Micro insurance & Occupationnal Safety and Health.

19

Micro insurance & Occupationnal Safety and Health W orkshop on Im proving O ccupational Safety and H ealth through the Provision ofM icrofinance, M icro-insurance and B anking Services D ec 7 th and 8 th , 2009 N ile H otel-Cairo

-

Upload

dana-carson -

Category

Documents

-

view

238 -

download

5

Transcript of Micro insurance & Occupationnal Safety and Health.

Micro insurance

&Occupationnal

Safety and Health

Workshop on Improving Occupational Safety and Health through the Provision of Microfinance, Micro-insurance and Banking Services

Dec 7th and 8th, 2009 Nile Hotel - Cairo

SUMMARY

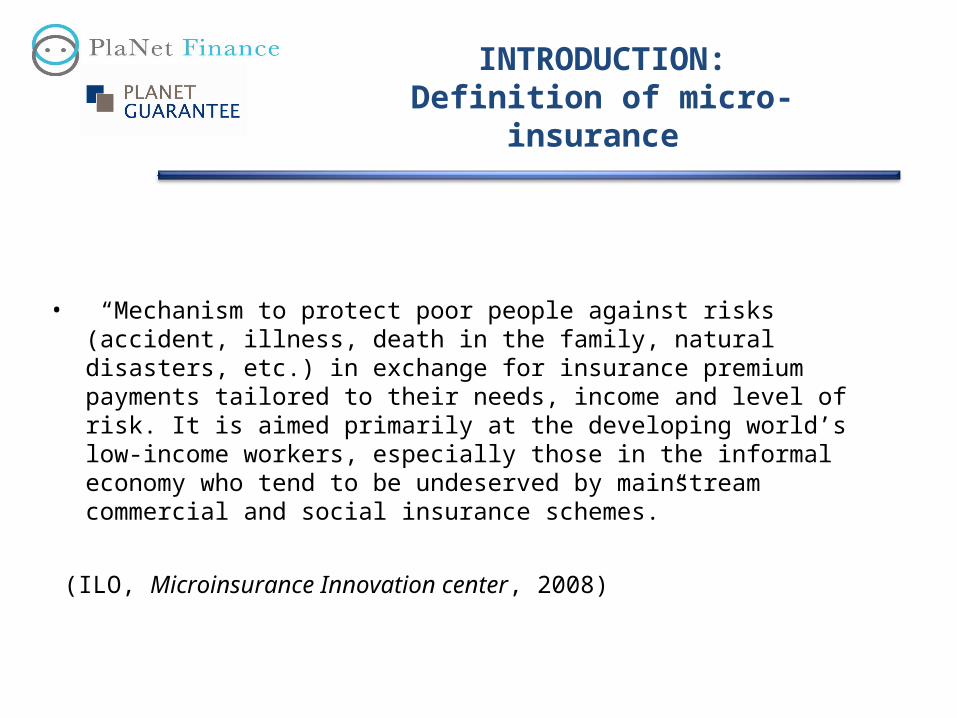

INTRODUCTION:Definition of micro-

insurance

• “Mechanism to protect poor people against risks (accident, illness, death in the family, natural disasters, etc.) in exchange for insurance premium payments tailored to their needs, income and level of risk. It is aimed primarily at the developing world’s low-income workers, especially those in the informal economy who tend to be undeserved by mainstream commercial and social insurance schemes.”

(ILO, Microinsurance Innovation center, 2008)

