Micro Ch 15

56

Chapter 15 Trade-offs Involving Time and Risk © 2015 Pearson Education, Inc.

-

Upload

mrbagzis -

Category

Economy & Finance

-

view

46 -

download

0

Transcript of Micro Ch 15

© 2015 Pearson Education, Inc.

Chapter 15 Trade-offs

Involving Time and Risk

© 2015 Pearson Education, Inc.

15 Trade-offs Involving Time and Risk

Chapter Outline

15.1 Modeling Time and Risk15.2 The Time Value of Money15.3 Time Preferences15.4 Probability and Risk15.5 Risk Preferences

© 2015 Pearson Education, Inc.

15 Trade-offs Involving Time and Risk

Key Ideas

1. Interest is the payment received for temporarily giving up the use of money.

2. Economists have developed tools to calculate the present value of payments received at different points in the future.

© 2015 Pearson Education, Inc.

15 Trade-offs Involving Time and Risk

Key Ideas

3. Economists have developed tools to calculate the value of risky payments.

© 2015 Pearson Education, Inc.

15 Trade-offs Involving Time and Risk

Evidenced-Based Economics Example:

Do people exhibit a preference for immediate gratification?

© 2015 Pearson Education, Inc.

15 Trade-offs Involving Time and Risk

One-third of long- term smokers die prematurely.

So what?

© 2015 Pearson Education, Inc.

15.1 Modeling Time and Risk

When is $1 not worth $1?

© 2015 Pearson Education, Inc.

15.1 Modeling Time and Risk

In the future = less value

© 2015 Pearson Education, Inc.

15.1 Modeling Time and Risk

Future outcomes have risk.

© 2015 Pearson Education, Inc.

15.1 Modeling Time and Risk

To compare costs/benefits of current events with costs/benefits of future events, use factors to weight time and risk.

© 2015 Pearson Education, Inc.

15.2 The Time Value of Money

When is $1 not worth $1?

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

PrincipalThe amount of an original investment

InterestThe payment received for temporarily giving

up the use of money (or payment for the opportunity to temporarily use someone else’s money)

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

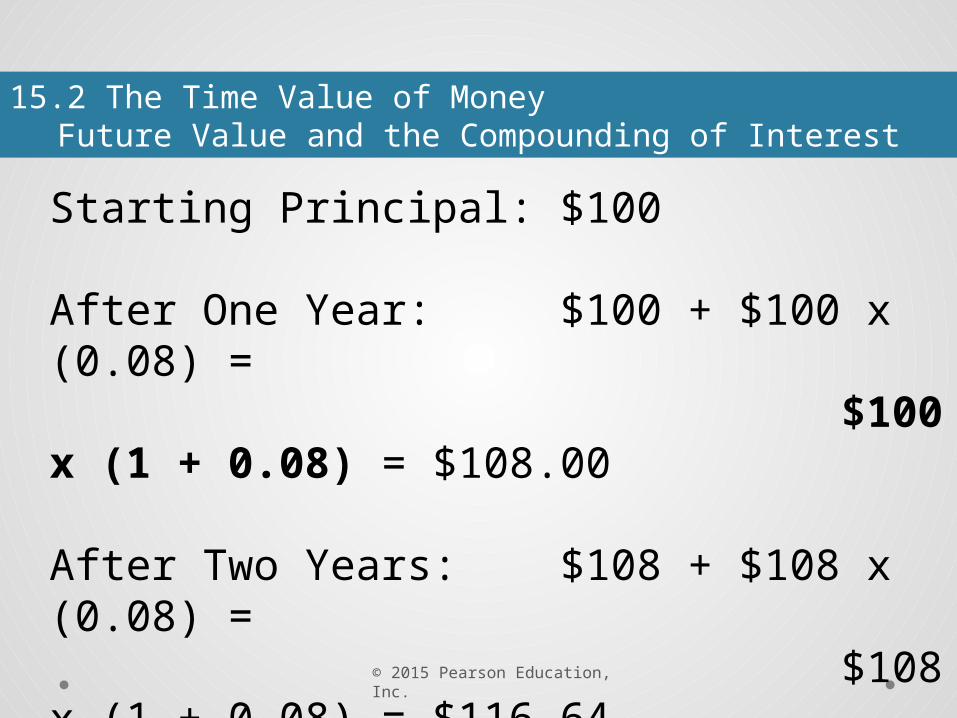

Starting Principal: $100 After One Year: $100 + $100 x (0.08) = $100 x (1 + 0.08) = $108.00

After Two Years: $108 + $108 x (0.08) = $108 x (1 + 0.08) = $116.64 = [$100 x (1 + 0.08)](1 + 0.08) = $100 x (1 + 0.08)2

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

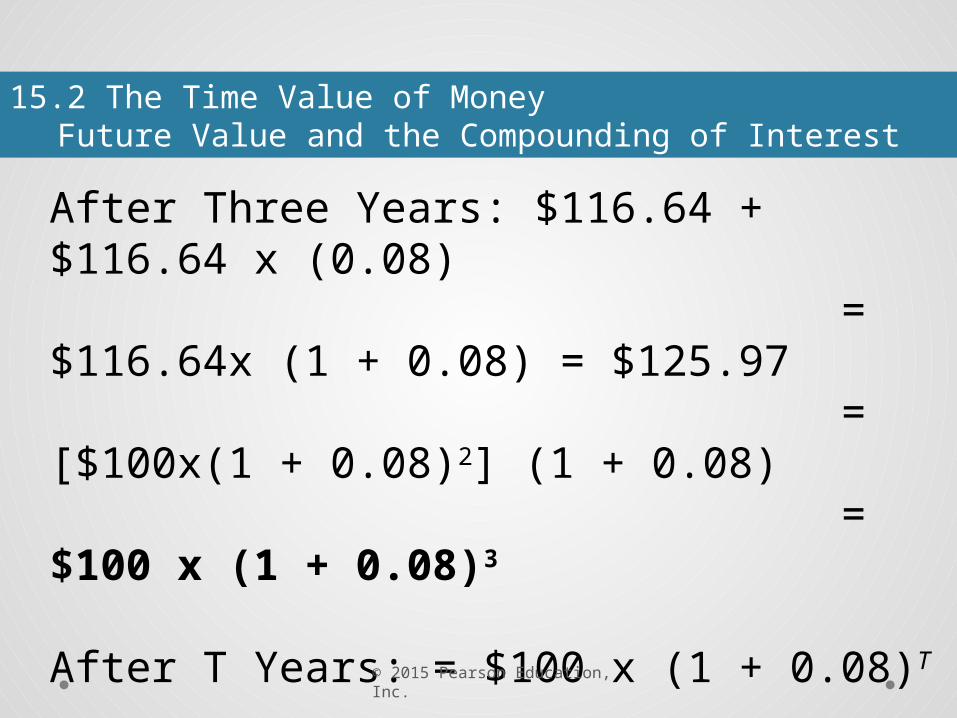

After Three Years: $116.64 + $116.64 x (0.08) = $116.64x (1 + 0.08) = $125.97 = [$100x(1 + 0.08)2] (1 + 0.08) = $100 x (1 + 0.08)3

