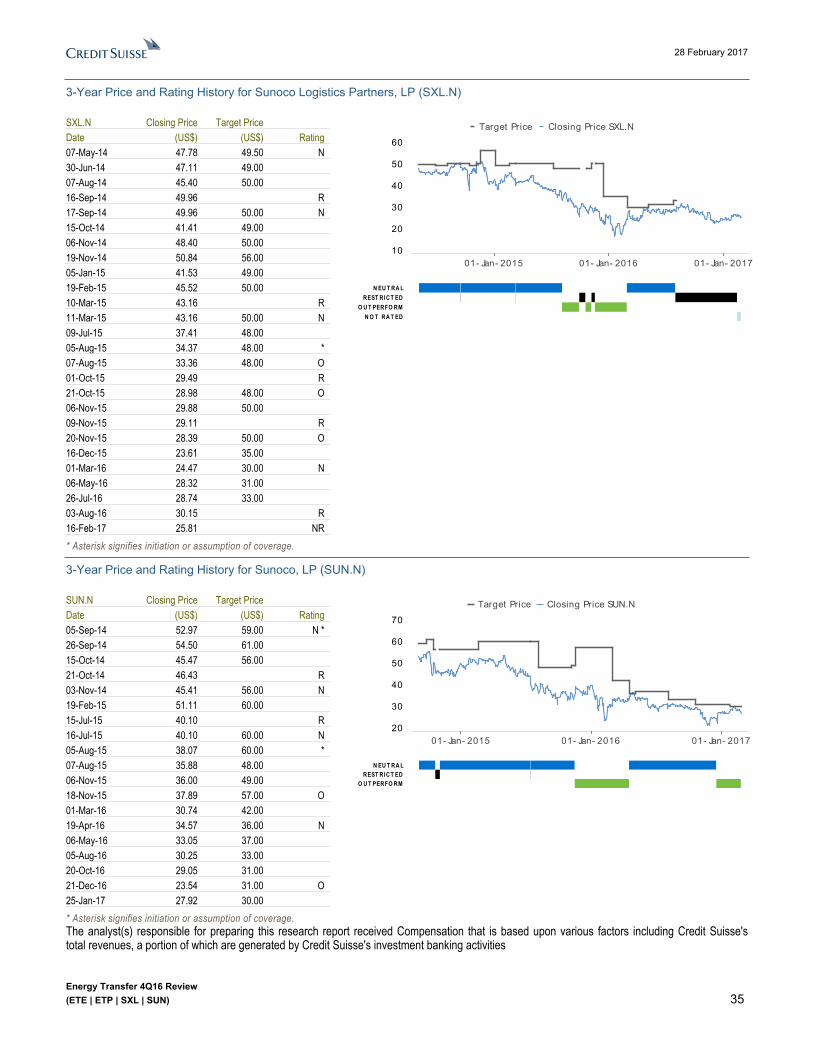

Merger Vote; Reinstating SXL with Outperform REINSTATEMENT ...

39

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 28 February 2017 Americas/United States Equity Research Master Limited Partnerships Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) REINSTATEMENT Research Analysts John Edwards, CFA 713 890 1594 [email protected] Bhavesh Lodaya 212 325 2337 [email protected] Dylan Nassano 212 325 8375 [email protected] Strong Momentum Going Into The SXL/ETP Merger Vote; Reinstating SXL with Outperform View From the Top: February 2017 has been an interesting month for the Energy Transfer franchise. Two mega growth projects in Rover and DAPL received their final regulatory approvals and SXL/ETP announced a slate of new growth projects signifying a bullish outlook for the group. Earlier this month, SXL announced the construction start-up of the 275 Mbpd Mariner East 2 and now expects the 250 Mbpd Mariner East 2 expansion to go on the floors post completion of the open season. Apart from these Marcellus focused projects, SXL also announced development of the 300 Mbpd Permian Express III. Keeping in theme with additional Permian basin takeaway projects announced recently by SXL’s competitors to take advantage of the 400-500 Mbpd of annual crude oil production growth out of the basin. This project will take SXL’s aggregate Permian takeaway capacity to 1 MMbpd. Separately, ETP announced a new 200 MMcf/d Arrowhead processing plant in Reeves county and a fifth 120 Mbpd Lone Star NGL fractionator along with related infrastructure. These announcements are expected to provide added impetus to the prospects of the combined SXL/ETP going into the April merger vote, showcasing the growth potential of the combined enterprise. ETE is expected to be a direct beneficiary of this underlying growth as the combined MLPs would be able to capture additional growth projects and derive synergistic benefits of the combined asset platform. In our view, the success of the merger would ultimately come down to mgmt.’s ability to execute on its growth initiatives, extract synergies and manage the balance sheet to protect the I/G rating. With respect to SUN, the focus clearly moves to disciplined and efficient operations in order to rationalize costs and balance distribution coverage and leverage. On simplification, which seems to be the flavor of the season, ETE did indicate that an eventual roll-up cannot be ruled out but is presently premature. Individual stock-specific takeaways are detailed below. ■ Reinstating Coverage of SXL with Outperform; Reiterating Outperform on ETE / ETP / SUN: After being restricted since the announcement of the DAPL stake sale (in August 2016), we are now reinstating coverage of SXL with a $31 TP and Outperform rating (~32% total return). We are raising our TP for ETE to $22 (from $20) and reiterate our $45 TP for ETP and $30 TP for SUN. We remain at an Outperform rating for the three stocks. Our current valuations for SXL and ETP are based on their standalone operations without giving any effect to the proposed merger. Per our SXL+ETP merger accretion math (details inside), we derive a $34 valuation for the combined entity (at the SXL level) implying ~44% NTM total return supportive of an Outperform rating for SXL (ETP is expected to merge into SXL with SXL being the surviving entity).

Transcript of Merger Vote; Reinstating SXL with Outperform REINSTATEMENT ...

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

28 February 2017Americas/United States

Equity ResearchMaster Limited Partnerships

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) REINSTATEMENTResearch Analysts

John Edwards, CFA713 890 1594

Bhavesh Lodaya212 325 2337

Dylan Nassano212 325 8375

Strong Momentum Going Into The SXL/ETP Merger Vote; Reinstating SXL with OutperformView From the Top: February 2017 has been an interesting month for the Energy Transfer franchise. Two mega growth projects in Rover and DAPL received their final regulatory approvals and SXL/ETP announced a slate of new growth projects signifying a bullish outlook for the group. Earlier this month, SXL announced the construction start-up of the 275 Mbpd Mariner East 2 and now expects the 250 Mbpd Mariner East 2 expansion to go on the floors post completion of the open season. Apart from these Marcellus focused projects, SXL also announced development of the 300 Mbpd Permian Express III. Keeping in theme with additional Permian basin takeaway projects announced recently by SXL’s competitors to take advantage of the 400-500 Mbpd of annual crude oil production growth out of the basin. This project will take SXL’s aggregate Permian takeaway capacity to 1 MMbpd. Separately, ETP announced a new 200 MMcf/d Arrowhead processing plant in Reeves county and a fifth 120 Mbpd Lone Star NGL fractionator along with related infrastructure. These announcements are expected to provide added impetus to the prospects of the combined SXL/ETP going into the April merger vote, showcasing the growth potential of the combined enterprise. ETE is expected to be a direct beneficiary of this underlying growth as the combined MLPs would be able to capture additional growth projects and derive synergistic benefits of the combined asset platform. In our view, the success of the merger would ultimately come down to mgmt.’s ability to execute on its growth initiatives, extract synergies and manage the balance sheet to protect the I/G rating. With respect to SUN, the focus clearly moves to disciplined and efficient operations in order to rationalize costs and balance distribution coverage and leverage. On simplification, which seems to be the flavor of the season, ETE did indicate that an eventual roll-up cannot be ruled out but is presently premature. Individual stock-specific takeaways are detailed below.■ Reinstating Coverage of SXL with Outperform; Reiterating Outperform

on ETE / ETP / SUN: After being restricted since the announcement of the DAPL stake sale (in August 2016), we are now reinstating coverage of SXL with a $31 TP and Outperform rating (~32% total return). We are raising our TP for ETE to $22 (from $20) and reiterate our $45 TP for ETP and $30 TP for SUN. We remain at an Outperform rating for the three stocks. Our current valuations for SXL and ETP are based on their standalone operations without giving any effect to the proposed merger. Per our SXL+ETP merger accretion math (details inside), we derive a $34 valuation for the combined entity (at the SXL level) implying ~44% NTM total return supportive of an Outperform rating for SXL (ETP is expected to merge into SXL with SXL being the surviving entity).

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 2

Stock-specific TakeawaysEnergy Transfer Equity (ETE)■ Earnings Debrief: ETE reported in line DCF of $299mm and it was positive to see

SG&A coming in substantially lower than prior quarters ($8mm for 4Q16 vs. $24mm/Q average for 9M16).

■ Estimates: Our net cash available for distribution forecasts for ETE move up by ~1%/2%/3% in 2017/18/19 driven by higher general partner distributions tied to higher equity issuance assumptions at ETP and SUN. We have not made any changes to our distribution forecasts for ETE and continue to expect distribution growth resumption in 2Q18.

■ Valuation: Our target price for ETE moves to $22 from $20, based on an equal weighted blend of P/DCF and 3-stage DDM. Our valuation implies a 23% upside supporting our Outperform rating on the stock.

Energy Transfer Partners (ETP)■ Earnings Debrief: ETP’s core business EBITDA of $960mm came in 4% below our

$999mm estimate, while overall EBITDA of $1,433mm was below us and the Street. This was primarily driven by weaker than expected performance of the midstream and interstate natural gas segments. ETP raised its 2017 growth capex guidance by ~$900mm to $2.8Bn, which reflects the addition of a fifth 120 Mbpd Lone Star fractionator with related infrastructure (September 2018 in service), a 200 MMcf/d Arrowhead natural gas processing plant (3Q17 in service) and full financing for the Rover pipeline. Frac 5 is fully subscribed by LT fee-based contracts. During 1Q17, ETP realized ~$1.8Bn of additional liquidity through the $1.2Bn proceeds from the Bakken pipeline stake sale and ~$570mm of equity issuance to ETE. Additional funding needs in 2017 are expected to be derived from ATM issuances and revolver borrowings. Rover pipeline – ETP has received 90% of tree clearing permits with the balance expected to be received this week. This should allow ETP to begin construction by March 1st and meet the July 2017 Phase 1 and November 2017 Phase 2 in service for the pipeline. Its 2017 capex budget includes full financing for the Rover pipeline and does not include any project financing. DAPL – the pipeline is 99% complete and ETP expects to place the pipe in service during 2Q17. ETP expects to start realizing full demand charges prior to June 1st from the project. With an open season currently underway, ETP is optimistic of contracting an additional 100 Mbpd on DAPL. Permian -- ETP’s midstream platform can realize 15-20% of volumetric growth driven by the ramp up in Permian production volumes. IDR Waivers -- During 2017, ETP benefits from $626mm in ETE IDR waivers before rolling off to $138mm/$128mm in 2018/19. The waivers during 2017 would be the highest for any fiscal year provided by ETE.

■ Estimates: Our EBITDA estimates move ~3%/2% lower in 2017/18, primarily driven by volumes which came in below forecast during Q4. We now model a full contribution from the Bakken pipeline (DAPL+ETCO) in 3Q17 and have added contribution from the Arrowhead plant and Frac 5 to our estimates. We have not made any changes to our distribution forecasts and continue to expect resumption of distribution growth beginning 1Q19, when leverage moves below 4.5x. We expect ETP to continue to make use of its ATM program and model $150mm of additional equity issuance in 2017 and $400mm/year in 2018/19. This would enable ETP to lower total debt leverage from ~5.5x in 4Q16, to 4.9x in 2017, 4.6x in 2018 and 4.4x in 2019. Higher than anticipated volumetric growth from additional Permian basin opportunities would move our EBITDA estimates higher and materially lower leverage to ~4x.

