Metro Phoenix Economic Snapshot 2013 presented by The Luckys

Upload

desert-lifestyle-publishingCategory

view

219download

2description

WeallknowtheValley’srealestatemarkethasbeenvolatileoverthelast5+years.Thegoodnewsisthingsarechanging.Distressedhomesaredownapproximately75%fromlastyearandtheactualsupplyofhomesisbelowthatofa“normalmarket”.TheValleyispositionedforacomeback.Notacomebackof2005proportions,butastable,steadycomebackwhichwewillwelcome. Keepinmindrealestateislocal.Whatyouhearnationallymaynotreflectwhatisactuallyhappeninginyourneighborhood.RememberwhenArizonawasreaching47%appreciationinoneyear,mostofthecountrywasnowherenearthatlevel.Thesameconceptisvalidagain.Arizonawas#3lastyearforforeclosuresanddistressedpropertiesbehindFloridaandNevada.Wearenow#27!Wearemovingrapidlyintherightdirection.Pleasestudythisinformationandfeelfreetopassitontoanyoneyouknowwhomayneedhelpdecipheringourcurrentmarket.Weallneedtoknowwhatourpropertyvalueisandwhereitisgoing.Thisisvalidwhetheryouarebuyingorselling.Let’sdiscussyourpersonalsituationandgoalsandcomeupwithaplan. IamveryexcitedaboutthepositivemovementArizonahashadandlookforwardtohelpingyougetthemostvalueoutofyourhome.

Jeannine

JEANNINE BARTNICKICRS,GRI,ABR,SRS,e-PRO,RSPS,CDPE,CLHMS

Certified Luxury Home Property SpecialistCertified Residential Specialist

senior sales & marketing consultant

If your home is currently listed, this is not a solicitation for that listing. ProducedbyDesertLifestylePublishing•480.460.0996•www.DesertLifestyle.net

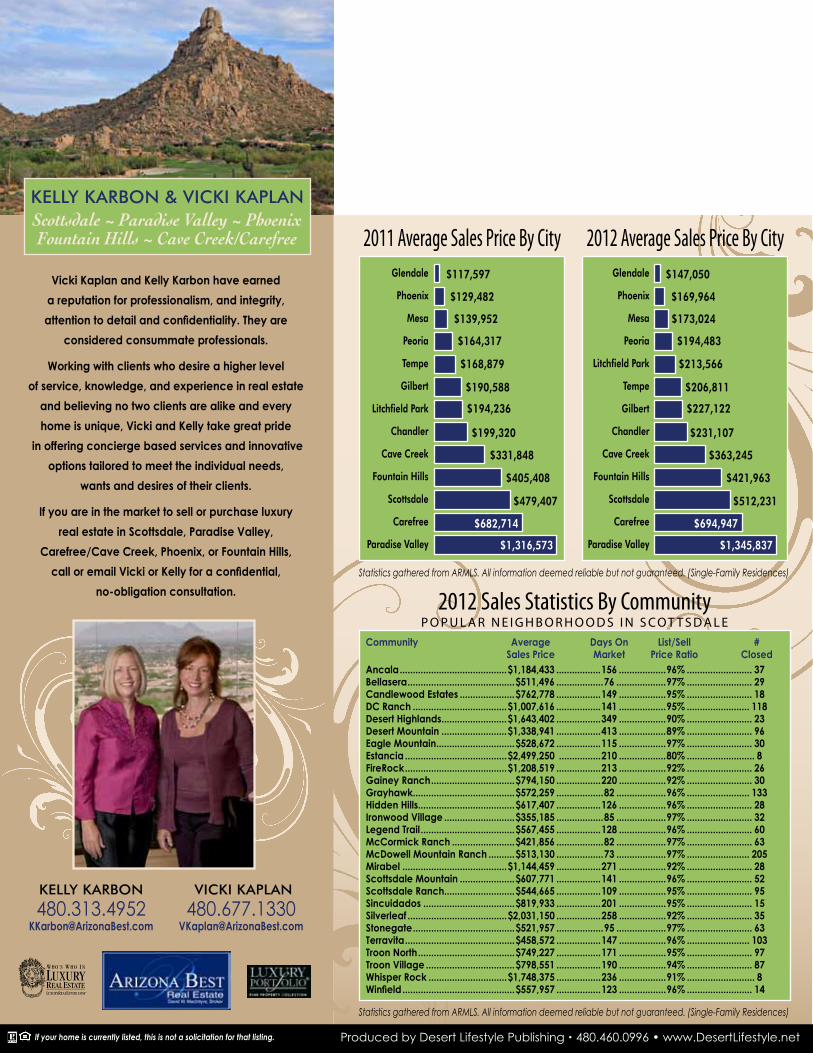

2011 Sales Statistics By CommunityCommunity Average DaysOn List/Sell # SalesPrice Market PriceRatio Closed

Ancala........................................$1,028,816................. 142..................93%..........................39