After T Years: = $100 x (1 + 0.08)T

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

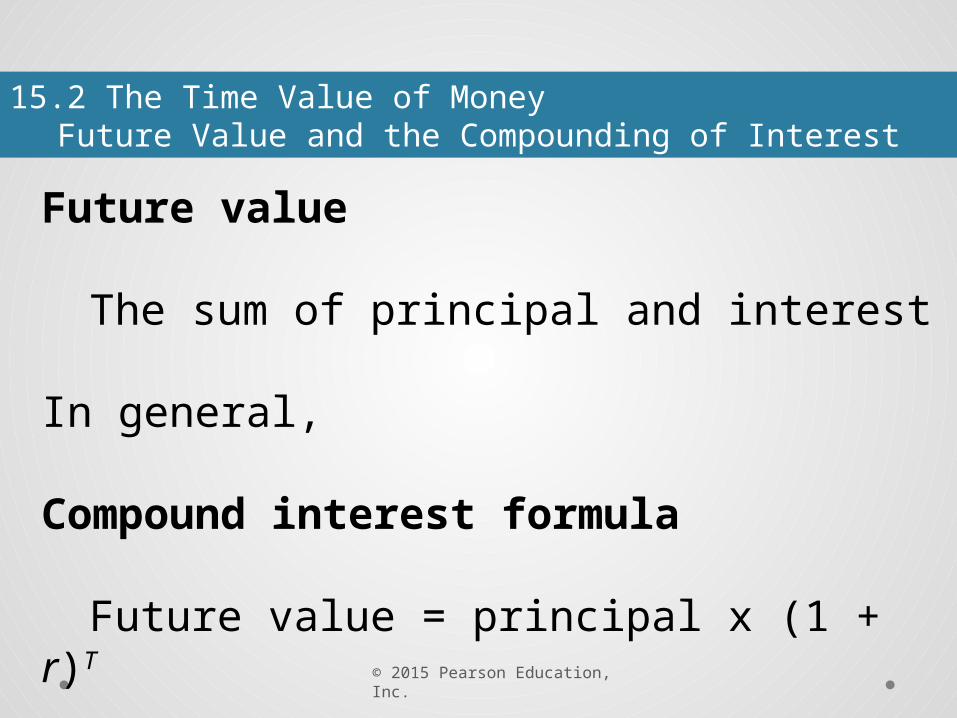

Future value

The sum of principal and interest In general,

Compound interest formula

Future value = principal x (1 + r)T

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

“Compound interest is the greatest invention of all time.”

A. Einstein

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

Cousin It:• Starts saving $2,000 per year beginning at

age 18• Saves at this rate up to and including age

25, then stops saving and lets the account sit• Earns 10% per year

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

Cousin Id:• Picks up where It left off and starts saving

$2,000 per year beginning at age 26• Saves at this rate up to and including age 62,

