, which is supported by the money earned through oil and gas exports. QP also oversees the development of Qatar’s petrochemicals industry, seen by many as the main pillar of economic diver-sification. The firm and its subsidiaries employ more Qataris than any other state-run enterprise, while the revenues it produces have underwritten the development of Qatar’s economy.

QP’s revenues have underwritten the development of Qatar’s economyQatar Petroleum

Qatar

Founded: 1935Chairman/managing director: Moham-med bin Saleh al-Sada (also oil and gas minister)Tel: (+974) 4 440 2000Web: www.qp.com.qa

Qatar GDP by sector, 2011

major hyDrocarbons Projects

Qatar oil anD Gas sector, 2012

GDP=Gross domestic product. Source: Government of QatarSource: BP

EPC=Engineering, procurement and construction; GTL=Gas to liquids; QP=Qatar Petroleum. Source: MEED Projects

MiningFinance

58

85

10 %11

Government services

Transport and communications

Construction 4

Manufacturing

Bank charges 2

Electricity and water 1

Social services 1

Oil production (thousand barrels a day)

1,965

Gas production (billion cubic feet a day)

15.1

Scheme Client Type Cost ($m) StatusPear 1 GTL QP/Shell Gas production

and processing18,000 Complete

Bul Haniane Redevelopment Project QP Oil production 13,000 Study

Barzan Gas Project RasGas Gas production 10,300 Under construction

Al-Karaana Petrochemical Project QP/Shell Petrochemicals 6,400 EPC under prequalification

Idd el-Shargi North Dome Expansion: Phase 5

Occidental Oil production 3,000 EPC under prequalification

Role in the global economyQatar is the world’s seventh-largest gas exporter and biggest LNG exporter. QP subsidiaries and joint ventures account for a quarter of world LNG supply, and Qatar has the world’s third-largest oil reserves. QP also runs two of the world’s four gas-to-liquids (GTL) plants, including the world’s biggest GTL facil-ity, Pearl GTL, a joint venture with UK/Dutch Shell. The firm aims to become a global producer, but the growth of its international arm, Qatar Petroleum International, has been somewhat limited.

StrategyIn 2011, QP reached the end of a 20-year invest-ment programme and announced a moratorium on gas production at its biggest field, the North Field. The firm has since turned its attention to develop-ing its capacity for liquid fuels, which accounted for 700,000 barrels a day (b/d) of Qatar’s stated 1.7 million b/d of oil production in 2012. QP is also

working on a series of downstream petrochemicals schemes, and wants to produce 23 million tonnes a year of petrochemicals by 2020.

SubsidiariesQP has about 20 major subsidiaries and joint ven-tures. Among the most important are Industries Qatar, a petrochemicals producer; Laffan Refinery, which runs the country’s main condensate refin-ery; Pearl GTL; Oryx GTL, another gas-to-liquids joint venture with South Africa’s Sasol; Qatar Chemical Company, a petrochemicals joint ven-ture with the US’ Chevron Phillips Petrochemical Company; Qatar Fertiliser Company, a regional fer-tilisers joint venture; Qatar Petrochemical Com-pany, a joint venture with France’s Total; Qatar Petroleum International; Qatargas, which over-sees most of the country’s LNG projects; Qatofin, a plastics producer; and RasGas, a joint-venture gas producer with ExxonMobil.