Bellasera........................................$441,157................. 139..................95%..........................19

DCRanch......................................$834,211................. 170..................95%.........................124

DesertHighlands.......................$1,283,186................. 277..................90%..........................18

DesertMountain........................$1,273,481................. 429..................88%.........................106

EagleMountain............................$515,914................. 193..................94%..........................27

Estancia......................................$1,973,181................. 294..................88%..........................11

FireRock......................................$1,151,845................. 271..................92%..........................24

GaineyRanch..............................$790,592................. 186..................93%..........................21

Grayhawk.....................................$526,555................. 122..................96%.........................142

HiddenHills....................................$664,171................. 133..................96%..........................32

IronwoodVillage..........................$337,443................. 105..................97%..........................44

LegendTrail...................................$507,262................. 150..................95%..........................51

McCormickRanch.......................$442,812................. 135..................96%..........................24

McDowellMountainRanch........$484,628................. 114..................95%.........................218

Mirabel..........................................$947,815................. 331..................89%..........................52

ScottsdaleMountain...................$639,893................. 157..................95%..........................40

ScottsdaleRanch.........................$431,296................. 112..................96%..........................77

Sincuidados..................................$771,923................. 184..................94%..........................13

Silverleaf.....................................$2,173,735................. 353..................86%..........................46

Stonegate.....................................$475,787................. 171..................94%..........................51

Terravita.........................................$425,710................. 142..................95%..........................76

WhisperRock.............................$1,866,900................. 667..................87%...........................5

Winfield..........................................$468,014................. 196..................96%..........................17

Statistics gathered from ARMLS. All information deemed reliable but not guaranteed.(Single-Family Residences)

2011 Average Sales Price By City

Statistics gathered from ARMLS. All information deemed reliable but not guaranteed. (Single-Family Residences)

Glendale

Phoenix

Mesa

Peoria

Tempe

Gilbert

Litchfield Park

Chandler

Cave Creek

Fountain Hills

Scottsdale

Carefree

Paradise Valley

$117,597

$129,482

$139,952

$331,848

$405,408

$479,407

$682,714

$1,316,573

$190,588

$168,879

$194,236

$164,317

$199,320

TherecoveryintheMetroPhoenixhousingmarketstartedquitegentlyinSeptember2011butgraduallygrewinstrength,andbythespringof2012itwasrunningattopspeed.Theimmediatelyobviousimpactwasastrongriseinpricing,infactagreaterpercentagerisethananyothermetropolitanareaintheUSA.Alookbackat2012comparedwith2011showsusthat:•Theannualaveragepricepersq.ft.rosebyover20% from$81.59to$98.24•Theannualaveragesalespriceincreased23%from $156,774to$192,549•Theannualmediansalespricejumped27%from$110,000 to$140,000 Inventorywaslowthroughout2012,causingintensecompetitionamongbuyers.Thiswasparticularlytrueatthelowerendofthemarket.Buyerswithcashheldasubstantialadvantage,sincetheycouldimpresssellerswiththefactthattheirofferdidnotdependonobtainingapprovalforaloanorasatisfactoryappraisal.Forthehigherpriceranges,supplyanddemandweremorebalanced,butpricesincreasedinmostareasasconfidencereturnedtothemarket. Salesvolumeswerelowerin2012than2011,butthiswaslargelyduetoashortageofaffordablehomestobuy,notbecauseoflackofdemand.Atthestartof2011,nearlyhalfofhomespurchasedwerelender-ownedforeclosures,butbytheendof2012thesehaddroppedtolessthan13%ofsales.Meanwhilenormalsalesgrewfromjust29%ofsalesinJanuary2011to61%inDecember2012.Shortsalestookoverfromforeclosuresasthepreferredmeansofresolving

