METROBANK, S.A. AND SUBSIDIARIES...METROBANK, S.A. AND SUBSIDIARIES Panama City, Panama October...

12

Translation Equilibrium Calificadora de Riesgo, S.A. Rating Report Contact: Fernando Arroyo [email protected] Reynaldo Coto [email protected] (507) 214-3790 The designation .pa reflects risks comparable only in Panama METROBANK, S.A. AND SUBSIDIARIES Panama City, Panama October 15th, 2015 Rating Category Definition of Rating Entity A-.pa Reflects high capacity to pay principal and interest in the terms and conditions agreed upon. The ability to pay is more susceptible to possible adverse changes in the economic conditions than the higher categories. Outlook (changed) To Positive from Stable “This rating is not a suggestion or recommendation to invest, nor an endorsement or guarantee of the issuance or the solvency of the rated entity”. --------------------------Millions of US$------------------------- Jun.15 Dec.14 Jun.15 Dec.14 Assets: 1,119.7 1,073.1 Income*: 13.4 11.1 Liabilities: 1,009.3 964.8 ROAA*: 1.3% 1.1% Equity: 110.4 108.2 ROAE*: 12.9% 10.9% *Takes into account performance during the last 12 months. The information used for the present analysis included the audited financial statements as of December 31 st , 2012, 2013 and 2014, and interim financial statements as of June 30, 2014 and 2015, as well as additional information furnished by Metrobank, S.A. and Subsidiaries. The Financial Statements for 2014 were prepared in accordance with the International Financial Reporting Standards (IFRS). The rating is performed pursuant to what is established in Agreements 2-2010 and 6-2010, issued by the Superintendency of Banks of Panama (SBP). Rationale: Equilibrium's Rating Committee affirms the rating A-.pa to Metrobank, S.A. and Subsidiaries, after evaluating interim information as of June 30, 2015. The outlook is changed to Positive from Stable. The rating assigned is supported by Metrobank's increasing base of earning assets, which in turn means reaching a higher positioning of its franchise in the local banking market. In this sense, Equilibrium also values the consistency of its business strategy focused mainly in the Corporate Banking segment, at the same time that the Entity makes efforts to enhance other lines of business to produce recurring income, in addition to the operating income typical from the financial intermediation business, supported by the competitive advantages derived from its technological infrastructure. Likewise, the conservative liquidity ratios in case of possible financial stress situations stand out, as shown by the legal liquidity ratio and the historic coverage of funds available for immediate exigibility of deposits; all these accompanied by an investments portfolio with a reasonable convertibility degree, good renewal ratios of its liability funding sources and a depositors' base with low concentration taking into account its business focus. Equilibrium also considers the good credit quality of the loans granted throughout the years, that together with the moderate backing of tangible collateral, allows it to diminish the requirement to create specific reserves under the current regulatory criteria. Regardless, the Bank's rating is restricted by its spread comparatively lower than the industry average, in turn highly influenced by the strong competition of the local banking environment, mainly in the segments served by the Bank. In this same line, Equilibrium also ponders the sensitivity of results before adverse unforeseen changes in default ratios, especially taking into account the exposure to the cumulative balance corresponding to the Top 20 economic groups debtors. This is combined with its lesser degree of capital adequacy compared to its peers in the market, albeit it should be noted that the capitalization is fully supported by Tier 1 capital elements. The Entity also faces challenges to continue diversifying its loan portfolio by economic sector, as well increasing the use of alternate funding sources, which participation on liabilities is still below its peers. The Positive outlook captures the plan for the future capitalization of the Bank recently approved by the Board of Directors, estimated to be completed at the closing of 2015. This will allow support the growth goals in the medium term, under a context of gradual growth in the generation of income and the expectation that the Bank will show little variation in its performance ratios. The annual growth of Metrobank's consolidated assets has averaged 18.4% during the last 3 and a half years, that, albeit it shows a slight gradual deceleration, it has allowed the Bank to increase its market share in the National Banking System (NBS). The strategy continues to favor gross loans, which represent 69.2% of total balance and which dynamism during the first 6 months of 2015 fully explains the asset growth for said period. The Bank has given special emphasis to the allocation of loans abroad, mainly Central America and the Caribbean, thus the participation of local loans has decreased from 90.1% to 84.9% during the last 12 months. On the other hand, the distribution of loans continues to favor the local commercial sector (participation of 38.0% as of June 2015), albeit it shows a slight contraction in balances granted to this activity since 2014, because of the circumstances of some related segments (for example, Colon Free Zone); this has been compensated by allocations to the services, construction and industrial sectors. Rating History: Entity → BBB.pa (05.30. 08), ↑ BBB+.pa (10.19.09), ↑ A-.pa (10.31.14).

Transcript of METROBANK, S.A. AND SUBSIDIARIES...METROBANK, S.A. AND SUBSIDIARIES Panama City, Panama October...

Translation

Equilibrium Calificadora de Riesgo, S.A.

Rating Report

Contact:

Fernando Arroyo

Reynaldo Coto

(507) 214-3790

The designation .pa reflects risks comparable only in Panama

METROBANK, S.A. AND SUBSIDIARIES Panama City, Panama October 15th, 2015

Rating Category Definition of Rating

Entity A-.pa Reflects high capacity to pay principal and interest in the terms and conditions

agreed upon. The ability to pay is more susceptible to possible adverse

changes in the economic conditions than the higher categories.

Outlook (changed)

To Positive from Stable

“This rating is not a suggestion or recommendation to invest, nor an endorsement or guarantee of the issuance or the solvency of the rated entity”.

--------------------------Millions of US$-------------------------

Jun.15 Dec.14 Jun.15 Dec.14

Assets: 1,119.7 1,073.1 Income*: 13.4 11.1

Liabilities: 1,009.3 964.8 ROAA*: 1.3% 1.1% Equity: 110.4 108.2 ROAE*: 12.9% 10.9%

*Takes into account performance during the last 12 months.

The information used for the present analysis included the audited financial statements as of December 31st, 2012, 2013 and 2014, and interim

financial statements as of June 30, 2014 and 2015, as well as additional information furnished by Metrobank, S.A. and Subsidiaries. The Financial

Statements for 2014 were prepared in accordance with the International Financial Reporting Standards (IFRS). The rating is performed pursuant to what is established in Agreements 2-2010 and 6-2010, issued by the Superintendency of Banks of Panama (SBP).

Rationale: Equilibrium's Rating Committee affirms the

rating A-.pa to Metrobank, S.A. and Subsidiaries, after

evaluating interim information as of June 30, 2015. The

outlook is changed to Positive from Stable.

The rating assigned is supported by Metrobank's increasing

base of earning assets, which in turn means reaching a

higher positioning of its franchise in the local banking

market. In this sense, Equilibrium also values the

consistency of its business strategy focused mainly in the

Corporate Banking segment, at the same time that the

Entity makes efforts to enhance other lines of business to

produce recurring income, in addition to the operating

income typical from the financial intermediation business,

supported by the competitive advantages derived from its

technological infrastructure. Likewise, the conservative

liquidity ratios in case of possible financial stress situations

stand out, as shown by the legal liquidity ratio and the

historic coverage of funds available for immediate

exigibility of deposits; all these accompanied by an

investments portfolio with a reasonable convertibility

degree, good renewal ratios of its liability funding sources

and a depositors' base with low concentration taking into

account its business focus. Equilibrium also considers the

good credit quality of the loans granted throughout the

years, that together with the moderate backing of tangible

collateral, allows it to diminish the requirement to create

specific reserves under the current regulatory criteria.

Regardless, the Bank's rating is restricted by its spread

comparatively lower than the industry average, in turn

highly influenced by the strong competition of the local

banking environment, mainly in the segments served by

the Bank. In this same line, Equilibrium also ponders the

sensitivity of results before adverse unforeseen changes in

default ratios, especially taking into account the exposure

to the cumulative balance corresponding to the Top 20

economic groups debtors. This is combined with its lesser

degree of capital adequacy compared to its peers in the

market, albeit it should be noted that the capitalization is

fully supported by Tier 1 capital elements. The Entity also

faces challenges to continue diversifying its loan portfolio

by economic sector, as well increasing the use of alternate

funding sources, which participation on liabilities is still

below its peers.

The Positive outlook captures the plan for the future

capitalization of the Bank recently approved by the Board

of Directors, estimated to be completed at the closing of

2015. This will allow support the growth goals in the

medium term, under a context of gradual growth in the

generation of income and the expectation that the Bank

will show little variation in its performance ratios.

The annual growth of Metrobank's consolidated assets has

averaged 18.4% during the last 3 and a half years, that,

albeit it shows a slight gradual deceleration, it has allowed

the Bank to increase its market share in the National

Banking System (NBS).

The strategy continues to favor gross loans, which

represent 69.2% of total balance and which dynamism

during the first 6 months of 2015 fully explains the asset

growth for said period. The Bank has given special

emphasis to the allocation of loans abroad, mainly Central

America and the Caribbean, thus the participation of local

loans has decreased from 90.1% to 84.9% during the last

12 months. On the other hand, the distribution of loans

continues to favor the local commercial sector

(participation of 38.0% as of June 2015), albeit it shows a

slight contraction in balances granted to this activity since

2014, because of the circumstances of some related

segments (for example, Colon Free Zone); this has been

compensated by allocations to the services, construction

and industrial sectors.