15 Qatar.indd 15 29/10/2013 10:05

C

M

Y

CM

MY

CY

CMY

K

www.meed.com National oil companies 2013 | MEED | 17

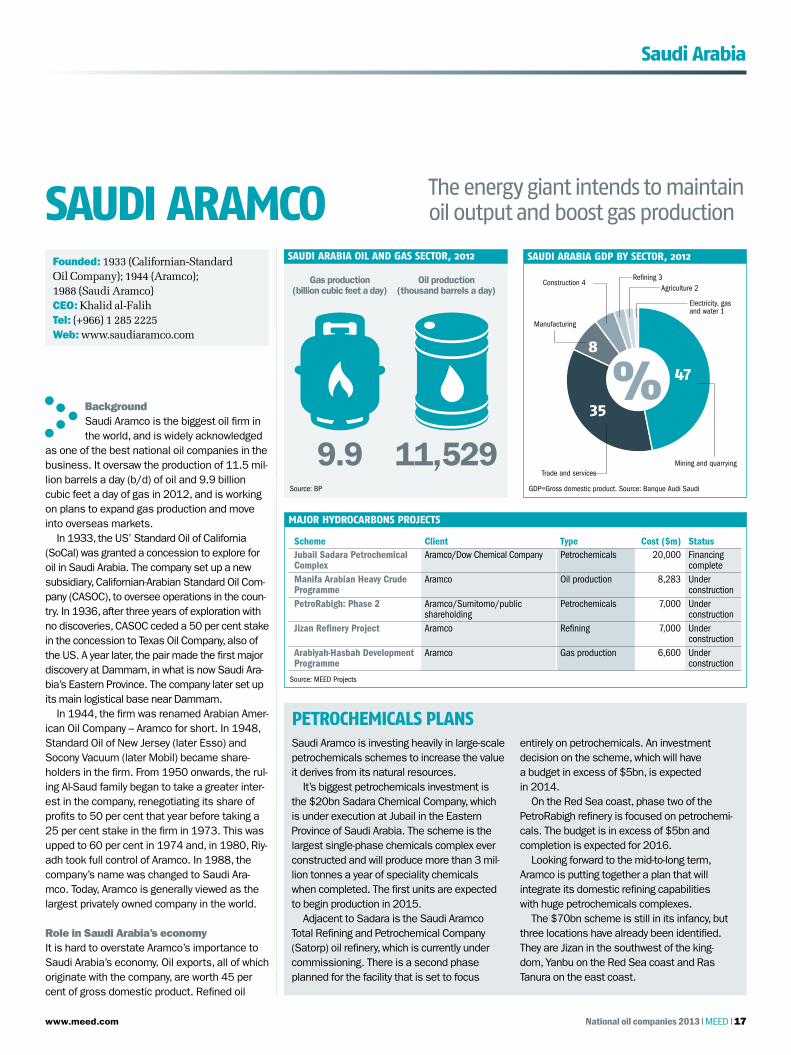

Saudi Arabia

BackgroundSaudi Aramco is the biggest oil firm in the world, and is widely acknowledged

as one of the best national oil companies in the business. It oversaw the production of 11.5 mil-lion barrels a day (b/d) of oil and 9.9 billion cubic feet a day of gas in 2012, and is working on plans to expand gas production and move into overseas markets.

In 1933, the US’ Standard Oil of California (SoCal) was granted a concession to explore for oil in Saudi Arabia. The company set up a new subsidiary, Californian-Arabian Standard Oil Com-pany (CASOC), to oversee operations in the coun-try. In 1936, after three years of exploration with no discoveries, CASOC ceded a 50 per cent stake in the concession to Texas Oil Company, also of the US. A year later, the pair made the first major discovery at Dammam, in what is now Saudi Ara-bia’s Eastern Province. The company later set up its main logistical base near Dammam.

In 1944, the firm was renamed Arabian Amer-ican Oil Company – Aramco for short. In 1948, Standard Oil of New Jersey (later Esso) and Socony Vacuum (later Mobil) became share-holders in the firm. From 1950 onwards, the rul-ing Al-Saud family began to take a greater inter-est in the company, renegotiating its share of profits to 50 per cent that year before taking a 25 per cent stake in the firm in 1973. This was upped to 60 per cent in 1974 and, in 1980, Riy-adh took full control of Aramco. In 1988, the company’s name was changed to Saudi Ara-mco. Today, Aramco is generally viewed as the largest privately owned company in the world.