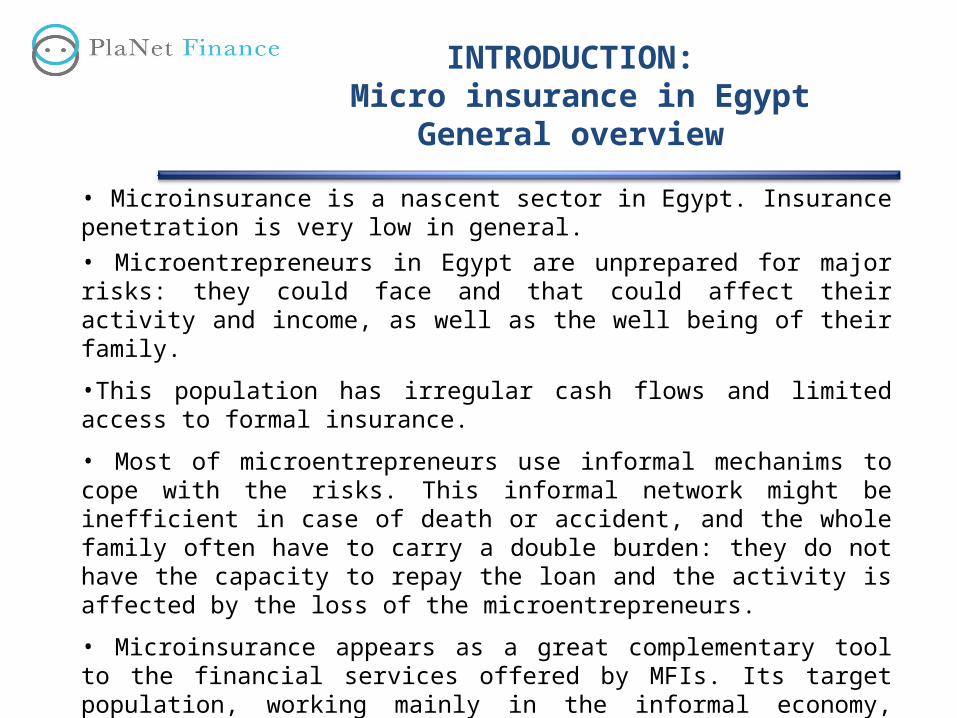

INTRODUCTION: Micro insurance in Egypt

General overview

• Microinsurance is a nascent sector in Egypt. Insurance penetration is very low in general.

• Microentrepreneurs in Egypt are unprepared for major risks: they could face and that could affect their activity and income, as well as the well being of their family.

•This population has irregular cash flows and limited access to formal insurance.

• Most of microentrepreneurs use informal mechanims to cope with the risks. This informal network might be inefficient in case of death or accident, and the whole family often have to carry a double burden: they do not have the capacity to repay the loan and the activity is affected by the loss of the microentrepreneurs.

• Microinsurance appears as a great complementary tool to the financial services offered by MFIs. Its target population, working mainly in the informal economy, would include 83 % of the enterprises in Egypt.

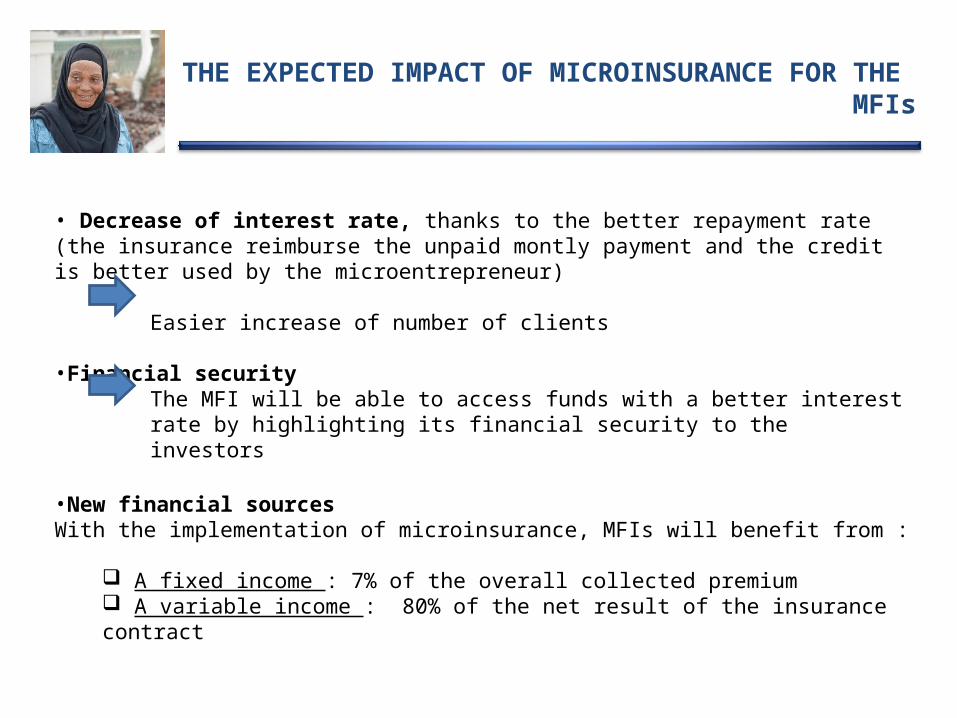

THE EXPECTED IMPACT OF MICROINSURANCE FOR THE MFIs

• Decrease of interest rate, thanks to the better repayment rate (the insurance reimburse the unpaid montly payment and the credit is better used by the microentrepreneur)

