Michael Johnson slide presentation

10

1 A better deal for savers: helping ordinary workers secure decent living standards in retirement with Rachel Reeves MP 29 May 2014 Michael Johnson www.cps.org.uk

-

Upload

resolutionfoundation -

Category

Government & Nonprofit

-

view

338 -

download

0

description

The struggle to set aside savings and the increasing difficulty that many working people find in securing a decent income at retirement is one of the less noticed but potentially most far-reaching issues in the living standards debate. In her first major speech on pensions policy since becoming Shadow Secretary of State for Work and Pensions, Rachel Reeves MP discussed Labour’s plans for helping those on modest and low incomes save for a pension and secure a decent income at retirement. These are the slides presented by Michael Johnson, Research Fellow at the Centre for Policy Studies who responded to the speech by Rachel Reeves MP on 29th May 2014.

Transcript of Michael Johnson slide presentation

1

A better deal for savers:

helping ordinary workers secure

decent living standards in retirement

with Rachel Reeves MP

29 May 2014

Michael Johnson

www.cps.org.uk

2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1970 1980 1990 2000 2010 2020 2030 2040 2050 2060

Impact of austerity

measures agreed

to 2017

99% in

2062-63

66% low

Ratio excluding

impact of ageing

population

(approx.)

Ratio including

impact of ageing

population

Central projection for Public Sector Net Debt to GDP (%)

We face a sovereign debt crisis

Source: OBR’s Fiscal Sustainability Report July 2013

3

We face a personal debt crisis

Source: Bank of England

* Incl. credit cards, motor and retail finance deals, overdrafts and unsecured loans

Mortgages

Consumer

credit * Total

Personal debt £1,280 billion £159 billion £1,439 billion

Average debt per household £48,454 £6,018 £54,472

Average debt per adult £25,505 £3,168 £28,673

Interest paid per household - - £2,242

Savings (2012) and demographics

Population aged 65+

UK Japan

1950 10.7% 4.9%

2010 16.5% 22.6%

2050 22.9% 37.8%

OECD; National Accounts at a glance 2014. Definition for HNSR: the ratio of household saving (plus

the change in net equity of households in pension funds) to household disposable income.

Household net Net debt

saving rate as % GDP

Greece -14.6% 102%

Japan 0.8% 140%

United Kingdom 2.4% 69%

Italy 3.6% 113%

Netherlands 4.1% 42%

Spain 4.4% 60%

Canada 5.0% 59%

Ireland 5.2% 83%

United States 5.8% 100%

Norway 8.2% -167%

Germany 10.3% 50%

Australia 10.4% 27%

France 11.7% 70%

Sweden 12.2% -24%

5

Ageing population / fewer workers per pensioner

+ Stagnant productivity growth

+ Rising interest rates (2015+ ?)

= Fiscal squeeze

+ Approaching saving tipping point

= Diminishing supply of domestic capital

Cost of capital to rise

We need a savings culture……but……

The squeeze is on

Tax relief, 2012-13

£270 billion of cash since 2001-02

Cost, £ billion

Up-front tax relief on employer contributions £21.3

Up-front tax relief on employee contributions £6.7

Tax-exempt 25% lump sum at retirement (approx.) £4.0

NICs relief on employer contributions £15.2

Tax foregone on investments held in pensions products £6.9

Total £54.1

HMRC; Table PEN 6: Cost of Registered Pension Scheme Tax Relief, February 2014

Tax relief: inequitably distributed

Income

distribution

% of all

contributions

% of total tax

relief

Corresponding

annual income*

Bottom half 16% 14% less than £24,000

Next 40% 35% 32% £24,001 to £51,000

Top 10% 49% 54% Over £51,000

100% 100%

Top 1% 15% 30% Over £100,000

Top 0.5% 10% 22% Over £150,000

* approx

Income tax is progressive, so tax relief is inevitably regressive

HMRC; Personal Incomes Statistics 2011-12, January 2014

8

• Scrap all tax relief 50p per £1 subscribed

• Independent of taxpaying status

• Highly redistributive & simple

• Max. £4,000 from HMT: focused on first £8,000 savings

Tax relief: CPS proposals to boost effectiveness*

* Retirement saving incentives: the end of tax relief, and a new beginning, MJ, 15 April 2014

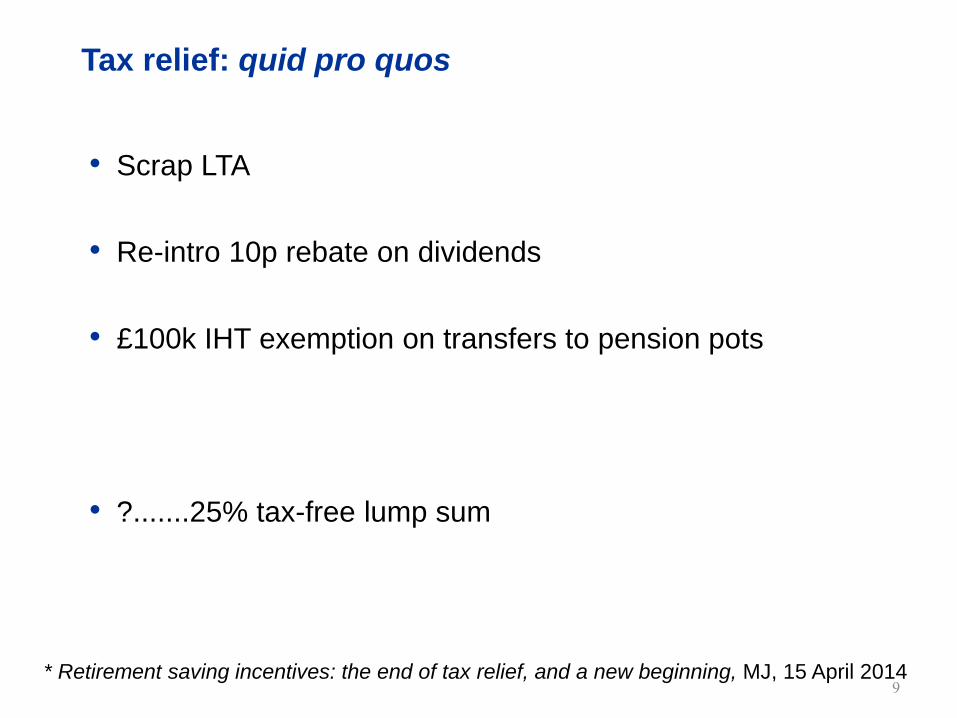

9

• Scrap LTA

• Re-intro 10p rebate on dividends

• £100k IHT exemption on transfers to pension pots

• ?.......25% tax-free lump sum

Tax relief: quid pro quos

* Retirement saving incentives: the end of tax relief, and a new beginning, MJ, 15 April 2014

10

• Capital crisis coming

• Industry lacks common purpose with consumers

• 80% of active managers not needed?

• Tax relief: the lowest hanging, juiciest fruit in Whitehall?

• Formally bring ISAs into the retirement arena……

………the Lifetime ISA

• What future private pensions?

Conclusion

![Adam michael johnson[1]](https://static.fdocuments.net/doc/165x107/55a34da01a28ab3e6e8b4825/adam-michael-johnson1.jpg)