then stops saving• Earns 10% per year

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

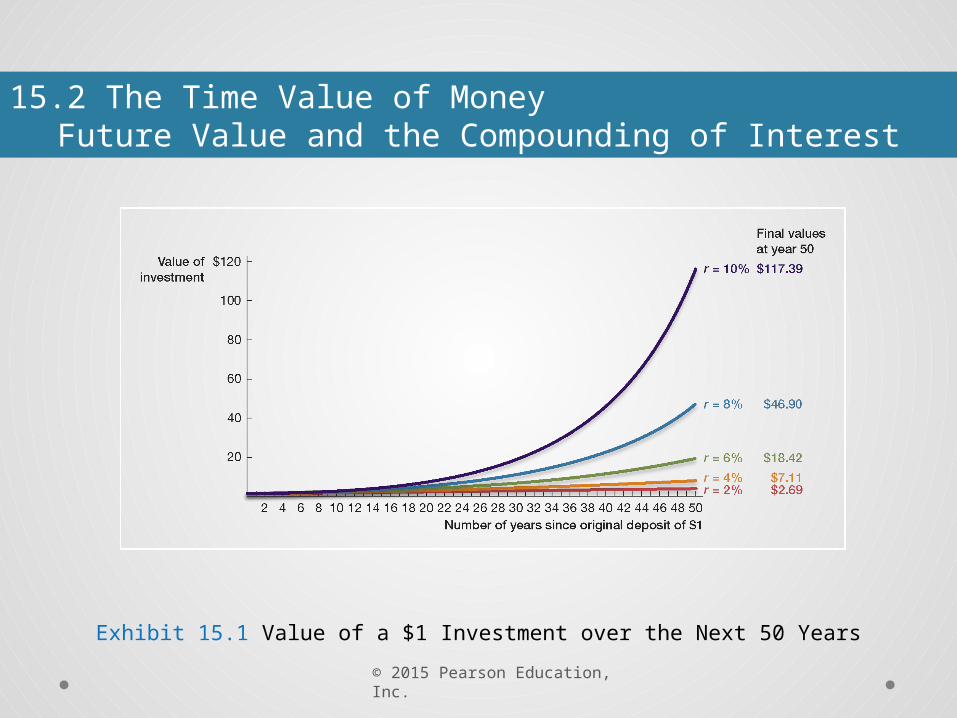

Exhibit 15.1 Value of a $1 Investment over the Next 50 Years

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

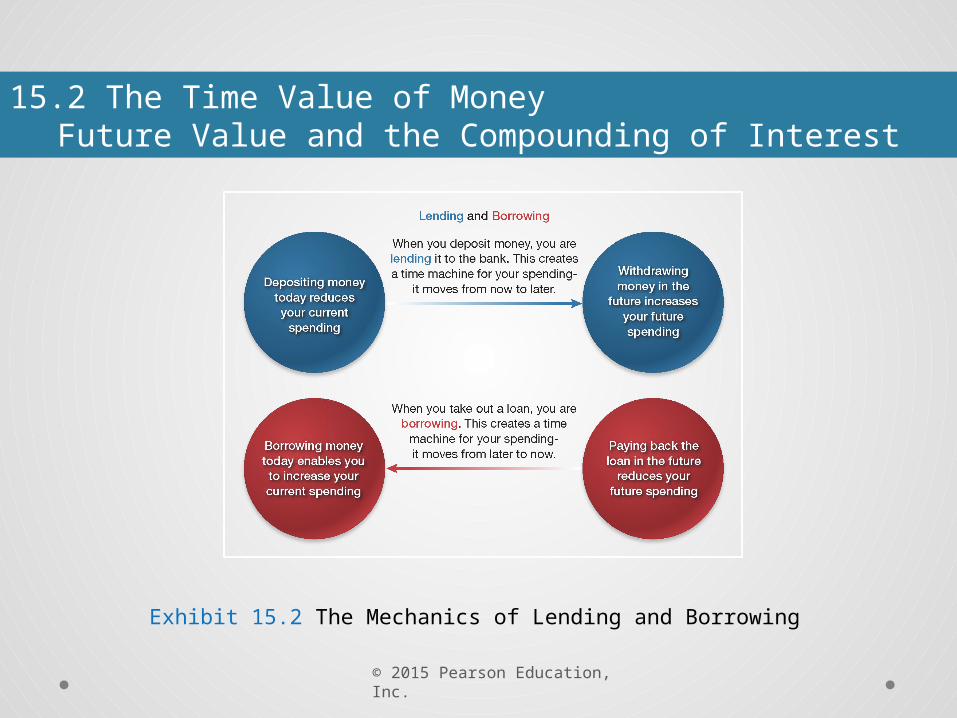

Exhibit 15.2 The Mechanics of Lending and Borrowing

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

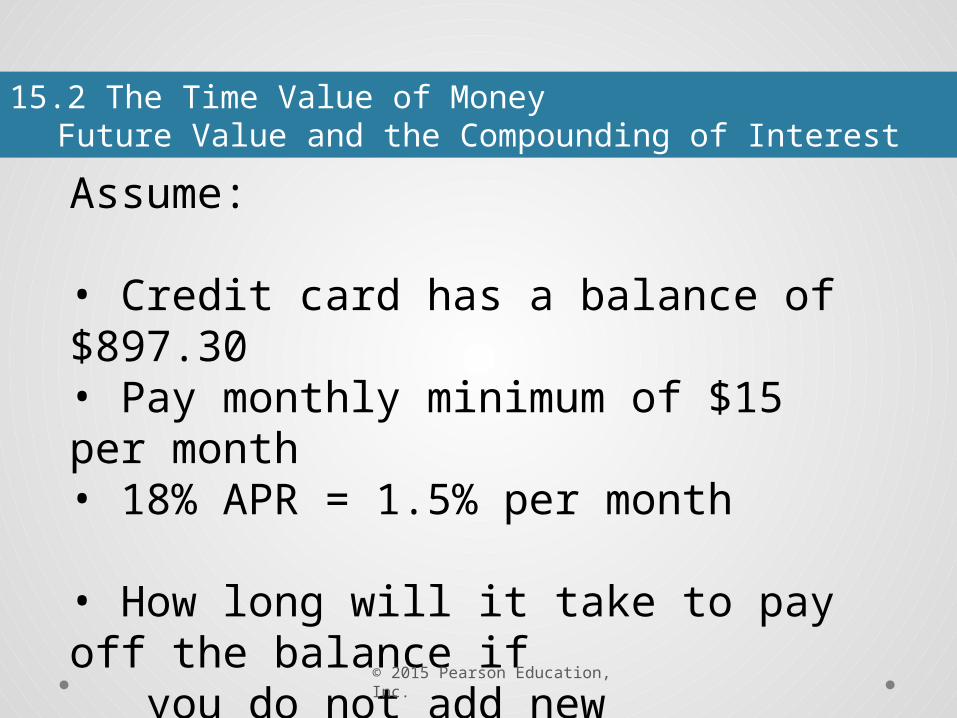

Assume:

• Credit card has a balance of $897.30• Pay monthly minimum of $15 per month• 18% APR = 1.5% per month

• How long will it take to pay off the balance if you do not add new purchases?

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyFuture Value and the Compounding of Interest

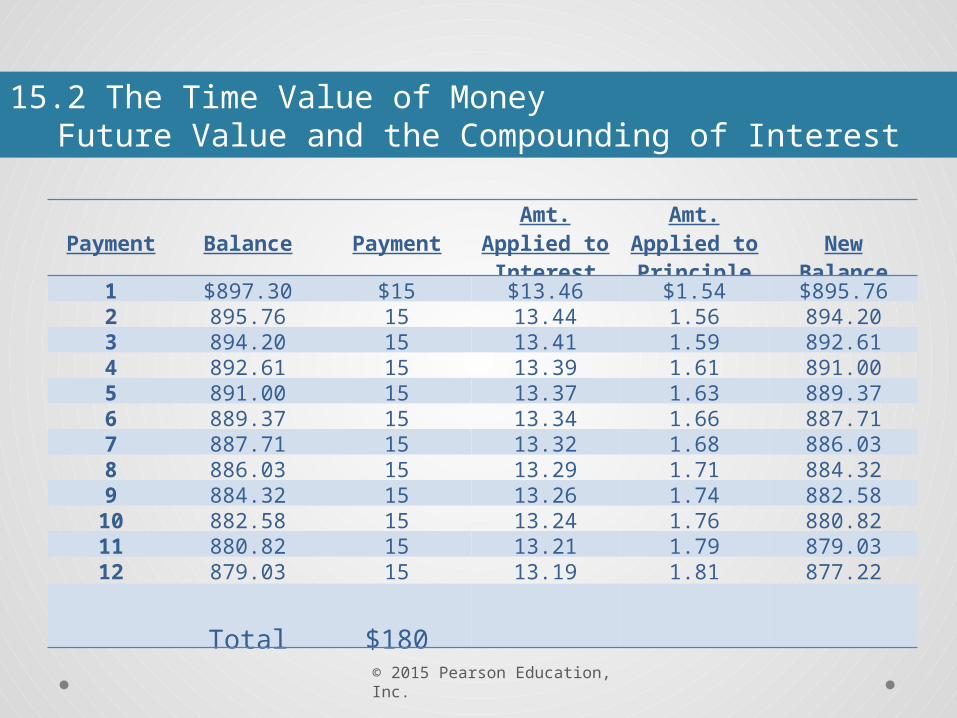

Payment Balance PaymentAmt. Applied

to InterestAmt. Applied to Principle New Balance

1 $897.30 $15 $13.46 $1.54 $895.762 895.76 15 13.44 1.56 894.203 894.20 15 13.41 1.59 892.614 892.61 15 13.39 1.61 891.005 891.00 15 13.37 1.63 889.376 889.37 15 13.34 1.66 887.717 887.71 15 13.32 1.68 886.038 886.03 15 13.29 1.71 884.329 884.32 15 13.26 1.74 882.58

10 882.58 15 13.24 1.76 880.8211 880.82 15 13.21 1.79 879.0312 879.03 15 13.19 1.81 877.22

Total $180

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

When is $1 not worth $1?