Easier increase of number of clients

•Financial securityThe MFI will be able to access funds with a better interest rate by highlighting its financial security to the investors

•New financial sourcesWith the implementation of microinsurance, MFIs will benefit from :

A fixed income : 7% of the overall collected premium A variable income : 80% of the net result of the insurance contract

THE EXPECTED IMPACT OF MICROINSURANCE FOR THE CLIENTS

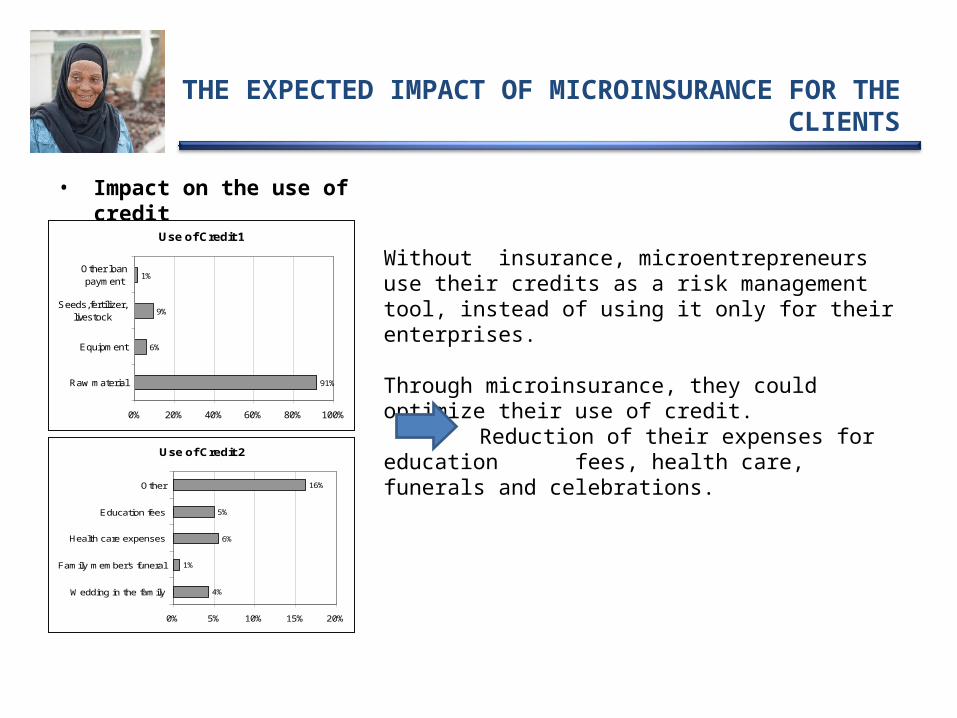

• Impact on the use of credit

Use of Credit 1

91%

6%

9%

1%

0% 20% 40% 60% 80% 100%

Raw material

Equipment

Seeds,fertilizer,livestock

Other loanpayment

Use of Credit 2

4%

1%

6%

5%

16%

0% 5% 10% 15% 20%

Wedding in the family

Family member's funeral

Health care expenses

Education fees

Other

Without insurance, microentrepreneurs use their credits as a risk management tool, instead of using it only for their enterprises.

Through microinsurance, they could optimize their use of credit.

Reduction of their expenses for education fees, health care, funerals and celebrations.

PlaNet Finance

PlaNet Finance Egypt is an affiliate of PlaNet Finance Group.

The PlaNet Finance Group is an International Solidarity Organization, which develops and promotes networks of MFIs, experts and local players in order to support the development of professional projects for men and women who wish to get out of poverty with dignity.

The PlaNet Finance Group responds to all the needs of those involved in microfinance by providing all microfinance actors with a wide range of services. Technical assistance is at the centre of PlaNet Finance’s activities.

PlaNet Guarantee

PlanNet Guarantee is a subsidiary of the PlaNet Finance Group dedicated to the promotion and the development of microinsurance.

PlaNet Guarantee is an insurance broker specialized in microinsurance. PlaNet Guarantee provides technical assistance to MFIs, banks, insurance and reinsurance companies, in order to protect microentrepreneurs from life accidents, by developing and managing microinsurance products.