homeloandelinquency.Theyconstituted21%ofsalesatthebeginningof2011,and26%bytheendof2012. Delinquenthomeloanswererunningashighas16.3%inArizonaasrecentlyasFebruary2010.ByOctober2012thishaddroppedto7.7%,accordingtoreportsbyLenderProcessingServices.Thisimprovementisthelargestofanystateinthenation.Arizona’snon-judicialforeclosureprocesshasallowedittoeliminatedelinquentloansatamuchfasterpacethanstateswithajudicialprocess.Thisisbadnewsfortheborrowersinvolved,butgoodnewsforthemarketsincewenolongerhavetheimpendingthreatofsignificantdistressedinventorycomingontothemarket. Manyfamilieswholosttheirhomesthroughforeclosureandshortsalesin2008and2009arenowplanningtostoprentingandgetbackintohomeownership.Thiswilladdtothe2013demandforhomestoown,ratherthantorent. Investorshavebeenaverysignificantpartofthedemandsinceearly2009andthisdidnotchangein2012.Whatdidchangeisthatmorepropertieswerepurchasedbylargemulti-nationalinvestorsinsteadofsmallerlocalplayers.Nowthatpricinghasrespondedtotheexcessdemandoversupply,weexpectdemandfromthelargeinvestorstoslowlydissipatein2013. Thenewhomemarkethassprungbacktolifeafteraprolongedhibernationbetween2008and2011.In2012,demandfornewhomesoutpaceddevelopers’abilitytobuildthem.Ashortageofskilledconstructionworkersandlimitedfinishedlotsinbuilders’ownershipmeantthatthegrowthinnewsaleswassomewhatstifled.Neverthelesswesawnewhomesalesgrowby49%between2011and2012despitesignificant

increasesinprices.Developersarenowbuyingupnewlandandfinishedlotstosetthemselvesuptosupplymorehomesin2013.Withtheexpectedincreaseinpopulationthough,thisisnotexpectedtobeenoughtomeetthecomingdemand. OveralltheMetroPhoenixhousingmarketisinastrongerpositionnowthanithasbeensincelate2005.Manythemesfrom2012willprobablycontinueinto2013asthemarketheadsbacktonormal.Foreclosuresandshortsalesareexpectedtodecline.Newhomeandnormalre-salesarelikelytoincrease,whilelowinventorywillcontinuetobeakeyfactorincausingpricestomovehigher.Withnosignificantsourceofnewsupply,wedon’tseeinventoryrisingbacktonormallevelsforaverylongtime. Inthecurrentmarket,homesareeasytosellbutsometimesbuyingcanbeachallengeduetocompetitionfromotherbuyers.Evenso,owningahomeisfinanciallymuchmoreattractivethanrentingbecauseinterestratesonhomeloansareunusuallylowandhomepricesarestillcheapbyhistoricalstandards,especiallywhencomparedwithrentalrates.Withtheinventoryofhomesforsaleexpectedtostaylowforsomeconsiderabletime,buyersarelikelytohavetheirpatiencerewardedwithcontinuedstrongappreciation.Mostofthosewhoboughthomesin2011havealreadyseenverystronggrowthinthevalueoftheirhome,andbythetimewereach2015wearelikelytobesayingthesameaboutthosewhopurchasedhomesbetween2009and2013.

AuthorandstatisticianMichaelOrristheDirectorofRealEstateStudiesatASU’sW.P.CareySchoolofBusiness,andPrincipalofTheCromfordReport.