Rating History: Entity → BBB.pa (05.30. 08), ↑ BBB+.pa

(10.19.09), ↑ A-.pa (10.31.14).

2

As of June 30, 2015, the balances granted to the Top 20

economic groups debtors (net of pledged deposits)

represent 24.2% of gross loans, an amount close to the

average shown by banks in its risk category. The exposure

level on this debtors group has remained at 1.9 times the

Tier 1 capital for the last 4 semesters, which level is

considered moderate taking into account the profile of

customers serviced by the Entity.

Regarding the credit quality of loans, non-performing

balances represent 0.6% of the portfolio as of the closing

of June 2015, a level that is below the NBS average

(0.9%). At the same time, the addition of loans classified in

B, C, D and E categories represent 0.9% of total loans, also

better than the system's average (3.4%). The above,

together with the value of tangible collateral that represents

approximately 101% of the total consolidated loan

portfolio, allows reducing possible expenses for specific

reserves. Indeed, the specific reserve for US$5.7 million

registered in the asset side is the result of the calculations

based in the IFRS methodology that takes into account the

concept of loss incurred on the portfolio.

As of June 30, 2015, total deposits received amount to

US$944.9 million after showing a 15.1% annual growth.

The composition of deposits by modality show a slight

increase in the participation of time deposits, as this

liability source has explained the greater part of the asset

growth throughout the last five-year period. The depositors'

base has been historically expanding and stable, also

showing an average annual renewal rate of time deposits

around 85% for the last 6 months, while the volatility rate

of demand and savings deposits is about 3.5%. Added to

this, the concentration of the Top 20 depositors over total

deposits is equivalent to 20.1% as of the closing of June

2015, a level that indicates a low exposure on the main

customers, taking into account their business focus.

Regarding other liability funding sources, the joint balance

of received financings and repos is equivalent to US$39.7

million, which means 4.0% of financial liabilities. This

level is lower when compared to the average of other

financial institutions rated in similar risk category, albeit it

should also be noted that Metrobank maintains available

lines for US$32.6 million.

The aggregate of cash, due from banks and financial

investments represent 139.9% of demand and savings

deposits as of the closing of June 2015, a percentage above

the NBS average (95.7%), an outstanding fact since this

coverage level has maintained relative consistency

throughout the years. Should the investments that guarantee

the repos in the liability side for an amount of US$39.7

million were excluded from the ratio, then the ratio would

change to 122.1%. On the other hand, the legal liquidity

ratio has averaged 64.5% during the first semester of 2015,

comparing favorably to the average of the local banking

industry.

Regarding liquidity matching under contractual scenarios,

the analysis takes into account demand and savings

deposits in the shortest term (0-30 days) bucket, while

investments are registered according to their maturity date

in the terms originally agreed upon, as well as the rest of

the items. In this way, 41.6% of the Bank's total assets have

maturity dates under 12 months, while 73.2% of liabilities

mature in the same interval, creating liquidity gaps. In the

very low probability of occurrence of financial stress

scenarios, the Bank would have the option to liquidate a

significant portion of its investments portfolio or use

available borrowing lines.

The book value of investments amounts to US$231.3

million as of the closing of June 2015 and is totally

comprised of securities available for sale of which 68.4%

are securities with local and international investment grade.

Historically, Management has favored the acquisition of

fixed rent securities issued in Panama and, to a lesser

degree, the United States. On the other hand, Sovereign

Debt of the Republic of Panama amount to 30.0% of

securities, thus it is the main issuer of the portfolio.

Regarding the market risk of the portfolio, unrealized gains

amount to US$278.4 thousand, that is distributed in a few

issuers which individual unrealized losses are not greater

than 1.6%, while securities issued in Brazil or other

economies from South America are not recorded.

As for the figures from the Statement of Income for the six

months ended as of June 30, 2015, the Bank accumulated a

net income of US$7.1 million, a 48.2% interannual

variation, thus the profitability ratios showed slight

increases, consistent with its business model.

Among the main aspects to highlight from the semester

performance and its interannual comparison, the financial

spread remained almost similar, given that the slight

increase in the funding cost was offset through a slight

adjustment to increase the average yield on gross loans.

This allowed the spread to remain at 2.1%, albeit it is below

the system average, given the nature of the corporate

customers serviced by the Bank.

It should be noted that the Bank is experiencing gradual

increases in net fees, where it has accumulated US$3.0

million during the first semester of 2015, acknowledging a

26.8% interannual increase, driven, in turn, -to a great

extent- by income from merchant acquisition and points of

sale services. The Entity also earns other income from the

Financiera Govimar operation and for advisory services and

referred customers, for a total amount of US$1.6 million.

General and administrative expenses represent 38.1% of

total interest on earning assets, a proportion that has

showed little variation during the last years. Said operating

expenses also showed a 16.2% annual increase in the

comparison between fiscal periods, slightly less than the

17.7% reflected by the gross financial income.

On the other hand, the Bank recognized gains on sale of

securities equivalent to US$1.4 million during the semester,

since it took advantage of opportunities in the securities

market, increasing, in turn, the extraordinary component in

net profit from 3.9% to 20.5% in the interannual

comparison.

Retained earnings have supported the net equity increase

during the last 18 months. Even if this contribution is

marginal regarding asset growth, it has provided for the

slow increase of the dynamic reserve, for up to US$11.9

million. On the other hand, the Capital Adequacy Ratio

(CAR) is equivalent to 12.8% as of June 30, 2015, a figure

below the NBS (14.9%) average and other banks in its risk

category, albeit it also stands out that the Bank's capital

funds fully compute as Tier 1 capital.

3

Strengths

1. Good quality of loans during the last years, reflected in the low balance of past-due and non-performing loans, prudential

coverages on expected loan losses, good tangible collateral backing, as well as low proportion of write-offs.

2. Prudential position regarding liquidity and moderate concentrations of depositors.

3. Growth of productive assets generates greater scale and allows the increasing generation of recurring income.

Weaknesses

1. Tight spread which limits the ability to absorb possible unexpected losses, as well as internal contribution to equity

growth.

2. The capital adequacy level tends to decrease as a result of strong growth.

3. Relative concentration in deposits as liability funding source.

Opportunities

1. Technological and service infrastructure that would allow cross-selling.

2. Synergies between the Bank and its subsidiaries’ operations.

3. Gradual increase of geographic loan portfolio diversification.

Threats

1. Strong competition in local market exerts pressure on spreads and demands permanent renewal of comparative advantages

that will allow the reduction of interest rate risks.

2. Local and international credit and price variation risks.

3. At the Panamanian banking sector level, possible impacts due to the inclusion of Panama in the Financial Action Task

Force on Money Laundering (FATF) Gray List.

4

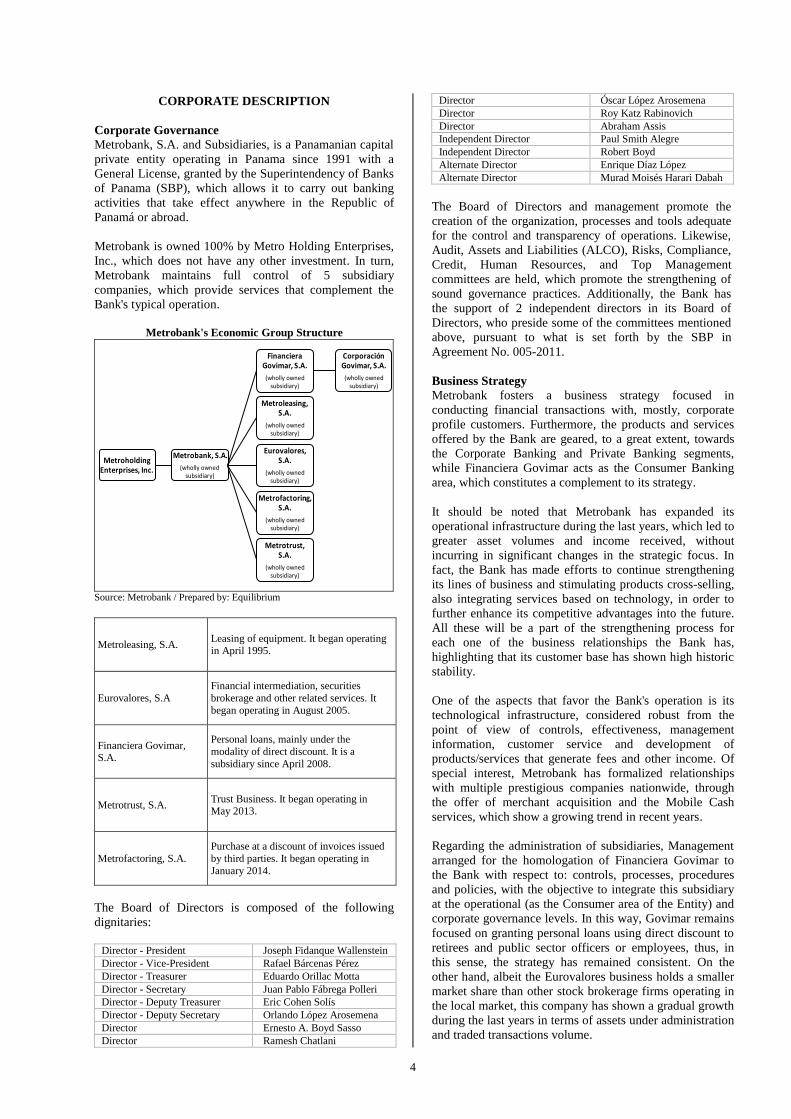

CORPORATE DESCRIPTION

Corporate Governance

Metrobank, S.A. and Subsidiaries, is a Panamanian capital

private entity operating in Panama since 1991 with a

General License, granted by the Superintendency of Banks

of Panama (SBP), which allows it to carry out banking

activities that take effect anywhere in the Republic of

Panamá or abroad.

