Metso and profitable growth and profitable growth ... Metso’s current business scope, order...

25

Metso and profitable growth Metso Breakfast Meeting in Helsinki October 29, 2007 Jorma Eloranta President and CEO

Transcript of Metso and profitable growth and profitable growth ... Metso’s current business scope, order...

Metso and profitable growth

Metso Breakfast Meeting in HelsinkiOctober 29, 2007

Jorma ElorantaPresident and CEO

2 © Metso Corporation 2007 October 29, 2007

Forward looking statements

It should be noted that certain statements herein which are not historical facts, including, withoutlimitation, those regarding expectations for general economic development and the market situation,expectations for customer industry profitability and investment willingness, expectations for companygrowth, development and profitability and the realization of synergy benefits and cost savings, andstatements preceded by ”expects”, ”estimates”, ”forecasts” or similar expressions, are forward-looking statements. These statements are based on current decisions and plans and currentlyknown factors. They involve risks and uncertainties which may cause the actual results to materiallydiffer from the results currently expected by the company.Such factors include, but are not limited to:(1) general economic conditions, including fluctuations in exchange rates and interest levels whichinfluence the operating environment and profitability of customers and thereby the orders receivedby the company and their margins(2) the competitive situation, especially significant technological solutionsdeveloped by competitors(3) the company’s own operating conditions, such as the success of production, productdevelopment and project management and their continuous development and improvement(4) the success of pending and future acquisitions and restructuring.

Q3 financial performance and short-term outlook

4 © Metso Corporation 2007 October 29, 2007

Highlights of the third quarter

10.610.8EBITA margin, %

22.222.124.5ROCE annualized, %

18113133Free cash flow, EUR million

120.66EPS, EUR10.39.9Operating profit margin, %

19120.4143.4Operating profit, EUR million

26124.4157.3EBITA, EUR million

241,1691,452Net sales, EUR million

503,0224,519Order backlog, EUR million91,3211,440Orders received, EUR million

Change %Q3/06Q3/07

0.59

5 © Metso Corporation 2007 October 29, 2007

Good/ExcellentPower, oil & gasSatisfactory/GoodPulp & Paper

Metso AutomationExcellentMetal recyclingExcellentMining

Good/ExcellentConstructionMetso Minerals

ExcellentPowerSatisfactoryTissue

Satisfactory/GoodPaper & BoardSatisfactory/GoodPulp

Metso Paper

Market outlook 2007–2008

6 © Metso Corporation 2007 October 29, 2007

Short-term financial outlook

The estimates concerning Metso’s financial performance are based onMetso’s current business scope, order backlog and market outlook.

2007

• It is estimated that Metso’s netsales for 2007 will grow by about25% on 2006 and that theoperating profit will clearlyimprove.

• The EBITA margin is estimatedto improve to about 10% andoperating profit margin to beabout 9%.

2008

• Metso’s profitable growth set tocontinue.

Market drivers and trends

8 © Metso Corporation 2007 October 29, 2007

We operate in growth businesses

Growing demandin our customer

industries

Importance of process andunit machine automation

Minerals consumption up forseveral years - mining movesto South and/or East

Investments in transportationand infrastructure development

Energy consumption growingworldwide

New pulp capacityin Southern Hemisphere

Demand for upgrades, rebuildsand service in developed countries

Rapid growth of paper and boardconsumption in emerging economies

Mining super-cycle, driven bycontinued growth of emergingeconomies

Development of newmining assets,especially in South & East

Increasing demand for newpower generation solutions

Recycling, renewable fuelsand other environmentalissues. Increasing demandfor ”clean technogy”products and services in,which Metso is wellestablished.

9 © Metso Corporation 2007 October 29, 2007

Resources and technology•Labor and talent markets globalizing•Ageing population in developed economies >>pressure for knowledge retention•Faster pace of economicinnovation•Constraints on supply orusage of natural resources

Customers and markets•Strong economic growth inemerging markets continues•Consumer landscape changesand expands significantly;new demand trends in emergingmarkets•Shifting economic activitybetween and within regions

Main drivers in the business developmentsupport our continuing profitable growth

Competitors and peers•Low-cost country (LCC) sourcing•R&D and support functions ingrowth markets•Geopolitical instability•Increased regulatory burden

Regulatory and macro environment•Non-traditional, global industry structures•Role and behavior of big businessunder sharp scrutiny•Increased regulatory burden•Geopolitical instability•Climate change impact onlegislation

10 © Metso Corporation 2007 October 29, 2007

Demand trends for Metso’s products

100

120

140

160

180

200

220

2006e 2007e 2008e 2009e 2010e 2011e 2013e 2014e

Mining 9.0%

Metal recycling5.0%

DCS 6.6%

Paper & Board3.5%

CAGR 06-14Indexed

Power 7.0%

Kraft pulp 3.6%

ConstructionMining Recycling Distributed control system (DCS)Kraft pulpValves Paper & Board Power