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 3

■ Valuation: We are reiterating our $45 target price and Outperform rating on ETP. Our target price implies ~31% NTM total return, above the median for our coverage group, supporting our Outperform rating. Our valuation is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM.

Sunoco Logistics Partners (SXL)■ Earnings Debrief: Although SXL reported earnings below the Street ($327mm vs.

$339mm), mgmt. provided insight into new growth projects that should drive ratable earnings growth. In October 2016, SXL fixed the cold box design issues at Mariner East 1 and was able to flow the full 70 Mbpd of capacity on the pipeline, up from 55 Mbpd in the prior quarters. SXL remains bullish on the prospects of US crude production out of the Permian and announced a new 300 Mbpd Permian Express III pipeline, which will take its aggregate Permian takeaway capacity to 1 MMbpd once complete. The pipeline is expected to come online in Phases with 100 Mbpd of Phase 1 capacity in mid-2017 and 200 Mbpd of Phase 2 capacity in 4Q18. SXL will be launching an open season for the pipeline in the next few months. SXL is well placed to capitalize on the incremental growth in the Permian following its JV with Exxon Mobil (XOM), that recently acquired 250,000 acres in the Delaware basin, close to SXL’s Delaware basin pipeline. SXL is XOM’s preferred midstream partner in the region. In order to cater to the growth in crude volumes, SXL plans to expand its Nederland terminal as well, that will include additional storage and dock enhancements. Other than the crude project, SXL confirmed it has enough commitments on the 250 Mbpd Mariner East 2 expansion project and we expect final details related to in-service timelines after completion of the ongoing open season for shipper commitments. The 275 Mbpd Mariner East 2 project received final permits and is under construction and expected to be complete in end-3Q17. This pipeline can be further expanded to 450 Mbpd. SXL would start deriving cash flows from DAPL in 2Q17 tied to its 15.30% stake. The $800mm cash infusion from the close of 49% of its stake in DAPL (was 30%) would enable SXL to de-lever and fund growth projects. ETE has provided SXL with an aggregate $60mm in IDR waivers, spread on a quarterly basis between 3Q16 through 2Q18.

■ Estimates: Coming off restriction we now expect SXL EBITDA of ~$1.65Bn/$1.95Bn/$2.2Bn in 2017/18/19, which includes the 3Q17 in service of the Mariner East 2 and Phase 1 of the Permian Express III projects. We forecast a 4Q18 in service for the Mariner East 2 expansion project. We expect SXL to grow distributions by ~10% annually and while SXL did not lay out capex guidance for 2017, we forecast total capex of ~$1.1Bn, including ~$84mm on maintenance. We forecast leverage of 4.3x/4.0x/3.8x for 2017/18/19 which includes 30%/70% equity and debt financing.

■ Valuation: We are reinstating coverage on SXL with a $31 target price and an Outperform rating, driven by ~32% NTM total return. Our valuation is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM.

Sunoco LP (SUN)■ Earnings Debrief: SUN’s $154mm 4Q16 EBITDA was substantially below us and the

Street. The weak 4Q performance was largely attributed to declining merchandise sales across its c-store footprint, although fuel sales/margins were ahead of estimates. Merchandise margins came in at 29.9% during 4Q16 vs. ~32% average during the year. Mgmt. attributed this to promotional activity at c-stores, which have now concluded and expect margins to move up to a more normalized 31-32%. Although SUN did not disclosed the actual promotional cost impact, we estimate this to be ~$10-12mm based on the merchandise gross profit during the quarter. While SUN has been

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 4

holding fuel market share among peers, mgmt. did acknowledge the fact that demand is expected to be flat going into 2017 and difficulties being faced by its stores in the oil producing regions of TX is expected to continue. This is primarily due to E&P efficiencies that requires lesser manpower than before negatively impacting customer counts at its C-stores. Mgmt.’s key initiatives during 2017 are focused on de-leveraging and distribution coverage management. These include ~$75mm in cost reductions, use of the $400mm ATM program, proceeds from sale of real estate (~100 C-stores/vacant land identified for sale), lower growth capex ($200mm target), lower maintenance capex than its $90mm target for 2017 and finally higher EBITDA from ~100 NTI sites opened since 2014. $27mm of the $75mm cost reduction includes $18mm in relocation costs and $9mm acquisition costs that would not appear in 2017. This leaves ~$48mm of costs to be eliminated during 2017. Growth capex during 2017 is expected to be spent on construction of just one NTI store and rebuilding/rebranding of stores along the Indiana toll road. While mgmt. has not specified the expected proceeds from the real estate sale, we expect it to generate ~$170-215mm. This is based on a 6-8x multiple on ~$0.35mm EBITDA per store (smaller than the newly developed ones) for the 65 C-stores and ~$1mm average assumed valuation for each of the 34 vacant properties. Our model assumes a 2Q sale at 7x for ~$193mm in proceeds ($350,000*65*7x) + ($1mm*34). SUN would be evaluating bids related to the sale over the next few weeks. With respect to sponsor support, ETE indicated that they remain open to supporting the growth at SUN but noted that the partnership had to work toward rationalizing its cost structure and operations.

■ Estimates: We continue to forecast normalized retail ($0.23-0.25/gal) and wholesale ($0.06-0.08/gal) margins. While our fuel volume and margin assumptions are relatively unchanged, our EBITDA forecasts move ~3% lower between 2017-19 due to 100bps lower merchandise margin estimates. We now forecast LT merchandise margins of 31.5% vs. 32.5%, based on mgmt.’s 31-32% guidance. Since, SUN indicated plans to make use of their $400mm ATM program, we now model ~$200mm of equity issuance in 2017, and $100mm/yr. in 2018/19. This should enable SUN to bring leverage down from 6.5x in 4Q16, to 5.5x in 2017, 5.1x in 2018 and 4.8x in 2019. We continue to forecast flat payouts at $0.8255/unit/Q for SUN due to the elevated leverage and do not foresee distribution growth until leverage moves to a 4-4.5x range in the long term.

■ Valuation: We are reiterating our $30 target price and Outperform rating on SUN. Our target price implies ~21% NTM total return, above the median for our coverage group, supporting our Outperform rating. Our valuation is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM.

SXL/ETP Merger Accretion MathSXL filed its second amendment to the S-4 a few weeks back. The record date for the merger has been set for 2/27, and mgmt. anticipates proxy to be mailed to unitholders in early March. The ETP unitholder vote and subsequent closure of merger is expected in mid-April. Per mgmt. integration teams are currently fully engaged in the integration, planning process, and are identifying cost and commercial synergies.

The accretion math, indicated below is based on our estimates for ETP and SXL.

■ Over the three years the merger is ~$0.75/unit or ~29% accretive to SXL unitholders and dilutive to ETE in year one (~10%) and year two (-6%) and ~3% accretive in year three. Importantly, the transaction consolidates the execution and funding of major Energy Transfer projects under one roof – Bakken pipeline, Rover pipeline, Revolution system and Mariner East 2/2X pipeline (~$6-8Bn combined capex for their share), all expected to be placed in service during 2017-18. This is expected to drive annual synergies of ~$200mm/yr. for the combination by 2019.

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 5

■ The combined pre-deal leverage improves from 4.9/4.6/4.4x (2017-19) to 4.9/4.3/4.0x post-merger with improvement from synergies and lower cost of equity financing (SXL yields ~8% vs. ~11% for ETP). We model 50% debt and equity financing for ETP related capex at the SXL level post the merger.

■ Post deal SXL’s total unit count is estimated to move up to ~1.1Bn, which includes the retirement of 67.1mm SXL units currently owned by ETP. We estimate distribution coverage of ~1.3x (year 2 post deal) vs. ~1.06x for SXL and ~1.03x for ETP based on our current estimates.

Figure 1: SXL ETP Merger Accretion

SXL Buys ETP Annual Accretion / (Dilution) 2017E 2018E 2019EETP common units o/s (mm) 551.6 DCF/unit $2.31 $2.60 $2.83SXL units o/s (mm) excl. Class B 332.4 LP Distribution per Unit $2.23 $2.47 $2.71ETP to SXL conversion ratio 1.50x %y/y growth 10% 11% 10%= New SXL units issued 827.3 GP Distribution per Unit $1.50 $1.78 $2.07- SXL units owned by ETP (retired) 67.1 Incremental LP Dist (adj. for retired units) $1,815 $1,934 $2,102= SXL units o/s (mm) 1,092.6 Incremental GP Dist (adj. for retired units) $1,220 $1,397 $1,602

SXL unit price (30-day avg VWAP) $26.52 ETP capex $2,800 $1,200 $800SXL unit price (Nov 18 2016 close) $26.19 Debt funded $1,400 $600 $400SXL yield (Nov 18 2016 close) 7.9% Equity funded ($mm) $1,400 $600 $400

Equity funded (mm units) 53.5 22.9 15.3ETP unit price (30-day avg VWAP) $36.13 Effective SXL units o/s 1,146.1 1,169.0 1,184.3ETP unit price (Nov 18 2016 close) $39.37ETP yield (Nov 18 2016 close) 10.7% ETP EBITDA $4,974 $5,620 $5,888

Effective multiple 9.3x 8.2x 7.8x= Effective ETP takeout price $39.29 - Maintenance Capex (ETP) $345 $355 $365Premium / discount (30-day avg) 8.7% = DCF (before financing) $4,629 $5,265 $5,523

Conversion ratio (30-day avg VWAP) 1.36x - Incremental Interest Expense (ETP debt) $1,159 $1,159 $1,159Premium / discount (Nov 18 2016 close) -0.2% - Incremental Interest Expense (new debt) $67 $29 $19

Conversion ratio (Nov 18 2016 close) 1.50x - Incremental LP Dist (adj. for retired units) $1,815 $1,934 $2,102- Incremental GP Dist (adj. for retired units) $1,220 $1,397 $1,602

= ETP equity value ($mm) $21,668 + Synergies ($200mm by 2019) $100 $150 $200ETP market cap (current) $20,464 + ETP DCF from unconsol affiliates $420 $420 $420

+ ETP IDR waivers flowing to SXL $626 $138 $128ETP Debt o/s (standalone) $24,403 + PTXP LP+GP distributions $34 $40 $46ETP Takeout EV $46,071 = Accretion / (Dilution) $1,548 $1,493 $1,435

ETP Capex Funding - GP Share of Accretion / (Dilution) $622 $626 $621% Debt Financed 50% GP Splits 40% 42% 43%% Equity Financed 50% = LP Accretion / (Dilution) $926 $867 $814Rate of interest 4.75%SXL unit issue price $26.19 = $ Accretion / (Dilution) per unit $0.81 $0.74 $0.69

= DCF % Accretion / (Dilution) per unit 34.9% 28.5% 24.3%DCF per unit (post deal) $3.12 $3.34 $3.52

SXL Accretion Analysis

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 6

Figure 2: Post deal leverage and distribution metrics for SXL

Figure 3: Change in LP cash distributions for ETP unitholders

Leverage Metrics 2017E 2018E 2019ESXL pre-deal EBITDA $1,648 $1,948 $2,198+ EBITDA from ETP acquisition $4,974 $5,620 $5,888SXL post-deal EBITDA $6,622 $7,568 $8,086