Metrobank is owned 100% by Metro Holding Enterprises,

Inc., which does not have any other investment. In turn,

Metrobank maintains full control of 5 subsidiary

companies, which provide services that complement the

Bank's typical operation.

Metrobank's Economic Group Structure

Metroholding Enterprises, Inc.

Metrobank, S.A.

(wholly owned subsidiary)

Financiera Govimar, S.A.

(wholly owned subsidiary)

Corporación Govimar, S.A.

(wholly owned subsidiary)

Metroleasing, S.A.

(wholly owned subsidiary)

Eurovalores, S.A.

(wholly owned subsidiary)

Metrofactoring, S.A.

(wholly owned subsidiary)

Metrotrust, S.A.

(wholly owned subsidiary)

Source: Metrobank / Prepared by: Equilibrium

Metroleasing, S.A. Leasing of equipment. It began operating in April 1995.

Eurovalores, S.A

Financial intermediation, securities

brokerage and other related services. It

began operating in August 2005.

Financiera Govimar, S.A.

Personal loans, mainly under the

modality of direct discount. It is a

subsidiary since April 2008.

Metrotrust, S.A. Trust Business. It began operating in May 2013.

Metrofactoring, S.A.

Purchase at a discount of invoices issued

by third parties. It began operating in

January 2014.

The Board of Directors is composed of the following

dignitaries:

Director - President Joseph Fidanque Wallenstein

Director - Vice-President Rafael Bárcenas Pérez

Director - Treasurer Eduardo Orillac Motta

Director - Secretary Juan Pablo Fábrega Polleri

Director - Deputy Treasurer Eric Cohen Solís

Director - Deputy Secretary Orlando López Arosemena

Director Ernesto A. Boyd Sasso

Director Ramesh Chatlani

Director Óscar López Arosemena

Director Roy Katz Rabinovich

Director Abraham Assis

Independent Director Paul Smith Alegre

Independent Director Robert Boyd

Alternate Director Enrique Díaz López

Alternate Director Murad Moisés Harari Dabah

The Board of Directors and management promote the

creation of the organization, processes and tools adequate

for the control and transparency of operations. Likewise,

Audit, Assets and Liabilities (ALCO), Risks, Compliance,

Credit, Human Resources, and Top Management

committees are held, which promote the strengthening of

sound governance practices. Additionally, the Bank has

the support of 2 independent directors in its Board of

Directors, who preside some of the committees mentioned

above, pursuant to what is set forth by the SBP in

Agreement No. 005-2011.

Business Strategy

Metrobank fosters a business strategy focused in

conducting financial transactions with, mostly, corporate

profile customers. Furthermore, the products and services

offered by the Bank are geared, to a great extent, towards

the Corporate Banking and Private Banking segments,

while Financiera Govimar acts as the Consumer Banking

area, which constitutes a complement to its strategy.

It should be noted that Metrobank has expanded its

operational infrastructure during the last years, which led to

greater asset volumes and income received, without

incurring in significant changes in the strategic focus. In

fact, the Bank has made efforts to continue strengthening

its lines of business and stimulating products cross-selling,

also integrating services based on technology, in order to

further enhance its competitive advantages into the future.

All these will be a part of the strengthening process for

each one of the business relationships the Bank has,

highlighting that its customer base has shown high historic

stability.

One of the aspects that favor the Bank's operation is its

technological infrastructure, considered robust from the

point of view of controls, effectiveness, management

information, customer service and development of

products/services that generate fees and other income. Of

special interest, Metrobank has formalized relationships

with multiple prestigious companies nationwide, through

the offer of merchant acquisition and the Mobile Cash

services, which show a growing trend in recent years.

Regarding the administration of subsidiaries, Management

arranged for the homologation of Financiera Govimar to

the Bank with respect to: controls, processes, procedures

and policies, with the objective to integrate this subsidiary

at the operational (as the Consumer area of the Entity) and

corporate governance levels. In this way, Govimar remains

focused on granting personal loans using direct discount to

retirees and public sector officers or employees, thus, in

this sense, the strategy has remained consistent. On the

other hand, albeit the Eurovalores business holds a smaller

market share than other stock brokerage firms operating in

the local market, this company has shown a gradual growth

during the last years in terms of assets under administration

and traded transactions volume.

5

FINANCIAL PERFORMANCE

Assets and Credit Quality

Metrobank's consolidated assets growth rhythm registered

a slight deceleration for the last 12 months ended as of June

30, 2015, almost matching the average shown by the

individual base of the National Banking System (NBS).

This is linked to the budget contemplated by the Entity for

2015, which considered factors such as the economic

deceleration of Panama and other international factors

prompting a more conservative growth rhythm.

0%

5%

10%

15%

20%

25%

30%

35%

0

200

400

600

800

1,000

1,200

Dec. 12

Dec. 13

Jun. 14

Dec. 14

Jun. 15

Gro

wth

rate

In U

S$ m

illi

on

s

Assets evolution and composition

Other assets

Loans

Investments

Cash and due from banks

Assets interannual growth % -MetrobankAssets growth % -NBS

Sources: Metrobank and SBP / Prepared by: Equilibrium

Regarding the balance structure, even if no significant

changes have been observed in the participation of earning

assets, there is a decrease in the participation of liquid

assets (cash + due from banks) from 11.4% to 10.0%

during the 6 first months of 2015, which was compensated

through an increase in the proportion of gross loans in the

same period. Therefore, the Bank has placed a greater

emphasis in the growth of its loan portfolio, since the

variation for this period is equivalent to US$46.6 million,

an amount that explains 100% of the growth of total assets

in absolute terms.

The loan portfolio totals US$774.6 million as of the closing

of June 2015, after showing a 15.7% annual increase, in

turn equivalent to US$104.9 million in terms of balances.

Interestingly, loans to the foreign sector contributed 48.4%

of said interannual growth, which meant a decrease of the

portfolio exposure degree to the local market during this

time lapse (from 90.1% down to 84.9%). The Bank's

Management contemplates maintaining the foreign loans

growth rhythm, mostly destined to highly prestigious

corporate groups in Central America, under the syndicated

loans modality and structured by top-rated prestigious

international financial entities as a counterbalance measure

against the deceleration of some sectors of the local

market.

Concerning the distribution by economic sector, the

balance granted to the commercial sector groups 38.1% of

the portfolio, thus it still predominates in the loan mix.

However, the balance allocated to said sector shrank during

the last 12 months, causing a drop in its relative

participation from 45.6% as of the closing of June 2014.

0%

5%

10%

15%

20%

25%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec. 12

Dec. 13

Jun. 14

Dec. 14

Jun. 15

ann

ual

var

iati

on

%

bal

ance

par

tici

pat

ion

%

Distribution of Loan Portfolio by Economic Sector

Other

Construction

Industrial

Consumer

Services

Commercial CFZ

Commercial non -CFZ

Source: Metrobank / Prepared by: Equilibrium

As shown in the previous graph, Metrobank focused in

granting facilities to the sectors: services, construction and

industrial (mainly to Central America and the Caribbean),

which has allowed to reflect a rise in the annual growth

rhythm as of the June 2015 closing.

Due to its focus in the Corporate Banking sectors,

Metrobank shows a relative concentration of loan balances

(net of pledged deposits) corresponding to its Top 20

debtors, equivalent to 24.2% of total loans and 1.7 times

the Tier 1 capital, both as of June 30, 2015, where said

levels have reflected a slight upward trend.

0.0

0.5

1.0

1.5

2.0

2.5

0%

5%

10%

15%

20%

25%

30%

Dec. 12

Dec. 13

Jun. 14

Dec. 14

Jun. 15

Pro

po

rtio

n o

f Tie

r 1

cap

ital

Par

tici

pat

ion

% o

n lo

ans

Concentration of Top 20 debtors*

Top 20 debtors /

Loans

Top 20 debtors /

Equity

* Net of pledged deposits

Source: Metrobank / Prepared by: Equilibrium

Regarding the credit quality, the non-performing balances

ratio is equivalent to 0.6% as of June 30, 2015, a

percentage that continues comparing favorably in relation

to the NBS average (0.9%), while the addition of non-

performing and past-due loans represents 0.8% of total

loans, also below the NBS average (2.0%). Also, the total

of loans classified in the “Special Mention” “Substandard”,

“Doubtful” and “Loss” (B, C, D and E) categories

according to Agreement 04-2013 represent 0.9% of the

loan portfolio; it stands out that said percentage has shown

consistency during the last years. This is particularly

advantageous to lighten possible additional specific

reserves requirements that could arise upon unexpected

events.

6

On the other hand, the market value of the tangible

collateral (pledged deposits; mortgages over personal

property and real estate and pledged securities) is

equivalent to approximately 101% of the total balance of

loans as of June 20, 2015. If we take into account the value

of collateral up to the loan balance they guarantee, the

coverage percentage is equivalent to 58.6% of the

consolidated portfolio (including Financiera Govimar),

indicating a favorable guarantee position, taking into

account the regulatory requirements in effect included in

Agreement 04-2013. It is precisely this condition, together

with the low default, that allows the recognition of specific

reserves, which total US$5.7 million as of the June 2015

closing, in turn obtained from the calculation under the

incurred loss principles, established by the International

Financial Reporting Standards (IFRS).