PlaNet Guarantee

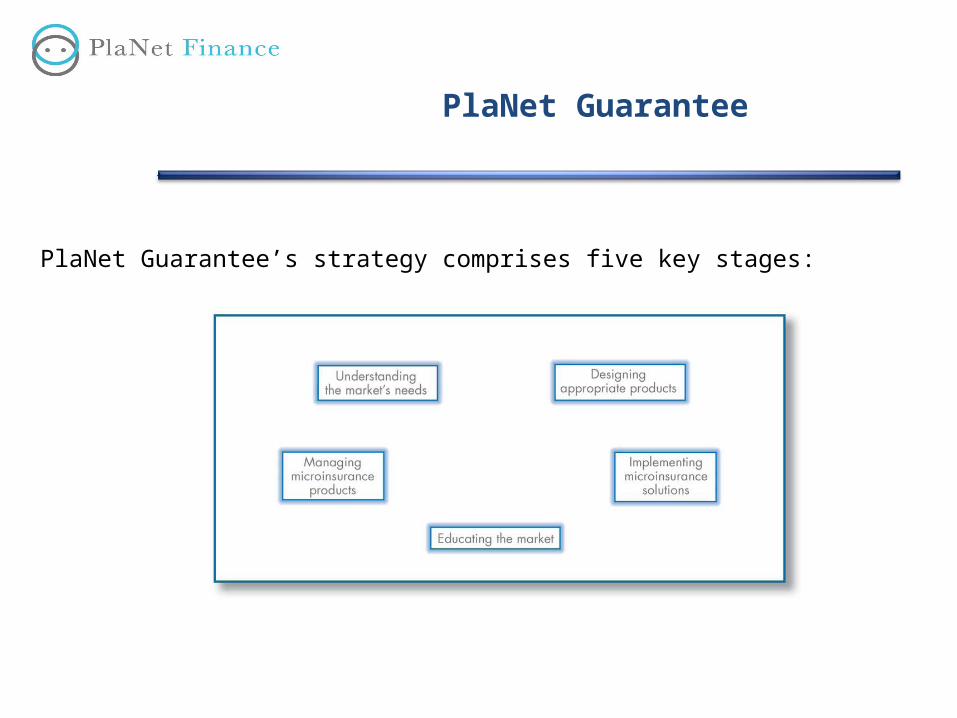

PlaNet Guarantee’s strategy comprises five key stages:

Develop and implement sustainable microinsurance

products in Egypt

Project, funded by FMO, aims to: offering a package of microinsurance products (credit life insurance and complementary products) for selected MFIs who will be the delivery channels towards their clients

Specific Objectives:• Promotion, distribution and management of the products conducted in a highly professional way, setting quality standards for the local and regional microfinance / microinsurance industry.

• Raising awareness among the insurers’ industry on the huge opportunities offered by the microinsurance market.

• Disseminations of learned lessons as best practices amongst microfinance practitioners.

• It will incentivize public agencies to provide regulatory support for the process of microinsurance product innovation, in order to encourage any adjustments needed to expand microinsurance in Latin America and Africa.

Market Survey about microinsurance needs Risks &

Products

Market Survey: 350 questionnaires in 4 governorates (Alexandria, Cairo, Fayoum and Aswan) + 10 focus group discussions

Risks identified:•Economic risks•Heath related risks•Retirement•Natural Disasters•Religious and Social events

Evaluation of the demand for formal insurance mechanisms•Insurance services use and access•Demand for insurance services