SXL Debt $7,157 $7,806 $7,821+ Debt from ETP acquistion $24,403 $24,403 $24,403+ ETP capex debt $1,400 $600 $400SXL post-deal Debt $32,960 $32,809 $32,624

Post Deal Leverage 4.9x 4.3x 4.0xPre Deal (SXL) 4.3x 4.0x 3.8xPre Deal (ETP standalone) 4.7x 4.4x 4.3xPre Deal (ETP + SXL) 4.9x 4.6x 4.4x

Distribution Coverage Metrics 2017E 2018E 2019ESXL DCF pre-deal $1,341 $1,621 $1,847SXL Distributions pre-deal $1,283 $1,527 $1,755SXL distribution coverage pre-deal 1.04x 1.06x 1.05xETP distribution coverage pre-deal 1.01x 1.03x 1.05x

SXL DCF post deal $5,298 $6,308 $6,857SXL Distributions post deal $3,692 $4,721 $5,331SXL + ETP combined post deal 1.43x 1.34x 1.29x

Distributions to ETP unitholders 2017E 2018E 2019EPre DealETP units o/s 551.6 551.6 551.6ETP unitholder Dist/unit $4.22 $4.22 $4.32ETP unitholder Distributions $2,328 $2,328 $2,383

Post DealSXL units issued in lieu of ETP units 827.3 827.3 827.3SXL unitholder Distribution/unit $2.23 $2.47 $2.71SXL unitholder Distributions $1,845 $2,043 $2,242Distributions Increase / (Decrease) -$483 -$284 -$141% Downside -21% -12% -6%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 7

ETE Accretion MathFigure 4: SXL ETP Merger Accretion – Impact to ETE Unitholders

ETP / SXL Ownership Annual Accretion / (Dilution) 2017E 2018E 2019EPre-deal ETP units owned 18.4 ETE DCF/LP unit $1.27 $1.73 $1.91

ETE Distribution / unit $1.14 $1.26 $1.58Pre-deal SXL units owned 0.0 ETP Distribution / unit $4.22 $4.22 $4.32Post-deal SXL units owned 27.6 SXL Distribution / unit $2.23 $2.47 $2.71

ETE units o/s (2017) 1,079.2 ETE AccretionETE units o/s (2018 and beyond) 1,158.2 Pre-deal DCF $1,368 $2,003 $2,208

ETP LP distributions $78 $78 $79ETP GP distributions $896 $1,405 $1,498ETP Class H (90% of SXL GP) $464 $576 $683- ETP cash flow prior to deal $1,438 $2,059 $2,260

SXL LP distributions $61 $68 $75100% SXL GP distrbutions (existing units) $516 $640 $759Incremental SXL GP Distributions (from deal) $1,220 $1,397 $1,602- ETP IDR waivers $626 $138 $128+ SXL cash flow post deal $1,172 $1,968 $2,308

= Post-deal DCF $1,103 $1,912 $2,255DCF per unit (post deal) $1.02 $1.65 $1.95

= $ Accretion / (Dilution) -$266 -$91 $47= DCF $ Accretion / (Dilution) per unit -$0.25 -$0.08 $0.04= DCF % Accretion / (Dilution) per unit -21.6% -6.2% 2.6%

Distribution Coverage Metrics 2017E 2018E 2019EETE distribution coverage pre-deal 1.36x 1.45x 1.20xETE distribution coverage post deal 0.90x 1.31x 1.23x

ETE Accretion Analysis

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 8

Implied Valuation for the Combined Entity

Figure 5: SXL Valuation post-Merger2019E Multiple EV

EBITDA Low Base High Low Base HighEV/EBITDA 8,086 10.5x 11.5x 12.5x 84,902 92,988 101,074Less: 2019 Net Debt 32,624 32,624 32,624Total Equity Value 52,278 60,364 68,450

Units TPAdd: SUN ownership 43.5 $30 1,305 1,305 1,305Net Equity Value 53,583 61,669 69,755SXL LP Take % 57% 57% 57%Units O/S 1,184 1,184 1,184Price/Unit - 2019 $26 $30 $33Discount Factor 0.84Price/Unit - NTM $22 $25 $28

2019E MultipleDCF/unit Low Base High Low Base High

Price/DCF $3.52 11.0x 12.0x 13.0x $39 $42 $46Discount Factor 0.84Price/Unit - NTM $33 $36 $39

Discount RateLow Base High Low Base High

3-Stage DDM 10.0% 9.0% 8.0% $38 $43 $50

Average Target Price - SXL+ ETP combined $31 $34 $39Distribution/unit (12-mo out) $2.32Yield (12-mo out) 6.8%Current Price $25.27Total Return (NTM) 44%

Metric

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 9

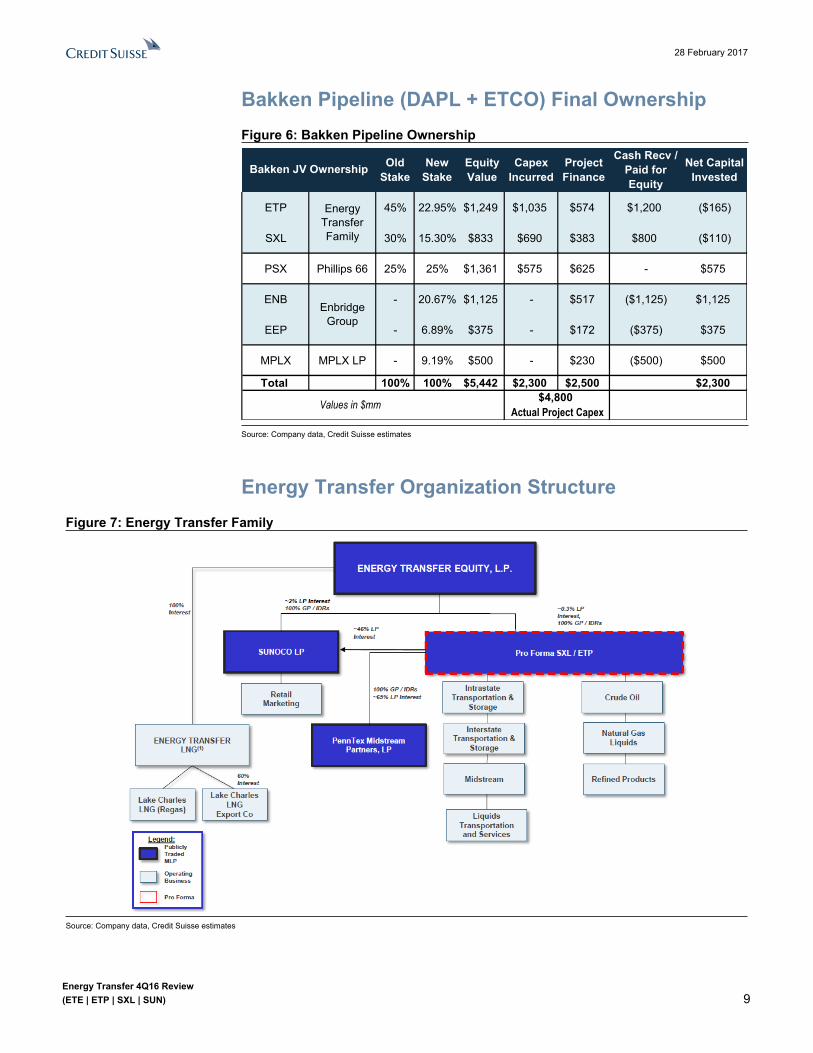

Bakken Pipeline (DAPL + ETCO) Final OwnershipFigure 6: Bakken Pipeline Ownership

Old Stake

New Stake

Equity Value

Capex Incurred

Project Finance

Cash Recv / Paid for Equity

Net Capital Invested

ETP 45% 22.95% $1,249 $1,035 $574 $1,200 ($165)

SXL 30% 15.30% $833 $690 $383 $800 ($110)

PSX Phillips 66 25% 25% $1,361 $575 $625 - $575

ENB - 20.67% $1,125 - $517 ($1,125) $1,125

EEP - 6.89% $375 - $172 ($375) $375

MPLX MPLX LP - 9.19% $500 - $230 ($500) $500

Total 100% 100% $5,442 $2,300 $2,500 $2,300

Energy Transfer Family

Bakken JV Ownership

Enbridge Group

$4,800Values in $mm Actual Project Capex

Source: Company data, Credit Suisse estimates

Energy Transfer Organization StructureFigure 7: Energy Transfer Family

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 10

Americas/United StatesMaster Limited Partnerships

Energy Transfer Equity, LP (ETE)Rating OUTPERFORM [V]Price (27-Feb-17, US$) 18.96Target price (US$) (from 20.00) 22.0052-week price range (US$) 19.86 - 6.45Market cap (US$ m) 19,850.12Adjusted EV -Target price is for 12 months.[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

John Edwards, CFA713 890 1594

Bhavesh Lodaya212 325 2337

Dylan Nassano212 325 8375

Raising TP to $22; Reiterate Outperform■ Investment Thesis: ETE has four sources of cash flow: (1) LP + GP

distributions from ETP; (2) 90% of SXL GP + IDRs via ETP Class H units; (1) LP + GP distributions from SUN; (4) 100% ownership of the Lake Charles terminal business. ETP accounts for the majority of ETE’s DCF.

■ Estimates: Our net cash available for distribution forecasts for ETE move up by ~1%/2%/3% in 2017/18/19 driven by higher general partner distributions tied to higher equity issuance assumptions at ETP and SUN. We have not made any changes to our distribution forecasts for ETE and continue to expect distribution growth resumption in 2Q18.

■ Valuation: Our target price for ETE moves to $22 from $20, based on an equal weighted blend of P/DCF and 3-stage DDM. Our valuation implies a 23% upside supporting our Outperform rating on the stock.

■ Risks: Risks include subsidiary business risks, extension of IDR waivers, tax treatment of MLPs, Liquefaction Project Risks, volumetric slowdown resulting from a commodity price downturn and access and cost of capital.