Liability Funding Structure

As of June 30, 2015, deposits taken from customers add up

to US$944.9 million, after reflecting a 5.1% increase

compared to December 2014 and 15.1% compared to June

2014. Particularly, time deposits have shown a greater

dynamism during the last year than the rest of modalities

(demand and savings deposits), which has allowed its

relative participation increase over the total takings. Time

deposits have contributed more than 100% of the asset

annual growth for the July 2014 - June 2015 period, which

also indicates a lower degree of funding diversification for

the last period. Favorably, the current funding strategy

allows extending the maturity terms of liabilities.

0%

5%

10%

15%

20%

25%

30%

0

200

400

600

800

1,000

1,200

Dec. 12

Dec. 13

Jun. 14

Dec. 14

Jun. 15

Gro

wth

rate

In U

S$ m

illio

ns

Liabilities evolution and composition

Other liabilities

Received financings + repos

Time deposits

Savings deposits

Demand deposits

Deposits interannual growth % - Metrobank

Deposits growth % - NBS

Sources: Metrobank and SBP / Prepared by: Equilibrium

On the other hand, the use of borrowing lines granted by

other financial entities, including securities sold under

repurchase agreement (repos), have maintained a low

representation on financial liabilities, as the management

strategy favors takings of resources through deposits from

the general public. Albeit the use of these financial

liabilities add up to US$39.7 million as of June 30, 2015,

the Bank holds available lines for another US$32.6 million.

It should be noted that the repo lines for US$27.5 million

are secured by Sovereign Debt from the Republic of

Panama registered in the Bank's investment portfolio,

which market value represent 144.2% of these facilities.

The Bank shows a low concentration degree in its top

depositors, which is consistent with its focus on the

Corporate Banking business. As of June 30, 2015, 20.1%

of total deposits correspond to the amounts taken through

the Top 20 depositors, a level close to the average reflected

by the banks in its risk category that have similar business

focus.

0%

5%

10%

15%

20%

25%

Dec.12 Dec.13 Jun.14 Dec.14 Jun.15

Exp

osu

re %

Top depositors / Total deposits

Top 10 depositors

Top 20 depositors

Source: Metrobank / Prepared by: Equilibrium

In a favorable light, the Bank has maintained a good

renewal percentage on its time deposits (around 85%

during the 6 months elapsed of 2015); additionally, the

average volatility ratios on demand and savings deposits

have remained below 3.5% during the last 2 years.

Liquidity and Maturity Matching

As of June 30, 2015, the amount of cash, due from banks

and financial investments (liquid funds available) represent

34.1% of total liabilities; even though said percentage is

slightly below the NBS average (35.2%), the high degree

of consistency during the last years stands out.

It should be noted that the legal liquidity ratio for

Metrobank averaged 64.5% during the first semester of

2015, a figure above the average of the Panamanian

banking industry; furthermore, the Bank has shown an

upward trend in this ratio. The above is consistent with the

type of funding used by the Bank, together with the

conservative quality of its investments portfolio.

30%

35%

40%

45%

50%

55%

60%

65%

70%

Dec. 12 Dec. 13 Jun. 14 Dec. 14 Jun. 15

Leg

al L

iqu

idit

y %

Average legal liquidity ratio evolution

Metrobank

Panamanian Private Banking

National Banking System

Sources: Metrobank and SBP / Prepared by: Equilibrium

On the other hand, the liquid funds available over demand

and savings deposits ratio is equivalent to 139.9% as of the

June 2015 closing, a percentage that is above the NBS

average (95.7%) on the same date. If the investments

securing repos were excluded from the numerator, the ratio

would be 122.1%, a level that continues being favorable

from the point of view of coverage of liquidity risk before

financial stress scenarios.

7

Regarding the liquidity matching as of June 30, 2015,

Metrobank reflects -under the contractual measurement-

gaps between assets and liabilities that exceed the equity

amount in the 0-30 days time interval. It should be taken

into account that the contractual analysis places the

demand and savings deposits in the shortest term bucket,

due to their free exigibility quality; additionally, the

financial investments are placed in the maturities originally

agreed upon (typically greater than 1 year), assuming that

the Bank will maintain its positions in the long term.

Nevertheless, the gaps can be remedied once the option to

liquidate securities with good market depth for up to

approximately US$141.2 million is considered. The above

is considered feasible, given the conservative profile of the

portfolio regarding both credit and market risk.

Investments Portfolio Profile

The aggregate of the market value corresponding to the

Bank's financial investments is equivalent to US$231.3

million as of June 30, 2015, in turn it is totally comprised

of securities available for sale. The variation rate of

investments was 4.7% compared to December 2014,

influenced to a great extent by a greater degree of sale of

securities, in order to recognize capital gains.

From the point of view of credit quality, we observe that

local and international investment grade securities

represent 68.4% of the total portfolio. It also stands out that

the securities corresponding to Sovereign Bonds and

Treasury Notes represent 36.6% of the portfolio, a majority

of which correspond to Sovereign Debt issue directly by

the Government of the Republic of Panama. This issuer is

the greatest individual protagonist in the portfolio, since it

represents 62.8% of the net shareholders' equity. Taking

this into account, the aggregate of the Top 10 issuers of the

portfolio groups 69.8% of the investments and represents

1.5 times the net shareholders' equity.

Corporate bonds

62.9%

Sovereign Debt

20.1%

Treasury Notes

16.6%

Other0.5%

Distribution of securities by type of instrument(as of June 30, 2015)

Source: Metrobank / Prepared by: Equilibrium

The above falls within the acquisition of securities strategy

established by the Board of Directors of Metrobank, since

that in addition of emphasizing fixed rate securities with

good convertibility degree (high component of Sovereign

Debt), it also favors securities issued from Panama, and, to

a lesser extent, the United States, resulting in a

geographical distribution very focused in these two

countries, consistent with the last years. Also, it should be

noted that the securities without investment grade group

24.5% of the portfolio, which in turn consist of securities

issued by prestigious Panamanian corporations and that

generally have good tangible collateral backing.

Regarding its market risk, the Bank registers an unrealized

gain of US$278.4 thousand in its securities available for

sale as of June, 2015 closing. Albeit this figure represents

an 89.5% decrease compared to December 2014, the above

is closely related to the sale of investments that took place

during the first semester of 2015 for the sum of US$57.1

million, taking into advantage the recognition of increases

in the value of some Panamanian and international

securities generated during prior periods. Currently, the

highest unrealized loss registered by an individual issuer is

equivalent to US$252.1 thousand, and the greatest loss

percentage is only 2.1%, with ample slack regarding the

stop-loss limits established by the Bank.

Solvency

As of the closing of June 2015, the Bank's net stockholders'

equity shows a 2.0% variation compared to December

2014, supported by retained earnings during the semester,

that later on contributed to increase the dynamic reserve, as

established in current the banking regulation. However, we

also observed some decreases in specific items, for instance

the decrease mentioned in unrealized gains on securities

available for sale; also, the Bank distributed dividends to

its common stock shareholders for the sum of US$2.5

million during the last semester, that is, 22.5% of the 2014

net profit, which is consistent with the management

practice for the past 5-year period (between 20% and 30%).

Therefore, the leverage ratio (liabilities / equity) remained

almost similar between the analyzed periods, as well as the

Capital Adequacy Ratio (CAR), while assets presented a

slightly slower growth rhythm than in 2014. Of particular

interest, Metrobank's CAR is below the NBS average and

the average shown by banks in its risk category. In spite of

this condition, we value that the computable capital funds

for the capital adequacy calculation consist totally of

ordinary Tier 1 capital elements in the case of Metrobank,

which is more favorable compared to some financial

institutions rated by Equilibrium, that could even have

CAR levels above the current regulation in effect

(Agreement 05-2008). Additionally, the Bank contemplates

receiving capital contributions from its shareholders as of

the closing of 2015, which could support at least 2 years of

growth.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

20

40

60

80

100

120

Dec.12Dec.13 Jun.14Dec.14 Jun.15

CAR

In U

S$ m

illio

ns

CAR evolution

Tier 1 Capital Funds

CAR -Metrobank

CAR - NBS

Sources: Metrobank y SBP / Prepared by: Equilibrium

It should be noted that the Goodwill generated by the

acquisition of Financiera Govimar and other financial

companies for an amount of US$10.1 million in 2008, has

8

been deducted from the computable capital funds,

according to the SBP's current regulations. If this

regulatory adjustment did not exist, the CAR as of June

2015 would have been 14.1%.