IN THE NATIONAL SPOTLIGHT Aswe’veturnedthepageonanotheryear,thenationaleconomycontinuesitsmodestrecovery.Optimismtingedwithuncertaintyseemtobetheprevailingsentiments.Althoughtheworsteffectsofthe“fiscalcliff”havebeenaverted,thereisstillawait-and-seeattitudeamongconsumersandemployersregardingtaxationandfederalspendingpolicies. Corporationsareflushwithcash,butarewarytospendonhiringorotherbusinessexpendituresuntilfurtherclarityontheeconomy’spathisavailable.However,onceCorporateAmericagainsconfidence,thetrillionsofdollarsandrecordprofitsthey’resittingoncanbeinjectedintothemarketplacethroughemployment,manufacturing,andotherbusinessinvestment. ThereisadirectcorrelationbetweenanincreaseinconsumerconfidenceandanincreaseintheGDP.Whenconsumersarecomfortableandconfident,theyspendmoney,pavingthewayforbusinessexpansion.Forconsumerstofeelconfidentin2013,thereneedstobeacontinuedimprovementinthefinancialmarketsandhomevalues,alongwithaprogressiveloweringoftheunemploymentratecoupledwithaveragewageincreases.TheGDPisexpectedtogrowatapproximately2%in2013,aboutthesameaslastyear. Ourfinancialmarketsenjoyedarobust2012withtheS&P500finishingwithjustundera12%growth.Whiletherecentlyenactedtaxlawchangesmaydampensomeoftheenthusiasmininvestingforsome,manymarketforecastersareprojectinga6%-12%growthfortheS&P500thisyear. Thebrightspotintheeconomyin2012wasthehousingmarket,aslowmortgageratesandaffordablehomepricesnationwidekepthomessellingatabriskpace.Fortunatelythattrendisexpectedtocontinuein2013.Infact,someareasareexperiencingsuchahousingshortagethattheconstructionindustryisstrugglingtomeetdemand.ThatisespeciallytrueinourArizonamarket(seetheResidentialRealEstatearticle.) Kiplinger.comforecastsamoderate,butsteadyjobgrowththrough2013withaprojectedannualtotalofanaddedtwomillionjobsbyyearend.Similarly,theunemploymentrateisprojectedtodriftdowntoabout7.5%vs.7.8%attheendof2012. Mosteconomistsareexpectinganoverallimprovementinournation’seconomic

healthin2013.WayneStutzer,SeniorVicePresidentandFinancialConsultantforRBCWealthManagement,explainsthecyclicalnatureoftheeconomy.“Thetopofthemarketwasin2006.Today,2013istheseventhyearofthetypicalseven-yeareconomiccycle.We’realmostoutofthewoods.”Thewildcardmaybehowthenewtaxlawsimpacttheeconomyasthehigh-incomeearnerstargetedwithtaxincreasesalsoaccountforhalfofournation’sconsumerspending.Weareexpectingslowbutencouragingprogressinalloftheseareasin2013.Stutzercontinues,“Ifthingsgowell,then2013willberememberedastheeconomicyearthatsetthestageformuchbetteryearstocome.”

ARIZONA HEATS UP AlongwithNevada,Arizonawasgroundzeroforthehousingmeltdown,plaguedbyhighforeclosuresandhighunemploymentduring2006-2010.However,Arizonastagedastrongeconomiccomebackin2012,boastingthebesthousingmarketinthenation. “AsofSeptember2012,Arizonarankedfifthamongstatesforjobgrowth,andtheMetroPhoenixareawasfourthamonglargemetropolitanareas,”saysLeeMcPheters,ResearchProfessorandDirectoroftheJPMorganChaseEconomicOutlookCenterattheW.P.CareySchoolofBusiness.ThisisanextraordinaryimprovementfromArizona’slowpointin2009whenArizonafellfromanenviablejobgrowthrankingofsecondin2006,toadismal49thofthe50statesin2009.“Arizonaisexpectedtoadd60,000jobsin2013.Weshouldfinallydipbelow8%unemploymentin2013–downto7.6%.” Arizona’seconomicgrowthhashistoricallybeenstokedbyencouragingbusinessesandpeopletomovehere.Arizonaoffersadesirableclimate,affordablehousing,andagrowingbusinessenvironmentwithreasonablestatetaxrates.ArizonastandstobenefitfromCalifornia’srecentlyenactedProposition30whichraisesanalreadyhighstatesalestaxevenhigher,whilesignificantlyraisingincometaxesonindividualsmaking$250,000ormore.TheGreaterPhoenixEconomicCouncilhasdoubledtheireffortstoattractCaliforniabusinessesandtheiremployeestoArizona.ThesenewCaliforniataxlawchangesareexpectedtosignificantlyincreasepopulationflowstoArizona’sadvantage. ElliottD.Pollack,CEOoflocaleconomicconsultingfirmElliottD.PollackandCompany,notestheimportanceofmigration

toourstate.“Intheabsenceofthefiscalcliff,thingsshouldcontinuetoimproveoverthenextseveralyears.By2015,thingsshouldbenormalized.AsIliketosay,we’reonlyonedecentpopulation-flowyearawayfromtheissuebeingresolved.” MetroPhoenixhasrisenfromitshousingmeltdownwithencouragingjobgrowthledbyahousingboomthathasnowcausedaresidentialhousingshortage.Homebuildersaresteadilydustingofftheirequipmentandbuildinghomestomeetdemand.NewhomesalesinjectfreshlifeintotheArizonaeconomyandtaxbase.ThejourneytowardcontinuedeconomicgrowthandprosperityforArizonaseemstoonceagainbeheadingdownthefamiliarpathofbuildingandsellinghomestomeetincreasingdemand.