Share price performance

ET E.N S& P 5 0 0 IN D EX

A p r - 1 6 Ju l - 1 6 O ct - 1 6 Jan - 1 75

1 0

1 5

2 0

On 27-Feb-2017 the S&P 500 INDEX closed at 2370.1Daily Feb26, 2016 - Feb27, 2017, 02/26/16 = US$6.81

DCF/LP Unit Q1 Q2 Q3 Q42016A 0.33 0.26 0.27 0.292017E 0.31 0.31 0.32 0.322018E 0.45 0.43 0.44 0.45

Financial and valuation metricsYear 12/16A 12/17E 12/18E 12/19EEBITDA (US$ m) 3,634 6,257 6,856 7,386Distribution/unit- DPU (US$ m) 1.14 1.14 1.26 1.58Earnings/unit - EPU (US$) 0.91 0.98 1.18 1.38Prev. Earnings/unit - EPU (US$) 0.97 1.33 1.54 1.67EPU - consensus (US$) 0.99 1.15 1.61 1.54Distribution coverage (x) 1.24 1.36 1.45 1.20P/DCF (x) 16.8 15.0 11.0 9.9Adj. current EV/EBITDA (x) - - - -

DPU (US$) 1.14 Distribution yld (%) 6.0Units outstanding (m) 1,047 GP take (%) -Net debt current (US$ m) 41,355.9 Net debt/EBITDA (x) -6-month ADV (000's) 1,419 Net debt/market cap. (%) -Free float (%) 72 Institutional ownership (%) -Source: Company data, Thomson Reuters, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 11

Energy Transfer Equity, LP (ETE)Price (27 Feb 2017): US$18.96; Rating: OUTPERFORM [V]; Target Price: (from US$20.00) US$22.00; Analyst: John EdwardsMLP Distributable Cash Flow (DCF)

12/16A 12/17E 12/18E 12/19E

Adjusted EBITDA 3,633.8 6,256.5 6,855.8 7,386.3(-) Maintenance Capex - - - -(-) Cash Interest Expenses 1,832.0 1,887.2 1,956.1 1,981.4(+/-) Other Adjustments 595.7 3,000.8 2,896.5 3,197.1Total Distributable Cash Flow (US$) 1,206.1 1,368.5 2,003.1 2,207.8(-) General Partner Adjustments 0.0 0.0 0.0 0.0DCF to limited partners 1,206.07 1,368.49 2,003.11 2,207.80DCF per LP unit (US$) 1.15 1.27 1.73 1.91Cash Distribution Declared Per Unit (US$)Distribution coverage (x) 1.24 1.36 1.45 1.20DCF/LP Unit Q1 Q2 Q3 Q42016A 0.33 0.26 0.27 0.292017E 0.31 0.31 0.32 0.322018E 0.45 0.43 0.44 0.45Capex 12/16A 12/17E 12/18E 12/19EExpansion Capex - - - -Acquisitions (1,570.0) .0 .0 .0Maintenance capex - - - -Cash Flow 12/16A 12/17E 12/18E 12/19ENet income (US$) 758.8 1,058.3 1,329.0 1,599.6DD&A 2,359.0 2,712.3 2,779.9 2,822.8Change in working capital (61.0) .0 .0 .0Other cash & non-cash items 2,203.2 787.4 739.8 711.2Cash flow from operations 3,417.0 4,331.6 4,815.7 5,274.7Free cashflow to the firm (4,675.0) 986.6 3,100.7 3,949.7Other investment/(outflows) 152.0 116.0 116.0 116.0Cash flow from investments (9,467.0) (3,229.0) (1,599.0) (1,209.0)Net share issue/(repurchase) - - - -Dividends paid (1,022.0) (1,003.7) (1,233.6) (1,750.3)Change in debt 6,657.0 1,737.2 282.9 (49.4)Other financing inflows/outflows 292.0 (1,836.0) (2,266.0) (2,266.0)Cashflow from financing activities 5,927.0 (1,102.6) (3,216.7) (4,065.7)Movements in cash/eq. (123.0) (.0) .0 .0Balance Sheet (US$) 12/16A 12/17E 12/18E 12/19EAssetsCash & cash equivalents 483.0 483.0 483.0 483.0Account receivables 3,604.0 3,604.0 3,604.0 3,604.0Other current assets 607.0 607.0 607.0 607.0Total current assets 6,985.0 6,985.0 6,985.0 6,985.0Total fixed assets 55,438.0 54,347.2 52,978.6 51,190.8Other assets 3,858.0 3,858.0 3,858.0 3,858.0Total assets 79,011.0 77,920.2 76,551.6 74,763.8LiabilitiesAccounts payables 3,544.0 3,544.0 3,544.0 3,544.0Short-term debt .0 .0 .0 .0Other short term liabilities 3,733.0 3,733.0 3,733.0 3,733.0Total current liabilities 7,277.0 7,277.0 7,277.0 7,277.0Long-term debt 42,608.0 43,763.0 44,880.0 45,804.6Other liabilities 6,609.0 6,240.6 5,583.1 4,932.2Total liabilities 56,494.0 57,280.6 57,740.1 58,013.8Minority interests / other 24,211.0 22,029.9 19,994.6 18,105.0Total liabilities and equity 79,011.0 77,920.2 76,551.6 74,763.8Financing Metrics 12/16A 12/17E 12/18E 12/19EEquity issuance - - - -Debt issuance/(repayment) 6,657.0 1,737.2 282.9 (49.4)Leverage (x) - - - -Per share 12/16A 12/17E 12/18E 12/19ENo. of shares (EOP) 1,046 1,075 1,129 1,158Earnings / unit EPU (US$) 0.91 0.98 1.18 1.38DPS (US$) 1.14 1.14 1.26 1.58Book value per share (1.62) (1.29) (1.05) (1.17)Operating cash flow/share 3.27 4.03 4.27 4.55Valuation metrics 12/16A 12/17E 12/18E 12/19EDiv yield (%) 6.0 6.0 6.6 8.3FCF yield (%) (23.2) 4.8 14.5 18.0EV/EBITDA (x) 17.1 10.2 9.6 9.1P/E (x) 20.7 19.3 16.1 13.7Price to book (x) (11.7) (14.7) (18.1) (16.2)Credit ratios 12/16A 12/17E 12/18E 12/19ENet debt/equity (%) 187.1 209.7 236.0 270.6Interest coverage ratio (X) 0.7 1.9 2.1 2.3Dividend payout ratio (%) (10.2) (10.0) (12.3) (17.5)

Company BackgroundEnergy Transfer Equity, L.P. (ETE) is a limited partnership company. The Company has two segments: Investment in ETP and Investment in Regency. ETP injects and holds natural gas in its Bammel storage facility

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 25.00Our blue sky valuation assumes 1.0x higher P/DCF multiples relative to base case and 100bps lower discount rate relative to the base case 3-stage DDM methodology.

Our Grey Sky Scenario (US$) 13.00Our grey sky valuation assumes 1.0x lower P/DCF multiples relative to base case and 100bps higher discount rate relative to the base case 3-stage DDM methodology. Our valuation also takes into account flat distribution payouts and grey sky case for underlying subsidiaries and flat distributions at ETE.

Share price performance

ET E.N S& P 5 0 0 IN D EX

A p r - 1 6 Ju l - 1 6 O ct - 1 6 Jan - 1 75

1 0

1 5

2 0

On 27-Feb-2017 the S&P 500 INDEX closed at 2370.1Daily Feb26, 2016 - Feb27, 2017, 02/26/16 = US$6.81

Source: Company data, Thomson Reuters, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 12

ETE ValuationOur $22 target price is based on an equal weighted blend P/DCF and 3-stage DDM. Our TP implies ~23% NTM total returns, supporting our Outperform rating on the stock

Figure 8: ETE Blended Valuation2018E Multiple

DCF/unit Low Base High Low Base HighPrice/DCF $1.73 9.0x 10.0x 11.0x $16 $17 $19

Discount RateLow Base High Low Base High

3-Stage DDM 10.5% 9.5% 8.5% $24 $27 $32

Average Target Price $20 $22 $25Distribution/unit (12-mo out) $1.14Yield (12-mo out) 5.2%Current Price $18.87Total Return (NTM) 23%

Source: Company data, Credit Suisse estimates

ETE Changes to EstimatesFigure 9: ETE Estimates Yr ending December 31($ millions, except per unit data)

1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019E 1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019EEPU $0.27 $0.32 $0.36 $0.39 $1.33 $1.54 $1.67 $0.18 $0.24 $0.27 $0.28 $0.98 $1.18 $1.38Average Units Outstanding 1,063 1,079 1,079 1,079 1,075 1,129 1,158 1,063 1,079 1,079 1,079 1,075 1,129 1,158

Cash Available for Dividends (DCF)Distributions from ETP

Limited Partner interest 19 19 19 19 78 78 79 19 19 19 19 78 78 79ETP Class H units (SXL 90.05% GP interest) 103 108 117 122 450 556 653 106 112 120 126 464 576 683General Partner interest +IDRs 234 229 227 217 907 1,394 1,477 230 225 225 216 896 1,405 1,498

Distributions from SUNLimited Partner interest 2 2 2 2 7 7 7 2 2 2 2 7 7 7General Partner interest +IDRs 20 20 20 20 81 81 83 21 22 22 22 88 92 94

Lake Charles LNG 45 45 45 45 180 180 180 45 46 45 46 182 182 182Gross Cash Available for Distributions 423 423 431 426 1,703 2,296 2,480 423 426 434 432 1,715 2,340 2,544SG&A Expenses, ex non-cash compensation expense 10 10 10 10 40 40 40 10 10 10 10 40 40 40Management incentive fee 0 0 0 0 0 0 0 0 0 0 0 0 0 0Interest expense, net of amortization 77 73 72 72 294 284 288 77 77 76 76 306 297 296Other expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0Net Cash Available for Distributions 336 340 348 344 1,369 1,973 2,151 336 339 347 346 1,368 2,003 2,208

Net Cash Available for Distributions per unit $0.31 $0.32 $0.32 $0.32 $1.27 $1.70 $1.86 $0.31 $0.31 $0.32 $0.32 $1.27 $1.73 $1.91

Cash Distribution Declared Per Unit $0.29 $0.29 $0.29 $0.29 $1.14 $1.26 $1.58 $0.29 $0.29 $0.29 $0.29 $1.14 $1.26 $1.58

Distribution Coverage (Total DCF/Total Distribution Declared) 1.34x 1.36x 1.39x 1.37x 1.36x 1.43x 1.17x 1.34x 1.35x 1.38x 1.38x 1.36x 1.45x 1.20x

Old Estimates New Estimates

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 13

ETE Risks■ Subsidiary Business Risks – ETE derives its cash flows from ownership of LP + GP

interests in ETP and SUN and ownership of GP interests in SXL. Any difficulties that affect the normal course of business at ETP/SXL/SUN will directly impact their distribution growth ability.

■ Project or financing delays - Further delays in growth project financing and execution at any of ETE’s underlying MLPs will limit their distribution growth potential. This will reduce cash flows for ETE and limit its distribution growth.

■ Extension of IDR Waivers – Currently, ETE provides IDR waivers only to ETP and SXL, which enables ETP/SXL to maintain distributions. Although, this results in a stable cash flow profile for ETE, it ultimately limits distribution growth at ETE. Any extension of waivers to ETP/SXL or provision of new IDR waivers to SUN will reduce distributable cash flow at ETE.

■ Liquefaction Project Risks – The next leg of growth at ETE is expected to be driven by the development of the Lake Charles LNG Liquefaction facility, in which ETE owns 60%. The project is expected to achieve FID in 2017 with first LNG production in 2021. We estimate this project to accrue ~$5/unit in value to ETE unitholders in 2021, though

we do not factor this in our estimated valuation. However, any delays in receipt of approvals or delays in execution will delay the realization of cash flows from the LNG business. Also, any changes in global LNG supply/demand fundamentals by the time the project is placed into service in 2020 could affect the economics of the project. Global LNG supply is expected to peak by the end of the decade.

■ Un-Simplified Cash Flow Source – Although, ETE and its subsidiaries operate within the broader MLP/GP structure, ETE does not operate as pure-play GP and its cash flow is derived from a web of intra company holdings within the Energy Transfer family. Due to this structure, ETE is not fully understood by the market. For example: (1) ETP owns the GP of SXL but accrues only 10% of GP cash flows. The balance 90% flows through ETE, which was made possible through issuance of a new class of ETP units held by ETE. (2) SUN is structured as an MLP but derives ~55% of EBITDA from retail operations which does not qualify as MLP income. SUN is able to stay as an MLP and keep taxes at a minimal level due to the PropCo structure which consolidates the retail c-stores business. Tax Treatment Of Underlying MLPs – ETP/SXL/SUN’s ability to pay distributions may be hindered should the tax treatment of MLPs be changed. Although the discussion of taxing MLPs arises from time to time, we view such an event as a low probability.