Construction5.0%

Valves5.4%

Market, EUR billion

Including aftermarket. All figures nominal, including inflation.Sources: Freedonia, ARC, Pöyry, European Renewable Energy Council, Metso estimates

11 © Metso Corporation 2007 October 29, 2007

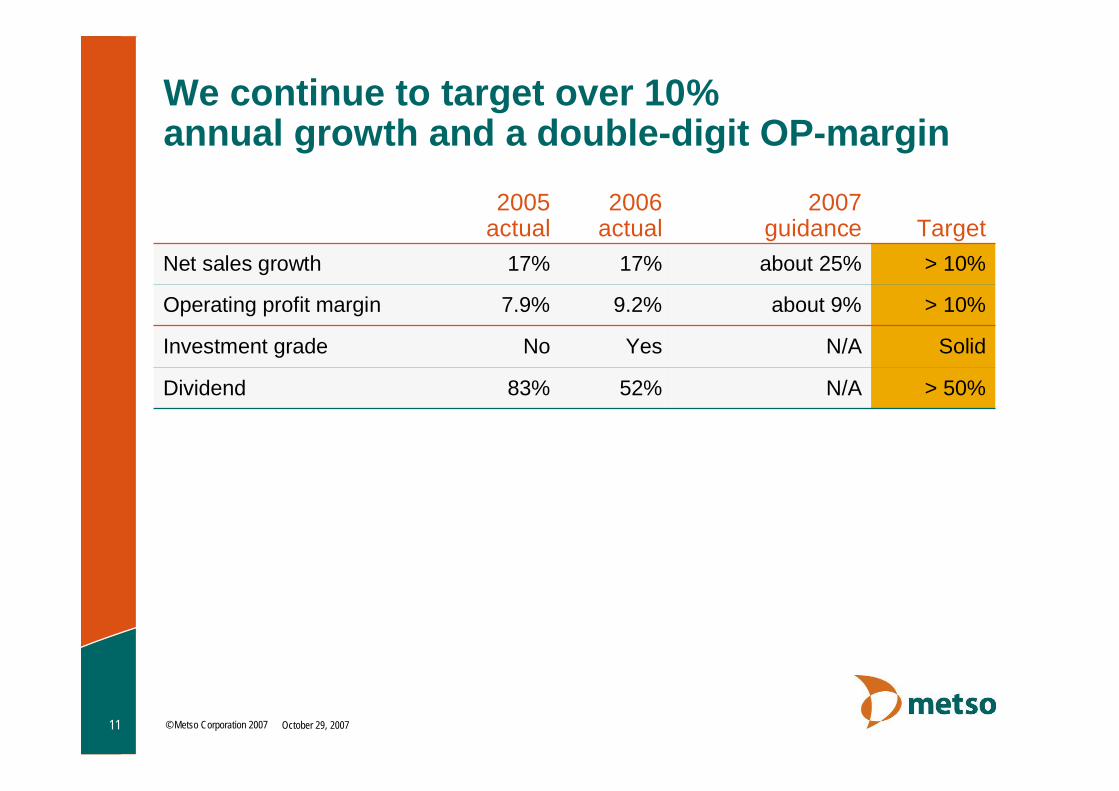

We continue to target over 10%annual growth and a double-digit OP-margin

N/A

N/A

about 9%

about 25%

2007guidance

> 50%

Solid

> 10%

> 10%Target

52%83%Dividend

YesNoInvestment grade

9.2%7.9%Operating profit margin

17%17%Net sales growth

2006actual

2005actual

Metso’s strategy and actions

13 © Metso Corporation 2007 October 29, 2007

Key value driversfor profitable growth

Global operationsfootprintimplementation

- Sales excellence

- Quality

Environmentalbusiness

Continued operationalexcellence improvement

- Productivity

Active acquisitionapproach

Service businessgrowth

Innovation andstrategic R&D

Talent andcompetencedevelopment

Sufficient investments development

Improving profitability

Drivi

nggr

owth

- Cost optimization

14 © Metso Corporation 2007 October 29, 200714

Global operational footprint”The world is flat”

Global resources, competencies, skills

Sales

ServiceManufacturing

EngineeringR&DSourcing

15 © Metso Corporation 2007 October 29, 2007

76 7369

63 6661

2427

3137

3439

0

10

20

30

40

50

60

70

80

2001 2002 2003 2004 2005 2006

Stronger presence in emerging markets

Net sales (%) Personnel (%)

Developedmarkets

Emergingmarkets

83 82 80 80 78 76

17 18 20 20 22 24

0

10

20

30

40

50

60

70

80

90

2001 2002 2003 2004 2005 2006

16 © Metso Corporation 2007 October 29, 2007

Strengthening global delivery capabilityMetso Paper

- Expansion of power boiler facilities in Lapua, Finland(operational in Q1/2008)

- Expansion of paper roll manufacturing in Jyväskylä, Finland(operational in Q4/07)