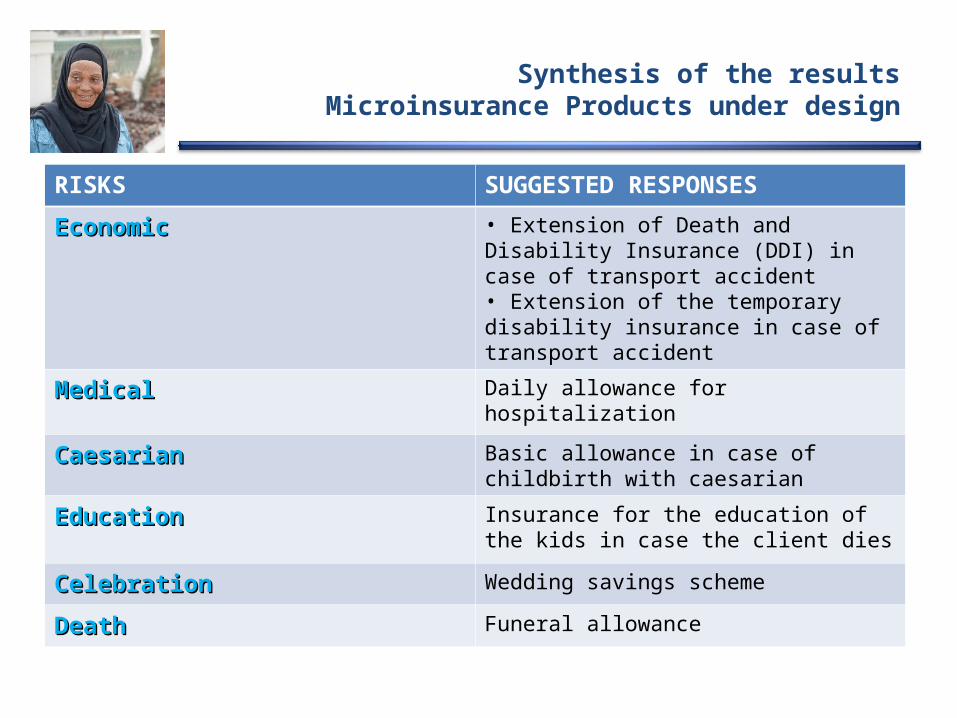

Synthesis of the resultsMicroinsurance Products under design

RISKS SUGGESTED RESPONSES

Economic Economic • Extension of Death and Disability Insurance (DDI) in case of transport accident• Extension of the temporary disability insurance in case of transport accident

Medical Medical Daily allowance for hospitalization

CaesarianCaesarian Basic allowance in case of childbirth with caesarian

Education Education Insurance for the education of the kids in case the client dies

Celebration Celebration Wedding savings scheme

Death Death Funeral allowance

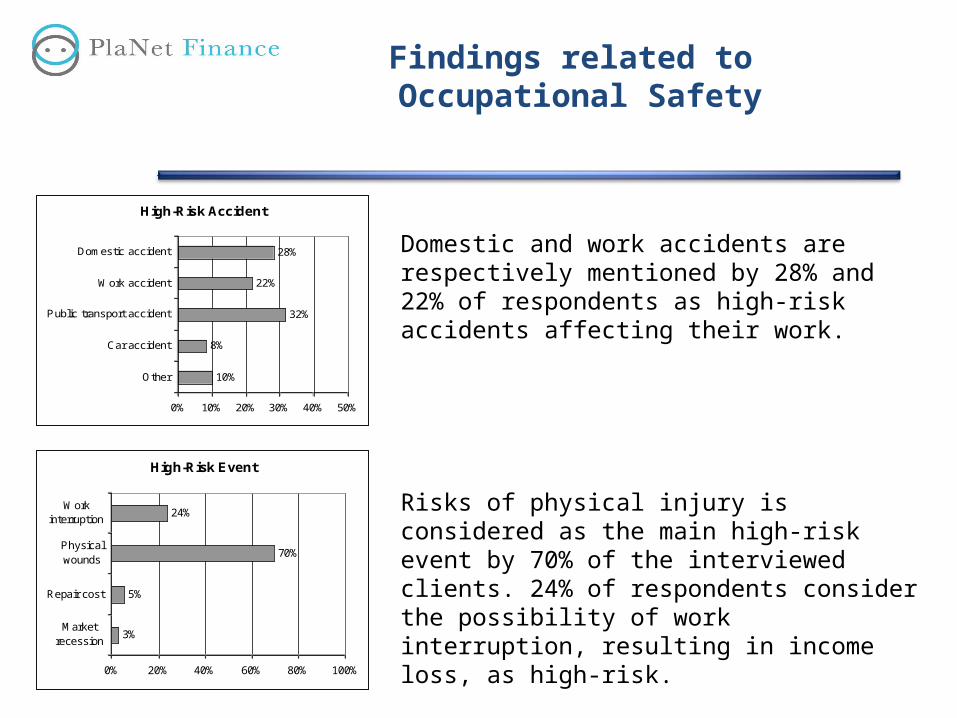

Findings related to Occupational Safety

High-Risk Accident

10%

8%

32%

22%

28%

0% 10% 20% 30% 40% 50%

Other

Car accident

Public transport accident

Work accident

Domestic accident

Domestic and work accidents are respectively mentioned by 28% and 22% of respondents as high-risk accidents affecting their work.

Risks of physical injury is considered as the main high-risk event by 70% of the interviewed clients. 24% of respondents consider the possibility of work interruption, resulting in income loss, as high-risk.