Role in Saudi Arabia’s economyIt is hard to overstate Aramco’s importance to Saudi Arabia’s economy. Oil exports, all of which originate with the company, are worth 45 per cent of gross domestic product. Refined oil

The energy giant intends to maintain oil output and boost gas productionSAudi ArAmco

Founded: 1933 (Californian-Standard Oil Company); 1944 (Aramco); 1988 (Saudi Aramco)CEO: Khalid al-FalihTel: (+966) 1 285 2225Web: www.saudiaramco.com

SAudi ArAbiA GdP by Sector, 2012

mAjor hydrocArbonS ProjectS

SAudi ArAbiA oil And GAS Sector, 2012

GDP=Gross domestic product. Source: Banque Audi SaudiSource: BP

Source: MEED Projects

Mining and quarrying

47

8

%35

Manufacturing

Construction 4Agriculture 2

Electricity, gas and water 1

Refining 3

Trade and services

Oil production (thousand barrels a day)

11,529

Gas production (billion cubic feet a day)

9.9

Scheme Client Type Cost ($m) StatusJubail Sadara Petrochemical Complex

Aramco/Dow Chemical Company Petrochemicals 20,000 Financing complete

Manifa Arabian Heavy Crude Programme

Aramco Oil production 8,283 Under construction

PetroRabigh: Phase 2 Aramco/Sumitomo/public shareholding

Petrochemicals 7,000 Under construction

Jizan Refinery Project Aramco Refining 7,000 Under construction

Arabiyah-Hasbah Development Programme

Aramco Gas production 6,600 Under construction

Saudi Aramco is investing heavily in large-scale petrochemicals schemes to increase the value it derives from its natural resources.

It’s biggest petrochemicals investment is the $20bn Sadara Chemical Company, which is under execution at Jubail in the Eastern Province of Saudi Arabia. The scheme is the largest single-phase chemicals complex ever constructed and will produce more than 3 mil-lion tonnes a year of speciality chemicals when completed. The first units are expected to begin production in 2015.

Adjacent to Sadara is the Saudi Aramco Total Refining and Petrochemical Company (Satorp) oil refinery, which is currently under commissioning. There is a second phase planned for the facility that is set to focus

entirely on petrochemicals. An investment decision on the scheme, which will have a budget in excess of $5bn, is expected in 2014.

On the Red Sea coast, phase two of the PetroRabigh refinery is focused on petrochemi-cals. The budget is in excess of $5bn and completion is expected for 2016.

Looking forward to the mid-to-long term, Aramco is putting together a plan that will integrate its domestic refining capabilities with huge petrochemicals complexes.

The $70bn scheme is still in its infancy, but three locations have already been identified. They are Jizan in the southwest of the king-dom, Yanbu on the Red Sea coast and Ras Tanura on the east coast.

Petrochemicals Plans

17-18 Saudi ArabiaSUBBED.indd 17 29/10/2013 10:05

www.meed.com18 | MEED | National oil companies 2013

Saudi Arabia

“Aramco’s most important function is as ‘swing’ producer, not just within Opec, but among oil producers worldwide”

products and petrochemicals – the feedstocks for which Aramco provides at cost – underpin the manufacturing sector, worth just under 8 per cent of economic output, while an esti-mated 90 per cent plus of government reve-nues are generated by Aramco, which effectively hands over its profi ts to Riyadh.

Aramco is also one of the biggest employers in the kingdom (second only to the government), with an estimated 54,000 staff, 85 per cent of whom are Saudi nationals. Its workforce is widely recognised as being among the country’s most professional and effi cient. The chemical feedstocks and energy that the company sup-plies to industrial projects help keep them com-petitive internationally, while Aramco-run refi ner-ies provide most of the fuel used to fi ll cars in the kingdom.