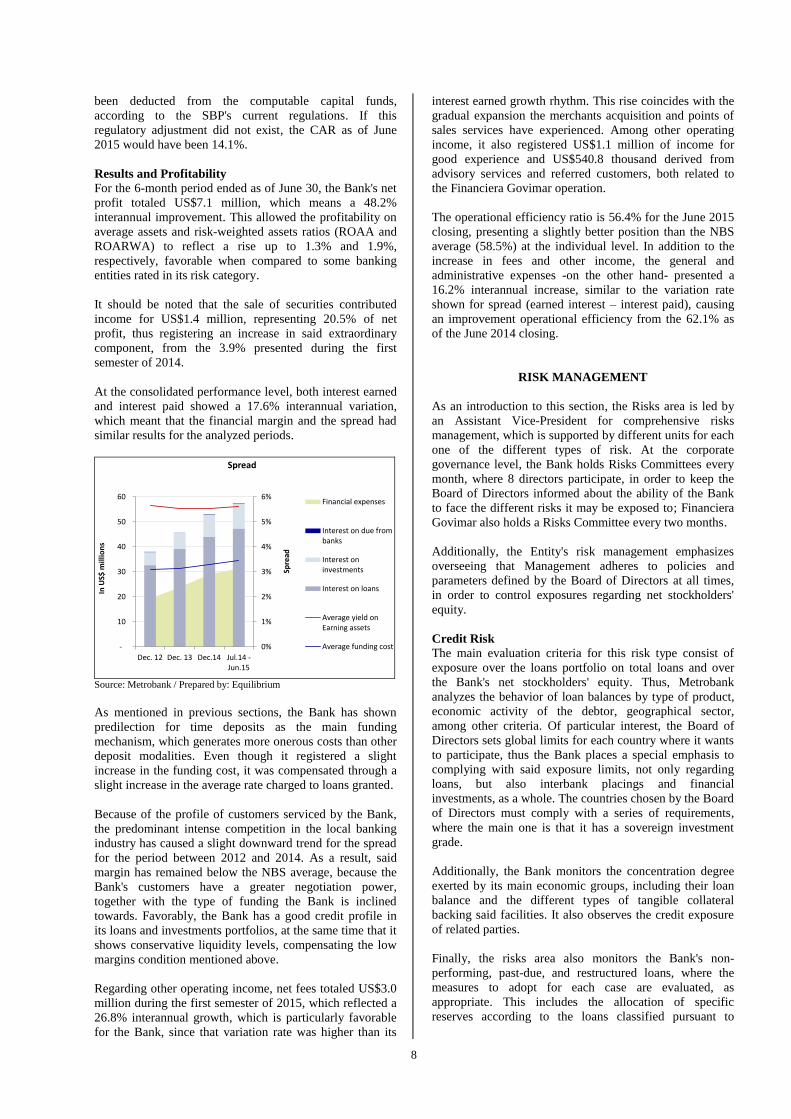

Results and Profitability

For the 6-month period ended as of June 30, the Bank's net

profit totaled US$7.1 million, which means a 48.2%

interannual improvement. This allowed the profitability on

average assets and risk-weighted assets ratios (ROAA and

ROARWA) to reflect a rise up to 1.3% and 1.9%,

respectively, favorable when compared to some banking

entities rated in its risk category.

It should be noted that the sale of securities contributed

income for US$1.4 million, representing 20.5% of net

profit, thus registering an increase in said extraordinary

component, from the 3.9% presented during the first

semester of 2014.

At the consolidated performance level, both interest earned

and interest paid showed a 17.6% interannual variation,

which meant that the financial margin and the spread had

similar results for the analyzed periods.

0%

1%

2%

3%

4%

5%

6%

-

10

20

30

40

50

60

Dec. 12 Dec. 13 Dec.14 Jul.14 -Jun.15

Spre

ad

In U

S$ m

illio

ns

Spread

Financial expenses

Interest on due frombanks

Interest oninvestments

Interest on loans

Average yield onEarning assets

Average funding cost

Source: Metrobank / Prepared by: Equilibrium

As mentioned in previous sections, the Bank has shown

predilection for time deposits as the main funding

mechanism, which generates more onerous costs than other

deposit modalities. Even though it registered a slight

increase in the funding cost, it was compensated through a

slight increase in the average rate charged to loans granted.

Because of the profile of customers serviced by the Bank,

the predominant intense competition in the local banking

industry has caused a slight downward trend for the spread

for the period between 2012 and 2014. As a result, said

margin has remained below the NBS average, because the

Bank's customers have a greater negotiation power,

together with the type of funding the Bank is inclined

towards. Favorably, the Bank has a good credit profile in

its loans and investments portfolios, at the same time that it

shows conservative liquidity levels, compensating the low

margins condition mentioned above.

Regarding other operating income, net fees totaled US$3.0

million during the first semester of 2015, which reflected a

26.8% interannual growth, which is particularly favorable

for the Bank, since that variation rate was higher than its

interest earned growth rhythm. This rise coincides with the

gradual expansion the merchants acquisition and points of

sales services have experienced. Among other operating

income, it also registered US$1.1 million of income for

good experience and US$540.8 thousand derived from

advisory services and referred customers, both related to

the Financiera Govimar operation.

The operational efficiency ratio is 56.4% for the June 2015

closing, presenting a slightly better position than the NBS

average (58.5%) at the individual level. In addition to the

increase in fees and other income, the general and

administrative expenses -on the other hand- presented a

16.2% interannual increase, similar to the variation rate

shown for spread (earned interest – interest paid), causing

an improvement operational efficiency from the 62.1% as

of the June 2014 closing.

RISK MANAGEMENT

As an introduction to this section, the Risks area is led by

an Assistant Vice-President for comprehensive risks

management, which is supported by different units for each

one of the different types of risk. At the corporate

governance level, the Bank holds Risks Committees every

month, where 8 directors participate, in order to keep the

Board of Directors informed about the ability of the Bank

to face the different risks it may be exposed to; Financiera

Govimar also holds a Risks Committee every two months.

Additionally, the Entity's risk management emphasizes

overseeing that Management adheres to policies and

parameters defined by the Board of Directors at all times,

in order to control exposures regarding net stockholders'

equity.

Credit Risk

The main evaluation criteria for this risk type consist of

exposure over the loans portfolio on total loans and over

the Bank's net stockholders' equity. Thus, Metrobank

analyzes the behavior of loan balances by type of product,

economic activity of the debtor, geographical sector,

among other criteria. Of particular interest, the Board of

Directors sets global limits for each country where it wants

to participate, thus the Bank places a special emphasis to

complying with said exposure limits, not only regarding

loans, but also interbank placings and financial

investments, as a whole. The countries chosen by the Board

of Directors must comply with a series of requirements,

where the main one is that it has a sovereign investment

grade.

Additionally, the Bank monitors the concentration degree

exerted by its main economic groups, including their loan

balance and the different types of tangible collateral

backing said facilities. It also observes the credit exposure

of related parties.

Finally, the risks area also monitors the Bank's non-

performing, past-due, and restructured loans, where the

measures to adopt for each case are evaluated, as

appropriate. This includes the allocation of specific

reserves according to the loans classified pursuant to

9

Agreement 04-2013, review of guarantees, and legal

procedures to initiate, if necessary.

The Bank has implemented an internal scoring system for

the Corporate Banking loan portfolio, with the objective of

assigning an internal rating based on determined qualitative

and quantitative criteria, according to its risk profile. This

would be particularly useful when submitting loan

proposals to the different committees, as well as when

following-up the credit behavior of each debtor.

It is worth mentioning that the Bank exercises a periodic

monitoring of customers' files, both at Head Office and

branch offices levels, as a quality control measure.

Market Risk

Metrobank's market risk is focused on its investment

portfolio. Therefore, the Assistant Vice-President monitors

specific portfolio variables, such as: average yield, type of

instrument, type of industry of the Issuer, risk rating,

average duration, participation of investments on total

loans, proportion of securities issued abroad, unrealized

gain/loss amount, among others. Albeit the foreign

securities (other than Latin America) are managed by an

external custodian, the Bank monitors its positions in these

securities the same way it does its local investments.

In addition, the Bank oversees the evolution of the VaR

and CVaR (Conditional Value at Risk), so that the

maximum loss limits allowed regarding the net

stockholders' equity are complied with.

Liquidity Risk

The risks area has prepared procedures for the activation of

the Contingency Plan, which has several levels depending

on the need for liquidity at a given time. The use of repos,

lines of credit, and the renewal of bank borrowings would

be contemplated in case the legal liquidity rate approaches

the regulatory limit.

At the same time, the Board of Directors is kept informed

about the evolution of the concentration degree of Top

depositors, including the different types of deposits they

have in the Bank and those that are pledged as collateral of

the loan portfolio.

Additionally, the Bank conducts a periodic review of

liquidity levels it maintains in the balance sheet, including

the average legal liquidity ratios (regulatory) and the

immediate liquidity ratio, which is an internal measure of

the institution that takes into consideration a more stringent

deposits base. This analysis is complemented through the

monthly monitoring of the liquidity matching position

under contractual and under renewal statistics scenarios, in

turn supported by overseeing the renewal percentages of

time deposits and the volatility ratios of the different types

of financial liabilities.

Operational Risk

The Assistant Vice-President has homologated the

incidents reporting system for both Metrobank and

Financiera Govimar, in order to monitor the operational

risk of both entities simultaneously.

The Entity has a software through which each area reports

materialized operational risks events, in order to duly

follow-up afterwards with the help of a preventive actions

matrix. Management indicated that the Bank is in the

process of updating the tool that measures potential losses.

As part of its main objectives, the operational risks area has

been able to evaluate all the risks inherent to the identified

processes. The Bank presents its Board of Directors a

summary of these processes by credit product or

management area, as they are updated in the risk matrix.

This way, a constant update of the corresponding risk

matrixes is maintained, so that the areas that own the

processes, implement measures to control the possible risks

observed, supervised by the Comprehensive Risks area.

After considering the controls applied to the inherent

losses, the Bank obtains a residual loss figure, which is

compared to the limit assigned by the Board of Directors.