High-Risk Event

3%

5%

70%

24%

0% 20% 40% 60% 80% 100%

Marketrecession

Repair cost

Physicalwounds

Workinterruption

Findings related to Health insurance

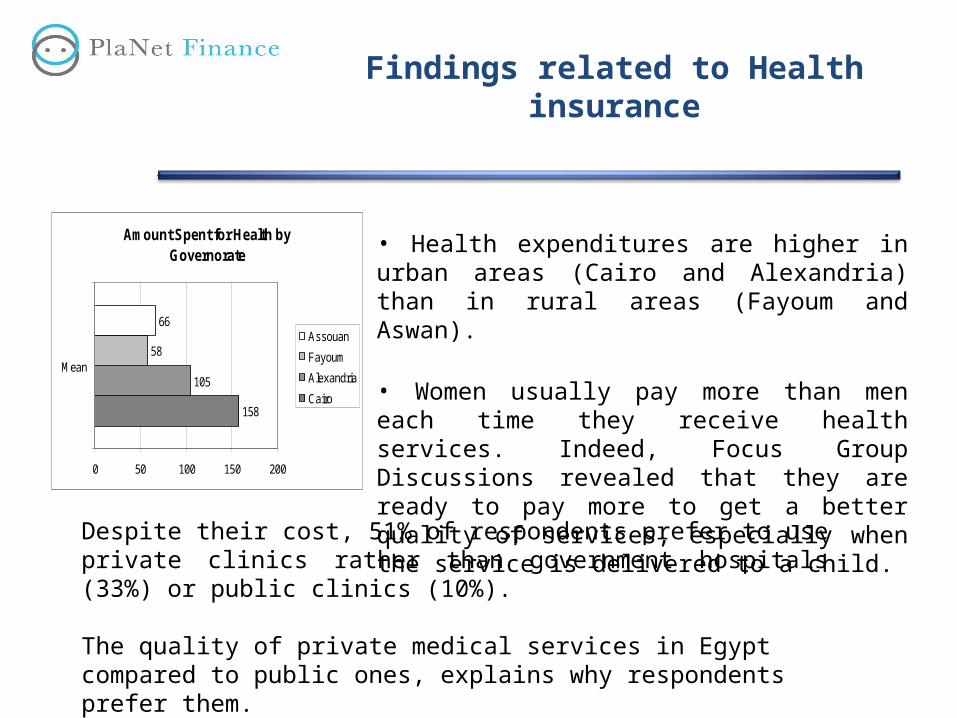

• Health expenditures are higher in urban areas (Cairo and Alexandria) than in rural areas (Fayoum and Aswan).

• Women usually pay more than men each time they receive health services. Indeed, Focus Group Discussions revealed that they are ready to pay more to get a better quality of services, especially when the service is delivered to a child.

Amount Spent for Health by Governorate

158

105

58

66

0 50 100 150 200

Mean

Assouan

Fayoum

Alexandria

Cairo

Despite their cost, 51% of respondents prefer to use private clinics rather than government hospitals (33%) or public clinics (10%).

The quality of private medical services in Egypt compared to public ones, explains why respondents prefer them.