Aramco offi cials have played a growing role in strategic planning in Riyadh over the past dec-ade, and are said to be among the most strin-gent critics of the huge fuel and feedstock sub-sidies in place in Saudi Arabia, which account for more than a tenth of government spending.

Role in the global economyAs the world’s largest oil producer and a found-ing member of Opec, Saudi Arabia is a hugely important cog in the machinery of the global economy, and so, by extension, is Aramco. Per-haps its most important function is as the ‘swing’ producer, not just within Opec but among oil producers worldwide. The company produced a total of 11.5 million b/d of oil in 2012, including about 1.8 million b/d of natural gas liquids, but can produce a maximum of 12.5 million b/d of oil alone. This means it has a production cushion of more than 1 million b/d – more than the average production of a number of Opec members. It is capable of increasing or decreasing output at will, helping to moderate or increase market prices.

StrategyWhile Aramco’s main aim over the past decade has been to increase its production capacity to 12.5 million b/d, its current strategy is to maintain oil output and increase gas production.

The company has become more dependent on ‘heavy’ oil, which is more viscous, sulphur-ous and expensive to produce than the sweet light crude that has been so key to the king-dom’s fortunes.

Aramco has also moved offshore, producing heavy crude from the Manifa fi eld, which, again, is more expensive and technically complex than producing oil from onshore installations. This means that, as the company becomes

more reliant on heavy oil, the marginal cost of production will increase. With oil at about $100 a barrel on international markets and the US and Canada, among others, now meeting their energy needs with shale oil and gas, the kingdom’s oil will remain both profi table and saleable, however.

Aramco sees development of the country’s gas resources as a good way of freeing up oil for export, and its exploration activities in the kingdom are increasingly focused on making new gas discoveries to expand output. The company is also quietly pushing for an increase in the price of gas to industrial customers, from 75 cents a million BTUs.

Aramco is in the middle of a massive expansion of its downstream production capac-ity, and is building new refi neries at Jubail, Yanbu and Jizan. The fi rst two units are being built by joint venture companies with China Pet-rochemical Corporation (Sinopec) and France’s Total respectively.

Both the joint-venture refi neries are designed to be able to process heavier grades of crude and produce fuel to international standards. They will provide feedstock for a series of giant petrochemicals projects in which Aramco is a partner, including PetroRabigh and Sadara, joint ventures with Japan’s Sumitomo and the US’ Dow Chemical Company.

Overseas ambitionsAramco has been building new downstream capacity abroad, and is expanding its joint-ven-ture refi nery at Port Arthur in the US, along with its partner UK/Dutch Shell.

The fi rm is also working on plans to build a major new refi nery at Yunnan in China with China National Petroleum Corporation, to accompany its existing refi ning and petrochemi-cals joint venture at Fujian.

SubsidiariesAramco operates a horizontal structure in Saudi Arabia, and does not have subsidiaries in the kingdom other than its joint ventures.

Internationally, it is the owner of a number of subsidiary companies engaged in invest-ment, refi ning, trading and marketing. These include Aramco Services Company, Aramco Associated Company, Aramco Training Services Company, Saudi Refi ning Incorporated and Saudi Petroleum International, all headquar-tered in the US; Aramco Far East Business Services Company in China; Saudi Petroleum Overseas in the UK; and Aramco Overseas Company in the Netherlands.

Concessions and partnersAramco does not usually work using contracts based on a production-sharing agreement model, but the fi rm does make some exceptions.

It has three joint-venture agreements with international oil companies for gas projects as part of the Saudi Gas Initiative, fi rst bro-kered in 2002.

The companies are South Rub al-Khali Company, a joint venture with Shell; Luksar Energy, with Russia’s Lukoil; and Sino Saudi Gas, with Sinopec.