■ Commodity Price Risk: Like most of mid-stream there is a strong correlation between valuation multiples and the price of crude, particularly to the downside. With the collapse of talks at the OPEC technical conference a couple of weeks ago, there is significantly less confidence in a deal coming out of the upcoming Nov 30 meeting with respect to help contain global oversupply of crude, which could continue to put downward pressure on the price of crude. In turn, given the correlation of valuation multiples to crude in the midstream including members of the Energy Transfer family, there could be downward pressure on the valuation, negatively impacting the ability of Energy Transfer family members achieving their respective Target Prices over the next 12 months.

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 14

ETE 4Q16 Earnings4Q16 In Line Adjusting for ETE Units Issuance and ETP Units Purchase Prior to Declaration of Distribution for 4Q16■ DCF In Line with CS: Net cash available for distribution of $299mm came in slightly

below our $308mm estimate (adj.) and included an $8mm transaction expense. We have adjusted our DCF calculation to give effect to the ~32mm units issued by ETE and the consequent purchase of ~15.8mm units of ETP. These transactions were done prior to record date of 4Q distributions which had an impact on the quarter’s DCF.

■ Distribution of $0.285/unit was in line with us and the Street.

Figure 10: ETE 4Q16 VarianceYr ending December 31($ millions, except per unit data) 4Q16 4Q16 CS Diff Diff (%) 4Q15 Y/Y (%)

Actual Estimate ActualEPU $0.26 $0.26 $0.00 0% $0.30 -13%Average Units Outstanding 1,047 1,047 (0) 0% 1,054 -1%

Cash Available for Dividends (DCF)Distributions from ETP

Limited Partner interest 20 19 1 7% 3 567%ETP Class H units (SXL 90.05% GP interest) 94 97 (3) -3% 77 22%General Partner interest +IDRs 221 235 (14) -6% 304 -27%

Distributions from SUNLimited Partner interest 2 2 0 0% 0 NMGeneral Partner interest +IDRs 20 20 0 0% 17 20%

Lake Charles LNG 46 45 1 2% 49 -6%Gross Cash Available for Distributions 403 418 (15) -4% 450 -10%SG&A Expenses, ex non-cash compensation expense 8 10 (2) -20% 12 -33%Management incentive fee 24 23 1 4% 24 0%Interest expense, net of amortization 80 77 3 3% 75 7%Other expenses 8 0 8 NM 4 100%Net Cash Available for Distributions 299 308 (8) -3% 343 -13%

Net Cash Available for Distributions per unit $0.29 $0.28 $0.01 3% $0.33 -13%

Cash Distribution Declared Per Unit $0.285 $0.285 $0.00 0% $0.29 0%

Distribution Coverage (Total DCF/Total Distribution Declared) 1.19x 1.21x -0.01x -1% 1.15x 4%Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 15

Americas/United StatesMaster Limited Partnerships

Energy Transfer Partners, LP (ETP)Rating OUTPERFORMPrice (27-Feb-17, US$) 37.68Target price (US$) 45.0052-week price range (US$) 42.85 - 26.40Market cap (US$ m) 20,447.74Adjusted EV -Target price is for 12 months.

Research Analysts

John Edwards, CFA713 890 1594

Bhavesh Lodaya212 325 2337

Dylan Nassano212 325 8375

Reiterate $45 TP and Outperform■ Investment Thesis: ETP is largest MLP under the ET Umbrella with ~46%

stake in SUN and owns SXL's GP and ~24% LP interest in SXL. We expect ETP distributions to stay flat through 2018, as it builds coverage and de-levers to ~4.5x while placing its ~$9Bn of projects in service through end-2017. The current set of IDR waivers provided by ETE expires in 2019.

■ Estimates: Our EBITDA estimates move ~3%/2% lower in 2017/18, primarily driven by volumes which came in below forecast during Q4. We now model a full contribution from the Bakken pipeline (DAPL+ETCO) in 3Q17 and have added contribution from the Arrowhead plant and Frac 5 to our estimates. We have not made any changes to our distribution forecasts and continue to expect resumption of distribution growth beginning 1Q19, when leverage moves below 4.5x. We expect ETP to continue to make use of its ATM program and model $150mm of additional equity issuance in 2017 and $400mm/year in 2018/19. This would enable ETP to lower total debt leverage from ~5.5x in 4Q16, to 4.9x in 2017, 4.6x in 2018 and 4.4x in 2019. Higher than anticipated volumetric growth from additional Permian basin opportunities would move our EBITDA estimates higher and materially lower leverage to ~4x.

■ Valuation: We are reiterating our $45 target price and Outperform rating on ETP. Our target price implies ~31% NTM total return, above the median for our coverage group, supporting our Outperform rating. Our valuation is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM.

■ Risks: Risks include delay in growth projects, high leverage, ETE IDR waivers expiration in 2019, tax treatment of MLPs, slower SXL and SUN distribution growth and access and cost of capital.

Share price performance

ET P.N S& P 5 0 0 IN D EX

A p r - 1 6 Ju l - 1 6 O ct - 1 6 Jan - 1 72 5

3 0

3 5

4 0

4 5

On 27-Feb-2017 the S&P 500 INDEX closed at 2370.1Daily Feb26, 2016 - Feb27, 2017, 02/26/16 = US$26.62

DCF/LP Unit Q1 Q2 Q3 Q42016A 0.79 0.87 0.77 0.912017E 0.83 0.96 1.20 1.352018E 1.06 1.09 1.15 1.15

Financial and valuation metricsYear 12/16A 12/17E 12/18E 12/19EEBITDA (US$ m) 5,605 6,622 7,568 8,086Distribution/unit- DPU (US$ m) 4.22 4.22 4.22 4.32Earnings/unit - EPU (US$) -2.01 0.76 0.96 1.39Prev. Earnings/unit - EPU (US$) (0.53) 1.29 1.62 1.70EPU - consensus (US$) -0.39 1.63 2.42 1.71Distribution coverage (x) 0.86 1.01 1.03 1.05P/DCF (x) 10.7 8.7 8.5 8.0Adj. current EV/EBITDA (x) - - - -

DPU (US$) 4.22 Distribution yld (%) 11.2Units outstanding (m) 543 GP take (%) 31.2Net debt current (US$ m) 30,683.4 Net debt/EBITDA (x) 5.76-month ADV (000's) 825 Net debt/market cap. (%) -Free float (%) 106 Institutional ownership (%) -Source: Company data, Thomson Reuters, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 16

Energy Transfer Partners, LP (ETP)Price (27 Feb 2017): US$37.68; Rating: OUTPERFORM; Target Price: US$45.00; Analyst: John EdwardsMLP Distributable Cash Flow (DCF)

12/16A 12/17E 12/18E 12/19E

Adjusted EBITDA 5,605.0 6,621.8 7,567.8 8,085.9(-) Maintenance Capex (368.0) (427.4) (452.4) (474.9)(-) Cash Interest Expenses 1,317.0 1,377.7 1,462.3 1,489.7(+/-) Other Adjustments 410.0 351.5 333.2 328.7Total Distributable Cash Flow (US$) 3,510.0 4,465.2 5,320.0 5,792.6(-) General Partner Adjustments 1817.5 2074.5 2830.8 3116.9DCF to limited partners 1,692.47 2,390.66 2,489.17 2,675.70DCF per LP unit (US$) 3.34 4.34 4.44 4.70Cash Distribution Declared Per Unit (US$)

3.18 2.77 3.72 3.78Distribution coverage (x) .86 1.01 1.03 1.05DCF/LP Unit Q1 Q2 Q3 Q42016A 0.79 0.87 0.77 0.912017E 0.83 0.96 1.20 1.352018E 1.06 1.09 1.15 1.15Capex 12/16A 12/17E 12/18E 12/19EExpansion Capex (7,182.0) (2,717.6) (1,102.6) (690.1)Acquisitions (1,227.0) .0 .0 .0Maintenance capex (368.0) (427.4) (452.4) (474.9)Cash Flow 12/16A 12/17E 12/18E 12/19ENet income (US$) (1,010.0) 421.0 540.0 791.9DD&A 1,986.0 2,340.0 2,429.9 2,486.3Change in working capital (117.0) .0 .0 .0Other cash & non-cash items 1,618.0 743.9 836.2 889.4Cash flow from operations 3,303.0 3,639.8 4,450.0 4,945.2Free cashflow to the firm 2,935.0 3,212.4 3,997.6 4,470.3Other investment/(outflows) 2,387.0 1,282.5 135.0 135.0Cash flow from investments (6,390.0) (1,862.5) (1,420.0) (1,030.0)Net share issue/(repurchase) 1,098.0 718.0 400.0 400.0Dividends paid (3,542.0) (3,647.3) (4,171.7) (4,558.1)Change in debt 4,221.0 1,740.0 1,329.7 830.9Other financing inflows/outflows 1,143.0 (588.0) (588.0) (588.0)Cashflow from financing activities 2,920.0 (1,777.3) (3,030.0) (3,915.2)Movements in cash/eq. (167.0) (.0) (.0) (.0)Balance Sheet (US$) 12/16A 12/17E 12/18E 12/19EAssetsCash & cash equivalents 360.0 360.0 360.0 360.0Account receivables 3,211.0 3,211.0 3,211.0 3,211.0Other current assets 446.0 446.0 446.0 446.0Total current assets 5,729.0 5,729.0 5,729.0 5,729.0Total fixed assets 50,917.0 50,522.0 49,647.1 48,325.8Other assets 4,952.0 5,689.0 6,450.5 7,231.8Total assets 70,191.0 70,533.1 70,419.6 69,879.7LiabilitiesAccounts payables 2,943.0 2,943.0 2,943.0 2,943.0Short-term debt .0 .0 .0 .0Other short term liabilities 3,260.0 3,260.0 3,260.0 3,260.0Total current liabilities 6,203.0 6,203.0 6,203.0 6,203.0Long-term debt 31,741.0 33,481.0 34,810.6 35,641.5Other liabilities 5,672.0 5,672.0 5,672.0 5,672.0Total liabilities 43,616.0 45,356.0 46,685.6 47,516.5Minority interests / other 7,885.0 7,681.0 7,477.0 7,273.0Total liabilities and equity 70,143.0 70,485.1 70,371.6 69,831.7Financing Metrics 12/16A 12/17E 12/18E 12/19EEquity issuance 1,098.0 718.0 400.0 400.0Debt issuance/(repayment) 4,221.0 1,740.0 1,329.7 830.9Leverage (x) 5.8 4.9 4.6 4.4Per share 12/16A 12/17E 12/18E 12/19ENo. of shares (EOP) 518 543 560 569Earnings / unit EPU (US$) (2.01) 0.76 0.96 1.39DPS (US$) 4.22 4.22 4.22 4.32Book value per share 36.01 32.16 28.94 26.42Operating cash flow/share 6.38 6.71 7.95 8.69Valuation metrics 12/16A 12/17E 12/18E 12/19EDiv yield (%) 11.2 11.2 11.2 11.5FCF yield (%) 15.8 15.7 18.9 20.8EV/EBITDA (x) 10.5 9.3 9.0 8.6P/E (x) (18.7) 49.7 39.1 27.1Price to book (x) 1.0 1.2 1.3 1.4Credit ratios 12/16A 12/17E 12/18E 12/19ENet debt/equity (%) 118.3 131.8 145.4 158.1Interest coverage ratio (X) 1.4 2.1 2.5 2.7Dividend payout ratio (%) (35.4) (36.5) (41.7) (45.6)

Company BackgroundEnergy Transfer Partners, L.P. is a ltd partnership based in the US engaged in natural gas operations, managed by the general partner, Energy Transfer Partners GP, L.P., which in turn is managed by its general partner, Energy Transfer Partners, L.L.C..