This allows showing a refined analysis of the main areas or

processes that should be reinforced, in order to reduce

future residual losses.

Metrobank continues developing the Business Impact

Analyses (BIA) for each one of the Bank's processes with

the objective to continue reinforcing its current Business

Continuity Plan to ensure operability in case of

technological failures or external events.

REGULATORY ASPECTS

Regulatory Framework for Capital Adequacy

On February 3, 2015, the SBP issued Agreement 01-2015,

which sets forth new requirements for the categorization of

the computable capital funds for the calculation of the

Capital Adequacy Ratio (CAR). This Agreement will be

applicable to all official banks, all General License Banks,

all International License Banks where the SBP is a home

country supervisor and to all the owners of bank stock

from banking groups that consolidate in Panama and that

the SBP is the home country supervisor.

This Agreement will require compliance with minimum

percentages of adequacy, according to the classification of

capital funds parameters. The components of each one of

the types of capital accepted by the regulation: ordinary

Tier 1 capital, additional Tier 1 capital, and Tier 2 capital,

will be determined.

The minimum percentage of Capital Adequacy will

continue being 8%, as it is required under Agreement 05-

2008, currently in effect. However, the new Agreement

sets forth limits for the Tier 1 capital, which will increase

gradually, until the adequation periods have elapsed.

The ordinary Tier 1 capital will consist of common shares,

retained and current period earnings, regulatory reserves,

and other elements included in the Agreement. The

calculation of Tier 1 capital according to the new

Agreement deducts Goodwill, in addition to other items or

regulatory adjustments that are not taken into account in

the current regulation. For example, the following are

mentioned:

10

Accumulated and current period

losses Other intangible assets

Shareholdings greater than 10% in the stockholders' equity of financial

entities that do not consolidate to in

the Bank

Shareholdings in non-

financial entities included

in the financial consolidation (greater than

10%)

Unrealized losses on securities

available for sale

Other adjustments

contemplated in the Agreement

It is worth mentioning that retained and current period

earnings must be validated by the external auditors, in

order to ensure the deduction of every possible,

foreseeable expense, interest, or dividend from said profits.

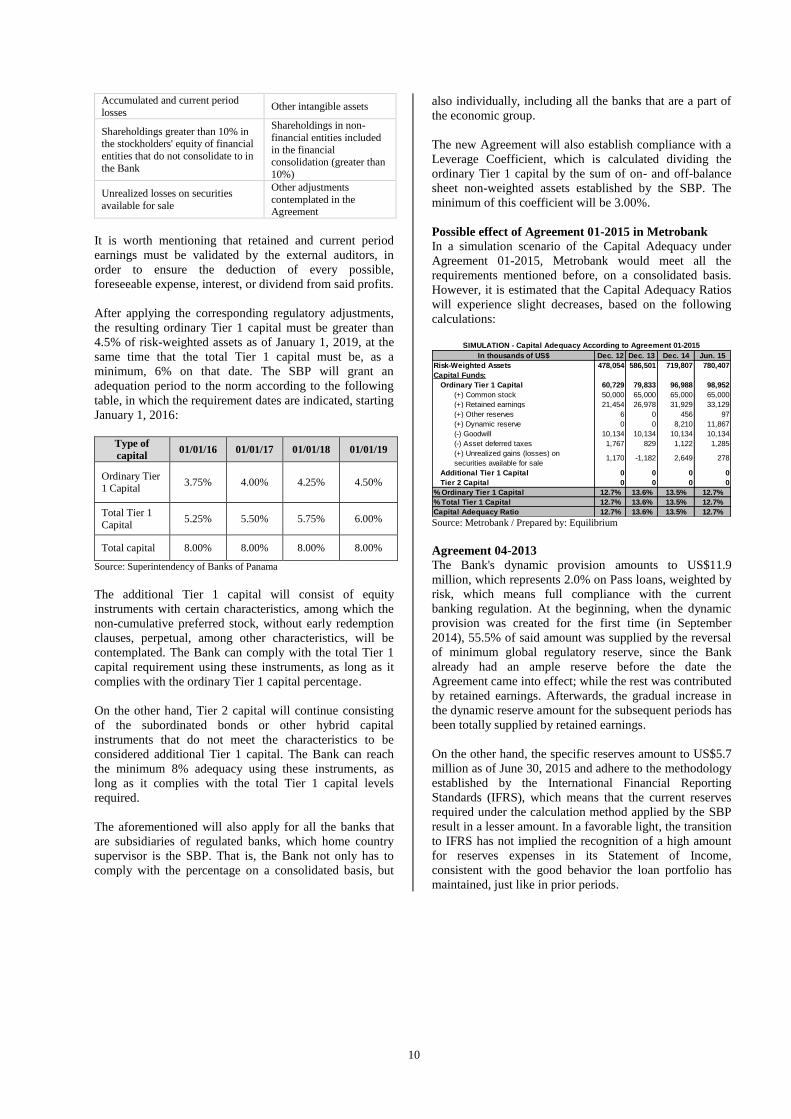

After applying the corresponding regulatory adjustments,

the resulting ordinary Tier 1 capital must be greater than

4.5% of risk-weighted assets as of January 1, 2019, at the

same time that the total Tier 1 capital must be, as a

minimum, 6% on that date. The SBP will grant an

adequation period to the norm according to the following

table, in which the requirement dates are indicated, starting

January 1, 2016:

Type of

capital 01/01/16 01/01/17 01/01/18 01/01/19

Ordinary Tier 1 Capital

3.75% 4.00% 4.25% 4.50%

Total Tier 1 Capital

5.25% 5.50% 5.75% 6.00%

Total capital 8.00% 8.00% 8.00% 8.00%

Source: Superintendency of Banks of Panama

The additional Tier 1 capital will consist of equity

instruments with certain characteristics, among which the

non-cumulative preferred stock, without early redemption

clauses, perpetual, among other characteristics, will be

contemplated. The Bank can comply with the total Tier 1

capital requirement using these instruments, as long as it

complies with the ordinary Tier 1 capital percentage.

On the other hand, Tier 2 capital will continue consisting

of the subordinated bonds or other hybrid capital

instruments that do not meet the characteristics to be

considered additional Tier 1 capital. The Bank can reach

the minimum 8% adequacy using these instruments, as

long as it complies with the total Tier 1 capital levels

required.

The aforementioned will also apply for all the banks that

are subsidiaries of regulated banks, which home country

supervisor is the SBP. That is, the Bank not only has to

comply with the percentage on a consolidated basis, but

also individually, including all the banks that are a part of

the economic group.

The new Agreement will also establish compliance with a

Leverage Coefficient, which is calculated dividing the

ordinary Tier 1 capital by the sum of on- and off-balance

sheet non-weighted assets established by the SBP. The

minimum of this coefficient will be 3.00%.

Possible effect of Agreement 01-2015 in Metrobank

In a simulation scenario of the Capital Adequacy under

Agreement 01-2015, Metrobank would meet all the

requirements mentioned before, on a consolidated basis.

However, it is estimated that the Capital Adequacy Ratios

will experience slight decreases, based on the following

calculations:

In thousands of US$ Dec. 12 Dec. 13 Dec. 14 Jun. 15

Risk-Weighted Assets 478,054 586,501 719,807 780,407

Capital Funds:

Ordinary Tier 1 Capital 60,729 79,833 96,988 98,952

(+) Common stock 50,000 65,000 65,000 65,000

(+) Retained earnings 21,454 26,978 31,929 33,129

(+) Other reserves 6 0 456 97

(+) Dynamic reserve 0 0 8,210 11,867

(-) Goodwill 10,134 10,134 10,134 10,134

(-) Asset deferred taxes 1,767 829 1,122 1,285

(+) Unrealized gains (losses) on

securities available for sale1,170 -1,182 2,649 278

Additional Tier 1 Capital 0 0 0 0

Tier 2 Capital 0 0 0 0

% Ordinary Tier 1 Capital 12.7% 13.6% 13.5% 12.7%

% Total Tier 1 Capital 12.7% 13.6% 13.5% 12.7%

Capital Adequacy Ratio 12.7% 13.6% 13.5% 12.7%

SIMULATION - Capital Adequacy According to Agreement 01-2015

Source: Metrobank / Prepared by: Equilibrium

Agreement 04-2013

The Bank's dynamic provision amounts to US$11.9

million, which represents 2.0% on Pass loans, weighted by

risk, which means full compliance with the current

banking regulation. At the beginning, when the dynamic

provision was created for the first time (in September

2014), 55.5% of said amount was supplied by the reversal

of minimum global regulatory reserve, since the Bank

already had an ample reserve before the date the

Agreement came into effect; while the rest was contributed

by retained earnings. Afterwards, the gradual increase in

the dynamic reserve amount for the subsequent periods has

been totally supplied by retained earnings.

On the other hand, the specific reserves amount to US$5.7

million as of June 30, 2015 and adhere to the methodology

established by the International Financial Reporting

Standards (IFRS), which means that the current reserves

required under the calculation method applied by the SBP

result in a lesser amount. In a favorable light, the transition

to IFRS has not implied the recognition of a high amount

for reserves expenses in its Statement of Income,

consistent with the good behavior the loan portfolio has

maintained, just like in prior periods.