G E N E R A L E C O N O M I C S NA P S H OT

R E S I D E N T I A L R E A L E S TAT E

2013 ECONOMIC FORECASTS

GDPGROWTH2% growth in ’13,

about the same as last year. . .

INTERESTRATESLittleornoincrease

inshort-termratesin‘13. . .

BUSINESSSPENDINGAbouta4%gainin’13,

halfof‘12’space. . .

HOUSINGSALESUp8%,helpingGDPin’13

. . .TRADEDEFICIT

Wideningby2%in’13,afteraslightdipin’12

. . .UNEMPLOYMENT

Headingtoabout7.5%bytheendof‘13

. . .INFLATION

Slightlyhigherthisyear,2.3%. . .

ENERGYOiltradingat$90-$95/barrel

throughearlyspring. . .

RETAILSALES5%growthin’13

afterstrongholidaysales

Source:TheKiplingerLetter

ByMichaelOrr

ACTIVE LISTING COUNTSGreaterPhoenix-ARMLSResidential

SALES PER MONTHGreaterPhoenix-ARMLSResidential-MeasuredMonthly

MONTHLY AVERAGE SALES PRICE PER SQUARE FOOTGreaterPhoenix-ARMLSResidential

TherecoveryintheMetroPhoenixhousingmarketstartedquitegentlyinSeptember2011butgraduallygrewinstrength,andbythespringof2012itwasrunningattopspeed.Theimmediatelyobviousimpactwasastrongriseinpricing,infactagreaterpercentagerisethananyothermetropolitanareaintheUSA.Alookbackat2012comparedwith2011showsusthat:•Theannualaveragepricepersq.ft.rosebyover20% from$81.59to$98.24•Theannualaveragesalespriceincreased23%from $156,774to$192,549•Theannualmediansalespricejumped27%from$110,000 to$140,000 Inventorywaslowthroughout2012,causingintensecompetitionamongbuyers.Thiswasparticularlytrueatthelowerendofthemarket.Buyerswithcashheldasubstantialadvantage,sincetheycouldimpresssellerswiththefactthattheirofferdidnotdependonobtainingapprovalforaloanorasatisfactoryappraisal.Forthehigherpriceranges,supplyanddemandweremorebalanced,butpricesincreasedinmostareasasconfidencereturnedtothemarket. Salesvolumeswerelowerin2012than2011,butthiswaslargelyduetoashortageofaffordablehomestobuy,notbecauseoflackofdemand.Atthestartof2011,nearlyhalfofhomespurchasedwerelender-ownedforeclosures,butbytheendof2012thesehaddroppedtolessthan13%ofsales.Meanwhilenormalsalesgrewfromjust29%ofsalesinJanuary2011to61%inDecember2012.Shortsalestookoverfromforeclosuresasthepreferredmeansofresolving

homeloandelinquency.Theyconstituted21%ofsalesatthebeginningof2011,and26%bytheendof2012. Delinquenthomeloanswererunningashighas16.3%inArizonaasrecentlyasFebruary2010.ByOctober2012thishaddroppedto7.7%,accordingtoreportsbyLenderProcessingServices.Thisimprovementisthelargestofanystateinthenation.Arizona’snon-judicialforeclosureprocesshasallowedittoeliminatedelinquentloansatamuchfasterpacethanstateswithajudicialprocess.Thisisbadnewsfortheborrowersinvolved,butgoodnewsforthemarketsincewenolongerhavetheimpendingthreatofsignificantdistressedinventorycomingontothemarket. Manyfamilieswholosttheirhomesthroughforeclosureandshortsalesin2008and2009arenowplanningtostoprentingandgetbackintohomeownership.Thiswilladdtothe2013demandforhomestoown,ratherthantorent. Investorshavebeenaverysignificantpartofthedemandsinceearly2009andthisdidnotchangein2012.Whatdidchangeisthatmorepropertieswerepurchasedbylargemulti-nationalinvestorsinsteadofsmallerlocalplayers.Nowthatpricinghasrespondedtotheexcessdemandoversupply,weexpectdemandfromthelargeinvestorstoslowlydissipatein2013. Thenewhomemarkethassprungbacktolifeafteraprolongedhibernationbetween2008and2011.In2012,demandfornewhomesoutpaceddevelopers’abilitytobuildthem.Ashortageofskilledconstructionworkersandlimitedfinishedlotsinbuilders’ownershipmeantthatthegrowthinnewsaleswassomewhatstifled.Neverthelesswesawnewhomesalesgrowby49%between2011and2012despitesignificant