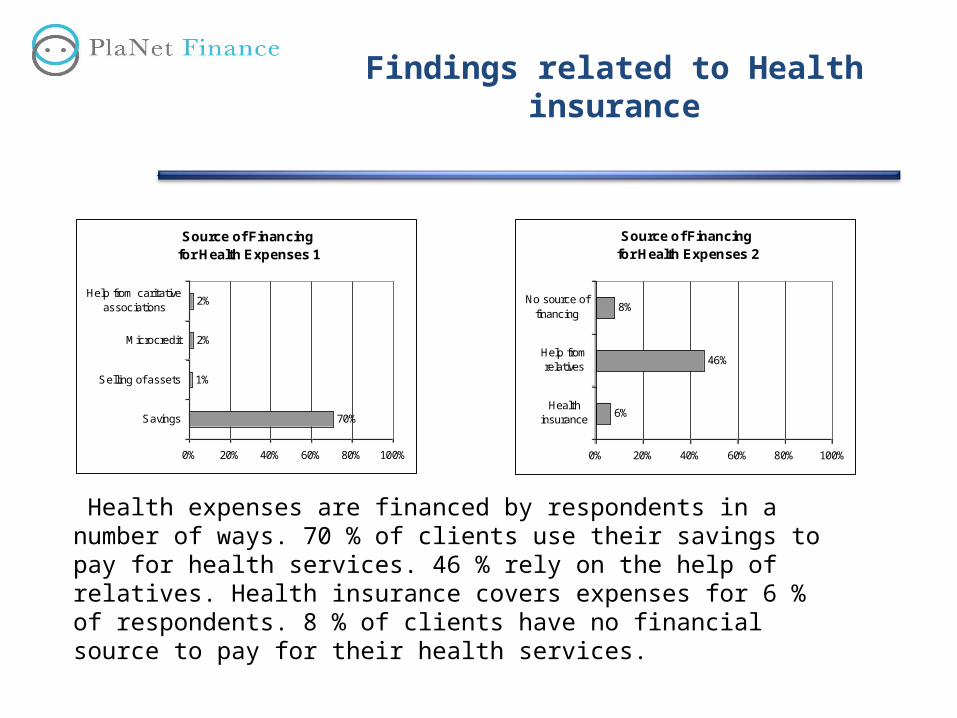

Source of Financing for Health Expenses 1

70%

1%

2%

2%

0% 20% 40% 60% 80% 100%

Savings

Selling of assets

Microcredit

Help from caritativeassociations

Source of Financing for Health Expenses 2

6%

46%

8%

0% 20% 40% 60% 80% 100%

Healthinsurance

Help fromrelatives

No source offinancing

Health expenses are financed by respondents in a number of ways. 70 % of clients use their savings to pay for health services. 46 % rely on the help of relatives. Health insurance covers expenses for 6 % of respondents. 8 % of clients have no financial source to pay for their health services.

Findings related to Health insurance

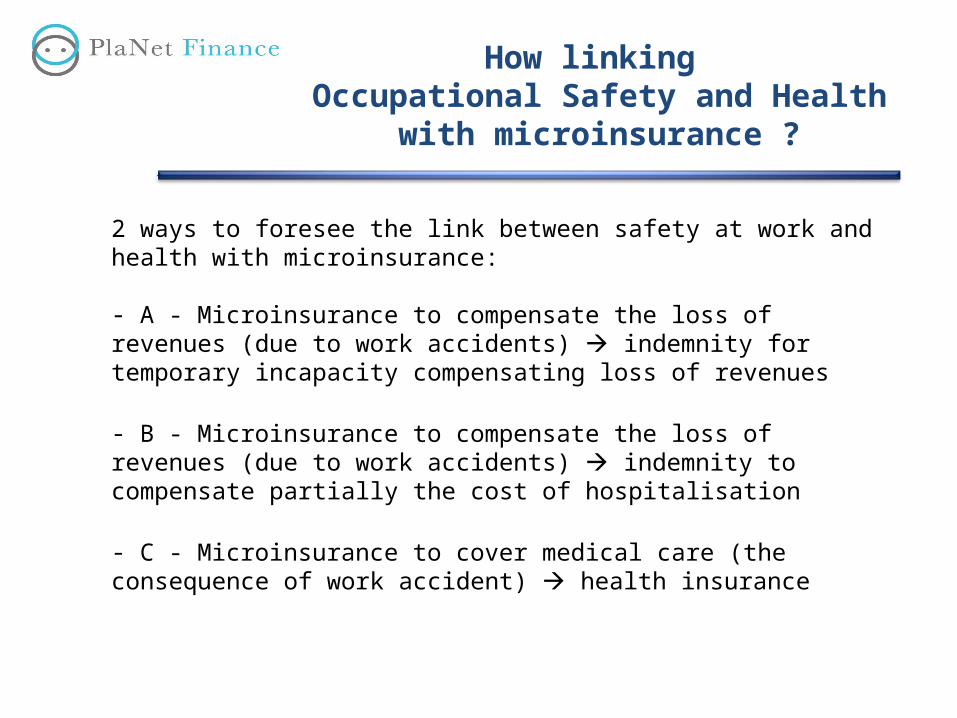

How linking Occupational Safety and Health

with microinsurance ?

2 ways to foresee the link between safety at work and health with microinsurance:

- A - Microinsurance to compensate the loss of revenues (due to work accidents) indemnity for temporary incapacity compensating loss of revenues

- B - Microinsurance to compensate the loss of revenues (due to work accidents) indemnity to compensate partially the cost of hospitalisation

- C - Microinsurance to cover medical care (the consequence of work accident) health insurance

A - Can we imagine microinsurance product - compensating loss of revenues ?