11

METROBANK, S.A. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

in thousands of dollars

ASSETS:

Cash and cash items 5,565 0.7% 5,970 0.6% 12,045 1.2% 6,862 0.6% 5,165 0.5% -1,697 -24.7%

Demand deposits due from banks 44,945 5.7% 72,360 7.8% 86,549 8.7% 76,172 7.1% 75,361 6.7% -811 -1.1%

Time deposits due from banks 40,645 5.1% 37,336 4.0% 36,369 3.7% 39,804 3.7% 31,901 2.8% -7,903 -19.9%

Total Cash and Due from Banks 91,155 11.5% 115,666 12.4% 134,962 13.6% 122,838 11.4% 112,427 10.0% -10,411 -8.5%

Investments in securities available for sale 137,040 17.3% 165,092 17.7% 190,636 19.2% 220,975 20.6% 231,324 20.7% 10,350 4.7%

Total Investments 137,040 17.3% 165,092 17.7% 190,636 19.2% 220,975 20.6% 231,324 20.7% 10,350 4.7%

Total Funds Available 228,195 28.9% 280,757 30.1% 325,598 32.8% 343,813 32.0% 343,751 30.7% -62 0.0%

Loans 569,145 72.0% 657,277 70.4% 669,683 67.4% 727,951 67.8% 774,554 69.2% 46,603 6.4%

Current loans 565,876 71.6% 652,926 70.0% 666,808 67.1% 720,670 67.2% 768,172 68.6% 47,502 6.6%

Non-performing loans 1,844 0.2% 3,980 0.4% 1,239 0.1% 5,122 0.5% 4,599 0.4% -523 -10.2%

Past-due loans 1,425 0.2% 371 0.0% 1,635 0.2% 2,160 0.2% 1,783 0.2% -377 -17.4%

Less:

Loan Loss Reserve 6,425 0.8% 3,343 0.4% 8,755 0.9% 5,196 0.5% 5,707 0.5% 511 9.8%

Discounted unearned interest, fees and insurance 29,492 3.7% 31,042 3.3% 30,447 3.1% 28,599 2.7% 28,651 2.6% 52 0.2%

Net loans and discounts 533,228 67.4% 622,892 66.8% 630,481 63.5% 694,156 64.7% 740,196 66.1% 46,040 6.6%

Property, Furniture, Equipment and Improvements 6,503 0.8% 10,348 1.1% 10,721 1.1% 10,759 1.0% 10,668 1.0% (91) -0.8%

Goodwill 10,134 1.3% 10,134 1.1% 10,134 1.0% 10,134 0.9% 10,134 0.9% 0 0.0%

Accrued interest receivable 2,639 0.3% 2,702 0.3% 3,027 0.3% 3,586 0.3% 3,525 0.3% (62) -1.7%

Other assets 10,123 1.3% 6,288 0.7% 9,614 1.0% 6,567 0.6% 7,342 0.7% 775 11.8%

Assets held for sale 0 0.0% 0 0.0% 4,035 0.4% 4,035 0.4% 4,035 0.4% 0 0.0%

TOTAL ASSETS 790,822 100.0% 933,122 100.0% 993,609 100.0% 1,073,052 100.0% 1,119,652 100.0% 46,600 4.3%

LIABILITIES:

Demand deposits 83,578 10.6% 89,247 9.6% 97,625 9.8% 113,910 10.6% 99,753 8.9% (14,158) -12.4%

Savings deposits 88,572 11.2% 101,009 10.8% 117,312 11.8% 124,784 11.6% 123,104 11.0% (1,679) -1.3%

Customers' certificates of deposits 434,069 54.9% 540,635 57.9% 571,145 57.5% 636,245 59.3% 705,332 63.0% 69,087 10.9%

Interbank certificates of deposits 30,642 3.9% 29,012 3.1% 35,110 3.5% 24,243 2.3% 16,759 1.5% -7,484 -30.9%

Total deposits 636,862 80.5% 759,903 81.4% 821,192 82.6% 899,182 83.8% 944,948 84.4% 45,766 5.1%

Borrowings 28,058 3.5% 25,965 2.8% 23,639 2.4% 17,517 1.6% 12,190 1.1% (5,327) -30.4%

Securities sold under repurchase agreement 37,199 4.7% 32,074 3.4% 32,074 3.2% 27,500 2.6% 27,500 2.5% 0 0.0%

Cashiers' checks and certified checks 3,833 0.5% 5,882 0.6% 3,707 0.4% 4,525 0.4% 8,608 0.8% 4,083 90.2%

Accrued interest payable 3,343 0.4% 3,596 0.4% 4,367 0.4% 4,457 0.4% 4,934 0.4% 477 10.7%

Pending acceptances 277 0.0% 0 0.0% 2,297 0.2% 746 0.1% 24 0.0% (723) -96.8%

Other liabilities 8,621 1.1% 9,992 1.1% 8,957 0.9% 10,879 1.0% 11,076 1.0% 198 1.8%

TOTAL LIABILITIES 718,192 90.8% 837,411 89.7% 896,233 90.2% 964,807 89.9% 1,009,280 90.1% 44,473 4.6%

STOCKHOLDERS' EQUITY:

Common stock 50,000 6.3% 65,000 7.0% 65,000 6.5% 65,000 6.1% 65,000 5.8% 0 0.0%

Change in securities available for sale 1,170 0.1% -1,182 -0.1% 2,135 0.2% 2,649 0.2% 278 0.0% -2,371 -89.5%

Reserve for foreclosed assets 6 0.0% 0 0.0% 81 0.0% 8 0.0% 4 0.0% -4 -49.4%

Regulatory reserve for assets under administration 0 0.0% 0 0.0% 0 0.0% 91 0.0% 94 0.0% 3 3.2%

Difference between regulatory specific reserve and IFRS reserve 0 0.0% 4,915 0.5% 0 0.0% 358 0.0% 0 0.0% -358 -100.0%

Dynamic reserve for loan losses 0 0.0% 0 0.0% 0 0.0% 8,210 0.8% 11,867 1.1% 3,657 44.5%

Net income for the period 6,873 0.9% 9,848 1.1% 4,768 0.5% 11,118 1.0% 7,067 0.6% (4,051) -36.4%

Retained earnings 14,581 1.8% 17,129 1.8% 25,393 2.6% 20,811 1.9% 26,062 2.3% 5,251 25.2%

TOTAL STOCKHOLDERS' EQUITY 72,630 9.2% 95,711 10.3% 97,376 9.8% 108,244 10.1% 110,372 9.9% 2,128 2.0%

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY 790,822 100.0% 933,122 100.0% 993,609 100.0% 1,073,052 100.0% 1,119,652 100.0% 46,600 4.3%

7.5% 26.1% 1.7% #¡DIV/0! 2.0%

METROBANK, S.A. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF INCOME

(in thousands of dollars)

Financial Income 37,990 100.0% 45,649 100.0% 25,105 100.0% 53,022 100.0% 29,530 100.0% 4,425 17.6%

Interest earned on loans 32,677 86.0% 39,288 86.1% 20,975 83.5% 43,962 82.9% 24,347 82.4% 3,372 16.1%

Interest earned on due from banks 99 0.3% 82 0.2% 39 0.2% 105 0.2% 93 0.3% 54 137.4%

Interest earned on investments in securities 5,214 13.7% 6,279 13.8% 4,091 16.3% 8,955 16.9% 5,090 17.2% 999 24.4%

Financial Expenses 19,238 50.6% 23,847 52.2% 13,790 54.9% 28,922 54.5% 16,212 54.9% 2,422 17.6%

Gross financial results 18,752 49.4% 21,802 47.8% 11,315 45.1% 24,100 45.5% 13,317 45.1% 2,003 17.7%

Net fees 2,958 7.8% 4,289 9.4% 2,373 9.5% 5,300 10.0% 3,008 10.2% 635 26.8%

Financial results before reserves 21,710 57.1% 26,092 57.2% 13,687 54.5% 29,400 55.4% 16,325 55.3% 2,638 19.3%

Loan loss reserve 1,339 3.5% 1,652 3.6% 603 2.4% 2,588 4.9% 689 2.3% 86 14.3%

Reserve for impairment losses on investments in securities 204 0.5% 0 0.0% 0 0.0% 0 0.0% 0 0.0% 0 -

Financial results after reserves 20,167 53.1% 24,440 53.5% 13,085 52.1% 26,812 50.6% 15,636 53.0% 2,552 19.5%

Dividends income 4 0.0% 4 0.0% 2 0.0% 5 0.0% 2 0.0% (1) -27.9%

Gain on sale of securities 1,045 2.7% 932 2.0% 185 0.7% 676 1.3% 1,448 4.9% 1,263 682.4%

Other 1,480 3.9% 2,564 5.6% 1,700 6.8% 5,299 10.0% 2,138 7.2% 438 25.7%

Other income (expenses) 2,529 6.7% 3,500 7.7% 1,888 7.5% 5,980 11.3% 3,588 12.1% 1,700 90.1%

Total operating income, net 22,695 59.7% 27,940 61.2% 14,972 59.6% 32,792 61.8% 19,224 65.1% 4,252 28.4%

General and administrative expenses 14,488 38.1% 17,013 37.3% 9,669 38.5% 20,661 39.0% 11,239 38.1% 1,570 16.2%

General operating expenses 6,450 17.0% 6,438 14.1% 3,780 15.1% 8,384 15.8% 4,743 16.1% 963 25.5%

Employee expenses and other compensations 7,541 19.8% 9,085 19.9% 5,101 20.3% 10,622 20.0% 5,625 19.0% 524 10.3%