increasesinprices.Developersarenowbuyingupnewlandandfinishedlotstosetthemselvesuptosupplymorehomesin2013.Withtheexpectedincreaseinpopulationthough,thisisnotexpectedtobeenoughtomeetthecomingdemand. OveralltheMetroPhoenixhousingmarketisinastrongerpositionnowthanithasbeensincelate2005.Manythemesfrom2012willprobablycontinueinto2013asthemarketheadsbacktonormal.Foreclosuresandshortsalesareexpectedtodecline.Newhomeandnormalre-salesarelikelytoincrease,whilelowinventorywillcontinuetobeakeyfactorincausingpricestomovehigher.Withnosignificantsourceofnewsupply,wedon’tseeinventoryrisingbacktonormallevelsforaverylongtime. Inthecurrentmarket,homesareeasytosellbutsometimesbuyingcanbeachallengeduetocompetitionfromotherbuyers.Evenso,owningahomeisfinanciallymuchmoreattractivethanrentingbecauseinterestratesonhomeloansareunusuallylowandhomepricesarestillcheapbyhistoricalstandards,especiallywhencomparedwithrentalrates.Withtheinventoryofhomesforsaleexpectedtostaylowforsomeconsiderabletime,buyersarelikelytohavetheirpatiencerewardedwithcontinuedstrongappreciation.Mostofthosewhoboughthomesin2011havealreadyseenverystronggrowthinthevalueoftheirhome,andbythetimewereach2015wearelikelytobesayingthesameaboutthosewhopurchasedhomesbetween2009and2013.

AuthorandstatisticianMichaelOrristheDirectorofRealEstateStudiesatASU’sW.P.CareySchoolofBusiness,andPrincipalofTheCromfordReport.

IN THE NATIONAL SPOTLIGHT Aswe’veturnedthepageonanotheryear,thenationaleconomycontinuesitsmodestrecovery.Optimismtingedwithuncertaintyseemtobetheprevailingsentiments.Althoughtheworsteffectsofthe“fiscalcliff”havebeenaverted,thereisstillawait-and-seeattitudeamongconsumersandemployersregardingtaxationandfederalspendingpolicies. Corporationsareflushwithcash,butarewarytospendonhiringorotherbusinessexpendituresuntilfurtherclarityontheeconomy’spathisavailable.However,onceCorporateAmericagainsconfidence,thetrillionsofdollarsandrecordprofitsthey’resittingoncanbeinjectedintothemarketplacethroughemployment,manufacturing,andotherbusinessinvestment. ThereisadirectcorrelationbetweenanincreaseinconsumerconfidenceandanincreaseintheGDP.Whenconsumersarecomfortableandconfident,theyspendmoney,pavingthewayforbusinessexpansion.Forconsumerstofeelconfidentin2013,thereneedstobeacontinuedimprovementinthefinancialmarketsandhomevalues,alongwithaprogressiveloweringoftheunemploymentratecoupledwithaveragewageincreases.TheGDPisexpectedtogrowatapproximately2%in2013,aboutthesameaslastyear. Ourfinancialmarketsenjoyedarobust2012withtheS&P500finishingwithjustundera12%growth.Whiletherecentlyenactedtaxlawchangesmaydampensomeoftheenthusiasmininvestingforsome,manymarketforecastersareprojectinga6%-12%growthfortheS&P500thisyear. Thebrightspotintheeconomyin2012wasthehousingmarket,aslowmortgageratesandaffordablehomepricesnationwidekepthomessellingatabriskpace.Fortunatelythattrendisexpectedtocontinuein2013.Infact,someareasareexperiencingsuchahousingshortagethattheconstructionindustryisstrugglingtomeetdemand.ThatisespeciallytrueinourArizonamarket(seetheResidentialRealEstatearticle.) Kiplinger.comforecastsamoderate,butsteadyjobgrowththrough2013withaprojectedannualtotalofanaddedtwomillionjobsbyyearend.Similarly,theunemploymentrateisprojectedtodriftdowntoabout7.5%vs.7.8%attheendof2012. Mosteconomistsareexpectinganoverallimprovementinournation’seconomic