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

Future value = principal x (1 + r)T

$3,000 = principal x (1.08)3

$3,000/(1.08)3 = principal

Or $2,381.50 = principal

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

Present value

The present value of a future payment is the amount of money that would need to be invested today to produce that future payment.

Also called the discounted value of a future payment

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

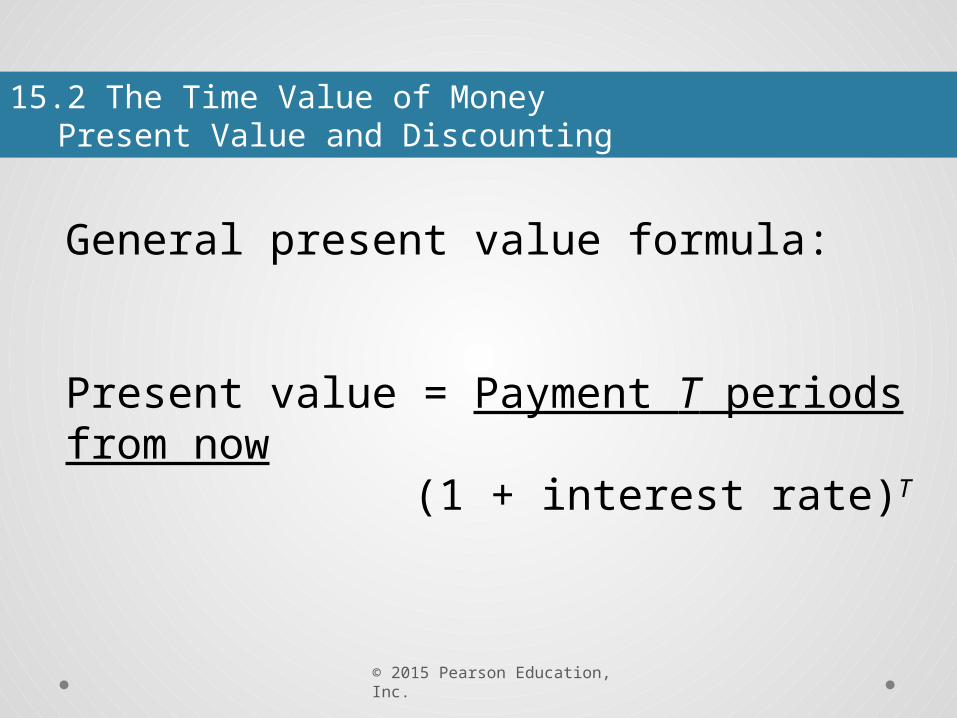

General present value formula:

Present value = Payment T periods from now (1 + interest rate)T

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

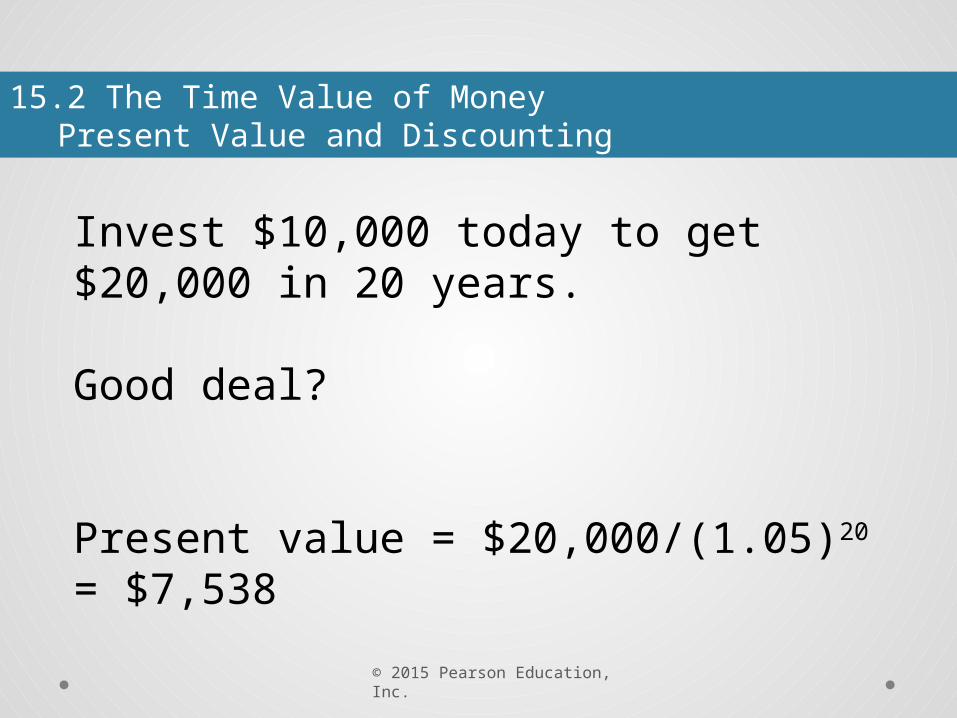

Invest $10,000 today to get $20,000 in 20 years.

Good deal?