- Paper machinery facility in Shanghai, China (operationalsince 2006)

- Expansion of service center in Wuxi, China (operational inQ3/07)

- Service center in Guangzhou, China (operational in 2008)- Service center for Metso Power in Charlotte, the US

(operational in Q3/08)Metso Minerals

- Expansion of mobile crusher assembly capacity in Bawal,India (operational in Q4/08)

- Expansion of the foundry in Ahmedabad, India (operationalin Q4/08)

- Expansion of crusher manufacturing in Brazil (operational inQ3/07)

- Expansion of mobile crushing production in Tampere,Finland (operational in Q2/07)

- Start of track mounted crushing equipment manufacturing inthe United States (operational since 2006)

- More than doubling of manufacturing and foundry capacityin India (operational since 2006)

Metso Automation- Expansion of valve production in Shanghai, China (ongoing)

17 © Metso Corporation 2007 October 29, 2007

Performanceprovider

Processagreement

Solutionprovider

Serviceagreement

Machinesupplier

Wears &Spares

Equipment

• The strong basis forservice in Metso is thewear&spare partsbusiness

• The business scope hasbeen expanded further incertain areas to includethe maintenanceagreements

• We are currentlyexpanding the scope tocover also processagreements throughconsulting the customersin the best use of theirequipment

Much potential in service business

Transformation from equipment supplierto lifecycle service provider

18 © Metso Corporation 2007 October 29, 2007

51%

49%

Metso is already a major environmentaltechnology provider

45%

55% ofNet Sales

25%

75%44%

Metso 2006

MetsoPaper

56%

MetsoMinerals

MetsoAutomation

Over 50% of our net sales can be classified as environmentalbusiness (OECD definition)

19 © Metso Corporation 2007 October 29, 2007

RenewableEnergy

TechnologyBioenergy

Our solutions portfolio serves our customers’environmental challenges

CleanTechnology

Energy-efficiency

Wastemanagementand recycling

Watermanagement

Processoptimization

Environmentalconsulting andmeasurements

Materialsefficiency

Metso EnvironmentalTechnology

20 © Metso Corporation 2007 October 29, 2007

Metso’s power opportunity• Environmentally sound, biomass and waste

based power generation solutions provideexciting new growth opportunities for Metso.

Metso Power• A forerunner in fluidized bed combustion of

biomass, coal and other fuels to power plants• A global leader in chemical recovery systems to

pulp and paper mills• Products:

Fluidized bed boilers and recovery boilers, oiland gas boilers, evaporators, environmentalsystems and services

• Annual net sales ~ EUR 500 million- 70% derived from the pulp industry- 30% from independent power producers

21 © Metso Corporation 2007 October 29, 2007

Continuous improvement of operationalexcellence

Productivity

Quality

Supply chainmanagement

Global sourcing andmanufacturing

Operationalexcellence

22 © Metso Corporation 2007 October 29, 2007

2005 2006 2007 20082008

Growth through acquisitionsMetso acquisition process

•Complement product/service offering•Stronger presencein emerging markets•Aftermarket potential•Closing geographicalgaps

Strategic fit

•Target businessto be shortlyearnings-enhancing

Financial fit

• Availability• Anti-trust requirements• Environmental liabilities• Unusual risks

Feasibility

Texas Shredder, Inc. (August 2005)Shanghai-Chenming Paper Machinery Co. Ltd (September 2006)

Aker Kvaerner Pulping & Power (December 2006)Svensk Gruvteknik AB and Svensk Pappersteknik AB (October 2006)

Bulk Equipment Systems and Technologies Inc. (March 2007)Mecanique et Depannage Industries s.a.r.l. (June 2007)

Bender Holdings Limited (July 2007)

23 © Metso Corporation 2007 October 29, 2007

Metso’s profitable growth continuesFast growth, strong profits and more value

- Strengthening globalpresence close to ourcustomers

- Further growth in theaftermarket business

- Making most of the trendsthat drive demand for ourenvironmental solutions

- Continuing efforts to furtherboost our operationalperformance

- Evaluating complementaryacquisitions

25 © Metso Corporation 2007 October 29, 2007

Metso’s financial statements and other financial information areavailable on Metso’s website at: www.metso.com/investors

Metso Corporation - Investor RelationsFabianinkatu 9 A, P.O. Box 1220, FIN-00101 Helsinki, FinlandTel. +358 20484 100 Fax +358 20 484 3236

Johanna Sintonen, Vice President, Investor RelationsTel. +358 20 484 [email protected]

Marja Kortesalo, Financial Communicator, Investor RelationsTel. +358 20 484 [email protected]

Lilli Riikonen, Financial Communicator, Investor RelationsTel. +358 20 484 [email protected]

Anne-Mari Ylikulppi, Assistant, Investor RelationsTel. +358 20 484 [email protected]

North America:Mike Phillips, Senior Vice President, Finance and Administration, Metso USA Inc.Tel. +1 770 246 [email protected]