Depreciation and amortization 497 1.3% 1,490 3.3% 788 3.1% 1,654 3.1% 871 3.0% 84 10.6%

Profits before income taxes 8,208 21.6% 10,927 23.9% 5,303 21.1% 12,131 22.9% 7,984 27.0% 2,681 50.6%

Income taxes 1,335 3.5% 1,079 2.4% 535 2.1% 1,013 1.9% 917 3.1% 382 71.3%

NET INCOME 6,873 18.1% 9,848 21.6% 4,768 19.0% 11,118 21.0% 7,067 23.9% 2,300 48.2%

%

Dec.12 % Dec.14 %

Dec.14Dec.13 %%Dec.12 Jun.14 %Jun.15 /

Jun.14

%

Variation

Jun.14 %Jun.15 /

Dec.14Jun.15 %

Jun.15 %

Dec.13 %%

Variation

12

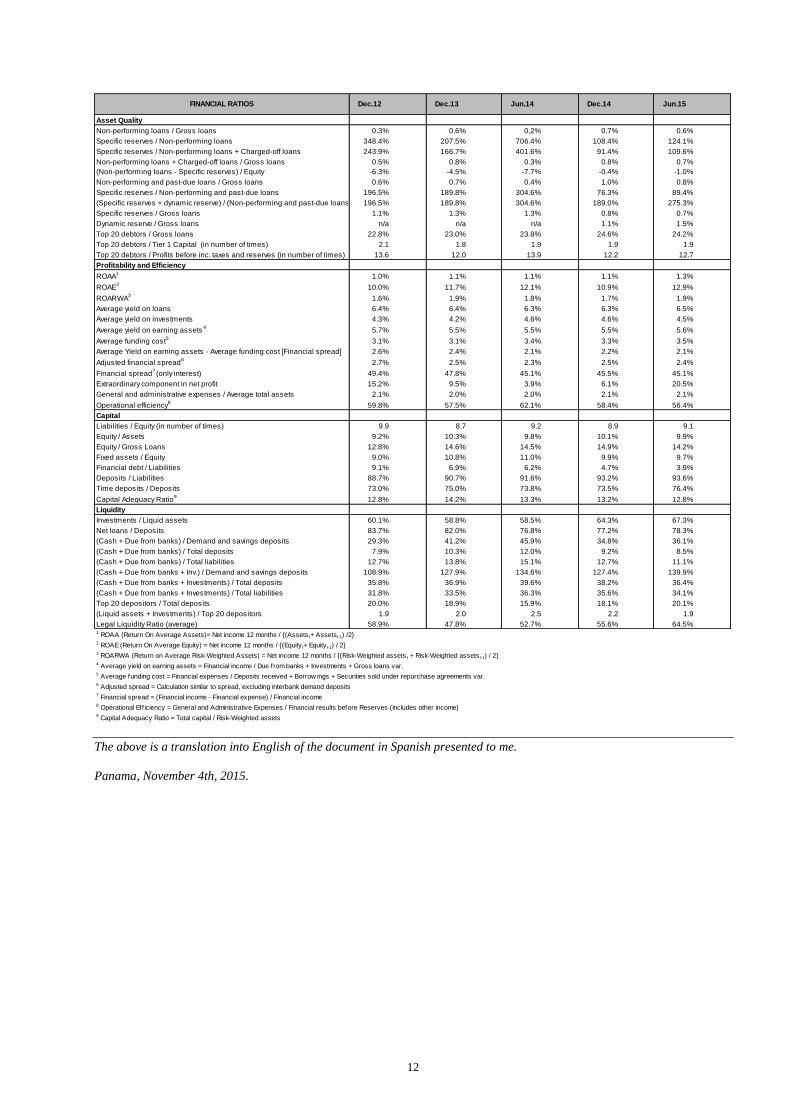

Asset Quality

Non-performing loans / Gross loans 0.3% 0.6% 0.2% 0.7% 0.6%

Specific reserves / Non-performing loans 348.4% 207.5% 706.4% 108.4% 124.1%

Specific reserves / Non-performing loans + Charged-off loans 243.9% 166.7% 401.6% 91.4% 109.6%

Non-performing loans + Charged-off loans / Gross loans 0.5% 0.8% 0.3% 0.8% 0.7%

(Non-performing loans - Specific reserves) / Equity -6.3% -4.5% -7.7% -0.4% -1.0%

Non-performing and past-due loans / Gross loans 0.6% 0.7% 0.4% 1.0% 0.8%

Specific reserves / Non-performing and past-due loans 196.5% 189.8% 304.6% 76.3% 89.4%

(Specific reserves + dynamic reserve) / (Non-performing and past-due loans) 196.5% 189.8% 304.6% 189.0% 275.3%

Specific reserves / Gross loans 1.1% 1.3% 1.3% 0.8% 0.7%

Dynamic reserve / Gross loans n/a n/a n/a 1.1% 1.5%

Top 20 debtors / Gross loans 22.8% 23.0% 23.8% 24.6% 24.2%

Top 20 debtors / Tier 1 Capital (in number of times) 2.1 1.8 1.9 1.9 1.9

Top 20 debtors / Profits before inc. taxes and reserves (in number of times) 13.6 12.0 13.9 12.2 12.7

Profitability and Efficiency

ROAA1

1.0% 1.1% 1.1% 1.1% 1.3%

ROAE2

10.0% 11.7% 12.1% 10.9% 12.9%

ROARWA3

1.6% 1.9% 1.8% 1.7% 1.9%

Average yield on loans 6.4% 6.4% 6.3% 6.3% 6.5%

Average yield on investments 4.3% 4.2% 4.6% 4.6% 4.5%

Average yield on earning assets4

5.7% 5.5% 5.5% 5.5% 5.6%

Average funding cost5

3.1% 3.1% 3.4% 3.3% 3.5%

Average Yield on earning assets - Average funding cost [Financial spread] 2.6% 2.4% 2.1% 2.2% 2.1%

Adjusted financial spread6

2.7% 2.5% 2.3% 2.5% 2.4%

Financial spread7 (only interest) 49.4% 47.8% 45.1% 45.5% 45.1%

Extraordinary component in net profit 15.2% 9.5% 3.9% 6.1% 20.5%

General and administrative expenses / Average total assets 2.1% 2.0% 2.0% 2.1% 2.1%

Operational efficiency8

59.8% 57.5% 62.1% 58.4% 56.4%

Capital

Liabilities / Equity (in number of times) 9.9 8.7 9.2 8.9 9.1

Equity / Assets 9.2% 10.3% 9.8% 10.1% 9.9%

Equity / Gross Loans 12.8% 14.6% 14.5% 14.9% 14.2%

Fixed assets / Equity 9.0% 10.8% 11.0% 9.9% 9.7%

Financial debt / Liabilities 9.1% 6.9% 6.2% 4.7% 3.9%

Deposits / Liabilities 88.7% 90.7% 91.6% 93.2% 93.6%

Time deposits / Deposits 73.0% 75.0% 73.8% 73.5% 76.4%

Capital Adequacy Ratio9

12.8% 14.2% 13.3% 13.2% 12.8%

Liquidity

Investments / Liquid assets 60.1% 58.8% 58.5% 64.3% 67.3%

Net loans / Deposits 83.7% 82.0% 76.8% 77.2% 78.3%

(Cash + Due from banks) / Demand and savings deposits 29.3% 41.2% 45.9% 34.8% 36.1%

(Cash + Due from banks) / Total deposits 7.9% 10.3% 12.0% 9.2% 8.5%

(Cash + Due from banks) / Total liabilities 12.7% 13.8% 15.1% 12.7% 11.1%

(Cash + Due from banks + Inv.) / Demand and savings deposits 108.9% 127.9% 134.6% 127.4% 139.9%

(Cash + Due from banks + Investments) / Total deposits 35.8% 36.9% 39.6% 38.2% 36.4%

(Cash + Due from banks + Investments) / Total liabilities 31.8% 33.5% 36.3% 35.6% 34.1%

Top 20 depositors / Total deposits 20.0% 18.9% 15.9% 18.1% 20.1%

(Liquid assets + Investments) / Top 20 depositors 1.9 2.0 2.5 2.2 1.9

Legal Liquidity Ratio (average) 58.9% 47.8% 52.7% 55.6% 64.5%1 ROAA (Return On Average Assets)= Net income 12 months / {(Assets t+ Assets t-1) /2}2 ROAE (Return On Average Equity) = Net income 12 months / {(Equity t+ Equityt-1) / 2}3 ROARWA (Return on Average Risk-Weighted Assets) = Net income 12 months / {(Risk-Weighted assets t + Risk-Weighted assets t-1) / 2}4 Average yield on earning assets = Financial income / Due from banks + Investments + Gross loans var.5 Average funding cost = Financial expenses / Deposits received + Borrow ings + Securities sold under repurchase agreements var.6 Adjusted spread = Calculation similar to spread, excluding interbank demand deposits7 Financial spread = (Financial income - Financial expense) / Financial income8 Operational Eff iciency = General and Administrative Expenses / Financial results before Reserves (Includes other income)9 Capital Adequacy Ratio = Total capital / Risk-Weighted assets

Dec.14FINANCIAL RATIOS Dec.12 Jun.14Dec.13 Jun.15

The above is a translation into English of the document in Spanish presented to me.

Panama, November 4th, 2015.