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 52.00Our blue sky valuation assumes 1.0x higher EV/EBITDA and P/DCF multiples relative to base case and 100bps lower discount rate relative to the base case 3-stage DDM methodology.

Our Grey Sky Scenario (US$) 37.00Our grey sky valuation assumes 1.0x lower EV/EBITDA and P/DCF multiples relative to base case and 100bps higher discount rate relative to the base case 3-stage DDM methodology. Our valuation also takes into account flat distribution payouts and grey sky case for underlying subsidiaries and flat distributions at ETP.

Share price performance

ET P.N S& P 5 0 0 IN D EX

A p r - 1 6 Ju l - 1 6 O ct - 1 6 Jan - 1 72 5

3 0

3 5

4 0

4 5

On 27-Feb-2017 the S&P 500 INDEX closed at 2370.1Daily Feb26, 2016 - Feb27, 2017, 02/26/16 = US$26.62

Source: Company data, Thomson Reuters, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 17

ETP ValuationOur $45 target price is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM. Our TP implies ~31% NTM total returns, supporting our Outperform rating on the stock

Figure 11: ETP Blended Valuation2017E Multiple EV

EBITDA Low Base High Low Base HighEV/EBITDAETP consolidated EBITDA 6,622Less: SXL EBITDA 1,648EBITDA attributable to ETP 4,974 9.0x 10.0x 11.0x 44,762 49,735 54,709

ETP Net consolidated debt 32,499Less: SXL net debt 7,116Net debt attributable to ETP 25,383 25,383 25,383 25,383

Total Equity Value 19,379 24,352 29,326ETP LP Take % 71% 71% 71%ETP LP share 13,788 17,327 20,865

SXL EV/EBITDA 10.5x 11.5x 12.5xTotal SXL Equity Value 10,192 11,840 13,488GP Take % 39% 39% 39%SXL GP stake (ETP Class H) 10% 10% 10%ETP share in SXL GP 400 465 530

Units TPAdd: SXL ownership 67.1 $31 2,079 2,079 2,079Add: SUN ownership 43.5 $30 1,305 1,305 1,305Net ETP Equity value 17,572 21,175 24,779Units O/S 552 552 552Price/Unit $32 $38 $45

2017E MultipleDCF/unit Low Base High Low Base High

Price/DCF $4.34 9.0x 10.0x 11.0x $39 $43 $48

Discount RateLow Base High Low Base High

3-Stage DDM 10.0% 9.0% 8.0% $48 $54 $61

Average Target Price $40 $45 $51Distribution/unit (12-mo out) $4.22Yield (12-mo out) 9.4%Current Price $37.71Total Return (NTM) 31%

Metric

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 18

ETP Changes to EstimatesFigure 12: ETP Estimates Yr ending December 31($ millions, except per unit data)

1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019E 1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019E

Intrastate Natural Gas Transportation And Storage EBITDA 140 142 145 147 575 597 619 143 146 149 151 588 606 617Interstate Natural Gas Transportation And Storage EBITDA 277 280 317 365 1,239 1,454 1,454 267 270 307 357 1,202 1,434 1,453Midstream EBITDA 297 309 322 331 1,260 1,353 1,370 290 302 316 326 1,234 1,343 1,396NGL Transportation And Services EBITDA 313 352 376 402 1,443 1,774 1,840 294 335 393 418 1,441 1,711 1,879Investment In Sunoco Logistics EBITDA 394 424 452 480 1,750 1,982 2,167 366 389 438 454 1,648 1,948 2,198All Other EBITDA 120 126 122 122 490 513 534 123 132 128 126 508 526 543Segment EBITDA 1,561 1,653 1,754 1,867 6,836 7,755 8,069 1,484 1,573 1,732 1,833 6,622 7,568 8,086Core EBITDA (Excl SXL, PTXP, Retail and Other) 1,027 1,084 1,160 1,245 4,516 5,179 5,283 995 1,052 1,166 1,253 4,465 5,094 5,344

Adjusted EBITDANet income (loss) 430 528 627 758 2,343 3,126 3,364 375 488 606 703 2,172 2,917 3,375Interest expense, net of interest capitalized 361 353 356 351 1,422 1,414 1,448 351 338 343 346 1,378 1,462 1,490Depreciation and amortization 566 572 577 571 2,286 2,327 2,378 582 578 586 594 2,340 2,430 2,486Income tax expense from continuing operations (20) (25) (30) (36) (112) (149) (160) (18) (23) (29) (33) (103) (139) (161)Adjusted EBITDA related to unconsolidated affiliates 268 269 270 268 1,075 1,098 1,120 249 253 254 250 1,007 1,024 1,041Equity in earnings of unconsolidated affiliates (82) (83) (85) (84) (334) (358) (380) (76) (80) (83) (80) (320) (345) (365)Other, net 38 39 39 39 155 296 300 20 20 55 55 150 219 219Adj. EBITDA 1,561 1,653 1,754 1,867 6,836 7,755 8,069 1,484 1,573 1,732 1,833 6,622 7,568 8,086

EPU $0.05 $0.23 $0.39 $0.62 $1.29 $1.62 $1.70 ($0.10) $0.10 $0.29 $0.47 $0.76 $0.96 $1.39Average Units Outstanding 550 557 557 557 550 557 562 541 552 553 555 543 560 569

Distributable Cash Flow (DCF)Adjusted EBITDA 1,561 1,653 1,754 1,867 6,836 7,755 8,069 1,484 1,573 1,732 1,833 6,622 7,568 8,086Adjusted EBITDA related to unconsolidated affiliates (268) (269) (270) (268) (1,075) (1,098) (1,120) (249) (253) (254) (250) (1,007) (1,024) (1,041)Distributions from unconsolidated affiliates (109) (101) (124) (111) (445) (445) (445) (137) (129) (152) (134) (552) (552) (552)Maintenance Capex (111) (113) (115) (116) (455) (469) (480) (105) (106) (108) (109) (427) (452) (475)Cash Interest Expenses (361) (353) (356) (351) (1,422) (1,414) (1,448) (351) (338) (343) (346) (1,378) (1,462) (1,490)Other Adjustments 1,242 1,244 1,203 1,213 4,903 4,924 5,046 1,119 1,112 1,078 1,108 4,417 4,635 4,747Total Distributable Cash Flow 950 1,044 1,168 1,278 4,440 5,367 5,627 933 1,029 1,207 1,296 4,465 5,320 5,793DCF Not Attributable to ETP 172 192 203 221 788 854 896 147 163 199 206 714 850 936Distributable Cash Flow Attributable to ETP 779 852 965 1,058 3,653 4,514 4,731 786 866 1,009 1,090 3,751 4,470 4,857Cash Paid to General Partner (GP) 234 229 227 217 907 1,394 1,477 230 225 225 216 896 1,405 1,498Class H units payments to general partner 103 108 117 122 450 556 653 106 112 120 126 464 576 683DCF to Limited Partners 442 515 621 718 2,296 2,564 2,601 451 529 663 748 2,391 2,489 2,676

DCF per LP unit $0.8052 $0.9240 $1.1133 $1.2880 $4.1304 $4.5990 $4.6269 $0.8336 $0.9573 $1.1986 $1.3487 $4.3381 $4.4441 $4.6985

Cash Distribution Declared Per Unit $1.0550 $1.0550 $1.0550 $1.0550 $4.2200 $4.2200 $4.3200 $1.0550 $1.0550 $1.0550 $1.0550 $4.2200 $4.2200 $4.3200

Distribution Coverage (Total DCF/Total Distribution Declared) 0.84x 0.92x 1.03x 1.14x 0.98x 1.05x 1.04x 0.86x 0.94x 1.08x 1.17x 1.01x 1.03x 1.05x

Capital Expenditures & AcquisitionsGrowth Capex 475 475 475 475 1,900 1,000 800 700 700 700 700 2,800 1,200 800Maintenance Capex 88 88 88 88 350 350 350 86 86 86 86 345 355 365Acquisitions 0 0 0 0 0 0 0 0 0 0 0 0 0 0Total Capital Expenditures & Acquisitions 563 563 563 563 2,250 1,350 1,150 786 786 786 786 3,145 1,555 1,165

Operating MetricsIntrastate Natural Gas Transportation And Storage

Natural gas transported (MMBtu/d) 8,218,813 8,268,613 8,368,213 8,467,813 8,330,863 8,696,783 9,049,908 7,942,467 8,040,867 8,139,267 8,237,667 8,090,067 8,354,465 8,522,812

Interstate Natural Gas Transportation And StorageNatural gas transported (MMBtu/d): 5,412,607 5,439,670 6,447,170 8,148,004 6,361,863 8,148,004 8,148,004 5,348,701 5,375,445 6,382,945 8,083,778 6,297,717 8,185,332 8,350,271Natural gas sold (MMBtu/d) - ETP Legacy Assets: 19,478 19,478 19,478 19,478 19,478 19,478 19,478 17,190 17,190 17,190 17,190 17,190 17,406 17,757

MidstreamGathered volumes (MMBtu/d): 10,375,316 10,700,316 11,025,316 11,340,316 10,860,316 11,690,316 11,840,316 10,018,728 10,343,728 10,718,728 11,083,728 10,541,228 11,521,228 11,978,757NGLs Produced including Equity NGLs (Bbl/d): 494,063 509,539 525,015 540,015 517,158 556,682 563,825 477,082 492,558 510,416 527,797 501,963 548,630 570,417

NGL Transportation And ServicesNGL transportation volumes (Bbl/d) 892,188 1,003,609 1,086,146 1,191,230 1,043,293 1,221,310 1,270,900 778,891 889,180 970,572 1,072,189 927,708 1,099,263 1,143,897NGL fractionation volumes (Bbl/d) 418,237 458,237 458,237 458,237 448,237 469,808 488,884 433,663 473,663 473,663 473,663 463,663 495,624 617,257

Old Estimates New Estimates

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 19

ETP 4Q16 Earnings4Q16 Mixed; Core EBITDA and Overall EBITDA Below CS and Street■ Total EBITDA Below Us and the Street: EBITDA of $1,433mm came in 5% below our

$1,510mm estimate and 3% below the Street’s $1,480mm estimate. The variance was primarily driven by the interstate natural gas and midstream segments. Details on ETP’s core business segments below -

− Intrastate Transportation EBITDA Beat on Higher Margins: $152mm EBITDA came in above our $142mm estimate (+7%). Volumes of 7,913 Bbtu/d missed our 8,169 Bbtu/d estimate (-3%), but were offset by higher gross margins ($0.26/Mmbtu vs. our $0.23/MMBtu estimate), which drove the EBITDA higher.

− Interstate Transportation EBITDA Missed on Lower Volumes: $269mm EBITDA came in below our $280mm estimate (-4%). Natural gas transportation volumes of 5,322 Bbtu/d were 1% below our 5,386 Bbtu/d estimate and natural gas sales volumes of ~17.2 Bbtu/d were 12% below our ~19.5 Bbtu/d estimate.

− Midstream EBITDA Missed on Lower Volumes and Margins: $258mm EBITDA came in 12% below our $294mm estimate. Gathering volumes of 9,694 Bbtu/d were 4% below our 10,050 Bbtu/d estimate and NGL production volumes of 459 MBbl/d were 4% below our 479 MBbl/d estimate. Gross margins of 32% were below our 36% estimate.