Microinsurance product:

Extension of the temporary disability insurance following a accident at work

•Beneficiaries: to be defined, for instance

o microentrepreneurs operating from his place of worko Beneficiaries of DDI, under 65o No medical selection

•Characteristics: o The insurance reimburses monthly repayment of loan for the disabled microentrepreneurs from the 15th to the 365th day of temporary disability.o Premium for this product paid at the same time of premium for DDI

• Conditions: o Police certificateo Medical certificates establishing the disability and the resumption of work

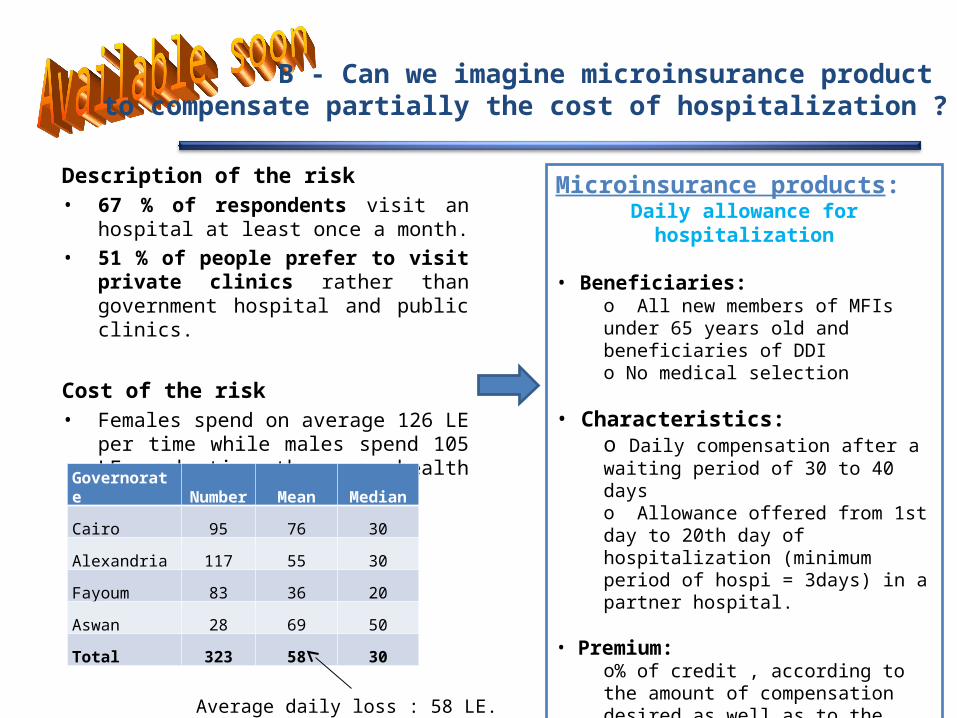

Description of the risk• 67 % of respondents visit an hospital at

least once a month. • 51 % of people prefer to visit private

clinics rather than government hospital and public clinics.

Cost of the risk• Females spend on average 126 LE per

time while males spend 105 LE each time they use health services.

Governorate Number Mean Median

Cairo 95 76 30

Alexandria 117 55 30

Fayoum 83 36 20

Aswan 28 69 50

Total 323 58 30

Average daily loss : 58 LE.

Microinsurance products:Daily allowance for hospitalization

• Beneficiaries: o All new members of MFIs under 65 years old and beneficiaries of DDIo No medical selection

• Characteristics: o Daily compensation after a waiting period of 30 to 40 dayso Allowance offered from 1st day to 20th day of hospitalization (minimum period of hospi = 3days) in a partner hospital.

• Premium:o% of credit , according to the amount of compensation desired as well as to the chacarateristics of the portfolio.o paid at once when credit is disbursedo Covers hospi. Fees and costs of medicine,with proof of payment

B - Can we imagine microinsurance product to compensate partially the cost of hospitalization ?

C - Health insuranceA key factor to minimize risks at work

• Health problems are among the main risks that people could face.

• Poor people cannot afford quality health services and depend on overcrowded public hospitals, suffering from lack of investment, poor infrastructure and corruption

Although the Ministry of Health is supposed to provide medical cover to the whole population, poor people do not have access to adequate medical services and medicines.

• Health risks imply not only the cost that comes with them but also the loss of income linked to work interruption.

• Today, offer medical insurance to cover the medical costs is a challenge