KUWAIT

QATAR

BAHRAIN

UAE

OMAN

OMAN

IRAN

SAUDI ARABIA

SAUDI ARABIA OIL AND GAS FIELDS

Oil fi eld

Gas fi eld

17-18 Saudi ArabiaSUBBED.indd 18 29/10/2013 10:05

www.meed.com National oil companies 2013 | MEED | 19

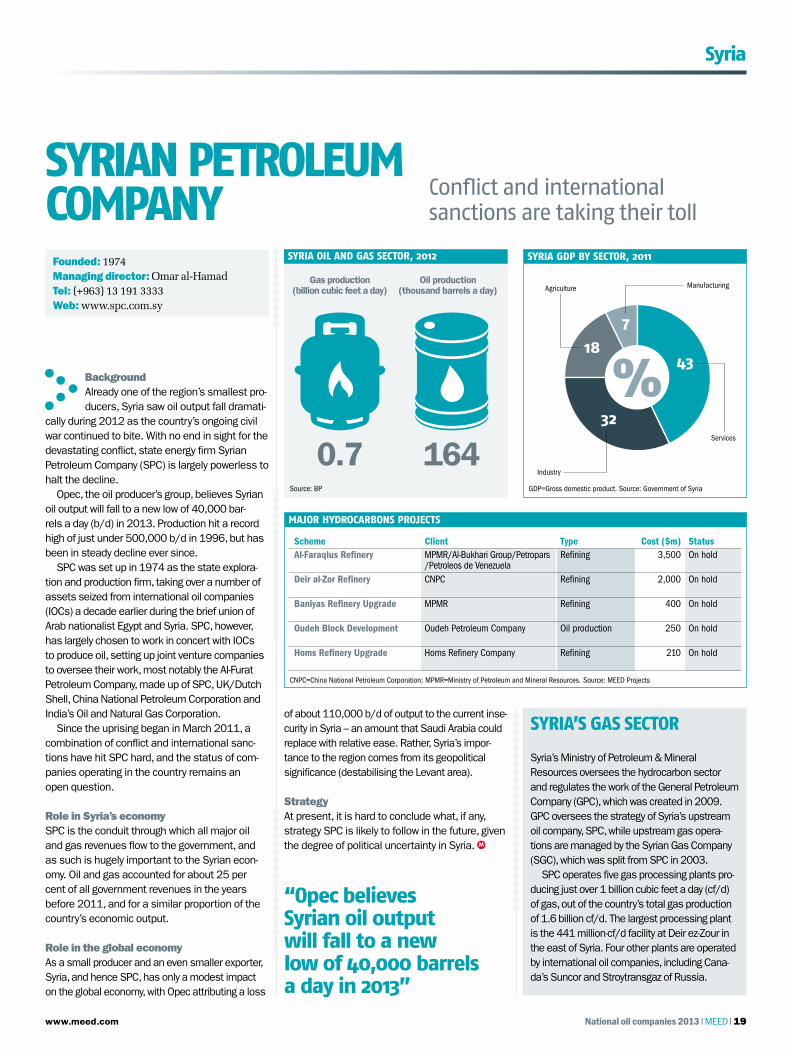

Syria

BackgroundAlready one of the region’s smallest pro-ducers, Syria saw oil output fall dramati-

cally during 2012 as the country’s ongoing civil war continued to bite. With no end in sight for the devastating conflict, state energy firm Syrian Petroleum Company (SPC) is largely powerless to halt the decline.

Opec, the oil producer’s group, believes Syrian oil output will fall to a new low of 40,000 bar-rels a day (b/d) in 2013. Production hit a record high of just under 500,000 b/d in 1996, but has been in steady decline ever since.

SPC was set up in 1974 as the state explora-tion and production firm, taking over a number of assets seized from international oil companies (IOCs) a decade earlier during the brief union of Arab nationalist Egypt and Syria. SPC, however, has largely chosen to work in concert with IOCs to produce oil, setting up joint venture companies to oversee their work, most notably the Al-Furat Petroleum Company, made up of SPC, UK/Dutch Shell, China National Petroleum Corporation and India’s Oil and Natural Gas Corporation.