healthin2013.WayneStutzer,SeniorVicePresidentandFinancialConsultantforRBCWealthManagement,explainsthecyclicalnatureoftheeconomy.“Thetopofthemarketwasin2006.Today,2013istheseventhyearofthetypicalseven-yeareconomiccycle.We’realmostoutofthewoods.”Thewildcardmaybehowthenewtaxlawsimpacttheeconomyasthehigh-incomeearnerstargetedwithtaxincreasesalsoaccountforhalfofournation’sconsumerspending.Weareexpectingslowbutencouragingprogressinalloftheseareasin2013.Stutzercontinues,“Ifthingsgowell,then2013willberememberedastheeconomicyearthatsetthestageformuchbetteryearstocome.”

ARIZONA HEATS UP AlongwithNevada,Arizonawasgroundzeroforthehousingmeltdown,plaguedbyhighforeclosuresandhighunemploymentduring2006-2010.However,Arizonastagedastrongeconomiccomebackin2012,boastingthebesthousingmarketinthenation. “AsofSeptember2012,Arizonarankedfifthamongstatesforjobgrowth,andtheMetroPhoenixareawasfourthamonglargemetropolitanareas,”saysLeeMcPheters,ResearchProfessorandDirectoroftheJPMorganChaseEconomicOutlookCenterattheW.P.CareySchoolofBusiness.ThisisanextraordinaryimprovementfromArizona’slowpointin2009whenArizonafellfromanenviablejobgrowthrankingofsecondin2006,toadismal49thofthe50statesin2009.“Arizonaisexpectedtoadd60,000jobsin2013.Weshouldfinallydipbelow8%unemploymentin2013–downto7.6%.” Arizona’seconomicgrowthhashistoricallybeenstokedbyencouragingbusinessesandpeopletomovehere.Arizonaoffersadesirableclimate,affordablehousing,andagrowingbusinessenvironmentwithreasonablestatetaxrates.ArizonastandstobenefitfromCalifornia’srecentlyenactedProposition30whichraisesanalreadyhighstatesalestaxevenhigher,whilesignificantlyraisingincometaxesonindividualsmaking$250,000ormore.TheGreaterPhoenixEconomicCouncilhasdoubledtheireffortstoattractCaliforniabusinessesandtheiremployeestoArizona.ThesenewCaliforniataxlawchangesareexpectedtosignificantlyincreasepopulationflowstoArizona’sadvantage. ElliottD.Pollack,CEOoflocaleconomicconsultingfirmElliottD.PollackandCompany,notestheimportanceofmigration

toourstate.“Intheabsenceofthefiscalcliff,thingsshouldcontinuetoimproveoverthenextseveralyears.By2015,thingsshouldbenormalized.AsIliketosay,we’reonlyonedecentpopulation-flowyearawayfromtheissuebeingresolved.” MetroPhoenixhasrisenfromitshousingmeltdownwithencouragingjobgrowthledbyahousingboomthathasnowcausedaresidentialhousingshortage.Homebuildersaresteadilydustingofftheirequipmentandbuildinghomestomeetdemand.NewhomesalesinjectfreshlifeintotheArizonaeconomyandtaxbase.ThejourneytowardcontinuedeconomicgrowthandprosperityforArizonaseemstoonceagainbeheadingdownthefamiliarpathofbuildingandsellinghomestomeetincreasingdemand.

G E N E R A L E C O N O M I C S NA P S H OT

R E S I D E N T I A L R E A L E S TAT E

2013 ECONOMIC FORECASTS

GDPGROWTH2% growth in ’13,

about the same as last year. . .

INTERESTRATESLittleornoincrease

inshort-termratesin‘13. . .

BUSINESSSPENDINGAbouta4%gainin’13,

halfof‘12’space. . .

HOUSINGSALESUp8%,helpingGDPin’13

. . .TRADEDEFICIT

Wideningby2%in’13,afteraslightdipin’12

. . .UNEMPLOYMENT

Headingtoabout7.5%bytheendof‘13

. . .INFLATION

Slightlyhigherthisyear,2.3%. . .

ENERGYOiltradingat$90-$95/barrel

throughearlyspring. . .