− Liquids Transportation and Services EBITDA In Line: $281mm EBITDA was in line with our $283mm estimate. Lower NGL transportation volumes were offset by higher NGL fractionation volumes and healthier margins. NGL transportation volumes of 670 Mbbl/d were lower than our 782 Mbbl/d estimate (-14%) and NGL fractionation volumes of 394 Mbbl/d were higher than our 378 Mbbl/d (+4%).

■ DCF Above CS: $906mm DCF came in 2% above our $888mm estimate. Lower interest expenses were offset by higher than forecast maintenance capex. ETP ended the quarter with a 0.89x coverage. Marks the 6th straight quarter of below 1x coverage (excl. 4Q15 income tax gain which kept coverage above 1.0x).

■ Distribution of $1.055/unit was in line with us and the Street.

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 20

Figure 13: ETP 4Q16 VarianceYr ending December 31($ millions, except per unit data) 4Q16 4Q16 CS Diff Diff (%) 4Q15 Y/Y (%)

Actual Estimate Actual

Intrastate Natural Gas Transportation And Storage EBITDA 152 142 10 7% 122 25%Interstate Natural Gas Transportation And Storage EBITDA 269 280 (11) -4% 283 -5%Midstream EBITDA 258 294 (36) -12% 264 -2%NGL Transportation And Services EBITDA 281 283 (2) -1% 222 27%Investment In Sunoco Logistics EBITDA 327 356 (29) -8% 317 3%All Other EBITDA 146 135 11 8% 152 -4%Segment EBITDA 1,433 1,510 (155) -5% 1,360 5%Core EBITDA (Excl SXL, PTXP, Retail and Other) 960 999 (39) -4% 891 8%

Adjusted EBITDANet income (loss) (362) 399 (761) -191% 21 -1824%Interest expense, net of interest capitalized 336 349 (13) -4% 312 8%Depreciation and amortization 517 559 (42) -8% 478 8%Income tax expense from continuing operations (55) (19) (36) 189% (103) -47%Adjusted EBITDA related to unconsolidated affiliates 235 263 (28) -11% 226 4%Equity in earnings of unconsolidated affiliates 201 (80) 281 -352% (81) -348%Other, net 561 23 538 NM 507 11%Adj. EBITDA 1,433 1,510 (77) -5% 1,360 5%

EPU ($1.47) $0.01 ($1.48) NM ($0.68) 116%Average Units Outstanding 523 536 (13) -2% 486 8%

Distributable Cash Flow (DCF)Adjusted EBITDA 1,433 1,510 (77) -5% 1,360 5%Adjusted EBITDA related to unconsolidated affiliates (235) (263) 28 -11% (226) 4%Distributions from unconsolidated affiliates (134) (111) (23) 21% (214) -37%Maintenance Capex (134) (121) (13) 10% (177) -24%Cash Interest Expenses (336) (349) 13 -4% (312) 8%Other Adjustments 1,098 1,244 (146) -12% 775 42%Total Distributable Cash Flow 906 888 18 2% 1,086 -17%DCF Not Attributable to ETP 110 143 (33) -23% 127 -13%Distributable Cash Flow Attributable to ETP 796 745 51 7% 959 -17%Cash Paid to General Partner (GP) 237 235 3 1% 320 -26%Class H units payments to general partner 94 97 (3) -3% 77 22%DCF to Limited Partners 465 413 52 13% 562 -17%

DCF per LP unit $0.8893 $0.7704 $0.12 15% $1.1124 -20%

Cash Distribution Declared Per Unit $1.0550 $1.0550 $0.00 0% $1.0550 0%

Distribution Coverage (Total DCF/Total Distribution Declared) 0.89x 0.82x 0.06x 8% 1.07x -17%

Capital Expenditures & AcquisitionsGrowth Capex 628 250 378 151% 1,267 -50%Maintenance Capex 111 100 11 11% 142 -22%Acquisitions 640 640 0 0% 200 220%Total Capital Expenditures & Acquisitions 1,379 990 389 39% 1,609 -14%

Operating MetricsIntrastate Natural Gas Transportation And Storage

Natural gas transported (MMBtu/d) 7,913,134 8,169,013 (255,879) -3% 7,926,907 0%

Interstate Natural Gas Transportation And StorageNatural gas transported (MMBtu/d): 5,322,091 5,385,679 (63,588) -1% 5,739,157 -7%Natural gas sold (MMBtu/d) - ETP Legacy Assets: 17,190 19,478 (2,288) -12% 18,665 -8%

MidstreamGathered volumes (MMBtu/d): 9,693,728 10,050,316 (356,588) -4% 10,051,612 -4%NGLs Produced including Equity NGLs (Bbl/d): 459,604 478,586 (18,982) -4% 473,178 -3%

NGL Transportation And ServicesNGL transportation volumes (Bbl/d) 669,694 781,869 (112,175) -14% 473,656 41%NGL fractionation volumes (Bbl/d) 393,663 378,237 15,426 4% 249,566 58%

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 21

Americas/United StatesMaster Limited Partnerships

Sunoco Logistics Partners, LP (SXL)Rating OUTPERFORMPrice (27-Feb-17, US$) 25.23Target price (US$) 31.0052-week price range (US$) 31.47 - 22.52Market cap (US$ m) 8,363.01Adjusted EV -Target price is for 12 months.

Research Analysts

John Edwards, CFA713 890 1594

Bhavesh Lodaya212 325 2337

Dylan Nassano212 325 8375

Reinstating with $31 TP and Outperform■ Investment Thesis: SXL is growing its NGLs business with the ~600 Mbpd

(expandable to 800 Mbpd) Mariner East (ME) franchise. The 70 Mbpd ME1 is already in service, the 275 Mbpd ME2 is expected to be placed into service in 2H17 and the 250 Mbpd ME2X currently under development. We expect SXL to grow it distribution at ~10-12%/yr., and maintain coverage at ~1.05x

■ Estimates: Coming off restriction we now expect SXL EBITDA of ~$1.65Bn/$1.95Bn/$2.2Bn in 2017/18/19, which includes the 3Q17 in service of the Mariner East 2 and Phase 1 of the Permian Express III projects. We forecast a 4Q18 in service for the Mariner East 2 expansion project. We expect SXL to grow distributions by ~10% annually and while SXL did not lay out capex guidance for 2017, we forecast total capex of ~$1.1Bn, including ~$84mm on maintenance. We forecast leverage of 4.3x/4.0x/3.8x for 2017/18/19 which includes 30%/70% equity and debt financing.

■ Valuation: We are reinstating coverage on SXL with a $31 target price and an Outperform rating, driven by ~32% NTM total return. Our valuation is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM.

■ Risks: Lower than expected NGL demand is primary risk for SXL as it is developing the Mariner East 2 and Mariner East 2 expansion projects. Other risks include, unfavorable WTI-LLS differentials, tax treatment of MLPs and growth and access and cost of capital.

Share price performance

SXL.N S& P 5 0 0 IN D EX

A p r - 1 6 Ju l - 1 6 O ct - 1 6 Jan - 1 72 22 42 62 83 03 2

On 27-Feb-2017 the S&P 500 INDEX closed at 2370.1Daily Feb26, 2016 - Feb27, 2017, 02/26/16 = US$24.39

DCF/LP Unit Q1 Q2 Q3 Q42016A 0.58 0.37 0.47 0.462017E 0.53 0.56 0.61 0.622018E 0.63 0.66 0.66 0.65

Financial and valuation metricsYear 12/16A 12/17E 12/18E 12/19EEBITDA (US$ m) 1,233 1,648 1,948 2,198Distribution/unit- DPU (US$ m) 2.02 2.23 2.47 2.71Earnings/unit - EPU (US$) 1.02 0.99 1.29 1.58Prev. Earnings/unit - EPU (US$) 0.88 1.14 1.35 1.54EPU - consensus (US$) 0.98 0.99 1.35 1.66Distribution coverage (x) 0.92 1.04 1.06 1.05P/DCF (x) 12.7 10.9 9.7 8.9Adj. current EV/EBITDA (x) - - - -

DPU (US$) 2.14 Distribution yld (%) 8.5Units outstanding (m) 331 GP take (%) 39.7Net debt current (US$ m) 6,645.1 Net debt/EBITDA (x) 5.66-month ADV (000's) 629 Net debt/market cap. (%) -Free float (%) 86 Institutional ownership (%) 45.6Source: Company data, Thomson Reuters, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 22

Sunoco Logistics Partners, LP (SXL)Price (27 Feb 2017): US$25.23; Rating: OUTPERFORM; Target Price: $31.00; Analyst: John EdwardsMLP Distributable Cash Flow (DCF)

12/16A 12/17E 12/18E 12/19E

Adjusted EBITDA 1,233.0 1,648.3 1,947.8 2,198.3(-) Maintenance Capex - - - -(-) Cash Interest Expenses 157.0 161.0 165.3 177.6(+/-) Other Adjustments 133.0 146.4 161.4 173.9Total Distributable Cash Flow (US$) 943.0 1,340.9 1,621.0 1,846.8(-) General Partner Adjustments 365.1 544.5 687.2 804.9DCF to limited partners 577.94 796.36 933.79 1,041.88DCF per LP unit (US$) 1.89 2.31 2.60 2.83Cash Distribution Declared Per Unit (US$)

3.96 4.02 4.19 4.32Distribution coverage (x) .92 1.04 1.06 1.05DCF/LP Unit Q1 Q2 Q3 Q42016A 0.58 0.37 0.47 0.462017E 0.53 0.56 0.61 0.622018E 0.63 0.66 0.66 0.65Capex 12/16A 12/17E 12/18E 12/19EExpansion Capex - - - -Acquisitions (786.0) .0 .0 .0Maintenance capex - - - -Cash Flow 12/16A 12/17E 12/18E 12/19ENet income (US$) 312.0 340.4 462.0 579.3DD&A 446.0 476.0 476.0 476.0Change in working capital (85.0) .0 .0 .0Other cash & non-cash items 328.0 351.0 346.7 334.4Cash flow from operations 888.0 1,344.9 1,593.7 1,832.0Free cashflow to the firm (1,061.0) 262.5 496.3 922.0Other investment/(outflows) (1,089.0) 800.0 .0 .0Cash flow from investments (3,824.0) (282.4) (1,097.4) (909.9)Net share issue/(repurchase) 1,388.0 324.7 329.2 273.0Dividends paid (966.0) (1,231.1) (1,474.4) (1,710.2)Change in debt - (156.1) 648.9 515.2Other financing inflows/outflows - .0 .0 .0Cashflow from financing activities 422.0 (1,062.5) (496.3) (922.0)Movements in cash/eq. (2,514.0) .0 .0 .0Balance Sheet (US$) 12/16A 12/17E 12/18E 12/19EAssetsCash & cash equivalents 41.0 41.0 41.0 41.0Account receivables 1,900.0 1,900.0 1,900.0 1,900.0Other current assets 31.0 31.0 31.0 31.0Total current assets 2,906.0 2,906.0 2,906.0 2,906.0Total fixed assets 12,324.0 12,930.4 13,551.8 13,985.7Other assets 1,033.0 1,033.0 1,033.0 1,033.0Total assets 18,849.0 19,455.4 20,076.8 20,510.7LiabilitiesAccounts payables 1,813.0 1,813.0 1,813.0 1,813.0Short-term debt .0 .0 .0 .0Other short term liabilities 325.0 325.0 325.0 325.0Total current liabilities 2,138.0 2,138.0 2,138.0 2,138.0Long-term debt 7,313.0 7,156.9 7,805.8 8,320.9Other liabilities 705.0 705.0 705.0 705.0Total liabilities 10,156.0 9,999.9 10,648.8 11,163.9Minority interests / other 33.0 33.0 33.0 33.0Total liabilities and equity 18,849.0 19,455.4 20,076.8 20,510.7Financing Metrics 12/16A 12/17E 12/18E 12/19EEquity issuance 1,388.0 324.7 329.2 273.0Debt issuance/(repayment) - (156.1) 648.9 515.2Leverage (x) 5.9 4.3 4.0 3.8Per share 12/16A 12/17E 12/18E 12/19ENo. of shares (EOP) 307 344 359 367Earnings / unit EPU (US$) 1.02 0.99 1.29 1.58DPS (US$) 2.02 2.23 2.47 2.71Book value per share 28.22 27.39 26.17 25.34Operating cash flow/share 2.89 3.91 4.44 4.99Valuation metrics 12/16A 12/17E 12/18E 12/19EDiv yield (%) 8.0 8.8 9.8 10.7FCF yield (%) (14.4) 3.0 5.5 9.9EV/EBITDA (x) 15.8 13.1 12.0 11.2P/E (x) 24.9 25.6 19.6 16.0Price to book (x) 0.9 0.9 1.0 1.0Credit ratios 12/16A 12/17E 12/18E 12/19ENet debt/equity (%) 83.7 75.3 82.4 88.6Interest coverage ratio (X) 4.1 6.2 7.5 8.4Dividend payout ratio (%) (9.7) (12.3) (14.7) (17.1)