Since the uprising began in March 2011, a combination of conflict and international sanc-tions have hit SPC hard, and the status of com-panies operating in the country remains an open question.

Role in Syria’s economySPC is the conduit through which all major oil and gas revenues flow to the government, and as such is hugely important to the Syrian econ-omy. Oil and gas accounted for about 25 per cent of all government revenues in the years before 2011, and for a similar proportion of the country’s economic output.

Role in the global economyAs a small producer and an even smaller exporter, Syria, and hence SPC, has only a modest impact on the global economy, with Opec attributing a loss

Conflict and international sanctions are taking their toll

Syrian Petroleum ComPany

Founded: 1974Managing director: Omar al-HamadTel: (+963) 13 191 3333Web: www.spc.com.sy

Syria GDP by SeCtor, 2011

major hyDroCarbonS ProjeCtS

Syria oil anD GaS SeCtor, 2012

GDP=Gross domestic product. Source: Government of SyriaSource: BP

CNPC=China National Petroleum Corporation; MPMR=Ministry of Petroleum and Mineral Resources. Source: MEED Projects

Services

43

7

18

%32

Agriculture Manufacturing

Industry

Oil production (thousand barrels a day)

164

Gas production (billion cubic feet a day)

0.7

Scheme Client Type Cost ($m) StatusAl-Faraqlus Refinery MPMR/Al-Bukhari Group/Petropars

/Petroleos de VenezuelaRefining 3,500 On hold

Deir al-Zor Refinery CNPC Refining 2,000 On hold

Baniyas Refinery Upgrade MPMR Refining 400 On hold

Oudeh Block Development Oudeh Petroleum Company Oil production 250 On hold

Homs Refinery Upgrade Homs Refinery Company Refining 210 On hold

of about 110,000 b/d of output to the current inse-curity in Syria – an amount that Saudi Arabia could replace with relative ease. Rather, Syria’s impor-tance to the region comes from its geopolitical significance (destabilising the Levant area).

StrategyAt present, it is hard to conclude what, if any, strategy SPC is likely to follow in the future, given the degree of political uncertainty in Syria.

“opec believes Syrian oil output will fall to a new low of 40,000 barrels a day in 2013”

Syria’s Ministry of Petroleum & Mineral Resources oversees the hydrocarbon sector and regulates the work of the General Petroleum Company (GPC), which was created in 2009. GPC oversees the strategy of Syria’s upstream oil company, SPC, while upstream gas opera-tions are managed by the Syrian Gas Company (SGC), which was split from SPC in 2003.

SPC operates five gas processing plants pro-ducing just over 1 billion cubic feet a day (cf/d) of gas, out of the country’s total gas production of 1.6 billion cf/d. The largest processing plant is the 441 million-cf/d facility at Deir ez-Zour in the east of Syria. Four other plants are operated by international oil companies, including Cana-da’s Suncor and Stroytransgaz of Russia.

Syria’S gaS Sector

19 SyriaSUBBED.indd 19 29/10/2013 10:04

www.meed.com20 | MEED | National oil companies 2013

Tunisia

BackgroundEntreprise Tunisienne d’Activites Petro-lieres (Etap) is Tunisia’s state oil and gas

producer. It was formed in 1972 as interest in the country’s potential as an oil producer grew. By 1982, Etap and its international partners were producing 120,000 barrels a day (b/d) of oil, a volume that could not be maintained. By the early 2000s, output had fallen to 68,000 b/d.

Etap and Tunis responded by making it easier for international oil companies (IOCs) to invest in the sector, and focused on enhanced oil recovery techniques, which helped push production back up to 97,000 b/d in 2007. Output has subse-quently fallen to 65,000 b/d in 2012, according to the UK’s BP.