Present value = $20,000/(1.05)20 = $7,538

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

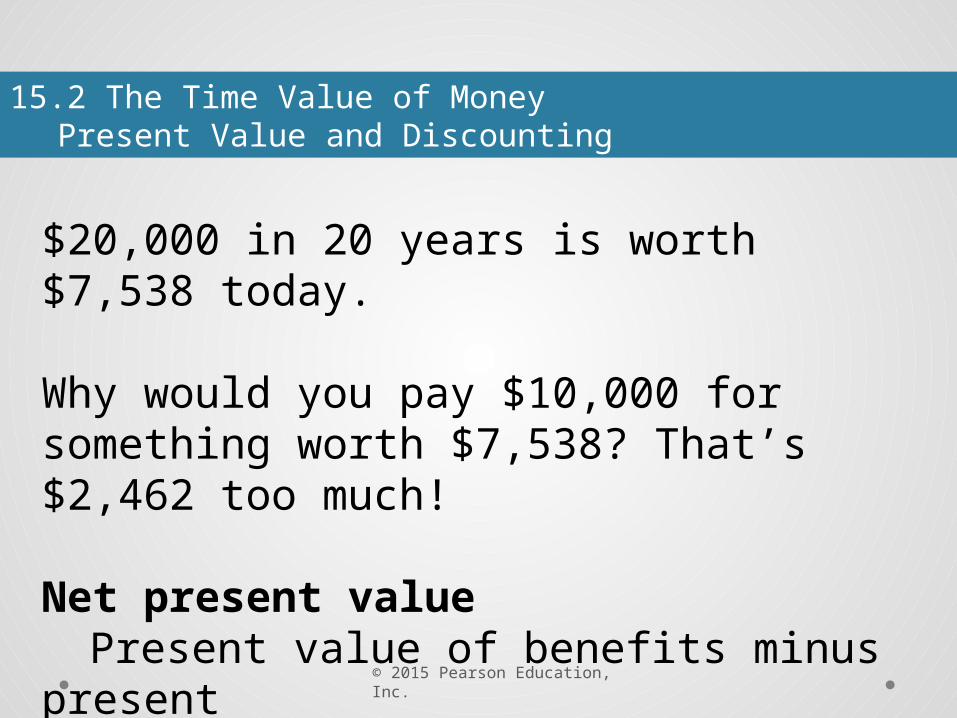

$20,000 in 20 years is worth $7,538 today.

Why would you pay $10,000 for something worth $7,538? That’s $2,462 too much!

Net present valuePresent value of benefits minus present

value of costs

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

Does it matter how you get the $20,000? What if you got $10,000 of it in ten years and $10,000 five years later?

Good deal?

© 2015 Pearson Education, Inc.

15.2 The Time Value of MoneyPresent Value and Discounting

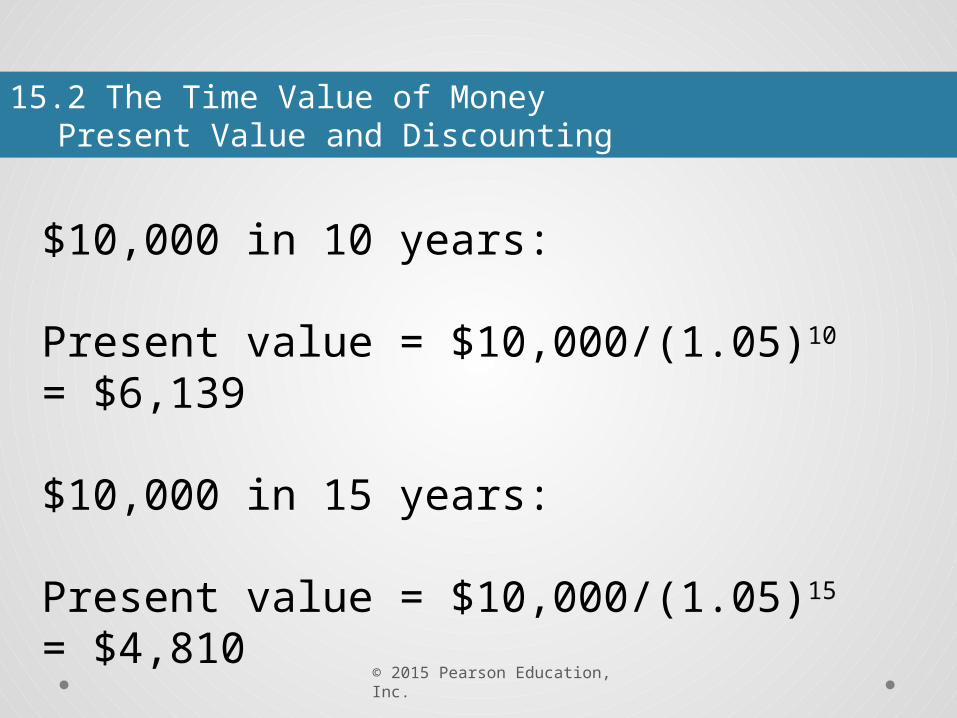

$10,000 in 10 years:

Present value = $10,000/(1.05)10 = $6,139

$10,000 in 15 years:

Present value = $10,000/(1.05)15 = $4,810

$6,139 + $4,810 = $10,949 - $10,000 = $949

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

What does time preference have to do with marshmallows?

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

Utils

Individual measures of utility or happiness

Discount weight

Multiplies future utils to translate them into

current utils

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

Choose between one marshmallow now or 2 marshmallows in 10 minutes.

Suppose each marshmallow has a utility of 6 utils. But the discount rate for waiting 10 minutes is 1/3.

One marshmallow now = 6 utilsTwo marshmallows in 10 minutes = 4 utils

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

Choose between one marshmallow now or 2 marshmallows in 10 minutes.

Suppose each marshmallow has a utility of 6 utils. If you are better at waiting, the discount rate could be 2/3.

One marshmallow now = 6 utilsTwo marshmallows in 10 minutes = 8 utils

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

What about starting a diet? Should you start a diet today or wait until tomorrow?

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

Starting today:Benefit is become healthier more quicklyCost is giving up food you enjoy earlier

Starting tomorrow:Benefit is you get to eat what you want for

another dayCost is delaying becoming healthier

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

Problem:

The benefit of starting today is in the future, while its cost is immediate.

The benefit of starting tomorrow is immediate, while the cost is in the future.

Result: diets that always start “tomorrow”

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

One-third of long- term smokers die prematurely.

So what?

© 2015 Pearson Education, Inc.

15.3 Time PreferencesTime Discounting

Evidenced-Based Economics Example:

Do people exhibit a preference for immediate gratification?

© 2015 Pearson Education, Inc.

15.4 Probability and Risk

Risk

When an outcome is not known with certainty in advance

© 2015 Pearson Education, Inc.

15.4 Probability and RiskRoulette Wheels and Probabilities

Probability

Frequency with which something occurs

© 2015 Pearson Education, Inc.

15.4 Probability and RiskIndependence and the Gambler’s Fallacy

Your lucky number is 27 and you’ve won 10 times in a row!

What number should you bet next?