RETAILSALES5%growthin’13

afterstrongholidaysales

Source:TheKiplingerLetter

ByMichaelOrr

ACTIVE LISTING COUNTSGreaterPhoenix-ARMLSResidential

SALES PER MONTHGreaterPhoenix-ARMLSResidential-MeasuredMonthly

MONTHLY AVERAGE SALES PRICE PER SQUARE FOOTGreaterPhoenix-ARMLSResidential

KELLY KARBON

VICKI KAPLAN

KELLY KARBON & VICKI KAPLANScottsdale ~ Paradise Valley ~ PhoenixFountain Hills ~ Cave Creek/Carefree

Vicki Kaplan and Kelly Karbon have earned

a reputation for professionalism, and integrity,

attention to detail and confidentiality. They are

considered consummate professionals.

Working with clients who desire a higher level

of service, knowledge, and experience in real estate

and believing no two clients are alike and every

home is unique, Vicki and Kelly take great pride

in offering concierge based services and innovative

options tailored to meet the individual needs,

wants and desires of their clients.

If you are in the market to sell or purchase luxury

real estate in Scottsdale, Paradise Valley,

Carefree/Cave Creek, Phoenix, or Fountain Hills,

call or email Vicki or Kelly for a confidential,

no-obligation consultation.

If your home is currently listed, this is not a solicitation for that listing. Produced by Desert Lifestyle Publishing • 480.460.0996 • www.DesertLifestyle.net

2012 Sales Statistics By CommunityP O P U L A R N E I G H B O R H O O D S I N S C OT T S D A L E

Community Average Days On List/Sell # Sales Price Market Price Ratio ClosedAncala .........................................$1,184,433 .................156 ..................96% ......................... 37Bellasera .........................................$511,496 ..................76 ...................97% ......................... 29Candlewood Estates .....................$762,778 .................149 ..................95% ......................... 18 DC Ranch ....................................$1,007,616 .................141 ..................95% ........................ 118Desert Highlands .........................$1,643,402 .................349 ..................90% ......................... 23Desert Mountain .........................$1,338,941 .................413 ..................89% ......................... 96Eagle Mountain ..............................$528,672 .................115 ..................97% ......................... 30Estancia .......................................$2,499,250 ................210 ..................80% .......................... 8FireRock .......................................$1,208,519 .................213 ..................92% ......................... 26Gainey Ranch ................................$794,150 .................220 ..................92% ......................... 30Grayhawk.......................................$572,259 ..................82 ...................96% ........................ 133Hidden Hills.....................................$617,407 .................126 ..................96% ......................... 28Ironwood Village ...........................$355,185 ..................85 ...................97% ......................... 32Legend Trail ....................................$567,455 .................128 ..................96% ......................... 60McCormick Ranch ........................$421,856 ..................82 ...................97% ......................... 63McDowell Mountain Ranch ..........$513,130 ..................73 ...................97% ........................ 205Mirabel ........................................$1,144,459 .................271 ..................92% ......................... 28Scottsdale Mountain .....................$607,771 .................141 ..................96% ......................... 52Scottsdale Ranch...........................$544,665 .................109 ..................95% ......................... 95Sincuidados ...................................$819,933 .................201 ..................95% ......................... 15Silverleaf ......................................$2,031,150 .................258 ..................92% ......................... 35Stonegate .......................................$521,957 ..................95 ...................97% ......................... 63Terravita ..........................................$458,572 .................147 ..................96% ........................ 103Troon North .....................................$749,227 .................171 ..................95% ......................... 97Troon Village ..................................$798,551 .................190 ..................94% ......................... 87Whisper Rock ..............................$1,748,375 .................236 ..................91% .......................... 8Winfield ...........................................$557,957 .................123 ..................96% ......................... 14

Statistics gathered from ARMLS. All information deemed reliable but not guaranteed. (Single-Family Residences)

2012 Average Sales Price By City

Statistics gathered from ARMLS. All information deemed reliable but not guaranteed. (Single-Family Residences)

Glendale

Phoenix

Mesa

Peoria

Litchfield Park

Tempe

Gilbert

Chandler

Cave Creek

Fountain Hills

Scottsdale

Carefree

Paradise Valley

$147,050

$169,964

$173,024

$363,245

$421,963

$512,231

$206,811

$213,566

$227,122

$194,483

$231,107

$694,947

$1,345,837

Glendale

Phoenix

Mesa

Peoria

Tempe

Gilbert

Litchfield Park

Chandler

Cave Creek

Fountain Hills

Scottsdale

Carefree

Paradise Valley

$117,597

$129,482

$139,952

$331,848

$405,408

$479,407

$682,714

$1,316,573

$190,588

$168,879

$194,236

$164,317

$199,320

2011 Average Sales Price By City