Company BackgroundSunoco Logistics Partners L.P. owns & operates a logistics business, consisting of a geographically diverse portfolio of complementary pipeline, terminalling, & crude oil acquisition & marketing assets.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 35.00Our blue sky valuation assumes 1.0x higher EV/EBITDA and P/DCF multiples relative to base case and 100bps lower discount rate relative to the base case 3-stage DDM methodology.

Our Grey Sky Scenario (US$) 23.00Our grey sky valuation assumes 1.0x lower EV/EBITDA and P/DCF multiples relative to base case and 100bps higher discount rate relative to the base case 3-stage DDM methodology. Our valuation also takes into account flat distribution payouts by SXL.

Share price performance

SXL.N S& P 5 0 0 IN D EX

A p r - 1 6 Ju l - 1 6 O ct - 1 6 Jan - 1 72 22 42 62 83 03 2

On 27-Feb-2017 the S&P 500 INDEX closed at 2370.1Daily Feb26, 2016 - Feb27, 2017, 02/26/16 = US$24.39

Source: Company data, Thomson Reuters, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 23

SXL ValuationOur $31 target price is based on an equal weighted blend of EV/EBITDA, P/DCF and 3-stage DDM. Our TP implies ~32% NTM total returns, supporting our Outperform rating on the stock.

Figure 14: SXL Blended Valuation2017E Multiple EV

EBITDA Low Base High Low Base HighEV/EBITDA 1,648 10.5x 11.5x 12.5x 17,308 18,956 20,604Less: 2017 Net Debt 7,116 7,116 7,116Total Equity Value 10,192 11,840 13,488SXL LP Take % 61% 61% 61%Units O/S 332 332 332Price/Unit $19 $22 $25

2017E MultipleDCF/unit Low Base High Low Base High

Price/DCF $2.31 11.0x 12.0x 13.0x $25 $28 $30

Discount RateLow Base High Low Base High

3-Stage DDM 10.0% 9.0% 8.0% $38 $43 $50

Average Target Price $27 $31 $35Distribution/unit (12-mo out) $2.32Yield (12-mo out) 7.5%Current Price $25.27Total Return (NTM) 32%

Metric

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 24

SXL Changes to EstimatesFigure 15: SXL EstimatesYr ending December 31

1Q17E 2Q17E 3Q17E 4Q17E 2017E 2018E 2019ECrude Oil 213 231 272 285 1,001 1,181 1,355Natural Gas Liquids 91 95 102 104 392 495 554Refined Products 62 63 64 65 254 271 290

Segment EBITDA 366 389 438 454 1,648 1,948 2,198

Net Income 182 207 232 248 869 1,118 1,356Interest cost, net of capitalized interest 41 40 40 40 161 165 178Depreciation and amortization 119 119 119 119 476 476 476Provision for income taxes 7 7 7 7 28 28 28Other items 17 17 40 40 114 161 161

Adjusted EBITDA 366 389 438 454 1,648 1,948 2,198

EPU $0.18 $0.24 $0.27 $0.29 $0.99 $1.29 $1.58Average Units Outstanding 335 338 350 353 344 359 367

Distributable Cash Flow (DCF)Adjusted EBITDA 366 389 438 454 1,648 1,948 2,198

Interest cost, net of capitalized interest 41 40 40 40 161 165 178Maintenance Capex 18 19 22 23 82 97 110Provision for income taxes 7 7 7 7 28 28 28Less: Other items 9 9 9 9 36 36 36

Total Distributable Cash Flow 291 314 360 375 1,341 1,621 1,847(-) General Partner (GP) Interest in DCF 115 126 148 155 545 687 805

DCF to Limited Partners 176 188 212 220 796 934 1,042

DCF per LP unit $0.5258 $0.5566 $0.6061 $0.6232 $2.3118 $2.6006 $2.8350

Cash Distribution Declared Per Unit $0.5350 $0.5500 $0.5650 $0.5800 $2.2300 $2.4700 $2.7100

Distribution Coverage (Total DCF/Total Distribution Declared) 0.98x 1.01x 1.09x 1.09x 1.04x 1.06x 1.05x

Operating MetricsCrude Oil

Pipeline throughput (Mbpd) 2,667 2,787 2,912 3,043 2,852 3,120 3,247Terminal throughput (Mbpd) 1,733 1,811 1,893 1,978 1,854 2,028 2,110

Natural Gas LiquidsPipeline throughput (Mbpd) 310 313 316 319 315 328 341Terminal throughput (Mbpd) 264 266 269 272 268 278 290

Refined ProductsPipeline throughput (Mbpd) 683 690 696 703 693 721 750Terminal throughput (Mbpd) 614 621 627 633 624 649 675

Capital Expenditures & AcquisitionsGrowth Capex 250 250 250 250 1,000 1,000 800Maintenance Capex 18 19 22 23 82 97 110Acquisitions 0 0 0 0 0 0 0

Total Capital Expenditures & Acquisitions 268 269 272 273 1,082 1,097 910

New Estimates

Source: Company data, Credit Suisse estimates

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 25

Risks■ Collapse in Crude Prices; Lower than Anticipated Production Growth: - SXL’s

recent acquisitions, JVs and growth projects have focused on capitalizing on the 400-500 Mbpd of annual crude oil production growth in the Permian basin. A commodity price recovery has made production growth even more lucrative for producers in the region, that depend on midstream operators like SXL for takeaway capacity. However, a collapse in crude prices would erode margins for these producers and restrict production growth, thereby indirectly affecting midstream volumes. On the other hand, slower than industry forecasted production growth, irrespective of price movements would result in lower utilizations across the midstream platform and impact operators such as SXL.

■ Lower Than Expected NGL Demand – SXL is developing the Mariner East 2 and Mariner East 2 expansion projects on the back of expected increase in demand for ethane by steam crackers and for export. Although, both these projects would contribute fixed, blue-bar rate-able cash flows, any changes to NGL demand/supply fundamentals would impact pipeline and terminal volumes at SXL.

■ Unfavorable WTI-LLS Differentials – Other than rate-able, blue-bar cash flows, SXL derives red-bar cash flows from its crude oil leasing business. It is able to capture these cash flows when there exists a significant spread between WTI and LLS crude prices. However, with crude prices falling since June 2014 and plunging to all-time lows in January 2016, SXL’s ability to generate red-bar cash flows has been limited. For 2016, SXL estimates negligible contribution from its crude oil leasing business. While, it does not depend on these cash flows in deciding the trajectory of distribution growth, the cash definitely helps in balance sheet preservation and keeping leverage in check.

■ Tax Treatment Of MLPs – SXL’s ability to pay distributions may be hindered should the tax treatment of MLPs be changed. Although the discussion of taxing MLPs arises from time to time, we view such an event as a low probability.

■ Access To Capital Markets – Unattractive capital markets might impact SXL’s ability to raise funds for future growth projects or M&A. Currently, we do not forecast any major equity/debt issuances outside of SXL’s ATM program.

■ Permitting – While the current administration has been friendlier on the regulatory front, there remains risks at the state level for various projects.

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 26

SXL 4Q16 Earnings4Q16 EBITDA Misses the StreetDue to Credit Suisse’s involvement in the Bakken pipeline stake sale transaction related to SXL, we do not have comparable estimates. The stake sale closed last week, on February 15th and we are in the process of publishing new estimates and a TP/Rating for SXL.

■ EBITDA Below The Street: EBITDA of $327mm came in 4% below the Street’s $339mm estimate.

− Crude Oil Segment EBITDA came in at $184mm. SXL reported pipeline throughput of 2,552 Mbpd (+1% q/q) and terminal throughput of 1,633 Mbpd (+5% q/q).

− NGL Segment EBITDA came in at $88mm. SXL reported pipeline throughput of 307 Mbpd (+6% q/q) and terminal throughput of 253 Mbpd (flat q/q).

− Refined Products Segment EBITDA came in at $55mm. SXL reported pipeline throughput of 676 Mbpd (+11% q/q) and terminal throughput of 565 Mbpd (-1% q/q).

■ DCF: SXL reported DCF of $247mm and distribution coverage was 0.87x for the quarter.

■ Distribution/unit of $0.52 was in line with us and the Street.

28 February 2017

Energy Transfer 4Q16 Review (ETE | ETP | SXL | SUN) 27

Americas/United StatesMaster Limited Partnerships

Sunoco, LP (SUN)Rating OUTPERFORMPrice (27-Feb-17, US$) 26.52Target price (US$) 30.0052-week price range (US$) 36.33 - 21.21Market cap (US$ m) 2,969.61Adjusted EV -Target price is for 12 months.

Research Analysts

John Edwards, CFA713 890 1594

Bhavesh Lodaya212 325 2337

Dylan Nassano212 325 8375

Reiterating $30 TP and Outperform■ Investment Thesis: Since Oct-2014, SUN has completed ~$7Bn in M&A,

including ~$5.7Bn of dropdowns from ETP. SUN's business now includes retail and wholesale fuel distribution, convenience stores, supply & trading, racing fuels and terminals. It’s operations are spread across 30 states. Brands include Sunoco motor fuel, Stripes stores, Laredo Taco, Aplus, MACS, Tigermarket, and Aloha. Third-party acquisitions of wholesale/retail fuel distributors will act as a growth catalyst for SUN.

■ Estimates: We continue to forecast normalized retail ($0.23-0.25/gal) and wholesale ($0.06-0.08/gal) margins. While our fuel volume and margin assumptions are relatively unchanged, our EBITDA forecasts move ~3% lower between 2017-19 due to 100bps lower merchandise margin estimates. We now forecast LT merchandise margins of 31.5% vs. 32.5%, based on mgmt.’s 31-32% guidance. Since, SUN indicated plans to make use of their $400mm ATM program, we now model ~$200mm of equity issuance in 2017, and $100mm/yr. in 2018/19. This should enable SUN to bring leverage down from 6.5x in 4Q16, to 5.5x in 2017, 5.1x in 2018 and 4.8x in 2019. We continue to forecast flat payouts at $0.8255/unit/Q for SUN due to the elevated leverage and do not foresee distribution growth until leverage moves to a 4-4.5x range in the long term.