© 2015 Pearson Education, Inc.

15.4 Probability and RiskExpected Value

Expected value

A probability-weighted value

Present and future values are weighted by time.

Expected values are weighted by probability of occurrence, or risk.

© 2015 Pearson Education, Inc.

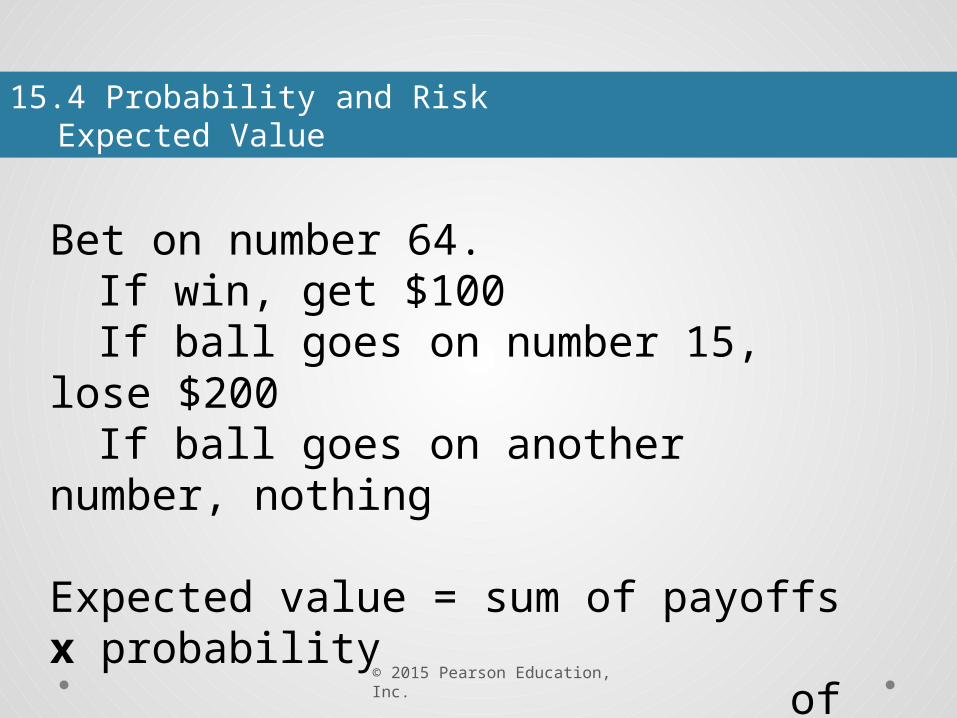

15.4 Probability and RiskExpected Value

Bet on number 64.If win, get $100If ball goes on number 15, lose $200If ball goes on another number, nothing

Expected value = sum of payoffs x probability of occurring

© 2015 Pearson Education, Inc.

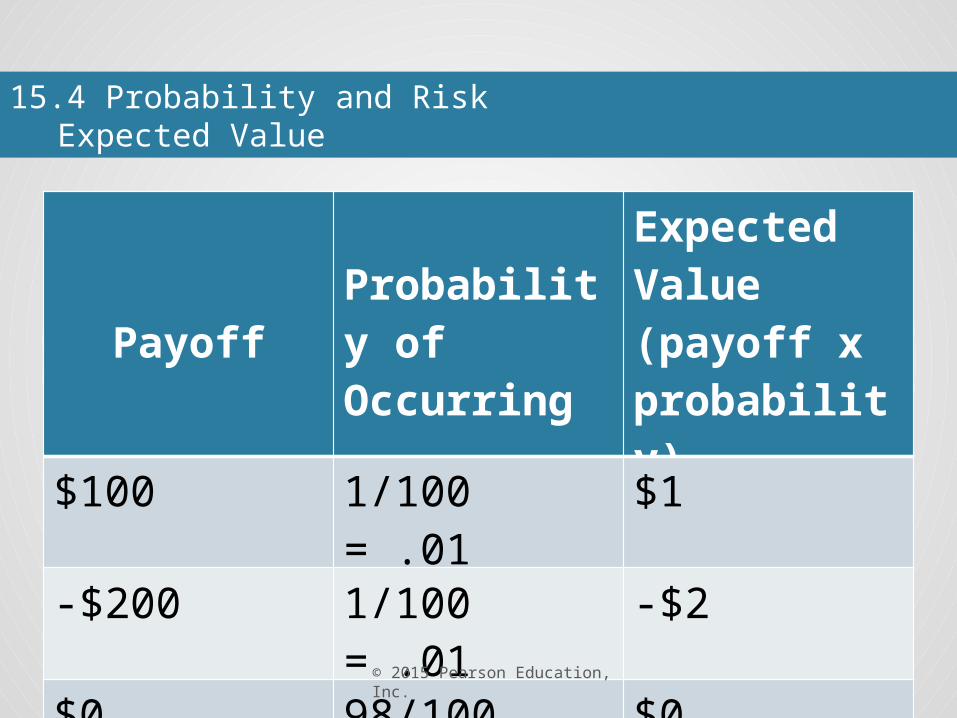

15.4 Probability and RiskExpected Value

PayoffProbability of Occurring

Expected Value (payoff x probability)

$100 1/100 = .01 $1

-$200 1/100 = .01 -$2

$0 98/100 = .98 $0

Sum 100/100 -$1

© 2015 Pearson Education, Inc.