Role in Tunisia’s economyTunisia is a rare example in the Middle East and North Africa of a country that is an overall importer of hydrocarbons – it exports gas, but imports oil, and the overall balance is negative. Etap, meanwhile, is a relatively small employer, with 792 workers at the end of 2011, and it depends heavily on partnerships with IOCs to help develop the country’s oil and gas assets.

Role in the global economyEtap does not play a major role in the global economy, although its gas exports contribute to the balance of energy.

StrategyEtap aims to bring as many IOCs into Tunisia as possible, in order to generate both the capital and expertise required by the sector to grow. The fi rm also displays a willingness to cooperate with other regional national oil companies. It has agreements with Libya’s National Oil Corporation, Syrian Petroleum Company and Sonatrach of Algeria, while Abu Dhabi-based investment vehi-cle Mubadala Development Company also holds stakes in the Tunisian energy sector. PH

OTO

GR

APH

: SH

UTT

ERS

TOC

K

ETAP Tunisia’s state oil and gas fi rm relies on international partnerships

TUNISIA GDP BY SECTOR, 2011

MAJOR HYDROCARBONS PROJECTS

TUNISIA OIL AND GAS SECTOR, 2012

Source: African Development BankSource: BP

QP=Qatar Petroleum; STIR=Tunisian Company for Refi ning Industries. Source: MEED Projects

Public administration, education, health and social work, community, social and personal services

18

18

9

7

13 %13 15

Transport, storage and communications

Mining

Manufacturing

Construction 4

Agriculture, hunting, forestry and fi shing

Electricity, gas and water 2

Other services 1

Finance, real estate and business services

Wholesale and retail trade, hotels and restaurants

Oil production (thousand barrels a day)

65

Gas production (billion cubic feet a day)

71.6

Scheme Client TypeCost ($m) Status

La Skhira Refi nery QP/STIR Refi ning 2,000 Under review

Mdhila Industrial Complex Triple Super Phosphate Plant

Tunisian Ministry of Industry

Petrochemicals 360 Under construction

Founded: 1972CEO: Mohamed AkroutTel: (+216) 7 128 5300 Web: www.etap.com.tn

The company is keen to exploit enthusiasm for offshore exploration in the Mediterranean and is offering offshore deepwater oil and gas blocks. It has also been considering the possibil-ity of developing shale gas. Etap’s focus has turned to international exploration and produc-tion opportunities.

Subsidiaries and concessionsKey subsidiaries include the driller Compagnie Tunisienne de Forage and the oil explorer Soci-ete de Recherches et d’Exploitation des Petroles en Tunisie, a joint venture with Austria’s OMV. Other subsidiaries involved in joint ven-tures working on oil and gas production include Compagnie Tuniso-Kowaitienne de Petrole (Tuni-sian-Kuwaiti Petroleum Company), with Kuwaiti investors, and Maretap, with Toronto-headquar-tered Canadax Energy Inc.

Etap also has a 50 per cent holding in Joint Oil in partnership with the government of Libya to over-see the development of offshore resources along the Tunisian-Libyan maritime border and in Num-hyd, a joint venture with Algeria’s Sonatrach.

TUNISIAALGERIA

LIBYA

Tunis

TUNISIA OIL AND GAS FIELDS

Oil fi eldGas fi eld

Oil fi eld non-developedGas fi eld non-developed

20 TunisiaSUBBED.indd 20 29/10/2013 10:03

www.meed.com National oil companies 2013 | MEED | 21

UAE

BackgroundAbu Dhabi National Oil Company (Adnoc) is the eighth-largest oil pro-

ducer in the world and the fourth-biggest Opec producer, making it by far the most important oil company in the UAE.

The firm was formed in 1971 to help increase Abu Dhabi’s share of oil production in the UAE, which had begun in 1962-63, when two international consortiums of oil companies, Abu Dhabi Marine Areas (Adma) and Abu Dhabi Petroleum Company (ADPC), started exporting oil from the offshore Umm Shaif and onshore Bu Hasa fields.