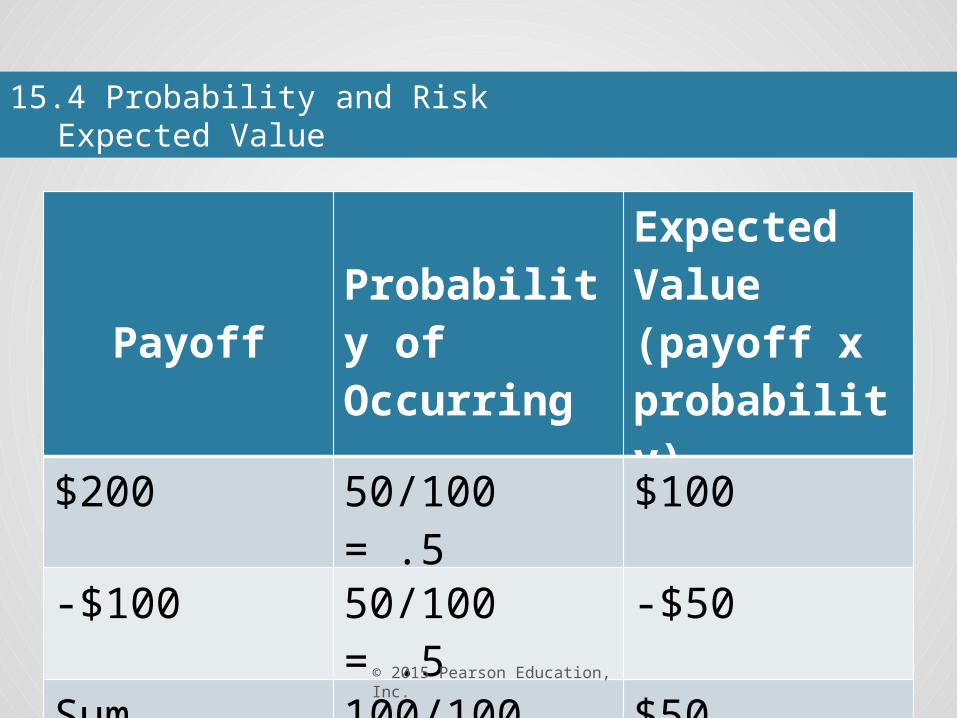

15.4 Probability and RiskExpected Value

If number is 50 or below, win $200

If number is 51 or higher, lose $100

© 2015 Pearson Education, Inc.

15.4 Probability and RiskExpected Value

PayoffProbability of Occurring

Expected Value (payoff x probability)

$200 50/100 = .5 $100

-$100 50/100 = .5 -$50

Sum 100/100 $50

© 2015 Pearson Education, Inc.

15.4 Probability and RiskExtended Warranties

You buy a $300 TV with a 1-year warranty included.

You can buy an extended warranty for years 2 and 3 for another $75.

Should you do it?

© 2015 Pearson Education, Inc.

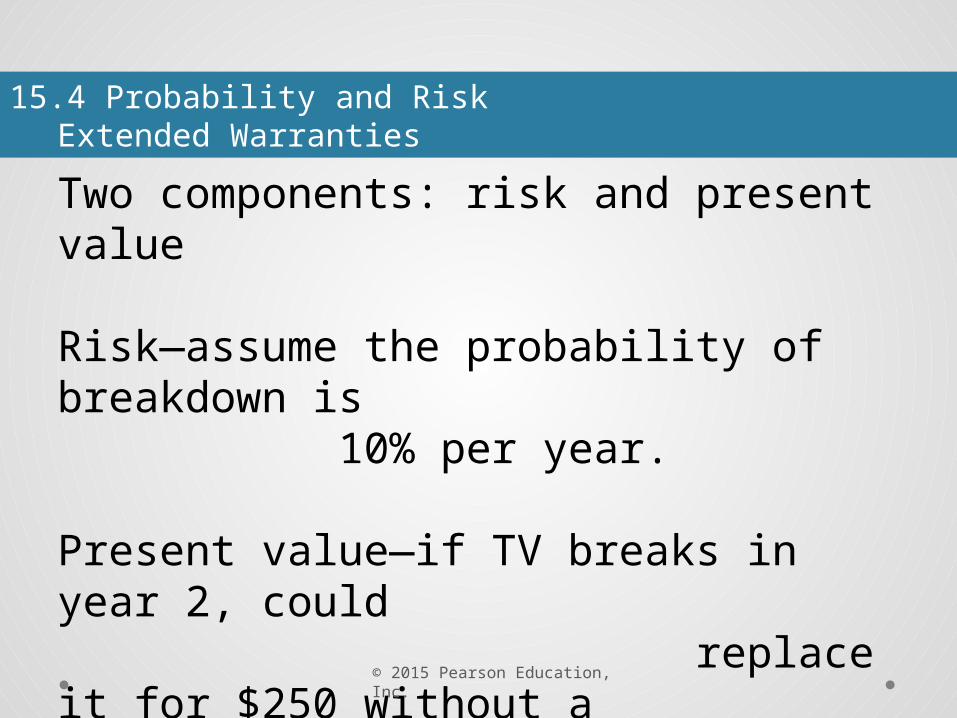

15.4 Probability and RiskExtended Warranties

Two components: risk and present value

Risk—assume the probability of breakdown is 10% per year.

Present value—if TV breaks in year 2, could replace it for $250 without a warranty;

in year 3, could replace for $200

© 2015 Pearson Education, Inc.

15.4 Probability and RiskExtended Warranties

First, present value (assume 10%):

Present value = - $75 + $250/(1.1)2 + $200/(1.1)3

= -$75 + $206.61 + $150.26

But these benefits do not occur with certainty, so to get expected value:

-$75 + $206.61(10/100) + $150.26(10/100)= -$39.31

© 2015 Pearson Education, Inc.

15.5. Risk Preferences

Given that, in general, extended warranties are not a good deal, why do people buy them?

© 2015 Pearson Education, Inc.

15.5. Risk Preferences

Loss aversion

Psychologically weighting a loss more heavily thanweighting a gain

© 2015 Pearson Education, Inc.

15.5. Risk Preferences

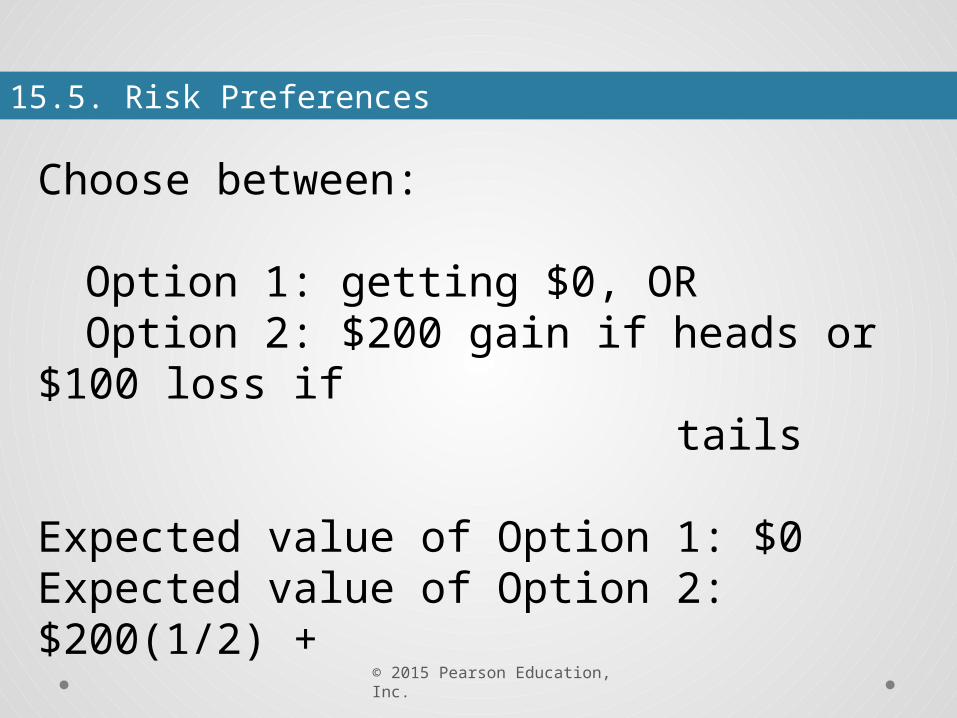

Choose between:

Option 1: getting $0, OROption 2: $200 gain if heads or $100 loss if

tails

Expected value of Option 1: $0Expected value of Option 2: $200(1/2) + (-$100)(1/2) = $50

© 2015 Pearson Education, Inc.

15.5. Risk Preferences

What if you’re this person?

Would you pick Option 2 if you have this amount of loss aversion?

Expected value = $200(1/2) + 2 x (-$100)(1/2) = $0

© 2015 Pearson Education, Inc.

15.5. Risk Preferences

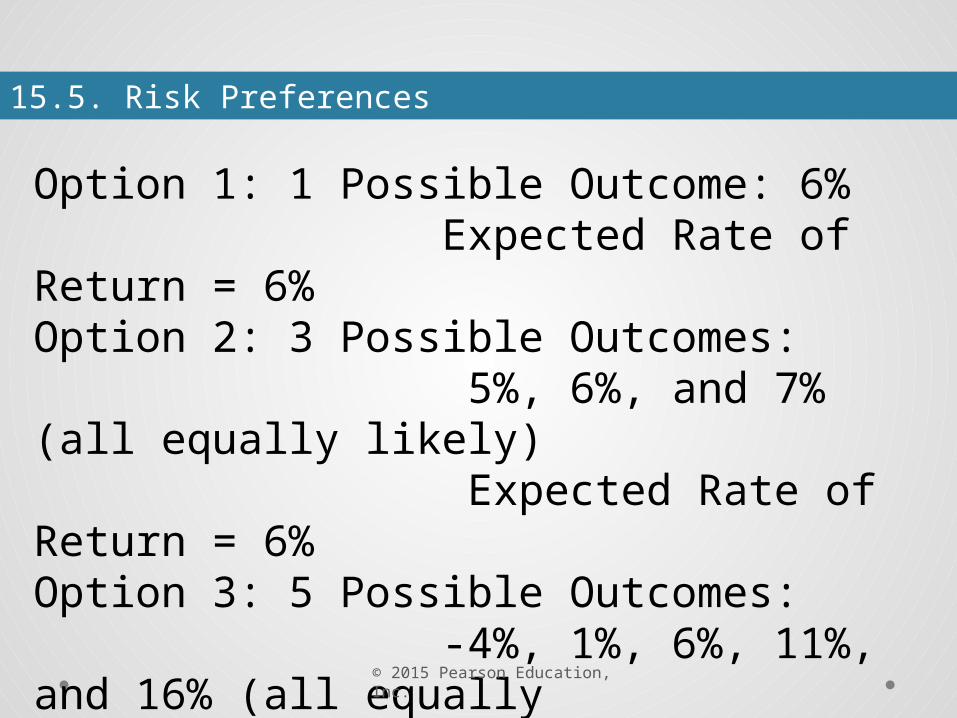

Option 1: 1 Possible Outcome: 6% Expected Rate of Return = 6% Option 2: 3 Possible Outcomes: 5%, 6%, and 7% (all equally likely) Expected Rate of Return = 6% Option 3: 5 Possible Outcomes: -4%, 1%, 6%, 11%, and 16% (all equally likely) Expected Rate of Return = 6%

© 2015 Pearson Education, Inc.

15.5. Risk Preferences

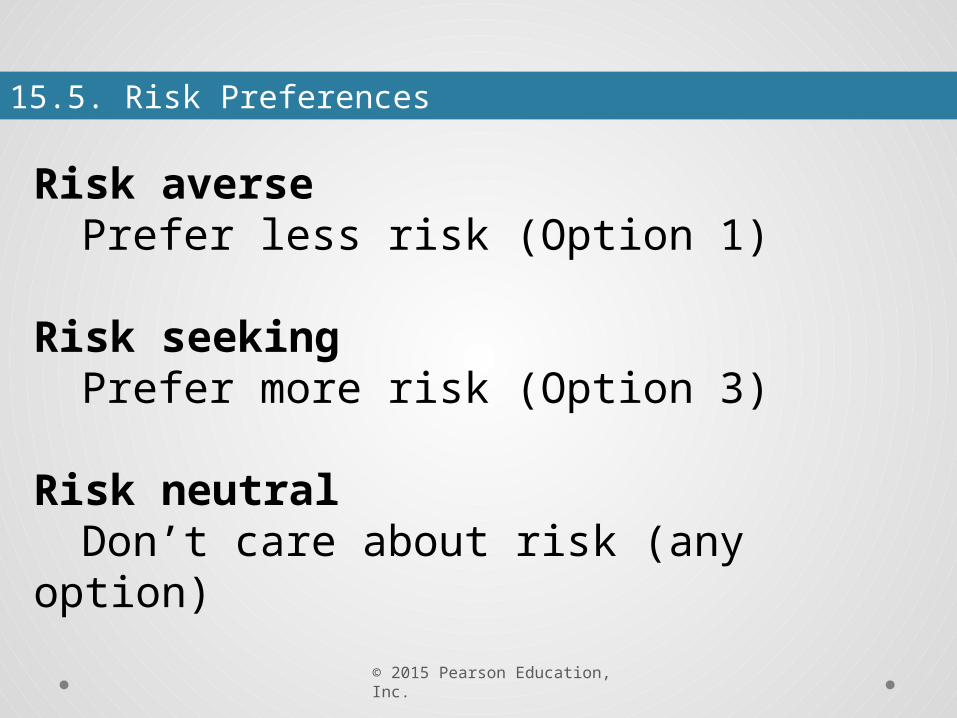

Risk aversePrefer less risk (Option 1)

Risk seekingPrefer more risk (Option 3)

Risk neutralDon’t care about risk (any option)